Embed Size (px)

Citation preview

“OIDMTC”Ontario Interactive Digital media Tax Credit

“Interactive digital media product” is defined by the regulation as a combination of one or more application files and one or more data

files, all in a digital format, that are integrated and are intended to be operated together”

• The OIDMTC is a refundable tax credit, which means that the amount of the credit, minus any Ontario taxes payable, will be paid to the qualifying corporation. The OIDMTC is based upon the Ontario labour expenditures and in some cases eligible marketing and distribution expenditures claimed by a qualifying corporation with respect to eligible products.

• There is no limit on the amount of eligible Ontario labour expenditures which may qualify and there are no per-project or annual corporate limits on the amount of the OIDMTC which may be claimed. Eligible marketing and distribution expenses are capped at $100,000 per eligible product.

• A qualifying corporation is a Canadian corporation (it may be Canadian or foreign-owned), that develops non-specified or specified products at a permanent establishment in Ontario operated by it, and files an Ontario corporate tax return.

• A qualifying small corporation is a Canadian corporation (it may be Canadian- or foreign-owned), that develops an eligible product at a permanent establishment in Ontario operated by it, had during the taxation year (on an associated company basis) neither annual gross revenues in excess of $20 million nor total assets in excess of $10 million, and files an Ontario corporate tax return.

What Types of Products Are Eligible? • There are four types of products that can be claimed under the OIDMTC, non-specified products,

specified products, eligible digital games developed by a qualifying digital game corporation, and eligible digital games developed by a specialized digital game corporation.

• To be eligible for the OIDMTC a product must be an interactive digital media product whose

primary purpose is to educate, inform, or entertain, and that achieves its primary purpose by presenting information in at least two of: (i) text, (ii) sound and (iii) images.

• Types of interactive digital media products that may be eligible for the tax credit include but are not restricted to games, educational or informational products. Operating system software is not eligible for the tax credit.

• In addition, the following requirements must be satisfied for a product to be a non-specified product of the qualifying corporation:

– 1. All or substantially all of the product was developed in Ontario by the qualifying corporation or by the qualifying corporation and a qualifying predecessor corporation.

– 2. The product was developed for sale or licensing by the qualifying corporation to one or more arm’s length parties who have not previously entered into an arrangement with the qualifying corporation or a qualifying predecessor corporation for the development of the product.

– 3. The product is not used primarily for interpersonal communication. – 4. The product is not used primarily to present or promote the qualifying corporation or a qualifying

predecessor corporation. – 5. The product is not used primarily to present, promote or sell the products or services of the qualifying

corporation or of a qualifying predecessor corporation.

