Embed Size (px)

Citation preview

Integrating Transfer Pricing Policy andActivity-Based Costing

The activity-based costing approach justifies the transfer pricesa multinational corporation uses to transfer unique companyparts or services among its divisions located in different coun-tries. This article illustrates how this approach reduces theprobability of costly tax audits and assists in obtaining an ad-vanced pricing agreement

As the global imperative propels more companies into the in-ternational marketing arena, the challenge of developing ef-fective pricing strategies becomes very complex. Indeed,pricing has been identified as one of the most significant andperplexing marketing complexities faced by multinational en-terprises (MNE; Cavusgil 1996; Weekly 1992). To deal withsuch complexities, marketers have historically relied on accu-rate accounting information to improve decision making (see,e.g., Beik and Buzby 1973; Dunne and Wolk 1977; Kirpaliniand Shapiro 1973). These decision complexities are espe-cially evident in situations in which the transfer of intangibleservices or component parts among subsidiaries is involved,because these transfers create internal revenues (Carter, Mal-oney, and Van Vranken 1998). Such revenues mean that taxauthorities will view the supplier of the service or componentpart as a seller and the receiver of such materials as a buyer,even though the transactions take place between units of thesame company. Thus, internal transfers have pricing andprofit implications that require the selling unit to determinean appropriate transfer price to charge the buying unit. Coodaccounting information is crucial for such decisions.

Determination of the "right" transfer price is influenced bymany factors. Indeed, one study (Burns 1980) identified tenfactors that have a bearing on transfer price determination.Among them were market conditions, economic conditions,competition in the foreign market, exchange and price con-trols, and U.S. and foreign income taxes. The role of taxationis especially important because the involvement of morethan one taxing authority frequently means different levels oftaxation and different taxation rules in different countries.Failure to satisfy all taxing authorities can have significantconsequences. These can include tax audits (which are ex-pensive in themselves) and substantial penalties if irregulari-ties are discovered. In some cases, the result is double

ABSTRACT

Thomas H. Stevensonand David W.E. Cabell

Submitted August 2001Accepted January 2002

©Journal of International MarketingVol. 10, No. 4, 2002, pp. 77-88ISSN 1069-031X

77

taxation; taxes are levied in the jurisdiction of both the sellerand the buyer (Fraedrich and Bateman 1996).

One potential trigger for such penalties is the tendency forsome companies to use transfer prices as a means to minimizetaxes. This is accomplished by companies pricing in such amanner that profits are higher in countries with lower tax ratesand lower in countries where tax rates are higher. For exam-ple, a company might set a low transfer price on componentsor services being sent into a low tax country so that later salesof finished goods from that country will yield higher profitsbecause of lower taxation. Conversely, a high transfer pricewould be used in a high tax country so that later sales wouldyield lower taxable profits. Such practices of some MNEs, aswell as the overall increase in transfers among internationalsubsidiaries, have resulted in an increase in governmentscrutiny and regulation of transfer pricing (Pearson andSchmidt 1991). Furthermore, complying with the diverse poli-cies established by different taxing authorities is very complex(Pearson and Schmidt 1998). Therefore, companies must care-fully consider their approaches to determining and reportingtransfer prices.

We review the typical approaches to transfer price determina-tion and demonstrate how they may be problematic when trans-fer pricing involves intracompany movement of uniquecompany services or component parts. We then show how theapplication of activity-based costing (ABC) can be useful in re-solving these issues. The overall objective of this article is to of-fer insights to companies seeking to avoid running afoul oftaxing authorities without losing sight of operational objectives.

^^^^^^^^^^^^^^^^^^^^^^^^'^^^ Prior to 1994, there were essentially four approaches in whichTRANSFER PRICING transfer prices could be determined to meet the Basic Arms

APPROACHES Length standard, the international standard for transfer pricedetermination accepted by tax authorities around the world.The first approach was the comparable/uncontrollablemethod, which required the seller to compare its transfer priceto that of an independent seller selling a similar good to an in-dependent buyer. The second approach was the resale price orgross margin method, which required the seller to compare itsgross profit margin to that attained by independent sellers sell-ing to independent buyers (i.e., comparable uncontrolledtransactions). The third approach was the cost-plus or grossmarkup method, which required the seller to add a gross profitto product costs that was comparable to that earned by compa-nies performing similar functions. If none of these three meth-ods applied, an alternate method could be used. Multinationalenterprises were required to apply these approaches in a hier-archical fashion; that is, the comparable/uncontrollable resalemethod was to be used unless the MNE rejected it as unsuit-able for its circumstances. The MNE could then try the resale

78 Thomas H. Stevenson and David W.E. Cabell

price method; if it was also unsuitable, the cost-plus methodcould be tried. If none of these approaches suited the uniquerequirements of the MNE, another approach could be used.However, alternate approaches were rarely used because of thepotential for closer scrutiny by taxing authorities.

