Sustainable Energy for All

Global Tracking Framework 2015

WORKSHOP ON Capacity Development for Mainstreaming Energy Sustainable Development Goals (SDGs), Targets and Indicators into Statistical Programmes in Selected Latin American Countries

Dr. Gabriela Elizondo Azuela, World Bank Panama City, Panama February 5th, 2015

Sustainable Energy for All (SE4ALL)

SE4ALL is a multi-stakeholder partnership between governments, private sector, and civil society, co-chaired by UN Secretary General and WB President.

By 2030, SE4ALL aims to:

Achieve universal access to modern energy services

Double the rate of improvement in energy efficiency

Double the share of renewable energy in the global energy mix

1 2 3

How can progress towards these objectives be tracked?

2

15

partners

2013

23

partners

2015

GTF: A growing Partnership

3

The launch of the first Global Tracking Framework 2013

was widely covered in the global press

4

Why 1.2 billion people still don’t have access to electricity (Washington Post Blog) Energy access (The Economist Blog) Five surprising facts about energy poverty (National Geographic) Step-up energy investments by >$600bn pa (The Economic Times of India) Global Tracking Framework puts numbers to Sustainable Energy Goals (All Africa) About 1.2 billion people lack access to electricity (Ghana Business News)

Bangladesh third most power starved country (Bangladesh News 24) Why wait for our grandchildren? (Gulf News) Energy gains burned by burgeoning population (Al Jazeera) Global energy poverty highlighted by report (The Environmental Blog) Energy transformation falling short (Renew Economy) Taking the long view on renewables growth (Power Engineering International)

Vienna Energy Forum sees launch of SE4ALL tracking framework (IISD) Governments face uphill struggle to hit UN energy goals (RTCC) High impact countries will have to double share of renewables (Greenwise) Renewables need global injection (Renewable Energy news)

What is the Global Tracking Framework

5

The GTF is an initial system for regular reporting based on indicators that are technically rigorous and feasible to compute from existing global data bases, and that offer scope for progressive improvement over time.

El Marco de Seguimiento Global propone un sistema para seguimiento periodico de los objectivos del SE4ALL basado en indicadores cuya medicion es factible via metodologias rigurosas, y que ademas ofrece una plataforma para el mejoramiento progresivo de este sistema

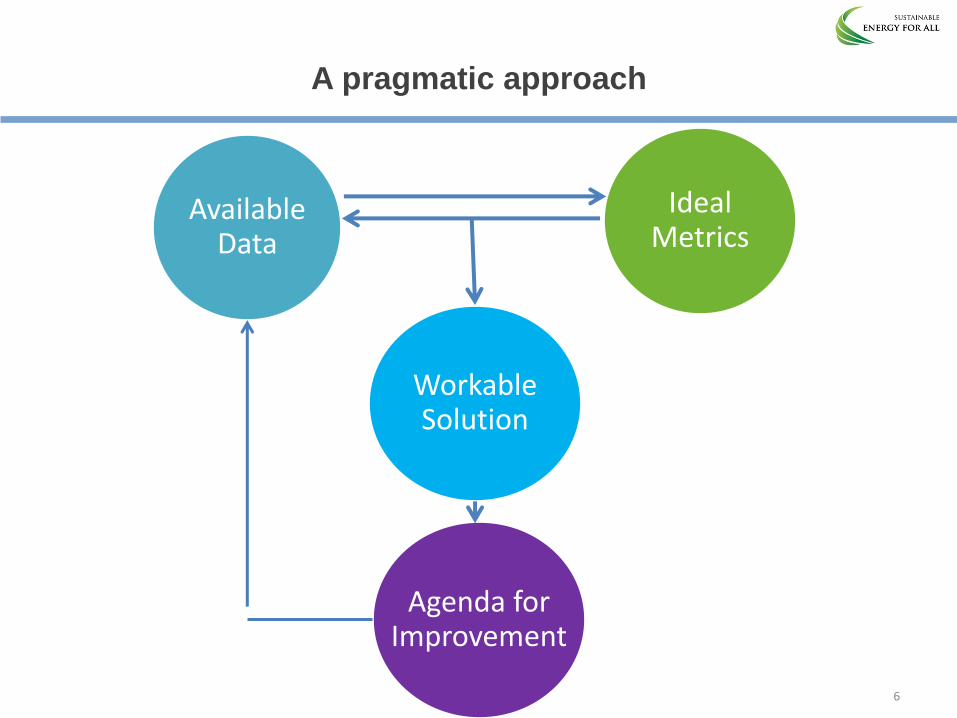

A pragmatic approach

6

Ideal Metrics

Workable Solution

Available Data

Agenda for Improvement

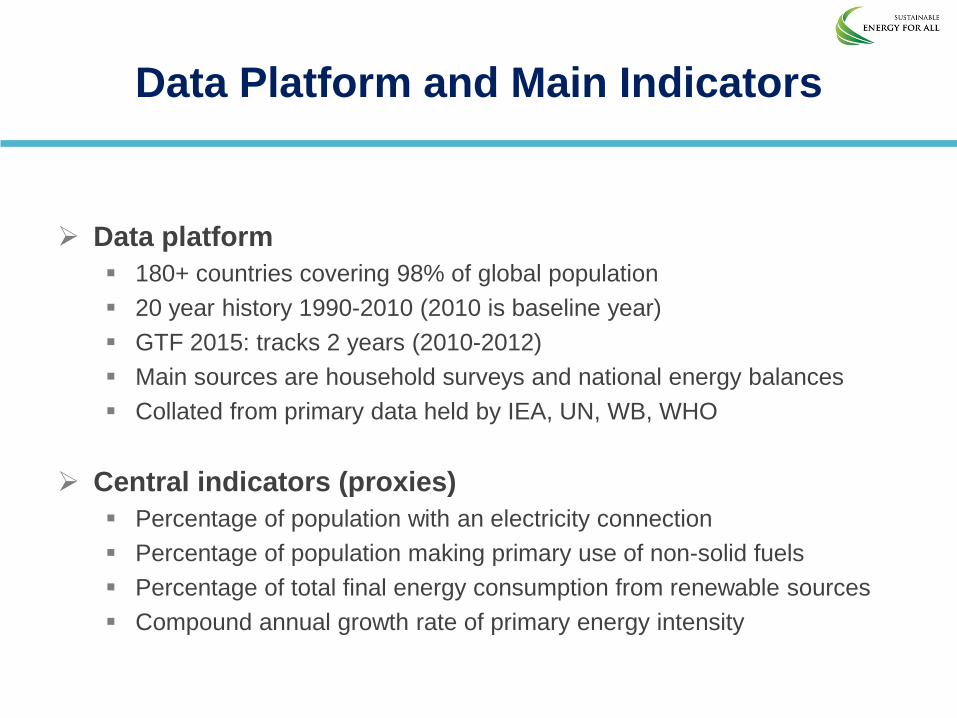

Data Platform and Main Indicators

Data platform

180+ countries covering 98% of global population

20 year history 1990-2010 (2010 is baseline year)

GTF 2015: tracks 2 years (2010-2012)

Main sources are household surveys and national energy balances

Collated from primary data held by IEA, UN, WB, WHO

Central indicators (proxies)

Percentage of population with an electricity connection

Percentage of population making primary use of non-solid fuels

Percentage of total final energy consumption from renewable sources

Compound annual growth rate of primary energy intensity

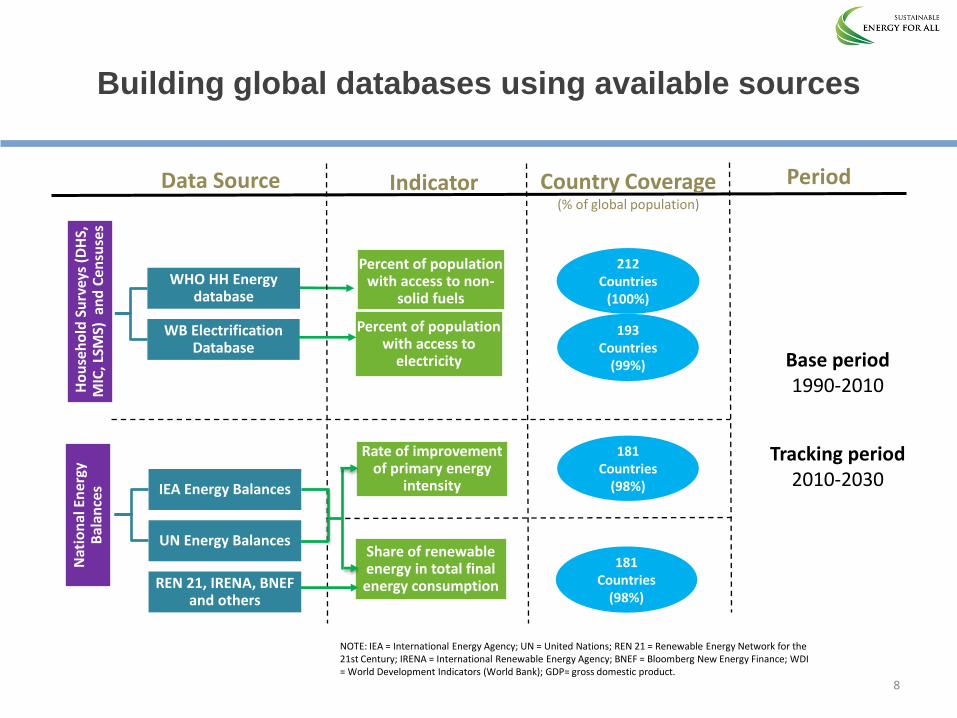

Building global databases using available sources H

ou

seh

old

Su

rvey

s (D

HS,

M

IC, L

SMS)

an

d C

en

suse

s

WHO HH Energy database

Percent of population with access to non-

solid fuels

WB Electrification Database

Nat

ion

al E

ner

gy

Bal

ance

s

Rate of improvement of primary energy

intensity IEA Energy Balances

UN Energy Balances

REN 21, IRENA, BNEF and others

Share of renewable energy in total final energy consumption

Indicator Data Source Country Coverage (% of global population)

212 Countries

(100%)

193 Countries

(99%)

181 Countries

(98%)

NOTE: IEA = International Energy Agency; UN = United Nations; REN 21 = Renewable Energy Network for the 21st Century; IRENA = International Renewable Energy Agency; BNEF = Bloomberg New Energy Finance; WDI = World Development Indicators (World Bank); GDP= gross domestic product.

181 Countries

(98%)

Period

Percent of population with access to

electricity Base period 1990-2010

Tracking period 2010-2030

8

ENERGY

ACCESS

9

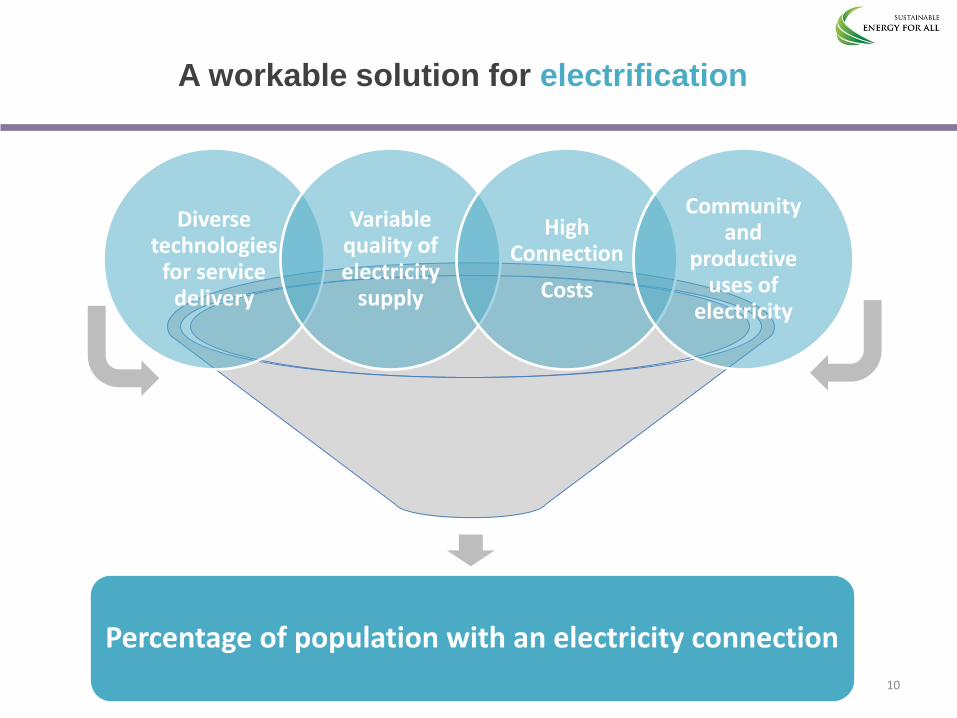

A workable solution for electrification

Diverse technologies

for service delivery

Variable quality of electricity

supply

High Connection

Costs

Community and

productive uses of

electricity

Percentage of population with an electricity connection

10

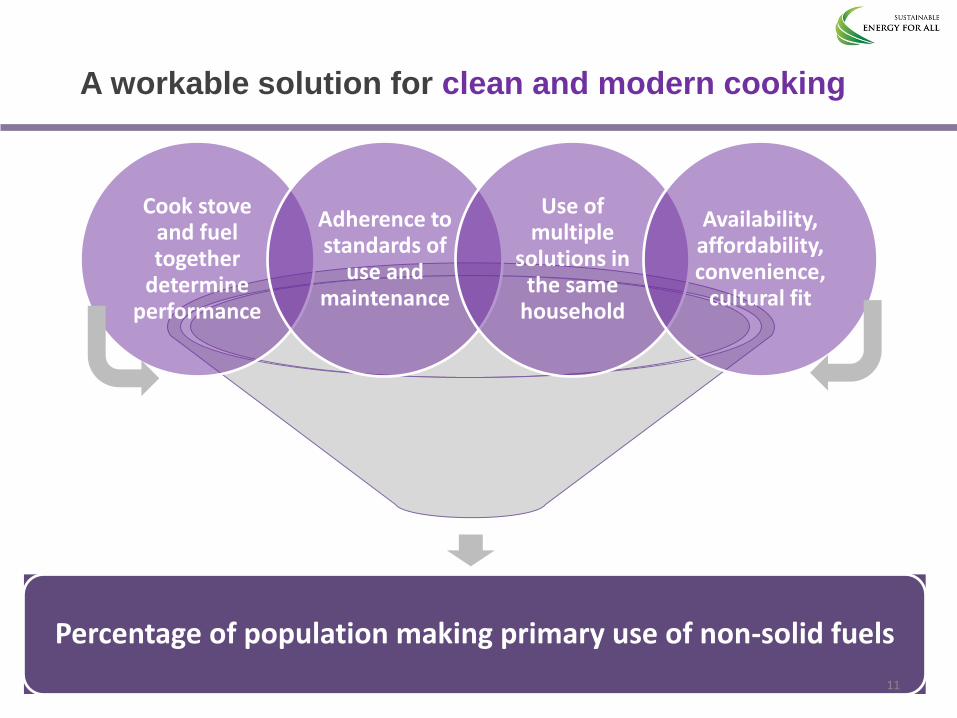

A workable solution for clean and modern cooking

Cook stove and fuel together

determine performance

Adherence to standards of

use and maintenance

Use of multiple

solutions in the same

household

Availability, affordability, convenience,

cultural fit

Percentage of population making primary use of non-solid fuels

11

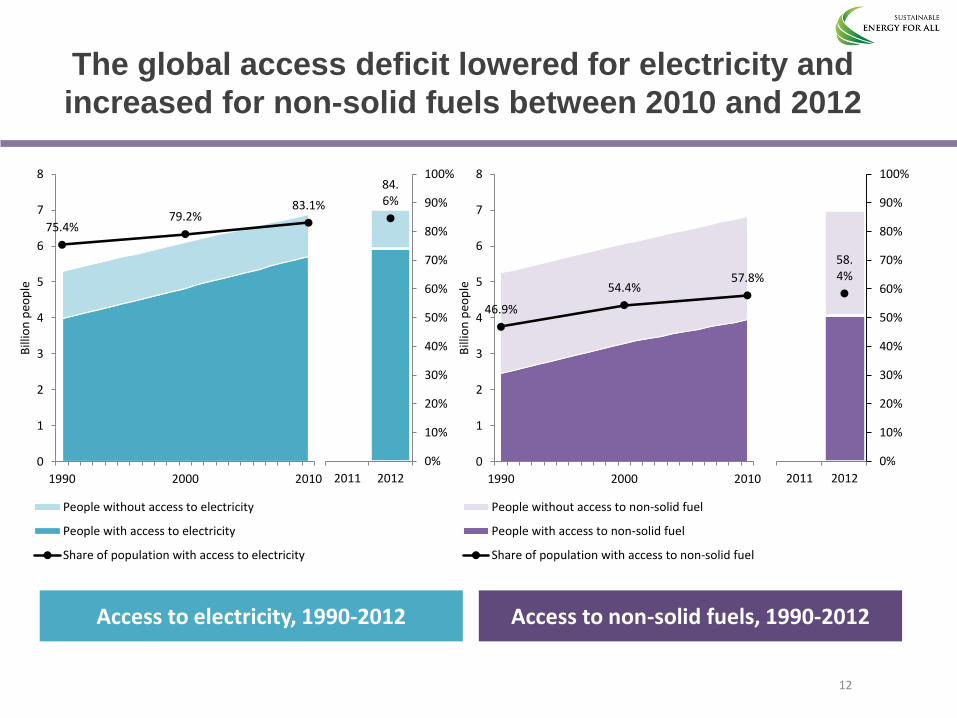

The global access deficit lowered for electricity and

increased for non-solid fuels between 2010 and 2012

Access to electricity, 1990-2012

75.4% 79.2%

83.1%

0

1

2

3

4

5

6

7

8

1990 2000 2010

Bill

ion

peo

ple

People without access to electricity

People with access to electricity

Share of population with access to electricity

Access to non-solid fuels, 1990-2012

46.9%

54.4% 57.8%

0

1

2

3

4

5

6

7

8

1990 2000 2010B

illio

n p

eop

le

People without access to non-solid fuel

People with access to non-solid fuel

Share of population with access to non-solid fuel

84.6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012

58.4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012

12

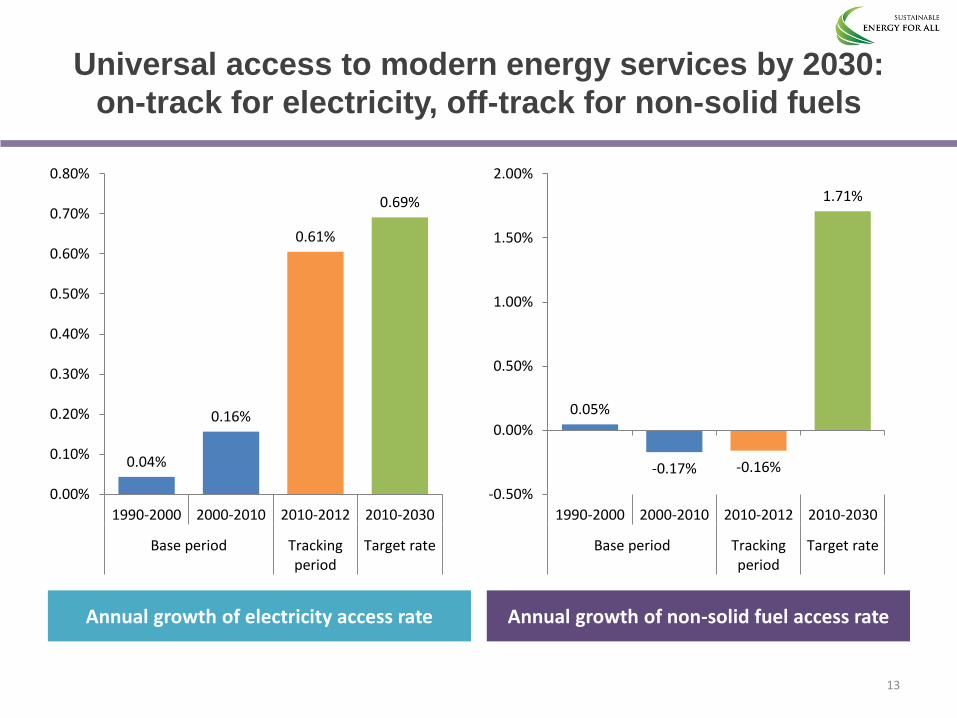

Universal access to modern energy services by 2030:

on-track for electricity, off-track for non-solid fuels

Annual growth of electricity access rate Annual growth of non-solid fuel access rate

