1

The Impact of the Financial Crisis on CARICOM countries

By

Preeya Mohan1

and

Patrick Kent Watson

Sir Arthur Lewis Institute of Social and Economic Studies

University of the West Indies

St. Augustine

Trinidad & Tobago

Tel: (868) 662-6965,

Fax: (868) 645-6329

Abstract

The current global financial crisis is a reminder of the inherent vulnerabilities faced by

CARICOM economies on their road to economic growth and development. The crisis has

negatively affected growth and, as data gradually become available, its far-reaching after-effects

are becoming more evident. A study of the impact of the crisis on economic growth in the region

is needed in the way forward for CARICOM development. As such the aftermath of the crisis on

the region requires detailed documentation. This paper seeks to examine the outcome of the

crisis on economic growth among CARICOM countries with particular emphasis on

international trade and private capital flows from which lessons and productive development

policies can be derived.

1 Corresponding author

2

1. Introduction

The development of the CARICOM region must begin with a comprehensive synopsis of the

developmental hurdles faced by the region. In other words the question “where are we now?”

must be answered before we know where we need to go. In April 2007 the United States (US)

sub-prime mortgage market went belly-up, which triggered a crash in its financial system and

marked the beginning of the International Financial Crisis (IFC). The crisis eventually spread to

the real sector of the US and, in December 2007, the economy went into a deep recession. In

September 2008, contagion effects led to the contamination of international financial markets

creating a worldwide calamity. The IFC then became a global economic crisis as, worldwide,

real sector effects materialized. Unlike recent crises which started off in emerging and

developing economies such as the 1994 Mexico crisis, Thailand and Korea in 1997, Indonesia,

Malaysia and Russia in 1998 and Argentina in 2001, this catastrophe originated in the world’s

largest economy creating the largest shock to economic growth since the 1930’s, which has since

been labeled the “Great Recession”.

The result has been a sharp downturn in world gross domestic product (GDP), commencing in

the latter half of 2008 to 2009. The recovery however remains highly uncertain. The

International Monetary Fund’s (IMF) World Economic Outlook (WEO) Report (October 2010)

states that recovery rests on two rebalancing acts, fiscal consolidation and a realignment of

international trade which entails increasing net exports in advanced economies and reducing net

exports in emerging economies. Furthermore, the global financial system is yet to recover and

there exists considerable uncertainty as sovereign and banking vulnerabilities persist which has

increased market volatility and reduced investor confidence. Sovereign balance sheets are highly

vulnerable to growth shocks, making debt sustainability less certain, prices in stock exchanges

have fallen and the risk premiums on corporate bonds have widened, and corporate bond issues

have slowed (Global Financial Stability Report October 2010). Nevertheless, in 2010, there has

been some recovery with emerging markets particularly, Asia at the forefront and advanced

economies lagging behind (table 1). The recovery is however questionable as it was being driven

by mammoth fiscal deficits which have since subsided while consumption and investment

remains depressed.

As the advanced and emerging economies undergo fiscal consolidation and attempt to develop

domestic sources of growth coupled with weak financial markets the worst of the crisis may yet

to come for the CARICOM region.

economic growth in CARICOM countri

financial capital flows as the transmission channel of the crisis has been on the balance of

payment accounts of CARICOM economies.

introduction. The rest of the paper is organized as fol

transmission mechanisms of the crisi

and private capital flows, section four the impact of the crisis on CARICOM’s macro economy,

section five provides a global outlook followed by

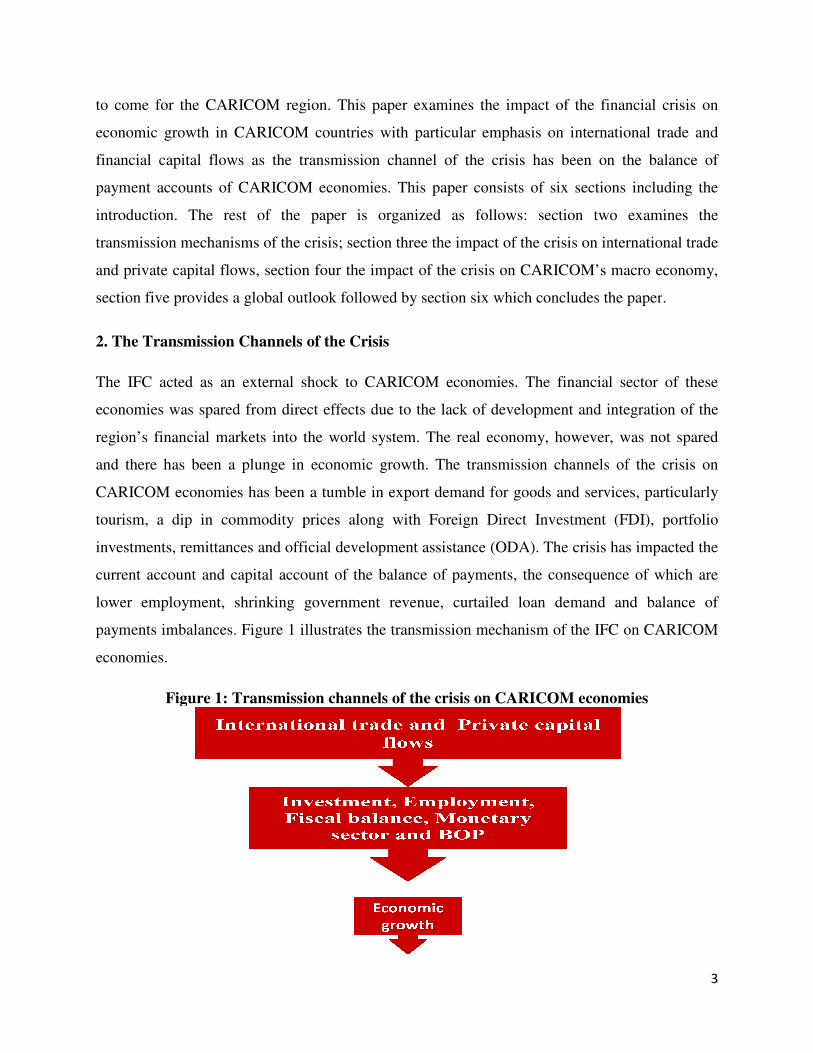

2. The Transmission Channels of the Crisis

The IFC acted as an external shock

economies was spared from direct effects due to t

region’s financial markets into the world system. The real economy, however, was not spared

and there has been a plunge in economic gr

CARICOM economies has been a tumble in

tourism, a dip in commodity prices along with

investments, remittances and official development assistance

current account and capital account of the balance of payments, the consequence of which are

lower employment, shrinking government revenue, curtailed loan demand and balance of

payments imbalances. Figure 1 illustrates the transmission mechanism of the IFC on CARICOM

economies.

Figure 1: Transmission c

region. This paper examines the impact of the financial crisis on

economic growth in CARICOM countries with particular emphasis on international trade

he transmission channel of the crisis has been on the balance of

payment accounts of CARICOM economies. This paper consists of six sections including the

The rest of the paper is organized as follows: section two

f the crisis; section three the impact of the crisis on international trade

and private capital flows, section four the impact of the crisis on CARICOM’s macro economy,

outlook followed by section six which concludes the paper

2. The Transmission Channels of the Crisis

as an external shock to CARICOM economies. The financial

direct effects due to the lack of development and i

l markets into the world system. The real economy, however, was not spared

n economic growth. The transmission channels

CARICOM economies has been a tumble in export demand for goods and services, particularly

tourism, a dip in commodity prices along with Foreign Direct Investment (FDI),

, remittances and official development assistance (ODA). The crisis has impacted the

capital account of the balance of payments, the consequence of which are

lower employment, shrinking government revenue, curtailed loan demand and balance of

payments imbalances. Figure 1 illustrates the transmission mechanism of the IFC on CARICOM

Figure 1: Transmission channels of the crisis on CARICOM economies

3

This paper examines the impact of the financial crisis on

national trade and

he transmission channel of the crisis has been on the balance of

sists of six sections including the

section two examines the

on international trade

and private capital flows, section four the impact of the crisis on CARICOM’s macro economy,

section six which concludes the paper.

to CARICOM economies. The financial sector of these

development and integration of the

l markets into the world system. The real economy, however, was not spared

owth. The transmission channels of the crisis on

xport demand for goods and services, particularly

eign Direct Investment (FDI), portfolio

The crisis has impacted the

capital account of the balance of payments, the consequence of which are

lower employment, shrinking government revenue, curtailed loan demand and balance of

payments imbalances. Figure 1 illustrates the transmission mechanism of the IFC on CARICOM

hannels of the crisis on CARICOM economies

4

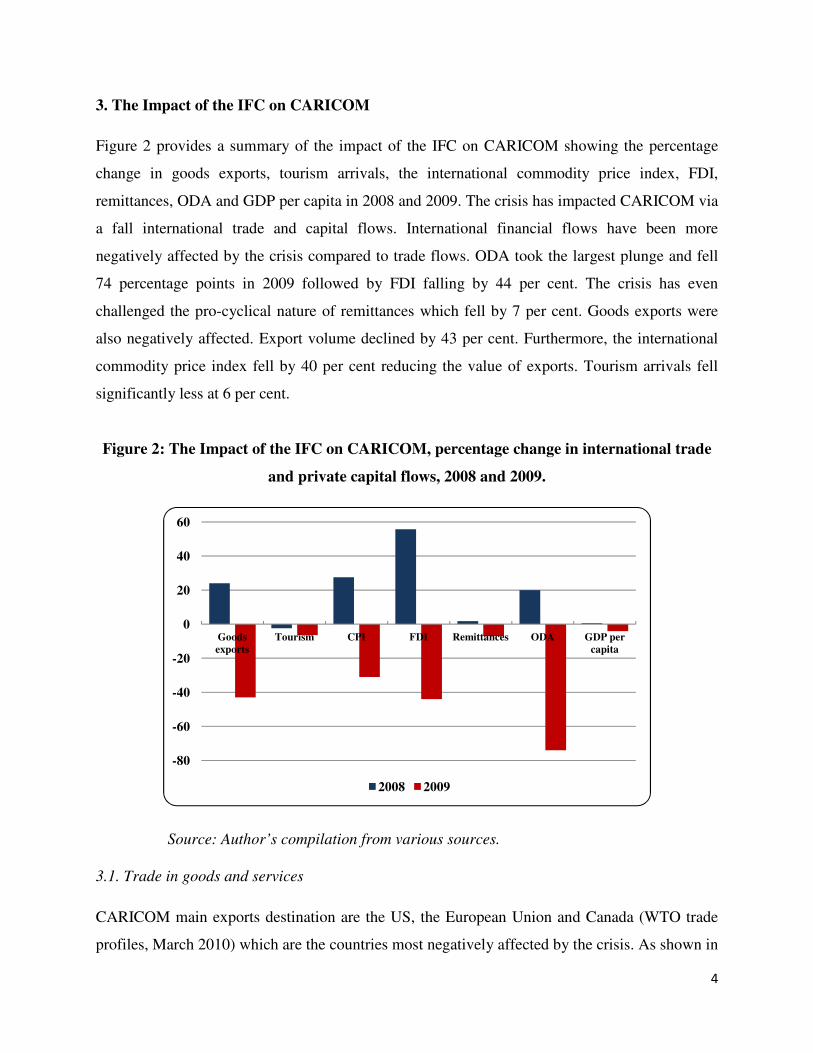

3. The Impact of the IFC on CARICOM

Figure 2 provides a summary of the impact of the IFC on CARICOM showing the percentage

change in goods exports, tourism arrivals, the international commodity price index, FDI,

remittances, ODA and GDP per capita in 2008 and 2009. The crisis has impacted CARICOM via

a fall international trade and capital flows. International financial flows have been more

negatively affected by the crisis compared to trade flows. ODA took the largest plunge and fell

74 percentage points in 2009 followed by FDI falling by 44 per cent. The crisis has even

challenged the pro-cyclical nature of remittances which fell by 7 per cent. Goods exports were

also negatively affected. Export volume declined by 43 per cent. Furthermore, the international

commodity price index fell by 40 per cent reducing the value of exports. Tourism arrivals fell

significantly less at 6 per cent.

