South East Asia’s Pharmerging Landscape

IBC Asia South East Asia Pharmaceutical Forum

Sep 2012

Singapore

Over the next 30 minutes we will touch briefly upon…

• The “Asian” Pharmerging Markets and growth opportunities therein

• Dynamics & trends that make South East Asia a unique and challenging environment

• Key success factors in South East Asia

2

• Q&A

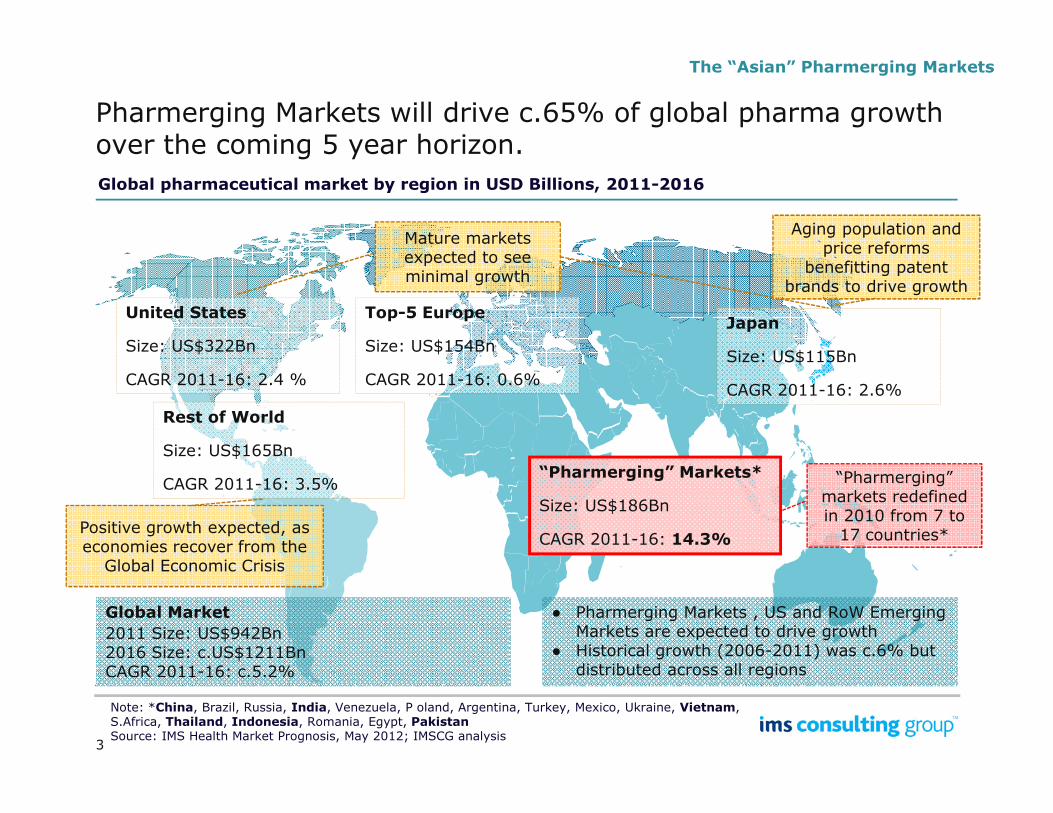

Pharmerging Markets will drive c.65% of global pharma growth over the coming 5 year horizon.

The “Asian” Pharmerging Markets

Global pharmaceutical market by region in USD Billions, 2011-2016

United States

Size: US$322Bn

CAGR 2011-16: 2.4 %

Japan

Size: US$115Bn

CAGR 2011-16: 2.6%

Top-5 Europe

Size: US$154Bn

CAGR 2011-16: 0.6%

Rest of World

Mature markets expected to see minimal growth

Aging population and price reforms

benefitting patent brands to drive growth

3

Note: *China, Brazil, Russia, India, Venezuela, P oland, Argentina, Turkey, Mexico, Ukraine, Vietnam, S.Africa, Thailand, Indonesia, Romania, Egypt, PakistanSource: IMS Health Market Prognosis, May 2012; IMSCG analysis

