©Blackwell Publishing Ltd, 2006

GLOBAL ENERGY REVIEW

West Africa: Prospects for Oil and Gas

A Report by Dr Paul McDonald

Consulting Editor, Oil and Energy Trends

A survey of the oil and gas reserves of West Africa;

With forecasts of production in 2015

26 November, 2006

©Blackwell Publishing Ltd, 2006

2

Contents

Introduction 4

Oil 6 Reserves & Production 6 Production Prospects 8

Countries in Decline 9 Cameroon 9 Congo (formerly Zaïre) 10 Gabon 10

Countries that have reversed their Decline 10 Congo-Brazzaville 10

Countries where Output is increasing 10 Angola 11 Equatorial Guinea 11 Ivory Coast 11 Nigeria 11

Countries with uncertain Prospects 12 Chad 12

Countries that may produce Oil by 2015 13 Niger 13 Sao Tome e Principe 13

Outlook for Oil Production to 2015 13

Natural Gas 16 Reserves & Production 16

Nigeria 17 LNG 17 Gas-to-Power 19

Outlook for Nigerian Gas 20 Other Gas Producers 20

Angola 20 Cameroon 21 Equatorial Guinea 21 Gabon 21 Ghana 22

Outlook for Natural Gas to 2015 22

Gas to Liquids 24

©Blackwell Publishing Ltd, 2006

3

List of Tables

Table 1 West Africa: Oil Reserves, 2006 6

Table 2 West Africa: Oil Production, 2006 7

Table 3 West Africa: Oil Reserves:Production Ratios, 2006 8

Table 4 West Africa: Oil Production 2005 and 2015 14

Table 5 West Africa: Proven Gas reserves, 2006 16

Table 6 Nigeria: LNG Exports, 2005 17

Table 7 Nigeria: Present and Future LNG Export Capacity 18

Table 8 West Africa: LNG Capacity, 2005 & 2015 22

Table 9 West Africa: Gas Production 2005 and 2015 23

©Blackwell Publishing Ltd, 2006

4

Introduction

West Africa contains less than 4% of the world’s proven oil reserves but accounts for just

over 6% of global output of crude oil and natural gas liquids (NGL). It is of particular

significance to the international oil industry, however, in that it contains four countries

where output is expected to increase. These countries are:

o Angola

o Equatorial Guinea

o Ivory Coast

o Nigeria

West African countries have attracted large amounts of upstream investment from the

international oil industry. Two of the countries, Angola and Nigeria, produce over

1 mn bpd each, and have considerable potential to increase their output. Equatorial

Guinea and Ivory Coast are expected to show reasonable gains from a much lower base.

Chad was once also forecast to provide significant gains in output, but its production has

recently gone into decline following major disagreements between the government and its

foreign oil industry partners.

The region is also well-endowed with natural gas and contains the world’s seventh-

largest exporter of liquefied natural gas (LNG), Nigeria. Its proven reserves constitute

3% of the world’s total. Commercial production outside Nigeria, however, is very low.

Much of West Africa’s gas is flared or reinjected into oil reservoirs. There is

considerable potential for commercial production of natural gas if markets can be

developed. Nigeria has progressed furthest with this, having LNG exports already and

being in the process of developing markets in neighbouring countries through the

development of a gas transmission system.

©Blackwell Publishing Ltd, 2006

5

Oil and gas developments in West Africa carry a considerable amount of political risk.

Relations between international oil companies and West African governments have not

always proved easy, as in the case of Chad. In Nigeria, the oil companies have come

under fierce attack from the inhabitants of the main oil- and gas-producing areas for what

is seen as their collusion with the federal government in diverting oil revenues away from

the producing regions to other parts of Nigeria, notably the Muslim north. In recent

years, these protests from the largely non-Muslim south-east have spilled over into

violence, leading to the kidnapping and even deaths of foreign oil workers. Some

international oil firms have been forced to shut-in production and plans to increase the

production of oil and gas have been delayed.

©Blackwell Publishing Ltd, 2006

6

Oil

Reserves & Production

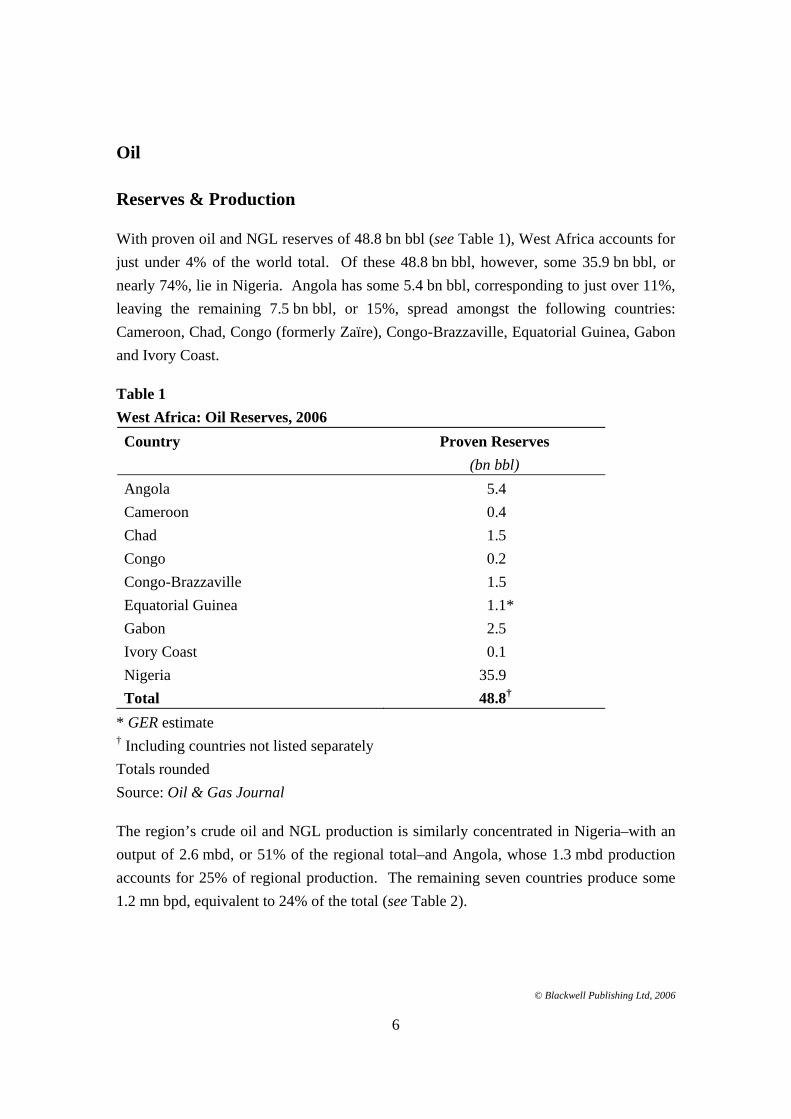

With proven oil and NGL reserves of 48.8 bn bbl (see Table 1), West Africa accounts for

just under 4% of the world total. Of these 48.8 bn bbl, however, some 35.9 bn bbl, or

nearly 74%, lie in Nigeria. Angola has some 5.4 bn bbl, corresponding to just over 11%,

leaving the remaining 7.5 bn bbl, or 15%, spread amongst the following countries:

Cameroon, Chad, Congo (formerly Zaïre), Congo-Brazzaville, Equatorial Guinea, Gabon

and Ivory Coast.

