Embed Size (px)

Citation preview

EE EEQUITY

QUITY

QUITY

QUITY RR RRESEARCH

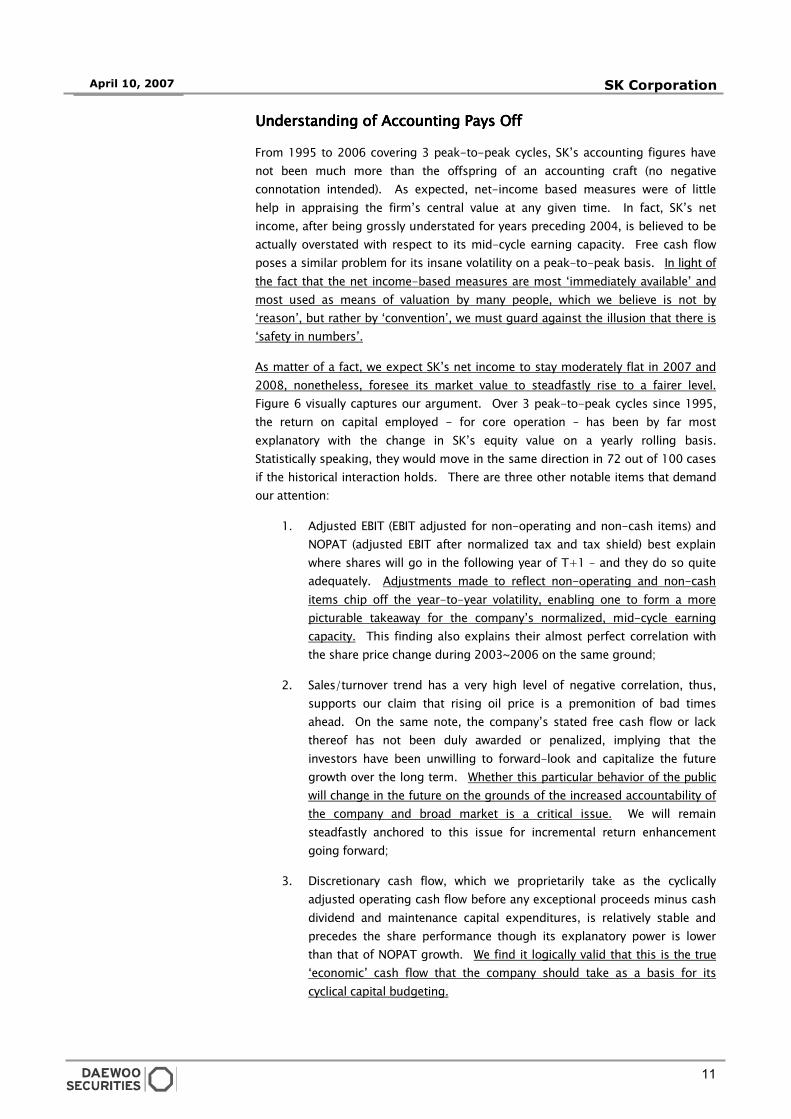

ESEARCH

ESEARCH

ESEARCH

DWS

DWS

DWS

DWS CC CCOMP

OMP

OMP

OMP LL LLAB

AB

AB

AB

CC CCOMPANY

OMPANY

OMPANY

OMPANY RR RREPORT

EPORT

EPORT

EPORT

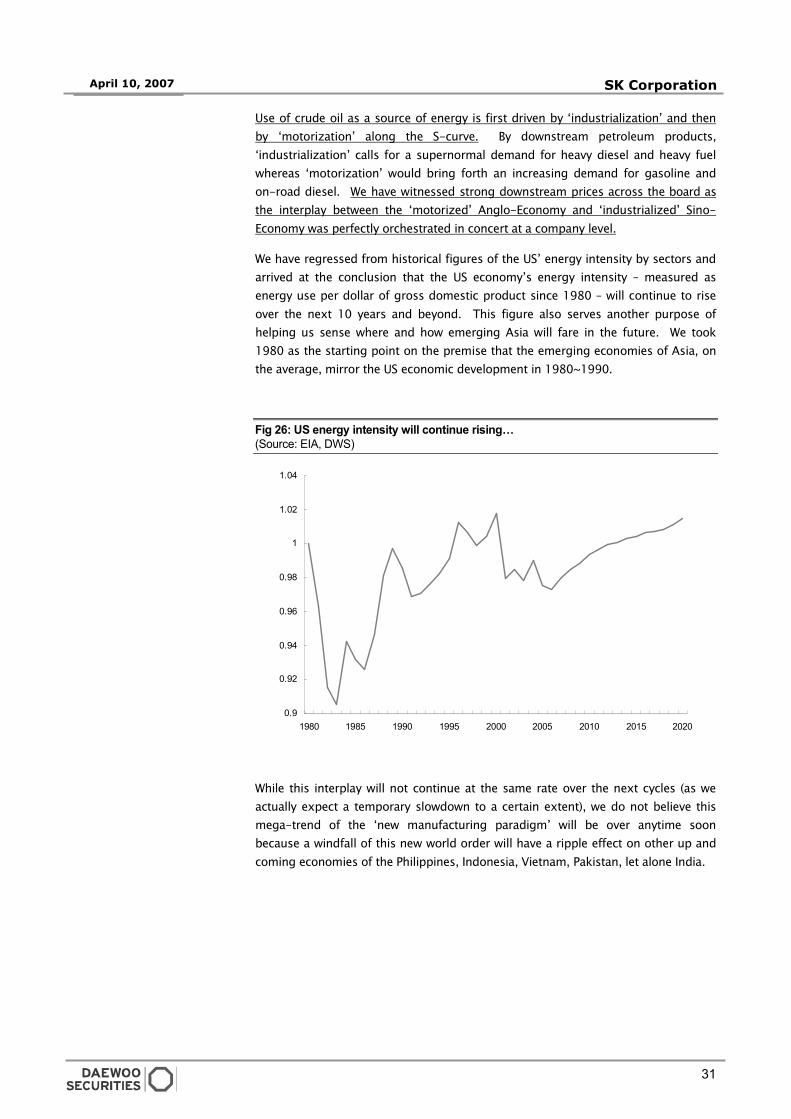

DDDDDDDDDDDDWWWWWWWWWWWWSSSSSSSSSSSS CCCCCCCCCCCCOOOOOOOOOOOOMMMMMMMMMMMMPPPPPPPPPPPPLLLLLLLLLLLLAAAAAAAAAAAABBBBBBBBBBBB

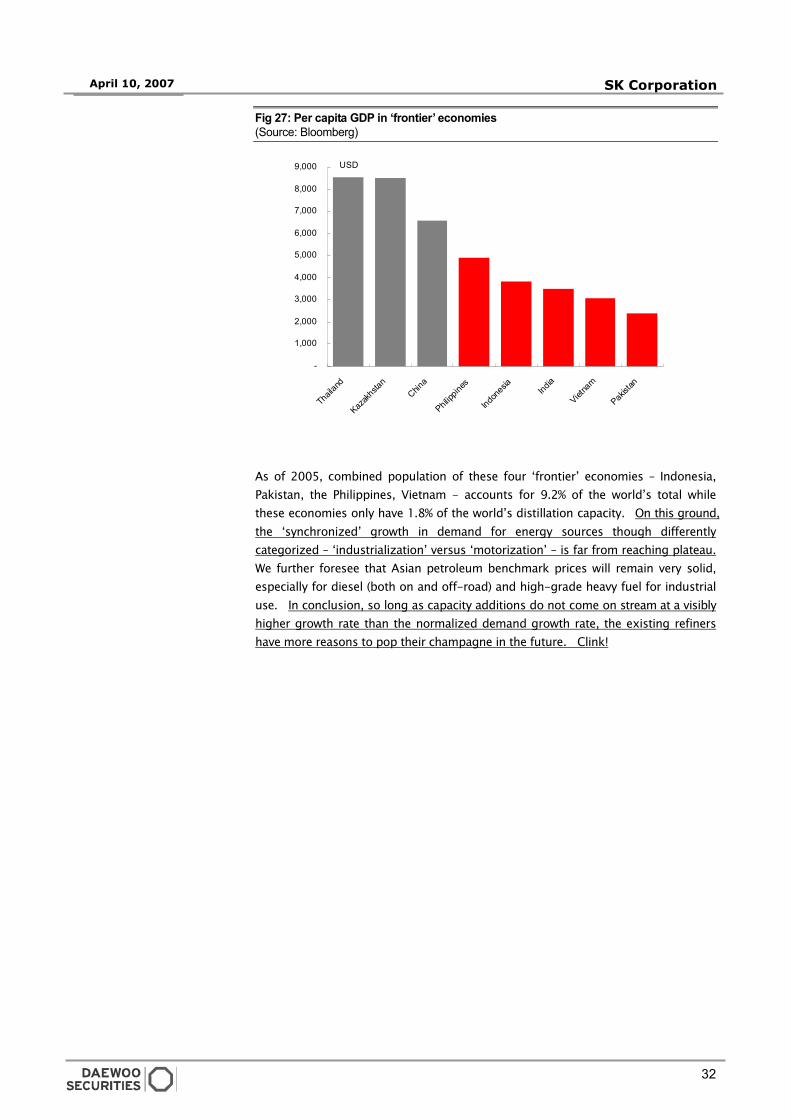

Please carefully read important notices in the last pages of this report.

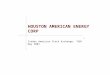

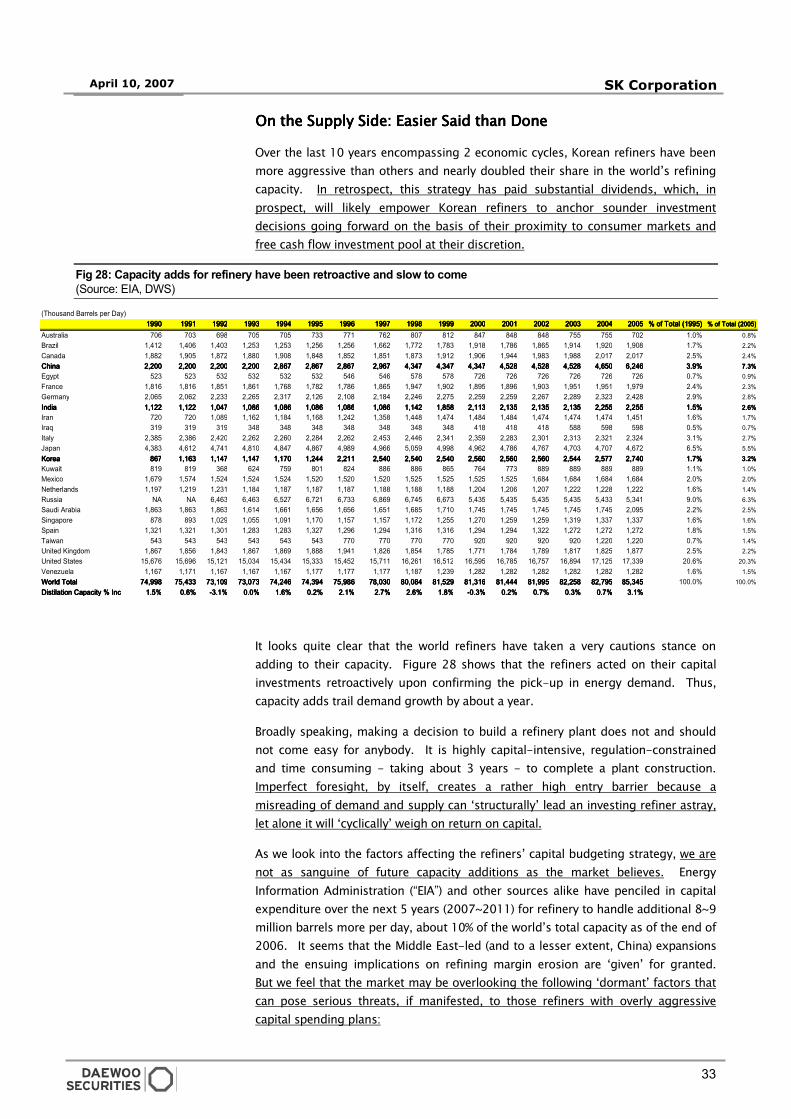

April 10, 2007April 10, 2007April 10, 2007April 10, 2007

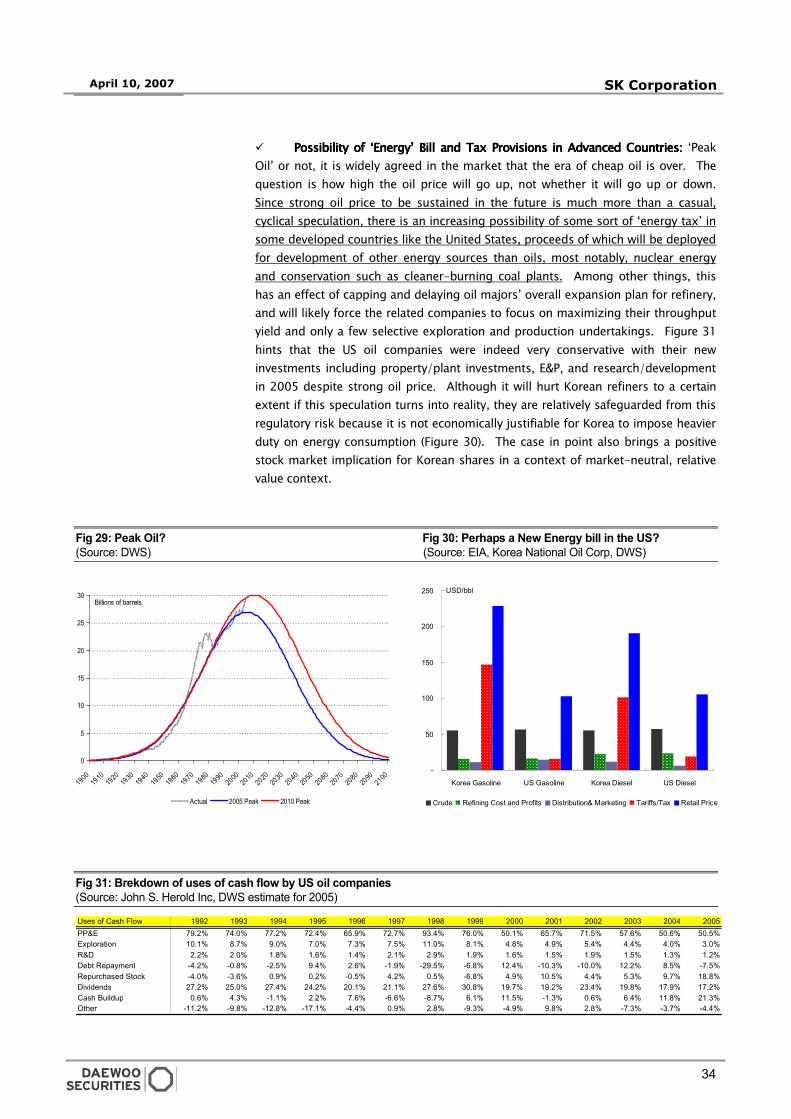

Country: Korea Sector: Refining/Petrochem Industry: Energy/Chemical Ticker: 003600

STRONG BUY SSKK CCOORRPPOORRAATTIIOONN Last Price (KRW)Last Price (KRW)Last Price (KRW)Last Price (KRW) 88,80088,80088,80088,800

Price Target (1Price Target (1Price Target (1Price Target (12M, KRW)2M, KRW)2M, KRW)2M, KRW) 120,000120,000120,000120,000

ForwardForwardForwardForward Range Range Range Range (12M, KRW)(12M, KRW)(12M, KRW)(12M, KRW) 89,000~134,00089,000~134,00089,000~134,00089,000~134,000

KOSPIKOSPIKOSPIKOSPI 1,499.161,499.161,499.161,499.16

SSSSSSSS̊̊imply imply imply imply KKKKKKKK̊̊osher for osher for osher for osher for ‘‘‘‘CorollaryCorollaryCorollaryCorollary’’’’ Investing Investing Investing Investing - A ‘can’t miss’ name for buyout investors?

PPPPRICERICERICERICE/P/P/P/PRICERICERICERICE RRRRELATIVEELATIVEELATIVEELATIVE

Performance (%)Performance (%)Performance (%)Performance (%) 1m1m1m1m 6m6m6m6m 12m12m12m12m

AbsoluteAbsoluteAbsoluteAbsolute 10.4%10.4%10.4%10.4% 47%47%47%47% 31313131.9%.9%.9%.9%

KOSPIKOSPIKOSPIKOSPI 5.3%5.3%5.3%5.3% 12.9%12.9%12.9%12.9% 7.2%7.2%7.2%7.2%

Alfred ParkAlfred ParkAlfred ParkAlfred Park +822-768-4143 [email protected]

Sammy LeeSammy LeeSammy LeeSammy Lee +822-768-4142 [email protected]

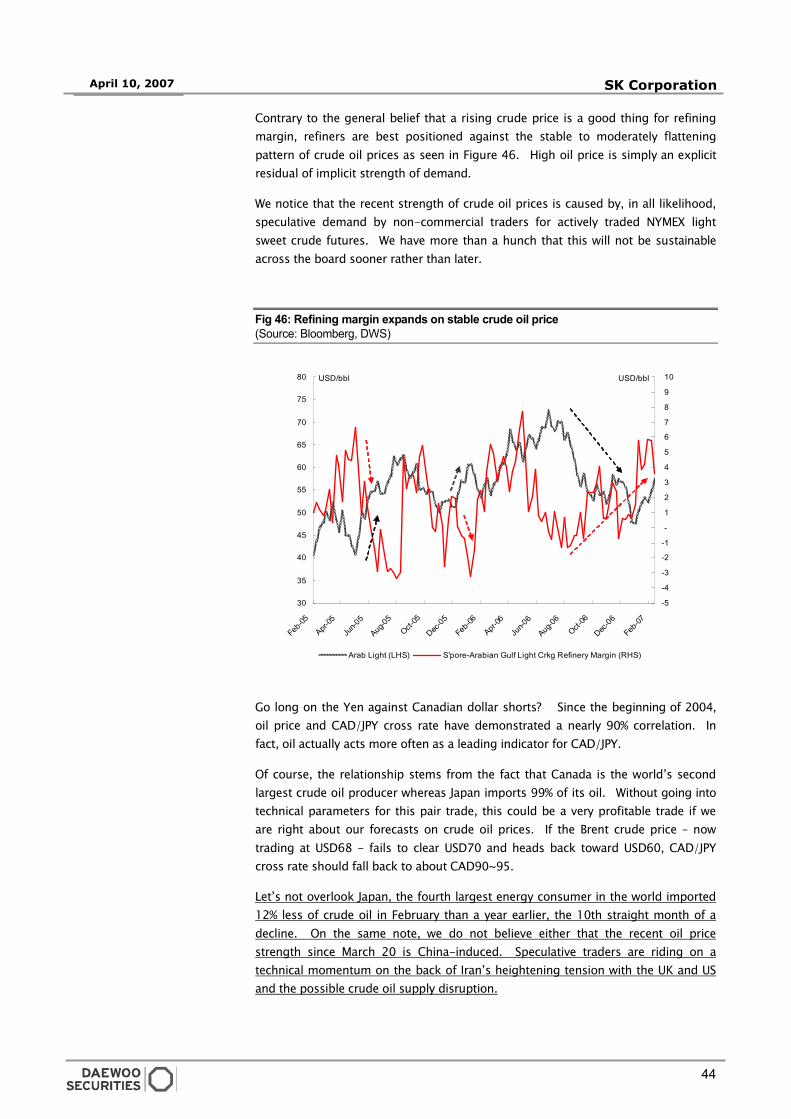

Atypical and Asymmetrical Opportunities for SK (Atypical and Asymmetrical Opportunities for SK (Atypical and Asymmetrical Opportunities for SK (Atypical and Asymmetrical Opportunities for SK (→→→→ PG PG PG PG 5~65~65~65~6, , , , 30~3230~3230~3230~32)))) ‘Reconfiguration’ of global supply chain – brought forth by the new manufacturing paradigm of ‘price=cost’ – is changing how corporations are doing business with one another in a profound fashion. Though not limited to Korea, ramifications will be more visibly pronounced in Korea due to ‘energy-intensive’ nature of its economy and co’s. Sustainable opportunities for excess economic rents – a situation that is atypical and asymmetrical by ‘convention’ - will continue to be conceded to SK.

