Embed Size (px)

DESCRIPTION

Citation preview

Page 1 of 7

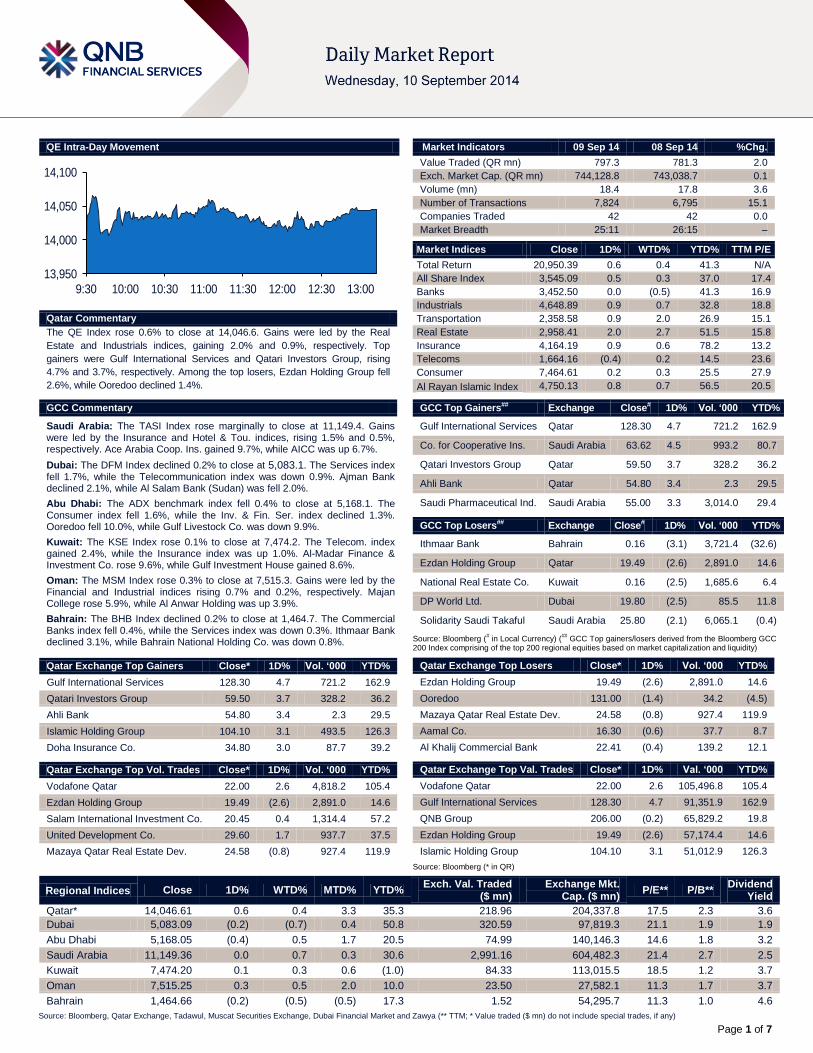

QE Intra-Day Movement

Qatar Commentary

The QE Index rose 0.6% to close at 14,046.6. Gains were led by the Real

Estate and Industrials indices, gaining 2.0% and 0.9%, respectively. Top

gainers were Gulf International Services and Qatari Investors Group, rising

4.7% and 3.7%, respectively. Among the top losers, Ezdan Holding Group fell

2.6%, while Ooredoo declined 1.4%.

GCC Commentary

Saudi Arabia: The TASI Index rose marginally to close at 11,149.4. Gains were led by the Insurance and Hotel & Tou. indices, rising 1.5% and 0.5%, respectively. Ace Arabia Coop. Ins. gained 9.7%, while AICC was up 6.7%.

Dubai: The DFM Index declined 0.2% to close at 5,083.1. The Services index fell 1.7%, while the Telecommunication index was down 0.9%. Ajman Bank declined 2.1%, while Al Salam Bank (Sudan) was fell 2.0%.

Abu Dhabi: The ADX benchmark index fell 0.4% to close at 5,168.1. The Consumer index fell 1.6%, while the Inv. & Fin. Ser. index declined 1.3%. Ooredoo fell 10.0%, while Gulf Livestock Co. was down 9.9%.

Kuwait: The KSE Index rose 0.1% to close at 7,474.2. The Telecom. index gained 2.4%, while the Insurance index was up 1.0%. Al-Madar Finance & Investment Co. rose 9.6%, while Gulf Investment House gained 8.6%.

Oman: The MSM Index rose 0.3% to close at 7,515.3. Gains were led by the Financial and Industrial indices rising 0.7% and 0.2%, respectively. Majan College rose 5.9%, while Al Anwar Holding was up 3.9%.