Table 1

West Africa: Oil Reserves, 2006

Country Proven Reserves

(bn bbl)

Angola 5.4

Cameroon 0.4

Chad 1.5

Congo 0.2

Congo-Brazzaville 1.5

Equatorial Guinea 1.1*

Gabon 2.5

Ivory Coast 0.1

Nigeria 35.9

Total 48.8†

* GER estimate † Including countries not listed separately

Totals rounded

Source: Oil & Gas Journal

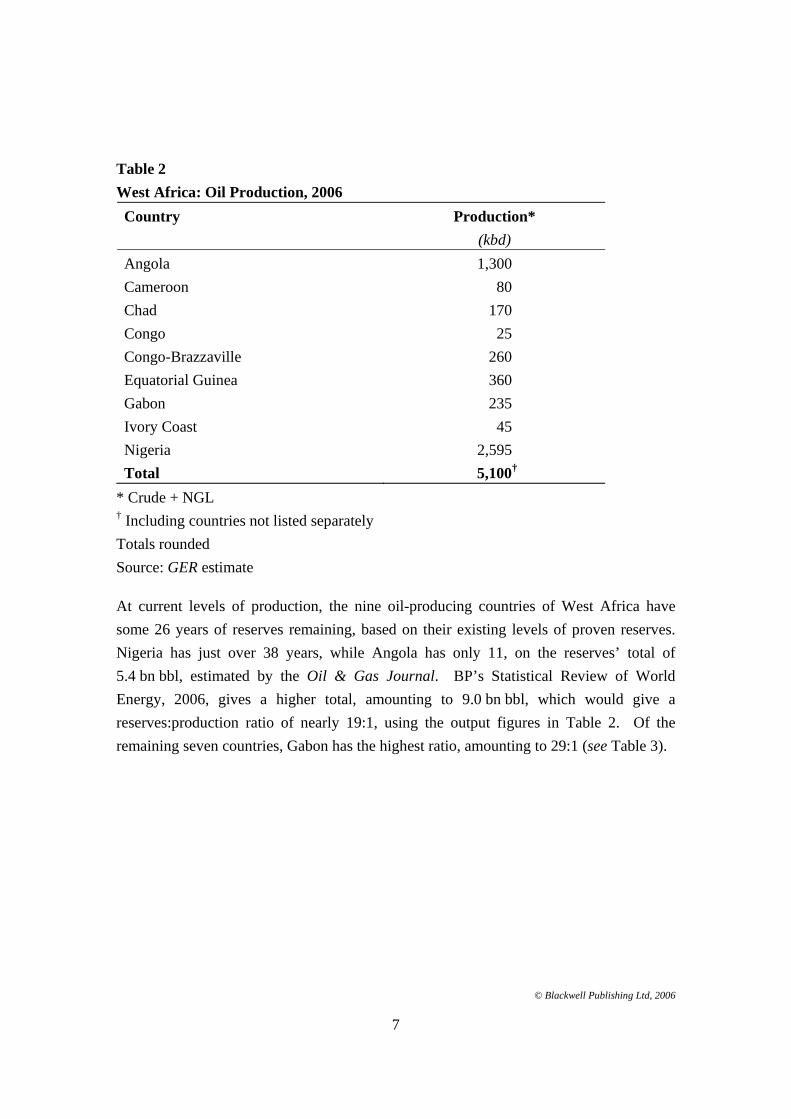

The region’s crude oil and NGL production is similarly concentrated in Nigeria–with an

output of 2.6 mbd, or 51% of the regional total–and Angola, whose 1.3 mbd production

accounts for 25% of regional production. The remaining seven countries produce some

1.2 mn bpd, equivalent to 24% of the total (see Table 2).

©Blackwell Publishing Ltd, 2006

7

Table 2

West Africa: Oil Production, 2006

Country Production*

(kbd)

Angola 1,300

Cameroon 80

Chad 170

Congo 25

Congo-Brazzaville 260

Equatorial Guinea 360

Gabon 235

Ivory Coast 45

Nigeria 2,595

Total 5,100†

* Crude + NGL † Including countries not listed separately

Totals rounded

Source: GER estimate

At current levels of production, the nine oil-producing countries of West Africa have

some 26 years of reserves remaining, based on their existing levels of proven reserves.

Nigeria has just over 38 years, while Angola has only 11, on the reserves’ total of

5.4 bn bbl, estimated by the Oil & Gas Journal. BP’s Statistical Review of World

Energy, 2006, gives a higher total, amounting to 9.0 bn bbl, which would give a

reserves:production ratio of nearly 19:1, using the output figures in Table 2. Of the

remaining seven countries, Gabon has the highest ratio, amounting to 29:1 (see Table 3).