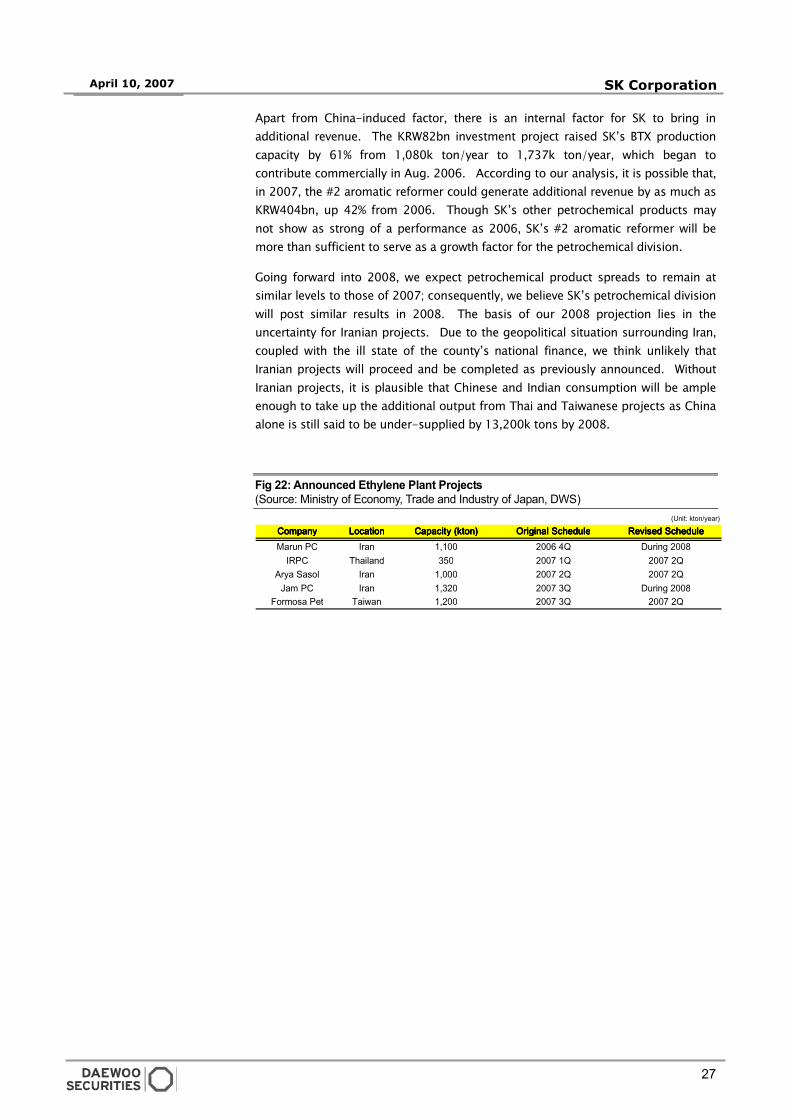

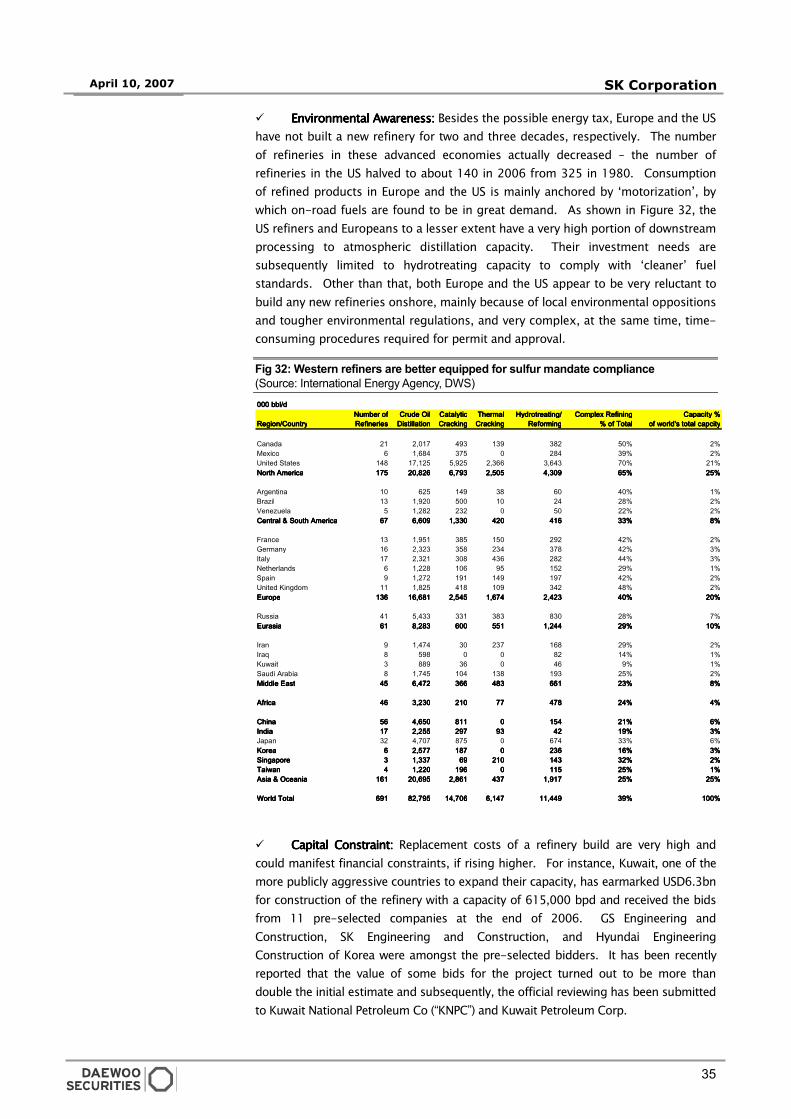

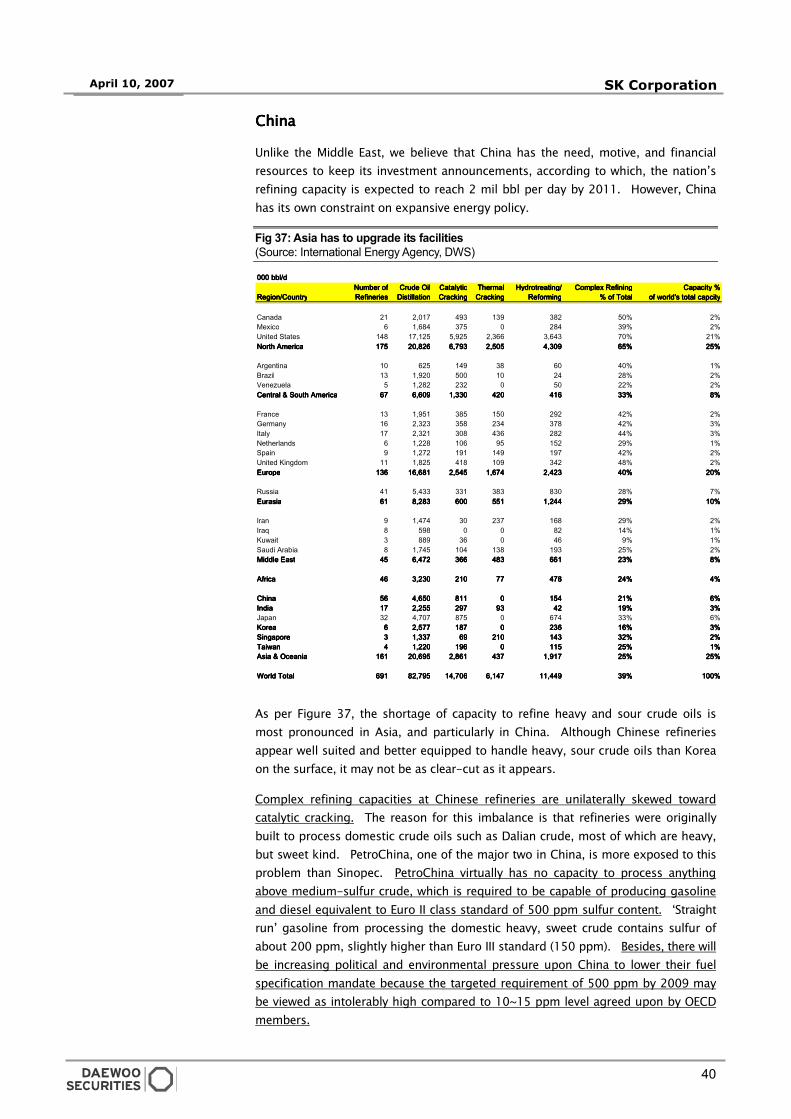

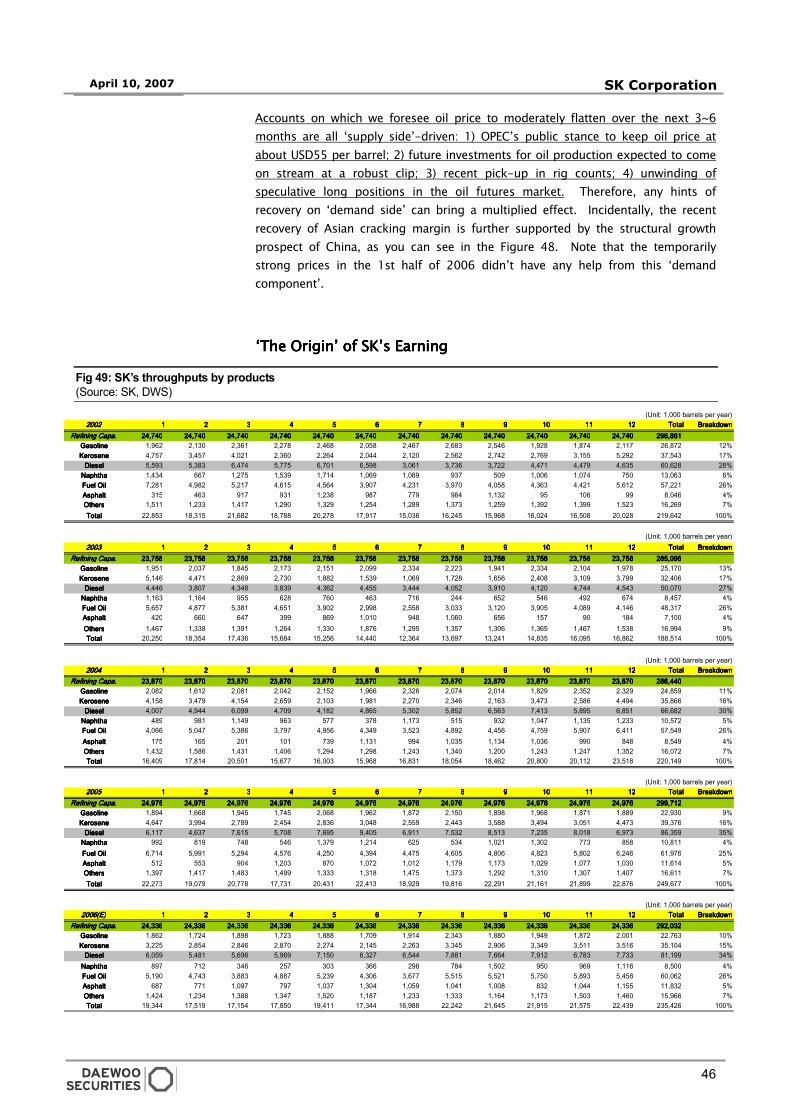

Supply Additions: Dilemma or the ‘CatchSupply Additions: Dilemma or the ‘CatchSupply Additions: Dilemma or the ‘CatchSupply Additions: Dilemma or the ‘Catch----22’? (22’? (22’? (22’? (→→→→ PG PG PG PG 7~87~87~87~8, , , , 33~4433~4433~4433~44)))) Complicated by a number of ‘circumstantial’ entry barriers, supply additions have not kept pace with the speed at which the demands (of emerging economies) are growing as well as the new mandates (of sulfur target) are taking effect. Counter to a casual expectation of capacity expansion, the Middle East and China are faced with their respective dilemma for capacity additions. A little too short, a little too late, outright capacity growth will continue to lag global oil demand growth.

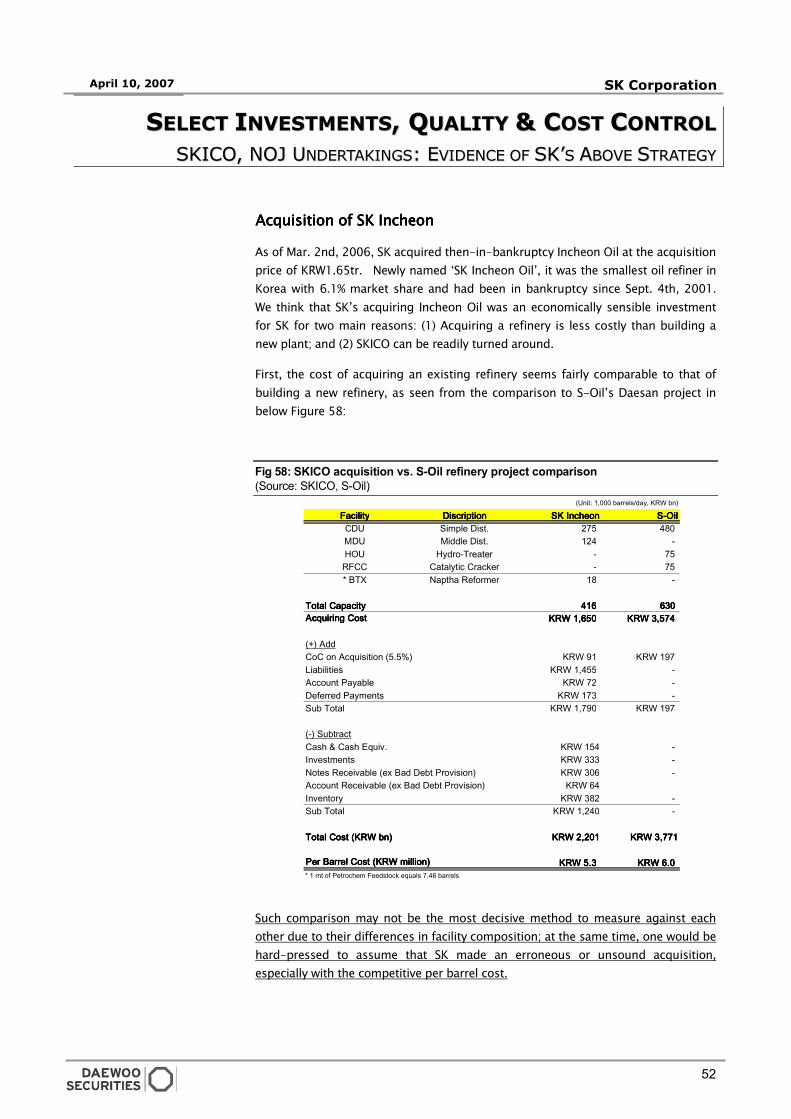

SKICO & NOJ: Characteristic of SK’s Growth Strategy (SKICO & NOJ: Characteristic of SK’s Growth Strategy (SKICO & NOJ: Characteristic of SK’s Growth Strategy (SKICO & NOJ: Characteristic of SK’s Growth Strategy (→→→→ PG PG PG PG 52525252)))) Acquisition of SK Incheon and alliance with Nippon Oil are well reflective of SK’s core strategy for selective expansion, quality control, and cost management. We believe both undertakings to be timely and value-generative, synchronously supporting the company’s Pan-Pacific strategic roadmap. (A related matter, we expect a delay for SK Incheon listing.)

We Are a Proponent of Primary Market Value (We Are a Proponent of Primary Market Value (We Are a Proponent of Primary Market Value (We Are a Proponent of Primary Market Value (→→→→ PG 2, 10 PG 2, 10 PG 2, 10 PG 2, 10~1~1~1~18)8)8)8) SK shares are trading at (‘economic’) book with cash yield of nearly 9% (PG2). Earnings visibility is set to rise on the back of earnings surprises to be expected throughout this year. With proliferation of buyout funds worldwide, we are betting that financial investors will soon decide to buy this attractive value name.

Worth W116,100~12Worth W116,100~12Worth W116,100~12Worth W116,100~122222,,,,999900/Shr…and a Consummate ‘Alpha’ Play00/Shr…and a Consummate ‘Alpha’ Play00/Shr…and a Consummate ‘Alpha’ Play00/Shr…and a Consummate ‘Alpha’ Play Our ‘primary’ market value-driven analysis makes it very hard to ignore SK shares even after share performances that are nothing short of being superlative over the last several years. SK is worth KRW116,100~122,900 per shr based on our reference scenario with our forecast range of KRW89,000~KRW134,000 over the next 12 months. More importantly, due to the asymmetry in economic rents to be appropriated by SK and Korea Inc, SK shares provide visible rewards in a market-neutral perspective. We have a strong conviction for an alpha-driven excess return of 20+% over the next 12 months.

Financial AbstractsFinancial AbstractsFinancial AbstractsFinancial Abstracts ConsolidatedConsolidatedConsolidatedConsolidated √√√√ Parent OnlyParent OnlyParent OnlyParent Only

(KRWbn, X, %)(KRWbn, X, %)(KRWbn, X, %)(KRWbn, X, %) 2004200420042004 2005200520052005 2006F2006F2006F2006F 2007200720072007((((FFFF)))) 2008200820082008((((FFFF))))

Sales/TurnoverSales/TurnoverSales/TurnoverSales/Turnover 17,406 21,915 23,652 24,269 25,344

EBIT*EBIT*EBIT*EBIT* 1,620 1,205 1,165 1,456 1,436 Cash EarningsCash EarningsCash EarningsCash Earnings 2,023 1,915 1,581 1,644 1,740 NOPAT NOPAT NOPAT NOPAT 1,153 981 982 1,062 1,061 NPAT NPAT NPAT NPAT 1,641 1,686 1,394 1,484 1,579 P/E P/E P/E P/E 4.4 4.0 6.7 8.1 7.6 EV/NOPAT EV/NOPAT EV/NOPAT EV/NOPAT 6.0 5.5 6.8 8.7 8.5 Price/BookPrice/BookPrice/BookPrice/Book 1.1 0.8 1.2 1.3 1.2 EV/Capital Employed EV/Capital Employed EV/Capital Employed EV/Capital Employed 0.9 0.6 0.8 1.1 0.9 Return on Equity Return on Equity Return on Equity Return on Equity 23.9 20.8 17.4 16.1 16.0 Return on Capital Employed Return on Capital Employed Return on Capital Employed Return on Capital Employed 15.0 11.9 11.6 12.3 10.9 (Core) Cash Yield(Core) Cash Yield(Core) Cash Yield(Core) Cash Yield 17.4 11.2 12.1 8.8 8.2

*Forecast EBIT stated are for ‘reported’ EBIT, which differ from ‘economic’ EBIT that we use for our analysis (DWS NM*Forecast EBIT stated are for ‘reported’ EBIT, which differ from ‘economic’ EBIT that we use for our analysis (DWS NM*Forecast EBIT stated are for ‘reported’ EBIT, which differ from ‘economic’ EBIT that we use for our analysis (DWS NM*Forecast EBIT stated are for ‘reported’ EBIT, which differ from ‘economic’ EBIT that we use for our analysis (DWS NM; P2; P2; P2; P2) and valuation) and valuation) and valuation) and valuation

SSSSTOCK TOCK TOCK TOCK SSSSUMMARYUMMARYUMMARYUMMARY Market Cap (KRWbn) 11,428

Market Cap (USDmn) 12,247

Major Shareholders SK C&C 11.16% TW Chey 0.97%

Foreign Ownership (%) Templeton 6.06%

Capital 5.01% Free Float (%) 61.8%

KKKKEYEYEYEY FFFFIGURES IGURES IGURES IGURES (07E)(07E)(07E)(07E) ROE (%) 16.1

RoCE (%) 12.3

EBIT Margin* (%) 6.0

SVA Spread (%) +5.1

SVA Spread (Trail 2yr Avg., %) +4.5

Cash Yield (%) 8.7

Dividend Yield (%) 2.0

LLLLIQUIDITYIQUIDITYIQUIDITYIQUIDITY SSSSUMMARYUMMARYUMMARYUMMARY Average Daily Volume (1M) 541,122

Average Turnover (1M, KRWbn) 47.3

Average Turnover (6M, KRWbn) 45.3

Daily High Turnover (1M, KRWbn) 92.2

Daily Low Turnover (1M, KRWbn) 17.8

RRRRISKISKISKISK SSSSUMMARYUMMARYUMMARYUMMARY Beta=0.86, Alpha=0.006

R-Squared =25%

Standard Error=0.03

Standard Error of Regression=0.2 Risk Summary figures are taken from a regression of the daily percent change in the share price (y-variable) against the daily percent change in the KOSPI 200 (x-variable) for the trailing 52 weeks (245 days).

