Pricing & Costing: including budgeting & life cycle costing

Anjana [email protected]

1www.bizkul.com

www.bizkul.com 2

Costs: Some terms Direct Indirect

Committed Flexible

www.bizkul.com 3

Costs

Fixed Variable Semi variable

www.bizkul.com 4

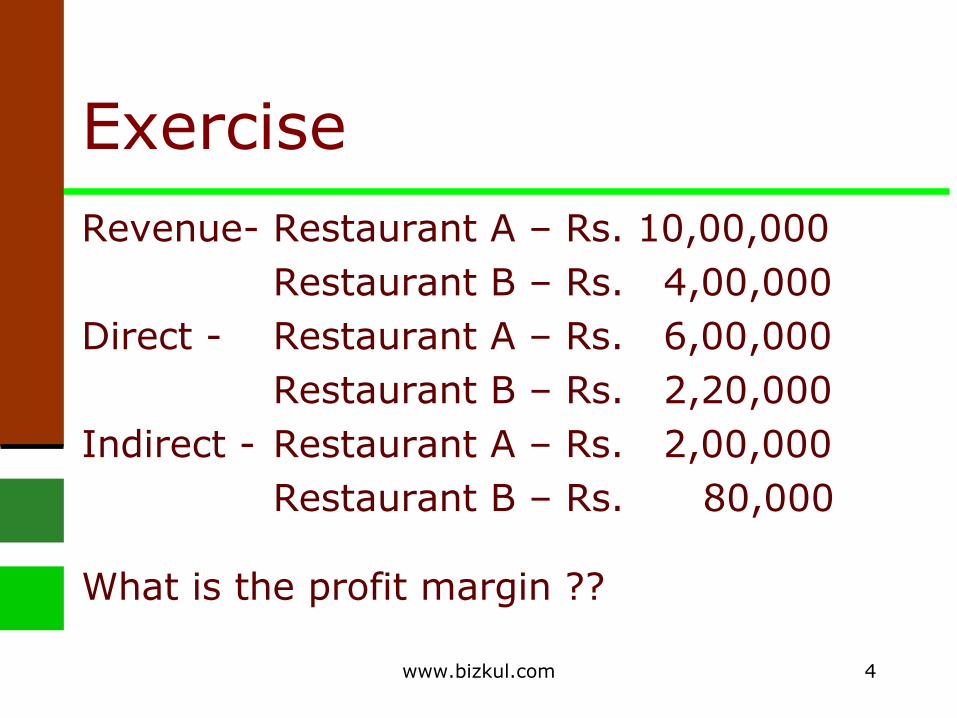

ExerciseRevenue- Restaurant A – Rs. 10,00,000

Restaurant B – Rs. 4,00,000Direct - Restaurant A – Rs. 6,00,000

Restaurant B – Rs. 2,20,000Indirect - Restaurant A – Rs. 2,00,000

Restaurant B – Rs. 80,000

What is the profit margin ??

www.bizkul.com 5

ExerciseRevenue- Restaurant A – Rs. 10,00,000

Restaurant B – Rs. 4,00,000Direct - Restaurant A – Rs. 6,00,000

Restaurant B – Rs. 2,20,000Indirect - Restaurant A – Rs. 2,00,000

Restaurant B – Rs. 80,000

What are your thoughts on the profit so calculated?