©Blackwell Publishing Ltd, 2006

8

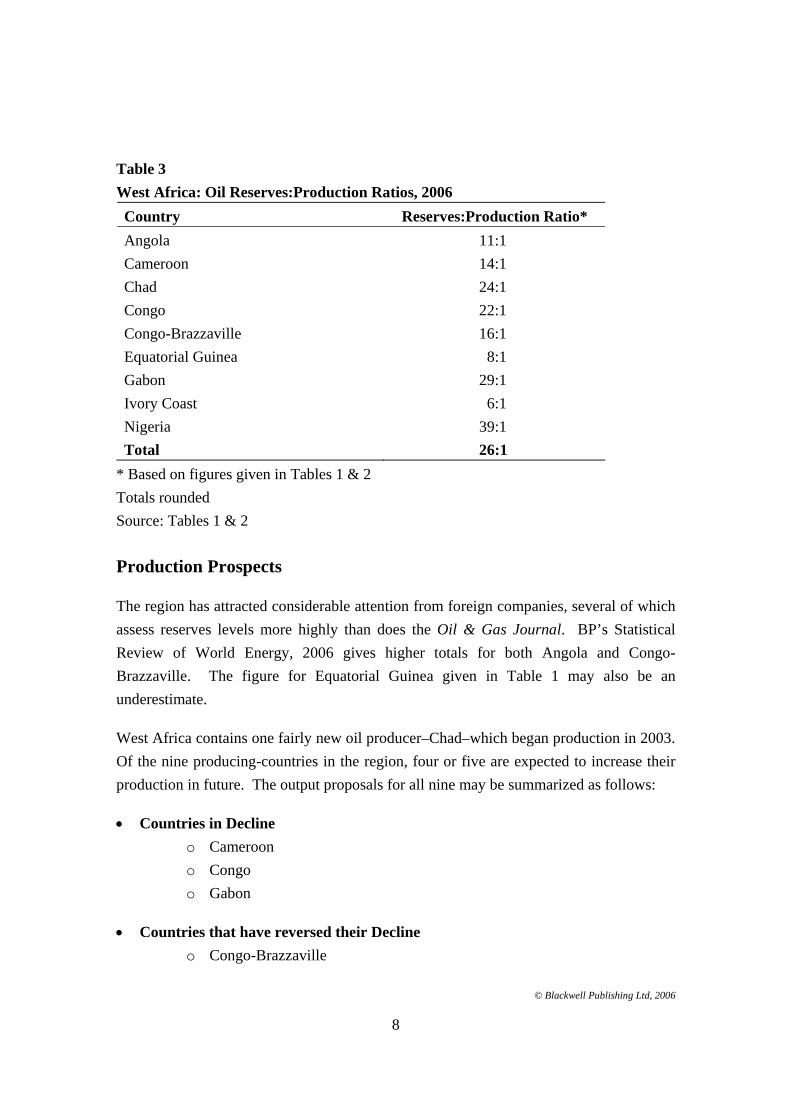

Table 3

West Africa: Oil Reserves:Production Ratios, 2006

Country Reserves:Production Ratio*

Angola 11:1

Cameroon 14:1

Chad 24:1

Congo 22:1

Congo-Brazzaville 16:1

Equatorial Guinea 8:1

Gabon 29:1

Ivory Coast 6:1

Nigeria 39:1

Total 26:1

* Based on figures given in Tables 1 & 2

Totals rounded

Source: Tables 1 & 2

Production Prospects

The region has attracted considerable attention from foreign companies, several of which

assess reserves levels more highly than does the Oil & Gas Journal. BP’s Statistical

Review of World Energy, 2006 gives higher totals for both Angola and Congo-

Brazzaville. The figure for Equatorial Guinea given in Table 1 may also be an

underestimate.

West Africa contains one fairly new oil producer–Chad–which began production in 2003.

Of the nine producing-countries in the region, four or five are expected to increase their

production in future. The output proposals for all nine may be summarized as follows:

Countries in Decline

o Cameroon

o Congo

o Gabon

Countries that have reversed their Decline

o Congo-Brazzaville

©Blackwell Publishing Ltd, 2006

9

Countries where Output is increasing

o Angola

o Equatorial Guinea

o Ivory Coast

o Nigeria

Countries with uncertain Prospects

o Chad

There are a few non-producing countries that are attracting attention from international

oil companies. Some of these may begin to produce oil within the next decade. The most

prospective of these countries appear to be:

o Niger

o Sao Tome e Principe

The prospects for each of these countries are considered in the following sections.

Countries in Decline

The following countries are in long term decline:

o Cameroon

o Congo

o Gabon

Cameroon

Cameroon’s reserves of 400 mn bbl and production of 80,000 bpd must both be

accounted modest, as must its reserves:production ratio of 14:1. Its production of oil has

been in continuous decline since 1997, when it stood at 125,000 bpd.

There appears little prospect of a recovery in output despite the government’s attempts to

encourage foreign exploration activity. Any new discoveries are expected to come from

the Logone Birni and Douala Basins, which are largely unexplored.

Further discoveries will do little more than slow down the rate of decline in Cameroon’s

production. Assuming one or two new developments, it might well be producing

between 30,000 and 50,000 bpd by 2015.

©Blackwell Publishing Ltd, 2006

10

Congo (formerly Zaïre)

The Congo is West Africa’s smallest producer, with output of only 25,000 bpd and

reserves of 200 mn bbl. Years of war have helped to keep outside investment interest

low. Output has declined since 1996, when it was 30,000 bpd. By 2015, it is likely to be

negligible or have ceased altogether.

Gabon

Gabon was once an important West African producer and a member of OPEC. Output

peaked in 1996 at 365,000 bpd, since when it has declined to 235,000 bpd. On the other

hand, it has the best reserves:production ratio of any producer in the region with the

exception of Nigeria. Output looks set to go on declining, perhaps to about 150,000 bpd

by 2015.

Countries that have reversed their Decline

There is just one country in this category.

Congo-Brazzaville

Congo-Brazzaville’s production peaked at 295,000 bpd in 1999 and fell to 240,000 bpd in

2004. Since then, production has revived slightly to 260,000 bpd.

This revival could continue in a modest way thanks to new finds at M’Boundi and Moho-

Bilondo. Production from these fields should partly offset the decline from Congo-

Brazzaville’s older fields. Some 150,000 bpd of new production is scheduled to be

commissioned by 2008. This could provide a temporary boost to output but Congo-

Brazzaville’s long term decline looks likely to resume before 2015, by which time it

should be producing around 200,000 bpd.

Countries where Output is increasing

Countries where output is increasing and expected to go on rising are:

o Angola

o Equatorial Guinea

o Ivory Coast

o Nigeria

©Blackwell Publishing Ltd, 2006

11

Angola

Angola’s output has already increased since 2005, when it produced about 1.3 mn bpd.

The field developments currently under way should more than offset the expected decline

from the older fields of Cabinda, Palanca, Quito and Xikomba. Among the planned

developments are Dalia, Blocks 18 & 31, Pazflor and a possible ultra-deepwater

development by Total in Block 32. Oil production should go on rising to 2010, when it

should be near 2.5 mn bpd. Thereafter there could be a dip in output as the number of

new field developments falls. By 2015, however, output could be in the region of

2.4 mn bpd, assuming Block 32 is by then in operation.

Equatorial Guinea

Equatorial Guinea has promising offshore acreage and production has risen from less

than 20,000 bpd in 1996 to 360,000 bpd in 2005. Increasing condensate production could

add a further 60,000 bpd this year, but the country appears to be more gas-prone than oil-

rich. A new field–the 60,000 bpd Okume development–is due on-stream in 2007.

Chad’s oil production is unlikely to exceed 500,000 bpd and will probably be in decline

by 2015 unless a further large discovery is made, though with further small discoveries it

could be in the region of 300,000 bpd.

Ivory Coast

With output of 45,000 bpd in 2005, Ivory Coast is a minor producer. Its reserves are also

correspondingly small. Rising production from the Baobab field could help to push

output above 60,000 bpd in 2006. Peak production looks likely to be around 100,000 bpd

and output could well be in decline by 2015 and back below 45,000 bpd.

Nigeria

Nigeria has recently raised its reserve estimates by nearly 50% to 35.9 bn bbl (see

Table 1) and has plans to raise this to 40.0 bn bbl by 2010. There has been considerable

upstream activity in Nigeria, much of it by foreign oil companies. Nigeria’s problems lie

not in its reserve levels but in the social and political unrest in the main oil-producing

areas, which has frequently spilled over into violence and delayed several field

developments.

