Embed Size (px)

Citation preview

Working capital issue

WORKING CAPITAL

• The capital of a business which is used in its day-to-day trading operations, calculated as the current assets minus the current liabilities.

Net Working CapitalCurrent Assets - Current Liabilities.

There are two concepts of working capital: Gross and Net.

Gross and net working capital

• Gross working capital- means the total current assets.

• Net working capital- can be defined in two ways-

o The difference between current assets and current liabilities.

o The portion of current assets which is financed with long term funds.

Working capital management

• Working capital management is concerned with the problems that arise in attempting to manage the current assets, the current liabilities and the interrelations that exist between them.

Current asset and current liabilities

• Current assets: refer to those assets which in the ordinary course of business can be, or will be, converted into cash within one year without undergoing a diminution in value and without disrupting the operations of the firm.

Examples- cash, marketable securities, accounts receivable and inventory.

• Current liabilities: are those liabilities which are intended, at their inception, to be paid in the ordinary course of business, within a year, out of the current assets or the earnings of the concern.

Examples- accounts payable, bills payable, bank overdraft and outstanding expenses.

Objective of Working Capital Management

• The goal of working capital management is to manage the firm’s current assets and liabilities in such a way that a satisfactory level of working capital is maintained.

• The interaction between current assets and current liabilities is, therefore the main theme of the theory of the working capital management.

Determinants of Working capital Requirement

• General nature of business• Production cycle• Business cycle fluctuations• Production policy• Credit policy• Growth and expansion• Profit level• Level of taxes• Dividend policy• Depreciation policy• Price level changes• Operating efficiency

The Operating-cycle and Working Capital Needs

• The working capital requirements of a firm depends, to a great extent upon the operating cycle of the firm. The operating cycle may be defined as the time duration starting from the procurement of goods or raw materials and ending with the sales realization.

• The length and nature of the operating cycle may differ from one firm to another depending upon the size and nature of the firm.

• The operating cycle of a firm consists of the time required for the completion of the chronological sequence of some or all of the following-

o Procurement of raw materials and services.o Conversion of raw materials into work-in-progress.o Conversion of work-in-progress into finished goods.o Sale of finished goods.o Conversion of receivables into cash.

Classifications of Working Capital

• Time– Permanent– Temporary

Components Cash, marketable securities,

receivables, and inventory

Types of working capital needs

• The working capital need can be divided into permanent working capital and temporary working capital.

• Permanent working capital- There is always a minimum level of working capital which is continuously required by a firm in order to maintain its activities like cash, stock and other current assets in order to meet its business requirements irrespective of the level of operations.

• Temporary working capital- Over and above the permanent working capital, the firm may also require additional working capital in order to meet the requirements arising out of fluctuations in sales volume. This extra working capital needed to support the increased volume of sales is known as temporary or fluctuating working capital.

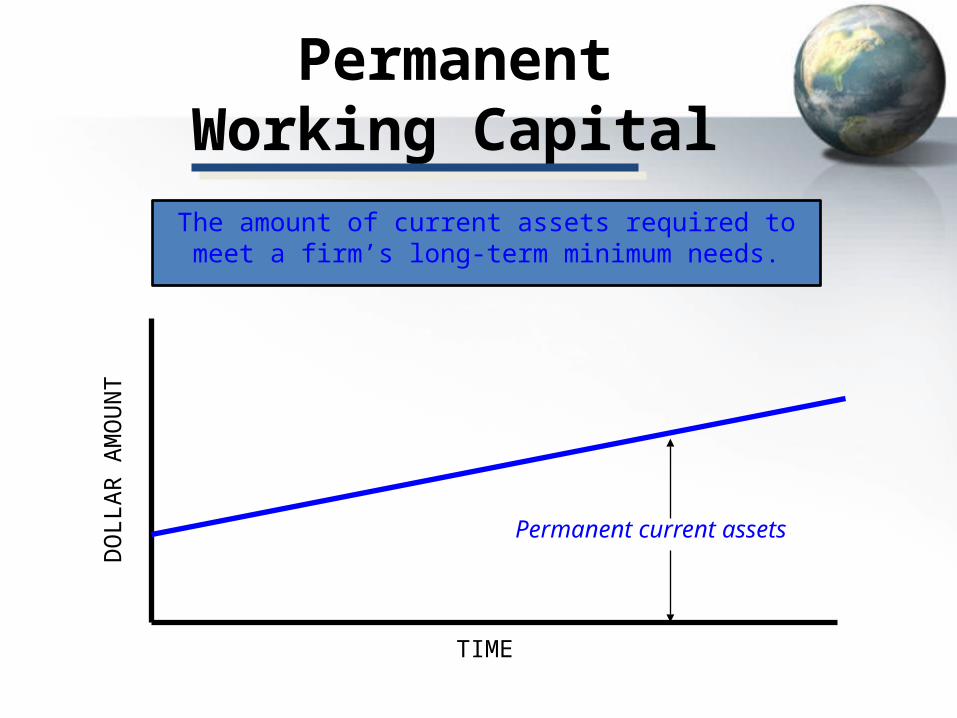

Permanent Working Capital

The amount of current assets required to meet a firm’s long-term minimum needs.

Permanent current assets

TIME

DO

LLAR

AM

OU

NT

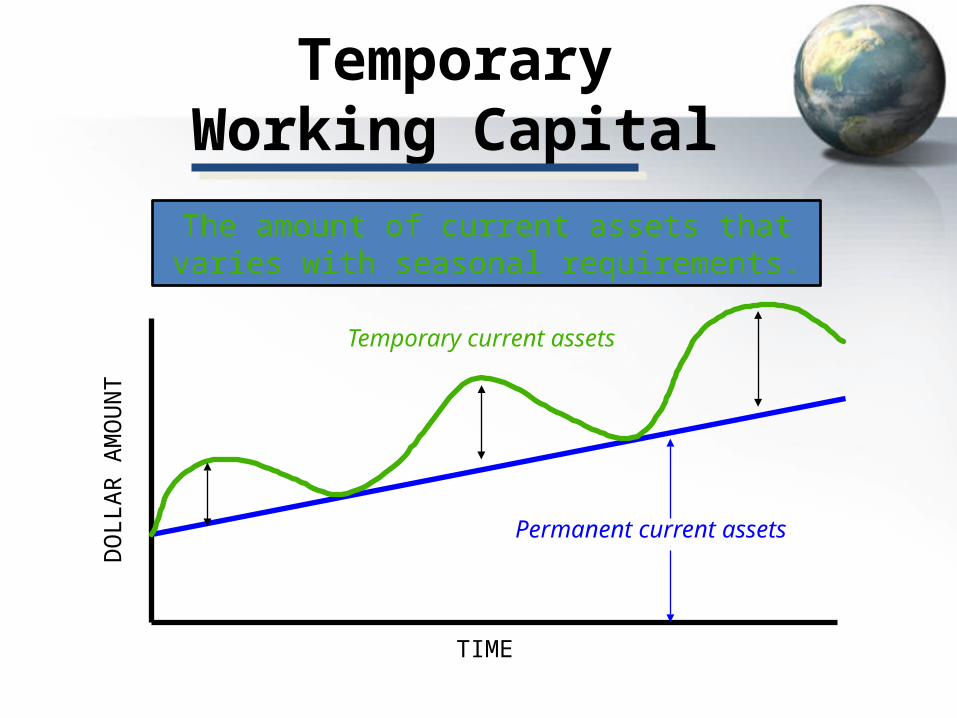

Temporary Working Capital

The amount of current assets that varies with seasonal requirements.

Permanent current assets

TIME

DO

LLAR

AM

OU

NT

Temporary current assets

Significance of Working Capital Management

• In a typical manufacturing firm, current assets exceed one-half of total assets.

• Excessive levels can result in a substandard Return on Investment (ROI).

• Current liabilities are the principal source of external financing for small firms.

• Requires continuous, day-to-day managerial supervision.

• Working capital management affects the company’s risk, return, and share price.

