Royal Dutch Shell plc June 7, 2016

Capital markets day 2016 Re-shaping Shell, to create a world-class investment case

“Let’s make the future”

Royal Dutch Shell | June 7, 2016

Royal Dutch Shell | June 7, 2016

Ben van Beurden Chief Executive Officer Royal Dutch Shell plc

Royal Dutch Shell | June 7, 2016 3

Definitions & cautionary note

Reserves: Our use of the term “reserves” in this presentation means SEC proved oil and gas reserves.

Resources: Our use of the term “resources” in this presentation includes quantities of oil and gas not yet classified as SEC proved oil and gas reserves. Resources are consistent with the Society of Petroleum Engineers (SPE) 2P + 2C definitions.

Resources and potential: Our use of the term “resources and potential” are consistent with SPE 2P + 2C + 2U definitions.

Organic: Our use of the term Organic includes SEC proved oil and gas reserves excluding changes resulting from acquisitions, divestments and year-average pricing impact.

Shales: Our use of the term ‘shales’ refers to tight, shale and coal bed methane oil and gas acreage.

The companies in which Royal Dutch Shell plc directly and indirectly owns investments are separate legal entities. In this release “Shell”, “Shell group” and “Royal Dutch Shell” are sometimes used for convenience where references are made to Royal Dutch Shell plc and its subsidiaries in general. Likewise, the words “we”, “us” and “our” are also used to refer to subsidiaries in general or to those who work for them. These expressions are also used where no useful purpose is served by identifying the particular company or companies. ‘‘Subsidiaries’’, “Shell subsidiaries” and “Shell companies” as used in this release refer to companies over which Royal Dutch Shell plc either directly or indirectly has control. Entities and unincorporated arrangements over which Shell has joint control are generally referred to as “joint ventures” and “joint operations” respectively. Entities over which Shell has significant influence but neither control nor joint control are referred to as “associates”. The term “Shell interest” is used for convenience to indicate the direct and/or indirect ownership interest held by Shell in a venture, partnership or company, after exclusion of all third-party interest.

This release contains forward-looking statements concerning the financial condition, results of operations and businesses of Royal Dutch Shell. All statements other than statements of historical fact are, or may be deemed to be, forward-looking statements. Forward-looking statements are statements of future expectations that are based on management’s current expectations and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in these statements. Forward-looking statements include, among other things, statements concerning the potential exposure of Royal Dutch Shell to market risks and statements expressing management’s expectations, beliefs, estimates, forecasts, projections and assumptions. These forward-looking statements are identified by their use of terms and phrases such as ‘‘anticipate’’, ‘‘believe’’, ‘‘could’’, ‘‘estimate’’, ‘‘expect’’, ‘‘goals’’, ‘‘intend’’, ‘‘may’’, ‘‘objectives’’, ‘‘outlook’’, ‘‘plan’’, ‘‘probably’’, ‘‘project’’, ‘‘risks’’, “schedule”, ‘‘seek’’, ‘‘should’’, ‘‘target’’, ‘‘will’’ and similar terms and phrases. There are a number of factors that could affect the future operations of Royal Dutch Shell and could cause those results to differ materially from those expressed in the forward-looking statements included in this release, including (without limitation): (a) price fluctuations in crude oil and natural gas; (b) changes in demand for Shell’s products; (c) currency fluctuations; (d) drilling and production results; (e) reserves estimates; (f) loss of market share and industry competition; (g) environmental and physical risks; (h) risks associated with the identification of suitable potential acquisition properties and targets, and successful negotiation and completion of such transactions; (i) the risk of doing business in developing countries and countries subject to international sanctions; (j) legislative, fiscal and regulatory developments including regulatory measures addressing climate change; (k) economic and financial market conditions in various countries and regions; (l) political risks, including the risks of expropriation and renegotiation of the terms of contracts with governmental entities, delays or advancements in the approval of projects and delays in the reimbursement for shared costs; and (m) changes in trading conditions. There can be no assurance that future dividend payments will match or exceed previous dividend payments. All forward-looking statements contained in this release are expressly qualified in their entirety by the cautionary statements contained or referred to in this section. Readers should not place undue reliance on forward-looking statements. Additional risk factors that may affect future results are contained in Royal Dutch Shell’s 20-F for the year ended December 31, 2015 (available at www.shell.com/investor and www.sec.gov ). These risk factors also expressly qualify all forward looking statements contained in this release and should be considered by the reader. Each forward-looking statement speaks only as of the date of this release, June 7, 2016. Neither Royal Dutch Shell plc nor any of its subsidiaries undertake any obligation to publicly update or revise any forward-looking statement as a result of new information, future events or other information. In light of these risks, results could differ materially from those stated, implied or inferred from the forward-looking statements contained in this release.

With respect to operating costs synergies indicated, such savings and efficiencies in procurement spend include economies of scale, specification standardisation and operating efficiencies across operating, capital and raw material cost areas.

We may have used certain terms, such as resources, in this release that United States Securities and Exchange Commission (SEC) strictly prohibits us from including in our filings with the SEC. U.S. Investors are urged to consider closely the disclosure in our Form 20-F, File No 1-32575, available on the SEC website www.sec.gov.

