Understanding the

Red Flags Rule

Ryan Lane

Director, KPA Sales & Finance Compliance

Jim Radogna

Sales & Finance Compliance Consultant

Moderator

Rebecca Ward

Sr. Marketing Content Specialist

(303) 219-7802

Presenter

Ryan Lane

Director, KPA Sales & Finance Compliance

(303) 802-3095

Presenter

Jim Radogna

Sales & Finance Compliance Consultant

(303) 228-8770

Questions

If you have questions during

the presentation, please

submit them using the

“Questions” feature

Questions will be answered

at the end of the webinar

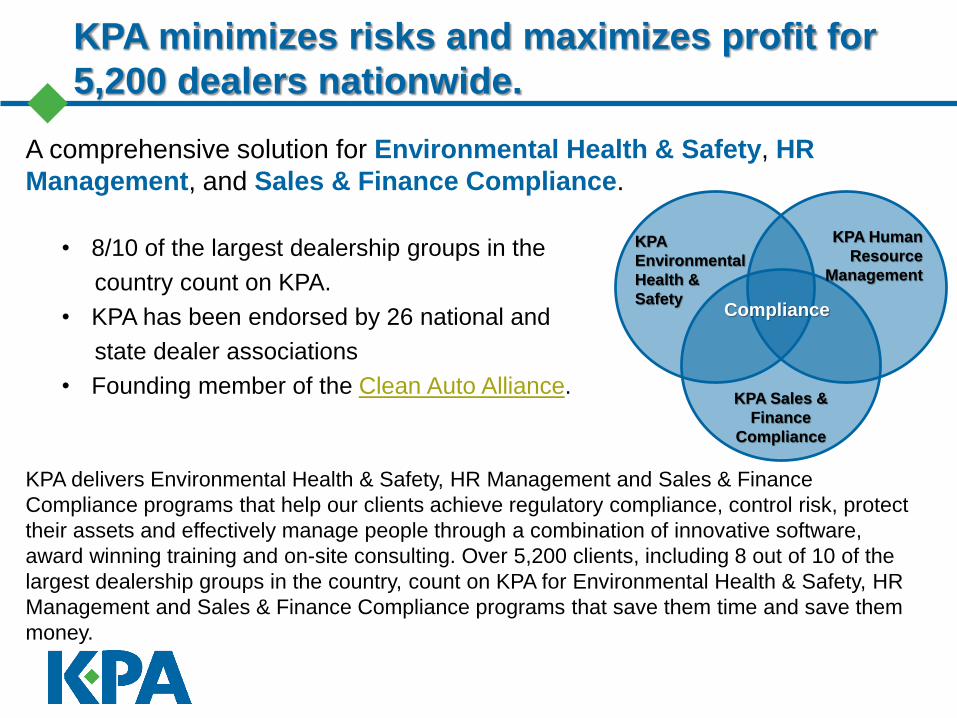

A comprehensive solution for Environmental Health & Safety, HR

Management, and Sales & Finance Compliance.

• 8/10 of the largest dealership groups in the

country count on KPA.

• KPA has been endorsed by 26 national and

state dealer associations

• Founding member of the Clean Auto Alliance.

KPA delivers Environmental Health & Safety, HR Management and Sales & Finance

Compliance programs that help our clients achieve regulatory compliance, control risk, protect

their assets and effectively manage people through a combination of innovative software,

award winning training and on-site consulting. Over 5,200 clients, including 8 out of 10 of the

largest dealership groups in the country, count on KPA for Environmental Health & Safety, HR

Management and Sales & Finance Compliance programs that save them time and save them

money.

KPA minimizes risks and maximizes profit for

5,200 dealers nationwide.