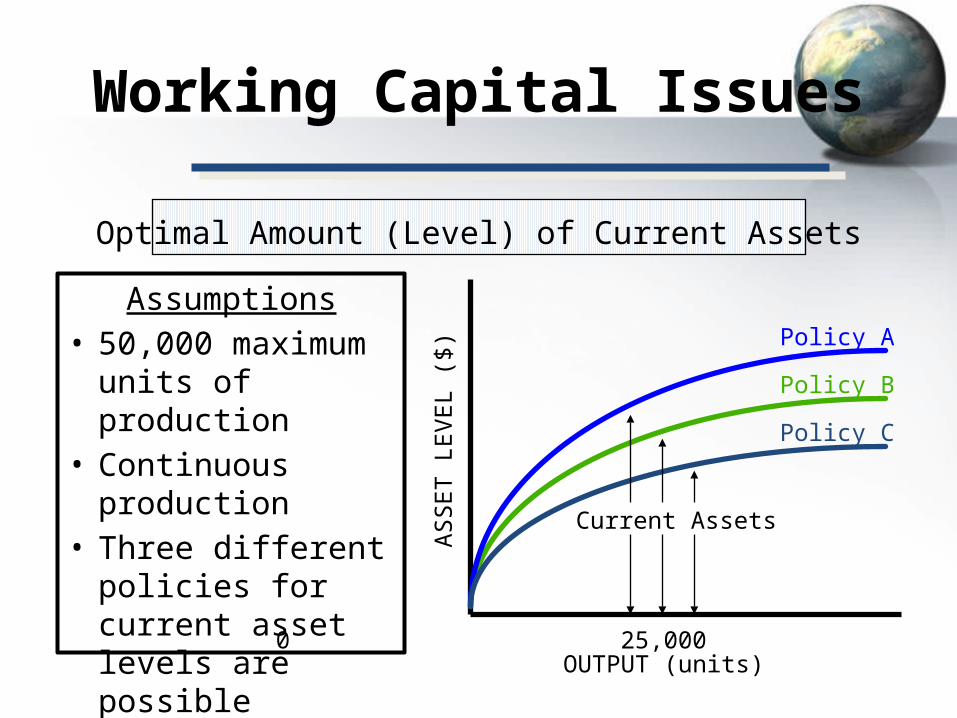

Working Capital Issues

Assumptions• 50,000 maximum units

of production• Continuous production• Three different

policies for current asset levels are possible

Optimal Amount (Level) of Current Assets

0 25,000 50,000OUTPUT (units)

ASSE

T LE

VEL

($)

Current Assets

Policy C

Policy A

Policy B

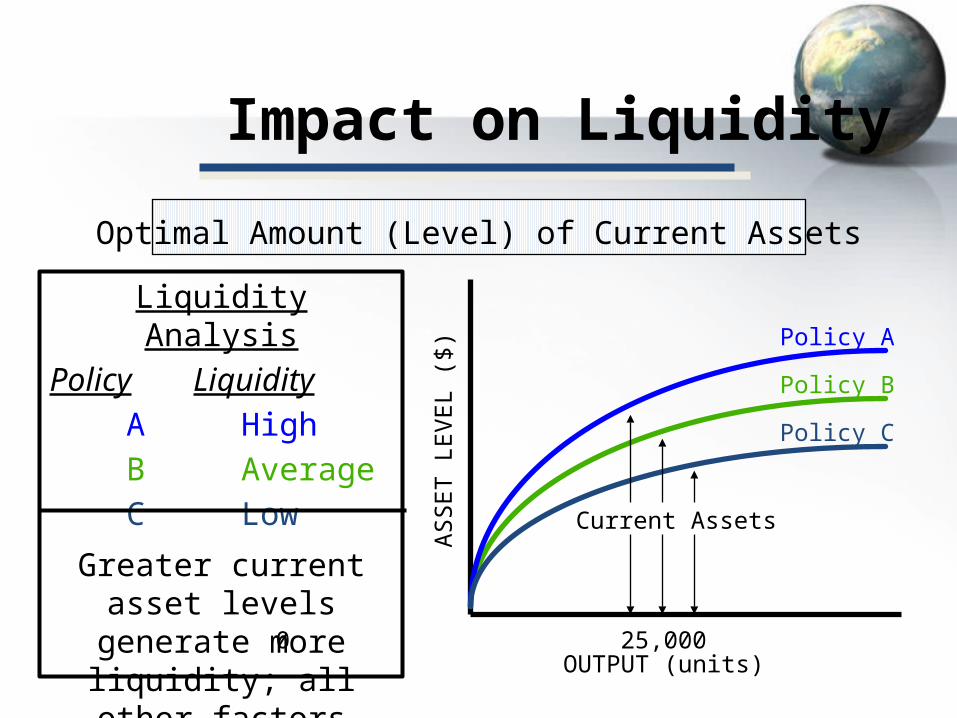

Impact on Liquidity

Liquidity AnalysisPolicy Liquidity A High B Average C Low

Greater current asset levels generate more

liquidity; all other factors held constant.

Optimal Amount (Level) of Current Assets

0 25,000 50,000OUTPUT (units)

ASSE

T LE

VEL

($)

Current Assets

Policy C

Policy A

Policy B

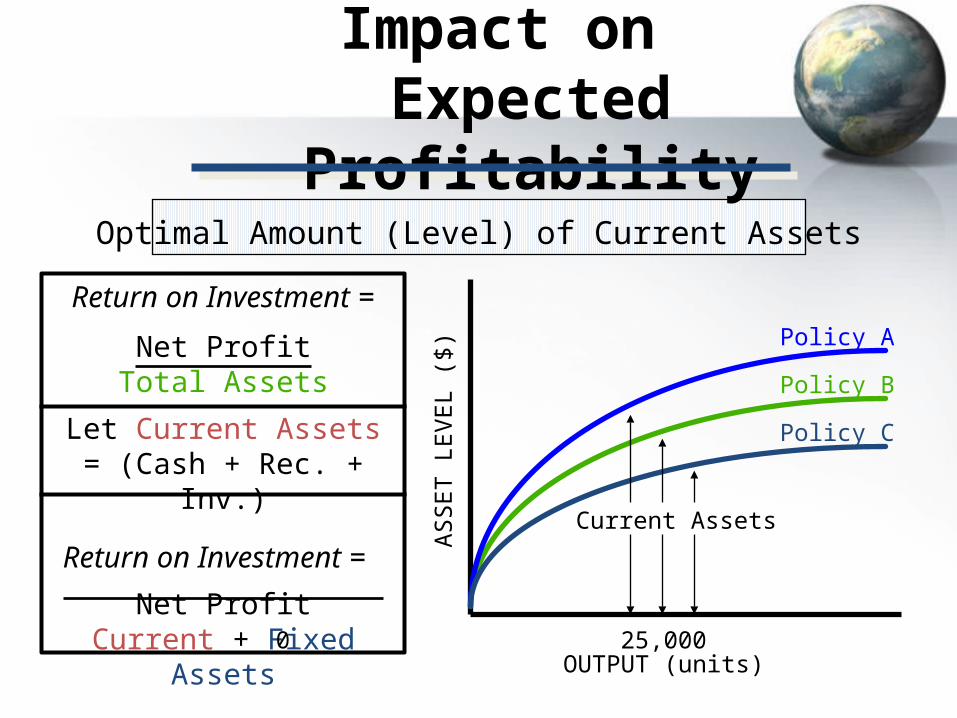

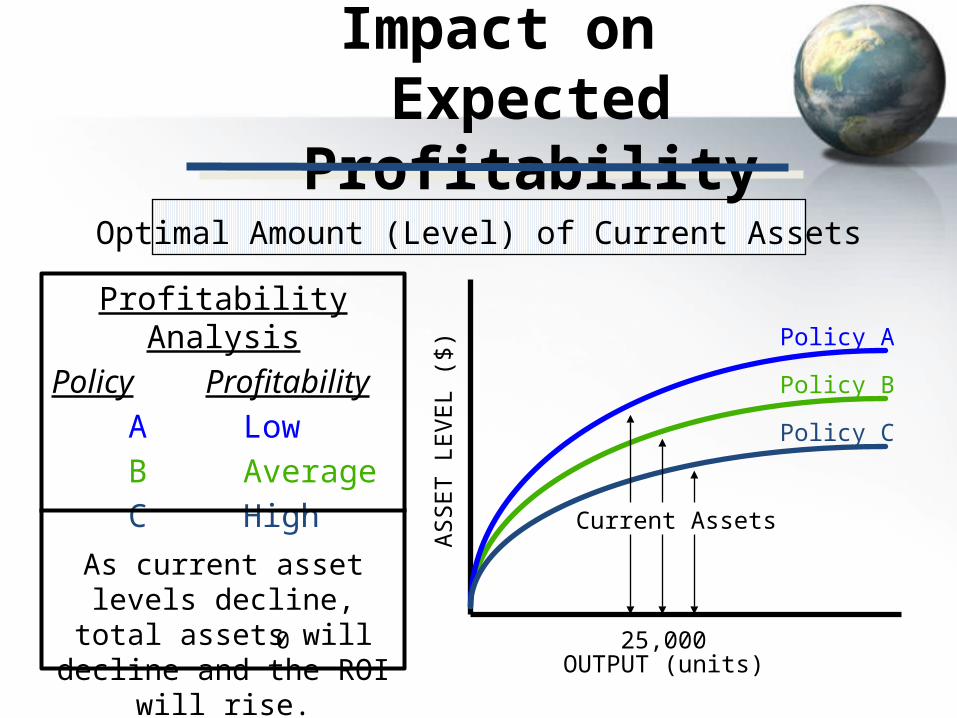

Impact on Expected Profitability

Return on Investment =

Net ProfitTotal Assets

Let Current Assets = (Cash + Rec. + Inv.)

Return on Investment =

Net ProfitCurrent + Fixed Assets

Optimal Amount (Level) of Current Assets

0 25,000 50,000OUTPUT (units)

ASSE

T LE

VEL

($)

Current Assets

Policy C

Policy A

Policy B

Impact on Expected Profitability

Profitability AnalysisPolicy Profitability A Low B Average C High

As current asset levels decline, total assets will

decline and the ROI will rise.