CCCCORPORATEORPORATEORPORATEORPORATE AAAACTIONCTIONCTIONCTION

Share Buyback

13 mln shrs

10/06~01/07

Estimate Dividend Per Share KRW2,000

~ KRW2,300

Next Earning Announcement Apr. 26

(27)

CCCCOMPANYOMPANYOMPANYOMPANY DDDDESCRIPTIONESCRIPTIONESCRIPTIONESCRIPTION SK refines, markets, and distributes oil. The company produces a variety of petroleum products such as petroleum, kerosene, liquefied petroleum gas (LPG), and diesel oil. SK also manufactures petrochemical products, including ethylene, benzene, paraxylene, synthetic resins, and styrene monomer. Controlling company for SK Group, SK provides financial services through subsidiaries. Primary Market: Korea/Asia

Primary Product: Petroleum &

Petrochemical Primary Raw Material: Crude Oil

Export/Total Sales: 46% by Volume

2

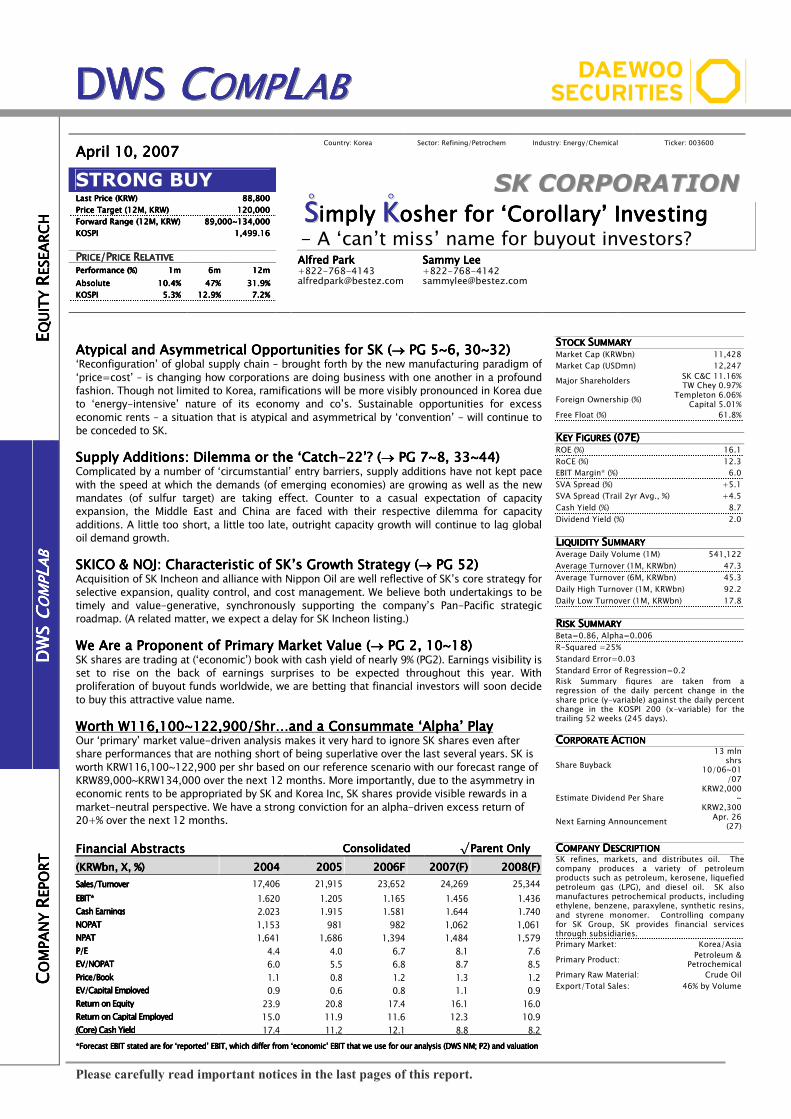

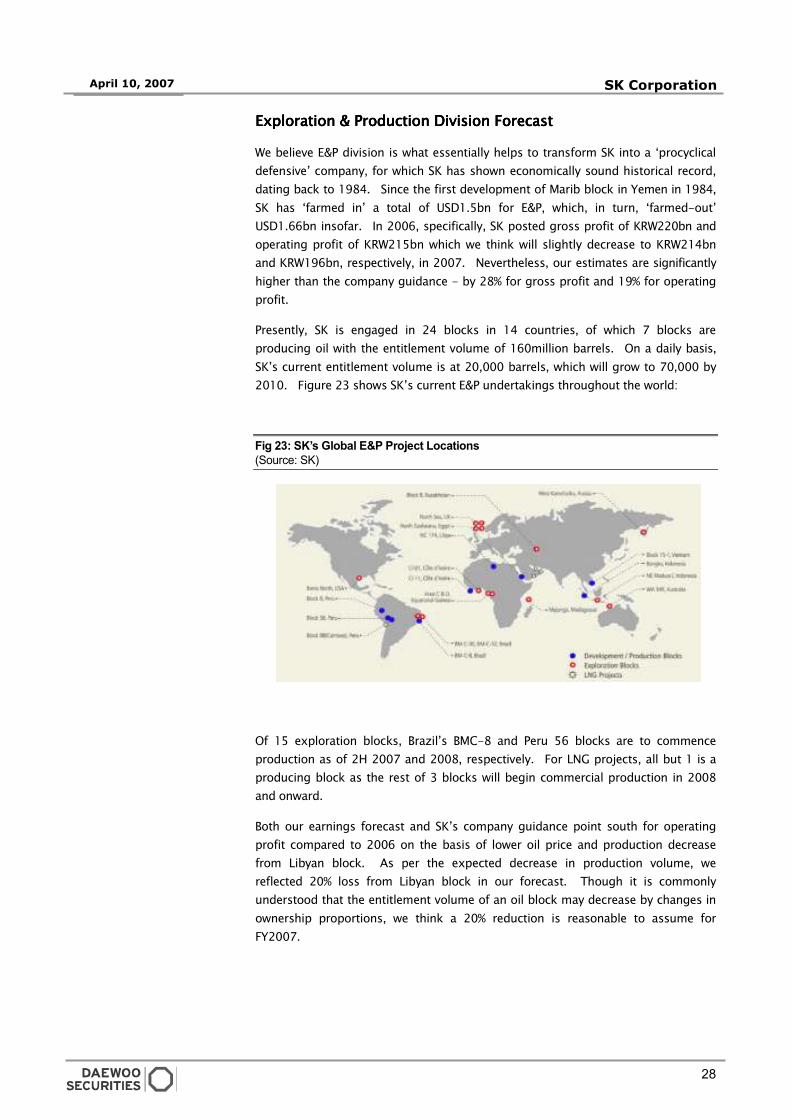

April 10, 2007 SK Corporation

These will not be ignored for long… These will not be ignored for long… These will not be ignored for long… These will not be ignored for long…

DWS NumberMill

(KRW Million, X) FY1997FY1997FY1997FY1997 FY1998FY1998FY1998FY1998 FY1999FY1999FY1999FY1999 FY2000FY2000FY2000FY2000 FY2001FY2001FY2001FY2001 FY2002FY2002FY2002FY2002 FY2003FY2003FY2003FY2003 FY2004FY2004FY2004FY2004 FY2005FY2005FY2005FY2005 FY2006FY2006FY2006FY2006 FY2007FY2007FY2007FY2007 FY2008FY2008FY2008FY2008

▶▶▶▶ PROFIT & LOSSTurnover/Sales 10,756,534 11,048,787 11,237,096 14,021,615 14,114,862 13,388,151 13,788,626 17,406,063 21,914,582 23,651,503 24,369,068 25,343,831

Gross Profit 2,646,327 1,463,396 1,463,920 1,677,285 1,378,742 1,294,171 1,772,282 2,694,096 2,325,071 2,374,326 2,665,000 3,013,582 (% of Sales) 24.6% 13.2% 13.0% 12.0% 9.8% 9.7% 12.9% 15.5% 10.6% 10.0% 10.9% 11.9%

SG&A 562,832 594,366 671,407 679,118 813,380 905,976 1,100,998 1,073,605 1,120,169 1,208,953 1,109,140 1,464,601 (% of Gross Profit) 21.3% 40.6% 45.9% 40.5% 59.0% 70.0% 62.1% 39.9% 48.2% 50.9% 41.6% 48.6%

EBITDA 2,796,678 1,537,162 1,295,557 1,470,296 1,038,460 894,667 1,141,949 2,099,002 1,665,449 1,591,674 2,012,221 2,026,362 EBIT 2,083,495 869,029 792,512 998,167 565,361 388,195 671,284 1,620,490 1,204,902 1,165,373 1,555,860 1,548,981

(% of Sales) 19.4% 7.9% 7.1% 7.1% 4.0% 2.9% 4.9% 9.3% 5.5% 4.9% 6.4% 6.1%Non-Operating Income Adjustment 323,332 669,537 319,775 215,618 185,885 421,693 286,877 596,585 334,350 464,458 338,557 340,492 Non-Operating Expense Adjustment 1,792,639 643,537 209,580 648,495 444,072 279,476 301,977 396,653 322,547 382,059 345,568 347,844 Other Non-Cash Items 43,291 75,553 47,331 44,361 66,966 87,462 405,966 61,929 90,439 69,106 61,379 63,922 Bad Debt Expenses (Cash Base) 5,909 7,306- 2,638- 232 0- 1,786 112,486 230,058 26,364 112 92,255 87,197 Severance Pay (Cash Base) 30,264 146,866 20,004 12,313 43,904 39,097 45,479 59,642 43,776 64,839 53,434 55,423

EBIT - Adjusted 621,306 831,022 932,673 597,106 330,236 576,991 904,185 1,592,651 1,237,004 1,251,927 1,464,539 1,462,931 (% of Sales) 5.8% 7.5% 8.3% 4.3% 2.3% 4.3% 6.6% 9.1% 5.6% 5.3% 6.0% 5.8%

Less: Adjusted Tax (1) 191,390 255,160 287,343 192,980 84,428 149,190 248,991 439,246 256,004 269,704 402,748 402,306 Plus: Amortization of Goodwill - - - - - - - - - - - - NOPAT 429,916 575,862 645,331 404,127 245,808 427,801 655,194 1,153,405 981,000 982,224 1,061,791 1,060,625

(% of Sales) 4.0% 5.2% 5.7% 2.9% 1.7% 3.2% 4.8% 6.6% 4.5% 4.2% 4.4% 4.2%Net Income 20,125 126,319 345,038 144,770 91,215 136,846 15,169 1,640,738 1,686,496 1,394,024 1,484,442 1,579,033

(% of Sales) 0.2% 1.1% 3.1% 1.0% 0.6% 1.0% 0.1% 9.4% 7.7% 5.9% 6.1% 6.2%Cash Earning (2) 688,318 760,162 814,090 532,146 494,759 573,785 393,156 2,023,159 1,914,568 1,580,684 1,643,915 1,740,607

▶▶▶▶ BALANCE SHEETTotal Assets 12,649,458 13,706,929 14,170,005 15,110,086 14,241,505 13,506,819 15,030,315 14,859,953 17,382,134 19,988,199 21,756,828 22,887,147

Cash 788,486 465,017 67,263 251,099 411,049 245,212 889,865 334,816 1,376,802 1,312,767 1,923,337 2,244,806 (Operating Cash) 2% 215,131 220,976 125,553 265,889 282,297 267,763 275,773 348,121 438,292 473,030 487,381 506,877 Working Capital (Core) 3,165,122 2,722,987 2,635,896 2,154,702 1,728,120 2,601,398 2,352,525 2,759,080 3,168,003 3,057,431 3,239,545 3,408,620 (% Of Capital Employed) 37.6% 28.9% 35.7% 28.2% 23.1% 41.3% 30.2% 36.6% 35.2% 38.5% 34.7% 33.5%Adjusted Working Capital 2,519,809 2,726,002 2,506,177 2,199,578 1,667,318 1,889,729 2,205,194 2,243,855 2,570,335 2,657,056 2,752,164 2,901,743 Other CA-CL 663,669- 969,566- 2,043,598- 1,522,813- 1,098,042- 1,546,627- 891,971- 946,529- 1,205,562- 1,907,309- 2,088,179- 2,160,201- Net Property, Plant & Equipment 4,995,154 7,066,119 6,608,559 6,513,114 6,301,482 6,028,559 5,803,663 5,616,587 5,194,340 5,331,671 6,053,943 6,482,024 (% Of Capital Employed) 59.3% 75.1% 89.6% 85.3% 84.2% 95.6% 74.4% 74.4% 57.7% 67.1% 64.9% 63.6%Other Operating Assets 111,469 104,347 87,143 218,458 125,057 150,168 152,863 154,884 444,945 130,298 162,612 172,263 (% Of Capital Employed) 1.3% 1.1% 1.2% 2.9% 1.7% 2.4% 2.0% 2.1% 4.9% 1.6% 1.7% 1.7%Other Non-Int Liabilities 7,988 1,582 - - - 1,195,215 770,000 400,000 - - - - Allowance for Bad debt 29,487 26,094 23,286 18,601 13,174 22,282 264,553 25,800 25,737 25,093 31,316 38,330 Cumulative Goodwill Amortization - - - - - - - - - - - -

(Core) Capital Employed 8,418,062 9,413,416 7,378,550 7,633,162 7,480,841 6,305,777 7,801,497 7,544,638 9,004,264 7,949,952 9,322,574 10,185,843 (% Gr Rate) 24.1% 11.8% -21.6% 3.5% -2.0% -15.7% 23.7% -3.3% 19.3% -11.7% 17.3% 9.3%

Average Capital Employed 7,600,717 8,915,739 8,395,983 7,505,856 7,557,001 6,893,309 7,053,637 7,673,067 8,274,451 8,477,108 8,636,263 9,754,209 (% Gr Rate) 31.4% 17.3% -5.8% -10.6% 0.7% -8.8% 2.3% 8.8% 7.8% 2.4% 1.9% 12.9%

(Shareholder Funds) 2,137,554 4,167,500 5,895,020 6,054,246 5,665,540 5,037,079 5,415,256 6,873,949 8,110,561 8,031,043 9,208,415 9,876,240

▶▶▶▶ CASH FLOWOperating Cash Flow 139,191 2,070,207 1,802,430 955,536 405,279 234,317- 452,071 1,108,597 1,045,148 1,818,460 841,284 595,513

Net Income 20,125 126,319 345,038 144,770 91,215 136,846 15,169 1,640,738 1,686,496 1,394,024 1,484,442 1,579,033 Depreciation 445,799 451,008 485,562 454,053 449,501 443,326 445,809 459,176 440,590 422,521 456,361 477,381 ∆Core Working Capital 909,053- 442,135 87,092 481,193 426,583 873,279- 248,874 406,555- 408,924- 110,572 182,114- 169,074- (∆Adjusted Working Capital) 762,394 206,192 219,825- 306,599- 532,260- 222,411 315,465 38,661 326,480 86,721 95,108 149,579 Other - Net Addbacks 582,319 1,050,744 884,738 124,481- 562,021- 58,789 257,781- 584,762- 673,015- 108,658- 494,753- 773,419-

Cash Flows from Investing 623,100- 1,250,927- 732,426- 1,098,921- 106,650- 1,303,859 1,071,171- 344,803- 517,468- 1,253,062- 577,241- 469,534- ∆CAPEX (PPE) 622,197- 492,328- 270,716- 400,561- 275,889- 251,901- 451,945- 301,006- 597,688- 702,171- 556,005- 357,340- Asset Sale 7,943 18,723 99,058 2,695 3,044 2,735 24,940 5,547 254,268 240,335 - - ∆Investments 132,966- 431,184- 1,069,717- 796,686- 54,429 1,505,346 735,766- 73,217- 199,005- 1,223,648- 21,236- 112,194-

Cash Flows from Financing 1,100,980 1,145,064- 1,467,758- 327,221 138,679- 1,235,379- 1,263,753 1,318,843- 514,306 629,432- 346,526 195,489 Dividend 44,990 34,289 33,993 84,754 69,555 69,533 92,678 96,091 232,476 239,641 296,888 315,807 ∆Debt 1,253,933 696,025- 1,823,161- 755,209 26,041- 1,113,532- 426,219 1,020,332- 1,028,872 1,022,447 614,646 244,748 Others 107,963- 414,750- 380,797- 343,234- 43,083- 52,314- 930,212 200,228- 282,090- 1,412,238- 28,769 266,548

∆Cash (+) or Net Debt 617,071 325,785- 397,754- 183,836 159,950 165,837- 644,654 555,050- 1,041,986 64,034- 610,570 321,468 Cash (Beginning) 173,731 790,801 465,017 67,263 251,099 411,049 245,212 889,865 334,816 1,376,802 1,312,767 1,923,337 Cash (Ending) 790,801 465,017 67,263 251,099 411,049 245,212 889,865 334,816 1,376,802 1,312,767 1,923,337 2,244,806 Reconciled 64,034- 610,570 321,468

Free Cash Flow 380,210- 1,212,525 1,055,713 952,739 861,996 201,060- 936,840 922,676 681,093 1,047,497 758,796 899,398 Free Cash Flow - Adjusted (3) 233,551- 564,198 1,188,446 778,145 967,674 449,807 372,501 1,290,570 763,537 850,204 845,803 918,893 Discretionary Cash Flow (4) 80,383 644,990 999,422 761,523 860,285 333,392 419,890 1,208,591 600,627 809,064 815,328 739,906 ∆ Cash (+) or Net Debt (-) 615,256 323,470- 397,754- 183,836 159,950 165,837- 644,654 555,050- 1,041,986 64,034- 610,570 321,469

▶▶▶▶ RATIOS

Cash Yield (5) 2.8% 8.7% 12.6% 10.5% 11.5% 5.5% 8.3% 13.5% 9.1% 9.4% 8.0% 7.7%Core Cash Yield (6) 1.1% 10.0% 22.8% 30.0% 31.2% 10.9% 9.9% 17.4% 11.2% 12.1% 8.8% 8.2%Dividend Pool Ratio (7) 7.9% 12.3% 16.5% 31.3% 30.2% 43.1% 10.4% 26.9% 50.8% 48.3% 46.3% 52.5%Debtor Turn Days 82.4 86.9 73.7 47.8 34.3 40.1 47.0 36.0 32.2 30.9 30.7 30.9 Inventory Held Days 17.1 18.0 19.9 19.3 20.9 22.1 32.0 33.6 30.9 35.4 40.0 40.3 Payable Days 14.0 14.8 12.1 9.8 12.1 10.7 20.6 22.5 20.3 25.3 29.5 29.4 Cash Conversion Days 85.5 90.1 81.4 57.3 43.1 51.5 58.4 47.1 42.8 41.0 41.2 41.8 Net Profit GR -70.5% 527.7% 173.1% -58.0% -37.0% 50.0% -88.9% 10716.3% 2.8% -17.3% 6.5% 6.4%NOPAT GR 23.3% 33.9% 12.1% -37.4% -39.2% 74.0% 53.2% 76.0% -14.9% 0.1% 8.1% -0.1%Total Asset GR 29.9% 8.4% 3.4% 6.6% -5.7% -5.2% 11.3% -1.1% 17.0% 15.0% 9.5% 5.5%Sales GR 1 yr. 29.3% 2.7% 1.7% 24.8% 0.7% -5.1% 3.0% 26.2% 25.9% 7.9% 3.0% 4.0%

3 yr. 22.4% 18.8% 10.5% 9.2% 8.5% 6.0% -0.6% 7.2% 17.9% 19.7%5 yr. 17.9% 15.7% 13.9% 16.3% 11.1% 4.5% 4.5% 9.1% 9.3% 10.9%

Average Capital GR 1 yr. 31.3% 17.4% -5.2% -11.0% -0.7% -4.9% 5.2% 5.1% 4.3% 0.0% 1.9% 12.9%3 yr. 26.1% 26.2% 13.5% -0.3% -5.7% -5.6% -0.2% 1.7% 4.9% 3.1%5 yr. 19.5% 21.0% 17.4% 11.2% 5.3% -1.3% -3.5% -1.4% 1.7% 1.9%

