September 2008

The Evolving Media Economy

www.MagnaInsights.com2

Once Upon a Time, Marketing = Media + Creative

•Traditional media was primary (sole?) venue for communications objectives

www.MagnaInsights.com3

But Fragmentation Fractured That Proposition

www.MagnaInsights.com4

Music Was The Canary In The Coal Mine

Source: Magna, RIAA

•Digitization changed production, distribution and consumption

6,000

8,000

10,000

12,000

14,000

16,000

18,000

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

Rev

enu

es (

$000

s)

TotalDigitalSales

RetailSales

Manufacturers'Shipments

Manufacturers' Shipments of Recorded Music

Napster Launched (June 1999)

BitTorrent, Kazaa, Grokster, etc. active

iTunes Launch (March 2003)

www.MagnaInsights.com5

And DVRs Were To Be The Last Nail In The Coffin

www.MagnaInsights.com6

With A Digital Revolution Blooming In The Aftermath

www.MagnaInsights.com7

But Traditional Media Never Died

“Television is the worst form of

advertising, except all the others that have been tried”

www.MagnaInsights.com8

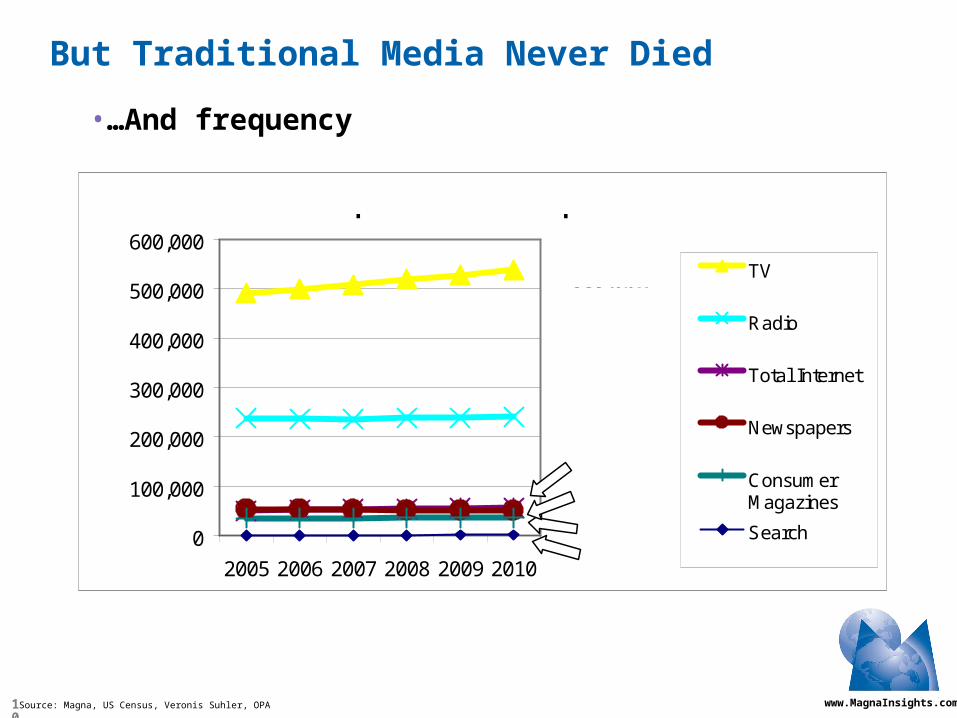

But Traditional Media Never Died

•New advertisers rely on it for mass branding effects

1 McDonald's 1 AT&T Wireless2 KFC 2 Verizon3 Burger King 3 Sprint4 Miller Lite 4 McDonald's5 Budweiser 5 Home Depot6 AT&T 6 T-Mobile7 Wendy's 7 Subway8 American Express 8 Toyota Tundra9 Miller High Life 9 Lowes

