Unión Andina de Cementos S.A.A. and Subsidiaries

Consolidated financial statements as of December 31, 2014 and 2013 together with the Independent Auditor’s Report

Unión Andina de Cementos S.A.A. and Subsidiaries

Consolidated financial statements as of December 31, 2014 and 2013

together with the Independent Auditor’s Report

Content

Independent Auditor’s Report

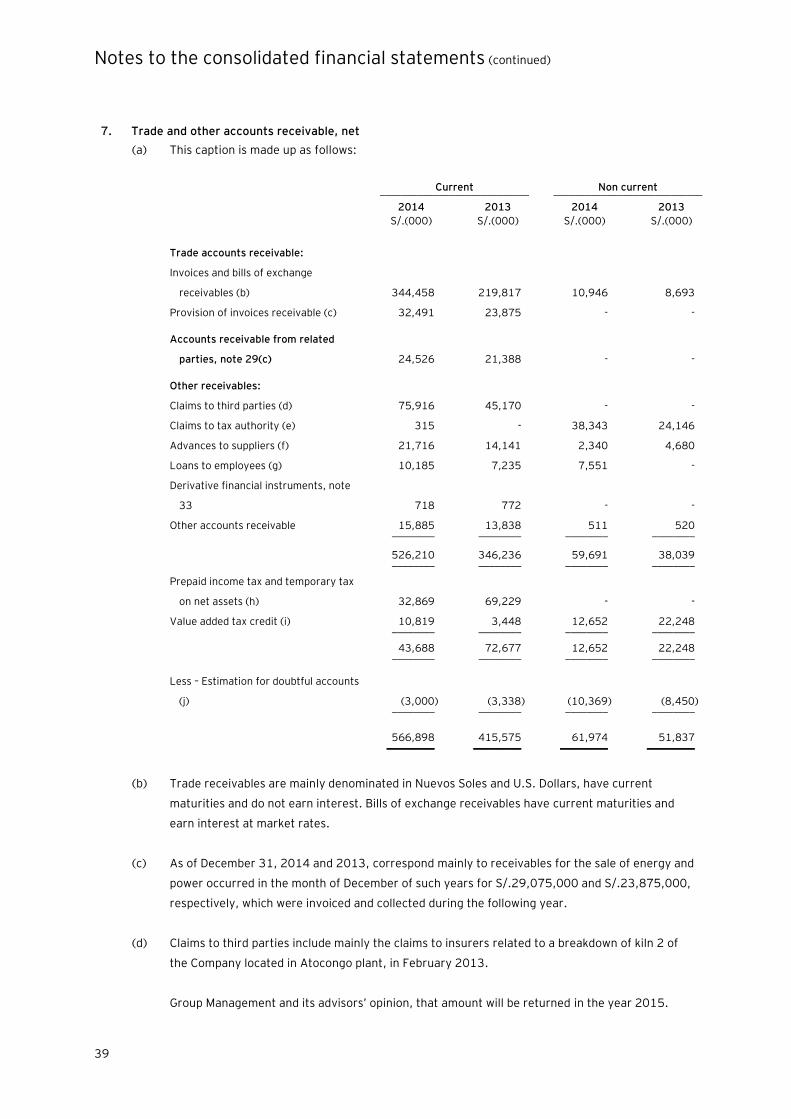

Consolidated financial statements

Consolidated statement of financial position

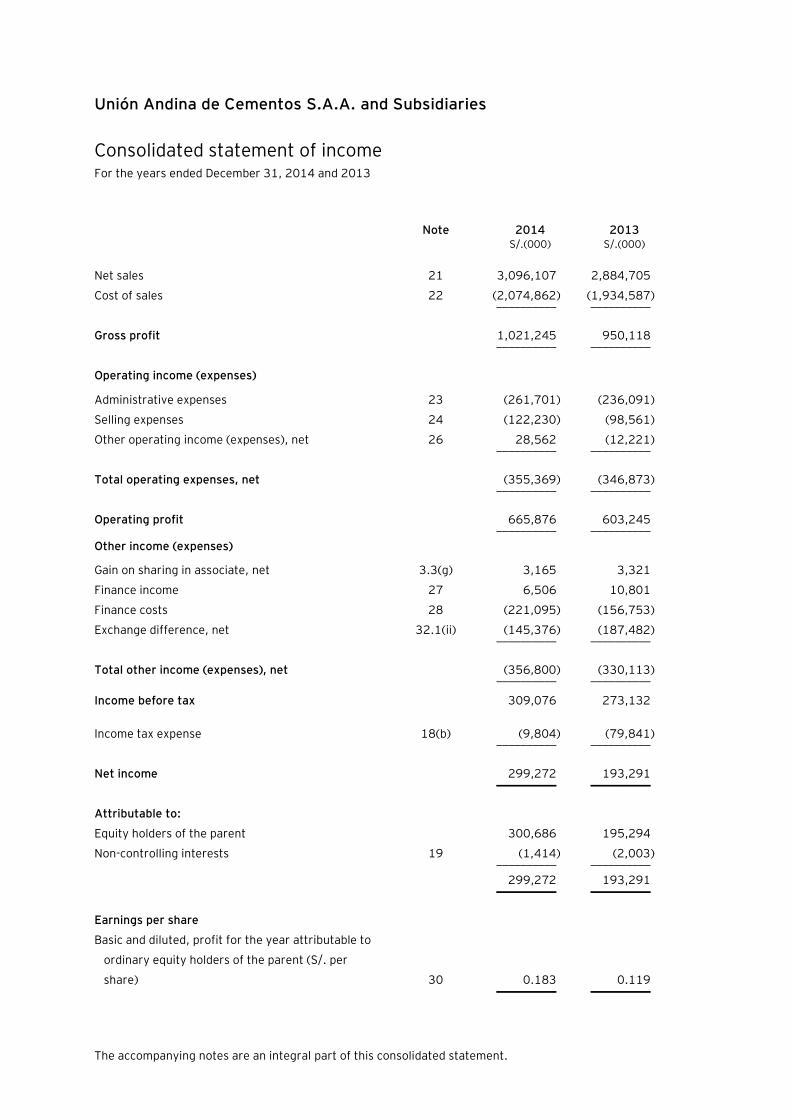

Consolidated statement of income

Consolidated statement of comprehensive income

Consolidated statement of changes in equity

Consolidated statement of cash flows

Notes to the consolidated financial statements

Inscrita en la partida 11396556 del Registro de Personas Jurídicas de Lima y Callao

Miembro de Ernst & Young Global

Independent Auditors’ Report

Paredes, Zaldívar, Burga & Asociados Sociedad Civil de Responsabilidad Limitada

To the Shareholders of Unión Andina de Cementos S.A.A. and Subsidiaries

We have audited the accompanying consolidated financial statements of Unión Andina de Cementos

S.A.A. (a Peruvian corporation), which comprise the consolidated statements of financial position as

of December 31, 2014 and 2013, and the related consolidated statements of income,

comprehensive income, changes in equity and cash flows for the years ended December 31, 2014

and 2013, and a summary of significant accounting policies and other explanatory notes.

Management responsibility for the Consolidated Financial Statements

Management is responsible for the preparation and fair presentation of these consolidated financial

statements in accordance with International Financial Reporting Standards and for the internal

control that Management determines is appropriate to the preparation of consolidated financial

statements that are free from material misstatement, whether due fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these consolidated financial statements based on our

audits. We conducted our audit in accordance with International Standards on Auditing approved for

application in Peru by the Board of Deans of Institutes of Peruvian Certified Public Accountants.

Those standards require that we comply with ethical standards, and to plan and perform the audit to

obtain reasonable assurance about whether the consolidated financial statements are free from

material misstatements.

An audit involves performing procedures to obtain audit evidence about the amounts and

disclosures in the consolidated financial statements. The procedures selected depend on the

auditor’s judgment, including the assessment of the risks of material misstatement of the

consolidated financial statements, whether due to fraud or error. In making those risk assessments,

the auditor considers internal control relevant to the entity’s preparation and fair presentation of

the consolidated financial statements in order to design audit procedures that are appropriate in the

circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s

internal control. An audit also includes evaluating the appropriateness of accounting policies used

and the reasonableness of accounting estimates made by Management, as well as evaluating the

overall presentation of the consolidated financial statements.

Independent Auditors’ Report (continued)

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis

for our audit opinion.

Opinion

In our opinion, the accompanying consolidated financial statements, present fairly, in all material

aspects, the consolidated financial position of Unión Andina de Cementos S.A.A. and Subsidiaries as

of December 31, 2014 and 2013, and its financial performance and cash flows for the years ended

December 31, 2014 and 2013, in accordance with International Financial Reporting Standards.

Lima, Peru,

March 26, 2015

Countersigned by:

__________________________

Mayerling Zambrano R.

C.P.C.C. Registration No. 23765

The accompanying notes are an integral part of this consolidated statement.