Royal Dutch Shell | June 7, 2016 4

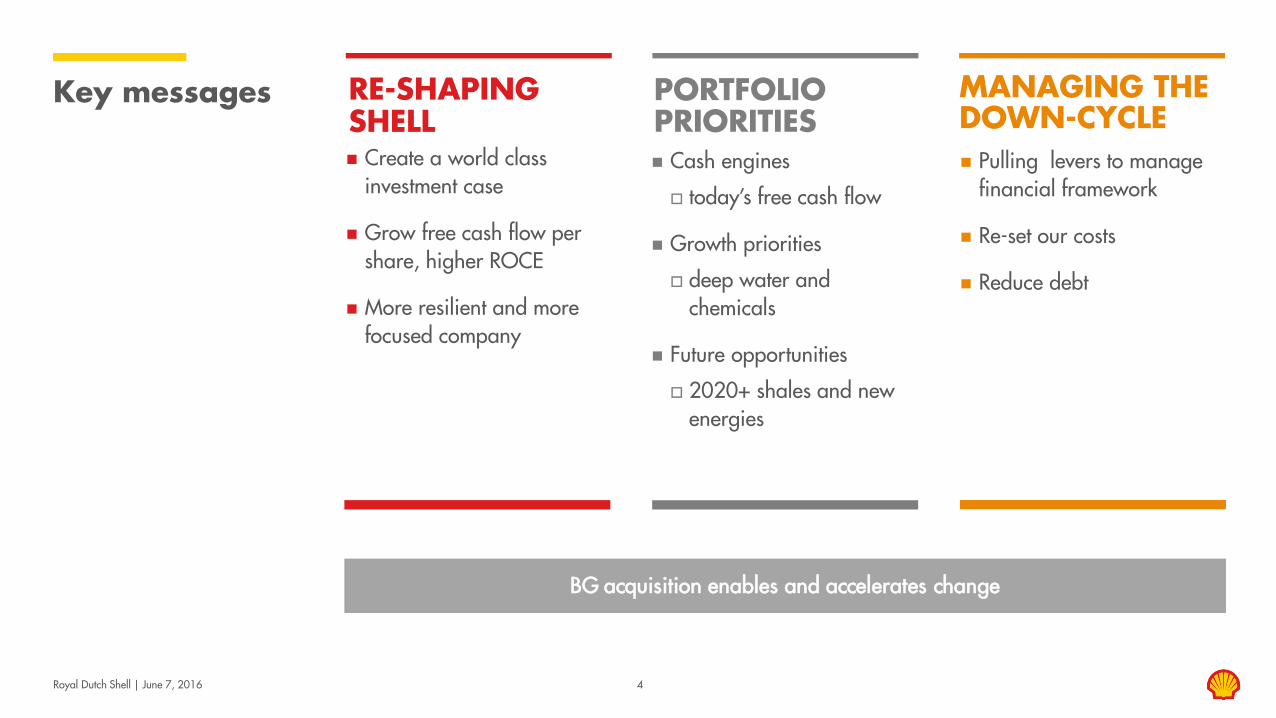

Key messages

Cash engines

today’s free cash flow

Growth priorities

deep water and chemicals

Future opportunities

2020+ shales and new energies

Create a world class investment case

Grow free cash flow per share, higher ROCE

More resilient and more focused company

RE-SHAPING SHELL

MANAGING THE DOWN-CYCLE

PORTFOLIO PRIORITIES

Pulling levers to manage financial framework

Re-set our costs

Reduce debt

BG acquisition enables and accelerates change

Royal Dutch Shell | June 7, 2016 5

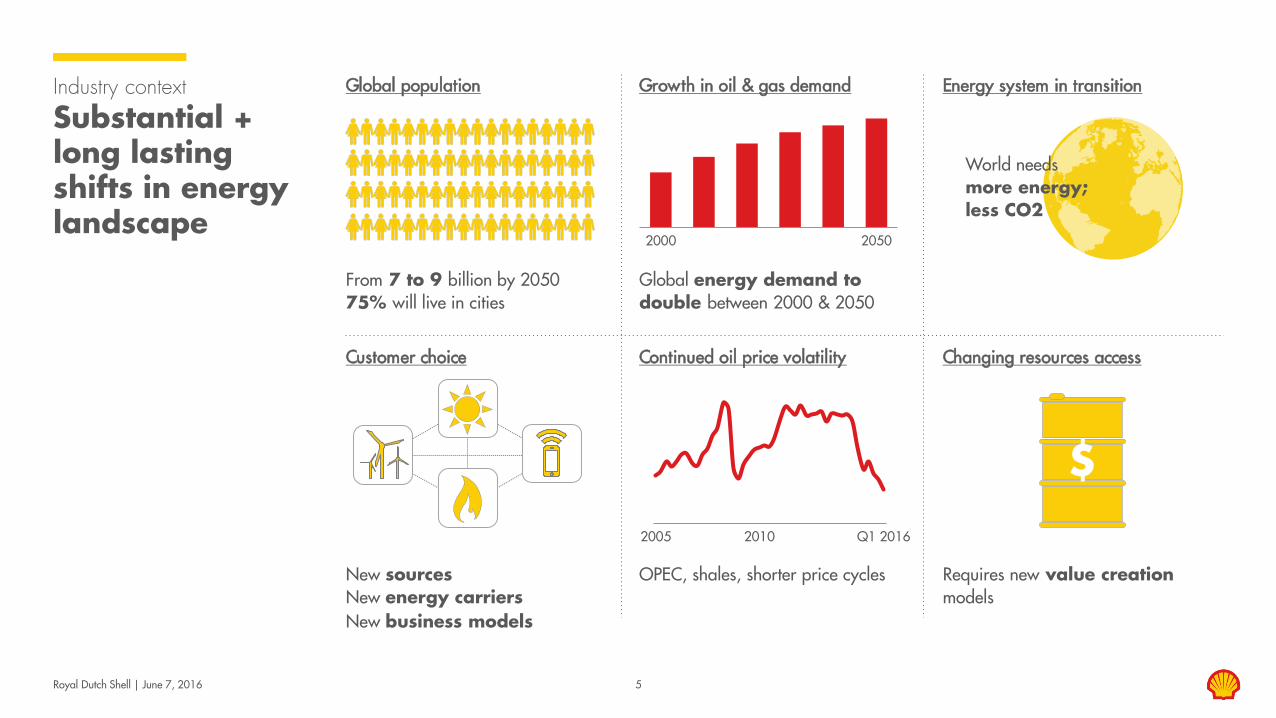

Industry context

Substantial + long lasting shifts in energy landscape

2005 2010 Q1 2016

2000 2050

$

From 7 to 9 billion by 2050 75% will live in cities

Global energy demand to double between 2000 & 2050

World needs more energy; less CO2

New sources New energy carriers New business models

OPEC, shales, shorter price cycles Requires new value creation models

Global population Growth in oil & gas demand Energy system in transition

Customer choice Continued oil price volatility Changing resources access

Royal Dutch Shell | June 7, 2016 6

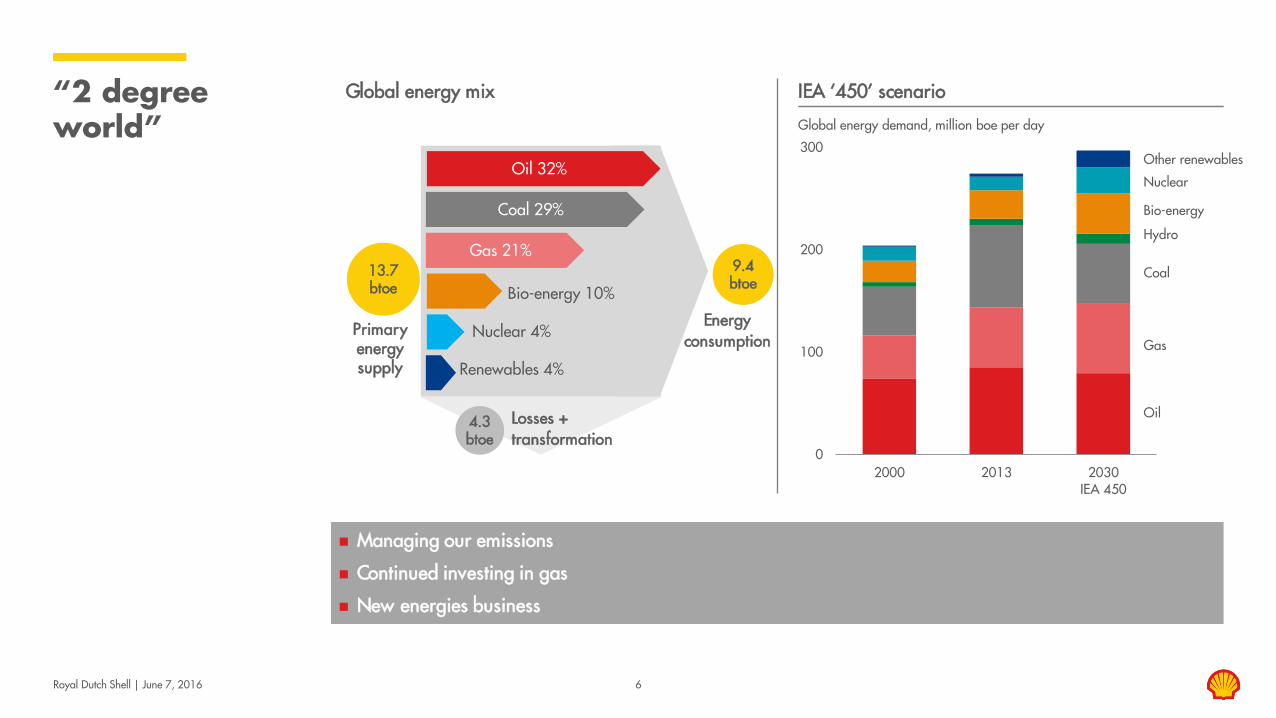

“2 degree world” Global energy demand, million boe per day

0

100

200

300

2000 2013 2030IEA 450

Global energy mix IEA ‘450’ scenario

Primary energy supply

Oil 32%

Coal 29%

Gas 21%

Renewables 4%

Nuclear 4%

13.7 btoe

Energy consumption

9.4 btoe

4.3 btoe

Losses + transformation

Bio-energy 10%

Managing our emissions

Continued investing in gas

New energies business

Gas

Oil

Nuclear

Coal

Bio-energy

Hydro

Other renewables

Royal Dutch Shell | June 7, 2016

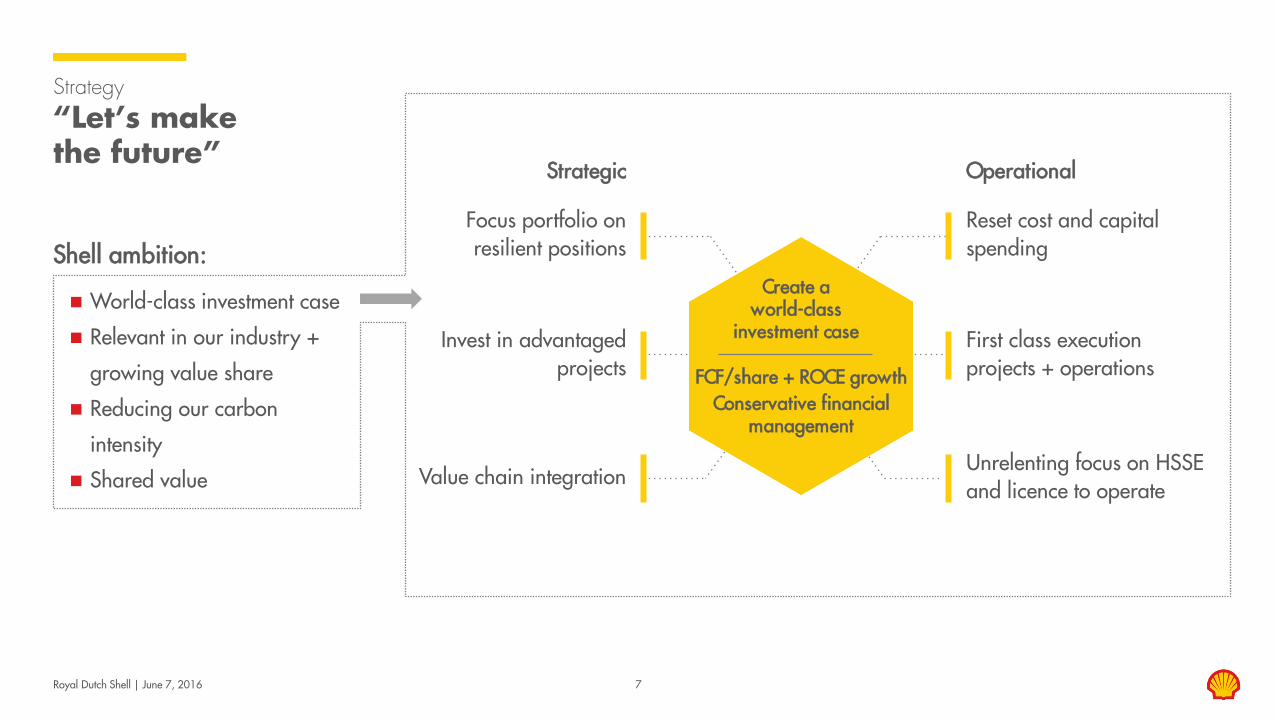

Strategy “Let’s make the future”

Focus portfolio on resilient positions

Invest in advantaged projects

Unrelenting focus on HSSE and licence to operate

Value chain integration

First class execution projects + operations

Reset cost and capital spending

Strategic Operational

FCF/share + ROCE growth Conservative financial

management

Create a world-class

investment case

7

Shell ambition:

World-class investment case

Relevant in our industry +

growing value share

Reducing our carbon

intensity

Shared value

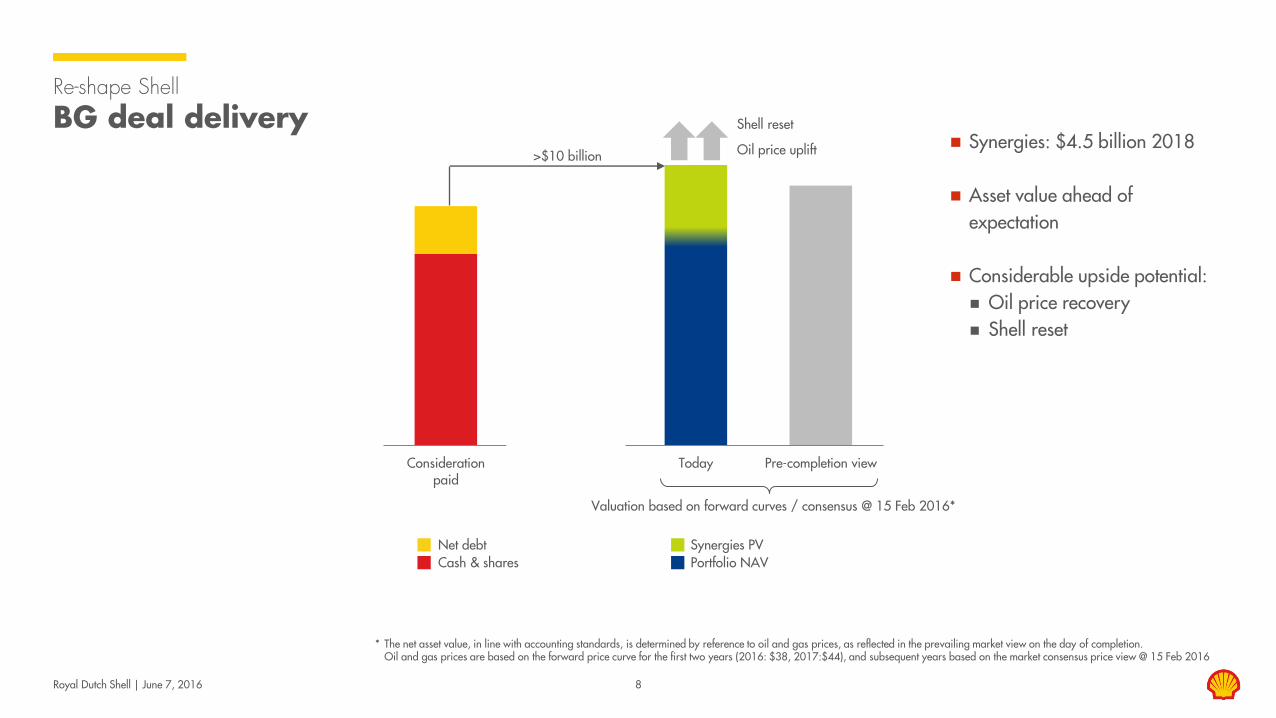

Considerationpaid

Today Pre-completion view

Royal Dutch Shell | June 7, 2016 8

Re-shape Shell BG deal delivery

* The net asset value, in line with accounting standards, is determined by reference to oil and gas prices, as reflected in the prevailing market view on the day of completion. Oil and gas prices are based on the forward price curve for the first two years (2016: $38, 2017:$44), and subsequent years based on the market consensus price view @ 15 Feb 2016

