Embed Size (px)

Citation preview

Discover What Checkbook IRA PromotersDon’t Want You to Know

10 Myths About Checkbook IRAs - Exposed

2

10 Myths About Checkbook IRAs – ExposedSelf-directed IRAs have been growing in popularity among savvy investors. Self-directed investors realize they’re able to take control of their financial future by taking advantage of many investment options, including real estate, notes, tax liens and precious metals, while potentially benefiting from tax advantages.

With any investment opportunity there is a risk that someone will look to exploit people or the system to make a few bucks. Among the most prevalent practices is companies willing to provide investors with “checkbook control” of their self-directed IRA. This involves using a self-directed IRA to invest in a single-member limited liability company (LLC) where the IRA owner is the managing member. This gives the investor the ability to directly manage his or her funds (i.e., to have “checkbook control” of the IRA).

Is “checkbook control” an approved strategy with the IRS? Read more to dispell the myths that could be dangerous for investors.

“ There’s pretty much no question that the standard Checkbook IRA and its variations are violating a number of IRS laws dealing with prohibited transactions and self dealing. It sounds great to be able to access your IRA money today without any tax or penalty, but it won’t work. The Checkbook IRA structures will eventually be officially declared illegal by the IRS. The penalty can be as high as the loss of your entire IRA.”

– Attorney Lee Phillips

1. Checkbook IRAs are IRS-ApprovedWhile many believe that checkbook control IRAs are IRS-approved, this is not the case. In fact, these accounts appear to be a major concern of the IRS, as evidenced by their repeated inclusion in the agency’s annual “Dirty Dozen” list of tax scams. Under the title “abusive retirement plans,” the IRS specifically mentions, “the use of limited liability companies to engage in activity that is considered prohibited.”

When the IRA holder has direct access to the funds via a single-member LLC arrangement, there is increased risk of prohibited transactions and violations of U.S. Tax Code. The penalty for a prohibited transaction is immediate account distribution, which will be subject to taxation and penalties.

3

See the note below from IRS Publication 590 on consequences:

“ Generally, if you are under age 59½, you must pay a 10 percent additional tax on the distribution of any assets (money or other property) from your traditional IRA. Distributions before you are age 59½ are called early distributions.

“ The 10 percent additional tax applies to the part of the distribution that you have to include in gross income. It is in addition to any regular income tax on that amount.”

– IRS Publication 590

2. I Am Not Putting My Entire Retirement at Risk By Using a Checkbook IRAWhen your Checkbook IRA is deemed prohibited, all assets in your account will be distributed to you. The value of your IRA will likely be deemed income to you and you will be taxed accordingly, and may be subject to additional penalties up to 15 percent.

The tax code makes clear the need for an independent custodian, stating that if you own the LLC and have unfettered access to the money (which is what checkbook control IRAs provide) you are violating the clear intent of the law. Below is the definition of a prohibited transaction, according to U.S. Tax Code Section 4975:

The term “prohibited transaction” means any direct or indirect—

(A) sale or exchange, or leasing, of any property between a plan and a disqualified person;

(B) lending of money or other extension of credit between a plan and a disqualified person;

(C) furnishing of goods, services, or facilities between a plan and a disqualified person;

(D) transfer to, or use by or for the benefit of, a disqualified person of the income or assets of a plan;

(E) act by a disqualified person who is a fiduciary whereby he deals with the income or assets of a plan in his own interests or for his own account; or

(F) receipt of any consideration for his own personal account by any disqualified person who is a fiduciary from any party dealing with the plan in connection with a transaction involving the income or assets of the plan.

Section 4975 also states that the tax on prohibited transaction “shall be equal to 15 percent of the amount involved with respect to the prohibited transaction for each year (or part thereof ) in the taxable period.”

4

Most attorneys have great concerns about the potential for prohibited transactions to occur when using a Checkbook IRA, mainly because the process is extremely complex.

“The lack of investment oversight by a qualified IRA or a custodian increases the potential for adverse tax consequences and the penalties that can ensue can result in a significant reduction in what the IRA owner thought was a building of his retirement nest egg,” according to Ron Kahn, partner and chair of the tax practice group Ulmer & Berne LLP.

Another respected source, The self-directed IRA workbook by real estate investors and speakers Dyches Boddiford and Peter Fortunato, put it this way:

“There is a perception that investing in an IRA through an entity is somehow a prohibited transaction washing machine which will protect the IRA from all the pesky rules of Section 4975. In fact, the opposite is true, since the additional layers of complexity make it more likely that an inadvertent prohibited transaction may occur.”

