Practical Lessons from 20 Years of Bubble Experiments

Overview of the Experimental Environment

The basic experimental set-up has the following features 15 period asset Dividend uncertainty Initial cash and shares Double Auction or Call market trading

mechanism Trader experience

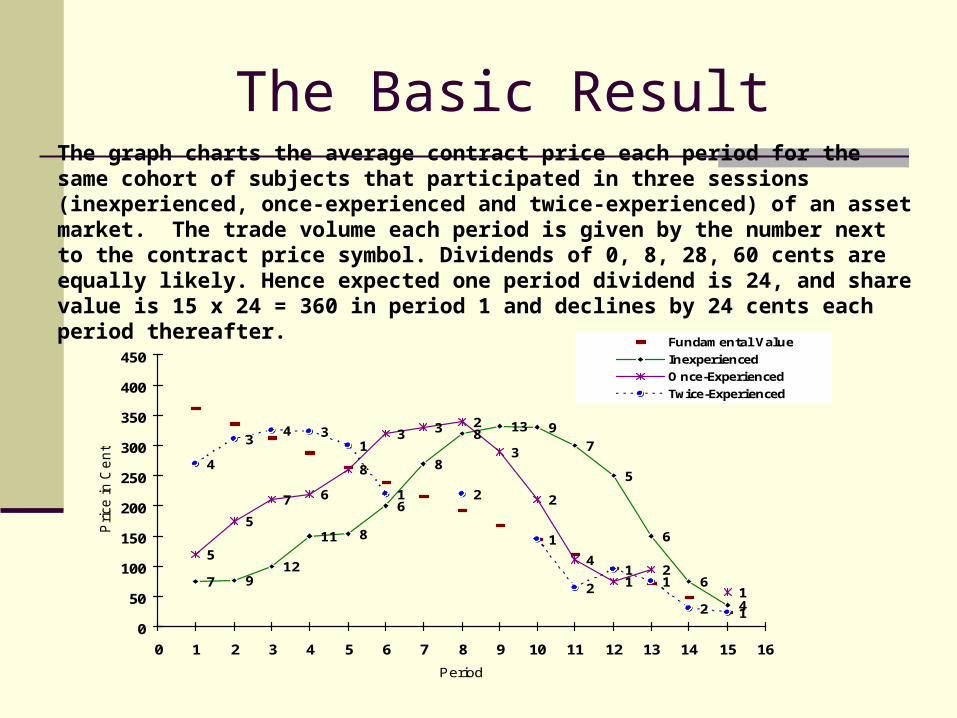

The Basic ResultThe graph charts the average contract price each period for the same cohort of subjects that participated in three sessions (inexperienced, once-experienced and twice-experienced) of an asset market. The trade volume each period is given by the number next to the contract price symbol. Dividends of 0, 8, 28, 60 cents are equally likely. Hence expected one period dividend is 24, and share value is 15 x 24 = 360 in period 1 and declines by 24 cents each period thereafter.

6

8

813 9

7

5

6

6

4

7 912

11 8

2

11

4

2

3

233

8

67

5

5

4

34 3

1

1 2

1

2

11

2 10

50

100

150

200

250

300

350

400

450

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

Period

Pri

ce

in

Ce

nts

Fundamental Value

Inexperienced

O nce-Experienced

Twice-Experienced

What Might be Causing This?