Stated ROE 0.9% 3.0% 5.9% 2.4% 1.6% 2.7% 0.3% 23.9% 20.8% 17.4% 16.1% 16.0%ROCE - Normalized 5.7% 6.5% 7.7% 5.4% 3.3% 6.2% 9.3% 15.0% 11.9% 11.6% 12.3% 10.9%

Capital Turn 1.5 1.3 1.4 1.9 1.9 1.9 1.9 2.3 2.7 3.0 2.8 2.6 EBIT Margin 19.4% 7.9% 7.1% 7.1% 4.0% 2.9% 4.9% 9.3% 5.5% 4.9% 6.4% 6.1%NOPAT Margin 4.0% 5.2% 5.7% 2.9% 1.7% 3.2% 4.8% 6.6% 4.5% 4.2% 4.4% 4.2%Net Profit Margin 0.2% 1.1% 3.1% 1.0% 0.6% 1.0% 0.1% 9.4% 7.7% 5.9% 6.1% 6.2%

Incremental ROCE 4.5% 11.1% -13.4% 27.1% -309.5% -27.4% 141.8% 80.4% -28.7% 0.6% 50.0% -0.1%Weighted Cost of Capital 18.5% 11.9% 15.3% 12.5% 12.3% 8.6% 7.3% 8.1% 7.3% 7.1% 7.2% 7.2%

▶▶▶▶ SHAREHOLDER VALUE-ADDEDShareholder Value-Added 979,725- 484,162- 639,997- 533,364- 684,087- 166,911- 141,967 530,991 379,539 380,349 439,980 358,322 Mid-Cycle Market Value-Added 312,042 47,875- 31,903 52,663 46,287 16,140- 110,244 334,051 206,709 437,377 618,130 532,114 Mid-Cycle MVA ex Non-Operating Asset 23,160- 289,787- 613,039- 620,694- 591,026- 330,065- 205,276- 58,989- 211,516- 128,771- 42,479 51,615- Primary Mkt P/E - Core Capital (8) 17.4 11.2 6.8 6.3 11.2 7.2 6.5 6.0 5.5 6.8 8.7 8.5 Primary Mkt P/E - Total Capital (9) 21.6 14.8 10.7 11.7 15.0 25.0 21.8 6.0 6.5 7.7 9.1 9.5 Accounting P/E 48.8 9.5 8.9 12.2 20.8 12.2 229.4 4.4 4.0 6.7 8.1 7.6 Primary Mkt P/B (10) 1.0 0.7 0.5 0.3 0.4 0.4 0.6 0.9 0.6 0.8 1.1 0.9 Accounting P/B 0.5 0.3 0.5 0.3 0.3 0.3 0.6 1.1 0.8 1.2 1.3 1.2 Equity Value (Common Stock) 983,054 1,201,511 3,086,295 1,764,505 1,897,795 1,662,951 3,479,055 7,286,775 6,703,974 9,393,284 11,967,102 11,967,102 Value of Preferred Stock 10,140 6,888 24,190 18,749 15,116 19,817 16,119 56,083 85,960 75,270 81,430 81,430 Net Debt Value 8,290,038 7,304,671 5,493,897 6,144,235 6,020,256 5,023,464 5,073,626 4,448,363 4,328,261 5,168,793 5,172,870 5,096,150 Firm Value 9,283,232 8,513,069 8,604,382 7,927,489 7,933,166 6,706,231 8,568,801 11,791,221 11,118,195 14,637,347 17,221,402 17,144,682 Firm Value ex Non-Operating Asset 7,475,842 6,478,376 4,391,504 2,536,374 2,753,897 3,067,521 4,232,387 6,945,852 5,364,571 6,663,431 9,226,250 9,037,335 MVA 1,682,515 402,670- 208,399 421,633 376,165 187,078- 1,515,163 4,118,153 2,843,744 6,160,239 8,585,139 7,390,473 MVA ex Non-Operating Asset 124,875- 2,437,363- 4,004,479- 4,969,481- 4,803,104- 3,825,789- 2,821,250- 727,216- 2,909,880- 1,813,677- 589,987 716,874-

(1) Tax Paid (cash)+Tax Shield(2) NOPAT+Depreciation+Amortization-Cash Dividend(3) NOPAT+Depreciation+Amortization+Other Non-Cash Items+Asset Sales-PPE CAPEX-Investment-∆Adjusted Working Capital-Cash Dividend(4) NOPAT+Depreciation+Amortization+Other Non-Cash Items-Maintenance CAPEX-∆Adjusted Working Capital-Cash Dividend(5) (Discretionary Cash Flow+Expected Yield from Non Operating Investment Asset)/Firm Value(6) Discretionary Cash Flow/Firm Value excluding Non-Operating Asset(7) (Retained Earning-Compulsory Reserve)/Market Value of Equity(8) NOPAT/Firm Value excluding Non Operating Asset(9) (Consolidated NOPAT- Minority Interest)/Firm Value(10) Firm Value exluding Non Operating Asset/Average Capital Employed for Core Operation

*Based on April 9 closing

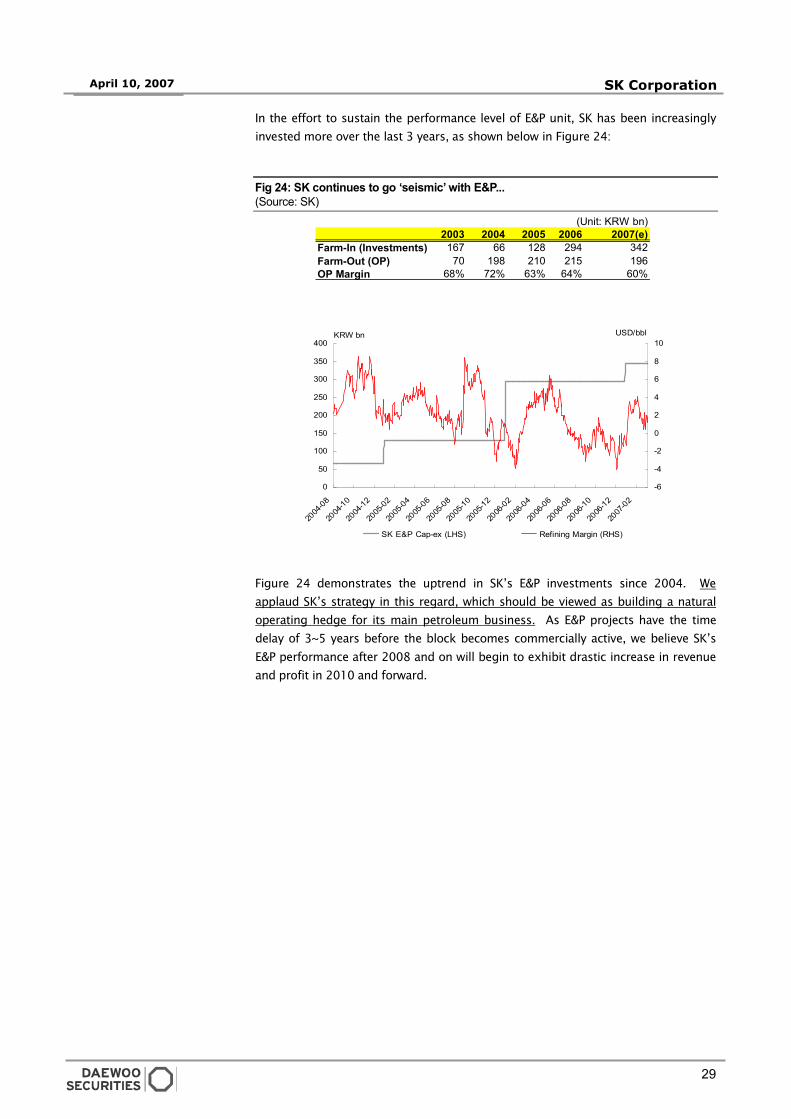

SK will put in more capital for core operation, pulling down RoCE…healthy and temporary!SK will put in more capital for core operation, pulling down RoCE…healthy and temporary!SK will put in more capital for core operation, pulling down RoCE…healthy and temporary!SK will put in more capital for core operation, pulling down RoCE…healthy and temporary!

Once again, buyout guys must be thinkin’ ‘trading at book’Once again, buyout guys must be thinkin’ ‘trading at book’Once again, buyout guys must be thinkin’ ‘trading at book’Once again, buyout guys must be thinkin’ ‘trading at book’?!?!?!?!?!?!?!?!

With the share buyback mechanically harder, SK should aWith the share buyback mechanically harder, SK should aWith the share buyback mechanically harder, SK should aWith the share buyback mechanically harder, SK should and will up its dividend payout nd will up its dividend payout nd will up its dividend payout nd will up its dividend payout

Onset of a midOnset of a midOnset of a midOnset of a mid----cycle breakout in 2007… cycle breakout in 2007… cycle breakout in 2007… cycle breakout in 2007…

3

April 10, 2007 SK Corporation

Investment ThesisInvestment ThesisInvestment ThesisInvestment Thesis....................................................................................................................................................................................................................................................4444

Atypical and Asmmetrical Opportunities for ExceAtypical and Asmmetrical Opportunities for ExceAtypical and Asmmetrical Opportunities for ExceAtypical and Asmmetrical Opportunities for Excess Economic Rentsss Economic Rentsss Economic Rentsss Economic Rents................................ 4444

Financial Analysis and ValuationFinancial Analysis and ValuationFinancial Analysis and ValuationFinancial Analysis and Valuation ........................................................................................................................................................10101010

What Causes SK’s Share Price to Behave the Way It Does?What Causes SK’s Share Price to Behave the Way It Does?What Causes SK’s Share Price to Behave the Way It Does?What Causes SK’s Share Price to Behave the Way It Does? .................................................................................... 10101010

2007 Operating Performance2007 Operating Performance2007 Operating Performance2007 Operating Performance ........................................................................................................................................................................21212121

Surprise! Surprise! Surprise!Surprise! Surprise! Surprise!Surprise! Surprise! Surprise!Surprise! Surprise! Surprise! ............................................................................................................................................................................................................................................................ 21212121

Demand VersDemand VersDemand VersDemand Versus Supplyus Supplyus Supplyus Supply ............................................................................................................................................................................................................30303030

Will supply additions be the culprit of margin contraction?Will supply additions be the culprit of margin contraction?Will supply additions be the culprit of margin contraction?Will supply additions be the culprit of margin contraction? ............................................................................ 30303030

Verdict Upon Supply AdditionsVerdict Upon Supply AdditionsVerdict Upon Supply AdditionsVerdict Upon Supply Additions ................................................................................................................................................................39393939

Simply a Dilemma or The Case of ‘CatchSimply a Dilemma or The Case of ‘CatchSimply a Dilemma or The Case of ‘CatchSimply a Dilemma or The Case of ‘Catch----22’?22’?22’?22’? .................................................................................................................................................... 39393939

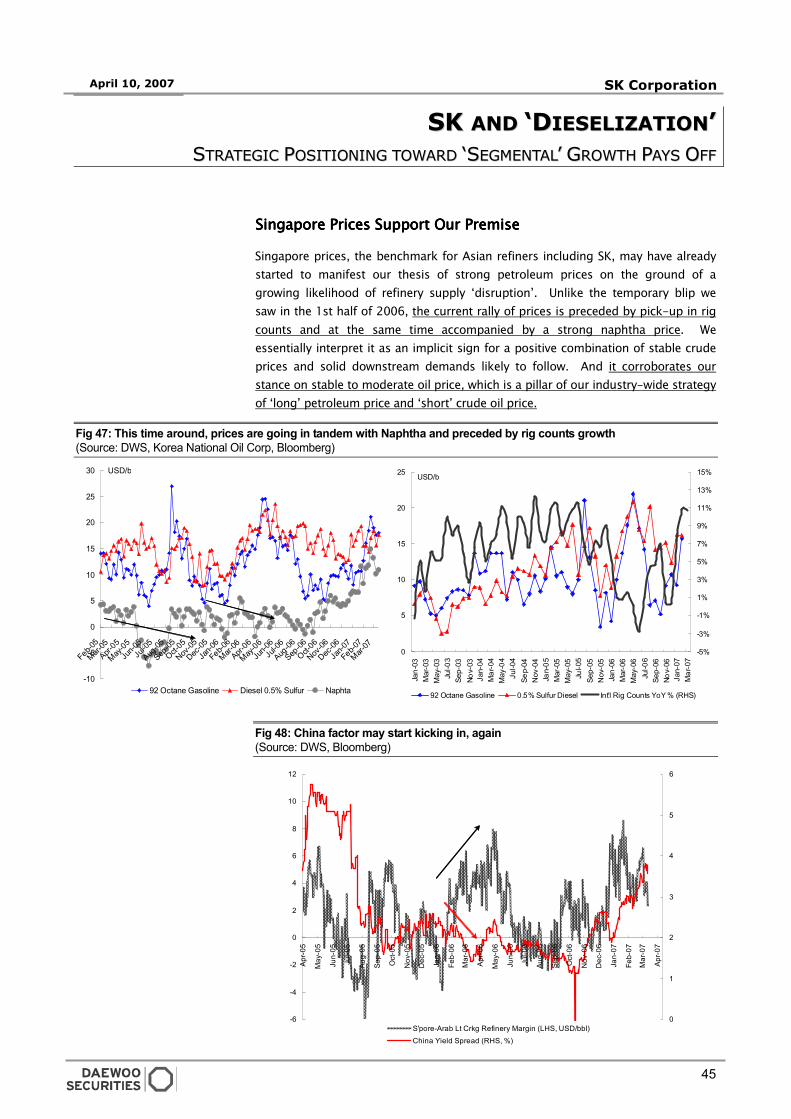

SK and ‘Dieselization’SK and ‘Dieselization’SK and ‘Dieselization’SK and ‘Dieselization’ ....................................................................................................................................................................................................................45454545

StraStraStraStrattttegiegiegiegic Positioning toward ‘Segmental’ Growth Pays Offc Positioning toward ‘Segmental’ Growth Pays Offc Positioning toward ‘Segmental’ Growth Pays Offc Positioning toward ‘Segmental’ Growth Pays Off ................................................................................ 45454545

Select Investments, QualitySelect Investments, QualitySelect Investments, QualitySelect Investments, Quality & & & & Cost ControlCost ControlCost ControlCost Control ............................................................................................52525252

SKICOSKICOSKICOSKICO,,,, NOJ Undertakings NOJ Undertakings NOJ Undertakings NOJ Undertakings: Evid: Evid: Evid: Evidence ence ence ence of SK’s Above Strategyof SK’s Above Strategyof SK’s Above Strategyof SK’s Above Strategy............................................................................ 52525252

ConclusionConclusionConclusionConclusion....................................................................................................................................................................................................................................................................................55555555

Table of Table of Table of Table of ContentContentContentContentssss

4

April 10, 2007 SK Corporation

2%

4%

6%

8%

10%

12%

14%

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Energy Consumption/GDP (LHS) SK Corp Share Price (KRW, RHS)

(Consolidated) gross margin of 9~13%

(Consolidated) gross margin of 15~20%

DeepDeepDeepDeepValue!!Value!!Value!!Value!!

New cyclical lower limit

New reference mid-cycle level of energy intensity

Shr px overshootShr px overshootShr px overshootShr px overshoot

IINNVVEESSTTMMEENNTT TTHHEESSIISS

AATTYYPPIICCAALL AANNDD AASSMMMMEETTRRIICCAALL OOPPPPOORRTTUUNNIITTIIEESS FFOORR EEXXCCEESSSS EECCOONNOOMMIICC RREENNTTSS

‘Structural Driver’ behind S‘Structural Driver’ behind S‘Structural Driver’ behind S‘Structural Driver’ behind SK’s PerformanceK’s PerformanceK’s PerformanceK’s Performance

SK Corporation (“SK” hereafter), one of my most favorite names for the last few years,

decisively outperformed the KOSPI200 by 36% over the last 4 months since its

reiteration as one of the ‘stalwart’ focus names for the year of 2007 in my previous

publication on investment strategy, <Comes 2007, Looms Sinister Twilight> dated

December 7, 2006. SK’s share price already exceeded the analysts’ weighted

consensus target price of KRW 82,633 per share (based on analysts’ target price

during the last 12 months).

In our effort to establish our investment opinion beyond a simple valuation call, we

undertake intensive studies into discovering ‘organic’ elements of a company that

are centrally subject to be researched, in order to derive the ‘corollary’ awaiting the

company in the upcoming cycle(s). By ‘corollary’ investing, we are referring to an

investing strategy, in which we seek to capitalize on the total sum of shareholder

value-added (thus ‘economic’ MVAs) on the basis of the ‘eventual’ - or ‘inevitable’-

results that are likely to be consummated along the line of the law and dynamics of

the market. In this respect, SK shares present a very convincing case whereby the

company should upstage the broad market with a clearly more visible mid-cycle

growth in a market-neutral perspective under today’s market conditions that

presumably guarantee the absence of arbitrage. As the word ‘corollary’ connotes

very little explicit guideline for the timeline to the point of materialization of the

shareholder value-added, we may not be entirely free of the risk of over-extended

lockup or temporary correction. However, we conclude that the reward, supported

by a high earnings visibility, significantly outweigh the risks.