These approaches were augmented in 1994 by two additionaltransfer approaches: the comparable profits method and theprofit-split method. The comparable profits method requiredthe seller to compare its profits to those of similar MNEs. Theprofit-split method allocated profits between business unitson the basis of the functions performed, assets used, andrisks assumed by each unit. The profit-split method thencompared relative profits with those of uncontrolled MNEsin similar situations.

In addition to offering two new transfer pricing options, the1994 regulations dropped the strict hierarchical approach toselection of a transfer pricing procedure and instead adopteda "best-method" rule. This rule allowed an MNE to select thetransfer pricing procedure that provided the most accurateprice for its unique situation. Thus, an MNE could chooseamong a total of six transfer pricing options (for a summaryof transfer pricing methods, see the Appendix).

Nevertheless, this flexibility was not a panacea because thecommon theme in each of these pricing methods is a compari-son to similar companies supplying similar products to inde-pendent buyers. However, in the case of companies transferringbusiness services or component parts, it is frequently difficult toidentify similar products and services in unrelated companies.This is especially true in the case of components, because thepolicy of having each subsidiary specialize in its most efficientactivity means that many services and components are uniqueto that subsidiary. To meet the taxing authorities' rule that pricesof products and services be comparable requires that labor, ma-terials, overhead, and profits associated with a given product orservice be compared with those provided by independent sup-pliers. Such comparisons are problematic for MNEs becauseeven if comparable suppliers exist for "work in progress" itemsor services, it is unlikely that costs would be comparable be-cause of different methods or rates of depreciation, labor andmaterial costs, labor/automation mixes, and overhead bases.Furthermore, even if information on material and labor costswas obtainable on a comparable basis, data on overhead and in-direct costs would be extremely difficult to obtain and evenmore difficult to compare across components or services. Thus,the existence of a comparable situation to meet taxing require-ments is problematic.

Nevertheless, the replacement of the strict hierarchical ap-proach with the more flexible best method rule enabled an

Integrating Transfer Pricing Policy and Activity-Based Costing 79

MNE to select the method that best met the unique needs ofthe seller, provided that the selection was made in good faith,was properly documented, and generated a reasonable result.Moreover, the best method for many producers is the cost-plusmethod because it is already widely used for determiningtransfer prices in industry (i.e., research has shown it to be apreferred pricing approach; Burns 1980; Kim, Swinnerton,and Ulferts 1997). Yet even as the cost-plus method is beingfrequently used in transfer pricing, the advent of ABC ischanging the way that costs are allocated in industry. Thiscould have implications in international transfer pricing be-cause using the cost-plus method in combination with ABC of-fers two potential advantages to MNEs. The first advantage isto provide a rigorous rationale for cost allocation, and the sec-ond is to generate the specifics needed for an advanced pricingagreement (APA) with taxing authorities (an APA is a negoti-ated agreement between a company and a taxing authority thatdetermines a transfer price that is acceptable to all parties, us-ing cost and profit information unique to the particular tax-payer). The purpose of the APA is to avoid time consumingand costly tax audits through the careful documentation ofcosts, which can be provided by ABC.

= = = = ^ ^ ^ ^ = = ^ ^ ^ ^ ^ = Pioneered by Cooper and Kaplan (1988), ABC is a differentABC w^y of viewing cost allocation. It grew out of the realization

that traditional accounting methods were inadequate in pro-viding comprehensive cost information for decision makingin today's business environment. This is because the full costof a manufactured part or service includes direct labor, mate-rial, variable overhead, and fixed costs. Direct labor and ma-terial are normally observed, measured, and maintained asstandards. The overhead costs are reported by responsibilitycenters, such as departments, plants, or subsidiaries. The dif-ficult decision is how to allocate overhead costs to productsor services.

In the traditional approach to cost allocation, the typicalbusiness uses a two-step system for absorbing costs. Costs areaccumulated in a pool and then allocated to specific prod-ucts or services by means of a companywide base such as di-rect hours used in producing the product or service (Collinsand Werner 1990). Other allocation bases are machine hoursor direct labor cost, for example. The traditional use of directlabor hours as an allocation basis traces back to the mid-1920s, when cost accounting systems were being developed.At that time, labor was a major expense, generating 80% ofall costs. Thus, it was a target of management attention. In re-cent years, however, direct labor accounts for no more than8% to 12% of all costs in advanced manufacturing industries(Smith 1989). Indeed, Kelly (1991, p. 43) notes that hands-onlabor costs in high-technology industries are "closer to 5%[while] overhead has ballooned to 55% or more."