Figure 2: The Impact of the IFC on CARICOM, percentage change in international trade

and private capital flows, 2008 and 2009.

Source: Author’s compilation from various sources.

3.1. Trade in goods and services

CARICOM main exports destination are the US, the European Union and Canada (WTO trade

profiles, March 2010) which are the countries most negatively affected by the crisis. As shown in

-80

-60

-40

-20

0

20

40

60

Goods exports

Tourism CPI FDI Remittances ODA GDP per capita

2008 2009

5

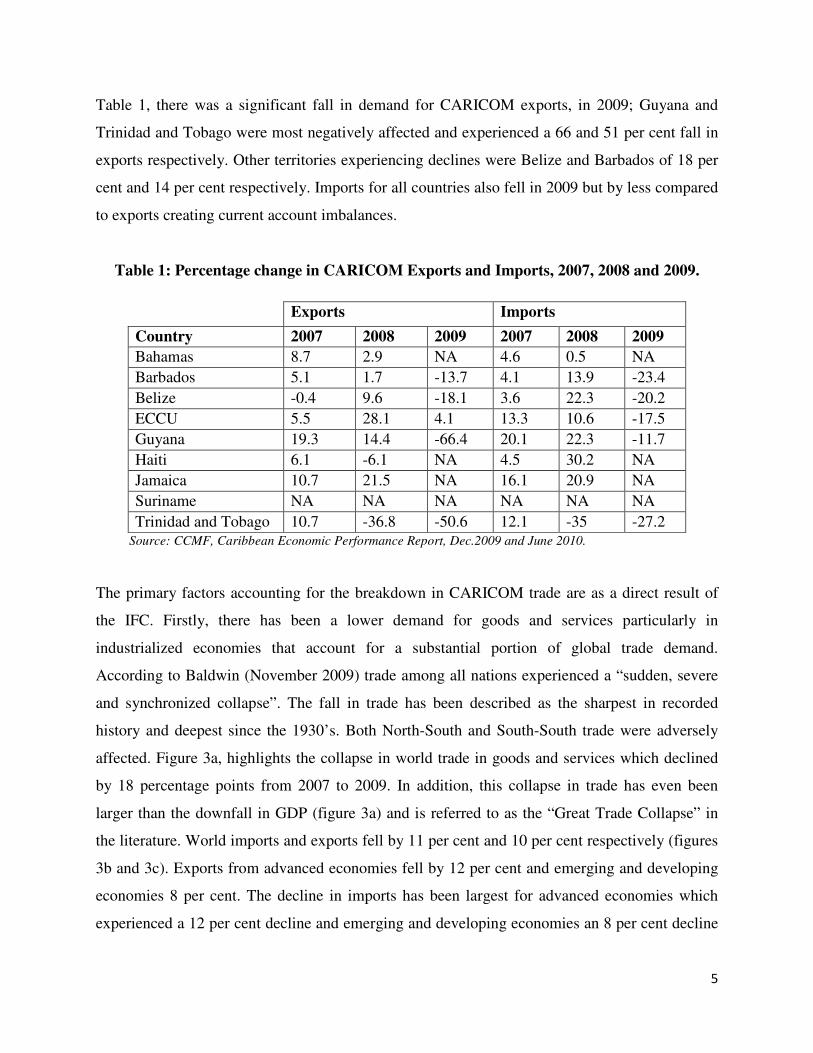

Table 1, there was a significant fall in demand for CARICOM exports, in 2009; Guyana and

Trinidad and Tobago were most negatively affected and experienced a 66 and 51 per cent fall in

exports respectively. Other territories experiencing declines were Belize and Barbados of 18 per

cent and 14 per cent respectively. Imports for all countries also fell in 2009 but by less compared

to exports creating current account imbalances.

Table 1: Percentage change in CARICOM Exports and Imports, 2007, 2008 and 2009.

Exports Imports

Country 2007 2008 2009 2007 2008 2009

Bahamas 8.7 2.9 NA 4.6 0.5 NA

Barbados 5.1 1.7 -13.7 4.1 13.9 -23.4

Belize -0.4 9.6 -18.1 3.6 22.3 -20.2

ECCU 5.5 28.1 4.1 13.3 10.6 -17.5

Guyana 19.3 14.4 -66.4 20.1 22.3 -11.7

Haiti 6.1 -6.1 NA 4.5 30.2 NA

Jamaica 10.7 21.5 NA 16.1 20.9 NA

Suriname NA NA NA NA NA NA

Trinidad and Tobago 10.7 -36.8 -50.6 12.1 -35 -27.2 Source: CCMF, Caribbean Economic Performance Report, Dec.2009 and June 2010.

The primary factors accounting for the breakdown in CARICOM trade are as a direct result of

the IFC. Firstly, there has been a lower demand for goods and services particularly in

industrialized economies that account for a substantial portion of global trade demand.

According to Baldwin (November 2009) trade among all nations experienced a “sudden, severe

and synchronized collapse”. The fall in trade has been described as the sharpest in recorded

history and deepest since the 1930’s. Both North-South and South-South trade were adversely

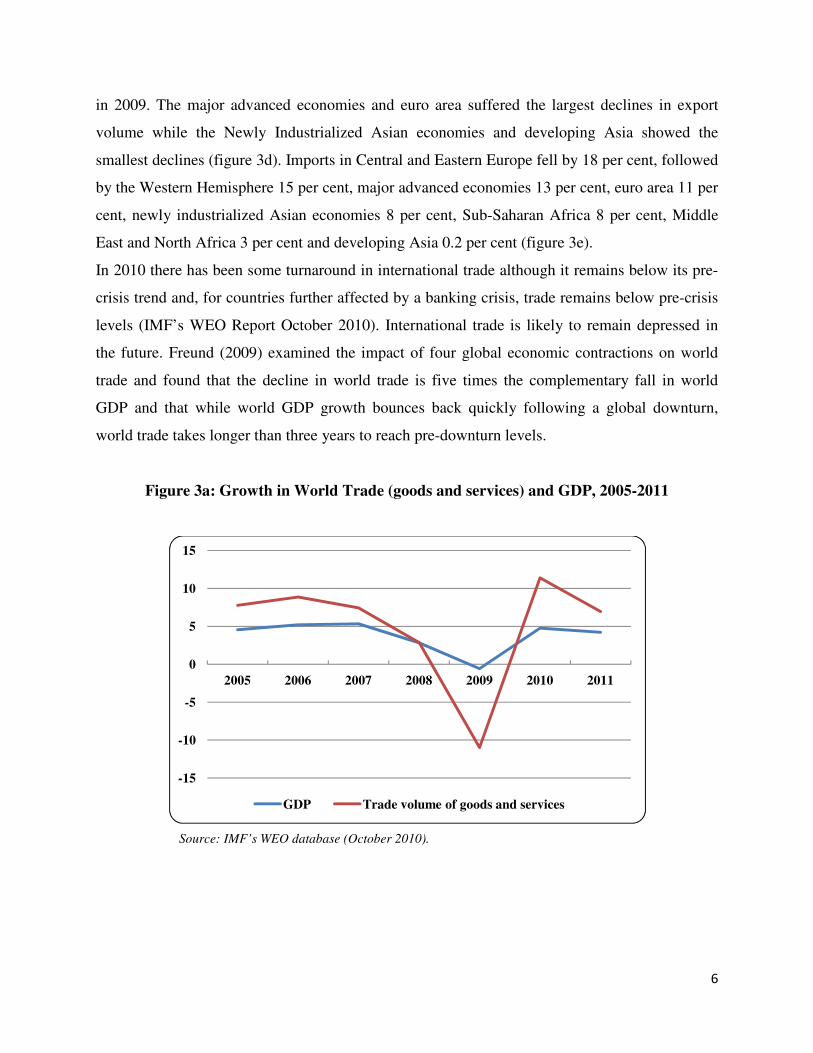

affected. Figure 3a, highlights the collapse in world trade in goods and services which declined

by 18 percentage points from 2007 to 2009. In addition, this collapse in trade has even been

larger than the downfall in GDP (figure 3a) and is referred to as the “Great Trade Collapse” in

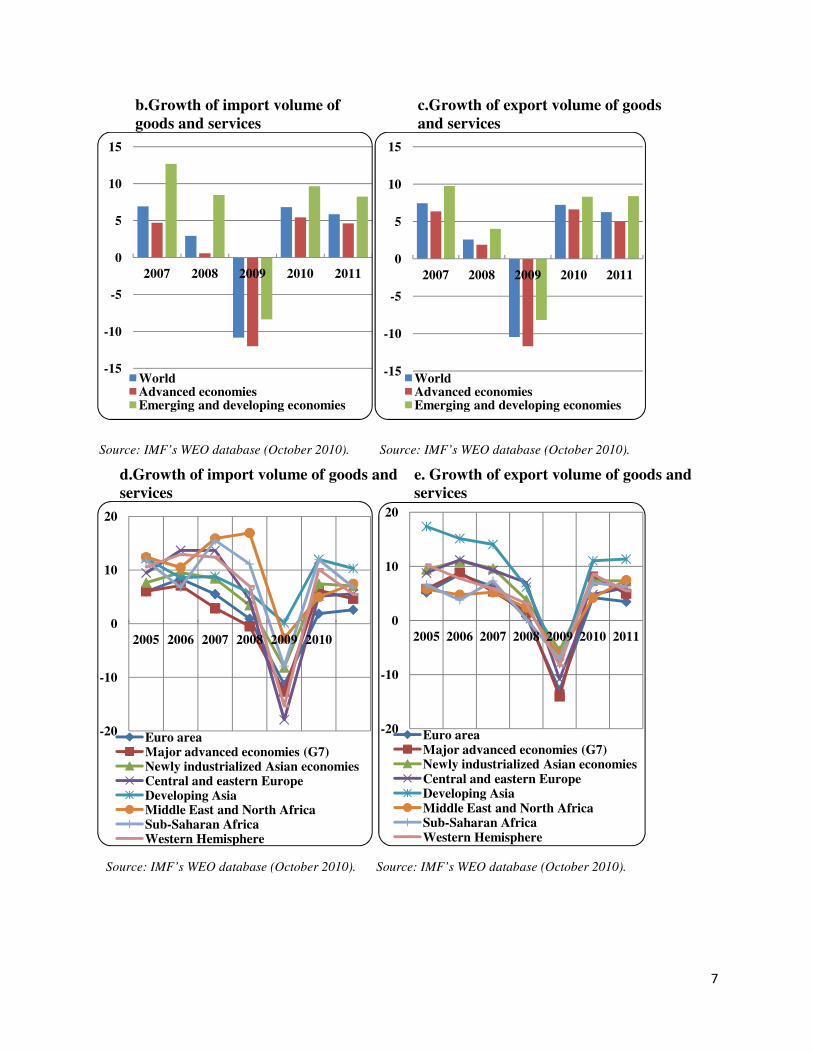

the literature. World imports and exports fell by 11 per cent and 10 per cent respectively (figures

3b and 3c). Exports from advanced economies fell by 12 per cent and emerging and developing

economies 8 per cent. The decline in imports has been largest for advanced economies which

experienced a 12 per cent decline and emerging and developing economies an 8 per cent decline

6

in 2009. The major advanced economies and euro area suffered the largest declines in export

volume while the Newly Industrialized Asian economies and developing Asia showed the

smallest declines (figure 3d). Imports in Central and Eastern Europe fell by 18 per cent, followed

by the Western Hemisphere 15 per cent, major advanced economies 13 per cent, euro area 11 per

cent, newly industrialized Asian economies 8 per cent, Sub-Saharan Africa 8 per cent, Middle

East and North Africa 3 per cent and developing Asia 0.2 per cent (figure 3e).