KPA

Environmental

Health &

Safety

KPA Human

Resource

Management

KPA Sales &

Finance

Compliance

Compliance

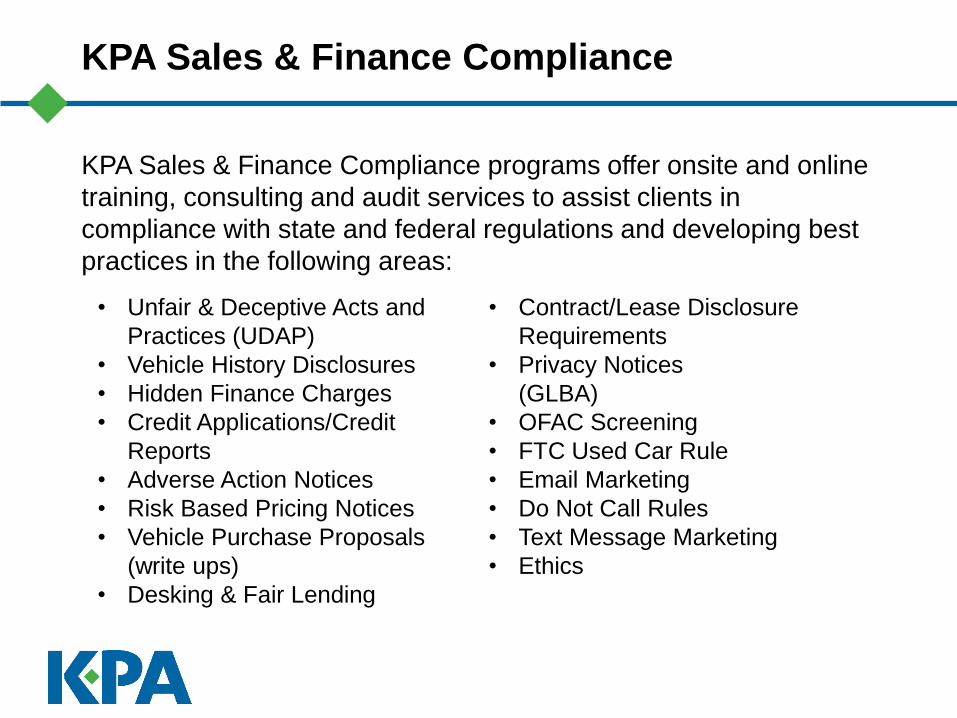

KPA Sales & Finance Compliance

KPA Sales & Finance Compliance programs offer onsite and online

training, consulting and audit services to assist clients in

compliance with state and federal regulations and developing best

practices in the following areas:

• Contract/Lease Disclosure

Requirements

• Privacy Notices

(GLBA)

• OFAC Screening

• FTC Used Car Rule

• Email Marketing

• Do Not Call Rules

• Text Message Marketing

• Ethics

• Unfair & Deceptive Acts and

Practices (UDAP)

• Vehicle History Disclosures

• Hidden Finance Charges

• Credit Applications/Credit

Reports

• Adverse Action Notices

• Risk Based Pricing Notices

• Vehicle Purchase Proposals

(write ups)

• Desking & Fair Lending

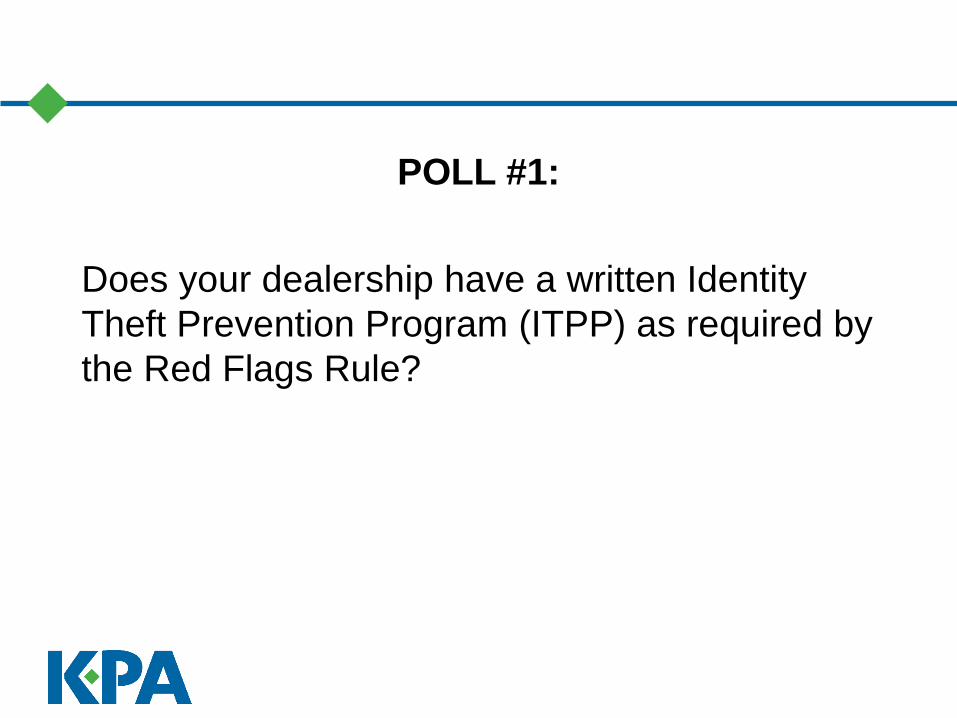

POLL #1:

Does your dealership have a written Identity

Theft Prevention Program (ITPP) as required by

the Red Flags Rule?