Synergies: $4.5 billion 2018 Asset value ahead of

expectation Considerable upside potential: Oil price recovery Shell reset

Cash & shares Net debt

Portfolio NAV Synergies PV

Valuation based on forward curves / consensus @ 15 Feb 2016*

Shell reset

Oil price uplift >$10 billion

Royal Dutch Shell | June 7, 2016 9

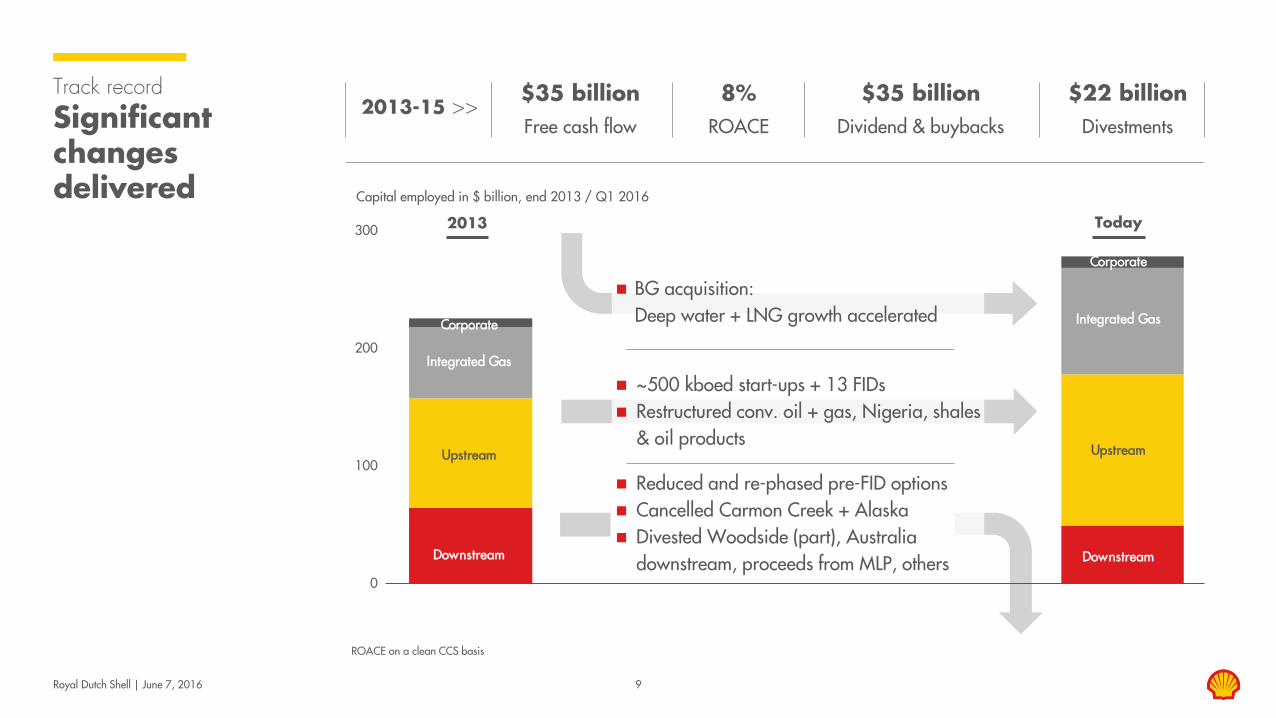

Track record

Significant changes delivered

ROACE on a clean CCS basis

0

100

200

300

Downstream

Upstream

Integrated Gas

Corporate

Downstream

Upstream

Integrated Gas

Corporate

$35 billion Free cash flow

8% ROACE

$35 billion Dividend & buybacks

$22 billion Divestments

2013-15 >>

2013 Today

Capital employed in $ billion, end 2013 / Q1 2016

BG acquisition: Deep water + LNG growth accelerated

Reduced and re-phased pre-FID options Cancelled Carmon Creek + Alaska Divested Woodside (part), Australia

downstream, proceeds from MLP, others

~500 kboed start-ups + 13 FIDs Restructured conv. oil + gas, Nigeria, shales

& oil products

Strong free cash flow and returns

Royal Dutch Shell | June 7, 2016

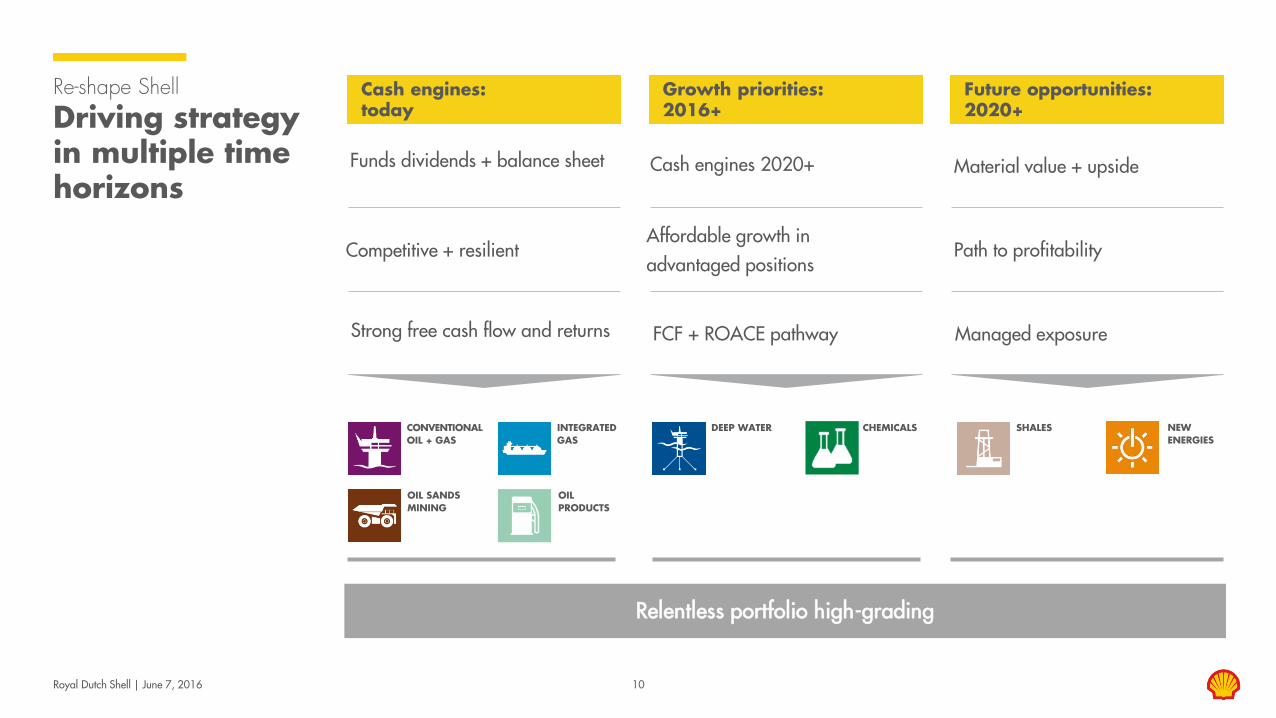

Re-shape Shell Driving strategy in multiple time horizons

CONVENTIONAL OIL + GAS

CHEMICALS

OIL PRODUCTS

DEEP WATER INTEGRATED GAS

OIL SANDS MINING

SHALES NEW ENERGIES

10

Cash engines: today

Growth priorities: 2016+

Future opportunities: 2020+

Competitive + resilient

Funds dividends + balance sheet

FCF + ROACE pathway

Affordable growth in advantaged positions

Material value + upside

Managed exposure

Path to profitability

Cash engines 2020+

Relentless portfolio high-grading

Royal Dutch Shell | June 7, 2016

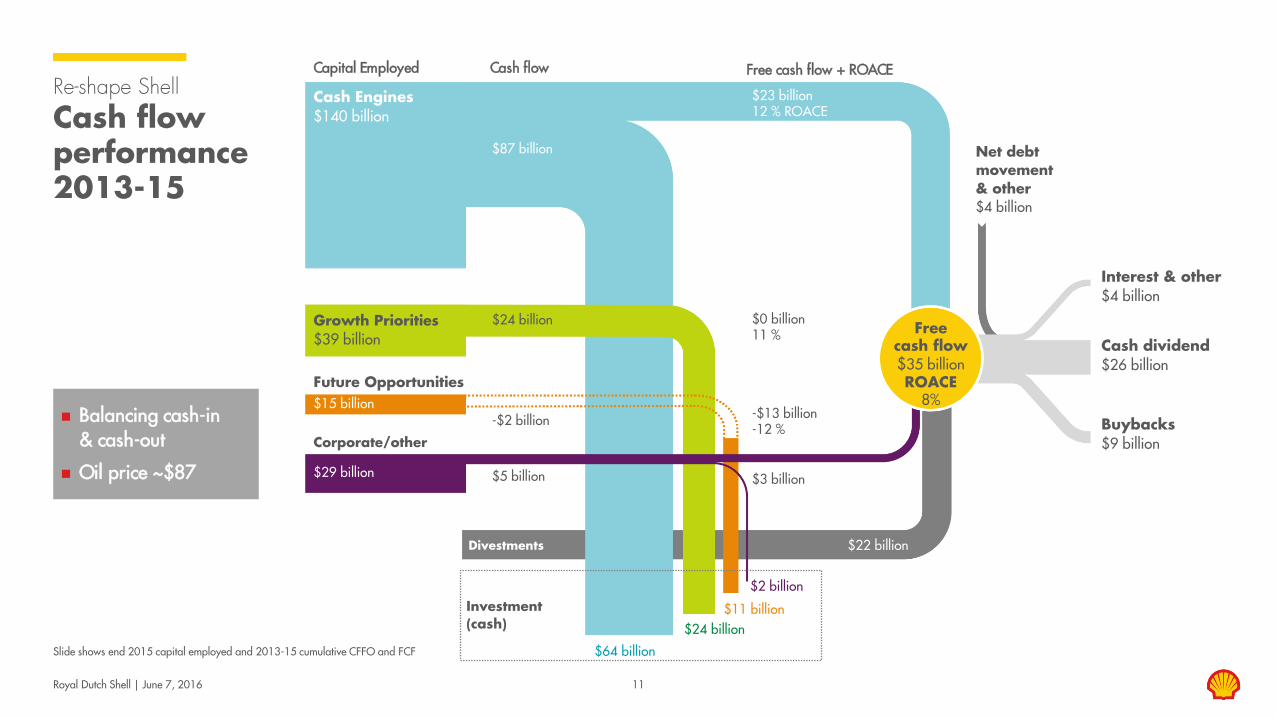

Re-shape Shell

Cash flow performance 2013-15

Free cash flow $35 billion ROACE

8%

Interest & other $4 billion

Cash dividend $26 billion

Buybacks $9 billion

Cash Engines $140 billion

Growth Priorities $39 billion

Future Opportunities $15 billion

Corporate/other

Divestments

Capital Employed Cash flow Free cash flow + ROACE

$87 billion

$23 billion 12 % ROACE

$24 billion $0 billion 11 %

-$2 billion

$64 billion

-$13 billion -12 %

$22 billion

$3 billion $5 billion

$24 billion $11 billion

$2 billion Investment (cash)