13

0.04%

0.16%

0.61%

0.69%

0.00%

0.10%

0.20%

0.30%

0.40%

0.50%

0.60%

0.70%

0.80%

1990-2000 2000-2010 2010-2012 2010-2030

Base period Trackingperiod

Target rate

0.05%

-0.17% -0.16%

1.71%

-0.50%

0.00%

0.50%

1.00%

1.50%

2.00%

1990-2000 2000-2010 2010-2012 2010-2030

Base period Trackingperiod

Target rate

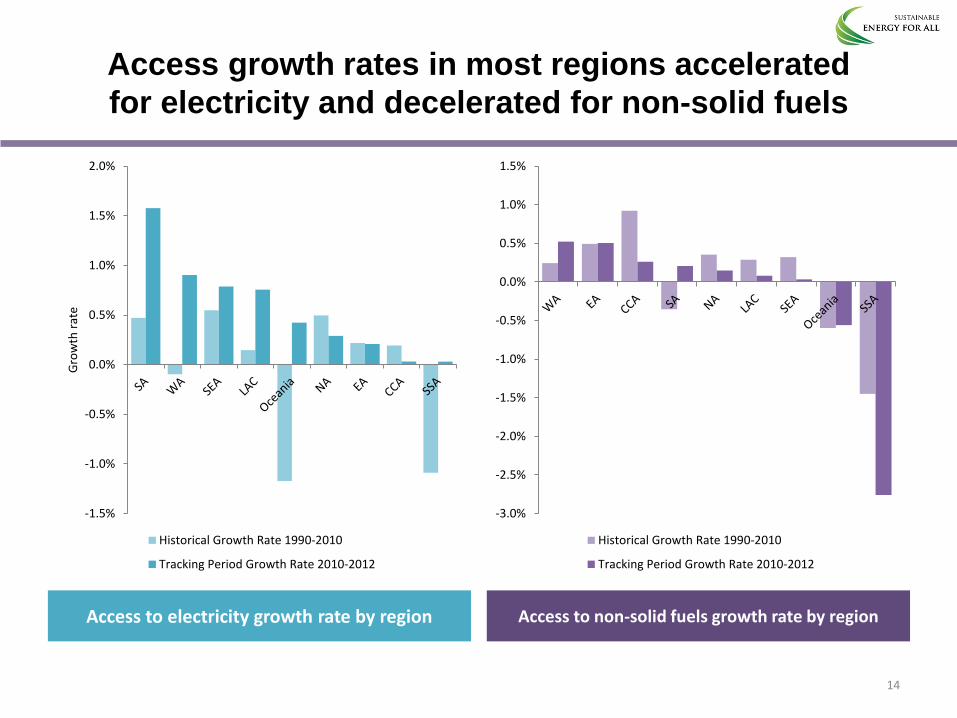

Access growth rates in most regions accelerated

for electricity and decelerated for non-solid fuels

Access to electricity growth rate by region Access to non-solid fuels growth rate by region

14

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

Gro

wth

rat

e

Historical Growth Rate 1990-2010

Tracking Period Growth Rate 2010-2012

-3.0%

-2.5%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

Historical Growth Rate 1990-2010

Tracking Period Growth Rate 2010-2012

15

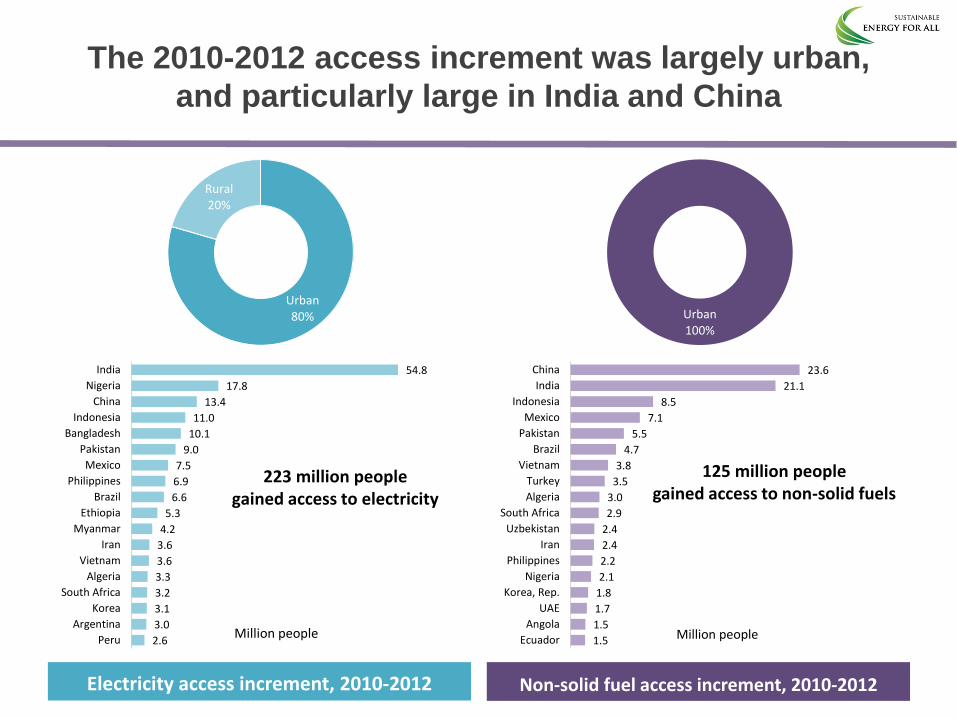

The 2010-2012 access increment was largely urban,

and particularly large in India and China

Electricity access increment, 2010-2012

Urban 80%

Rural 20%

Non-solid fuel access increment, 2010-2012

1.5

1.5

1.7

1.8

2.1

2.2

2.4

2.4

2.9

3.0

3.5

3.8

4.7

5.5

7.1

8.5

21.1

23.6

Ecuador

Angola

UAE

Korea, Rep.

Nigeria

Philippines

Iran

Uzbekistan

South Africa

Algeria

Turkey

Vietnam

Brazil

Pakistan

Mexico

Indonesia

India

China

Million people

125 million people gained access to non-solid fuels

223 million people gained access to electricity

Urban 100%

2.6

3.0

3.1

3.2

3.3

3.6

3.6

4.2

5.3

6.6

6.9

7.5

9.0

10.1

11.0

13.4

17.8

54.8

Peru

Argentina

Korea

South Africa

Algeria

Vietnam

Iran

Myanmar

Ethiopia

Brazil

Philippines

Mexico

Pakistan

Bangladesh

Indonesia

China

Nigeria

India

Million people

223 million people gained access to electricity

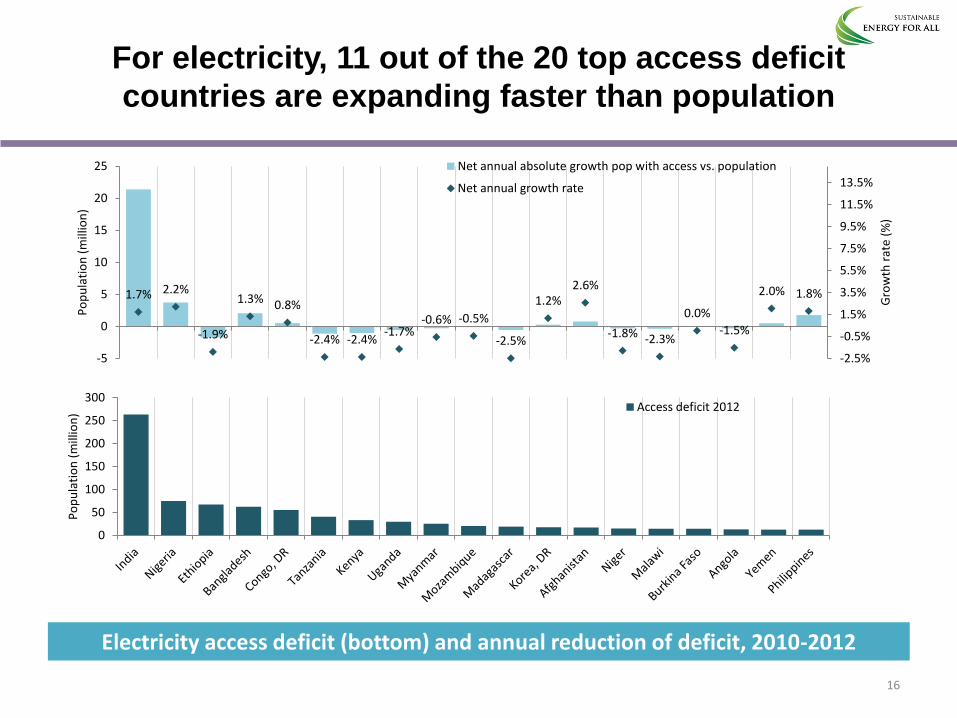

For electricity, 11 out of the 20 top access deficit

countries are expanding faster than population

Electricity access deficit (bottom) and annual reduction of deficit, 2010-2012

16

1.7% 2.2%

-1.9%

1.3% 0.8%

-2.4% -2.4% -1.7%

-0.6% -0.5%

-2.5%

1.2% 2.6%

-1.8% -2.3%

0.0%

-1.5%

2.0% 1.8%

-2.5%

-0.5%

1.5%

3.5%

5.5%

7.5%

9.5%

11.5%

13.5%

-5

0

5

10

15

20

25

Gro

wth

rat

e (%

)

Po

pu

lati

on

(m

illio

n)

Net annual absolute growth pop with access vs. population

Net annual growth rate

0

50

100

150

200

250

300

Po

pu

lati

on

(m

illio

n) Access deficit 2012

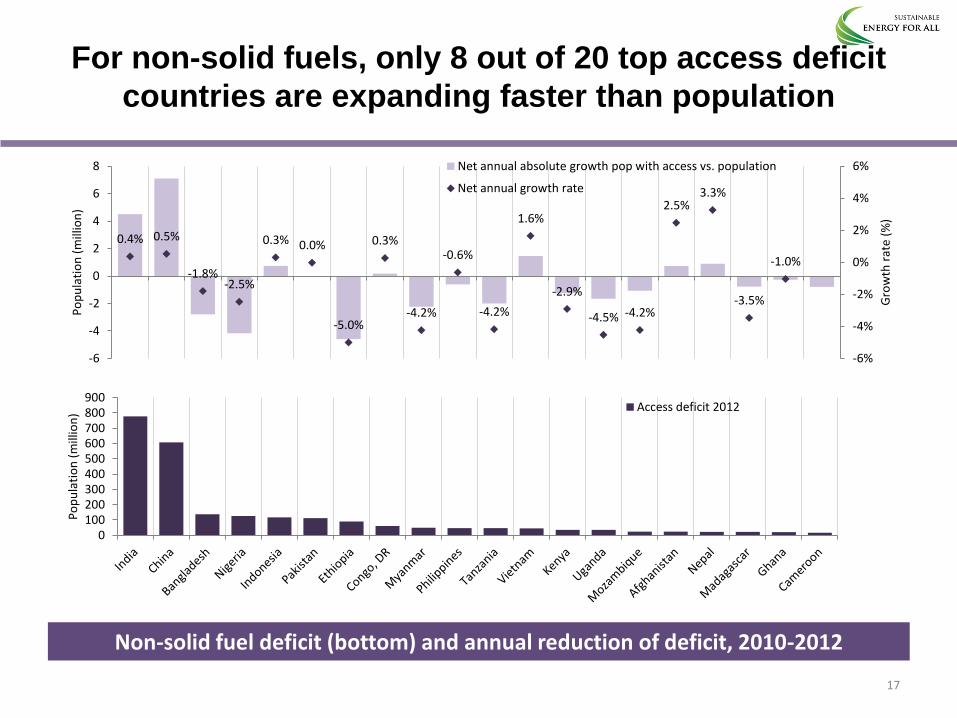

For non-solid fuels, only 8 out of 20 top access deficit

countries are expanding faster than population

Non-solid fuel deficit (bottom) and annual reduction of deficit, 2010-2012

17

0100200300400500600700800900

Po

pu

lati

on

(m

illio

n) Access deficit 2012

0.4% 0.5%

-1.8% -2.5%

0.3% 0.0%

-5.0%

0.3%

-4.2%

-0.6%

-4.2%

1.6%

-2.9%

-4.5% -4.2%

2.5% 3.3%

-3.5%

-1.0%

-6%

-4%

-2%

0%

2%

4%

6%

-6

-4

-2

0

2

4

6

8

Gro

wth

rat

e (%

)

Po

pu

lati

on

(m

illio

n)

Net annual absolute growth pop with access vs. population

Net annual growth rate

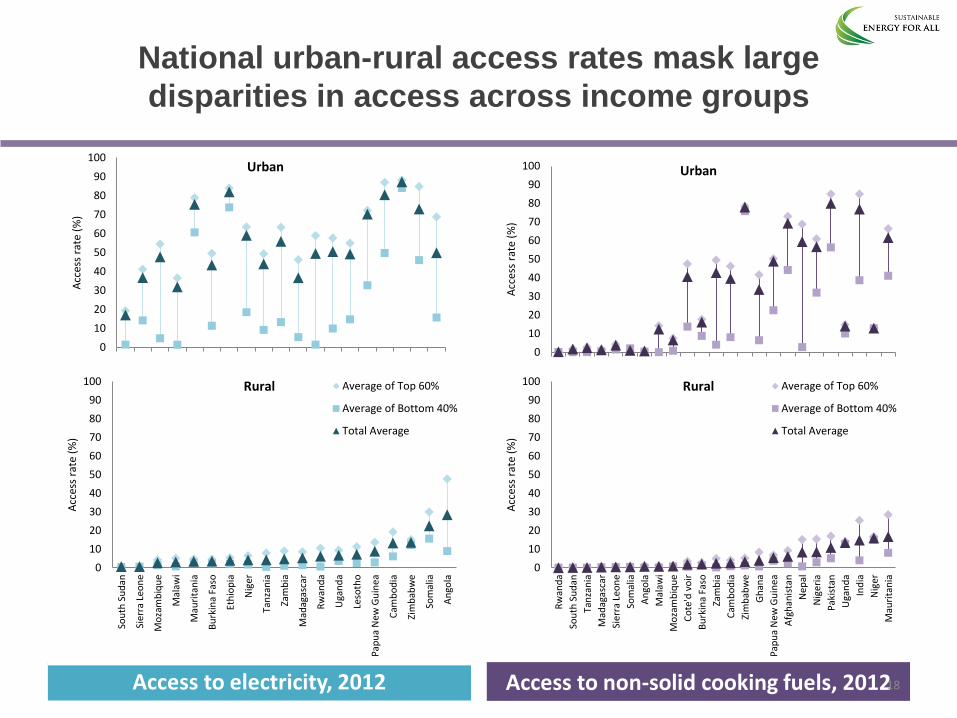

National urban-rural access rates mask large

disparities in access across income groups

Access to electricity, 2012

0

10

20

30

40

50

60

70

80

90

100

Acc

ess

rate

(%

)

Urban

Access to non-solid cooking fuels, 2012

0

10

20

30

40

50

60

70

80

90

100

Acc

ess

rate

(%

)

Urban

0

10

20

30

40

50

60

70

80

90

100

Rw

and

a

Sou

th S

ud

an

Tan

zan

ia

Mad

agas

car

Sier

ra L

eon

e

Som

alia

An

gola

Mal

awi

Mo

zam

biq

ue

Co

te'd

vo

ir

Bu

rkin

a Fa

so

Zam

bia

Cam

bo

dia

Zim

bab

we

Gh

ana

Pap

ua

New

Gu

inea

Afg

han

ista

n

Nep

al

Nig

eria

Pak

ista

n

Uga

nd

a

Ind

ia

Nig

er

Mau

rita

nia

Acc

ess

rate

(%

)

Rural Average of Top 60%

Average of Bottom 40%

Total Average

18

0

10

20

30

40

50

60

70

80

90

100

Sou

th S

ud

an

Sier

ra L

eon

e

Mo

zam

biq

ue

Mal

awi

Mau

rita

nia

Bu

rkin

a Fa

so

Eth

iop

ia

Nig

er

Tan

zan

ia

Zam

bia

Mad

agas

car

Rw

and

a

Uga

nd

a

Leso

tho

Pap

ua

New

Gu

inea

Cam

bo

dia

Zim

bab

we

Som

alia

An

gola

Acc

ess

rate

(%

)