POLL #2:

Does your dealership have a Red Flags

Compliance Officer as required by the Red

Flags Rule?

POLL #3:

Have all sales department staff members who

interact with customers in your dealership

received Red Flags training?

What Is The Red Flags Rule?

• The RED FLAGS RULE was created by the

Federal Trade Commission. It requires dealers

to develop and implement an Identity Theft

Prevention Program (ITPP) that is designed to

detect, prevent and mitigate identity theft.

• IDENTITY THEFT means fraud committed or

attempted using the identifying information ofanother person without authority.

What Makes the Red Flags Rule Different?

Dealership personnel are required to be far more proactive than

with other regulations. Unfortunately this can slow down a

transaction.

Red Flags regulations require a dealership to not only be a good

citizen, but to be a cop as well.

Dealerships are required to have a Red Flags Compliance

Officer in-house.

All relevant dealership personnel must be trained on the Red

Flags Rue.

Risk Assessment

The Red Flags Rule requires dealers to, initially, and periodically thereafter,

determine whether they offer or maintain “covered accounts” as defined by the rule.

Accordingly, they must conduct a risk assessment of their accounts to determine

which of these accounts are “covered accounts” as defined above. In doing so, they

must take into consideration the following risk factors:

Types of accounts they maintain

Determination of the methods used to open accounts

The methods used to access accounts

Their previous experiences with identity theft

A Risk Assessment should take place individually for each account offered or

maintained on a department-by-department basis (e.g. new and used-car sales

departments, parts and service, etc.) and by customer type (e.g. consumers,

businesses, fleet businesses, vendors, employees, etc.)

Identifying Red Flags

First, the Program must identify relevant “Red Flags” for new and existing “covered accounts” and incorporate those Red Flags into the Program.

• RED FLAG means a pattern, practice or specific activity that indicates the possible existence of identity theft.

• COVERED ACCOUNT means an account that a creditor offers or maintains, primarily for personal, family, or household purposes that involves multiple payments or transactions, or any other account for which there is a reasonably foreseeable risk to customers of identity theft.

So… What Are Covered Accounts?

The following types of accounts are generally

considered to be “covered accounts” at dealerships:

• Vehicles purchased on credit for personal use

• Vehicles leased for personal use.

• Commercial credit sales where an individual co-signs

• Commercial leases where an individual co-signs

Identifying Red Flags At The Dealership

There are 6 typical categories of Red Flags at most dealerships:

1. ALERTS, NOTIFICATIONS AND WARNINGS FROM CREDIT REPORTING AGENCIES

OR SERVICE PROVIDERS, SUCH AS FRAUD DETECTION SERVICES:

Report of fraud accompanying a credit report

Notice or report from a credit agency of a credit freeze on a customer or applicant

Notice or report from a credit agency of an active duty alert for an applicant

Notice or report from a credit agency of an address discrepancy for an applicant

The credit report contains an alert with respect to the Social Security number used by the applicant, such as multiple Social Security numbers on file, Social Security number never issued, or a Social Security number that indicates that the individual is deceased

