Embed Size (px)

Citation preview

....Laird Research - Economics

December 12, 2014

Where we are now . . . . . . . . . . . . . . . . . . . . . . . . 1

Indicators for US Economy . . . . . . . . . . . . . . . . . . . 2

Global Financial Markets . . . . . . . . . . . . . . . . . . . . 3

US Key Interest Rates . . . . . . . . . . . . . . . . . . . . . . 8

US Inflation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

QE Taper Tracker . . . . . . . . . . . . . . . . . . . . . . . . . 10

Exchange Rates . . . . . . . . . . . . . . . . . . . . . . . . . . 11

US Banking Indicators . . . . . . . . . . . . . . . . . . . . . . 12

US Employment Indicators . . . . . . . . . . . . . . . . . . . 13

US Business Activity Indicators . . . . . . . . . . . . . . . . 15

US Consumption Indicators . . . . . . . . . . . . . . . . . . 16

US Housing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Global Business Indicators . . . . . . . . . . . . . . . . . . . 19

Canadian Indicators . . . . . . . . . . . . . . . . . . . . . . . 22

European Indicators . . . . . . . . . . . . . . . . . . . . . . . 24

Chinese Indicators . . . . . . . . . . . . . . . . . . . . . . . . 26

Global Climate Change . . . . . . . . . . . . . . . . . . . . . 27

Where we are now

Welcome to the Laird Report. We present a selection economic datafrom around the world to help figure where we are today.

I don’t think that reproducing a chart of the oil price is that helpfulright now - mainly because everyone has already seen it. A numberof analysts have produced charts showing the sensitivity of GDP to oilprice in an effort to identify winners versus losers - but unless yourcountries name ends in “ussia”, “audi Arabia”, “enuzuala” or rhymeswith “Iran” - then you are probably pretty happy with the drop in oil.

Canada is a bit of a special case because the country is so bifurcatedbetween oil rich Alberta and everywhere else (okay, Newfoundland too)- the drop in oil price is a massive consumer boost. I’ve been hearinganecdotal polls indicating that most of the saving is being plowed intoChristmas presents - this is probably indicative of consumer spendingin North America, China and Europe (assuming Russia is still willingto sell them oil). It accounts for 68% of the US GDP.

Keep in mind that oil is more than just gas in one’s car - hydrocar-

bons form the precursor materials for most of our goods from plasticto fertilizers. A sustained drop in oil prices will create deflationarypressure in a good way - raw materials get cheaper. The savings maystay at the corporate level or trickle down to the consumer in the formof lower prices - but someone along the line is going to be happy. Theimportance of the timing of this drop when China and Europe (okay,France Germany - Spain is getting better and the UK is hopping) areboth sputtering is critical to consumer spending - aka the driver of allthat is good in the world.

Formatting Notes The grey bars on the various charts are OECDrecession indicators for the respective countries. In many cases, the lastavailable value is listed, along with the median value (measured fromas much of the data series as is available).

Subscription Info For a FREE subscription to this monthly re-port, please visit sign up at our website: www.lairdresearch.com

Laird Research, December 12, 2014

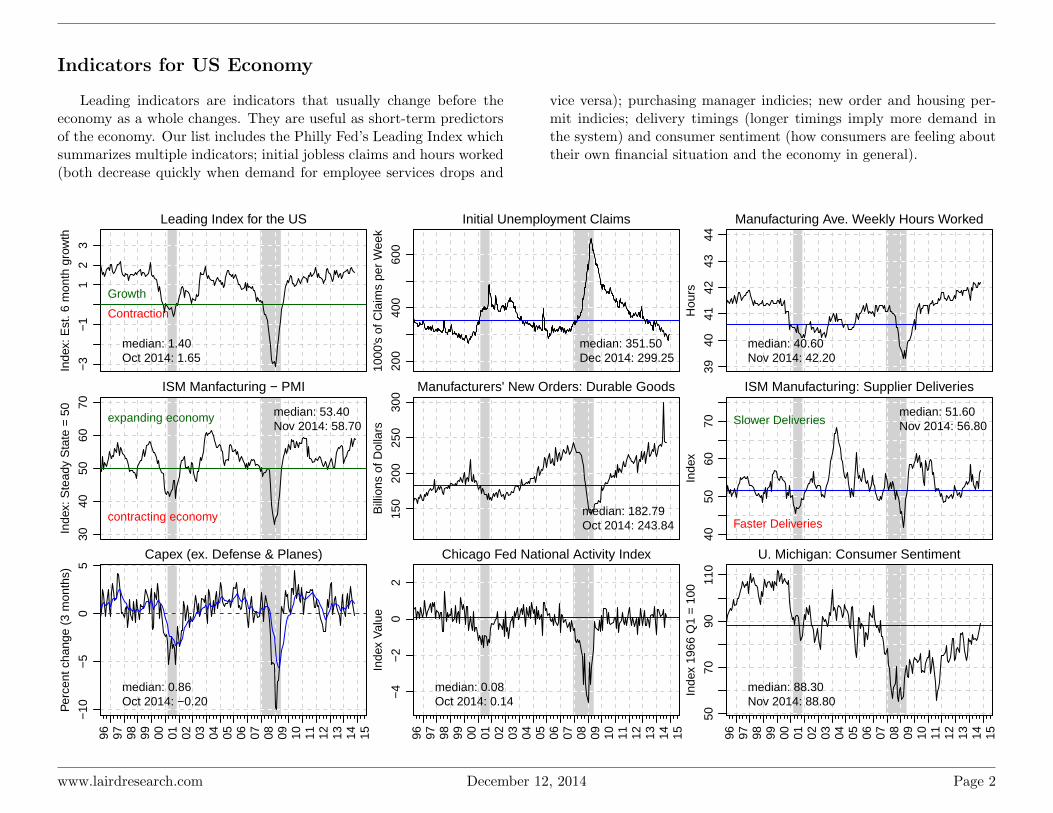

Indicators for US Economy

Leading indicators are indicators that usually change before theeconomy as a whole changes. They are useful as short-term predictorsof the economy. Our list includes the Philly Fed’s Leading Index whichsummarizes multiple indicators; initial jobless claims and hours worked(both decrease quickly when demand for employee services drops and

vice versa); purchasing manager indicies; new order and housing per-mit indicies; delivery timings (longer timings imply more demand inthe system) and consumer sentiment (how consumers are feeling abouttheir own financial situation and the economy in general).

Leading Index for the US

Inde

x: E

st. 6

mon

th g

row

th

−3

−1

12

3

median: 1.40Oct 2014: 1.65

Growth

Contraction

Initial Unemployment Claims

1000

's o

f Cla

ims

per

Wee

k

200

400

600

median: 351.50Dec 2014: 299.25

Manufacturing Ave. Weekly Hours Worked

Hou

rs

3940

4142

4344

median: 40.60Nov 2014: 42.20

ISM Manfacturing − PMI

Inde

x: S

tead

y S

tate

= 5

0

3040

5060

70 median: 53.40Nov 2014: 58.70

expanding economy

contracting economy

Manufacturers' New Orders: Durable GoodsB

illio

ns o

f Dol

lars

150

200

250

300

median: 182.79Oct 2014: 243.84

ISM Manufacturing: Supplier Deliveries

Inde

x

4050

6070

median: 51.60Nov 2014: 56.80Slower Deliveries

Faster Deliveries

Capex (ex. Defense & Planes)

Per

cent

cha

nge

(3 m

onth

s)