“Pharmerging” Markets*

Size: US$186Bn

CAGR 2011-16: 14.3%

Rest of World

Size: US$165Bn

CAGR 2011-16: 3.5% “Pharmerging”markets redefined in 2010 from 7 to 17 countries*Positive growth expected, as

economies recover from the Global Economic Crisis

Global Market

2011 Size: US$942Bn2016 Size: c.US$1211BnCAGR 2011-16: c.5.2%

● Pharmerging Markets , US and RoW Emerging Markets are expected to drive growth

● Historical growth (2006-2011) was c.6% but distributed across all regions

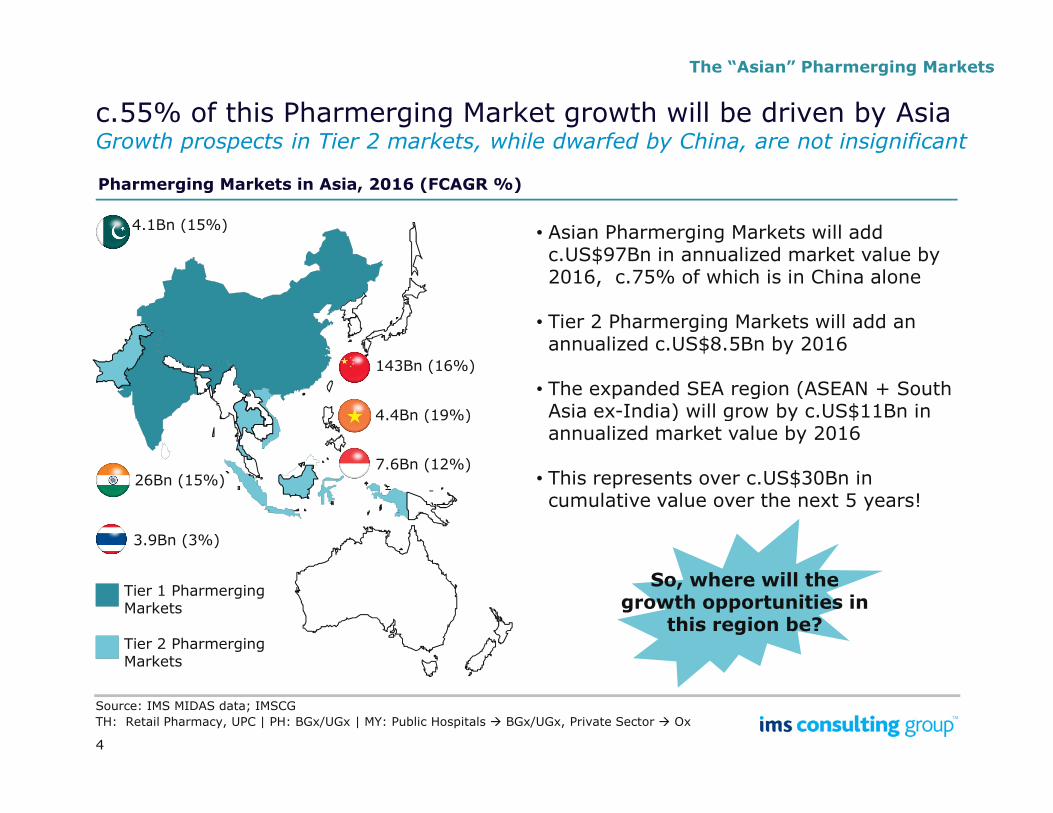

c.55% of this Pharmerging Market growth will be driven by AsiaGrowth prospects in Tier 2 markets, while dwarfed by China, are not insignificant

The “Asian” Pharmerging Markets

Pharmerging Markets in Asia, 2016 (FCAGR %)

• Asian Pharmerging Markets will add c.US$97Bn in annualized market value by 2016, c.75% of which is in China alone

• Tier 2 Pharmerging Markets will add an annualized c.US$8.5Bn by 2016

• The expanded SEA region (ASEAN + South Asia ex-India) will grow by c.US$11Bn in

143Bn (16%)

4.1Bn (15%)

4.4Bn (19%)

4

Tier 1 PharmergingMarkets

Source: IMS MIDAS data; IMSCG

Asia ex-India) will grow by c.US$11Bn in annualized market value by 2016

• This represents over c.US$30Bn in cumulative value over the next 5 years!

Tier 2 PharmergingMarkets

26Bn (15%)

3.9Bn (3%)

7.6Bn (12%)

4.4Bn (19%)

TH: Retail Pharmacy, UPC | PH: BGx/UGx | MY: Public Hospitals � BGx/UGx, Private Sector � Ox

So, where will the growth opportunities in

this region be?