Unión Andina de Cementos S.A.A. and Subsidiaries

Consolidated statement of financial position As of December 31, 2014 and 2013

Note 2014 2013 S/.(000) S/.(000)

Assets

Current assets

Cash and cash equivalents 6 135,982 322,348

Trade and other receivables, net 7 566,898 415,575

Inventories, net 8 699,682 559,244

Prepaid expenses 9 30,884 29,861

___________ ___________

Total current assets 1,433,446 1,327,028 ___________ ___________

Non-current assets

Trade and other receivables, net 7 61,974 51,837

Investment in associate 3.3(g) 14,812 12,951

Mining concessions and property, plant and

equipment, net 10 7,025,281 6,154,657

Deferred stripping cost 11 135,952 142,815

Intangible assets, net and goodwill 12 1,383,536 220,902

Deferred income tax assets 18(a) 186,084 127,811

Other non-financial assets 13 13,617 1,159

___________ ___________

Total non-current assets 8,821,256 6,712,132 ___________ ___________

Total assets 10,254,702 8,039,160

___________ ___________

Note 2014 2013 S/.(000) S/.(000)

Liability and equity

Current liabilities

Other financial liabilities 14 742,308 892,908

Trade and other payables 15 590,689 390,512

Deferred income 16 62,733 44,495

Liability for income tax 29,522 661

Provisions 17 57,775 24,766 ___________ ___________

Total current liabilities 1,483,027 1,353,342 ___________ ___________

Non-current liabilities

Other financial liabilities 14 4,137,487 2,339,277

Trade and other payables 15 45,265 46,069

Derivative financial instruments 33 41,439 52,307

Deferred income tax liability 18(a) 590,100 598,295

Provisions 17 23,765 13,663 ___________ ___________

Total non-current liabilities 4,838,056 3,049,611 ___________ ___________

Total liabilities 6,321,083 4,402,953 ___________ ___________

Equity 20

Capital stock 1,646,503 1,646,503

Legal reserve 299,214 270,303

Unrealized net loss on hedging financial derivative

instruments (38,096) (39,803)

Result from foreign currency translation 25,292 (35,065)

Retained earnings 1,784,952 1,606,202 ___________ ___________

Equity attributable to equity holders of the parent 3,717,865 3,448,140

Non-controlling interests 19 215,754 188,067 ___________ ___________

Total equity 3,933,619 3,636,207 ___________ ___________

Total liabilities and equity 10,254,702 8,039,160 ___________ ___________

The accompanying notes are an integral part of this consolidated statement.

Unión Andina de Cementos S.A.A. and Subsidiaries

Consolidated statement of income For the years ended December 31, 2014 and 2013

Note 2014 2013 S/.(000) S/.(000)

Net sales 21 3,096,107 2,884,705

Cost of sales 22 (2,074,862) (1,934,587) __________ __________

Gross profit 1,021,245 950,118 __________ __________

Operating income (expenses)

Administrative expenses 23 (261,701) (236,091)

Selling expenses 24 (122,230) (98,561)

Other operating income (expenses), net 26 28,562 (12,221) __________ __________

Total operating expenses, net (355,369) (346,873) __________ __________

Operating profit 665,876 603,245 __________ __________

Other income (expenses)

Gain on sharing in associate, net 3.3(g) 3,165 3,321

Finance income 27 6,506 10,801

Finance costs 28 (221,095) (156,753)

Exchange difference, net 32.1(ii) (145,376) (187,482) __________ __________

Total other income (expenses), net (356,800) (330,113) __________ __________

Income before tax 309,076 273,132

Income tax expense 18(b) (9,804) (79,841) __________ __________

Net income 299,272 193,291 __________ __________

Attributable to:

Equity holders of the parent 300,686 195,294

Non-controlling interests 19 (1,414) (2,003) __________ __________

299,272 193,291 __________ __________

Earnings per share

Basic and diluted, profit for the year attributable to

ordinary equity holders of the parent (S/. per

share) 30 0.183 0.119 __________ __________

The accompanying notes are an integral part of this consolidated statement.

Unión Andina de Cementos S.A.A. and Subsidiaries

Statements of comprehensive income For the years ended December 31, 2014 and 2013

2014 2013 S/.(000) S/.(000)

Net income 299,272 193,291 _________ _________

Other comprehensive income

Changes in the fair value of hedging derivative financial

instruments, note 32.1(i) 6,493 22,422

Income tax effect, note 32.1(i) and 18 (2,042) (5,157)

Result from foreign currency translation 61,753 77,291 _________ _________

Other comprehensive income, net of income tax 66,204 94,556 _________ _________

Total comprehensive income 365,476 287,847 _________ _________

Attributable to:

Equity holders of the parent 362,750 285,609

Non-controlling interests 2,726 2,238 _________ _________

365,476 287,847 _________ _________

Las Notas a los estados financieros consolidados adjuntos son parte integrante de este estado.

Unión Andina de Cementos S.A.A. and Subsidiaries

Consolidated statement of changes in equity For the years ended December 31, 2014 and 2013

Equity attributable to equity holders of the parent __________________________________________________________________________________________________________

Capital

stock

Legal

reserve

Unrealized net

loss on hedging

financial

derivative

instruments

Result from

foreign currency

translation

Retained

earnings Total

Non-controlling

interests

Total

equity S/.(000) S/.(000) S/.(000) S/.000 S/.(000) S/.(000) S/.(000) S/.(000)

Balance as of January 1, 2013 1,646,503 249,871 (56,321) (108,862) 1,529,497 3,260,688 183,410 3,444,098 __________ __________ __________ __________ __________ __________ __________ __________

Net income - - - - 195,294 195,294 (2,003) 193,291

Other comprehensive income for the year, net of

income tax - - 16,518 73,797 - 90,315 4,241 94,556 __________ __________ __________ __________ __________ __________ __________ __________

Total comprehensive net income - - 16,518 73,797 195,294 285,609 2,238 287,847

Dividend distributions, note 20(d) - - - - (83,971) (83,971) - (83,971)

Transfer to legal reserve, note 20(b) - 20,475 - - (20,475) - - -

Changes in non-controlling interests and other - (43) - - (14,143) (14,186) 2,419 (11,767) __________ __________ __________ __________ __________ __________ __________ __________

Balance as of December 31, 2013 1,646,503 270,303 (39,803) (35,065) 1,606,202 3,448,140 188,067 3,636,207

Net income - - - - 300,686 300,686 (1,414) 299,272

Other comprehensive income for the year, net of

income tax - - 1,707 60,357 - 62,064 4,140 66,204 __________ __________ __________ __________ __________ __________ __________ __________

Total comprehensive net income - - 1,707 60,357 300,686 362,750 2,726 365,476

Dividend distributions, note 20(d) - - - - (85,619) (85,619) - (85,619)

Transfer to legal reserve, note 20(b) - 29,011 - - (29,011) - - -

Changes in non-controlling interests and other - (100) - - (3,278) (3,378) 3,378 -

Non-controlling interests arising on a business

combination, note 2(a) and (b) - - - -

-

-

23,228

23,228

Acquisition of non-controlling interests, note 2(b) - - - - (4,028) (4,028) (1,645) (5,673) __________ __________ __________ __________ __________ __________ __________ __________

Balance as of December 31, 2014 1,646,503 299,214 (38,096) 25,292 1,784,952 3,717,865 215,754 3,933,619 __________ __________ __________ __________ __________ __________ __________ __________

The accompanying notes are an integral part of this consolidated statement.

Unión Andina de Cementos S.A.A. and Subsidiaries

Consolidated statement of cash flows For the years ended December 31, 2014 and 2013

2014 2013 S/.(000) S/.(000)

Operating activities

Collections from customers 3,708,772 3,790,120

Payments to suppliers (2,353,929) (2,765,713)

Payments to employees (300,271) (258,845)

Taxes paid (179,911) (124,824)

Interest paid (194,712) (129,091)

Other payments, net (42,802) (57,327) __________ __________

Net cash flows from operating activities 637,147 454,320 __________ __________

Investing activities

Sale of property, plant and equipment 827 2,240

Purchase of property, plant and equipment (461,891) (356,604)

Purchase of intangible assets (9,345) (15,768)

Acquisition of a subsidiary, net of cash acquired (1,502,675) -

Capital contribution to related (1,950) -

Dividends received 3,322 2,892

Acquisition of land available for sale (13,220) -

Other collections (payments) 2,131 2,313 __________ __________

Net cash flows used in investing activities (1,982,801) (364,927) __________ __________

Financing activities

Proceeds from bank overdrafts and loans 455,536 1,002,382

Proceeds from financial obligations 2,160,655 627,763

Payment of bank overdrafts and loans (649,186) (973,126)

Payment of financial obligations (729,317) (526,758)

Dividends paid (85,619) (83,971)

Acquisition of non-controlling interests (5,673) - __________ __________

Net cash flows from financing activities 1,146,396 46,290 __________ __________

(Net decrease) net increase in cash and cash equivalents (199,258) 135,683

Foreign exchange difference on cash and cash equivalents 12,892 5,456

Cash and cash equivalents at the beginning of the year 322,348 181,209 __________ __________

Cash and cash equivalents at the end of the year 135,982 322,348 __________ __________

Significant non-cash transactions -

Acquisition of property, plant and equipment under finance leasing 69,931 70,229

Otther property, plant and equipment 20,765 -

Other intangible assets 37 -

Compensation of leaseback - 138,156

Capitalized interest - 25,381

Unión Andina de Cementos S.A.A. and Subsidiaries

Note to the consolidated financial statements As of December 31, 2014 and 2013

1. Economic activity

Unión Andina de Cementos S.A.A. (hereinafter “the Company” or “UNACEM”) was incorporated in

December 1967. The Company is a subsidiary of Sindicato de Inversiones y Administración S.A.

