WISCONSIN FREIGHT RAIL DAYOCTOBER 26, 2012

Superior Silica Sands“We’re in the Logistics Business”

Rick ShearerPresident & CEOSuperior Silica Sands

WELL STIMULATION AND FRACTURING

Hydraulic fracturing is a well stimulation process to optimize or restore production of oil and gas Over 90% of the wells drilled in the U.S. now require hydraulic fracturing to produce at economic rates,

according to IPAA Fractures created along the borehole of a well increases the surface area exposed and operators are able

to produce 10 times the amount of energy while drilling 1/10 th the number of wells Fractures created are kept open using a proppant – typically sieved round sand, a resin coated sand or a

manufactured ceramic proppant Proppant accounts for approximately 10 – 15% of the total cost of drilling and completing a typical

horizontal well

1

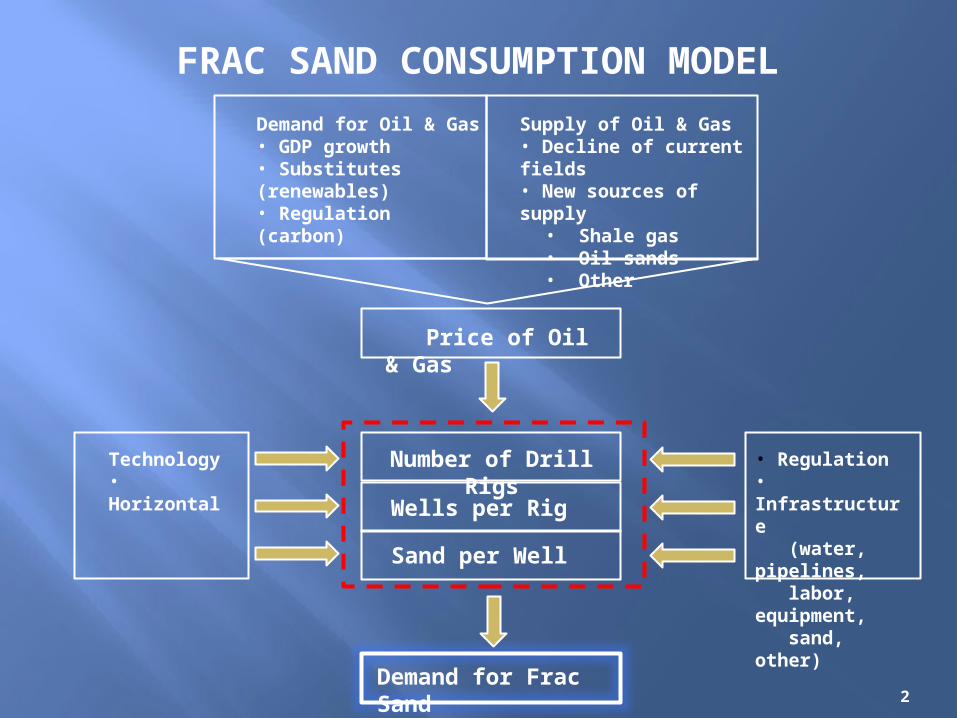

FRAC SAND CONSUMPTION MODEL

Demand for Oil & Gas• GDP growth• Substitutes (renewables)• Regulation (carbon)

Supply of Oil & Gas• Decline of current fields• New sources of supply• Shale gas• Oil sands• Other

Price of Oil & Gas

Number of Drill Rigs

Wells per Rig

Sand per Well

Demand for Frac Sand

Technology• Horizontal drilling• Hydraulic fracturing

• Regulation• Infrastructure (water, pipelines, labor, equipment, sand, other)

2

Atwood Industry Review 20070601 v2

DRIVERS OF DEMAND FOR FRAC SAND

NUMBER OF RIGS SAND PER WELLWELLS PER RIG

• The number of wells drilled per rig per year has increased by 50% since 2002

• This improvement has been caused primarily by the rise of horizontal drilling and hydraulic fracturing

• 3.8% annual growth since 2002

• There is a very modest amount of sand consumed for vertical drilling

• The penetration of horizontal drilling and hydraulic fracturing has greatly increased the average amount of sand used per well drilled

• 30.8% annual growth since 2002

Sources: EIA; US Geological Survey; Baker Hughes

Frac sand consumption is a product of 3 variables:

-

50

100

150

200

250

300

350

400

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Sand

per

Wel

l (to

ns)

3

• Historically, the number of rigs has been primarily driven by the price of energy

• Horizontal drilling and hydraulic fracturing make it economic to drill at much lower price levels for oil and gas

• 9.5% annual growth since 2002

-

500

1,000

1,500

2,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Ann

ual R

ig C

ount

HORIZONTAL DRILLING PENETRATION

4

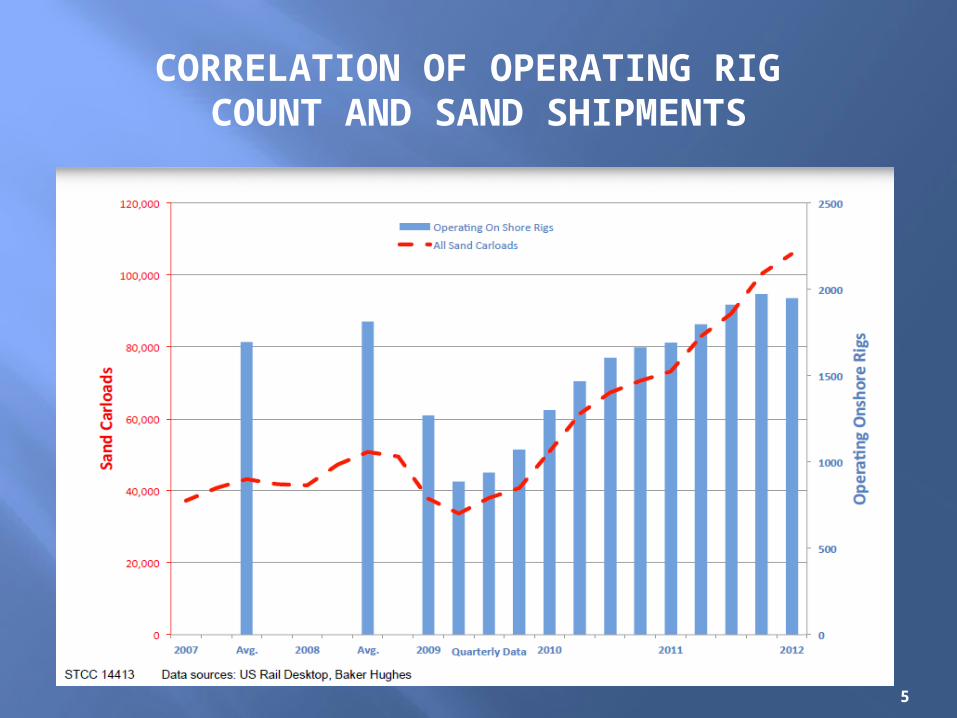

CORRELATION OF OPERATING RIG COUNT AND SAND SHIPMENTS

5