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

−10

−5

05

median: 0.86Oct 2014: −0.20

Chicago Fed National Activity Index

Inde

x V

alue

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

−4

−2

02

median: 0.08Oct 2014: 0.14

U. Michigan: Consumer Sentiment

Inde

x 19

66 Q

1 =

100

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

5070

9011

0

median: 88.30Nov 2014: 88.80

www.lairdresearch.com December 12, 2014 Page 2

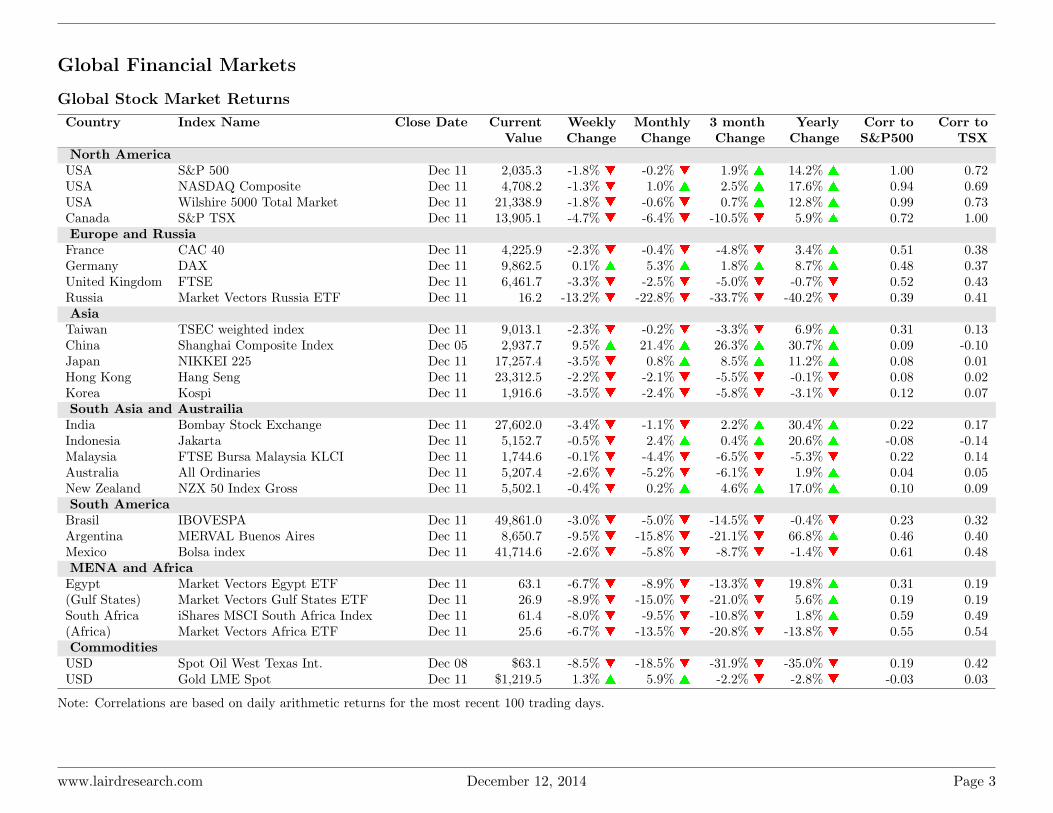

Global Financial Markets

Global Stock Market Returns

Country Index Name Close Date CurrentValue

WeeklyChange

MonthlyChange

3 monthChange

YearlyChange

Corr toS&P500

Corr toTSX

North AmericaUSA S&P 500 Dec 11 2,035.3 -1.8% t -0.2% t 1.9% s 14.2% s 1.00 0.72USA NASDAQ Composite Dec 11 4,708.2 -1.3% t 1.0% s 2.5% s 17.6% s 0.94 0.69USA Wilshire 5000 Total Market Dec 11 21,338.9 -1.8% t -0.6% t 0.7% s 12.8% s 0.99 0.73Canada S&P TSX Dec 11 13,905.1 -4.7% t -6.4% t -10.5% t 5.9% s 0.72 1.00Europe and RussiaFrance CAC 40 Dec 11 4,225.9 -2.3% t -0.4% t -4.8% t 3.4% s 0.51 0.38Germany DAX Dec 11 9,862.5 0.1% s 5.3% s 1.8% s 8.7% s 0.48 0.37United Kingdom FTSE Dec 11 6,461.7 -3.3% t -2.5% t -5.0% t -0.7% t 0.52 0.43Russia Market Vectors Russia ETF Dec 11 16.2 -13.2% t -22.8% t -33.7% t -40.2% t 0.39 0.41AsiaTaiwan TSEC weighted index Dec 11 9,013.1 -2.3% t -0.2% t -3.3% t 6.9% s 0.31 0.13China Shanghai Composite Index Dec 05 2,937.7 9.5% s 21.4% s 26.3% s 30.7% s 0.09 -0.10Japan NIKKEI 225 Dec 11 17,257.4 -3.5% t 0.8% s 8.5% s 11.2% s 0.08 0.01Hong Kong Hang Seng Dec 11 23,312.5 -2.2% t -2.1% t -5.5% t -0.1% t 0.08 0.02Korea Kospi Dec 11 1,916.6 -3.5% t -2.4% t -5.8% t -3.1% t 0.12 0.07South Asia and AustrailiaIndia Bombay Stock Exchange Dec 11 27,602.0 -3.4% t -1.1% t 2.2% s 30.4% s 0.22 0.17Indonesia Jakarta Dec 11 5,152.7 -0.5% t 2.4% s 0.4% s 20.6% s -0.08 -0.14Malaysia FTSE Bursa Malaysia KLCI Dec 11 1,744.6 -0.1% t -4.4% t -6.5% t -5.3% t 0.22 0.14Australia All Ordinaries Dec 11 5,207.4 -2.6% t -5.2% t -6.1% t 1.9% s 0.04 0.05New Zealand NZX 50 Index Gross Dec 11 5,502.1 -0.4% t 0.2% s 4.6% s 17.0% s 0.10 0.09South AmericaBrasil IBOVESPA Dec 11 49,861.0 -3.0% t -5.0% t -14.5% t -0.4% t 0.23 0.32Argentina MERVAL Buenos Aires Dec 11 8,650.7 -9.5% t -15.8% t -21.1% t 66.8% s 0.46 0.40Mexico Bolsa index Dec 11 41,714.6 -2.6% t -5.8% t -8.7% t -1.4% t 0.61 0.48MENA and AfricaEgypt Market Vectors Egypt ETF Dec 11 63.1 -6.7% t -8.9% t -13.3% t 19.8% s 0.31 0.19(Gulf States) Market Vectors Gulf States ETF Dec 11 26.9 -8.9% t -15.0% t -21.0% t 5.6% s 0.19 0.19South Africa iShares MSCI South Africa Index Dec 11 61.4 -8.0% t -9.5% t -10.8% t 1.8% s 0.59 0.49(Africa) Market Vectors Africa ETF Dec 11 25.6 -6.7% t -13.5% t -20.8% t -13.8% t 0.55 0.54CommoditiesUSD Spot Oil West Texas Int. Dec 08 $63.1 -8.5% t -18.5% t -31.9% t -35.0% t 0.19 0.42USD Gold LME Spot Dec 11 $1,219.5 1.3% s 5.9% s -2.2% t -2.8% t -0.03 0.03

Note: Correlations are based on daily arithmetic returns for the most recent 100 trading days.

www.lairdresearch.com December 12, 2014 Page 3

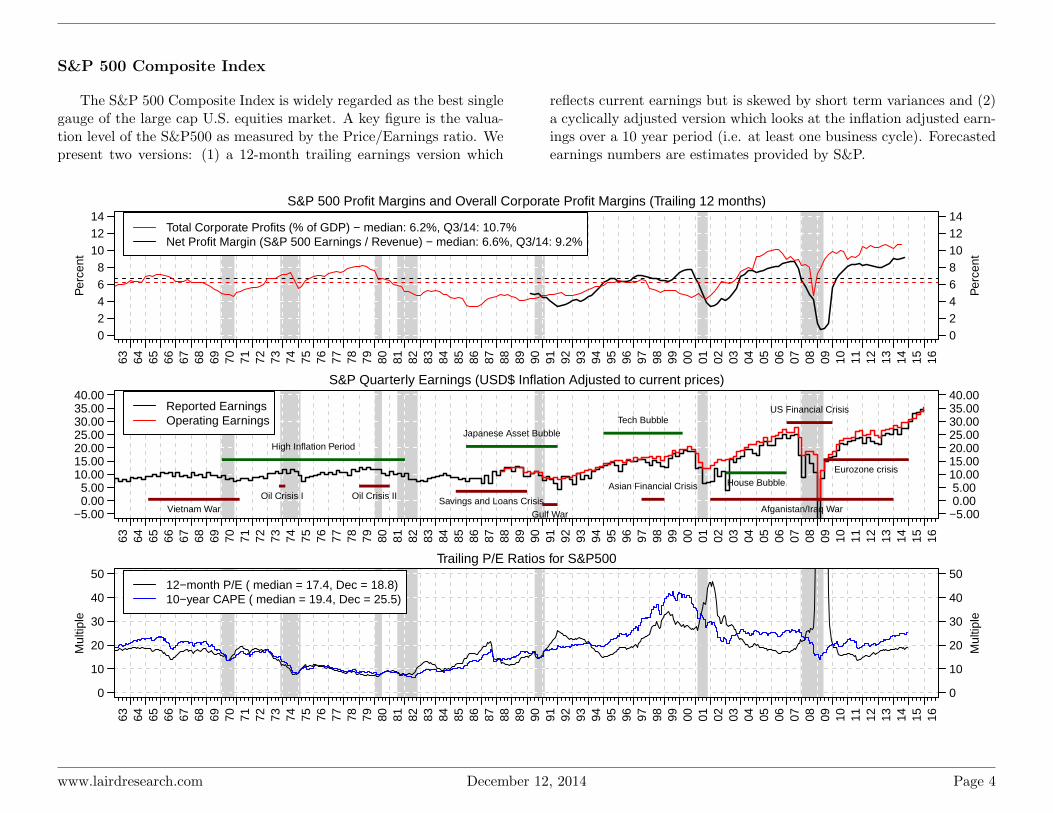

S&P 500 Composite Index

The S&P 500 Composite Index is widely regarded as the best singlegauge of the large cap U.S. equities market. A key figure is the valua-tion level of the S&P500 as measured by the Price/Earnings ratio. Wepresent two versions: (1) a 12-month trailing earnings version which

reflects current earnings but is skewed by short term variances and (2)a cyclically adjusted version which looks at the inflation adjusted earn-ings over a 10 year period (i.e. at least one business cycle). Forecastedearnings numbers are estimates provided by S&P.

S&P 500 Profit Margins and Overall Corporate Profit Margins (Trailing 12 months)

Per

cent

63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

02468

101214

02468101214

Per

cent

Total Corporate Profits (% of GDP) − median: 6.2%, Q3/14: 10.7%Net Profit Margin (S&P 500 Earnings / Revenue) − median: 6.6%, Q3/14: 9.2%

S&P Quarterly Earnings (USD$ Inflation Adjusted to current prices)

63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

−5.00 0.00 5.0010.0015.0020.0025.0030.0035.0040.00

−5.00 0.00 5.0010.0015.0020.0025.0030.0035.0040.00

Tech BubbleJapanese Asset Bubble

House BubbleAsian Financial Crisis

US Financial Crisis

Eurozone crisis

Oil Crisis I Oil Crisis II

Gulf WarSavings and Loans Crisis

High Inflation Period

Afganistan/Iraq WarVietnam War

Reported EarningsOperating Earnings

Trailing P/E Ratios for S&P500

63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

0

10

20

30

40

50

0

10

20

30

40

50

Mul

tiple

Mul

tiple

12−month P/E ( median = 17.4, Dec = 18.8)10−year CAPE ( median = 19.4, Dec = 25.5)

www.lairdresearch.com December 12, 2014 Page 4

S&P 500 Composite Distributions

This is a view of the price performance of the S&P 500 index com-panies. The area of each box is proportional to the company’s marketcap, while the colour is determined by the percentage change in price

over the past month. In addition, companies are sorted according totheir industry group.

AAPL2.5%

MSFT−0.57%

GOOG−4.8%

FB5.2%

ORCL4.5%

INTC7.7%

V8.9%

IBM−1.3%

CSCO9.8%

QCOM

MA

EMC

TXN

MU

NFLX FIS

MSI

EA

CA

BRK−B6.6%

WFC2.7%

JPM0.43%

BAC1.2%

C1.9%

GS

USB

AIG

MS

MET BLK

SPG

BK

PRU

ACE

BEN

CME

ALL

BBT

AON

CCI

CB WY

IVZ

L

RF

JNJ−0.69%

PFE5.7%

MRK0.71%

GILD−5.2%

AMGN2.8%

ABBV

UNH5.1%

CELG

BIIB

LLY

ACT

ABT

AGN

ESRXREGN

AET

VRTX

CI

ZTS A

DIS0.044%

CMCSA0.54%

HD4.4%

MCD

NKE

FOXA

TWX

LOW

F

PCLN GM

TGT

TJX

DTV

TWC LB

MAR

M

CMG OMC

RCL

GPS

WMT9.9%

PG3.5%

KO

PEP0.48%

PM−3.6%

CVS5.6%

MO2.6%

WAG

MDLZ

CL

GIS

KR

EL K

LO

GE−1.1%

UTX

MMM3.8%

UNP

UPS

BA

LMT

CAT

GD

DAL

PCP

RTN

NSC

ETN

DE

NOC

LUV

GLW

CMI

IR

XOM−5.7%

CVX

SLB COP

OXY

KMI

PSX

WMB

NOV

VLO

SE

HES

PXD

DD

MON

DOW

LYB

PX

PPG

SHW

IP

AA

CF

DUK

NEE

SO

D ED

VZ−8%

T−6.1%

Information Technology Financials

Health Care

Consumer Discretionary

Consumer Staples

Industrials

Energy Materials

Utilities

TelecommunicationsServices

<−25.0% −20.0% −15.0% −10.0% −5.0% 0.0% 5.0% 10.0% 15.0% 20.0% >25.0%

% Change in Price from Nov 3, 2014 to Dec 11, 2014

Average Median Median MedianSector Change P/Sales P/Book P/EHealth Care 3.7% s 3.4 4.1 25.4Consumer Staples 3.6% s 1.9 5.1 22.9Consumer Discretionary 3.6% s 1.6 4.2 20.3Financials 3.0% s 3.1 1.6 18.2Information Technology 2.4% s 3.4 3.9 21.3

Average Median Median MedianSector Change P/Sales P/Book P/EIndustrials 1.4% s 1.6 3.4 19.3Utilities 0.9% s 1.6 1.7 19.0Materials 0.2% s 1.6 3.5 23.6Telecommunications Services -6.7% t 1.3 4.3 30.9Energy -11.1% t 1.4 1.5 13.1

www.lairdresearch.com December 12, 2014 Page 5

US Equity Valuations

A key valuation metric is Tobin’s q: the ratio between the marketvalue of the entire US stock market versus US net assets at replacementcost (ie. what you pay versus what you get). Warren Buffet famouslyfollows stock market value as a percentage of GNP, which is highly(93%) correlated to Tobin’s q.

We can also take the reverse approach: assume the market hasvaluations correct, we can determine the required returns of future es-

timated earnings. These are quoted for both debt (using BAA ratedsecurities as a proxy) and equity premiums above the risk free rate (10year US Treasuries). These figures are alternate approaches to under-standing the current market sentiment - higher premiums indicate ademand for greater returns for the same price and show the level ofrisk-aversion in the market.