80 Thomas H. Stevenson and David W.E. Cabell

Activity-based costing responds to the changes in the way costsare incurred in business today by recognizing "that virtually allactivities taking place within a firm support the production,marketing and delivery of goods and services" (Goebel, Mar-shall, and Locander 1998, p. 50). By using ABC, firms can iden-tify systematic cause and effect linkages among products,markets, and costs before resorting to across-the-board alloca-tions. These linkages, called "cost drivers," are activities thatcause costs to be "driven" up or down. These costs occvir whenan activity is performed, so a cost driver is a way of allocating acost to a particular activity. For example, in marketing a costdriver would be the number of shipments made to a particularregion, number of orders entered, or sales calls made in a re-gion; these drivers are used to allocate costs. In using ABC,firms accumulate costs but then allocate them to products, ser-vices, or regions by the appropriate drivers. For example, a re-gion requiring 15% of sales force time might be charged 15% oftotal sales overhead; a region using 20% of order entry timewould be charged 20% of order entry overhead.

Allocating costs in this manner provides an accurate andmore complete picture of the costs and profitability of prod-ucts or services. As a result, the number of companies usingABC continues to increase. However, ABC does have limita-tions. Some companies find ABC difficult to implement be-cause it requires changes in the way costs are trackedthroughout the organization. It also requires the education ofemployees at all levels about the purpose of and reasons forusing ABC. These changes can be costly and time consumingto implement. Furthermore, strong employee resistance as aresult of organizational and functional changes required byABC is the biggest identified obstacle to ABC implementation(Ness and Cucuzza 1995). Yet it is apparent that these obsta-cles can be overcome because there has been rapid diffusionof ABC throughout industry. This was demonstrated by theresults of a recent sin-vey by the Institute of Management Ac-countants in which 49% of responding firms had adoptedABC, up from 41% the previous year (Krumwiede 1998).

The advantage of the ABC method is its focus on the alloca- ^ = ^ = ^ ^ = ^ ^ = ^ : ^ ^ = ^ ^ = ^ ^tion of overhead costs. These costs can be substantial when ABC AND TRANSFER PRICINGcompanies transfer components or services between differenttaxing jurisdictions. Examples of such costs are machineoverhead; set-up costs; packing/transportation; research anddevelopment (R&D); documentation; site services; warehous-ing; travel; and sales, advertising, and other costs related tomarketing of the finished product. In contrast to the ABC ap-proach, the traditional absorption method reports these ac-tivities to responsibility centers and allocates them toproducts or territories by means of a base of machine hoursor direct labor, for example. This approach tends to overstateor understate costs associated with manufacturing compo-

Integrating Transfer Pricing Policy and Activity-Based Costing 81

nent parts or services intended for transfer among companyunits and could be viewed as arbitrary by taxing authorities.For example, packing or transportation requirements couldvary among regions, and their costs could be overstated insome regions and understated in others. However, using ABCclearly allocates costs to the most appropriate cost driver andremoves the arbitrariness. Moreover, using ABC to associateoverhead costs with a particular product, service, or regiongives companies faced with transfer pricing issues some ofthe needed detail to support APAs between companies andtaxing authorities regarding transfer pricing methodologies.As Fallon (1997) notes, the advantage of APAs is that they ad-dress transfer pricing issues before administrative examinationsor litigation become necessary. The result, in cost/benefitterms, is potentially so significant that countries such as Aus-tralia, Belgium, Canada, France, Germany, Japan, Korea,Spain, the United Kingdom, the United States, and others arecompleting APAs (Durst 1998).

This is not to say that APAs can eliminate all transfer pricingdisagreements and disputes, but the costs, uncertainties, andtime involved can be greatly reduced. The following sectiondescribes how the detail needed for an APA is generatedthrough ABC and compares ABC to traditional costing.

^^==^^^^=^^^^==^^^ Tables 1-4 provide a theoretical example that shows howTRANSFER PRICING USING ABC affects the allocation of costs and the potential tax lia-

ABC: A N ILLUSTRATION bility of a company involved in transfer pricing decisions.For readers interested in a more technical description ofABC implementation, the literature is replete with exam-ples (see Coburn, Crove, and Cook 1997; Krupnicki andTyson 1997).