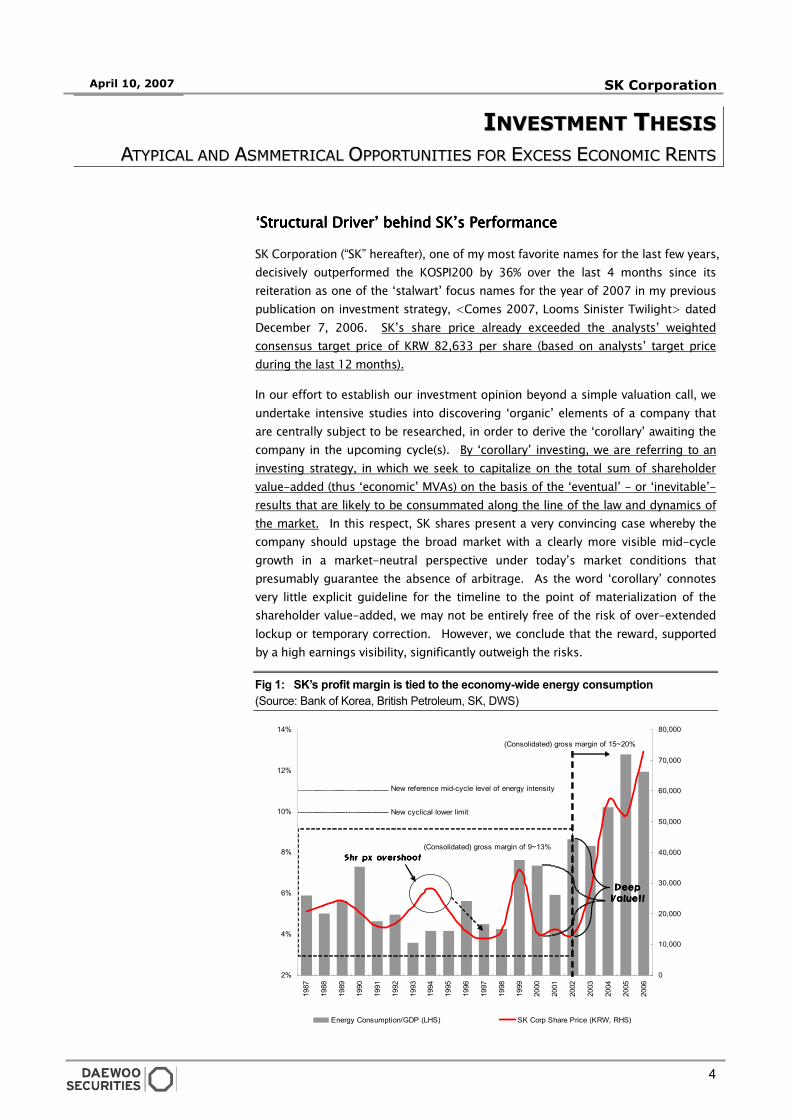

Fig 1: SK’s profit margin is tied to the economy-wide energy consumption

(Source: Bank of Korea, British Petroleum, SK, DWS)

5

April 10, 2007 SK Corporation

-

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

2000

2001

2002

2003

2004

2005

2006

2

3

4

5

6

7

8

Energy Intensity Coefficient (LHS) Korea Output Real Growth (%, RHS)

Reference level of US' energy intensity Coefficient (0.3~0.4)

SK’s gross margin expansion has been closely, if not directly, tied to the economy-

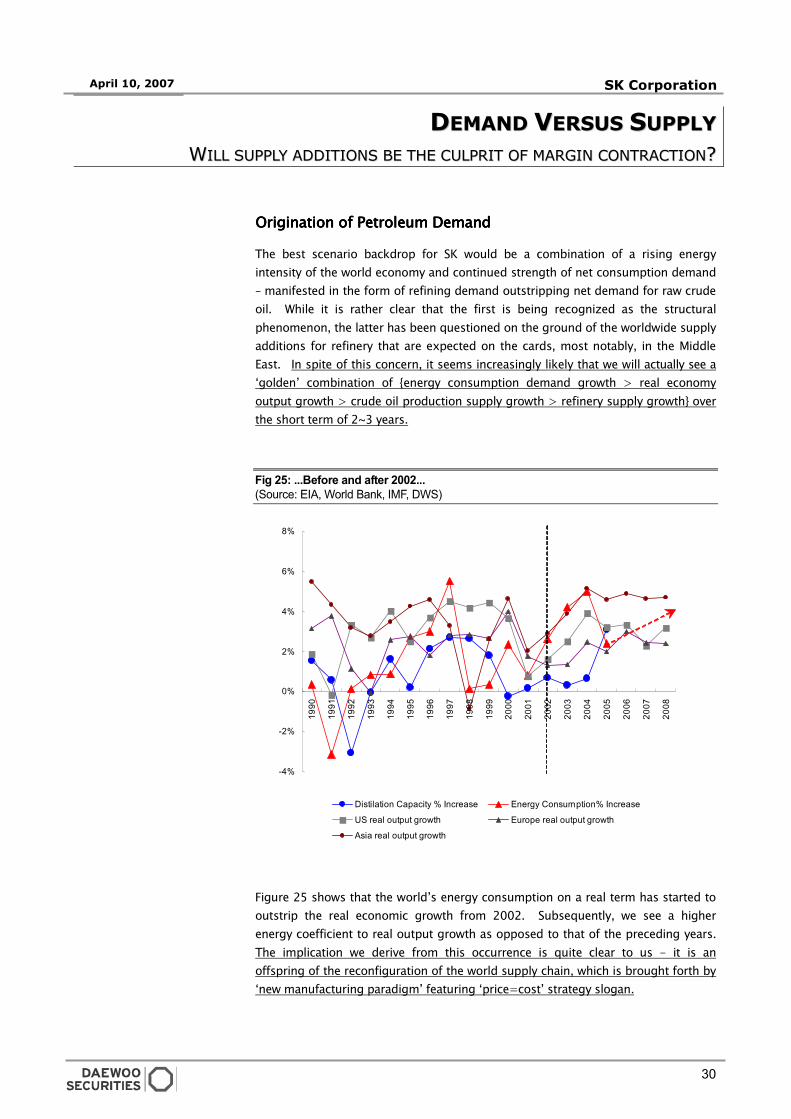

wide increase in energy consumption of Korea Inc. As Figure 1 illustrates, SK’s

shares offered a ‘deep value’ at the end of 2002 while the company-level financial

numbers synchronously supported this case of turnaround at the end of the 1st half

of 2003. This case of ‘deep value’ was warranted of its due rerating in the 2nd half

of 2003 and thereafter.

One might challenge that our premise aforementioned may be short of valid on the

ground of ‘supernormal’ oil price having an inflationary effect on nominal energy

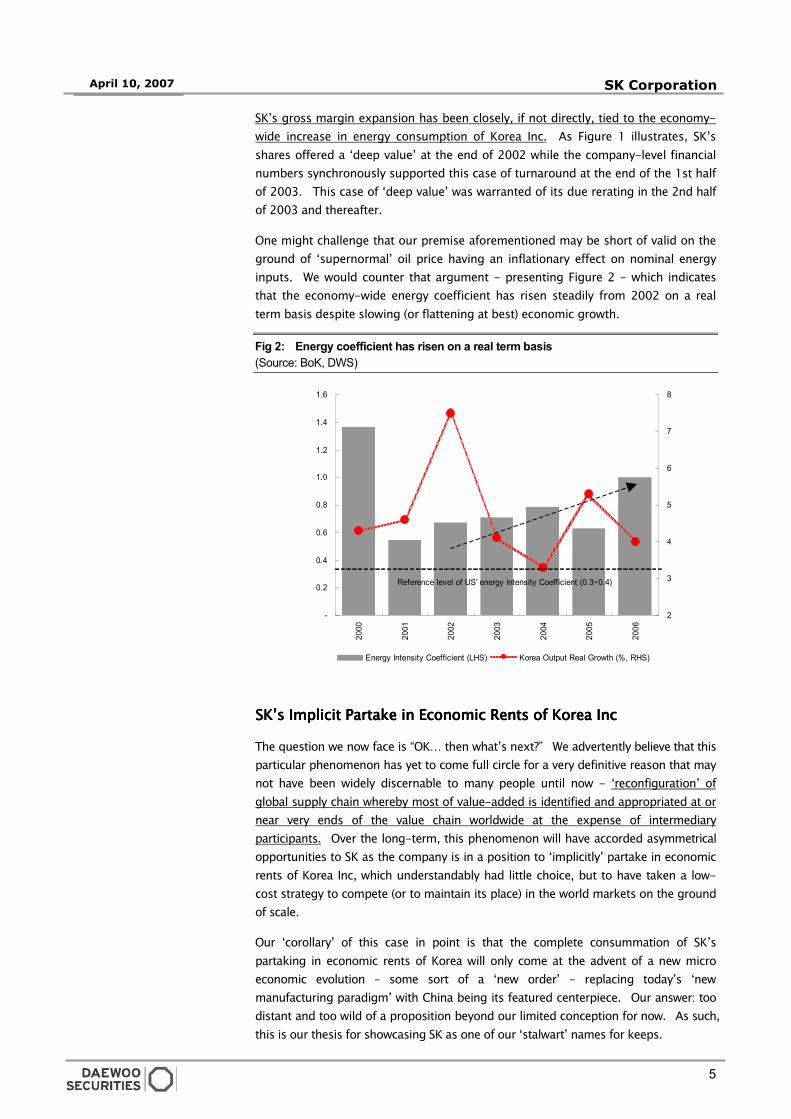

inputs. We would counter that argument - presenting Figure 2 - which indicates

that the economy-wide energy coefficient has risen steadily from 2002 on a real

term basis despite slowing (or flattening at best) economic growth.

Fig 2: Energy coefficient has risen on a real term basis

(Source: BoK, DWS)

SK’sSK’sSK’sSK’s Implicit Partake in Economic Rents of Korea Inc Implicit Partake in Economic Rents of Korea Inc Implicit Partake in Economic Rents of Korea Inc Implicit Partake in Economic Rents of Korea Inc

The question we now face is “OK… then what’s next?” We advertently believe that this

particular phenomenon has yet to come full circle for a very definitive reason that may

not have been widely discernable to many people until now - ‘reconfiguration’ of

global supply chain whereby most of value-added is identified and appropriated at or

near very ends of the value chain worldwide at the expense of intermediary

participants. Over the long-term, this phenomenon will have accorded asymmetrical

opportunities to SK as the company is in a position to ‘implicitly’ partake in economic

rents of Korea Inc, which understandably had little choice, but to have taken a low-

cost strategy to compete (or to maintain its place) in the world markets on the ground

of scale.

Our ‘corollary’ of this case in point is that the complete consummation of SK’s

partaking in economic rents of Korea will only come at the advent of a new micro

economic evolution – some sort of a ‘new order’ - replacing today’s ‘new

manufacturing paradigm’ with China being its featured centerpiece. Our answer: too

distant and too wild of a proposition beyond our limited conception for now. As such,

this is our thesis for showcasing SK as one of our ‘stalwart’ names for keeps.

6

April 10, 2007 SK Corporation

Interestingly, this thesis of ours would also bring forth one very noteworthy

technical implication: it would be held in the best interest of the nation’s economy

to lower SK’s business cost. While we do not know whether or not Korean National

Pension and other municipal funds alike have acted on this vested interest, we

believe that the market’s intuition will - more likely than not - manifest it. Why not

take advantage of the fire spreading leeward?

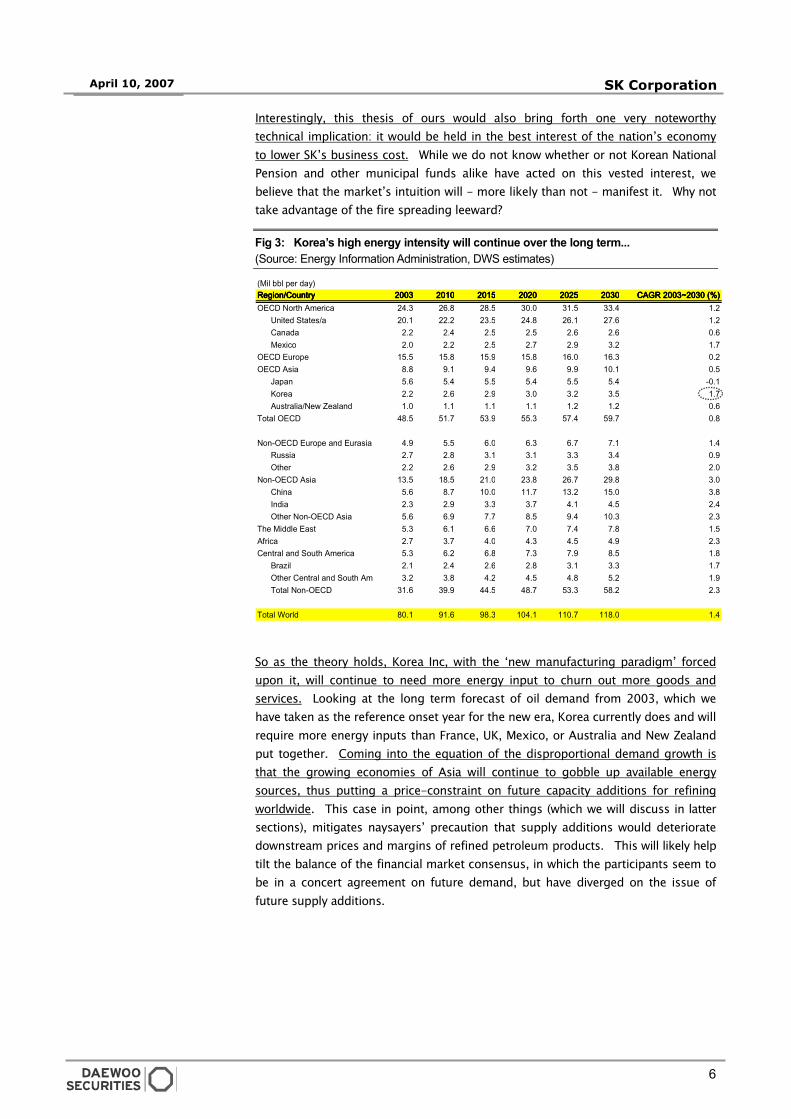

Fig 3: Korea’s high energy intensity will continue over the long term...

(Source: Energy Information Administration, DWS estimates)

So as the theory holds, Korea Inc, with the ‘new manufacturing paradigm’ forced

upon it, will continue to need more energy input to churn out more goods and

services. Looking at the long term forecast of oil demand from 2003, which we

have taken as the reference onset year for the new era, Korea currently does and will

require more energy inputs than France, UK, Mexico, or Australia and New Zealand

put together. Coming into the equation of the disproportional demand growth is

that the growing economies of Asia will continue to gobble up available energy

sources, thus putting a price-constraint on future capacity additions for refining

worldwide. This case in point, among other things (which we will discuss in latter

sections), mitigates naysayers’ precaution that supply additions would deteriorate

downstream prices and margins of refined petroleum products. This will likely help

tilt the balance of the financial market consensus, in which the participants seem to

be in a concert agreement on future demand, but have diverged on the issue of

future supply additions.

(Mil bbl per day) Region/CountryRegion/CountryRegion/CountryRegion/Country 2003200320032003 2010201020102010 2015201520152015 2020202020202020 2025202520252025 2030203020302030 CAGR 2003~2030 (%)CAGR 2003~2030 (%)CAGR 2003~2030 (%)CAGR 2003~2030 (%)OECD North America 24.3 26.8 28.5 30.0 31.5 33.4 1.2 United States/a 20.1 22.2 23.5 24.8 26.1 27.6 1.2 Canada 2.2 2.4 2.5 2.5 2.6 2.6 0.6 Mexico 2.0 2.2 2.5 2.7 2.9 3.2 1.7OECD Europe 15.5 15.8 15.9 15.8 16.0 16.3 0.2OECD Asia 8.8 9.1 9.4 9.6 9.9 10.1 0.5 Japan 5.6 5.4 5.5 5.4 5.5 5.4 -0.1 Korea 2.2 2.6 2.9 3.0 3.2 3.5 1.7 Australia/New Zealand 1.0 1.1 1.1 1.1 1.2 1.2 0.6Total OECD 48.5 51.7 53.9 55.3 57.4 59.7 0.8

Non-OECD Europe and Eurasia 4.9 5.5 6.0 6.3 6.7 7.1 1.4 Russia 2.7 2.8 3.1 3.1 3.3 3.4 0.9 Other 2.2 2.6 2.9 3.2 3.5 3.8 2.0Non-OECD Asia 13.5 18.5 21.0 23.8 26.7 29.8 3.0 China 5.6 8.7 10.0 11.7 13.2 15.0 3.8 India 2.3 2.9 3.3 3.7 4.1 4.5 2.4 Other Non-OECD Asia 5.6 6.9 7.7 8.5 9.4 10.3 2.3The Middle East 5.3 6.1 6.6 7.0 7.4 7.8 1.5Africa 2.7 3.7 4.0 4.3 4.5 4.9 2.3Central and South America 5.3 6.2 6.8 7.3 7.9 8.5 1.8 Brazil 2.1 2.4 2.6 2.8 3.1 3.3 1.7 Other Central and South America 3.2 3.8 4.2 4.5 4.8 5.2 1.9 Total Non-OECD 31.6 39.9 44.5 48.7 53.3 58.2 2.3

Total World 80.1 91.6 98.3 104.1 110.7 118.0 1.4

7

April 10, 2007 SK Corporation

Coming into Equation for Strong Petroleum Prices is a Possible Coming into Equation for Strong Petroleum Prices is a Possible Coming into Equation for Strong Petroleum Prices is a Possible Coming into Equation for Strong Petroleum Prices is a Possible

Supply DisruptSupply DisruptSupply DisruptSupply Disruptionionionion

In fact, we have noted that capacity additions – worldwide - are coming on stream at

a much slower pace than previously anticipated. According to <Oil & Gas Journal

Worldwide Refining Survey and Construction Report>, the total new worldwide

atmospheric crude distillation capacity under construction is counting about

600,000 bpd as of the end of 2006. However, even with these works-in-progress,

it is clear that the number of new refineries needed is still significant, and more

critically, these additions should already be in the engineering phase to be fully

operational by 2010. As of today, none of them is!

Another event weighing on the supply side is the worldwide enforcement of ‘cleaner

air’ mandates for tighter specifications. Capacity investments will be hampered by

the reality that the need to meet sulfur regulatory changes is a primary pull on

refiner’s capital. Hydroprocessing has been by far the most significant processing

investment over the last 5 years. Reduced sulfur targets for global products,

including potentially residual fuels and heating oil as well, will complicate the supply

side because ‘simple’ refiners that have not made the necessary investments for

‘upgrade’ will have no option other than to purchase increasingly expensive sweet

crude oil or else throw in the towel. We believe that some 8% of refiners worldwide

are exposed to this predicament. Further, we expect about 1% of current motor

gasoline volume to be lost as a result of octane levels being reduced during the

hydrotreating process.

Lastly on the supply issue, as refinery capacity additions lag, the fragility of the

distribution infrastructure will become more visible. In the Far East, the

downstream distribution systems will need extensive development. Meanwhile, the

United States will need significant additions for tankage and pipelines, which have

become yet another problematic issue due to sulfur mandates presenting the

challenge to handle the necessary ‘segregation’ and ‘contamination’ of ‘sweet’

products. In addition, the globalization of products and phase-out of single-hull

tankers will require large investments in product vessels to handle the long-range

movement of products in the downstream arena.

8

April 10, 2007 SK Corporation

-4%

-2%

0%

2%

4%

6%

8%

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Distilation Capacity % Increase Energy Consumption% Increase

US real output growth Europe real output growth

Asia real output growth

Supply Additions Supply Additions Supply Additions Supply Additions ---- aaaa LLLLittle too Short, a ittle too Short, a ittle too Short, a ittle too Short, a LLLLittle too Lateittle too Lateittle too Lateittle too Late

Supply additions will come full-fledged only if the aforementioned issues are

addressed first. Whether this takes place in due process remains to be seen as it

requires more active dialogues among the policymakers, regulators, up/

downstream players, and investment banks. It will greatly depend on who is willing

to ‘ante-up’ for the volume. Since the ramifications for both the ‘winner’ and the

‘loser’ will be significant, all interested parties may be less than willing to roll the

dice yet.

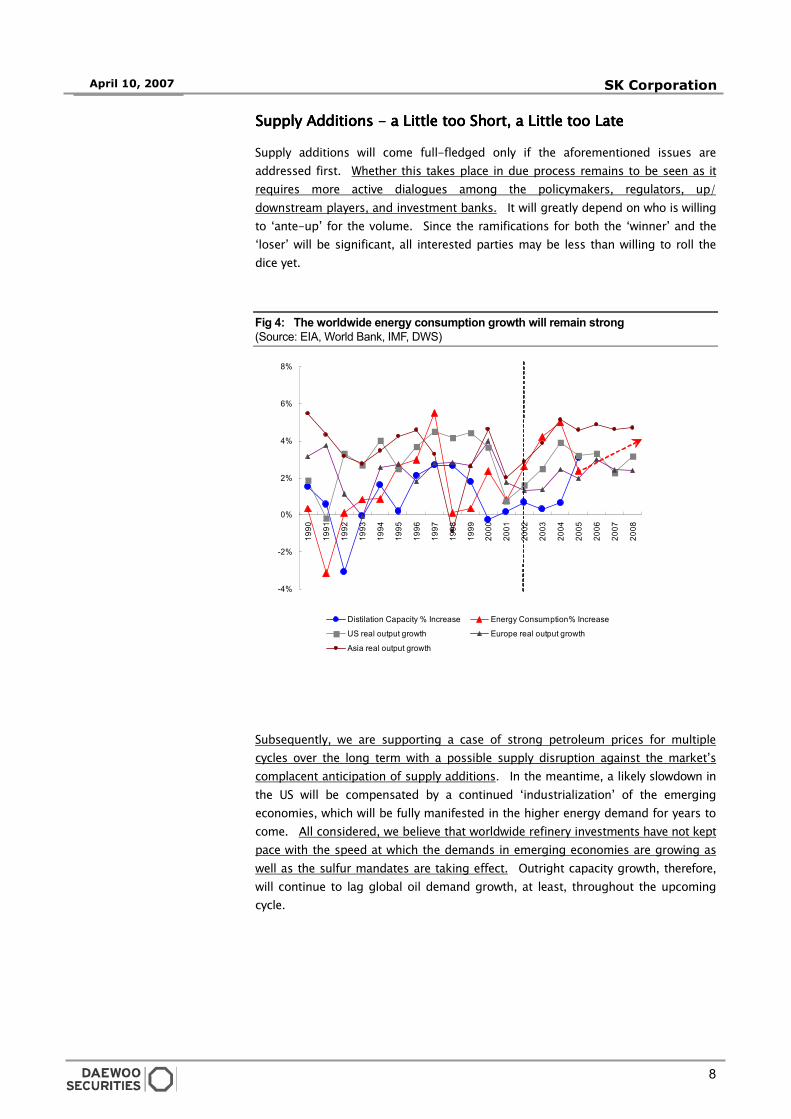

Fig 4: The worldwide energy consumption growth will remain strong

(Source: EIA, World Bank, IMF, DWS)

Subsequently, we are supporting a case of strong petroleum prices for multiple

cycles over the long term with a possible supply disruption against the market’s

complacent anticipation of supply additions. In the meantime, a likely slowdown in

the US will be compensated by a continued ‘industrialization’ of the emerging

economies, which will be fully manifested in the higher energy demand for years to

come. All considered, we believe that worldwide refinery investments have not kept

pace with the speed at which the demands in emerging economies are growing as

well as the sulfur mandates are taking effect. Outright capacity growth, therefore,

will continue to lag global oil demand growth, at least, throughout the upcoming

cycle.