Optimal Amount (Level) of Current Assets

0 25,000 50,000OUTPUT (units)

ASSE

T LE

VEL

($)

Current Assets

Policy C

Policy A

Policy B

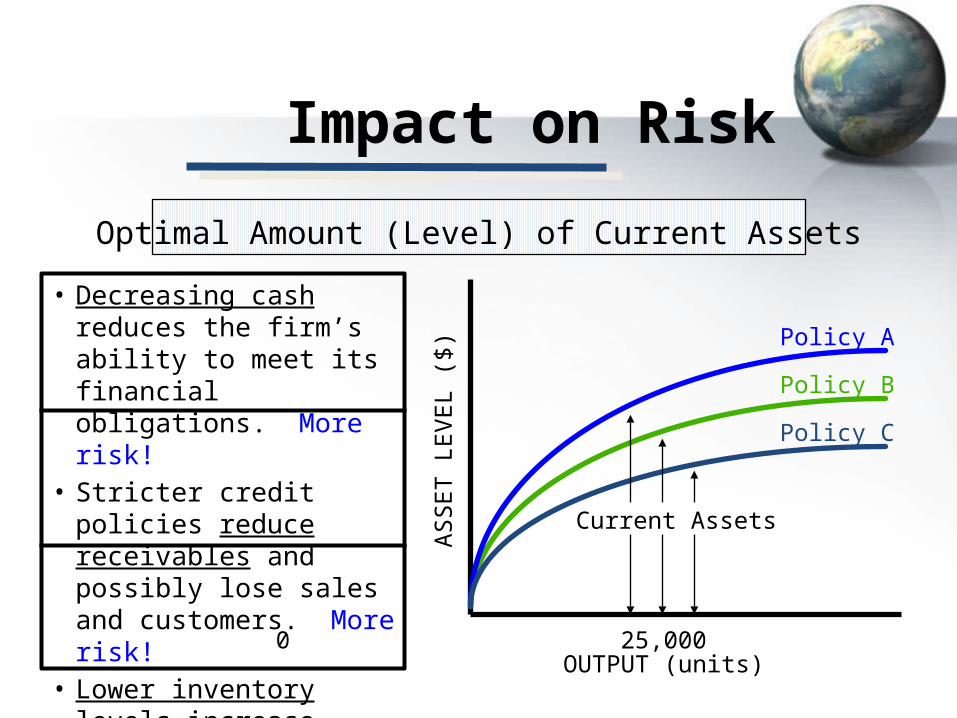

Impact on Risk

• Decreasing cash reduces the firm’s ability to meet its financial obligations. More risk!

• Stricter credit policies reduce receivables and possibly lose sales and customers. More risk!

• Lower inventory levels increase stockouts and lost sales. More risk!

Optimal Amount (Level) of Current Assets

0 25,000 50,000OUTPUT (units)

ASSE

T LE

VEL

($)

Current Assets

Policy C

Policy A

Policy B

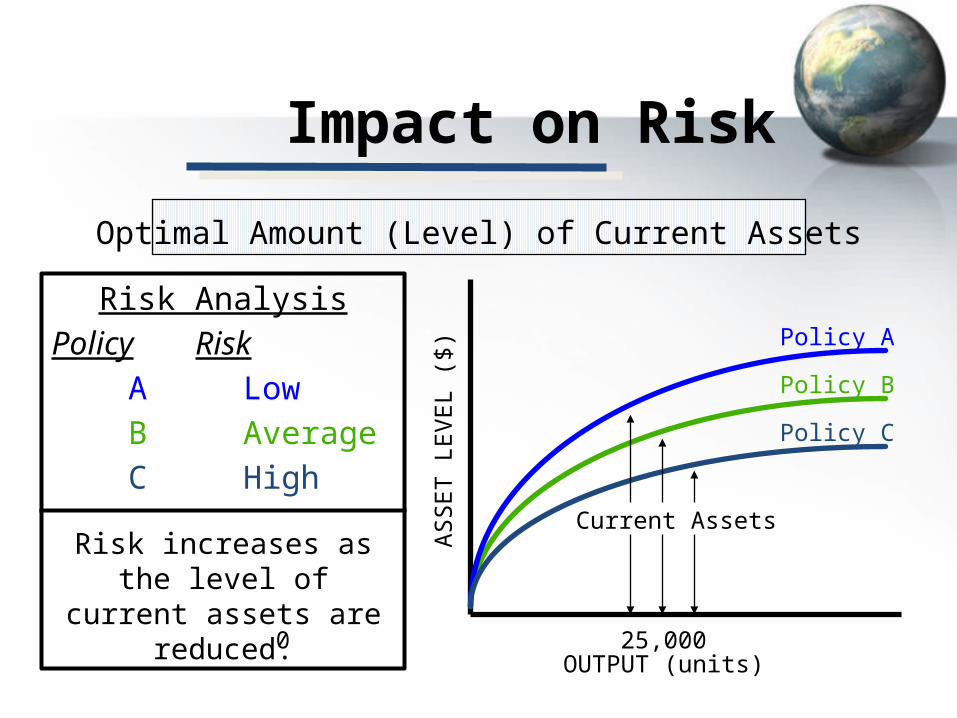

Impact on Risk

Risk AnalysisPolicy Risk A Low B Average C High

Risk increases as the level of current assets are reduced.

Optimal Amount (Level) of Current Assets

0 25,000 50,000OUTPUT (units)

ASSE

T LE

VEL

($)

Current Assets

Policy C

Policy A

Policy B

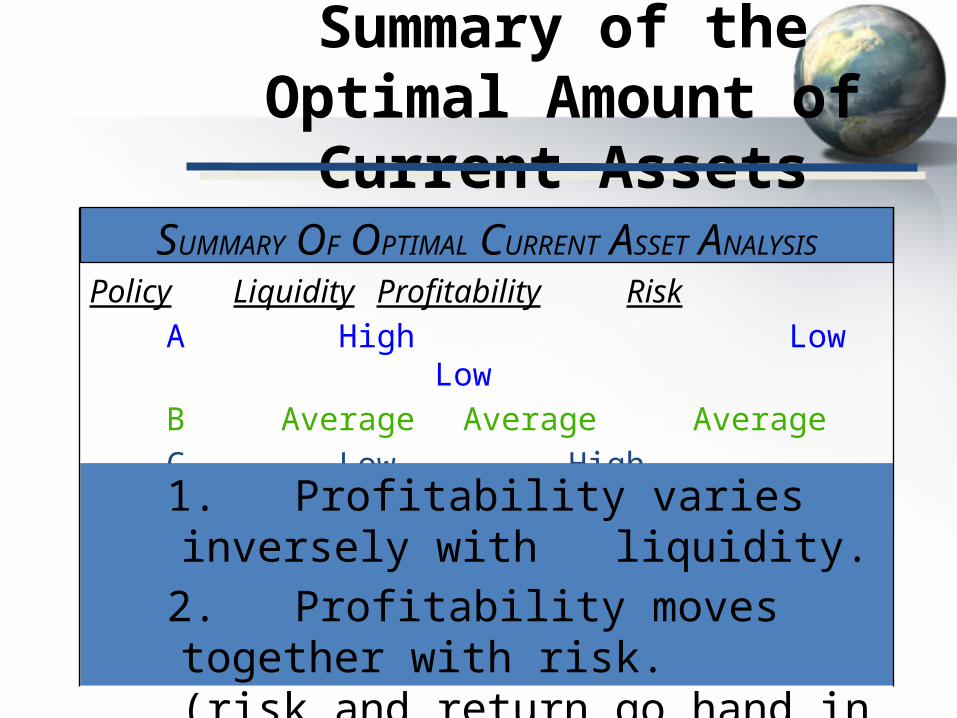

Summary of the Optimal Amount of Current Assets

SUMMARY OF OPTIMAL CURRENT ASSET ANALYSIS

Policy Liquidity Profitability Risk A High Low Low B Average Average Average C Low High High

1. Profitability varies inversely with liquidity.

2. Profitability moves together with risk.(risk and return go hand in hand!)

Current asset working capital

• For instance, if the owner makes an additional investment of $20,000 in her company, the company's total current assets will increase by $20,000 but there is no increase in its current liabilities. As a result, the company's working capital increases by $20,000. (The other change is an increase in the owner's capital account.)

Current asset working capital

Current asset working capital

• If a company borrows $50,000 and agrees to repay the loan in 90 days, the company's working capital has not increased. The reason is that the current asset Cash increased by $50,000 and the current liability Loans Payable also increased by $50,000.

Current asset working capital

• The use of $30,000 to buy merchandise for inventory will not change the amount of working capital. The reason is that the total amount of current assets will not change. The current asset Cash decreases by $30,000 and the current asset Inventory increases by $30,000.

