Embed Size (px)

Citation preview

LendIt USA 2017March 6 & 7

NYCSynopses of Attended Sessions

Preface

Ralph Daloisio 2

• The 5th annual LendIt conference was held at the Jacob Javits Center in NYC on March 6th and 7th

• Around 5,800 people attended

• There were 11 “tracks,” of which up to 9 were occurring simultaneously– making it impossible for one person to cover the entire conference

• This deck of slides summarizes 18 of the 36 keynote addresses and panels, + one breakout panel

• Slide inlays come directly from the presenters themselves

• Added bullet-‐point comments reflect notes I took to record the points being made by presenters

• Words appearing in “[ ]” are my own comments, but these have been kept to a minimum

• Slide #8 lists all 36 keynotes, and highlights the ones summarized in this deck

• Slides #9 thru #11 contain my conclusions (to be read at your own peril, if read at all)

• Slides #12 thru #14 contain the “Top Takeaways” from the sessions covered

• I hope you find some useful information in what follows

Table of Contents (1/2)

Ralph Daloisio 3

Topic or Presenter(s) Page Numbers

Historical Number of Attendees and Exhibitors 5,6

LendIt USA 2017 ”Bandwidth”: Categories, Topics, and (Number of Sessions) 7

List of Keynote Sessions and Panels 8

My Conclusions (read at your own peril) 9-‐11

Top Takeaways 12-‐14

Scott Sanborn, President & CEO, Lending Club 15

Ash Gupta, President of Global Credit Risk and Information Management at American Express 16

Nigel Morris, Managing Partner, QED 17-‐19

Rob Frohwein, CEO & Co-‐Founder, Kabbage 20-‐24

Ram Ahluwalia, CEO, PeerIQ 25-‐31

Investor Insights Panel: Every Originator Will Launch a Fund 32

Anthony Hsieh, CEO, LoanDepot 33-‐39

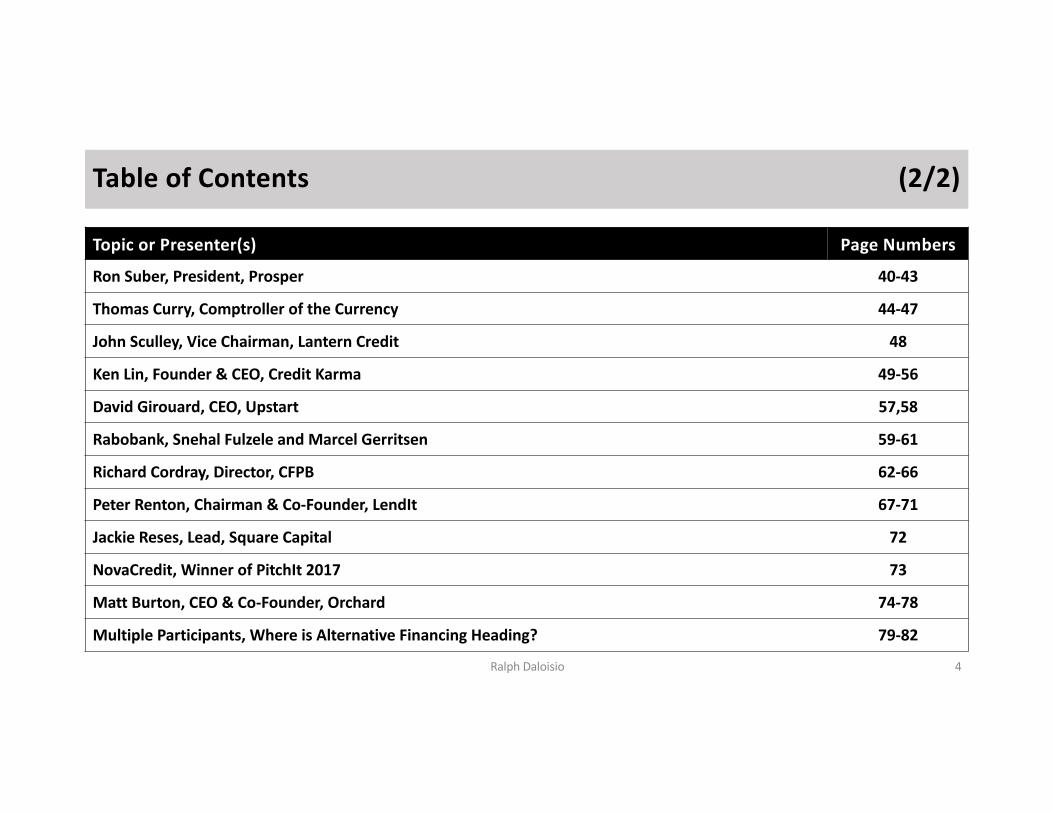

Table of Contents (2/2)

Ralph Daloisio 4

Topic or Presenter(s) Page Numbers

Ron Suber, President, Prosper 40-‐43

Thomas Curry, Comptroller of the Currency 44-‐47

John Sculley, Vice Chairman, Lantern Credit 48

Ken Lin, Founder & CEO, Credit Karma 49-‐56

David Girouard, CEO, Upstart 57,58

Rabobank, Snehal Fulzele and Marcel Gerritsen 59-‐61

Richard Cordray, Director, CFPB 62-‐66

Peter Renton, Chairman & Co-‐Founder, LendIt 67-‐71

Jackie Reses, Lead, Square Capital 72

NovaCredit, Winner of PitchIt 2017 73

Matt Burton, CEO & Co-‐Founder, Orchard 74-‐78

Multiple Participants, Where is Alternative Financing Heading? 79-‐82

LendIt USA Attendance (Historical)

375 975

2,500

3,500

5,800

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2013 2014 2015 2016 2017

LendIt2USA2Attendance

#"of"Attendees

Ralph Daloisio 5

Source: “The LendIt Story.” deBanked Magazine January/February 2017

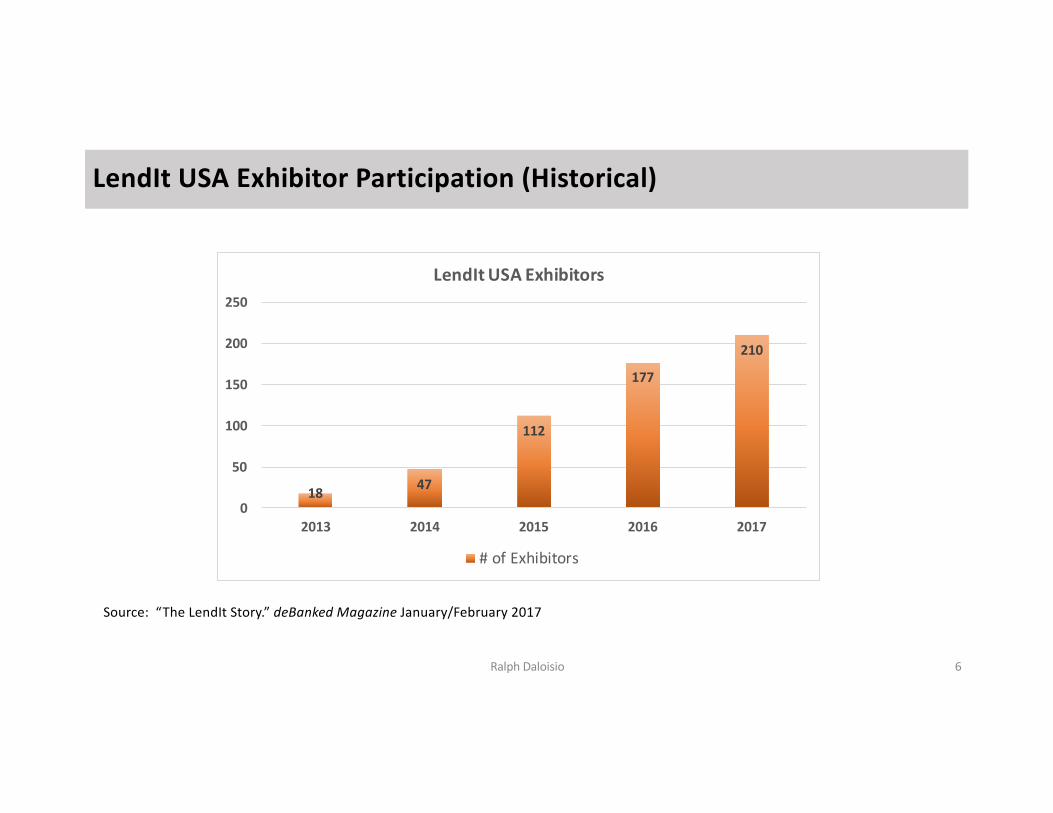

LendIt USA Exhibitor Participation (Historical)

18 47

112

177

210

0

50

100

150

200

250

2013 2014 2015 2016 2017

LendIt0USA0Exhibitors

#"of"Exhibitors

Ralph Daloisio 6

Source: “The LendIt Story.” deBanked Magazine January/February 2017

LendIt USA 2017 “Bandwidth”: Categories, Topics & (# of Sessions)

KeynoteSessions

Innovation in Lending

Innovationin Real Estate

The Fintech Universe

Bank Technology

The Investor’s Perspective

Company Demos

GlobalPerspective

Policy & Regulation

Financial Inclusion

Training for Staff

DAY1

(19)Small

Business Lending

(8)

Block-‐chain(4)

Investor Insights

(7)(25) (8) (8) (8)

Sales and

Mrkting (4)

Insur-‐Tech(4)

FundManager Pitches(14)

Tech & Ops(4)

DAY2 (17)

Credit and

Under-‐writing (9)

Digital Mort-‐gages (4)

DigitalWealth Manage-‐ment(4)

Bank Partner-‐ships(4)

Autos, SLs,

Equip.Etc.(7)

(20)Consum-‐

erLending

(8)

Resi-‐ & Commer-‐cial Real Estate (4)

Fintech AI &

Biomet-‐rics(3)

Digital Banking

(3)

FundManager Pitches(15)

Ralph Daloisio 7

List of Keynote Speeches and Panels (All Held in the Special Events Hall)Summaries Contained within are Highlighted in Yellow

KEYNOTE DAY ONE MARCH 6TH DAY TWO MARCH 7TH

1 Welcome Remarks (Brustkern, Jones, and Renton) Welcome Remarks (Renton)

2 Investing in the Future (Sanborn) Blockchain Revolution (Don and Alex Tapscott)

3 Innovation in Credit Granting with Big Data (Gupta) The End of the Beginning (Jenkins and King)

4 If I Were to Start a Bank Today, This is What it Would Look Like (Morris) Cognitive Computing & AI are Transforming Financial Services (Walter)