Tobin's q (Market Equity / Market Net Worth) and S&P500 Price/Sales

63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

0.25

0.50

0.75

1.00

1.25

1.50

1.75

0.25

0.50

0.75

1.00

1.25

1.50

1.75

Buying assets at a discount

Paying up for growth

Tobin Q (median = 0.75, Sep = 1.09)S&P 500 Price/Sales (median = 1.32, Sep = 1.73)

Equity and Debt Risk Premiums: Spread vs. Risk Free Rate (10−year US Treasury)

63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

0%

2%

4%

6%

8%

10%

0%

2%

4%

6%

8%

10%Implied Equity Premium (median = 4.2%, Nov = 4.9%)Debt (BAA) Premium (median = 2.0%, Nov = 2.6%)

www.lairdresearch.com December 12, 2014 Page 6

US Mutual Fund Flows

Fund flows describe the net investments in equity and bond mutualfunds in the US market, as described in ICI’s “Trends in Mutual FundInvesting” report. Note however that this is only part of the story as

it does not include ETF fund flows - part of the changes are investorsentering or leaving the market, and part is investors shifting to ETF’sfrom mutual funds.

US Net New Investment Cash Flow to Mutual Funds

US

$ bi

llion

s (m

onth

ly)

2007 2008 2009 2010 2011 2012 2013 2014

−40

−20

020

40

Domestic EquityWorld EquityTaxable BondsMunicipal Bonds

US Net New Investment Cash Flow to Mutual Funds

US

$ bi

llion

s (M

onth

ly)

2007 2008 2009 2010 2011 2012 2013 2014

−60

−40

−20

020

4060

Flows to EquityFlows to BondsNet Market Flows

www.lairdresearch.com December 12, 2014 Page 7

US Key Interest Rates

Interest rates are often leading indicators of stress in the financialsystem. The yield curve show the time structure of interest rates ongovernment bonds - Usually the longer the time the loan is outstanding,the higher the rate charged. However if a recession is expected, thenthe fed cuts rates and this relationship is inverted - leading to negativespreads where short term rates are higher than long term rates.

Almost every recession in the past century has been preceeded by an

inversion - though not every inversion preceeds a recession (just mostof the time).

For corporate bonds, the key issue is the spread between bond rates(i.e. AAA vs BAA bonds) or between government loans (LIBOR vsFedfunds - the infamous “TED Spread”). Here a spike correlates to anaversion to risk, which is an indication that something bad is happen-ing.

US Treasury Yield Curves

For

war

d In

stan

tane

ous

Rat

es (

%)

14 15 16 17 18 19 20 21 22 23 240.0

0.5

1.0

1.5

2.0

2.5

3.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0Dec 10, 2014 (Today)Nov 10, 2014 (1 mo ago)Sep 10, 2014 (3 mo ago)10 Dec 2013 (1 yr ago)

3 Month & 10 Yr Treasury Yields

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

0%

1%

2%

3%

4%

5%

6%

7%

0%

1%

2%

3%

4%

5%

6%

7%10 Yr Treasury3 Mo TreasurySpread

AAA vs. BAA Bond Spreads

4%

5%

6%

7%

8%

9%

4%

5%

6%

7%

8%

9%

Per

cent

AAABAA

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

median: 90.00Dec 2014: 89.00

0100200300

0100200300

Spr

ead

(bps

)

LIBOR vs. Fedfunds Rate

0%

1%

2%

3%

4%

5%

6%

7%

0%

1%

2%

3%

4%

5%

6%

7%

Per

cent

3 mos t−billLIBOR

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

median: 36.81Dec 2014: 20.54

0100200300

0100200300

Spr

ead

(bps

)

www.lairdresearch.com December 12, 2014 Page 8

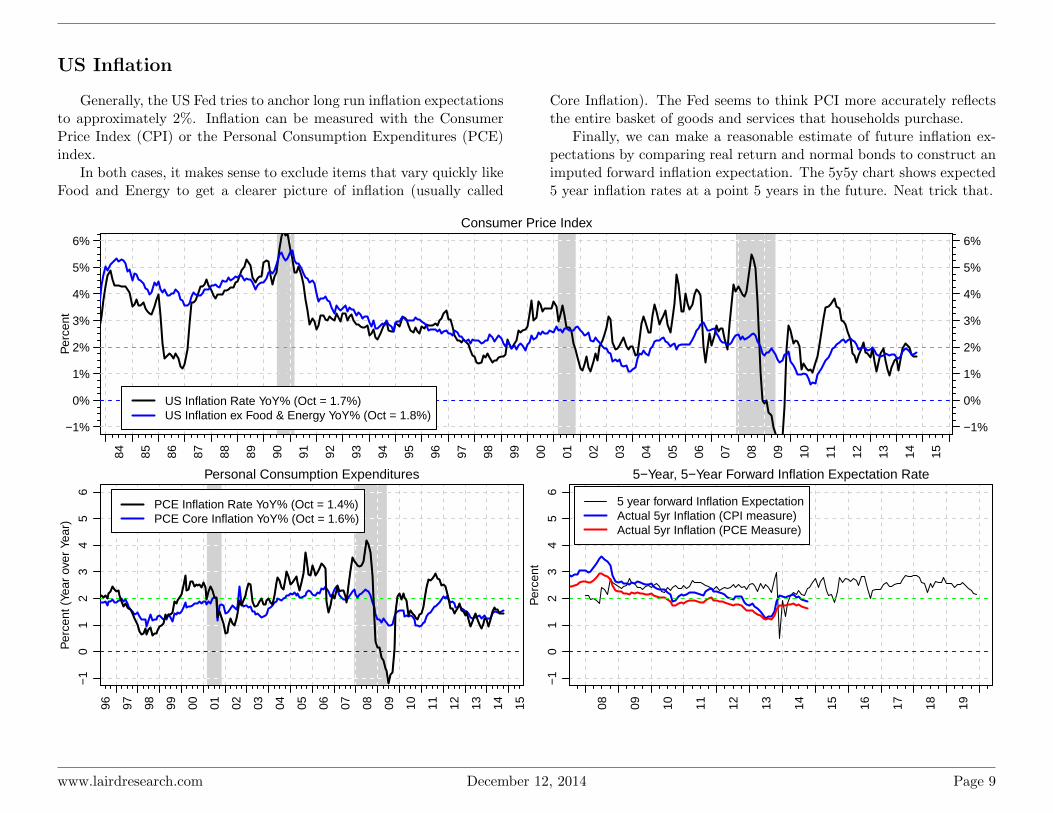

US Inflation

Generally, the US Fed tries to anchor long run inflation expectationsto approximately 2%. Inflation can be measured with the ConsumerPrice Index (CPI) or the Personal Consumption Expenditures (PCE)index.

In both cases, it makes sense to exclude items that vary quickly likeFood and Energy to get a clearer picture of inflation (usually called

Core Inflation). The Fed seems to think PCI more accurately reflectsthe entire basket of goods and services that households purchase.

Finally, we can make a reasonable estimate of future inflation ex-pectations by comparing real return and normal bonds to construct animputed forward inflation expectation. The 5y5y chart shows expected5 year inflation rates at a point 5 years in the future. Neat trick that.

Consumer Price Index

Per

cent

84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

−1%

0%

1%

2%

3%

4%

5%

6%

−1%

0%

1%

2%

3%

4%

5%

6%

US Inflation Rate YoY% (Oct = 1.7%)US Inflation ex Food & Energy YoY% (Oct = 1.8%)

Personal Consumption Expenditures

Per

cent

(Ye

ar o

ver

Year

)

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

−1

01

23

45

6

PCE Inflation Rate YoY% (Oct = 1.4%)PCE Core Inflation YoY% (Oct = 1.6%)

5−Year, 5−Year Forward Inflation Expectation Rate

Per

cent

08 09 10 11 12 13 14 15 16 17 18 19

−1

01

23

45

6

5 year forward Inflation ExpectationActual 5yr Inflation (CPI measure)Actual 5yr Inflation (PCE Measure)

www.lairdresearch.com December 12, 2014 Page 9

QE Taper Tracker

The US has been using the program of Quantitative Easing to pro-vide monetary stimulous to its economy. The Fed has engaged in aseries of programs (QE1, QE2 & QE3) designed to drive down longterm rates and improve liquidity though purchases of treasuries, mor-gage backed securites and other debt from banks.

The higher demand for long maturity securities would drive up theirprice, but as these securities have a fixed coupon, their yield would bedecreased (yield ≈ coupon / price) thus driving down long term rates.

In 2011-2012, “Operation Twist” attempted to reduce rates withoutincreasing liquidity. They went back to QE in 2013.

The Fed chairman suggested in June 2013 the economy was recover-ing enough that they could start slowing down purchases (“tapering”).The Fed backed off after a brief market panic. The Fed announced inDec 2013 that it was starting the taper, a decision partly driven byseeing key targets of inflation around 2% and unemployment being lessthan 6.5%. In Oct 2014, they announced the end of purchases.

QE Asset Purchases to Date (Treasury & Mortgage Backed Securities)

Trill

ions

0.00.51.01.52.02.5

0.00.51.01.52.02.5

QE1 QE2 Operation Twist QE3 TaperTreasuries

Mortgage Backed Securities

Total Monthly Asset Purchases (Treasury + Mortgage Backed Securities)

Bill

ions

−100−50

050

100150200

−100−50050100150200

Month to date Dec 10: $−0.06

Inflation and Unemployment − Relative to Targets

Per

cent

02468

10

0246810

Target Unemployment 6.5%Target Inflation 2%

U.S. 10 Year and 3 Month Treasury Constant Maturity Yields

Per

cent

012345

012345

2008 2009 2010 2011 2012 2013 2014

Short Term Rates:Once at zero, Fed moved to QE

Long Term Rates:Moving up in anticipation of Taper?

www.lairdresearch.com December 12, 2014 Page 10

Exchange Rates

10 Week Moving Average CAD Exchange Rates

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

0.62

0.71

0.81

0.90

1.00

1.09

US

A /

CA

D

0.55

0.61

0.66

0.72

0.77

0.82

Eur

o / C

AD

59.

16 7

4.71

90.

2610

5.81

121.