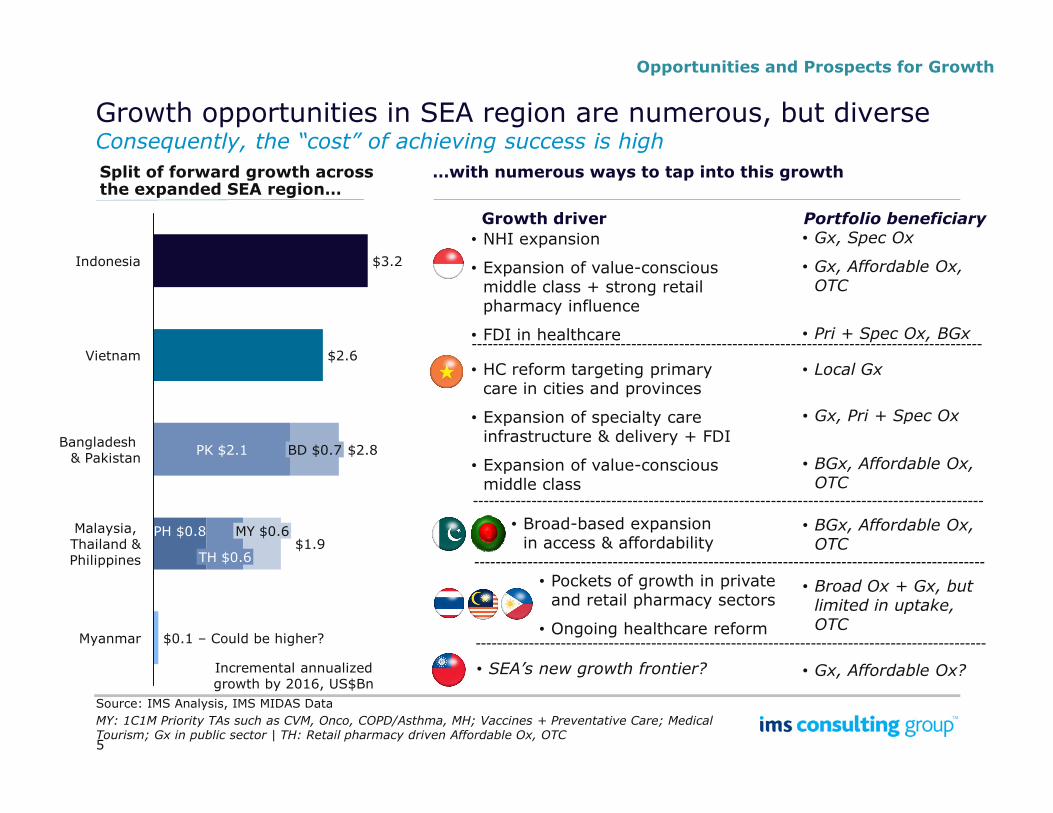

Growth opportunities in SEA region are numerous, but diverseConsequently, the “cost” of achieving success is high

Opportunities and Prospects for Growth

…with numerous ways to tap into this growthSplit of forward growth across the expanded SEA region…

• NHI expansion

• Expansion of value-conscious middle class + strong retail pharmacy influence

• FDI in healthcare

Growth driver Portfolio beneficiary

• HC reform targeting primary care in cities and provinces

Expansion of specialty care

• Gx, Spec Ox

• Gx, Affordable Ox, OTC

• Pri + Spec Ox, BGx

Vietnam $2.6

Indonesia $3.2

• Local Gx

• Gx, Pri + Spec Ox

5

• Expansion of specialty care infrastructure & delivery + FDI

• Expansion of value-conscious middle class

• Broad-based expansion in access & affordability

• Pockets of growth in private and retail pharmacy sectors

• Ongoing healthcare reform

• SEA’s new growth frontier?

$1.9TH $0.6

Malaysia, Thailand &Philippines

PK $2.1Bangladesh & Pakistan

Myanmar

MY $0.6

$0.1 – Could be higher?

$2.8

PH $0.8

BD $0.7

Incremental annualized growth by 2016, US$Bn

Source: IMS Analysis, IMS MIDAS Data

• Gx, Pri + Spec Ox

• BGx, Affordable Ox, OTC

• BGx, Affordable Ox, OTC

• Broad Ox + Gx, but limited in uptake, OTC

MY: 1C1M Priority TAs such as CVM, Onco, COPD/Asthma, MH; Vaccines + Preventative Care; Medical Tourism; Gx in public sector | TH: Retail pharmacy driven Affordable Ox, OTC

• Gx, Affordable Ox?

