Russian teddy-bear in search of free honey market

Leonid Glazytchev

Logrus International Corporation

Russian Economy

Is There the Market at All?

• Russian economy is extremely unhomogeneous

• Maturity levels for different economy sectors are significantly different

• IT is way ahead of the others

Reasons for IT’s Lead

• The most dynamic sector of the economy worldwide

• The most internationally integrated• No rotten roots – young industry• Attracts young and educated people

without political or economic prejudices• Very high level of technical competence

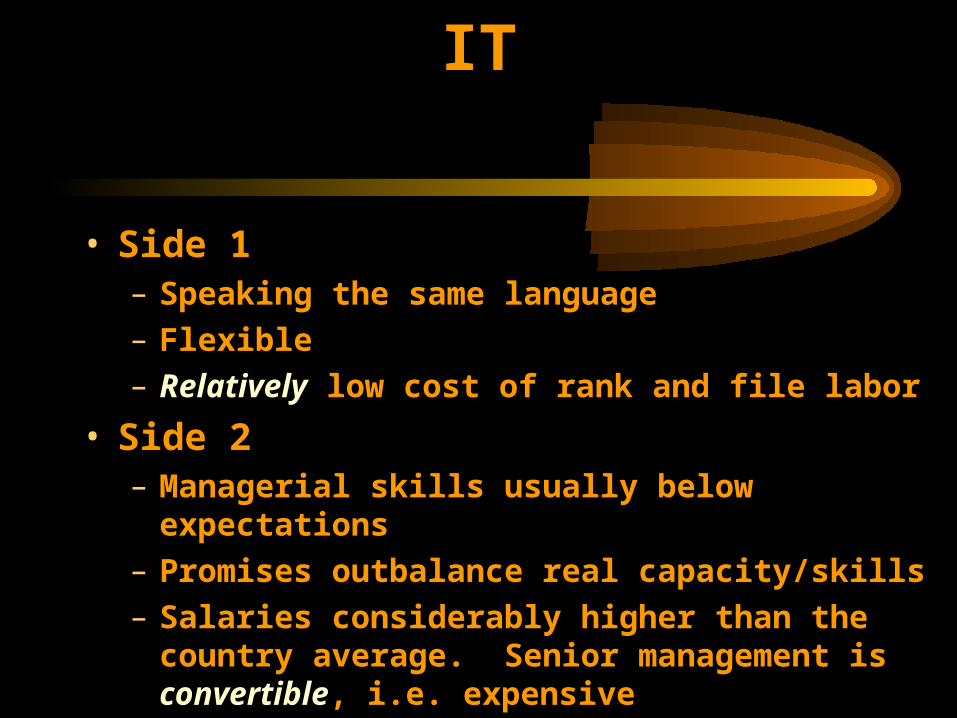

The Two Sides of Russian IT

• Side 1– Speaking the same language– Flexible– Relatively low cost of rank and file labor

• Side 2– Managerial skills usually below expectations– Promises outbalance real capacity/skills– Salaries considerably higher than the country

average. Senior management is convertible, i.e. expensive

Show Us the Data!

• Officially published data is often unreliable

• Most of the data are based on private conversations with top management of major software and hardware distributors, and on Logrus experience

• Internet data supplied by Russian nOn-profit Center for Internet Technologies (ROCIT)