The subject pool is not representative

Period

Pric

e i

n C

en

ts

0

50

100

150

200

250

300

350

400

450

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

8

8

7

2

3

7

3

4

6

25

8

138

9

Figure 6. Mean Contract Price and Volume, Arizona Executives

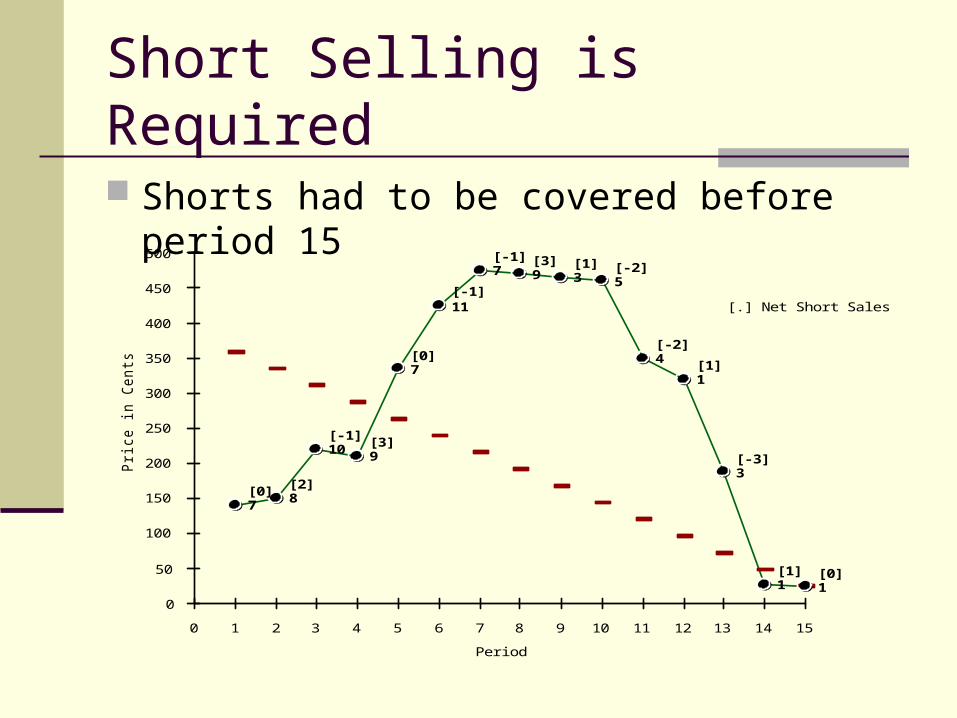

Short Selling is Required

Shorts had to be covered before period 15

Period

Pri

ce

in

Ce

nts

0

50

100

150

200

250

300

350

400

450

500

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

11

7 9 3 5

4

1

3

1 1

7 8

10 9

7

[0] [2]

[-1] [3]

[0]

[-1]

[-1] [3] [1] [-2]

[-2]

[1]

[-3]

[1] [0]

[.] Net Short Sales

Insiders Will Take Hold

Experienced traders – grad students

Period

Pri

ce

in

Ce

nts

0

50

100

150

200

250

300

350

400

450

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

23

3 33 2

2 4

4

62

3

6 2

[4][0]

[-1]

[-4] [-1] [-1][-1]

[0] [-2][0] [-1]

[-1] [-1]

[1]