Current asset working capital

• If a company sells a product for $3,400 which is in its inventory at a cost of $2,500 the company's working capital will increase by $900. Working capital increased because 1) the current asset accounts Cash or Accounts Receivable will increase by $3,400 and Inventory will decrease by $2,500; 2) current liabilities will not change. Owner's equity will increase by $900.

Current liability working capital

• Payment made to creditors causes decrease in current assets and also decrease in current liability but not affect working capital.

• Bank overdraft paid by issue of preference shares cause decrease in current liability but increase in non current liability.

Current liability working capital

• Bank over draft to redeem debenture causes an increase in current liability but also decrease non current liability.

• If a company borrows $50,000 and agrees to repay the loan in 90 days, the company's working capital has not increased. The reason is that the current asset Cash increased by $50,000 and the current liability Loans Payable also increased by $50,000.

Financing current assets and short term and long term mix

What is financing?

• Financing is defined as a means of obtaining the resources to purchase an item, then paying back the loan in a set time period for a set monthly, weekly, yearly.

What is short term financing

• Arranging of available External funds to meet the needs of a firm for a year or less time.

Why Do Firms Need Short-term Financing

Cash flow from operations may not be sufficient to keep up with growth-related financing needs.

Firms may prefer to borrow now for their inventory or other short term asset needs rather than wait until they have saved enough.

Firms may prefer short-term financing instead of long-term sources of financing.

Sources for short term financing

Trade credit Accrued expenses Bank financing Factoring Commercial paper

1.Trade credit

It is a credit that a customer gets from supplier of goods.

It is the spontaneous source of financing. In this the buying firm don’t pay immediately. Deferral of payments is a short- term

financing called “Trade Credit.”

2. Accrued expenses

• It represents the liability that a firm has to pay for those services which have been received earlier.

Accrued wages and salaries Accrued taxes and interest

3.Bank financing

Bank overdraft Cash credit Purchase and discounting of bills Short term loan Letter of credit

4. Commercial paper

• It is unsecured money market instruments issued in the form of a promissory note.

It was introduced in India in 1990. RBI regulates the Commercial paper. Corporates, primary dealers, Indian financial

institution are eligible to issue it. A corporate firm can be eligible to offer a

Commercial paper if it has the value of 10 crore. Maturity of Cp in india is 91 to 180 days.

5.Factoring

It is financial transaction where a firm sells its account receivable to any third party.

It emphasizes on the receivable financial assets

It involves the purchase of financial assetsIt involves three parties Period for factoring is 90 to 150 days.

Sources for long term financing

The main sources of long term finance are as follows:1. Shares: These are issued to the general public. These may be

of two types: (i)Equity & (ii)Preference. The holders of shares are the owners of the business.

2. Debentures: These are also issued to the general public. The holders of debentures are the creditors of the company.

3. Public Deposits :General public also like to deposit their savings with popular and well established company which can pay interest periodically and pay-back the deposit when due.

.

4. Retained earnings: The company may not distribute the whole of its

profits among its shareholders. It may retain a part of the profits and utilize it as capital

5. Term loans from banks: Many industrial development banks, cooperative banks

and commercial banks grant medium term loans for a period of three to five years.

6. Loan from financial institutions: There are many specialized financial institutions

established by the Central and State governments which give long term loans at reasonable rate of interest.

Financing Current Assets: Short-Term and Long-Term Mix

Spontaneous Financing: Trade credit, and other payables and accruals, that arise spontaneously in the firm’s day-to-day operations.

– Based on policies regarding payment for purchases, labor, taxes, and other expenses.

– We are concerned with managing non-spontaneous financing of assets.

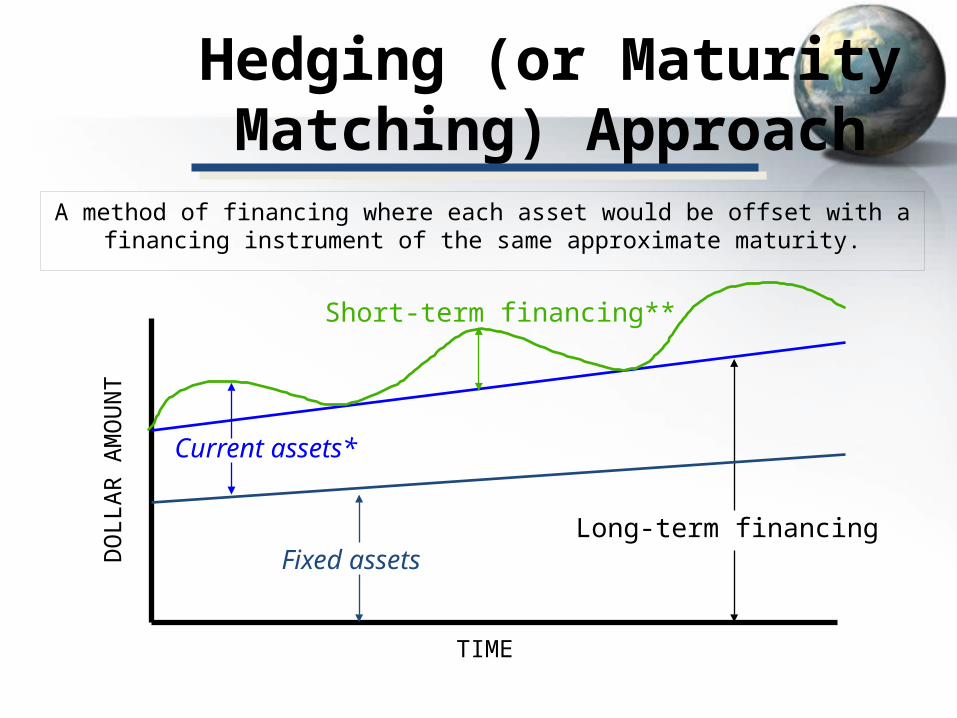

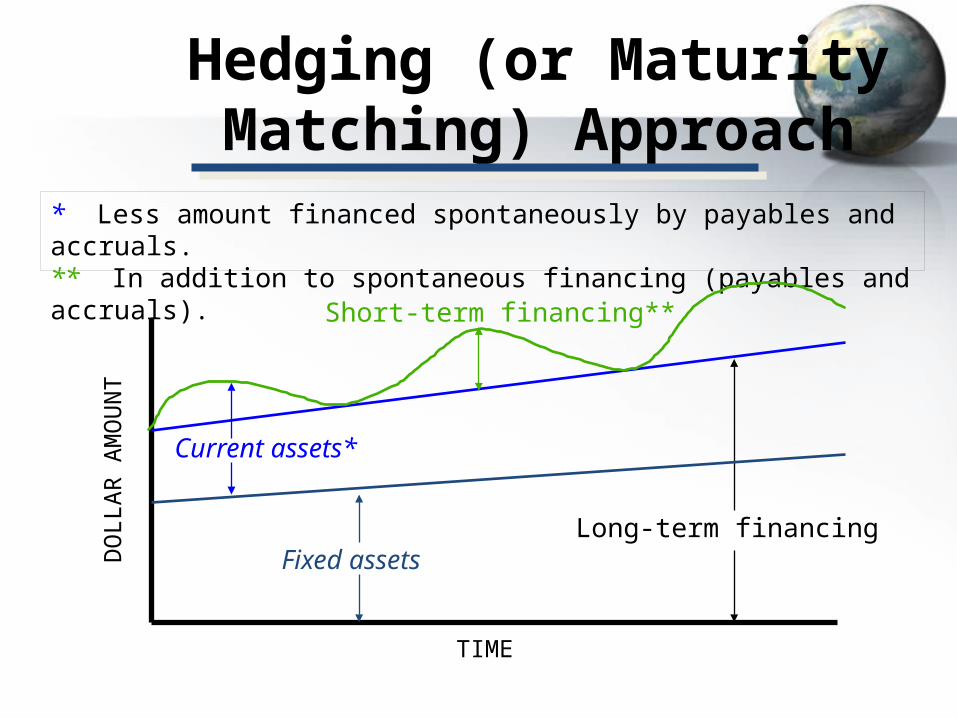

Hedging (or Maturity Matching) Approach

A method of financing where each asset would be offset with a financing instrument of the same approximate maturity.

TIME

DO

LLAR

AM

OU

NT

Long-term financingFixed assets

Current assets*

Short-term financing**

Hedging (or Maturity Matching) Approach

* Less amount financed spontaneously by payables and accruals.** In addition to spontaneous financing (payables and accruals).

TIME

DO

LLAR

AM

OU

NT

Long-term financingFixed assets

Current assets*

Short-term financing**

Financing Needs and the Hedging Approach

• Fixed assets and the non-seasonal portion of current assets are financed with long-term debt and equity (long-term profitability of assets to cover the long-term financing costs of the firm).

• Seasonal needs are financed with short-term loans (under normal operations sufficient cash flow is expected to cover the short-term financing cost).

Self-Liquidating Nature of Short-Term Loans

• Seasonal orders require the purchase of inventory beyond current levels.

• Increased inventory is used to meet the increased demand for the final product.

