P3 Challenge for A/E Firms

Monday, April 20, 2015 – 9:30am – 11:30am

Moderator: Rick Volk, CH2M Hill

ABOUT THE SPEAKERS

Federal Perspective Presented by

State Perspective Presented by

Ms. Pauline Thorndike is the Alternative Financing Program Manager with the U.S. Army Corps of Engineers.

She develops and leads teams to support alternative financing initiatives within the Corps of Engineers and

serves as the primary interface for alternative financing coordination, communications and strategic integration.

Mr. Andrew Heller is the Acting Assistant Commissioner for the U.S. General Services Administration’s Public

Buildings Service (PBS) Office of Real Property Asset Management. He sets the strategic direction for

management of the vast owned and leased assets in GSA’s real estate portfolio. This includes executing optimal

investment decisions for the acquisition, construction, renovation, leasing and utilization of the PBS portfolio.

Mr. Richard Ornitz is Senior Counsel at McKenna, Long & Aldridge. A recognized market leader in

infrastructure in the U.S. and globally in emerging markets, he focuses his practice on international,

privatization, private equity and cross-border finance matters.

Mr. Douglas Koelemay has served as Director of the Virginia Office of Public Private Partnerships (VAP3)

since January 2014. In 1993 Koelemay edited “Financing the Future: Report of the Commission to Promote

Investment in America’s Infrastructure,” which sparked creation of TIFIA, private activity bonds and other U.S.

alternate financing tools.

Mr. D.J. Gribbin is a Managing Director and Head, US Government Advisory and Relations for Macquarie

Capital, having spent 15 years working on public policy and business development in the infrastructure sector.

He has led advisory teams working on transactions in Texas, Puerto Rico, New Jersey, and Colorado and has

worked on numerous public private partnership deals in the US.

Ms. Sallye Perrin is a Senior Vice President at Parsons Brinckerhoff (PB). She is nationally recognized for her

ability to help agencies find innovative and cost effective means to implement their transportation programs and

projects and is noted for her expertise in public-private partnerships and alternative delivery projects.

1

American Council of Engineering CompaniesApril 20, 2015

Andrew HellerActing Assistant CommissionerReal Property Asset ManagementPublic Buildings ServiceU.S. General Services Administration

PBS Priorities

2

• Working with Federal Tenants to Reduce their Footprint

• Leveraging Disposal and Exchange Authorities

• Reforming our Approach to Leasing

• Reducing the Cost of Building Operations and Greening our Portfolio

Common theme: to meet agency real property requirements in a fiscally responsible and environmentally sustainable way.

2

FBF Annual Revenue vs Obligation Authority

0

2

4

6

8

10

2008 2009 2010 2011 2012 2013 2014 2015

Rent Estimates

Enacted NOA

IN BILLIONS

3

FY2016 Budget Request

4

$10.37 Billion—Total GSA Budget Request

• $1.26 Billion for New Construction

• $933 Million for Major Repairs and Alterations

• $314 Million for Minor Repairs and Alterations

• $5.58 Billion for Rent in Leased Facilities

3

Public‐Private Partnership Options

5

• Maximizing Disposal and Exchange Authorities:

- Outleasing

- Swap/Construct

• Energy Savings Performance Contracts (ESPCs)

Maximizing Disposal and Exchange Authorities

6

Hanger One at Moffett Field, Mountain View, CA

4

Maximizing Disposal and Exchange Authorities

7

Old Post Office Building, Washington, DC

Maximizing Disposal and Exchange Authorities

8

Volpe DOT Complex, Cambridge, MA

5

Maximizing Exchange and Disposal Authority

9

J. Edgar Hoover Building, Washington, DC

Energy Savings Performance Contracts

10

Fort Buchannan, Puerto Rico

IRS Financial Services Center, New Carrollton, MD

1

P3 CHALLENGE: AMERICAN COUNCILOF ENGINEERING COMPANIES

Douglas Koelemay, Director

VIRGINIA P3 PORTFOLIO

2

I‐95 EXPRESS LANES PROJECT

• I‐95 Express Lanes opened December 2014

• Meeting traffic and revenue estimates

• Virginia contribution of $71 million leveraged $925 million project

• Adds to managed lanes (HOT) system that includes I‐495 Express Lanes

• Virginia’s contribution of $409 million leveraged the $1.7 billion I‐495 project

TRANSFORM I‐66 MANAGEDLANES PROJECT

Multimodal Improvements 25‐miles East from U.S. 15 to I‐495

• 3 General Purpose Lanes, 2 Express Lanes (variable toll)