[.] Net Purchases byInsiders

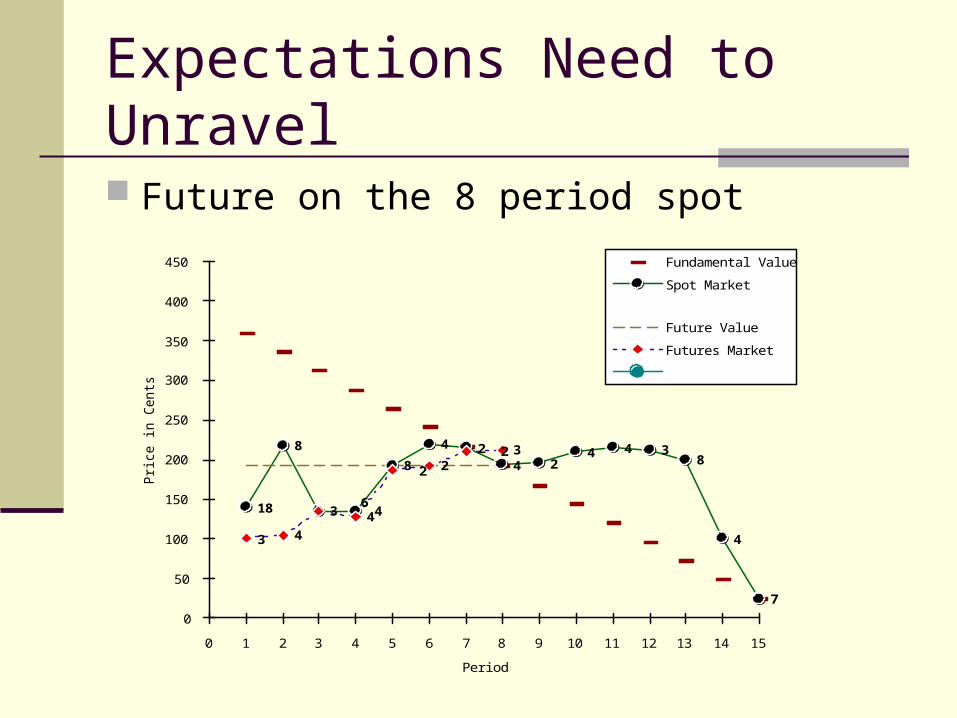

Expectations Need to Unravel

Future on the 8 period spot

Period

Pri

ce

in

Ce

nts

0

50

100

150

200

250

300

350

400

450

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

4 24 2

4 4 38

4

7

18

8

6 4

8 2

3 44

2 23

3

Fundamental Value

Spot Market

Future Value

Futures Market

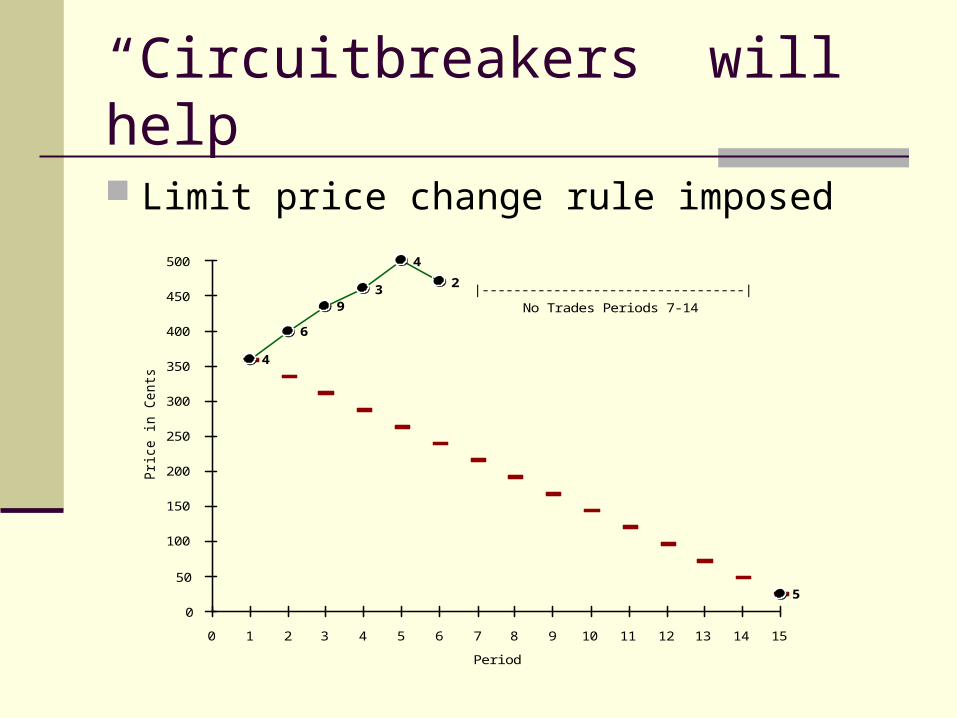

“Circuitbreakers” will help

Limit price change rule imposed

Period

Pri

ce

in

Ce

nts

0

50

100

150

200

250

300

350

400

450

500

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

2

5

4

6

93

4

|---------------------------------|No Trades Periods 7-14

Understanding Expectations Formation What generates the bubbles?

Home grown expectations

Forecasting abilities Forecasts lag behind significant changes in the trend Forecasts miss turning points Prices converge faster than forecasts Past market experience has a strong effect on

forecasts

1111 )( ttttt OBPP

Momentum Trading

Trade is influenced by price changes. Positive changes brings in more buy orders

and pushes prices up This continues until the momentum traders

become cash constrained and then fundamentals push prices down

Momentum traders then sell-off causing the violent crash

Implications from Momentum

At the initial throws of price increase, the further price is from fundamentals the larger the bubble will be