Bahrain: The BHB Index declined 0.2% to close at 1,464.7. The Commercial Banks index fell 0.4%, while the Services index was down 0.3%. Ithmaar Bank declined 3.1%, while Bahrain National Holding Co. was down 0.8%.

Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD%

Gulf International Services 128.30 4.7 721.2 162.9

Qatari Investors Group 59.50 3.7 328.2 36.2

Ahli Bank 54.80 3.4 2.3 29.5

Islamic Holding Group 104.10 3.1 493.5 126.3

Doha Insurance Co. 34.80 3.0 87.7 39.2

Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD%

Vodafone Qatar 22.00 2.6 4,818.2 105.4

Ezdan Holding Group 19.49 (2.6) 2,891.0 14.6

Salam International Investment Co. 20.45 0.4 1,314.4 57.2

United Development Co. 29.60 1.7 937.7 37.5

Mazaya Qatar Real Estate Dev. 24.58 (0.8) 927.4 119.9

Market Indicators 09 Sep 14 08 Sep 14 %Chg.

Value Traded (QR mn) 797.3 781.3 2.0

Exch. Market Cap. (QR mn) 744,128.8 743,038.7 0.1

Volume (mn) 18.4 17.8 3.6

Number of Transactions 7,824 6,795 15.1

Companies Traded 42 42 0.0

Market Breadth 25:11 26:15 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 20,950.39 0.6 0.4 41.3 N/A

All Share Index 3,545.09 0.5 0.3 37.0 17.4

Banks 3,452.50 0.0 (0.5) 41.3 16.9

Industrials 4,648.89 0.9 0.7 32.8 18.8

Transportation 2,358.58 0.9 2.0 26.9 15.1

Real Estate 2,958.41 2.0 2.7 51.5 15.8

Insurance 4,164.19 0.9 0.6 78.2 13.2

Telecoms 1,664.16 (0.4) 0.2 14.5 23.6

Consumer 7,464.61 0.2 0.3 25.5 27.9

Al Rayan Islamic Index 4,750.13 0.8 0.7 56.5 20.5

GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD%

Gulf International Services Qatar 128.30 4.7 721.2 162.9

Co. for Cooperative Ins. Saudi Arabia 63.62 4.5 993.2 80.7

Qatari Investors Group Qatar 59.50 3.7 328.2 36.2

Ahli Bank Qatar 54.80 3.4 2.3 29.5

Saudi Pharmaceutical Ind. Saudi Arabia 55.00 3.3 3,014.0 29.4

GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD%

Ithmaar Bank Bahrain 0.16 (3.1) 3,721.4 (32.6)

Ezdan Holding Group Qatar 19.49 (2.6) 2,891.0 14.6

National Real Estate Co. Kuwait 0.16 (2.5) 1,685.6 6.4

DP World Ltd. Dubai 19.80 (2.5) 85.5 11.8

Solidarity Saudi Takaful Saudi Arabia 25.80 (2.1) 6,065.1 (0.4)

Source: Bloomberg (# in Local Currency) (

## GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD%

Ezdan Holding Group 19.49 (2.6) 2,891.0 14.6

Ooredoo 131.00 (1.4) 34.2 (4.5)

Mazaya Qatar Real Estate Dev. 24.58 (0.8) 927.4 119.9

Aamal Co. 16.30 (0.6) 37.7 8.7

Al Khalij Commercial Bank 22.41 (0.4) 139.2 12.1

Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD%

Vodafone Qatar 22.00 2.6 105,496.8 105.4

Gulf International Services 128.30 4.7 91,351.9 162.9

QNB Group 206.00 (0.2) 65,829.2 19.8

Ezdan Holding Group 19.49 (2.6) 57,174.4 14.6

Islamic Holding Group 104.10 3.1 51,012.9 126.3

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded

($ mn) Exchange Mkt.

Cap. ($ mn) P/E** P/B**

Dividend Yield

Qatar* 14,046.61 0.6 0.4 3.3 35.3 218.96 204,337.8 17.5 2.3 3.6

Dubai

5,083.09 (0.2) (0.7) 0.4 50.8 320.59 97,819.3 21.1 1.9 1.9

Abu Dhabi

5,168.05 (0.4) 0.5 1.7 20.5 74.99 140,146.3 14.6 1.8 3.2

Saudi Arabia

11,149.36 0.0 0.7 0.3 30.6 2,991.16 604,482.3 21.4 2.7 2.5

Kuwait 7,474.20 0.1 0.3 0.6 (1.0) 84.33 113,015.5 18.5 1.2 3.7

Oman 7,515.25 0.3 0.5 2.0 10.0 23.50 27,582.1 11.3 1.7 3.7

Bahrain 1,464.66 (0.2) (0.5) (0.5) 17.3 1.52 54,295.7 11.3 1.0 4.6

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

13,950

14,000

14,050

14,100

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

Page 2 of 7

Qatar Market Commentary

The QE Index rose 0.6% to close at 14,046.6. The Real Estate and Industrials indices led the gains. The index rose on the back of buying support from non-Qatari shareholders despite selling pressure from Qatari shareholders.

