Embed Size (px)

Citation preview

February 2015

The mortgage debt ratio in Ireland is the highest in the

eurozone, standing at 73%

Avoiding overzealous property lending could have prevented

the banking crisis, the Oireachtas Banking Inquiry has heard

Moody’s has released its Annual Ireland Credit Analysis

HML News

A third of interest-only

customers immediately take

up free mortgage advice.

It has perhaps gone a little bit quiet on the

interest-only mortgages front. During 2013,

interest-only mortgages were a hot topic – and

at HML, we certainly haven’t taken our foot off

the pedal when it comes to customer contact

campaigns.

Contacting interest-only customers to make

them aware of the need to fully repay their

loan upon maturity is an important starting

point, but lenders should offer as many

repayment options as possible – and, ideally,

offer free mortgage advice.

The FCA’s interest-only review identified that

approximately 600,000 interest-only borrowers

will see their mortgage mature before 2020, so

it is imperative that lenders ramp up their

contact and support efforts – and providing

free advice is one sensible option.

Two lenders, similar findings

HML deployed a free mortgage advice

strategy on behalf of two of our clients – and

the results were similar. In both cases, of

those interest-only customers contacted to ask

if they would like to take advantage of free

mortgage advice, around a third for both

lenders were prepared to be passed over to a

mortgage adviser there and then. Customers

were then provided with whole-of-market

options.

Interestingly, we carried out these particular

campaigns for our clients before the Mortgage

Market Review (MMR) came in. The demand

for free mortgage advice was there prior to the

regulation and, it could be said, backs up why

the MMR is an important introduction to the

mortgage market.

If lenders are prepared to offer free advice

to their interest-only mortgage customers,

this will result in appropriate outcomes for

both parties. For customers, receiving

mortgage advice can help ensure the

product they are on is the most suitable

for their needs. Offering to put them

immediately in contact with an adviser

means one less thing for a customer to do

and could result in them taking action to

improve their financial situation – such as

converting to part-and-part or full

repayment. In some cases, it may be an

acknowledgement that the customer

cannot afford to repay the outstanding

balance and therefore needs to take steps

towards selling the property at the

appropriate time.

For lenders, having interest-only

customers move to a more affordable

product or increase their repayments so

they will clear their mortgage at end of

term improves the credit risk profile of

their portfolio.

The message is clear; interest-only

customers are willing to accept free

mortgage advice. The question is, will

other lenders step up and provide this

service?

This blog is by Chris Mills, HML’s chief

commercial officer, exclusively for

Mortgage Solutions.

HML News

5 analytics tools that debt

purchasers should be using.

As we continue to forge ahead into 2015, it’s

clear that the increasing trend we saw last

year of debt purchasers entering the market

and acquiring mortgage portfolios continues.

Private equity firms, asset traders and others

within the wider debt purchasing arena are fast

entering the traditional lender market - and at

HML, we are particularly seeing a trend of

overseas players recognising the value of UK

and European mortgage portfolios.

Mars Capital purchasing Springboard and

Investec selling both Start and Kensington (the

former to Lone Star and the latter to

Blackstone and TPG) are just two of the

market’s most significant transactions that we

have recently seen.

These lenders - and more importantly, their

mortgage portfolios and value potential -

obviously proved attractive to these global

players. Portfolios don’t necessarily need to be

underperforming in order to attract the right

purchaser, but whatever the performance of

assets, there are five analytics tools that will

provide peace of mind that the deal is a sound

one to make.

1) Servicing review and due diligence

A servicing review and the associated due

diligence can ensure debt purchasers and

other investors make the correct strategic

decisions when sourcing a portfolio – and this

extends to all types of credit, not just home

loans.

There are several components to this,

including looking at how the book has

previously been serviced and whether the

assets are of the quality that the seller says

they are.

Using advanced analytics to carry out a loan-

level risk assessment means investors can

have further confidence in the deal - and debt

purchasers should certainly ensure any third

party they work with tailors this review to their

specific requirements.

Integrating servicing reviews with analytical

scorecards and credit reference data means a

full picture can be painted for purchasers as to

whether they should invest in a portfolio.