Cash to Asset Value is crucial to the bubble size and path The higher the cash infusion the bigger the

bubble

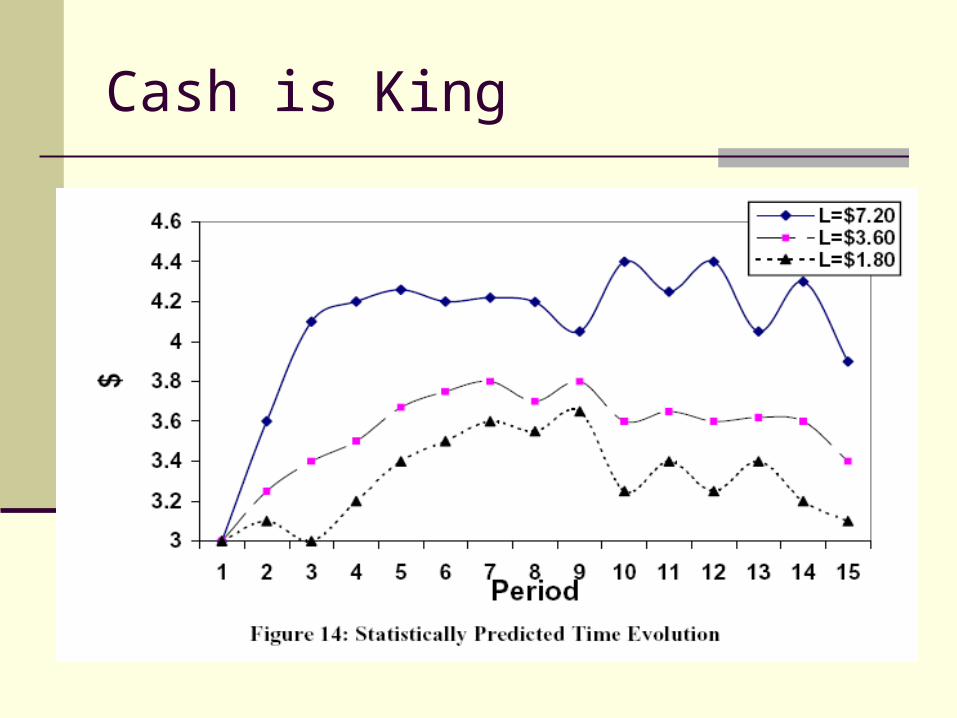

Cash is King

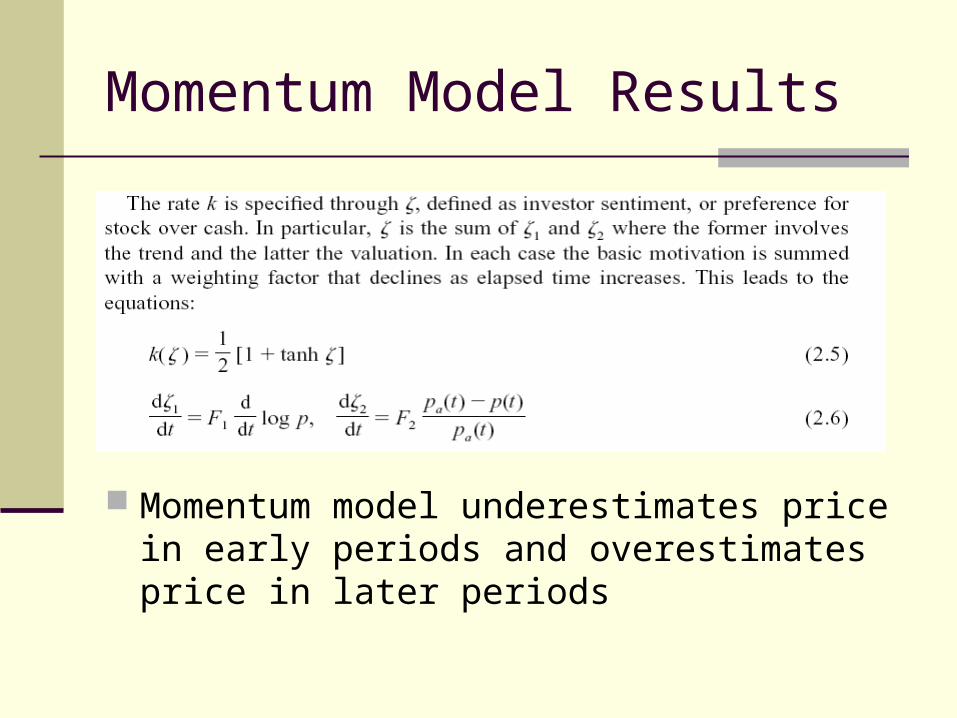

Momentum Model Results

Momentum model underestimates price in early periods and overestimates price in later periods

