Embed Size (px)

Citation preview

1

The economic risk factors;

demand of formal and informal care of elderly people

- a critical appraisal of the research literature.

Version 4.0

15.11.2011

Eero Siljander

Centre for Health and Social Economics

National Institute for Health and Welfare

PO BOX 30

00271 Helsinki

Finland

Abstract

Long-term care is a form of health and social services and family care that aims at caring for the func-

tional ability and maintaining it at a decent level for the elderly and the disabled. The focus here is on

financial incentives and institutional structures that play a key role in determining admittance to institu-

tional care and its economic risk factors. Strategic decision making and bargaining at family level de-

termine the amount and quality of informal care given. Formal and informal care can be either substi-

tutes or complements. The risk of having to resort to institutional care is also a question of long-term

care insurance. It is important to investigate the possibilities for cost-effective services in the field of

elderly care. Therefore the following questions are to be investigated in this literature review. Firstly

what are the economic demand and socio-economic need factors for institutional care? Do wealth, edu-

cational status and family characteristics play an essential role? Secondly, how do economic and altruis-

tic incentives such as informal care subsidies, bequest motives and family ties affect family decision

making on informal care and formal care types chosen? What and how should informal care allowances,

caregivers leave days and another similar benefits be tailor made to encourage care at home. Thirdly,

could government and insurance firms screen for potential long-term care clients in a cost-effective or

profitable way and by what generally acceptable means? These themes are critically reviewed based on

research literature as part of the author’s PhD thesis.

Keywords: Long-term care, demand for care, informal care, formal care, services, costs.

2

Introduction

As defined by Edward C. Norton in his seminal article on long-term care in the handbook of health

economics (2000): “long-term care (LTC) is care not cure for the elderly. It aims to keep the elderly

functional ability and quality of life at a decent and society acceptable level up until death.” This

paper is interested with the issues of economic incentives and prevention of risk factors of long-

term care.

The goal of the research project is to produce new evidence on the economics of health and social

care of the elderly. The motivation is to search and look for economic, socio-economic risk factors

of LTC-care - formal care at care institutions and at home and of informal care at home. Thus the

results can be used for prevention of health and social hazards that lead to premature loss of elderly

peoples’ functional ability in society and institutional care or informal care.

The market equilibrium prices of formal care are a matter of demand for and supply for care. By

reducing demand and shifting the demand curve to the left it is possible to obtain care at a lower

price when demand curves slope down and supply curves slope up. This means reducing the supply

for formal care through growth of informal care and care at home. Therefore It is important to in-

vestigate the possibilities for cost-effective services in the field of elderly care.

Therefore the following questions are to be investigated in this literature review. Firstly what are the

economic demand and socio-economic need factors for institutional care. Do wealth, educational

status and family characteristics play an essential role? Secondly, how do economic and altruistic

incentives such as customer fees, bequest motives and family ties affect family decision making on

informal care and formal care types chosen? What and how should informal care allowances, care-

givers leave days and other similar benefits be custom made to encourage care at home. Thirdly,

could society and insurance firms screen for potential long-term care clients in a cost-effective or

profitable way and by what generally acceptable means? Can LTC-insurance be a viable and gener-

ally acceptable option for care in the Nordic countries and in Finland?

Literature review – search and database strategy

The literature review was conducted using a search strategy for key terms of long-term care, formal

care, informal care, economics. Other search terms included phrases such as family bargaining, al-

truism, bequests, income transfers and econometrics. The scientific databases were Web of science,

Web of knowledge, Pubmed, Ebsco, Academic search elite and some minor information sources

(like library services of THL). The total number articles used for title, abstract review was in the

range 150-200 of which approximately 50 were selected for full reading and critical review.

The selection of articles for reading was based on economics of LTC-care. The articles had to con-

sist of theoretical or empirical results in a context of an scientific economic framework and be pub-

lished in a peer reviewed journal. The impact factor of the journal was not a search criterion. How-

ever the majority of key articles for reference had been published in health economics journals like

Health economics or the Journal health economics, Economica, Handbook of health economics,

International economic review, the Inquiry, the Gerontologist. The literature review search strategy

produced most studies on LTC from US studies followed by central European and UK studies.

There has been much research on LTC in the Nordic countries but however mostly from a sociolog-

ical and social work point of view.

3

Because of dominance of market based system studies it is easier to understand the economics of

financing, reimbursing and buying LTC from the private services marketplace. Thus scientific

knowledge of health insurance and incentives of family decision making have advanced to a greater

extent than the economics of say public LTC services (in the US nursing homes are predominantly

private). The non-profit sector and NGOs have however a highly substantial role in the European

and especially Nordic context. Therefore much attention and work was devoted to finding theoreti-

cal framework results and empirical results in this context.

For the Nordic countries and finnish service provision framework – the welfare state model – there

was applicable theoretical material found. This was concerning public financing and reimbursing

for quality of care and providing incentives for informal care. The results are in a welfare econom-

ics framework with altruistic family members. The government (referred to as the “social planner”)

has to find first and second best optimal solutions (with respect to informational asymmetries) in

this framework by levying distorting taxes and making income transfers as well as providing nurs-

ing care. The state budget must however remain balanced so that expenditures equal income and

changes in policy are cost-neutral (i.e. trade off between policy alternatives).

The distinction between formal and informal care on the other and public and private care on the

other are the key definitions that separate services and their financing. In both formal and informal

care frameworks social benefits can be in-kind or in-cash type. This gives differing incentives to

differing families depending on their productivity, wealth, housing status and other assets. The fam-

ily strategy is to make economic decision before the risks of institutionalization and dependency

occur. What is considered as a family are the dependent parent, his or her spouse and their children.

These involve income transfers, bequest planning, informal care subsidy and LTC-insurance con-

siderations. Altruism may be introduced into the models but it is not necessary for general results to

hold. Thus it is ex-ante decisions on economics that the literature is interested in. Ex-post when de-

pendency and care needs occur the families stick to their strategy and act accordingly.

The critical things for this strategy to work in empirics is that the elderly person has a family in the

first place and that the children live geographically nearby. It has been found in empirical literature

that family events such as distance to relatives and death of spouse have a significant effect on the

risk of institutional care. Moreover people living alone or never married have higher probabilities of

institutional care at the baseline. Critically considered the strategy won’t work these population

groups.

The studies are mostly concerned with either comparing the financing of LTC or substitution be-

tween care forms. Empirical studies in Europe investigate substitution and complement issues while

US studies are mostly interested in financing and reimbursing care. Critically reviewed it seems that

European investigators take the public service system as fixed and look for cost-effectiveness inside

it while their US colleagues have great interest in developing the insurance based private system

from an outside financing view with budgets fixed. This has probably mostly to do with historical

issues and development path dependence.

4

Long-term care (LTC) production and demand for health

The demand side are the expectations of persons in need of LTC and general population expecta-

tions of care available based on needs. The region, provincial or municipal budgets form the budget

constraint which are financed by regional taxation. Services must be accessible and available to the

general population with generally acceptable out-of-pocket costs. From an economics viewpoint

one must understand what is produced, by whom and to whom, and what is the utility generated by

this process of inputs and outputs. Families and households are production (Grossman, 1972) and

insurance units that produce and buy care from the market (Eisen & Mager, 1996). This applies to

adding to and consuming the capital good stock of health. In the seminal article by Grossman

(1972) households are considered the production units of health. This is done by using household

time, buying health care and services. The decision on production is influenced by human capital

and wealth consideration (Grossman & Rand, 1974). The demand for health care services is derived

demand because it is used as an input in the health production function.

It should be noted that Grossman does not explicitly deal with uncertainty in his model. He does

however indicate, that uncertainty can be introduced into the model by probability distribution of

depreciation rates (Grossman & Rand, 1974). The depreciation rate is stochastic for each individual

and with chronic illness the shock is to increase the depreciation rate. The rise in the depreciation

rate lowers the quantity of health capital supplied by an unit increase in medical care received all

other things being equal. Thus it is shown by Grossman’s investment model that with other va-

riables being constant the consumers with chronic conditions should demand more medical care

than other patient groups such as acute patients.

In Grossman’s pure consumption model of health the additional result of income spent on health

will rise as the depreciation rate rises (i.e. second result with chronic illness). A third important re-

sult from health demand model (1972) is that schooling makes individuals more efficient producers

of health and thus health care demand falls. However with chronic illness this effect is expected to

be lower than for the standard Grossman models (Grossman & Rand, 1974). Fourth Grossman

models depreciation based on the life cycle so that older age groups have higher depreciation rates.

The demand for medical care is thus larger for persons with chronic conditions if the demand curve

for health is less elastic for them than for others. The fifth and last key variable in Grossman’s mod-

el is the distance parameter which is measured as distance to care. One of the most important time

inputs in the health production function is the time it takes the consumer to traver to the source of

medical care. In geneneral the quantity of medical care demanded should be negatively related to

the amount of travel time required to obtain a unit of care.

Since Grossman’s work the health shock is assumed to be the probability of needing institutional or

long-term care in general. In the analysis of long-term care this means a probability distribution of

needing institutional long-term care when retired old over the elderly population (Eisen & Mager,

1996). It is the framework of chronic illness by with health as a durable consumption good with

investment decisions (including depreciation) that applies to long-term care decisions. This frame-

work is adapted from the article by Grossman & Rand (1974) for informal care decision by for ex-

ample VanHoutven & Norton (2004), Norton (2000), Nocera & Zweifel (1996) and Zweifel &

Struwe (1998). The key is noticing that the inputs into the production for health function of a parent

are informal care by children, demand for medical care by the parent and human capital of the par-

ent. This produces utility for both the parent and the children. This is the basic idea of LTC care

decision making. The parent does not use his or her own effort but the effort is replaced by that of

children compared to the standard Grossman model.