$29 billion

Net debt movement & other $4 billion

Balancing cash-in & cash-out

Oil price ~$87

11

Slide shows end 2015 capital employed and 2013-15 cumulative CFFO and FCF

Royal Dutch Shell | June 7, 2016 12

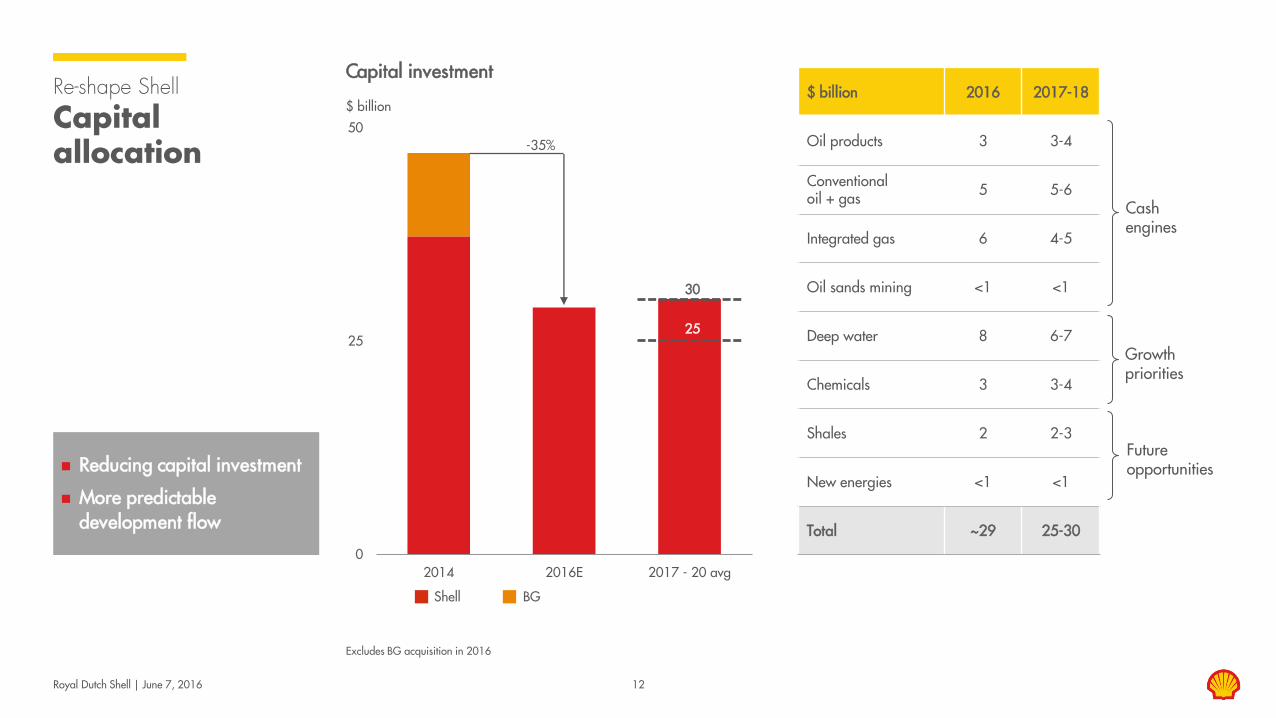

Re-shape Shell

Capital allocation

Excludes BG acquisition in 2016

0

25

50

2014 2016E 2017 - 20 avg

Reducing capital investment

More predictable development flow

Future opportunities

Growth priorities

Cash engines

$ billion

Capital investment

-35%

Shell BG

30

25

$ billion 2016 2017-18

Oil products 3 3-4

Conventional oil + gas 5 5-6

Integrated gas 6 4-5

Oil sands mining <1 <1

Deep water 8 6-7

Chemicals 3 3-4

Shales 2 2-3

New energies <1 <1

Total ~29 25-30

Royal Dutch Shell | June 7, 2016 13

Re-shape Shell

Cash engines Conventional oil + gas

Integrated Gas

Oil Products

Oil sands mining

High grade portfolio

Exploration to maintain running room

Moderate capacity growth rate

Prioritise for cash delivery

Strengthen the retained core

Selective marketing growth

Improve macro resilience Capture price upside

Name

0

15

30

45

2000 2005 2010 2015

Royal Dutch Shell | June 7, 2016

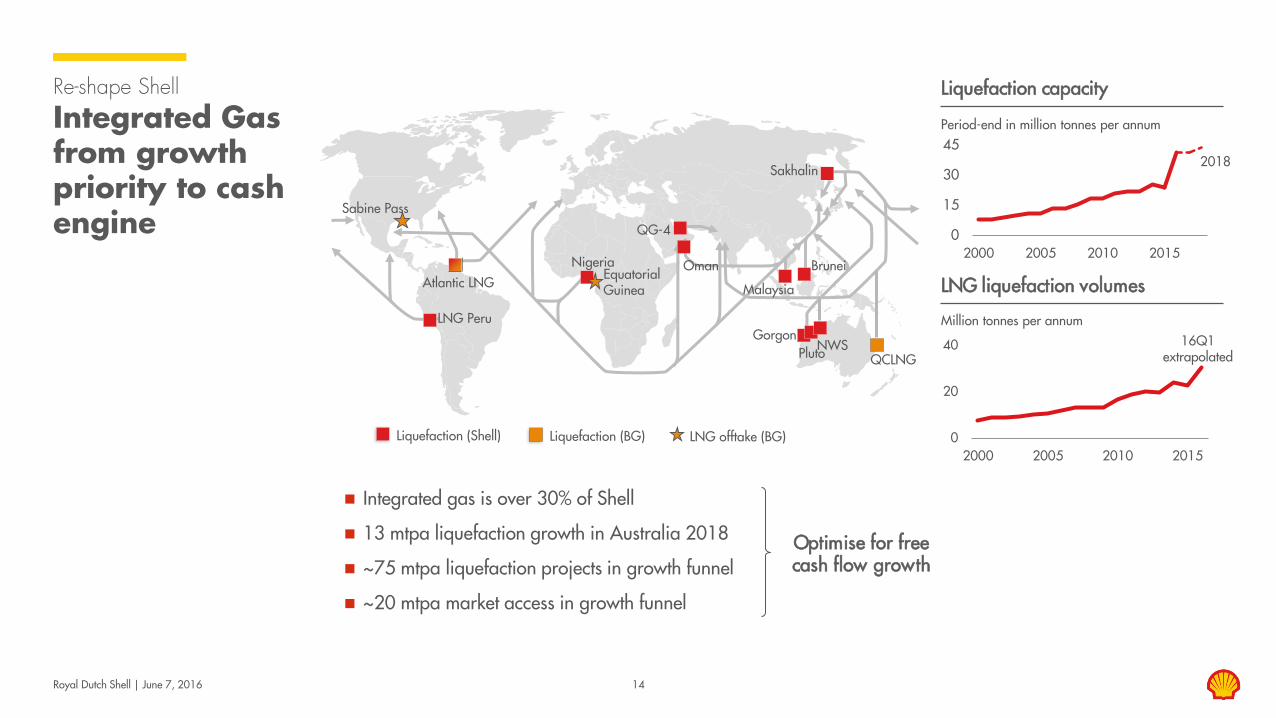

Re-shape Shell

Integrated Gas from growth priority to cash engine

Period-end in million tonnes per annum

Liquefaction capacity

Million tonnes per annum

LNG liquefaction volumes

0

20

40

2000 2005 2010 2015Liquefaction (Shell) LNG offtake (BG)

LNG Peru

Nigeria

QG-4

Atlantic LNG Oman

Sakhalin

Malaysia

Sabine Pass

Equatorial Guinea

Pluto NWS

Brunei

QCLNG

Gorgon

Integrated gas is over 30% of Shell

13 mtpa liquefaction growth in Australia 2018

~75 mtpa liquefaction projects in growth funnel

~20 mtpa market access in growth funnel

Optimise for free cash flow growth

16Q1 extrapolated

2018

14

Liquefaction (BG)

Royal Dutch Shell | June 7, 2016 15

Re-shape Shell

Growth priorities Deep water

Chemicals

Growth in advantaged geology

Brazil + GOM in focus

Multi-billion barrels potential

Advantaged feedstock + growth markets

USA + China growth

Royal Dutch Shell | June 7, 2016 16

Re-shape Shell

Future opportunities

Shales

New energies

~12 billion barrels resources + potential

Mature to ‘growth priority’