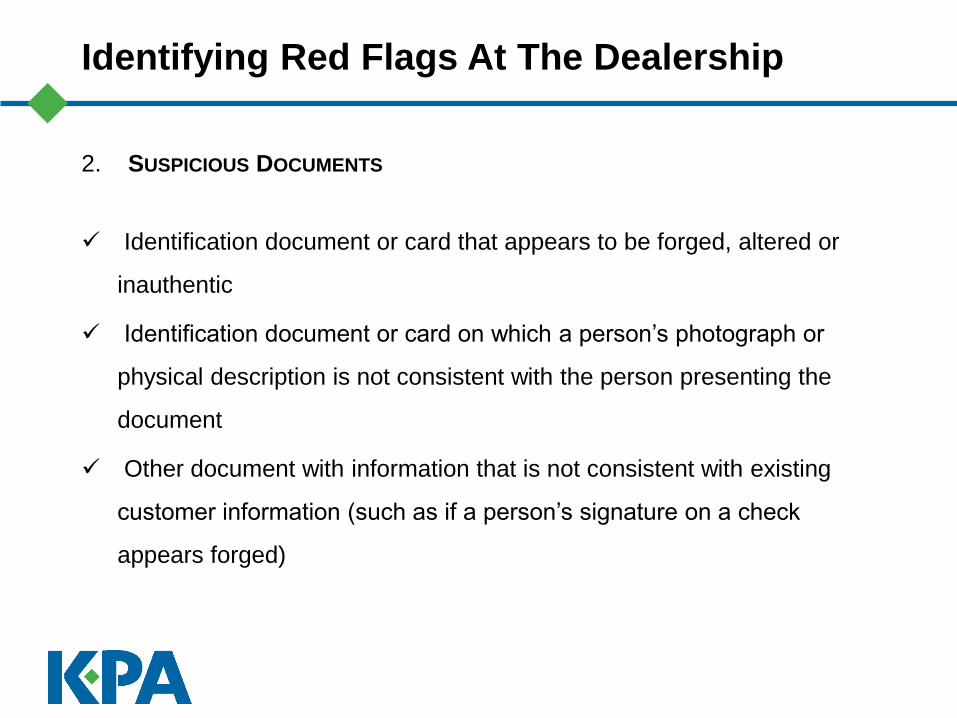

Identifying Red Flags At The Dealership

2. SUSPICIOUS DOCUMENTS

Identification document or card that appears to be forged, altered or

inauthentic

Identification document or card on which a person’s photograph or

physical description is not consistent with the person presenting the

document

Other document with information that is not consistent with existing

customer information (such as if a person’s signature on a check

appears forged)

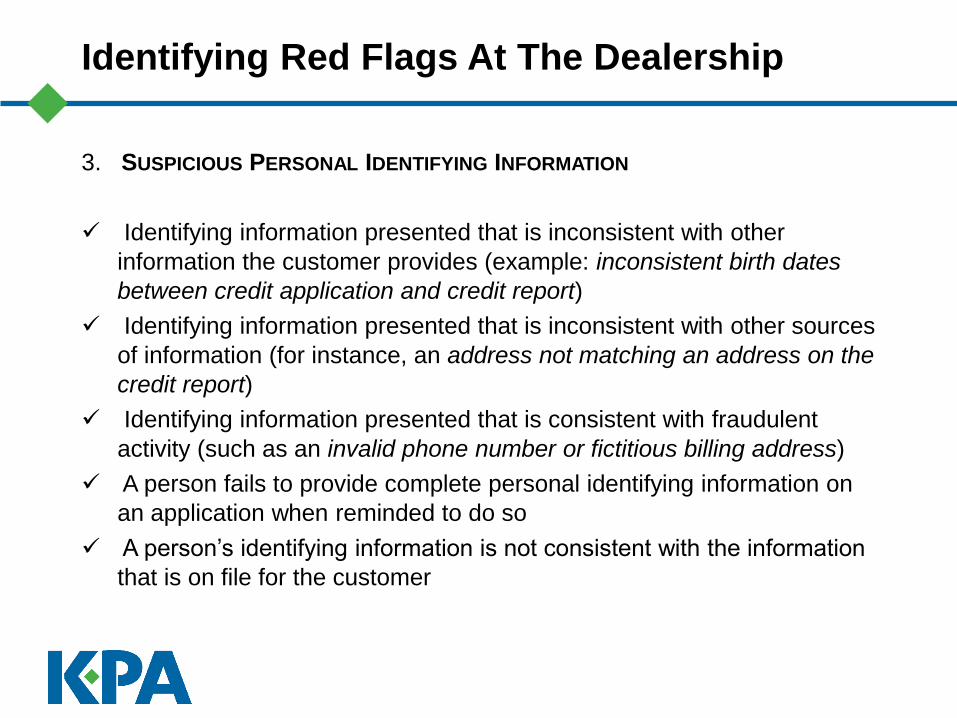

Identifying Red Flags At The Dealership

3. SUSPICIOUS PERSONAL IDENTIFYING INFORMATION

Identifying information presented that is inconsistent with other

information the customer provides (example: inconsistent birth dates

between credit application and credit report)

Identifying information presented that is inconsistent with other sources

of information (for instance, an address not matching an address on the

credit report)

Identifying information presented that is consistent with fraudulent

activity (such as an invalid phone number or fictitious billing address)