Gulf International Services and Qatari Investors Group were the top gainers, rising 4.7% and 3.7%, respectively. Among the top losers, Ezdan Holding Group fell 2.6%, while Ooredoo declined 1.4%.

Volume of shares traded on Tuesday rose by 3.6% to 18.4mn from 17.8mn on Monday. Further, as compared to the 30-day moving average of 17.5mn, volume for the day was 5.4% higher. Vodafone Qatar and Ezdan Holding Group were the most active stocks, contributing 26.1% and 15.7% to the total volume respectively.

Source: Qatar Exchange (* as a % of traded value)

Global Economic Data

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

09/09 US Federal Reserve Consumer Credit July $26.006B $17.350B $17.255B

09/09 US Nat'l Fed. of Ind. Busin. NFIB Small Business Optimism August 96.1 96 95.7

09/09 France Ministry of the Economy Budget Balance YTD July -84.1B – -59.4B

09/09 France Ministry of the Economy Trade Balance July -5,539M -5,000M -5,380M

09/09 UK British Retail Consortium BRC Sales Like-For-Like YoY August 1.30% 0.30% -0.30%

09/09 UK ONS Visible Trade Balance GBP/Mn July -£10,186 -£9,100 -£9,413

09/09 UK ONS Trade Balance Non EU GBP/Mn July -£4,345 -£3,600 -£3,841

09/09 UK ONS Trade Balance July -£3,348 -£2,300 -£2,459

09/09 UK ONS Industrial Production MoM July 0.50% 0.20% 0.30%

09/09 UK ONS Industrial Production YoY July 1.70% 1.30% 1.20%

09/09 UK ONS Manufacturing Production MoM July 0.30% 0.30% 0.30%

09/09 UK ONS Manufacturing Production YoY July 2.20% 2.20% 1.90%

09/09 UK National Institute of Eco. NIESR GDP Estimate August 0.60% – 0.60%

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted

News

Qatar

Qatar Exchange plans to raise volume of shares 10 times –

Qatar Exchange’s (QE) CEO Mr. Rashid bin Ali Al-Mansoori told reporters at a conference in Doha that the Value of each share traded on the QE will be reduced to 1/10 of the current value in order to compensate for volume increase. The change in share volume is being studied as a measure to increase liquidity. The implementation is expected next year. (Bloomberg)

QE participates in joint workshop on empowering SMEs in Qatar, QE venture market to begin early 2015 – Qatar

Exchange (QE) participated in the workshop, entitled “Empowering SMEs”, which was hosted by the Doha Bank (DHBK) and held in Doha on September 8, 2014 at the Doha Bank auditorium. The workshop was attended by CEOs and top management officials from QE, DHBK, Qatar Development Bank (QDB), Enterprise Qatar (EQ) , Qatar Business Incubation Centre (QBIC) and UK Trade Investment center, who met together to discuss and highlight opportunities for SMEs to grow and flourish. Meanwhile, QE’s CEO, Mr. Rashid bin Ali Al-Mansoori said that Qatar’s venture or junior stock market listing small & medium-sized enterprises (SMEs) is all set to be operational by early 2015. He said that to begin with, five SMEs will be listed on the Qatar Exchange (QE) Venture Market, while several others are in the process of getting approval from the authorities concerned. (QE, Peninsula Qatar)

MDPS: Qatar’s August 2014 CPI estimated at 118.9 –

According to the Ministry of Development Planning & Statistics (MDPS), Qatar’s Consumer Price Index (CPI) of August 2014 is estimated at 118.9 showing an increase of 0.7% as compared to the CPI of July 2014, and an increase of 3.8% as compared to the CPI of August 2013. The overall monthly increase of 0.7% in CPI of August 2014 as compared to CPI of July 2014 has resulted from the effect of price increases recorded in the main groups: food & beverages and tobacco by 1.7%, miscellaneous goods & services by 1.1%, garments & footwear by 1.0%, rentals, fuel & energy by 0.7%, entertainment, recreation & culture and furniture, textiles & home appliances by 0.3% for each and transport & communication by 0.2%. The overall CPI of August 2014 as compared to August 2013 has increased by 3.8%. The year-on-year price increases are observed in all of the groups: Rentals, fuel & energy by 7.9%(mainly hikes noticed in rentals of residential buildings), furniture, textiles & home appliances by 5.1%, garments & footwear by 3.3%, transport & communication by 2.5%, miscellaneous goods & services by 1.6%, entertainment, recreation & culture and food, beverages & tobacco by 1.2% for each, and medical care by 0.7%. (MDPS)