www.bizkul.com 6

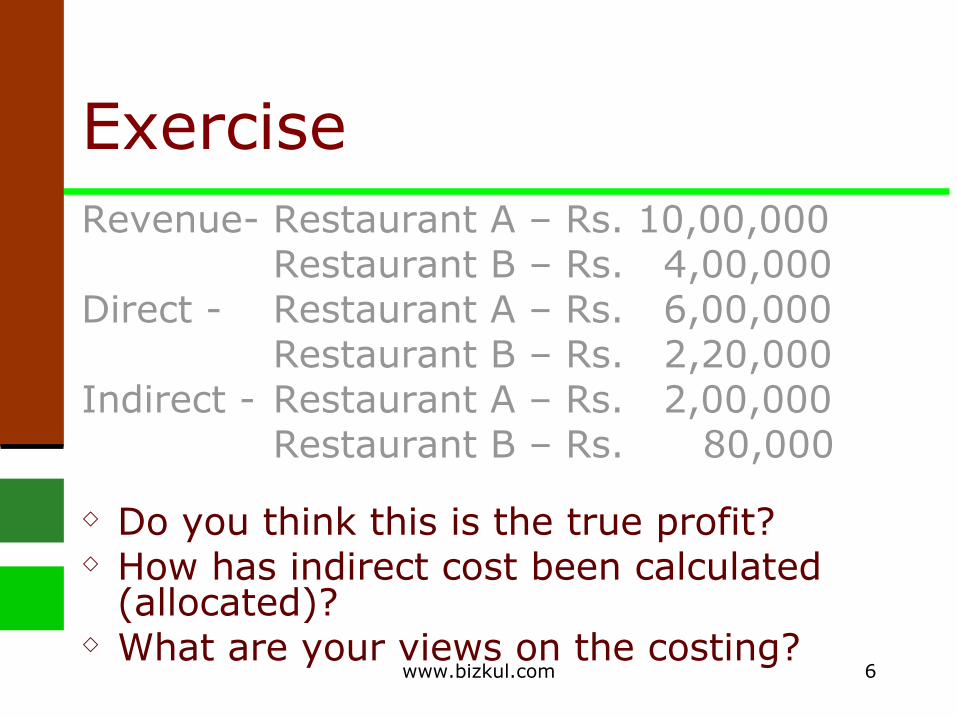

ExerciseRevenue- Restaurant A – Rs. 10,00,000

Restaurant B – Rs. 4,00,000Direct - Restaurant A – Rs. 6,00,000

Restaurant B – Rs. 2,20,000Indirect - Restaurant A – Rs. 2,00,000

Restaurant B – Rs. 80,000

Do you think this is the true profit? How has indirect cost been calculated

(allocated)? What are your views on the costing?

www.bizkul.com 7

ExerciseRevenue- Restaurant A – Rs. 10,00,000

Restaurant B – Rs. 4,00,000Direct - Restaurant A – Rs. 6,00,000

Restaurant B – Rs. 2,20,000Indirect - Restaurant A – Rs. 2,00,000

Restaurant B – Rs. 80,000

How does change in basis of allocation impact profit ?

www.bizkul.com 8

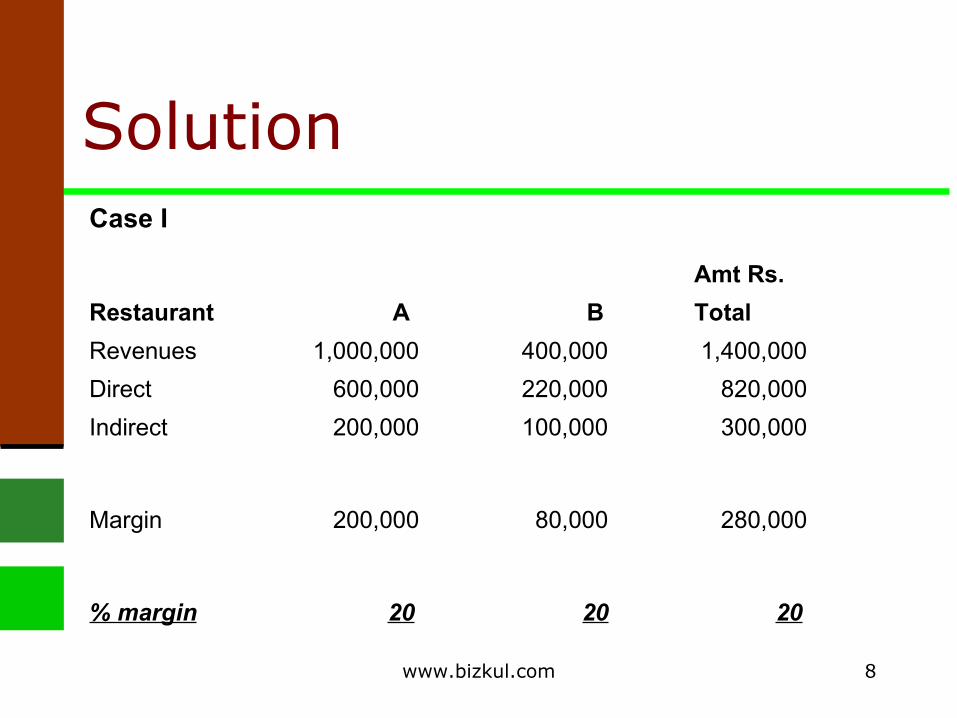

SolutionCase I

Amt Rs.