A person fails to provide complete personal identifying information on

an application when reminded to do so

A person’s identifying information is not consistent with the information

that is on file for the customer

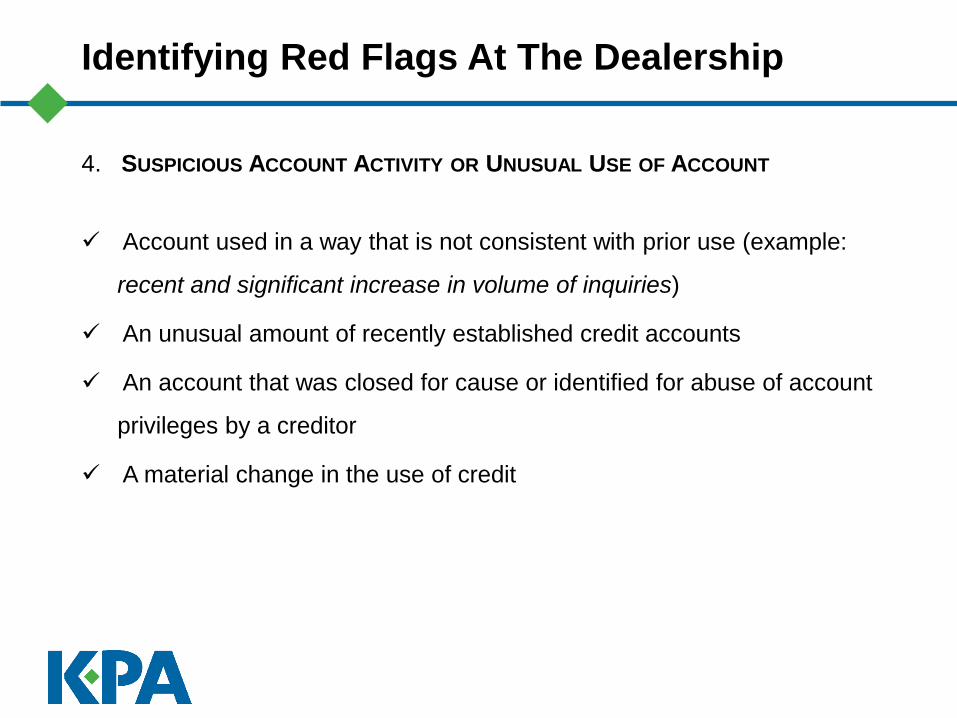

Identifying Red Flags At The Dealership

4. SUSPICIOUS ACCOUNT ACTIVITY OR UNUSUAL USE OF ACCOUNT

Account used in a way that is not consistent with prior use (example:

recent and significant increase in volume of inquiries)