(hereinafter “the Principal”) which holds 43.38 percent of the Company’s capital stock, which in turn is

a subsidiary of Nuevas Inversiones S.A., ultimate parent of the consolidated economic group.

The registered office of the Company is located at Av. Atocongo 2440, Villa María del Triunfo, Lima,

Peru.

The Company’s main activity is the production and sale, for local and foreign sales of cement and

clinker. For this purpose, the Company owns two plants located at Lima and Junin, whose capacity is

6.68 million tonnes of clinker and 7.60 million tonnes of cement.

The consolidated financial statements of the Company and Subsidiaries (hereinafter “the Group”) as of

December 31, 2013 were approved by General Shareholders Meeting held on March 27, 2014. The

consolidated financial statements the year 2014 were approved by Management of Group.

As of December 31, 2014 and 2013, the consolidated financial statements include the financial

statements of the Company and the following subsidiaries:

- Skanon Investments, Inc. – SKANON

It is an entity incorporated in February 2007 in the state of Arizona, United States of America, in

which the Company owns directly and indirectly 95.36 percent share of the capital stock as of

December 31, 2014 (95.06 percent as of December 31, 2013), whose main activity is

investment in securities.

As of December 31, 2014 and 2013, SKANON holds a share in the capital of Drake Cement LLC

of 93.98 and 93.95 percent, respectively. DRAKE is an entity located in the United States of

America, whose main business is the production and marketing of cement in the states of Arizona

and Nevada.

Additionally, SKANON maintains 100 percent stake in the capital of Sunshine Concrete &

Materials, Inc. ("Drake Materials"), an entity located in the United States of America, whose main

activity is the sale of ready-mix concrete, sand and gravel.

Notes to the consolidated financial statements (continued)

2

- Inversiones Imbabura S.A. - IMBABURA

On July 2014, the Company established IMBABURA and owns directly and indirectly the 100

percent of the shares of capital. IMBABURA main activity is investment in securities in entities

domiciled in Ecuador, mainly dedicated to the cement industry related activities, ready-mixed

concrete, building materials and related activities.

IMBABURA´s subsidiaries are entities that belong to the group UNACEM Ecuador S.A. ("UNACEM

Ecuador" formerly Lafarge Cement S.A.) and subsidiaries, whose main activity is the exploitation,

industrialization cement and its derivatives and related services. Due to that the acquisition of

UNACEM Ecuador was realized on November 25, 2014, the income for the consolidated

statements of income correspond to 37 days after the date of control´s took until December 31,

2014, for more details see note 2(b).

- Compañía Eléctrica El Platanal S.A. – CELEPSA

It is an entity incorporated in December 2005, direct subsidiary of the Company who owns 90

percent share of the capital stock. The main activity of CELEPSA is the generation and sale of

electricity using water resources.

On November 2014, CELEPSA acquired Hidroeléctrica Marañón S.C.R.L. ("HIDRO Marañón") with

purpose of to implement the project of the future Marañon´s Hydroelectric Central. CELEPSA

owns directly and indirectly 100 percent share of the capital stock, for more details see note

2(c).

- Inversiones en Concreto y Afines S.A. - INVECO

It is an entity constituted in Lima in April 1996, Company´s direct subsidiary, who owns 93.38

percent share of the capital stock. It is dedicated to investing in companies principally engaged in

supplying concrete pre-mixed, building materials and related activities through its subsidiary

Union Concreteras S.A., which holds 99.99 per cent stake, which in turn owns 99.99 percent of

Firth Industries Perú S.A., dedicated to the same category.

- Unión de Concreteras S.A. – UNICON

It is an entity constituted in December 1995, Company´s indirect subsidiary, through INVECO

holds 99.99 percent share of the capital stock. UNICON main activity is the development and

commercialization of concrete, and to a lesser extent related products such as bricks and

concrete sleepers. For the preparation of concrete, UNICON requires mainly cement, stone, sand

and additives.

- Firth Industries Perú S.A. – FIRTH

It is an entity constituted in March 1995, Company´s indirect subsidiary, through INVECO holds

99.99 percent share of the equity shares of UNICON who in turn holds 99.99 percent of the

shares of capital FIRTH since October 10, 2011. The main activity FIRTH is the development and

commercialization of concrete, and to a lesser extent related products such as pre-stressed

beams, bagged products and aggregates.

Notes to the consolidated financial statements (continued)

3

- Prefabricados Andinos Perú S.A.C. – PREANSA Perú

It is an entity constituted in October 2007, Company´s direct subsidiary, who holds 50.02 and

50.00 percent share of the capital stock as of December 31, 2014 and 2013, respectively. The

main activity is the manufacture PREANSA Perú prestressed concrete and precast concrete

structures, as well as marketing, both in Peru and abroad.

In May 2013, PREANSA Perú constituted Prefabricados Andinos Colombia S.A.S. (Preansa

Colombia), an indirect subsidiary of the Company, with a share of the capital stock of 100

percent. Preansa Colombia is in pre-operational stage and its main activity is the manufacture of

prestressed and precast concrete structures as well as commercial activities in Colombia. In

2015 the construction of the plant will start in 2016 and begin operations.

- Prefabricados Andinos S.A. – PREANSA Chile

It is an entity constituted in November 1996, Company´s direct subsidiary since January 2014,

which owns 51 percent share of the capital stock. PREANSA Chile´s main activity is the

manufacture prestressed and precast concrete structures as well as marketing in Chile, see

details in note 2(a).

- Transportes Lurín S.A. – LURIN

It is an entity constituted in June 1990, Company´s direct subsidiary, which holds 99.99 percent

share of the capital stock. LURIN main activity is investment in securities, mainly in Skanon

Investment Inc. (a company incorporated in the United States of America).

- Generación Eléctrica de Atocongo S.A. - GEA

It is an entity constituted in May 1993, Company´s direct subsidiary, which holds directly and

indirectly 100 percent ownership of the shares of capital. GEA's main activity is the generation

and sale of electricity to the Company. As of February 15, 2013, the Ministry of Energy and

Mines granted the authorization to UNACEM to perform activities of power generation directly,

consequently, from that date; the Company signed a contract with GEA to take charge Operation

of the power plant.

- Depósito Aduanero Conchán S.A. - DAC

It is an entity constituted in July 1990, Company´s direct subsidiary, who owns 99.50 percent

share of the capital stock. DAC's main activity is the provision of warehousing services, goods

and merchandise Authorized owned and third customs warehouse and promotion services,

transportation, storage, management and delivery of cement manufactured by the Company.

Notes to the consolidated financial statements (continued)