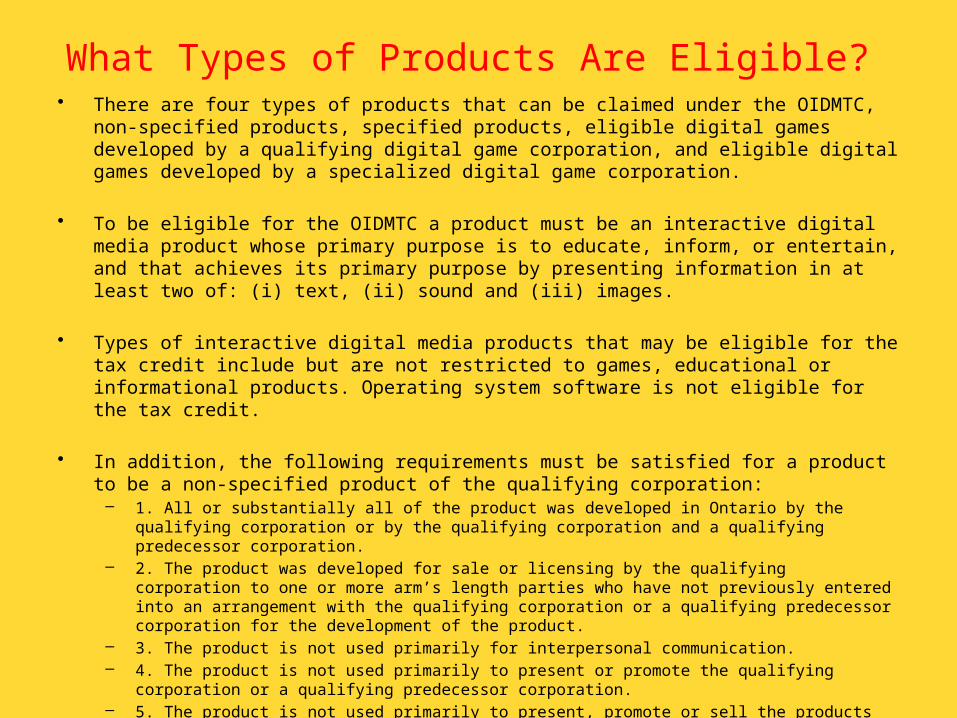

• The OIDMTC is calculated as 40% of the qualifying expenditures incurred after March 26, 2009, by a qualifying corporation, regardless of size of corporation, to create eligible interactive digital media products in Ontario. The OIDMTC is also available to qualifying corporations that develop “specified” products under a fee-for-service arrangement in Ontario calculated as 35% of the qualifying expenditures incurred after March 26, 2009. For products completed prior to March 26, 2009 and applicable tax credit rates prior to that rate see OIDMTC Rates & Eligibility Periods Chart below.

• The OIDMTC is calculated as 35% of qualifying labour expenditures incurred after March 26, 2009 for the creation of eligible digital games developed in whole or in part by a qualifying digital game corporation or a specialized digital game corporation.

OIDMTC Rates and Eligibility Periods Chart for Non-Specified and Specified ProductsProduct Completion Date Prior to 24 March 2006 After 23 March 2006 & Prior

to 26 March 2008 After 25 March 2008 & Prior to 27 March 2009

After 26 March 2009

Qualifying Small Corporation Rate Non-Specified Product 20% 30% 30% 40%Specified Product N/A 20% 25% 35%Qualifying Corporation Rate Non-Specified Product N/A 20% 25% 40%Specified Product N/A 20% 25% 35%Qualifying Wage Expenditure Non-Specified Product 100% 100% 100% 100%Specified Product N/A 100% 100% 100%Qualifying Remuneration Expenditure Non-Specified Product 50% 50% 50% 100%Specified Product N/A N/A N/A 100%Marketing & Distribution Expenditure (Non-Specified Products Only) 100% to a maximum $100,000 per product

Labour Expenditure Period

(*going back in time from…)

*24 months from the beginning of the month in which the product was completed

*25 months from the end of the month in which the product was completed

*37 months from the end of the month in which the product was completed

*37 months from the end of the month in which the product was completed

Marketing & Distribution Expenditure Period 24 months

• Must be an interactive digital media product• 90% or more of the product must be developed in

Ontario by the applicant• Must be developed for sale or licensing to arm’s-length

parties (not developed under a fee-for-service arrangement)

• Not used primarily for interpersonal communication• Not used primarily for promotion of the applicant or the

applicant’s products or services

• Must be an interactive digital media product• 90% or more of the product must be developed in Ontario by the

applicant• Product is developed by the applicant under the terms of an

agreement with an arm’s length purchaser corporation• Product must be for sale or license to one or more people who deal

at arm’s-length with the purchaser• Must not be used primarily to present/promote the qualifying

corporation or the purchaser corporation, or to promote/sell their products and services

• The development of the product must be completed after March 23, 2006

Non-Specified VS Specified products

Developed by applicant for saleor license to arm’s-length parties

Developed by applicant under an agreement with arm’s-length purchaser corporationFor sale or license to one or more people who deal at arm’s- length with the purchaser

Non-Specified vs. Specified

Eligibility requirements for:

Non-Specified VS Specified products

-labour expenditures: a)salaries & wages of employees, and

b)b) remuneration (arm’s-length contract labour)-marketing & distribution expenditures

-Rate = 40%

-labour expenditures:a) salaries & wages of employeesandb) remuneration (arm’s-length contract labour)

-Rate = 35%

Non-Specified vs. SpecifiedQualifying Expenditures for:

Eligible Digital Games Developed by Digital Game Corporations

An eligible digital game developed by a Qualifying Digital Game Corporation or Specialized Digital Game Corporation includes but is not limited to the following components:

– played on one or more multiple platforms using digital technology

– played interactively by one or more users, involves a set of rules for game play

– has variable outcomes, may have a number of elements that are used in combination (i.e. narrative, visual representation, music, sound, etc.)

– screen based interactive game that should be intended to entertain and may also be intended to educate or inform, a general consumer audience (with caveat that customized games may be considered on a case by case basis)

Note that games must still meet the eligibility requirements of an interactive digital media product and include at least two of text, sound and images.

• Company must carry on a business that includes the development of eligible digital games

• Incurs a minimum of $1million in Ontario labour costs in a 36 month period on a digital game that is developed under an agreement with a purchaser corporation

Benefits:• Company is not required to develop 90% or more of the game• The digital game does not need to be completed• The purchaser corporation does not need to be arm’s length from

the applicant company

Eligible Digital Games Developed by Qualifying Digital Game Corporations

Company must meet either A) or B):

A) 80%of the company’s salaries and wages for services rendered in Ontario are directly attributable to the development of digital games;

OR

B) 90%of the company’s gross revenues are directly attributable to the development of digital games;

AND• The company must incur a minimum of $1million in eligible labour that

is directly attributable to the development of eligible digital games in a taxation year.

Benefits:• Company is not required to develop 90% or more of the game(s)• The digital games do not need to be completed• If there is a purchaser corporation, it does not need to be arm’s length from the

applicant company• If the company qualifies as a Specialized Digital Game Corporation they can apply to

the OMDC on an annual basis

Eligible Digital Games Developed by Specialized Digital Game Corporations

Eligible Costs Digital Game Corporations

For qualifying and specialized digital game corporations eligible costs include:

• 100% qualifying wages and salaries* of employees for work rendered in Ontario that is directly attributable to the development of the digital game(s)

• 100% qualifying arm’s length remuneration*(non-employees) for services rendered in Ontario paid to individuals, personal services corporations for the services of the sole shareholder, partnerships for the services of one of the partners

For digital game corporations claiming under s.93.1 or s.93.2 qualifying remuneration does not include amounts paid to another taxable Canadian corporation for the services of their employees.

* Eligible costs are incurred after March 26, 2009

Eligible Digital Games Developed by Digital Game Corporations Recap

Qualifying Digital Game Corporation Specialized Digital Game CorporationLabour expenditures:

-salaries and wages (employees)

- remuneration (contracted labour) arm’slength

-excludes remuneration paid to another taxable Canadian corporation for services of their employees

-minimum $1million in Ont labour incurred in36 month period for a game that is developed under an agreement with a purchaser corporation

- rate 35%

Labour expenditures:

-salaries and wages (employees)

-remuneration (contracted labour) arm’slength

-excludes remuneration paid to another taxable Canadian corporation for services of their employees

- minimum $1 million in Ont labour incurred in one taxation year for a game or games developed in whole or in part by the applicant

- rate 35%

- claimed in tax year when applicant has incurred the minimum $1million in eligible Ontario labour costs over a 36 month period

-annual claim

-Includes costs incurred in the one tax year

For non-specified and specified products (s. 93):• corporations apply to the OMDC for each taxation year that they complete

products in. The OMDC issues a “Certificate of Eligibility” for each taxation year for products that have been completed in that year.

• If more than one product is completed by applicant in that year, the Certificate will be issued for the costs incurred for multiple products.