In 2010 there has been some turnaround in international trade although it remains below its pre-

crisis trend and, for countries further affected by a banking crisis, trade remains below pre-crisis

levels (IMF’s WEO Report October 2010). International trade is likely to remain depressed in

the future. Freund (2009) examined the impact of four global economic contractions on world

trade and found that the decline in world trade is five times the complementary fall in world

GDP and that while world GDP growth bounces back quickly following a global downturn,

world trade takes longer than three years to reach pre-downturn levels.

Figure 3a: Growth in World Trade (goods and services) and GDP, 2005-2011

Source: IMF’s WEO database (October 2010).

-15

-10

-5

0

5

10

15

2005 2006 2007 2008 2009 2010 2011

GDP Trade volume of goods and services

7

b.Growth of import volume of goods and services

c.Growth of export volume of goods and services

Source: IMF’s WEO database (October 2010). Source: IMF’s WEO database (October 2010).

d.Growth of import volume of goods and services

e. Growth of export volume of goods and services

Source: IMF’s WEO database (October 2010). Source: IMF’s WEO database (October 2010).

-15

-10

-5

0

5

10

15

2007 2008 2009 2010 2011

WorldAdvanced economiesEmerging and developing economies

-15

-10

-5

0

5

10

15

2007 2008 2009 2010 2011

WorldAdvanced economiesEmerging and developing economies

-20

-10

0

10

20

2005 2006 2007 2008 2009 2010

Euro area Major advanced economies (G7)Newly industrialized Asian economiesCentral and eastern EuropeDeveloping AsiaMiddle East and North AfricaSub-Saharan AfricaWestern Hemisphere

-20

-10

0

10

20

2005 2006 2007 2008 2009 2010 2011

Euro area Major advanced economies (G7)Newly industrialized Asian economiesCentral and eastern EuropeDeveloping AsiaMiddle East and North AfricaSub-Saharan AfricaWestern Hemisphere

8

The crisis has also caused a dwindling of trade credit and finance which has resulted in a fall i

international trade (Qalo 2009, WTO/OECD 2009). The cost of trade credit instruments rose

astronomically in the latter part of 2008 and, in March 2009, there was an excess demand for

credit financing between US$100 billion and US$300 billion on an annual and roll-over basis

(WTO/OECD 2009). A fall in countries’ foreign exchange reserves is another cause cited for the

fall in trade (Qalo 2009). Another consequence of the crisis has been burgeoning protectionism.

Since the start of the crisis, nations have proposed approximately 78 trade measures and, of

these, 47 eventually were implemented, the effect of which has been to restrict trade (Gamberoni

and Newfarmer 2009). In addition, antidumping initiatives grew by 15 per cent and the

imposition of duties grew by 22 per cent from 2007 to 2008 (Gamberoni and Newfarmer 2009).

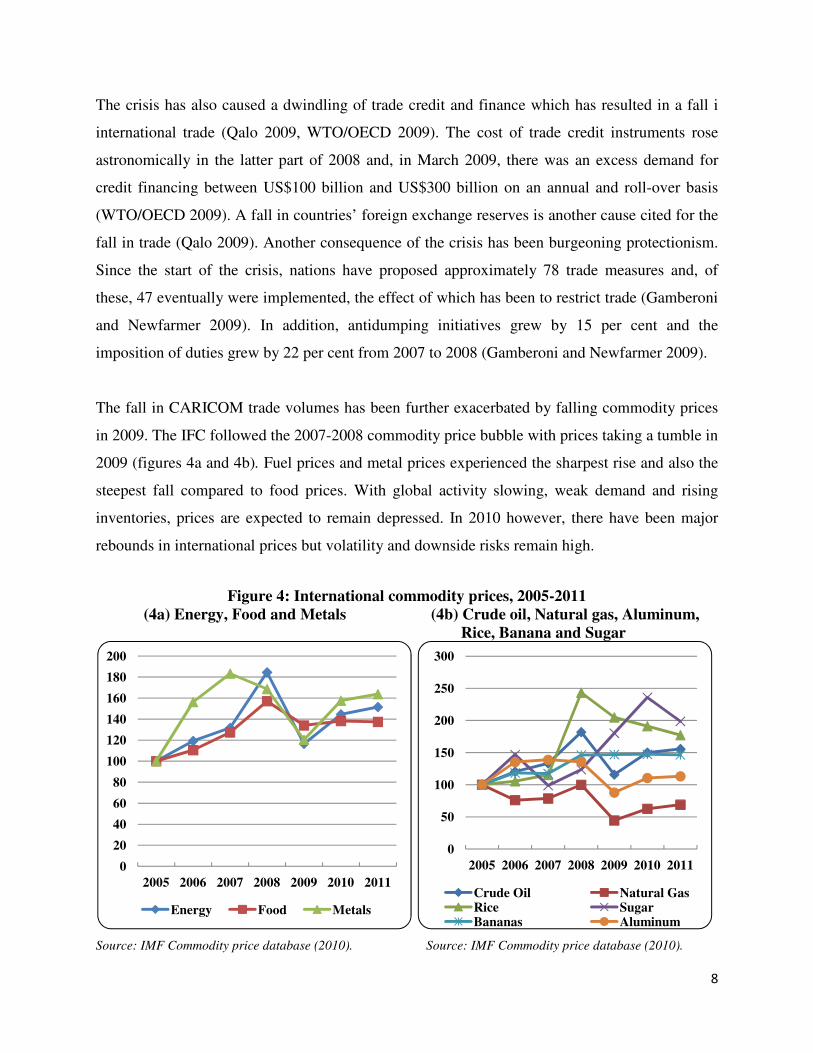

The fall in CARICOM trade volumes has been further exacerbated by falling commodity prices

in 2009. The IFC followed the 2007-2008 commodity price bubble with prices taking a tumble in

2009 (figures 4a and 4b). Fuel prices and metal prices experienced the sharpest rise and also the

steepest fall compared to food prices. With global activity slowing, weak demand and rising

inventories, prices are expected to remain depressed. In 2010 however, there have been major

rebounds in international prices but volatility and downside risks remain high.

Figure 4: International commodity prices, 2005-2011 (4a) Energy, Food and Metals (4b) Crude oil, Natural gas, Aluminum,

Rice, Banana and Sugar

Source: IMF Commodity price database (2010). Source: IMF Commodity price database (2010).

0

20

40

60

80

100

120

140

160

180

200

2005 2006 2007 2008 2009 2010 2011

Energy Food Metals

0

50

100

150

200

250

300

2005 2006 2007 2008 2009 2010 2011

Crude Oil Natural GasRice SugarBananas Aluminum

9

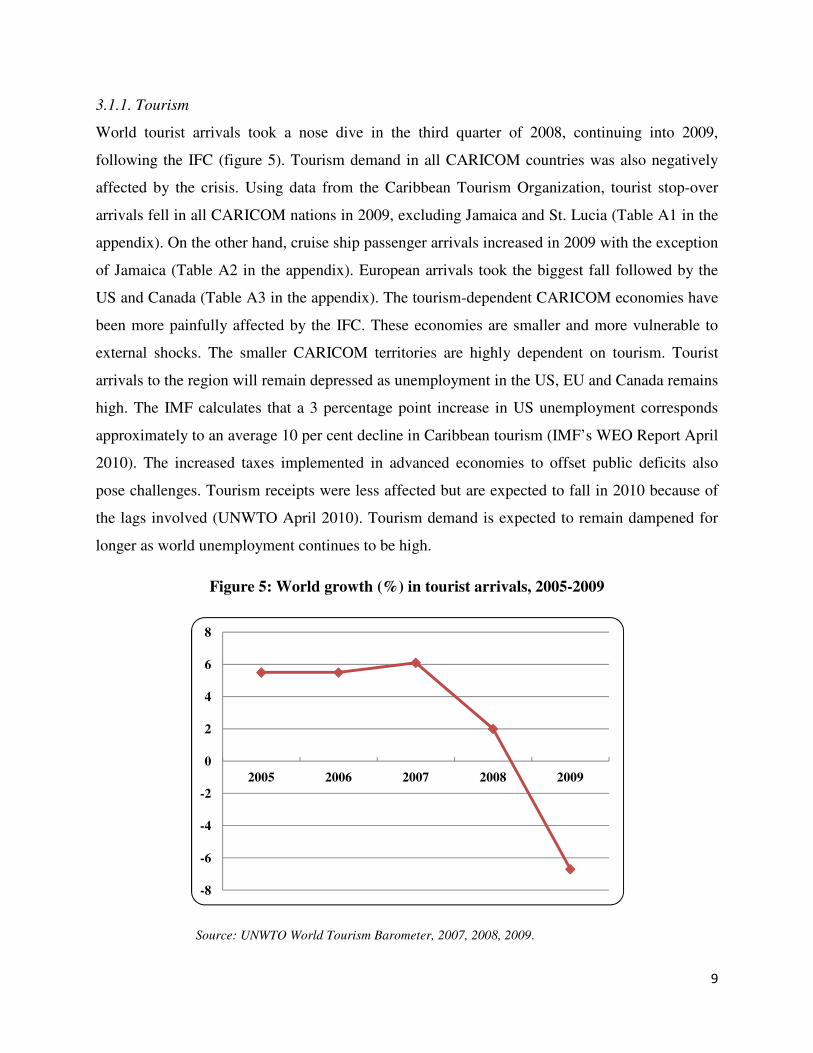

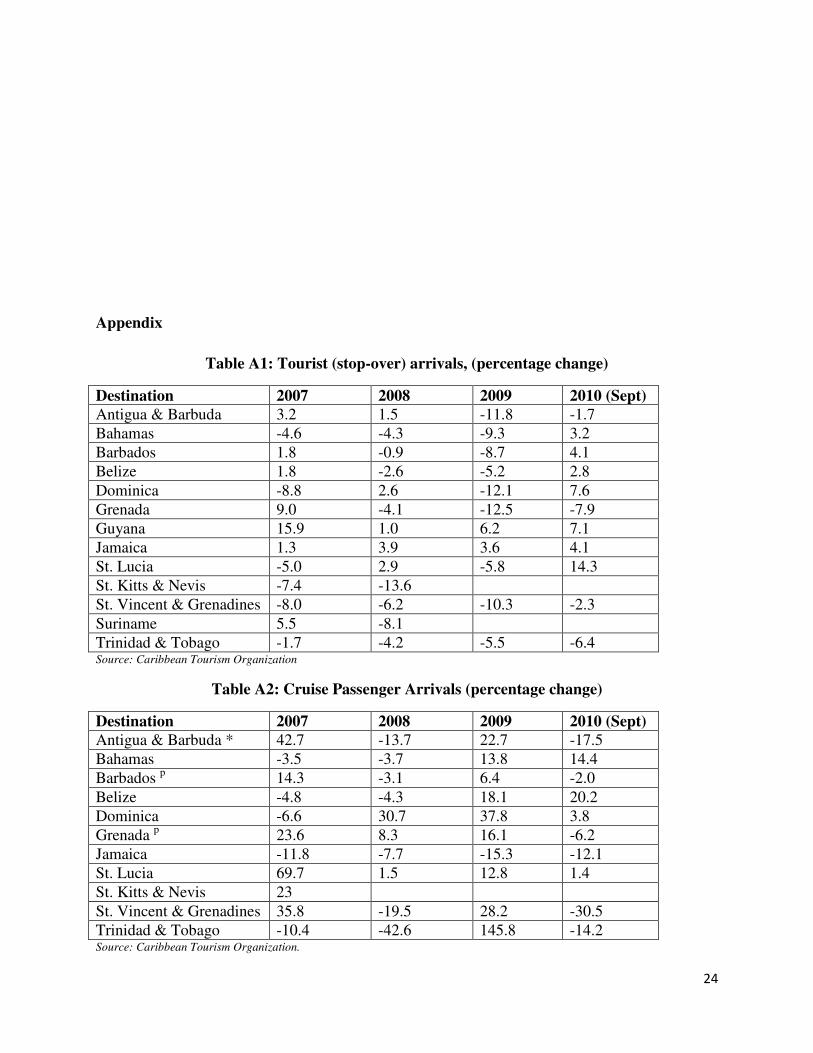

3.1.1. Tourism

World tourist arrivals took a nose dive in the third quarter of 2008, continuing into 2009,

following the IFC (figure 5). Tourism demand in all CARICOM countries was also negatively

affected by the crisis. Using data from the Caribbean Tourism Organization, tourist stop-over

arrivals fell in all CARICOM nations in 2009, excluding Jamaica and St. Lucia (Table A1 in the

appendix). On the other hand, cruise ship passenger arrivals increased in 2009 with the exception