©Blackwell Publishing Ltd, 2006

12

These delays, coupled with disagreements between the government and some foreign oil

companies over upstream contract terms, threaten plans both to find new reserves and to

raise production by 1.4 mn bpd to 4.0 mn bpd. There is also some doubt whether the

deeper parts of the continental shelf contain as much oil as has been estimated. If the

deepwater fields are to be exploited successfully, Nigeria will have to improve its

attractiveness to large international oil companies, since they alone have the funds and

the expertise to develop these fields.

With large scale international involvement and an end to the unrest in the Delta region,

which is the country’s largest producing area, Nigeria might eventually achieve its

4 mn bpd target. Without such developments, it may not go much above 3 mn bpd

between now and 2015.

Countries with uncertain Prospects

There is one country in this category.

Chad

Chad was once considered a most promising oil prospect until a dispute broke out

between the government and a foreign consortium consisting of ExxonMobil, Petronas

and Chevron, which is responsible for Chad’s oil production. The government alleges

under-payment of taxes by the oil companies. On the other hand, the government is

accused by the World Bank of failing to ensure that oil revenues were properly invested

in alleviating poverty and improving the economic infrastructure. The World Bank

helped to finance the development of Chad’s oilfields and the 1,070-mile export pipeline

to Kribi on the Gulf of Guinea. Chad first began producing oil in 2003.

The dispute has not exactly helped Chad’s prospects as an oil producer. A further

problem has arisen, however, which threatens future levels of output. The main

producing area, known as Doba Basin, contains more water in its reservoir structures than

was originally expected. Output in 2005, at 170,000 bpd, is 60,000 bpd, or 26% lower

than planned. Production in 2006 has continued at disappointing levels for what have

been described as ‘technical’ reasons.

The foreign consortium brought a new field, Moundouli, on-stream in 2006 and

announced plans to drill another one, Maikeri, in 2007. Another basin, Lake Chad, is

thought to be prospective and capable of providing commercial quantities of oil. Despite

©Blackwell Publishing Ltd, 2006

13

this, the outlook for Chadian production remains uncertain. It seems unlikely that Chad

will be producing much above 200,000 bpd in 2015.

Countries that may produce Oil by 2015

There are two countries in West Africa that might begin producing oil between now and

2015. They are:

o Niger

o Sao Tome e Principe

Niger

Niger is attracting interest from Asian companies and Algeria’s Sonatrach. Petronas has

already discovered oil, though reserves are thought to be modest. Output in 2015 is

unlikely to exceed 100,000 bpd.

Sao Tome e Principe

Considerable optimism has been expressed for the continental shelf surrounding Sao

Tome e Principe. Development has been delayed, however, by arguments over upstream

terms and the need to agree offshore boundaries. Some foreign companies have dropped

out. Production-sharing contracts are currently being negotiated for an area shared with

Nigeria, known as the Joint Development Zone. Some of the companies involved in

recent licensing rounds have lacked the necessary offshore experience to operate in this

area. There could nevertheless be some production–up to 300,000 bpd–by 2015.

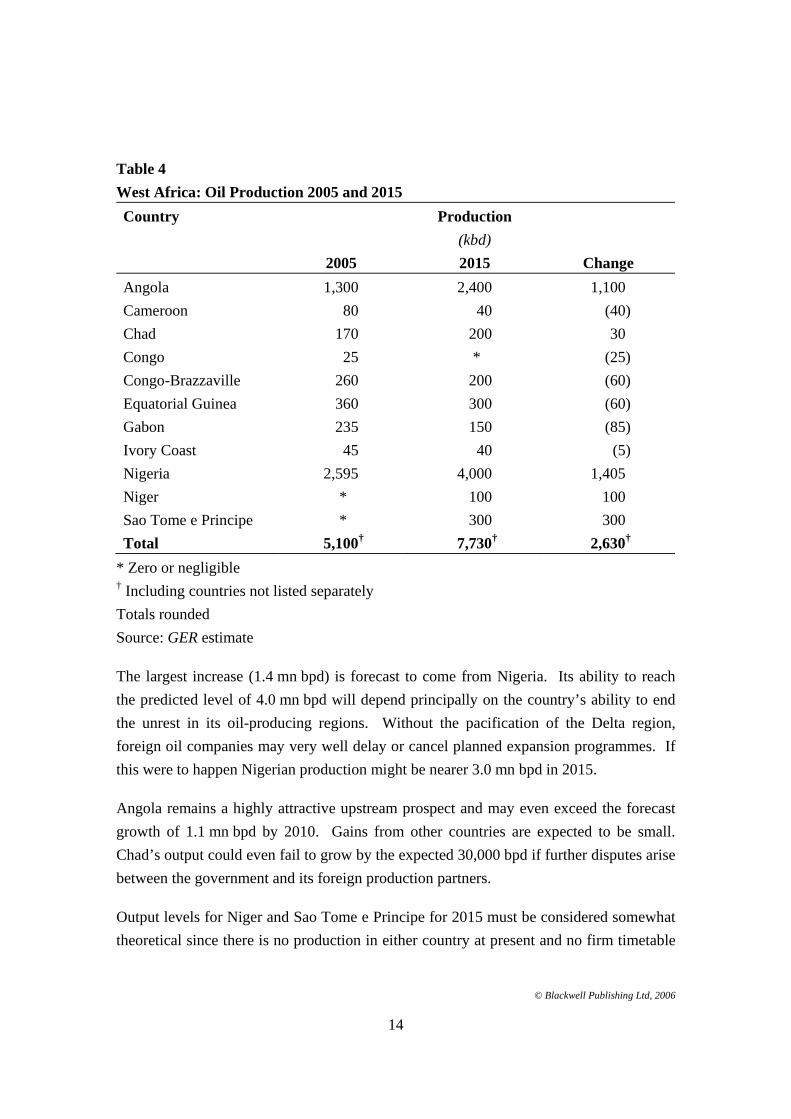

Outlook for Oil Production to 2015

West African oil production should show a net gain by 2015 thanks to growth in six of

the nine oil producers and the start of oil production in two more countries. A complete

forecast is given in Table 4.

©Blackwell Publishing Ltd, 2006

14

Table 4

West Africa: Oil Production 2005 and 2015

Country Production

(kbd)

2005 2015 Change

Angola 1,300 2,400 1,100

Cameroon 80 40 (40)

Chad 170 200 30

Congo 25 * (25)

Congo-Brazzaville 260 200 (60)

Equatorial Guinea 360 300 (60)

Gabon 235 150 (85)

Ivory Coast 45 40 (5)

Nigeria 2,595 4,000 1,405

Niger * 100 100

Sao Tome e Principe * 300 300

Total 5,100† 7,730† 2,630†

* Zero or negligible † Including countries not listed separately

Totals rounded

Source: GER estimate

The largest increase (1.4 mn bpd) is forecast to come from Nigeria. Its ability to reach

the predicted level of 4.0 mn bpd will depend principally on the country’s ability to end

the unrest in its oil-producing regions. Without the pacification of the Delta region,

foreign oil companies may very well delay or cancel planned expansion programmes. If

this were to happen Nigerian production might be nearer 3.0 mn bpd in 2015.