Emir chairs meeting of economic affairs council – HH the

Emir Sheikh Tamim bin Hamad al-Thani, Chairman of the Supreme Council for Economic Affairs and Investment, chaired the council’s fourth meeting at the Emiri Diwan. HE the Prime Minister and Minister of Interior Sheikh Abdullah bin Nasser bin Khalifa al-Thani attended the meeting. HE Minister of Finance

Overall Activity Buy %* Sell %* Net (QR)

Qatari 68.57% 68.92% (2,741,895.46)

Non-Qatari 31.43% 31.09% 2,741,895.46

Page 3 of 7

Ali Shareef al-Emadi said that the council discussed the topics on schedule, followed up on the implementation of the previous decisions, in addition to discussing the latest developments related to the industrial and petrochemical sector. The council also discussed Qatar Petroleum International’s (QPI) projects and approved Qatar Petroleum’s (QP) request regarding an agreement on development partners and the amended financial conditions required for Ras Laffan 3. (Gulf-Times.com)

Qatar Cool’s 50th tower now operational – Qatar District

Cooling Company (Qatar Cool) has its 50th tower operational in Doha’s West Bay. In line with Qatar’s National Vision 2030 for sustainable development, West Bay already boasts of a comprehensive district cooling system delivered by Qatar Cool. MZ &Partners’ MEP manager Hasan Sultan observed that the district cooling is increasingly being recognized by governments, developers and end-users alike. MZ & Partners is a leading consultant company in Qatar which has designed many towers in West Bay. Qatar Cool is preparing to open its third plant in the West Bay area, which will provide residential & commercial towers with nearly 40,000 tons of refrigeration of cooling. A big part of this capacity has been sold even prior to starting construction. Qatar Cool’s chief financial officer (acting CEO) Ahmad Shehadeh said that developers prefer district cooling. He added that it not only reduces operating and maintenance costs, but also carbon footprints, which is in line with the country’s national objectives. (Gulf-Times.com)

Airport Street diversion removed – The Public Works

Authority (Ashghal) has announced the removal of the road diversion on Airport Street in the direction from Doha to Al Wakra. The main road was thrown open for traffic on September 5. Ashghal removed the diversion after completion of works in the area as part of the F Ring Road project, which aims to create entrances and exits to Hamad International Airport (HIA) and links that directly connect southern parts of Doha, in addition to developing infrastructure in the area. (Peninsula Qatar)

DSE wins AED110mn district cooling plant contract in Qatar – Drake & Scull Engineering (DSE) a unit of Drake & Scull

International, has won a contract worth AED110mn for a district cooling plant at Lusail City. Under the contract, DSE Qatar will design and build a district cooling plant of 14,250 tons of refrigeration capacity for supplying chilled water to buildings in Lusail City, and is expected to be ready by July 2015. The scope of work includes building of a district cooling plant along with all the associated equipments. Lusail is a new city under construction in Qatar by Lusail Real Estate Development Company. (DFM)

Woqod gets nod to display, sell cooking gas cylinders at petrol stations – Woqod (QFLS) has received an approval from

the Civil Defense Department to display and sell cooking gas cylinders at petrol stations. The company said its professional team has selected safe places to display Shafaf cylinders with guidance from Civil Defense. The company said the high demand for transparent cylinders in Qatar has led to the sale of cylinders in 200 supermarkets and it was safe to sell them at petrol stations. The advantage of Shafaf cylinders is that it does not explode even when there is fire in a place where other cylinders can explode due to excessive heat. Meanwhile, residents complained about a shortage of cylinders in Muather, Al Rayyan, Al Wakra, Umm Salal and other areas. (Peninsula Qatar)

ORDS eShop visitors on the rise – Ooredoo (ORDS)

customers are increasingly using digital and self-service features to meet their communication needs, as it increases the

range and diversity of customer services online. ORDS’s eShop, the online portal offering devices, services and advanced technology, has seen a sharp rise in visits and purchases in recent months, becoming one of Qatar’s most popular online shopping destinations. This rise has been partly driven by ORDS’ most recent offer, which gives customers a free 15GB Data Scratch Card when they purchase selected smartphones at the Ooredoo eShop. Interest in the new generation of smart devices has also created a sharp rise in the number of searches at the Ooredoo online store. (Peninsula Qatar)

Real estate deals stood at QR431.4mn between August 31 and September 4 – The Department of Real Estate Registration

said that the volume of trading in real estate registered with the Real Estate Registration Department at Qatar's Ministry of Justice during the period from August 31 to September 4, 2014 stood at QR431.4mn. The list of real estate sales included plots of land, two-story villas, supplements and residential buildings. Most of the sales were registered in the municipalities of Umm Salal, Al-Khor, Al Thakhira, Doha, Al Rayyan, Al Za'ayen and Al Wakra. (Peninsula Qatar)