3. The Promoter I am Using to Set Up My Checkbook IRA Guarantees the Safety of My IRA and Will Defend Me Against the IRS

Promoters of the Checkbook IRA scheme will often make outrageous claims online to the benefits and validity of the program, however, what really matters is what is in the document that you sign. Be sure to read the fine print. These promoters typically have a clause hidden in the document that states, “we cannot be sure that this will work and if an issue arises in the future you are on your own.” How could any reputable business put their firm at such risk by accepting the responsibility of this scheme working and in return make just $3,000-$5,000?

When speaking with an administrator who supports Checkbook IRAs ask them how they will specifically support you if your Checkbook IRA performs a prohibited transaction and be sure to read the documents very carefully. You will be amazed at what you discover.

4. I Will Have Legal Support After I Set Up My Checkbook IRAOn many Checkbook IRA websites, legal support is “included.” Typically, before you buy you will be told that you will have the help of attorneys and former IRS employees to stay compliant; however, once your Checkbook IRA is set up, this support evaporates.

These attorneys are hired by the promoters, or are the promoters themselves, and their focus is to sell you the product and move on to the next sale. Many prospective clients assume that for the $1,500-$3,000 investment to set up a Checkbook IRA, they will get complete legal coverage for the life of the IRA. This is simply not the case.

These attorneys do not have a formal relationship with you and typically offer broad and inconclusive direction—if you can even get in touch with them. The simple fact is that it does not make economic sense to a Checkbook IRA promoter to earn $1,500 from you and then turn around and pay a qualified ERISA attorney $300 per hour to cover all of your investment and structural issues.

The penalties are real and potentially large. Why risk losing all the wealth you worked so hard to build?

5

Keep in mind that using a Checkbook IRA adds complexity to any transaction and the majority of prohibited transactions don’t occur during the setup, they occur when you start investing. Assuming you plan on using the IRA regularly to invest, you shouldn’t count on detailed support from the promoters. To review any deal, you need to know the specifics and at least two to three hours to understand and review all of the details. How would they make money if they took this much time for each client?

[Checkbook IRA] accounts

appear to be a major concern

of the IRS, as evidenced by their

inclusion in the agency’s annual

“Dirty Dozen” list of tax scams

again. Under the title “abusive

retirement plans,” the IRS

specifically mentions, “the use

of limited liability companies

to engage in activity that is

considered prohibited.”

Questions to ask Checkbook IRA promoters

• How long have you been in business?

• Are you regulated by any financial regulator?

• Do you have capital in case something happens to the firm?

• Can I see the firm’s balance sheet?

• Do you have insurance? What type and what are the limits?

• Do you require me to sign an indemnification releasing you from claims?

5. Promoters of Checkbook IRAs are Regulated or at Least Have Some Form of Oversight

This is one of the biggest surprises about the promoters of Checkbook IRAs. Even though they deal with such a complicated topic, the promoters may not be regulated, have regulatory oversight, capital requirements, and insurance to protect you. Do your homework and ask questions. You will be surprised by how small many of these firms are, and more importantly, how little they have in terms of assets to back up their claims.

Keep in mind that the firm will have you sign a document when you set up your Checkbook IRA. This document is likely to say that they cannot guarantee that this structure will be IRS compliant and that if there is an issue with the IRS you will be responsible to fight it and that they will have no liability! You must read the fine print.

Once you have the Checkbook IRA, you are responsible for it. Imagine buying a new car today and the manufacturer asks you to sign a document that states they don’t know if it will run, they don’t know if it meets all of the legal requirements, and if it doesn’t, or if the car harms you, the manufacturer is not responsible. Would you buy that car?