Angola remains a highly attractive upstream prospect and may even exceed the forecast

growth of 1.1 mn bpd by 2010. Gains from other countries are expected to be small.

Chad’s output could even fail to grow by the expected 30,000 bpd if further disputes arise

between the government and its foreign production partners.

Output levels for Niger and Sao Tome e Principe for 2015 must be considered somewhat

theoretical since there is no production in either country at present and no firm timetable

©Blackwell Publishing Ltd, 2006

15

for future developments. Of the two, Sao Tome e Principe appears the more prospective

for oil, though it is something of an exaggeration to say–as some consultants have–that it

may be thought of as ‘the new Kuwait’.

With all these considerations in mind, it is possible to think of West African production

around 7.7 mn bpd in 2015: a rise of 2.6 mn bpd, or just over 50%. This figure of

7.7 mn bpd should nevertheless be considered as a ‘best case scenario’ assuming, as it

does, that major political problems in Nigeria, Chad and elsewhere, will be satisfactorily

resolved.

In the event that these problems are not solved or that further ones arise, then the

forecasts presented in Table 4 may need to be revised downwards by 1.0 mn bpd or more.

The biggest numerical uncertainty exists over Nigeria, which accounts for nearly all the

1 million-plus bpd of uncertainty described above.

The future could nevertheless be bright for the region given the right political

circumstances. Moreover, by 2015, there could even be interest in certain other countries

not listed in Table 4, notably Namibia and the Canary Islands, not to mention in several

unexplored parts of the Gulf of Guinea.

©Blackwell Publishing Ltd, 2006

16

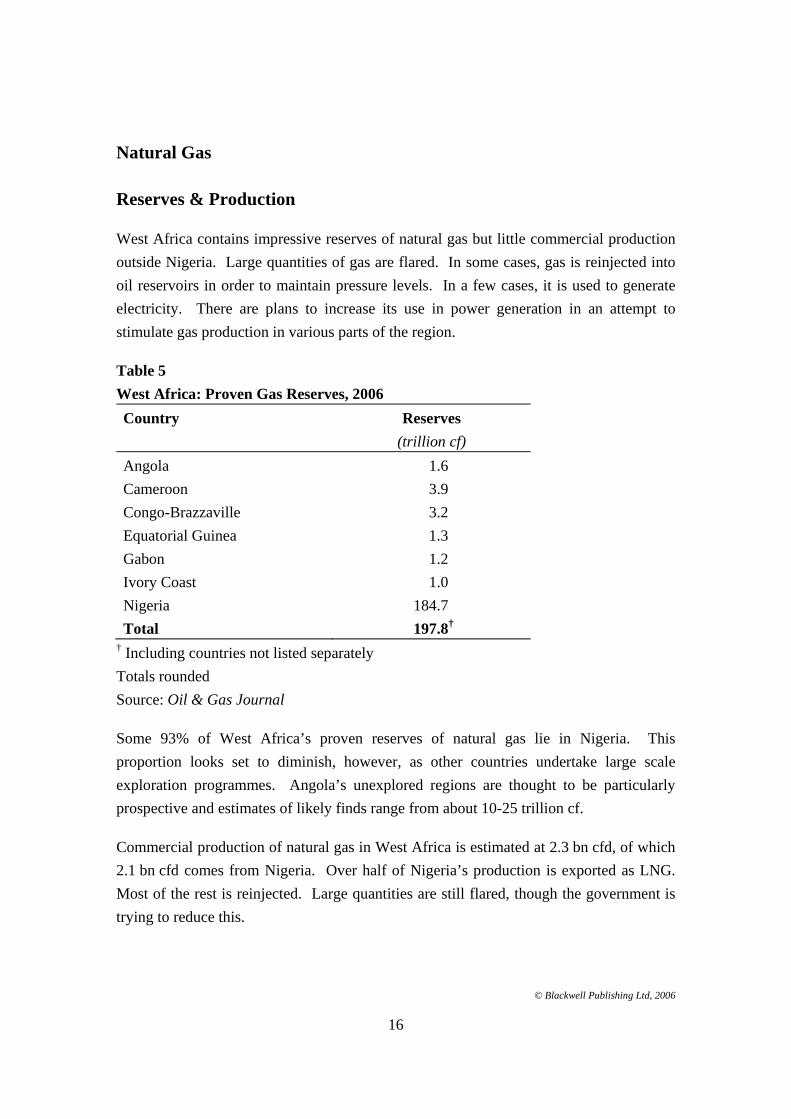

Natural Gas

Reserves & Production

West Africa contains impressive reserves of natural gas but little commercial production

outside Nigeria. Large quantities of gas are flared. In some cases, gas is reinjected into

oil reservoirs in order to maintain pressure levels. In a few cases, it is used to generate

electricity. There are plans to increase its use in power generation in an attempt to

stimulate gas production in various parts of the region.

Table 5

West Africa: Proven Gas Reserves, 2006

Country Reserves

(trillion cf)

Angola 1.6

Cameroon 3.9

Congo-Brazzaville 3.2

Equatorial Guinea 1.3

Gabon 1.2

Ivory Coast 1.0

Nigeria 184.7

Total 197.8†

† Including countries not listed separately

Totals rounded

Source: Oil & Gas Journal

Some 93% of West Africa’s proven reserves of natural gas lie in Nigeria. This

proportion looks set to diminish, however, as other countries undertake large scale

exploration programmes. Angola’s unexplored regions are thought to be particularly

prospective and estimates of likely finds range from about 10-25 trillion cf.

Commercial production of natural gas in West Africa is estimated at 2.3 bn cfd, of which

2.1 bn cfd comes from Nigeria. Over half of Nigeria’s production is exported as LNG.

Most of the rest is reinjected. Large quantities are still flared, though the government is

trying to reduce this.

©Blackwell Publishing Ltd, 2006

17

On current production levels, Nigeria’s gas reserves are sufficient to last for more than

100 years, as are those of the rest of West Africa. The increase of commercial production

should reduce these reserves:production ratios considerably across the region.