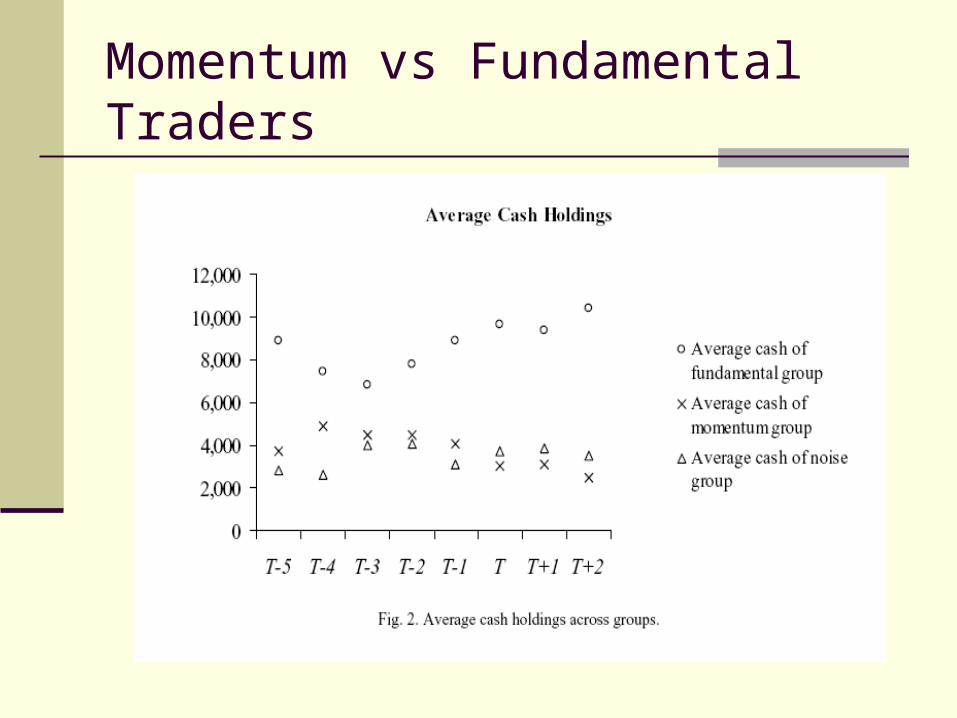

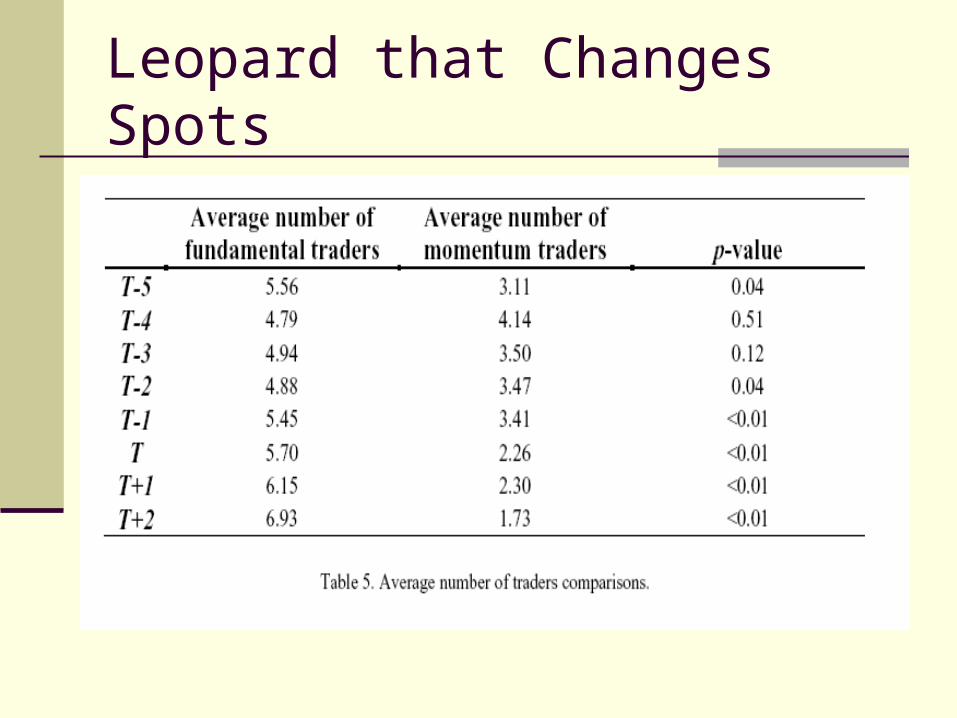

Momentum vs Fundamental Traders

Leopard that Changes Spots

Who Forecasts Better?

ARIMA Random Walk Random Walk and Pure Momentum combined

Momentum Recalculate F1 and F2 based on past and

current data Excess Bids

Bids minus Asks Model Humans