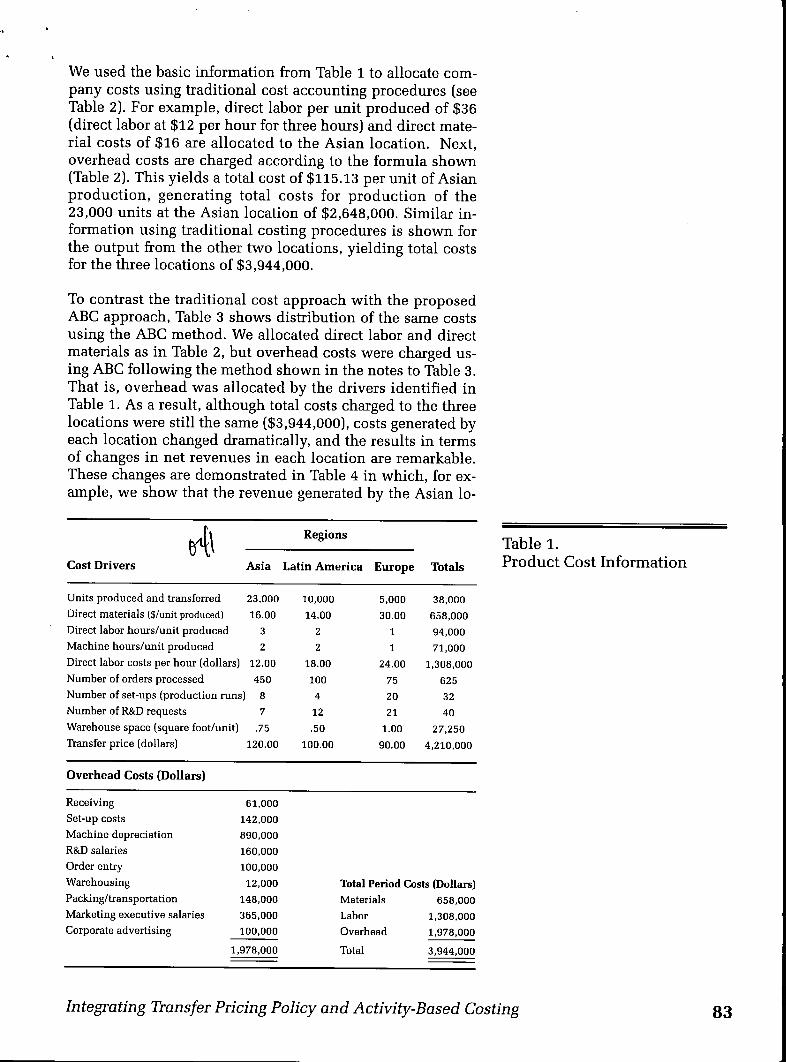

Table 1 provides basic manufacturing (e.g., labor hours, ma-chine hours, direct materials) and marketing (e.g., R&D re-quirements, order entry, executive salary, corporateadvertising) costs that are associated with three different man-ufacturing locations: one in Asia, one in Latin America, andone in Europe. Direct costs, transfer prices, cost drivers, andoverhead costs are shown for each location. The total costs forall three locations are also shown. For example. Table 1 showsthat 23,000 units were produced in Asia at a direct materialcost of $16 per unit. This generated $368,000 of material costsfor Asia. Similar calculations for Latin America and Europeyield total company material costs of $658,000. Likewise, pro-duction and transfer of 23,000 units in Asia required two ma-chine hours per unit, or a total of 46,000 machine hours.Repeating this calculation for Latin America and Europeyielded 71,000 machine hours required to produce total com-pany output of 38,000 units. Totals shown in Table 1 weregenerated in a similar fashion, and overhead costs and totalperiod costs are also shown in the table.