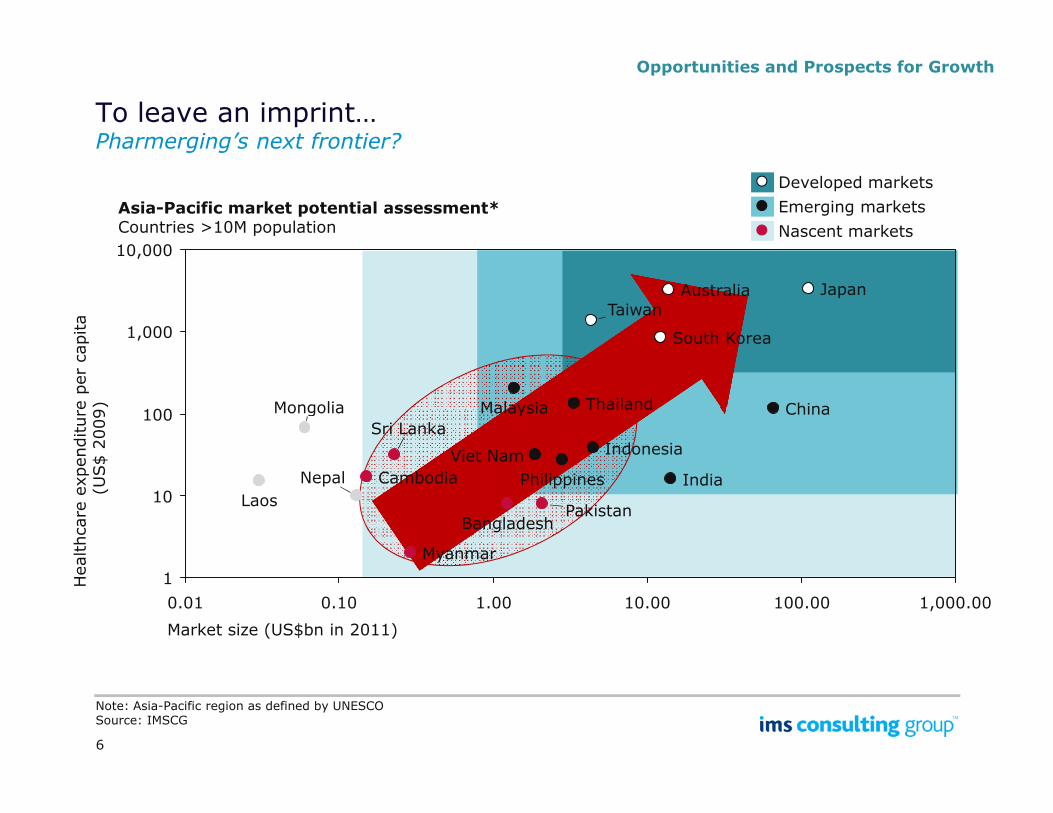

To leave an imprint…Pharmerging’s next frontier?

Asia-Pacific market potential assessment*Countries >10M population Nascent markets

Emerging markets

Developed markets

Healthcare expenditure per capita

(US$ 2009)

10,000

1,000

100 Mongolia ThailandMalaysia China

Taiwan

South Korea

JapanAustralia

Opportunities and Prospects for Growth

6

Note: Asia-Pacific region as defined by UNESCOSource: IMSCG

Healthcare expenditure per capita

(US$ 2009)

100

10

1

Market size (US$bn in 2011)