Predictors Battle Royal

For one-period ahead predictions Excess Bids wins, followed by humans. Momentum and ARIMA (1,1,1) are similar in 1-

period accuracy For two-period ahead predictions momentum

model is the most accurate All other models fail in longer horizon

prediction

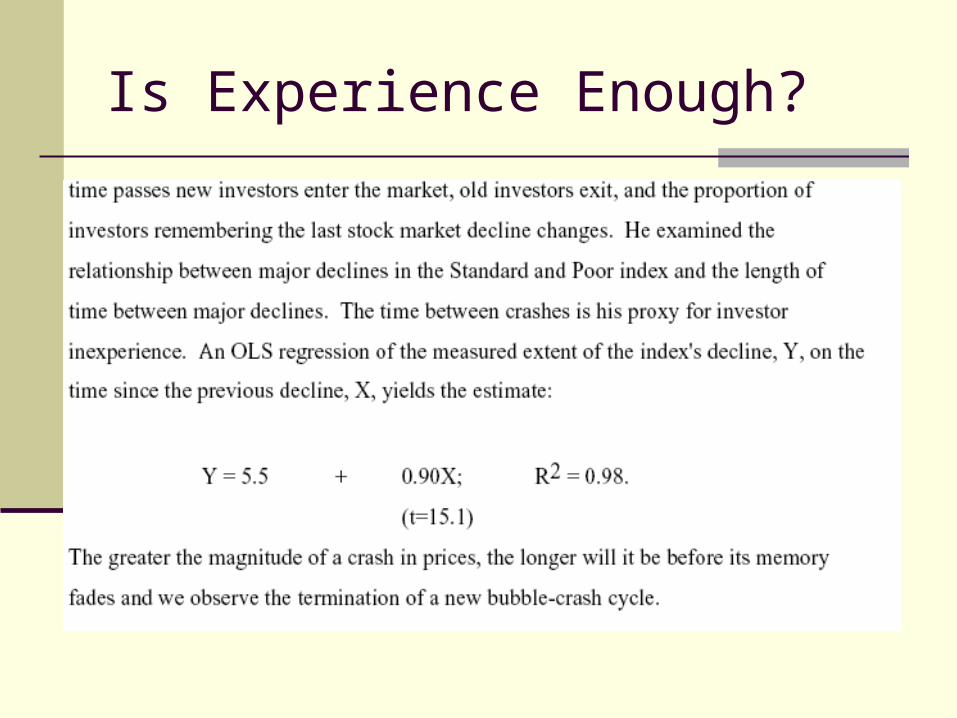

Is Experience Enough?