Restaurant A B Total

Revenues 1,000,000 400,000 1,400,000

Direct 600,000 220,000 820,000

Indirect 200,000 100,000 300,000

Margin 200,000 80,000 280,000

% margin 20 20 20

www.bizkul.com 9

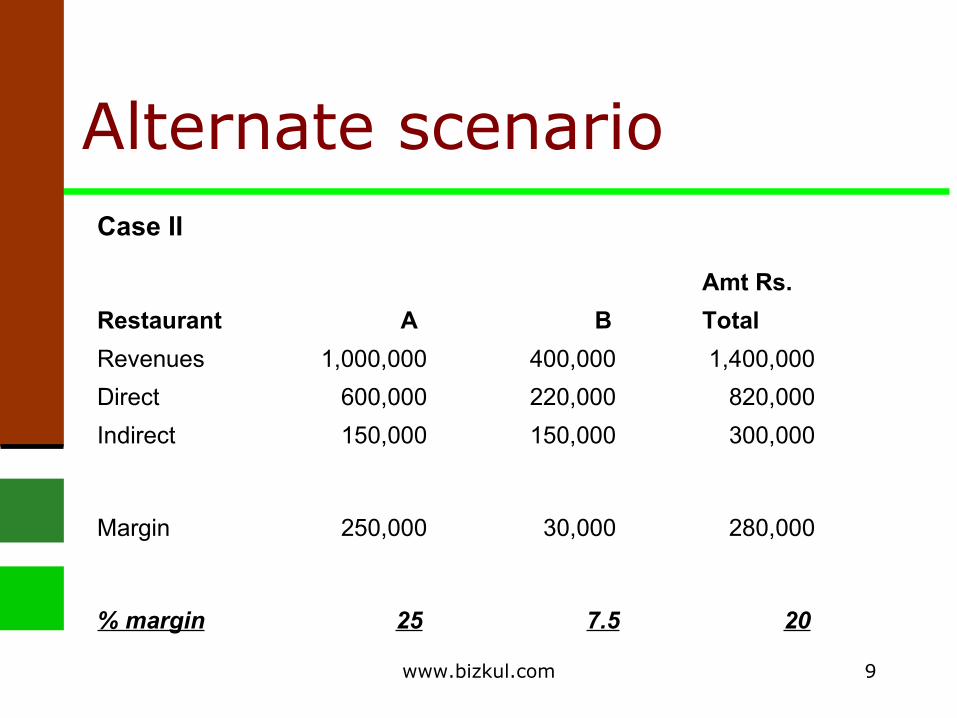

Alternate scenarioCase II

Amt Rs.

Restaurant A B Total

Revenues 1,000,000 400,000 1,400,000

Direct 600,000 220,000 820,000

Indirect 150,000 150,000 300,000

Margin 250,000 30,000 280,000

% margin 25 7.5 20

www.bizkul.com 10

Costs Costs are incurred in a variety of

functions in business–Establishing business–R&D–Production / Delivery of service–Sales and marketing–After sales service–Administration

www.bizkul.com 11

Importance of costing

Planning Controlling Decision making Implementing Continuous improvement

www.bizkul.com 12

Costs Controllable Joint Discretionary Relevant Sunk Opportunity

www.bizkul.com 13

Costs: Analysis Useful to decide what is controllable

and what is not Helps to understand what is relevant

to decision making Must be done with care to avoid

incorrect decisions

www.bizkul.com 14

Relevant costs Expected future costs to help in making

decisions Differ with alternate courses of action

– Managers make decisions based on costs allocated

– Managers may make short run decisions that may affect long term business and sales