1,000.00100.0010.001.000.100.01

Nepal

Mongolia

Laos

Sri Lanka

Pakistan

Myanmar

Cambodia

Bangladesh

Viet Nam

Thailand

Philippines

Malaysia

Indonesia

India

China

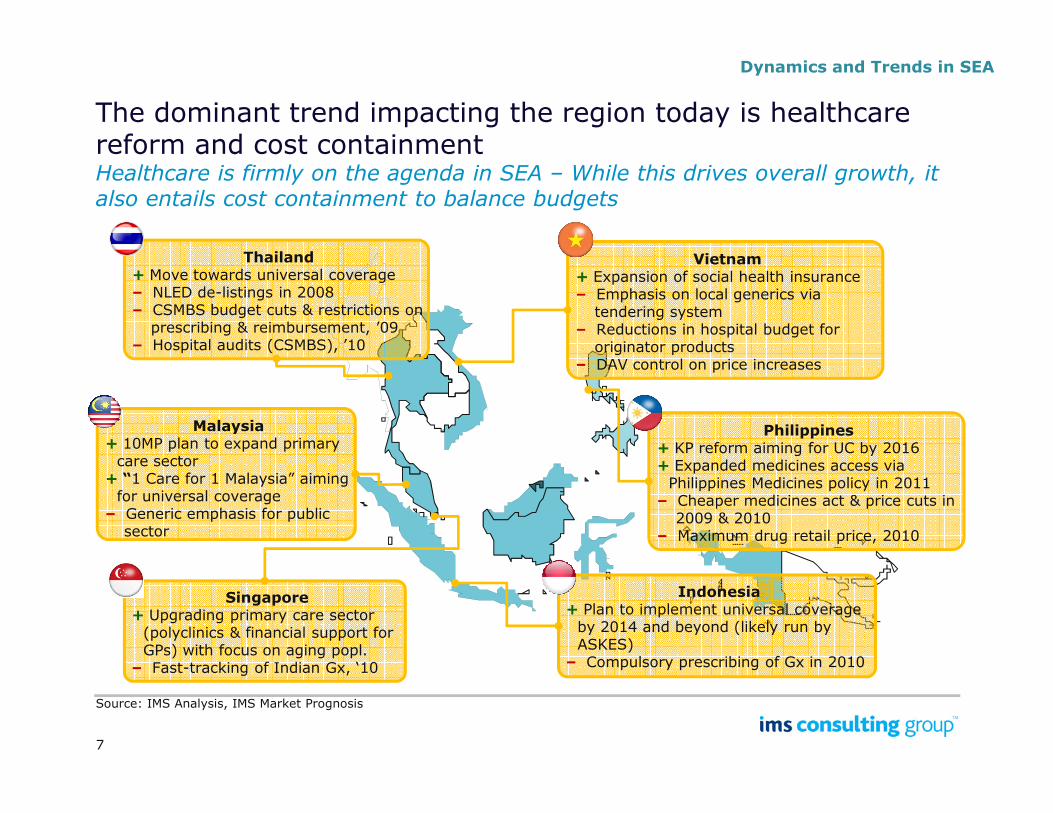

The dominant trend impacting the region today is healthcare reform and cost containment Healthcare is firmly on the agenda in SEA – While this drives overall growth, it also entails cost containment to balance budgets

Dynamics and Trends in SEA

Thailand+ Move towards universal coverage – NLED de-listings in 2008– CSMBS budget cuts & restrictions on

prescribing & reimbursement, ’09– Hospital audits (CSMBS), ’10

Vietnam+ Expansion of social health insurance– Emphasis on local generics via

tendering system– Reductions in hospital budget for

originator products– DAV control on price increases

7

Malaysia+ 10MP plan to expand primary care sector+ “1 Care for 1 Malaysia” aiming for universal coverage– Generic emphasis for public

sector

Indonesia + Plan to implement universal coverage by 2014 and beyond (likely run by ASKES)– Compulsory prescribing of Gx in 2010

Singapore+ Upgrading primary care sector (polyclinics & financial support for GPs) with focus on aging popl.– Fast-tracking of Indian Gx, ‘10

Philippines+ KP reform aiming for UC by 2016+ Expanded medicines access via Philippines Medicines policy in 2011– Cheaper medicines act & price cuts in