What Might Cause a Bubble to Rekindle? Great stock market booms as driven by

waves of new technology such environments introduce new sources of

unpredictable yield uncertainty parallel with this development we see much

new liquidity attracted into equity investment Can structural changes in the environment

reignite what was a converging market

Baseline vs Rekindle Environments

Dividends {0,8,28,60}

Initial Portfolios Average Portfolio is

4 shares and 720 cents in cash

Twice Experienced Same cohort

Dividends {0,1,8,28,98}

Initial Portfolios Average Portfolio is

2 shares and 1530 cents in cash

Twice Experienced Mixed traders

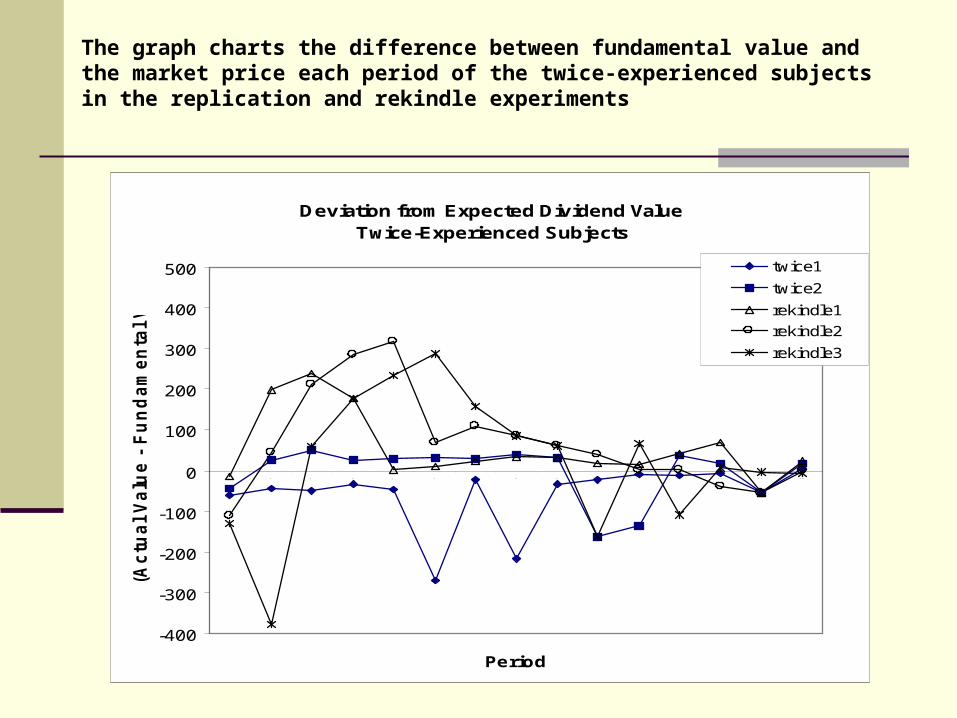

The graph charts the difference between fundamental value and the market price each period of the twice-experienced subjects in the replication and rekindle experiments

Deviation from Expected Dividend ValueTwice-Experienced Subjects

-400

-300

-200

-100

0

100

200

300

400

500

1 2 3 4 5 6 7 8 9 1 0 1 1 1 2 1 3 1 4 1 5

Period

(Ac

tua

l V

alu

e -

Fu

nd

am

en

tal

Va

lue

) twice1

twice2

rekindle1

rekindle2

rekindle3

Do Speculative Stocks Influence Value Stock Behavior? An overreaction in the speculative stock tends to

divert investment capital away from value stocks Trading prices of value stocks are generally lower

and more volatile when one of the assets is a speculative stock.

In addition, the temporal minimum price of the value stock during the last phase of the experiment is lower in the presence of the speculative stock (when the trading price of the speculative asset is declining sharply). suggesting that the psychological impact of rapidly falling

prices in the speculative asset lead to more conservative bidding and aggressive selling of the value asset, even though the latter does not suffer negative earnings updates during this period (affect heuristic).

Overreaction and Information

Groups with disparate beliefs about the fundamentals of a stock

Each group has information that the asset will be worth either 10 or 100

Group 1 has information that leads to a 25% chance of 10 and a 75% chance that it is 100

Group 1 has information that leads to a 75% chance of 10 and a 25% chance that it is 100