5

However parental human capital, wealth and income influence decision making through bequest

and planning motives (Zweifel & Struwe, 1998; Eisen & Sloan 1996). This requires the parent to be

in an aware mental state in making decision on care purchases and bequests. Otherwise children

make decision on behalf of the parent (unaware case). Based on the above arguments disability and

handicaps in cognitive and functional ability can be specified as an increased depreciation rate in

the Grossman model or losses in household productivity. Persons facing such problems have to

counterbalance them with investment in health as informal or formal care. This is where family de-

cision making and household and service technologies based on economic considerations come into

the health economics framework (Eisen & Sloan, 1996).

Informal care by children for their parents in need of LTC can be viewed as a specific care service

that exists primarily for three reasons. The other is the value of informal care stems from the direct

health utility of care to the elderly but also from indirect utility that is associated with affection and

safety. Norton and Vanhoutven (2004) model this in that the parent and child get direct utility from

informal care. Resoning for the existence of informal care can be provided cheaper than formal care

for two reasons. One is the restriction of household budget constraint to buy formal care and the

non-optimal demand for long-term care savings in earlier periods (Eisen & Mager, 1996). Second

there are LTC care restrictions on formal care based on public (government) budget constraints

which cause excess demand (Norton, 2000). Thirdly and probably most importantly the affective

relationship that characterizes a normal family plays a special role in that it can create altruistic be-

havior necessary for the delivery of informal care. Even in the case of non-altruism by children

there exist according to the literature economic bequest motives (including inter-vivos transfers)

that induce informal care (Pestieau & Sato, 2008; Zweifel & Struwe, 1998).

Macro- and mesoeconomics of LTC demand

Long-term care (LTC) is care not cure of chronic conditions, sickness and disability (Norton, 2000).

This points out to the individual medical and social demand factors for care. Impairments can be of

cognitive or functional type or both. Most often LTC-care is divided into formal care (including

institutional care and home care by social and health care professionals) and informal care (non-

paid care at home or cash transfers for formal care). Thus depending on adult children’s productivi-

ty in the labor market the informal care will be given as time devoted to care or cash transfers to the

elderly to buy care (Kuhn & Nuscheler, 2011). Informal care can be substitute or complement to

formal care depending on formal care type (VanHoutven & Norton, 2004).

Eisen & Sloan (1996) present a framework of determinants of long-term care at the macroeconom-

ic-, mesoeconomic- and at the microeconomic levels. Starting from the macro level there is the So-

cial and health legislation, legal-institutional basic conditions, supply of professional care services

and supportive infrastructure. These must provide a legitimate framework for old age care that is

accepted by the general population. Services must be accessible and available to the general popula-

tion with generally acceptable societal costs. The economic resources in action are the wealth of

nations or in more common terms national income (GDP). These form the societal budget constraint

for LTC demand (we abstract from other government sectors like education, defense, etc.). The sub-

sidies for informal care, LTC insurance and regional governments or municipalities are decided on

central government level based on national and federal taxation. The link between macro-, meso-

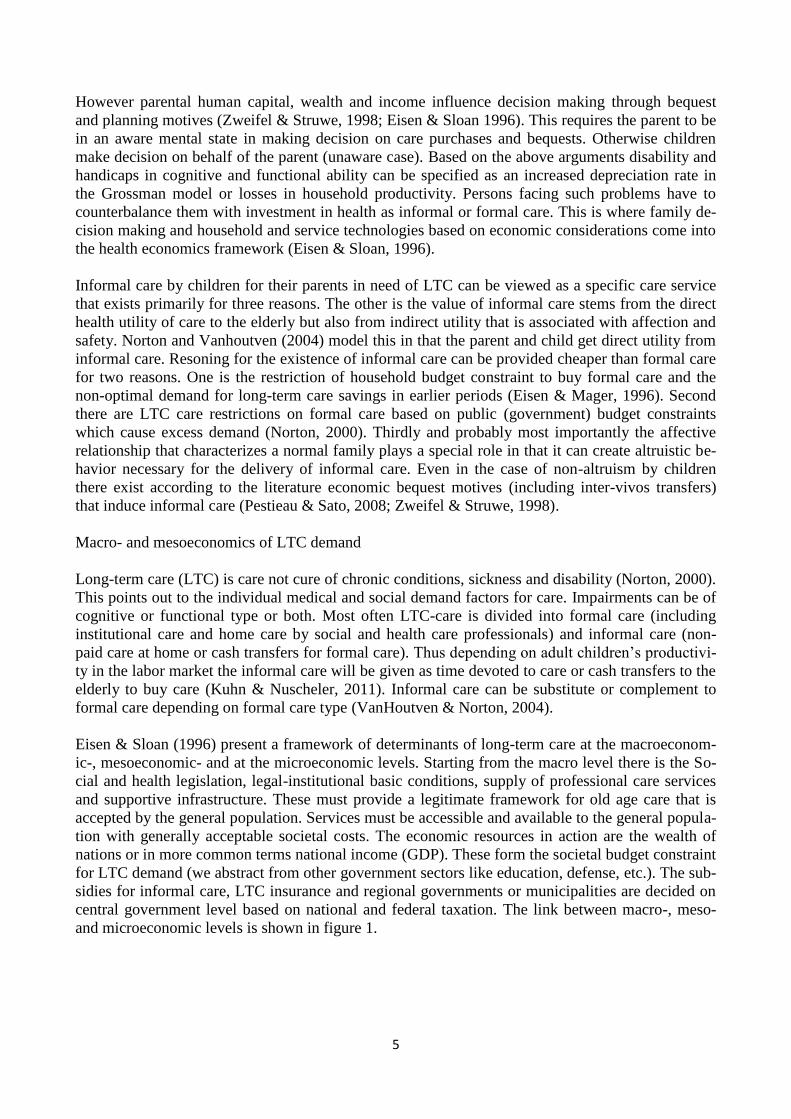

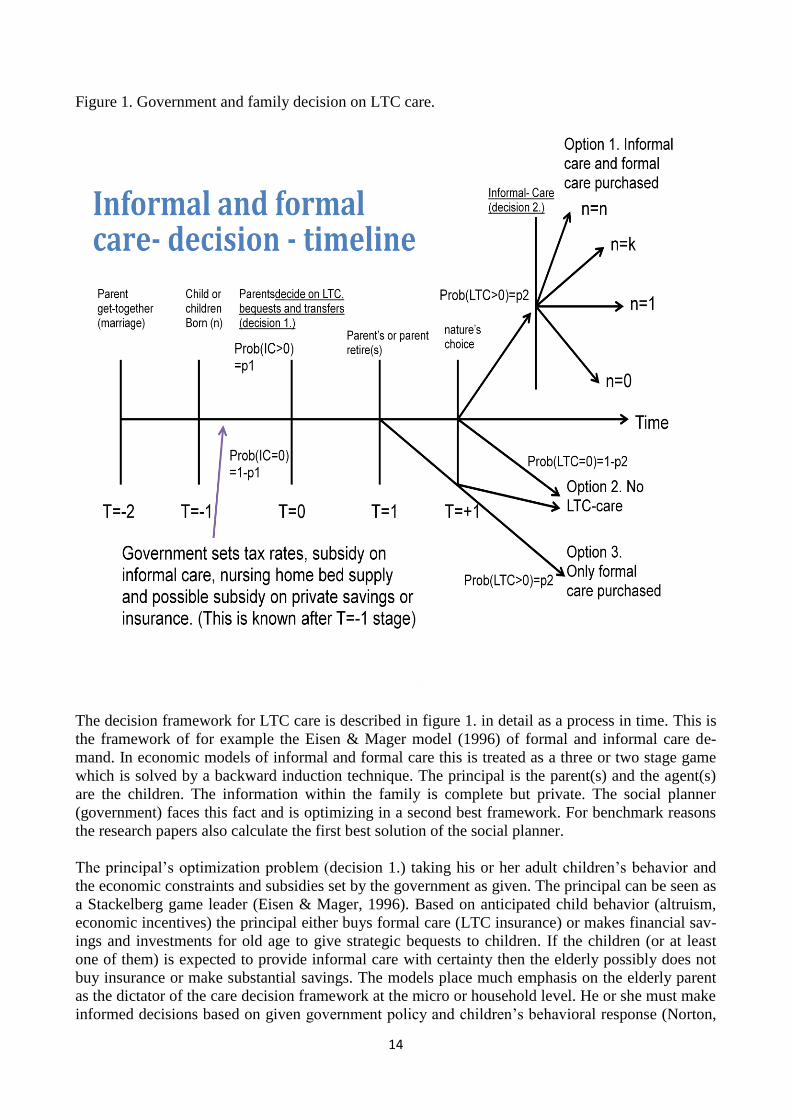

and microeconomic levels is shown in figure 1.

6

Figure 1. The demand and for long-term care (LTC) at the macro and micro levels in Finland

In figure 1. the demand pathway to institutional care is depicted from a determinants and financing

point of view. What we are interested in this paper are the economic incentives that influence this

pathway that are in the left circle boxes of economic and family structure resources at the micro

level (households, families) controlling for sickness and disability. Economics of informal care cov-

ers family structure and bargaining which determine care resources at home. Socio-economic re-

sources affect the possibilities for pension, formal care and LTC-insurance savings. The key box in

figure 1. is the “family and material resources” from the economist’s point of view. Out-of pocket

payments are related to the box “formal caring”. The key questions are: how can economic incen-

tives be used to prevent use of nursing home and institutional care? What are these incentives and

how should they be used? What are the demand and supply side factors and dynamics of long-term

care services?