4

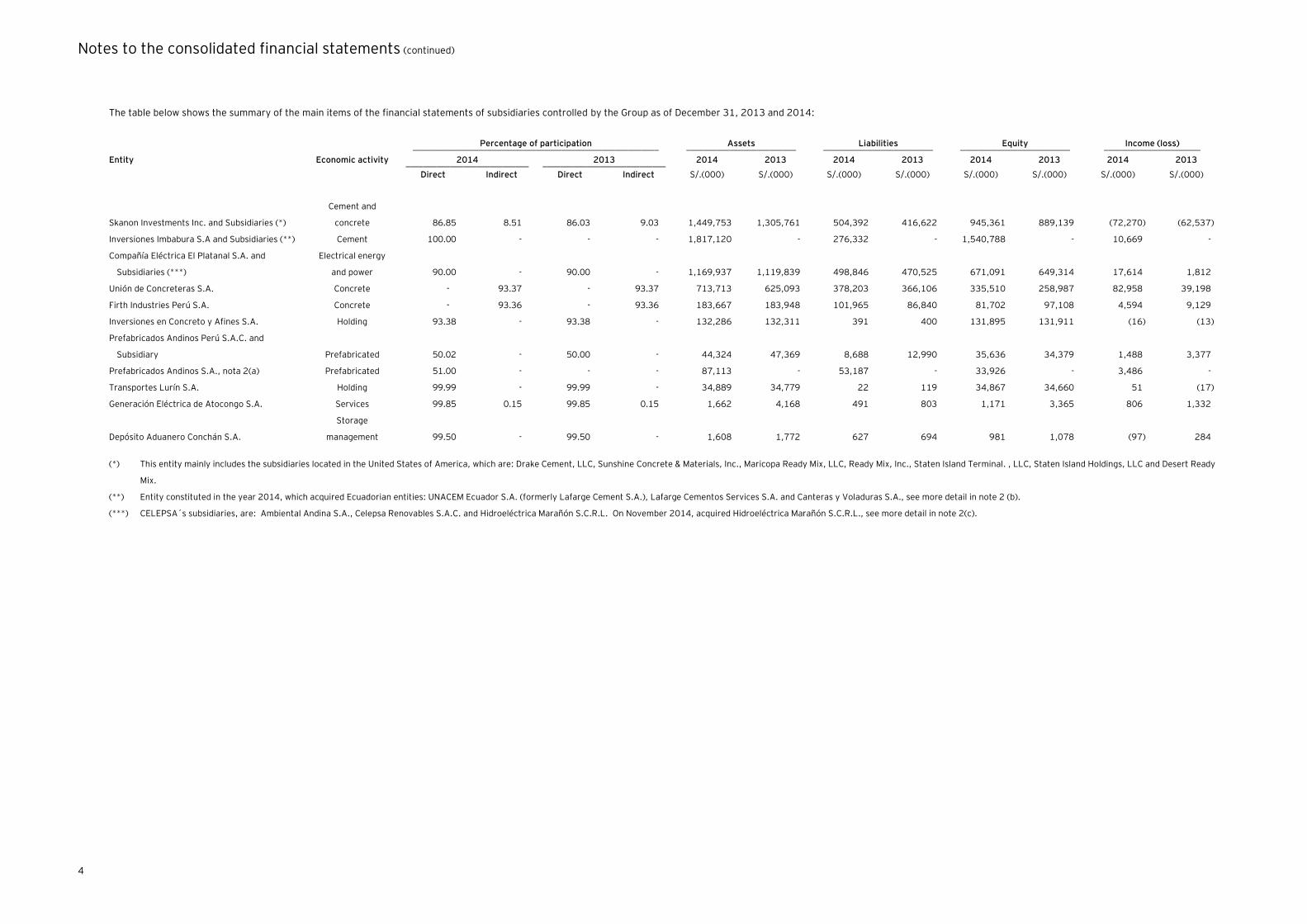

The table below shows the summary of the main items of the financial statements of subsidiaries controlled by the Group as of December 31, 2013 and 2014:

Percentage of participation Assets Liabilities Equity Income (loss) ________________________________________________________ _________________________ _________________________ _________________________ ______________________

Entity Economic activity 2014 2013 2014 2013 2014 2013 2014 2013 2014 2013 ____________________________ ____________________________

Direct Indirect Direct Indirect S/.(000) S/.(000) S/.(000) S/.(000) S/.(000) S/.(000) S/.(000) S/.(000)

Skanon Investments Inc. and Subsidiaries (*)

Cement and

concrete 86.85 8.51 86.03 9.03 1,449,753 1,305,761 504,392 416,622 945,361 889,139 (72,270) (62,537)

Inversiones Imbabura S.A and Subsidiaries (**) Cement 100.00 - - - 1,817,120 - 276,332 - 1,540,788 - 10,669 -

Compañía Eléctrica El Platanal S.A. and

Subsidiaries (***)

Electrical energy

and power 90.00 - 90.00 - 1,169,937 1,119,839 498,846 470,525 671,091 649,314 17,614 1,812

Unión de Concreteras S.A. Concrete - 93.37 - 93.37 713,713 625,093 378,203 366,106 335,510 258,987 82,958 39,198

Firth Industries Perú S.A. Concrete - 93.36 - 93.36 183,667 183,948 101,965 86,840 81,702 97,108 4,594 9,129

Inversiones en Concreto y Afines S.A. Holding 93.38 - 93.38 - 132,286 132,311 391 400 131,895 131,911 (16) (13)

Prefabricados Andinos Perú S.A.C. and

Subsidiary

Prefabricated 50.02 - 50.00 - 44,324 47,369 8,688 12,990 35,636 34,379 1,488 3,377

Prefabricados Andinos S.A., nota 2(a) Prefabricated 51.00 - - - 87,113 - 53,187 - 33,926 - 3,486 -

Transportes Lurín S.A. Holding 99.99 - 99.99 - 34,889 34,779 22 119 34,867 34,660 51 (17)

Generación Eléctrica de Atocongo S.A. Services 99.85 0.15 99.85 0.15 1,662 4,168 491 803 1,171 3,365 806 1,332

Depósito Aduanero Conchán S.A.

Storage

management 99.50 - 99.50 - 1,608 1,772 627 694 981 1,078 (97) 284

(*) This entity mainly includes the subsidiaries located in the United States of America, which are: Drake Cement, LLC, Sunshine Concrete & Materials, Inc., Maricopa Ready Mix, LLC, Ready Mix, Inc., Staten Island Terminal. , LLC, Staten Island Holdings, LLC and Desert Ready

Mix.

(**) Entity constituted in the year 2014, which acquired Ecuadorian entities: UNACEM Ecuador S.A. (formerly Lafarge Cement S.A.), Lafarge Cementos Services S.A. and Canteras y Voladuras S.A., see more detail in note 2 (b).

(***) CELEPSA´s subsidiaries, are: Ambiental Andina S.A., Celepsa Renovables S.A.C. and Hidroeléctrica Marañón S.C.R.L. On November 2014, acquired Hidroeléctrica Marañón S.C.R.L., see more detail in note 2(c).

Notes to the consolidated financial statements (continued)

5

2. Business combinations and acquisition of non-controlling interests

(a) Acquisition of Prefabricados Andinos S.A. –

On January 2014, the Group acquired 51 percent of the voting shares of Prefabricados Andinos

S.A. (hereinafter “Preansa Chile”) an unlisted company, dedicated in manufacturing, sales and

rentals of all kinds of construction products especially precast concrete structures.

The Group acquired Preansa Chile because it significantly helps to form a group of companies in

South American (Peru, Colombia and Chile), that generates synergies, optimizations of expenses

and can share engineering experience between countries.

The fair value of the identifiable assets and liabilities of Preansa Chile as of the date of acquisition

were:

Fair value

recognized on

acquisition

S/.(000)

Assets

Cash and cash equivalents 924

Trade and other receivables, net 26,301

Inventories 18,191

Property, plant and equipment, net 36,871

Intangible assets, net 218

Other assets 2,627 _________

85,132 _________

Liability

Trade and other payables (8,900)

Other financial liabilities (30,257)

Other liabilities (13,007) _________

(52,164) _________

Total identifiable net assets at fair value 32,968

Non-controlling interest measured at fair value (16,154)

Goodwill arising on acquisition, note 12(c) 3,207 _________

Purchase consideration transferred 20,021 _________

Net cash acquired with the subsidiary 924

Cash paid (20,021) _________

Net cash flow on acquisition (19,097) _________

Notes to the consolidated financial statements (continued)

6

The Group elected to measure the non-controlling interest in the acquiree at the proportionate

share of its interest in the acquiree’s identifiable net assets.

At the date of the acquisition, the fair value of the trade receivables was S/.26,301,000. The

gross amount of trade receivables is S/.27,007,000. The difference between the fair value and

the gross amount is the result of discounting over the expected timing of the cash collection and

an adjustment for counterparty credit risk. As of December 31, 2014, none of the trade

receivables have been impaired.

As of December 31, 2014, the valuation was completed and was determined the final fair value

of the identifiable net assets of Preansa Chile.

Since the acquisition date, has contributed Preansa Chile S/.61,630,000 and S/.3,486,000 for

income and income before income taxes, respectively, for continuing operations.

The goodwill recognized is mainly attributed to the expected synergies and other benefits from

combining the assets and activities of Preansa Chile with the Group.

The transaction costs of buying Preansa Chile for approximately S/.109,000 are included in

administrative expenses in the consolidated statement of income and are part of operating cash

flows in the consolidated statement of cash flows.

(b) Acquisition of UNACEM Ecuador S.A. (formerly Lafarge Cementos S.A.) and Subsidiaries -

On July 16, 2014, the Company constituted Inversiones Imbabura S.A. with the purpose of which

is the vehicle to purchase shares of UNACEM Ecuador S.A. (formerly Lafarge Cement S.A.)

On November 25, 2014, IMBABURA acquired 98.57 percent of total shares representing of

Lafarge´s capital and took control of the operations thereof, whose economic activity is the

production and sale of cement in Ecuador with a capacity of production of 1.4 million tonnes of

cement per year. At the date of acquisition, UNACEM Ecuador are:

(i) Lafarge Cementos Services S.A., dedicated to the activity of advice in accounting,

advertising, audit and legal; and

(ii) Canteras y Voladuras S.A. which is dedicated to conducting mining activities, operation

and sales of all kinds of mineral, smelting, refining and alloys of non-ferrous metals such

as copper, lead, chromium, magnesium, zinc, aluminum, nickel, and tin.

