Embed Size (px)

Citation preview

International Monetary Regimes

MBF 3rd Batch (Group 8 Member List)Roll No – 6Ma Chit Chit NaingRoll No – 8Ma Chue Wai PhyoRoll No – 12 Mg Hein Thu AungRoll No – 13 Ma Hla Hla KhinRoll No – 31 Ma Khin Thit YeeRoll No – 37 Mg Kyaw San NaingRoll No – 76 Ma Sandar LinnRoll No – 80 Ma Shin Phone waiRoll No – 89 Ma Su Win MyatRoll No – 109 Ma Wai Mar Soe

International Monetary Regimes1. Introduction

2. What Does a Monetary Regime Need to Do?

3. The Gold Standard, 1880-1913:Panacea or Rose-Colored Glasses?

4. The Interwar Years, 1919-1939:Search for an International Monetary System

5. Bretton Woods, 1945-1971:A Negotiated International Monetary System

6. Post-Bretton Woods,1973-:Another Search for an International Monetary System

7. The Fixed-Versus-Flexible Debate

8. Money in the European Union From EMS To EMU

International Monetary Regimes

1. IntroductionThe goal of this Chapter:

1) Choice of exchange rate regime.

2) Outline some of the available alternatives.

3) Evaluate the strengths and weaknesses of alternate regimes.

2. What Does a Monetary Regime Need to Do? Different countries choose different arrangement decision

involves

trade-offs.

Facilitating international trade and investment.

Support International borrowing and lending.

Promote balance-of-payment adjustment to prevent the

disruptions and crises BOP imbalances.

3. The Gold Standard,1880-1913:Panacea or Rose-Colored Glasses?

3.1 What Is a Gold Standard? Gold functioned as money - scare, durable, transportable, easily

measurable and mintable into uniform coins. As economies grew the use of currency or paper money as a

substitute for gold. Currency was convertible. Government defined the value of its currency in terms of gold- eg –

U.S defined dollar value of an ounce of gold as $ 20.67 and Britain defined the pound price value of an ounce of gold as £ 4.24.

3.2 How Is a Gold Standard Supposed to Work? At the worldwide level, the money stock can’t grow faster than the

total world stock of gold. At the national level, each country’s money stock can’t grow faster

than that central bank’s stock of gold. Specie-flow-mechanism, international flows of gold (money) correct

BOP disequilibria, E.g.U.S has a balance-of-payments deficit with Britain under a gold standard. The value of goods and services the U.S imports from Britain exceeds that of U.S exports to Britain. To cover the difference and settle its account, the U.S must ship gold to Britain. This movement of gold reduces the U.S money stock and increases Britain.

3.3 How did the Gold Standard Really Work? A goal standard links the growth of the domestic money stock.

Faster growth in gold than in output would put upward pressure on the

price of goods relative to gold as countries accumulated gold reserve.

Slower growth in gold than in output would put downward pressure on

the price of goods relative to gold and create a shortage of reserves for

the growing economies.

4. The Interwar Years, 1919-1939:Search for an International Monetary System

World War I disrupted all aspects of the world economy, including the gold

standard.

Monetary policy makers printed money to cover the fiscal expenditures except U.S.

Demands of financing the war and reconstruction had produced high rates

of inflation in most economies.

Handful of countries reestablished a partial gold standard in 1925.

4. The Interwar Years, 1919-1939:Search for an International Monetary System

British government’s determination to return the pound to gold convertibility at its prewar rate.

Germany_saddled with a devastated economy and war reparations that it attempted to pay by printing massive quantities of money_suffered hyperinflation.

Beginning in 1931, the brief return to a gold standard collapsed in the midst of Great Depression.

After Great Depression did macroeconomic stability and internal balance become central goals of government policy.

One result of the interwar and Depression experiences to build stable and open international trade and monetary systems.

5. Bretton Woods, 1945-1971:A Negotiated International Monetary System

In 1940s, policy maker viewed flexible exchange rates as viable basis for an international monetary regime

- Three major changes

New regime represented a gold-exchange standard rather than a gold standard.