2) Portfolio performance to date

The second analytics tool that debt purchasers

should draw upon is assessing portfolio

performance to date. HML manages the UK’s

largest publically-available data pool of

mortgage performances, with one million

accounts to hand. These one million accounts

mean we can forecast the performance of a

mortgage portfolio based on past performance,

including during rate rises.

3) Portfolio modelling

Once it is clear how a portfolio has performed,

portfolio modelling can be carried out. Drawing

upon a comprehensive multi-lender data pool

means statistical models can be developed.

From this, debt purchasers can look at

predictions of future losses, account profitability

and mortgage redemption – a powerful tool for

any debt purchaser.

4) Portfolio valuation and pricing

This fourth analytical tool is a combination of

portfolio performance and modelling and

enables debt purchasers to get an accurate

view of cash-flows and different pricing

scenarios. A range of financial, outcome and

economic assumptions should be included at

this stage, as these will all impact upon

valuation.

Continued over the page

HML News

This also means debt purchasers’ and sellers’

assumptions can be challenged and validated

and is an essential safeguard within this

process.

5) Primary and special servicing

The final analytics weapon that should be in a

debt purchaser’s armoury is access to primary

and special servicing, driven by advanced

analytics. It is no use owning a mortgage

portfolio if true value cannot be derived

through bespoke collections, debt and arrears

management strategies.

In the example of special servicing, drawing

upon analytical and predictive modelling tools

mean the most appropriate customer servicing

strategies can be deployed, increasing cash

collected and reducing loss and bad debt

charge. This leaves debt purchasers to focus

on their core business - investing in new

profitable portfolios.

As an aside, while it is important that debt

purchasers derive value from a portfolio, it’s

imperative that any third party they use to

provide the above analytics tools also has a

sound understanding of conduct risk and other

regulatory requirements. While advanced

analytics should be at the centre of debt

purchaser’s strategies, neither the Financial

Conduct Authority nor borrowers will tolerate

poor customer outcomes - and it will be those

debt purchasers that effectively balance

conduct risk and portfolio profitability that will

be best placed to lead the charge of

successful trading in 2015.

This article was written by Damian Riley

exclusively for Credit Today.

“As an aside, while it is

important that debt

purchasers derive value from

a portfolio, it’s imperative that

any third party they use to

provide the above analytics

tools also has a sound

understanding of conduct

risk and other regulatory

requirements,” Damian Riley,

HML.

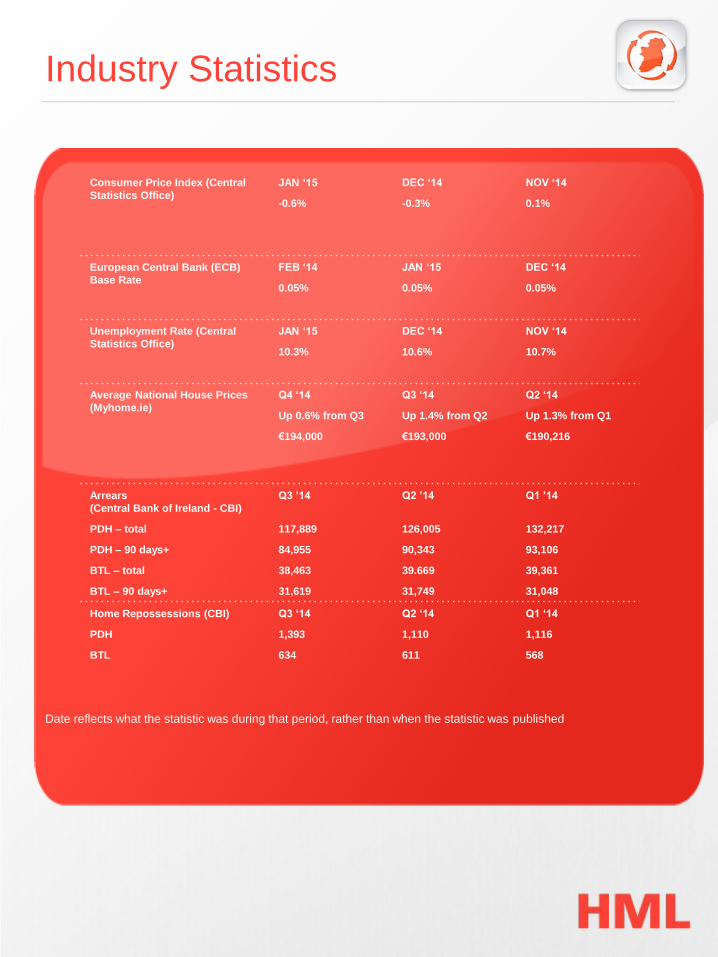

Industry Statistics

Date reflects what the statistic was during that period, rather than when the statistic was published