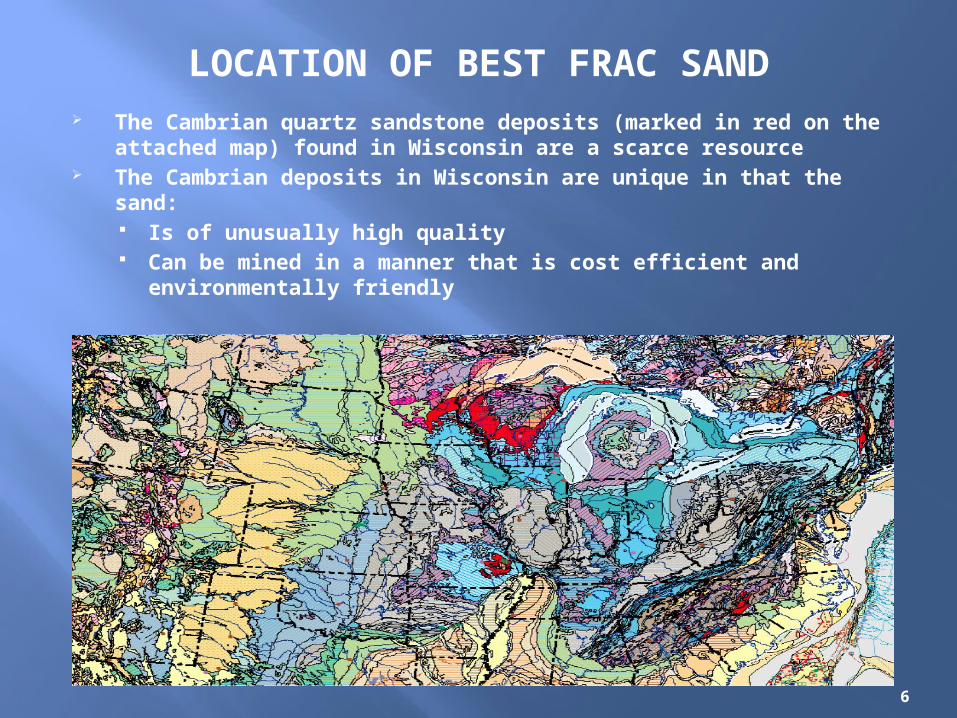

LOCATION OF BEST FRAC SAND The Cambrian quartz sandstone deposits (marked in red on the attached map) found

in Wisconsin are a scarce resource The Cambrian deposits in Wisconsin are unique in that the sand:

Is of unusually high quality Can be mined in a manner that is cost efficient and environmentally friendly

WHERE THE BEST FRAC SAND IS (RED)

Source: Where-the-best-sand-is – Brown Presentation

6

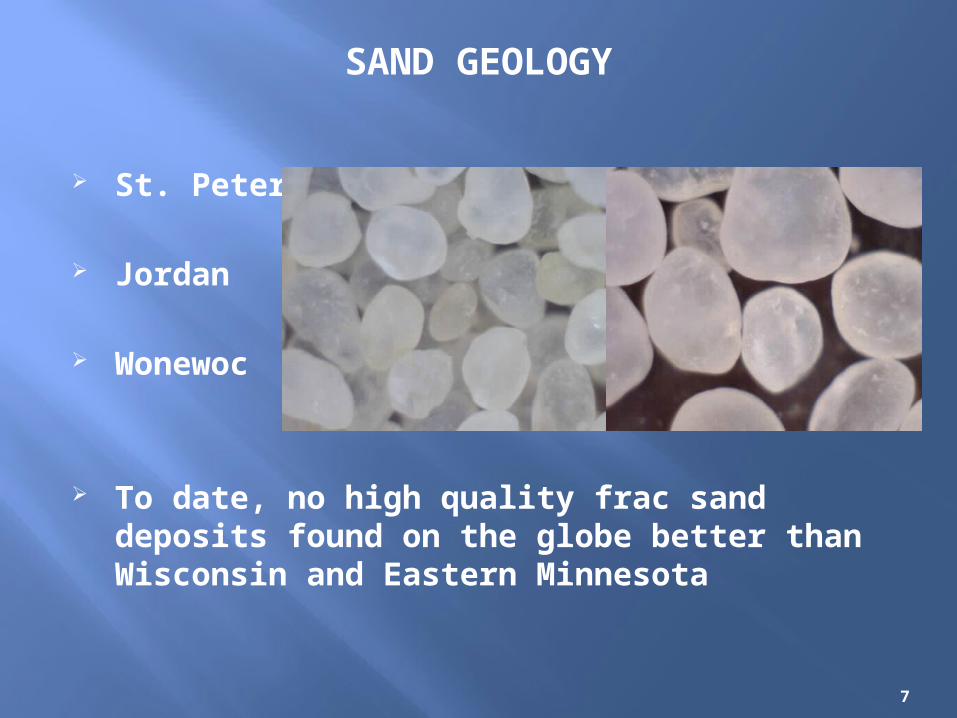

St. Peter’s

Jordan

Wonewoc

To date, no high quality frac sand deposits found on the globe better than Wisconsin and Eastern Minnesota