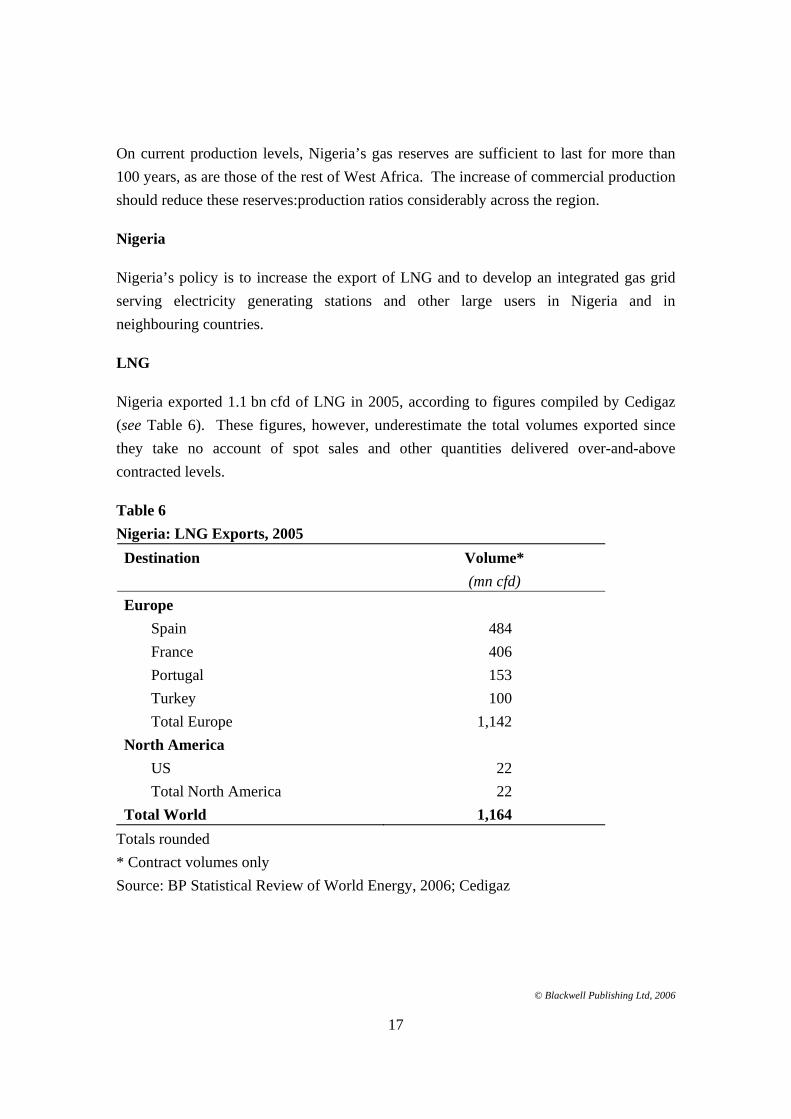

Nigeria

Nigeria’s policy is to increase the export of LNG and to develop an integrated gas grid

serving electricity generating stations and other large users in Nigeria and in

neighbouring countries.

LNG

Nigeria exported 1.1 bn cfd of LNG in 2005, according to figures compiled by Cedigaz

(see Table 6). These figures, however, underestimate the total volumes exported since

they take no account of spot sales and other quantities delivered over-and-above

contracted levels.

Table 6

Nigeria: LNG Exports, 2005

Destination Volume*

(mn cfd)

Europe

Spain 484

France 406

Portugal 153

Turkey 100

Total Europe 1,142

North America

US 22

Total North America 22

Total World 1,164

Totals rounded

* Contract volumes only

Source: BP Statistical Review of World Energy, 2006; Cedigaz

©Blackwell Publishing Ltd, 2006

18

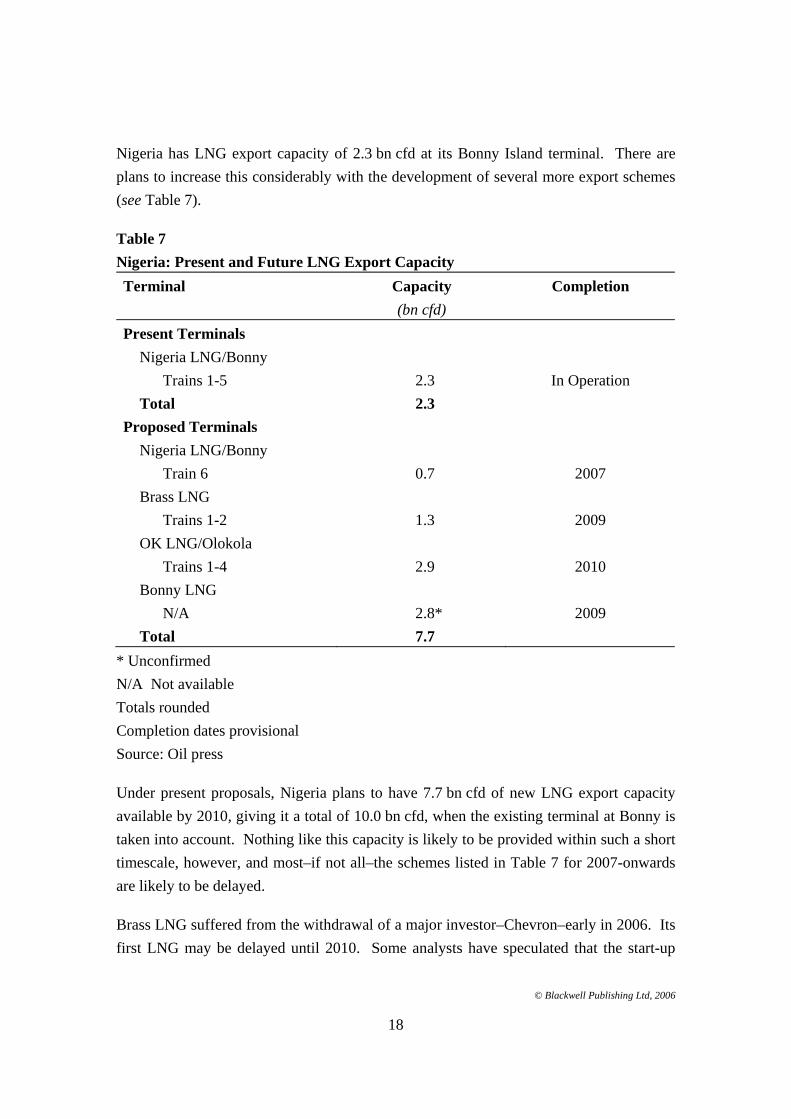

Nigeria has LNG export capacity of 2.3 bn cfd at its Bonny Island terminal. There are

plans to increase this considerably with the development of several more export schemes

(see Table 7).

Table 7

Nigeria: Present and Future LNG Export Capacity

Terminal Capacity Completion

(bn cfd)

Present Terminals

Nigeria LNG/Bonny

Trains 1-5 2.3 In Operation

Total 2.3

Proposed Terminals

Nigeria LNG/Bonny

Train 6 0.7 2007

Brass LNG

Trains 1-2 1.3 2009

OK LNG/Olokola

Trains 1-4 2.9 2010

Bonny LNG

N/A 2.8* 2009

Total 7.7

* Unconfirmed

N/A Not available

Totals rounded

Completion dates provisional

Source: Oil press

Under present proposals, Nigeria plans to have 7.7 bn cfd of new LNG export capacity

available by 2010, giving it a total of 10.0 bn cfd, when the existing terminal at Bonny is

taken into account. Nothing like this capacity is likely to be provided within such a short

timescale, however, and most–if not all–the schemes listed in Table 7 for 2007-onwards

are likely to be delayed.