10 Advil 10 Wendy's

20071987

Top 10 Network TV Advertisers

Source: Magna analysis of TNS-CMR data

www.MagnaInsights.com9

But Traditional Media Never Died

•Large brand-based advertisers: focus on reach…

Network TV Prime Time Reach - Live Only Adults 18-49

96.17% 96.72%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

2002 2007

Source: Initiative Analysis of Nielsen Data

www.MagnaInsights.com10

Source: Magna, US Census, Veronis Suhler, OPA

But Traditional Media Never Died

•…And frequency

0

100,000

200,000

300,000

400,000

500,000

600,000

2005 2006 2007 2008 2009 2010

TV

Radio

Total Internet

Newspapers

ConsumerMagazines

Search

1.8bn

37.0bn

51.3bn

56.9bn

241.3bn

539.0bn

Total US Population: Hours Spent With Media

Mil

lio

ns

of

Per

son

-Ho

urs

Per

Yea

r

www.MagnaInsights.com11

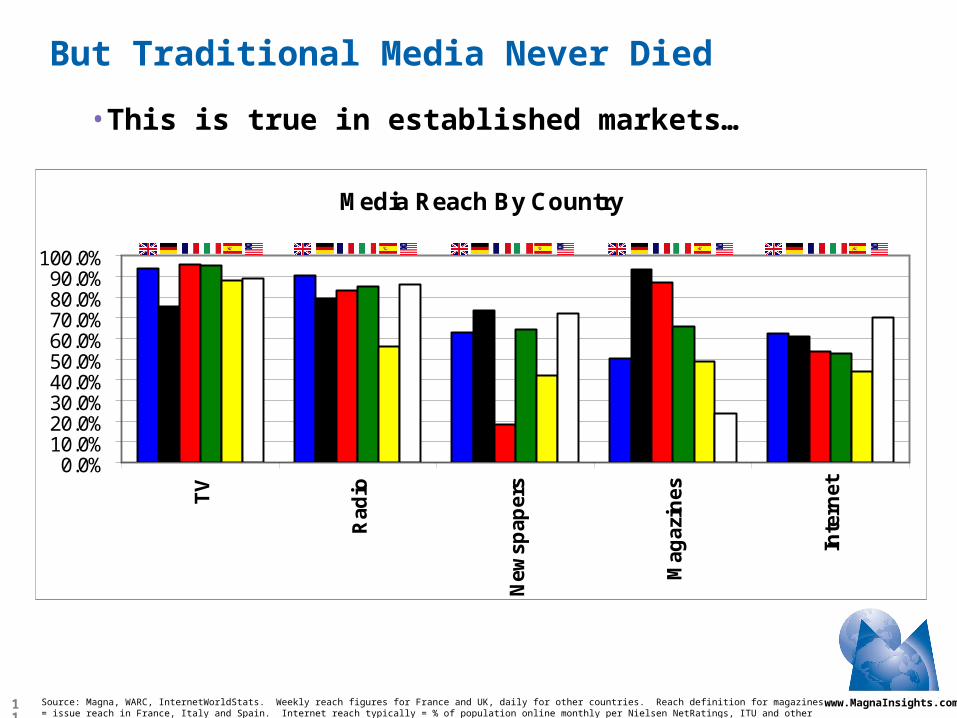

Source: Magna, WARC, InternetWorldStats. Weekly reach figures for France and UK, daily for other countries. Reach definition for magazines = issue reach in France, Italy and Spain. Internet reach typically = % of population online monthly per Nielsen NetRatings, ITU and other sources as of June 30 2007 (except for US = March 31, 2007)

But Traditional Media Never Died

•This is true in established markets…

Media Reach By Country

0.0%10.0%20.0%30.0%40.0%50.0%60.0%70.0%80.0%90.0%

100.0%

TV

Rad

io

New

spap

ers

Mag

azin

es

Inte

rnet

www.MagnaInsights.com12

But Traditional Media Never Died

•…And emerging ones

Source: Magna, WARC, InternetWorldStats. Weekly figures for Brazil and Russia. Russia, China and India magazines are issue reach figures. Indian TV and radio = daily, newspapers = issue. Chinese TV = weekly and radio = daily. Internet typically = % of population online monthly per Nielsen NetRatings, ITU and other sources as of June 30 2007