SAND GEOLOGY

7

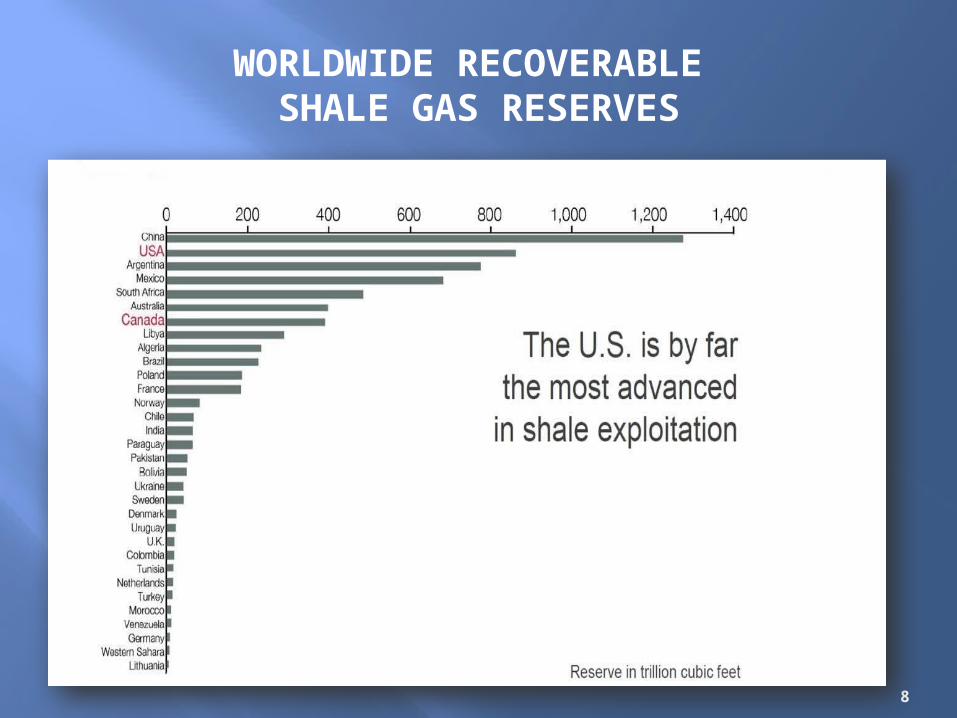

WORLDWIDE RECOVERABLE SHALE GAS RESERVES

8

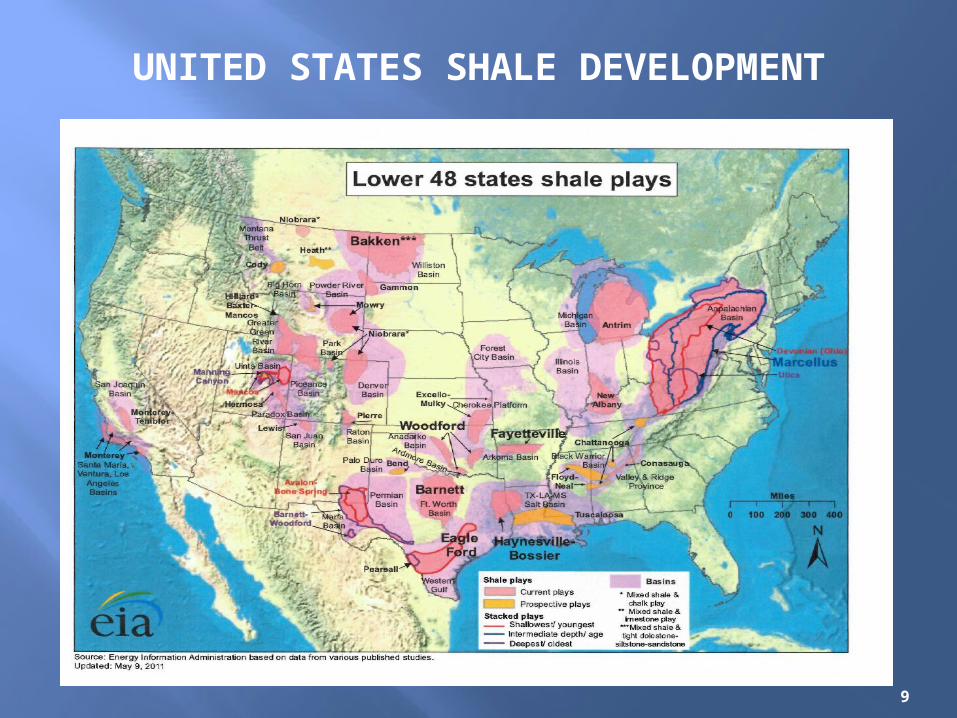

UNITED STATES SHALE DEVELOPMENT

9

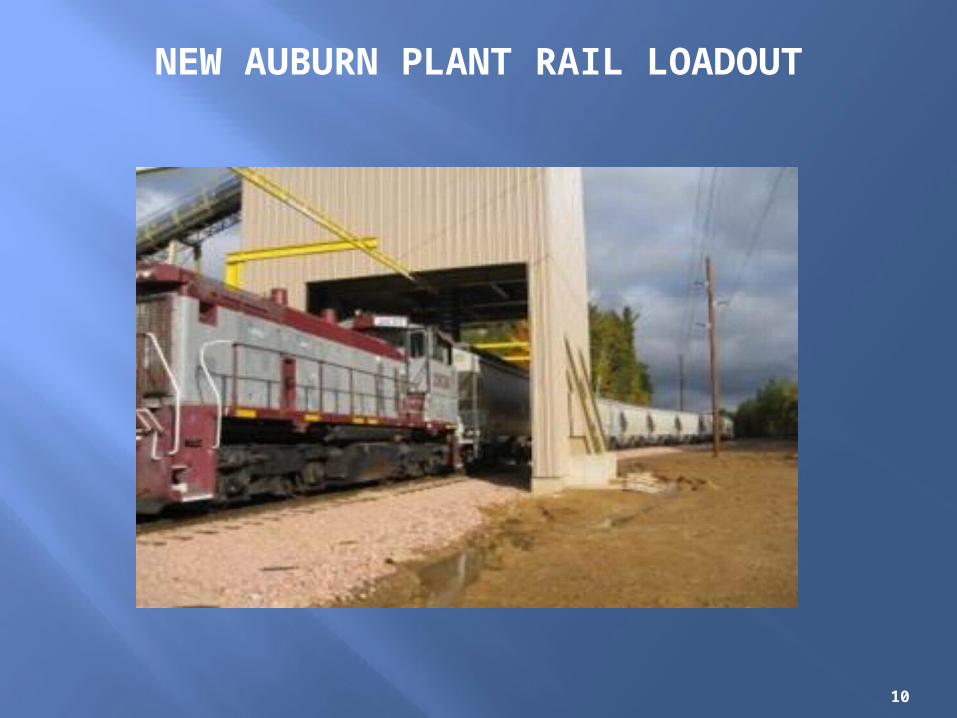

NEW AUBURN PLANT RAIL LOADOUT

10

CLINTON PLANT

11

FRAC SAND PRODUCER SUCCESS IS BASEDON THE

SUPPLIER’S LOGISTICS CAPABILITIES

12

Rail Infra-structure at Plant

Storage Track at Plant

Rail Service

Transit Time to Strategic Destinations

One-Line Haul Capabilities

Competitive Rates

Destination Storage/Transload Services

By definition, “We are in the Logistics Business”

SUPERIOR SILICA SANDS COMMITMENT TOOUTSTANDING LOGISTICS FOR OUR

CUSTOMERS

13

New Auburn Plant: Directly on Progressive Rail Short-Line to UP Railroad @ ALTOONA 260 Railcar Storage Capability

Clinton Plant: Directly on CN Rail 500 Railcar Storage Capability

Providing our Customers shipment flexibility throughout North America

Building a network of storage/transload locations

Oil & Gas Service Companies are demanding more…

SSS PARTNERED RAIL LINES

14

Canadian National Union Pacific

FRAC SAND: LOOKING INTO THE FUTURE

Dramatic annual growth will level off to about 8% per annum

Frac Market will be cyclical, but with milder peaks and troughs

More capacity coming into the market but leaders remain

International Markets will begin to show significant frac sand demand

Sand producer base will diversify as Service Companies and E&P’s back integrate

Logistics will drive economics

15

WHAT IT ALL MEANS TO YOU …. THE RAILROADS

Shipping more sand to numerous new destinations Unit train shipments more common Managing bottlenecks and turnaround times becomes

more crucial With freight prices not dropping, service is king Storage and Transload sites are over populated in some

locales Railroad Partnerships

16

CONCLUSIONS

The Frac Sand Boom is a “Once in a Lifetime” event. Wisconsin is the Global Epicenter Efficiency and cost Effectiveness in shipping this

important proppant is critical Rail is a major focal point to complete market success Any successful frac sand producer is actually in the

Logistics Business!

17

Recommended