Embed Size (px)

Citation preview

Dr. Kamakhya Nr. Singh, CFO, LAPO Microfinance Bank http://ng.linkedin.com/in/kamakhyasingh/

Pa

ge1

Panel Discussion 1 -- Topic: Increasing Access to Finance

Panelists:

1. Mrs. Eme Essien Lore, Country Manager, IFC Nigeria

2. Mr. Waheed Olagunju, Executive Director, Bank of Industry

3. Dr. Yemi Kale, Statistician General/CEO, National Bureau of Statistics

4. Dr. Friday Okpara, Director (Strategic Partnership & Liaison Small &

Medium Enterprises Development Agency of Nigeria (SMEDAN)

5. Dr. Kamakhya singh, Chief Financial Officer, LAPO Microfinance Bank Ltd

My Structure for discussion

- A. Why increasing access to Finance

- B. Aspects of increasing access to Finance

- C. Finance Plus for handholding and enhancing capability

- D. Stakeholders to “Increasing Access to Finance”

- E. Providing access to those who have no access in Nigeria

- F. What is being done by institutions like LAPO MfB

Dr. Kamakhya Nr. Singh, CFO, LAPO Microfinance Bank http://ng.linkedin.com/in/kamakhyasingh/

Pa

ge2

A. Why increasing access to Finance

a) Empowerment – social, gender, geographical

b) Development – Economical, Financial – Development of self as also to society/economy (as jobs get created and economic activity gets enhanced)

Dr. Kamakhya Nr. Singh, CFO, LAPO Microfinance Bank http://ng.linkedin.com/in/kamakhyasingh/

Pa

ge3

B. Aspects of increasing access to Finance 1. Increasing access to those who already have access –

A) for example providing adequate funding to MSME sector (e.g. Private equity, venture capital, collateral Management, development capital, etc.), meeting newer demands for financially included such as leasing finance, mortgage finance, pension services, etc. B) Peculiarities of Financing, as per the life cycle of SMEs

-Start-up – Angel funding – SMEs by the lack of scalability may not attract the typical venture funding -Term lending -Working capital finance to help keep the operation running

C) The economics literature on enterprise financing has identified four main obstacles that may prevent SME from obtaining adequate financing. These obstacles are as follows: a) The existence of marked informational asymmetries between small

businesses and lenders, or outside investors; b) The intrinsic higher risk associated with small scale activities; c) The existence of sizeable transactions costs in handling SME financing. d) A fourth problem very often cited in the literature (and loudly lamented by

small entrepreneurs) is the lack of collateral that typically characterizes SME. Biggest issue in Nigeria (especially, from formal/commercial banking perspective) is that evaluation/due diligence of borrowers is collateral based rather than credit-risk based

2. Missing Middle – those enterprises, which are in a category higher than that of micro enterprises, but are below the category of formal SME

3. Providing access to those who have NO access

Dr. Kamakhya Nr. Singh, CFO, LAPO Microfinance Bank http://ng.linkedin.com/in/kamakhyasingh/

Pa

ge4

C. Finance Plus – Handholding and Enhancing capability It’s not enough to provide access to finance, when it comes to “micro” enterprises. At least in the initial stages, handholding, through training and programmes on financial literacy. The idea is that borrowers should be in a position to judiciously use the fun, generate returns effeciently so that they benefit as well as are able to return.

Dr. Kamakhya Nr. Singh, CFO, LAPO Microfinance Bank http://ng.linkedin.com/in/kamakhyasingh/

Pa

ge5

D. Stakeholders to “Increasing Access to Finance” a) Who are the stakeholders i) Government ii) Banking Sector iii) Non-Bank Financial players – MFIs, Insurance, Mortgage, Leasing,

Pension agencies iv) Service Providers and supporting Businesses – Telcos,

Network/Internet survice providers v) Media, especially in creating awareness and bringing issues for

urgent attention vi) Reserch Institutions, NGOs, public in general vii) Customers b)What interest would the stakeholders have in “Increasing Access to Finance” c) Need to have a strategy where a business case is made for all the stakeholders, i.e. “Increasing Access to Finance” doesn’t take place at the cost of business/profit of any stakeholder

Dr. Kamakhya Nr. Singh, CFO, LAPO Microfinance Bank http://ng.linkedin.com/in/kamakhyasingh/

