Embed Size (px)

Citation preview

SITE Academic Conference

Stockholm, December 5-6, 2016

Bas B. Bakker

Senior Regional Resident Representative

for Central and Eastern Europe

CESEE:

Remaining challenges for faster growth

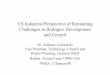

Change in GDP

per capita in DEU,

1995-16

Since the mid-1990s, CESEE has converged

with Germany

2GDP per capita in 1995

(PPP adjusted 2015 USD, thousands)

Ch

an

ge in

GD

P p

er

cap

ita, 1995-1

6

(perc

en

t)

GDP per capita in 1995 and its change, 1995-16

ALB

AUTBEL

BIH

BGR HRV

CYP

CZE

DNK

EST

FIN

FRA

RUS

GRC

HUN

IRL

ITA

LVA

LTU

UKR

MKDMLT

SRB & MNE

NLD

POL

PRT

ROMSVK

SVN

ESP

SWETURGBP

BLR

MDA

0

50

100

150

200

250

300

350

0 5 10 15 20 25 30 35 40

However, CESEE is still much poorer than

Germany

3

ALB

ROU

RUSPOL

UKRBIH

SRB & MNE

MKD

BLR BGR

HRV

LVA LTUHUN

SVK

EST

CZE

SVN

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

50000

1950 1960 1970 1980 1990 2000 2010

GDP per capita in Germany

(in constant 2014 dollars, PPP-adjusted)

Per capita income in CESEE

countries as of 2015

0

10

20

30

40

50

60

0 10 20 30 40 50 60 70 80 90 100

Why is CESEE poorer? Result of less labor input

and lower labor productivity.

4

Labor productivity and employment to total population ratio, 2015

Flags size reflects GDP per capita in 2015 (PPP-adjusted).

Em

plo

ym

en

t to

tota

l p

op

ula

tio

n r

ati

o

(perc

en

t)

Labor productivity

(PPP adjusted 2014 USD, thousands)

What determines labor input and labor

productivity?

Labor input per capita determined by

Employment rate of working age population

Share of working age population in

population

Labor productivity determined by

Capital stock per worker

Total factor productivity

5

Let’s look at these factors in more detail

What are prospects for further increase of

employment to population rate?

What is happening with growth of capital

stock?

What is happening with TFP — and what can

be done to boost it?

6

65

66

67

68

69

70

71

72

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

The share of the working age population is

relatively high—although it is now declining

7

CIS

SEE non-EU

CE-5

SEE EU

Baltics

Population ages 15-64

(percent of total population)

Note: Simple average of given countries.

Germany

0

10

20

30

40

50

60

70

80

90

0 10 20 30 40 50 60 70 80 90 100

If we compare employment to working age

population rate differences in labor input with

Germany are more pronounced

8

Em

plo

ym

en

t ra

te

(perc

en

t o

f w

ork

ing

ag

e p

op

.)

Labor productivity

(PPP adjusted 2014 USD, thousands)

Labor productivity and utilization, 2015

Flags size reflects GDP per capita in 2015 (PPP-adjusted).

50

55

60

65

70

75

80

2000 2002 2004 2006 2008 2010 2012 2014

Employment rates are still well below

Germany—with the exception of Baltics

9

20

25

30

35

40

45

50

2000 2002 2004 2006 2008 2010 2012 2014

DEU

Baltics

CE-5

SEE EU

CIS

SEE non-EU

Employment rate

(percent)

Note: Simple average of given countries.

20

22

24

26

28

30

32

34

36

38

40

2000 2002 2004 2006 2008 2010 2012 2014

With unemployment rates falling rapidly, it will be

important to increase labor force participation

10

0

2

4

6

8

10

12

14

16

18

20

2000 2002 2004 2006 2008 2010 2012 2014

SEE

non-EU

SEE EU

Baltics

CE-5

CIS

Unemployment rate

(percent)

Note: Simple average of given countries.

40

45

50

55

60

65

70

75

80

85

90

MD

A

BIH

HR

V

SR

B

UK

R

BG

R

ALB

PO

L

HU

N

RO

M

SV

N

LTU

MK

D

SV

K

LVA

RU

S

EST

CZ

E

DEU

Including of women

11

Labor force participation rate, 2015

(percent of either male or female population ages 15-64)

40

45

50

55

60

65

70

75

80

85

90

BIH

MD

A

MK

D

ALB

SR

B

RO

M

UK

R

PO

L

HR

V

HU

N

SV

K

BG

R

CZ

E

SV

N

RU

S

LTU

LVA

EST

DEU

Male Female

It’s important given that the impact of

aging will accelerate in the next decade…

12

Working age (15-64) population growth

(percent)