For qualifying digital game corporations (s. 93.1):• qualifying digital game corporations apply to the OMDC at the end of the 36

month period in which they incur $1million in eligible labour for a digital game

For specialized digital game corporations (s. 93.2):• •Specialized digital game corporations apply to the OMDC at the end of the

taxation year in which they incur $1million in eligible labour on digital game(s)

• There are now four types of products that can be claimed under the OIDMTC:

– Non-Specified

– Specified

– Qualified Digital Game Corporations

– Specialized Digital Game Corporations

• To be eligible for the OIDMTC a product must be an interactive digital media product whose primary purpose is to

(1) Educate

(2) Inform

(3) Entertain

HOW DO WE ACHIEVE THIS?

The primary purpose is presenting information in at least two ways:

• (1) text

• (2) sound

• (3) images

• They are intended to be used by individuals.

• By interacting with them, the user can choose what information is to be presented and the form and sequence in which it is to be presented.

• Types of interactive digital media products that may be eligible for the tax credit include but are not restricted to games, educational or informational products.

• Such products may include, but are not limited to: websites, CD-ROMS, DVD-ROMS and kiosks.

• Operating system software and software such as word processing, spreadsheet and database software may not constitute an eligible product.

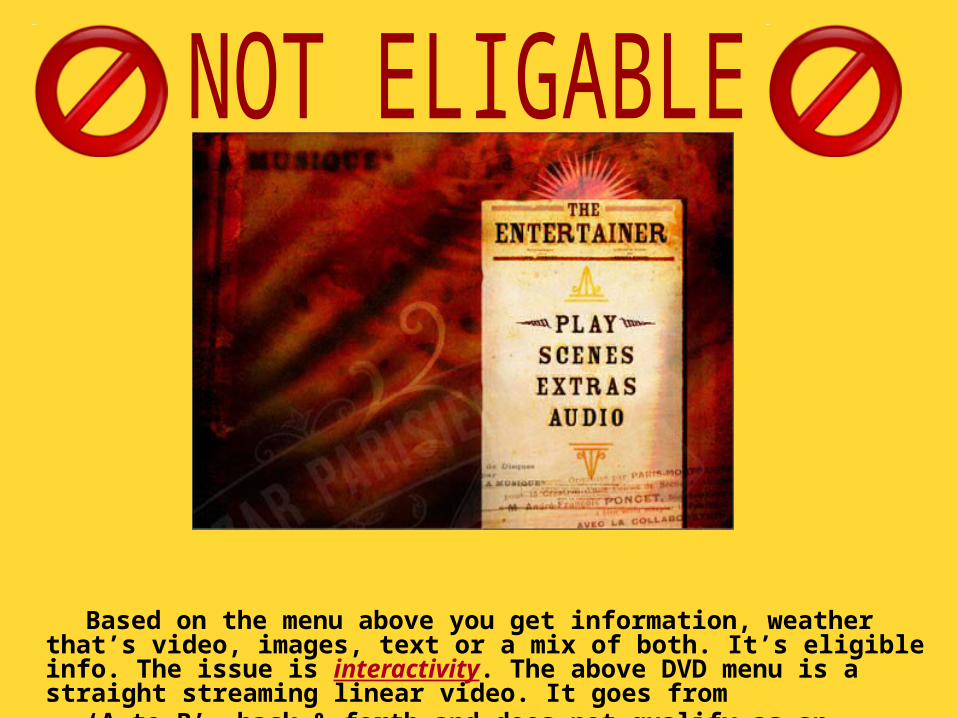

Based on the menu above you get information, weather that’s video,

images, text or a mix of both. It’s eligible info. The issue is interactivity. The above DVD menu is a straight streaming linear video. It goes from

‘A to B’, back & forth and does not qualify as an interactive digital media product. You need to have control over the sequence and events.