3613

6.91

Japa

n / C

AD

0.38

0.44

0.49

0.55

0.61

0.67

U.K

. / C

AD

0.59

0.98

1.36

1.74

2.12

2.51

Bra

zil /

CA

D

CAD Appreciating

CAD Depreciating

Change in F/X: Nov 3 2014 to Dec 5 2014(Trade Weighted Currency Index of USD Trading Partners)

−3.0%

−1.5%

1.5%

3.0%

Euro−1.1%

UK−0.2%

Japan 3.8%

South Korea 1.0%

China−2.1%

India−1.8%

Brazil 1.5%

Mexico 3.1%

Canada−1.7%

USA 2.7%

Country vs. Average

AppreciatingDepreciating

% Change over 3 months vs. Canada

<−10.0% −8.0% −6.0% −4.0% −2.0% 0.0% 2.0% 4.0% 6.0% 8.0% >10.0%

CAD depreciatingCAD appreciating

ARG 2.7%

AUS −5.1%

BRA −8.9%

CHN 4.9%

IND 2.0%

RUS−29.1%

USA 4.6%

EUR0.6%

JPY−5.7%

KRW−1.7%

MXN−5.3%

ZAR−0.9%

www.lairdresearch.com December 12, 2014 Page 11

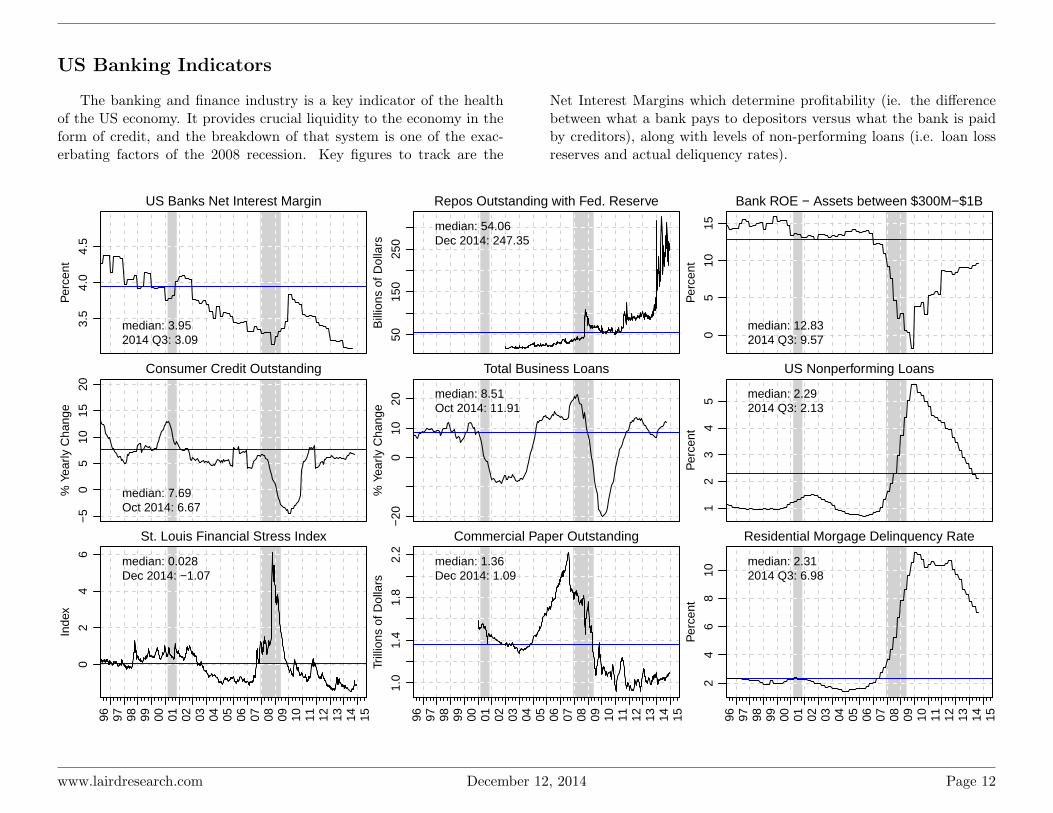

US Banking Indicators

The banking and finance industry is a key indicator of the healthof the US economy. It provides crucial liquidity to the economy in theform of credit, and the breakdown of that system is one of the exac-erbating factors of the 2008 recession. Key figures to track are the

Net Interest Margins which determine profitability (ie. the differencebetween what a bank pays to depositors versus what the bank is paidby creditors), along with levels of non-performing loans (i.e. loan lossreserves and actual deliquency rates).

US Banks Net Interest Margin

Per

cent

3.5

4.0

4.5

median: 3.952014 Q3: 3.09

Repos Outstanding with Fed. Reserve

Bill

ions

of D

olla

rs

5015

025

0

median: 54.06Dec 2014: 247.35

Bank ROE − Assets between $300M−$1B

Per

cent

05

1015

median: 12.832014 Q3: 9.57

Consumer Credit Outstanding

% Y

early

Cha

nge

−5

05

1015

20

median: 7.69Oct 2014: 6.67

Total Business Loans%

Yea

rly C

hang

e

−20

010

20median: 8.51Oct 2014: 11.91

US Nonperforming Loans

Per

cent

12

34

5

median: 2.292014 Q3: 2.13

St. Louis Financial Stress Index

Inde

x

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

02

46

median: 0.028Dec 2014: −1.07

Commercial Paper Outstanding

Trill

ions

of D

olla

rs

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

1.0

1.4

1.8

2.2

median: 1.36Dec 2014: 1.09

Residential Morgage Delinquency Rate

Per

cent

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

24

68

10

median: 2.312014 Q3: 6.98

www.lairdresearch.com December 12, 2014 Page 12

US Employment Indicators

Unemployment rates are considered the “single best indicator ofcurrent labour conditions” by the Fed. The pace of payroll growth ishighly correlated with a number of economic indicators.Payroll changesare another way to track the change in unemployment rate.

Unemployment only captures the percentage of people who are inthe labour market who don’t currently have a job - another measure

is what percentage of the whole population wants a job (employed ornot) - this is the Participation Rate.

The Beveridge Curve measures labour market efficiency by lookingat the relationship between job openings and the unemployment rate.The curve slopes downward reflecting that higher rates of unemploy-ment occur coincidentally with lower levels of job vacancies.

Unemployment Rate

Per

cent

79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

median: 6.20Nov 2014: 5.804

56789

1011

4567891011

Per

cent

4 5 6 7 8 9 10

2.0

2.5

3.0

3.5

4.0

Beveridge Curve (Unemployment vs. Job Openings)

Unemployment Rate (%)

Job

Ope

ning

s (%

tota

l Em

ploy

men

t)

Dec 2000 − Dec 2008Jan 2009 − Sep 2014Oct 2014

Participation Rate

Per

cent

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

6364

6566

67

median: 66.10Nov 2014: 62.80

Total Nonfarm Payroll Change

Mon

thly

Cha

nge

(000

s)

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

−50

00

500

median: 162.00Nov 2014: 321.00

www.lairdresearch.com December 12, 2014 Page 13

There are a number of other ways to measure the health of employ-ment. The U6 Rate includes people who are part time that want afull-time job - they are employed but under-utilitized. Temporary helpdemand is another indicator of labour market tightness or slack.

The large chart shows changes in private industry employment lev-els over the past year, versus how well those job segments typically pay.Lots of hiring in low paying jobs at the expense of higher paying jobsis generally bad, though perhaps not unsurprising in a recovery.

Median Duration of Unemployment

Wee

ks

510

1520

25 median: 8.60Nov 2014: 12.80

(U6) Unemployed + PT + Marginally Attached

Per

cent

810

1214

16

median: 9.70Nov 2014: 11.40

4−week moving average of Initial Claims

Jan

1995

= 1

00

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

5010

015

020

0

median: 108.07Dec 2014: 92.01

Unemployed over 27 weeks

Mill

ions

of P

erso

ns

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

01

23

45

67

median: 0.78Nov 2014: 2.77

Services: Temp Help

Mill

ions

of P

erso

ns

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

1.5

2.0

2.5

3.0

median: 2.24Nov 2014: 2.98

0 200 400 600

15

20

25

30

35

Annual Change in Employment Levels (000s of Workers)

Ave

rage

wag

es (

$/ho

ur)

Private Industry Employment Change (1 year)

ConstructionDurable Goods

Education

Financial Activities

Health Services

Information

Leisure and Hospitality

Manufacturing

Mining and Logging

Nondurable GoodsOther Services

Professional &Business Services

Retail Trade

Transportation

Utilities

Wholesale Trade

Circle size relative to total employees in industry

www.lairdresearch.com December 12, 2014 Page 14

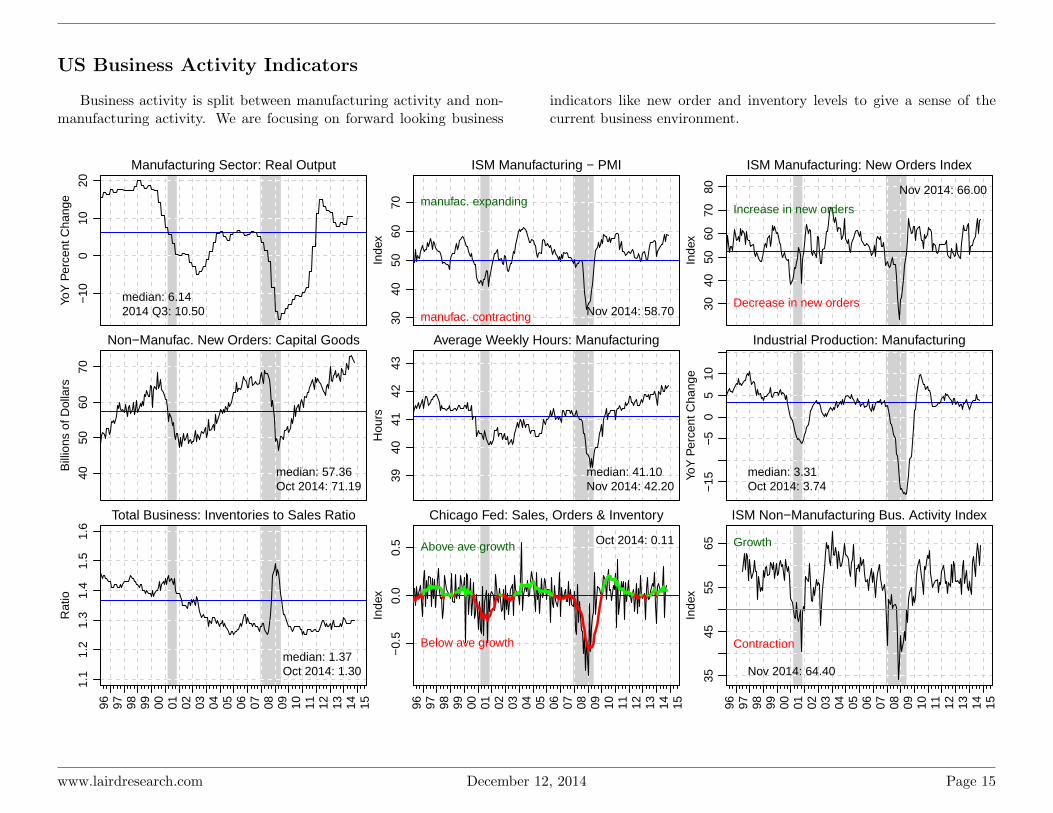

US Business Activity Indicators

Business activity is split between manufacturing activity and non-manufacturing activity. We are focusing on forward looking business

indicators like new order and inventory levels to give a sense of thecurrent business environment.

Manufacturing Sector: Real Output

YoY

Per

cent

Cha

nge

−10

010

20

median: 6.142014 Q3: 10.50

ISM Manufacturing − PMI

Inde

x

3040

5060

70

Nov 2014: 58.70

manufac. expanding

manufac. contracting

ISM Manufacturing: New Orders Index

Inde

x

3040

5060

7080 Nov 2014: 66.00

Increase in new orders

Decrease in new orders

Non−Manufac. New Orders: Capital Goods

Bill

ions

of D

olla

rs

4050

6070

median: 57.36Oct 2014: 71.19

Average Weekly Hours: Manufacturing

Hou

rs

3940

4142

43

median: 41.10Nov 2014: 42.20

Industrial Production: Manufacturing

YoY

Per

cent

Cha

nge

−15

−5

05

10

median: 3.31Oct 2014: 3.74

Total Business: Inventories to Sales Ratio

Rat

io

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

1.1

1.2

1.3

1.4

1.5

1.6

median: 1.37Oct 2014: 1.30

Chicago Fed: Sales, Orders & Inventory

Inde

x

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

−0.

50.

00.