Qatar Airways to launch domestic Saudi operations soon –

According to source, Qatar Airways (QA) is expected to launch domestic flights in Saudi Arabia shortly. The new service will be operating under the brand, Al-Maha Airways, in the Kingdom. A fleet of nine aircraft, mainly Airbus A320, would initially be deployed to connect major cities in Saudi Arabia. QA and Saudi Gulf from the Al-Qahtani Group secured the permission to operate domestic flights in the Kingdom last December. Saudi Arabia’s national carrier, Saudi Arabian Airlines, and Flynas are the sole domestic route operators in the country. According to the General Authority for Civil Aviation (GACA), nine domestic airports in the Kingdom receive foreign airlines. Around 1.6mn passengers have patronized these domestic airports in 2013. (Bloomberg)

International

US job openings hold near 13-year high in July; steps initiated to plug infrastructure funding gap – According to a

report from the U.S. Department of Labor, the US job openings held near a 13-year high in July while hiring picked up. The Labor Department said job openings were at a seasonally adjusted 4.673mn compared with 4.675mn in June. Job openings are used to measure labor demand. Federal Reserve policy makers are closely monitoring the JOLTS report as they mull their next step on monetary policy. Employers hired 4.872mn people in July, up from 4.791mn in June. While the quits rate held steady a 1.8%, the overall number of Americans who voluntarily left their jobs in July hit the highest level since June 2008, a sign that more people are increasingly confident that they can find a better job elsewhere. Meanwhile, the Obama administration announced a series of measures to help shore up the crumbling US infrastructure, including half a billion dollars in loans for the electric grid. The moves are part of the administration’s efforts to address what it says is a $1tn funding gap for transportation, water & electricity needs over the next six years. US Treasury Secretary Jack Lew said investing in infrastructure has historically been one of the best ways to create jobs and boost economic growth, but spending has fallen over the past decade, as two-thirds of roads are now in disrepair, and one out of the nine US bridges have structural deficiencies. (Reuters)

EU pushes for urgent energy deal in US trade pact – The

European Union (EU) trade commissioner Karel De Gucht said the US should commit to exporting oil and natural gas to Europe under a transatlantic trade deal in light of the European Union's

Page 4 of 7

geopolitical situation. Tension between Russia and the West over the future of Ukraine is spurring the European Union to renew efforts to end decades of dependence on Russian gas. One solution would be greater access to abundant US resources. Overturning a 40-year US ban on oil exports by agreeing to send oil to Europe could pressure Russian President Vladimir Putin by lowering global crude prices. The rewards of a US-EU energy agreement could be big for the European Union, where natural gas prices are around three times than those in the US. The Europeans want a detailed chapter in the trade pact that lays out US commitments to energy exports, hoping to make supply more secure. (Reuters)

Japan machinery orders rise, ease concern about outlook; BOJ's Iwata upbeat on economy – Japan's core machinery

orders rose for a second straight month in July, a tentative sign of a pick-up in business investment that is needed to propel Japan out of the slump caused by April's sales tax hike. The 3.5% rise in core orders, a highly volatile data series regarded as an indicator of capital spending in the coming six to nine months, was less than the median estimate of a 4.0% increase in a Reuters poll of economists, but still enough to show investment rising. That followed a 8.8% rise in June and a 19.5% drop in May, which was the biggest drop in data going back to 2005. The data followed a recent run of weak economic indicators that suggest a rebound expected this quarter from April's slump may not prove as strong as originally thought. Weak readings cloud the prospects of a planned increase in the sales tax in October 2015, while keeping policy makers under pressure to provide fresh stimulus to prop up the economy. Meanwhile, Bank of Japan Deputy Governor Kikuo Iwata reiterated policy makers' conviction that the economy can recover from a deep slump, saying that households and companies will boost spending as the pain from an April sales tax hike eases. Iwata acknowledged that weak exports and the rising burden on households from the tax hike were among risks to the outlook, but said a pick-up in global demand and wages will keep the Japanese economy on track for a moderate recovery (Reuters)

China money-supply growth eases to five-month low –

Chinese Premier Li Keqiang said China’s money-supply growth unexpectedly eased to the slowest pace in five months, indicating a sign of credit constraints as a property slump weighs on the economy. Li said M2, the government’s broadest measure, rose 12.8% in August from a year earlier. That compares with a 13.5% pace in July, which was also the median estimate for August in a Bloomberg News survey of analysts. The slowdown in money-supply expansion follows July’s plunge in new credit to the lowest level since 2008. Li said the rate of M2 growth is within a controllable range and that the nation is capable of meeting its economic targets for the year. He reiterated that the growth can be slightly above or below the goal of about 7.5%. Li further added that China will continue to implement a “prudent” monetary policy. (Bloomberg)