Pa

ge6

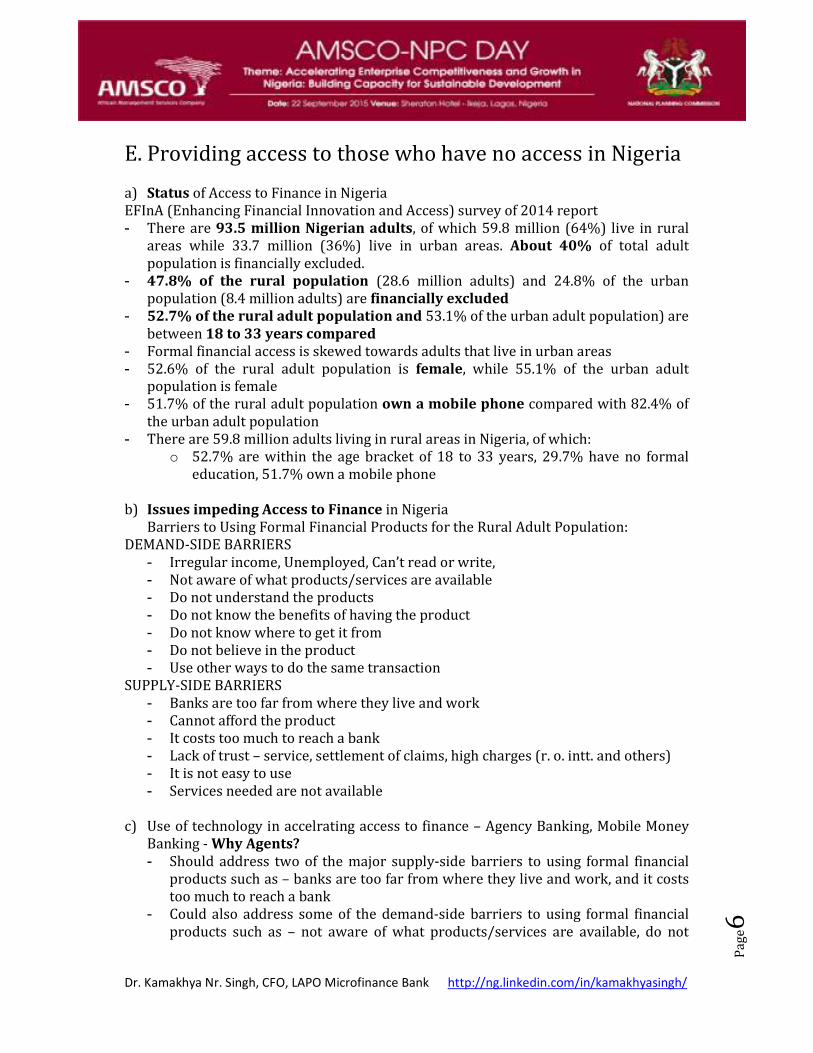

E. Providing access to those who have no access in Nigeria

a) Status of Access to Finance in Nigeria EFInA (Enhancing Financial Innovation and Access) survey of 2014 report - There are 93.5 million Nigerian adults, of which 59.8 million (64%) live in rural

areas while 33.7 million (36%) live in urban areas. About 40% of total adult population is financially excluded.

- 47.8% of the rural population (28.6 million adults) and 24.8% of the urban population (8.4 million adults) are financially excluded

- 52.7% of the rural adult population and 53.1% of the urban adult population) are between 18 to 33 years compared

- Formal financial access is skewed towards adults that live in urban areas - 52.6% of the rural adult population is female, while 55.1% of the urban adult

population is female - 51.7% of the rural adult population own a mobile phone compared with 82.4% of

the urban adult population - There are 59.8 million adults living in rural areas in Nigeria, of which:

o 52.7% are within the age bracket of 18 to 33 years, 29.7% have no formal education, 51.7% own a mobile phone

b) Issues impeding Access to Finance in Nigeria Barriers to Using Formal Financial Products for the Rural Adult Population:

DEMAND-SIDE BARRIERS - Irregular income, Unemployed, Can’t read or write, - Not aware of what products/services are available - Do not understand the products - Do not know the benefits of having the product - Do not know where to get it from - Do not believe in the product - Use other ways to do the same transaction

SUPPLY-SIDE BARRIERS - Banks are too far from where they live and work - Cannot afford the product - It costs too much to reach a bank - Lack of trust – service, settlement of claims, high charges (r. o. intt. and others) - It is not easy to use - Services needed are not available

c) Use of technology in accelrating access to finance – Agency Banking, Mobile Money

Banking - Why Agents? - Should address two of the major supply-side barriers to using formal financial

products such as – banks are too far from where they live and work, and it costs too much to reach a bank

- Could also address some of the demand-side barriers to using formal financial products such as – not aware of what products/services are available, do not

Dr. Kamakhya Nr. Singh, CFO, LAPO Microfinance Bank http://ng.linkedin.com/in/kamakhyasingh/

Pa

ge7

understand the products, do not know the benefits of having the products, and do not know where to get products from

d) Use a targeted Approach Target – i) Segment of Population/Geography - RURAL, YOUTH, WOMEN ii) Means of providing access – TECHNOLOGY, AGENCY iii) Environment – ENABLING, SECURE

Dr. Kamakhya Nr. Singh, CFO, LAPO Microfinance Bank http://ng.linkedin.com/in/kamakhyasingh/

Pa

ge8

F. What is being done by institutions like LAPO MfB

o Status of LAPO MfB – network and financial strength

� 386 branches across 27 states (+FCT), with about 1.9 million clients

� Total Asset of ~US$242 million and Gross Loan Portfolio of ~US$207 million

� Disbursement of 2014 - US$471 million; Projected for 2015 - US$689 million

o Products and Services of LAPO for addressing diverse needs of clients � Credit Products - Asset Loans, Business Loans, Enterprise

Loans, Agricultural Loans, Festival Loans, Affordable Housing, SUFEN

� Savings Products - Regular Savings, Festival Business Savings, Golden Savings, Social Deposits

� Insurance Products - Life, Fire, Child Delivery Expense � Innovative Products and Services - Affordable Housing, SUFEN,

Green Products, Agency Banking

o Women Empowerment - More than 90% of our clients are women; about 60% of staff members are female

o Pillars of Strategy 2013-17 – Clients, Products, HR (Staffs), Performance Management and Technology

o Non Financial products to bring additional benefits – Scholarship, Legal Aid (for women who face threats of social injustice), Health (Offer trainings which addresses issues on poor nutrition, ill health, discrimination, injustice, gender inequity and other entrenched obnoxious socio-cultural practices), Insurance