Energy transition themes

Explore + invest for longer term

Royal Dutch Shell | June 7, 2016 17

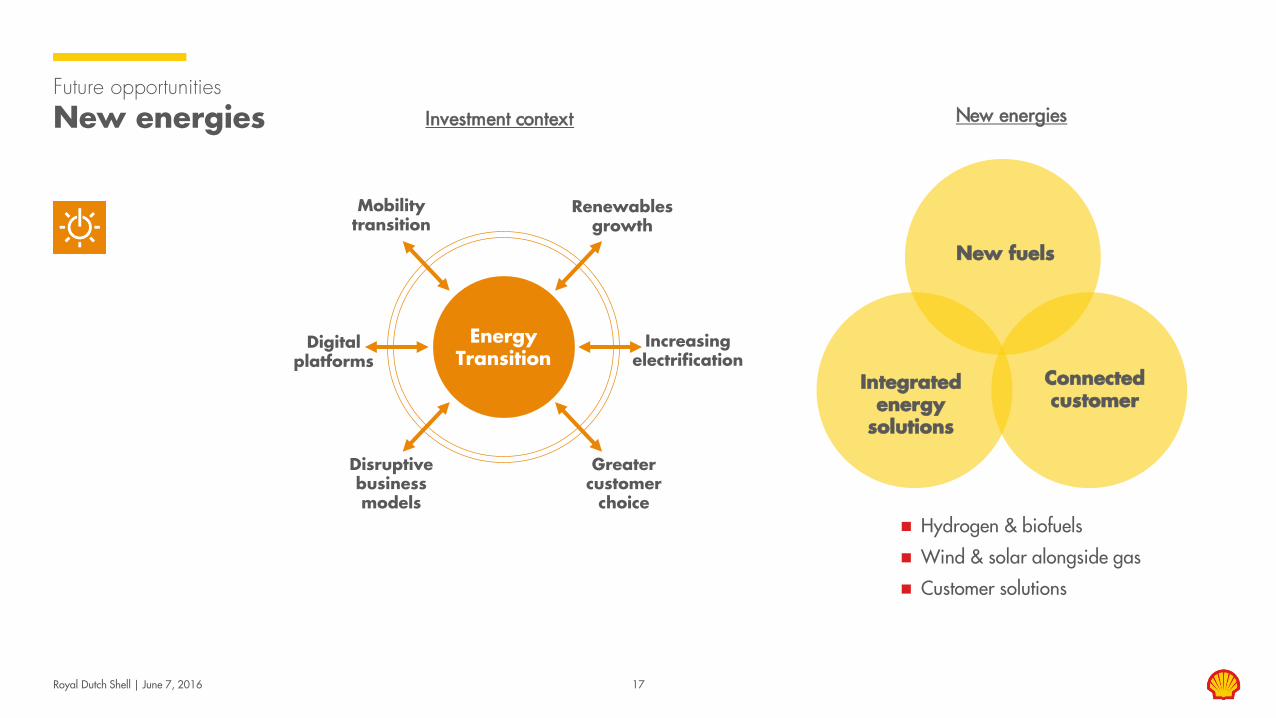

Future opportunities New energies

Hydrogen & biofuels

Wind & solar alongside gas

Customer solutions

New energies Investment context

Energy Transition

Digital platforms

Increasing electrification

Greater customer

choice

Renewables growth

Disruptive business models

Mobility transition

Integrated

energy solutions

New fuels

Connected customer

Simon Henry Chief Financial Officer Royal Dutch Shell plc

Royal Dutch Shell | June 7, 2016

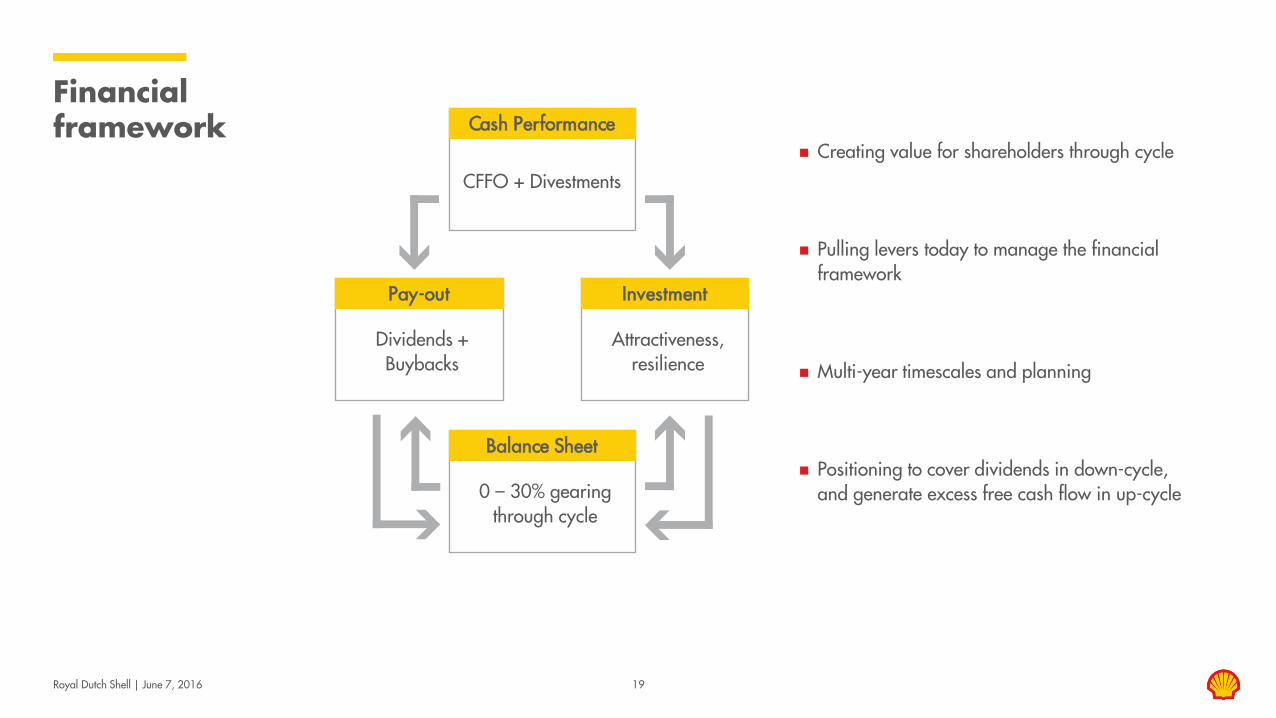

CFFO + Divestments

Attractiveness,

resilience

Dividends + Buybacks

0 – 30% gearing

through cycle

Royal Dutch Shell | June 7, 2016 19

Financial framework Cash Performance

Investment Pay-out

Balance Sheet

Creating value for shareholders through cycle

Pulling levers today to manage the financial framework

Multi-year timescales and planning

Positioning to cover dividends in down-cycle, and generate excess free cash flow in up-cycle

Royal Dutch Shell | June 7, 2016 20

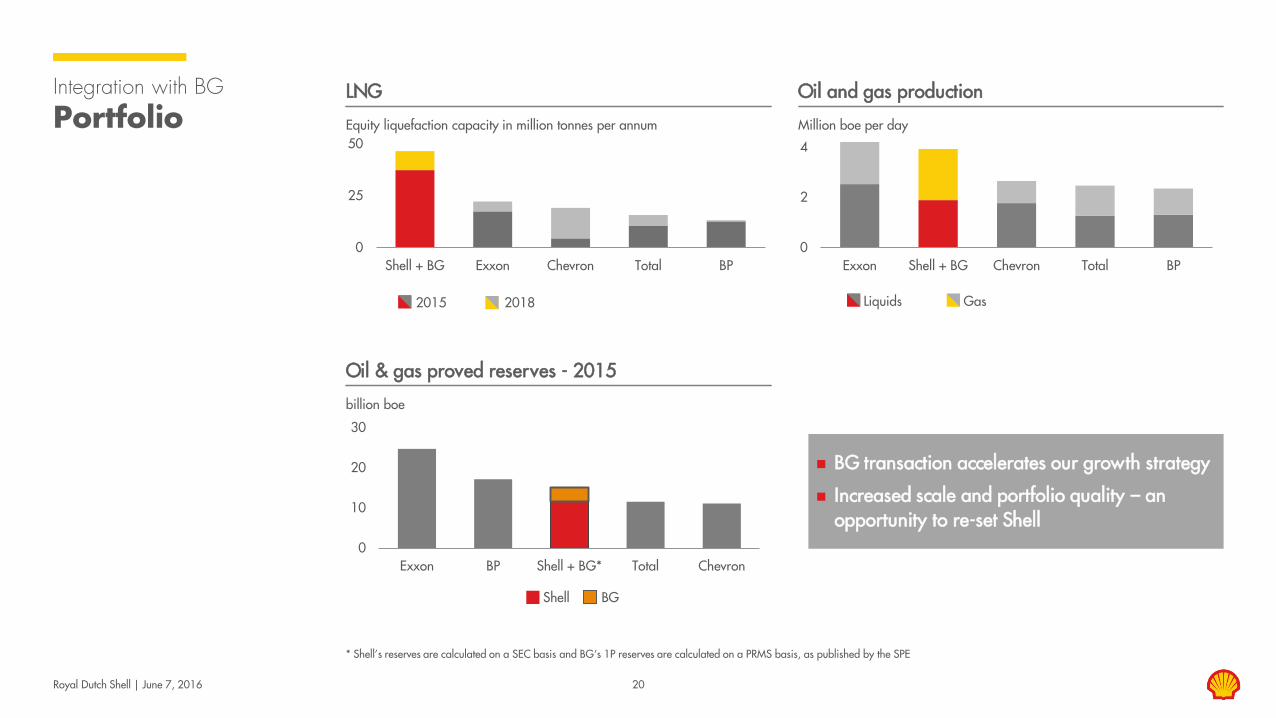

Integration with BG

Portfolio

* Shell’s reserves are calculated on a SEC basis and BG‘s 1P reserves are calculated on a PRMS basis, as published by the SPE