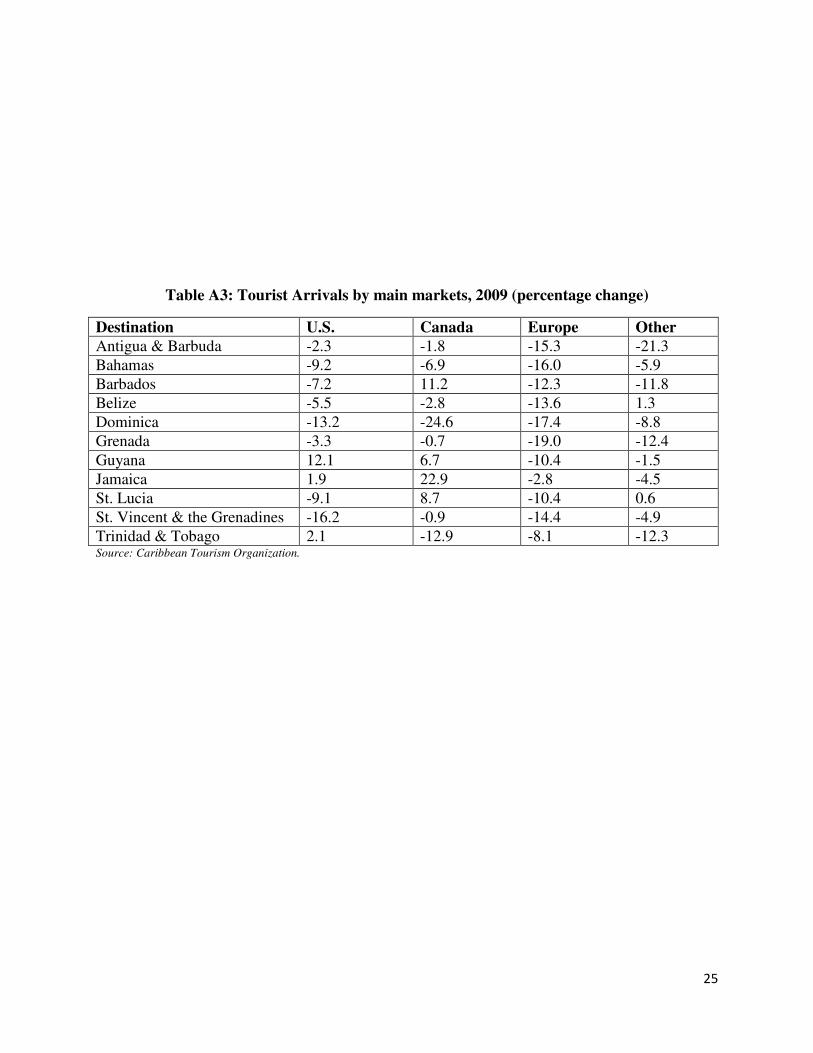

of Jamaica (Table A2 in the appendix). European arrivals took the biggest fall followed by the

US and Canada (Table A3 in the appendix). The tourism-dependent CARICOM economies have

been more painfully affected by the IFC. These economies are smaller and more vulnerable to

external shocks. The smaller CARICOM territories are highly dependent on tourism. Tourist

arrivals to the region will remain depressed as unemployment in the US, EU and Canada remains

high. The IMF calculates that a 3 percentage point increase in US unemployment corresponds

approximately to an average 10 per cent decline in Caribbean tourism (IMF’s WEO Report April

2010). The increased taxes implemented in advanced economies to offset public deficits also

pose challenges. Tourism receipts were less affected but are expected to fall in 2010 because of

the lags involved (UNWTO April 2010). Tourism demand is expected to remain dampened for

longer as world unemployment continues to be high.

Figure 5: World growth (%) in tourist arrivals, 2005-2009

Source: UNWTO World Tourism Barometer, 2007, 2008, 2009.

-8

-6

-4

-2

0

2

4

6

8

2005 2006 2007 2008 2009

10

3.2. International Private Capital Flows

The flow of capital like trade was severely affected by the IFC impacting the capital account of

the balance of payment. Prior to the IFC net foreign private capital flows especially to

developing countries had surged stimulating growth in these economies. However, the onset of

the crisis has led to sudden stops and even reversals of these flows.

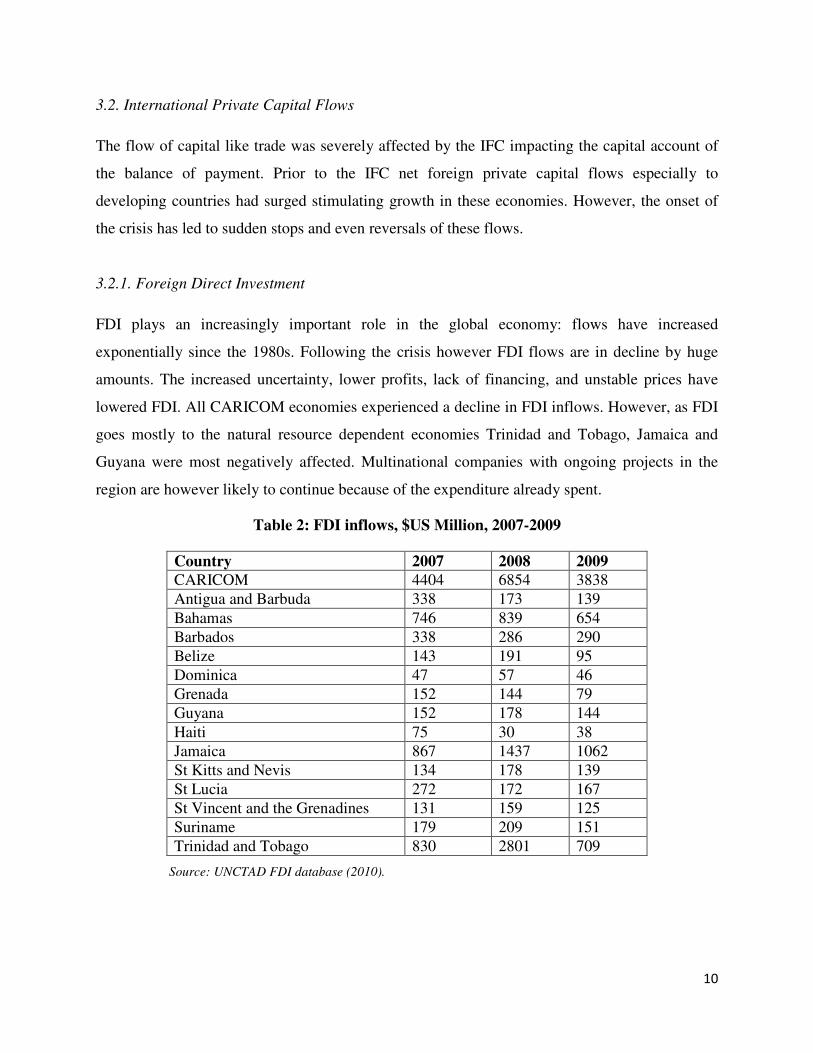

3.2.1. Foreign Direct Investment

FDI plays an increasingly important role in the global economy: flows have increased

exponentially since the 1980s. Following the crisis however FDI flows are in decline by huge

amounts. The increased uncertainty, lower profits, lack of financing, and unstable prices have

lowered FDI. All CARICOM economies experienced a decline in FDI inflows. However, as FDI

goes mostly to the natural resource dependent economies Trinidad and Tobago, Jamaica and

Guyana were most negatively affected. Multinational companies with ongoing projects in the

region are however likely to continue because of the expenditure already spent.

Table 2: FDI inflows, $US Million, 2007-2009

Country 2007 2008 2009 CARICOM 4404 6854 3838

Antigua and Barbuda 338 173 139

Bahamas 746 839 654

Barbados 338 286 290

Belize 143 191 95

Dominica 47 57 46

Grenada 152 144 79

Guyana 152 178 144

Haiti 75 30 38

Jamaica 867 1437 1062

St Kitts and Nevis 134 178 139

St Lucia 272 172 167

St Vincent and the Grenadines 131 159 125

Suriname 179 209 151

Trinidad and Tobago 830 2801 709

Source: UNCTAD FDI database (2010).

11

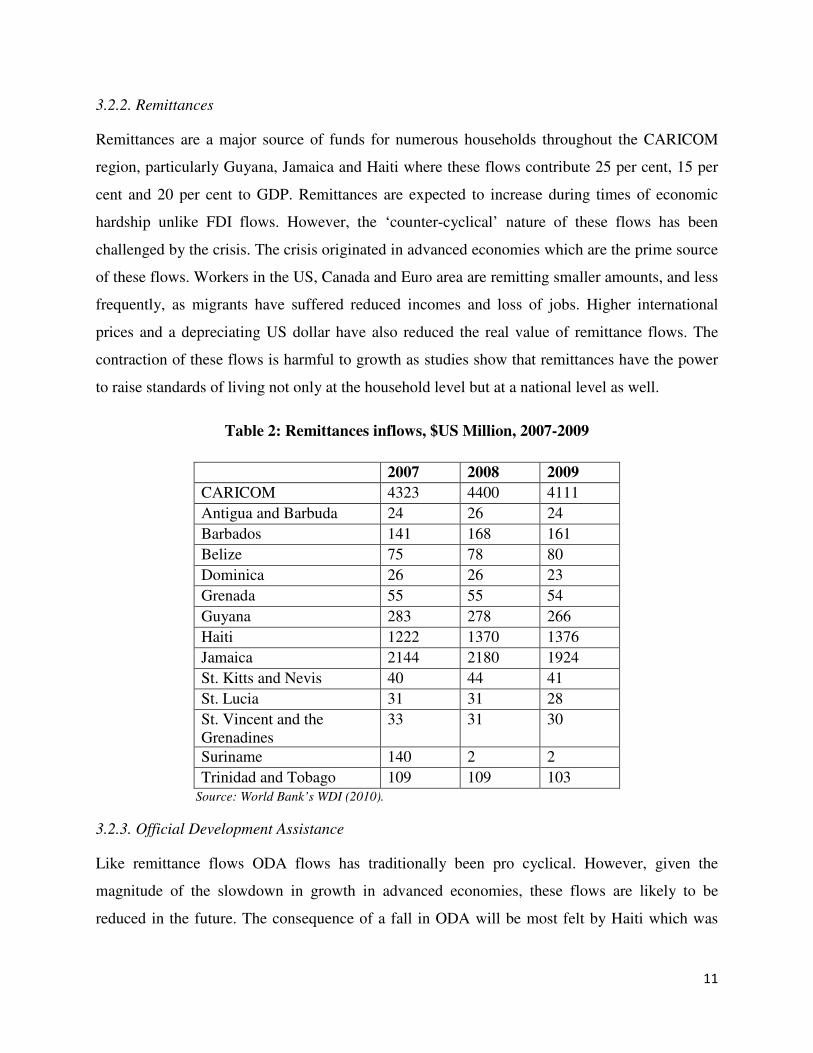

3.2.2. Remittances

Remittances are a major source of funds for numerous households throughout the CARICOM

region, particularly Guyana, Jamaica and Haiti where these flows contribute 25 per cent, 15 per

cent and 20 per cent to GDP. Remittances are expected to increase during times of economic

hardship unlike FDI flows. However, the ‘counter-cyclical’ nature of these flows has been

challenged by the crisis. The crisis originated in advanced economies which are the prime source

of these flows. Workers in the US, Canada and Euro area are remitting smaller amounts, and less

frequently, as migrants have suffered reduced incomes and loss of jobs. Higher international

prices and a depreciating US dollar have also reduced the real value of remittance flows. The

contraction of these flows is harmful to growth as studies show that remittances have the power

to raise standards of living not only at the household level but at a national level as well.