Rural Average of Top 60%

Average of Bottom 40%

Total Average

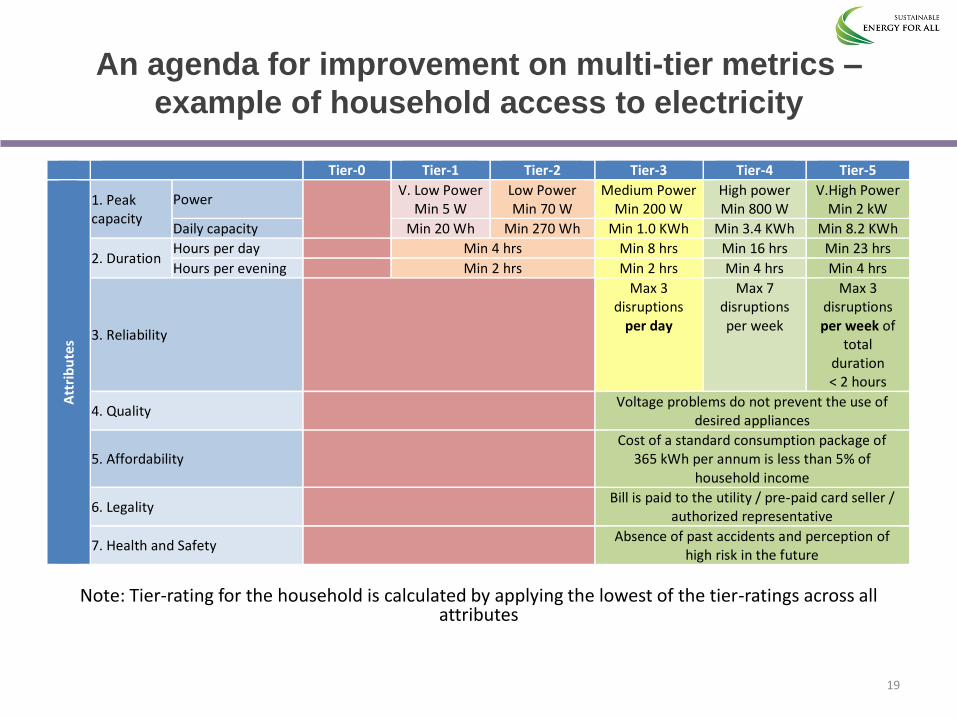

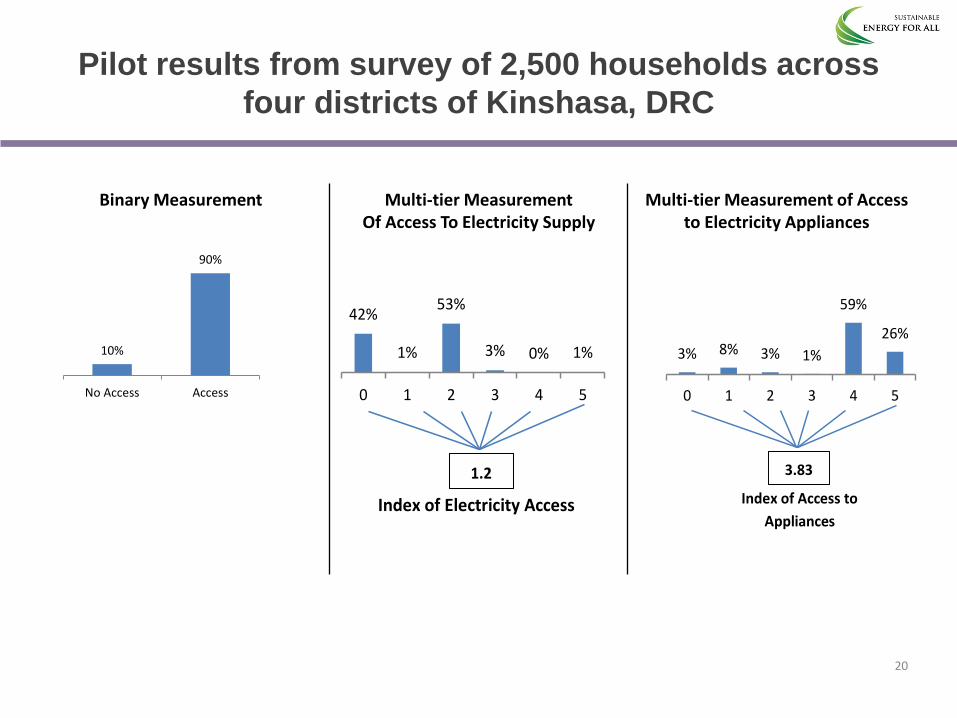

An agenda for improvement on multi-tier metrics –

example of household access to electricity

Note: Tier-rating for the household is calculated by applying the lowest of the tier-ratings across all attributes

19

Tier-0 Tier-1 Tier-2 Tier-3 Tier-4 Tier-5

Att

rib

ute

s

1. Peak capacity

Power

V. Low Power Min 5 W

Low Power Min 70 W

Medium Power Min 200 W

High power Min 800 W

V.High Power Min 2 kW

Daily capacity Min 20 Wh Min 270 Wh Min 1.0 KWh Min 3.4 KWh Min 8.2 KWh

2. Duration Hours per day Min 4 hrs Min 8 hrs Min 16 hrs Min 23 hrs

Hours per evening Min 2 hrs Min 2 hrs Min 4 hrs Min 4 hrs

3. Reliability

Max 3 disruptions

per day

Max 7 disruptions per week

Max 3 disruptions per week of

total duration < 2 hours

4. Quality Voltage problems do not prevent the use of

desired appliances

5. Affordability Cost of a standard consumption package of

365 kWh per annum is less than 5% of household income

6. Legality Bill is paid to the utility / pre-paid card seller /

authorized representative

7. Health and Safety Absence of past accidents and perception of

high risk in the future

42%

1%

53%

3% 0% 1%

0 1 2 3 4 5

Index of Electricity Access

1.2

3% 8% 3% 1%

59%

26%

0 1 2 3 4 5

Index of Access to

Appliances

3.83

10%

90%

No Access Access

Binary Measurement

Multi-tier Measurement Of Access To Electricity Supply

Multi-tier Measurement of Access to Electricity Appliances

Pilot results from survey of 2,500 households across

four districts of Kinshasa, DRC

20

21

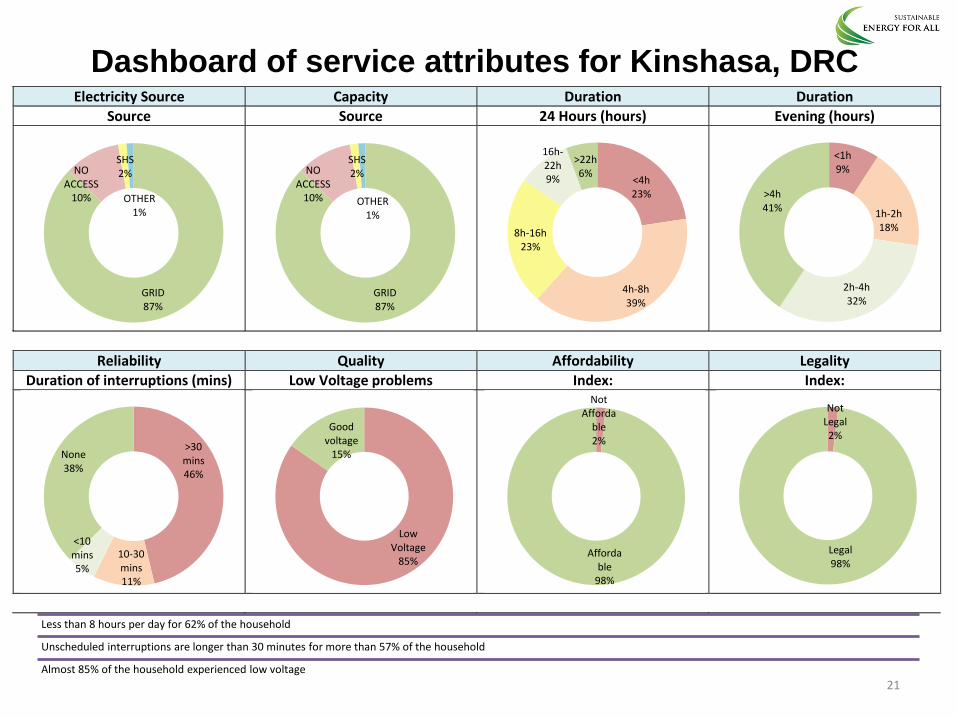

Electricity Source Capacity Duration Duration

Source Source 24 Hours (hours) Evening (hours)

Reliability Quality Affordability Legality

Duration of interruptions (mins) Low Voltage problems Index: Index:

GRID 87%

NO ACCESS

10%

SHS2%

OTHER1%

GRID 87%

NO ACCESS

10%

SHS2%

OTHER1%

<4h23%

4h-8h39%

8h-16h23%

16h-22h9%

>22h6%

<1h9%

1h-2h18%

2h-4h32%

>4h41%

>30 mins46%

10-30 mins11%

<10 mins5%

None38%

Low Voltage

85%

Good voltage

15%

Not Afforda

ble2%

Affordable

98%

Not Legal2%

Legal98%

Dashboard of service attributes for Kinshasa, DRC

Less than 8 hours per day for 62% of the household

Unscheduled interruptions are longer than 30 minutes for more than 57% of the household

Almost 85% of the household experienced low voltage

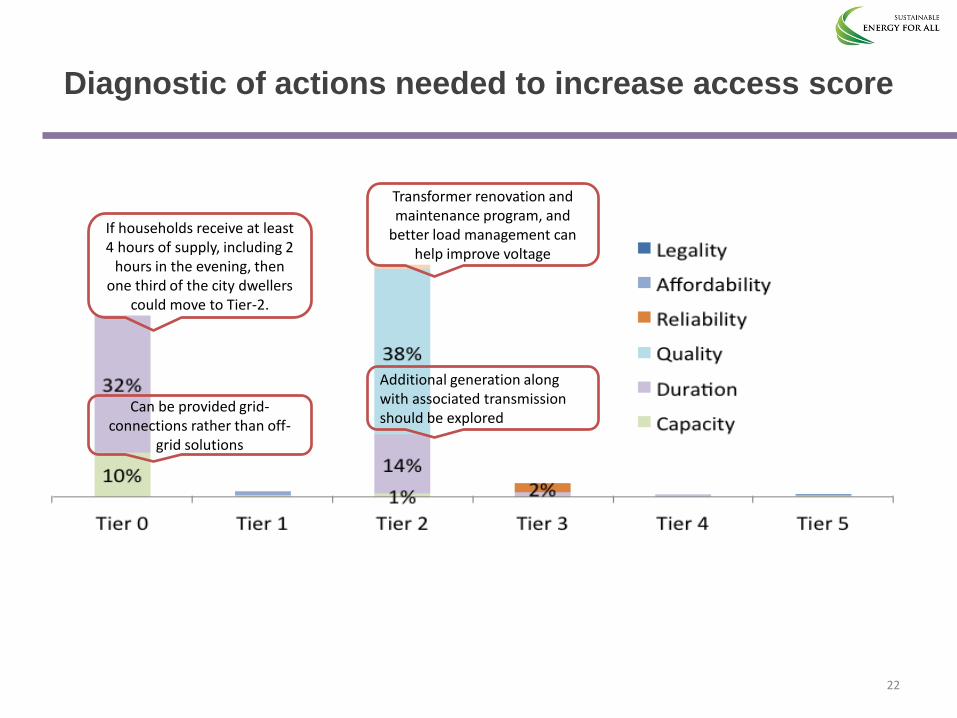

Diagnostic of actions needed to increase access score

22

Can be provided grid-connections rather than off-

grid solutions

If households receive at least 4 hours of supply, including 2

hours in the evening, then one third of the city dwellers

could move to Tier-2.

Transformer renovation and maintenance program, and

better load management can help improve voltage

Additional generation along with associated transmission should be explored

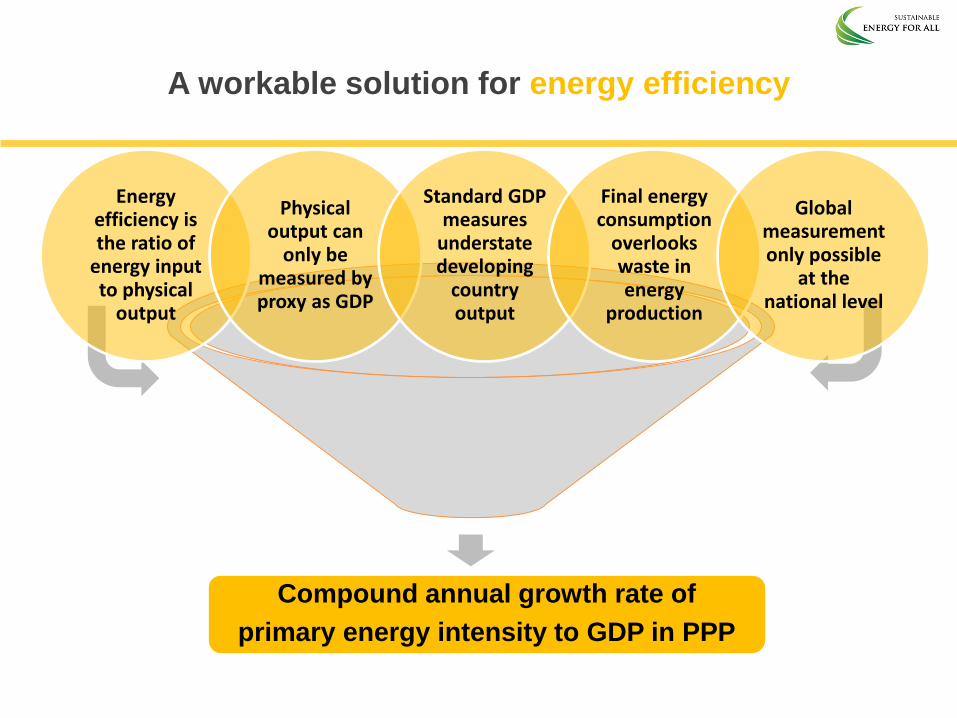

ENERGY EFFICIENCY

23

A workable solution for energy efficiency

Compound annual growth rate of

primary energy intensity to GDP in PPP

Energy efficiency is the ratio of

energy input to physical

output

Physical output can

only be measured by proxy as GDP

Standard GDP measures

understate developing

country output

Final energy consumption

overlooks waste in energy

production

Global measurement only possible

at the national level

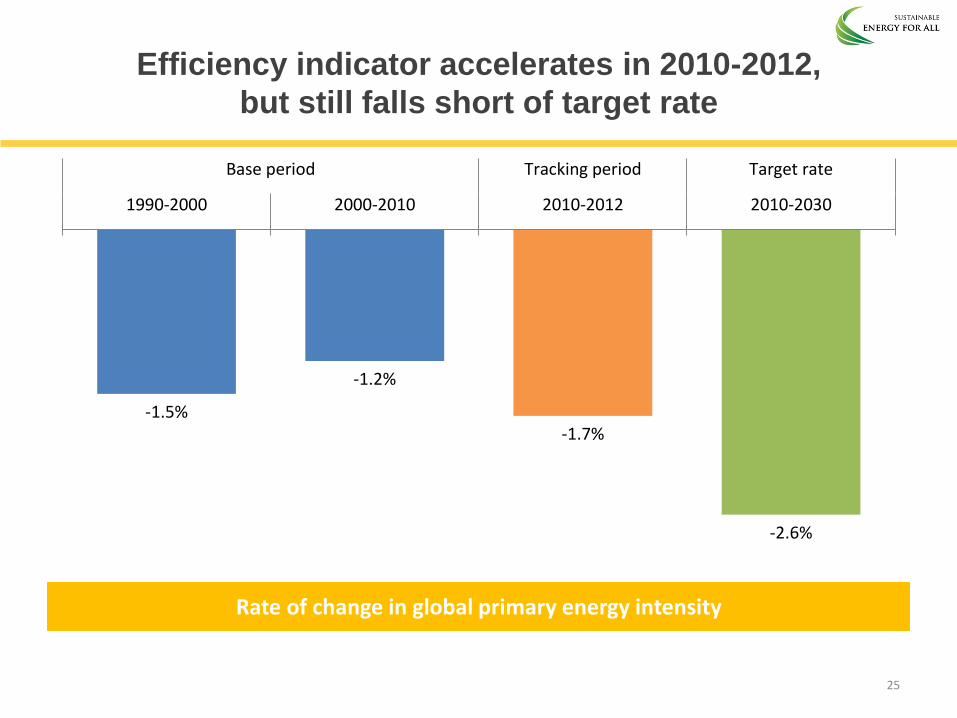

Efficiency indicator accelerates in 2010-2012,

but still falls short of target rate

Rate of change in global primary energy intensity

-1.5%

-1.2%

-1.7%

-2.6%

1990-2000 2000-2010 2010-2012 2010-2030

Base period Tracking period Target rate

25

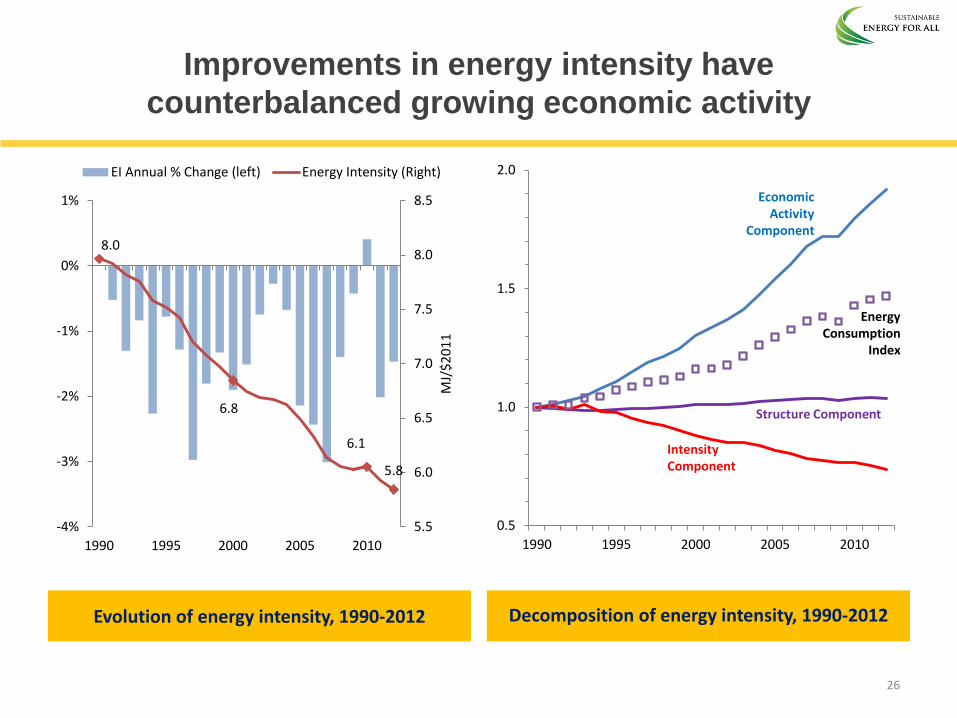

Improvements in energy intensity have

counterbalanced growing economic activity

Evolution of energy intensity, 1990-2012 Decomposition of energy intensity, 1990-2012