5 Alternative Lending is Dead, Long Live Data (Frohwein) China Fintech Opportunity to the World (Hai and Guo)

6 Why Securitization & Online Lending are So Important (Ahluwalia) Unstoppable Trends in Online Lending (Breslow)

7 Fintech: The View from Congress (Congressman McHenry) Scaling the Movement of Financial Inclusion (Jung)

8 The Future of Advice (Stein) Investing with Impact: Digital Wealth with a Conscience (Walia)

9 Modern Lending: Today & Tomorrow (Hsieh) How Marcus is Altering the Online Lending Landscape (Talwar & O’Connell)

10 Trade Finance on the Blockchain (Htite) The Marketplace Lending Global Overview (Renton)

11 Online Lending: An Industry Built to Last (Suber) Tech Chat: The Role Lending Can Play in Empowering More Businesses (Reses)

12 Financial Technology Innovation & the Federal Banking System (Curry) Pitchit @ LendIt Winner’s Company Demo (Sigel)

13 The Intersection of Technology and Consumer Credit (Sculley) Expanding the Tent for Both Investors and Originators (Burton)

14 From Wild to Healthy Growth: China Fintech (Fang & Cao) Three Years Out: Where is Alternative Financing Heading? (5-‐Person Panel)

15 Personal Loans: The Keys to Success (Lin) Pitchit @ LendIt AudienceWinner’s Company Demo (Sigel)

16 Is Fintech More Fin than Tech? (Girouard) Taking the High Road: There’s a Lot Less Traffic There (Wang)

17 Innovation at the Edge: Banks Transition to Hybrids (Fulzele & Gerritsen) Closing Remarks (Renton)

18 The Latest M&A Trends in Fintech (McLaughlin and Ciporin)

19 Fintech Innovation: The View of the CFPB (Cordray) Ralph Daloisio 8

My Conclusions (read at your own peril) (1/3)

• The threat of the “titans of tech” (Amazon, Google, Facebook, etc) stampeding over the nascent Fintech industry is overblown, baring an act by Congress and the current Administration to undo the Bank Holding Company Act which clearly separates banking and commerce. (Walmart has been trying to expand into banking for years with minimal inroads.) And given the ties between the current Administration and Goldman Sachs (the best marriage yet between technology and banking), it’s only a distant possibility at best.

• There is a lot of ”smoke and mirrors” around alternative data’s predictive qualities.

• Good science often leads us to counter-‐intuitive results. Beware of what “feels right.”

• More independent and scientific rigor is needed to validate conclusions drawn from new sets of data.

• If alternative data results are coming from someone who is trying to offer a better mousetrap, there’s an inherent bias already that needs to be overcome.

Ralph Daloisio 9

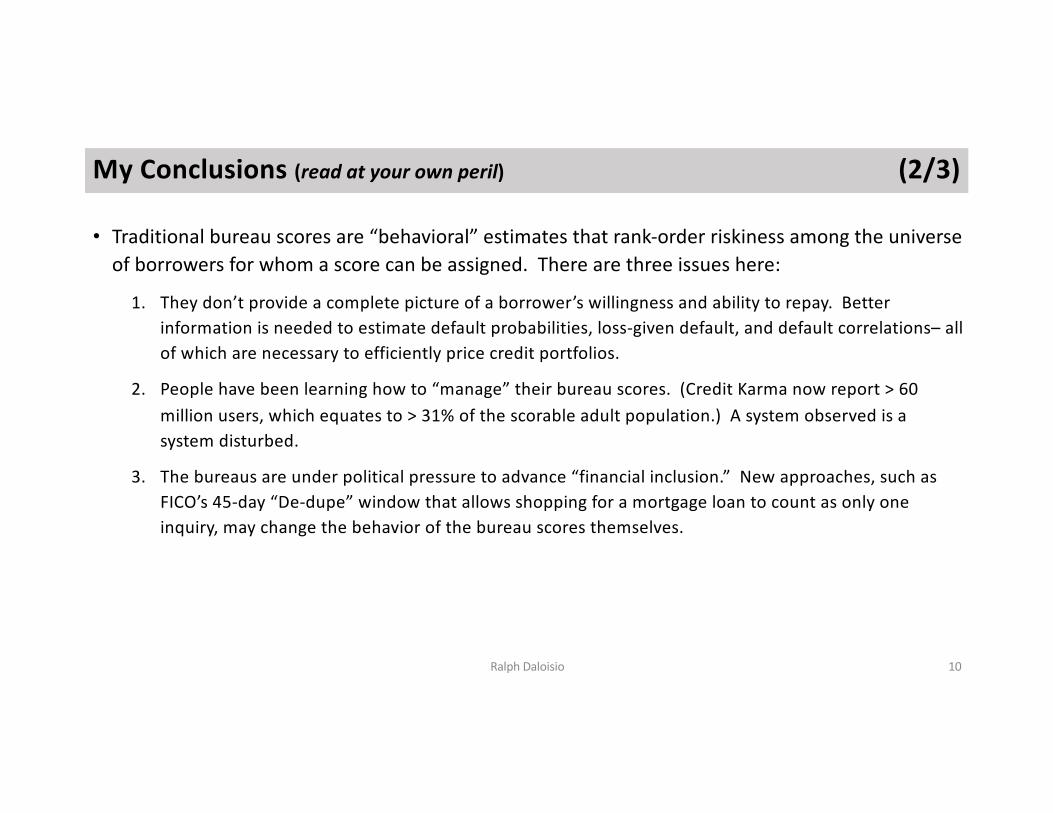

My Conclusions (read at your own peril) (2/3)

• Traditional bureau scores are “behavioral” estimates that rank-‐order riskiness among the universe of borrowers for whom a score can be assigned. There are three issues here:

1. They don’t provide a complete picture of a borrower’s willingness and ability to repay. Better information is needed to estimate default probabilities, loss-‐given default, and default correlations– all of which are necessary to efficiently price credit portfolios.

2. People have been learning how to “manage” their bureau scores. (Credit Karma now report > 60 million users, which equates to > 31% of the scorable adult population.) A system observed is a system disturbed.

3. The bureaus are under political pressure to advance “financial inclusion.” New approaches, such as FICO’s 45-‐day “De-‐dupe” window that allows shopping for a mortgage loan to count as only one inquiry, may change the behavior of the bureau scores themselves.

Ralph Daloisio 10

My Conclusions (read at your own peril) (3/3)

Ralph Daloisio 11

• The incursion of tech into information-‐heavy businesses (e.g, finance and insurance) will transform those industries even more so than robotics have transformed the manufacturing industries. Tech can automate paper and paper-‐based decisioning in a way that’s cheaper, faster, and better than outsourcing manufacturing to the world’s cheapest labor pools.

• Those with the best data (not the most data) and most insightful algorithms will have the advantage.

• The industry is young, mercurial, and unstable. There is ample opportunity to facilitate maturity, dependability, and stability.

• The next phase of growth may very well be disruptive to the disruptors as many thinly capitalized entrants fail to advance to the next level.

• The financial economy will evolve the way the individual financial consumers (savers and borrowers) need it to evolve, and not the way those in temporary “control” of their money want it to. Give the borrowers and savers what they really need to prudently manage their current finances and build a pathway to higher levels of financial success, and one can make money while delivering a social good. After all, it is Main Street investing and lending to Main Street. Wall Street just connects the two sides of Main Street.

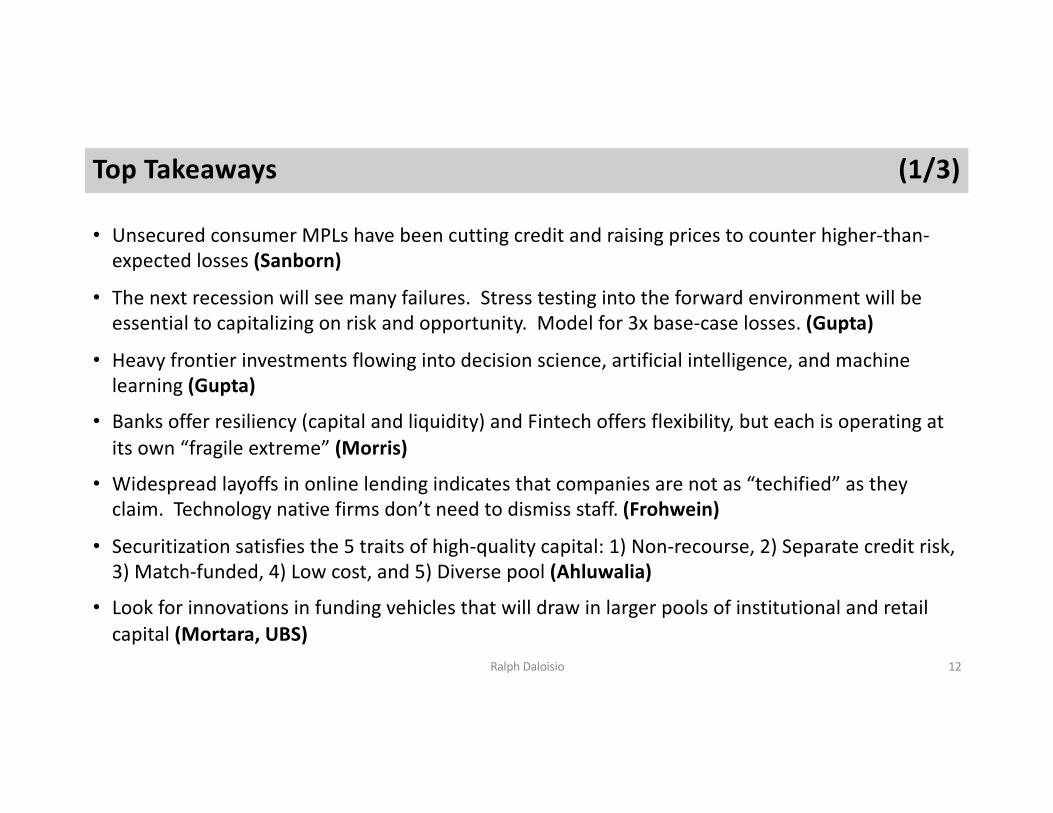

Top Takeaways (1/3)

• Unsecured consumer MPLs have been cutting credit and raising prices to counter higher-‐than-‐expected losses (Sanborn)