82 Thomas H. Stevenson and David W.E. Cabell

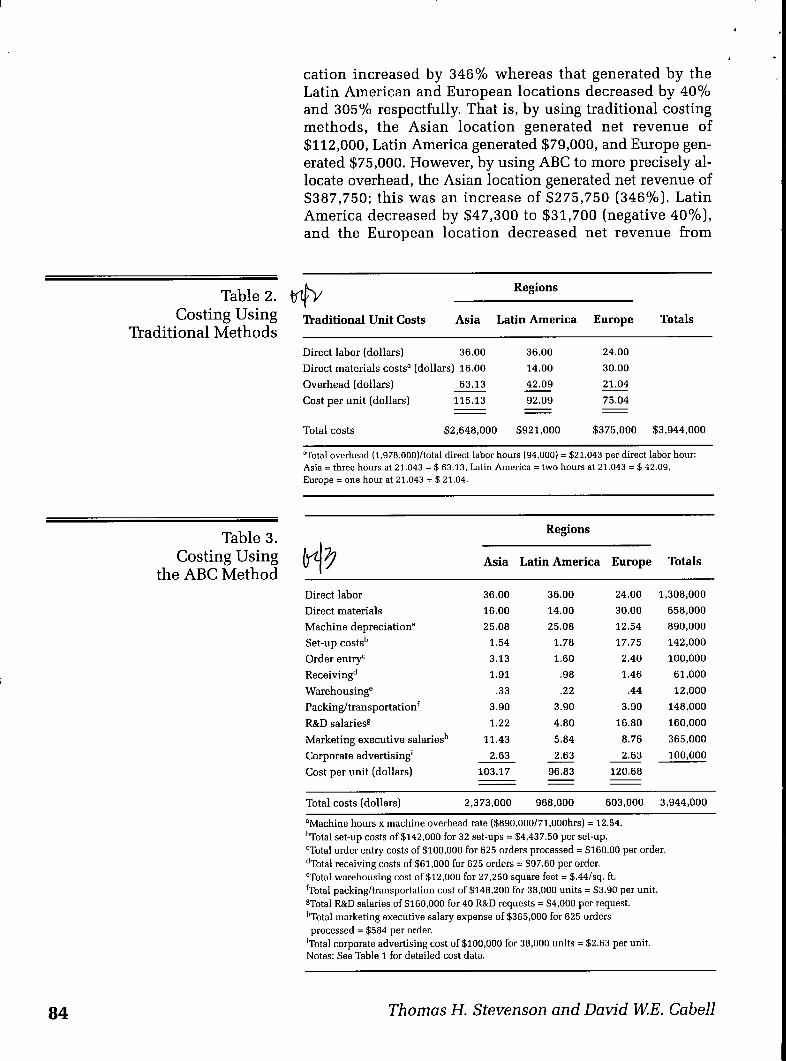

We used the basic information from Table 1 to allocate com-pany costs using traditional cost accounting procedures (seeTable 2). For example, direct labor per unit produced of $36(direct labor at $12 per hour for three hours) and direct mate-rial costs of $16 are allocated to the Asian location. Next,overhead costs are charged according to the formula shown(Table 2). This yields a total cost of $115.13 per unit of Asianproduction, generating total costs for production of the23,000 units at the Asian location of $2,648,000. Similar in-formation using traditional costing procedures is shown forthe output from the other two locations, yielding total costsfor the three locations of $3,944,000.

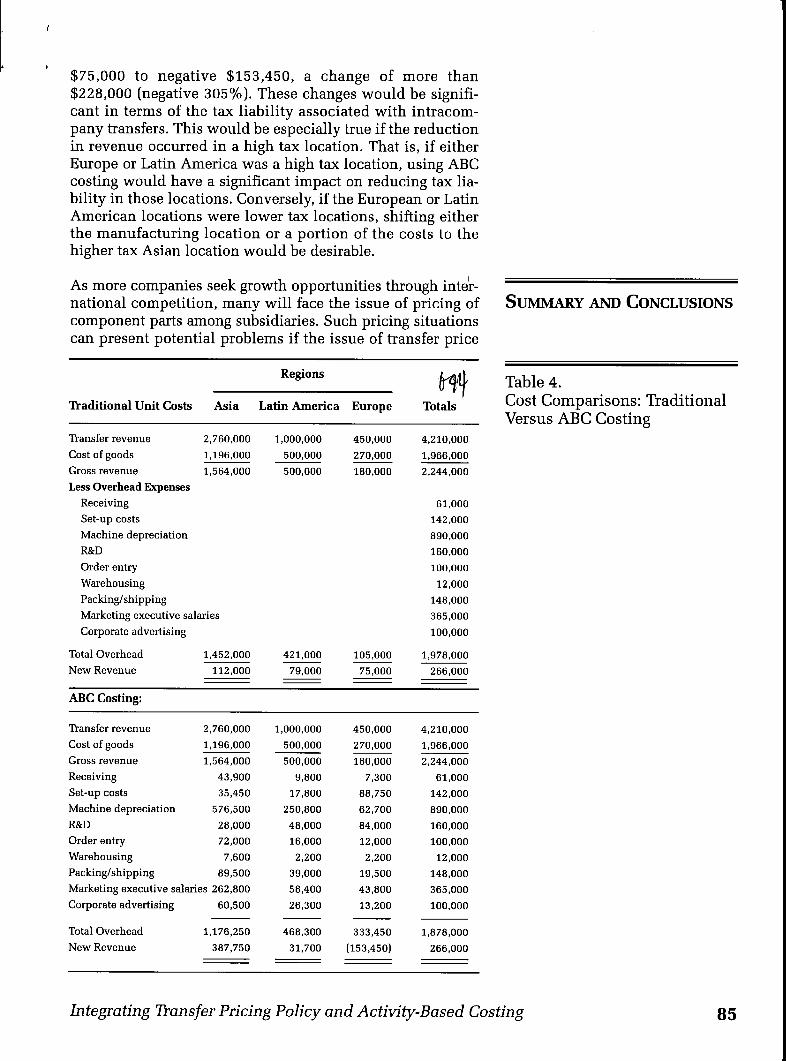

To contrast the traditional cost approach with the proposedABC approach, Table 3 shows distribution of the same costsusing the ABC method. We allocated direct labor and directmaterials as in Table 2, but overhead costs were charged us-ing ABC following the method shown in the notes to Table 3.That is, overhead was allocated by the drivers identified inTable 1. As a result, although total costs charged to the threelocations were still the same ($3,944,000), costs generated byeach location changed dramatically, and the results in termsof changes in net revenues in each location are remarkable.These changes are demonstrated in Table 4 in which, for ex-ample, we show that the revenue generated by the Asian lo-