The middle circle boxes of financing and risk-sharing at the macro level (population, government)

are of interest because the risk sharing takes place there. The government pays subsidies for infor-

mal care, sets taxes, pays subsidies for LTC-insurance and provides state grants for LTC care. Also

municipalities set taxes and decide on provision of nursing home care. Social insurance subsidizes

informal and formal LTC care but collects no taxes. The out-of-pocket payments are the contribu-

tion of the population to LTC care costs (in addition to taxes). Private insurance and private saving

finance all care forms.

The right hand side box depicting supply of services is a controlling mesoeconomic factor that is

produced at the municipal, regional levels. Knapp (1984) describes in his seminal work the relation-

ships between inputs, output and outcomes of social care. At the mesoeconomic level the progress

of technic-medical knowledge and innovation guide technological efficiency of production. These

7

combined with physicians’ and social care staff’ effort, attitudes and moral concepts produce alloca-

tions. These allocations can in first and second best settings possibly be cost-effective and cost-

efficient (Norton, 2000). Productivity and efficiency of allocation at the mesoeconomic level deter-

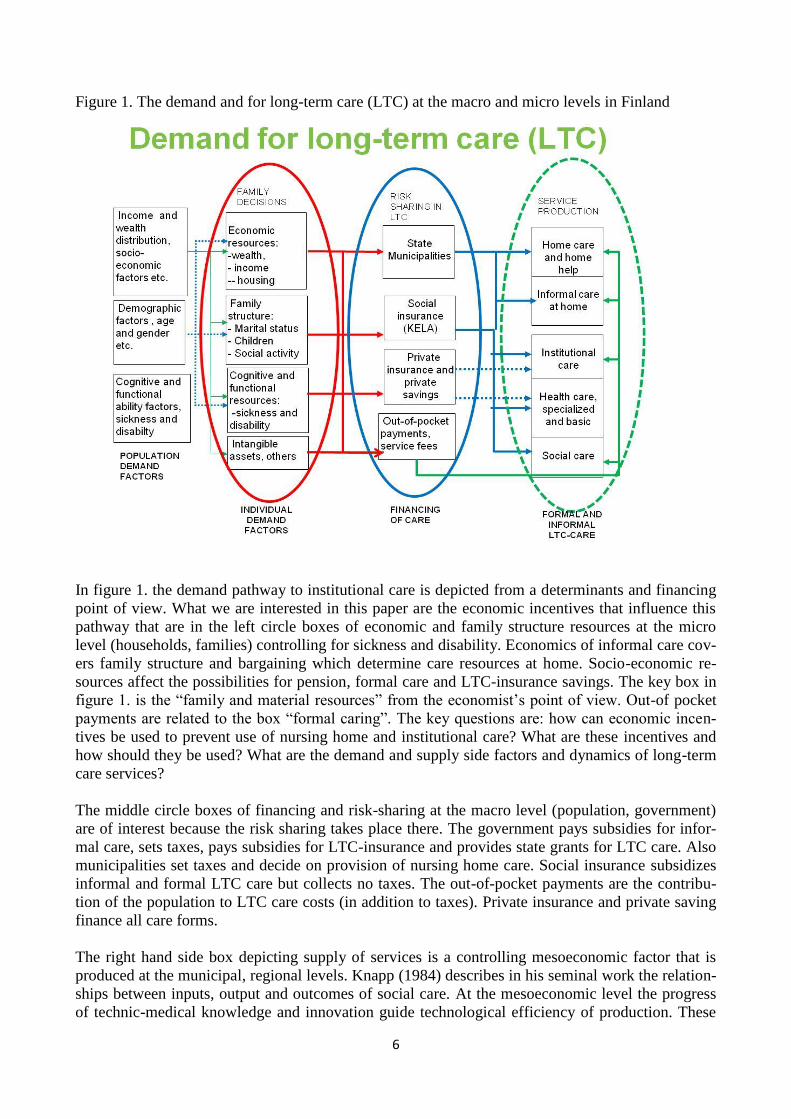

mine health and social outcomes. Figure x. depicts old-age services in Finland, 2011.

Figure 2. Old-age LTC services in Finland in 2011.

4

OUT-CLIENT

SERVICES

INTERMEDIATE

SERVICESINTERMEDIATE

SERVICES

INSTITUTIONAL

SERVICES

OUT-PATIENT

SERVICES

SPECIALIZED

HOSPITAL CARE

- somatic.

- psychiatric.

DAY HOSPITALS

- day and night care etc.

NURSING HOMES

24H SHELTERED HOUSING

REGULAR SHELTERED

HOUSING

HEALTH CARE LTC SOCIAL CARE LTC

LTC SERVICES

FINLAND 2011.

1. Home help services.

2. Support services

- meals on wheels,

- transport services

3. Informal care

subsidies

1. Home medical services.

PRIMARY HEALTH CARE

- long-term wards.

ACUTE

IN-PATIENT CARE

LONG-TERM

IN-PATIENT

CARE

HEALTH CARE

SERVICESELDERLY SOCIAL WORK

HOME CARE

-listing

DAY CENTRES / DAY CARE

Source: modified

from Noro, 2004,

THL.

SPECIALIZED CARE

– out-patient visits.

PRIMARY CARE

-out-patient visits

HOME CARE

-listing

Formal and informal long term care

The supply (services) of formal care in LTC is given by qualified professional and experts in the

field of social and health care. On the other hand care for the elderly might not be a phenomenon of

formal services but for the most part informal care at home by relatives of friends (Norton 2000).

Informal care is most often given by unpaid and unprofessional family members, relatives, friends

etc. This is what makes long-term care a wide area of research with hard to define boundaries as

concluded in research papers (Vanhoutven & Norton, 2004). Official statistics capture only the

work being paid for or exchanged at the market. Most of informal care is outside of this definition

(Norton, 2010) as it is done as part of non-market household work or monetary transfers. It is care

that is valued only by a fraction into national standardized health accounts (SHA) data. According

to US based estimates informal care would account for 70 % of all care if it were in SHA data.

8

Thus LTC care may be paid or unpaid care depending on individual conditions and family ties.

What matters for economic incentives of informal care are family bargaining (Stern 1994), informal

care allowances and bequest motives (Zweifel et. al., 1996, 1998), income transfers and distance

between family members because of travel costs and time (Engers & Stern, 2000). The key in un-

derstanding family decisions is knowledge of strategic bargaining and game theoretical considera-

tions in economics. These include family bargaining in the form of co-operative and non-

cooperative games. Key concepts are Nash equilibrium, welfare economics, social first and second

best.

There are several ways in which an elderly person can protect him- or herself from the risk of insti-

tutionalization. This can be done by relying on informal care through altruism or bequest motives,

taking an LTC insurance policy, saving for retirement or taking for example an inverse house loan.

Informal care comes into game theoretic play if the spouse and children are altruistic in their beha-

vior or respond to bequest motives.

Informal care also partly predicts the reason why so few private LTC-insurance policies are pur-

chased worldwide (OECD, Help wanted, 2011). Another reason is that LTC-insurance cost cover-

age is relatively low worldwide and elderly people are scared of the possible “opt-out of care” mor-

al hazard imposed on relatives and municipality if they purchase care insurance or care for them-

selves. LTC-insurance is often compared in the literature to flood insurance, i.e. most often recog-

nized and applied for after the damage has been done. It has been shown to be the case that people

are unaware of risks of LTC care not that they don’t care (Zhou-Richter et.al., 2009). This is also a

question of how altruistic relatives are perceived to be if any (Jousten et.al. 2005, Van Houtven,

2004).

In the absence of informal care and formal home care the elderly have only the option of institu-

tional care or which might impose a large disutility (Kuhn & Nuscheler, 2011). Most elderly people

want to live at home as long as possible according to survey results (Vaarama et.al., 1999). The

greatest risk factors for admittance to institutional care are sickness and disability, low socio-

economic status, living alone and having few or no close relatives.

Public systems of long-term care – taxes or LTC-care insurance ?

Almost all OECD countries have a system for delivering and financing long-term care. The financ-

ing is through state and municipal taxes or health insurance premiums. The service provision can be

by public, private or third sector organizations. Long-term care insurance is an insurance policy

that delivers LTC-care in benefits in-kind or in benefits in cash against sickness and disability in

older age. The insurance policy holders pay insurance premiums until time of retirement or time of

receiving paid care. It is an insurance policy that has been compared to flood insurance by Zhou-

Richter et.al. (2009). Risk perception and risk aversion attitudes towards old-age related expendi-

tures are low or very low among the general population and this constrains demand and purchase of

LTC-insurance. Most people don’t expect to be institutionalized at old age and strongly prefer to

live at home as long as possible (Vaarama, Moisio, Karvonen, 2010). In Finland they also expect

the public sector to take care of them if needed and attitudes towards purchasing private services are

on the decline because of the financial crisis (Maunu 2010). This is confirmed by Brown et.al.

(2009) who claim demand side-constraints as the most important factors for lack of LTC-insurance

markets.

9

In a paper on the supply side of LTC-insurance Brown et.al. (2007) place also emphasis on supply

failures which make private insurance too expensive and insurance policies premiums too costly in

relation to expected benefits for the majority of the population. In particular, the typical private in-

surance policy purchased exhibits premiums marked up substantially above expected benefits. It

also provides very limited coverage relative to the total expenditure risk. However this is in part due

according to Norton (2000) to limited and highly uncertain predictions of the costs of long-term

care in the distant future of 30 to 40 years forward which are non-diversifiable risks for insurance in

the long run. This is why almost all private insurance sold and bough are benefits in-cash type. Be-

cause of these and other considerations explained later (adverse selection and moral hazard) the

public provision and financing of long-term care is the predominant form of providing elderly care.