Brass LNG suffered from the withdrawal of a major investor–Chevron–early in 2006. Its

first LNG may be delayed until 2010. Some analysts have speculated that the start-up

©Blackwell Publishing Ltd, 2006

19

may be even later. OK LNG’s commissioning has already been put back from 2009 to

2010 and could slip into 2011. Bonny LNG is reported behind its original schedule and

may not open until around 2012.

The success of these schemes depends to a considerable extent on the ability of the

Nigerian authorities to bring the unrest in its oil and gas-producing regions under control.

Several foreign companies, which constitute a major target for protestors, are known to

be uneasy about the continuing rise in violence in the Delta region. What is particularly

alarming is the way the violence has spread from its original target–the oil industry–to

include installations operated by foreign gas companies.

Gas-to-Power

In addition to its ambitious LNG export plans, Nigeria wants to build a pipeline

transmission system connecting its gasfields with potential consumers in neighbouring

countries. The principal target is the power sector, and the aim is to establish an

integrated gas and power grid across large parts of West Africa, consisting of gas-fired

power stations linked by a new electricity grid covering the region.

The gas transmission network will be based on a trunkline known as the West African

Gas Pipeline, which is to be built in stages westwards from Nigeria. It is hoped that other

large gas-using customers will sign-up for supplies to supplement the volumes taken by

the power generators.

©Blackwell Publishing Ltd, 2006

20

Outlook for Nigerian Gas

There is no physical reason why Nigeria should not greatly increase its present level of

gas production of 2.1 bn cfd considerably. Much of the increase will be dictated by the

speed at which new LNG terminals can be built. Nigeria could have more than

10.0 bn cfd of LNG and pipeline export capacity by 2015, though this figure could be

considerably lower if one or more of the LNG schemes listed in Table 7 were to be

further delayed or even cancelled. Much will depend on the government’s ability to bring

peace to its south-eastern region.

Other Gas Producers

Small amounts of gas are produced outside Nigeria, but a great deal is flared.

Commercial production in the rest of West Africa looks to be in the region of 0.2 bn cfd.

Several countries, however, plan to develop domestic markets for their gas and, in some

cases, to export it.

The principal potential gas producers are:

o Angola

o Cameroon

o Equatorial Guinea

o Gabon

o Ghana

Angola

Angola’s proven reserves of 1.6 trillion cf are at present modest, but this figure is likely

to increase sharply as exploration increases. The country’s gas is at present flared,

reinjected into oil reservoirs or processed for the recovery of LPG. The government

plans to reduce flaring and develop a domestic market, but the main stimulus to gas

exploration and production is likely to come from the possibility of exporting it as LNG.

The national oil company Sonangol, has joined BP, ExxonMobil, Total and Chevron in

promoting a 0.7 bn cfd LNG export scheme. First gas is due sometime before 2011,

though this timetable could slip.

Once the LNG scheme acquires a firm timetable, exploration should receive a

considerable boost. Outside estimates put Angola’s likely future proven reserve levels

©Blackwell Publishing Ltd, 2006

21

around 10 trillion cf, and some even go as high as 25 trillion cf. Everything depends,

however, on the possibilities for export.

Cameroon

Cameroon has the largest proven gas reserves in West Africa outside Nigeria at present,

with an estimated total of 3.9 trillion cf. More discoveries of associated gas are expected

in the Kribi-Campo, Douala and Rio Del Rey Basins, but the local gas market is tiny.

Gas production may nevertheless rise as a result of the development of local gas-using

industries, but output is likely to remain small for the foreseeable future.

Equatorial Guinea

Equatorial Guinea’s 1.3 trillion cf of reserves lie offshore, mainly in the Alba and Zafiro

fields. Some are associated gas from the Zafiro oilfield, but most are found in the Alba

gasfield. The total is expected to rise following the start of work on the first train of an

LNG export terminal.

The LNG Project, which is led by Marathon and includes Mitsui, Marubeni and state gas

company Sonagas, is due for completion in the third quarter of 2007, with an initial

capacity of 0.5 bn cfd. Additions to capacity are being considered to handle gas from

Equatorial Guinea and possibly from neighbouring countries.

The gas for the first stage will come from the Alba field, but the government wants

associated gas that is currently flared on ExxonMobil’s Zafiro oilfield to be piped to the

new LNG terminal. Some 190 mn cfd of gas is flared at present, according to the

country’s Ministry of Mines, Industry and Energy.

Gabon

Gabon has a small gas production based on its reserves of 1.2 trillion cf. Output is in the

region of 0.1 bn cfd. A small local market exists, based mainly on electricity generation

and some heavy industry. Some gas is also reinjected into the Rabi-Kounga oilfield.

There are plans to make further use of gas in the industrial sector, but production is

unlikely to rise by very much over the coming years.

©Blackwell Publishing Ltd, 2006

22

Ghana

Proven reserves of 840 bn cf and plans to liberalize the country’s petroleum licensing

regime are beginning to arouse outside interest in both oil and gas in Ghana. Plans to

reduce the share of unreliable hydro-electricity in the country’s energy balance may

stimulate further interest in exploration for gas, which is emerging as the fuel of choice

for future electricity generating plants. Despite this, gas production is unlikely to be

more than 0.1 bn cfd by 2015.