9

April 10, 2007 SK Corporation

Internal Initiatives to Chime with Macro DevelopmentInternal Initiatives to Chime with Macro DevelopmentInternal Initiatives to Chime with Macro DevelopmentInternal Initiatives to Chime with Macro Development

Having implied that we are convinced of the world’s inexorable trend with respect to

how differently corporations are operating, we commend SK for what it has done

internally to further strengthen its (already solid) leadership position: (1) made

selective investments into ‘strategic’ segments of refining (low-sulfur diesel and

kerosene) and petrochemicals (BTX) to optimize its crude ‘slate’; (2) disposed of

excess assets and non-operating assets over the last 5 years; (3) acquired SK

Incheon (“SKICO” hereafter), which it successfully integrated and branded into ‘SK

realm’; and (4) inked in a strategic tie-up with Nippon Oil of Japan (“NOJ” hereafter).

In our opinion, the ‘value’ driver over the next 6~12 months for SK shares will be

accredited more to ‘follow-through’ of these internal initiatives than to

exploration/production (‘E&P’) business unit or a possible transition into a holding

company structure, both of which have been limelighted as the rerating catalyst in

the financial market. According to our studies, SK’s mid-cycle profitability, as

measured by return on capital employed, will convincingly escalate to about 13%

from the current level of 9% (2001~2005) due to these initiatives, which we suspect

have yet to be fully priced in. Over the next 3 years, we expect SK to take on the

form of a rare breed of the ‘procyclical-defensive’. Not only do we reiterate SK as

our favorite top pick among the large-capitalization universe stocks in Korea, we

also suggest that the company’s shares provide visible rewards in a market-neutral

perspective that they should demand a spot in your investment portfolio as a

consummate alpha play with an alpha-driven excess return target of 20%+ over the

next 12 months.

10

April 10, 2007 SK Corporation

FFIINNAANNCCIIAALL AANNAALLYYSSIISS AANNDD VVAALLUUAATTIIOONN

WWHHAATT CCAAUUSSEESS SSKK’’SS SSHHAARREE PPRRIICCEE TTOO BBEEHHAAVVEE TTHHEE WWAAYY IITT DDOOEESS??

DonDonDonDon’’’’t Judge a Book by Its Cover t Judge a Book by Its Cover t Judge a Book by Its Cover t Judge a Book by Its Cover ---- More Often thanMore Often thanMore Often thanMore Often than Not Not Not Not, It is , It is , It is , It is nnnnot ot ot ot

What ItWhat ItWhat ItWhat It Reads Reads Reads Reads

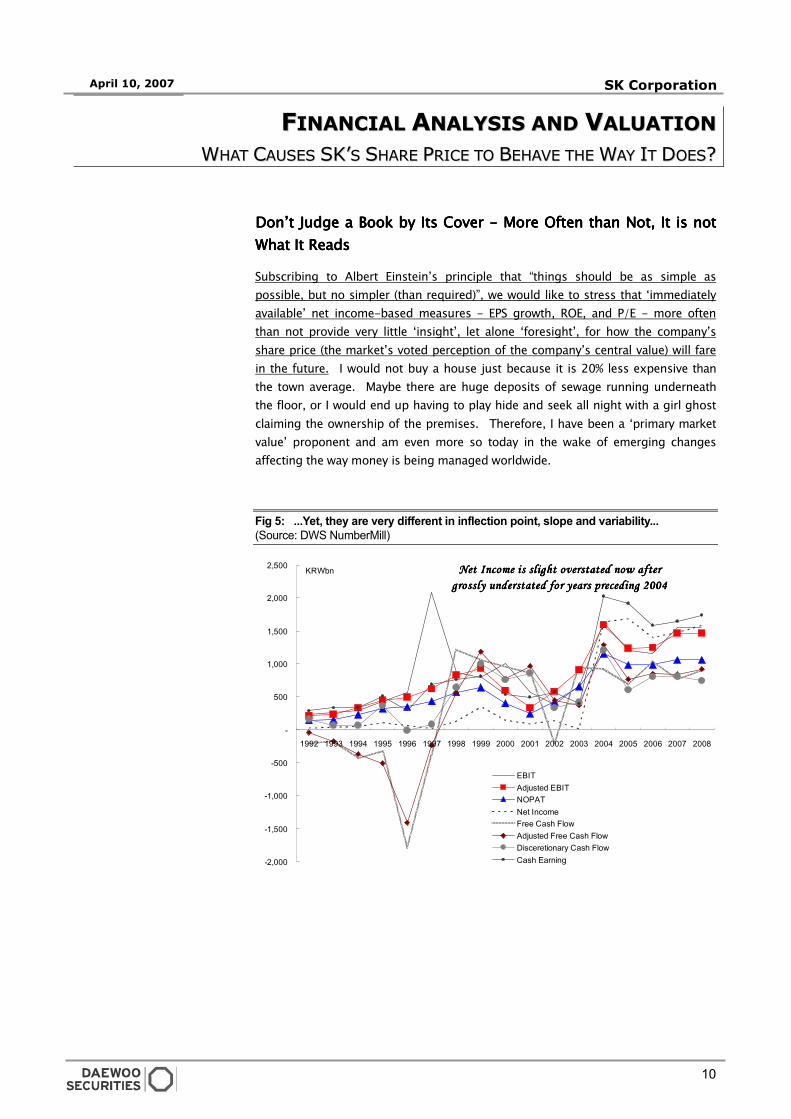

Subscribing to Albert Einstein’s principle that “things should be as simple as

possible, but no simpler (than required)”, we would like to stress that ‘immediately

available’ net income-based measures - EPS growth, ROE, and P/E - more often

than not provide very little ‘insight’, let alone ‘foresight’, for how the company’s

share price (the market’s voted perception of the company’s central value) will fare

in the future. I would not buy a house just because it is 20% less expensive than

the town average. Maybe there are huge deposits of sewage running underneath

the floor, or I would end up having to play hide and seek all night with a girl ghost

claiming the ownership of the premises. Therefore, I have been a ‘primary market

value’ proponent and am even more so today in the wake of emerging changes

affecting the way money is being managed worldwide.

Fig 5: ...Yet, they are very different in inflection point, slope and variability...

(Source: DWS NumberMill)

-2,000

-1,500

-1,000

-500

-

500

1,000

1,500

2,000

2,500

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

EBITAdjusted EBITNOPATNet IncomeFree Cash FlowAdjusted Free Cash FlowDisceretionary Cash FlowCash Earning

KRWbn Net Income is slight overstated now afterNet Income is slight overstated now afterNet Income is slight overstated now afterNet Income is slight overstated now after

grossly understated for years preceding 2004grossly understated for years preceding 2004grossly understated for years preceding 2004grossly understated for years preceding 2004

11

April 10, 2007 SK Corporation

Understanding of AccounUnderstanding of AccounUnderstanding of AccounUnderstanding of Accounting Pays Offting Pays Offting Pays Offting Pays Off

From 1995 to 2006 covering 3 peak-to-peak cycles, SK’s accounting figures have

not been much more than the offspring of an accounting craft (no negative

connotation intended). As expected, net-income based measures were of little

help in appraising the firm’s central value at any given time. In fact, SK’s net

income, after being grossly understated for years preceding 2004, is believed to be

actually overstated with respect to its mid-cycle earning capacity. Free cash flow

poses a similar problem for its insane volatility on a peak-to-peak basis. In light of

the fact that the net income-based measures are most ‘immediately available’ and

most used as means of valuation by many people, which we believe is not by

‘reason’, but rather by ‘convention’, we must guard against the illusion that there is

‘safety in numbers’.

As matter of a fact, we expect SK’s net income to stay moderately flat in 2007 and

2008, nonetheless, foresee its market value to steadfastly rise to a fairer level.

Figure 6 visually captures our argument. Over 3 peak-to-peak cycles since 1995,

the return on capital employed - for core operation – has been by far most

explanatory with the change in SK’s equity value on a yearly rolling basis.

Statistically speaking, they would move in the same direction in 72 out of 100 cases

if the historical interaction holds. There are three other notable items that demand

our attention:

1. Adjusted EBIT (EBIT adjusted for non-operating and non-cash items) and

NOPAT (adjusted EBIT after normalized tax and tax shield) best explain

where shares will go in the following year of T+1 – and they do so quite

adequately. Adjustments made to reflect non-operating and non-cash

items chip off the year-to-year volatility, enabling one to form a more

picturable takeaway for the company’s normalized, mid-cycle earning

capacity. This finding also explains their almost perfect correlation with

the share price change during 2003~2006 on the same ground;

2. Sales/turnover trend has a very high level of negative correlation, thus,

supports our claim that rising oil price is a premonition of bad times

ahead. On the same note, the company’s stated free cash flow or lack

thereof has not been duly awarded or penalized, implying that the

investors have been unwilling to forward-look and capitalize the future

growth over the long term. Whether this particular behavior of the public

will change in the future on the grounds of the increased accountability of

the company and broad market is a critical issue. We will remain

steadfastly anchored to this issue for incremental return enhancement

going forward;

3. Discretionary cash flow, which we proprietarily take as the cyclically

adjusted operating cash flow before any exceptional proceeds minus cash

dividend and maintenance capital expenditures, is relatively stable and

precedes the share performance though its explanatory power is lower

than that of NOPAT growth. We find it logically valid that this is the true

‘economic’ cash flow that the company should take as a basis for its

cyclical capital budgeting.

12

April 10, 2007 SK Corporation

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

Turn

over

/Sal

esTu

rnov

er/S

ales

Turn

over

/Sal

esTu

rnov

er/S

ales

EB

IT

EB

IT

EB

IT

EB

IT

Adj

uste

d E

BIT

Adj

uste

d E

BIT

Adj

uste

d E

BIT

Adj

uste

d E

BIT

NO

PA

T N

OP

AT

NO

PA

T N

OP

AT

Net

Inco

me

Net

Inco

me

Net

Inco

me

Net

Inco

me

Fre

e C

ash

Flo

w

Fre

e C

ash

Flo

w

Fre

e C

ash

Flo

w

Fre

e C

ash

Flo

w

Dis

cere

tiona

ryD

isce

retio

nary

Dis

cere

tiona

ryD

isce

retio

nary

Cas

h Fl

owC

ash

Flow

Cas

h Fl

owC

ash

Flow

Cas

h E

arni

ngC

ash

Ear

ning

Cas

h E

arni

ngC

ash

Ear

ning

Sta

ted

RO

ES

tate

d R

OE

Sta

ted

RO

ES

tate

d R

OE

RO

CE

- In

vest

edR

OC

E -

Inve

sted

RO

CE

- In

vest

edR

OC

E -

Inve

sted

Cap

ital

Cap

ital

Cap

ital

Cap

ital

RO

CE

- C

ore

RO

CE

- C

ore

RO

CE

- C

ore

RO

CE

- C

ore

Ope

ratin

g C

apita

lO

pera

ting

Cap

ital

Ope

ratin

g C

apita

lO

pera

ting

Cap

ital

Pearson Coefficient to Stock Price(1995~2006)Pearson Coefficient to Stock Price(2003~2006)Pearson Coefficient to Stock Price ofT+1 year

Reference level of 'meaningfulness'Reference level of 'meaningfulness'Reference level of 'meaningfulness'Reference level of 'meaningfulness'

Highest Explanation Power - 52%Highest Explanation Power - 52%Highest Explanation Power - 52%Highest Explanation Power - 52%

?

Fig 6: Forget RoE and EPS... Monitor RoCE and economic earning growth

(Source: DWS NumberMill)

When well schematized and practised, these findings should translate into a better-

than-average, if not superior, trading/investment strategy. An acute observer, who

grounds his/her analysis in valuing the company’s normalized ‘economic’ earning

with the additory focus on the probability assessment of earning visibility and the

rate of capital expenditures, should identify consistent opportunities with relative

ease. It should also help in a behavioral investing perspective if one knows what

everyone else may be thinking on their possibly illusory premise.

13

April 10, 2007 SK Corporation

-1,500

-1,000

-500

0

500

1,000

FY

1991

FY

1991

FY

1991

FY

1991

FY

1992

FY

1992

FY

1992

FY

1992

FY

1993

FY

1993

FY

1993

FY

1993

FY

1994

FY

1994

FY

1994

FY

1994

FY

1995

FY

1995

FY

1995

FY

1995

FY

1996

FY

1996

FY

1996

FY

1996

FY

1997

FY

1997

FY

1997

FY

1997

FY

1998

FY

1998

FY

1998

FY

1998

FY

1999

FY

1999

FY

1999

FY

1999

FY

2000

FY

2000

FY

2000

FY

2000

FY

2001

FY

2001

FY

2001

FY

2001

FY

2002

FY

2002

FY

2002

FY

2002

FY

2003

FY

2003

FY

2003

FY

2003

FY

2004

FY

2004

FY

2004

FY

2004

FY

2005

FY

2005

FY

2005

FY

2005

FY

2006

FY

2006

FY

2006

FY

2006

FY

2007

FY

2007

FY

2007

FY

2007

FY

2008

FY

2008

FY

2008

FY

2008

Shareholder Value-Added

Annual Average Market Value Added excluding Non Op Assets

Annual Average Market Value Added

(KRW bn)

How Should We Value SK How Should We Value SK How Should We Value SK How Should We Value SK andandandand Why? Why? Why? Why?

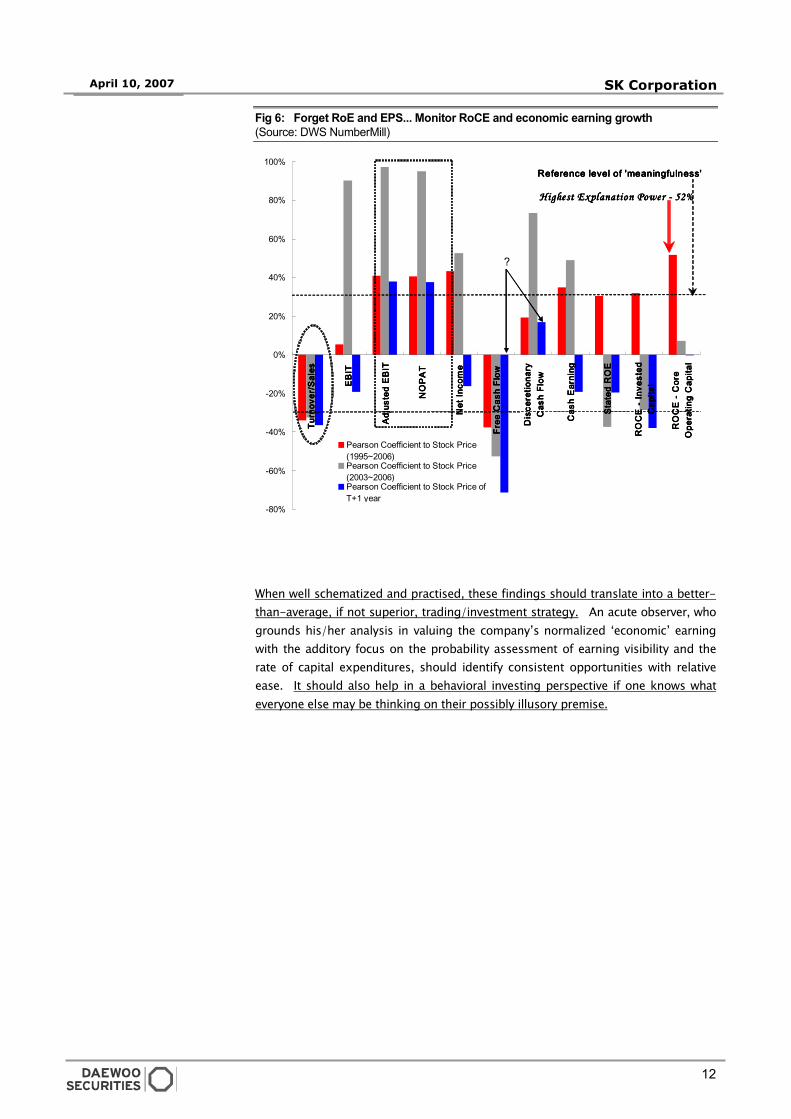

SK share performance of the last several years has been nothing short of being

superlative. After the full-body of rerating during 2003~2004, SK shares have

started to steepen up again from November 2006. The current price of KRW92,000

is well above the analysts’ consensus and the unexpected strength of prices is

largely interpreted by the market as the due premium accounting for the likelihood

of SK wearing a holding company outfit whereby asset values of its investment

holdings will likely be more justifiably and ‘transparently’ reflected.

While we do not completely disagree that such a proposition is certainly one casual

way to explain the recent strength of its share price, we find a better explanation for

the case of undervaluation in the ‘post-2003’ trend and pattern of SK’s core

operating earning.

Fig 7: Could an average investor have been led astray by pileup of miscalculations over the years?.. (Source: DWS NumberMill)

First, despite the clear difference in the trend and pattern of SK’s core operating

earning before and after 2003, the analyst community appears to be still reserved

with the company’s earning over the next two years, unwilling to capitalize on its

future earning in the upcoming cycles. Fully detailed in the following section, we

are clearly more positive on SK’s earning visibility and forward-look at its earning

stream in justifiably going-concern perspective with the conscious effort not to err

of stretching beyond what we ought to ‘normatively’ envisage. Second, charting

the historical pattern of SK’s value-added generation, or lack thereof, we can see

that it was the public’s recognition of SK’s investments that actually supported the

share price until 1997. Otherwise, it would be logically difficult to explain the case

of SK’s huge overvaluation throughout the entire ’90s unless the market was so

inefficient to the extent that any analytic effort was of little, if not none, utility (as

indicated by the dotted line). What do you think?

14

April 10, 2007 SK Corporation

The bottom line we wish to address is that, simply, the market may have not caught

up with the degree (or slope) of the turnaround in SK’s earning yet enough and even

perhaps expect its shares to be somewhat gravitational for a technical reason – that

is because the share prices went up ‘too much’. To add to the mystery of SK’s

undervaluation is the perversity of the current trend toward (liquidity-driven)

indexation pushing financial investors to stocks whose characteristics are not

necessarily synonymous with best value. This is about to change as we believe that

the current M&A boom is symptomatic of value being snatched up by ‘industrial’

buyers. If you can borrow at 5~6% and are asked to entertain a possible purchase

of a company like SK that has a cash yield of 8~9%, which financial investors seem to

ignore anyway, you are having the time of your life. But we see that financial

investors will not be ‘robbed’. Instead, with proliferation of buyout funds, we are

now ready to bet that they will soon decide to buy these assets themselves.

To align ourselves in this expected setting, we choose to look at SK from a ‘primary’

market value perspective (as ‘they’ are) for what it’s worth. The actual, ‘economic’

value of SK’s investments, whether the company is a controlling firm or legally a

holding company, does not change. Our reasoning by choice is to appraise the

company’s core business operation based on its future earning subject to our (or of

anyone deemed to be an expert) fair visibility and then add up this appraised value

and non-operating investments assets minus the sum of probability-weighted

‘value destruction’, which we will state in terms of percent of capital employed, for

the ‘conglomerate’ discount.

The conglomerate discount exists when a conglomerate would be worth more to

shareholders if it were split up and sold as separate business units than it is

currently valued by the market. And, we do believe that SK’s petroleum and its

upstream E&P business, if separated, can demand a higher price tag. Among many

factors, a conglomerate discount exists, in our opinion, due to management costs

(associated with bureaucracy and cross-subsidy risk), minority costs (associated

with an individual or family’s possible malfeasance), and technical costs (associated

with loss of clarity in financial accounts and higher costs to keep investors informed).

We would mainly discount SK for management costs because there aren’t enough

material signs to suggest that the last two must be accounted for.