New system was an adjustable-peg exchange rate system rather than

affixed-rate system.

Bretton woods system, represented the outcomes of international bargaining.

5.1 How Was Bretton Woods Supposed to Work?Bretton Woods agreement contained three important element to

incorporate this flexibility.

1. An adjustable-peg exchange rate system

2. IMF lending facilities and

3. Permission for countries to institute or continue to use exchange controls

on some types of international transactions

The Adjustable Peg Negotiators at Bretton Woods recognized the need for periodic

devaluations and revaluations to correct chronic balance-of-payments problems.

Open the possibility of occasional currency realignments.

Allowed countries to devalue or revalue their currencies under specified conditions.

A system of fixed exchange rates that embodies rules for periodic adjustment of rates as economic conditions change is called an adjustment of rates as economic conditions change is called an adjustable-peg system.

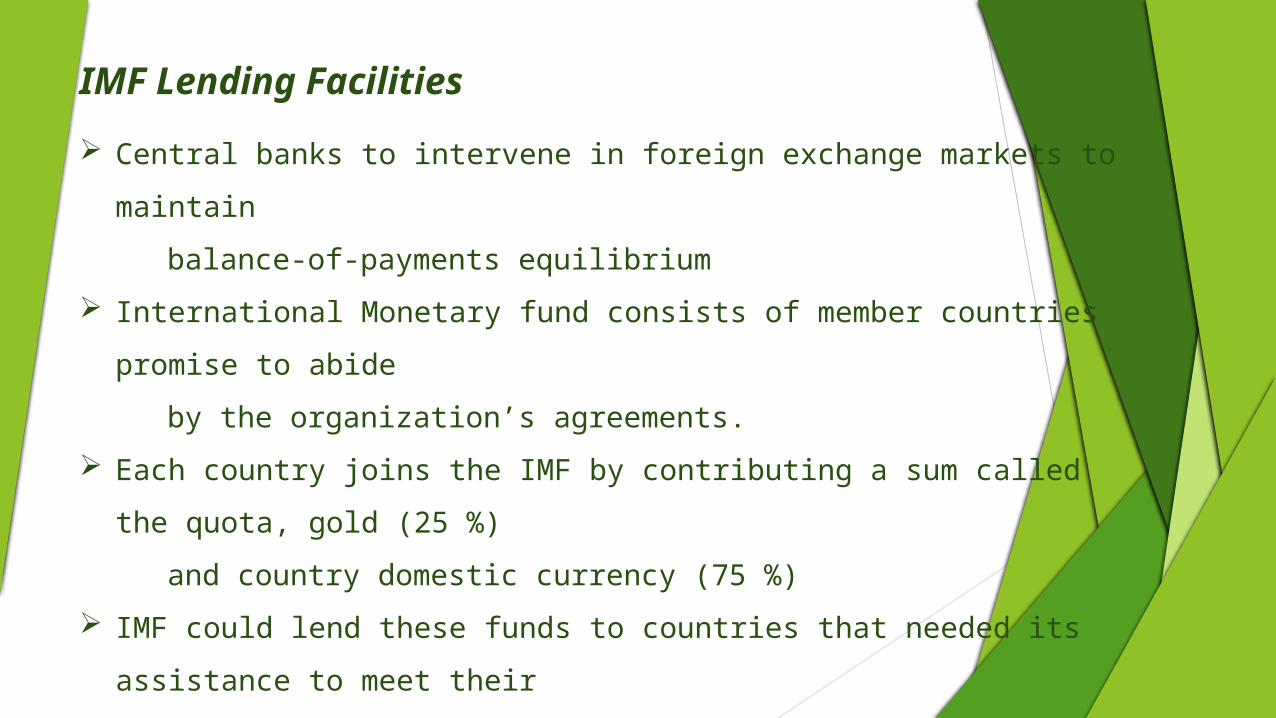

IMF Lending Facilities Central banks to intervene in foreign exchange markets to maintain balance-of-payments equilibrium International Monetary fund consists of member countries promise to

abide by the organization’s agreements. Each country joins the IMF by contributing a sum called the quota,

gold (25 %) and country domestic currency (75 %) IMF could lend these funds to countries that needed its assistance to

meet their Bretton Woods obligations. Countries could use their quotas to buy specific currencies they

needed for foreign exchange market intervention.