Media Reach By Country

0.0%10.0%20.0%30.0%40.0%50.0%60.0%70.0%80.0%90.0%

100.0%

TV

Rad

io

New

spap

ers

Mag

azin

es

Inte

rnet

www.MagnaInsights.com13

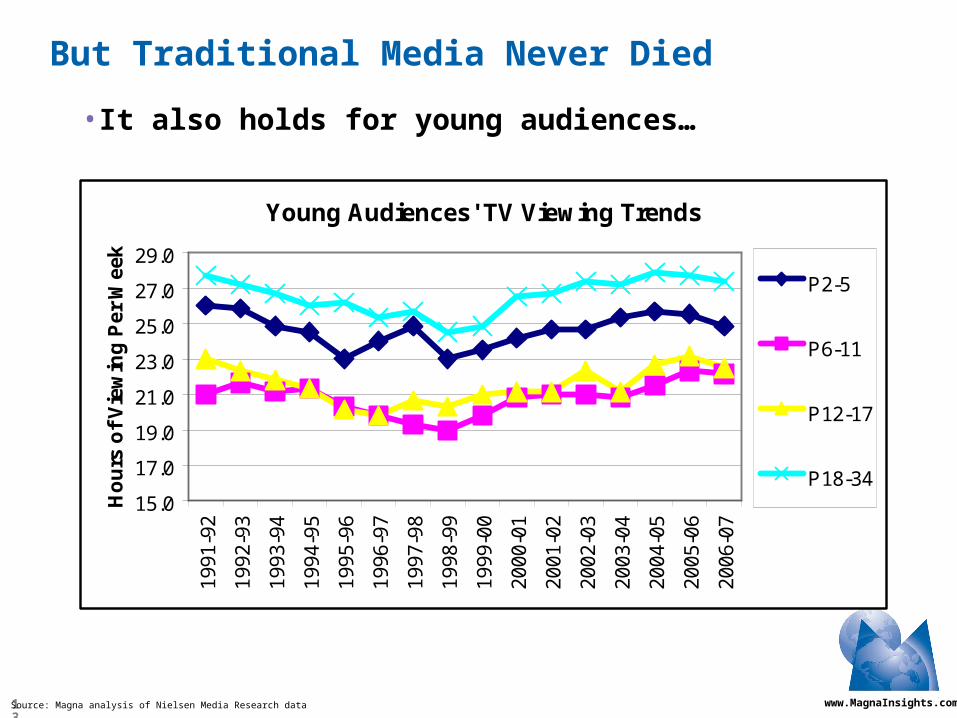

But Traditional Media Never Died

•It also holds for young audiences…

Young Audiences' TV Viewing Trends

15.0

17.0

19.0

21.0

23.0

25.0

27.0

29.0

1991

-92

1992

-93

1993

-94

1994

-95

1995

-96

1996

-97

1997

-98

1998

-99

1999

-00

2000

-01

2001

-02

2002

-03

2003

-04

2004

-05

2005

-06

2006

-07

Ho

urs

of

Vie

win

g P

er W

eek

P2-5

P6-11

P12-17

P18-34

Source: Magna analysis of Nielsen Media Research data

www.MagnaInsights.com14

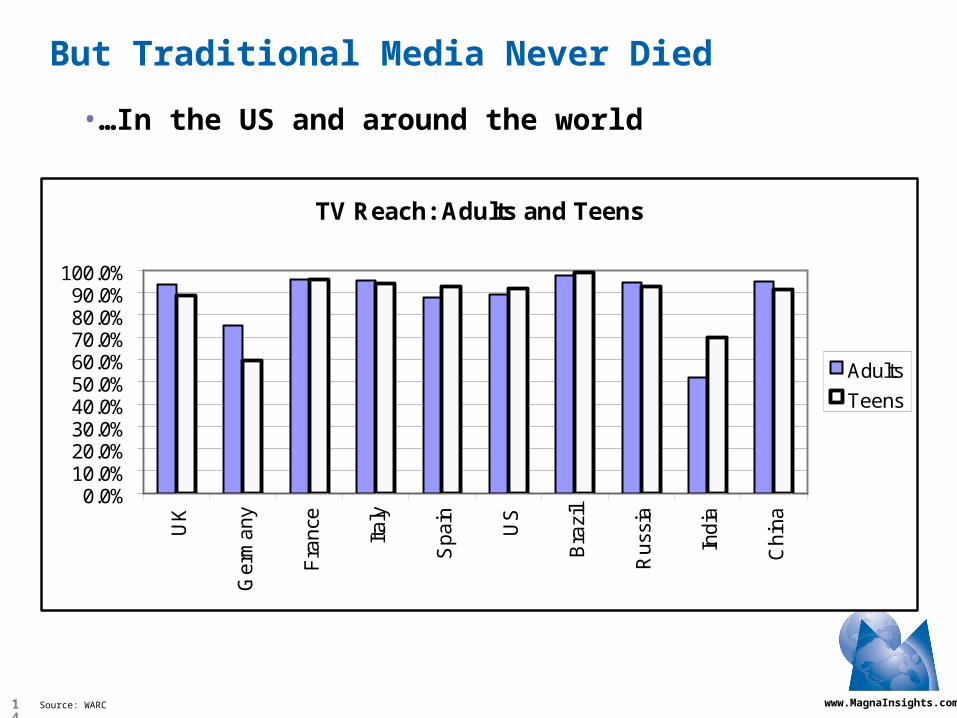

But Traditional Media Never Died

•…In the US and around the world

Source: WARC

TV Reach: Adults and Teens

0.0%10.0%20.0%30.0%40.0%50.0%60.0%70.0%80.0%90.0%

100.0%

UK

Ger

man

y

Fra

nce

Italy

Spa

in

US

Bra

zil

Rus

sia

Indi

a

Chi

na

Adults

Teens

www.MagnaInsights.com15

Consequences of Reach and Frequency Paradigm

20 YEARS AGO

•Models that were well-designed…

www.MagnaInsights.com16

Consequences of Reach and Frequency Paradigm

20 YEARS AGO

•…For an era of homogenous media platform access…

www.MagnaInsights.com17

Consequences of Reach and Frequency Paradigm

TODAY

•…May not be as well-suited for a world of Web 2.0%…