Trading continues with this information for 10 minutes New information is revealed to one for the gropus that

aligns with the other group For example, Group 1 is told there is new information that

determines that there is a 75% chance of 10 and a 25% chance that it is 100

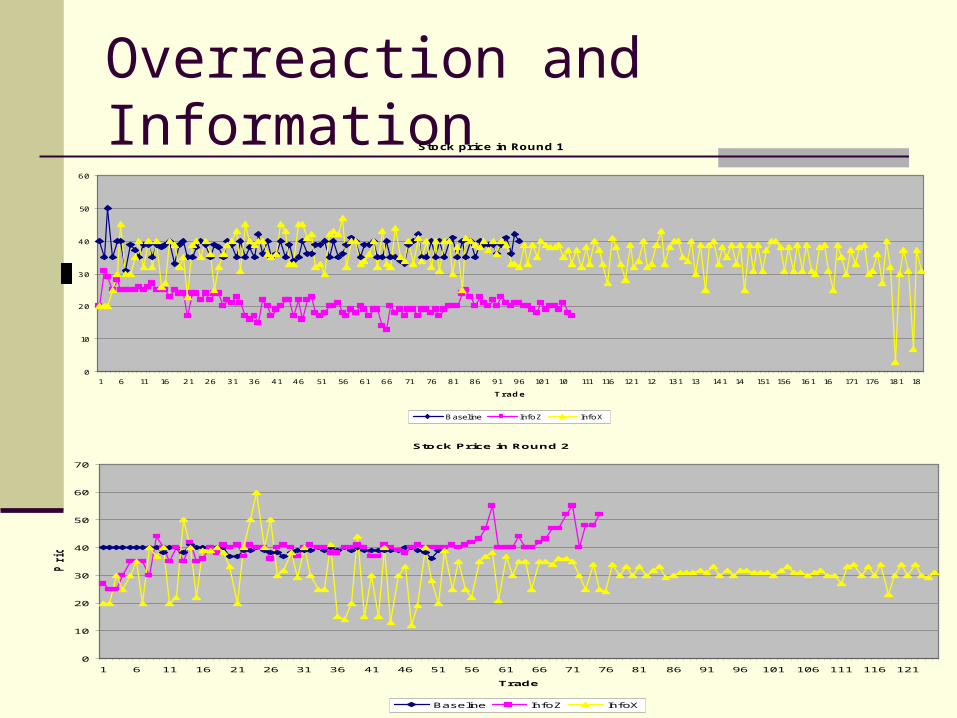

Overreaction and InformationStock price in Round 1

0

10

20

30

40

50

60

1 6 11 16 21 26 31 36 41 46 51 56 61 66 71 76 81 86 91 96 101 10 111 116 121 12 131 13 141 14 151 156 161 16 171 176 181 18

Trade

Baseline InfoZ InfoX

Stock Price in Round 2

0

10

20

30

40

50

60

70

1 6 11 16 21 26 31 36 41 46 51 56 61 66 71 76 81 86 91 96 101 106 111 116 121

Trade

Pric

e

Baseline InfoZ InfoX

Overreaction and Information

Traders underreact to the updated valuation Price and valuation history have a significant

effect on trader behavior Traders tend to “anchor” their price expectations to

the pre-existing prices and/or valuations

News causes an immediate increased variance

Trend is not effected

Irrationality?

Capital gains expectations are not the base cause

Irrationality via probability judgment errors (low-probability high-payoff outcomes) induces more bubbles

Speculation multi-period versus single period markets.

The combination of probability judgment error and speculation increases the probability that bubbles will occur.

The Effect of Noise and Liquidity Traders Noise traders push stocks away from

fundamentals They trend chase They increase volatility

The effect of noise traders is mitigated through call markets Liquidity traders are no harmed Volatility significantly reduced

Recap

Bubbles are pervasive and persistence Attempts to moderate bubbles through

institutional changes do not work or exacerbate the price bubbles

Bubbles a very dependant on the underlying environment Bubbles are fueled by excess cash Uncertainty in dividends that create probability

judgment error ignites bubbles Reignite

Recap

Timing the market from all of the tested models is not possible Chasing the market can leave you holding the

bag Forecasts lag the market and miss turning

points The combination of probability judgment error

and speculation increases the probability that bubbles will occur.

Recap

There are spillovers from speculation in one stock to another Volatility begets volatility Crash in one market can have a affect

heuristic in another There is an underreaction to expectations

alignment Traders anchor on the price trend

The presence of noise traders increase the bubble characteristics and price volatility

Recommended