2009 & 2010– Maximum drug retail price, 2010

Source: IMS Analysis, IMS Market Prognosis

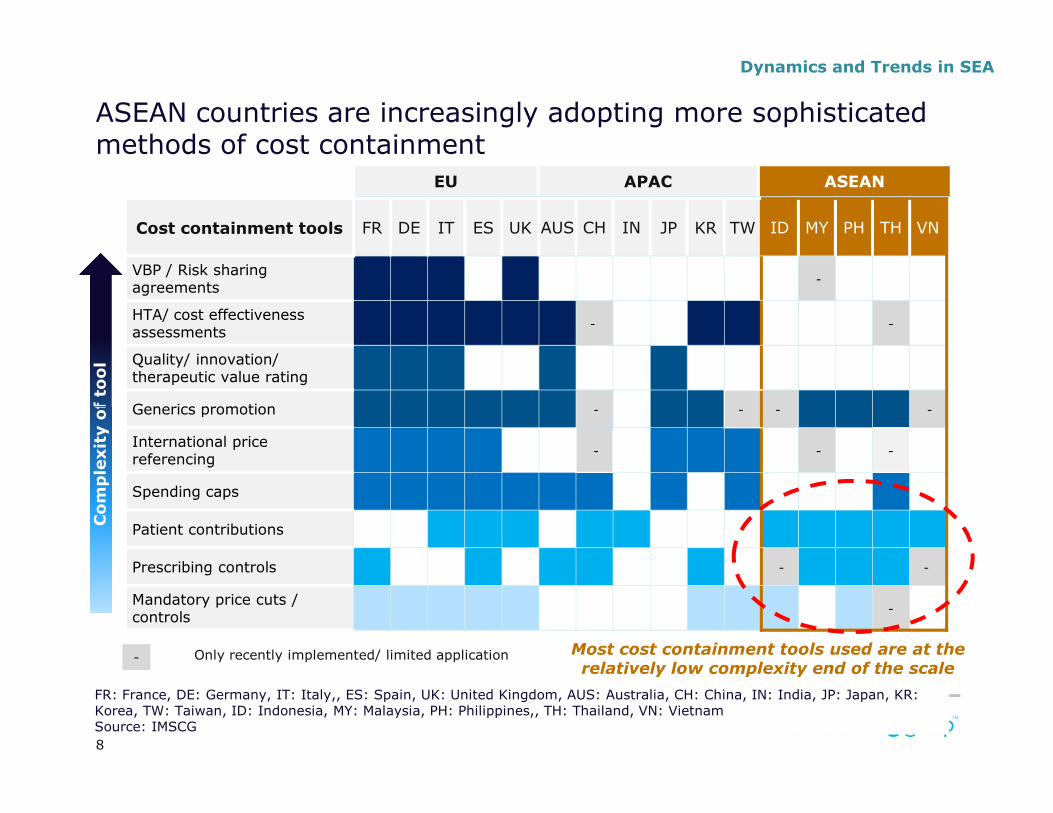

Cost containment tools FR DE IT ES UK AUS CH IN JP KR TW ID MY PH TH VN

VBP / Risk sharing agreements

-

HTA/ cost effectiveness assessments

- -

Quality/ innovation/ therapeutic value rating

Generics promotion - - - -

EU APAC ASEAN

of tool

ASEAN countries are increasingly adopting more sophisticated methods of cost containment

Dynamics and Trends in SEA

8

Generics promotion - - - -

International price referencing

- - -

Spending caps

Patient contributions

Prescribing controls - -

Mandatory price cuts / controls

-

Only recently implemented/ limited application

Complexity of tool

FR: France, DE: Germany, IT: Italy,, ES: Spain, UK: United Kingdom, AUS: Australia, CH: China, IN: India, JP: Japan, KR: Korea, TW: Taiwan, ID: Indonesia, MY: Malaysia, PH: Philippines,, TH: Thailand, VN: VietnamSource: IMSCG

Most cost containment tools used are at the relatively low complexity end of the scale

-

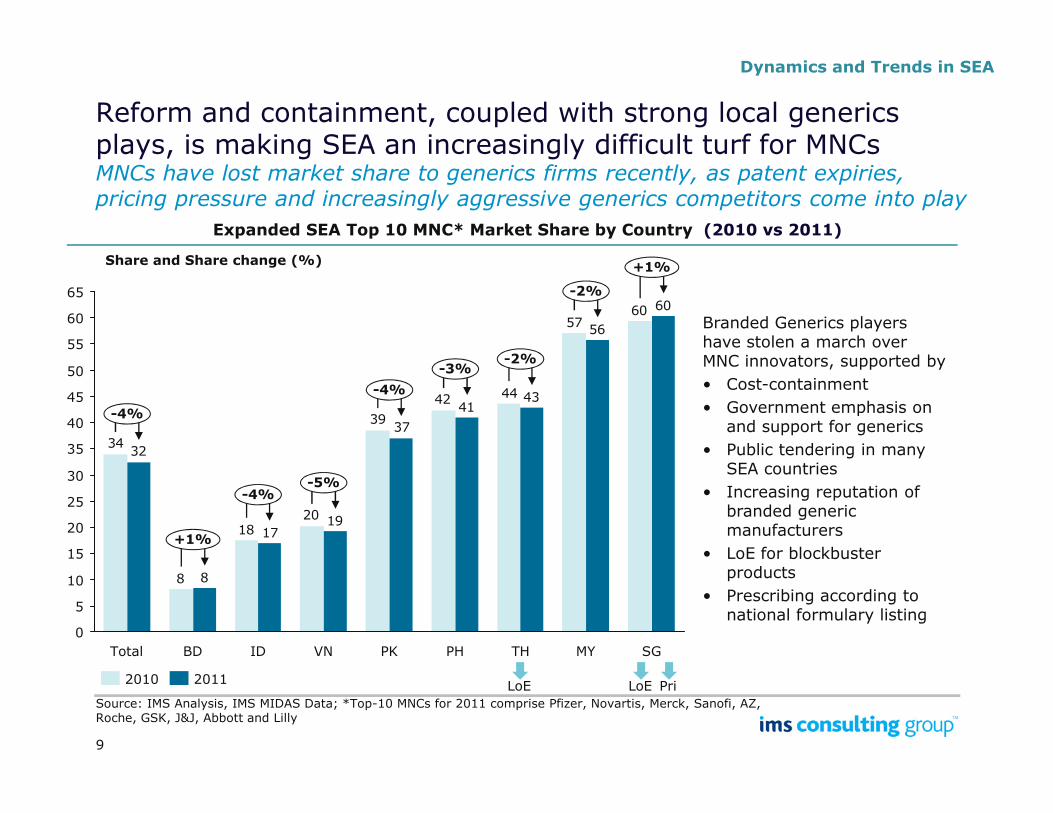

Reform and containment, coupled with strong local generics plays, is making SEA an increasingly difficult turf for MNCsMNCs have lost market share to generics firms recently, as patent expiries, pricing pressure and increasingly aggressive generics competitors come into play

Dynamics and Trends in SEA

6057

4442

60

56

4341

45

65

60

55

50

-4%

-2%-3%

-4%

-2%

+1%

Expanded SEA Top 10 MNC* Market Share by Country (2010 vs 2011)