• Sales become receivables.• Receivables are collected and become cash.• The resulting cash funds can be used to pay off the

seasonal short-term loan and cover associated long-term financing costs.

Risks vs. Costs Trade-Off (Conservative Approach)

• Long-Term Financing Benefits– Less worry in refinancing short-term obligations– Less uncertainty regarding future interest costs

• Long-Term Financing Risks– Borrowing more than what is necessary– Borrowing at a higher overall cost (usually)

• Result– Manager accepts less expected profits in exchange for

taking less risk.

Risks vs. Costs Trade-Off (Conservative Approach)

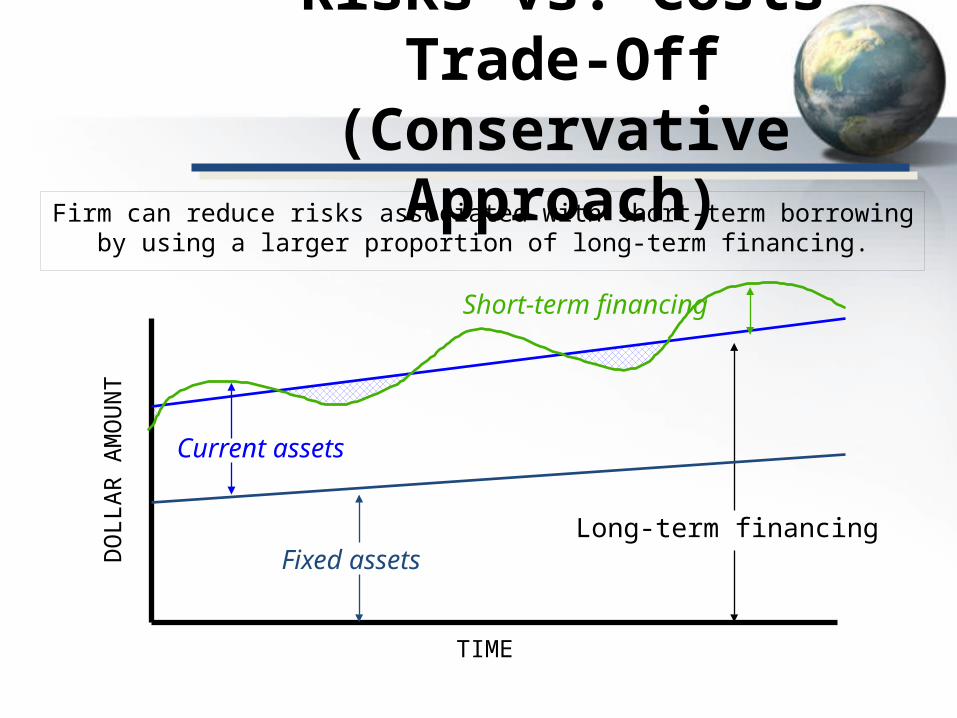

Firm can reduce risks associated with short-term borrowing by using a larger proportion of long-term financing.

TIME

DO

LLAR

AM

OU

NT

Long-term financingFixed assets

Current assets

Short-term financing

Comparison with an Aggressive Approach

• Short-Term Financing Benefits– Financing long-term needs with a lower interest cost than

short-term debt– Borrowing only what is necessary

• Short-Term Financing Risks– Refinancing short-term obligations in the future– Uncertain future interest costs

• Result– Manager accepts greater expected profits in exchange for

taking greater risk.

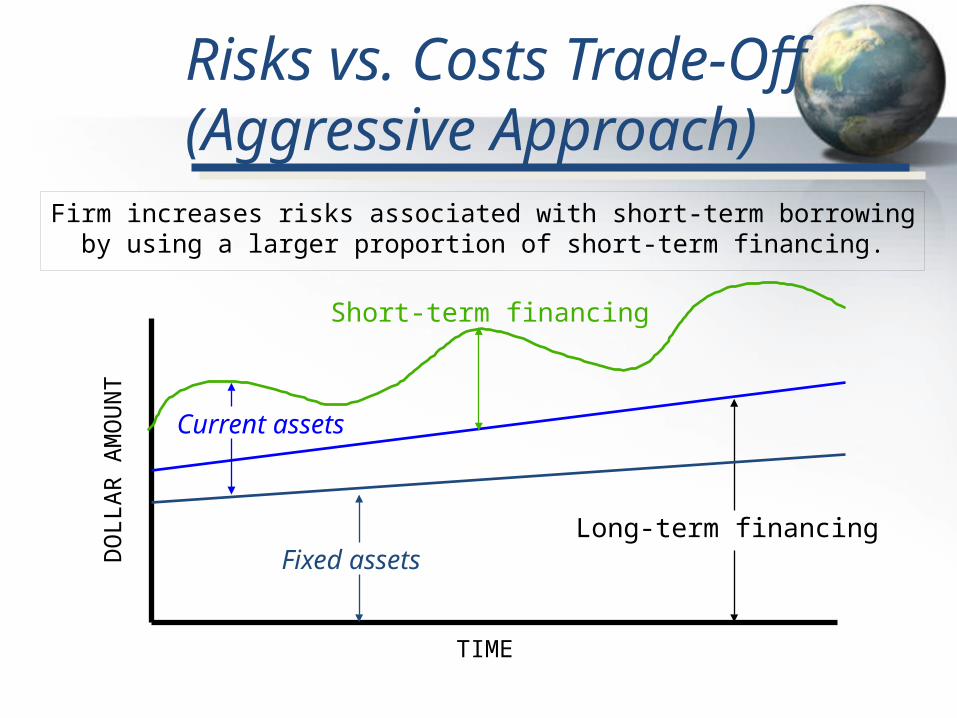

Firm increases risks associated with short-term borrowing by using a larger proportion of short-term financing.

TIME

DO

LLAR

AM

OU

NT

Long-term financingFixed assets

Current assets

Short-term financing

Risks vs. Costs Trade-Off (Aggressive Approach)

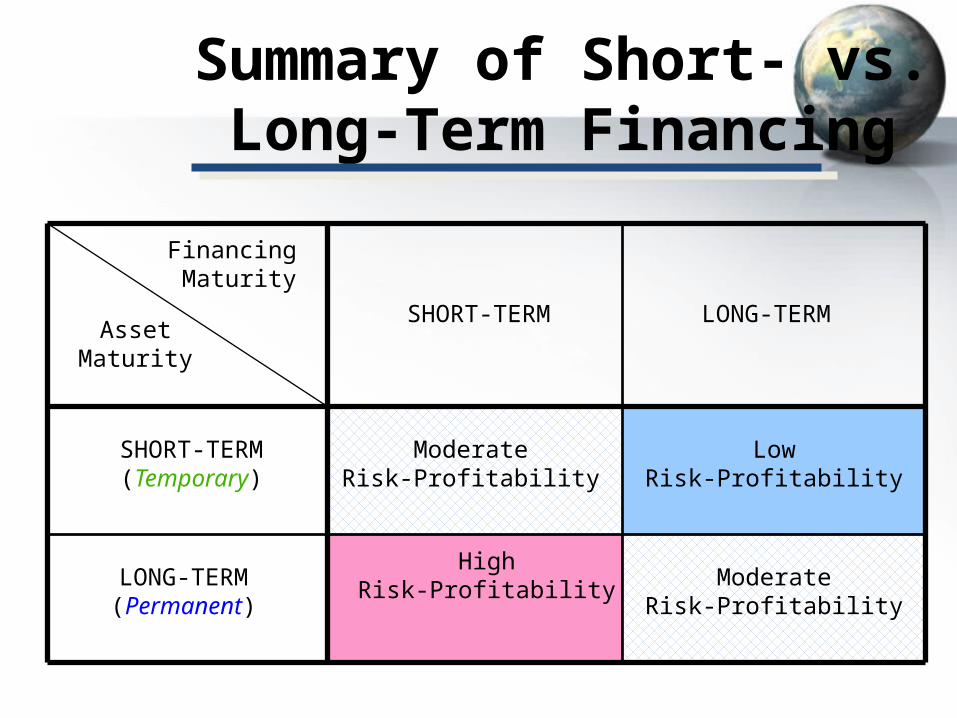

Summary of Short- vs. Long-Term Financing

Financing Maturity

AssetMaturity

SHORT-TERM LONG-TERM

LowRisk-Profitability

ModerateRisk-Profitability

ModerateRisk-Profitability

HighRisk-Profitability

SHORT-TERM(Temporary)

LONG-TERM(Permanent)

Motives for holding cash

WHAT IS CASH?

• In narrow sense: currency and generally accepted equivalents of cash like cheques, drafts etc.

• In broad sense: includes near-cash assets, such as marketable securities and time deposits in banks.– They can be readily sold and converted into cash.– Can serve as a reserve pool of liquidity.– Also provide short term investment outlet for excess cash.

Motives for holding cash

• Transaction motive• Precautionary motive• Speculative motive • compensating motive

Transaction motive

• Holding of cash to meet routine cash requirements to finance the transactions which a firm carries on in the ordinary course of business.