• The next recession will see many failures. Stress testing into the forward environment will be essential to capitalizing on risk and opportunity. Model for 3x base-‐case losses. (Gupta)

• Heavy frontier investments flowing into decision science, artificial intelligence, and machine learning (Gupta)

• Banks offer resiliency (capital and liquidity) and Fintech offers flexibility, but each is operating at its own “fragile extreme” (Morris)

• Widespread layoffs in online lending indicates that companies are not as “techified” as they claim. Technology native firms don’t need to dismiss staff. (Frohwein)

• Securitization satisfies the 5 traits of high-‐quality capital: 1) Non-‐recourse, 2) Separate credit risk, 3) Match-‐funded, 4) Low cost, and 5) Diverse pool (Ahluwalia)

• Look for innovations in funding vehicles that will draw in larger pools of institutional and retail capital (Mortara, UBS)

Ralph Daloisio 12

Top Takeaways (2/3)

• LoanDepot is the 2nd largest non-‐bank lender in the marketplace industry and it has less than 2% market share. Hence, we are still in the very early innings (bottom of 1st/top of 2nd) (Hsieh)

• Of the $12.6 trillion in consumer debt outstanding, 71% of it is mortgage related, making it the single largest addressable market in consumer finance. (Hsieh)

• The 5 keys to future success, in 2017: 1) Loan performance, 2) Data transparency, 3) Platform profitability, 4) Customer acquisition, and 5) Automation (Suber)

• The OCC has the clear legal authority to issue “Fintech charters.” The charter will not be supervisory-‐lite and will not be granted to applicants with predatory or abusive lending businesses or applicants seeking to combine banking and commerce activities. (Curry)

• We no longer live in “linear times.” We live in “logarithmic times.” Change is occurring in larger amounts over shorter time periods, and the effects are compounding. (Sculley)

• We are about to see a huge change in consumer credit. Banking services will be delivered to banking customers in fundamentally new ways. Many companies will participate. (Sculley)

Ralph Daloisio 13

Top Takeaways (3/3)

• The most interesting change is the potential for machine learning—White Box vs Black Box, where White Box = transparent, human readable. Non-‐linear symbolic regression (“NLSR”) is the best information technology for processing the incredible “exhaust” of consumer data being generated by banks– and banks use only 1% of their data exhaust today. (Sculley)

• 80% of Credit Karma’s 60 million users are active on mobile. Increasingly, consumer borrowers are accessing via mobile and not desktop. (Lin)

• Lenders can win market share by offering (1) approval certainty, (2) price transparency, and (3) simplicity. (Lin) [Most borrowers are not lawyers or bankers.]

• China has, [get this], over 2,448 P2P lenders, and this number is down from its peak in 2015 (Renton)

• MPLs targeting small businesses can do what banks can’t: lend to the 28 million businesses in the US which need a simpler way of borrowing <$500,000 (Reses)

• Online lending is expected to grow from $40 billion today to $1 trillion by 2020. (Burton)

• There will be more businesses folding than starting. If VCs stop funding unprofitable companies, they will have no alternatives. (Carroll)

Ralph Daloisio 14

Scott Sanborn, President & CEO, Lending Club

• 60% of Lending Club’s business is refinancing credit card debt with amortizing loans

• Customers report saving 25% over their credit card option

• Expansion into “Innovative Micro-‐Services” (e.g., identity verification, loan pricing)

• Can be offered from existing Fintech business models

• Some tech firms will carve market niches in one or more innovative micro-‐services

• 3 key marketing determinants when originating consumer loans

1. Will you give me a loan?

2. How much will it cost?

3. How hard are you going to make it for me?

Ralph Daloisio 15

Ash Gupta, President of Global Credit Risk and Information Management at American Express• Heavy investments are being made in decision sciences, machine learning, and artificial intelligence

• AmEx has 1,500 data scientists spread across the company

• Non-‐bank suppliers of funds (endowments, pensions, insurance companies, and SWFs) could enter in a big way to ally with Fintech’s market-‐share grab from banks

• Getting traditional investors into new asset classes being approached in new ways is a real challenge

• The Next Recession

• MPL’s should be modeling for 3x current credit loss in the next recession

• Lots of the post-‐crisis lenders will fail in the next recession

• Planning and organizing for this will be highly rewarding

• Stress testing into the forward environment is critical to positioning for risk and reward

Ralph Daloisio 16

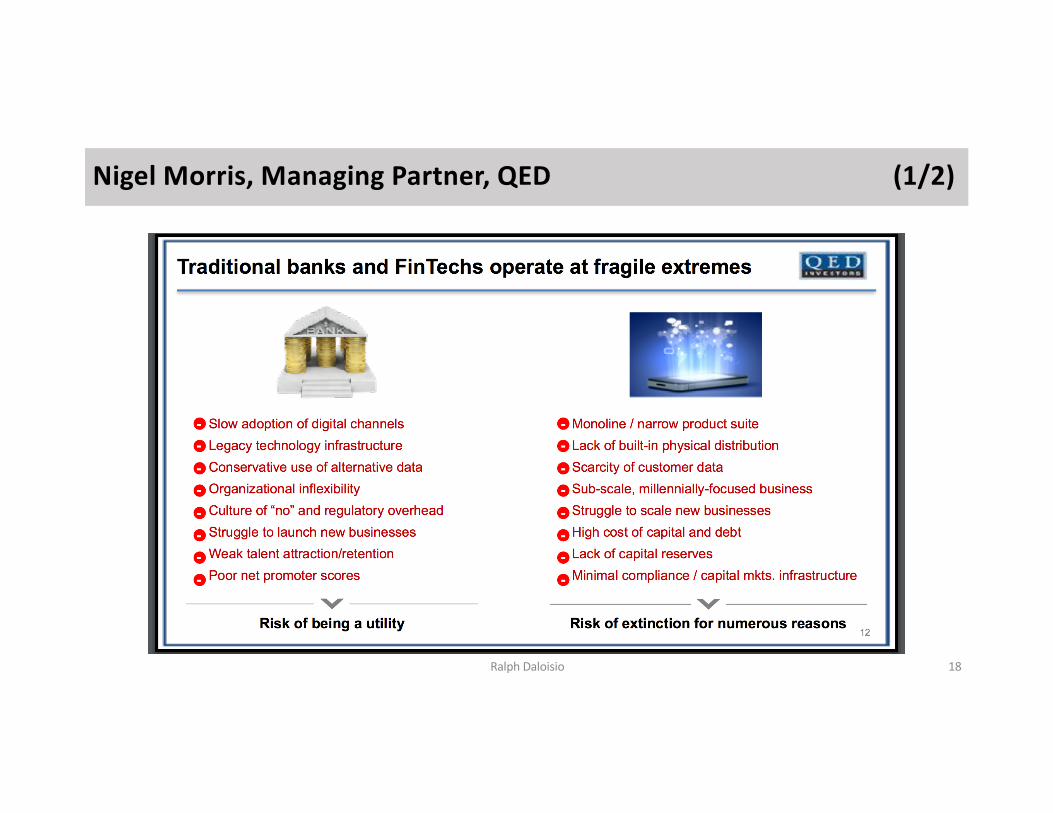

Nigel Morris, Managing Partner, QED

• Banks and Fintech are operating at unsustainable “fragile extremes”• Banks have capital and liquidity trapped within an inflexible business model• Fintech has flexibility that’s restrained by a lack of capital and liquidity• Each needs to move closer to the other

• Since the Great Recession, banks have not covered their post-‐crisis average cost of capital

• Striking the right balance between Resilience (Banks) and Flexibility (Fintech) is “devilishly difficult”

Ralph Daloisio 17

Nigel Morris, Managing Partner, QED (1/2)

Ralph Daloisio 18

Since the Great Recession of 2008, banks have not covered their post crisis cost of equity capital

Nigel Morris, Managing Partner, QED (2/2)

Ralph Daloisio 19

Rob Frohwein, CEO & Co-‐Founder, Kabbage (1/5)

• The question most Fintech Alt Lenders asked: Can we fill the void left by banks?

• The question most Fintech Alt Lenders should have asked: Why aren’t the banks filling the void left by banks?

• Asking the wrong question left them racing for growth in customers and capital

• Most online lenders started their business the day they made their first loan• 4 Expense Categories

• Acquisition and Utilization

• Bad Debt

• Capital

• Other Operating Expenses

• The Fintech Alt Lenders can’t generate a lower cost of capital than banks, but they can fundamentally change financial services if their technology can materially lower one of the other 3 expense categories

Ralph Daloisio 20

Rob Frohwein, CEO & Co-‐Founder, Kabbage (2/5)

• The biggest piece of technology offered by most Fintech Alt Lenders is the online application

• There is nothing special about the online application

• NextCard debuted the online application in 1999, over 17 years ago.

• Many online lenders had to layoff employees at the slightest sign of trouble

• Digitally native lenders would not have to cut staff

• Kabbage answered the right question by concluding that banks cannot profitably service small business customers

• Kabbage connects to its 100,000+ small business customers through APIs with daily data updates

• Kabbage forged bank partnerships with 3 leading Global Banks: ING, Santander, and Scotia Bank

Ralph Daloisio 21

Rob Frohwein, CEO & Co-‐Founder, Kabbage (3/5)

• Early on Kabbage required borrower consents to access their API data on an continual basis as an ongoing lending condition

• Banks need to identify a more cost effective way to serve individuals and small businesses

• A focus on leveraging technology for growth and funding will not create a sustainable partnership with banks

• Companies that understand how to reduce the costs of acquisition, bad debt, and operations will build long-‐lasting partnerships with banks

• There has been mass adoption of Kabbage’s data infrastructure globally by banks

• Kabbage will build more vertically directed products leveraging its existing data infrastructure to align each of marketing, business development, risk, payments & collections

• Partnership success requires one to solve issues banks have

Ralph Daloisio 22

Rob Frohwein, CEO & Co-‐Founder, Kabbage (4/5)

Ralph Daloisio 23

Rob Frohwein, CEO & Co-‐Founder, Kabbage (5/5)