While higher labor input will help, higher capital stock

and thereby labor productivity may be even more

important

13

AUT

BEL

CYP

EST

FIN

FRA

DEU

GRC

IRL

ITA

LVA

LTU

LUX

MLT

NLD

PRT

SVK

SVNESP

BGR

HRV

CZE

DNK

HUN

POL

ROU

SWE

GBP

y = 0,3451x + 1,6927

R² = 0,8514

0

10

20

30

40

50

60

70

80

90

0 50 100 150 200

Capital stock and GDP per capita, 2015

(thousands of 2010 EUR)

Capital stock per capita

GD

P p

er

cap

ita

AUT

BEL

CYP

EST

FIN

FRADEU

GRC

IRL

ITA

LVA

LTU

LUX

MLT

NLD

PRTSVK

SVNESP

BGRHRV

CZE

DNK

HUNPOL

ROU

SWEGBP

y = 0,7094x - 6,5368

R² = 0,0276

0

10

20

30

40

50

60

70

80

90

35 40 45 50 55

Employment to population ratio and GDP per

capita, 2015

(percent and thousands of 2010 EUR)

Employment to population ratio

-1

0

1

2

3

4

5

6

7

8

9

10

11

12

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

However, growth of capital stock has

slowed…

14

ROM

EST

CZE

SVK

HUN

Net capital stock per worker growth

(3-year annualized change, percent)

…as investment rates post-crisis are (too)

low.

15

Investment to GDP ratio, 2015

(percent)

0

5

10

15

20

25

30

35

UKR BIH SRB HRV SVN POL LTU BGR HUN RUS LVA SVK MDA EST ROM CZE MNE ALB UVK BLR

Emerging markets and developing economies

Low investment not only problem: TFP growth

has slowed as well…

16

-8

-6

-4

-2

0

2

4

6

8

10

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

EST SVK CZE

HUN ROM POL

Total factor productivity growth

(3-year annualized change, percent)

…which means that a given increase in production

factors now leads to smaller increase in output.

17

Capital stock and GDP per capita

(2008=100, in logarithmic scales)

Capital stock per capita

GD

P p

er

cap

ita

So what should be done?

18

Address factors that might constrain

productivity (REI May-16)

Insufficient protection of property rights and

Inefficient legal systems and other government

services

Limited access to financial services (e.g. for

SMEs)

Infrastructural gaps

19

Improve public investment management

and tax administration (REI Nov-16)

Closing efficiency gaps in public investment and tax collection could bring sizable benefits.

Further upgrades of public investment management should focus on improving allocation and implementation frameworks and procedures.

Improvements in tax administration should aim at reducing compliance gaps.

Design of reforms should include elements that help reduce resistance to reforms and build the support base for their successful completion.

20

0

5

10

15

20

25

30

35

MNE BIH SRB ALB UKR LTU MDA POL LVA SVK BGR HRV RUS ROM SVN EST HUN CZE BLR MKD

Challenge: saving is very low, and may

constrain investment

21

National saving rates, 2015

(percent of GDP)

Emerging markets and developing economies

But can saving be raised?

Household saving difficult to influence

Corporate saving more likely to fall as labor

markets tighten further

Little appetite for boosting government saving

(i.e., reduce deficits)

22

ESTLVA

SVK

SVN

HRV

CZEHUN

POL

-10

-8

-6

-4

-2

0

2

4

-3 -2 -1 0 1 2 3 4 5 6

Scarcity of labor will likely reduce

corporate profits and saving

23

Change in wage share of income and corporate saving, 2013-16

(percentage points)

Change in adjusted wage share

(percent of GDP)

Ch

an

ge in

gro

ss s

avin

g o

f co

rpo

rate

sect

or

(perc

en

t o

f co

rpo

rate

sect

or

GV

A)

Higher wage share

Hig

her

savin

g

Only few countries are planning a meaningful increase

of the structural balance (>1/2 percentage point a

year) – even though unemployment is falling rapidly

24

Change in unemployment rate and structural balance

(percentage points)

BIH

BGR

HRV

CZEEST

HUN

LVA

LTUPOL

ROU

RUS

SRBSVK

SVN

TUR

UKR

-6

-5

-4

-3

-2

-1

0

1

2

3

-2,5 -2,0 -1,5 -1,0 -0,5 0,0 0,5 1,0 1,5

Ch

an

ge in

un

em

plo

ym

en

t ra

te, 2013-1

6

Change in structural balance

(percent of potential GDP), 2015-17

Conclusion

Further catch-up will necessitate

Increase labor force participation rate, which

would also help to offset declining share of

working age population

Higher investment, as capital stock is low

More efficient use of resources—boosting

TFP

Improving institutions and frameworks key.

25

Thank you