Precautionary motive

• The cash balances held in reserve for random and unforeseen fluctuations in cash flows.

• A cushion to meet unexpected contingencies.– Floods, strikes and failure of imp customers– Unexpected slowdown in collection of accounts receivable– Sharp increase in cost of raw materials– Cancellation of some order of goods

• Defensive in nature

Speculative motive

• Is a motive for holding cash/near-cash to quickly take advantage of opportunities typically outside the normal course of business.

• Positive and aggressive approach• Helps to take advantage of:– An opportunity to purchase raw materials at reduced price– Make purchase at favorable prices– Delay purchase on anticipation of decline in prices– Buying securities when interest rate is expected to decline

Compensating motive

• Is a motive for holding cash/near-cash to compensate banks for providing certain services or loans.

• Clients are supposed to maintain a minimum balance of cash at the bank which they cannot use themselves.

Speeding up cash receipts and slowing down cash payments

Speeding Up Cash Receipts

• Expedite preparing and mailing the invoice• Accelerate the mailing of payments from

customers• Reduce the time during which payments received

by the firm remain uncollected

Collections

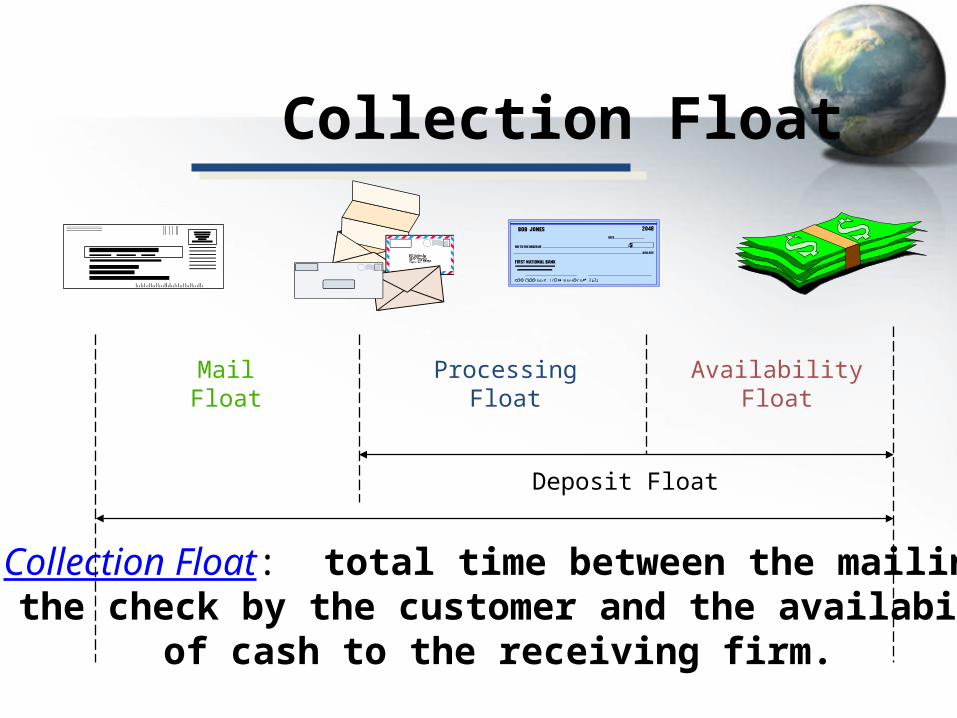

Collection Float

Collection Float: total time between the mailingof the check by the customer and the availability

of cash to the receiving firm.

ProcessingFloat

AvailabilityFloat

MailFloat

Deposit Float

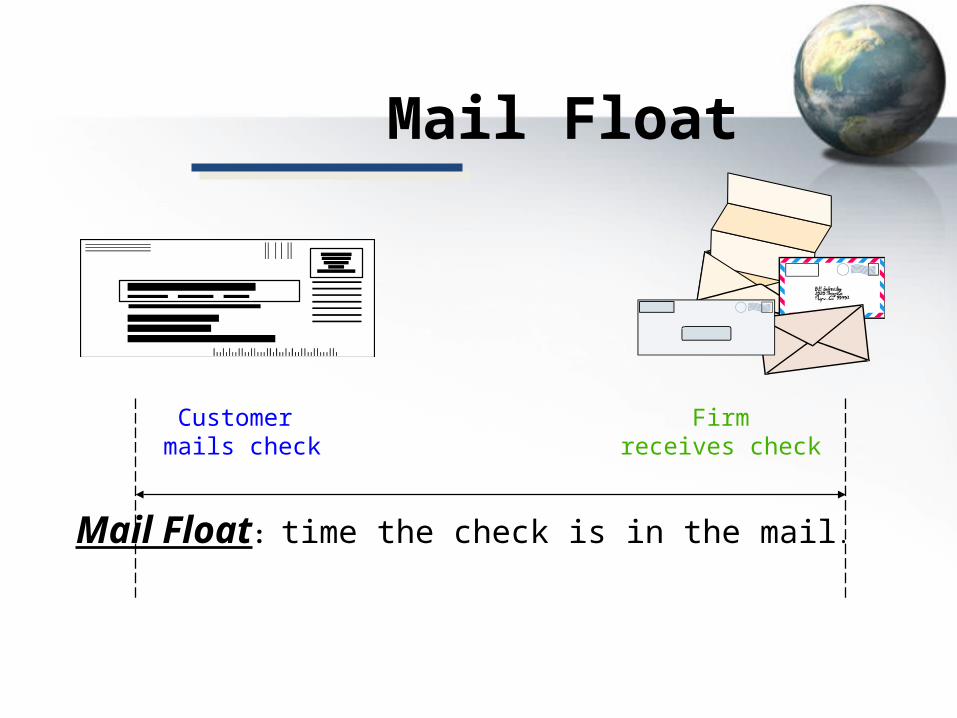

Mail Float

Mail Float: time the check is in the mail.

Customer mails check

Firmreceives check

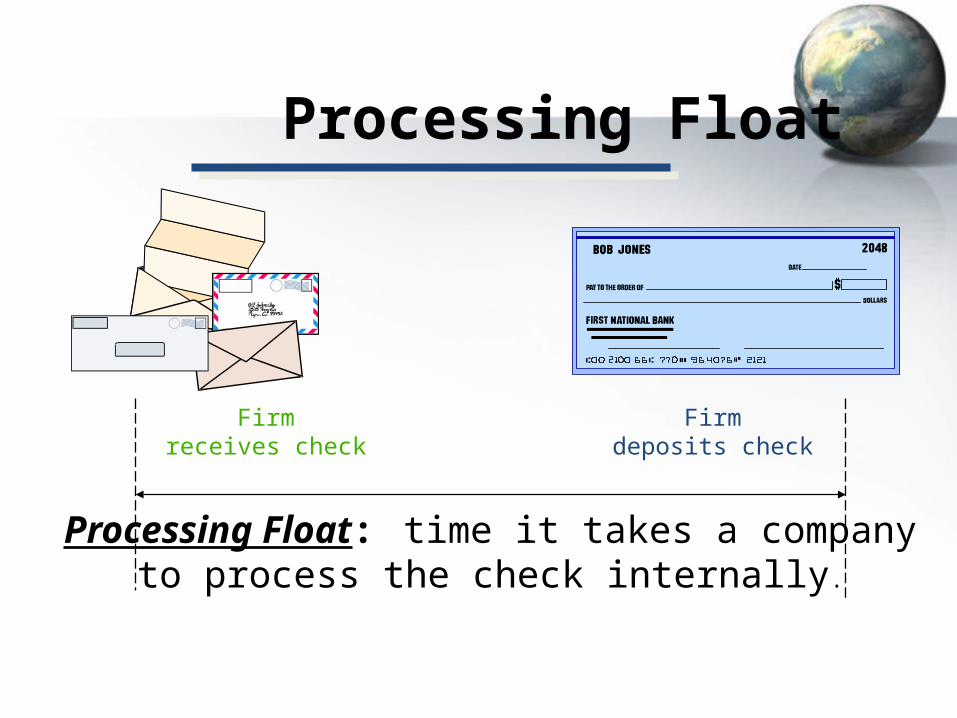

Processing Float

Processing Float: time it takes a companyto process the check internally.