Ralph Daloisio 24

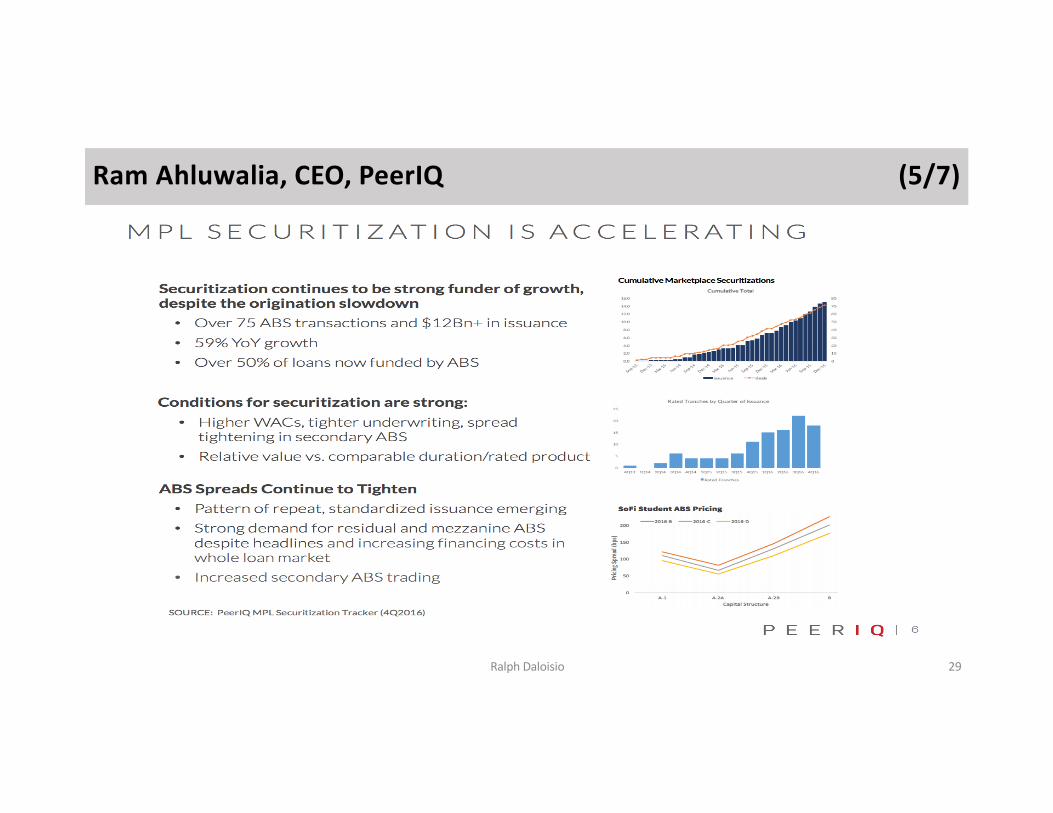

Ram Ahluwalia, CEO, PeerIQ (1/7)

• PeerIQ’s core competency is a data and analytics provider focused on MPLs

• A lack of data and performance history is making it difficult for ratings agencies to project expected losses (EL). This can be seen in the divergence in EL estimates from different raters (20% in a latest SoFi deal) and split ratings (IG/Non-‐IG). [I would add ratings shopping, which is still occurring.]

• Discrete differentiation across multiple platforms

• More retail friendly products

• Movement towards a 3rd party ecosystem for data verification, loss estimates, etc.

• Credit bureau data is highly predictive

• Acquisition channel is usefully predictive too

• Benchmarking is important

Ralph Daloisio 25

Ram Ahluwalia, CEO, PeerIQ (2/7)

Ralph Daloisio 26

Ram Ahluwalia, CEO, PeerIQ (3/7)

Ralph Daloisio 27

Ram Ahluwalia, CEO, PeerIQ (4/7)

Ralph Daloisio 28

Ram Ahluwalia, CEO, PeerIQ (5/7)

Ralph Daloisio 29

Ram Ahluwalia, CEO, PeerIQ (6/7)

Ralph Daloisio 30

Ram Ahluwalia, CEO, PeerIQ (7/7)

Ralph Daloisio 31

Investor Insights Panel: Every Originator Will Launch a Fund

• Every asset should have 3 ways of being funded (Glenn Goldman, CEO of Credibly)

• Cross River is prepared to keep skin in the game by retaining what is being originated for their lender partnerships. Now important for Cross River to create its own fund and would look to partner with a third-‐party fund manager. Big question: Asset origination vs asset management. Should the twain remain connected or better to separate? (Gilles Gade, Founder, CEO & Chairman, Cross River)

• Players don’t consider the cost of not having diversified and the need for permanent capital funding as insurance against the illiquid periods. West Coast less concerned about diversity and sustainability than East Coast. (Jeff Mortara, UBS)

• Big bid for yield from pension and sovereign, but they are looking for big ticket. Publicly traded pass through with retail participation will be a generic optimal structure to emerge in the coming years. (Jeff Mortara, UBS)

• Money360 utilizes a traditional Reg D Private Fund exempt from the ‘40 ACT. Designed to be as tax efficient as possible to appeal to as broad a swath of investors, and that allows leverage to be added to the capital structure to lower cost of capital. (Dan Vetter, COO, Money360)

Ralph Daloisio 32

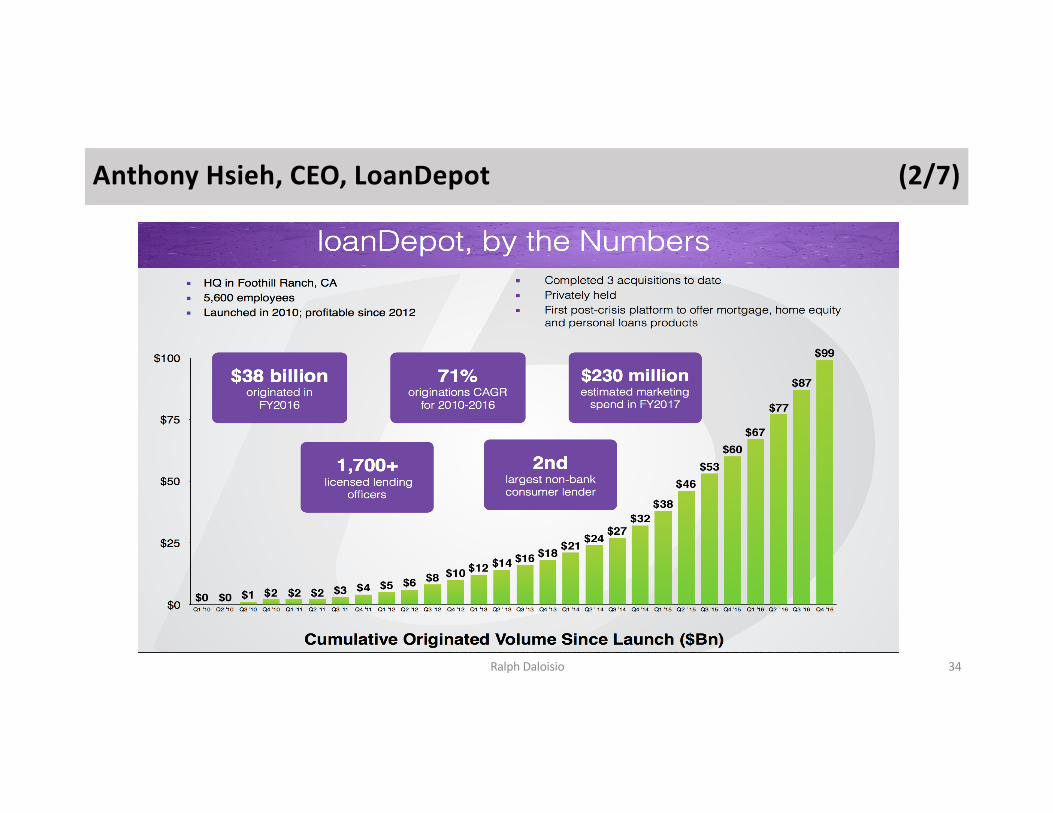

Anthony Hsieh, CEO, LoanDepot (1/7)

• The industry is still in its very early stages: the “bottom of the 1st” or “top of the 2nd” inning. LoanDepot is the 2nd largest non-‐bank lender in the marketplace industry and it has less than 2% market share.

• Since the 2008 peak of $12.7 trillion, consumer debt fell to a low of $11.3T in 2012. It has taken 8 years to get back to 2008 levels, standing at $12.6T in 2016.

• Mortgage debt as a % of total consumer debt has fallen from 79% in 2007 to 71% in 2016.

• When the market “pivots back” to residential real estate finance, those marketplace lenders that can service a multi-‐line business will be in a stronger position.

• LoanDepot operates a “state licensing campus” internally to manage their state licensing requirements and support their >1,000 LOs who collectively hold over 10,000 state licenses.

• Non-‐banks must be very smart about following the money supply, acknowledging where we are, and sourcing the capital necessary to fund the platforms.

Ralph Daloisio 33

Anthony Hsieh, CEO, LoanDepot (2/7)

Ralph Daloisio 34

Anthony Hsieh, CEO, LoanDepot (3/7)

Ralph Daloisio 35

Anthony Hsieh, CEO, LoanDepot (4/7)

Ralph Daloisio 36

Anthony Hsieh, CEO, LoanDepot (5/7)

Ralph Daloisio 37

Anthony Hsieh, CEO, LoanDepot (6/7)