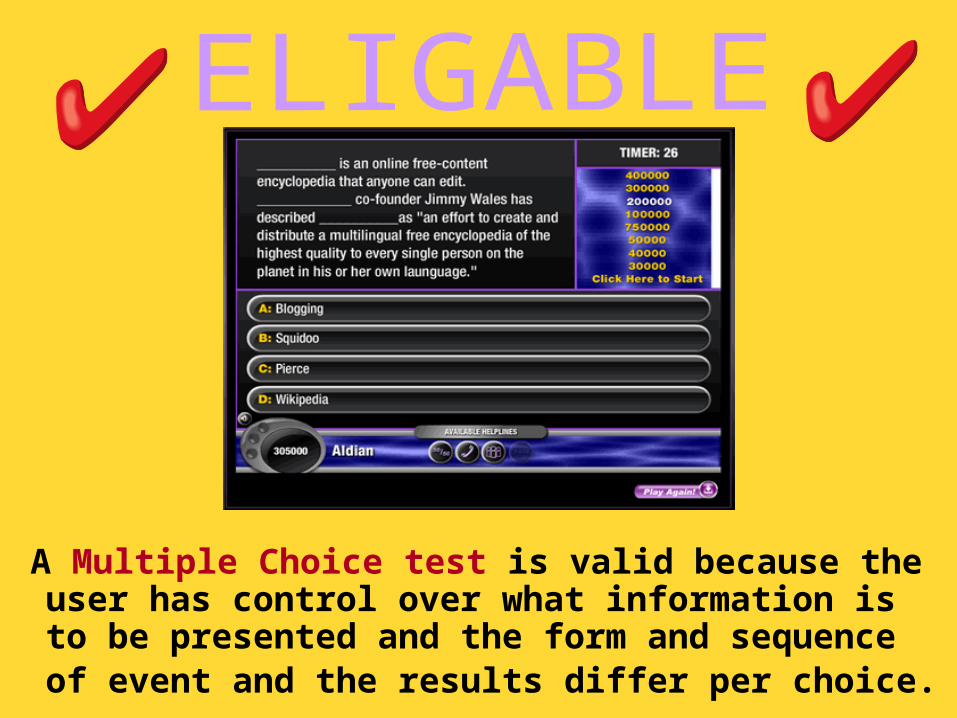

A Multiple Choice test is valid because the

user has control over what information is to be presented and the form and sequence of event and the results differ per choice.