Firmdeposits check

Firmreceives check

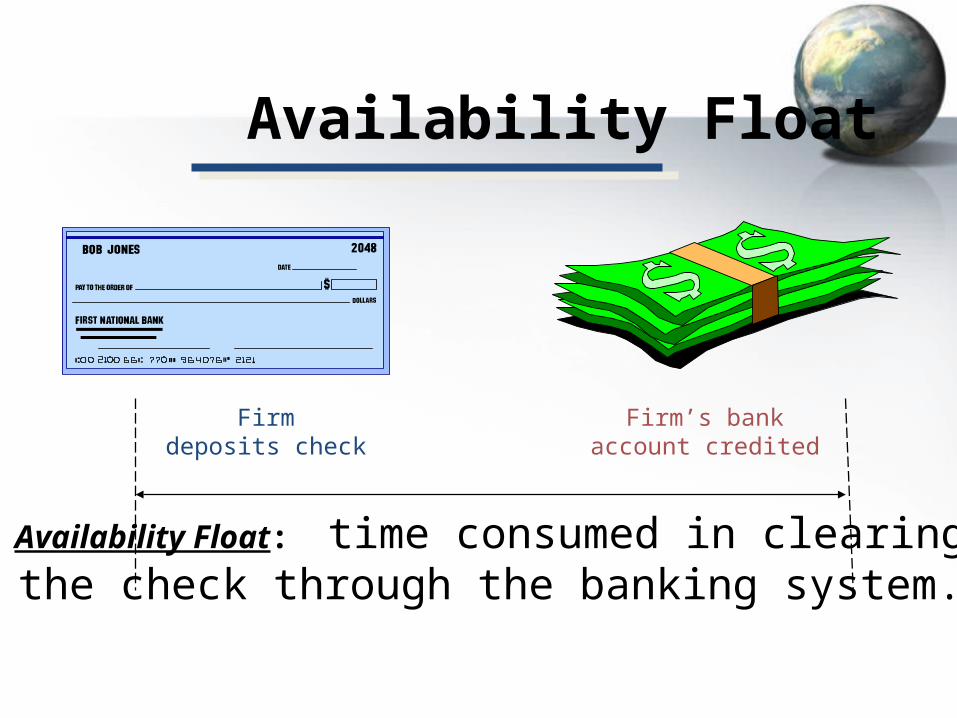

Availability Float

Availability Float: time consumed in clearingthe check through the banking system.

Firmdeposits check

Firm’s bankaccount credited

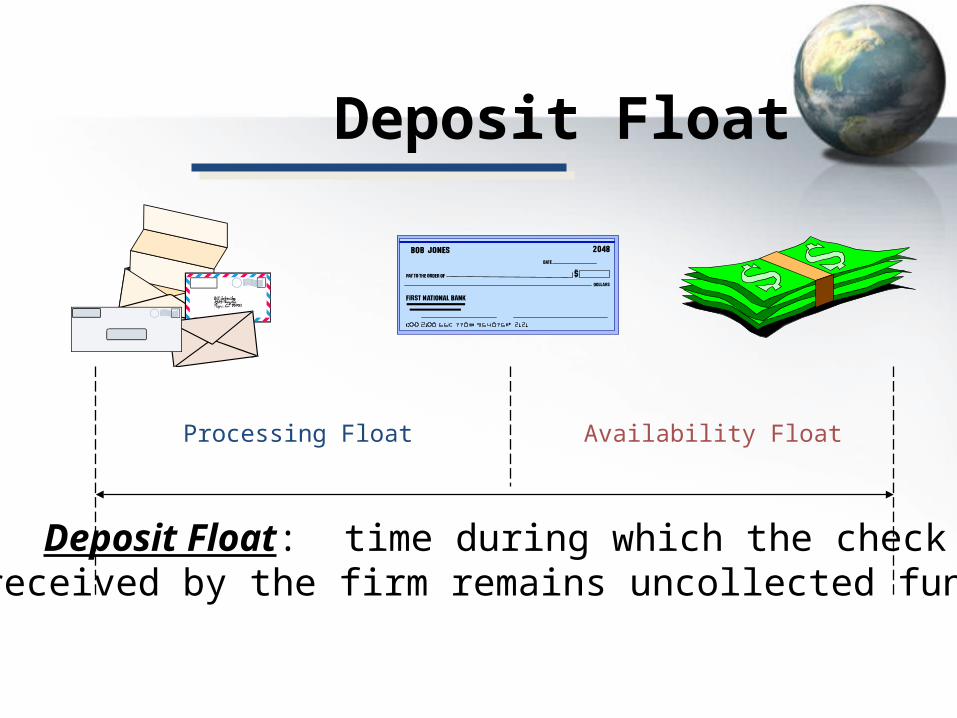

Deposit Float

Deposit Float: time during which the check received by the firm remains uncollected funds.

Processing Float Availability Float

Earlier Billing

Accelerate preparation and mailing of invoices

– computerized billing– invoices included with shipment– invoices are faxed– advance payment requests– preauthorized debits

Preauthorized Payments

Preauthorized debit The transfer of funds from a payor’s bank

account on a specified date to the payee’s bank account; the transfer is initiated by the payee

with the payor’s advance authorization.

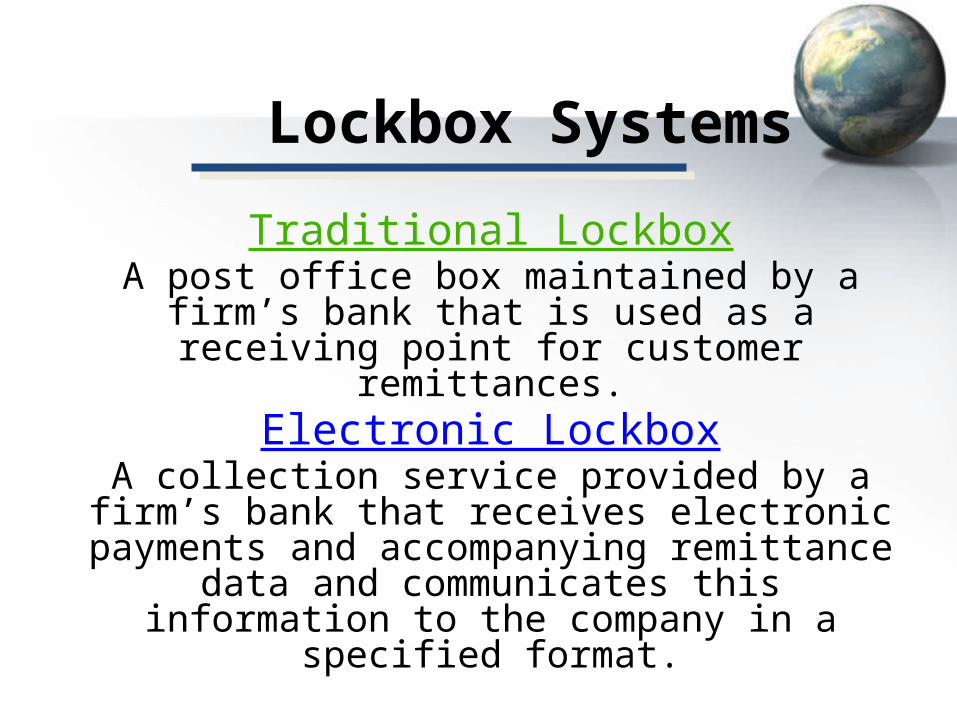

Lockbox Systems

Traditional LockboxA post office box maintained by a firm’s bank that is used as a receiving point for customer remittances.

Electronic LockboxA collection service provided by a firm’s bank that receives electronic payments and accompanying

remittance data and communicates this information to the company in a specified format.

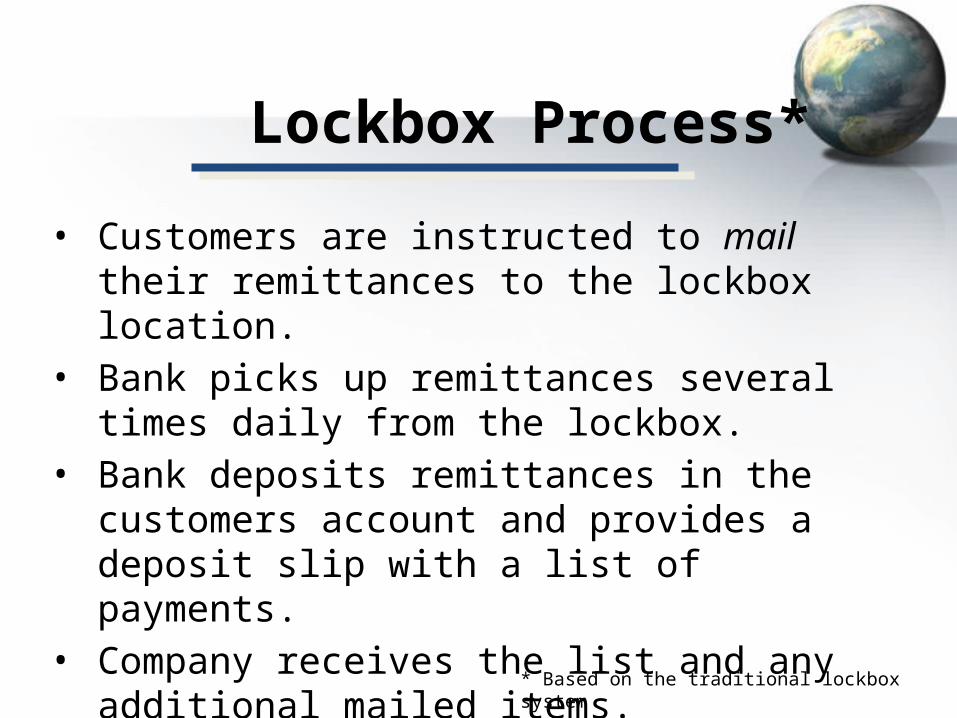

Lockbox Process*

• Customers are instructed to mail their remittances to the lockbox location.