• Rapid bus and HOV free

• Park and ride facilities

• Request for Qualifications –Spring 2015

• Federal Tier 2 NEPA approval – Late 2015

• Construction 2017

3

ELIZABETH RIVER TUNNEL PROJECT

• New Midtown Tunnel ‐‐Norfolk to Portsmouth

• Rehabilitation of existing Midtown & Downtown tunnels

• Construction of Martin Luther King (MLK) Extension connecting the two tunnels

• Six of 11 tunnel elements immersed

• More than 50% complete• On Time, On Budget

HAMPTON ROADS TRANSPORTATION ACCOUNTABILITY COMMISSION

• Run multiple scenarios to

see the cause and effect

of different assumptions

• Forecast project costs,

revenues and funding

availability

• Informs decisions on

project and program

delivery

VAP3‐developed capital planning tool allows regional bodyto evaluate scenarios of project mix, prioritization,

financing and delivery.

4

PIPELINE OF P3 PROJECTS

ELEMENTS OF VIRGINIA SUCCESSES

Virginia’s P3

Program

Public Sector Capacity

Risk Analysis &

Optimization

Political/ Public Support

Standardized Processes

Pipeline of Projects

P3 Law

1

STRICTLY CONFIDENTIALSTRICTLY CONFIDENTIAL

The P3 Challenge for A/E Firms

ACEC Conference

April 20, 2015

PAGE 1STRICTLY CONFIDENTIAL MacquarieCapital

"Macquarie Capital" refers to Macquarie Capital Group Limited, its worldwide subsidiaries and the funds or other investment vehicles that they manage. Macquarie Capital Group Limited is an indirect, wholly-owned subsidiary of Macquarie Group Limited.

This document and its contents are confidential to the person(s) to whom it is delivered and should not be copied or distributed, in whole or in part, or its contents disclosed by such person(s) to any other person. Notwithstanding the foregoing, the recipient (which includes each employee, representative, or other agent of the recipient) is hereby expressly authorized to disclose to any and all persons, without limitation of any kind, the tax structure and US federal income tax treatment of the proposed transaction and all materials of any kind (including opinions and other tax analysis) if any, that are provided to the recipient related to the tax structure and US federal income tax treatment.

This document does not constitute an offer to sell or a solicitation of an offer to buy any securities. It is an outline of matters for discussion only. You may not rely upon this document in evaluating the merits of investing in any securities referred to herein. This document does not constitute and should not be interpreted as either an investment recommendation or advice, including legal, tax or accounting advice.

Future results are impossible to predict. Opinions and estimates offered in this presentation constitute our judgement and are subject to change without notice, as are statements about market trends, which are based on current market conditions. This presentation may include forward-looking statements that represent opinions, estimates and forecasts, which may not be realized. We believe the information provided herein is reliable, as of the date hereof, but do not warrant its accuracy or completeness. In preparing these materials, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources.

Nothing in this document contains a commitment from any member of Macquarie Capital to subscribe for securities, to provide debt, to arrange any facility, to invest in any way in any transaction described herein or otherwise imposes any obligation on Macquarie Capital. Macquarie Capital does not guarantee the performance or return of capital from investments. Any participation by Macquarie Capital in any transaction would be subject to its internal approval process.

None of the entities noted in this document are authorized deposit-taking institutions for the purposes of the Banking Act 1959 (Commonwealth of Australia). The obligations of these entities do not represent deposits or other liabilities of Macquarie Bank Limited ABN 46 008 583 542 (MBL). MBL does not guarantee or otherwise provide assurance in respect of the obligations of these entities.

CIRCULAR 230 DISCLOSURE

Macquarie Capital does not provide any tax advice. Any tax statement herein regarding any US federal income tax is not intended or written to be used, and cannot be used, by any taxpayer for the purpose of avoiding any penalties. Any such statement herein was written to support the marketing or promotion of the transaction(s) or matter(s) to which the statement relates. Each taxpayer should seek advice based on the taxpayer's particular circumstances from an independent tax advisor.

2015 Macquarie Capital (USA) Inc.

Important notice and disclaimer

2

01 Insert divider title 3

A Insert divider title 7

ContentsContents

STRICTLY CONFIDENTIALSTRICTLY CONFIDENTIAL

01 History of P3s in the US 3

02 Project Pipeline 7

03 The Future of P3s 9

04 Equity Available 11

05 Contact Information 13

STRICTLY CONFIDENTIALSTRICTLY CONFIDENTIAL

History of P3s in the US

01

3

PAGE 4STRICTLY CONFIDENTIAL MacquarieCapital

States with Public-Private Partnership Authorization– 1995

Legal Authority Grows

States without PPP AuthorityStates with PPP Authority

States with Public-Private Partnership Authorization – 2015

Puerto Rico

PAGE 5STRICTLY CONFIDENTIAL MacquarieCapital

States with dedicated Public-Private Partnership Offices

Managing A Public Private Partnership

States without PPP OfficesStates with PPP Offices

Puerto Rico

4

PAGE 6STRICTLY CONFIDENTIAL MacquarieCapital

Revenue Risk

Availability Payment

Route 1 Gateway

407 East PH 1

Waterloo LRT

Windsor-Essex Pkwy

Edmonton Ring Rd

SE Calgary Ring Road

Golden Ears Bridge

Denver FasTracks

I-69 Sec. 5

East End (ORB)