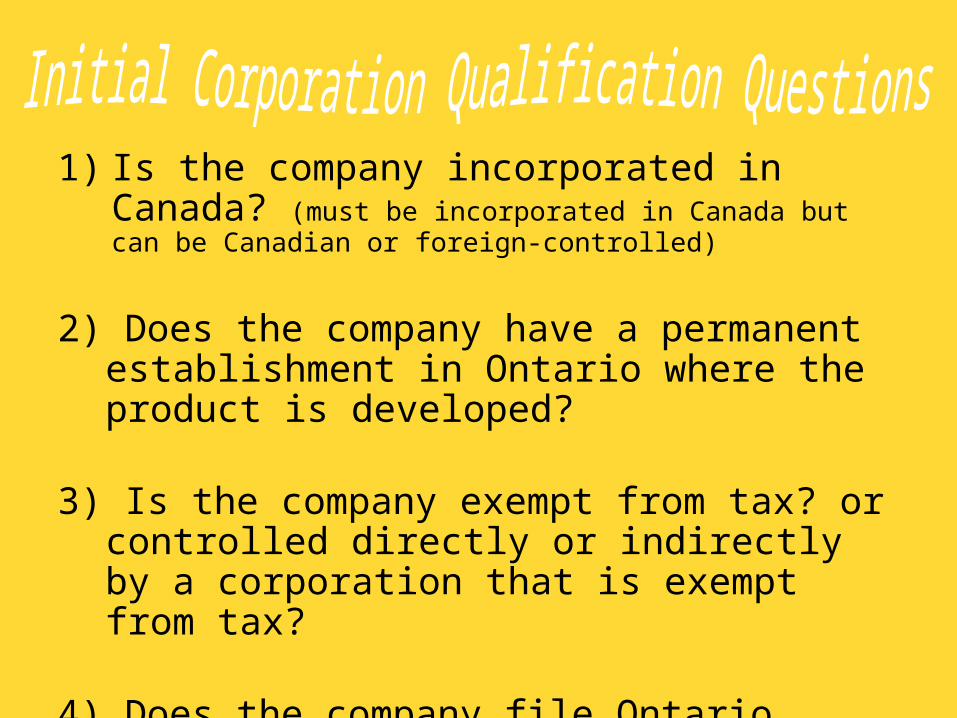

1) Is the company incorporated in Canada? (must be incorporated in Canada but can be Canadian or foreign-controlled)

2) Does the company have a permanent establishment in Ontario where the product is developed?

3) Is the company exempt from tax? or controlled directly or indirectly by a corporation that is exempt from tax?

4) Does the company file Ontario Corporate Tax?

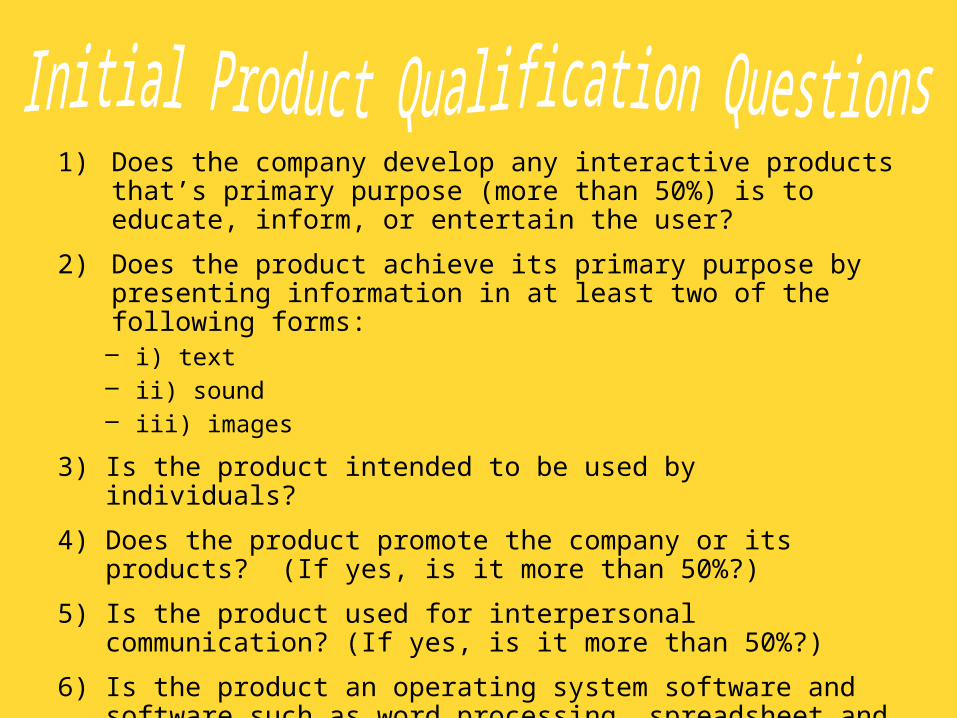

1) Does the company develop any interactive products that’s primary purpose (more than 50%) is to educate, inform, or entertain the user?

2) Does the product achieve its primary purpose by presenting information in at least two of the following forms:– i) text– ii) sound– iii) images

3) Is the product intended to be used by individuals?

4) Does the product promote the company or its products? (If yes, is it more than 50%?)

5) Is the product used for interpersonal communication? (If yes, is it more than 50%?)

6) Is the product an operating system software and software such as word processing, spreadsheet and database software? (If yes, is it more than 50%?)