• Bank picks up remittances several times daily from the lockbox.

• Bank deposits remittances in the customers account and provides a deposit slip with a list of payments.

• Company receives the list and any additional mailed items.

* Based on the traditional lockbox system

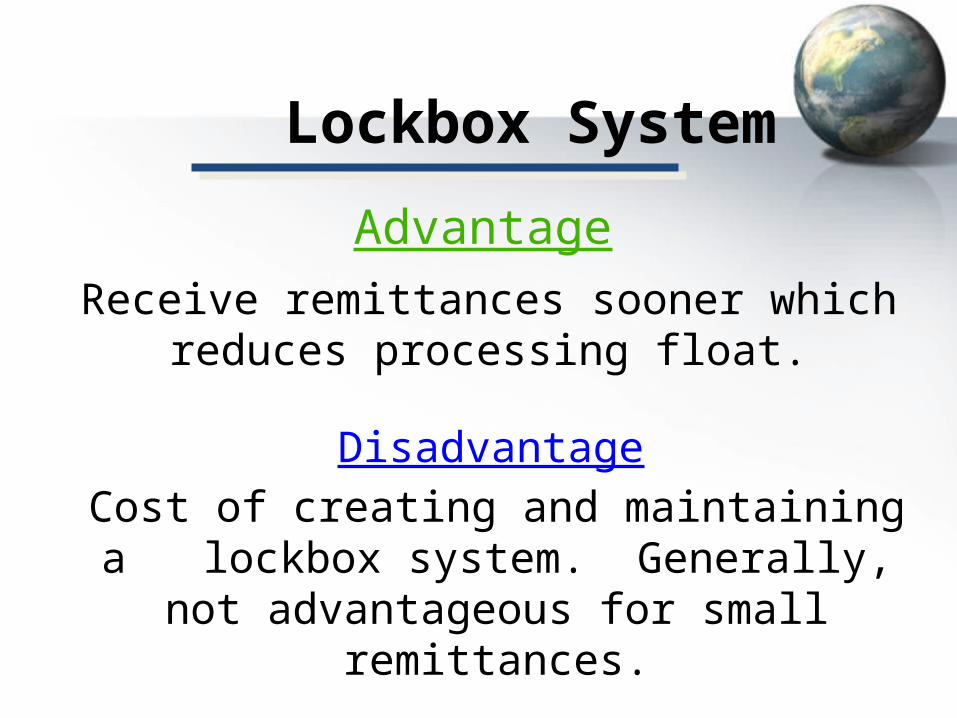

Lockbox System

DisadvantageCost of creating and maintaining a lockbox

system. Generally, not advantageous for small remittances.

AdvantageReceive remittances sooner which reduces

processing float.

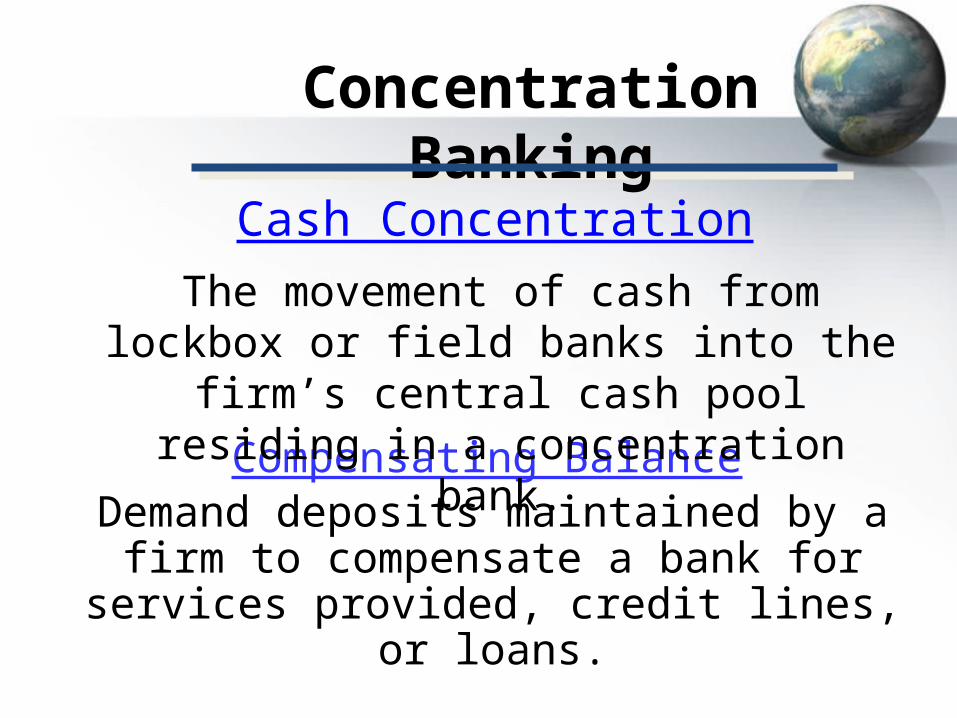

Concentration Banking

Compensating BalanceDemand deposits maintained by a firm to

compensate a bank for services provided, credit lines, or loans.

Cash ConcentrationThe movement of cash from lockbox or field

banks into the firm’s central cash pool residing in a concentration bank.

Concentration Banking

• Improves control over inflows and outflows of corporate cash.

• Reduces idle cash balances to a minimum.• Allows for more effective investments by

pooling excess cash balances.

Moving cash balances to a central location:

Concentration Services for Transferring Funds

Definition: A non-negotiable check payable to a single company account at a concentration bank.

Funds are not immediately available upon receipt of the DTC.

(1) Depository Transfer Check (DTC)

Concentration Services for Transferring Funds

Definition: An electronic version of the depository transfer check (DTC).

(1) Electronic check image version of the DTC.(2) Cost is not significant and is replacing DTC.

(2) Automated Clearinghouse (ACH) Electronic Transfer

Concentration Services for Transferring Funds

Definition: A generic term for electronic funds transfer using a two-way communications system, like Fedwire.

Funds are available upon receipt of the wire transfer. Much more expensive.

(3) Wire Transfer

S-l-o-w-i-n-g D-o-w-n Cash Payouts

• “Playing the Float”• Control of Disbursements– Payable through Draft (PTD)– Payroll and Dividend

Disbursements– Zero Balance Account (ZBA)

• Remote and Controlled Disbursing

“Playing the Float”

You write a check today, which is subtracted from your calculation of the account balance. The check has not cleared, which creates float. You can potentially earn

interest on money that you have “spent.”

Net Float -- The dollar difference between the balance shown in a firm’s (or individual’s)

checkbook balance and the balance on the bank’s books.

Control of Disbursements

Solution:

Centralize payables into a single (smaller number of) account(s). This provides better control of the

disbursement process.

Firms should be able to:1. shift funds quickly to banks from which

disbursements are made.2. generate daily detailed information on

balances, receipts, and disbursements.

Methods of Managing Disbursements

• Delays the time to have funds on deposit to cover the draft.

• Some suppliers prefer checks.• Banks will impose a higher service charge due to

the additional handling involved.

Payable Through Draft (PTD):A check-like instrument that is drawn against the payor

and not against a bank as is a check. After a PTD is presented to a bank, the payor gets to decide whether to

honor or refuse payment.

Methods of Managing Disbursements

• Many times a separate account is set up to handle each of these types of disbursements.

• A distribution scheduled is projected based on past experiences.

• Funds are deposited based on expected needs.• Minimizes excessive cash balances.

Payroll and Dividend DisbursementsThe firm attempts to determine when payroll and dividend checks will be presented for collection.

Methods of Managing Disbursements

• Eliminates the need to accurately estimate each disbursement account.• Only need to forecast overall cash needs.

Zero Balance Account (ZBA):A corporate checking account in which a zero balance is

maintained. The account requires a master (parent) account from which funds are drawn to cover negative

balances or to which excess balances are sent.

Remote and Controlled Disbursing

Example: A Vermont business pays a Maine supplier with a check drawn on a bank in Montana.

This may stress supplier relations, and raises ethical issues.

Remote Disbursement -- A system in which the firm directs checks to be drawn on a bank that is

geographically remote from its customer so as to maximize check-clearing time.

This maximizes disbursement float.

Remote and Controlled Disbursing

Late check presentments are minimal, which allows more accurate predicting of disbursements on a day-to-day

basis.

Controlled Disbursement -- A system in which the firm directs checks to be drawn on a bank (or branch bank) that is able to give early or mid-

morning notification of the total dollar amount of checks that will be presented against its account

that day.

Combining liability structure and current assets decision

Combining Liability Structure and Current Asset Decisions

• The level of current assets and the method of financing those assets are interdependent.

• A conservative policy of “high” levels of current assets allows a more aggressive method of financing current assets.

• A conservative method of financing(all-equity) allows an aggressive policy of “low” levels of current assets.