5 Oct 2014: 0.11Above ave growth

Below ave growth

ISM Non−Manufacturing Bus. Activity Index

Inde

x

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

3545

5565

Nov 2014: 64.40

Growth

Contraction

www.lairdresearch.com December 12, 2014 Page 15

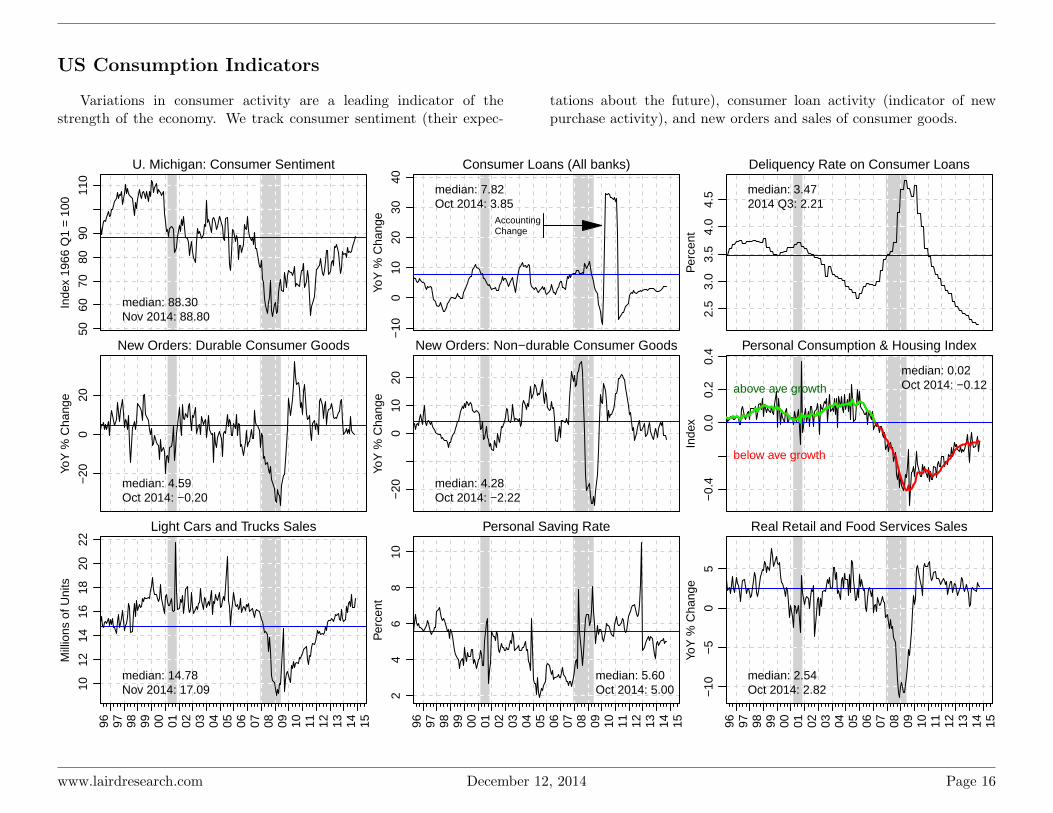

US Consumption Indicators

Variations in consumer activity are a leading indicator of thestrength of the economy. We track consumer sentiment (their expec-

tations about the future), consumer loan activity (indicator of newpurchase activity), and new orders and sales of consumer goods.

U. Michigan: Consumer Sentiment

Inde

x 19

66 Q

1 =

100

5060

7080

9011

0

median: 88.30Nov 2014: 88.80

Consumer Loans (All banks)

YoY

% C

hang

e

−10

010

2030

40

median: 7.82Oct 2014: 3.85

AccountingChange

Deliquency Rate on Consumer Loans

Per

cent

2.5

3.0

3.5

4.0

4.5 median: 3.47

2014 Q3: 2.21

New Orders: Durable Consumer Goods

YoY

% C

hang

e

−20

020

median: 4.59Oct 2014: −0.20

New Orders: Non−durable Consumer Goods

YoY

% C

hang

e

−20

010

20

median: 4.28Oct 2014: −2.22

Personal Consumption & Housing Index

Inde

x

−0.

40.

00.

20.

4

median: 0.02Oct 2014: −0.12above ave growth

below ave growth

Light Cars and Trucks Sales

Mill

ions

of U

nits

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

1012

1416

1820

22

median: 14.78Nov 2014: 17.09

Personal Saving Rate

Per

cent

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

24

68

10

median: 5.60Oct 2014: 5.00

Real Retail and Food Services Sales

YoY

% C

hang

e

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

−10

−5

05

median: 2.54Oct 2014: 2.82

www.lairdresearch.com December 12, 2014 Page 16

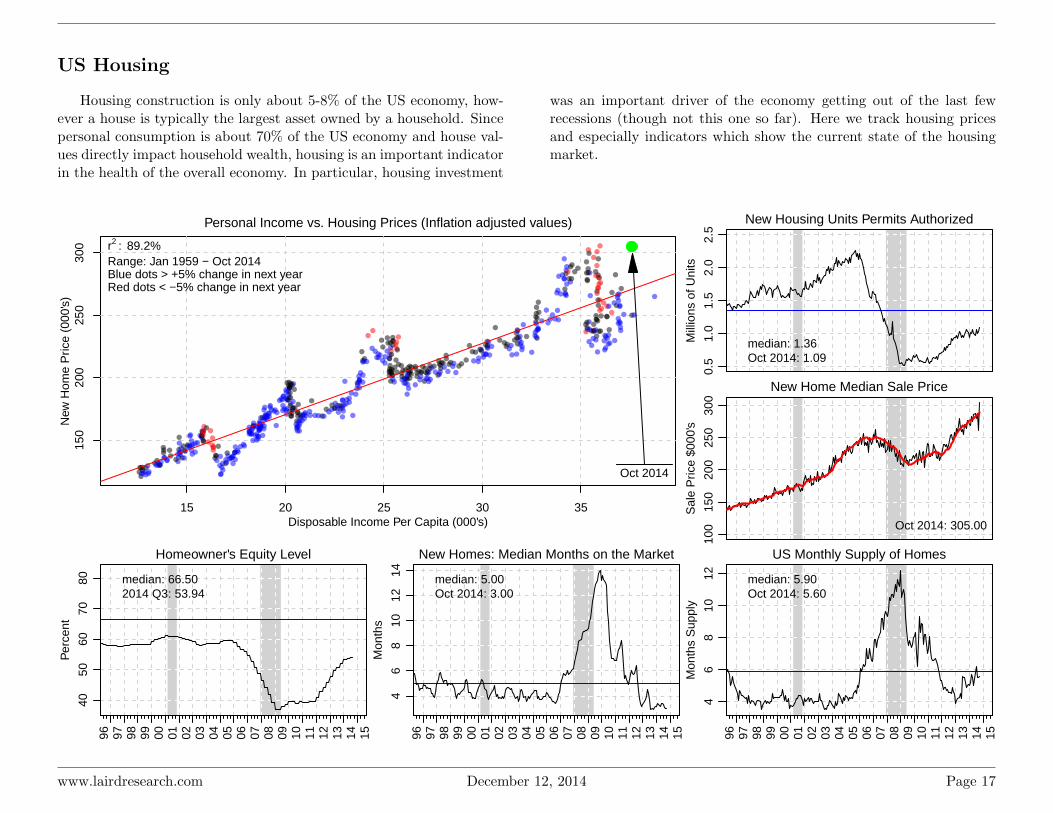

US Housing

Housing construction is only about 5-8% of the US economy, how-ever a house is typically the largest asset owned by a household. Sincepersonal consumption is about 70% of the US economy and house val-ues directly impact household wealth, housing is an important indicatorin the health of the overall economy. In particular, housing investment

was an important driver of the economy getting out of the last fewrecessions (though not this one so far). Here we track housing pricesand especially indicators which show the current state of the housingmarket.

15 20 25 30 35

150

200

250

300

Personal Income vs. Housing Prices (Inflation adjusted values)

New

Hom

e P

rice

(000

's)

Disposable Income Per Capita (000's)

Oct 2014

r2 : 89.2%Range: Jan 1959 − Oct 2014Blue dots > +5% change in next yearRed dots < −5% change in next year

New Housing Units Permits Authorized

Mill

ions

of U

nits

0.5

1.0

1.5

2.0

2.5

median: 1.36Oct 2014: 1.09

New Home Median Sale Price

Sal

e P

rice

$000

's

100

150

200

250

300

Oct 2014: 305.00

Homeowner's Equity Level

Per

cent

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

4050

6070

80 median: 66.502014 Q3: 53.94

New Homes: Median Months on the Market

Mon

ths

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

46

810

1214 median: 5.00

Oct 2014: 3.00

US Monthly Supply of Homes

Mon

ths

Sup

ply

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

46

810

12 median: 5.90Oct 2014: 5.60

www.lairdresearch.com December 12, 2014 Page 17

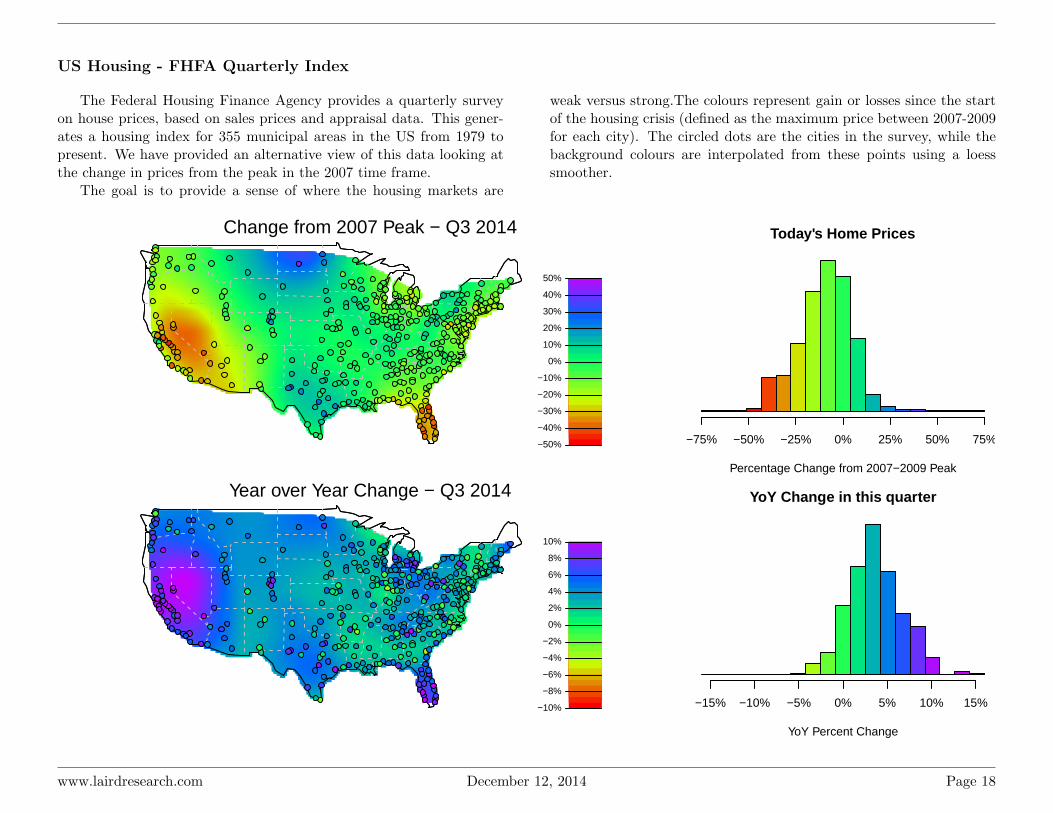

US Housing - FHFA Quarterly Index

The Federal Housing Finance Agency provides a quarterly surveyon house prices, based on sales prices and appraisal data. This gener-ates a housing index for 355 municipal areas in the US from 1979 topresent. We have provided an alternative view of this data looking atthe change in prices from the peak in the 2007 time frame.