I-4 Ultimate Project

Port of Miami Tunnel

I-595 Corridor

Tolled Traffic

Goethals Bridge

Autoroute 30

S. Fraser Perimeter Road

Windsor-Essex Pkwy

I-69 Sec. 5

NTE Parts 1&2

SH 130 Seg. 5&6

IH-635 LBJ Freeway

Midtown Tunnel

I-895 Pocahontas Parkway

I-95 Express Lanes

I-495 Capital Beltway

Dulles Greenway

Autoroute 25

Overview of P3 MarketTOP 30 NORTH AMERICAN DEALS CLOSED 2005-PRESENT

Puerto Rico

$37,265 million$2,265 million $615 million

Total Value of Concessions:$40,145 million

Transit (2) Airports (1) Roads (27)

STRICTLY CONFIDENTIALSTRICTLY CONFIDENTIAL

Project Pipeline

02

5

PAGE 8STRICTLY CONFIDENTIAL MacquarieCapital

No P3 Legislation

Current P3 Legislation

Virginia

I-66 finalizing feasibility study, issuing RFQ April 2015

California

Long Beach Civic Center selected preferred bidder

Puerto Rico

Ohio

Portsmouth Bypass financial close end March 2015

Indiana

Illiana Expressway (Indiana portion) placed on hold

Maryland

Purple Line transit project currently on hold

North Carolina

I-77 HOT Lanes expected to close April 2015

Kentucky

Brent Spence Bridge placed on hold to evaluate financing

Recent Developments

Massachusetts

Sagamore Bridge procuring as a P3, issuing RFQ in H1 2015

Florida

I-395 set to procure as PPP

Illinois

Illiana Expressway (Illinois portion) placed on hold

Michigan

NITC deal signed between US & Canada

Colorado

I-70 East RFQ released March 2015

California

UC Merced shortlisted 3 parties in Jan. 2015

Texas

I-35 undertaking a feasibility study in consideration of PPP

Florida

South Miami Heights Water Treatment Plant, award April/May 2015

STRICTLY CONFIDENTIALSTRICTLY CONFIDENTIAL

The Future of P3s

03

6

PAGE 10STRICTLY CONFIDENTIAL MacquarieCapital

Where Can P3s Be Used?