The Group acquired UNACEM Ecuador and Subsidiaries, as part of the strategy of consolidation

and diversification of our cement and prefabricated in the region. It also seeks to generate

synergies, cost optimization and engineering experience sharing among countries.

Notes to the consolidated financial statements (continued)

7

The fair value of the assets and liabilities of UNACEM Ecuador and Subsidiaries as of the date of

acquisition were:

Fair value

recognized on

acquisition

S/.(000)

Assets

Cash and cash equivalents 41,328

Trade and other receivables, net 29,199

Inventories, net 70,053

Property, plant and equipment 529,875

Intangible assets, net 129,373

Deferred income tax asset 101

Other assets 88 _________

800,017 _________

Liabilities

Other financial liabilities (147,347)

Trade and other payables (91,685)

Deferred income tax liability (57,335)

Provisions (10,591) _________

(306,958) _________

Total identifiable net assets at fair value 493,059

Non-controlling interest measured at fair value (7,074)

Goodwill arising on acquisition, note 12(c) 1,029,058 _________

Purchase consideration transferred 1,515,043 ________

Net cash acquired with the subsidiary 41,328

Cash paid (1,515,043) _________

Net cash flow on acquisition (1,473,715) ________

As of December 31, 2014, the Group´s Management has made its best estimate regarding this

transaction; however, according to IFRS 3, the Group´s Management has a period of one year

from the date of purchase to establish the final asset and liability fair values of UNACEM Ecuador.

In the opinion Group´s Management, significant changes in its initial assessment should not exist.

The Group decided to measure the non-controlling interest at its proportionate interest in the

identifiable net assets acquired.

Notes to the consolidated financial statements (continued)

8

Since the date of acquisition, UNACEM Ecuador and Subsidiaries have contributed

S/.52,041,000 and S/.10,756,000 of income and income before income taxes, respectively,

from continuing operations. If the combination had taken place at the beginning of the year,

income from continuing operations would have been S/.558,311,000 and income before tax

from continuing operations would have been S/.167,583,000.

The goodwill is mainly attributable to the expected synergies and other benefits from combining

the assets and activities UNACEM Ecuador and Subsidiaries with the Group.

Acquisition of an additional interest in UNACEM Ecuador and Subsidiaries –

In December 2014, the Group acquired an additional 0.32 percent of the shares with right to

vote of UNACEM Ecuador and increasing its ownership interest to 98.89 percent. Non-controlling

shareholders received a cash payment of US$1,916,000 (equivalent to S/.5,673,000). The

carrying amount of the net assets of UNACEM Ecuador (excluding the gain arising on the original

acquisition) at that date was S/.514,072,000. Then the additional interest acquired is as follows:

S/.(000)

Cash consideration paid to non-controlling shareholders 5,673

Carrying value of the additional interest (1,645) _________

Difference recognized in retained earnings 4,028 ________

(c) Acquisition of Hidroeléctrica Marañón S.C.R.L. –

On November 2014, CELEPSA and its subsidiary Celepsa Renovables S.A.C. acquired 100

percent of the shares of Hidroeléctrica Marañón S.C.R.L. with the purpose of implement the

future project Hydroelectric Central´s Marañon, with waters of the Marañon River to 2,900

m.s.n.m., near the town of Nuevas Flores, Huamalíes province, Huanuco city, Peru.

The project, with a final generation concession to 88 MW, has been recast in 20 MW to increase

factor of firm ground, while reducing construction (geological), environmental and social risks.

The work is already underway and is expected to be operating the plant on December 2016.

Notes to the consolidated financial statements (continued)

9

The fair value of the assets and liabilities of Hidroeléctrica Marañón as of the date of acquisition

were:

Fair value

recognized on

acquisition S/.(000)

Assets

Cash and cash equivalents 4,638

Trade and other receivables, net 2,968

Mining concessions and property, plant and equipment, net 34,712

Intangible assets, net 933

Deferred income tax asset 1,871 _________

45,122 _________

Liabilities

Trade and other payables (30,621) _________

Total identifiable net assets at fair value 14,501 _________

Goodwill arising on acquisition - _________

Purchase consideration transferred 14,501 _________

Net cash acquired with the subsidiary 4,638

Cash paid (14,501) _________

Net cash flow on acquisition (9,863) _________

3. Summary of significant accounting policies

3.1 Basis of preparation -

The consolidated financial statements have been prepared in accordance to International

Financial Reporting Standards (hereinafter “IFRS”) issued for the International Accounting

Standards Board (hereinafter “IASB “) prevailing as of December 31, 2014.

The financial consolidated statements have been prepared on a historical cost basis, except for

derivative financial instruments that have been measured at fair value, from the accounting

records of each of the subsidiaries in the Group. The consolidated financial statements are

presented in Nuevos Soles and all values are rounded to the nearest thousand (S/.000), except

when otherwise indicated.

The accounting policies adopted are consistent with those applied in previous years, the only

exception being t that the Group has adopted the new IFRS and revised IAS that are mandatory

for periods beginning on or after January 1, 2014, as described below; however, due to the

structure of the Company and nature of its operations, the adoption of these standards did not,

have a significant effect on its financial position and results, therefore, it has not been necessary

to modify the comparative consolidated financial statements of the Group.

Notes to the consolidated financial statements (continued)

10

- Investment entities. Amendments to IFRS 10, IFRS 12 and IAS 27

These amendments provide an exception to the consolidation requirement for entities that

meet the definition of an “investment entity” under IFRS 10 Consolidated Financial

Statements and must be applied retrospectively, subject to certain transition relief. The

exception to consolidation requires investment entities to account for subsidiaries at fair

value through profit or loss. These amendments have no impact on the Company, since

none of the entities in the Group qualifies to be an investment entity under IFRS 10.

- Offsetting financial assets and financial liabilities. Amendments to IAS 32

These amendments clarify the meaning of “currently has a legally enforceable right to set-

off” and the criteria for non-simultaneous settlement mechanisms of clearing houses to

qualify for offsetting and is applied retrospectively. These amendments have no impact on

the Group, since none of the entities in the Company has any offsetting arrangements.

- Novation of derivatives and continuation of hedge accounting. Amendments to IAS 39

These amendments provide relief from discontinuing hedge accounting when novation of

a derivative designated as a hedging instrument meets certain criteria and retrospective

application is required. These amendments have no impact on the Group since it has not

novated its derivatives during the current or prior periods.

- IFRIC 21 Levies

IFRIC 21 clarifies that an entity recognizes a liability for a levy when the activity that

triggers payment, as identified by the relevant legislation, occurs. For a levy that is

triggered upon reaching a minimum threshold, the interpretation clarifies that no liability

should be anticipated before the specified minimum threshold is reached. Retrospective

application is required for IFRIC 21. This interpretation has no impact on the Group as it

has applied the recognition principles under IAS 37 Provisions, Contingent Liabilities and

Contingent Assets consistent with the requirements of IFRIC 21 in prior years.

- Annual Improvements 2010-2012 Cycle

In the 2010-2012 annual improvements cycle, the IASB issued seven amendments to six

standards, which included an amendment to IFRS 13 Fair Value Measurement. The

amendment to IFRS 13 is effective immediately and, thus, for periods beginning on

January 1st, 2014, and it clarifies in the Basis for Conclusions that short-term receivables

and payables with no stated interest rates can be measured at invoice amounts when the

effect of discounting is immaterial. This amendment to IFRS 13 has no impact on the

Group.

- Annual Improvements 2011-2013 Cycle

In the 2011-2013 annual improvements cycle, the IASB issued four amendments to four

standards, which included an amendment to IFRS 1 First-time Adoption of International

Financial Reporting Standards. The amendment to IFRS 1 is effective immediately and,

thus, for periods beginning a on January 1st, 2014, and clarifies in the Basis for

Conclusions that an entity may choose to apply either a current standard or a new

standard that is not yet mandatory, but permits early application, provided either

Notes to the consolidated financial statements (continued)

11

standard is applied consistently throughout the periods presented in the entity’s first IFRS

financial statements. This amendment to IFRS 1 has no impact on the Group, since it

already prepares its financial statements consistent with IFRS and is not a first-time

adopter of IFRS.

3.2 Basis of consolidation -

The consolidated financial statements comprise the financial statements of the Group and its

subsidiaries as of December 31, 2014. Control is achieved when the Group is exposed, or has

rights, to variable returns from its involvement with the investee and has the ability to affect

those returns through its power over the investee.

Specifically, the Group controls an investee if, and only if, the Group has:

- Power over the investee (i.e., existing rights that give it the current ability to direct the

relevant activities of the investee).

- Exposure, or rights, to variable returns from its involvement with the investee.