Equity liquefaction capacity in million tonnes per annum

0

25

50

Shell + BG Exxon Chevron Total BP

LNG

billion boe

0

10

20

30

Exxon BP Shell + BG* Total Chevron

Oil & gas proved reserves - 2015

Million boe per day

Oil and gas production

BG transaction accelerates our growth strategy

Increased scale and portfolio quality – an opportunity to re-set Shell

Liquids Gas 2015 2018

Shell BG

0

2

4

Exxon Shell + BG Chevron Total BP

Royal Dutch Shell | June 7, 2016 21

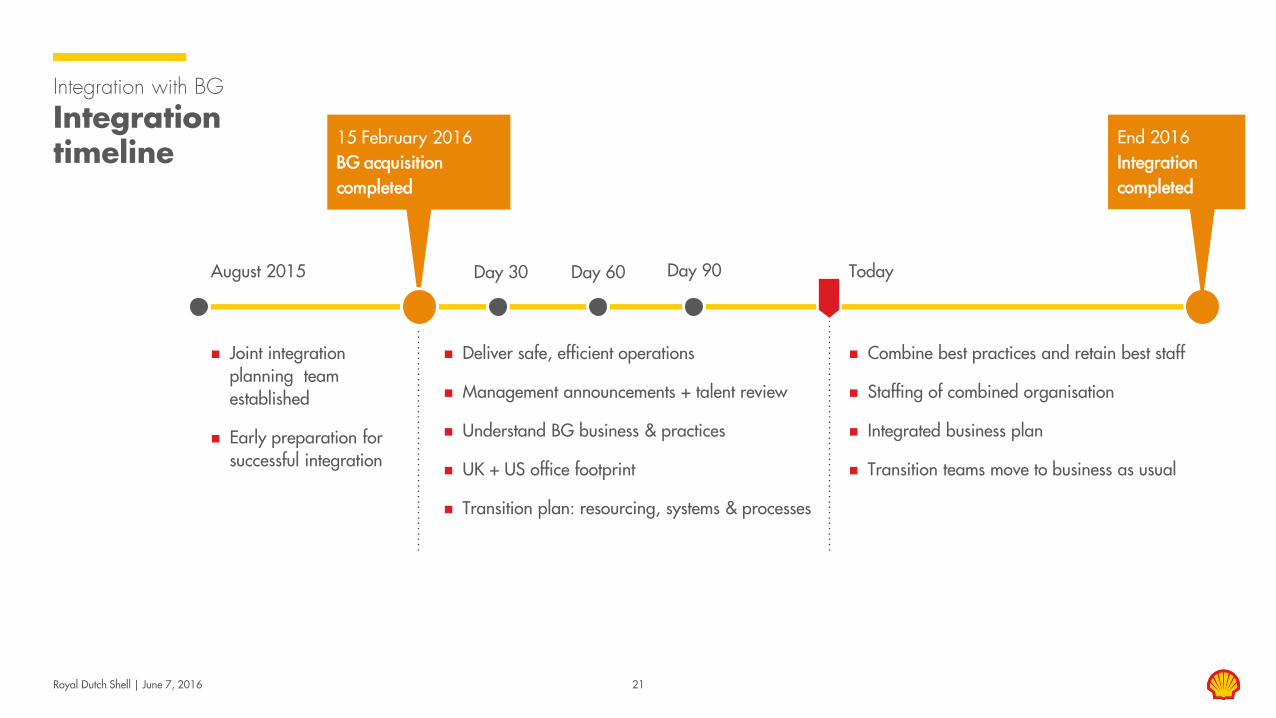

Integration with BG

Integration timeline

Deliver safe, efficient operations

Management announcements + talent review

Understand BG business & practices

UK + US office footprint

Transition plan: resourcing, systems & processes

End 2016 Integration completed

15 February 2016 BG acquisition completed

Day 60 Day 30 Day 90

Combine best practices and retain best staff

Staffing of combined organisation

Integrated business plan

Transition teams move to business as usual

Today

Joint integration planning team established

Early preparation for successful integration

August 2015

2016 2017 2018

-1

0

1

2

3

4

Royal Dutch Shell | June 7, 2016 22

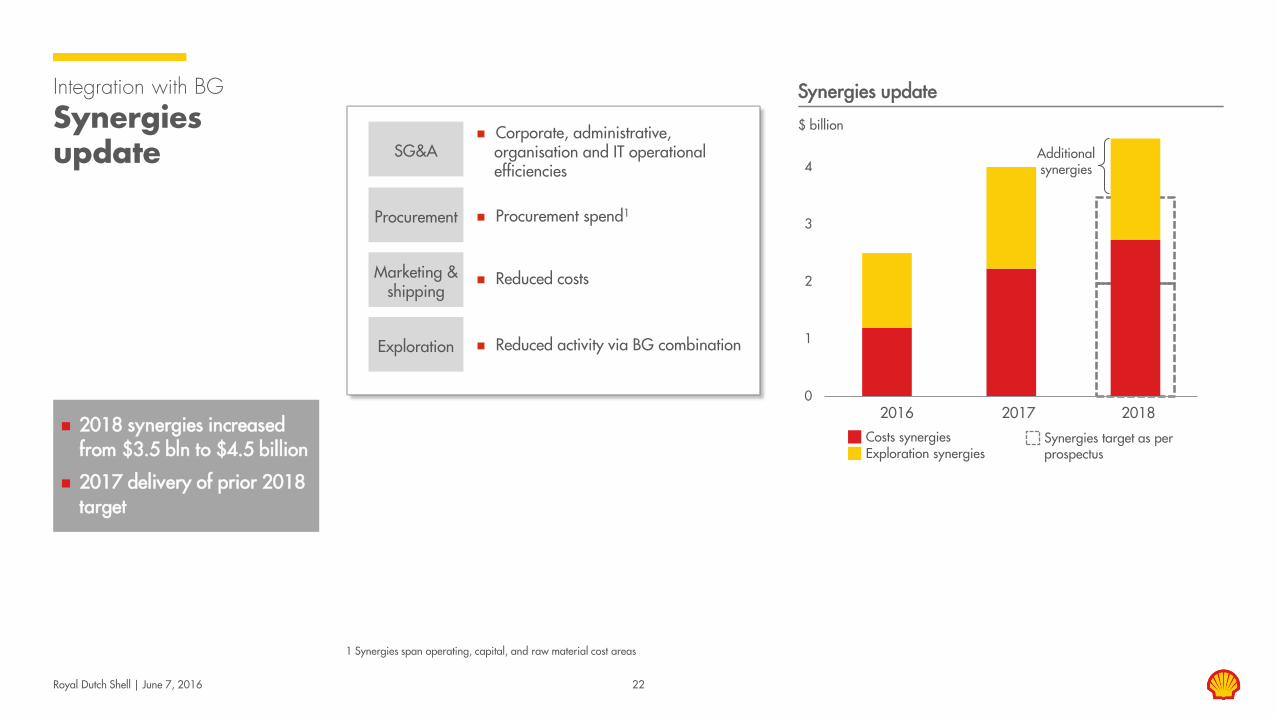

Integration with BG

Synergies update

1 Synergies span operating, capital, and raw material cost areas

$ billion

Synergies update

2018 synergies increased from $3.5 bln to $4.5 billion

2017 delivery of prior 2018 target

Additional synergies

SG&A

Procurement

Marketing & shipping

Corporate, administrative, organisation and IT operational efficiencies

Reduced costs

Procurement spend1

Exploration Reduced activity via BG combination

Exploration synergies Costs synergies Synergies target as per

prospectus

Royal Dutch Shell | June 7, 2016 23

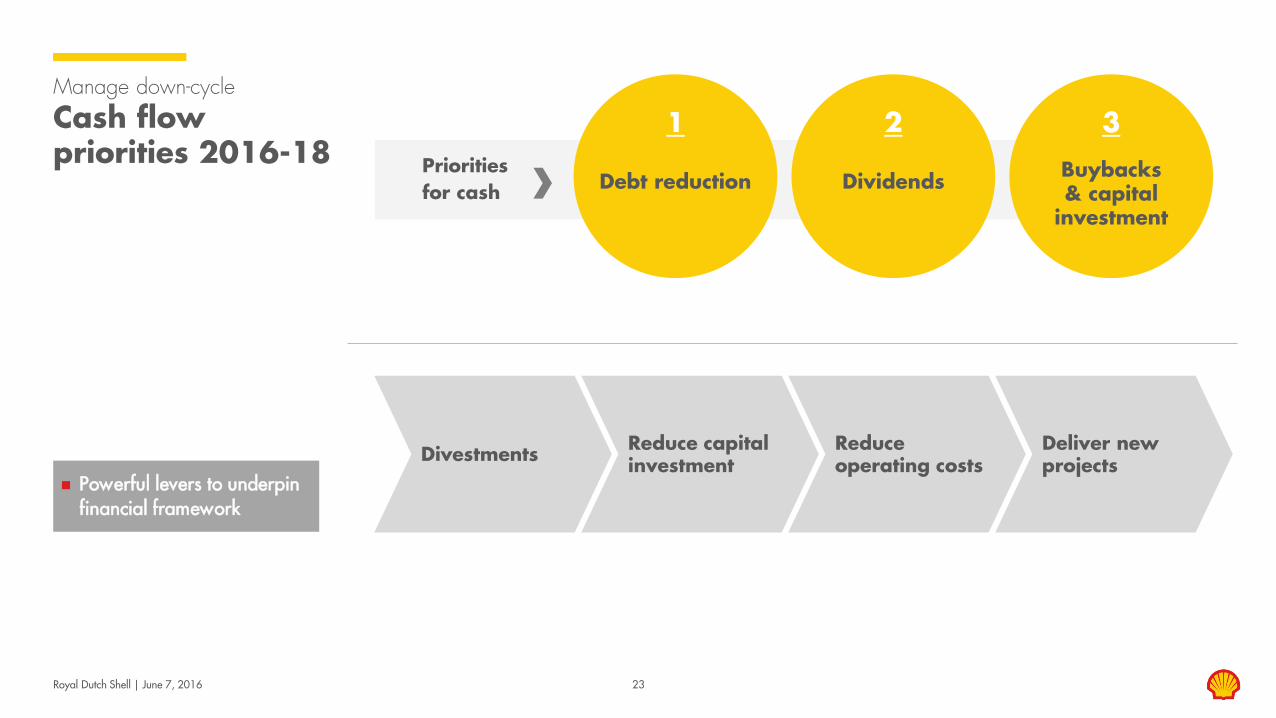

Manage down-cycle

Cash flow priorities 2016-18

Powerful levers to underpin financial framework

Priorities for cash Debt reduction Dividends

Buybacks & capital

investment

1

2

3

Divestments Reduce capital investment

Reduce operating costs

Deliver new projects

Royal Dutch Shell | June 7, 2016 24

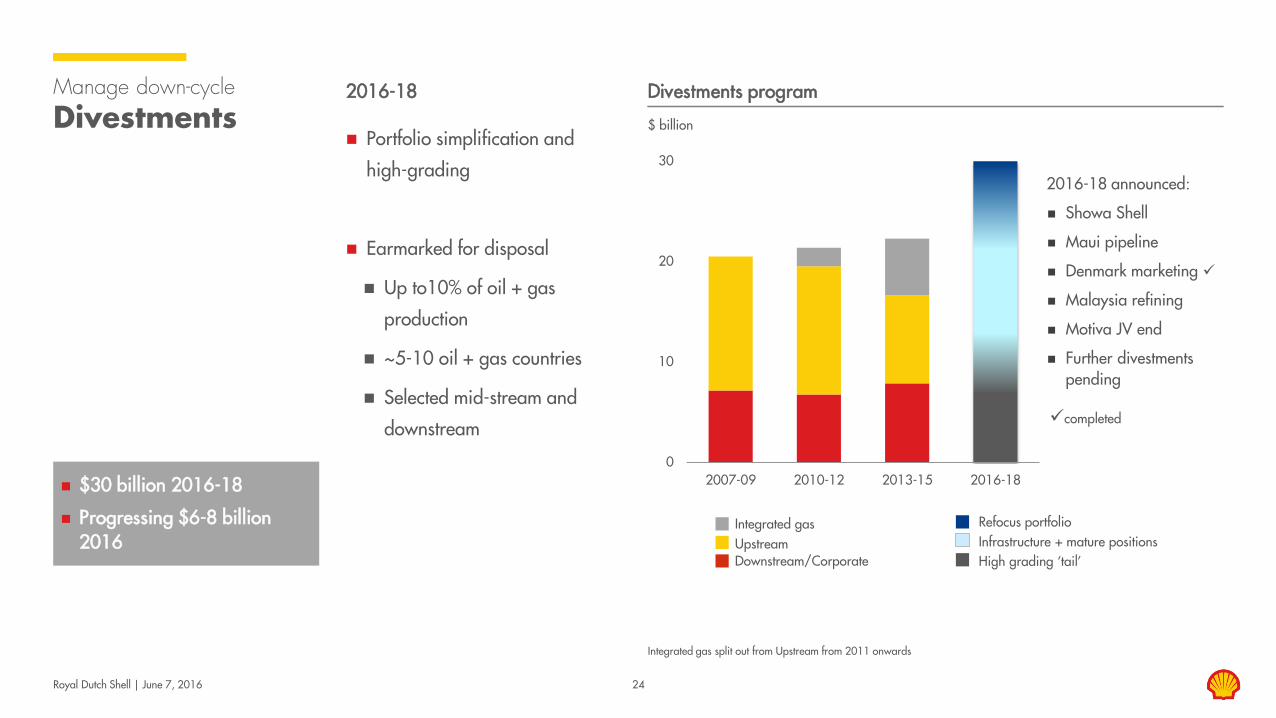

Manage down-cycle Divestments

Integrated gas split out from Upstream from 2011 onwards

$ billion

2016-18

Portfolio simplification and

high-grading

Earmarked for disposal

Up to10% of oil + gas

production

~5-10 oil + gas countries

Selected mid-stream and

downstream

Divestments program

$30 billion 2016-18

Progressing $6-8 billion 2016

0

10

20

30

2007-09 2010-12 2013-15 2016-18

Downstream/Corporate High grading ‘tail’ Infrastructure + mature positions Refocus portfolio

2016-18 announced:

Showa Shell

Maui pipeline

Denmark marketing

Malaysia refining

Motiva JV end

Further divestments pending

completed

Upstream Integrated gas

Royal Dutch Shell | June 7, 2016 25

Manage down-cycle

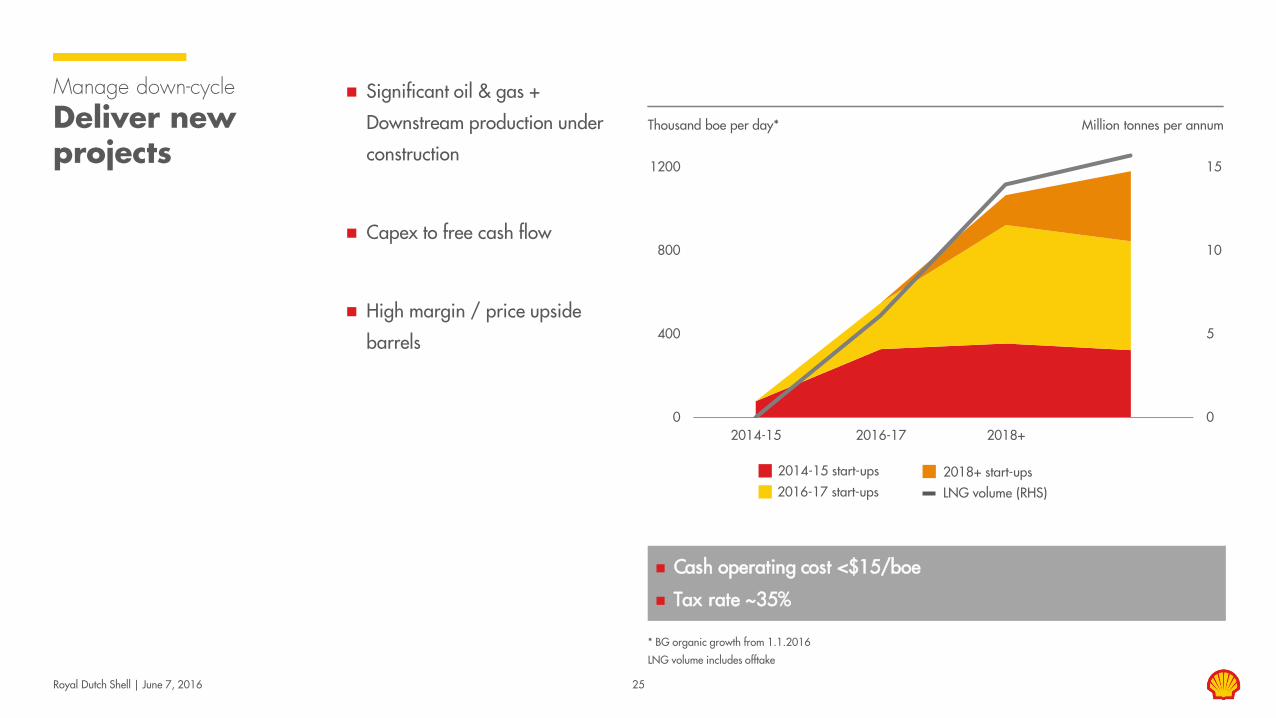

Deliver new projects

* BG organic growth from 1.1.2016

LNG volume includes offtake

Thousand boe per day*

Significant oil & gas +

Downstream production under

construction

Capex to free cash flow

High margin / price upside

barrels

2016-17 start-ups

2014-15 start-ups

LNG volume (RHS) 2018+ start-ups

Million tonnes per annum

Cash operating cost <$15/boe

Tax rate ~35%

0

5

10

15

0

400

800

1200

2014-15 2016-17 2018+

Royal Dutch Shell | June 7, 2016 26

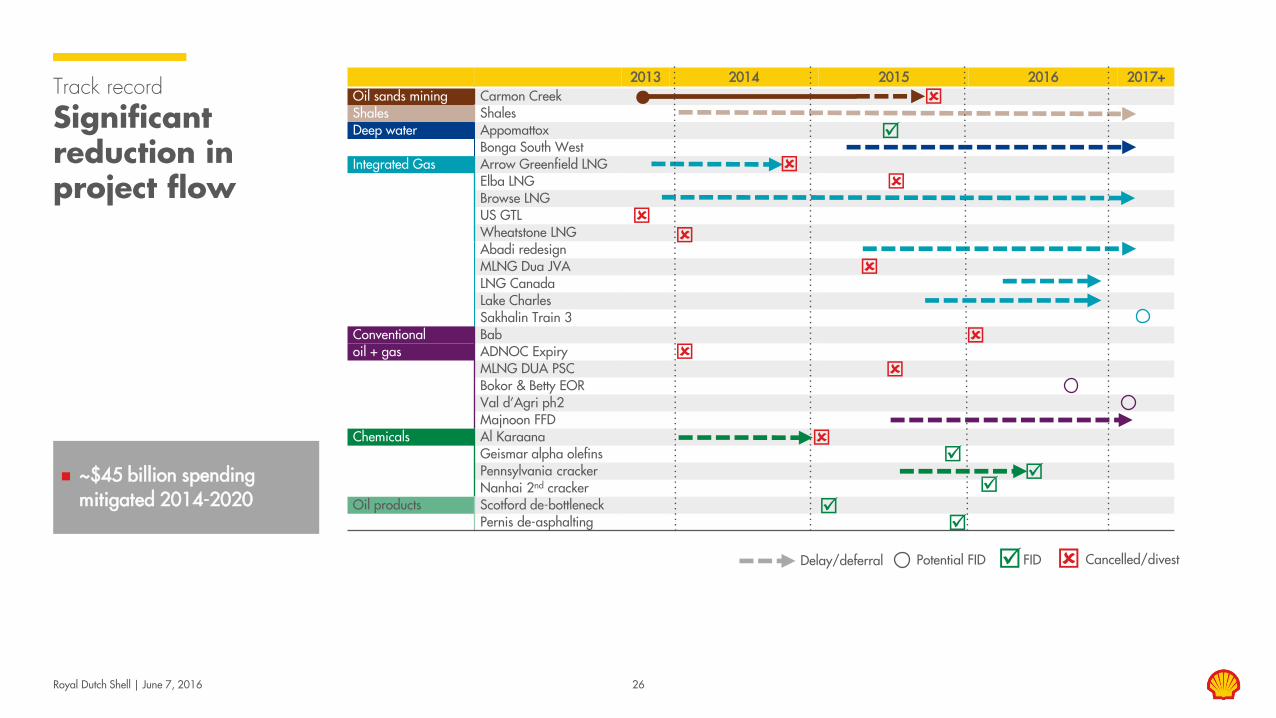

Track record

Significant reduction in project flow

2013 2014 2015 2016 2017+ Oil sands mining Carmon Creek Shales Shales Deep water Appomattox

Bonga South West Integrated Gas Arrow Greenfield LNG

Elba LNG Browse LNG US GTL Wheatstone LNG Abadi redesign MLNG Dua JVA LNG Canada Lake Charles Sakhalin Train 3

Conventional Bab oil + gas ADNOC Expiry

MLNG DUA PSC Bokor & Betty EOR Val d’Agri ph2 Majnoon FFD

Chemicals Al Karaana Geismar alpha olefins Pennsylvania cracker Nanhai 2nd cracker

Oil products Scotford de-bottleneck Pernis de-asphalting

~$45 billion spending mitigated 2014-2020

FID Cancelled/divest Potential FID Delay/deferral

Frontier

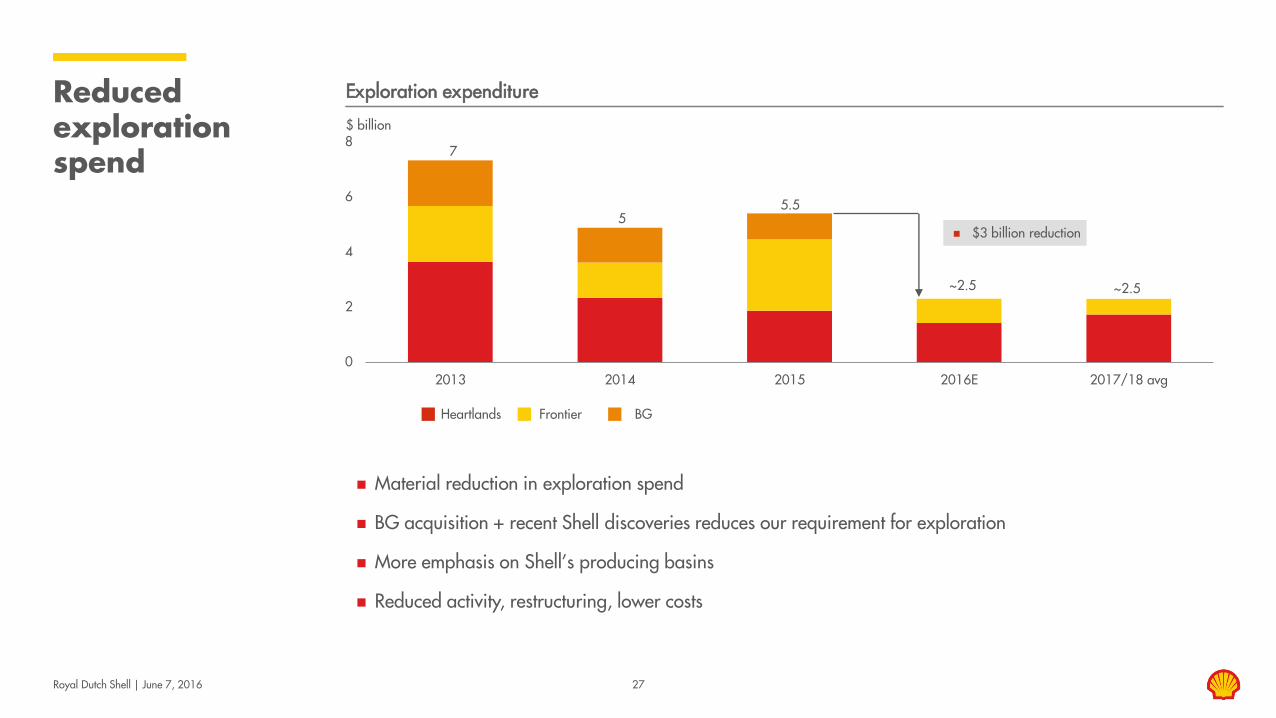

Material reduction in exploration spend

BG acquisition + recent Shell discoveries reduces our requirement for exploration