Share and Share change (%)

Branded Generics players have stolen a march over MNC innovators, supported by

• Cost-containment

• Government emphasis on

9

39

2018

8

34

41

37

1917

8

32

25

20

15

10

40

35

PKVNIDTotal BD SG

30

0

-4%

-5%

5

+1%

MYTHPH

-4%

20112010

Source: IMS Analysis, IMS MIDAS Data; *Top-10 MNCs for 2011 comprise Pfizer, Novartis, Merck, Sanofi, AZ, Roche, GSK, J&J, Abbott and Lilly

LoE LoE Pri

• Government emphasis on and support for generics

• Public tendering in many SEA countries

• Increasing reputation of branded generic manufacturers

• LoE for blockbuster products

• Prescribing according to national formulary listing

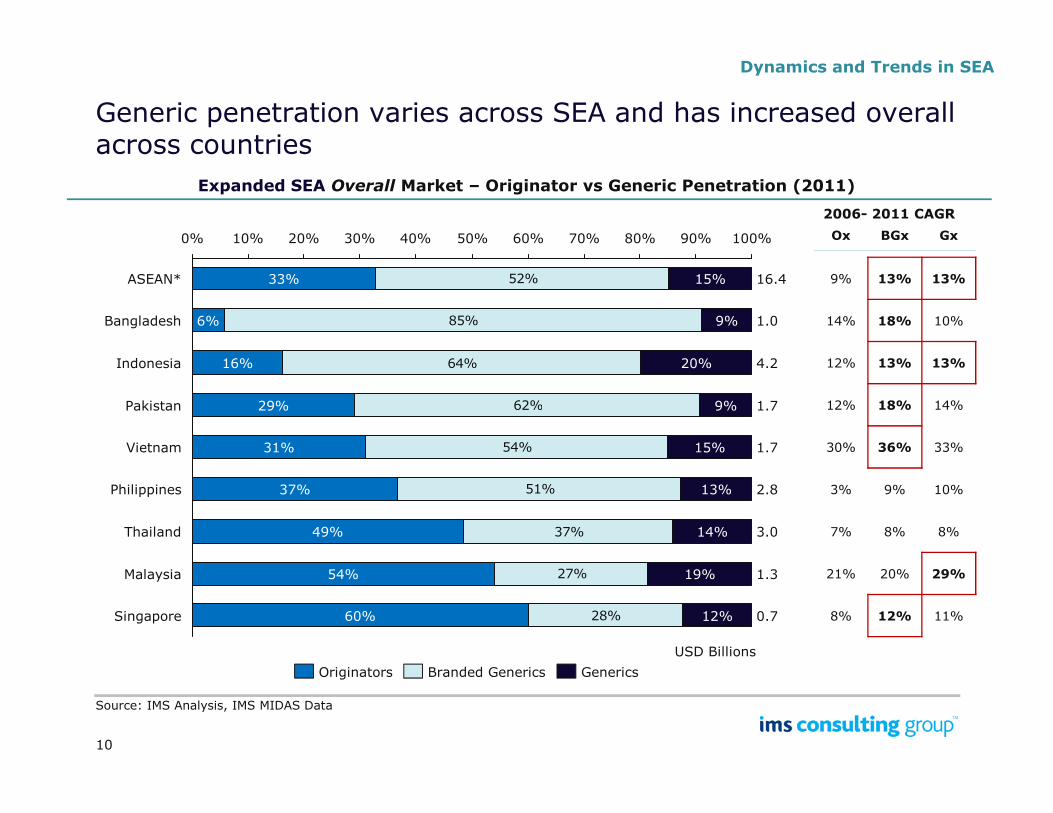

Generic penetration varies across SEA and has increased overall across countries

52%

85%

64%

62%Pakistan 1.729% 9%

Indonesia 4.216% 20%

Bangladesh 1.06% 9%

100%90%80%70%60%50%40%30%20%10%0%

ASEAN* 16.433% 15%

Expanded SEA Overall Market – Originator vs Generic Penetration (2011)