Outlook for Natural Gas to 2015

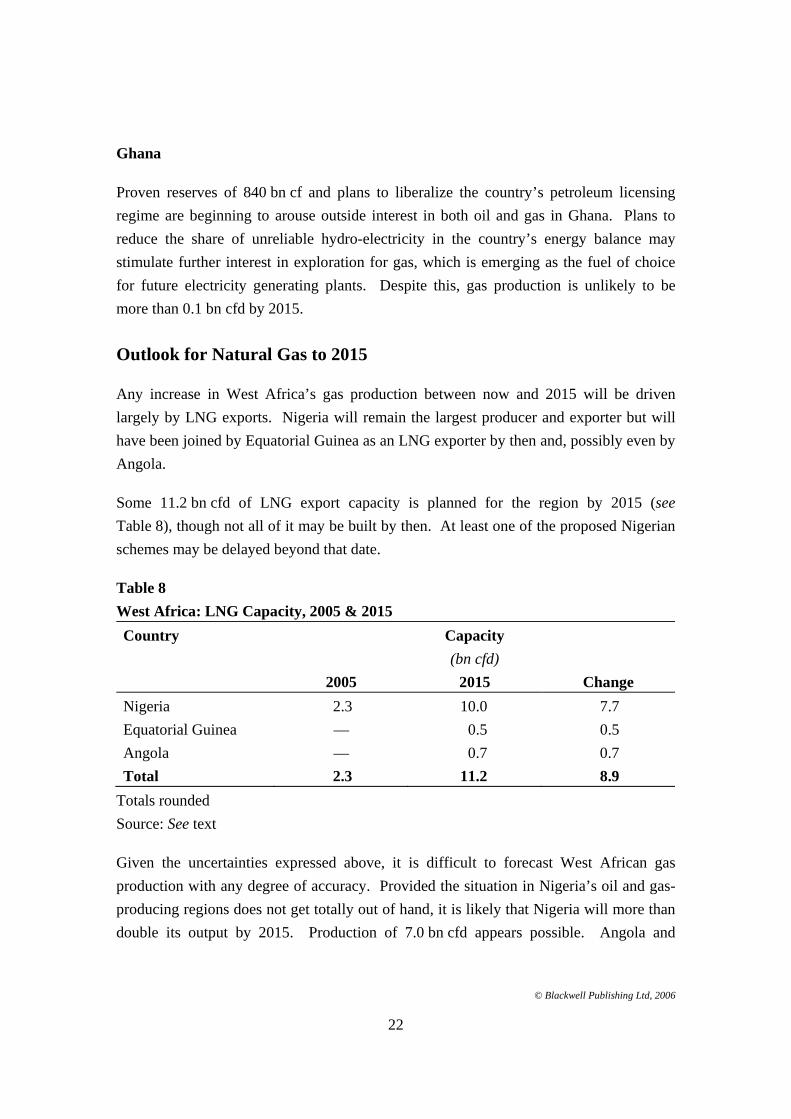

Any increase in West Africa’s gas production between now and 2015 will be driven

largely by LNG exports. Nigeria will remain the largest producer and exporter but will

have been joined by Equatorial Guinea as an LNG exporter by then and, possibly even by

Angola.

Some 11.2 bn cfd of LNG export capacity is planned for the region by 2015 (see

Table 8), though not all of it may be built by then. At least one of the proposed Nigerian

schemes may be delayed beyond that date.

Table 8

West Africa: LNG Capacity, 2005 & 2015

Country Capacity

(bn cfd)

2005 2015 Change

Nigeria 2.3 10.0 7.7

Equatorial Guinea — 0.5 0.5

Angola — 0.7 0.7

Total 2.3 11.2 8.9

Totals rounded

Source: See text

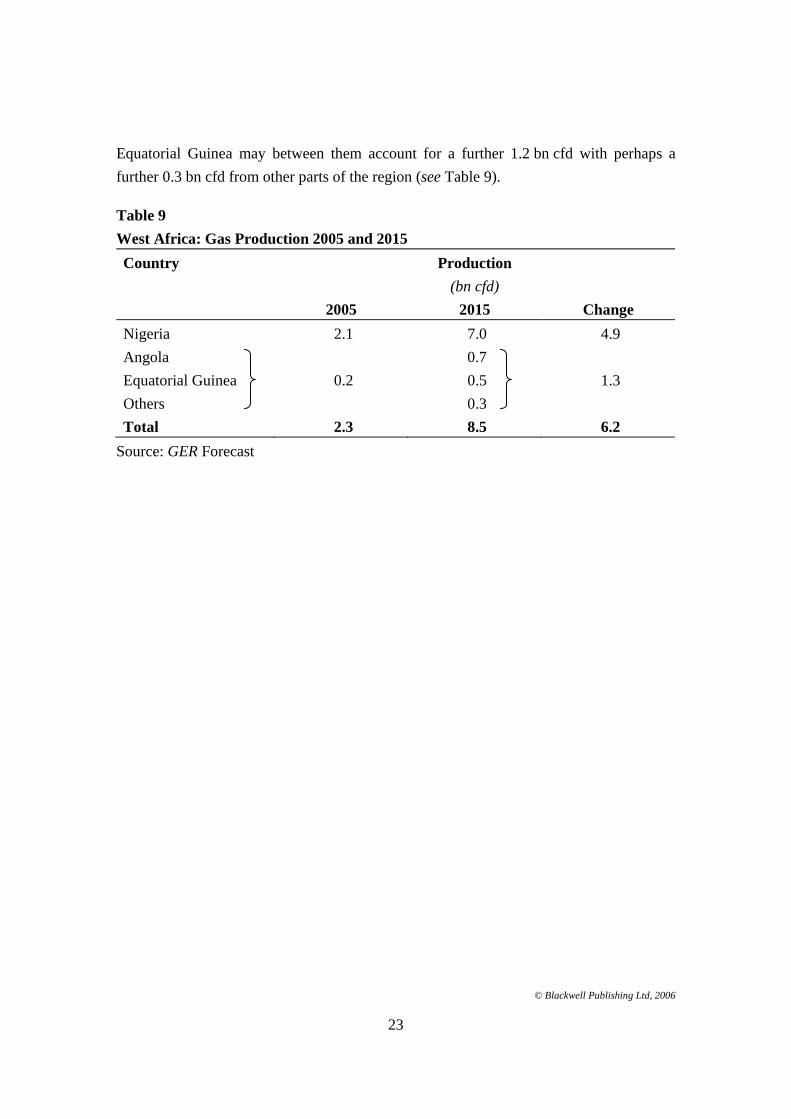

Given the uncertainties expressed above, it is difficult to forecast West African gas

production with any degree of accuracy. Provided the situation in Nigeria’s oil and gas-

producing regions does not get totally out of hand, it is likely that Nigeria will more than

double its output by 2015. Production of 7.0 bn cfd appears possible. Angola and

©Blackwell Publishing Ltd, 2006

23

Equatorial Guinea may between them account for a further 1.2 bn cfd with perhaps a

further 0.3 bn cfd from other parts of the region (see Table 9).

Table 9

West Africa: Gas Production 2005 and 2015

Country Production

(bn cfd)

2005 2015 Change

Nigeria 2.1 7.0 4.9

Angola 0.7

Equatorial Guinea 0.2 0.5 1.3

Others 0.3

Total 2.3 8.5 6.2

Source: GER Forecast

©Blackwell Publishing Ltd, 2006

24

Gas to Liquids

Small amounts of liquids produced from the synthesis of natural gas in the gas-to-liquids

(GTL) process may be available from West Africa by 2015. Several schemes have been

proposed, notably in Nigeria.

A project to produce 34,000 bpd of GTL naphtha, diesel and LPG is under way at

Escravos in Nigeria. It will use about 300 mn cfd of gas that is at present flared. The

prime mover behind the Escravos project is Chevron. Other companies interested in

developing GTL in Nigeria are South Africa’s Sasol and Syntroleum of the US, both of

which have developed processing technology for GTL.

GTL could provide a useful way of monetizing small and isolated gas deposits in the

absence of any gas transmission network. Nigeria could well have production in the

region of 100,000 bpd by 2015, and a similar amount may be produced elsewhere in the

region by then.

Recommended