More emphasis on Shell’s producing basins

Reduced activity, restructuring, lower costs

Royal Dutch Shell | June 7, 2016 27

Reduced exploration spend

$ billion

Exploration expenditure

0

2

4

6

8

2013 2014 2015 2016E 2017/18 avg

$3 billion reduction

BG Heartlands

~2.5

7

5 5.5

~2.5

Royal Dutch Shell | June 7, 2016 28

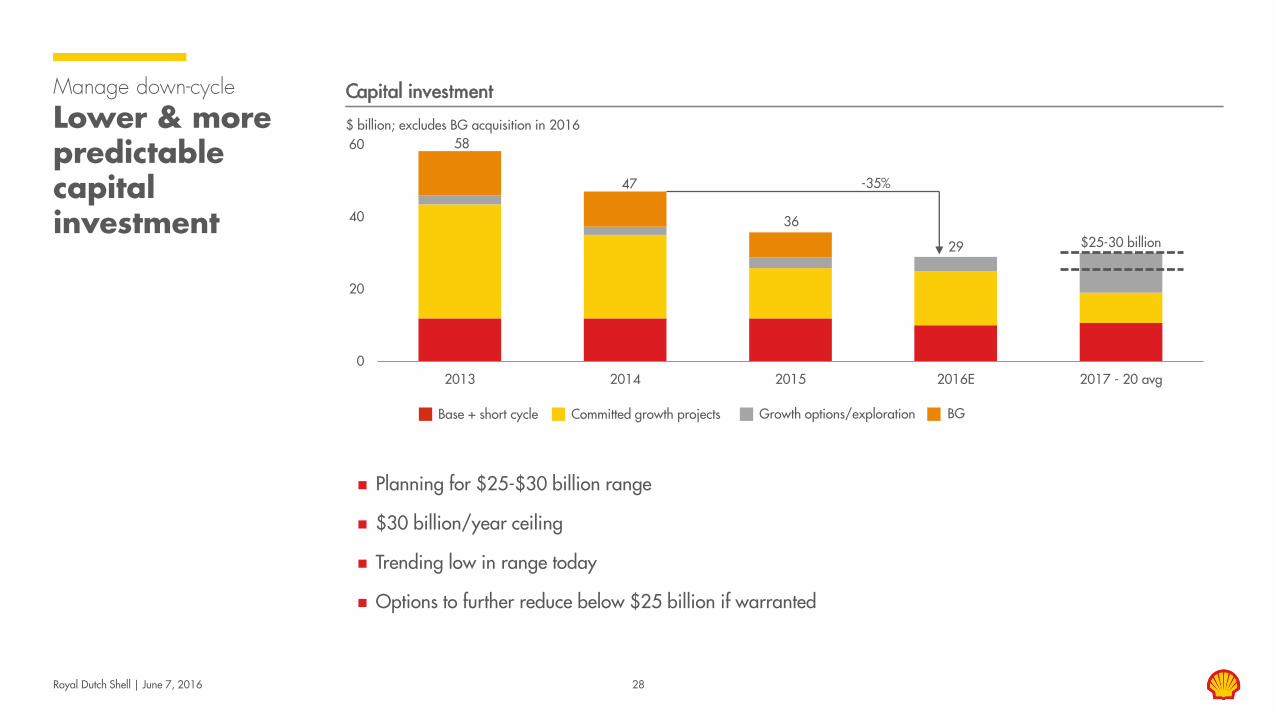

Manage down-cycle

Lower & more predictable capital investment

$ billion; excludes BG acquisition in 2016

Capital investment

Planning for $25-$30 billion range

$30 billion/year ceiling

Trending low in range today

Options to further reduce below $25 billion if warranted

0

20

40

60

2013 2014 2015 2016E 2017 - 20 avg

Growth options/exploration Base + short cycle Committed growth projects BG

$25-30 billion

58

47

36

29

-35%

Royal Dutch Shell | June 7, 2016 29

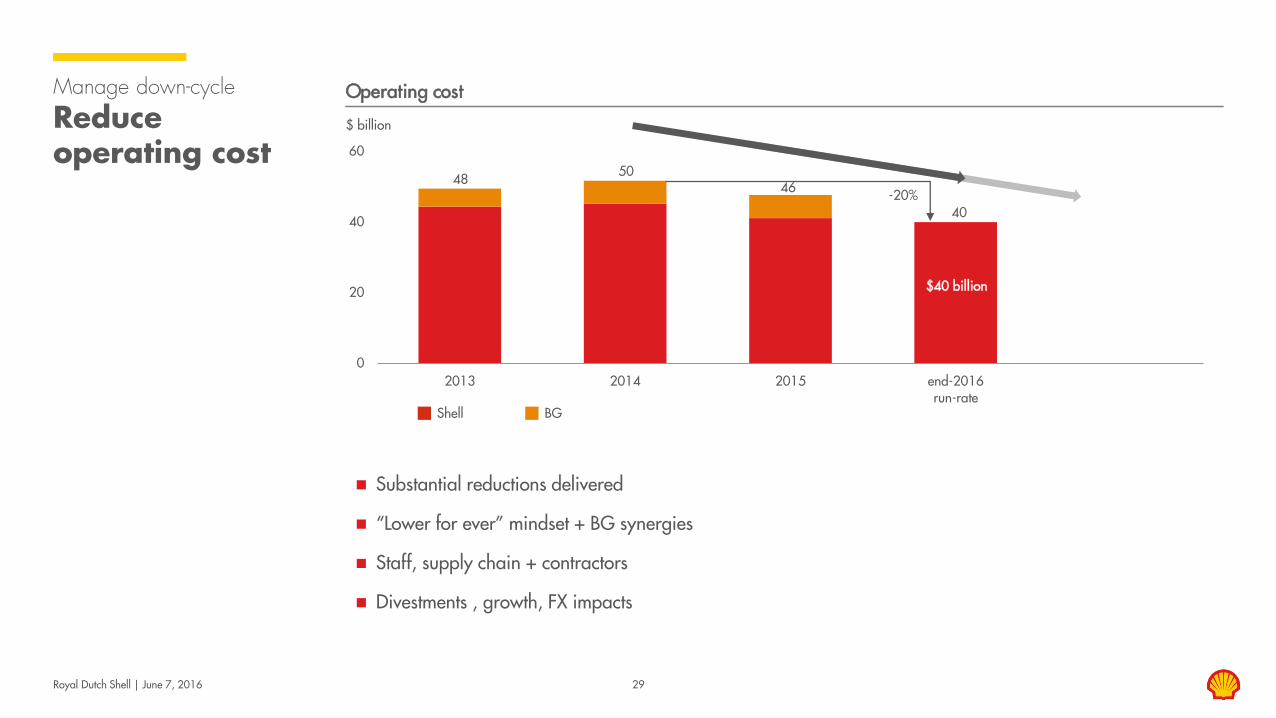

Manage down-cycle

Reduce operating cost

$ billion

Operating cost

0

20

40

60

2013 2014 2015 end-2016run-rate

$40 billion

-20%

Substantial reductions delivered

“Lower for ever” mindset + BG synergies

Staff, supply chain + contractors

Divestments , growth, FX impacts

Shell BG

48 50 46

40

Royal Dutch Shell | June 7, 2016 30

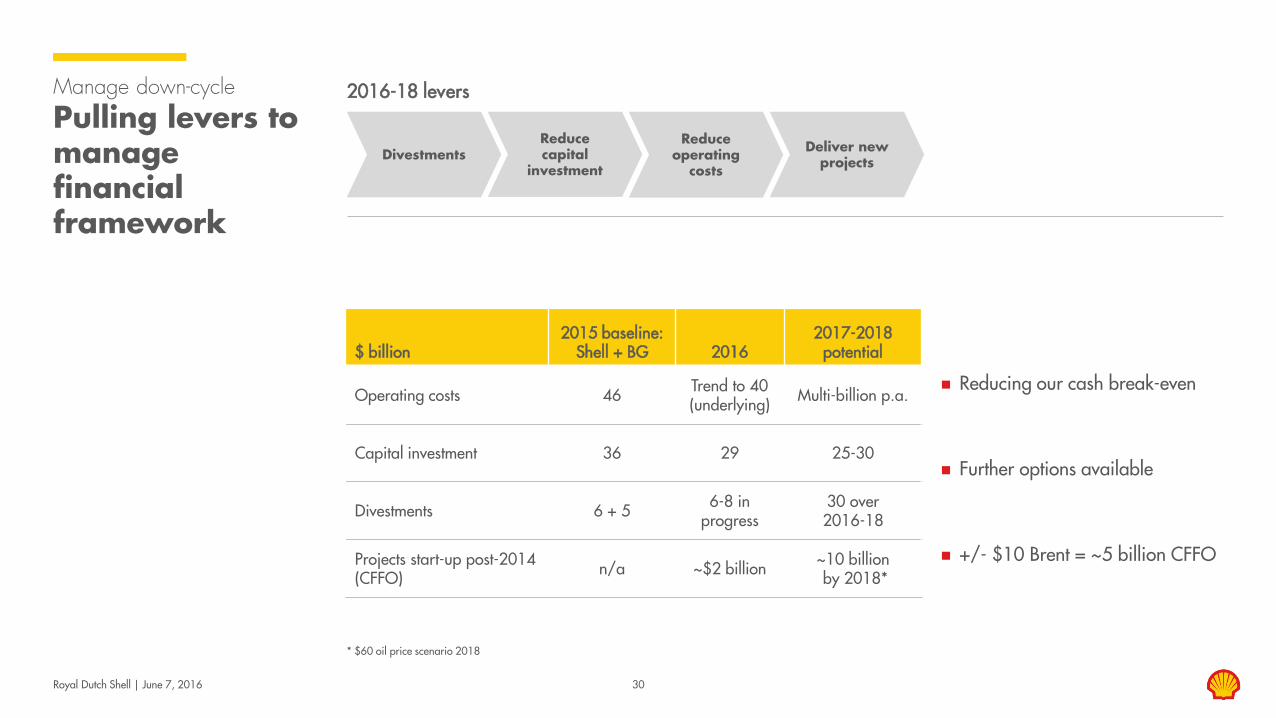

Manage down-cycle

Pulling levers to manage financial framework

* $60 oil price scenario 2018

2016-18 levers

Reducing our cash break-even

Further options available

+/- $10 Brent = ~5 billion CFFO

Divestments Reduce capital

investment

Reduce operating

costs

Deliver new projects

$ billion 2015 baseline:

Shell + BG 2016 2017-2018

potential

Operating costs 46 Trend to 40 (underlying) Multi-billion p.a.

Capital investment 36 29 25-30

Divestments 6 + 5 6-8 in progress

30 over 2016-18

Projects start-up post-2014 (CFFO) n/a ~$2 billion ~10 billion

by 2018*

Ben van Beurden Chief Executive Officer Royal Dutch Shell plc

Royal Dutch Shell | June 7, 2016

Royal Dutch Shell | June 7, 2016

Transformation

CREATE A WORLD CLASS INVESTMENT CASE

Improved capital efficiency: reduced investment/FCF ratio

Energy transition: CO2 footprint & new energies strategy

Simpler company: Exit ~10% production; 5-10 countries

Less cost + fewer people with BG than Shell stand-alone: 12,500 fewer staff

Capital efficiency: 2013 spending halved & $45 billion mitigated

Improving our metrics: FCF/share; ROCE; net debt

$30bn divestments: Innovative deals like Motiva, Showa and MLP

Portfolio growth: 1 mboe/d adds $10 bln cash flow

2019-2021 average

2013-2015 average

Brent

ROACE

~$60

~10%

~$90

8%

Organic free cash flow $20-25 billion p.a. $5 billion p.a.

32

Questions & Answers

Royal Dutch Shell | June 7, 2016

Royal Dutch Shell plc June 7, 2016

Capital markets day 2016 Re-shaping Shell, to create a world-class investment case

“Let’s make the future”

Royal Dutch Shell | June 7, 2016

Recommended