An unusual amount of recently established credit accounts

An account that was closed for cause or identified for abuse of account

privileges by a creditor

A material change in the use of credit

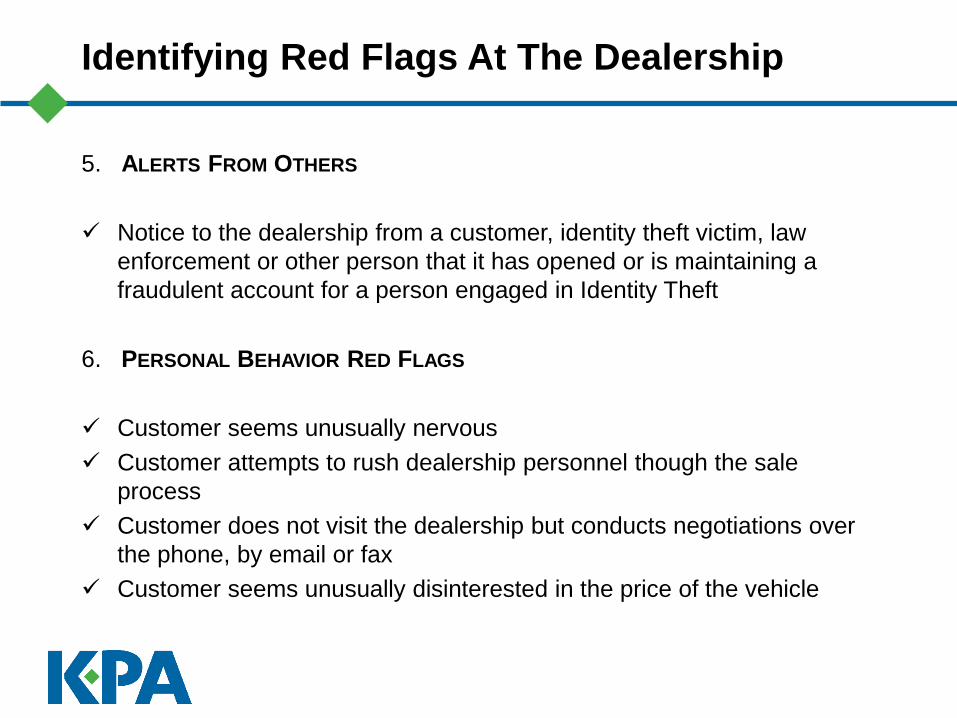

Identifying Red Flags At The Dealership

5. ALERTS FROM OTHERS

Notice to the dealership from a customer, identity theft victim, law

enforcement or other person that it has opened or is maintaining a

fraudulent account for a person engaged in Identity Theft

6. PERSONAL BEHAVIOR RED FLAGS

Customer seems unusually nervous

Customer attempts to rush dealership personnel though the sale

process

Customer does not visit the dealership but conducts negotiations over

the phone, by email or fax

Customer seems unusually disinterested in the price of the vehicle

Detecting Red Flags

Next, the Program must set forth procedures to detect those Red Flags that

were identified and incorporated into the Program.

In order to detect any of the Red Flags identified, the dealership’s personnel should

take the following steps to obtain and verify the identity of the person opening the

account:

A credit application should be completed and signed prior to the running of a

credit report.

Credit applications should be filled out completely, including at least 5 years of

residence and employment history.

Credit applications should be compared with information provided in the credit

report for consistency in order to detect address and other discrepancies.

Credit reports should be reviewed carefully for fraud or active duty alerts, or

credit freezes.

Detecting Red Flags

All credit applications should be accompanied by acceptable

identification. Sales personnel should not be permitted to deliver a

vehicle without first collecting and verifying acceptable identification.

Acceptable identification is any one of the following:

• Unexpired, state government issued drivers license with picture

• Unexpired, state government issued identification card with picture

• Unexpired, Military identification card with picture

• Unexpired, U.S. passport with picture

The picture on the identification should be confirmed to be the same

person that is applying for credit. You should ensure the picture on the

acceptable identification bears a reasonable resemblance to the

customer.

Detecting Red Flags

You should compare the signature on the acceptable identification to the signature on the credit application and other documents.

You should check the form of identification presented by the applicant to see if it appears to be forged or altered. If you are unfamiliar with the appearance or security features of a particular form of identification, a valid reference source should be consulted for verification (e.g. lookup on line).

If there is any question as to the validity of the identification, personnel should seek approval from senior management or the Red Flags Coordinator.

Responding to Red Flags

Finally, the Program must set forth procedures to

respond appropriately to detected Red Flags to

prevent or mitigate (reduce the impact of) identity

theft.

The presence of one or more Red Flags does not

necessarily mean that the applicant is an identity thief,

however you should take additional steps to ensure that

the person attempting to purchase on credit or lease a

vehicle is not using someone else’s identity.

Responding to Red Flags

If a Red Flag is detected, you may utilize the following procedures for identity verification:

A second form of identification should be presented by the customer. Secondary forms of identification include:

State government issued driver’s license/ID card with picture Passport Vehicle title or registration US Military ID card with picture Utility bill Major credit card

Responding to Red Flags

Credit History Quiz

When a Red Flag is detected, the customer should be asked credit history

questions based upon the contents of the credit report. These “out of

wallet” questions are based on data that is probably not known by an

identity thief because a person is not likely to carry such information in his

or her wallet.

The customer must be able to answer most of the questions correctly. If

the customer cannot correctly answer the questions, the transaction can

only proceed upon approval by senior management. Examples of credit

history quiz questions are (“Out of Wallet” questions may also be

generated by automated systems, such as DealerTrack or RouteOne):

What is the approximate balance on your Visa credit card?

What is the name of your previous employer?

What is your previous address?

Responding to Red Flags

In what U.S. state/territory were you residing when you (or your

parent/guardian) applied for your social security card? *

What is the approximate balance on your Home Depot credit card?

What is the amount of your mortgage payment?

What is the name of the company that you make your mortgage

payment to?

What is the name of the company that you make your car payment to?

* To determine if customer’s response is correct, dealer personnel should

refer to the Social Security Number Allocation table at

www.socialsecurity.gov/employer/stateweb.htm.