www.MagnaInsights.com18

Consequences of Reach and Frequency Paradigm

TODAY

•…Which will reach some audiences and miss others

www.MagnaInsights.com19

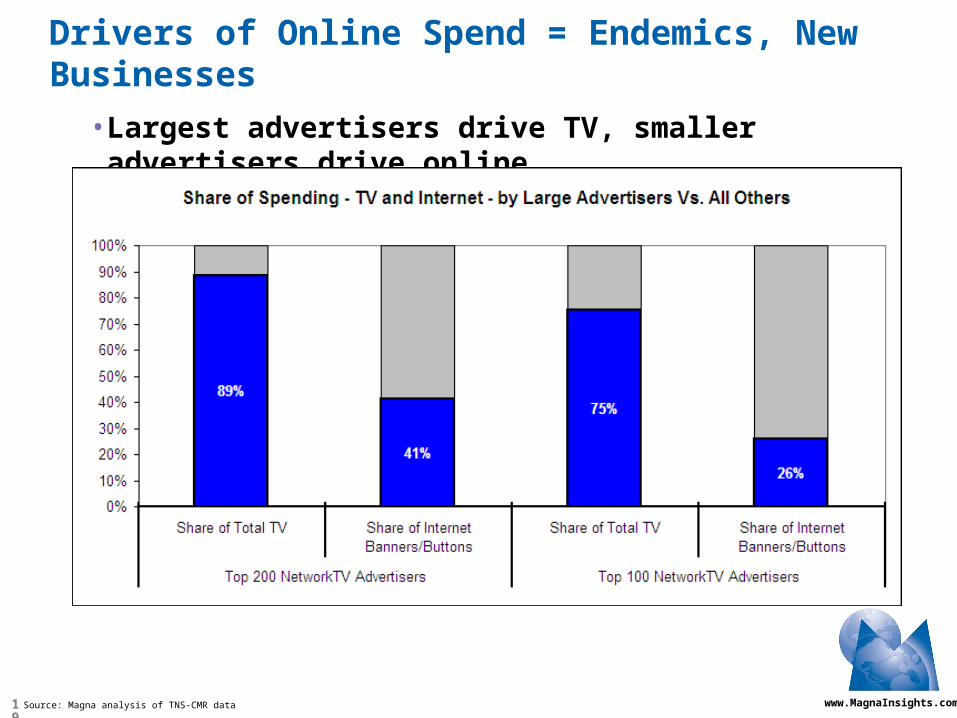

Drivers of Online Spend = Endemics, New Businesses

•Largest advertisers drive TV, smaller advertisers drive online

Source: Magna analysis of TNS-CMR data

www.MagnaInsights.com20

Source: Magna, US Census, Veronis Suhler

Drivers of Online Spend = Endemics, New Businesses

•Reflecting effectiveness for SMEs…

$0.00$1.00$2.00$3.00$4.00$5.00$6.00$7.00$8.00$9.00

$10.00

2005 2006 2007 2008 2009 2010

Search

Newspapers

Total Internet

ConsumerMagazinesTV

Radio

Advertising Dollars Spent Per Hour of Media Consumption

$9.39

$0.94

$0.08

$0.58

$0.10

$0.33

www.MagnaInsights.com21

Drivers of Online Spend = Endemics, New Businesses

•…Who benefit from a Democratization of Advertising

Source: Magna analylsis of IRS data

Ad Expenditures By Small Businesses

4.0

4.2

4.4

4.6

4.8

5.0

5.2

5.4

5.6

5.8

Mil

lio

ns

of

US

Co

rpo

rati

on

s W

ith

<$1

0mm

Ass

ets

(5.0)

5.0

15.0

25.0

35.0

45.0

55.0

Bil

lio

ns

of

Ad

Exp

end

itu

re $

by

Co

rpo

rati

on

s W

ith

<$1

0mm

A

sset

s

Expenditures

Small Businesses

www.MagnaInsights.com22

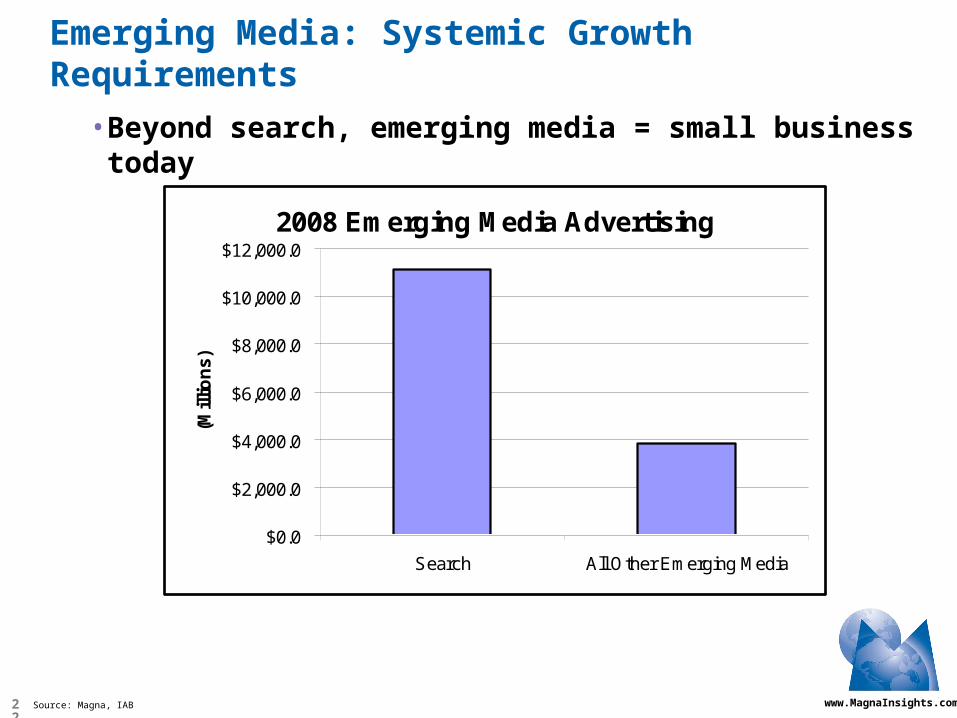