Ralph Daloisio 38

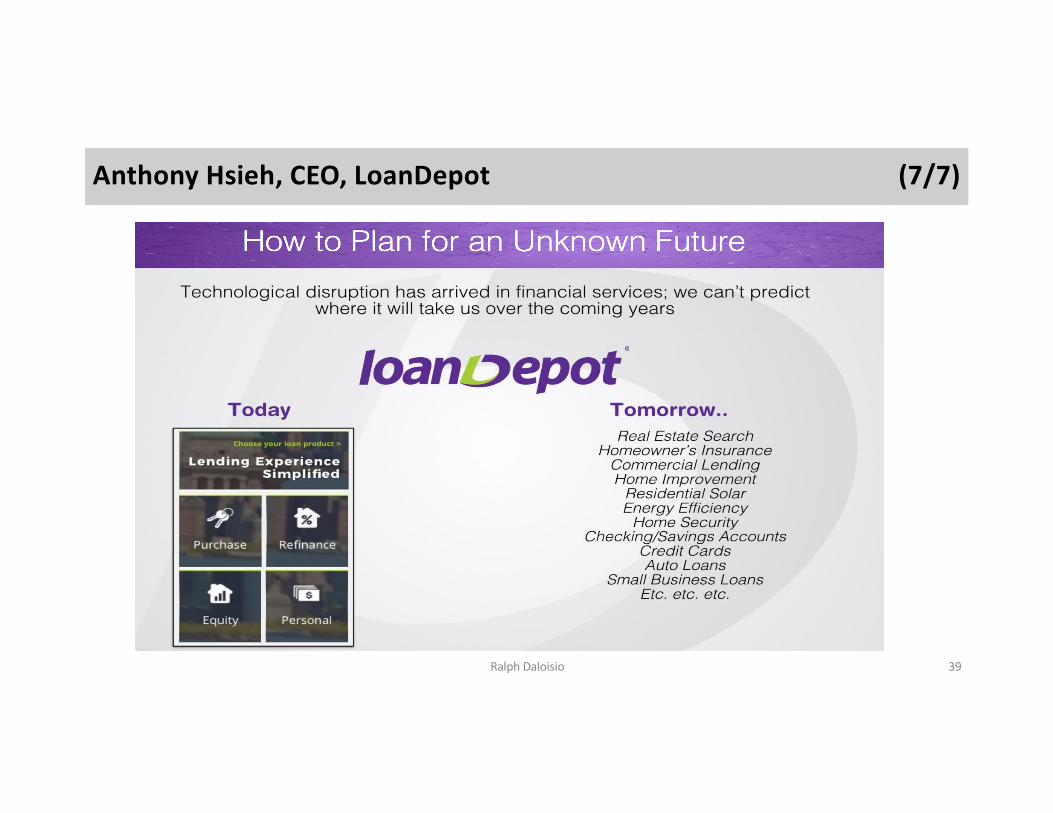

Anthony Hsieh, CEO, LoanDepot (7/7)

Ralph Daloisio 39

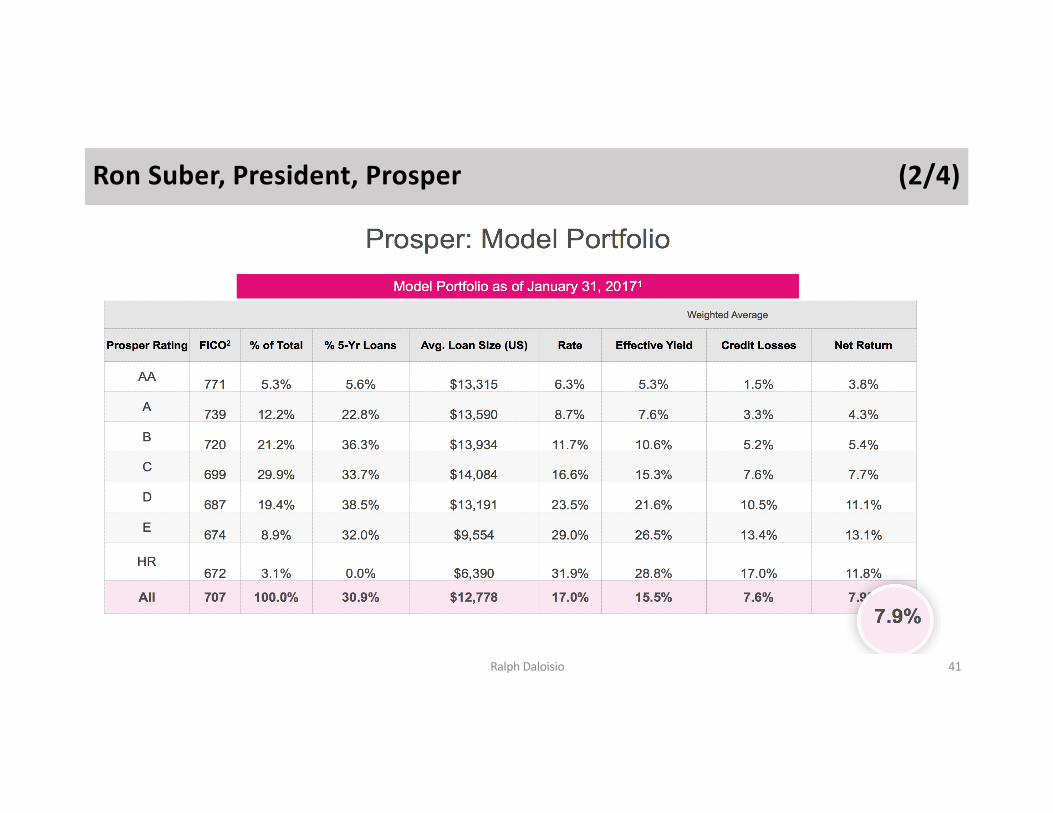

Ron Suber, President, Prosper (1/4)

Ralph Daloisio 40

Ron Suber, President, Prosper (2/4)

Ralph Daloisio 41

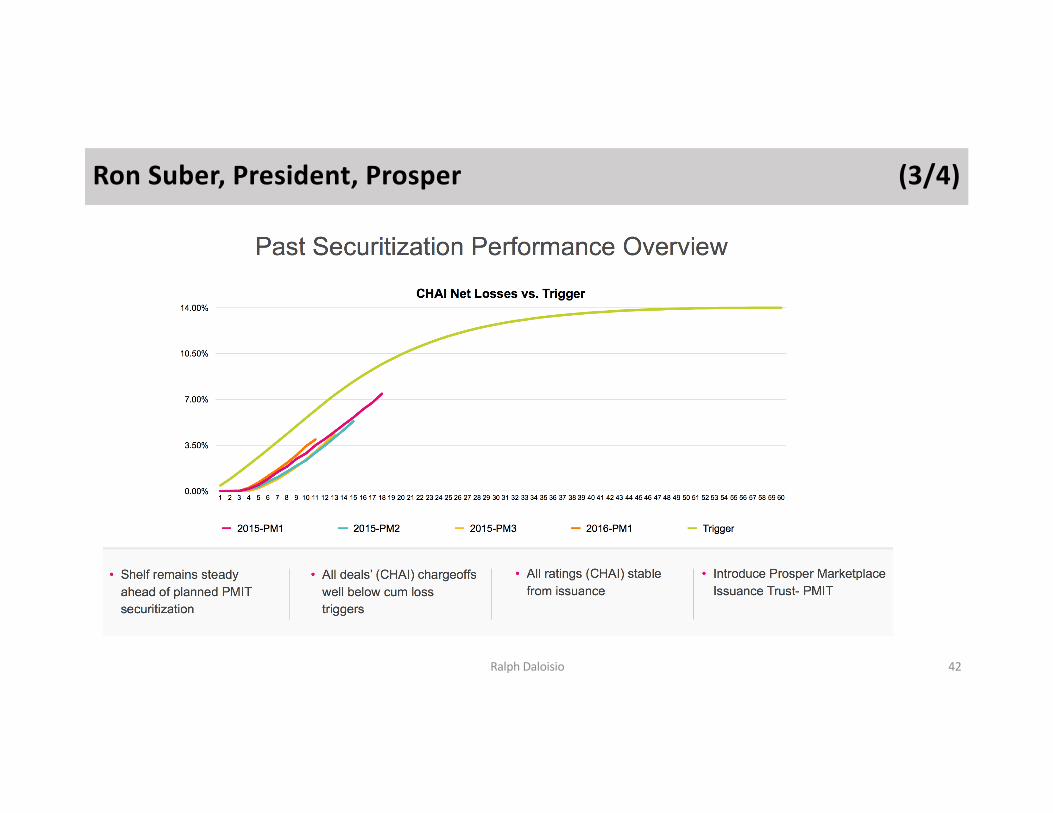

Ron Suber, President, Prosper (3/4)

Ralph Daloisio 42

Ron Suber, President, Prosper (4/4)

Ralph Daloisio 43

Thomas Curry, Comptroller of the Currency (1/4)

• The OCC supervises 1,400 national banks and federal savings associations that account for 2/3rds of the assets held by U.S. banks (ie, >$11 Trillion) and nearly 2/3rds of all credit card balances.

• He specifically notes the power of the Fintech industry to “expand financial inclusion” to bring “those who are unbanked and underbanked into the fold, and too many of those individuals are concentrated in low-‐ and moderate-‐income communities that are often the most vulnerable to financial difficulty and predatory practices.”

• The OCC’s initiatives are centered around the concept of ”responsible innovation,” defined to mean “innovation that meets the evolving needs of consumers, businesses, and communities in a manner consistent with sound risk management and is aligned with a company’s overall business strategy.” For Fintech’s that would pursue a special purpose national bank charter, this includes ”rigorous controls and governance to ensure [they] comply with applicable laws and regulations, provide fair access to [their] services, and treat [their] customers fairly.” Compliance and risk management should be built into the company’s DNA as early as possible in the evolution of their business.

• The OCC has and will continue to take measures to support and foster “responsible innovation.”Ralph Daloisio 44

Thomas Curry, Comptroller of the Currency (2/4)

OCC Milestones Towards the Special Purpose National Bank (“SPNB”) charter for Fintech Companies:

ü March 2016: Issues “Perspective on Responsible Innovation”

ü June 2016: Convenes a Forum on Innovation

ü October 2016: Issues Framework for Responsible Innovation

ü October 2016: Establishes the Office of Innovation

ü December 2016: Announces Charters for Fintech Companies

ü December 2016: Issues Final Rule Governing Receivership for Uninsured National Banks