Relevant costs help choose between alternatives

www.bizkul.com 15

Costs - relevant / not relevant

Equipment replacement–Book value of old equipment – not

relevant–Current disposal price of old equipment

– relevant–Cost of equipment - relevant

www.bizkul.com 16

Costing: Some terms

Contribution margin Break even point

www.bizkul.com 17

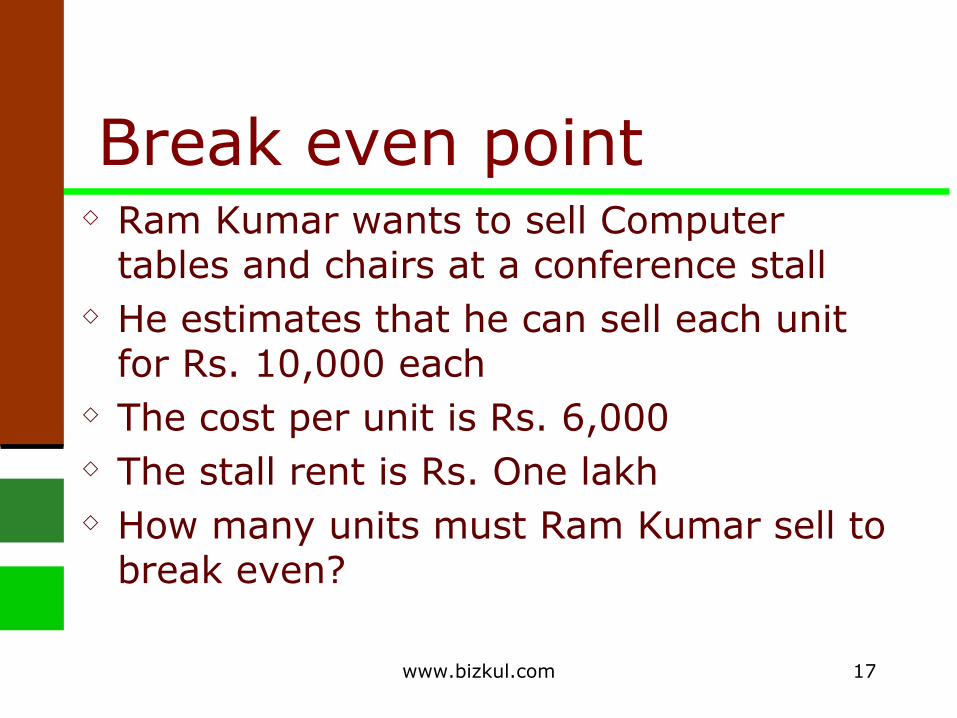

Break even point Ram Kumar wants to sell Computer

tables and chairs at a conference stall He estimates that he can sell each unit

for Rs. 10,000 each The cost per unit is Rs. 6,000 The stall rent is Rs. One lakh How many units must Ram Kumar sell to

break even?