8.0

6.8

6.1

5.8

5.5

6.0

6.5

7.0

7.5

8.0

8.5

-4%

-3%

-2%

-1%

0%

1%

1990 1995 2000 2005 2010

MJ/

$2

01

1

EI Annual % Change (left) Energy Intensity (Right)

0.5

1.0

1.5

2.0

1990 1995 2000 2005 2010

Economic Activity

Component

Structure Component

Intensity Component

Energy Consumption

Index

26

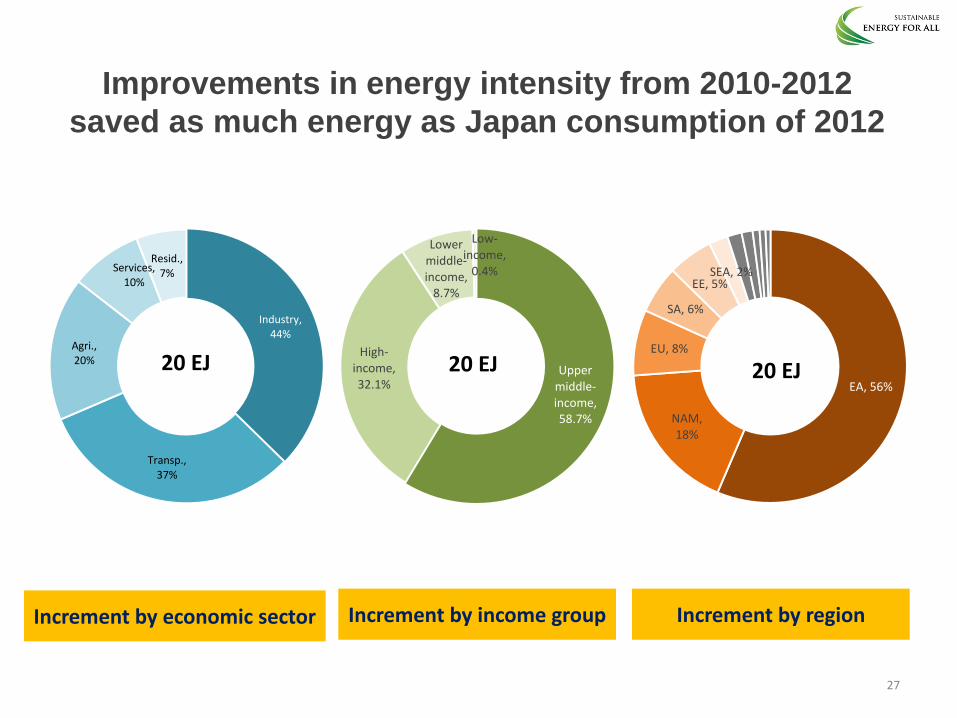

Improvements in energy intensity from 2010-2012

saved as much energy as Japan consumption of 2012

Increment by economic sector Increment by income group

27

Increment by region

EA, 56%

NAM, 18%

EU, 8%

SA, 6%

EE, 5% SEA, 2%

20 EJ Upper middle-income, 58.7%

High-income, 32.1%

Lower middle-income,

8.7%

Low-income,

0.4%

20 EJ

Industry, 44%

Transp., 37%

Agri., 20%

Services, 10%

Resid., 7%

20 EJ

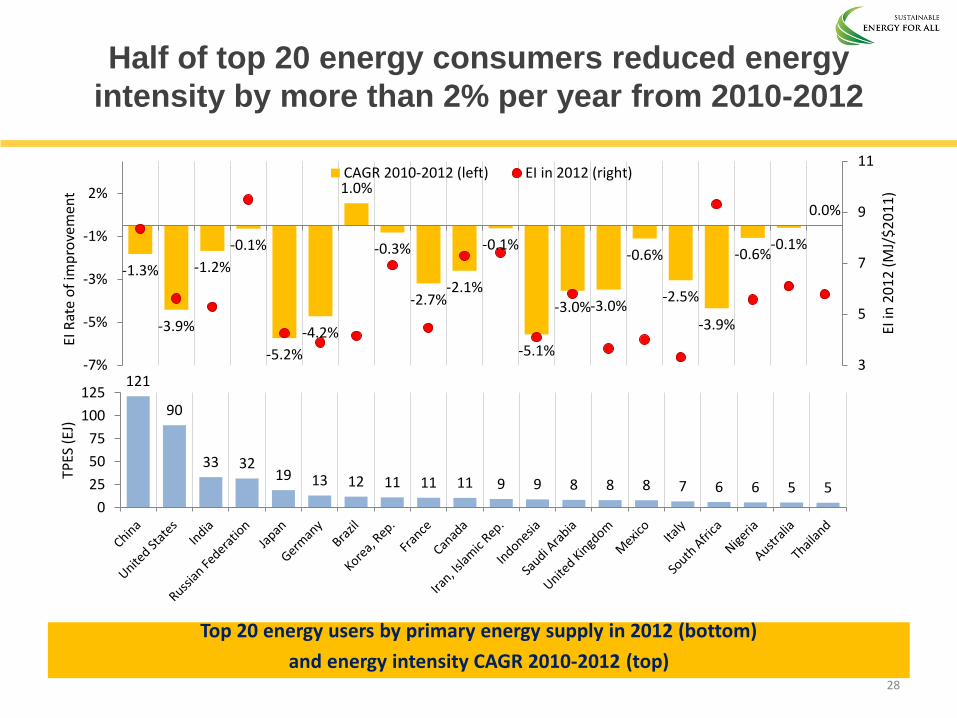

Half of top 20 energy consumers reduced energy

intensity by more than 2% per year from 2010-2012

Top 20 energy users by primary energy supply in 2012 (bottom)

and energy intensity CAGR 2010-2012 (top) 28

121

90

33 32 19 13 12 11 11 11 9 9 8 8 8 7 6 6 5 5

0

25

50

75

100

125

TPES

(EJ

)

-1.3%

-3.9%

-1.2%

-0.1%

-5.2%

-4.2%

1.0%

-0.3%

-2.7% -2.1%

-0.1%

-5.1%

-3.0% -3.0%

-0.6%

-2.5%

-3.9%

-0.6% -0.1%

0.0%

3

5

7

9

11

-7%

-5%

-3%

-1%

2%

EI in

20

12

(M

J/$

20

11

)

EI R

ate

of

imp

rove

men

t

CAGR 2010-2012 (left) EI in 2012 (right)

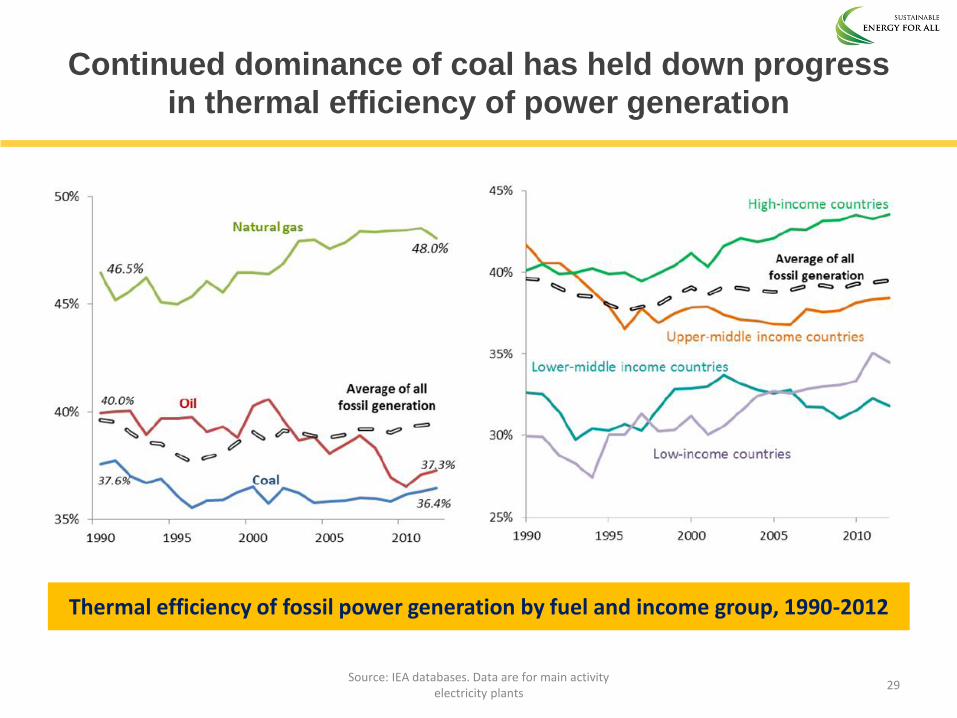

Continued dominance of coal has held down progress

in thermal efficiency of power generation

Thermal efficiency of fossil power generation by fuel and income group, 1990-2012

29 Source: IEA databases. Data are for main activity

electricity plants

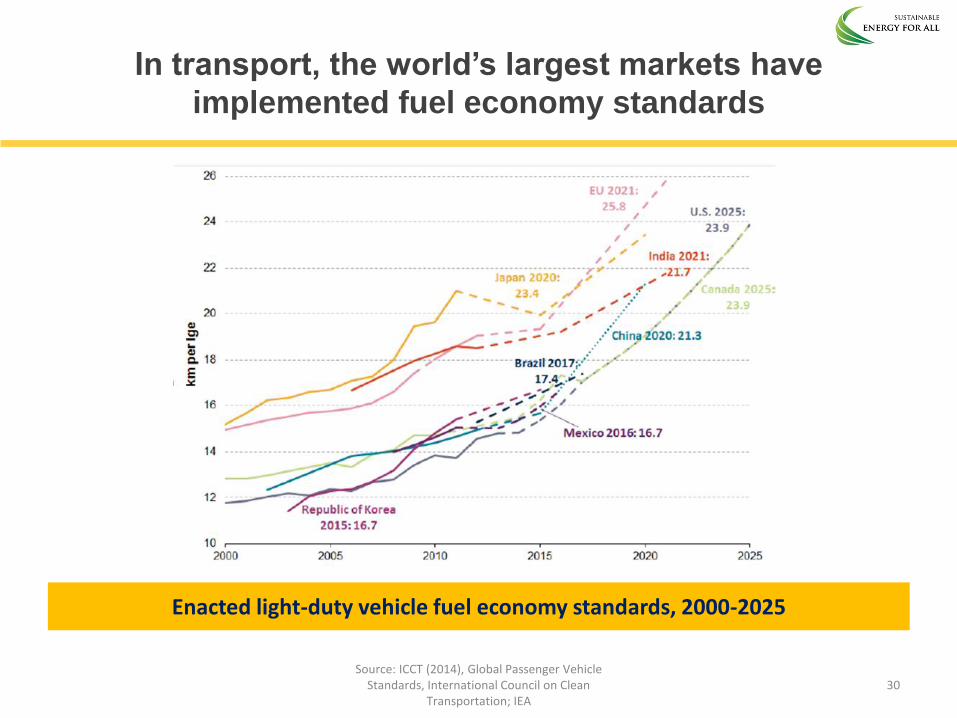

In transport, the world’s largest markets have

implemented fuel economy standards

Enacted light-duty vehicle fuel economy standards, 2000-2025

Source: ICCT (2014), Global Passenger Vehicle Standards, International Council on Clean

Transportation; IEA 30

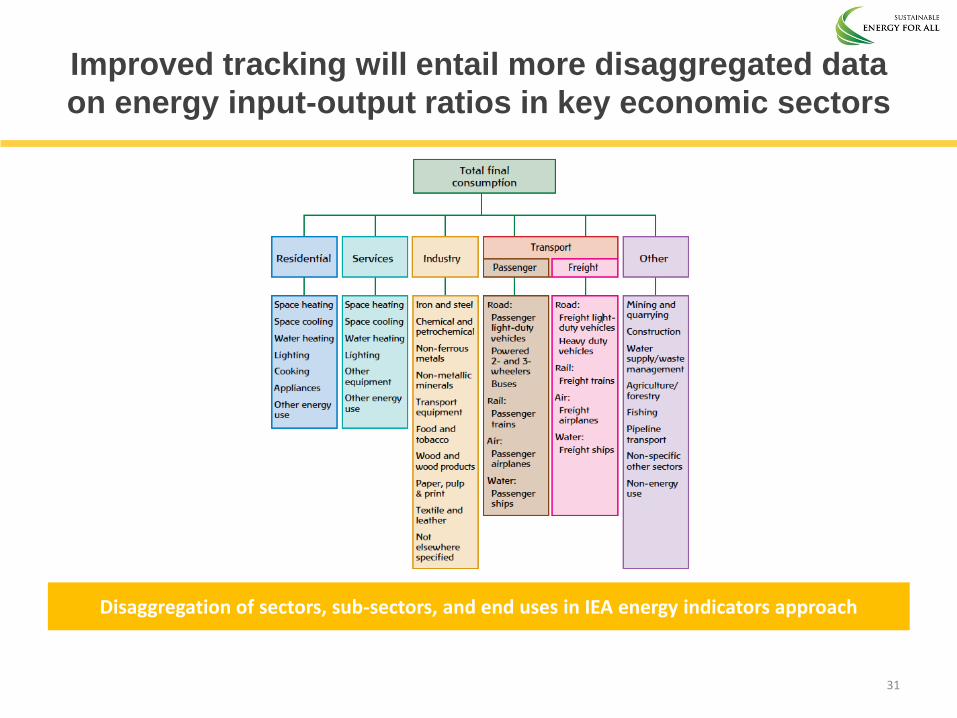

Improved tracking will entail more disaggregated data

on energy input-output ratios in key economic sectors

Disaggregation of sectors, sub-sectors, and end uses in IEA energy indicators approach

31

32

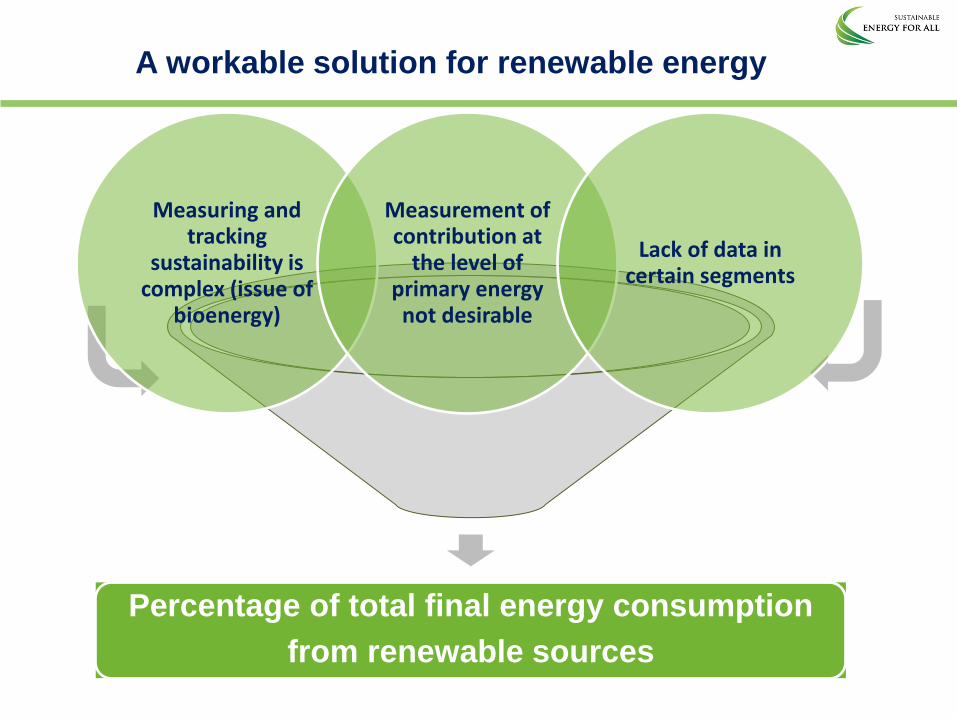

A workable solution for renewable energy

Percentage of total final energy consumption

from renewable sources

Measuring and tracking

sustainability is complex (issue of

bioenergy)

Measurement of contribution at

the level of primary energy not desirable

Lack of data in certain segments

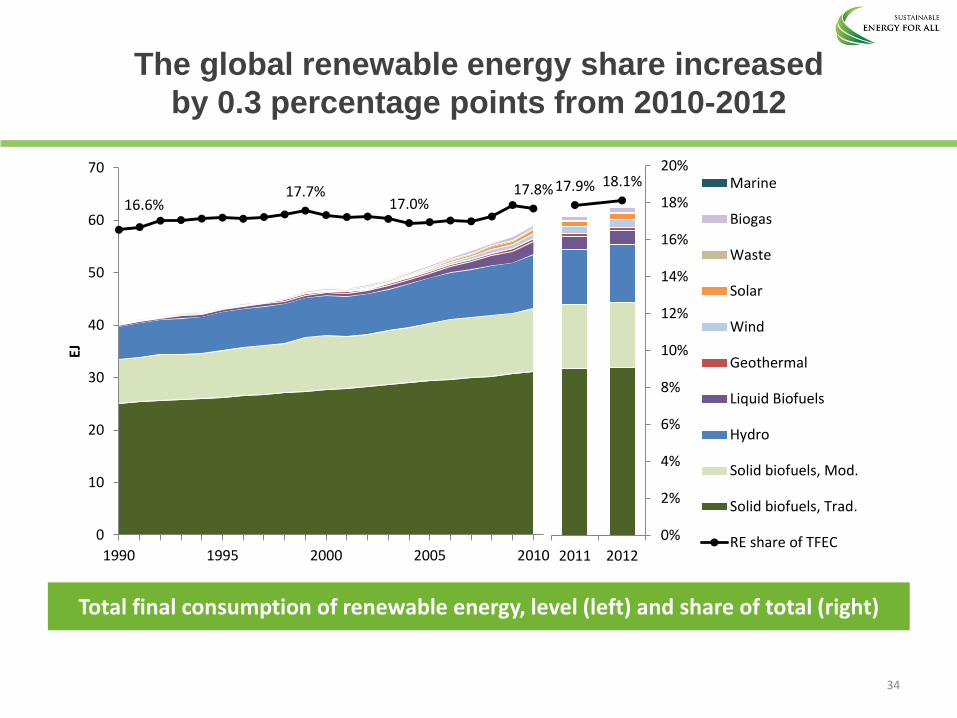

The global renewable energy share increased

by 0.3 percentage points from 2010-2012

Total final consumption of renewable energy, level (left) and share of total (right)

16.6% 17.7%

17.0% 17.8%

0

10

20

30

40

50

60

70

1990 1995 2000 2005 2010

EJ

34

17.9% 18.1%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

2011 2012

Marine

Biogas

Waste

Solar

Wind

Geothermal

Liquid Biofuels

Hydro

Solid biofuels, Mod.