ü March 2017: Issues Draft Licensing Manual for Fintech Charters

Ralph Daloisio 45

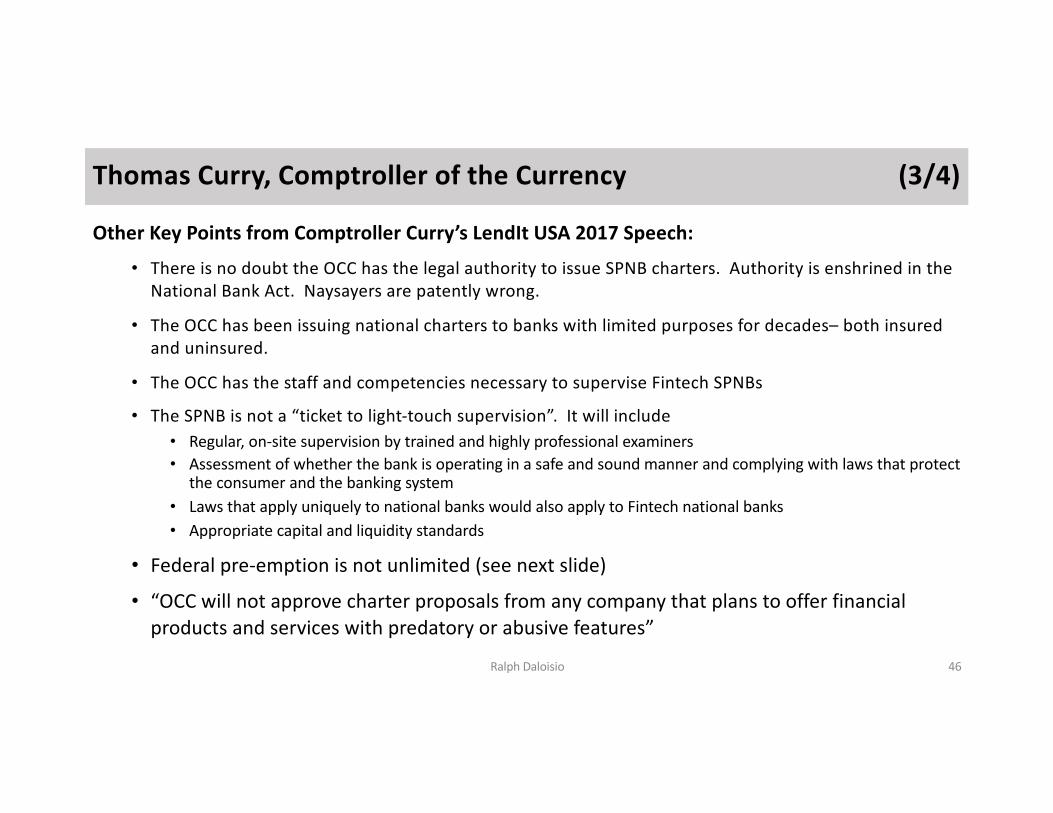

Thomas Curry, Comptroller of the Currency (3/4)

Other Key Points from Comptroller Curry’s LendIt USA 2017 Speech:

• There is no doubt the OCC has the legal authority to issue SPNB charters. Authority is enshrined in the National Bank Act. Naysayers are patently wrong.

• The OCC has been issuing national charters to banks with limited purposes for decades– both insured and uninsured.

• The OCC has the staff and competencies necessary to supervise Fintech SPNBs

• The SPNB is not a “ticket to light-‐touch supervision”. It will include• Regular, on-‐site supervision by trained and highly professional examiners• Assessment of whether the bank is operating in a safe and sound manner and complying with laws that protect

the consumer and the banking system• Laws that apply uniquely to national banks would also apply to Fintech national banks• Appropriate capital and liquidity standards

• Federal pre-‐emption is not unlimited (see next slide)

• “OCC will not approve charter proposals from any company that plans to offer financial products and services with predatory or abusive features”

Ralph Daloisio 46

Thomas Curry, Comptroller of the Currency (4/4)

• Federal pre-‐emption is not unlimited

• State laws will still apply in the following areas:

• Discrimination, Fair Lending, Debt Collection, Taxation, Zoning, Crime, and Torts

• Federal laws apply to national banks

• Federal Trade Commission Act, outlawing unfair or deceptive acts or practices (“UDAP”)

• OCC has taken the position that state UDAP laws apply to national banks

• State banks have the same power as national banks to export the usury laws in their home state (granted by Congress in 1980)

• OCC understands the importance of maintaining the longstanding separation of banking and commerce

• Proposals that would mix the two would not be approved

Ralph Daloisio 47

John Sculley, Vice Chairman, Lantern Credit

• We are living in “exponential time” where timeframes are rapidly shortening for change. We are no longer in “linear time.”

• We are about to see a huge change in consumer credit. Many companies will participate. The most interesting is the potential for machine learning—White Box vs Black Box, where White Box = transparent, human readable.

• Non-‐linear symbolic regression (“NLSR”)— acquired this technology from a commodities trading firm.

• Banks are generating an incredible “exhaust” of consumer data and using only 1% of it. Lantern can process this massive amounts of data through a NLSR machine-‐learning platform.

• Lantern is a White Label B2B2C platform.

• He’s amazed by how much talent has entered the industry, and globally. • Bill Gates: We will have to “tax the robots” because tech will replace human labor.

• Lantern will be launching in the US by middle of this year with their White Box solution to consumer credit, with partners he cannot disclose.

• There are fundamentally new ways in which banking services will be delivered to customers.

Ralph Daloisio 48

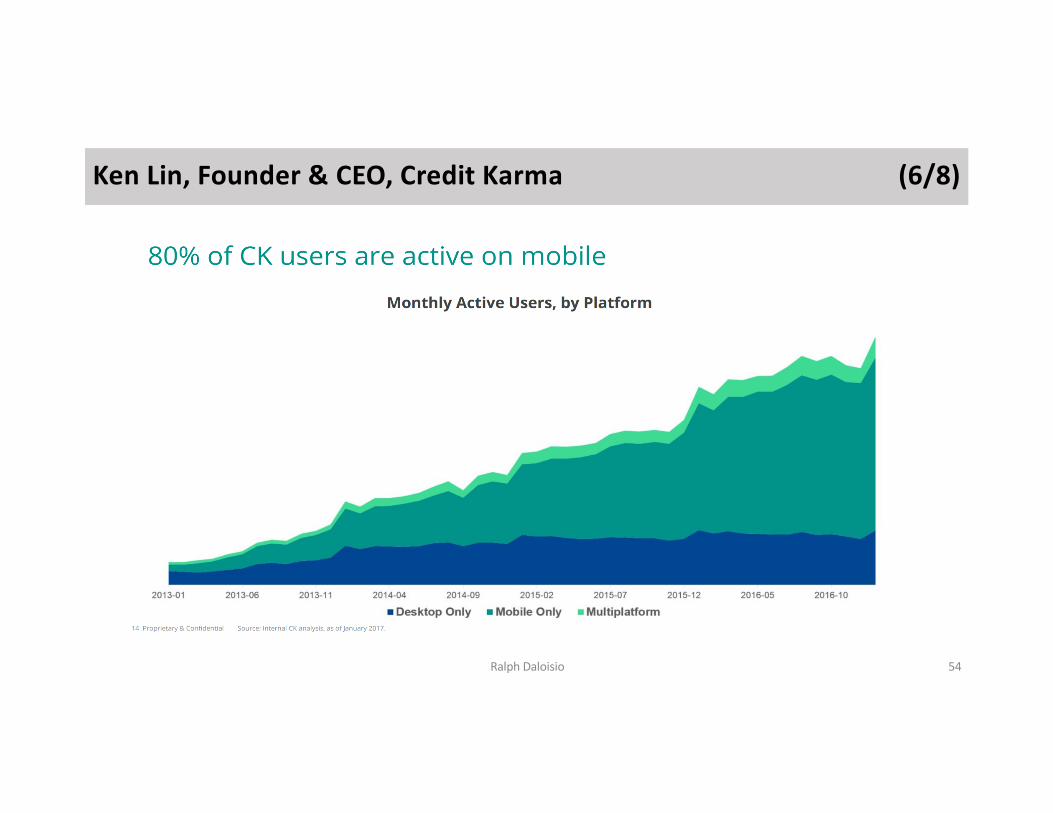

Ken Lin, Founder & CEO, Credit Karma (1/8)

• With 60 million members, Credit Karma sees almost $4T of consumer credit (~25%)

• Credit performance has been deteriorating among online lenders

• They have raised APRs and tightened underwriting in response, causing them to lose market share

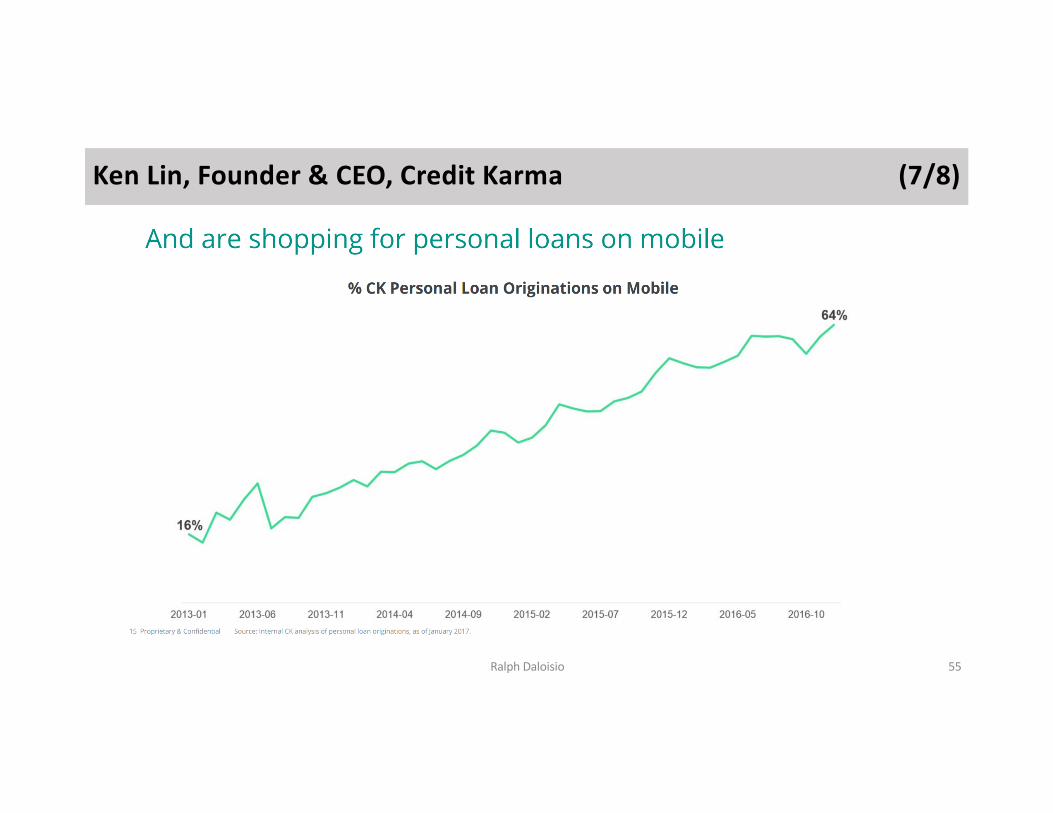

• Increasingly, consumer borrowers are accessing via mobile and not desktop

• There is a need to utilize alternative data sets to reduce reliance on credit bureaus

• User data can be captured to drive insights into behavior for predictive purposes

• Three consumer “pain points” to solve for the consumer in order to win market share

1. Certainty. Give them certainty of approval before they apply.

2. Transparency. They need to know how much it will cost.

3. Simplicity. Make it easy for them to engage and understand. [Most are not lawyers or bankers.]

• Use UserX to drive a differentiated experience and drive down acquisition costs

Ralph Daloisio 49

Ken Lin, Founder & CEO, Credit Karma (2/8)

Ralph Daloisio 50

Ken Lin, Founder & CEO, Credit Karma (3/8)

Ralph Daloisio 51

Ken Lin, Founder & CEO, Credit Karma (4/8)

Ralph Daloisio 52

Ken Lin, Founder & CEO, Credit Karma (5/8)

Ralph Daloisio 53

Ken Lin, Founder & CEO, Credit Karma (6/8)

Ralph Daloisio 54

Ken Lin, Founder & CEO, Credit Karma (7/8)

Ralph Daloisio 55

Ken Lin, Founder & CEO, Credit Karma (8/8)

[Is Unsecured Personal Credit Efficiently Priced, or are Bureau Scores Poor Predictors of Expected Loss?]