Table 2: Remittances inflows, $US Million, 2007-2009

2007 2008 2009

CARICOM 4323 4400 4111

Antigua and Barbuda 24 26 24

Barbados 141 168 161

Belize 75 78 80

Dominica 26 26 23

Grenada 55 55 54

Guyana 283 278 266

Haiti 1222 1370 1376

Jamaica 2144 2180 1924

St. Kitts and Nevis 40 44 41

St. Lucia 31 31 28

St. Vincent and the Grenadines

33 31 30

Suriname 140 2 2

Trinidad and Tobago 109 109 103 Source: World Bank’s WDI (2010).

3.2.3. Official Development Assistance

Like remittance flows ODA flows has traditionally been pro cyclical. However, given the

magnitude of the slowdown in growth in advanced economies, these flows are likely to be

reduced in the future. The consequence of a fall in ODA will be most felt by Haiti which was

12

endured a catastrophic earthquake in the beginning of 2010 and is most dependent CARICOM

nation on ODA. Table three provides information on ODA to CARICOM countries.

Table 3: Total Net bilateral aid flow from donor countries, $US Million, 2006-2008

2006 2007 2008

CARICOM 656 909 1084

Antigua and Barbuda 3 4 3

Barbados -1 13 4

Belize 7 13 17

Dominica 15 18 19

Grenada 8 6 11

Guyana 64 57 95

Haiti 446 532 674

Jamaica 32 23 70

St. Kitts and Nevis 6 5 43

St. Lucia 2 12 15

St. Vincent and the Grenadines

4 62 23

Suriname 58 146 99

Trinidad and Tobago 11 180 116 Source: World Bank’s WDI (2010).

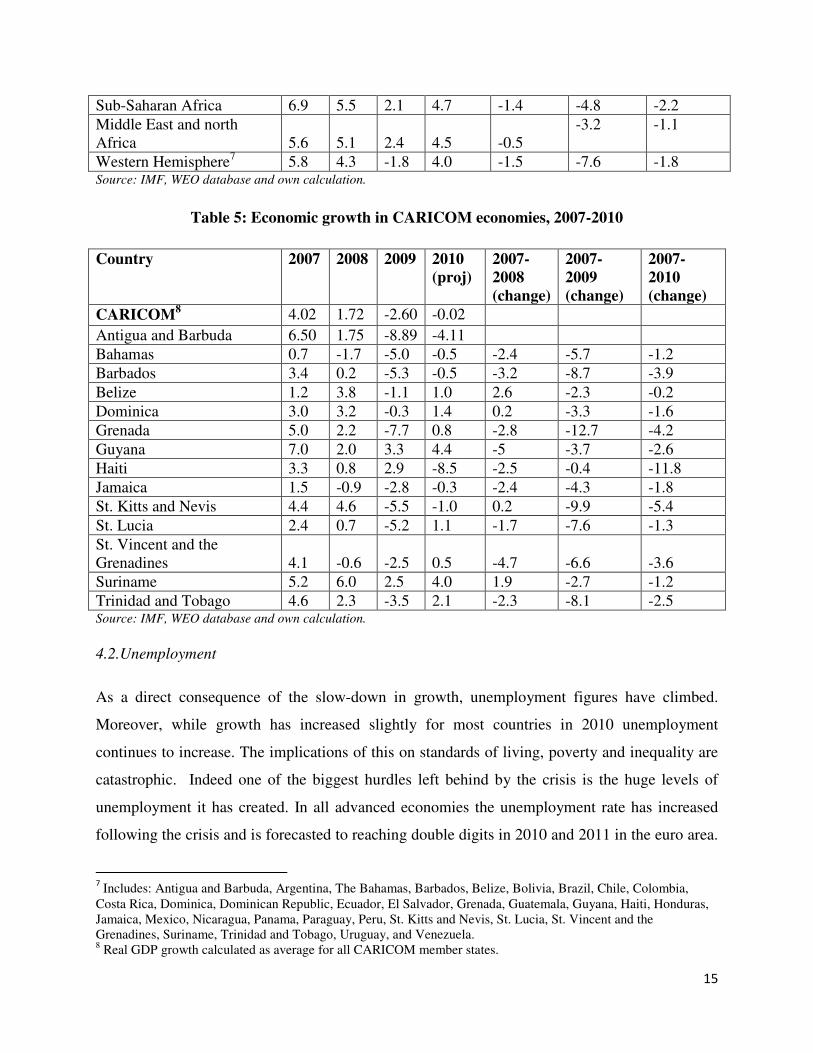

4. The Impact of the IFC on the CARICOM Macroeconomy

4.1. Impact of the crisis on economic growth

Most countries of the world experienced a slowdown in growth following the crisis. The change

in the rate of growth is calculated for country groupings (Table 4) and individual CARICOM

economies (Table 5) for 2007 to 2010 using the IMF’s WEO Report (October 2010). The change

is computed by taking the absolute difference in the value of the real GDP growth rates between

2007 and 2010. This method avoids calculating large declines in growth for countries that had

low growth rates prior to the crisis in 2007 (Goldstein and Xie 2009).

The downturn was severe and global in nature as all country groupings were negatively affected

in 2008, 2009 and 2010 (estimate) subsequent to the crisis (table 4). The full impact of the crisis

occurred in 2009 which recorded the largest decline in growth. World real GDP growth declined

from 5.2 per cent in 2007 to negative 0.6 per cent in 2009, a fall in the growth rate of 5.8 per

cent. The decline is expected to slow in 2010 with a growth rate of 4.2 per cent.

13

The growth of real GDP of advanced economies and emerging and developing economies in

2009 was negative 3.2 per cent and 2.4 per cent respectively. In the advanced economy grouping

the euro area was most negatively affected with negative growth of 4.1 per cent in 2009 followed

by Canada, the US and newly industrialized Asian economies. Looking at emerging and

developing economies, Central and eastern Europe were most negatively affected with a fall in

economic growth of 3.7 per cent followed by the Western Hemisphere, Sub-Saharan Africa, the

middle East and north Africa and developing Asia. This demonstrates that the decline developing

economies has been larger than advanced economies but these economies have been recovering

steadily. This is reasonable given that, prior to the crisis, emerging and developing economies

were experiencing more robust growth. The recovery of advanced economies has been sluggish.

Developing Asia has been most successful at riding out the crisis. The IMF World Economic

Outlook Report (April 2010) forecast positive growth for all regions in 2010.

The IMF does not give real GDP growth for a CARICOM grouping, but the average growth rate

of all CARICOM members was calculated. The region experienced a decline in average growth

of negative 6.7 per cent and negative 2 per cent from 2007 to 2009 and 2007 to 2010, a fall in the

growth rate of 11 per cent and 6.3 per cent. In comparing CARICOM’s real GD growth with the

major country groupings, the region has had higher growth than advanced economies but lower

than emerging and developing economies and the world economy. CARICOM has had better

growth than the euro area and comparable growth to the US and Canada but lower than newly

industrialized Asia. In the emerging and developing economies category the region has only

performed better than central and eastern Europe. Hence, CARICOM’s performance through the

crisis is expected to be better than that of advanced economies but lagging behind all other

developing regions.

Examining individual CARICOM countries, economic growth was negatively affected in all

territories. All countries had positive growth prior to the crisis. Though, historically, all

CARICOM economies have faced greater declines in growth, the fall in growth initiated by the

crisis is noteworthy as it occurred concurrently across all countries. Tourism-dependent

economies were most negatively affected experiencing colossal contractions in growth between

5 to 12.7 per cent over the period 2007 to 2009. Three of these countries entered a recession in

2008-2009: The Bahamas, Barbados and Jamaica (Caribbean Economic Performance Report

14

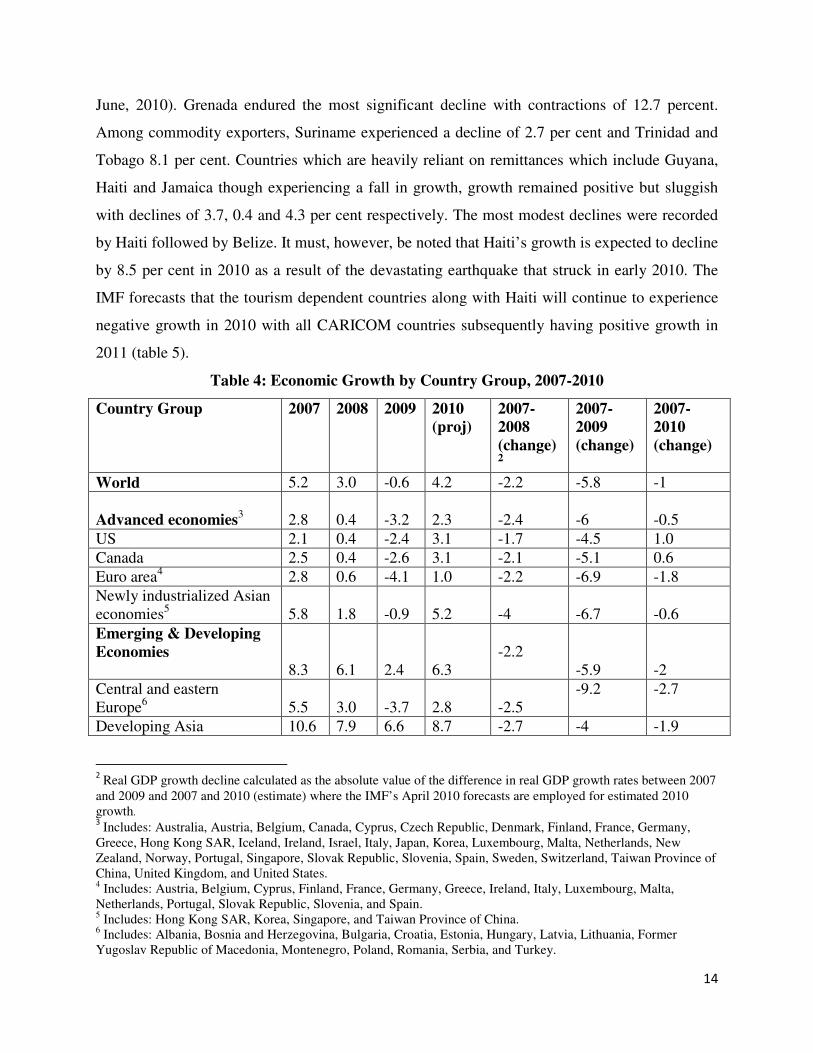

June, 2010). Grenada endured the most significant decline with contractions of 12.7 percent.

Among commodity exporters, Suriname experienced a decline of 2.7 per cent and Trinidad and

Tobago 8.1 per cent. Countries which are heavily reliant on remittances which include Guyana,

Haiti and Jamaica though experiencing a fall in growth, growth remained positive but sluggish

with declines of 3.7, 0.4 and 4.3 per cent respectively. The most modest declines were recorded

by Haiti followed by Belize. It must, however, be noted that Haiti’s growth is expected to decline

by 8.5 per cent in 2010 as a result of the devastating earthquake that struck in early 2010. The

IMF forecasts that the tourism dependent countries along with Haiti will continue to experience

negative growth in 2010 with all CARICOM countries subsequently having positive growth in

2011 (table 5).