The goal is to provide a sense of where the housing markets are

weak versus strong.The colours represent gain or losses since the startof the housing crisis (defined as the maximum price between 2007-2009for each city). The circled dots are the cities in the survey, while thebackground colours are interpolated from these points using a loesssmoother.

Change from 2007 Peak − Q3 2014

−50%

−40%

−30%

−20%

−10%

0%

10%

20%

30%

40%

50%

Today's Home Prices

Percentage Change from 2007−2009 Peak

Fre

quen

cy

−75% −50% −25% 0% 25% 50% 75%

Year over Year Change − Q3 2014

−10%

−8%

−6%

−4%

−2%

0%

2%

4%

6%

8%

10%

YoY Change in this quarter

YoY Percent Change

Fre

quen

cy

−15% −10% −5% 0% 5% 10% 15%

www.lairdresearch.com December 12, 2014 Page 18

Global Business Indicators

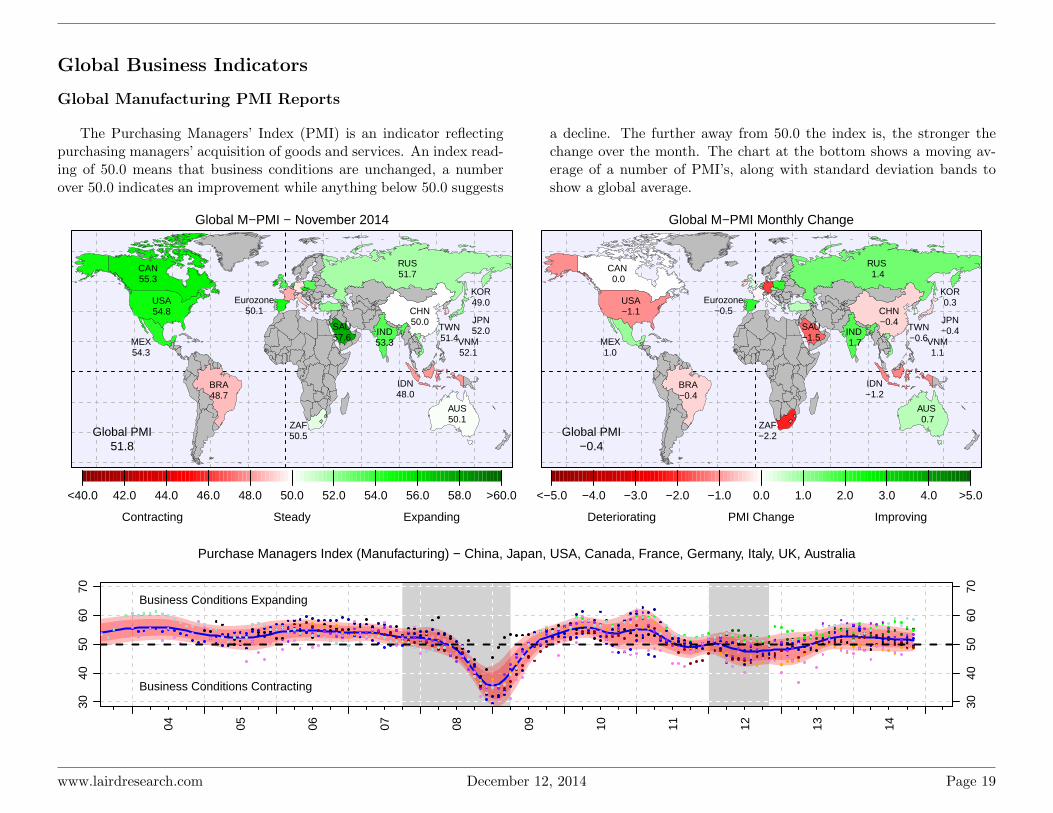

Global Manufacturing PMI Reports

The Purchasing Managers’ Index (PMI) is an indicator reflectingpurchasing managers’ acquisition of goods and services. An index read-ing of 50.0 means that business conditions are unchanged, a numberover 50.0 indicates an improvement while anything below 50.0 suggests

a decline. The further away from 50.0 the index is, the stronger thechange over the month. The chart at the bottom shows a moving av-erage of a number of PMI’s, along with standard deviation bands toshow a global average.

Global M−PMI − November 2014

<40.0 42.0 44.0 46.0 48.0 50.0 52.0 54.0 56.0 58.0 >60.0

Steady ExpandingContracting

Eurozone50.1

Global PMI51.8

TWN51.4MEX

54.3

KOR49.0

JPN52.0

VNM52.1

IDN48.0

ZAF50.5

AUS50.1

BRA48.7

CAN55.3

CHN50.0

IND53.3

RUS51.7

SAU57.6

USA54.8

Global M−PMI Monthly Change

<−5.0 −4.0 −3.0 −2.0 −1.0 0.0 1.0 2.0 3.0 4.0 >5.0

PMI Change ImprovingDeteriorating

Eurozone−0.5

Global PMI−0.4

TWN−0.6MEX

1.0

KOR0.3

JPN−0.4

VNM1.1

IDN−1.2

ZAF−2.2

AUS 0.7

BRA−0.4

CAN 0.0

CHN−0.4

IND 1.7

RUS 1.4

SAU−1.5

USA−1.1

Purchase Managers Index (Manufacturing) − China, Japan, USA, Canada, France, Germany, Italy, UK, Australia

04 05 06 07 08 09 10 11 12 13 14

3040

5060

70

3040

5060

70

Business Conditions Contracting

Business Conditions Expanding

www.lairdresearch.com December 12, 2014 Page 19

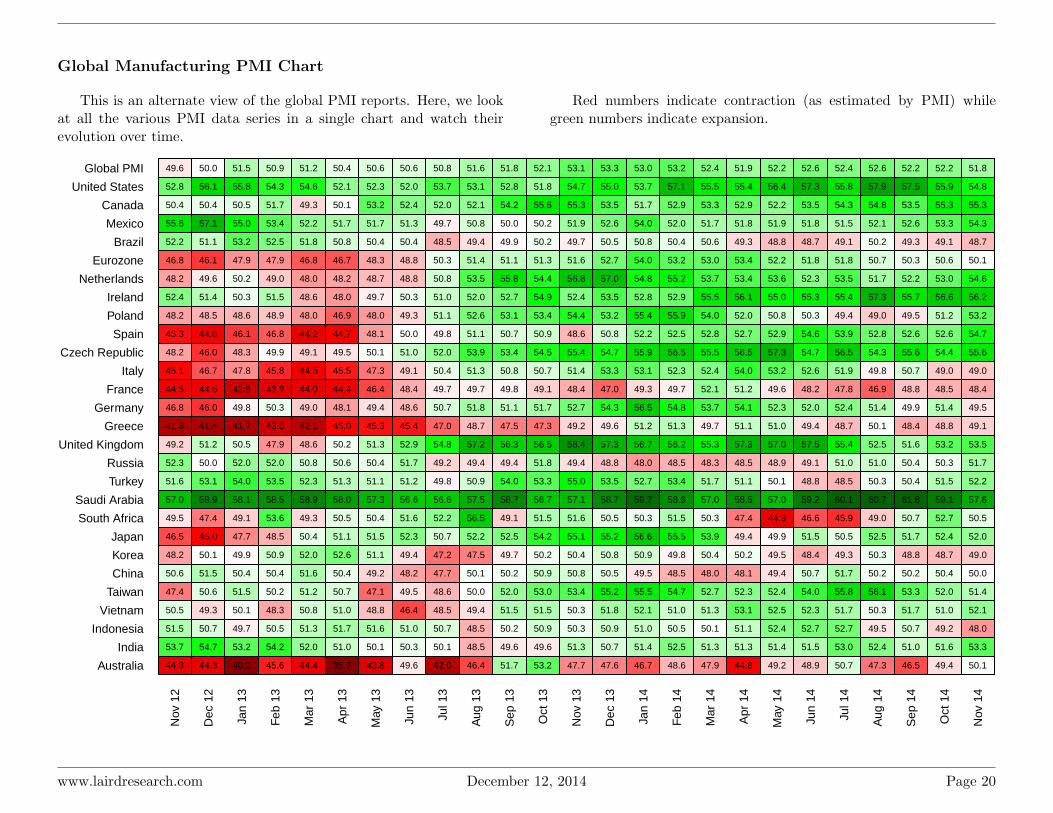

Global Manufacturing PMI Chart

This is an alternate view of the global PMI reports. Here, we lookat all the various PMI data series in a single chart and watch theirevolution over time.

Red numbers indicate contraction (as estimated by PMI) whilegreen numbers indicate expansion.

Nov

12

Dec

12

Jan

13

Feb

13

Mar

13

Apr

13

May

13

Jun

13

Jul 1

3

Aug

13

Sep

13

Oct

13

Nov

13

Dec

13

Jan

14

Feb

14

Mar

14

Apr

14

May

14

Jun

14

Jul 1

4

Aug

14

Sep

14

Oct

14

Nov

14

Australia

India

Indonesia

Vietnam

Taiwan

China

Korea

Japan

South Africa

Saudi Arabia

Turkey

Russia

United Kingdom

Greece

Germany

France

Italy

Czech Republic

Spain

Poland

Ireland

Netherlands

Eurozone

Brazil

Mexico

Canada

United States

Global PMI 49.6 50.0 51.5 50.9 51.2 50.4 50.6 50.6 50.8 51.6 51.8 52.1 53.1 53.3 53.0 53.2 52.4 51.9 52.2 52.6 52.4 52.6 52.2 52.2 51.8

52.8 56.1 55.8 54.3 54.6 52.1 52.3 52.0 53.7 53.1 52.8 51.8 54.7 55.0 53.7 57.1 55.5 55.4 56.4 57.3 55.8 57.9 57.5 55.9 54.8

50.4 50.4 50.5 51.7 49.3 50.1 53.2 52.4 52.0 52.1 54.2 55.6 55.3 53.5 51.7 52.9 53.3 52.9 52.2 53.5 54.3 54.8 53.5 55.3 55.3

55.6 57.1 55.0 53.4 52.2 51.7 51.7 51.3 49.7 50.8 50.0 50.2 51.9 52.6 54.0 52.0 51.7 51.8 51.9 51.8 51.5 52.1 52.6 53.3 54.3

52.2 51.1 53.2 52.5 51.8 50.8 50.4 50.4 48.5 49.4 49.9 50.2 49.7 50.5 50.8 50.4 50.6 49.3 48.8 48.7 49.1 50.2 49.3 49.1 48.7

46.8 46.1 47.9 47.9 46.8 46.7 48.3 48.8 50.3 51.4 51.1 51.3 51.6 52.7 54.0 53.2 53.0 53.4 52.2 51.8 51.8 50.7 50.3 50.6 50.1

48.2 49.6 50.2 49.0 48.0 48.2 48.7 48.8 50.8 53.5 55.8 54.4 56.8 57.0 54.8 55.2 53.7 53.4 53.6 52.3 53.5 51.7 52.2 53.0 54.6

52.4 51.4 50.3 51.5 48.6 48.0 49.7 50.3 51.0 52.0 52.7 54.9 52.4 53.5 52.8 52.9 55.5 56.1 55.0 55.3 55.4 57.3 55.7 56.6 56.2