Cost Drivers

Units produced and transferredDirect materials [$/unit produced)Direct labor hours/unit producedMachine hours/unit producedDirect labor costs per hour (dollars)Number of orders processed

Asia

23,00016.00

3

2

1 12.00450

Number of set-ups (production runs) 8Number of R&D requestsWarehouse space (square foot/unit)TYansfer price (dollars)

Overhead Costs (Dollars)

ReceivingSet-up costsMachine depreciationR&D salariesOrder entryWarehousingPacking/transportationMarketing executive salariesCorporate advertising

1,

7

.75

120.00

61,000142,000890,000160,000100,00012,000

148,000365,000100,000

978,000

Regions

Latin America Europe

10,00014.00

2

2

18.00100

4

12

.50

100.00

5,00030.00

1

1

24.0075

20

21

1.0090.00

Totals

38,000658,00094,00071,000

1,308,000625

32

40

27,2504,210,000

Total Period Costs (Dollars)MaterialsLaborOverhead

Total

658,0001,308,0001,978,000

3,944,000

Table 1.Product Cost Information

Integrating Transfer Pricing Policy and Activity-Based Costing 83

cation increased by 346% whereas that generated by theLatin American and European locations decreased by 40%and 305% respectfully. That is, by using traditional costingmethods, the Asian location generated net revenue of$112,000, Latin America generated $79,000, and Europe gen-erated $75,000. However, by using ABC to more precisely al-locate overhead, the Asian location generated net revenue of$387,750; this was an increase of $275,750 (346%). LatinAmerica decreased by $47,300 to $31,700 (negative 40%),and the European location decreased net revenue from

Table 2.Costing Using

Traditional Methods

Table 3.Costing Using

the ABC Method

Traditional Unit Costs

Direct labor (dollars)Direct materials costs" (dollars)Overhead (dollars)Cost per unit (dollars)

Total costs $2

Regions

Asia Latin America

36.001 16.00

63.13115.13

!,648,000

36.0014.0042.0992.09

$921,000

"Total overhead (l,978,000)/total direct labor hours (94,000) = $21Asia = three hours at 21.043 = $ 63.Europe = one hour at 21.043 = $ 21

Direct laborDirect materialsMachine depreciation"Set-up costs'"Order entry"̂Receiving''Warehousing"Packing/transportation'R&D salaries?Marketing executive salaries'"Corporate advertising"Cost per unit (dollars)

Total costs (dollars)

Europe

24.0030.0021.0475.04

$375,000

Totals

$3,944,000

.043 per direct labor hour:,13, Latin America = two hours at 21.043 = $ 42.09,.04.

Asia

36.0016.0025.08

1.543.131.91

.33

3.901.22

11.432.63

103.17

2,373,000

Regions

Latin America Europe

36.0014.0025.08

1.781.60

.98

.22

3.904.805.842.63

96.83

968,000

24.0030.0012.5417.752.401.46

.44

3.9016.808.762.63

120.68

603,000

Totals

1,308,000658,000890,000142,000100,00061,00012,000

148,000160,000365,000100,000

3,944,000

"Machine hours x machine overhead rate ($890,000/71,000hrs) = 12.54.••Total set-up costs of $142,000 for 32 set-ups = $4,437.50 per set-up.•̂ Total order entry costs of $100,000 for 625 orders processed = $160.00 per order.''Total receiving costs of $61,000 for 625 orders = $97.60 per order."Total warehousing cost of $12,000 for 27,250 square feet = $.44/sq. ft.•Total packing/transportation cost of $148,200 for 38,000 units = $3.90 per unit.STotal R&D salaries of $160,000 for 40 R&D requests = $4,000 per request.•"Total marketing executive salary expense of $365,000 for 625 ordersprocessed = $584 per order.

'Total corporate advertising cost of $100,000 for 38,000 units = $2.63 per unit.Notes: See Table 1 for detailed cost data.

84 Thomas H. Stevenson and David W.E. Cahell

$75,000 to negative $153,450, a change of more than$228,000 (negative 305%). These changes would be signifi-cant in terms of the tax liability associated with intracom-pany transfers. This would be especially true if the reductionin revenue occurred in a high tax location. That is, if eitherEvirope or Latin America was a high tax location, using ABCcosting would have a significant impact on reducing tax lia-bility in those locations. Conversely, if the European or LatinAmerican locations were lower tax locations, shifting eitherthe manufacturing location or a portion of the costs to thehigher tax Asian location would be desirable.