Table 4: Economic Growth by Country Group, 2007-2010

Country Group 2007 2008 2009 2010 (proj)

2007-2008 (change)2

2007-2009 (change)

2007- 2010 (change)

World 5.2 3.0 -0.6 4.2 -2.2 -5.8 -1

Advanced economies3 2.8 0.4 -3.2 2.3

-2.4

-6

-0.5

US 2.1 0.4 -2.4 3.1 -1.7 -4.5 1.0

Canada 2.5 0.4 -2.6 3.1 -2.1 -5.1 0.6

Euro area4 2.8 0.6 -4.1 1.0 -2.2 -6.9 -1.8

Newly industrialized Asian

economies5 5.8 1.8 -0.9 5.2 -4

-6.7

-0.6

Emerging & Developing Economies

8.3 6.1 2.4 6.3

-2.2

-5.9

-2

Central and eastern Europe6 5.5 3.0 -3.7 2.8

-2.5

-9.2 -2.7

Developing Asia 10.6 7.9 6.6 8.7 -2.7 -4 -1.9

2 Real GDP growth decline calculated as the absolute value of the difference in real GDP growth rates between 2007

and 2009 and 2007 and 2010 (estimate) where the IMF’s April 2010 forecasts are employed for estimated 2010 growth. 3 Includes: Australia, Austria, Belgium, Canada, Cyprus, Czech Republic, Denmark, Finland, France, Germany,

Greece, Hong Kong SAR, Iceland, Ireland, Israel, Italy, Japan, Korea, Luxembourg, Malta, Netherlands, New Zealand, Norway, Portugal, Singapore, Slovak Republic, Slovenia, Spain, Sweden, Switzerland, Taiwan Province of China, United Kingdom, and United States. 4 Includes: Austria, Belgium, Cyprus, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, Malta, Netherlands, Portugal, Slovak Republic, Slovenia, and Spain. 5 Includes: Hong Kong SAR, Korea, Singapore, and Taiwan Province of China. 6 Includes: Albania, Bosnia and Herzegovina, Bulgaria, Croatia, Estonia, Hungary, Latvia, Lithuania, Former Yugoslav Republic of Macedonia, Montenegro, Poland, Romania, Serbia, and Turkey.

15

Sub-Saharan Africa 6.9 5.5 2.1 4.7 -1.4 -4.8 -2.2

Middle East and north Africa 5.6 5.1 2.4 4.5

-0.5

-3.2 -1.1

Western Hemisphere7 5.8 4.3 -1.8 4.0 -1.5 -7.6 -1.8 Source: IMF, WEO database and own calculation.

Table 5: Economic growth in CARICOM economies, 2007-2010

Country 2007 2008 2009 2010 (proj)

2007-2008 (change)

2007-2009 (change)

2007- 2010 (change)

CARICOM8 4.02 1.72 -2.60 -0.02

Antigua and Barbuda 6.50 1.75 -8.89 -4.11

Bahamas 0.7 -1.7 -5.0 -0.5 -2.4 -5.7 -1.2

Barbados 3.4 0.2 -5.3 -0.5 -3.2 -8.7 -3.9

Belize 1.2 3.8 -1.1 1.0 2.6 -2.3 -0.2

Dominica 3.0 3.2 -0.3 1.4 0.2 -3.3 -1.6

Grenada 5.0 2.2 -7.7 0.8 -2.8 -12.7 -4.2

Guyana 7.0 2.0 3.3 4.4 -5 -3.7 -2.6

Haiti 3.3 0.8 2.9 -8.5 -2.5 -0.4 -11.8

Jamaica 1.5 -0.9 -2.8 -0.3 -2.4 -4.3 -1.8

St. Kitts and Nevis 4.4 4.6 -5.5 -1.0 0.2 -9.9 -5.4

St. Lucia 2.4 0.7 -5.2 1.1 -1.7 -7.6 -1.3

St. Vincent and the Grenadines

4.1

-0.6

-2.5

0.5

-4.7

-6.6

-3.6

Suriname 5.2 6.0 2.5 4.0 1.9 -2.7 -1.2

Trinidad and Tobago 4.6 2.3 -3.5 2.1 -2.3 -8.1 -2.5 Source: IMF, WEO database and own calculation.

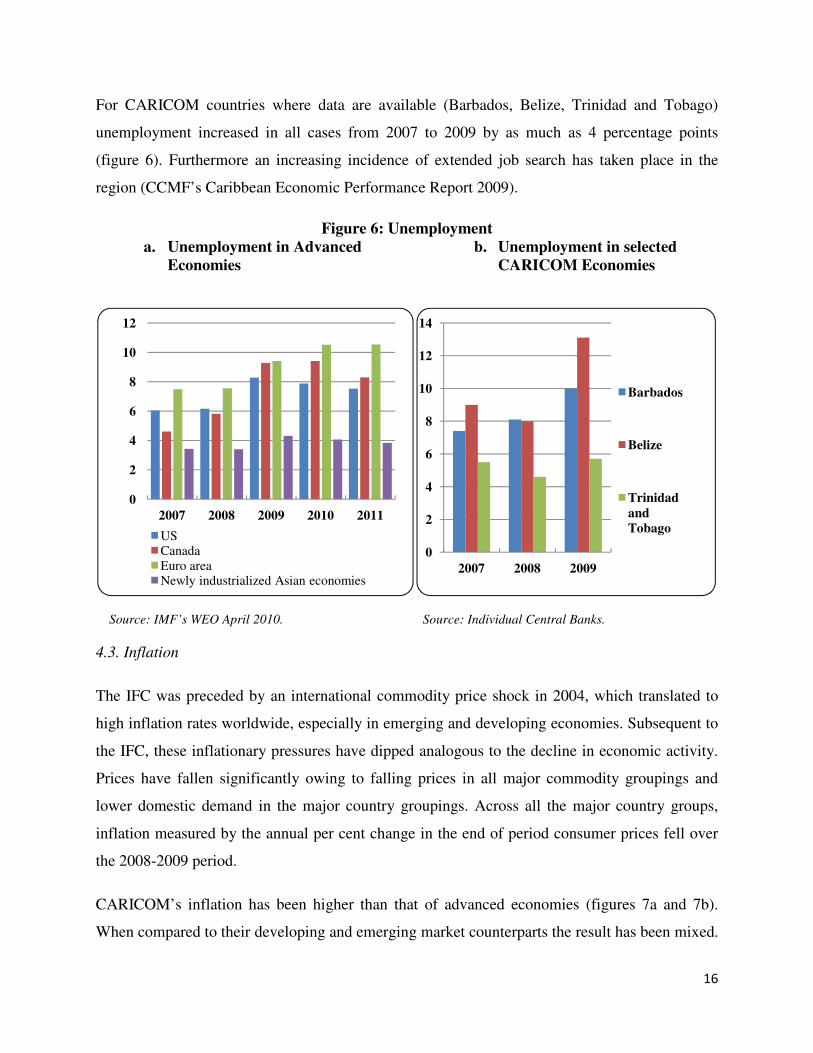

4.2.Unemployment

As a direct consequence of the slow-down in growth, unemployment figures have climbed.

Moreover, while growth has increased slightly for most countries in 2010 unemployment

continues to increase. The implications of this on standards of living, poverty and inequality are

catastrophic. Indeed one of the biggest hurdles left behind by the crisis is the huge levels of

unemployment it has created. In all advanced economies the unemployment rate has increased

following the crisis and is forecasted to reaching double digits in 2010 and 2011 in the euro area.

7 Includes: Antigua and Barbuda, Argentina, The Bahamas, Barbados, Belize, Bolivia, Brazil, Chile, Colombia,

Costa Rica, Dominica, Dominican Republic, Ecuador, El Salvador, Grenada, Guatemala, Guyana, Haiti, Honduras, Jamaica, Mexico, Nicaragua, Panama, Paraguay, Peru, St. Kitts and Nevis, St. Lucia, St. Vincent and the Grenadines, Suriname, Trinidad and Tobago, Uruguay, and Venezuela. 8 Real GDP growth calculated as average for all CARICOM member states.

16

For CARICOM countries where data are available (Barbados, Belize, Trinidad and Tobago)

unemployment increased in all cases from 2007 to 2009 by as much as 4 percentage points

(figure 6). Furthermore an increasing incidence of extended job search has taken place in the

region (CCMF’s Caribbean Economic Performance Report 2009).

Figure 6: Unemployment a. Unemployment in Advanced

Economies b. Unemployment in selected

CARICOM Economies

Source: IMF’s WEO April 2010. Source: Individual Central Banks.

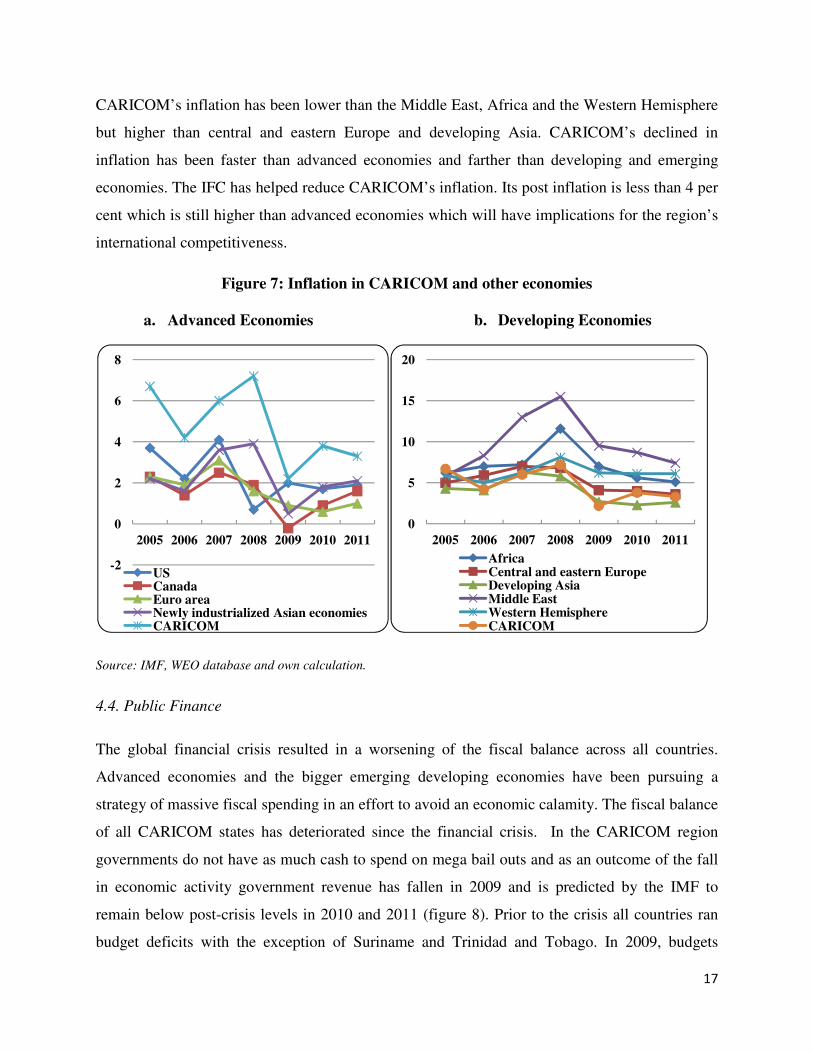

4.3. Inflation

The IFC was preceded by an international commodity price shock in 2004, which translated to

high inflation rates worldwide, especially in emerging and developing economies. Subsequent to

the IFC, these inflationary pressures have dipped analogous to the decline in economic activity.