Exchange and capital Controls At the end of World War II, most national countries weren’t

convertible. Bretton Woods agreement urged member countries to restore

currency convertibility quickly. Agreement limited the call for convertibility to current-account and

avoided requiring convertibility of capital account. Currencies become convertible for capital account transactions

private capital flows increased. This development enhanced the opportunity for countries to reap

gains from intertemporal trade. Some countries, private capital flow could offset current-account

deficits or surpluses and reduce the need for foreign exchange intervention.

5.2 How Did Bretton Woods Really work? After World War II, reconstruction meant that European and Japanese

economies ran large current-account deficits.

Those deficits required central banks to intervene on a large scale to maintain the countries’ fixed exchange.

U.S had to make available enough dollars to provide adequate world liquidity

or reserves.

In the mid-1960s, U.S pursued more expansionary monetary policy and

its ran balance-of-payment deficits.

5.2 How Did Bretton Woods Really work? Expansionary U.S monetary policy meant that foreign central

banks had to

buy large quantities of dollars from FX market.

U.S responsibilities under the system sometimes conflicted central banks faced conflicts between their international responsibilities and macroeconomic policies.

Conflicts between country’s international and domestic economic obligations could quickly trigger a capital outflow and a balance-of-payment crisis.

6. Post-Bretton Woods,1973-:Another Search for an International Monetary System

Individual countries unilaterally choose their own exchange rate arrangements.

Today’s system as a managed float, the arrangement in use by the major

industrial economies

Managed float refers to a system in which the forces of supply and demand

in foreign exchange markets.

But central banks intervene when they perceive markets as “disorderly”.

The period since 1973, the major currencies have been allowed to float.