Brazil rating outlook cut to negative by Moody’s on growth – Brazil’s credit rating outlook was cut to negative by Moody’s

Investors Service, which said the slow economic growth is unlikely to improve in the short-term. Moody’s affirmed Brazil’s Baa2 rating, its second-lowest investment grade. The change in outlook comes after data last month showed Latin America’s largest economy entered a recessionary phase for the first time in five years, and as President Dilma Rousseff seeks election to a second term in October. Brazil’s benchmark dollar bonds dropped the most since March and the real weakened after the Moody’s report, which came on the heels of a voter poll that showed Rousseff gaining support and in a statistical tie with her

main opponent. Brazil’s Ibovespa stock index had posted the best returns among major global gauges since March, when voter surveys first started showing Rousseff losing support for her effort to win another four-year term after overseeing Brazil’s slowest economic growth for any president in two decades. (Bloomberg)

Regional

EY: GCC gross Takaful contribution estimated to reach $8.9bn in 2014 – According to Ernst & Young’s (EY) “Global

Takaful Insights 2014” report, gross Takaful contribution in the GCC region is estimated to reach around $8.9bn in 2014 from an estimated $7.9bn in 2013. The report forecasts a continued double-digit growth in the global Takaful market of about 14% during 2013-2016 and expects the industry to reach $20bn by 2017. This is against a backdrop of continued buoyancy in the estimated $2tn global Islamic finance market. Within the GCC region, Saudi Arabia accounts for the majority of the gross Takaful contribution at 77%, followed by the UAE at 15%. The remaining Gulf countries account for just 8% of the gross Takaful contribution. The Kingdom is likely to remain the core market of Islamic insurance business, commanding approximately half (48%) of the global contributions. Turkey and Oman are the new entrants into the Takaful industry, offering a first mover advantage to Takaful operators, whereas established Takaful markets in Africa like Sudan, offer great prospects for replication across new African markets. (GulfBase.com)

Ventures Onsite: Precast concrete market expands in GCC – According to a report by Ventures Onsite, a construction

intelligence consultancy firm, the demand for precast concrete in the construction sector is increasing steadily, as developers realize its value in faster completion of major projects. As per the report, precast concrete is becoming increasingly popular in Saudi Arabia and the UAE. In Dubai, demand for precast concrete is forecasted to increase from 2015, with high-end architectural projects coming up for the World Expo 2020. Precast developers are also likely to see opportunities for temporary products, which can be disassembled after the event and transported to other locations. In the UAE, precast concrete is being used to support large infrastructure projects, while in Saudi Arabia it will be used to meet government targets of 500,000 new homes. (GulfBase.com)

Saudi-Bahrain causeway to cost $5bn – Bahrain’s

Transportation Minister, Kamal Ahmed, said that a second causeway connecting Bahrain with Saudi Arabia will cost $5bn to build. To be called “King Hamad Causeway”, the second bridge will be used by vehicles as well as trains. The causeway will become a part of the GCC railway network, which is expected to be completed by 2017, stretching over a distance of 2,000 kilometers. The first one named “King Fahd Causeway”, which opened in 1986, already connects Saudi Arabia to Bahrain through a series of bridges and roads that stretch across 25 kilometers. (GulfBase.com, Bloomberg)

S&P: Sukuk issuance in Gulf region declines – According to

a report by Standard & Poor’s (S&P), corporate and infrastructure Sukuk issuance has trended downward in 2014 in the GCC region and Malaysia, despite supportive market conditions such as low interest rates and steady appetite from investors. Issuance in the GCC region fell 33% YoY in the first eight months of 2014 to $6.5bn. Low-priced bank debt continues to be an attractive option for issuers in the GCC region and Malaysia as compared to the capital markets. Loans as a proportion of the total funding have increased from less than 50% in 2012 to over 60% in the GCC region during 2014-YTD. Corporate and infrastructure issuers are increasingly turning to

Page 5 of 7

conventional issuance over Sukuk, based on the issuance levels in 2Q2014 and 3Q2014 relative to levels in 4Q2013, when Sukuk predominated. The S&P report estimates that approximately $17bn of Sukuk in the GCC will mature between July 2014 and December 2016, which is equivalent to 65% of primary issuance in the year to December 31, 2013. The resulting refinancing needs could also boost Sukuk issuance by corporate and infrastructure entities over this period. (GulfBase.com)

Petromin launches Petropower Plus – Saudi-based Petromin

Corporation, an oil marketing company, has launched a new product range for marine power engine lubrication named ‘Petropower Plus’. The new Petropower Plus series will raise the benchmarking standards for the overall lubrication performance in trunk piston engines. (GulfBase.com)