- The ability to use its power over the investee to affect its returns.

When the Group has less than a majority of the voting or similar rights of an investee, the Group

considers all relevant facts and circumstances in assessing whether it has power over an

investee, including:

- The contractual arrangement with the other vote holders of the investee.

- Rights arising from other contractual arrangements.

- The Group’s voting rights and potential voting rights.

The Group re-assesses whether or not it controls an investee if facts and circumstances indicate

that there are changes to one or more of the three elements of control. Consolidation of a

subsidiary begins when the Group obtains control over the subsidiary and ceases when the Group

loses control of the subsidiary. Assets, liabilities, income and expenses of a subsidiary acquired

or disposed of during the year are included in the consolidated financial statements from the date

the Group gains control until the date the Group ceases to control the subsidiary.

Profit or loss and each component of other comprehensive income (OCI) are attributed to the

equity holders of the parent of the Group and to the non-controlling interests, even if this results

in the non-controlling interests having a deficit balance. When necessary, adjustments are made

to the financial statements of subsidiaries to bring their accounting policies into line with the

Group’s accounting policies. All intra-group assets and liabilities, equity, income, expenses and

cash flows relating to transactions between members of the Group are eliminated in full on

consolidation.

A change in the ownership interest of a subsidiary, without a loss of control, is accounted for as

an equity transaction.

Notes to the consolidated financial statements (continued)

12

If the Group loses control over a subsidiary, it derecognizes the related assets (including

goodwill), liabilities, non-controlling interest and other components of equity while any resultant

gain or loss is recognized in profit or loss. Any investment retained is recognized at fair value.

3.3 Summary of significant accounting policies -

The following are the significant accounting policies applied by the Group’s Management in

preparing its consolidated financial statements:

(a) Business combinations and goodwill -

Business combinations

Business combinations are accounted for using the acquisition method. The cost of an

acquisition is measured as the aggregate of the consideration transferred measured at

acquisition date fair value and the amount of any non-controlling interests in the acquiree.

For each business combination, the Group elects whether to measure the non-controlling

interests in the acquiree at fair value or at the proportionate share of the acquiree’s

identifiable net assets. Acquisition-related costs are expensed as incurred and included in

the caption “Administrative expenses” in the consolidated statement of income.

When the Group acquires a business, it assesses the financial assets and liabilities

assumed for appropriate classification and designation in accordance with the contractual

terms, economic circumstances and pertinent conditions as at the acquisition date.

If the business combination is achieved in stages, any previously held equity interest is re-

measured at its acquisition date fair value and any resulting gain or loss is recognized in

profit or loss.

Any contingent consideration to be transferred by the acquirer will be recognized at fair

value at the acquisition date. Contingent consideration classified as an asset or liability

that is a financial instrument and within the scope of IAS 39 “Financial Instruments:

Recognition and Measurement”, is measured at fair value with changes in fair value

recognized either in either profit or loss or as a change to OCI. Contingent consideration

that is classified as equity is not re-measured and subsequent settlement is accounted for

within equity.

Goodwill

Goodwill is initially measured at cost, being the excess of the aggregate of the

consideration transferred and the amount recognized for non-controlling interests, and

any previous interest held, over the net identifiable assets acquired and liabilities

assumed. If the fair value of the net assets acquired is in excess of the aggregate

consideration transferred, the Group re-assesses whether it has correctly identified all of

the assets acquired and all of the liabilities assumed and reviews the procedures used to

measure the amounts to be recognized at the acquisition date.

If the re-assessment still results in an excess of the fair value of net assets acquired over

the aggregate consideration transferred, then the gain is recognized in profit or loss.

Notes to the consolidated financial statements (continued)

13

After initial recognition, goodwill is measured at cost less any accumulated impairment

losses. For the purpose of impairment testing, goodwill acquired in a business combination

is, from the acquisition date, allocated to each of the Group’s cash-generating units that

are expected to benefit from the combination, irrespective of whether other assets or

liabilities of the acquire are assigned to those units.

Where goodwill has been allocated to a cash-generating unit and part of the operation

within that unit is disposed of, the goodwill associated with the disposed operation is

included in the carrying amount of the operation when determining the gain or loss on

disposal. Goodwill disposed in these circumstances is measured based on the relative

values of the disposed operation and the portion of the cash-generating unit retained.

(b) Cash and cash equivalents -

Cash and cash equivalents in the consolidated statement of financial position comprise

petty cash, funds to deposit, demand deposits and time deposits with a maturity of three

month or less. For the purpose of the consolidated statement of cash flows, cash and cash

equivalents consist of cash and short–term deposits as defined above.

(c) Financial instruments: initial recognition and subsequent measurement -

(i) Financial assets -

Initial recognition and measurement –

Financial assets within the scope of the International Accounting Standard (IAS) 39

"Financial Instruments: Recognition and Measurement", at the moment of initial

recognition, as financial assets at fair value through profit or loss, loans and

receivables, held-to-maturity investments, available-for-sale financial investments,

or as derivatives designated as hedging instruments in an effective hedge, as

appropriate.

All financial assets are recognized initially at fair value plus, in the case of assets

not at fair value with changes through profit or loss, the transaction costs are

attributable to the acquisition of the financial asset.

Purchases or sales of financial assets that require delivery of assets within a time

frame established by regulation or convention in the market place are recognized

on the date that the Group commits to purchase or sell such assets.

The Group financial assets include cash and cash equivalents, trade and other

receivables and derivative financial instruments.

Notes to the consolidated financial statements (continued)

14

Subsequent measurement -

For purposes of subsequent measurement, financial assets are classified in four

categories:

- Financial assets at fair value through profit or loss;

- Loans and receivables;

- Held-to-maturity investments; and

- Available-for-sale financial investments

Financial assets at fair value through profit or loss -

Financial assets at fair value through profit or loss includes financial assets held for

trading and financial assets designated upon initial recognition as at fair value

through profit or loss. Financial assets are classified as held for trading if they are

acquired for the purpose of selling or repurchasing in the near term.

This category includes derivative financial instruments entered into by the

Company that are not designated as hedging instruments in hedge relationships as

defined by IAS 39.

Loans and receivables -

Loans and receivables are non-derivative financial assets with fixed or

determinable payments that are not quoted in an active market. After initial

measurement, such financial assets are subsequently measured at amortized cost

using the effective interest rate method (EIR), less impairment provisions. The

amortized cost is calculated by taking into account any discount or premium on

acquisition and fees or costs that are an integral part of the EIR. The amortization

of EIR is included in the finance income in the income statement. The losses arising

from impairment are recognized as finance cost in the consolidated statements of

income.

Held-to-maturity investments -

Non-derivative financial assets with fixed or determinable payments and fixed

maturities are classified as held-to-maturity investments when the Group has the

positive intention and ability to hold them to maturity.

The Group did not have any held-to-maturity investments as of December 31, 2014

and 2013.

Available-for-sale financial assets -

Are those designated as such, as they are kept indefinitely and may be sold due to

liquidity needs or changes in interest rates, exchange rates or equity prices; or not

qualified to be classified as at fair value through the income statement or held to

maturity.

Notes to the consolidated financial statements (continued)

15

After initial recognition, available-for-sale financial investments are measured at

fair value. The unrealized gains or losses are recognized directly in the equity,

under caption “unrealized gains or losses”, net of deferred income tax. When the

financial investment is sold, the cumulative gain or loss previously recognized

under net equity is now recognized in the income statement under caption “Finance

costs” or “Finance income”, accordingly.

Dividends earned throughout the investment timeframe are recognized in the

consolidated income statement when the right to collect is established.

The Group has not classified any financial asset as an available-for-sale financial

assets as of December 31, 2014 and 2013.

Derecognition -

A financial asset (or, where applicable, a part of a financial asset or part of a group

of similar financial assets) is derecognized when:

- The rights to receive cash flow from such asset have expired;

- The Group has transferred its rights to receive cash flows from the asset or

has assumed an obligation to pay the received cash flows in full without

material delay to a third party under a “pass through” agreement; and

either (a) the Group has transferred substantially all the risks and rewards of

the asset, or (b) the Group has neither transferred nor retained substantially

all the risks and rewards of the asset, but has transferred control of the

asset.

When the Group has transferred its contractual rights to receive cash flows from an

asset or has entered into a pass-through arrangement, and has neither transferred

nor retained substantially all of the risks and rewards of the asset nor transferred

control of it, the asset is recognized to the extent of the Company’s continuing

involvement in it. In that case, the Group also recognizes an associated liability.

The transferred asset and the associated liability are measured on a basis that

reflects the rights and obligations that the Group has retained.