Consumer Price Index (Central

Statistics Office)

JAN ‘15

-0.6%

DEC ‘14

-0.3%

NOV ‘14

0.1%

European Central Bank (ECB)

Base Rate

FEB ‘14

0.05%

JAN ‘15

0.05%

DEC ‘14

0.05%

Unemployment Rate (Central

Statistics Office)

JAN ‘15

10.3%

DEC ‘14

10.6%

NOV ‘14

10.7%

Average National House Prices

(Myhome.ie)

Q4 ‘14

Up 0.6% from Q3

€194,000

Q3 ‘14

Up 1.4% from Q2

€193,000

Q2 ‘14

Up 1.3% from Q1

€190,216

Arrears

(Central Bank of Ireland - CBI)

PDH – total

PDH – 90 days+

BTL – total

BTL – 90 days+

Q3 ’14

117,889

84,955

38,463

31,619

Q2 ’14

126,005

90,343

39.669

31,749

Q1 ’14

132,217

93,106

39,361

31,048

Home Repossessions (CBI)

PDH

BTL

Q3 ‘14

1,393

634

Q2 ‘14

1,110

611

Q1 ‘14

1,116

568

Industry Statistics

Consumer Price Index

The CPI in January was 0.6% lower than the

same month in 2014. Notable downward

pressures came from the Transport (6.6%),

Clothing and Footwear (3.1%) and Food and

Non-Alcoholic Beverages (2.4%) sectors.

ECB Interest Rate

The ECB base rate remained at 0.05% in

February. There was no press statement from

Mario Draghi, president of the ECB. The next

rate decision will be made in early March.

Unemployment Rate

The unemployment rate stood at 10.3% in

January 2015, down from 10.6% in December.

In the year to Q4 2014, there was a 1.5%

increase in employment, representing 29,100

people.

House Prices

The national average house price in Ireland

stood at €194,000 in Q4 2014, a 0.6%

increase on the previous quarter, according to

Myhome.ie’s analysis of asking prices.

During 2014, house prices rose nationally by

2.6%, the strongest year for value growth

since Q2 2007.

Angela Keegan, managing director

of Myhome.ie, said: “The Property Price

Register indicates that in the year to

September over 27,000 transactions had

taken place.

Based on current trends, total transactions in

2014 look set to hit the 40,000 mark, an

increase of 38% on the 29,000 recorded in

2013. This is very heartening and while still

short of the level required for a properly

functioning property market it shows the

recovery is gaining ground.”

Arrears

Principal Dwelling Houses (PDH)

The number of PDH mortgage accounts in

arrears declined by 6.4% between Q2 2014 and

Q3 2014. Out of the total mortgage accounts,

15.5% were in arrears, representing 117,889.

The number of PDH mortgage accounts in over

90 days of arrears also declined during Q3,

falling by 6%. These accounts totalled 84,955,

11.2% of all the PDH mortgages in arrears.

Accounts in arrears of more than 720 days

increased in number by 418 during Q3 and

currently account for almost 7.6% of total PDH

mortgage accounts. The outstanding balance of

such accounts was just over €8 billion at the

end of September.

Buy-to-let (BTL)

The number of BTL mortgage accounts in

arrears decreased between Q2 and Q3 2014 to

38,463 (26.8% of the total accounts) from

39,669 (27.5% of the total accounts).

Home Repossessions

At the end of Q3 2014, there were 1,393 PDHs

and 634 BTLs in lenders’ possession. Of the

PDHs, 302 were taken into possession during

the quarter, 47 of which were the result of a

court order, while 255 were abandoned or

voluntarily surrendered.

Top News Stories

Avoiding overzealous

property lending could have

prevented the banking

crisis.

This is according to Gregory Connor, banking

policy expert at Maynooth University, who has

provided evidence to the Oireachtas Banking

Inquiry.