Assessing the comprehensiveness of a country’s LTC-system is all but easy. Universality of en-

titlements to care is but one aspect, which has been used to derive the typology of systems presented

earlier. But not all universal LTC systems are comprehensive. For example a significant share of

spending is still paid out-of-pocket by users. In Switzerland, nearly 60% of total LTC spending is

privately financed (36% if including cash benefits granted under the Invalidity and Survivors’ in-

surance). In Portugal out-of-pocket LTC financing accounts for 45% total LTC cost, while the cor-

responding figure for Germany and Spain is around 30% of total LTC cost (OECD, 2000). In the

United States, out-of-pocket spending represents 22% of LTC cost (Kaiser Commission, 2010).

Eligibility rules – whether a system is universal or means-tested – are but one dimension to assess

comprehensiveness of LTC coverage. In fact, three dimensions can be identified: eligibility rules –

universal (primarily all citizens qualified) versus means-tested systems (income qualification); the

basket of services covered - breadth of coverage across LTC-service forms; and the extent of pri-

vate cost sharing on public coverage (extent of out of pocket payments) - depth of public coverage.

All countries have eligibility rules setting the care-dependency status and, in means-tested system,

the income and assets levels triggering eligibility to public LTC support. Eligibility to care and the

level of public support is determined on the basis of a care-need assessment based on physical

and/or cognitive limitations. Need assessment helps governments target care needs, and can follow

more or less stringent rules depending on the country. While many of the functional capacities

which are measured are similar, assessment systems and dependency levels on which eligibility is

determined are not uniform across countries and, in some cases, can vary across sub-national juris-

dictions.

For example, Germany provides public benefits to 10.5% of its seniors, whereas Japan provides

public benefits to 13.5% of its population aged over 65 years (Campbell et al., 2009). Health and/or

social-care professionals are involved in the assessment process, although a medical doctor is in-

volved in only a few countries, for example Belgium and France. For eligible people, the benefit

amount is typically adjusted to need. An income and/or asset test may also be carried out to deter-

mine user cost sharing or the amount of the public subsidy. Next we present some LTC-system

types.

Tax based nordic LTC-systems

Norway, Sweden, Denmark and Finland provide universal, tax-funded, public long-term care ser-

vices as an integral component of welfare and health-care services for the entire population. The co-

payments for care are however means-tested and in some countries high in levels. While the overall

responsibility for the care of elderly and disabled rests with a public authority: the state, local au-

10

thority or individual municipality the main feature of these countries is the large autonomy of local

governments (e.g., municipalities, counties, councils) in organising service provision and in financ-

ing care, including the right to levy taxes at local government levels (Karlsson and Iversen, 2010).

In a tax based system the state typically contributes to financing by paying non-earmarked subsidies

either to municipalities (e.g., Finland) or to regional authorities (e.g., Denmark), adjusted to the

population structure and need. Public long-term care services are broad and comprehensive, result-

ing in a relatively large share of GDP spent on LTC – ranging from 2% in Denmark to 3.6% in

Sweden.

Beside personal-care support in institutions and at home, they can include for example help with

domestic care (Denmark, Sweden, Finland), as well as the provision of sheltered housing, home

adaptations, assisting devises and covering transport costs (OECD, 2008). Out-of-pocket payments

for LTC account for relatively low shares of financing (although high in individual levels), for ex-

ample around 4% of revenues in Sweden, and the private contributions to cost are capped in Swe-

den and Norway. In Finland the institutional population have a 100 euro a month protected income

share of personal income.

Finland provides universal coverage within a single system of municipal services for LTC-care for

all citizens. The financing is through municipal taxes (60 percent), state grants to municipalities (31

percent) and the rest are clients’ out-of-pocket payments (9 percent). Municipal in-kind services

cover institutional care in elderly homes, sheltered housing and home care services. There are also

benefits in cash payments and vouchers available for care. One can however opt-out of municipal

services by purchasing private care (OECD, 2011). The old-age benefits in kind were 2 billion euro

and benefits in cash 16 billion euro in 2009 which account in total for 10,5 percent of GDP, 1,2 per-

cent in-kind and 9,3 percent in-cash respectively, (Esspros data – National Institute for Health and

welfare, Finland).

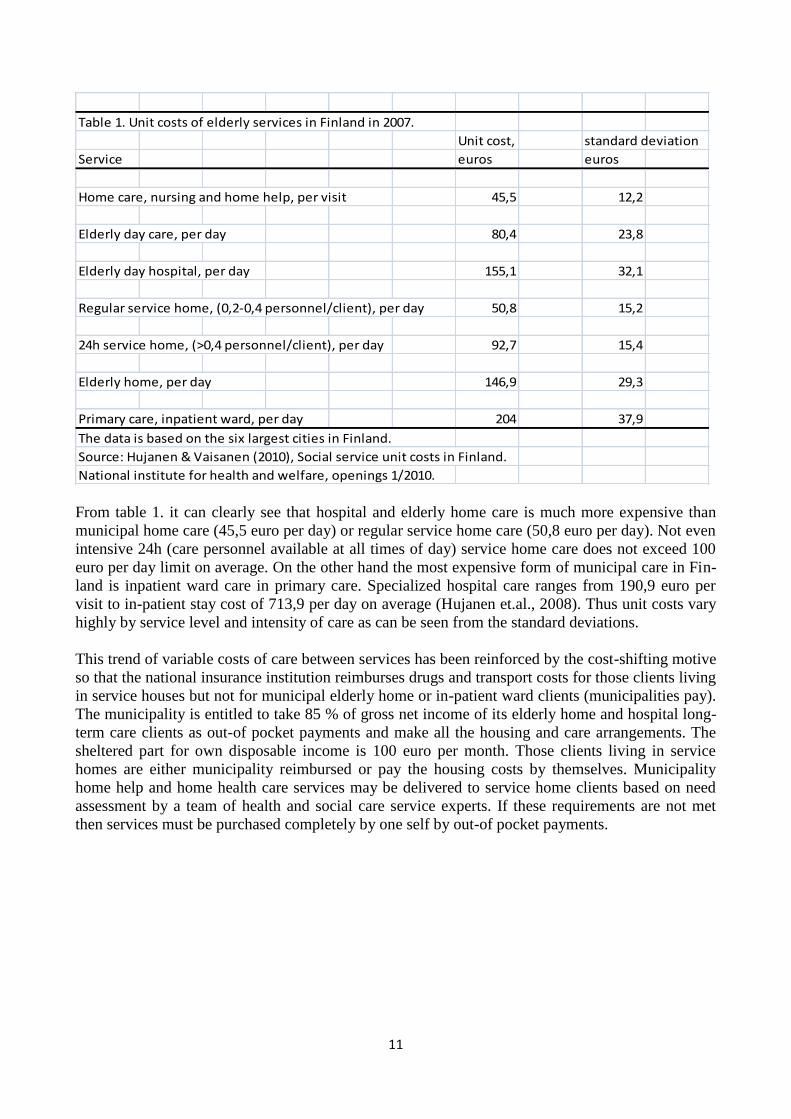

Long-term care services and costs in Finland

Following the fact that Finland has a multi-channel funding system for health and long-term care on

the other hand and highly variable unit costs between service levels it follows that municipalities

have switched elderly homes to service home status (also known as sheltered housing) and bought

service home care for their residents (Pekurinen; 2010). This due to cost-shifting motives. For ex-

ample some clients get medicine reimbursements from the national insurance institution and others

from the municipality. Thus the municipalities have moved clients to state medicine reimbursement

covered services. Some basic information on prices of home care and institutional formal are pre-

sented in the following table 1. It displays the costs of elderly care in the 6 largest cities in Finland.

The system described in short above makes it a many tier reimbursement and out of pocket frame-

work. The lightest form of municipal elderly services is home nursing and home help (including

meals on wheels) delivered to the elderly person’s own home. The first step towards institutional

care can be described as is living in a regular service home at own cost and being drug reimbursed

by the national insurance institution. The general definition of institutional care in Finland is living

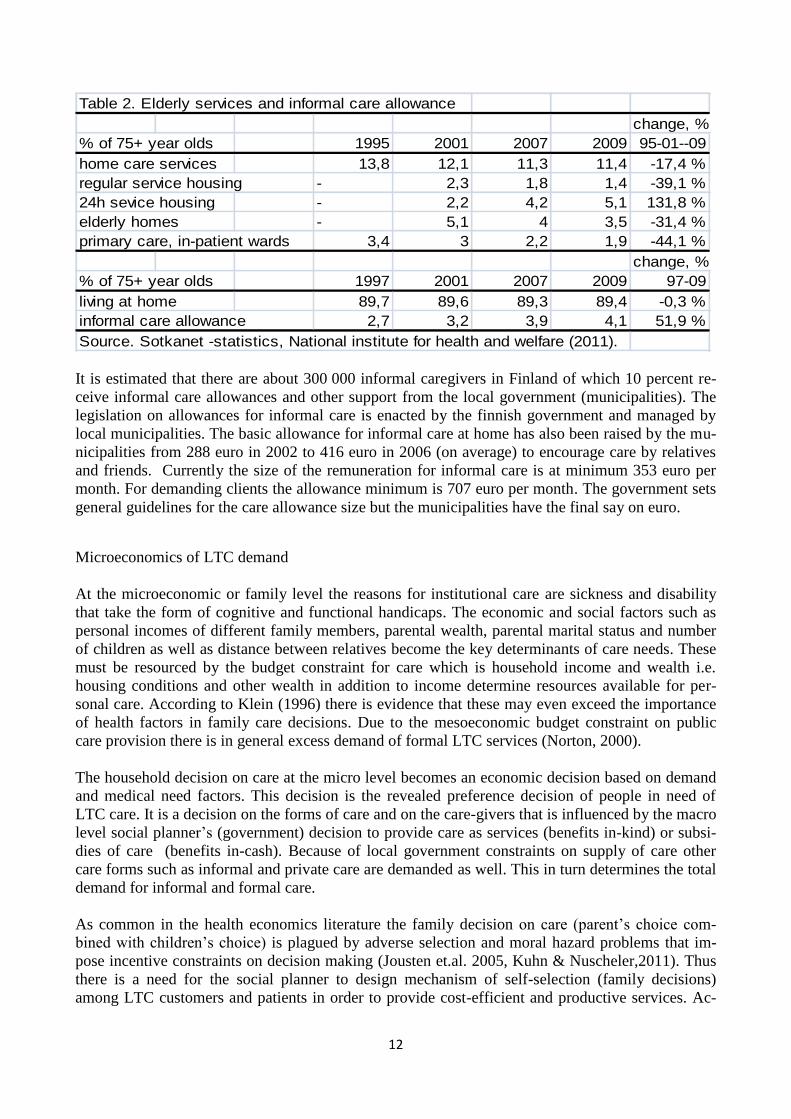

in a 24h service home or elderly home or being in in-patient care. The following table 2. gives in-

formation on services and informal care.