Intematix, SABIC to deliver increased efficiency for LED systems – US-based Intematix Corporation has collaborated

with the Innovative Plastics business of Saudi Basic Industries Corporation (SABIC) to create the ChromaLit Linear, a state-of-the-art LED product developed for the lighting industry. By using Intematix’s remote phosphor technology and SABIC’s LEXAN LUX resins, lighting customers can now achieve the energy efficiency and reliability benefits of LEDs, while also experiencing increased optical efficiency and better light uniformity, a critical factor for commercial environments. (Bloomberg)

AHAB forms creditors' steering committee – Saudi Arabian

conglomerate Ahmad Hamad Algosaibi & Brothers (AHAB) said that a steering committee of creditors has been formed to negotiate its debt restructuring. AHAB said that a creditors' committee had been formed on September 9, 2014 comprising representatives from five Gulf and international institutions. AHAB said that 87 of 108 claimants, who represent about 59% of the company’s overall debt and around 89% of the debt claimed by non-Saudi institutions, are now formally engaged in the settlement process. Earlier in May 2014, AHAB had stated that it had direct liabilities to financial institutions worth around $6bn. (Reuters)

Sharjah sets initial price guidance on a 10-year Sukuk – The

Emirate of Sharjah has announced initial price guidance of around 120 basis points over mid-swaps for its US dollar benchmark-sized 10-year Sukuk. Demand for the bond, which is expected to be priced on September 10, 2014 is more than $4bn. HSBC, KFH Investment, National Bank of Abu Dhabi, Sharjah Islamic Bank and Standard Chartered are acting as lead managers on the Reg S Sukuk. (Reuters)

Dana Gas secures AED367.24mn loan – Dana Gas, through

its wholly owned subsidiary Dana Gas Explorations, has secured an AED367.24mn term facility for the Zora Field Development Project, which spans across the territorial waters of Ajman and Sharjah. This facility will contribute the debt component of the financing needed to complete the project and bring the Zora gas field on-stream. Repayment for the term facility is spread over 15 quarterly installments. (Bloomberg)

Deyaar completes sale of residential units at Montrose –

Deyaar Development has completed the sale of residential units in Tower-1 of its new Montrose project on September 6, 2014. These housing units are set to be delivered by December 2016. The recently unveiled Montrose project, located at Barsha South in DuBiotech in Dubai, comprises three towers – a hotel apartment tower and two residential towers. (DFM)

DMCC, AstroLabs team up to launch technology hub –

AstroLabs Dubai and Dubai Multi Commodities Centre (DMCC)

are planning to launch Dubai’s first technology hub by early 2015 in the DMCC Free Zone, in an effort to invite technology entrepreneurs across the globe to access high growth emerging markets. The hub named as ‘AstroLabs Dubai’ will occupy 6,500 square feet at the DMCC Free Zone, which includes training spaces where in-house experts on user experience, design and digital marketing will advise entrepreneurs. (GulfBase.com, Bloomberg)

Emirates NBD sets IPT on Tier 1 perpetual bond – Emirates

NBD has set initial price thoughts (IPT) for its Tier 1 capital-boosting bond issue at around 6%. The US dollar denominated bond issue has a perpetual tenure but can be bought back by the lender after the sixth year. The bond will be of benchmark size – which traditionally meant to be worth $500mn or above. (Reuters)

ADNEC hosts 56% more exhibitions in 1H2014 – Abu Dhabi

National Exhibitions Centre (ADNEC) hosted 28 exhibitions in 1H2014, up 56% from 18 exhibitions hosted in 1H2013. The facility also hosted three regional and three international conferences during 1H2014, demonstrating versatility of its event offering. (GulfBase.com)

ADCB sets IPT for five-year bond issue – Abu Dhabi

Commercial Bank (ADCB) has set the initial price thoughts (IPT) for a benchmark five-year bond issue in the 95 basis points area over midswaps. ADCB has picked Barclays, ING, JP Morgan and Mizuho to arrange for the bond sale. The dollar-denominated bond will be issued through a special purpose vehicle incorporated in the Cayman Islands and will be listed on the Irish Stock Exchange. (Reuters)

GIH seeks to relist in KSE – Global Investment House (GIH)

has announced its intention to relist its shares on the Kuwait Stock Exchange (KSE), after its listing was cancelled in 2013 due to accumulated debt. GIH’s CEO Maha Al Ghoneim said the company is now debt-free following its loan restructuring in 2013. The company’s relisting would be discussed at its annual general meeting, and is subject to shareholders’ approval. (Reuters)

Kuwait to suspend offset scheme – Kuwait is suspending a

program under which foreign companies handling big government contracts are required to invest in the local economy. The suspension is aimed at attracting more overseas companies to the Gulf state. The offset program was introduced in 1992 as a way to reduce Kuwait’s reliance on oil and gain access to new technologies. (Reuters)