Ralph Daloisio 56

David Girouard, CEO, Upstart (1/2)

• MPLs are not meeting the definition of a “marketplace” (dynamic pricing, superior liquidity, near zero acquisition costs, and network effects)

• True tech disruption is “qualified borrowers have easy access to credit at rates that reflect risk.” We cannot be further from this today. We are leaving out at least half the people who should have access to credit and those with access to it are paying too much for it.

• In a decade, every credit decision will be made by AI/ML (more data, advanced math, real-‐time continuous learning). More data will generally prove more people credit worthy than not.

• Gradient smoothing and gradient boosting are supplanting liner regression. These technologies are being used in Alexa and Autonomous driving. Discrete version releases are not real-‐time continuous learning.

• R2 for FICO is 41% on their 50,000 loans (each red dot represents 4,000 loans-‐-‐ shown on next slide). Upstart had 54% R2 in their May 2014 release, which improved to 86% in Jan 2017. Upstart score now more than twice the R2 of FICO.

Ralph Daloisio 57

David Girouard, CEO, Upstart (2/2)

Ralph Daloisio 58

Rabobank, Snehal Fulzele and Marcel Gerritsen (1/3)

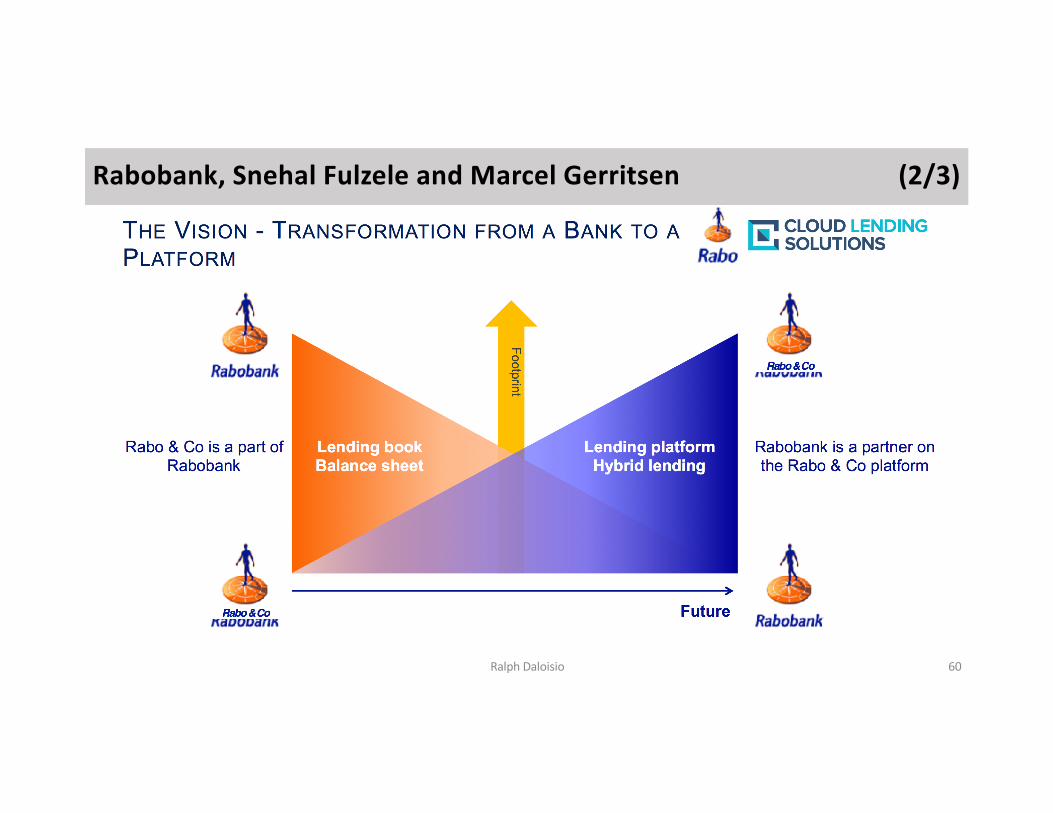

• Rabobank is transforming itself from a bank to a hybrid platform lender, where it will match fund alongside a variety of co-‐investors with varied investment parameters.

• Rabobank will retain 51% of the loan and “syndicate/distribute” 49%.

• Rabobank is a good candidate for this transformation

• Founded over 100 years ago as a cooperative of wealthy farmers to lend money to the poorer farmers;

• Currently bank 2 of every 3 SMEs operating in the Netherlands.

Ralph Daloisio 59

Rabobank, Snehal Fulzele and Marcel Gerritsen (2/3)

Ralph Daloisio 60

Rabobank, Snehal Fulzele and Marcel Gerritsen (3/3)

Ralph Daloisio 61

Richard Cordray, Director, CFPB (1/5)

• As innovations drive new services for consumers and transform how they conduct their finances, the CFPB wants to put consumers first and provide them with more tools to take control of their financial lives

• The CFPB is the single federal agency whose sole mission is to protect consumers in the financial marketplace, which includes monitoring rapid changes in new technologies affecting:

• Transactions

• Lending

• Underwriting

• Money management

Ralph Daloisio 62

Richard Cordray, Director, CFPB (2/5)

• Two Overarching Principles

1. A level playing field for all providers of consumer financial products and services. All market participants– whether large banks or small Fintech startups– must be held to the same standards of compliance with the law.

2. All providers should make sure that consumer protections are built into emerging products and services right from the start. They must be essential elements of the business model.

• Three broad areas of focus

1. Project Catalyst

2. Consumer control over personal financial data

3. Benefits and risks of using unconventional sources of data to underwrite loans

• The information consumers need to make decisions about their economic opportunities must be accessible, accurate, and reliable.

Ralph Daloisio 63

Richard Cordray, Director, CFPB (3/5)

• Project Catalyst• “Office Hours” program where the CFPB engages with startups, nonprofits, banks, and other financial

companies.• What does and does not work for consumers• Potential challenges facing entrepreneurs and investors

• Two examples of research pilot programs• Pilot program for consumer savings plan• Early-‐intervention credit counseling pilot

• Trial Disclosure Waiver Policy• Design and testing of alternative consumer disclosures via new technologies and innovative approaches• Goal is greater transparency, better consumer understanding, and/or reduced costs

• No-‐Action Letter Policy• Intended to promote novel products falling outside existing regulatory structure• States that the CFPB does not intend to recommend any supervisory or enforcement action based on the

covered innovations for a defined period.

Ralph Daloisio 64

Richard Cordray, Director, CFPB (4/5)

• Consumer Financial Data

• The information being recorded on consumers from their many different financial accounts (e.g., checking, savings, investment, mortgage, credit card, auto loan, student loan, etc.) can be a valuable asset.

• Such information matters as much or more to their financial situations than the dollars they actually have in their accounts at any given time.

• Request for Information issued in November 2016 inquiring about the challenges consumers face in accessing, using, and securely sharing their financial records.

• Concerned about reports that some institutions may be limiting or restricting access unduly.

Ralph Daloisio 65

Richard Cordray, Director, CFPB (5/5)

• Alternative Data• CFPB estimates that 26 million Americans are “credit invisible” (no credit history)• CFPB estimates that another 19 million Americans have credit histories that are too limited or have

been inactive for too long to generate a reliable credit score• So, 45 million Americans are credit-‐removed. For them, in comparison to the credit-‐connected (~190

million), financing their lives is riskier, takes longer, costs more, and does not help their financial futures as much.

• Adding alternative data may make it possible to open up more affordable and accessible forms of credit for millions of additional consumers.

• February 2017 Request for Information• Alternative data available today, and the advantages and disadvantages in using it• Alternative data and technologies of the future• Main topics of inquiry:

1. Can alternative data help lenders better assess creditworthiness and open access to the credit-‐removed?2. Will this lead to more complex lending decisions for consumers and industry?3. How will the costs and services in making credit decisions be impacted?4. Is alternative data error prone, and how difficult will it be for consumers to identify and correct the errors?5. How might the use of alternative data violate fair lending laws or create other risks for vulnerable consumers?

Ralph Daloisio 66

Peter Renton, Chairman & Co-‐Founder, LendIt (1/5)

• Profitability is now the focus

• Banks are going to become ever more important to the development of this industry

• There were 262 entries for LendIt’s PitchIt. NovaCredit won.

• US Platforms thinking of raising $ should be in China. China’s influence is growing.

• Biggest US stories in 2016

• Lending Club challenges

• OCC Fintech Charter

• Goldman Sachs launches Marcus

• The first lending platform failures

• Securitization market grows

• Industry associations get some traction

Ralph Daloisio 67

Peter Renton, Chairman & Co-‐Founder, LendIt (2/5)

Ralph Daloisio 68

Peter Renton, Chairman & Co-‐Founder, LendIt (3/5)

Ralph Daloisio 69

Peter Renton, Chairman & Co-‐Founder, LendIt (4/5)

Ralph Daloisio 70

Peter Renton, Chairman & Co-‐Founder, LendIt (5/5)

Ralph Daloisio 71

Jackie Reses, Lead, Square Capital• Vast majority of the very small businesses in the US want loans <$500,000 while lenders’ minimum is $1,000,000.

• Documentation is too complex and demanding for these types of borrowers (28 million in the USA).

• With 2.1 million merchants on the Square dashboard, offers are displayed and within 3 clicks and within 24 hours the small business can get the capital it needs over the time it needs it.