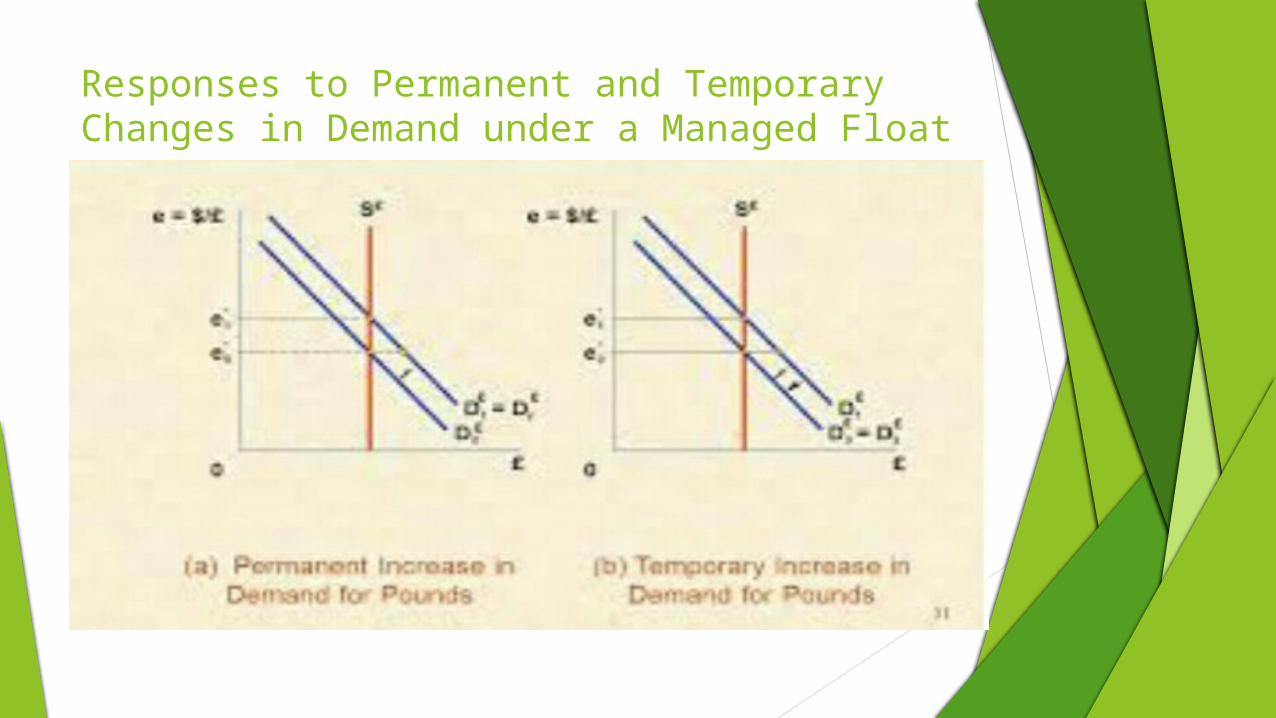

6.1 How Is Managed Float Supposed to Work? By combining market-determined exchange rates with some foreign exchange market intervention To capture the more desirable aspects of both fixed and flexible exchange rates To avoid short-term exchange rate fluctuations Central Bank avoid long-term intervention _ to determine long run movements in exchange rate In panel (a)

- allow the exchange rate to float in response to the forces of supply and demand

- Moving to a higher dollar price of pounds at e*1 - By selling pound denominated assets from foreign exchange reserves to hold

the exchange rate at e*0

Panel (b) Temporary increase in the demand of pound. Under a floating exchange regime, the dollar price of pounds would move upward from e*0 to e*1 and then back to e*0. Under an ideal money float

the appropriate response to the temporary disturbance with be temporary intervention to hold the exchange rate at its underlying equilibrium level, e*0

A managed float aims to limit exchange rate uncertainly by using intervention in foreign exchange markets to smooth short-run fluctuations in exchange rates At the same time, manage float allows market forces to determine long-run exchange rate. Breaking the link between the BOP and the money stock and preventing chronic payments dis-equilibria.Achieving two virtues of a flexible exchange rate.

How Is Managed Float Supposed to Work?