(ii) Impairment of financial assets -

The Group assess at each reporting date whether there is any objective evidence

that a financial asset or a group of financial assets is impaired. A financial asset or

a group of financial assets is deemed to be impaired if, and only if, there is

objective evidence of impairment as a result of one or more events that has

occurred after the initial recognition of the asset (an incurred “loss event”) and

that loss event has an impact on the estimated future cash flows of the financial

asset or the group of financial assets that can be reliably estimated. Evidence of

impairment may include indications that the debtors or a group of debtors is

experiencing significant financial difficulty, default or delinquency in interest or

principal payments, the probability that they will enter bankruptcy or other

Notes to the consolidated financial statements (continued)

16

financial reorganization and where observable data indicate that there is a

measurable decrease in the estimated future cash flows, such as changes in arrears

or economic conditions that correlate with defaults.

Financial assets carried at amortized cost -

For financial assets carried at amortized cost, the Group first assesses whether

objective evidence of impairment exists individually for financial assets that are

individually significant, or collectively for financial assets that are not individually

significant. If the Group determines that no objective evidence of impairment for an

individually assessed financial asset, whether significant or not, it includes the

asset in a group of financial assets with similar credit risk characteristics and

collectively assesses them for impairment. Assets that are individually assessed for

impairment and for which an impairment loss is, or continues to be, recognized are

not included in a collective assessment of impairment.

If there is objective evidence that an impairment loss has been incurred, the

amount of the loss is measured as the difference between the assets carrying

amount and the present value of estimated future cash flows (excluding future

expected credit losses that have not yet been incurred). The present value of the

estimated future cash flows is discounted at the financial asset’s original effective

interest rate. If a loan has a variable interest rate, the discount rate for measuring

any impairment loss is the current effective interest rate.

The carrying amount of the asset is reduced through the use of an allowance

account and the amount of the loss is recognized in the consolidated income

statement. Interest income continues to be accrued on the reduced carrying

amount and is accrued using the interest rate used to discount the future cash

flows for the purpose of measuring the impairment loss.

The interest income is recorded as part of finance income in the consolidated

statement of income. Loans together with the associated allowance are written off

when there is no realistic prospect of future recovery and all collateral has been

realized or has been transferred to the Group. If, in a subsequent year, the amount

of the estimated impairment loss increases or decreases because of an event

occurring after the impairment was recognized, the previously recognized

impairment loss is increased or reduced by adjusting the allowance account. If the

estimated loss decreases, the reversal shall not result in a carrying amount of the

financial asset that exceeds what the amortized cost would have been had the

impairment not been recognized at the date the impairment is reversed. If a future

write-off is later recovered, the recovery is credited to finance costs in the

consolidated statement of income.

Notes to the consolidated financial statements (continued)

17

(iii) Financial liabilities -

Initial recognition and measurement -

Financial liabilities within the scope of IAS 39 are classified as financial liabilities at

fair value through profit or loss, loans and borrowings, or as derivatives designated

as hedging instruments in an effective hedge, as appropriate. The Group

determines the classification of its financial liabilities at initial recognition.

All financial liabilities are recognized initially at fair value and, in the case of loans

and borrowings, carried at amortized cost. This includes directly attributable

transaction costs.

As of December 31, 2014 and 2013, the Group’s financial liabilities include other

financial liabilities, trade and other payables and derivative financial instruments.

Subsequent measurement -

The subsequent measurement of financial liabilities depends on their classification

as follows:

Financial liabilities at fair value through profit or loss -

Financial liabilities at fair value through profit or loss include financial liabilities held

for trading and financial liabilities designated upon initial recognition as at fair

value through profit or loss.

Financial liabilities are classified as held for trading if they are acquired for the

purpose of selling in the near term. This category includes financial derivative

instruments which are not designated as hedge instruments as required by IAS 39.

The embedded derivatives are also classified as negotiable, unless they are

designated as effective hedge instruments. Gains or losses on liabilities held for

trading are recognized in the consolidated statement of income.

Loans and borrowings -

After their initial recognition, interest-bearing loans and borrowings are

subsequently measured at amortized cost using the effective interest rate method.

Gains and loss are recognized in the statement of income when the liabilities are

derecognized as well as through the effective interest rate method (EIR)

amortization process. Amortized cost is calculated by taking into account any

discount or premium on acquisition and fees or costs that are an integral part of

the EIR. The EIR amortization is included in the finance costs in the statement of

income.

Derecognition -

A financial liability is derecognized when the obligation under the liability is

discharged or cancelled or expired. When an existing financial liability is replaced

by another one from the same lender on substantially different terms, or the terms

are substantially modified, such replacement or amendment is treated as a

derecognition of the original liability and the recognition of a new liability, and the

Notes to the consolidated financial statements (continued)

18

difference in the respective carrying amount is recognized in the consolidated

statement of income.

(iv) Offsetting of financial instruments -

Financial assets and financial liabilities are offset and the net amount reported in

the consolidated statement of financial position if, and only if, there is a currently

enforceable legal right to offset the recognized amounts and there is an intention

to settle on a net basis, or to realize the assets and settle the liabilities

simultaneously.

(v) Fair value of financial instruments -

The Group measures financial instruments, such as, derivatives at fair value at

each consolidated statement of financial position date.

Fair value is the price that would be received to sell an asset or paid to transfer a

liability in an orderly transaction between market participants at the measurement

date. The fair value measurement is based on the presumption that the transaction

to sell the asset or transfer the liability takes place either:

- In the principal market for the asset or liability, or

- In the absence of a principal market, in the most advantageous market for

the asset or liability.

The principal or the most advantageous market must be accessible by the Group.

The fair value of an asset or a liability is measured using the assumptions that

market participants would use when pricing the asset or liability, assuming that

market participants act in their economic best interest.

A fair value measurement of a non-financial asset takes into account a market

participant's ability to generate economic benefits by using the asset in its highest

and best use or by selling it to another market participant that would use the asset

in its highest and best use.

The Group uses valuation techniques that are appropriate in the circumstances and

for which sufficient data are available to measure fair value, maximizing the use of

relevant observable inputs and minimizing the use of unobservable inputs.

All assets and liabilities for which fair value is measured or disclosed in the

consolidated financial statements are categorized within the fair value hierarchy,

described as follows, based on the lowest level input that is significant to the fair

value measurement as a whole:

- — Quoted (unadjusted) market prices in active markets for identical

assets or liabilities.

Notes to the consolidated financial statements (continued)

19

- — Valuation techniques for which the lowest level input that is

significant to the fair value measurement is directly or indirectly observable.

- vel 3 — Valuation techniques for which the lowest level input that is

significant to the fair value measurement is unobservable.

For assets and liabilities that are recognized in the consolidated financial

statements on a recurring basis, the Group determines whether transfers have

occurred between Levels in the hierarchy by re-assessing categorization (based on

the lowest level input that is significant to the fair value measurement as a whole)

at the end of each reporting period.

The Group’s Management determines the policies and procedures for both

recurring fair value measurement. At each reporting date, the Group’s

Management analyses the movements in the values of assets and liabilities which

are required to be re-measured or re-assessed as per the Group’s accounting

policies.

For the purpose of fair value disclosures, the Group has determined classes of

assets and liabilities on the basis of the nature, characteristics and risks of the

asset or liability and the level of the fair value hierarchy as explained above.

An analysis of fair values of financial instruments and further details as to how they

are measured are provided in Note 33.

Derivative financial instruments -

Initial recognition and subsequent measurement -

The Group uses derivative financial instruments, such as forward currency

contracts and interest rate swaps contracts, to hedge its foreign currency risks and

interest rate risks, respectively. Such derivative financial instruments are initially

recognized at fair value on the date on which a derivative contract is entered into

and are subsequently re-measured at fair value. Derivatives are carried as financial

assets when the fair value is positive and as financial liabilities when the fair value

is negative.

The purchase contracts that meet the definition of a derivative under IAS 39 are

recognized in the consolidated statement of income as costs. Commodity contracts

that are entered into and continue to be held for the purpose of the receipt or

delivery of a non-financial item in accordance with the Group’s expected purchase,

sale or usage requirements are held at cost.

Any gains or losses arising from changes in the fair value of derivatives are taken

directly to consolidated profit or loss, except for the effective portion of cash flow

hedges, which is recognized in consolidated of other comprehensive income and

later reclassified to profit or loss when the hedge item affects profit or loss.

Notes to the consolidated financial statements (continued)

20

For the purpose of hedge accounting, hedges are classified as:

- Fair value hedges when hedging the exposure to changes in the fair value of

a recognized asset or liability or an unrecognized firm commitment;

- Cash flow hedges when hedging the exposure to variability in cash flows that

is either attributable to a particular risk associated with a recognized asset

or liability or a highly probable forecast transaction or the foreign currency

risk in an unrecognized firm commitment; or

- Hedges of a net investment in a foreign operation.

At the inception of a hedge relationship, the Group formally designates and

documents the hedge relationship to which the Company wishes to apply hedge

accounting, the risk management objective and strategy for undertaking the hedge.