11

Table 1. Unit costs of elderly services in Finland in 2007.

Unit cost, standard deviation

Service euros euros

Home care, nursing and home help, per visit 45,5 12,2

Elderly day care, per day 80,4 23,8

Elderly day hospital, per day 155,1 32,1

Regular service home, (0,2-0,4 personnel/client), per day 50,8 15,2

24h service home, (>0,4 personnel/client), per day 92,7 15,4

Elderly home, per day 146,9 29,3

Primary care, inpatient ward, per day 204 37,9

The data is based on the six largest cities in Finland.

Source: Hujanen & Vaisanen (2010), Social service unit costs in Finland.

National institute for health and welfare, openings 1/2010.

From table 1. it can clearly see that hospital and elderly home care is much more expensive than

municipal home care (45,5 euro per day) or regular service home care (50,8 euro per day). Not even

intensive 24h (care personnel available at all times of day) service home care does not exceed 100

euro per day limit on average. On the other hand the most expensive form of municipal care in Fin-

land is inpatient ward care in primary care. Specialized hospital care ranges from 190,9 euro per

visit to in-patient stay cost of 713,9 per day on average (Hujanen et.al., 2008). Thus unit costs vary

highly by service level and intensity of care as can be seen from the standard deviations.

This trend of variable costs of care between services has been reinforced by the cost-shifting motive

so that the national insurance institution reimburses drugs and transport costs for those clients living

in service houses but not for municipal elderly home or in-patient ward clients (municipalities pay).

The municipality is entitled to take 85 % of gross net income of its elderly home and hospital long-

term care clients as out-of pocket payments and make all the housing and care arrangements. The

sheltered part for own disposable income is 100 euro per month. Those clients living in service

homes are either municipality reimbursed or pay the housing costs by themselves. Municipality

home help and home health care services may be delivered to service home clients based on need

assessment by a team of health and social care service experts. If these requirements are not met

then services must be purchased completely by one self by out-of pocket payments.

12

Table 2. Elderly services and informal care allowance

change, %

% of 75+ year olds 1995 2001 2007 2009 95-01--09

home care services 13,8 12,1 11,3 11,4 -17,4 %

regular service housing - 2,3 1,8 1,4 -39,1 %

24h sevice housing - 2,2 4,2 5,1 131,8 %

elderly homes - 5,1 4 3,5 -31,4 %

primary care, in-patient wards 3,4 3 2,2 1,9 -44,1 %

change, %

% of 75+ year olds 1997 2001 2007 2009 97-09

living at home 89,7 89,6 89,3 89,4 -0,3 %

informal care allowance 2,7 3,2 3,9 4,1 51,9 %

Source. Sotkanet -statistics, National institute for health and welfare (2011).

It is estimated that there are about 300 000 informal caregivers in Finland of which 10 percent re-

ceive informal care allowances and other support from the local government (municipalities). The

legislation on allowances for informal care is enacted by the finnish government and managed by

local municipalities. The basic allowance for informal care at home has also been raised by the mu-

nicipalities from 288 euro in 2002 to 416 euro in 2006 (on average) to encourage care by relatives

and friends. Currently the size of the remuneration for informal care is at minimum 353 euro per

month. For demanding clients the allowance minimum is 707 euro per month. The government sets

general guidelines for the care allowance size but the municipalities have the final say on euro.

Microeconomics of LTC demand

At the microeconomic or family level the reasons for institutional care are sickness and disability

that take the form of cognitive and functional handicaps. The economic and social factors such as

personal incomes of different family members, parental wealth, parental marital status and number

of children as well as distance between relatives become the key determinants of care needs. These

must be resourced by the budget constraint for care which is household income and wealth i.e.

housing conditions and other wealth in addition to income determine resources available for per-

sonal care. According to Klein (1996) there is evidence that these may even exceed the importance

of health factors in family care decisions. Due to the mesoeconomic budget constraint on public

care provision there is in general excess demand of formal LTC services (Norton, 2000).

The household decision on care at the micro level becomes an economic decision based on demand

and medical need factors. This decision is the revealed preference decision of people in need of

LTC care. It is a decision on the forms of care and on the care-givers that is influenced by the macro

level social planner’s (government) decision to provide care as services (benefits in-kind) or subsi-

dies of care (benefits in-cash). Because of local government constraints on supply of care other

care forms such as informal and private care are demanded as well. This in turn determines the total

demand for informal and formal care.

As common in the health economics literature the family decision on care (parent’s choice com-

bined with children’s choice) is plagued by adverse selection and moral hazard problems that im-

pose incentive constraints on decision making (Jousten et.al. 2005, Kuhn & Nuscheler,2011). Thus

there is a need for the social planner to design mechanism of self-selection (family decisions)

among LTC customers and patients in order to provide cost-efficient and productive services. Ac-

13

cording to Pestieau & Sato (2008) there have to be care budget equalizing choices on the table for

clients (keeping equal shares of public budget to different care forms). This creates true opportunity

for freedom of choice.

Economic decisions on informal care are determined according to literature by bequests, inter-vivos

transfers, government subsidies on informal care and private insurance (notwithstanding altruism

within the family). Economic decisions on formal care are primarily based on relative prices of care

types, availability of informal care, household wealth and income and government provision of care

(coverage and eligibility). The decision making framework can be either an economics principal-

agent or game theoretic framework. The outcomes can be at best be Nash equilibriums with Pareto

efficiency. Adverse selection and moral hazard separate for first and second best welfare economics

solutions which can in some cases coincide with one another (Kuhn & Nuscheler, 2011). In a

framework of imperfect information the government must decide on subsidies (tax credits, vouch-

ers, benefits-in-cash) and service provision (coverage, eligibility, access) for families in deciding on

optimal care (Pestieau & Sato, 2008; Norton, 2000).

Inter- and intra-generational decision of LTC - the family as a production unit.

The decision making units are the government and the family (see for example Pestieau & Sato,

2008). The family consists of parents and their children, usually of a composite model of one parent

and one child –family type which can produce informal care or buy formal care from the market.

The economic theory is most often based on stage gaming where the government first sets econom-

ic incentives and the family makes decisions based on those incentives. The decision maker within

the family is first the elderly parent taking the child response as given. Secondly the children or a

child make decision(s) in the last stage after observing what the elderly has decided. If the parent is

mentally unaware then his or her child is assumed to be the only decision maker in the family. The

following timeline figure describes the structure of the usual family decision (Eisen & Sloan, 1996).

14

Figure 1. Government and family decision on LTC care.

The decision framework for LTC care is described in figure 1. in detail as a process in time. This is

the framework of for example the Eisen & Mager model (1996) of formal and informal care de-

mand. In economic models of informal and formal care this is treated as a three or two stage game

which is solved by a backward induction technique. The principal is the parent(s) and the agent(s)

are the children. The information within the family is complete but private. The social planner

(government) faces this fact and is optimizing in a second best framework. For benchmark reasons

the research papers also calculate the first best solution of the social planner.

The principal’s optimization problem (decision 1.) taking his or her adult children’s behavior and

the economic constraints and subsidies set by the government as given. The principal can be seen as

a Stackelberg game leader (Eisen & Mager, 1996). Based on anticipated child behavior (altruism,

economic incentives) the principal either buys formal care (LTC insurance) or makes financial sav-

ings and investments for old age to give strategic bequests to children. If the children (or at least

one of them) is expected to provide informal care with certainty then the elderly possibly does not

buy insurance or make substantial savings. The models place much emphasis on the elderly parent

as the dictator of the care decision framework at the micro or household level. He or she must make

informed decisions based on given government policy and children’s behavioral response (Norton,

15

2000; Eisen & Mager, 1996; Zweifel & Struwe, 1996). Children respond to parental decision by

providing informal care in time or money depending on their level of altruism, productivity in the

labor market and parental transfers of wealth (bequest, inter-vivos transfers).

Children provide care to their parents in-kind or in-cash. The decision to provide in-kind care as

time devoted to personal care activities (home help, shopping, etc.) is well studied in the literature.

Zweifel & Nocera (1996), Zweifel & Struwe (1996), Eisen & Mager (1996), Norton & Van Hout-

ven (2004) study this decision thoroughly in light of economic theory. The effects of devoting fi-

nancial resources (cash) into care of a dependent parent are much less studied. These are handled in

more recently studied in Kuhn & Nuscheler (2011), Pestieau & Sato (2008) and Jousten et.al.

(2005). The general result is that children with relatively low productivity (in the labor market) de-

vote time to informal care and high productivity children provide informal care as in-cash transfers

to parents (to buy formal care).