Prices have fallen significantly owing to falling prices in all major commodity groupings and

lower domestic demand in the major country groupings. Across all the major country groups,

inflation measured by the annual per cent change in the end of period consumer prices fell over

the 2008-2009 period.

CARICOM’s inflation has been higher than that of advanced economies (figures 7a and 7b).

When compared to their developing and emerging market counterparts the result has been mixed.

0

2

4

6

8

10

12

2007 2008 2009 2010 2011

USCanadaEuro area Newly industrialized Asian economies

0

2

4

6

8

10

12

14

2007 2008 2009

Barbados

Belize

Trinidad and Tobago

17

CARICOM’s inflation has been lower than the Middle East, Africa and the Western Hemisphere

but higher than central and eastern Europe and developing Asia. CARICOM’s declined in

inflation has been faster than advanced economies and farther than developing and emerging

economies. The IFC has helped reduce CARICOM’s inflation. Its post inflation is less than 4 per

cent which is still higher than advanced economies which will have implications for the region’s

international competitiveness.

Figure 7: Inflation in CARICOM and other economies

a. Advanced Economies b. Developing Economies

Source: IMF, WEO database and own calculation.

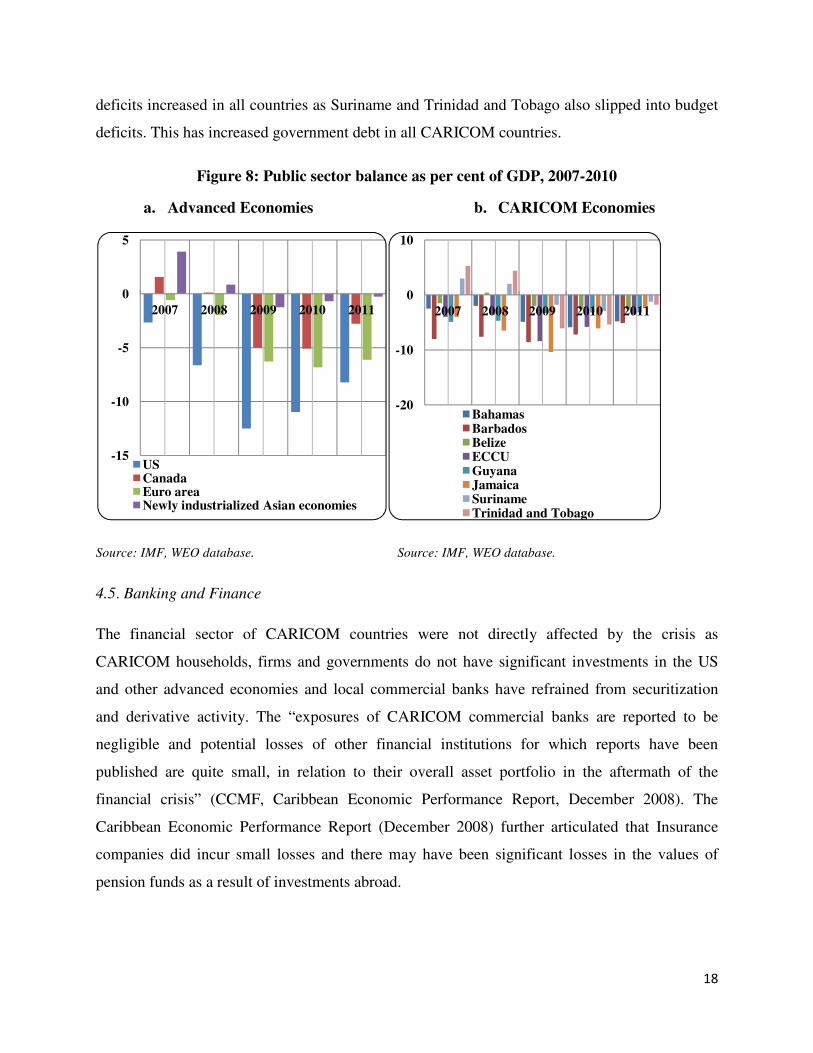

4.4. Public Finance

The global financial crisis resulted in a worsening of the fiscal balance across all countries.

Advanced economies and the bigger emerging developing economies have been pursuing a

strategy of massive fiscal spending in an effort to avoid an economic calamity. The fiscal balance

of all CARICOM states has deteriorated since the financial crisis. In the CARICOM region

governments do not have as much cash to spend on mega bail outs and as an outcome of the fall

in economic activity government revenue has fallen in 2009 and is predicted by the IMF to

remain below post-crisis levels in 2010 and 2011 (figure 8). Prior to the crisis all countries ran

budget deficits with the exception of Suriname and Trinidad and Tobago. In 2009, budgets

-2

0

2

4

6

8

2005 2006 2007 2008 2009 2010 2011

USCanadaEuro area Newly industrialized Asian economiesCARICOM

0

5

10

15

20

2005 2006 2007 2008 2009 2010 2011

AfricaCentral and eastern EuropeDeveloping AsiaMiddle EastWestern HemisphereCARICOM

18

deficits increased in all countries as Suriname and Trinidad and Tobago also slipped into budget

deficits. This has increased government debt in all CARICOM countries.

Figure 8: Public sector balance as per cent of GDP, 2007-2010

a. Advanced Economies b. CARICOM Economies

Source: IMF, WEO database. Source: IMF, WEO database.

4.5. Banking and Finance

The financial sector of CARICOM countries were not directly affected by the crisis as

CARICOM households, firms and governments do not have significant investments in the US

and other advanced economies and local commercial banks have refrained from securitization

and derivative activity. The “exposures of CARICOM commercial banks are reported to be

negligible and potential losses of other financial institutions for which reports have been

published are quite small, in relation to their overall asset portfolio in the aftermath of the

financial crisis” (CCMF, Caribbean Economic Performance Report, December 2008). The

Caribbean Economic Performance Report (December 2008) further articulated that Insurance

companies did incur small losses and there may have been significant losses in the values of

pension funds as a result of investments abroad.

-15

-10

-5

0

5

2007 2008 2009 2010 2011

USCanadaEuro area Newly industrialized Asian economies

-20

-10

0

10

2007 2008 2009 2010 2011

BahamasBarbadosBelizeECCUGuyanaJamaicaSurinameTrinidad and Tobago

19

The falling output, as well as a decline in employment, government revenue, FDI and foreign

portfolio investment and increased pressures on the exchange rates have impacted on the

financial sector of CARICOM countries. The main risk facing the financial systems in the region

is credit risk stemming from depressed economic conditions. There has also been increased risk

aversion which had led to slower credit, falling financial asset prices and lower interest rates

(CCMF, Caribbean Economic Performance Report, December 2009). The January 2009 collapse

of the Trinidad and Tobago based CL Financial Group and the collapse of the Stanford Financial

Group in Antigua and Barbuda have compounded the increased risk aversion. Both experiences

point to the need to improve regional regulation and cross-border cooperation. The fiscal expense

of dealing with these collapses is still indeterminate. Higher exposure and high debt levels in

several countries in the rest of the Caribbean pose significant challenges in dealing with the

problems created by the CL’s insurance subsidiaries, the Colonial Life Insurance Company

(CLICO) and the British American Insurance Company (BAICO).

In addition, the crisis has brought with it an increase in regulation costs for CARICOM countries

with Offshore Financial Centers. These countries are required to comply with increasingly

tighter international standards (spearheaded by the G20) in fiscal/tax and financial regulatory

areas (IMF, World Economic Outlook, 2010). This represents an additional cost and applies

mainly to the eastern Caribbean countries which have already had significant reductions in

growth from lower tourism demand.

4.6. External Accounts

CARICOM economies recorded a widespread deterioration in their external accounts. Preceding

the crisis all countries apart from Suriname and Trinidad and Tobago had current account deficits

(table A5). Following the crisis these deficits have grown in size with Suriname also slipping

into a deficit. Trinidad and Tobago retained its surplus despite the fact that it dwindled. This has

contributed to higher debt levels. Foreign Direct Investment (FDI), portfolio investment and

reserves have also been negatively affected. The global recession largely manifested itself in

terms of a collapse in commodity prices and a fall in tourism demand in most countries. The fall

in non agriculture commodity prices was more severe than the fall out in agriculture prices

(figure). Regional exports struggled in 2009, as exports declined in most territories, except for

20

the ECCU where it actually increased by 4.1 per cent for the year largely on account of its

performances in the first and second quarter. The most dramatic declines in exports were

registered by Guyana where they fell by 66.4 per cent and in Trinidad and Tobago where exports

halved (50.6 per cent).

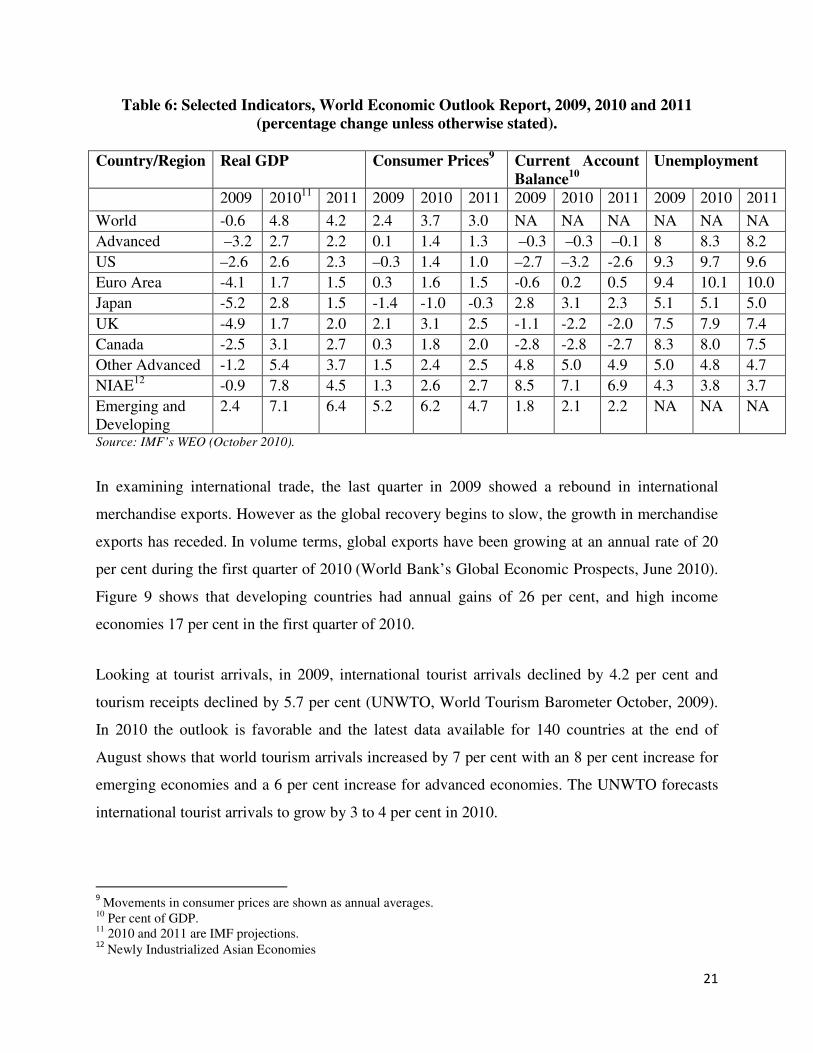

5. The Global Outlook

While there has been some recovery from the crisis in 2010 significant uncertainties prevail. The

main economic indicators for major country groupings from the IMF’s WEO Report (October

2010) are summarized in table 6. From the table global economic activity is forecasted to grow

by 4.8 per cent in 2010 and 4.2 per cent in 2011. For advanced economies growth is projected at

2.7 and 2.2 per cent, respectively with Euro area slowing considerably more and for emerging.