www.bizkul.com 18

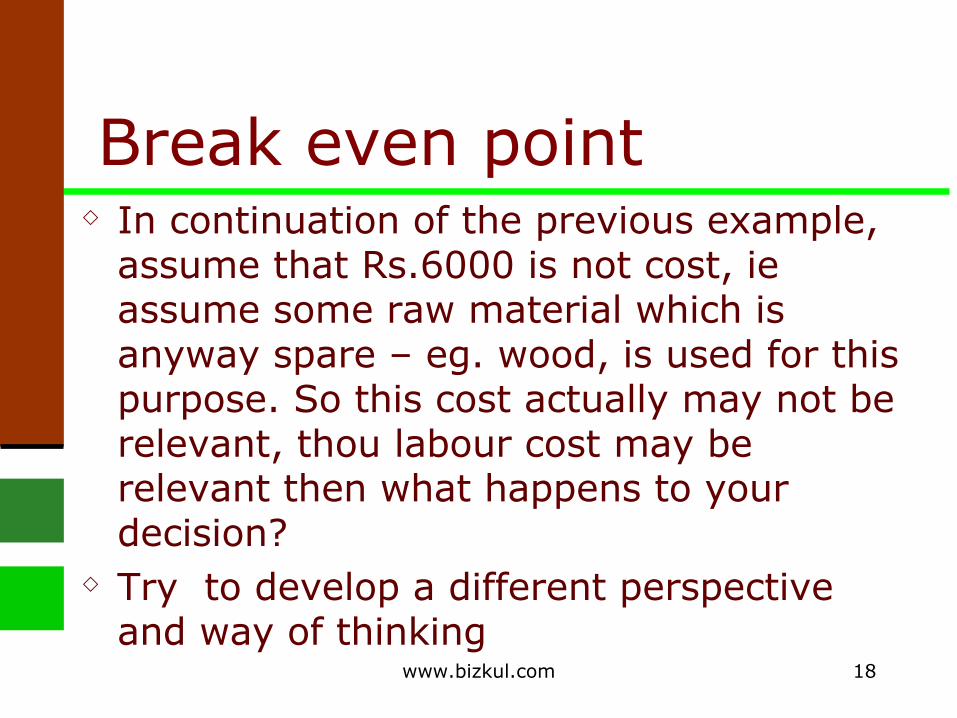

Break even point In continuation of the previous example,

assume that Rs.6000 is not cost, ie assume some raw material which is anyway spare – eg. wood, is used for this purpose. So this cost actually may not be relevant, thou labour cost may be relevant then what happens to your decision?

Try to develop a different perspective and way of thinking

www.bizkul.com 19

Costing: Some terms

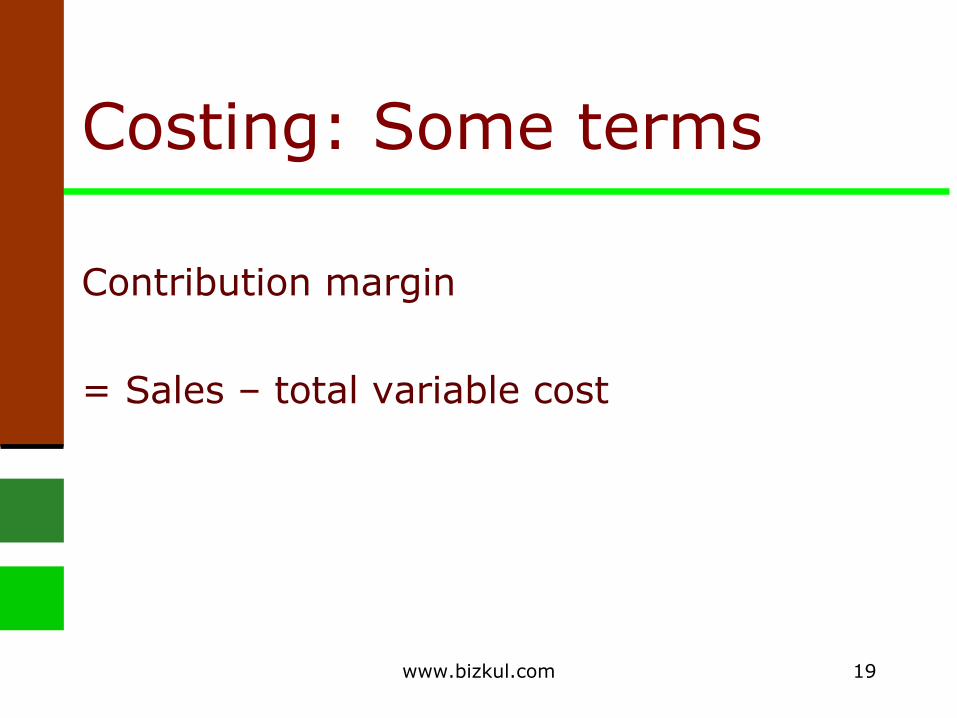

Contribution margin

= Sales – total variable cost

www.bizkul.com 20

Costs: Analysis

Identify cost objects / cost centres Accumulate costs Assign / trace costs to cost objects

www.bizkul.com 21

Assignment / Allocation

Selection of Activity base – people; machine hours;

material consumed Activity level – normal/abnormal

www.bizkul.com 22

Budgets Plan performance in advance for a

given time frame Review performance with budget Understand reasons for variation Take remedial measures if required Plan again based on actual

