TOPIC FOCUS ONPROCESS COSTING

TF2

WHEN IS A YARD NOT A YARD?

► Bradley Textile Mills started working on 500,000 yards of jersey fabric

► The month-end report showed only 450,000 yards in process

► So how do you reconcile the 50,000 yard difference when you know there was no spoilage?

TF2

HOW DO THEY DIFFER?

Custom Cabinetmaker Textile Mill

• Each job is unique• Product costs are easy

to trace to a specific job/product

• Fabric is mass-produced• Impossible to trace

product costs to a specific yard of fabric

How do you determine the cost of a product in a mass-production environment?

TF2

COST FLOWS IN PROCESS COSTING SYSTEM

TF2

COSTING SYSTEM COMPARISON

Process CostingJob Order Costing

Similarities

Objective To accumulate and assign manufacturing costs to products

To accumulate and assign manufacturing costs to products

Product costs Direct material, direct labor, manufacturing overhead

Direct material, direct labor, manufacturing overhead

Cost flows From RM to WIP to FG to COGS

From RM to WIP to FG to COGS

Differences

Production schedule Identical products produced over a long period, often in a continuous production process

Many different products produced, each with different materials, labor, and/or overhead requirements

Cost accumulation By production department

By job

Key document Department production report

Job cost sheet

TF2

THINK ABOUT IT…

When are direct materials added in this process?

What are conversion costs

and when are they incurred?

Which of these departments could have ending WIP?

How is the product in Mixing WIP ending inventory different from the product being transferred from mixing to baking?

TF2

PROCESS COSTING ISSUES

► Materials costs versus conversion costs• Timing differences lead to costing differences

► Equivalent units• Often not the same as the number of physical units• May be different for direct materials and for

conversion• 10 cookies that are 60% complete = 6 equivalent

units (10 × 60%)

TF2

EQUIVALENT UNITS

Two units that are 50% complete have required the same inputs and effort as one unit that is 100% complete. So

these two physical units are one equivalent unit.

# of physical units × % of completion = Equivalent Units

TF2

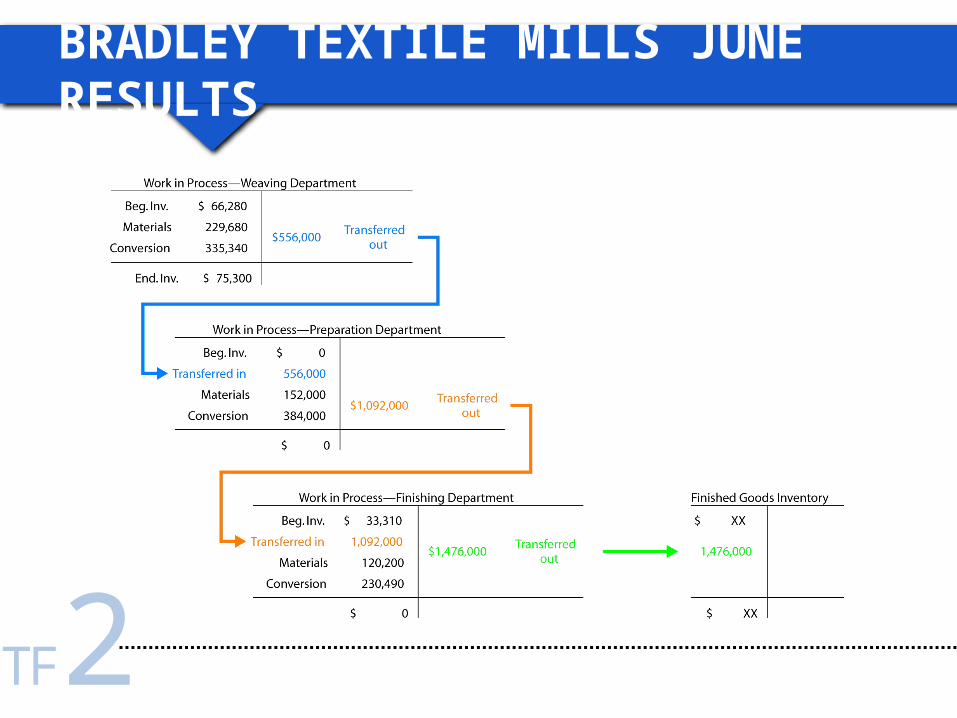

BRADLEY TEXTILE MILLS JUNE RESULTS

TF2

CALCULATING UNIT COST

Beginning WIP $ + Costs added during the period

Completed physical units + Ending WIP equivalent units

Weaving Dept. – Materials

Work in process, June 1 $ 37,120

+ Costs added during June 565,020

= Total costs to be accounted for $266,800

Completed yards transferred 400,000

+ Ending WIP equivalent yards 60,000

÷ Equivalent yards 460,000

= Cost per equivalent unit $ 0.58

TF2

PROCESS COSTING RECAP

► Calculate the physical unit flow► Calculate the equivalent units of production► Calculate the cost per equivalent unit► Allocate the equivalent unit costs of production► Reconcile the costs of production► Repeat for each production department

Recommended