The formulation of Rees (1990) that the principal-agent model contains a principal optimization

problem given reaction function(s) and a cooperative or non-cooperative sub game to be played

among agents has become the standard in economics of family decisions. There exist different pos-

sibilities to model the sub game (decision 2.). Either we choose to play a game leading to Nash

equilibrium that is to play a game where each participant makes his or her decision taking the other

players decisions as given or there is cooperative behavior among the children. From game theory it

is known that cooperative games produce Pareto-optimal outcomes (Eisen & Mager; 1996). This

means that no one can be made better off without someone being made worse-off. argue that this

approach is plausible in the present framework where the actors are attached to each other by family

ties and personal relationships. Altruism should thus be expected to play a major role. Producing a

surplus utility for care from relationship such as the family normally requires commitments and

long-term contracts which characterizes any cooperative behavior. Honoring the inter-generational

agreement is key (i.e. I cared for you when young, now you care for me when I’m old).

Game theoretic analysis on the other hand concentrate on the maximization of individual utilities.

They are structural models that incorporate strategic family bargaining and cash transfers between

children (Stern, 1994, Engers & Stern, 2002). The aim of the transfers is to agree upon a primary

care-giver who is almost completely responsible for care. This requires a implicit or explicit con-

tract among family members. These games are cooperative or non-cooperative by nature. In this

context cooperative games result in Pareto-optimal solutions where as non-cooperative do not in

general. The internal allocation of production and services are determined by bargaining power of

the family members. It can be however argued that in the presence of moral hazard and adverse

selection there are gains from breach of contract and free-riding (i.e. children giving no informal

care) Furthermore, non-cooperative equilibrium points are in general not Pareto-optimal (Eisen &

Mager, 1996).

In Eisen and Magers (1996) theoretical model of family bargaining in a game theoretical framework

the game is a cooperative game with rational negotiations. The maximum utility attainable is the

sum of all family members utilities. First there are changes in the environment that have conse-

quences for the individual outcomes. These are changes in public subsidies and old-age care sys-

tems. Second the so called threat points are points that are determined by past family decision on

savings, insurance, labor force participation. Using the Nash equilibrium concept the authors show

16

that the family’s maximum utility is the utility frontier and efficient bargaining solutions must be on

this frontier. The threat points lie inside the frontier and are sub-optimal from a co-operative point

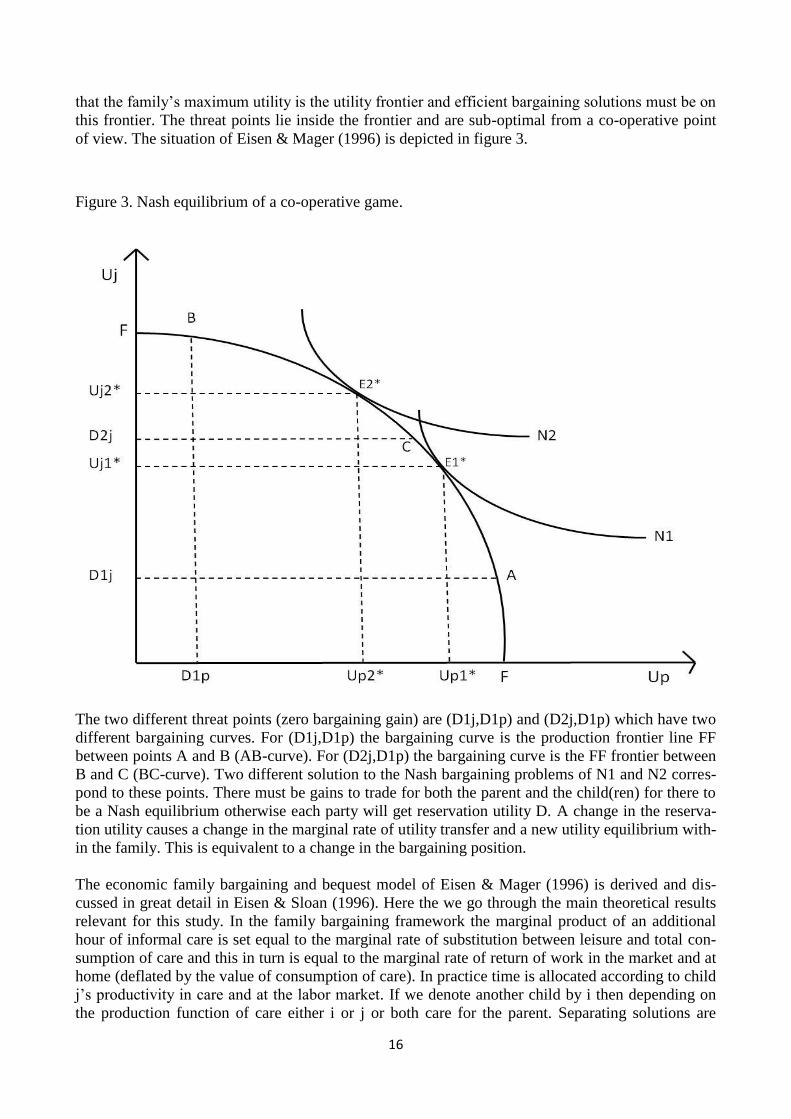

of view. The situation of Eisen & Mager (1996) is depicted in figure 3.

Figure 3. Nash equilibrium of a co-operative game.

The two different threat points (zero bargaining gain) are (D1j,D1p) and (D2j,D1p) which have two

different bargaining curves. For (D1j,D1p) the bargaining curve is the production frontier line FF

between points A and B (AB-curve). For (D2j,D1p) the bargaining curve is the FF frontier between

B and C (BC-curve). Two different solution to the Nash bargaining problems of N1 and N2 corres-

pond to these points. There must be gains to trade for both the parent and the child(ren) for there to

be a Nash equilibrium otherwise each party will get reservation utility D. A change in the reserva-

tion utility causes a change in the marginal rate of utility transfer and a new utility equilibrium with-

in the family. This is equivalent to a change in the bargaining position.

The economic family bargaining and bequest model of Eisen & Mager (1996) is derived and dis-

cussed in great detail in Eisen & Sloan (1996). Here the we go through the main theoretical results

relevant for this study. In the family bargaining framework the marginal product of an additional

hour of informal care is set equal to the marginal rate of substitution between leisure and total con-

sumption of care and this in turn is equal to the marginal rate of return of work in the market and at

home (deflated by the value of consumption of care). In practice time is allocated according to child

j’s productivity in care and at the labor market. If we denote another child by i then depending on

the production function of care either i or j or both care for the parent. Separating solutions are

17

possible (i.e. some children specialize in only work at the market). The probability of frailty (p,

nature’s choice, figure 1.) determines the amount of LTC insurance bought (premiums paid).

The model comparative statics operates through bargaining and wealth effects. The increase in pa-

rental wealth increases formal care demanded and increases bargaining power of the parent. An

increase in the price of formal care decreases the bargaining power of the parent and decreases the

amount of formal care demanded. An increase in the wage rate increases the bargaining power of

each child who works in the labor market and for all children together this decreases informal care.

An increase in LTC insurance coverage strengthens the bargaining power of the parent and because

of the wealth effect formal care demanded increases. These are the results of a principal-agent prob-

lem which is a parent’s decision in the first and co-operative game in the second stage.

The limitations and caveats of the above described model are couples with no children and parents

who are mentally unaware in decision making. However in the case of mentally unaware parents

Sloan & Hoerger & Picone (1996) present a model in which children make all the decisions neces-

sary. The model of Eisen & Mager (1996) abstracts from the moral hazard problem and equalizes

bequests among children. Despite these shortcomings it gives highly powerful predictions and re-

sults.

From economic models of LTC care we have thus learned that altruism prevails (Jousten 2005;

Kuhn & Nuscheler, 2011; Frey & Meier, 2004) or bequest motives may be needed to keep family

and friends motives in check according to Zweifel & Struwe (1998) and Eisen & Mager (1996). For

bequests to induce informal care both the principal and the agent have to be risk-averse in financial

behavior e.g. formal care expense avoiders. The bequest can come also in the form of an inter-vivos

or ex-ante transfers before the risks materialize which makes them more effective according to Pes-

tieau & Sato (2008). However the gain from ex-post bequests is that they will keep informal care-

givers “in-check” for a longer period. In international research literature on inter-generational trans-

fers they are seen as the economic motive for informal care besides intrinsic altruism and family

ties.

Economics of informal care – substitute or complement to formal care?

Van Houtven and Norton have presented a very simple and appealing model of informal care de-

mand which is slightly modified in this paper (Van Houtven & Norton 2004, Van Houtven, 2004).

As opposed to models by Zweifel et.al. (1996, 1998) with only monetary incentives the model in-

cludes altruistic behavior by the caregiver (spouse, child). This is done by including the care reci-

pient’s utility function in the caregivers utility function. Thus the caregiver receives utility from the

well-being of the care recipient (elderly). The theoretical model is based on a basic principal-agent

model where there is a single principle and many agents.

First we tackle the effect of informal care on formal care probability. The starting point is usually

altruistic family bargaining where the caregiver optimizes her own utility function by including into

it a part of the recipient’s utility function (Van Houtven, Norton, 2004). The care recipient optimiz-

es utility with respect to formal care and consumption taken informal care as given. The caregiver

optimizes (usually her) utility with respect to informal care, consumption and leisure. As a result of

informal care the care recipient has better health status and needs to purchase less formal care which

leaves more resources for other consumption purposes. The results for the caregiver indicate that

the higher the wage or more preference for consumption he/she the less informal care is given.

18

The theoretical model is a two stage model. In the first stage the agents maximize utility subject to

their budget constraints. In the second stage the principal maximizes his/her utility taking into ac-

count the informal care received and his/her budget constraint. The decision variables for caregivers

(agents) are consumption (X), leisure (L), informal care hours per diem (A). The decision variables

for the care recipient (principal) are functional ability (h) as function of formal care (M) and con-

sumption (X). For the principal leisure (L) is a residual variable which is perfectly determined by

optimization of M and X.