•Beyond search, emerging media = small business today

Emerging Media: Systemic Growth Requirements

Source: Magna, IAB

2008 Emerging Media Advertising

$0.0

$2,000.0

$4,000.0

$6,000.0

$8,000.0

$10,000.0

$12,000.0

Search All Other Emerging Media

(Mill

ion

s)

www.MagnaInsights.com23

Emerging Media: Systemic Growth Requirements

•Impacting “gut” decisions

= ?

www.MagnaInsights.com24

Emerging Media: Systemic Growth Requirements

•Establishing better infrastructure

www.MagnaInsights.com25

Emerging Media: Systemic Growth Requirements

•Re-aligning organizational structure

Operating Division

Retail Distribution

Product Development

Branding

CEO

Other Corporate Functions

COO

PR / Corporate Communications

Operating Division

Product Development

Branding

Operating Division

Product Development

Branding

CMO / Central Marketing

Creative OtherMedia

Marketing, PR, Retail, Sales

Marketing, PR, Retail, Sales

Marketing, PR, Retail, Sales

Source: Magna

Direct / Online Sales

www.MagnaInsights.com26

Emerging Media: Systemic Growth Requirements

•Focusing on people, not pages (or ratings)

www.MagnaInsights.com27

Emerging Media: Systemic Growth Requirements

•Assessing value, not cost

Top 10 DMAs

$>$National Network

www.MagnaInsights.com28

Emerging Media: Systemic Growth Requirements

•Transforming data into actionable insights

= + ?