As more companies seek growth opportunities through inter-national competition, many will face the issue of pricing ofcomponent parts among subsidiaries. Such pricing situationscan present potential problems if the issue of transfer price

Traditional Unit Costs

TVansfer revenueCost of goodsGross revenueLess Overhead Expenses

ReceivingSet-up costsMachine depreciationR&DOrder entryWarehousingPacking/shipping

Asia

2,760,0001,196,0001,564,000

Marketing executive salariesCorporate advertising

Total OverheadNew Revenue

ABC Costing:

Transfer revenueCost of goodsGross revenueReceivingSet-up costsMachine depreciationR&DOrder entryWarehousingPacking/shipping

1,452,000112,000

2,760,0001,196,0001,564,000

43,90035,450

576,50028,00072,0007,600

89,500Marketing executive salaries 262,800Corporate advertising

Total OverheadNew Revenue

60,500

1,176,250387,750

Regions

Latin America

1,000,000500,000500,000

421,00079,000

1,000,000500,000500,000

9,80017,800

250,80048,00016,0002,200

39,00058,40026,300

468,30031,700

Europe

450,000270,000180,000

105,00075,000

450,000270,000180,000

7,30088,75062,70084,00012,0002,200

19,50043,80013,200

333,450(153,450)

1Totals

4,210,0001,966,0002,244,000

61,000142,000890,000160,000100,00012,000

148,000365,000100,000

1,978,000266,000

4,210,0001,966,0002,244,000

61,000142,000890,000160,000100,000

12,000148,000365,000100,000

1,878,000266,000

SUMMARY AND CONCLUSIONS

Table 4.Cost Comparisons: TraditionalVersus ABC Costing

Integrating Transfer Pricing Policy and Activity-Based Costing 85

APPENDIX.TRANSFER

PRICING METHODS

taxation is not addressed properly. Although there is no pric-ing approach that is without possible negative tax conse-quences and none that will work for all companies and in allsituations, many companies are seeking advanced pricingagreements to reduce the potential for tax problems going for-ward. Furthermore, many companies view cost-plus pricingas an effective way to provide necessary detail in a tax author-ity acceptable framework. However, ABC, a procedure thatmore accurately reflects tbe way tbat costs are generated incontemporary industry and reduces mucb of tbe arbitrarinessassociated witb tbe traditional approacb to costing, is increas-ingly supplanting traditional cost-plus pricing.

Tbis article contrasts tbe traditional and ABC approacbes andsbows bow tbe approacbes can significantly affect transferpricing tax liability. It also demonstrates tbe detailed informa-tion generated by ABC tbat could provide tbe documentationneeded for an APA, wbicb would significantly reduce tbe riskof a costly tax audit. Tbis approacb makes it possible to justifytbe overbead costs associated witb tbe transfer of unique com-ponents and services among tbe divisions of an MNE. Furtber-more, it provides tbe rationale for differences in transfer pricestbat occur among divisions operating in different countries.Tbis flexibility allows tbe MNE to adjust costs and prices tocope witb country-specific conditions.

Wbetber ABC or traditional costing is tbe most appropriatemetbod for a particular company depends on many factors,only one of wbicb is potential for negative tax consequences.Fvirtber researcb tbat examines tbe reiationsbip between ABCand transfer pricing would be useful. For example, empiricalstudies of MNEs using ABC in conjimction witb APAs could beundertaken. Case studies could be carried out to explore tbe ef-fectiveness of ABC in reducing tax audits. Otber studies couldexamine tbe impact of ABC beyond transfer pricing, for exam-ple, in relation to otber issues in international marketing, sucbas relative profitability of product lines or alternative marketingstrategies. Nevertbeless, for tbose concerned witb transfer pric-ing issues, tbis article provides a glimpse of tbe potential ofABC in tbe development of an effective transfer pricing mecba-nism, one tbat lowers tbe risk of a transfer price audit and givestbe MNE tbe flexibility to adjust costs to compete successfullyin tbe global market.

1. Comparable uncontrolled price metbod evaluates wbetbertbe amount cbarged in a controlled transaction is arm'slengtb by reference to tbe amount cbarged in a comparableuncontrolled transaction.

2. Resale price metbod evaluates wbetber tbe amount cbargedin a controlled transaction is arm's lengtb by reference totbe gross profit margin realized in comparable uncontrolled

86 Thomas H. Stevenson and David W.E. Cabell

transactions. The resale price method measures the value offunctions performed and is ordinarily used in cases involv-ing the purchase and resale of tangible property in whichthe reseller has not added substantial value to the tangiblegoods by altering tbem before resale.

3. Cash plus metbod evaluates wbetber tbe amount cbargedin a controlled transaction is arm's lengtb by reference totbe gross profit margin realized in comparable uncon-trolled transactions. Tbe cost-plus metbod is ordinarilyused in cases involving tbe manufacture, assembly, orotber production of goods tbat are sold to related parties.