The principal’s utility maximization problem with respect to M and X (given exogenous C

iA ) is the

following:

(1)

*

,1

max ( , , , ( , , ))Cp P

X

npP P P C P P

iM Xi

P m P P

U X L A h A M E

Y p M p X

,where Y is principal income and p’s are prices of formal care and consumption. The first order

conditions (FOC) with respect to ( , )P PM X are:

(2)

' ' 0Pm

P h M

dLU h p

dM

(3)

' 0PX

P X

dLU p

dX

mathematically rearranging equations (2) and (3) we get:

(4)

' '

'

P

X

hM

XP

h M

X

MU

MU

U hp

p U

From equation (4) we see that in optimum the principal sets the ratio of marginal utilities from func-

tional ability and consumption equal to price ratio of formal care and consumption. The higher is

the price of formal care the more informal care is needed to obtain same functional ability without

reducing care recipient’s consumption level of other goods. Totally differentiating equation (2) with

respect to A we get:

(5) 2 0M MM MA A MA Ahh h h hh

U h M U h M U h U h h

Rearranging terms this can be written:

(6) 2M MM MA MA Ahh h h hh

M U h U h U h U h h

, or

(7) 2

* MMA Ah hhA

M MMhh h

U h U h hMM

A U h U h

,

From equation (7) it is possible to make inferences on the marginal effect of informal care hours on

formal care purchase. The theoretical model is interested in the sign of this effect. We assume strict-

19

ly increasing and concave utility functions. Therefore decreasing returns to scale apply to formal

and informal care. It is assumed in the model that the marginal effect of formal care ( Mh >0) and

informal care ( Ah >0) is positive on functional ability. It is also assumed that utility is concave

function ( 0, 0MM AAh h ). By producing equation (7) in signs form we see that the only unknown

term with respect to sign is ?MAh ,which is marginal productivity of formal and informal care

combination on functional ability (Van Houtven & Norton, 2004). Now we have three different

cases by sign of the partial derivative MAh . which reduce by simple inspection into two cases (the

zero case is trivial to see). If and only if we have equation (9A) valid

(9A) 0MAh or 0MAh , then it holds that:

(10A) 0AM ,

comparative statics negative, and informal care (A) is a substitute for formal care (B) and thus in-

creasing informal care reduces the need for formal care and increases consumption possibilities. On

the other hand if and only if we have equation (9B) valid

(9B) 0M AhhMA

h

U h hh

U

, then it holds that:

(10B) 0AM ,

comparative statics positive, and informal care (A) is a complement to formal care (M) and thus

increasing informal care increases formal care and decreases consumption possibilities. Note that

the condition 0MAh is not enough for informal and formal care to be complements but some

leverage is needed for this to be achieved. Thus we have established the requirements for informal

care and formal care substitution and complementary relationships. It can be noted that the demand

price elasticity’s with respect to formal care price and consumption price together with changes in

Y’s as income effect determine formal care use (M) and consumption (X). The optimization prob-

lem of the altruistic caregiver (agent, spouse or child) with respect to care giving hours (A), con-

sumption (X) and leisure (L) by taking into account the care recipient (principal):

(9)

*

, ,1

max ( , , , ( , , ))

s.t. ( )

C C C

npC C C C C P P

iA X Li

pc C C C m X C

U X L A h A M E

w T L A C p M p X

Note that time can be standardized for example as 24 hours a day, 168 hours a week or by some

other hourly measure. In the model all caregivers i =1,…,n are assumed to have equal productivity

which contradicts the Zweifel & Nocera model (1996). The first order condition for optimal beha-

vior of agent i are as follows (FOC):

? ?( )( ) ( )( )( ) ( )*( )( ) ( )( ) ( )

MA MAA

h hMM

A

20

(10) ' 0CC

C L

dLU w

dL

(11) ' 0CX

C X

dLU p

dX

(12) ' '' ' 0C C CCi i

hA A L

dUU U h U

dA

From equations (10), (11) and (12) we get by rearranging and combining terms:

(13)

'

'

CC L

XXC

L

X

U MUw

MUp U

(14)

' '

, ( 0)'

C Ci

Ci h

L AU U

dh

dA U

For equation (14) to be according to assumptions of the model, increases in informal care have to

increase functional ability of the principal (eq. 14. is positive in sign) and we get :

(15) ' 'C C

iL AU U

From equation (13) we find that the labor market wage and the product market price –ratio equals

the marginal utility ratio from consumption and leisure. Thus the care decision is not involved in

preferences on free time and consumption. We need to assume equation (15) to get rational results

for informal care. Nobody would demand or provide informal care in the model if its impact was

negative on the principal’s functional ability. Therefore the marginal utility from leisure must be

higher than the marginal utility from care giving (which is also assumed positive) in equation (15).

From the model we see that the higher are the labor market wages, higher consumption prices and

the lower formal care prices the less informal care is provided. With high out-of-pocket payments

for formal care there are strong economic incentives to avoid institutionalization and increase in-

formal care at home by relatives.

Bequest and income transfer motives of informal care

In general there exist bequests of four different types according to inter-generational utility consid-

erations economics literature (Gale & Slemrod, 2001). These are unintentional bequests, altruistic

bequests, strategic bequest motives and of pure joy of giving type bequests. The essential difference

between these is the utility awareness of the elderly person in making decisions. The unintentional

and joy of giving motives are non-utilitarian in the the utility of the giver or receiver is not consi-

dered ex-ante. Oppositely in the strategic and altruistic motives there are ex-ante considerations of

either utility for the parent or the children. Strategic bequest are given for informal care reasons and

altruistic ones for reason of income equality of children.

The empirical evidence is thus less clear cut on motives. In addition there may be mixed motives of

all four types which make bequests theoretically manageable but empirically harder to disentangle.

21

Lassila, Rantala and Valkonen (2002) summarize it as giving evidence for strongly heterogeneous

behavior among parents and mixed motives. Eisen & Sloan (1996) point out there is some evidence

of strategic bequest behavior in US data. This is related to phone calls and visits to parents by child-

ren. The literature gives also little guidelines on the savings incentives of taxation of bequests (Las-

sila et.al., 2002). In Finland the bequest motive has also been studied by Kruhse-Lehtonen (1995)

who gives evidence that there are no differences in total consumption between couples with and

without children. However there is finnish evidence that those with children have higher wealth and

higher propensity to save just before retirement. This is evidence for a strategic bequest motive.

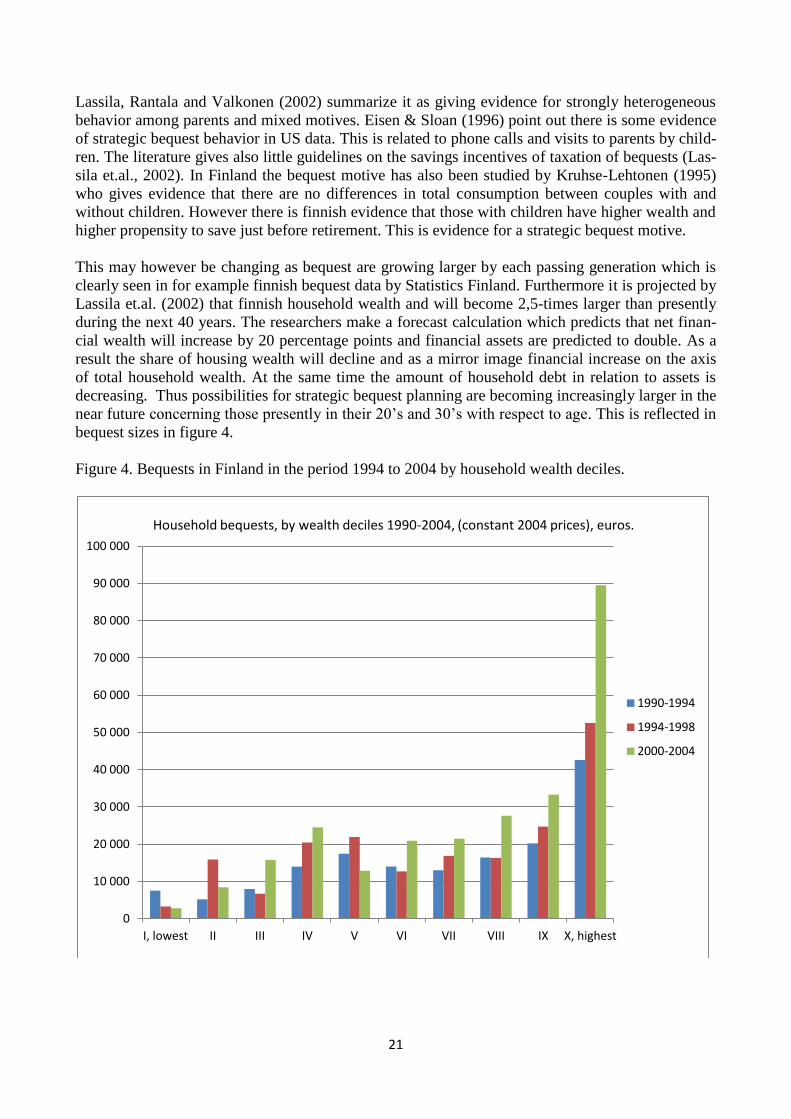

This may however be changing as bequest are growing larger by each passing generation which is

clearly seen in for example finnish bequest data by Statistics Finland. Furthermore it is projected by

Lassila et.al. (2002) that finnish household wealth and will become 2,5-times larger than presently

during the next 40 years. The researchers make a forecast calculation which predicts that net finan-

cial wealth will increase by 20 percentage points and financial assets are predicted to double. As a

result the share of housing wealth will decline and as a mirror image financial increase on the axis

of total household wealth. At the same time the amount of household debt in relation to assets is

decreasing. Thus possibilities for strategic bequest planning are becoming increasingly larger in the

near future concerning those presently in their 20’s and 30’s with respect to age. This is reflected in

bequest sizes in figure 4.