15

April 10, 2007 SK Corporation

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

FY1997

FY1998

FY1999

FY2000

FY2001

FY2002

FY2003

FY2004

FY2005

FY2006

FY2007

FY2008

Total Asset Sales/Turnover Operating Capital

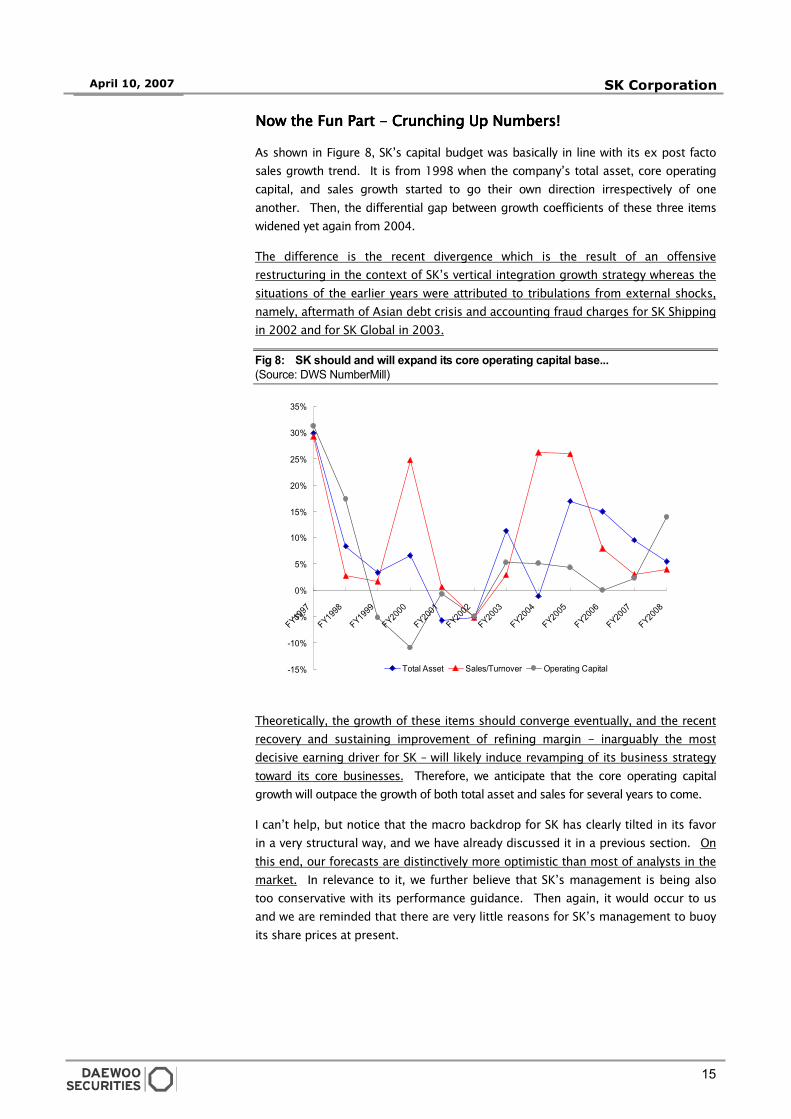

Now the Fun Part Now the Fun Part Now the Fun Part Now the Fun Part ---- Crunching Up Numbers! Crunching Up Numbers! Crunching Up Numbers! Crunching Up Numbers!

As shown in Figure 8, SK’s capital budget was basically in line with its ex post facto

sales growth trend. It is from 1998 when the company’s total asset, core operating

capital, and sales growth started to go their own direction irrespectively of one

another. Then, the differential gap between growth coefficients of these three items

widened yet again from 2004.

The difference is the recent divergence which is the result of an offensive

restructuring in the context of SK’s vertical integration growth strategy whereas the

situations of the earlier years were attributed to tribulations from external shocks,

namely, aftermath of Asian debt crisis and accounting fraud charges for SK Shipping

in 2002 and for SK Global in 2003.

Fig 8: SK should and will expand its core operating capital base...

(Source: DWS NumberMill)

Theoretically, the growth of these items should converge eventually, and the recent

recovery and sustaining improvement of refining margin - inarguably the most

decisive earning driver for SK – will likely induce revamping of its business strategy

toward its core businesses. Therefore, we anticipate that the core operating capital

growth will outpace the growth of both total asset and sales for several years to come.

I can’t help, but notice that the macro backdrop for SK has clearly tilted in its favor

in a very structural way, and we have already discussed it in a previous section. On

this end, our forecasts are distinctively more optimistic than most of analysts in the

market. In relevance to it, we further believe that SK’s management is being also

too conservative with its performance guidance. Then again, it would occur to us

and we are reminded that there are very little reasons for SK’s management to buoy

its share prices at present.

16

April 10, 2007 SK Corporation

0

100

200

300

400

500

600

700

Petroleum Petrochemical Lubricant E&P Others

SK GuidanceDWS EstimateDWS Estimate - Economic EBIT

KRWbn

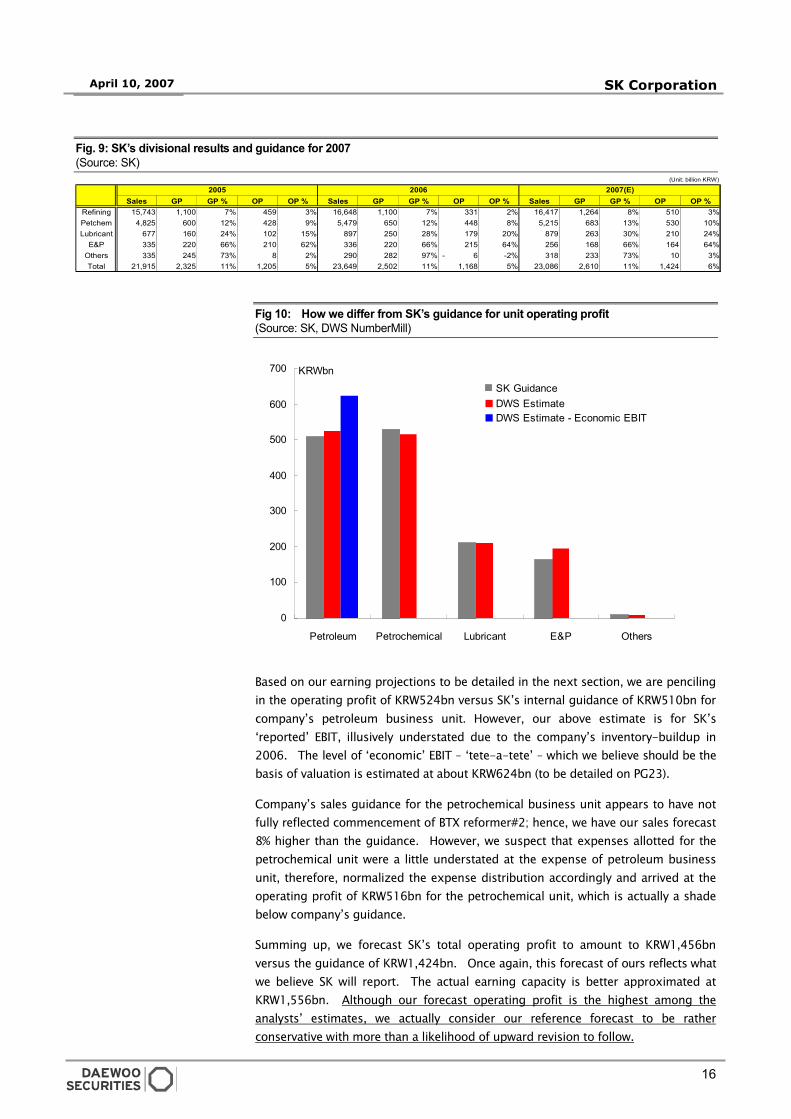

Fig. 9: SK’s divisional results and guidance for 2007

(Source: SK)

Fig 10: How we differ from SK’s guidance for unit operating profit

(Source: SK, DWS NumberMill)

Based on our earning projections to be detailed in the next section, we are penciling

in the operating profit of KRW524bn versus SK’s internal guidance of KRW510bn for

company’s petroleum business unit. However, our above estimate is for SK’s

‘reported’ EBIT, illusively understated due to the company’s inventory-buildup in

2006. The level of ‘economic’ EBIT – ‘tete-a-tete’ – which we believe should be the

basis of valuation is estimated at about KRW624bn (to be detailed on PG23).

Company’s sales guidance for the petrochemical business unit appears to have not

fully reflected commencement of BTX reformer#2; hence, we have our sales forecast

8% higher than the guidance. However, we suspect that expenses allotted for the

petrochemical unit were a little understated at the expense of petroleum business

unit, therefore, normalized the expense distribution accordingly and arrived at the

operating profit of KRW516bn for the petrochemical unit, which is actually a shade

below company’s guidance.

Summing up, we forecast SK’s total operating profit to amount to KRW1,456bn

versus the guidance of KRW1,424bn. Once again, this forecast of ours reflects what

we believe SK will report. The actual earning capacity is better approximated at

KRW1,556bn. Although our forecast operating profit is the highest among the

analysts’ estimates, we actually consider our reference forecast to be rather

conservative with more than a likelihood of upward revision to follow.

(Unit: billion KRW)

Sales GP GP % OP OP % Sales GP GP % OP OP % Sales GP GP % OP OP %

Refining 15,743 1,100 7% 459 3% 16,648 1,100 7% 331 2% 16,417 1,264 8% 510 3%

Petchem 4,825 600 12% 428 9% 5,479 650 12% 448 8% 5,215 683 13% 530 10%

Lubricant 677 160 24% 102 15% 897 250 28% 179 20% 879 263 30% 210 24%

E&P 335 220 66% 210 62% 336 220 66% 215 64% 256 168 66% 164 64%

Others 335 245 73% 8 2% 290 282 97% - 6 -2% 318 233 73% 10 3%

Total 21,915 2,325 11% 1,205 5% 23,649 2,502 11% 1,168 5% 23,086 2,610 11% 1,424 6%

2005 2006 2007(E)

17

April 10, 2007 SK Corporation

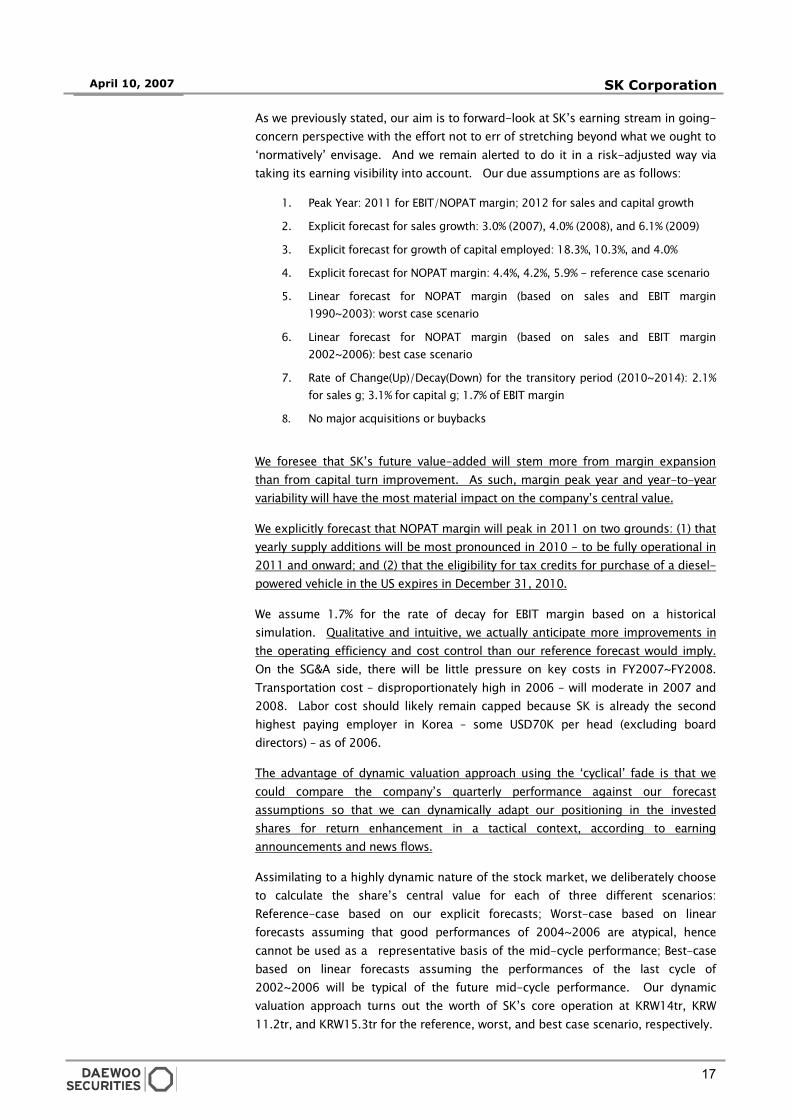

As we previously stated, our aim is to forward-look at SK’s earning stream in going-

concern perspective with the effort not to err of stretching beyond what we ought to

‘normatively’ envisage. And we remain alerted to do it in a risk-adjusted way via

taking its earning visibility into account. Our due assumptions are as follows:

1. Peak Year: 2011 for EBIT/NOPAT margin; 2012 for sales and capital growth

2. Explicit forecast for sales growth: 3.0% (2007), 4.0% (2008), and 6.1% (2009)

3. Explicit forecast for growth of capital employed: 18.3%, 10.3%, and 4.0%

4. Explicit forecast for NOPAT margin: 4.4%, 4.2%, 5.9% - reference case scenario

5. Linear forecast for NOPAT margin (based on sales and EBIT margin

1990~2003): worst case scenario

6. Linear forecast for NOPAT margin (based on sales and EBIT margin

2002~2006): best case scenario

7. Rate of Change(Up)/Decay(Down) for the transitory period (2010~2014): 2.1%

for sales g; 3.1% for capital g; 1.7% of EBIT margin

8. No major acquisitions or buybacks

We foresee that SK’s future value-added will stem more from margin expansion

than from capital turn improvement. As such, margin peak year and year-to-year

variability will have the most material impact on the company’s central value.

We explicitly forecast that NOPAT margin will peak in 2011 on two grounds: (1) that

yearly supply additions will be most pronounced in 2010 - to be fully operational in

2011 and onward; and (2) that the eligibility for tax credits for purchase of a diesel-

powered vehicle in the US expires in December 31, 2010.

We assume 1.7% for the rate of decay for EBIT margin based on a historical

simulation. Qualitative and intuitive, we actually anticipate more improvements in

the operating efficiency and cost control than our reference forecast would imply.

On the SG&A side, there will be little pressure on key costs in FY2007~FY2008.

Transportation cost – disproportionately high in 2006 – will moderate in 2007 and

2008. Labor cost should likely remain capped because SK is already the second

highest paying employer in Korea – some USD70K per head (excluding board

directors) – as of 2006.

The advantage of dynamic valuation approach using the ‘cyclical’ fade is that we

could compare the company’s quarterly performance against our forecast

assumptions so that we can dynamically adapt our positioning in the invested

shares for return enhancement in a tactical context, according to earning

announcements and news flows.

Assimilating to a highly dynamic nature of the stock market, we deliberately choose

to calculate the share’s central value for each of three different scenarios:

Reference-case based on our explicit forecasts; Worst-case based on linear

forecasts assuming that good performances of 2004~2006 are atypical, hence

cannot be used as a representative basis of the mid-cycle performance; Best-case

based on linear forecasts assuming the performances of the last cycle of

2002~2006 will be typical of the future mid-cycle performance. Our dynamic

valuation approach turns out the worth of SK’s core operation at KRW14tr, KRW

11.2tr, and KRW15.3tr for the reference, worst, and best case scenario, respectively.

18

April 10, 2007 SK Corporation

0%

2%

4%

6%

8%

10%

12%

14%

16%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30

Sales Growth Core Operating Capital Growth ROCE Cost of Capital

0%

2%

4%

6%

8%

10%

12%

14%

16%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30

Sales Growth Core Operating Capital Growth ROCE Cost of Capital

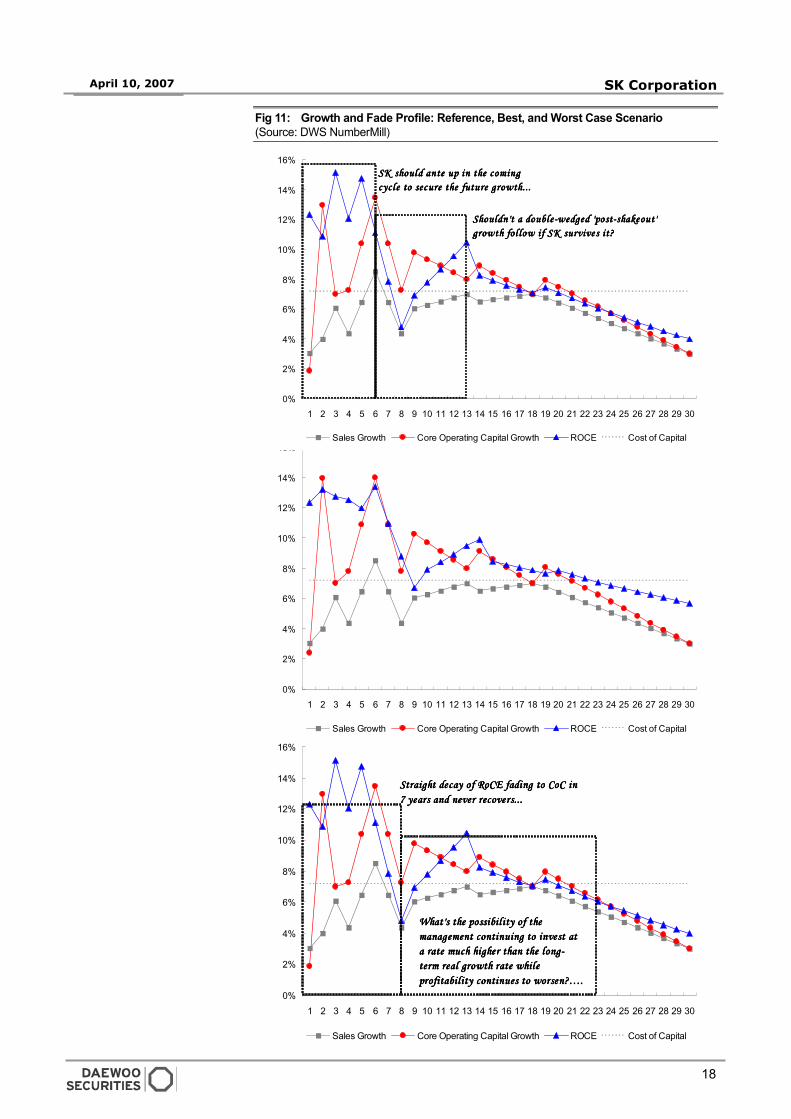

Straight decay of RoCE fading to CoC inStraight decay of RoCE fading to CoC inStraight decay of RoCE fading to CoC inStraight decay of RoCE fading to CoC in

7 years and never recovers...7 years and never recovers...7 years and never recovers...7 years and never recovers...

What's the possibility of theWhat's the possibility of theWhat's the possibility of theWhat's the possibility of the

management continuing to invest atmanagement continuing to invest atmanagement continuing to invest atmanagement continuing to invest at

a rate much higher than the long-a rate much higher than the long-a rate much higher than the long-a rate much higher than the long-

term real growth rate whileterm real growth rate whileterm real growth rate whileterm real growth rate while

profitability continues to worsen?….profitability continues to worsen?….profitability continues to worsen?….profitability continues to worsen?….

Fig 11: Growth and Fade Profile: Reference, Best, and Worst Case Scenario

(Source: DWS NumberMill)

0%

2%

4%

6%

8%

10%

12%

14%

16%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30

Sales Growth Core Operating Capital Growth ROCE Cost of Capital

SK should ante up in the comingSK should ante up in the comingSK should ante up in the comingSK should ante up in the coming

cycle to secure the future growth...cycle to secure the future growth...cycle to secure the future growth...cycle to secure the future growth...

Shouldn't a double-wedged 'post-shakeout'Shouldn't a double-wedged 'post-shakeout'Shouldn't a double-wedged 'post-shakeout'Shouldn't a double-wedged 'post-shakeout'

growth fol low if SK survives it?growth fol low if SK survives it?growth fol low if SK survives it?growth fol low if SK survives it?