4. Comparable profits metbod evaluates wbetber tbe amountcbarged in a controlled transaction is arm's lengtb on tbebasis of objective measures of profitability derived fromuncontrolled taxpayers tbat engage in similar business ac-tivities under similar circumstances.

5. Profit split metbod evaluates wbetber tbe allocation of tbecombined operating profit or loss attributable to one ormore controlled transactions is arm's lengtb by referenceto tbe relative value of eacb controlled taxpayer's contri-bution to tbat combined operating profit or loss.

6. Unspecified metbods may be used to evaluate wbetber tbeamount cbarged in a controlled transaction is arm's lengtb.An unspecified metbod sbould provide information onprices or profits tbat tbe controlled taxpayer could baverealized by cboosing a realistic alternative to tbe con-trolled transaction.

THE AUTHORS

Thomas H. Stevenson isCullen Professor of Marketing,University of North Carolinaat Charlotte.

David W.E. Cabell is AssistantProfessor of Management,McNeese State University.

Source: Excerpted from Pugh (2000).

Beik, Leland L. and Stephen L. Buzby (1973), "Profitability Analy-sis by Market Segments," Journal of Marketing, 37 (3), 48-53.

Burns, Jane O. (1980), "Transfer Pricing Decisions in U.S. Multina-tional Corporations," fournal of International Business Studies,11 (2), 23-39.

Carter, William K., David M. Maloney, and M. H. Van Vranken(1998), "The Problems of Transfer Pricing," Journal of Accoun-tancy, 186 (1), 37-40.

Cavusgil, S. Tamer (1996), "Pricing for Global Markets," The Co-lumbia Journal of World Business, 31 (4), 66-78.

Coburn, Steve, Hugh Grove, and Tom Cook (1997), "How ABC WasUsed in Capital Budgeting," Management Accounting, 78 (11),38-46.

Collins, Frank and Michael L. Werner (1990), "Improving Perfor-mance with Cost Drivers," Journal of Accountancy, 169 (6),131-34.

REFERENCES

Integrating Transfer Pricing Policy and Activity-Based Costing 87

Cooper, Robin and Robert S. Kaplan (1988], "Measure Costs Right:Make the Right Decisions," Harvard Business Review, 66 (5),96-103.

Dunne, Patricia M. and Harry L. Wolk (1977), "Marketing CostAnalysis: A Modularized Contribution Approach," Journal ofMarketing, 41 (3), 83-94.

Durst, Michael C. (1998), "Transfer Pricing Documentation andAPAs in the Era of Worldwide Transfer Pricing Scrutiny—SomePractice Points," Tax Management International Journal, 27 (3),131-35.

Fallon, Geralyn M. (1997), "Advance Pricing Agreements," Taxes,25 (6), 304-28.

Fraedrich, John P. and Connie R. Bateman (1996), "Transfer PricingBy Multinational Marketers: Risky Business," BusinessHorizons, 39 (1), 17-22.

Goebel, Daniel J., Greg W. Marshall, and William B. Locander(-1998), "Activity-Based Costing: Accounting for a Marketing Ori-entation," Industrial Marketing Management, 27 (6), 497-510.

Kelly, Kevin (1991), "A Bean-Counter's Best Friend," Business-Week, (October 25), 42-43.

Kim, Suk H., Eugene Swinnerton, and Gregory Ulferts (1997),"1994 Final Transfer Pricing Regulations of the United States,"Multinational Business Review, 5 (1), 17-25.

Kirpalani, V. H. and Stanley S. Shapiro (1973), "Financial Dimen-sions of Marketing Management," Journal of Marketing, 37 (3),1-18.

Krumwiede, Kip R. (1998), "ABC: Why It Is Tried and How It Suc-ceeds," Management Accounting, 79 (10), 32-38.

Krupnicki, Michael and Thomas Tyson (1997), "Using ABC to De-termine the Cost of Servicing Customers," Management Ac-counting, 79 (6), 40-46.

Ness, Joseph A. and Thomas G. Gucuzza (1995), "Tapping the FullPotential of ABG," Harvard Business Review, 73 (4), 130-38.

Pearson, Thomas G. and Dennis R. Schmidt (1991), "Information Re-porting, Record Maintenance, and Transfer Pricing Audits of For-eign and Foreign-Owned Gorporations," Taxes, 69 (3), 172-80.

and (1998), "Transfer Pricing Tax Concerns forGlobal Financial Gompanies," Taxes, 76 (7), 23-33.

Pugh, Richard G., ed. (2000), International Income Taxation.Ghicago: GGH Inc., 1155-63.

Smith, Roger B. (1989), "Gompetitiveness in the '90s," Manage-ment Accounting, 71 (3), 24-29.

Weekly, James K. (1992), "Pricing in Foreign Markets: Pitfalls andOpportunities," Industrial Marketing Management, 21 (2),173-79.

88 Thomas H. Stevenson and David W.E. Cahell