Solid biofuels, Trad.

RE share of TFEC

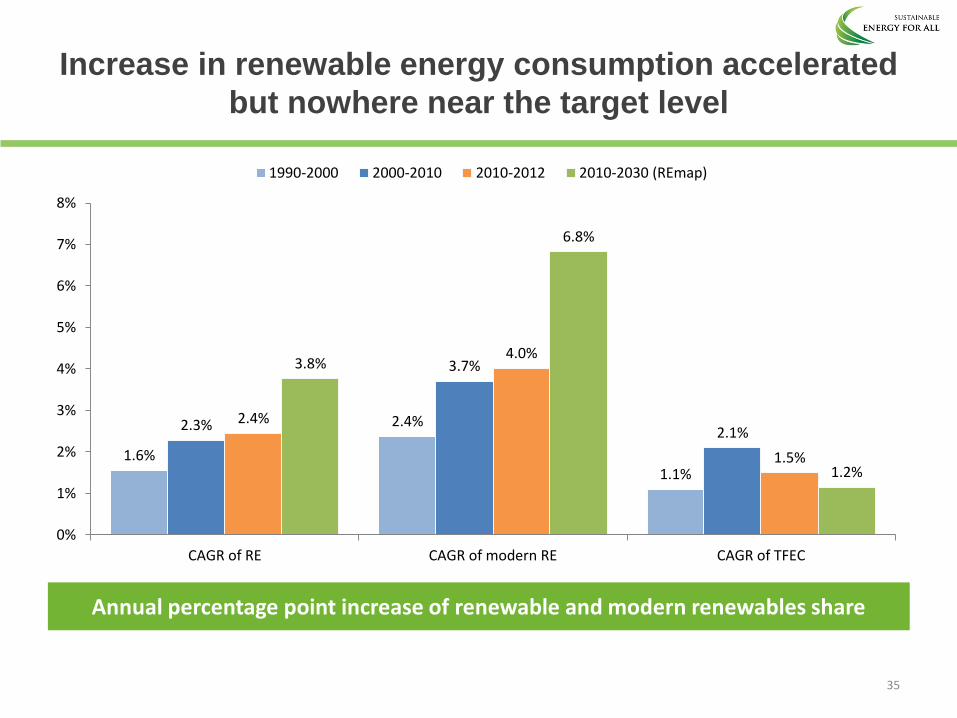

Increase in renewable energy consumption accelerated

but nowhere near the target level

Annual percentage point increase of renewable and modern renewables share

35

1.6%

2.4%

1.1%

2.3%

3.7%

2.1% 2.4%

4.0%

1.5%

3.8%

6.8%

1.2%

0%

1%

2%

3%

4%

5%

6%

7%

8%

CAGR of RE CAGR of modern RE CAGR of TFEC

1990-2000 2000-2010 2010-2012 2010-2030 (REmap)

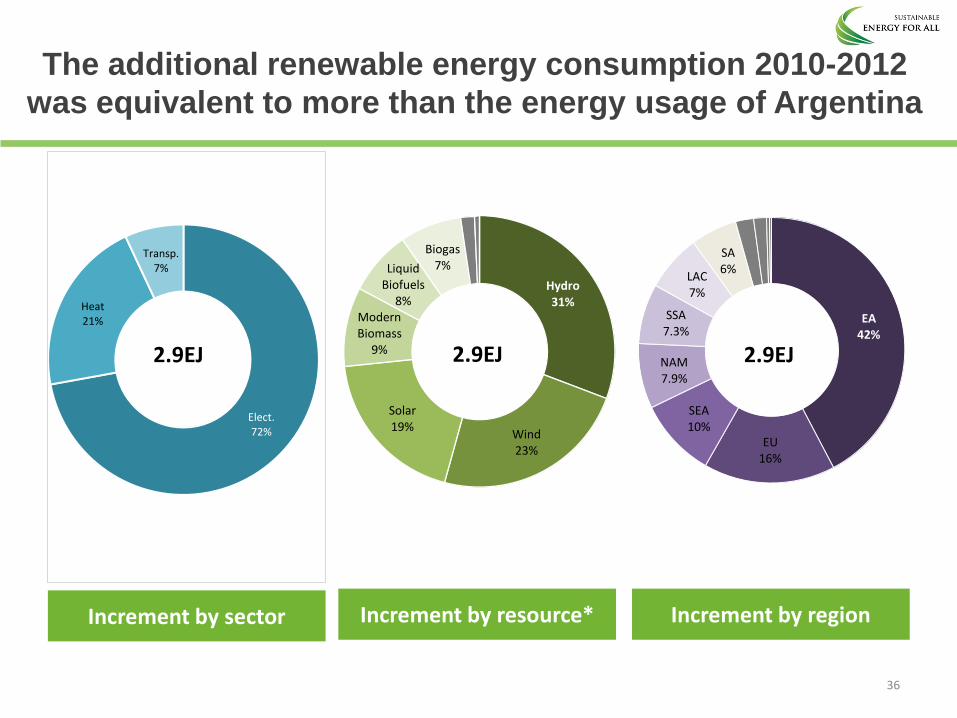

The additional renewable energy consumption 2010-2012

was equivalent to more than the energy usage of Argentina

Increment by sector Increment by resource*

36

Increment by region

EA 42%

EU 16%

SEA 10%

NAM 7.9%

SSA 7.3%

LAC 7%

SA 6%

2.9EJ

Hydro 31%

Wind 23%

Solar 19%

Modern Biomass

9%

Liquid Biofuels

8%

Biogas 7%

2.9EJ

Elect. 72%

Heat 21%

Transp. 7%

2.9EJ

Wide variations across regions as to what types

of renewable energy are increasing (and decreasing)

Renewable energy increment by region and resource, 2010-2012

37

-300 -100 100 300 500 700 900

NAM

EU

EE

CCA

WA

EA

SEA

SA

OCEANIA

LAC

NAf

SSA

PJ

Solid Biofuels, Mod.

Solid Biofuels, Trad.

Hydro

Liquid Biofuels

Geothermal

Biogas

Solar

Wind

Waste

Marine

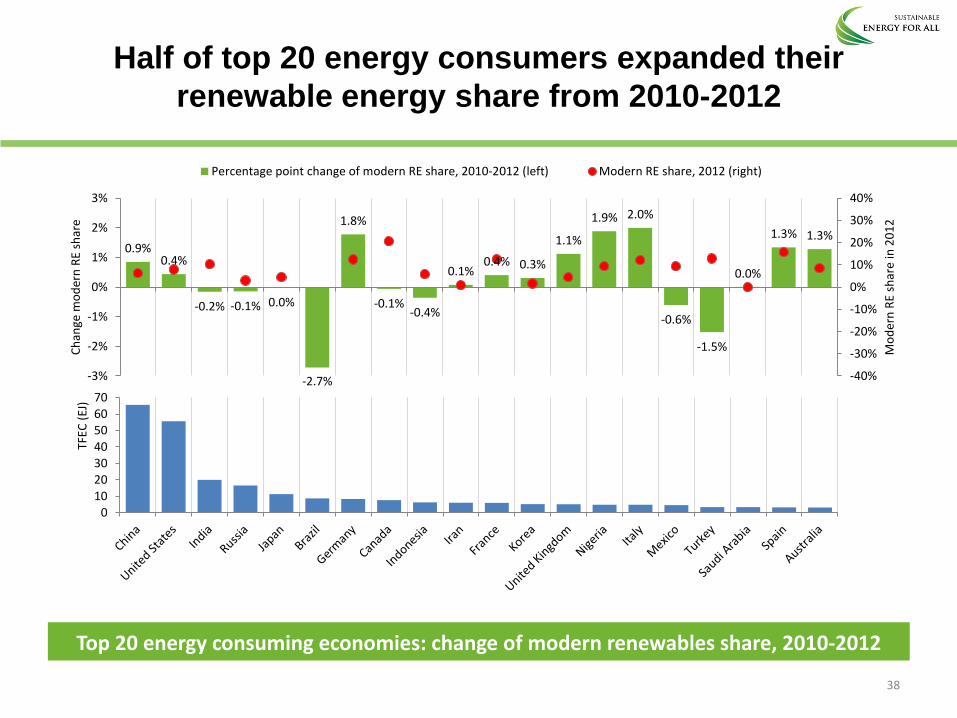

Half of top 20 energy consumers expanded their

renewable energy share from 2010-2012

Top 20 energy consuming economies: change of modern renewables share, 2010-2012

38

010203040506070

TFEC

(EJ

)

0.9% 0.4%

-0.2% -0.1% 0.0%

-2.7%

1.8%

-0.1% -0.4%

0.1% 0.4% 0.3%

1.1%

1.9% 2.0%

-0.6%

-1.5%

0.0%

1.3% 1.3%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

-3%

-2%

-1%

0%

1%

2%

3%

Mo

der

n R

E sh

are

in 2

01

2

Ch

ange

mo

der

n R

E sh

are

Percentage point change of modern RE share, 2010-2012 (left) Modern RE share, 2012 (right)

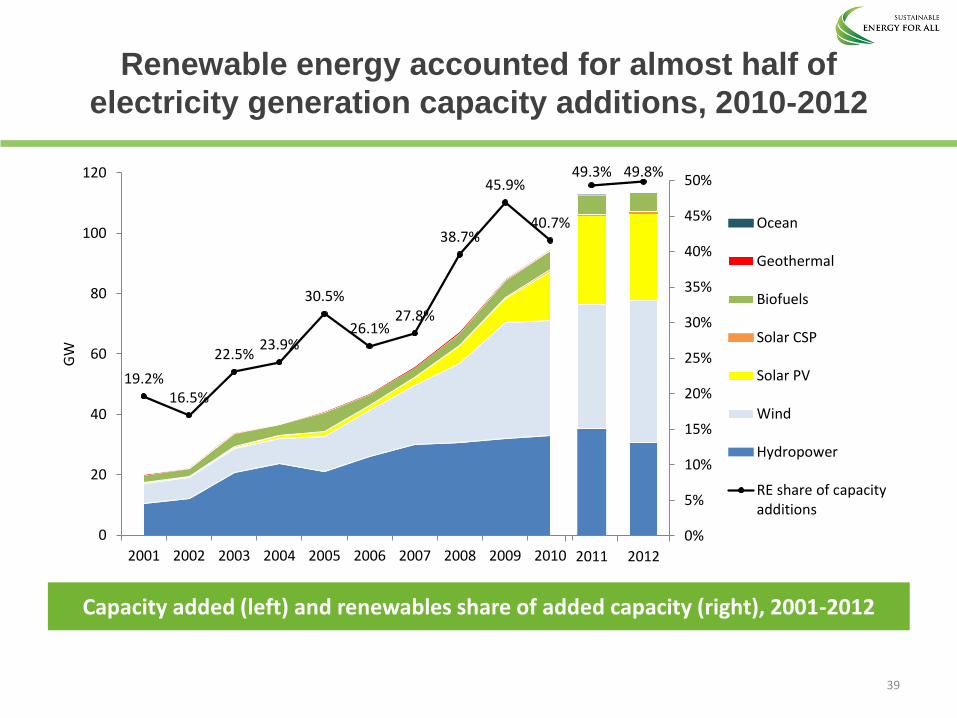

Renewable energy accounted for almost half of

electricity generation capacity additions, 2010-2012

Capacity added (left) and renewables share of added capacity (right), 2001-2012

39

49.3% 49.8%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2011 2012

Ocean

Geothermal

Biofuels

Solar CSP

Solar PV

Wind

Hydropower

RE share of capacityadditions

19.2% 16.5%

22.5% 23.9%

30.5%

26.1% 27.8%

38.7%

45.9%

40.7%

0

20

40

60

80

100

120

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

GW

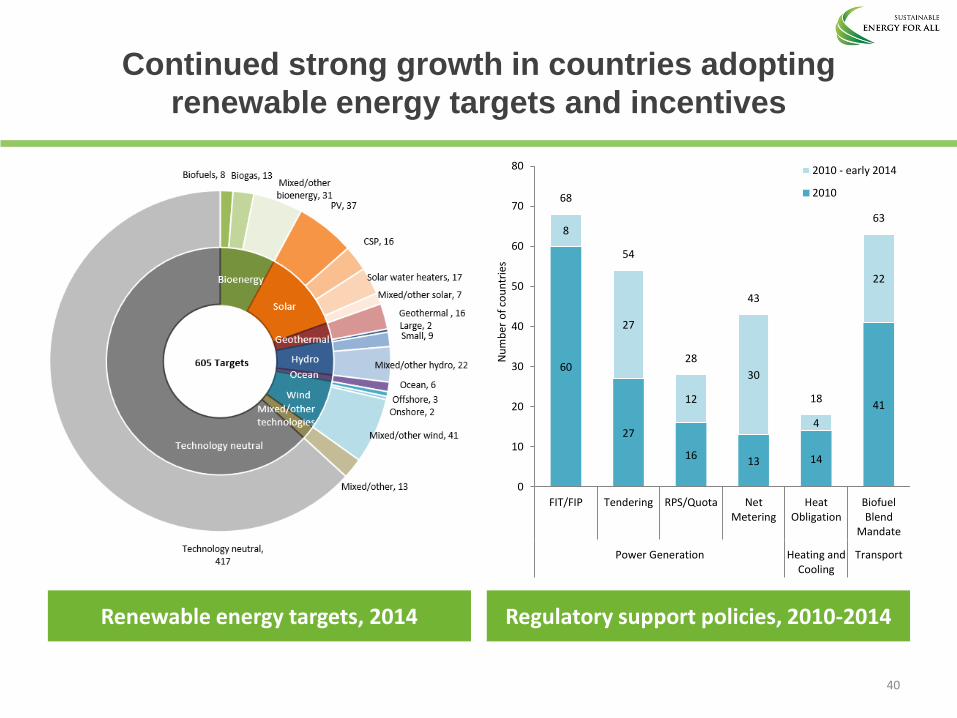

Continued strong growth in countries adopting

renewable energy targets and incentives

Renewable energy targets, 2014 Regulatory support policies, 2010-2014

60

27

16 13 14

41

8

27

12

30

4

22

68

54

28

43

18

63

0

10

20

30

40

50

60

70

80

FIT/FIP Tendering RPS/Quota NetMetering

HeatObligation

BiofuelBlend

Mandate

Power Generation Heating andCooling

Transport

Nu

mb

er o

f co

un

trie

s

2010 - early 2014

2010

40

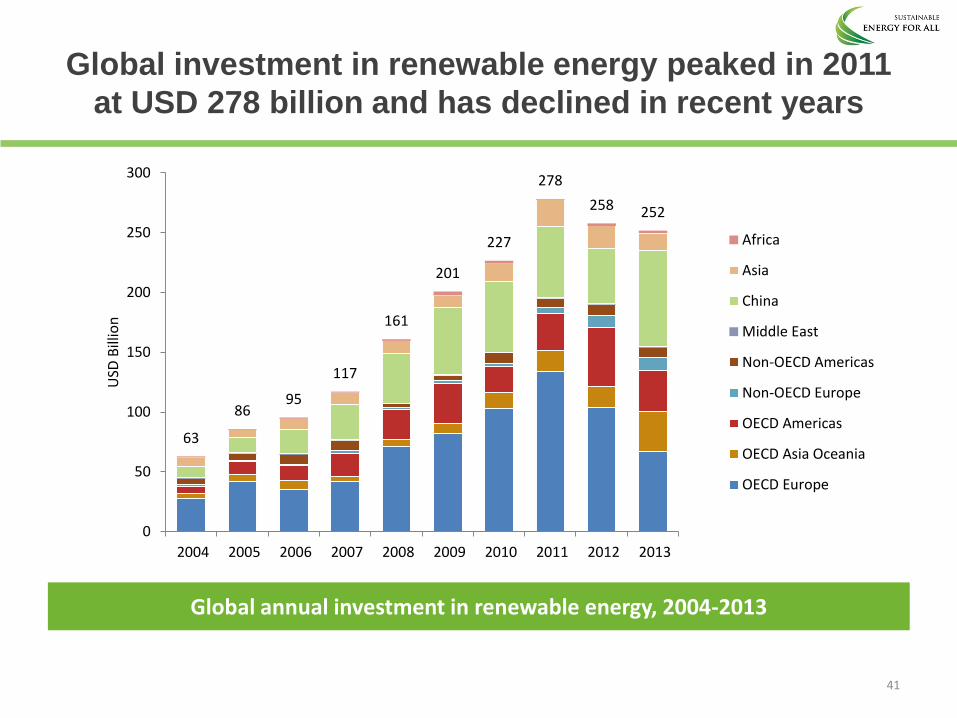

Global investment in renewable energy peaked in 2011

at USD 278 billion and has declined in recent years

Global annual investment in renewable energy, 2004-2013

63

86 95

117

161

201

227

278

258 252

0

50

100

150

200

250

300

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

USD

Bill

ion

Africa

Asia

China

Middle East

Non-OECD Americas

Non-OECD Europe

OECD Americas

OECD Asia Oceania

OECD Europe

41

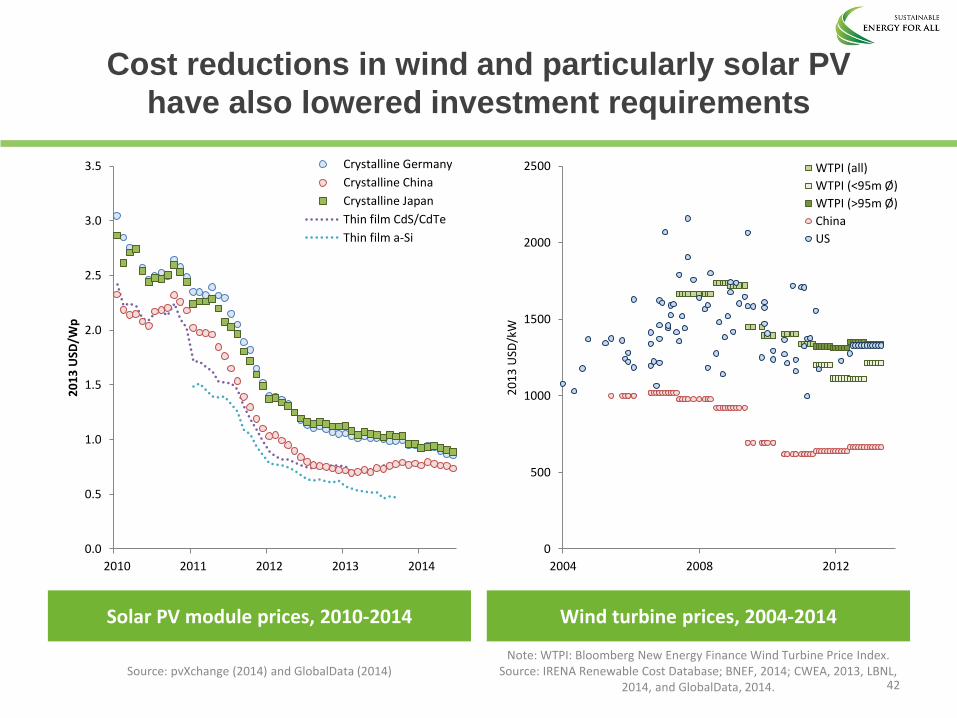

Cost reductions in wind and particularly solar PV

have also lowered investment requirements

Solar PV module prices, 2010-2014 Wind turbine prices, 2004-2014

Source: pvXchange (2014) and GlobalData (2014) 42

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2010 2011 2012 2013 2014

20

13

USD

/Wp

Crystalline Germany

Crystalline China

Crystalline Japan

Thin film CdS/CdTe

Thin film a-Si

0

500

1000

1500

2000

2500

2004 2008 2012

20

13

USD

/kW

WTPI (all)

WTPI (<95m Ø)

WTPI (>95m Ø)

China

US

Note: WTPI: Bloomberg New Energy Finance Wind Turbine Price Index. Source: IRENA Renewable Cost Database; BNEF, 2014; CWEA, 2013, LBNL,

2014, and GlobalData, 2014.