Address Verification

This step is only necessary if any of the Red Flags identified an address

discrepancy or if there is a need to verify a delivery address for a

transaction where the customer does not visit the dealership. The

customer must produce proof of current, physical address using any of the

documents described in this section. In the event the customer cannot

provide acceptable proof of current, physical address, the transaction can

only proceed upon approval by senior management. Address can be

verified by:

Current utility bill (not mobile/wireless phone)

Current mortgage statement

Recent property tax bill

Current lease agreement

Approval or Denial of Transaction

Dealership staff should either certify completion of the

Red Flags detection process and approve the

transaction or deny the transaction. In the event the

applicant is unable to adequately respond to and/or

provide documentation for detected Red Flags, the

transaction should be denied unless a waiver is

approved by senior management. Each denial that

takes place must be submitted to the Red Flags

Coordinator for further review.

Approval or Denial of Transaction

The Red Flags Coordinator should determine which of the

following additional actions will be taken on a case-by-case

basis:

Contact applicant for additional information and/or

documentation

Refuse to deliver the vehicle to customer

Contact law enforcement

Contact the suspected or confirmed identity theft victim

Contact credit reporting agency to report that an inquiry was

bogus

Issue an adverse action notice

Determine that no further response is necessary

Red Flags Coordinator Responsibilities

The Red Flags (Program) Coordinator shall be responsible for the development,

implementation, oversight and continued administration of the Program. The

Coordinator may engage the services of an outside consultant(s) to assist in the

development and implementation of the Program.

The Program Coordinator shall put a program in place to train staff, as

necessary, to effectively implement the Program.

The Program Coordinator shall exercise appropriate and effective oversight of

service provider arrangements.

The Program Coordinator shall be responsible for assignment of specific

responsibility for implementation of the Program to other senior level managers.

The Program Coordinator will be responsible for conducting initial and periodic

risk assessments to identify potential identity theft risks, identifying relevant identity

theft Red Flags, implementing methods to detect Red Flags, creating processes to

respond appropriately when Red Flags are detected, review of reports prepared by

staff regarding compliance, approval of material changes to the Program as

necessary to address changing risks of identity theft, identification of the steps for

preventing and mitigating Identity Theft, and determining which steps of prevention

and mitigation should be taken in particular circumstances.

Red Flags Coordinator Responsibilities

The Program Coordinator shall report to the company ownership at least

annually on compliance by the organization with the Program.

The report shall address material matters related to the Program and evaluate

issues such as:

– The effectiveness of the policies and procedures in addressing the risk of identity

theft in connection with the opening of covered accounts and with respect to existing

covered accounts

– Service provider agreements

– Significant incidents involving identity theft and management’s response

– Recommendations for material changes to the Program

Automated Red Flags Programs

A Number of companies such as DealerTrack,

RouteOne and credit reporting agencies offer

automated Red Flags programs. These can

save a great deal of time.

So You Have A Red Flags Program…Now What?

• There’s some due diligence required on the part of

dealership personnel when potential “Red Flags” are

detected.

• We’ve found a number of situations during

compliance audits where the red flags program has

prompted that a “high risk has been detected” and that

“out of wallet questions are required”, but the questions

have not been asked of the customer.

• While it can certainly be uncomfortable to ask a

customer personal questions or request that they supply

additional proof of identity or address, it is important that

these steps not be avoided.

Staff Responsibilities

If an identity theft does occur and the proper steps were

not taken, it’s conceivable that the dealership’s

exposure to liability will be increased dramatically. The

same holds true in a situation where the dealer’s Red

Flags procedures are audited by a regulator. Staff

members’ proclamations that they had a ‘gut feeling’

that the customers were who they said they were will

not likely be enough to satisfy the investigators. The fact

that the employees were prompted to follow a particular

procedure and failed to do so would almost certainly

make matters much worse.

The Bottom Line

Even the best Red Flags program is not infallible.

Chances are that an experienced identity thief will

succeed despite a dealership’s best efforts. That’s

understandable. As long as the company can show that

they have performed their due diligence and did not

take any shortcuts, their exposure will likely be lessened

dramatically.