6

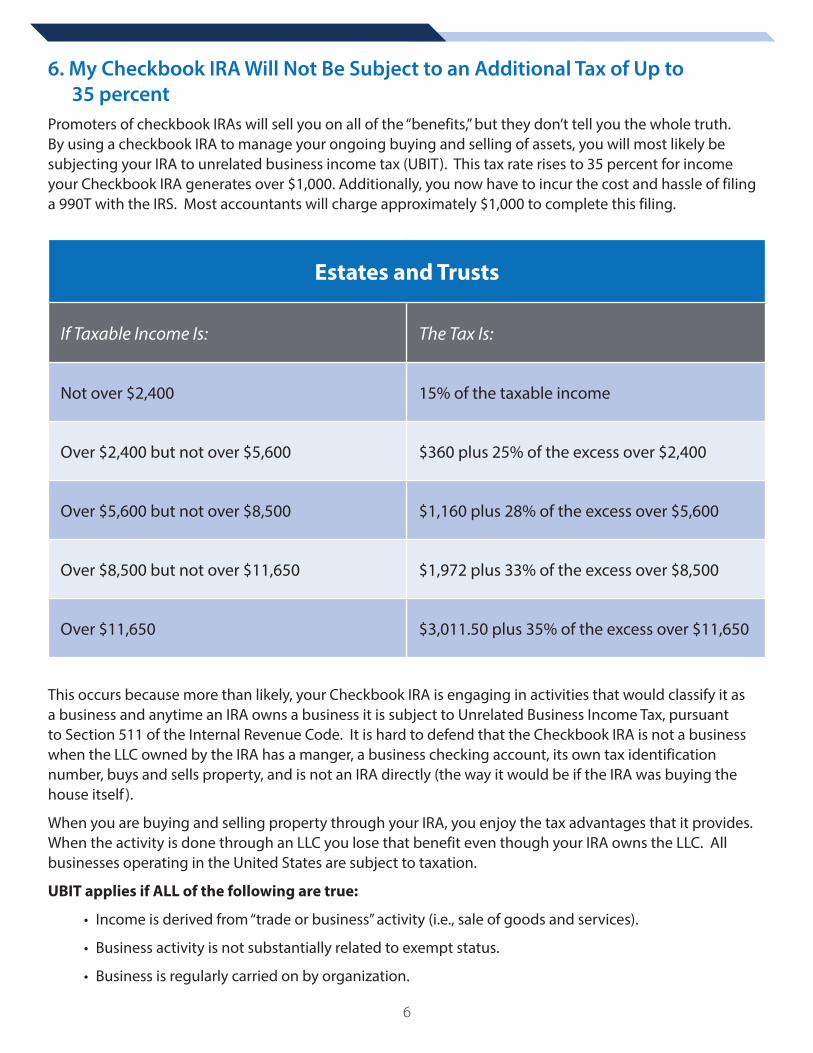

6. My Checkbook IRA Will Not Be Subject to an Additional Tax of Up to 35 percent

Promoters of checkbook IRAs will sell you on all of the “benefits,” but they don’t tell you the whole truth. By using a checkbook IRA to manage your ongoing buying and selling of assets, you will most likely be subjecting your IRA to unrelated business income tax (UBIT). This tax rate rises to 35 percent for income your Checkbook IRA generates over $1,000. Additionally, you now have to incur the cost and hassle of filing a 990T with the IRS. Most accountants will charge approximately $1,000 to complete this filing.

Estates and Trusts

If Taxable Income Is: The Tax Is:

Not over $2,400 15% of the taxable income

Over $2,400 but not over $5,600 $360 plus 25% of the excess over $2,400

Over $5,600 but not over $8,500 $1,160 plus 28% of the excess over $5,600

Over $8,500 but not over $11,650 $1,972 plus 33% of the excess over $8,500

Over $11,650 $3,011.50 plus 35% of the excess over $11,650

This occurs because more than likely, your Checkbook IRA is engaging in activities that would classify it as a business and anytime an IRA owns a business it is subject to Unrelated Business Income Tax, pursuant to Section 511 of the Internal Revenue Code. It is hard to defend that the Checkbook IRA is not a business when the LLC owned by the IRA has a manger, a business checking account, its own tax identification number, buys and sells property, and is not an IRA directly (the way it would be if the IRA was buying the house itself ).

When you are buying and selling property through your IRA, you enjoy the tax advantages that it provides. When the activity is done through an LLC you lose that benefit even though your IRA owns the LLC. All businesses operating in the United States are subject to taxation.

UBIT applies if ALL of the following are true:

• Income is derived from “trade or business” activity (i.e., sale of goods and services).

• Business activity is not substantially related to exempt status.

• Business is regularly carried on by organization.

7

7. I Will Save Time Using a Checkbook IRA vs. Using a Self-Directed IRA Custodian

Checkbook IRA promoters often focus on the increased paperwork and time that may correspond with using an IRA custodian as opposed to a Checkbook IRA. Keep in mind that paperwork documenting the investments in your account and trained professionals processing your account take the burden off you and pay dividends in the long run.

Do you have the settlement statement from a deal you did four years ago? How about the receipt from the plumber you used last summer? If you are using a full-service custodian, they will. The amount of bookkeeping and administrative work required to properly maintain a Checkbook IRA can be enormous. Full-service custodians keep complete records for your account, including images of all documents, an accounting of all income and expenses in your account, and all correspondence with third parties. As the manager of your Checkbook IRA, you will be responsible to keep and maintain all of these records.

Remember, this isn’t a normal LLC, it is one owned by your IRA and it needs to be segregated. In fact, because you are using an option considered questionable by the IRS, you should assume that you will be audited and be prepared to defend every action taken by the LLC.

8. I Will Save Money Using a Checkbook IRAThe greatest myth propounded by Checkbook IRA promoters is that you will save money using an LLC vs. a self-directed IRA custodian. In most instances, this is simply not true.

Full-service custodians typically charge between $300-$500 per year for most accounts. This fee is often all-inclusive, which means it covers all of your transactions for the entire year so you don’t get nickel-and-dimed every time you want to do something with your IRA.