Mr Connor said the Central Bank of Ireland

should have reined in property lending, as well

as clamping down on foreign banks placing

cash into Ireland’s property market.

In addition, regulators missed important

warning signs in both 2006 and 2007 at the

potential risks ahead.

"The Central Bank and financial regulator

should have blocked the enormous debt

capital inflow and the too-fast growth in

property development lending.

"If it had done either of those things, in my

opinion, the Irish banking crisis wouldn’t have

happened - and it should have done both.

"There's a massive failure by the Irish Central

Bank and financial regulator in not blocking

both of these, “ Mr Connor stated.

€3.5 billion of International

Monetary Fund (IMF) loans

have been repaid early. This means €12.5 billion of IMF loans have

been cleared early to date and an additional

€1.5 billion in interest saved.

The growth potential of Ireland’s economy and

the increased sustainability of the country’s

debt position means Ireland can borrow at

record low interest rates, minister for

finance Michael Noonan explained.

He added that Ireland’s deficit is expected to be

below 2015’s deficit target, with debt on a

downward trajectory.

The mortgage debt ratio in

Ireland is the highest in the

eurozone.

The average ratio in Ireland is almost 73% for

owner-occupier mortgages, with the average in

the eurozone just 37%, the CSO has reported.

The median value of main residences stands at

€150,000, with 70.5% if all households owning

their main property.

In addition, the report also noted that 56.8% of

households have some form of debt. The

median debt for overdrafts is €1,000, €1,400 for

credit cards and €129,000 for mortgages.

Variable mortgage rates are

“excessive” in Ireland.

Speaking to the Irish Times, MEP Brian Hayes

referred to data which showed the typical rate of

standard variable mortgages in the country was

4.26%. This is much higher than the 0.05%

charged by the European Central Bank.

He said the Competition and Consumer

Protection Commission should investigate the

variable rates charged by banks.

Continued over the page

Top News Stories

Mr Hayes told the newspaper: “ECB

interest rates are at an all-time low of 0.05%.

This low interest rate environment has been

reflected in many eurozone countries through

lower variable rates but in Ireland banks are

still comfortable offering variable rates of over

4%.”

The Oireachtas Joint Finance Committee has

heard from Ireland’s biggest banks that

mortgage rates are higher compared to other

countries within the EU due to more expensive

funding.

Over 75% of new jobs

created last year were by

Irish companies. Just under 30,000 jobs were created in 2014,

chair of the Oireachtas Jobs Committee and

Fine Gael TD Marcella Corcoran Kennedy

stated.

“There is great fanfare when foreign direct

investment (FDI) is announced in any part of

the country and for very good reason, as FDI

brings huge employment opportunities and

with it a knock on boost to local economies.

“However for every FDI job that was created in

2014, three more indigenous Irish jobs came

on stream. This is extremely encouraging and

indicates the steady and consistent recovery

of the economy,” Ms Corcoran Kennedy

added.

High public debt remains a

constraint in Ireland.

According to Moody’s, which rates Ireland at

Baa1, stable, the country’s economy is

recovering at a fairly strong rate. However,

high public debt levels is still holding recovery

back. Another constraint noted by the rating

agency is the weakness in Ireland’s banking

sector.

Commenting on the Annual Ireland

Credit Analysis, Moody’s senior credit

officer Kathrin Muehlbronner said: "Ireland's 2014 economic performance was

strong, with real GDP growth estimated at

around 5%, and the country's growth prospects

remain solid. However, we believe that the

strong growth in exports is unlikely to be

repeated, as it was partly due to special factors

related to offshore production activity.

“We expect economic growth rates of 3.8% and

3.0% in 2015 and 2016, respectively, which is

still a very solid performance.”

The report also noted that while there is a

robust investment recovery, this will need to be

matched by bank lending, but the banking

sector continues to be “weak”. Of total loans,

non-performing ones make up a quarter.

Despite this, Moody’s commented on the

materially reduced risks on the government’s

balance sheet coming from the banking sector.

Improved funding profiles, liquidity and capital

have contributed to this, along with quicker-

than-expected repayment of government-

backed debt.

"Ireland's 2014 economic

performance was strong, with

real GDP growth estimated

at around 5%, and the

country's growth prospects

remain solid,” Moody’s.