www.MagnaInsights.com30

Discussion

•Roger Keating

SVP, Digital Media

Hearst-Argyle Television

•Steve McGowan

SVP, Insights and Client Research Initiatives

The Nielsen Company

www.MagnaInsights.com31

Issue #1

•Consumers in Control Vs. Controlled Consumers?

0%

20%

40%

60%

80%

100%

120%

2006 2007 2008 2009 2010 2011

TV

Co

nsu

mp

tio

n I

nd

ex

Increase Due toPopulation Growth

Increase Due toHousehold TVConsumptionGrowth

Baseline - Today'sTV ConsumptionLess DVR Usage

-2%

+5% +5%

+8%

Source: Magna

www.MagnaInsights.com32

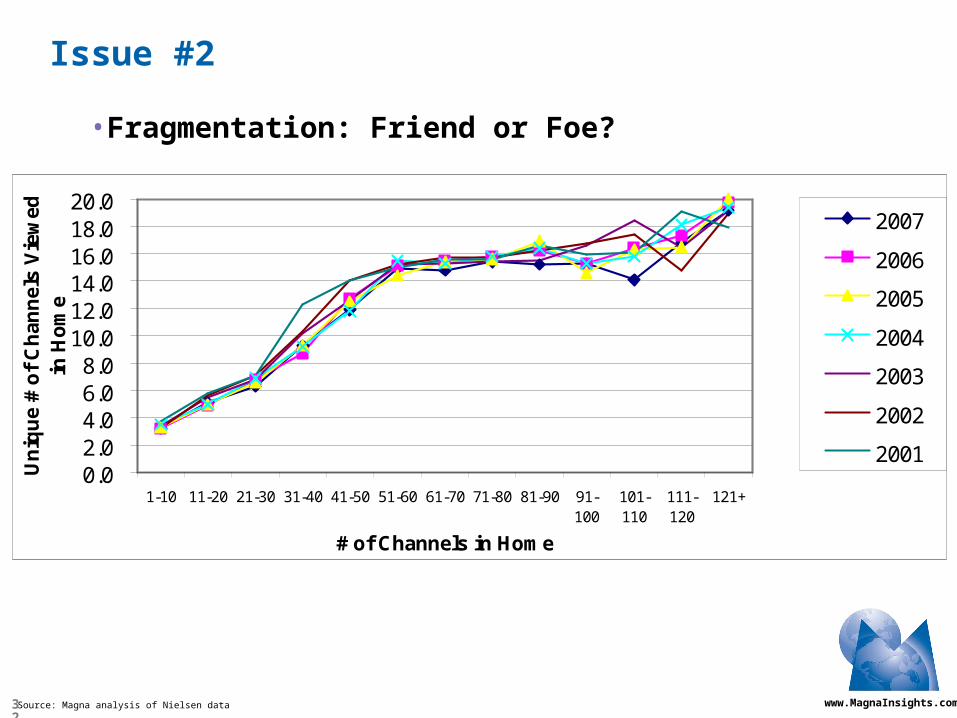

Issue #2

•Fragmentation: Friend or Foe?

0.02.04.06.08.0

10.012.014.016.018.020.0

1-10 11-20 21-30 31-40 41-50 51-60 61-70 71-80 81-90 91-100

101-110

111-120

121+

# of Channels in Home

Un

iqu

e #

of

Ch

ann

els

Vie

wed

in

Ho

me

2007

2006

2005

2004

2003

2002

2001

Source: Magna analysis of Nielsen data

www.MagnaInsights.com33

Issue #3

•Who Crosses Platforms?

Multichannel Homes

DVR Homes

VOD Homes

Broadband Homes

Satellite Radio Subscriptions

HD Subscriptions

Mobile Phone Subscriptions

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

% o

f U

S H

ou

seh

old

s

Source: Magna

Recommended