Figure 4. Bequests in Finland in the period 1994 to 2004 by household wealth deciles.

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

80 000

90 000

100 000

I, lowest II III IV V VI VII VIII IX X, highest

1990-1994

1994-1998

2000-2004

Household bequests, by wealth deciles 1990-2004, (constant 2004 prices), euros.

22

Altruism among family members is the most likely and plausible explanation of why informal care

is given to the elderly (Eisen et.al., 1996). This is however hard to measure in economics ways.

However in common sense it is easy to understand that people get married and have children also

for the motives of care. It is hard to imagine a relationship between family members without no

compassion and inter generational altruism. And there is economic evidence in favor of altruistic

behavior among the general population that this for example given by Frey & Meier (2004). They

argue that there exists (intrinsic) altruism even in the case of anonymous beneficiaries from public

goods. This is the case although also peer effect influence decision making (i.e. what the other do-

nators contribute).

The case that the authors study is contribution to student funds in an university setting in which they

use survey data linked to actual donation registers. The sample is panel data with 136 000 observa-

tions. The results indicate that a substantial share of the population are willing to donate to charity

based on free choice even with anonymous beneficiaries (level effect). Peer effects come in a way

that the more other people are anticipated to co-operate the more people behave altruistically (see

more on peer effects in Angrist &Pischke, 2009). However the participation must be by generally

acceptable conditions. The study concludes that different people have different degree’s of pro-

social behavior after age and gender are standardized (related to different preferences and shape of

utility function).

First and second best models of demand and supply of care – effects of imperfect information.

The model of long-term care presented by Pestieau and Sato (2008) is perhaps the most interesting

one. They present an optimal policy of the state (social planner) with perfect and imperfect informa-

tion about the client structure. The policy parameters of the social planner are: income tax of rate t,

subsidy to informal care (sigma), long-term care private insurance subsidy (tau) and nursing home

quality g. The decision parameter of the parent is G that represent inter-vivos intergenerational

transfers to the child. This may take the form of a gift, testament or pre-mortum bequest. The parent

faces a probability of (phi) needing LTC care and probability of (1-phi) of not needing LTC in life

course. Given the inter-vivos transfer (G) the child, with productivity w, then decides on informal

care in-kind (own time) denoted by h or in-cash (care payments) denoted by s. Note that it assumed

that w is drawn from a stochastic distribution with cumulative density function F(w) for the children

population. The productivity of caring activities w0 is assumed same across the population of child-

ren. However if the parent opts to go to a public nursing home or for a private insurance policy the

child will get no inter-vivos transfer and gives no informal care. The authors allow for heterogeneity

of wealth (I) for parents. After that the authors present optimal policy from the welfare economics

point of view in the first and second best cases. The decision makers are the social planner, parent

and the child in this ordering.

In the model it is assumed that there is private information on To keep matters simple yet robust to

changes in assumptions (and enough general) the authors assume Cobb-Douglas specification and

additively separative utility functions for the one-parent and one-child. The child is altruistic with

parameter (0<beta<1) towards his/her parent and includes parental utility in his/her decision mak-

ing. The authors solve their model by backward induction and derive comparative statics results.

The main findings that come out from the Pestieau & Sato (2008) model are the following. proposi-

tion 1. states that if there is no LTC insurance market available, or if parents have a low endowment

of wealth (I), the informal care of low-wage children to their dependent parents takes the form of

devoted time to caring activities (in-benefits) and declines with child’s earnings capacity in the la-

23

bor market until it is equal to the child’s nursing productivity (which is assumed same for all child-

ren).

After that threshold point the child will resort to financial assistance (in-cash) of his/her parent and

devotes no time to care. In proposition 1. (ibid.) if there is a market for LTC insurance then and

parents have sufficient wealth endowments then there is an intermediate range of children’s wages

for which the parents prefers to buy insurance or care instead of informal care. Outside this range

the parents are always willing to make an ex-ante gift(s) of size G to ensure informal care in the

case of needing LTC. As there is no social planner present this is called the “laissez-faire” equili-

brium of LTC care.

Introducing the social planner with full information on case-mix of parent-child combinations and

total control of the economy allows the maximization of a social welfare function. The welfare

function is additive and is a utilitarian welfare function but the weighting of children’s and parents’

utilities is different (also different utilities for different generations). Here the weights are both set

to equal one. In equilibrium all the partial derivatives of individual utility functions must be equal

including the utility from informal care function. For this optimum to be a plausible one, there

would need to be markets between families for informal care (not just within families). One would

also need individualized transfers allowing for redistribution of wealth across individuals, inter-

generationally and between the two states of the parent dichotomy. (independent or dependent of

care)

When the social planner has imperfect information on family types the following results appear as a

result of self selection mechanism induced by financial incentives described earlier. Proposition 2.

states that when the government instruments are restricted to a flat tax rate t and subsidy on child’s

informal care (sigma) the level of both of these incentive parameters is likely to be high when par-

ents have a low wealth endowment and when the majority of children have a labor market produc-

tivity below w0. In other words there is much scope for informal care and the social planner acts

according to this care environment.

The authors show that self selection of the two types of parents can be part of optimal policy of the

social planner when there are different wealth levels in the elderly parent population. When parents

have heterogenous wealth endowments (high and low for simplicity), it might be socially desirable

to choose policy instruments in a way that induces high wealth parents to choose private LTC insur-

ance and those parents with low wealth endowment to choose public nursing home care. This sepa-

rating solution is more likely when there is a wide difference between high and low wealth values

or continues distributions of wealth have high variance or fat tales (pareto distribution).

To conclude Pestieau et.al. (2008) find that informal care of children can be of two types: time allo-

cated to care (in-kind) by low labor productivity children (small work income) and in-cash allocated

as transfers by high productivity children (high work income). The authors find that parents of mid-

dle-income children tend to rely on public nursing home care. However in the case of nursing home

care or private insurance they make no inter-vivos transfers (ex-ante gifts) to their children. Private

insurance is a substitute for nursing home care but not for children’s informal care. The case of pub-

lic nursing home provision (including sheltered housing) is strong when private long-term care

markets are underdeveloped and inefficient.

Vica versa long-term insurance subsidies are viable when costs of public nursing care are high

compared to private care (in the unit cost sense). The case for subsidizing informal care or private

insurance is unclear however and depends on health system type. For redistributive concerns a

24

scheme of tax subsidy for insurance premiums is desirable in general, as it tends to narrow down

differences in consumption patterns among the population. On the other hand it can have undesira-

ble effects on informal care and distort the levels of inter-generational transfers. If family care type

(low or high need of LTC-care) can not be observed by the social planner then we are faced with a

traditional moral hazard problem. Thus families tend to over-report the level of care needs to obtain

higher benefit and care levels or it is possible that children reduce effort with growing informal care

benefits that is they have lower extrinsic motives (Kuhn & Nuscheler, 2011).

Substitution effects between care types: relationship between informal and formal care.

Adverse selection and moral hazard issues arise also in Kuhn & Nuscheler (2011) and Jousten et.al.

(2005). Regarding Kuhn et.al. paper the supply of informal and formal care is subject to adverse

selection of dependency type. There is available formal home care or institutional care by nursing

homes. Adverse selection is modeled as private information on parent type. The information rents

come in a manner that families with low (L) dependency members start to mimic high (H) depen-

dency families in expectation of better care assistance and supply from the government. In their

model there are two types of care needs for parents, that is high and low levels. The model is again

one parent - one child family type. The parent gets informal care from the child in sense of benefits

in-cash and there is a disutility associated with institutionalization ( ) and the productivity of a

nursing home is given by ( ). The care at home is formal but funded by potential informal ca-

regivers (children). Thus also more dependent case-mixes can be handled by professional care. The

model introduces a model with only home care and then adds supply of nursing homes to it.

Under perfect information the social planner (state or government) can set informal care allowances

and nursing home prices so that there is a first best optimal policy of giving care at home to the low

dependency parents and nursing home care to high dependency parents. In the first best case con-

sumption across children of different families is equal in equilibrium (redistribution of income) and

more care is provided to those in higher need. However there is a difference between care at home

and nursing home care. In an equilibrium without nursing homes the difference in quantity of care

received by type smaller than with institutional care available. Therefore supply and access to insti-

tutional care favors those with higher care needs in the sense that they receive a larger share of the

care budget. As a result, in a pure home care setting the L-type’s child pays taxes and H-type’s child

receives subsidies. In a setting of nursing home and home care both available, both types pay taxes,

services are provided by type classification (home for L-type and nursing home for H-type). It is

important to note that both type’s consumption is lower when nursing homes are supplied. The

productivity increases of nursing home care increase welfare when there is no disutility present oth-

erwise the disutility of nursing care increases with productivity gains. The provision of nursing

home care is efficient when productivity gains are high enough to offset increasing disutility (the

function is increasing and convex). Then an area of welfare gains lies under this curve and is

zero at the curve (Kuhn & Nuscheler, 2011).

The interesting result of the described Kuhn et.al. (2011) asymmetric information model of demand

and supply is that there exists a range of parameters that make provision of institutional care

optimal under asymmetric information but not under full information. This means that there is

excess supply of care in the adverse selection case. There exists also the opposite case but it very

hard to argument for in practice. The disutility of nursing home care facilitates self selection of

clients and makes first best solution attainable for the government. Then efficient levels of home

care and nursing home care are provided and consumption smoothing between families adopted.

However when productivity of nursing homes is low the level of institutional care is below first best

under adverse selection. Then the redistributing element is lost and self selection is not available.

25

The model is restrictive in that the zone for the intersection of first and second best is strictly li-

mited. In summary by expanding the model by making the key parameters endogenous produces as

a result weaker hotel quality in relation to medical quality . The source of financing, public