48.2 48.5 48.6 48.9 48.0 46.9 48.0 49.3 51.1 52.6 53.1 53.4 54.4 53.2 55.4 55.9 54.0 52.0 50.8 50.3 49.4 49.0 49.5 51.2 53.2

45.3 44.6 46.1 46.8 44.2 44.7 48.1 50.0 49.8 51.1 50.7 50.9 48.6 50.8 52.2 52.5 52.8 52.7 52.9 54.6 53.9 52.8 52.6 52.6 54.7

48.2 46.0 48.3 49.9 49.1 49.5 50.1 51.0 52.0 53.9 53.4 54.5 55.4 54.7 55.9 56.5 55.5 56.5 57.3 54.7 56.5 54.3 55.6 54.4 55.6

45.1 46.7 47.8 45.8 44.5 45.5 47.3 49.1 50.4 51.3 50.8 50.7 51.4 53.3 53.1 52.3 52.4 54.0 53.2 52.6 51.9 49.8 50.7 49.0 49.0

44.5 44.6 42.9 43.9 44.0 44.4 46.4 48.4 49.7 49.7 49.8 49.1 48.4 47.0 49.3 49.7 52.1 51.2 49.6 48.2 47.8 46.9 48.8 48.5 48.4

46.8 46.0 49.8 50.3 49.0 48.1 49.4 48.6 50.7 51.8 51.1 51.7 52.7 54.3 56.5 54.8 53.7 54.1 52.3 52.0 52.4 51.4 49.9 51.4 49.5

41.8 41.4 41.7 43.0 42.1 45.0 45.3 45.4 47.0 48.7 47.5 47.3 49.2 49.6 51.2 51.3 49.7 51.1 51.0 49.4 48.7 50.1 48.4 48.8 49.1

49.2 51.2 50.5 47.9 48.6 50.2 51.3 52.9 54.8 57.2 56.3 56.5 58.4 57.3 56.7 56.2 55.3 57.3 57.0 57.5 55.4 52.5 51.6 53.2 53.5

52.3 50.0 52.0 52.0 50.8 50.6 50.4 51.7 49.2 49.4 49.4 51.8 49.4 48.8 48.0 48.5 48.3 48.5 48.9 49.1 51.0 51.0 50.4 50.3 51.7

51.6 53.1 54.0 53.5 52.3 51.3 51.1 51.2 49.8 50.9 54.0 53.3 55.0 53.5 52.7 53.4 51.7 51.1 50.1 48.8 48.5 50.3 50.4 51.5 52.2

57.0 58.9 58.1 58.5 58.9 58.0 57.3 56.6 56.6 57.5 58.7 56.7 57.1 58.7 59.7 58.6 57.0 58.5 57.0 59.2 60.1 60.7 61.8 59.1 57.6

49.5 47.4 49.1 53.6 49.3 50.5 50.4 51.6 52.2 56.5 49.1 51.5 51.6 50.5 50.3 51.5 50.3 47.4 44.3 46.6 45.9 49.0 50.7 52.7 50.5

46.5 45.0 47.7 48.5 50.4 51.1 51.5 52.3 50.7 52.2 52.5 54.2 55.1 55.2 56.6 55.5 53.9 49.4 49.9 51.5 50.5 52.5 51.7 52.4 52.0

48.2 50.1 49.9 50.9 52.0 52.6 51.1 49.4 47.2 47.5 49.7 50.2 50.4 50.8 50.9 49.8 50.4 50.2 49.5 48.4 49.3 50.3 48.8 48.7 49.0

50.6 51.5 50.4 50.4 51.6 50.4 49.2 48.2 47.7 50.1 50.2 50.9 50.8 50.5 49.5 48.5 48.0 48.1 49.4 50.7 51.7 50.2 50.2 50.4 50.0

47.4 50.6 51.5 50.2 51.2 50.7 47.1 49.5 48.6 50.0 52.0 53.0 53.4 55.2 55.5 54.7 52.7 52.3 52.4 54.0 55.8 56.1 53.3 52.0 51.4

50.5 49.3 50.1 48.3 50.8 51.0 48.8 46.4 48.5 49.4 51.5 51.5 50.3 51.8 52.1 51.0 51.3 53.1 52.5 52.3 51.7 50.3 51.7 51.0 52.1

51.5 50.7 49.7 50.5 51.3 51.7 51.6 51.0 50.7 48.5 50.2 50.9 50.3 50.9 51.0 50.5 50.1 51.1 52.4 52.7 52.7 49.5 50.7 49.2 48.0

53.7 54.7 53.2 54.2 52.0 51.0 50.1 50.3 50.1 48.5 49.6 49.6 51.3 50.7 51.4 52.5 51.3 51.3 51.4 51.5 53.0 52.4 51.0 51.6 53.3

44.3 44.3 40.2 45.6 44.4 36.7 43.8 49.6 42.0 46.4 51.7 53.2 47.7 47.6 46.7 48.6 47.9 44.8 49.2 48.9 50.7 47.3 46.5 49.4 50.1

www.lairdresearch.com December 12, 2014 Page 20

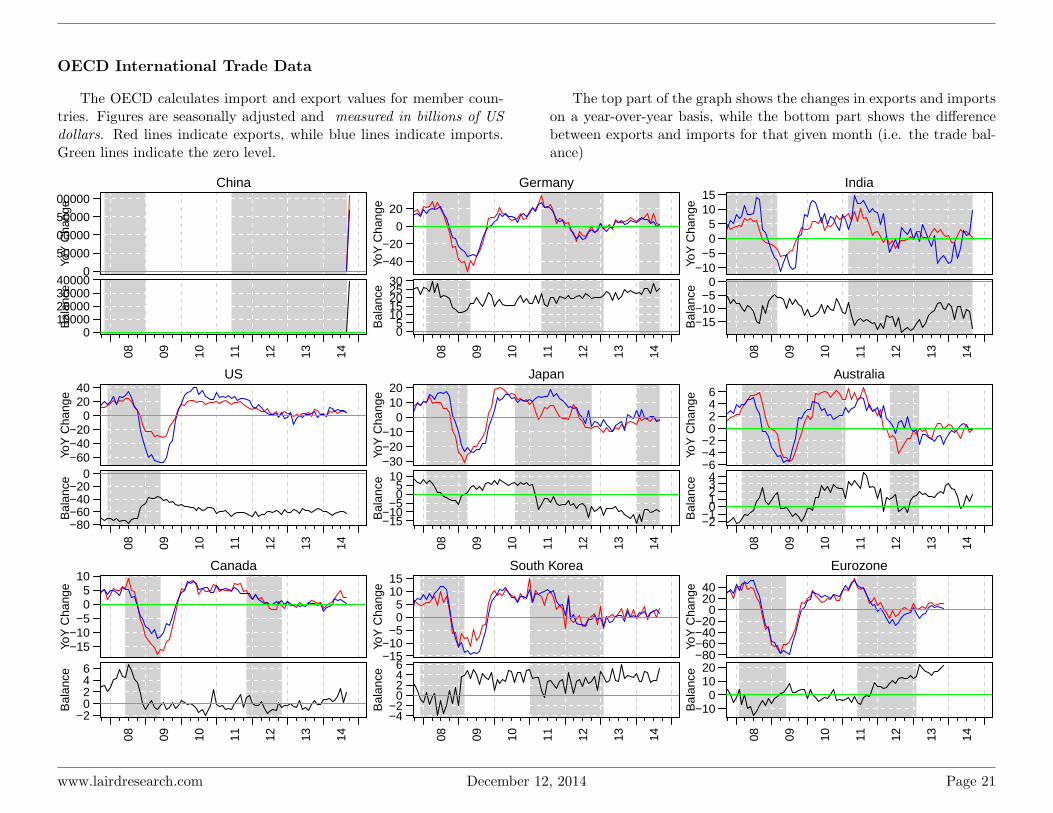

OECD International Trade Data

The OECD calculates import and export values for member coun-tries. Figures are seasonally adjusted and measured in billions of USdollars. Red lines indicate exports, while blue lines indicate imports.Green lines indicate the zero level.

The top part of the graph shows the changes in exports and importson a year-over-year basis, while the bottom part shows the differencebetween exports and imports for that given month (i.e. the trade bal-ance)

China

YoY

Cha

nge

0

50000

100000

150000

200000

Bal

ance

08 09 10 11 12 13 140

10000200003000040000

US

YoY

Cha

nge

−60−40−20

02040

Bal

ance

08 09 10 11 12 13 14

−80−60−40−20

0

Canada

YoY

Cha

nge

−15−10−5

05

10

Bal

ance

08 09 10 11 12 13 14

−20246

Germany

YoY

Cha

nge

−40

−20

0

20

Bal

ance

08 09 10 11 12 13 14

05

1015202530

JapanYo

Y C

hang

e

−30−20−10

01020

Bal

ance

08 09 10 11 12 13 14

−15−10−5

05

10

South Korea

YoY

Cha

nge

−15−10−5

05

1015

Bal

ance

08 09 10 11 12 13 14

−4−2

0246

India

YoY

Cha

nge

−10−5

05

1015

Bal

ance

08 09 10 11 12 13 14

−15−10−5

0

Australia

YoY

Cha

nge

−6−4−2

0246

Bal

ance

08 09 10 11 12 13 14

−2−1

01234

Eurozone

YoY

Cha

nge

−80−60−40−20

02040

Bal

ance

08 09 10 11 12 13 14

−100

1020

www.lairdresearch.com December 12, 2014 Page 21

Canadian Indicators

Retail Trade (SA)

YoY

Per

cent

Cha

nge

−5

05

10

median: 4.73Sep 2014: 4.53

Total Manufacturing Sales Growth

YoY

Per

cent

Gro

wth

−20

010

20

median: 4.21Sep 2014: 7.26

Manufacturing New Orders Growth

YoY

Per

cent

Gro

wth

−30

−10

010

2030

median: 4.58Sep 2014: 13.94

10yr Government Bond Yields

02

46

810

median: 5.78Nov 2014: 1.93

Manufacturing PMI

5051

5253

5455

Nov 2014: 55.30

Sales and New Orders (SA)

YoY

Per

cent

Cha

nge

−20

010

20

SalesNew Orders (smoothed)

Tbill Yield Spread (10 yr − 3mo)

Spr

ead

(Per

cent

)

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

−1

01

23

4

median: 1.35Nov 2014: 1.02

Inflation (total and core)

YoY

Per

cent

Cha

nge

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

−1

01

23

4

median: 1.97Oct 2014: 2.36

TotalCore

Inventory to Sales Ratio (SA)

Rat

io

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

1.3

1.4

1.5

1.6

median: 1.35Sep 2014: 1.34

www.lairdresearch.com December 12, 2014 Page 22

6.9 7.0 7.1 7.2 7.3 7.4 7.5 7.6

1.3

1.4

1.5

1.6

1.7

1.8

1.9

Beveridge Curve (Mar 2011 − Aug 2014)

Unemployment Rate

Vac

ancy

rat

e (I

ndus

tria

l)

Mar 2011 − Dec 2012Jan 2013 − Jul 2014Aug 2014

Ownership/Rental Price Ratio

Rat

io o

f Acc

omod

atio

n O

wne

rshi

p/R

ent R

atio

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

9010

011

012

013

014

015

0

CalgaryMontrealVancouverToronto

Note: Using prices relative to 2002 as base year

Ownership relatively moreexpensive vs 2002

Rent relatively more expensive vs 2002

Unemployment Rate (SA)