Growth for the newly Industrialized Asian economies will slow by almost half in 2011 compared

to 2010. Developing economies, growth will expand at rates of 7.1 and 6.4 per cent, in 2010 and

2011 respectively. Unemployment is expected to remain persistently high. Current account

imbalances between advanced and emerging and developing economies are predicted to persist.

Inflation is projected to remain low generally with slightly higher rates in the emerging and

developing economies.

The report further states the downside risk remains and recovery rests on two rebalancing acts,

fiscal consolidation and current account imbalances. Furthermore, the global financial system is

yet to recover and there exists considerable uncertainty as significant sovereign and banking

vulnerabilities exist. These balance sheets are highly vulnerable to growth shocks, making debt

sustainability less certain, prices in stock exchanges have fallen and the risk premiums on

corporate bonds have widened, and corporate bond issues have slowed (Global Financial

Stability Report October 2010). As the recovery progresses the momentum gained from fiscal

stimulus is slowing and growth must now be determined by private investment and household

consumption.

21

Table 6: Selected Indicators, World Economic Outlook Report, 2009, 2010 and 2011 (percentage change unless otherwise stated).

Country/Region Real GDP Consumer Prices9 Current Account

Balance10 Unemployment

2009 201011 2011 2009 2010 2011 2009 2010 2011 2009 2010 2011

World -0.6 4.8 4.2 2.4 3.7 3.0 NA NA NA NA NA NA

Advanced –3.2 2.7 2.2 0.1 1.4 1.3 –0.3 –0.3 –0.1 8 8.3 8.2

US –2.6 2.6 2.3 –0.3 1.4 1.0 –2.7 –3.2 -2.6 9.3 9.7 9.6

Euro Area -4.1 1.7 1.5 0.3 1.6 1.5 -0.6 0.2 0.5 9.4 10.1 10.0

Japan -5.2 2.8 1.5 -1.4 -1.0 -0.3 2.8 3.1 2.3 5.1 5.1 5.0

UK -4.9 1.7 2.0 2.1 3.1 2.5 -1.1 -2.2 -2.0 7.5 7.9 7.4

Canada -2.5 3.1 2.7 0.3 1.8 2.0 -2.8 -2.8 -2.7 8.3 8.0 7.5

Other Advanced -1.2 5.4 3.7 1.5 2.4 2.5 4.8 5.0 4.9 5.0 4.8 4.7

NIAE12 -0.9 7.8 4.5 1.3 2.6 2.7 8.5 7.1 6.9 4.3 3.8 3.7

Emerging and Developing

2.4 7.1 6.4 5.2 6.2 4.7 1.8 2.1 2.2 NA NA NA

Source: IMF’s WEO (October 2010).

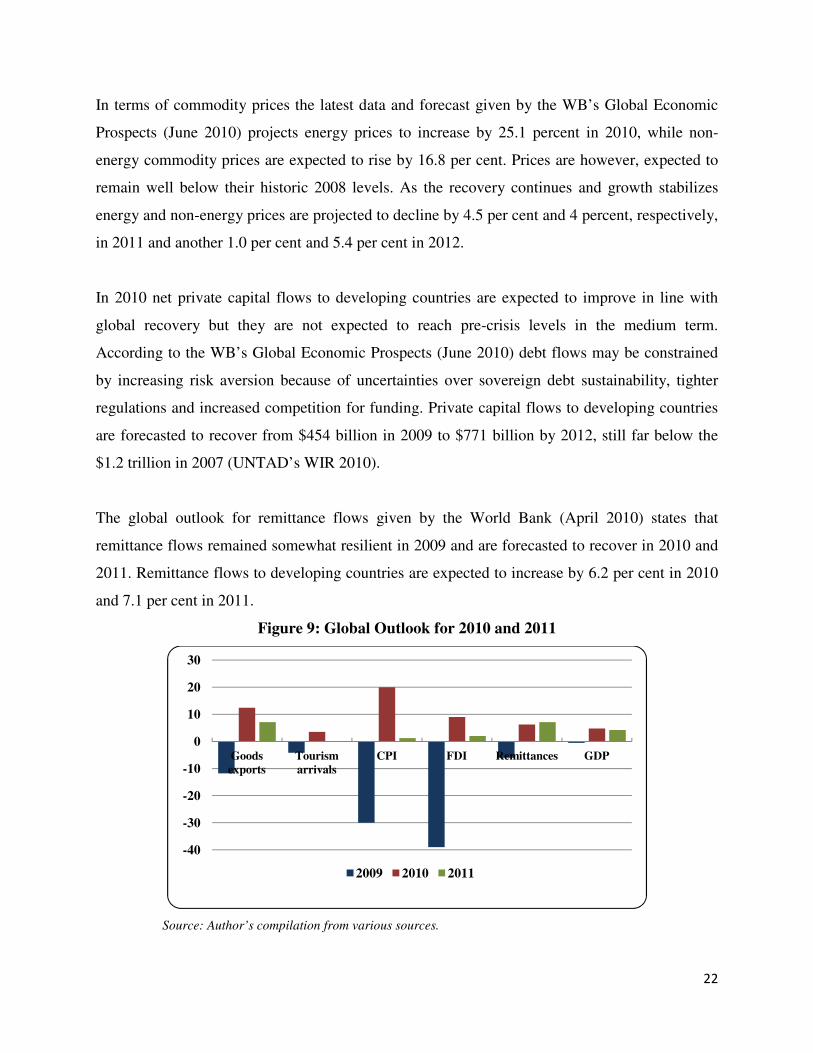

In examining international trade, the last quarter in 2009 showed a rebound in international

merchandise exports. However as the global recovery begins to slow, the growth in merchandise

exports has receded. In volume terms, global exports have been growing at an annual rate of 20

per cent during the first quarter of 2010 (World Bank’s Global Economic Prospects, June 2010).

Figure 9 shows that developing countries had annual gains of 26 per cent, and high income

economies 17 per cent in the first quarter of 2010.

Looking at tourist arrivals, in 2009, international tourist arrivals declined by 4.2 per cent and

tourism receipts declined by 5.7 per cent (UNWTO, World Tourism Barometer October, 2009).

In 2010 the outlook is favorable and the latest data available for 140 countries at the end of

August shows that world tourism arrivals increased by 7 per cent with an 8 per cent increase for

emerging economies and a 6 per cent increase for advanced economies. The UNWTO forecasts

international tourist arrivals to grow by 3 to 4 per cent in 2010.

9 Movements in consumer prices are shown as annual averages.

10 Per cent of GDP. 11 2010 and 2011 are IMF projections. 12

Newly Industrialized Asian Economies

22

In terms of commodity prices the latest data and forecast given by the WB’s Global Economic

Prospects (June 2010) projects energy prices to increase by 25.1 percent in 2010, while non-

energy commodity prices are expected to rise by 16.8 per cent. Prices are however, expected to

remain well below their historic 2008 levels. As the recovery continues and growth stabilizes

energy and non-energy prices are projected to decline by 4.5 per cent and 4 percent, respectively,

in 2011 and another 1.0 per cent and 5.4 per cent in 2012.

In 2010 net private capital flows to developing countries are expected to improve in line with

global recovery but they are not expected to reach pre-crisis levels in the medium term.

According to the WB’s Global Economic Prospects (June 2010) debt flows may be constrained

by increasing risk aversion because of uncertainties over sovereign debt sustainability, tighter

regulations and increased competition for funding. Private capital flows to developing countries

are forecasted to recover from $454 billion in 2009 to $771 billion by 2012, still far below the

$1.2 trillion in 2007 (UNTAD’s WIR 2010).

The global outlook for remittance flows given by the World Bank (April 2010) states that

remittance flows remained somewhat resilient in 2009 and are forecasted to recover in 2010 and

2011. Remittance flows to developing countries are expected to increase by 6.2 per cent in 2010

and 7.1 per cent in 2011.

Figure 9: Global Outlook for 2010 and 2011

Source: Author’s compilation from various sources.

-40

-30

-20

-10

0

10

20

30

Goods exports

Tourism arrivals

CPI FDI Remittances GDP

2009 2010 2011

23

6. Conclusion

The IFC has negatively affected international trade and financial flows of CARICOM countries

resulting in a fall in economic growth. International financial flows have been more severely

affected particularly ODA followed by FDI. Remittances have been less negatively affected

though there was a decrease. In terms of international trade exports of goods and services were

more negatively affected than imports. However, merchandise exports fell more than services

exports which includes primarily tourism. Nevertheless, when looking at the impact of the crisis

on growth tourism dependent were most negatively impacted followed by remittance dependent

economies and least negatively impacted were economies than export goods. Tourism dependent

economies face great uncertainties as their recovery rests solely on activity in the tourism sector.

The remittance dependent economies are also most dependent on ODA which has an unfavorable

outlook. The remaining economies which are export merchandisers face a gloomy outlook as the

recent spike in international commodity prices in 2010 are unlikely to continue into 2011.

Moreover, world exports are predicted to decease in 2011. The FDI outlook in 2011 is also likely

to fall as international firms wrap up ongoing investments.

References

Caribbean Centre for Money and Finance, 2009, Caribbean Economic Performance Report.

Inter-American Development Bank, 2009, Remittances in Times of Financial Instability

(Washington, March).

International Monetary Fund, 2010, World Economic Outlook Report (Washington, April).

24

Appendix

Table A1: Tourist (stop-over) arrivals, (percentage change)

Destination 2007 2008 2009 2010 (Sept) Antigua & Barbuda 3.2 1.5 -11.8 -1.7

Bahamas -4.6 -4.3 -9.3 3.2

Barbados 1.8 -0.9 -8.7 4.1

Belize 1.8 -2.6 -5.2 2.8

Dominica -8.8 2.6 -12.1 7.6

Grenada 9.0 -4.1 -12.5 -7.9

Guyana 15.9 1.0 6.2 7.1

Jamaica 1.3 3.9 3.6 4.1

St. Lucia -5.0 2.9 -5.8 14.3

St. Kitts & Nevis -7.4 -13.6

St. Vincent & Grenadines -8.0 -6.2 -10.3 -2.3

Suriname 5.5 -8.1

Trinidad & Tobago -1.7 -4.2 -5.5 -6.4 Source: Caribbean Tourism Organization

Table A2: Cruise Passenger Arrivals (percentage change)

Destination 2007 2008 2009 2010 (Sept) Antigua & Barbuda * 42.7 -13.7 22.7 -17.5

Bahamas -3.5 -3.7 13.8 14.4

Barbados p 14.3 -3.1 6.4 -2.0

Belize -4.8 -4.3 18.1 20.2

Dominica -6.6 30.7 37.8 3.8

Grenada p 23.6 8.3 16.1 -6.2

Jamaica -11.8 -7.7 -15.3 -12.1

St. Lucia 69.7 1.5 12.8 1.4

St. Kitts & Nevis 23

St. Vincent & Grenadines 35.8 -19.5 28.2 -30.5

Trinidad & Tobago -10.4 -42.6 145.8 -14.2 Source: Caribbean Tourism Organization.

25

Table A3: Tourist Arrivals by main markets, 2009 (percentage change)

Destination U.S. Canada Europe Other Antigua & Barbuda -2.3 -1.8 -15.3 -21.3

Bahamas -9.2 -6.9 -16.0 -5.9

Barbados -7.2 11.2 -12.3 -11.8

Belize -5.5 -2.8 -13.6 1.3

Dominica -13.2 -24.6 -17.4 -8.8

Grenada -3.3 -0.7 -19.0 -12.4

Guyana 12.1 6.7 -10.4 -1.5

Jamaica 1.9 22.9 -2.8 -4.5

St. Lucia -9.1 8.7 -10.4 0.6

St. Vincent & the Grenadines -16.2 -0.9 -14.4 -4.9

Trinidad & Tobago 2.1 -12.9 -8.1 -12.3 Source: Caribbean Tourism Organization.

Recommended