19

April 10, 2007 SK Corporation

21.8% 90.8%

40.6% 91.1%

44.2% 60.0%

22.7%72.1% 29.6%

22.7%51.0% SK GasSK GasSK GasSK Gas 50% 67.1%

39.4% Daehan GasDaehan GasDaehan GasDaehan Gas 40%Busan GasBusan GasBusan GasBusan Gas 40%

90.6% Pohang GasPohang GasPohang GasPohang Gas 100% 30.0%Chungjoo GasChungjoo GasChungjoo GasChungjoo Gas 100%Koomi GasKoomi GasKoomi GasKoomi Gas 100%

40.1% Choongnam GasChoongnam GasChoongnam GasChoongnam Gas 100% 22.7%Kangwon GasKangwon GasKangwon GasKangwon Gas 100%Iksan GasIksan GasIksan GasIksan Gas 100%Chunnam GasChunnam GasChunnam GasChunnam Gas 100%

32.4%

65.0%

96.7%

SKSKSKSK SK TelecomSK TelecomSK TelecomSK Telecom

SK NetworksSK NetworksSK NetworksSK Networks

SKCSKCSKCSKC

K-PowerK-PowerK-PowerK-Power

OK CashbackOK CashbackOK CashbackOK Cashback

SKSKSKSKSecuritiesSecuritiesSecuritiesSecurities

SKSKSKSKChemicalsChemicalsChemicalsChemicals

SK E&CSK E&CSK E&CSK E&C

Dong-ShinDong-ShinDong-ShinDong-Shin

SK ShippingSK ShippingSK ShippingSK Shipping

SKE&SSKE&SSKE&SSKE&S

DOPCODOPCODOPCODOPCO

SK TelinkSK TelinkSK TelinkSK Telink

SKSKSKSKCommunicationCommunicationCommunicationCommunication

SeoulSeoulSeoulSeoulRecordsRecordsRecordsRecords

TU MediaTU MediaTU MediaTU Media

PantechPantechPantechPantech

SK IncheonSK IncheonSK IncheonSK Incheon

PaxnetPaxnetPaxnetPaxnet

SKC&CSKC&CSKC&CSKC&C

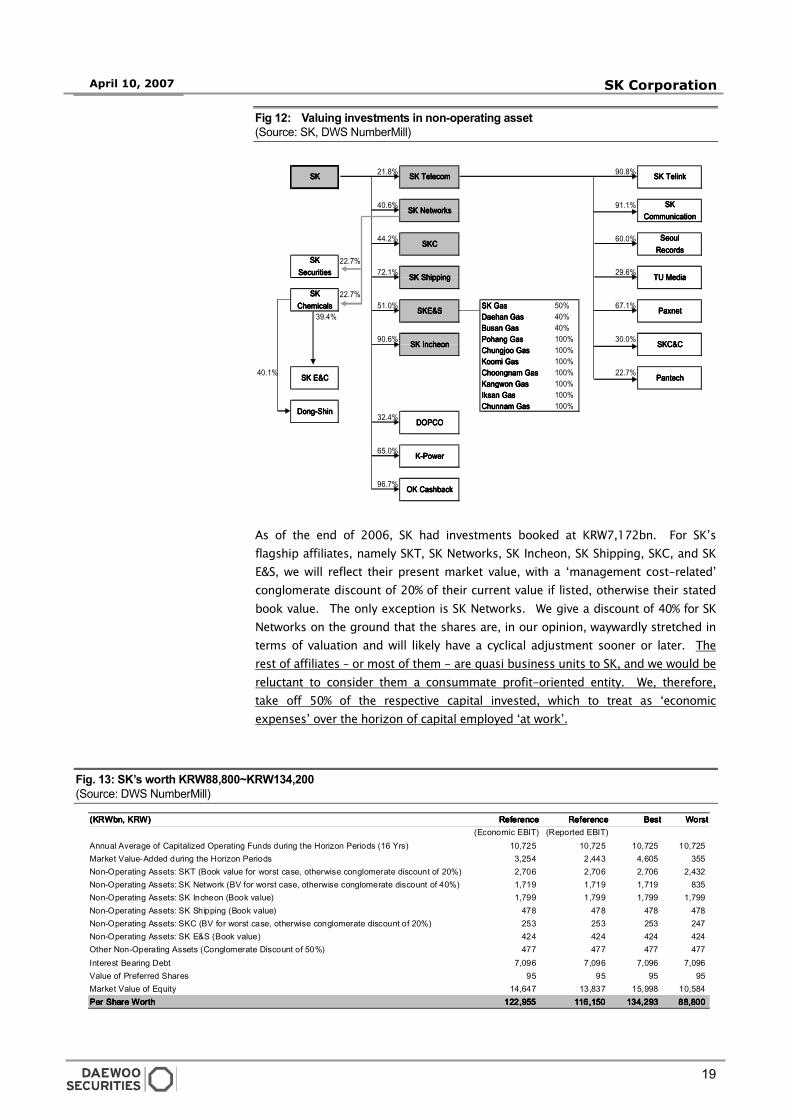

Fig 12: Valuing investments in non-operating asset

(Source: SK, DWS NumberMill)

As of the end of 2006, SK had investments booked at KRW7,172bn. For SK’s

flagship affiliates, namely SKT, SK Networks, SK Incheon, SK Shipping, SKC, and SK

E&S, we will reflect their present market value, with a ‘management cost-related’

conglomerate discount of 20% of their current value if listed, otherwise their stated

book value. The only exception is SK Networks. We give a discount of 40% for SK

Networks on the ground that the shares are, in our opinion, waywardly stretched in

terms of valuation and will likely have a cyclical adjustment sooner or later. The

rest of affiliates – or most of them - are quasi business units to SK, and we would be

reluctant to consider them a consummate profit-oriented entity. We, therefore,

take off 50% of the respective capital invested, which to treat as ‘economic

expenses’ over the horizon of capital employed ‘at work’.

Fig. 13: SK’s worth KRW88,800~KRW134,200

(Source: DWS NumberMill)

(KRWbn, KRW)(KRWbn, KRW)(KRWbn, KRW)(KRWbn, KRW) ReferenceReferenceReferenceReference ReferenceReferenceReferenceReference BestBestBestBest WorstWorstWorstWorst(Economic EBIT) (Reported EBIT)

Annual Average of Capitalized Operating Funds during the Horizon Periods (16 Yrs) 10,725 10,725 10,725 10,725 Market Value-Added during the Horizon Periods 3,254 2,443 4,605 355 Non-Operating Assets: SKT (Book value for worst case, otherwise conglomerate discount of 20%) 2,706 2,706 2,706 2,432 Non-Operating Assets: SK Network (BV for worst case, otherwise conglomerate discount of 40%) 1,719 1,719 1,719 835 Non-Operating Assets: SK Incheon (Book value) 1,799 1,799 1,799 1,799 Non-Operating Assets: SK Shipping (Book value) 478 478 478 478 Non-Operating Assets: SKC (BV for worst case, otherwise conglomerate discount of 20%) 253 253 253 247 Non-Operating Assets: SK E&S (Book value) 424 424 424 424 Other Non-Operating Assets (Conglomerate Discount of 50%) 477 477 477 477 Interest Bearing Debt 7,096 7,096 7,096 7,096 Value of Preferred Shares 95 95 95 95 Market Value of Equity 14,647 13,837 15,998 10,584 Per Share WorthPer Share WorthPer Share WorthPer Share Worth 122,955122,955122,955122,955 116,150116,150116,150116,150 134,293134,293134,293134,293 88,80088,80088,80088,800

20

April 10, 2007 SK Corporation

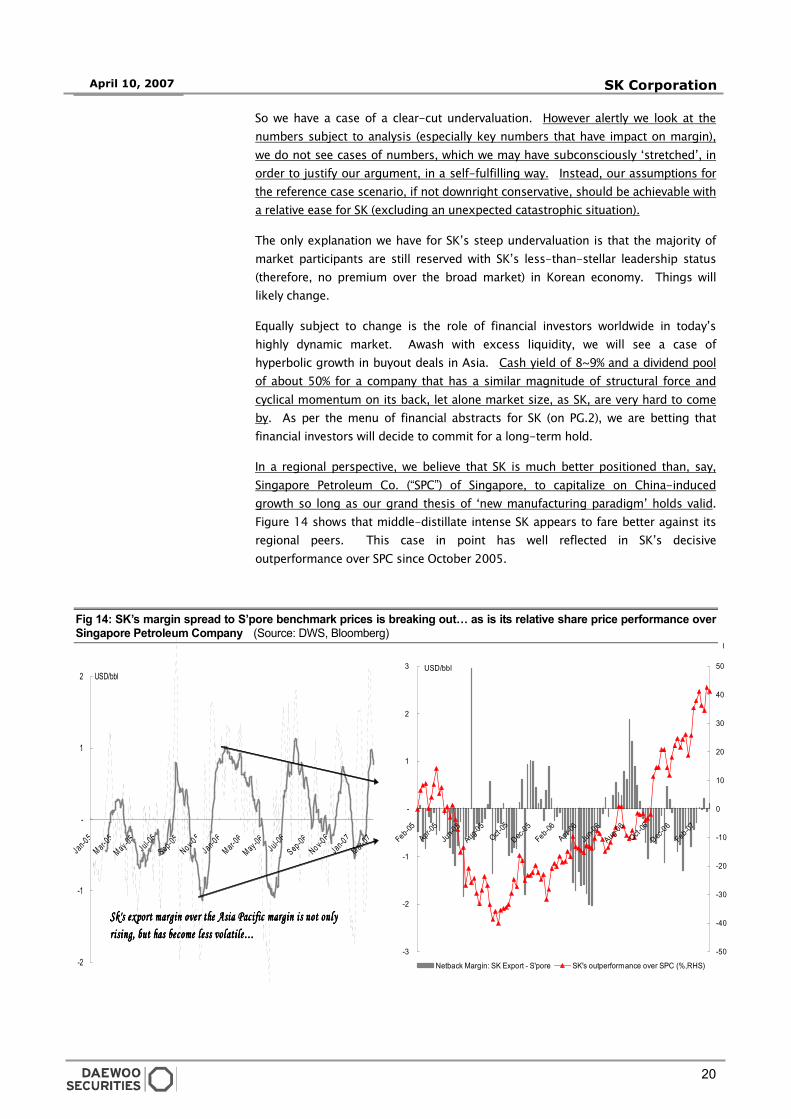

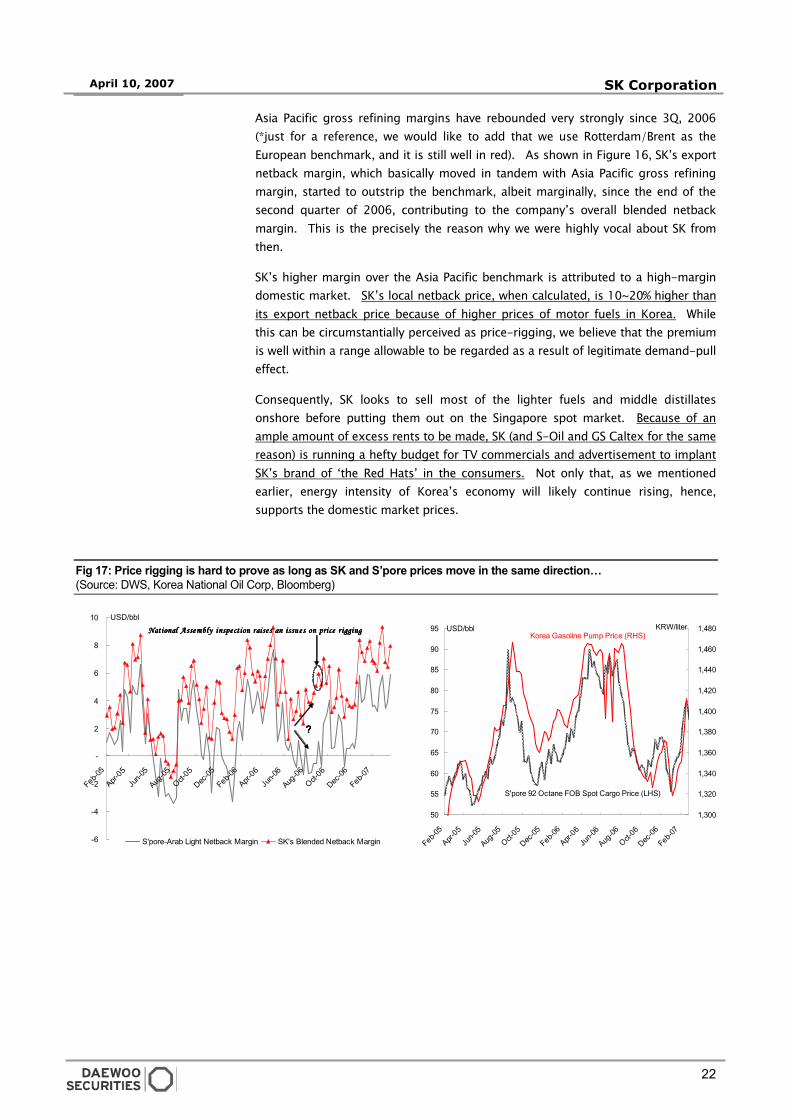

So we have a case of a clear-cut undervaluation. However alertly we look at the

numbers subject to analysis (especially key numbers that have impact on margin),

we do not see cases of numbers, which we may have subconsciously ‘stretched’, in

order to justify our argument, in a self-fulfilling way. Instead, our assumptions for

the reference case scenario, if not downright conservative, should be achievable with

a relative ease for SK (excluding an unexpected catastrophic situation).

The only explanation we have for SK’s steep undervaluation is that the majority of

market participants are still reserved with SK’s less-than-stellar leadership status

(therefore, no premium over the broad market) in Korean economy. Things will

likely change.

Equally subject to change is the role of financial investors worldwide in today’s

highly dynamic market. Awash with excess liquidity, we will see a case of

hyperbolic growth in buyout deals in Asia. Cash yield of 8~9% and a dividend pool

of about 50% for a company that has a similar magnitude of structural force and

cyclical momentum on its back, let alone market size, as SK, are very hard to come

by. As per the menu of financial abstracts for SK (on PG.2), we are betting that

financial investors will decide to commit for a long-term hold.

In a regional perspective, we believe that SK is much better positioned than, say,

Singapore Petroleum Co. (“SPC”) of Singapore, to capitalize on China-induced

growth so long as our grand thesis of ‘new manufacturing paradigm’ holds valid.

Figure 14 shows that middle-distillate intense SK appears to fare better against its

regional peers. This case in point has well reflected in SK’s decisive

outperformance over SPC since October 2005.

Fig 14: SK’s margin spread to S’pore benchmark prices is breaking out… as is its relative share price performance over Singapore Petroleum Company (Source: DWS, Bloomberg)

-3

-2

-1

-

1

2

3

Feb-05Apr-0

5

Jun-0

5

Aug-05

Oct-05

Dec-05

Feb-06Apr-0

6

Jun-0

6

Aug-06

Oct-06

Dec-06

Feb-07

-50

-40

-30

-20

-10

0

10

20

30

40

50

Netback Margin: SK Export - S'pore SK's outperformance over SPC (%,RHS)

USD/bbl

-2

-1

-

1

2

Jan-05

Mar-05

May-05

Jul-05

Sep-05

Nov-05

Jan-06

Mar-06

May-06

Jul-06

Sep-06

Nov-06

Jan-0 7

Mar-07

USD/bbl

Sk's export margin over the Asia Pacific margin is not onlySk's export margin over the Asia Pacific margin is not onlySk's export margin over the Asia Pacific margin is not onlySk's export margin over the Asia Pacific margin is not only

rising, but has become less volati le…rising, but has become less volati le…rising, but has become less volati le…rising, but has become less volati le…

21

April 10, 2007 SK Corporation

-6

-4

-2

-

2

4

6

8

10

Feb-05

Apr-05

Jun-0

5

Aug-05

Oct-05

Dec-05

Feb-06

Apr-06

Jun-0

6

Aug-06

Oct-06

Dec-06

Feb-07

S'pore-Arab Light Netback Margin SK's Blended Netback Margin

USD/bbl

-6

-4

-2

-

2

4

6

8

10

12

Feb-05

Apr-05

Jun-0

5

Aug-05

Oct-05

Dec-05

Feb-06

Apr-06

Jun-0

6

Aug-06

Oct-06

Dec-06

Feb-07

S'pore-Arab Light Netback Margin SK's Export Netback Margin

USD/bbl

22000077 OOPPEERRAATTIINNGG PPEERRFFOORRMMAANNCCEE

SSUURRPPRRIISSEE!! SSUURRPPRRIISSEE!! SSUURRPPRRIISSEE!!

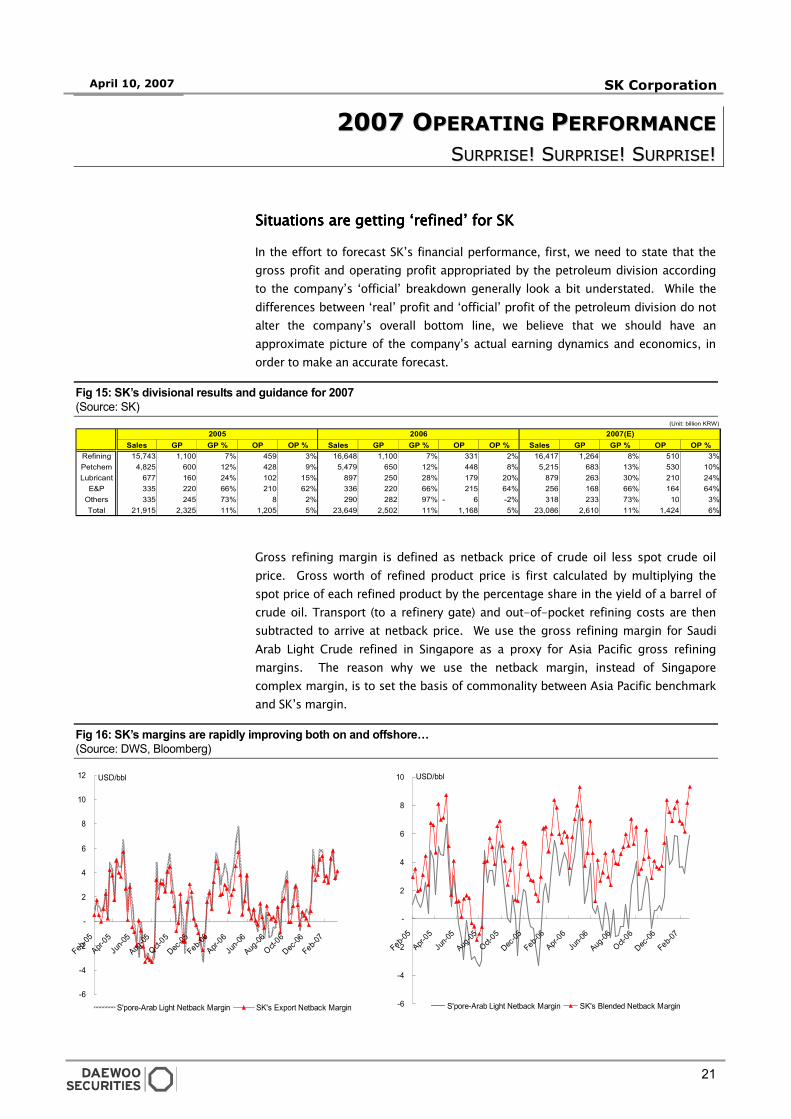

Situations Situations Situations Situations are are are are getgetgetgettingtingtingting ‘refined’ for SK ‘refined’ for SK ‘refined’ for SK ‘refined’ for SK

In the effort to forecast SK’s financial performance, first, we need to state that the

gross profit and operating profit appropriated by the petroleum division according

to the company’s ‘official’ breakdown generally look a bit understated. While the

differences between ‘real’ profit and ‘official’ profit of the petroleum division do not

alter the company’s overall bottom line, we believe that we should have an

approximate picture of the company’s actual earning dynamics and economics, in

order to make an accurate forecast.

Fig 15: SK’s divisional results and guidance for 2007

(Source: SK)

Gross refining margin is defined as netback price of crude oil less spot crude oil

price. Gross worth of refined product price is first calculated by multiplying the

spot price of each refined product by the percentage share in the yield of a barrel of

crude oil. Transport (to a refinery gate) and out-of-pocket refining costs are then

subtracted to arrive at netback price. We use the gross refining margin for Saudi

Arab Light Crude refined in Singapore as a proxy for Asia Pacific gross refining