Oman plans OMR200mn Sukuk issue – The Omani

government is planning to raise OMR200mn through its debut sovereign Islamic bond or Sukuk issue. In this regard, the government has also invited specialized institutions who are knowledgeable in structuring Sukuk issue. The government had earlier formed a working committee to issue sovereign Sukuk in a move to fund infrastructure projects. The committee members are from the Ministry of Finance, the central bank and the Capital Market Authority, who are now discussing various aspects of raising funds through an asset-backed sovereign Sukuk. The purpose of the Sukuk issue is to deepen the financial market in the Sultanate. (Bloomberg)

OPWP open bids for Qurayat seawater desalination project – Oman Power & Water Procurement Company (OPWP), on

September 8, 2014, opened the bids for developing a new seawater desalination project in Qurayat in South Muscat. The project’s scope includes the construction, ownership, and operation of a high efficiency desalination facility with an output of 200,000 cubic meters per day of potable water. (Bloomberg)

Page 6 of 7

Nawras to be rebranded as Ooredoo – Omani Qatari

Telecommunications Company (Nawras) has decided to change its brand named from ‘Nawras’ to ‘Ooredoo’ by 2014-end. The company’s shareholders approved the board recommendation to enter into a brand license agreement with Ooredoo IP on September 9, 2014. The rebranding will facilitate communications for Omani customers who travel overseas and also for international travelers visiting Oman. (Bloomberg)

Contacts

Saugata Sarkar Abdullah Amin, CFA Shahan Keushgerian

Head of Research Senior Research Analyst Senior Research Analyst

Tel: (+974) 4476 6534 Tel: (+974) 4476 6569 Tel: (+974) 4476 6509

[email protected] [email protected] [email protected]

Sahbi Kasraoui Ahmed Al-Khoudary QNB Financial Services SPC

Manager – HNWI Head of Sales Trading – Institutional Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6544 Tel: (+974) 4476 6548 PO Box 24025 [email protected] [email protected] Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts, QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 7 of 7

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg (* Market closed on 09 September 2014) Source: Bloomberg (* Market closed on 09 September 2014)

80.090.0

100.0110.0120.0130.0140.0150.0160.0170.0180.0190.0200.0210.0

Aug-10 Aug-11 Aug-12 Aug-13 Aug-14

QE Index S&P Pan Arab S&P GCC

0.0%

0.6%

0.1%

(0.2%)

0.3%

(0.4%)

(0.2%)

(0.6%)

(0.3%)

0.0%

0.3%

0.6%

0.9%

Saud

i Ara

bia

Qata

r

Kuw

ait

Bah

rain

Om

an

Abu D

habi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD%

Global Indices Performance Close 1D% WTD% YTD%

Gold/Ounce 1,255.50 0.0 (1.1) 4.1 DJ Industrial 17,013.87 (0.6) (0.7) 2.6

Silver/Ounce 19.06 0.2 (0.7) (2.1) S&P 500 1,988.44 (0.7) (1.0) 7.6

Crude Oil (Brent)/Barrel (FM Future)

99.16 (1.0) (1.6) (10.5) NASDAQ 100 4,552.29 (0.9) (0.7) 9.0

Natural Gas (Henry Hub)/MMBtu

3.94 2.3 2.6 (9.3) STOXX 600 344.87 (0.4) (0.8) 5.1

LPG Propane (Arab Gulf)/Ton* 106.38 0.0 0.7 (15.9) DAX 9,710.70 (0.5) (0.4) 1.7

LPG Butane (Arab Gulf)/Ton 124.50 (0.6) (1.0) (8.3) FTSE 100 6,829.00 (0.1) (0.4) 1.2

Euro 1.29 0.3 (0.1) (5.9) CAC 40 4,452.37 (0.5) (0.8) 3.6

Yen 106.20 0.2 1.1 0.8 Nikkei 15,749.15 0.3 0.5 (3.3)

GBP 1.61 0.0 (1.4) (2.7) MSCI EM 1,087.54 (0.7) (0.8) 8.5

CHF 1.07 0.3 (0.2) (4.3) SHANGHAI SE Composite 2,326.53 0.0 0.0 10.0

AUD 0.92 (0.8) (1.9) 3.2 HANG SENG * 25,190.45 0.0 (0.2) 8.1

USD Index 84.28 0.1 0.6 5.3 BSE SENSEX 27,265.32 (0.2) 0.9 28.8

RUB 37.05 0.2 0.0 12.7 Bovespa 58,676.34 (0.9) (3.3) 13.9

BRL 0.44 (0.7) (1.8) 3.4 RTS 1,246.64 0.1 (0.8) (13.6)

201.8

170.0

151.2