• Repayment can occur through daily card sales which matches their cash inflow to their debt service burden.

• $120B estimated in pent up demand for small business loans vs maybe $15 billion outstanding in all of US Fintech.

• Small businesses really need outsourced services for credit and management.

• Square earns the trust of their merchants from the very beginning, since they commence the relationship with merchant card services. Shows simple and transparent figures for borrowings that foster trust.

• In 2016 switched MCA product to a loan. Sellers wanted to prepay their MCA but could not due to the “product design.”

• Feels the entire industry has only just started. Loans have been around for hundreds of years and capital fungibility is high. Speed, Transparency, and Flexibility have only recently become features of the commoditized product of lending.

• Rates to rise due to GDP, Employment, Inflation… but Square has not had to raise rates and expects overtime its cost of capital will decline as it scales. Small business is less yield sensitive in the economy. [No wonder. APRs are huge.]

Ralph Daloisio 72

NovaCredit, Winner of PitchIt 2017• 1st Place in a field of 262 entries.

• Took 1st in both the Company Demo Category AND the Audience Demo Category

• Arose to address a market need: individual credit profiles did not follow the individuals as they relocated around the globe.

• Local lenders could not or did not want to lend money to their customer in a foreign jurisdiction and currency, while local lenders had no access to credit bureau information for use in making local lending decisions.

• “Globetrotters” were “credit paralyzed”.

• NovaCredit converts localized, immobile systems of credit-‐grading individuals into a global, mobile system.

• NovaCredit is building a cross border credit bureau.

• NovaCredit’s Passport is their answer to assembling data from multiple credit bureaus around the world.

• Interacting with 200 bureaus around the world now.

• NovaCredit has emerged as the “Switzerland” of credit bureaus.

• Fully reciprocal system allows positive and negative information to be reported cross border.

Ralph Daloisio 73

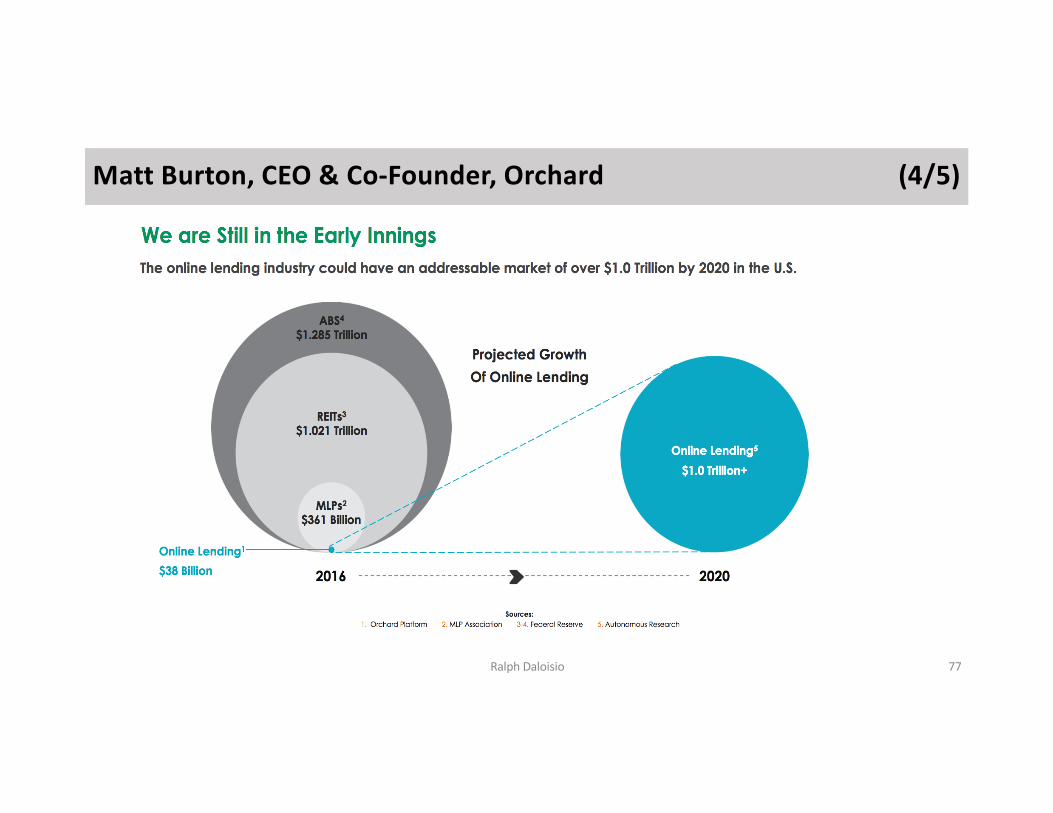

Matt Burton, CEO & Co-‐Founder, Orchard (1/5)

• Reading headlines from last year gave a misleading indication that the industry was dying.

• Companies are ready to scale now. They feel they have the underwriting down, the people in place, and need to scale to profitability.

• 2014 was the emergence of the asset class. 2015 was the hype. 2016 was the bump in the road. • Believes retail, whole loan sales, bank participations, and securitization will grow, especially the latter.

• Build, buy, or partner. Partner is the cheapest and lowest risk approach.

• Still just the beginning of a real shift because consumer attitudes and behaviors are changing.

• The industry needs more bank investors, SWFs, pension, and insurance cos. Credit product by user-‐type (dentist, restaurant, etc) is driving customization.

• Cumulative platform loan originations through 2016 > $40 billion (~$8 billion small business and ~$32 billion consumer)

• Cumulative securitizations of marketplace loans through 2016 > $11 billion

• There are now > 500 participants in the U.S. marketplace lending industry

• New assets classes are creating new investment opportunities

• Online lending is expected to grow from $40 billion today to $1 trillion by 2020. [Buckle up?!]

Ralph Daloisio 74

Matt Burton, CEO & Co-‐Founder, Orchard (2/5)

Ralph Daloisio 75

Matt Burton, CEO & Co-‐Founder, Orchard (3/5)

Ralph Daloisio 76

Matt Burton, CEO & Co-‐Founder, Orchard (4/5)

Ralph Daloisio 77

Matt Burton, CEO & Co-‐Founder, Orchard (5/5)

Ralph Daloisio 78

Multiple Participants, Where is Alternative Financing Heading? (1/4)David Klein, CEO, CommonBond: • Very excited about their “401(k)”-‐like product that allows employers to make payments on student loans• 2 to 4 securitizations a year at AA ratings• 50/50 split between securitization and whole loan sales• Structuring forward flow agreements with banks willing to accept lower returns than LP investors. Banks

will buy 4% to 7% yielding assets. • 3 Cs.

• Capital. What are the long-‐term sustainable sources of capital outside of banks? • Credit. The industry has not gone through a credit cycle. How will Alt Credit perform relative to traditional credit? • Customer. How to keep customer acquisition costs low over time. This answer gets into brand. How to move from

a silo to a re-‐bundling that keeps customer acquisition costs down. [Strategy will be customer retention, and expanded product offerings as the customer’s financial life broadens and deepens.]

• Buckets of risk: Credit, Market, Liquidity, Political, Regulatory, Operational. Can control operational risk well. Capital and liquidity risk management limited by available risk mitigants and their costs. Common Bond is looking forward to prove out their sustainability during a downturn, as this proof would drive down their capital costs because it will cause big players with marginal investment in them to invest larger sums.

• Goals are to sure up the capital base, keep credit incredibly strong, and lower customer acquisition costs.Ralph Daloisio 79

Brendan Carroll, Senior Partner & Co-‐Founder, Victory Park Capital• 37 deals since inception. $4B invested in debt and equity.• Equity investor in Common Bond. • Industry has evolved during a benign credit period. • Whole loan sales are uncommitted and buyers can walk. • Contractual balance sheet facility obliges lender to lend. • Their investors are institutional and require higher returns than being generated by the originated assets. • Individual states control consumer rate laws, not the Federal government. If CFPB is defanged, state laws may increase to

fill the gap. • Large corporates with large installed customer base reluctant to lend to them because of regulatory uncertainty and

strategy shift. • There will be more businesses folding than starting. If VCs stop funding unprofitable companies, they will have no

alternatives. • Half the country as defined by a FICO score will not get a loan from a bank. LendUP and others like them have better

options than PAYDAY loans. No question that there is demand for the product but lack of regulatory clarity is chilling that market. [Are loan options “predatory” or necessary and constructive? Where to draw the line?]

• 30% of their volume is outside the US. Looks for businesses with the right governance, platform, and board. Even if achieved, the currency risk is great for VPC to have full confidence around this. Looking for ways to eliminate that risk.

• Lower our own cost of capital to get our businesses to grow. Will continue to look outside the US.

Ralph Daloisio 80

Multiple Participants, Where is Alternative Financing Heading? (2/4)

Gilles Gade, Founder, CEO & Chairman, Cross River Bank• 18 Platform engagements. • In the business of risk management, not risk elimination.

• Buy a bank, take a limited OCC charter, or partner with a bank to solve challenges. “Bank in a Box.”

• Industry missing regulatory clarity. Examiners have their own interpretations as different examiners can see the same items but reach different conclusions.

• No agreement among regulators on how to best address the unbanked and underbanked. Same fractured dialogue around financial inclusion.

• Payments a big theme. The ability to make cross-‐border payments quickly and efficiently is not available. Western Union and others overcharging for this service. Further improvements in payments on the horizon over the next three years. The regulatory framework (AML) on payments is a lot clearer than it is on consumer lending.

• Refuse the status quo. We are serving the disruptors, so we need to be a disruptor ourselves.

Ralph Daloisio 81

Multiple Participants, Where is Alternative Financing Heading? (3/4)

Raul Vasquez, CEO, Oportun• 10 years lending $3 billion to thin file borrowers.

• Big risk is if consumers get hurt by alternative lending.

• Expects consolidation in the industry as companies struggle to deliver sustainable business models. What will be their unique value proposition instead of feeding at the same trough?

• Entering a time when there will be higher degrees of income and expense volatility in the employment world (eg, chatbots, autonomy, etc.)

• Recession will be a big challenge, especially with the country divided as it is.

• Billions of people underserved globally. Talla, Branch, and other companies like those are exciting to them.

• 232 physical locations across 6 states, which is ironic, but their customers are comfortable in cash. “We were profitable first, scalable first, and now we are moving into mobile.”

Ralph Daloisio 82

Multiple Participants, Where is Alternative Financing Heading? (4/4)

Ralph Daloisio 83

THE END