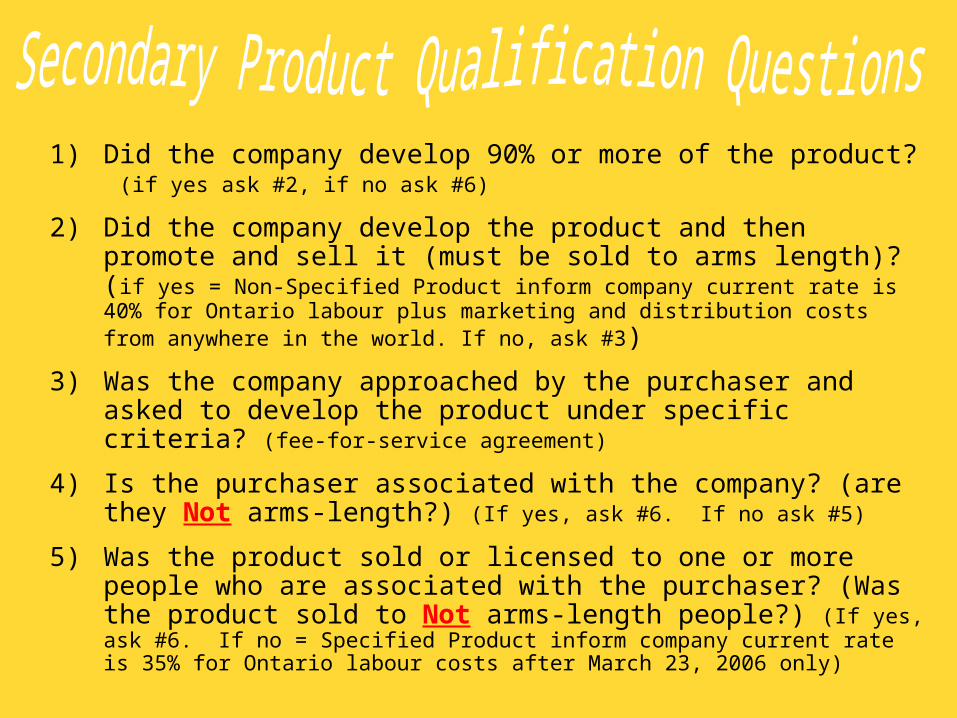

1) Did the company develop 90% or more of the product? (if yes ask #2, if no ask #6)

2) Did the company develop the product and then promote and sell it (must be sold to arms length)? (if yes = Non-Specified Product inform company current rate is 40% for Ontario labour plus marketing and distribution costs from anywhere in the world. If no, ask #3)

3) Was the company approached by the purchaser and asked to develop the product under specific criteria? (fee-for-service agreement)

4) Is the purchaser associated with the company? (are they Not arms-length?) (If yes, ask #6. If no ask #5)

5) Was the product sold or licensed to one or more people who are associated with the purchaser? (Was the product sold to Not arms-length people?) (If yes, ask #6. If no = Specified Product inform company current rate is 35% for Ontario labour costs after March 23, 2006 only)

6) Is the product a digital game? (If yes, ask # 7. If no, product does not qualify)

7) Did the company incur a minimum of $1million in labour to develop the product within a taxation year (must be after March 27, 2009)? (If yes, ask #9. If no, ask #8)

8) Did the company incur a minimum of $1million in labour to develop the digital game in a 36 month period (must be after March 27, 2009)? (If yes, company is a Qualifying Digital Game Corporation and rate is 35% for Ontario labour. If no, product does not qualify)

9) Is 80% of the company’s salaries and wages for services rendered in Ontario are directly attributable to the development of digital games? (if yes, company is a Specialized Digital Game Corporation and rate is 35% for Ontario labour. If no, ask #10)

10) Is 90%of the company’s gross revenues are directly attributable to the development of digital games? (if yes, company is a Specialized Digital Game Corporation and rate is 35% for Ontario labour. If no, product does not qualify)