performance and feedback

www.bizkul.com 23

Budgets Keep company objectives in mind Long term and short term Rolling budgets

www.bizkul.com 24

Budgets Master budget, comprising of

detailed budgets for eg. budgets for – Income–Production–Direct costs–R&D–Administration

www.bizkul.com 25

Product budget Expected sale Inventory on hand Production schedule Direct costs Indirect costs Company policies and strategy

www.bizkul.com 26

Life cycle costing Considers entire life cycle of product from

start to finish Provides important information for pricing

decisions For example, if a mobile phone is built, if

the R&D costs are high for the company, the repairs and maintenance cost to the customer may be low; so the life cycle is across the life of the product and considers costs and impact on prices

www.bizkul.com 27

Life cycle costs Upstream costs

–R&D, design, prototyping, testing, quality development

Manufacturing/Operations costs–Purchasing, manufacture/service

Downstream costs–marketing, sales and distribution,

customer service and warranty

www.bizkul.com 28

Life cycle costs Product life cycle costs vary with

industry and nature of industry R&D is not only at start of product

life, this may also occur at other stages, ie development of additional features in product

Life cycle may also depend on markets targeted, ie country, region, socio-economic background etc.

www.bizkul.com 29

Implementation of LCC Identify stages in product life cycle Identify target customer Understand target customers

perspective and estimate need Analyse cost and pricing in detail Educate employees about LCC

www.bizkul.com 30

Implementation of LCC Develop product and pricing structure

based on LCC Create appropriate organisation structure

for implementation Educate customer on LCC, eg. mobile

phone referred to in earlier slide Focus on strategic marketing to address

customer requirements and needs, stated and unstated

Continuous life cycle budgeting and monitoring and modify/change as required

www.bizkul.com 31

Life cycle costing benefits

Optimisation of profit over product life

Full set of costs associated with products are ascertained–Most accounting systems capture

manufacturing costs–Other areas like R&D at start and

customer service as close do not get much importance

www.bizkul.com 32

Life cycle costing benefits

Differences in percentages in committed costs at initial stage of business is highlighted–The higher the initial costs, the more

critical it is for management to develop better predictions about revenues

www.bizkul.com 33

Life cycle costing benefits

Interrelationships across cost categories are highlighted–Many companies with high R&D &

product refinement costs may experience less customer service costs and vice versa. Such costs are often hidden and affect quality of product

www.bizkul.com 34

Pricing

Intuitive Rule of thumb Trial and error Discount Premium Mark up

www.bizkul.com 35

Pricing decisions

Influenced by Costs Competitors Customers Time horizon – short run or long run

decisions Strategic reasons

www.bizkul.com 36

Target Pricing Develop product Set target price Try to achieve target cost

Target cost = Competitive price – desired profit

www.bizkul.com 37

Pricing for short run Decide on relevant costs that should be

used Compute costs, direct, indirect and total Compute any special costs that need to

be incurred and savings that may be possible

Decide on pricing based on other factors such as long term impact, competition etc.

www.bizkul.com 38

Pricing for long run Important to consider long term

pricing for long term sustainability and growth of business

Initial pricing and short term pricing should keep long term pricing in mind

Image and brand of business to be considered in pricing

Costs to be understood and allocated Consistency in pricing in long term

www.bizkul.com 39

…..to trigger thinking

www.bizkul.com 40

A cup of coffee A cup of coffee costs Rs. 10 to make

HOW will you plan to price this?

……….. continued..

www.bizkul.com 41

A cup of coffee

Will you charge based on the price of coffee in similar coffee shops and restaurants?

……….. continued..

www.bizkul.com 42

A cup of coffee

Will you charge cost plus a margin?

……….. continued..

www.bizkul.com 43

A cup of coffee

OR will you think differently?

……….. continued..

www.bizkul.com 44

A cup of coffeeFor example …

You could charge differently during the rush hour

You could have special rates in non rush hours

www.bizkul.com 45

Some thoughts…

You can … if you want

Think differently about your pricing Think differently about your

negotiations for pricing and selling

Recommended