If you open a Checkbook IRA you still need to use a limited service custodian, which is likely a separate company from the promoter who helped you establish the LLC. Here’s a breakdown of the typical charges associated with a Checkbook IRA:

• Checkbook IRA setup fee: $1,500 to $3,000

• Limited-service custodian: $150 per year

• State fee to maintain LLC status (varies by state): Anywhere from $150 to more than $300 per year, depending on size of LLC

• Fee to have a 990T tax form prepared (required if your LLC produces income): $1,000 –This is the cost just to complete and file the 990T. Keep in mind that your IRA likely will be subject to UBIT (Unrelated Business Income Tax).

Beyond these overt costs, don’t forget that you are also responsible for the full administration and bookkeeping of the Checkbook IRA. As an investor, your time is valuable so in many cases you will be paying someone to handle this. Again – an additional cost that may not be mentioned by Checkbook IRA promoters.

The bottom line is that you end up spending a lot more money, all while exposing your retirement to risk! If using a Checkbook IRA provides any benefits, saving money is definitely not one of them.

8

9. I Cannot Use My IRA to Purchase Investments at an auction if I Don’t Have a Checkbook IRA

One of the most popular myths of self directed IRAs is that you need a Checkbook IRA to participate in auctions of tax liens, foreclosed properties, and distressed properties. This is not the case; in fact, thousands of investors using full-service custodians participate in auctions each month. There are a number of solutions that make it extremely simple to participate with your IRA while not placing your retirement at risk for a prohibited transaction.

Although having a checkbook in your pocket would seem to make this process effortless, purchasing the investments are just the first step. The real work begins after the auction. Often times, the work includes a tremendous amount of paperwork and administration, including ensuring the county recorded the right liens, the proper title is being used, redemptions are not sent in error, etc. With a full-service custodian, all of these functions are handled by the custodian, allowing you to participate in the auction and not have to worry about any possible headaches afterwards.

By using a full-service custodian, you receive the best of both worlds: the convenience of participating in the auction and not having to deal with the administration after the auction.

10. I’ve Already Set up an LLC in my IRA – I Can’t Reverse ItYou are probably beginning to realize that checkbook control LLCs owned by your IRA are not as great as the promoters would like you to believe. In fact, checkbook IRAs present a risk, and greater potential costs. If you have already purchased one you might be a bit concerned and second-guessing your choice.

The good news is that it is extremely easy to shut down your Checkbook IRA and move the assets directly to a full-service custodian. Unlike checkbook control promoters, a full-service custodian offers multiple options that allow investors to make any legal transaction in their IRA with a simple process and behind-the-scenes support to make it convenient.

Full-service custodian Equity Trust Company,with owners who have been in this business since 1974, provides that support in the form of cutting-edge online technology and a knowledgeable staff that makes transactions easier. The experience is there – Equity Trust completes an average of 10,000 transactions per week and custodies $30 billion in assets.

Self-directed investors have the convenience of one-stop shopping when it comes to their IRAs – no need to seek out a custodian elsewhere, as is the case when you’re working with checkbook control promoters. This convenience comes with an all-inclusive fee, as opposed to all the “a la carte” charges that accompany a checkbook control LLC.

When your Checkbook IRA

is deemed prohibited, all

of your IRA assets will be

distributed to you. The

value of your IRA may be

deemed income to you

and you will be taxed

accordingly and may

be subject to additional

penalties up to 15 percent.

9

Reverse Your Checkbook IRA in 3 Easy Steps1. Establish an IRA with a trusted and qualified self-directed IRA custodian such as Equity Trust. The

Company is very familiar with this process and can guide you through it step-by-step – call a Senior Account Executive at 855-673-4721.

2. Consult with a professional, such as a CPA or attorney, familiar with the dissolution process of a single-member LLC. While a professional will provide the appropriate process for your unique situation, generally you will need to complete these steps:

• File a certificate of dissolution or cancellation in all states the LLC is registered.

• The LLC must be in good standing, so any fees or taxes must be current.

• Notify any creditors of your intent for the LLC to dissolve. In some states, all creditor claims must be settled before you can move forward.

• Depending on the structure, you might have to file a corporate dissolution form with the IRS.

3. You will have to transfer assets from the Checkbook IRA to your new IRA. Instruct all assets/liabilities of the former Checkbook IRA to be distributed/re-titled to your new IRA custodian.

It’s as simple as 1-2-3, but it is important that you have an experienced custodian to help during the transition. If you want to learn more, call Equity Trust for a free transition consultation with one of our specialists. While Equity Trust doesn’t provide tax or legal advice, our specialists can help you get started.

Don’t Fall Victim to the Taxes, Penalties, Time Requirements

and Extra Fees of a Checkbook Control IRA

Call for a FREE Consultation:

855-673-4721

© 2016 Equity Trust®. All Rights Reserved.ET0002-15

1 Equity Way, Westlake, OH 44145855-673-4721

www.TrustETC.com