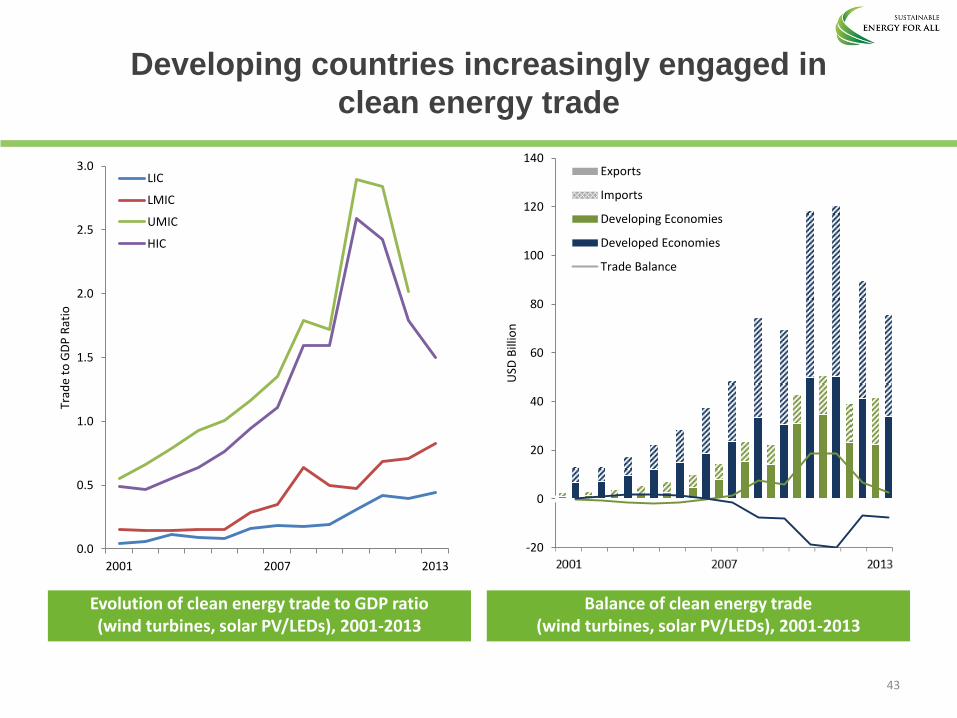

Developing countries increasingly engaged in

clean energy trade

Evolution of clean energy trade to GDP ratio (wind turbines, solar PV/LEDs), 2001-2013

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2001 2007 2013

Trad

e to

GD

P R

atio

LIC

LMIC

UMIC

HIC

Balance of clean energy trade (wind turbines, solar PV/LEDs), 2001-2013

43

-20

0

20

40

60

80

100

120

140

USD

Bill

ion

Exports

Imports

Developing Economies

Developed Economies

Trade Balance

Towards a better understanding of solid biofuels for

traditional energy uses

• Traditional solid biofuels accounted for 53% of global renewable energy consumption in 2012 (modern solid biofuels for about 18%, so together 70%)

• To answer whether traditional solid biofuel consumption is sustainable we must first define sustainability itself

• Sustainability has environmental, economic and social dimensions, a full tracking of which is not possible

• Yet semi-quantitative indicators (e.g. coverage of certification schemes) and qualitative indicators (e.g. those developed by the Global Bioenergy Partnership) exist which, when tracked over time, can help distinguish progress towards sustainable use of solid biofuels.

44

THE WAY FORWARD

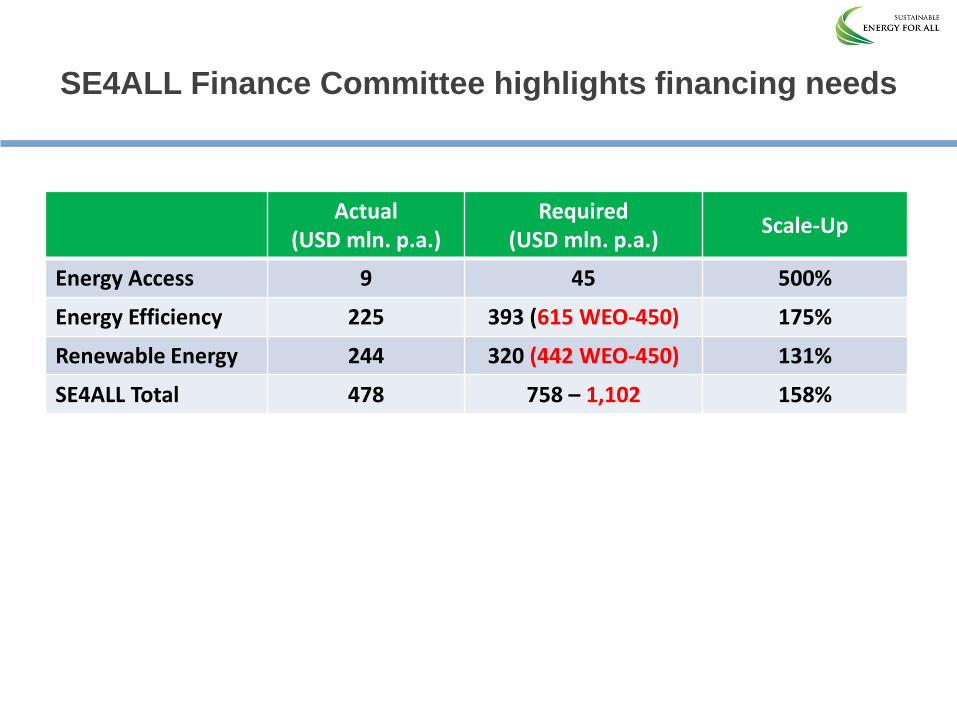

SE4ALL Finance Committee highlights financing needs

Actual (USD mln. p.a.)

Required (USD mln. p.a.)

Scale-Up

Energy Access 9 45 500%

Energy Efficiency 225 393 (615 WEO-450) 175%

Renewable Energy 244 320 (442 WEO-450) 131%

SE4ALL Total 478 758 – 1,102 158%

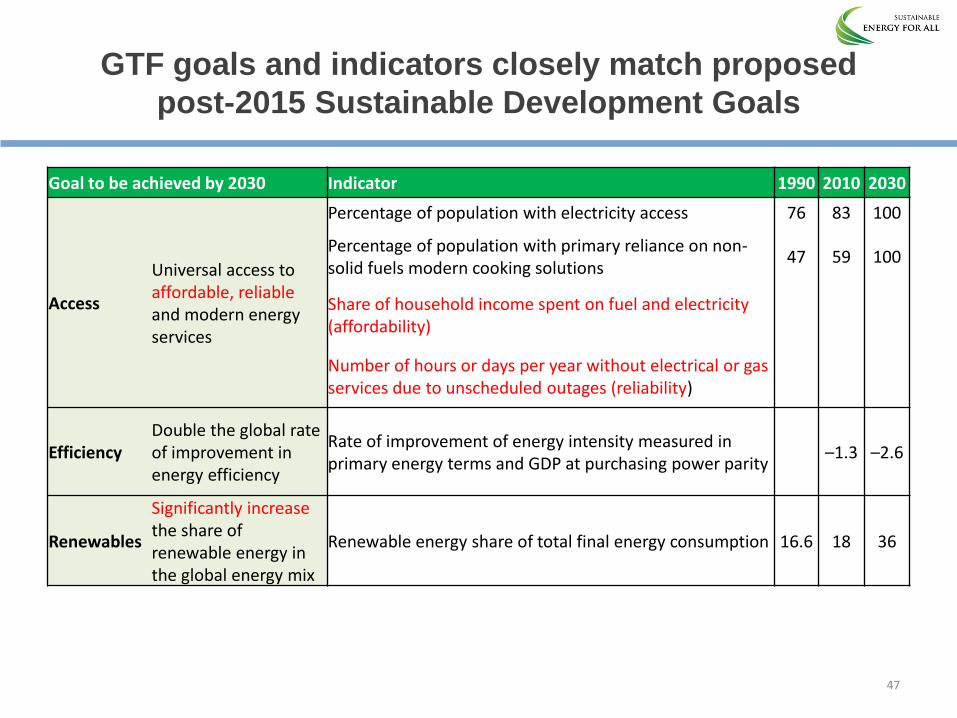

GTF goals and indicators closely match proposed

post-2015 Sustainable Development Goals

Goal to be achieved by 2030 Indicator 1990 2010 2030

Access

Universal access to affordable, reliable and modern energy services

Percentage of population with electricity access 76 83 100

Percentage of population with primary reliance on non-solid fuels modern cooking solutions

47 59 100

Share of household income spent on fuel and electricity (affordability)

Number of hours or days per year without electrical or gas services due to unscheduled outages (reliability)

Efficiency Double the global rate of improvement in energy efficiency

Rate of improvement of energy intensity measured in primary energy terms and GDP at purchasing power parity

–1.3 –2.6

Renewables

Significantly increase the share of renewable energy in the global energy mix

Renewable energy share of total final energy consumption 16.6 18 36

47

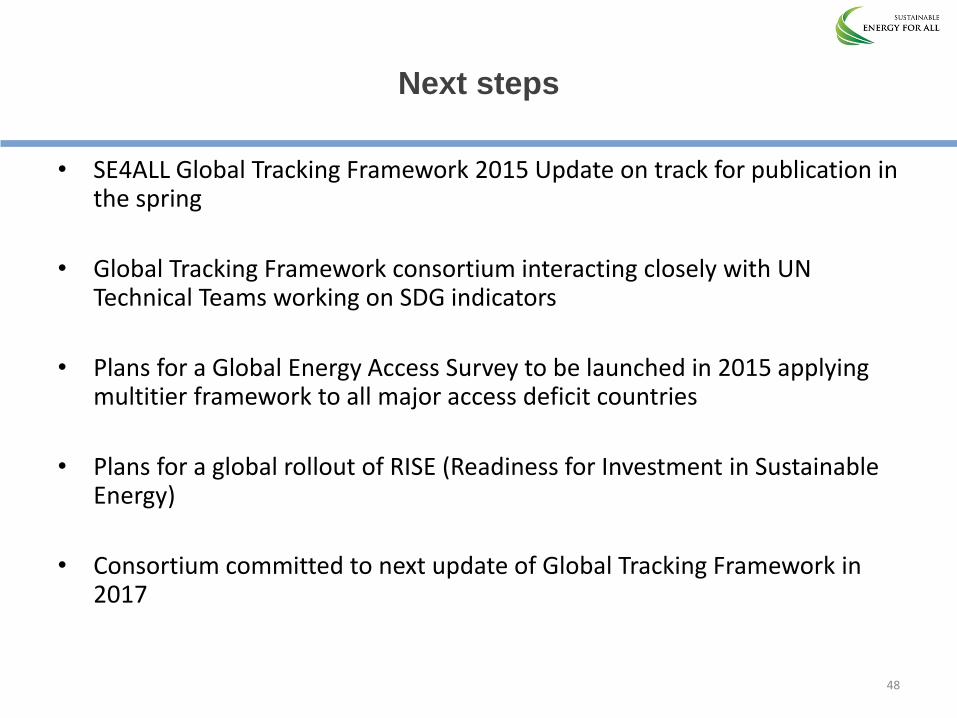

Next steps

• SE4ALL Global Tracking Framework 2015 Update on track for publication in the spring

• Global Tracking Framework consortium interacting closely with UN Technical Teams working on SDG indicators

• Plans for a Global Energy Access Survey to be launched in 2015 applying multitier framework to all major access deficit countries

• Plans for a global rollout of RISE (Readiness for Investment in Sustainable Energy)

• Consortium committed to next update of Global Tracking Framework in 2017

48

49

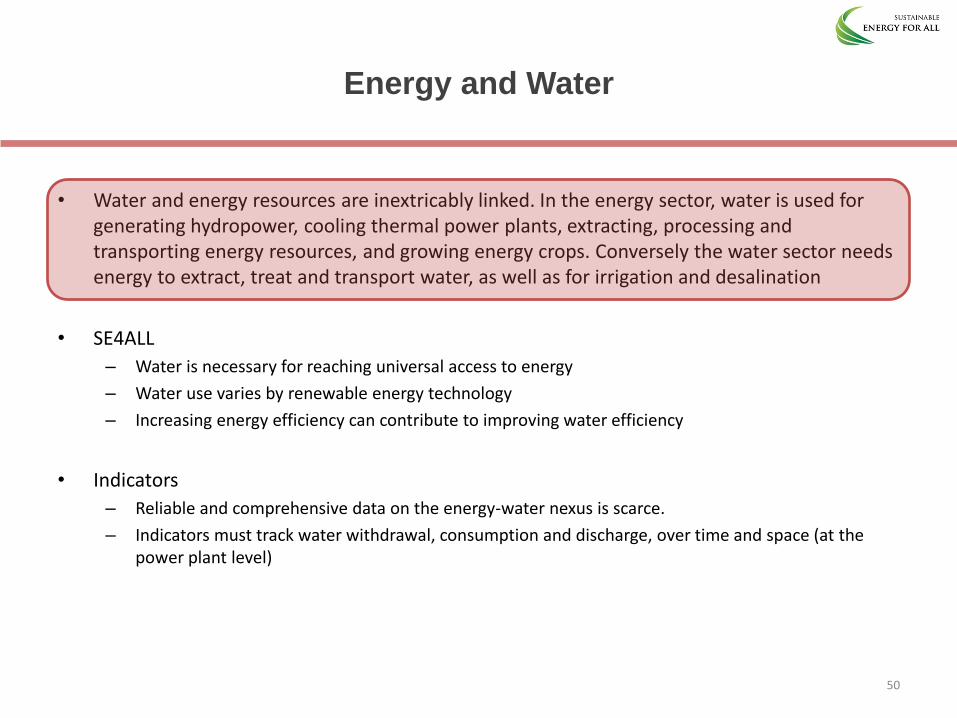

Energy and Water

• Water and energy resources are inextricably linked. In the energy sector, water is used for generating hydropower, cooling thermal power plants, extracting, processing and transporting energy resources, and growing energy crops. Conversely the water sector needs energy to extract, treat and transport water, as well as for irrigation and desalination

• SE4ALL

– Water is necessary for reaching universal access to energy

– Water use varies by renewable energy technology

– Increasing energy efficiency can contribute to improving water efficiency

• Indicators

– Reliable and comprehensive data on the energy-water nexus is scarce.

– Indicators must track water withdrawal, consumption and discharge, over time and space (at the power plant level)

50

Energy and Water, possible indicators

Water and energy nexus

Indicator Source

Water requirements of the energy sector by energy source

Global water use for energy production by scenario WWDR 2014

Water footprint of energy generation by fuel WWDR 2014

Water use for electricity generation by cooling technology ISO certification WWDR 2014

Yields and water requirements for major biofuel crops WWDR 2014

Number of energy companies disclosing their water use (withdrawal, consumption, discharge) New indicator

Water intensity (m3/GJ) by energy technology by regional climate New indicator - collected from plants

Water withdrawn and discharged by the energy sector New indicator - collected from plants

Use of alternative water sources (such as saline water and wastewater) New

Energy requirement in the water sector

Energy requirements to deliver 1m3 of water safe for human consumption from various water sources WWDR 2014

Energy requirements and cost implications of desalination by technology WWDR 2014

Power consumption trends in seawater reverse osmosis desalination WWDR 2014

Water risks for energy companies

Level of water risk to business operations CDP

Water-related business impacts in the past five years CDP

Environmental impacts of the energy sector on water resources

Quality of discharged water New indicator

Time, place, and quality of water abstraction and releases New indicator

Policy and planning

Perceived change over the past 20 years in the importance of water for energy WWDR 2014

National energy policy/strategy/plan with water resources management component WWDR 2014

Water considered at planning stage or during project development New indicator

51

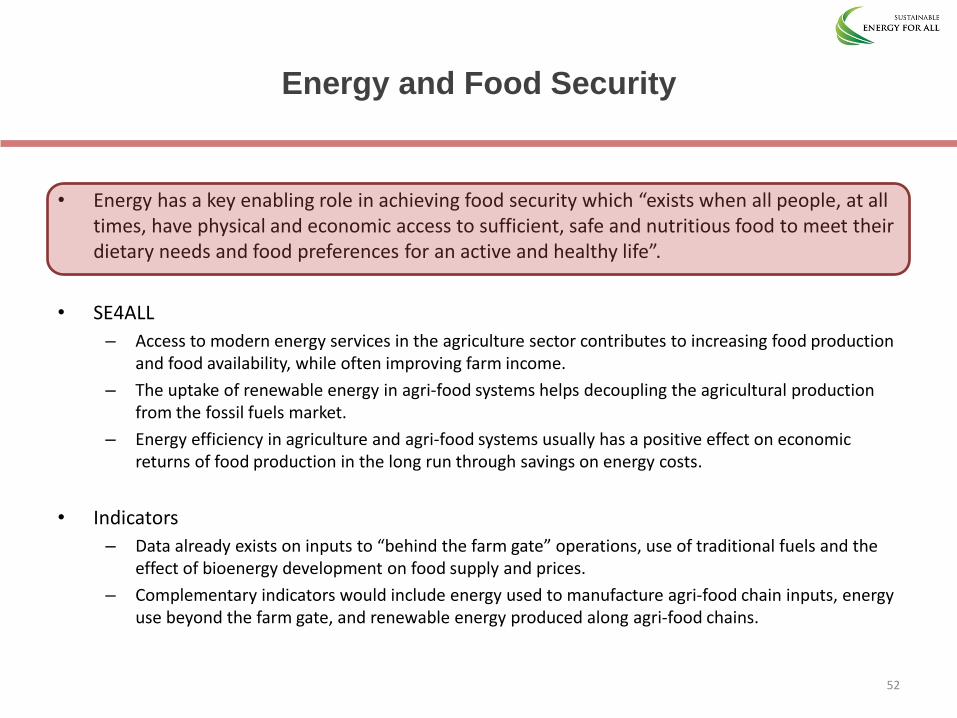

Energy and Food Security

• Energy has a key enabling role in achieving food security which “exists when all people, at all times, have physical and economic access to sufficient, safe and nutritious food to meet their dietary needs and food preferences for an active and healthy life”.