Per

cent

34

56

78

910

Canada 6.6%Alberta 4.5%Ontario 7.0%

Debt Service Ratios (SA)

Per

cent

46

810

Total Debt: 6.9%Mortgage: 3.5%Consumer Debt: 6.5%

Housing Starts and Building Permits (smoothed)

YoY

Per

cent

Cha

nge

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

−40

−20

020

40

PermitsStarts

www.lairdresearch.com December 12, 2014 Page 23

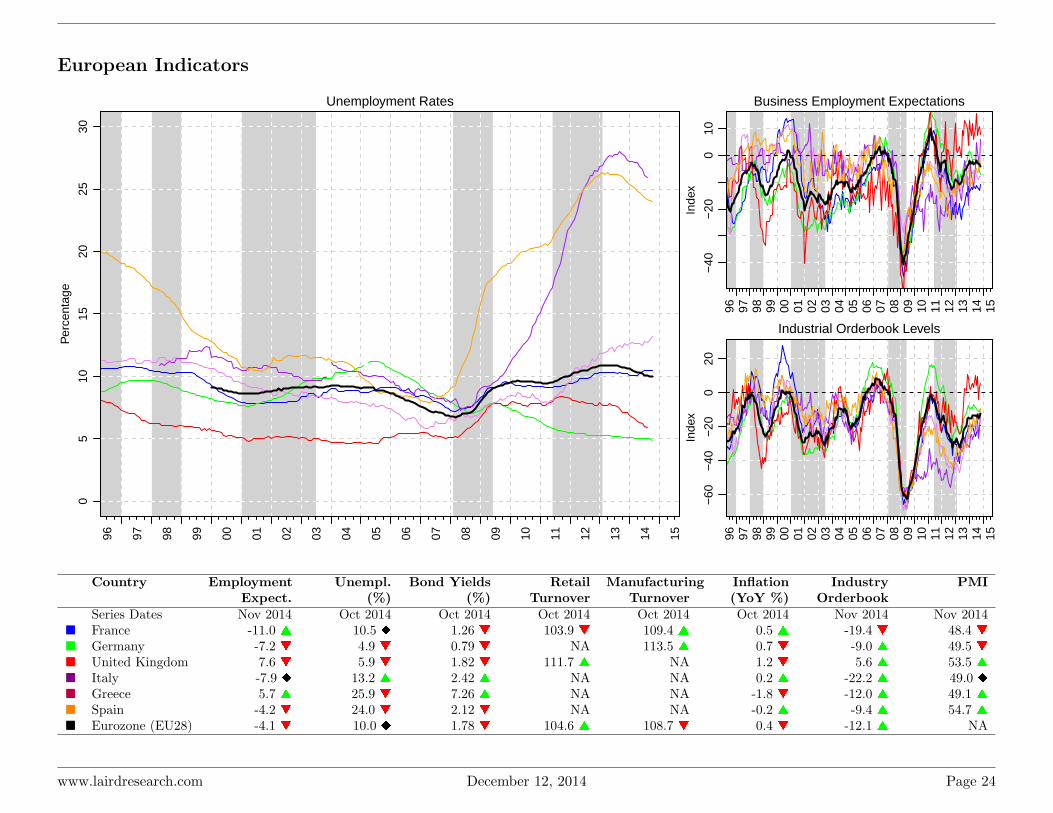

European Indicators

Unemployment Rates

Per

cent

age

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

05

1015

2025

30

Business Employment Expectations

Inde

x

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

−40

−20

010

Industrial Orderbook Levels

Inde

x

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

−60

−40

−20

020

Country EmploymentExpect.

Unempl.(%)

Bond Yields(%)

RetailTurnover

ManufacturingTurnover

Inflation(YoY %)

IndustryOrderbook

PMI

Series Dates Nov 2014 Oct 2014 Oct 2014 Oct 2014 Oct 2014 Oct 2014 Nov 2014 Nov 2014� France -11.0 s 10.5 u 1.26 t 103.9 t 109.4 s 0.5 s -19.4 t 48.4 t� Germany -7.2 t 4.9 t 0.79 t NA 113.5 s 0.7 t -9.0 s 49.5 t� United Kingdom 7.6 t 5.9 t 1.82 t 111.7 s NA 1.2 t 5.6 s 53.5 s� Italy -7.9 u 13.2 s 2.42 s NA NA 0.2 s -22.2 s 49.0 u� Greece 5.7 s 25.9 t 7.26 s NA NA -1.8 t -12.0 s 49.1 s� Spain -4.2 t 24.0 t 2.12 t NA NA -0.2 s -9.4 s 54.7 s� Eurozone (EU28) -4.1 t 10.0 u 1.78 t 104.6 s 108.7 t 0.4 t -12.1 s NA

www.lairdresearch.com December 12, 2014 Page 24

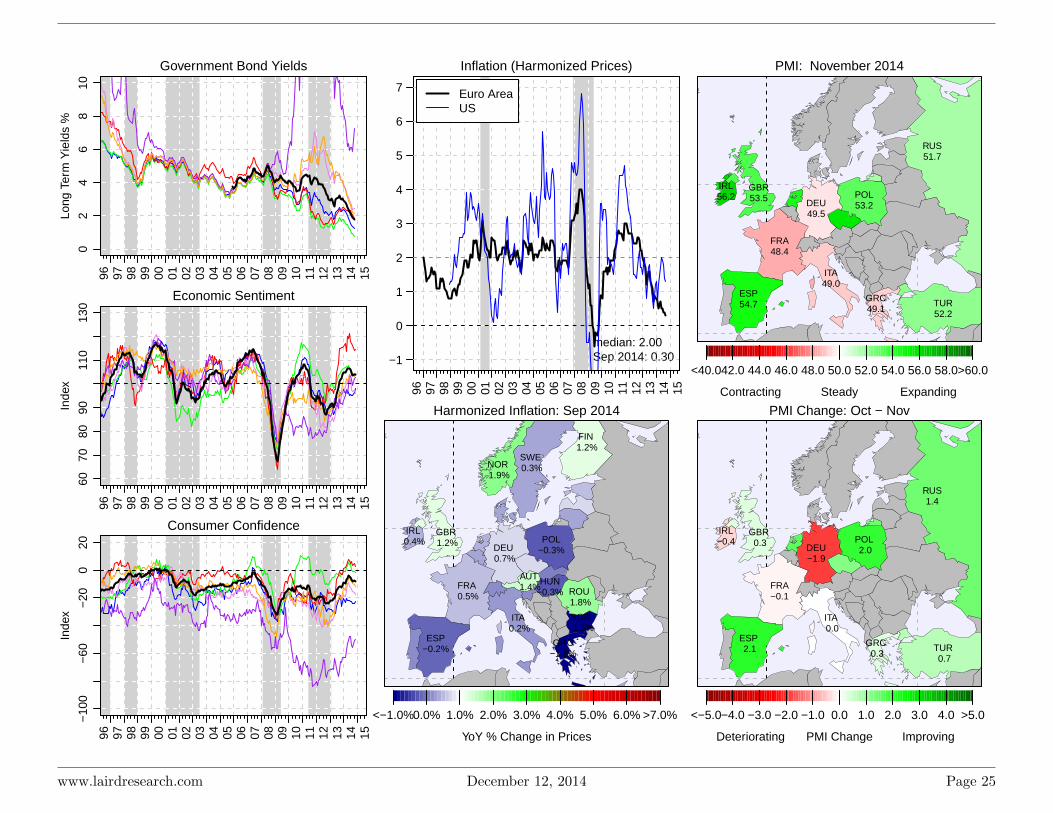

Government Bond YieldsLo

ng T

erm

Yie

lds

%

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

02

46

810

Economic Sentiment

Inde

x

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

6070

8090

110

130

Consumer Confidence

Inde

x

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

−10

0−

60−

200

20Inflation (Harmonized Prices)

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

median: 2.00Sep 2014: 0.30−1

0

1

2

3

4

5

6

7 Euro AreaUS

Harmonized Inflation: Sep 2014

AUT 1.4%

BGR−1.5%

DEU 0.7%

ESP−0.2%

FIN 1.2%

FRA 0.5%

GBR 1.2%

GRC−1.8%

HUN−0.3%

IRL 0.4%

ISL 1.0%

ITA 0.2%

NOR 1.9%

POL−0.3%

ROU 1.8%

SWE 0.3%

<−1.0%0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0% >7.0%

YoY % Change in Prices

PMI: November 2014

<40.042.0 44.0 46.0 48.0 50.0 52.0 54.0 56.0 58.0>60.0

Steady ExpandingContracting

BRA48.7

CAN55.3

DEU49.5

ESP54.7

FRA48.4

GBR53.5

GRC49.1

IRL56.2

ITA49.0

MEX54.3

POL53.2

SAU57.6

TUR52.2

USA54.8

RUS51.7

PMI Change: Oct − Nov

<−5.0−4.0 −3.0 −2.0 −1.0 0.0 1.0 2.0 3.0 4.0 >5.0

PMI Change ImprovingDeteriorating

CAN 0.0

DEU−1.9

ESP 2.1

FRA−0.1

GBR 0.3

GRC 0.3

IRL−0.4

ITA 0.0

POL 2.0

TUR 0.7

USA−1.1

RUS1.4

www.lairdresearch.com December 12, 2014 Page 25

Chinese Indicators

Tracking the Chinese economy is a tricky. As reported in the Fi-nancial Times, Premier Li Keqiang confided to US officials in 2007 thatgross domestic product was “man made” and “for reference only”. In-stead, he suggested that it was much more useful to focus on three alter-native indicators: electricity consumption, rail cargo volumes and bank

lending (still tracking down that last one). We also include the PMI- which is an official version put out by the Chinese government anddiffers slightly from an HSBC version. Finally we include the ShanghaiComposite Index as a measure of stock performance.

Manufacturing PMI

99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

4045

5055

60

Nov 2014: 50.00

Shanghai Composite Index

Inde

x V

alue

(M

onth

ly H

igh/

Low

)

99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

010

0030

0050

00

Dec 2014: NA

Electricity Generated

100

Mill

ion

KW

H (

log

scal

e)

99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

1000

2000

3000

5000

Sep 2014: 4542.00

Electricity GeneratedLong Term TrendShort Term Average

Consumer Confidence Index

Inde

x

99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

9810

010

210

410

610

8

median: 103.10Sep 2014: 105.40

Exports

YoY

Per

cent

Cha

nge

99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

−20

020

4060

80

median: 19.20Sep 2014: 15.30

Retail Sales Growth

YoY

Per

cent

Cha

nge

99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

1015

20

median: 13.10Sep 2014: 11.60

www.lairdresearch.com December 12, 2014 Page 26

Global Climate Change

Temperature and precipitation data are taken from the US NationalClimatic Data Center and presented as the average monthly anomalyfrom the previous 6 months. Anomalies are defined as the difference

from the average value over the period from 1961-1990 for precipitationand 1971-2000 for temperature.

Average Temperature Anomalies from May 2014 - Oct 2014

<−4.0 −3.0 −2.0 −1.0 0.0 1.0 2.0 3.0 >4.0Anomalies in Celcius WarmerCooler Anomalies in Celcius

−4 −2 0 2 4

Average 6 month Precipitation Anomalies from May 2014 - Oct 2014

<−40.0 −30.0 −20.0 −10.0 0.0 10.0 20.0 30.0 >40.0Anomalies in millimeters WetterDrier Anomalies in millimeters

−40 −20 0 20 40

www.lairdresearch.com December 12, 2014 Page 27