Responses to Permanent and Temporary Changes in Demand under a Managed Float

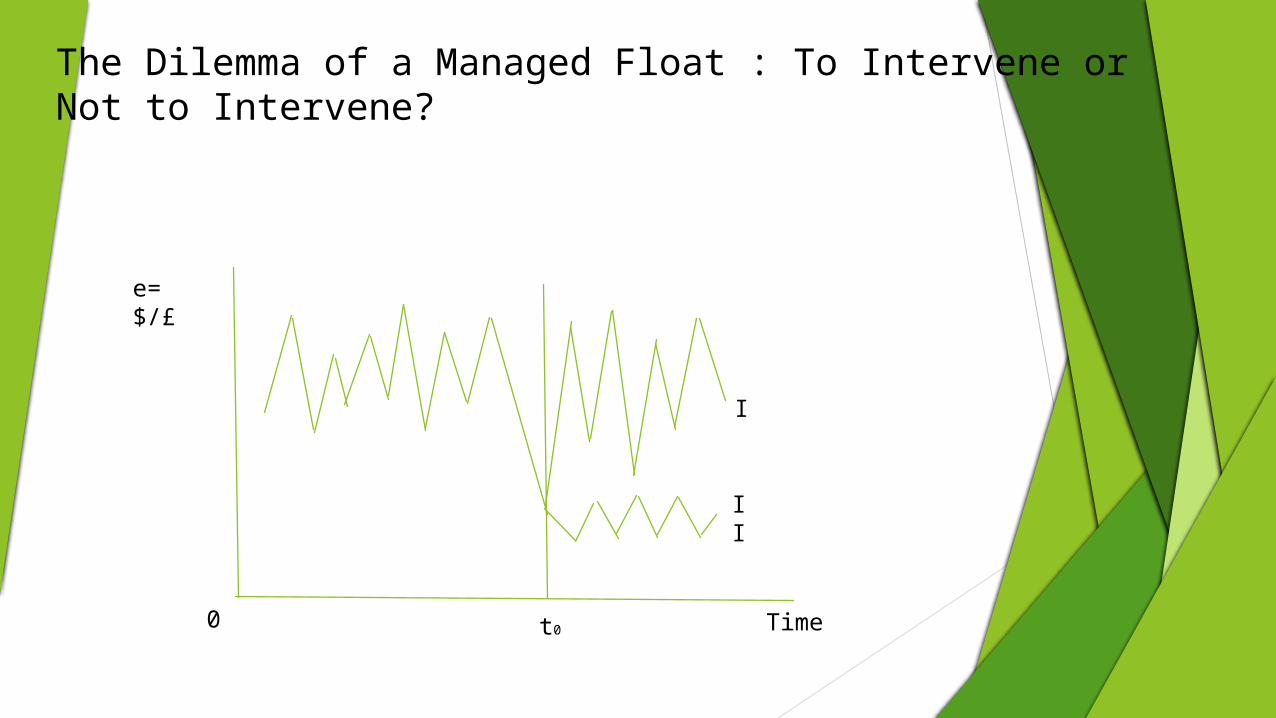

The Dilemma of a Managed Float : To Intervene or Not to Intervene?

I

II

e= $/£

0 t0 Time

6.2What Are the Problems with a Managed Float? The major criticism of managed floating exchange rates is practical rather than

theoretical. A regime with rules that require intervention in the case of temporary

disturbances No intervention in the case of permanent disturbances performs satisfactorily. the horizontal axis represents the passage of time while the vertical axis measure the exchange rate. Under a managed float, intervention should occur only if the appreciation

represents a short-term “blip” And not a fundamental change in the equilibrium exchange rate between dollars

and pounds. Central banks often intervene just enough to dampen or slow the exchange rate

movement but not enough to stop it. Such policies are called leaning against the wind. A manage float doesn’t change the basic rule that correction of a payments

imbalance requires a change in either the exchange rate or the money stock.

How Has the Macroeconomy performed in the Post –Bretton Woods Years?

US pursued expansionary policies in the mid-1970s – to end its OPEC induced economic slowdownThe effects of slowdown in U.S monetary growth hit the economy at about the same time as a second round of OPEC oil price increases in 1979-80After the 1973-1974 oil shock and the economy underwent a severe recessionThe dollar appreciated dramatically – shifted demand away from U.S made goods and services toward foreign ones.G-5_ US , Britain ,Japan ,Germany and France agreed to intervene in FX market , G-7 consist _ Canada and Italy join the G-5 The dollar has experienced period of both appreciation and depreciation against the currencies of most major trading partners

How Has the Macroeconomy performed in the Post –Bretton Woods Years?

Since 1973 represent a period of widely varying degrees of management of exchange rates.

The history of Int’l monetary regimes can’t answer the fundamental question of which arrangement is best

Each historical period brought unique challenges and shocks to the world economy

The next two sections , we summarize evaluate the main argumentsfor using fixed versus flexible exchange rates as a basis for the

international monetary system.

Pros and Cons

Fixed Exchange Rates Price Discipline Reduced volatility and

Uncertainty Real Exchange Rate

Adjustment Exchange Crises

Flexible Exchange Rate Crisis Avoidance Policy Independence and

Symmetry Consistency with Capital Mobility Excessive Volatility and Real

Exchange Rates

Money in the European Union (from EMS to EMU) European Rate Mechanism (ERM) European Union Fixed EU

currency European Currency Unit (ECU) Non EU currencies such as Dollar and

others Floated in European monetary system (EMS) European monetary integration

(1) To improve European economic performance(2) To compete with US economic site(3) To encourage intra- european trade and investment(4) To use policy creditability of government and other institutions(5) To contribute the more unified policy making in Europe

Insulation from Economic Shocks

Three major shocks disturb economies and require responses from policiy makers:

(1)Shocks to the domestic money market(2)Shocks to the domestic goods and services(3)Supply Shocks

Summary The major type of regimes Fixed exchange rate(1)Flexible exchange rate(2)Managed floating (3)Pros and Cons of exchange rates

Q & A?

Thank You