• SE4ALL

– Access to modern energy services in the agriculture sector contributes to increasing food production and food availability, while often improving farm income.

– The uptake of renewable energy in agri-food systems helps decoupling the agricultural production from the fossil fuels market.

– Energy efficiency in agriculture and agri-food systems usually has a positive effect on economic returns of food production in the long run through savings on energy costs.

• Indicators

– Data already exists on inputs to “behind the farm gate” operations, use of traditional fuels and the effect of bioenergy development on food supply and prices.

– Complementary indicators would include energy used to manufacture agri-food chain inputs, energy use beyond the farm gate, and renewable energy produced along agri-food chains.

52

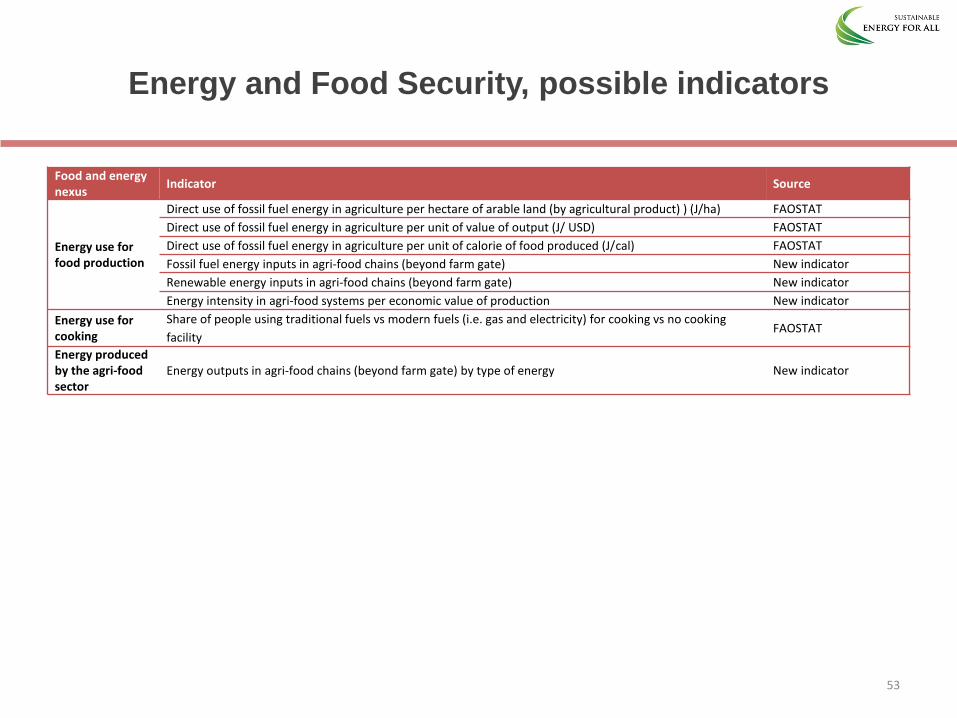

Energy and Food Security, possible indicators

Food and energy nexus

Indicator Source

Energy use for food production

Direct use of fossil fuel energy in agriculture per hectare of arable land (by agricultural product) ) (J/ha) FAOSTAT

Direct use of fossil fuel energy in agriculture per unit of value of output (J/ USD) FAOSTAT

Direct use of fossil fuel energy in agriculture per unit of calorie of food produced (J/cal) FAOSTAT

Fossil fuel energy inputs in agri-food chains (beyond farm gate) New indicator

Renewable energy inputs in agri-food chains (beyond farm gate) New indicator

Energy intensity in agri-food systems per economic value of production New indicator

Energy use for cooking

Share of people using traditional fuels vs modern fuels (i.e. gas and electricity) for cooking vs no cooking

facility FAOSTAT

Energy produced by the agri-food sector

Energy outputs in agri-food chains (beyond farm gate) by type of energy New indicator

53

Energy and Gender

• Energy interventions are likely to impact women and men differently

• SE4ALL

– Access to affordable modern energy services can reduce both time and effort spent in reproductive and productive labor, improve women’s mobility and maternal health care

– Women can, together with men, play a significant role as energy providers, expanding energy access to the poor and ‘hard to reach’ customers

– Women and men respond differently to energy efficiency incentives and energy use alternatives

• Indicators

– Existing surveys and databases shed light on the relationships between gender and energy, providing information on time poverty, women's economic empowerment, mortality and morbidity rates

– However a quantitative assessment of differential impacts of energy on the lives of women, men, girls and boys is limited.

54

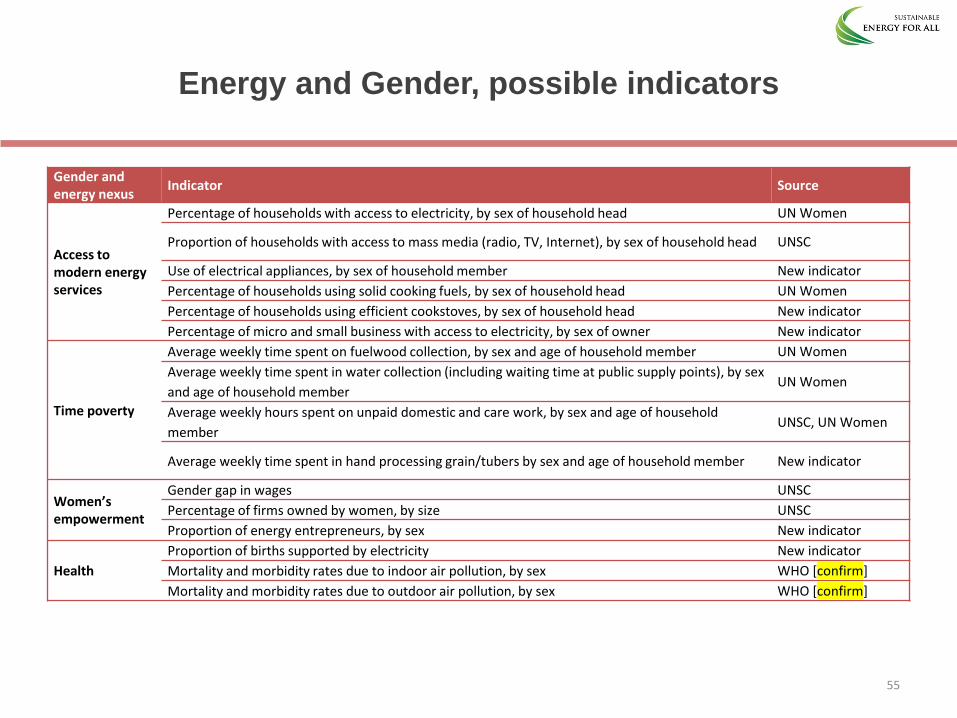

Energy and Gender, possible indicators

Gender and energy nexus

Indicator Source

Access to modern energy services

Percentage of households with access to electricity, by sex of household head UN Women

Proportion of households with access to mass media (radio, TV, Internet), by sex of household head UNSC

Use of electrical appliances, by sex of household member New indicator

Percentage of households using solid cooking fuels, by sex of household head UN Women

Percentage of households using efficient cookstoves, by sex of household head New indicator

Percentage of micro and small business with access to electricity, by sex of owner New indicator

Time poverty

Average weekly time spent on fuelwood collection, by sex and age of household member UN Women

Average weekly time spent in water collection (including waiting time at public supply points), by sex

and age of household member UN Women

Average weekly hours spent on unpaid domestic and care work, by sex and age of household

member UNSC, UN Women

Average weekly time spent in hand processing grain/tubers by sex and age of household member New indicator

Women’s empowerment

Gender gap in wages UNSC

Percentage of firms owned by women, by size UNSC

Proportion of energy entrepreneurs, by sex New indicator

Health

Proportion of births supported by electricity New indicator

Mortality and morbidity rates due to indoor air pollution, by sex WHO [confirm]

Mortality and morbidity rates due to outdoor air pollution, by sex WHO [confirm]

55

Energy and Health

• Energy is both an essential pre-requisite of good health, as well as a source of many serious health risks – most notably air pollution.

• SE4ALL

– Access to reliable and affordable modern energy services can significantly reduce the burden of disease related to household (indoor) air pollution and plays a critical role in health care provision

– Wider uptake of renewable energy, particularly for electricity, hot water heating and space heating of homes and health facilities, also have the potential to reduce indoor air pollution and enhance health care provision.

– Energy efficiency improvements in power generation, transport and buildings can yield a range of health benefits, including reduction of urban air pollution

• Indicators

– Existing indicators approximate exposure and burden of disease from indoor and outdoor air pollution. Measurement of electricity access in health care facilities is also being developed.

– Ongoing efforts to improve energy-health nexus indicators, including development of safety standards for cooking solutions, exposure rates to indoor air pollution from heating and lighting

56

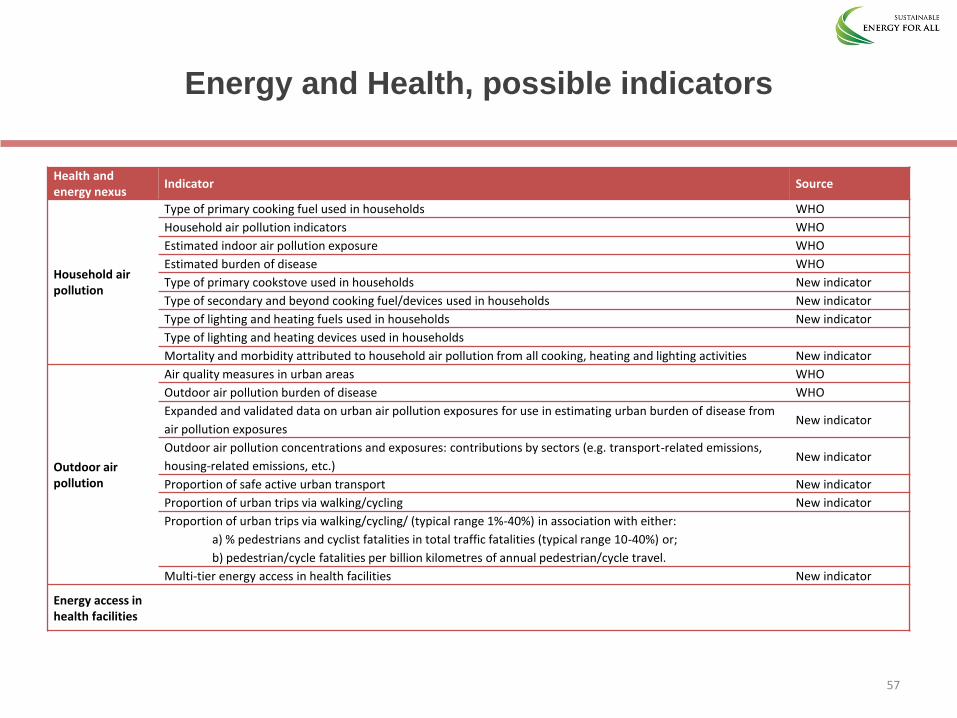

Energy and Health, possible indicators

Health and energy nexus

Indicator Source

Household air pollution

Type of primary cooking fuel used in households WHO

Household air pollution indicators WHO

Estimated indoor air pollution exposure WHO

Estimated burden of disease WHO

Type of primary cookstove used in households New indicator

Type of secondary and beyond cooking fuel/devices used in households New indicator

Type of lighting and heating fuels used in households New indicator

Type of lighting and heating devices used in households

Mortality and morbidity attributed to household air pollution from all cooking, heating and lighting activities New indicator

Outdoor air pollution

Air quality measures in urban areas WHO

Outdoor air pollution burden of disease WHO

Expanded and validated data on urban air pollution exposures for use in estimating urban burden of disease from

air pollution exposures New indicator

Outdoor air pollution concentrations and exposures: contributions by sectors (e.g. transport-related emissions,

housing-related emissions, etc.) New indicator

Proportion of safe active urban transport New indicator

Proportion of urban trips via walking/cycling New indicator

Proportion of urban trips via walking/cycling/ (typical range 1%-40%) in association with either:

a) % pedestrians and cyclist fatalities in total traffic fatalities (typical range 10-40%) or;

b) pedestrian/cycle fatalities per billion kilometres of annual pedestrian/cycle travel.

Multi-tier energy access in health facilities New indicator

Energy access in health facilities

57

ANNEX 2: FINANCE

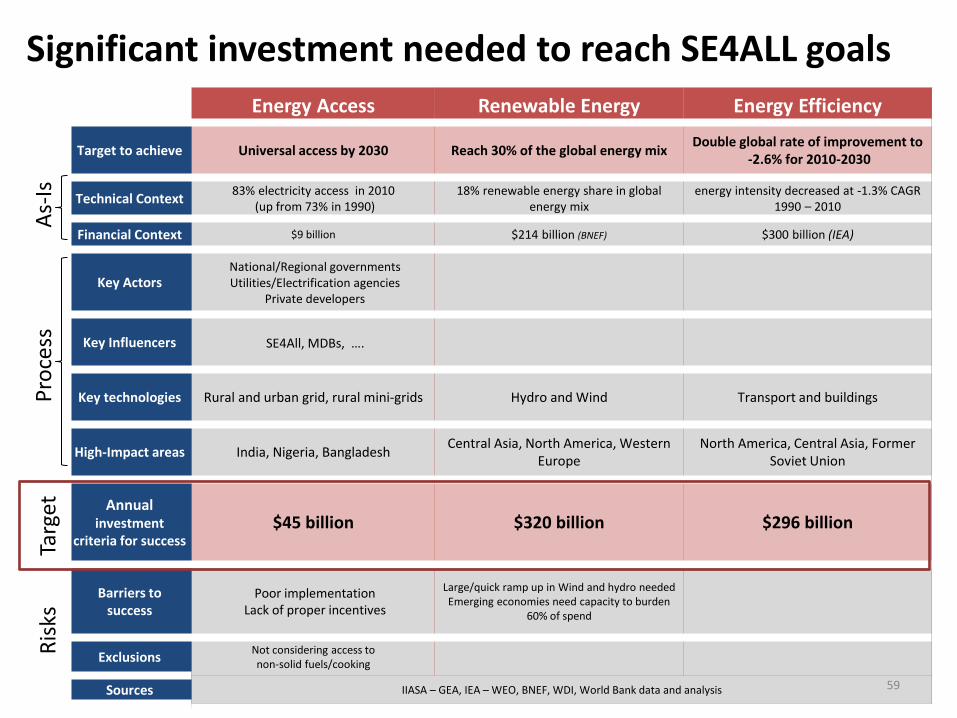

Energy Access Renewable Energy Energy Efficiency

Target to achieve Universal access by 2030 Reach 30% of the global energy mix Double global rate of improvement to

-2.6% for 2010-2030

Technical Context 83% electricity access in 2010

(up from 73% in 1990) 18% renewable energy share in global

energy mix energy intensity decreased at -1.3% CAGR

1990 – 2010

Financial Context $9 billion $214 billion (BNEF) $300 billion (IEA)

Key Actors National/Regional governments Utilities/Electrification agencies

Private developers

Key Influencers SE4All, MDBs, ….