There hasn’t been a lot of enforcement action YET, but

there likely will be in the foreseeable future. And the

FTC LOVES targeting auto dealers…

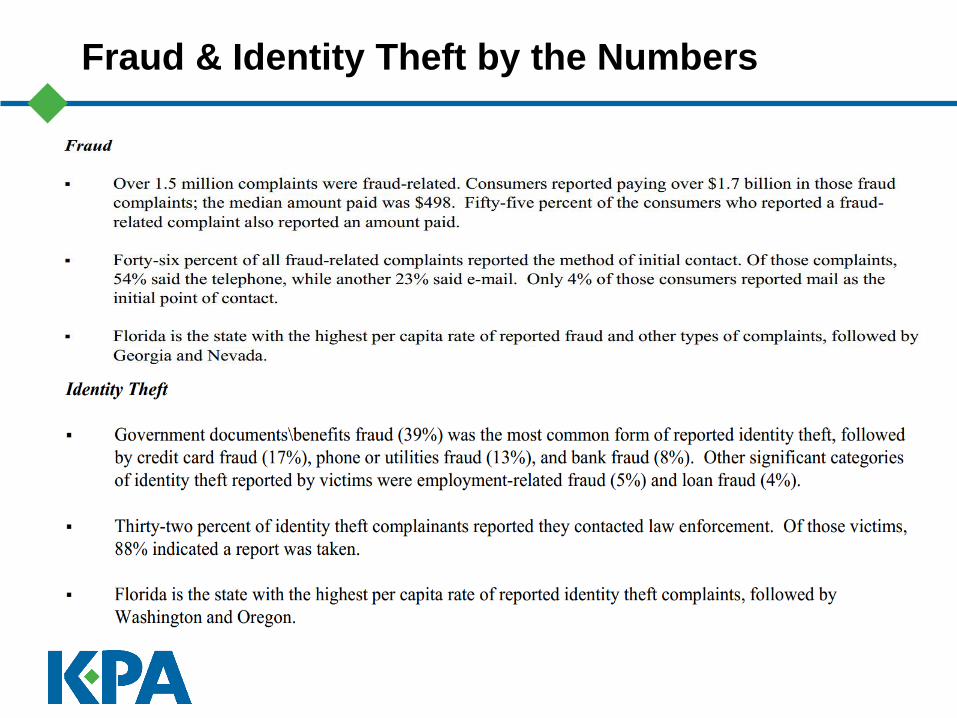

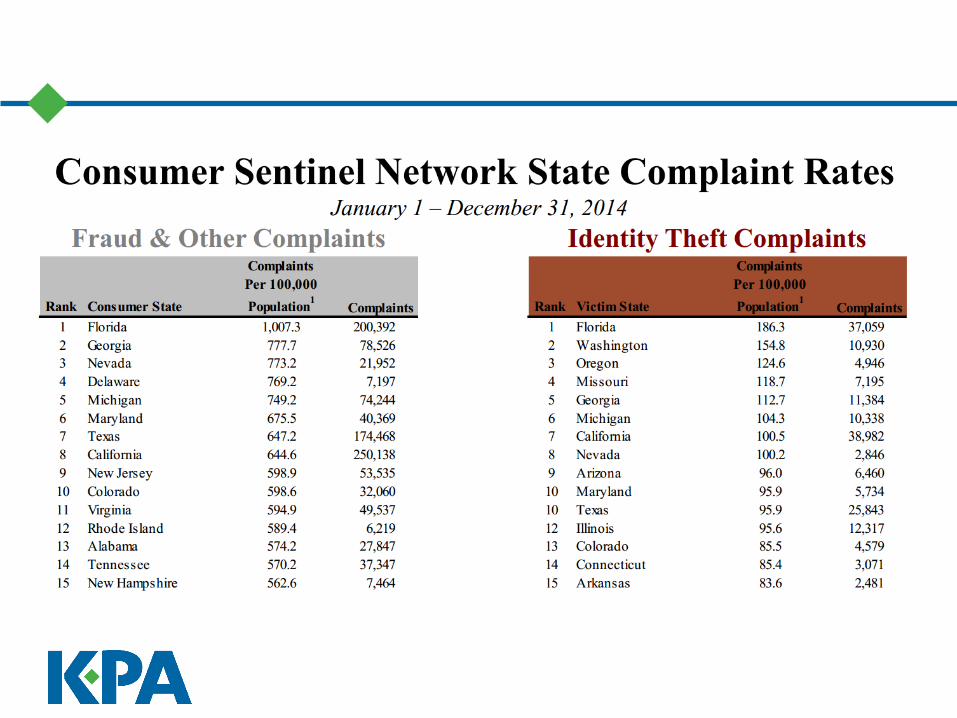

Fraud & Identity Theft by the Numbers

Questions and Answers

Contact Information

The recorded webinar and presentation slides will be emailed to

you today including your local representative’s contact information.

www.kpaonline.com

866-228-6587

Recommended