Software Sales

Crisis: QIII’98; currency devalued fourfold

FY

2000

- E

stim

ate

FY

99

- C

ris

is

FY

98

FY

97

1996

, Q

III

1996

, Q

IV

1997

, Q

I 1997

, Q

II

1997

, Q

III

1997

, Q

IV

1998

, Q

I

1998

, Q

II

1998

, Q

III

1998

, Q

IV

1999

, Q

I

1999

, Q

II

1999

, Q

III

1999

, Q

IV

$0m

$50m

$100m

$150m

$200m

$250m

FY97FY98

FY99

FY2000

$0m

$20m

$40m

$60m

Sales by FY

Sales by Quater

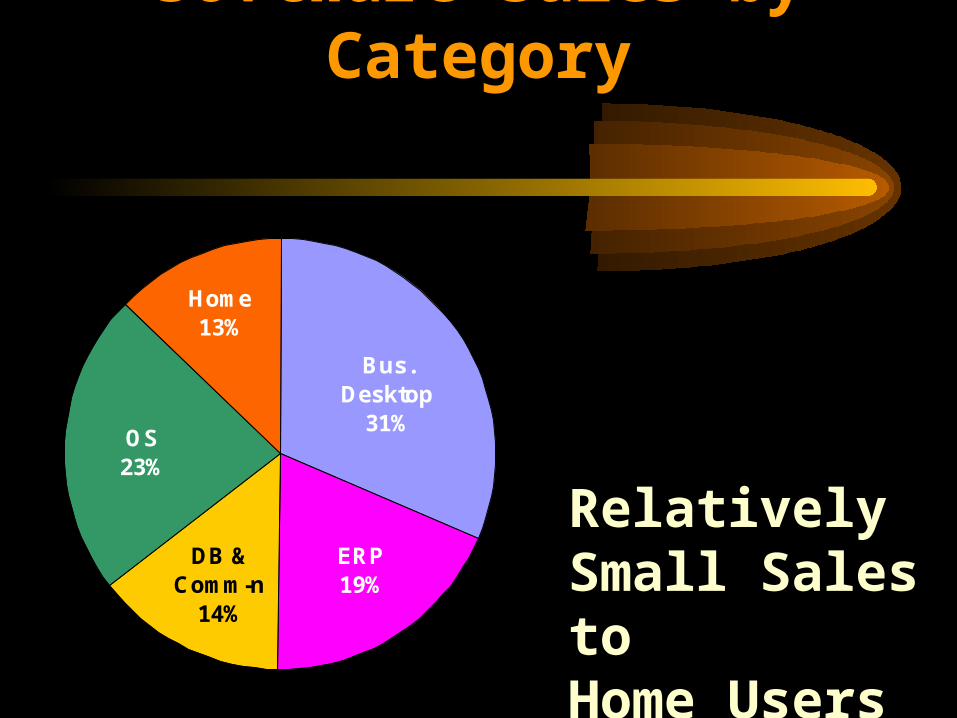

Software Sales by Category

ERP19%

Home13%

OS23%

DB & Comm-n

14%

Bus. Desktop

31%

Relatively Small Sales to Home Users

Multimedia Sales

Circulation (Legal)

2000

4000

6000

Average Success Hit

Gross Sales by Year

$20m$20m

$8,5m

1998 1999 2000

Circulation 1000 – 10 000 5 000 – 30 000

Titles per Year 80 300

Average Retail Price $20,00 $2,50

Gross Revenue $3 500 000 $5 000 000

PC Sales & Internet Users

0,55

1

1,6

2,3

0,450,6 0,7

0,0m

0,5m

1,0m

1,5m

2,0m

2,5m

95 96 97 98 99

PC Sales Internet Users Internet Growth

• Decommissioned 0,4-0,6 million PCs

• Purchased New 1,2-1,25 million PCs

Total Expected by 2001: 3,8 million modern PCsTotal Expected by 2004: 5-6 million

(9 million with upgrades)

66% on the Internet

PC Facts

Internet Facts

Population: 146m

36m Intend toBecome Users

4,7 – 5,2mInternet Audience

2,3mRegistered

PC/Net users per 1000: 27/10 (Russia), 116/50 (Mow)

Localization Industry• Didn’t exist 10 years ago

• Mostly very small companies or departments with a single major client

• No reliable revenue statistics

• Continuous turnover of players on the market

• Lack of professionalism on a wide scale

• Approximate gross revenues for FY99: $3 – 4 million (~30% - internal localizations)

• Contradictory and inconsistent data on technical translation market volume

Forecast

- At least now will you tell me intelligibly: Up or Down???

Up

Down

BOTHWAYS

SUMMARY

• S/w and hardware sectors have survived the crisis and give all signs of revival

• Internet is growing rapidly

• For three consecutive years: s/w sales > $100m, computer sales > 1m

• We can expect an upward spiral both in the IT industry and in localization

Recommended