Key technologies Rural and urban grid, rural mini-grids Hydro and Wind Transport and buildings

High-Impact areas India, Nigeria, Bangladesh Central Asia, North America, Western

Europe North America, Central Asia, Former

Soviet Union

Annual investment

criteria for success $45 billion $320 billion $296 billion

Barriers to success

Poor implementation Lack of proper incentives

Large/quick ramp up in Wind and hydro needed Emerging economies need capacity to burden

60% of spend

Exclusions Not considering access to non-solid fuels/cooking

Sources IIASA – GEA, IEA – WEO, BNEF, WDI, World Bank data and analysis

As-

Is

Pro

cess

Ta

rget

R

isks

Significant investment needed to reach SE4ALL goals

59

Sub-Saharan Africa, 38%

East Asia & Pacific,

18% East & Central Asia, 1%

Latin America &

the Caribbean,

5%

Middle East & North

Africa, 5%

South Asia, 33%

Share of Annual Investment by Region

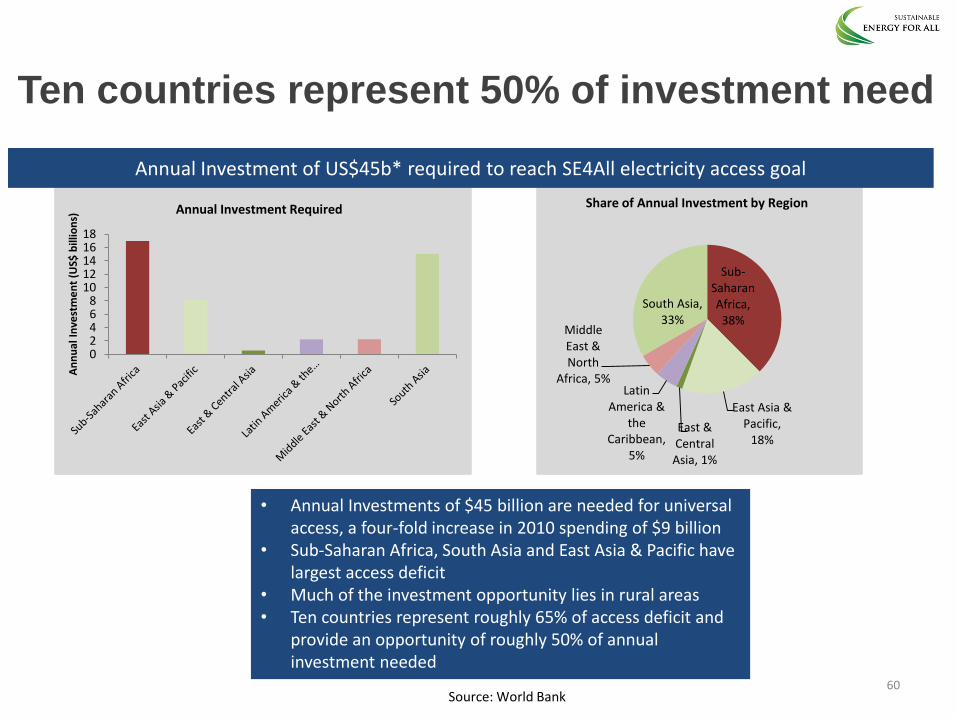

Ten countries represent 50% of investment need

• Annual Investments of $45 billion are needed for universal access, a four-fold increase in 2010 spending of $9 billion

• Sub-Saharan Africa, South Asia and East Asia & Pacific have largest access deficit

• Much of the investment opportunity lies in rural areas • Ten countries represent roughly 65% of access deficit and

provide an opportunity of roughly 50% of annual investment needed

Annual Investment of US$45b* required to reach SE4All electricity access goal

02468

1012141618

An

nu

al I

nve

stm

en

t (U

S$ b

illio

ns)

Annual Investment Required

60 Source: World Bank

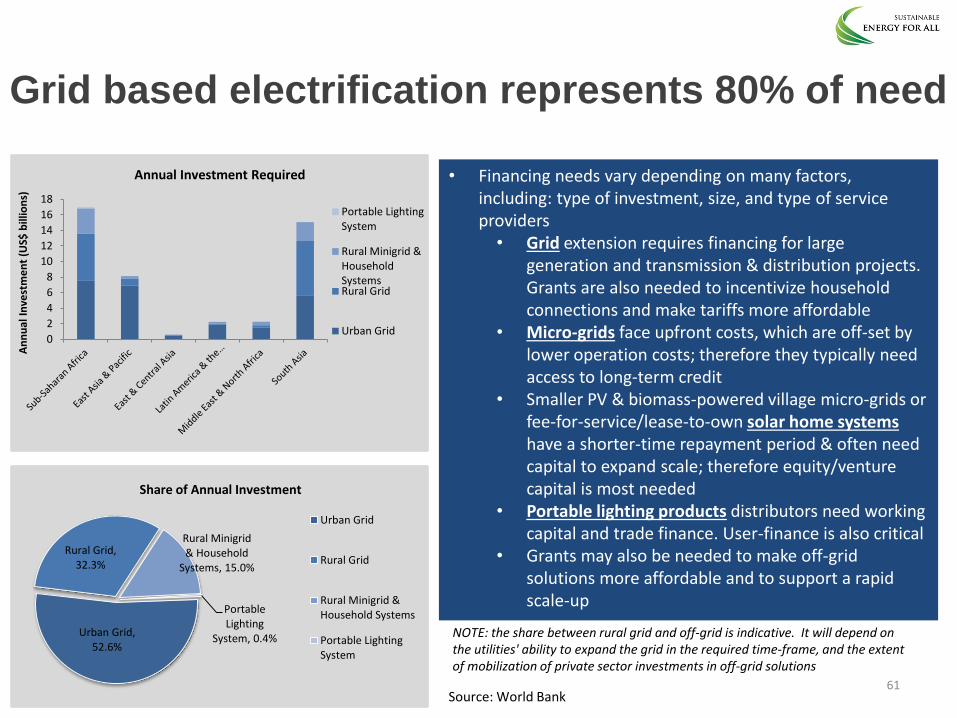

Grid based electrification represents 80% of need

• Financing needs vary depending on many factors, including: type of investment, size, and type of service providers • Grid extension requires financing for large

generation and transmission & distribution projects. Grants are also needed to incentivize household connections and make tariffs more affordable

• Micro-grids face upfront costs, which are off-set by lower operation costs; therefore they typically need access to long-term credit

• Smaller PV & biomass-powered village micro-grids or fee-for-service/lease-to-own solar home systems have a shorter-time repayment period & often need capital to expand scale; therefore equity/venture capital is most needed

• Portable lighting products distributors need working capital and trade finance. User-finance is also critical

• Grants may also be needed to make off-grid solutions more affordable and to support a rapid scale-up

61 Source: World Bank

NOTE: the share between rural grid and off-grid is indicative. It will depend on the utilities' ability to expand the grid in the required time-frame, and the extent of mobilization of private sector investments in off-grid solutions

0

2

4

6

8

10

12

14

16

18

An

nu

al I

nve

stm

en

t (U

S$ b

illio

ns)

Annual Investment Required

Portable LightingSystem

Rural Minigrid &HouseholdSystemsRural Grid

Urban Grid

Urban Grid, 52.6%

Rural Grid, 32.3%

Rural Minigrid & Household

Systems, 15.0%

Portable Lighting

System, 0.4%

Share of Annual Investment

Urban Grid

Rural Grid

Rural Minigrid &Household Systems

Portable LightingSystem

0

10

20

30

40

50

60

An

nu

al I

nve

stm

en

t (U

S$ b

illio

ns)

Avg. Annual Demand-Side Investment Required

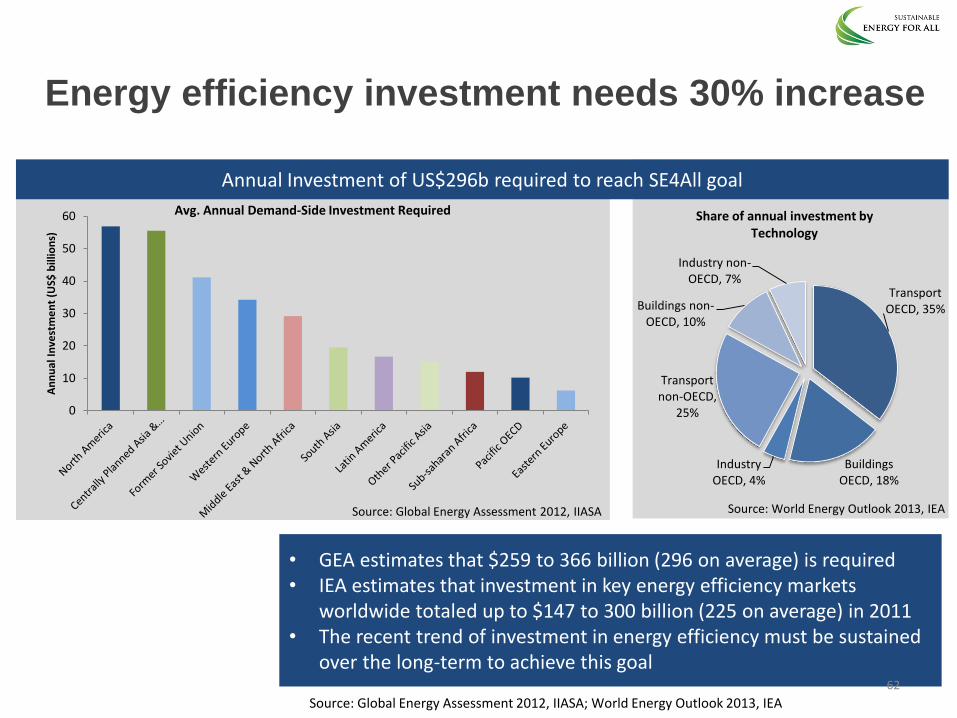

Energy efficiency investment needs 30% increase

• GEA estimates that $259 to 366 billion (296 on average) is required • IEA estimates that investment in key energy efficiency markets

worldwide totaled up to $147 to 300 billion (225 on average) in 2011 • The recent trend of investment in energy efficiency must be sustained

over the long-term to achieve this goal

Transport OECD, 35%

Buildings OECD, 18%

Industry OECD, 4%

Transport non-OECD,

25%

Buildings non-OECD, 10%

Industry non-OECD, 7%

Share of annual investment by Technology

Source: World Energy Outlook 2013, IEA

62

Annual Investment of US$296b required to reach SE4All goal

Source: Global Energy Assessment 2012, IIASA

Source: Global Energy Assessment 2012, IIASA; World Energy Outlook 2013, IEA

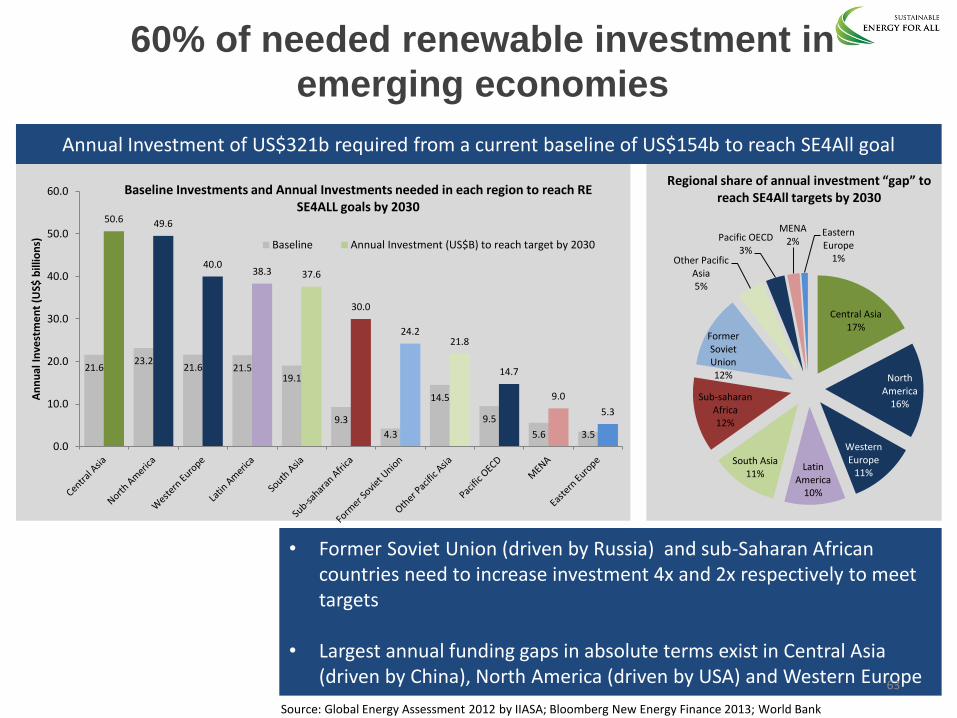

60% of needed renewable investment in

emerging economies

21.6 23.2

21.6 21.5 19.1

9.3

4.3

14.5

9.5

5.6 3.5

50.6 49.6

40.0 38.3 37.6

30.0

24.2 21.8

14.7

9.0

5.3

0.0

10.0

20.0

30.0

40.0

50.0

60.0

An

nu

al I

nve

stm

en

t (U

S$ b

illio

ns)

Baseline Investments and Annual Investments needed in each region to reach RE SE4ALL goals by 2030

Baseline Annual Investment (US$B) to reach target by 2030

Central Asia 17%

North America

16%

Western Europe

11% Latin

America 10%

South Asia 11%

Sub-saharan Africa 12%

Former Soviet Union 12%

Other Pacific Asia 5%

Pacific OECD 3%

MENA 2%

Eastern Europe

1%

Regional share of annual investment “gap” to reach SE4All targets by 2030

• Former Soviet Union (driven by Russia) and sub-Saharan African countries need to increase investment 4x and 2x respectively to meet targets

• Largest annual funding gaps in absolute terms exist in Central Asia

(driven by China), North America (driven by USA) and Western Europe

Annual Investment of US$321b required from a current baseline of US$154b to reach SE4All goal

63

Source: Global Energy Assessment 2012 by IIASA; Bloomberg New Energy Finance 2013; World Bank

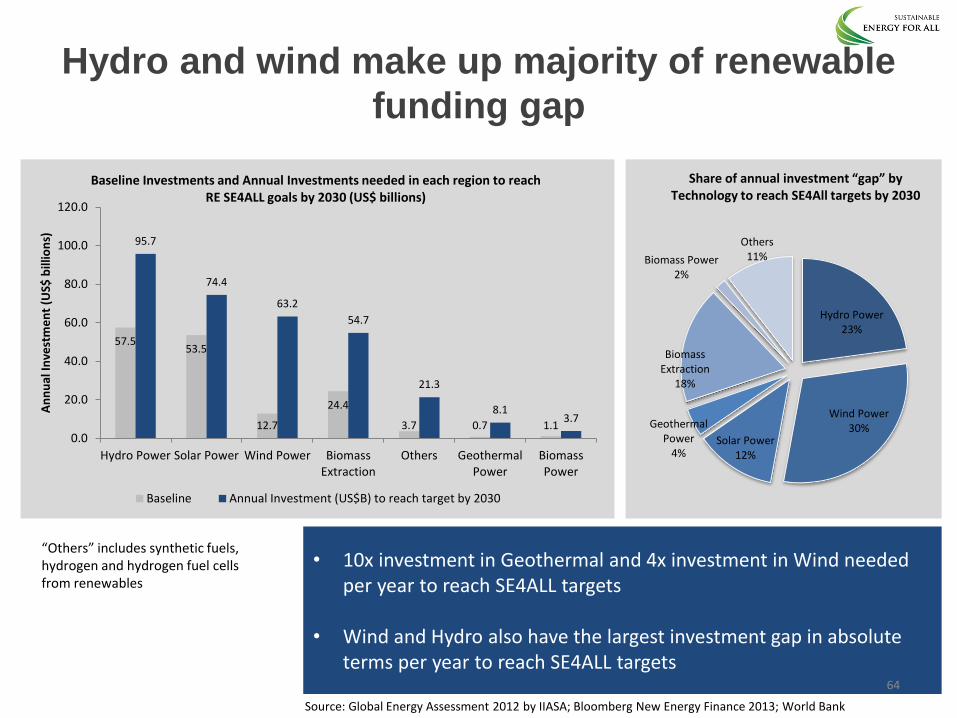

Hydro Power 23%

Wind Power 30%

Solar Power 12%

Geothermal Power

4%

Biomass Extraction

18%

Biomass Power 2%

Others 11%

Share of annual investment “gap” by Technology to reach SE4All targets by 2030

Hydro and wind make up majority of renewable

funding gap

• 10x investment in Geothermal and 4x investment in Wind needed per year to reach SE4ALL targets

• Wind and Hydro also have the largest investment gap in absolute terms per year to reach SE4ALL targets

“Others” includes synthetic fuels, hydrogen and hydrogen fuel cells from renewables

57.5 53.5

12.7

24.4

3.7 0.7 1.1

95.7

74.4

63.2

54.7

21.3

8.1 3.7

0.0

20.0

40.0

60.0

80.0

100.0

120.0

Hydro Power Solar Power Wind Power BiomassExtraction

Others GeothermalPower

BiomassPower

An

nu

al In

vest

me

nt

(US$

bill

ion

s)

Baseline Investments and Annual Investments needed in each region to reach RE SE4ALL goals by 2030 (US$ billions)

Baseline Annual Investment (US$B) to reach target by 2030

64

Source: Global Energy Assessment 2012 by IIASA; Bloomberg New Energy Finance 2013; World Bank

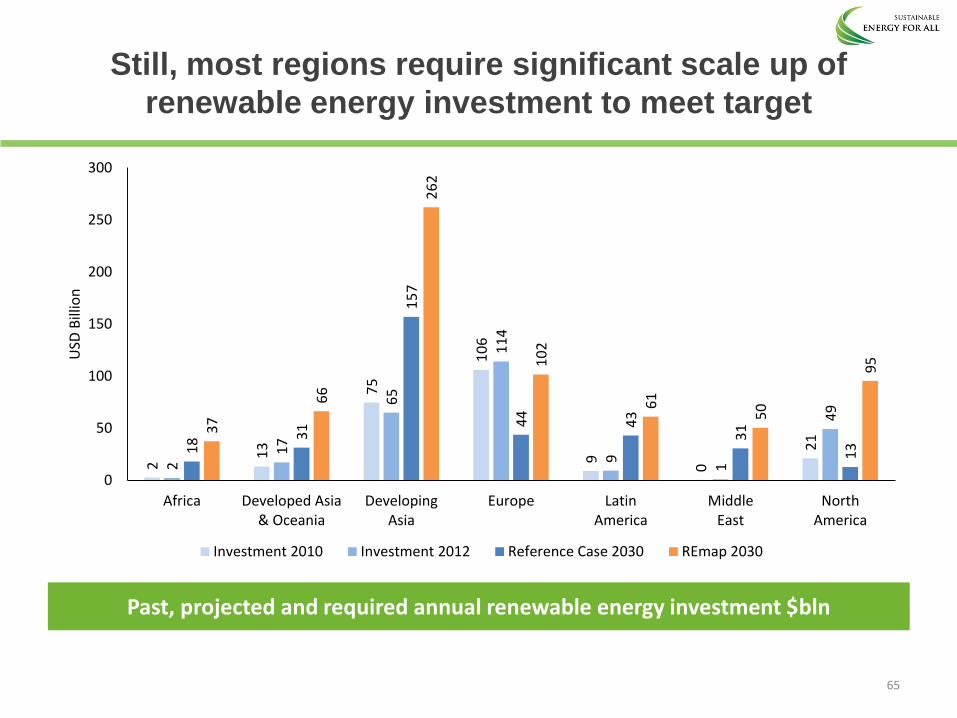

Still, most regions require significant scale up of

renewable energy investment to meet target

Past, projected and required annual renewable energy investment $bln

2 1

3

75

10

6

9

0

21

2 1

7

65

11

4

9

1

49

18

31

15

7

44

43

31

13

37

66

26

2

10

2

61

50

95

0

50

100

150

200

250

300

Africa Developed Asia& Oceania

DevelopingAsia

Europe LatinAmerica

MiddleEast

NorthAmerica

USD

Bill

ion

Investment 2010 Investment 2012 Reference Case 2030 REmap 2030

65

Recommended