The documentation includes identification of the hedging instrument, the hedged

item or transaction, the nature of the risk being hedged and how the Group will

assess the effectiveness of changes in the hedging instrument’s fair value in

offsetting the exposure to changes in the hedged item’s fair value or cash flows

attributable to the hedged risk.

The Group expects that such hedges are to be highly effective in achieving

offsetting changes in fair value or cash flows. The Group assessed on an ongoing

basis to determine that they actually have been highly effective throughout the

financial reporting periods for which they were designated.

Hedges that meet the strict criteria for hedge accounting are accounted for, as

described below:

Fair value hedges -

The change in the fair value of a hedging derivative is recognized in the

consolidated statement of profit or loss as finance costs. The change in the fair

value of the hedged item attributable to the risk hedged is recorded as part of the

carrying value of the hedged item and is also recognized in the consolidated

statement of income as finance costs.

For fair value hedges relating to items carried at amortized cost, any adjustment to

carrying value is amortized through profit or loss over the remaining term of the

hedge using the EIR method. EIR amortization may begin as soon as an adjustment

exists and no later than when the hedged item ceases to be adjusted for changes in

its fair value attributable to the risk being hedged.

If the hedged item is derecognized, the unamortized fair value is recognized

immediately in consolidated profit or loss.

Notes to the consolidated financial statements (continued)

21

When an unrecognized firm commitment is designated as a hedged item, the

subsequent cumulative change in the fair value of the firm commitment

attributable to the hedged risk is recognized as an asset or liability with a

corresponding gain or loss recognized in consolidated profit and loss.

Cash flow hedges -

The effective portion of the gain or loss on the hedging instrument is recognized in

OCI in the cash flow hedge reserve, while any ineffective portion is recognized

immediately in the consolidated statement of profit or loss as finance costs.

The Group uses swaps contracts as hedges of its risk exposure to the exchange rate

and interest rate expected transactions. The ineffective portion relating to swaps

contracts of exchange and /or interest rate is recognized as finance costs.

Amounts recognized as OCI are transferred to profit or loss when the hedged

transaction affects profit or loss, such as when the hedged finance income or

financial expense is recognized or when a forecast sale occurs. When the hedged

item is the cost of a non-financial asset or non-financial liability, the amounts

recognized as OCI are transferred to the initial carrying amount of the non-financial

asset or liability.

If the hedging instrument expires or is sold, terminated or exercised without

replacement or rollover (as part of the hedging strategy), or if its designation as a

hedge is revoked, or when the hedge no longer meets the criteria for hedge

accounting, any cumulative gain or loss previously recognized in OCI remains

consolidated in equity until the forecast transaction occurs or the foreign currency

firm commitment is met.

Hedges of a net investment in a foreign operation -

Hedges of a net investment in a foreign operation, including a hedge of a monetary

item that is accounted for as part of the net investment, are accounted for in a way

similar to cash flow hedges.

As of December 31, 2014 and 2013, the Group has no hedging instruments of a

net investment in a foreign operation.

(d) Current versus non-current classification -

The Group presents assets and liabilities in consolidated statement of financial position

based on current/non-current classification. An asset is current when it is:

- It is expected to be realized or intended to be sold or consumed within a normal

operating cycle;

- It is held primarily for trading purposes;

- Expected to be realized within twelve months after the reporting period;

Notes to the consolidated financial statements (continued)

22

- It is cash or cash equivalent, unless it is restricted from being exchanged or used to

settle a liability for, at least, twelve months after the reporting period.

All other assets are classified as non-current. A liability is current when it is:

- Expected to be settled within a normal operating cycle;

- Held primarily for trading purposes;

A liability is current when:

- It is expected to be settled in normal operating cycle;

- It is held primarily for the purpose of trading

- It is due to be settled within twelve months after the reporting period

- There is no unconditional right to defer the settlement of the liability for at least

twelve months after the reporting period.

The Group classifies all other liabilities as non-current.

Deferred tax assets and liabilities are classified as non-current assets and liabilities.

(e) Foreign currency translation -

The Group’s consolidated financial statements are presented in Nuevos Soles, which is

also the parent company’s functional currency. For each entity the Group determines the

functional currency and items included in the financial statements of each entity are

measured using that functional currency.

The accompanying consolidated financial statements have been prepared to show the

joint activity of the companies comprising the Group; so it has been established as the

presentation currency used by the Company, the Nuevo Sol. Accordingly, the balances of

the financial statements of companies operating in countries with a functional currency

other than the Nuevo Sol have been converted in accordance with the methodologies set

out in IAS 21 "The Effects of Changes in exchange rates of foreign currency".

Balances and transactions in foreign currency -

Balances or transactions in foreign currency are made in a currency other than the

functional currency. Transactions in foreign currency are initially recorded in the

functional currency using the exchange rates prevailing at the dates of the transactions in

which initially qualify for recognition. Monetary assets and liabilities denominated in

foreign currencies are subsequently translated into the functional currency using the

exchange rates prevailing at the date of the consolidated statement of financial position.

The differences between the exchange rates prevailing at the dates of the consolidated

financial statements presented and the exchange rate initially used to record transactions

are recognized in the consolidated income statement in the period in which they occur, in

the "Exchange difference, net".

Notes to the consolidated financial statements (continued)

23

Non-monetary assets and liabilities acquired in foreign currency are converted at the

exchange rate at the dates of the initial transactions.

As required by IAS 21, exchange differences arising from transactions between related

parties eliminated on consolidation and are not included as part of the net investment in a

foreign operation, should be recorded in profit or loss in the consolidated financial

statements.

Group companies -

On consolidation, the assets and liabilities of foreign operations are translated into Nuevos

Soles at the rate of exchange prevailing at the reporting date and their income statements

are translated at exchange rates prevailing at the dates of the transactions. The exchange

differences arising on translation for consolidation are recognized in other comprehensive

income.

Any goodwill arising on the acquisition of a foreign operation and any fair value

adjustments to the carrying amounts of assets and liabilities arising on the acquisition are

treated as assets and liabilities of the foreign operation and translated at the spot rate of

exchange at the reporting date.

(f) Inventories -

Inventories are valued at the lower of cost and net realizable value. Costs incurred in

bringing each product to its present location and conditions are accounted for as follows:

- Raw materials and supplies, packages and packing –

Purchase cost, using the weighted average method.

- Finished goods and work in progress -

At the cost of direct materials and supplies, services provided by third parties, raw

material, direct labor cost, other direct cost, general manufacturing expenses and

an overhead based on fixed and variable cost based on normal operating capacity,

using the weighted average method, but excluding borrowing costs and exchange

currency differences.

- Inventory in transit purchase cost.

Net realizable value is the sales price obtained in the ordinary course of business, less the

estimated costs of placing the inventories into a ready-for-sale condition and the

commercialization and distribution expenses.

The Group´s management periodically evaluates the impairment and obsolescence of

these assets. The estimation for impairment and obsolescence, if any, is recognized with

charge to the profit and loss.

Notes to the consolidated financial statements (continued)

24

(g) Investments in associate -

The Group’s investment in BASF Construction Chemicals Perú S.A. and Preinco Ltda. with

a 30 and 50 percent as of December 31, 2014, respectively (as of December 31, 2013, a

30 percent of BASF Construction Chemicals Peru S.A.) and are accounted for using the

equity method. An associate is an entity over which the Group has significant influence.

The considerations made in determining significant influence or joint control is similar to

those necessary to determine control over subsidiaries.

Under the equity method, the investment in an associate or a joint venture is initially

recognized at cost. The carrying amount of the investment is adjusted to recognize

changes in the Group’s share of net assets of the associate or joint venture since the

acquisition date. Goodwill relating to the associate or joint venture is included in the

carrying amount of the investment and is neither amortized nor individually tested for

impairment.

The statement of profit or loss reflects the Group’s share of the results of operations of

the associate. Any change in OCI of those investees is presented as part of the Group’s

OCI. In addition, when there has been a change recognized directly in the equity of the

associate, the Group recognizes its share of any changes, when applicable, in the

statement of changes in equity. Unrealized gains and losses resulting from transactions

between the Group and the associate are eliminated to the extent of the interest in the

associate or joint venture.

The Group's share of results of the associate is presented in a single line on the

consolidated income statement, operating profit outside. This participation includes the

net of tax and non-controlling interests in subsidiaries of the associate.

The financial statements of the associate are prepared for the same reporting period as

the Group. When necessary, adjustments are made to bring the accounting policies in line

with those of the Group.

After application of the equity method, the Group determines whether it is necessary to

recognize an impairment loss on its investment in its associate or joint venture. At each

reporting date, the Group determines whether there is objective evidence that the

investment in the associate is impaired. If there is such evidence, the Group calculates the

amount of impairment as the difference between the recoverable amount of the associate

and its carrying value, and then recognizes the loss as ‘Share of profit of an associate and

a joint venture’ in the consolidated statement of income.

Upon loss of significant influence over the associate, the Group measures and recognizes

any retained investment at its fair value. Any difference between the carrying amount of