Ox BGx Gx

9% 13% 13%

14% 18% 10%

12% 13% 13%

12% 18% 14%

2006- 2011 CAGR

Dynamics and Trends in SEA

10

62%

54%

51%

37%

27%

28%

2.837% 13%

Vietnam 1.731% 15%

Pakistan 1.729% 9%

Malaysia 1.354% 19%

Thailand 3.049% 14%

Philippines

0.760%Singapore 12%

Originators Branded Generics Generics

USD Billions

Source: IMS Analysis, IMS MIDAS Data

12% 18% 14%

30% 36% 33%

3% 9% 10%

7% 8% 8%

21% 20% 29%

8% 12% 11%

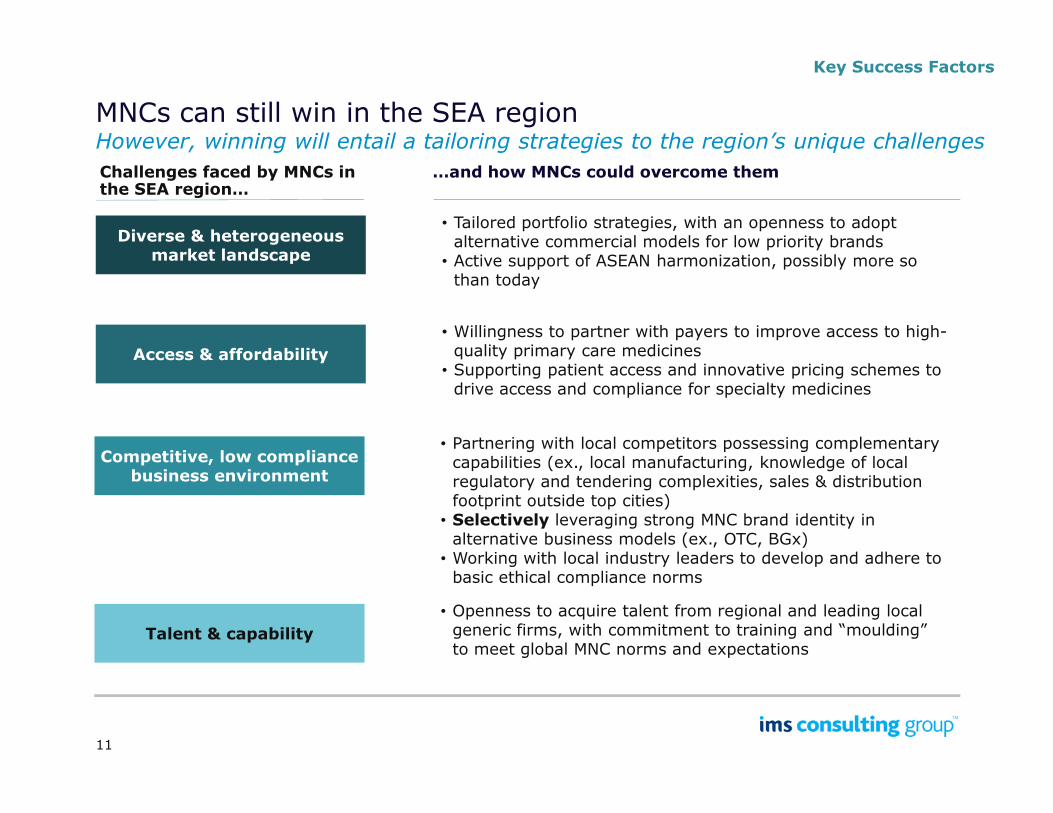

MNCs can still win in the SEA regionHowever, winning will entail a tailoring strategies to the region’s unique challenges

Key Success Factors

…and how MNCs could overcome themChallenges faced by MNCs in the SEA region…

Diverse & heterogeneous market landscape

• Tailored portfolio strategies, with an openness to adopt alternative commercial models for low priority brands

• Active support of ASEAN harmonization, possibly more so than today

Access & affordability

• Willingness to partner with payers to improve access to high-quality primary care medicines

• Supporting patient access and innovative pricing schemes to drive access and compliance for specialty medicines

11

Competitive, low compliance business environment

• Partnering with local competitors possessing complementary capabilities (ex., local manufacturing, knowledge of local regulatory and tendering complexities, sales & distribution footprint outside top cities)

• Selectively leveraging strong MNC brand identity in alternative business models (ex., OTC, BGx)

• Working with local industry leaders to develop and adhere to basic ethical compliance norms

Talent & capability

• Openness to acquire talent from regional and leading local generic firms, with commitment to training and “moulding” to meet global MNC norms and expectations

About IMS Consulting Group

IMS Consulting Group is present across 70 countries with over 500 consultants across the globe. As it focuses only on healthcare and life-sciences sector, our team of consultants bring a wide- and in-depth focuses only on healthcare and life-sciences sector, our team of consultants bring a wide- and in-depth skill set that is unmatched by any other firm.

IMS Consulting Group works with clients to facilitate a wide range of mission critical business decisions. Some typical work includes strategies to enter to specific geographic/ business/ therapy/ product markets and operational excellence initiatives to cover sales force as well as internal operations.

If you would like to know more about what we can do for your business, contact us at:

Dr. Srikanth Rajagopal: [email protected] / +65 6412 7381

Recommended