Prisons

Parking

Bridges

Power

Water

Schools

Telecom Services

Ports

Hospitals

CourthousesRail

Roads

Airports

Universities

STRICTLY CONFIDENTIALSTRICTLY CONFIDENTIAL

Equity Available

04

7

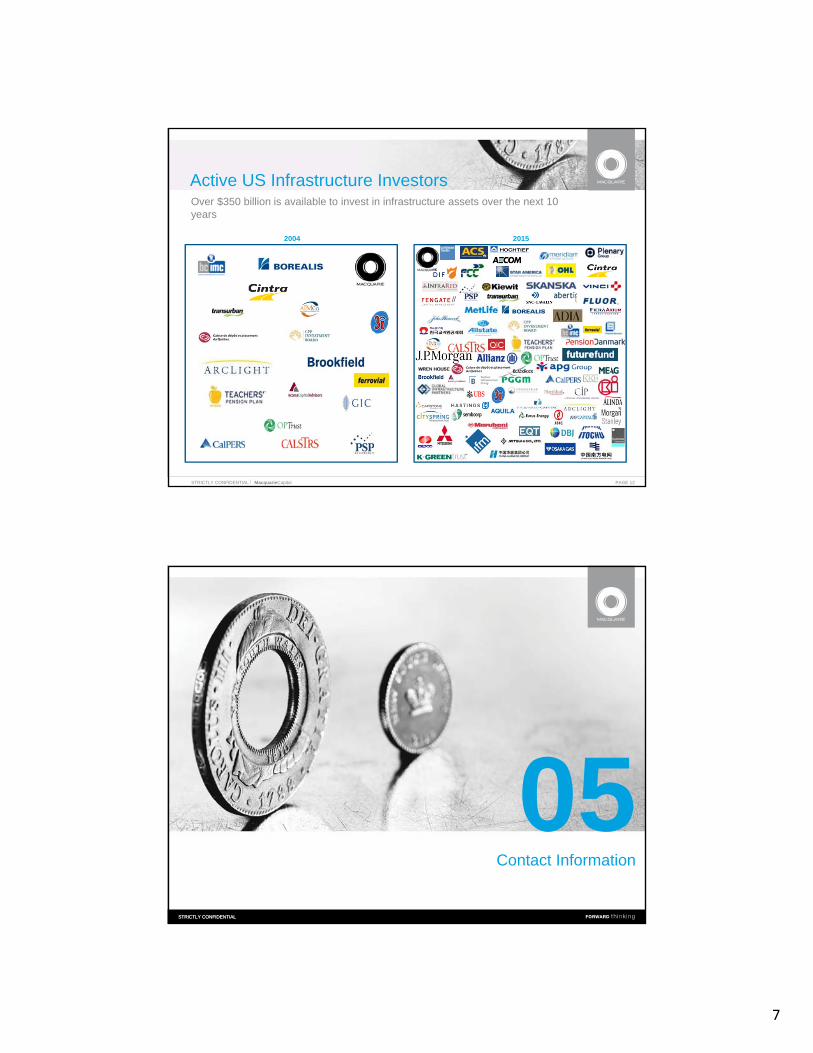

PAGE 12STRICTLY CONFIDENTIAL MacquarieCapital

Over $350 billion is available to invest in infrastructure assets over the next 10 years

20152004

Active US Infrastructure Investors

STRICTLY CONFIDENTIALSTRICTLY CONFIDENTIAL

Contact Information

05

8

PAGE 14STRICTLY CONFIDENTIAL MacquarieCapital

D.J. Gribbin

Head, Government Advisory and Affairs

Macquarie Capital

125 W 55th Street, Level 16

New York, NY 10019

(646) 204-6772

Contact Information

1

Sallye PerrinSenior Vice President Parsons Brinckerhoff

Since 2008, P3s have been used to deliver over $27 bn of transportation infrastructure◦ 21 projects (highway/bridge/rail)◦ Trending to close 3 P3s per year ($2.5 bn in 2015)◦ Cap Ex portion of bids have been consistently 10%

to 30% below engineers estimates◦ Schedules have been accelerated on average by 4

months So how did we get here?.................

2

3

In P3s, A/Es are joining Developer/Concessionaire teams. ◦ Local knowledge and relationships are still important ◦ Innovation, efficiencies, and life cycle come into play.

P3s come with lots of agreements. ◦ The Developer/Concessionaire will pass down risks to

the D/B. ◦ D/B will pass those risks to down to the A/E. ◦ Each agreement will be unique.

Opportunity to increase profits and share in the value of our work

4

SPVSpecial Purpose

VehicleDebt

FinancialEquity

ContractorEquity

O&M JV

ConstructionJV

HoldCo

Designer Contractor

Concession orComprehensive Development

Agt (CDA)

Public Sector

TechnicalAdvisor

FinancialAdvisor

TechnicalAdvisor

FinancialAdvisor

O&M Provider

TechnicalAdvisor

P3s and alternative design are becoming acceptable options for delivering large complex projects

35+ states have P3 legislation in place Because of financing, P3s allow state DOTs to

advance major projects that would otherwise sit on the books for years…..

Project Neon and AZ 202 are now D/B. P3 failures can still mean projects are getting built

5

Traditional Highway and Bridge◦ I-70 E (Colorado)◦ I-66 (Virginia)◦ Brent Spence Bridge (Ohio and Kentucky)

Bundled Projects: PA Bridges◦ Smaller projects combined to meet size thresholds

Tolling vs Availability Payments◦ Different risk profiles and incentives

Social Infrastructure◦ Gaining ground in the US

P3s are a tool in the toolbox…..they do not replace federal and state funding

A/E firms need to support reauthorization and support long term solutions for the Trust Fund

TIFIA and PABS are critical to the delivery of major projects

New ideas like QPIBS or Move America Bonds will strengthen our ability to accelerate infrastructure delivery

6

Engineering Opportunities with Smart Cities

and Smart Cars

Monday, April 20, 2015 – 9:30am – 11:30am

Presented by Richard Azer, Black & Veatch; Cliff Thomas, Cisco; Robert

Wimmer, Toyota Motor North America; Shane Stevens, First Element Fuels.

ABOUT THE SPEAKERS

Cliff Thomas, is Managing Director, Cisco Global Segment. He leads the team responsible for

Cisco’s Smart + Connected Communities (S+CC) focus on intelligent urbanization. His global team

is responsible for developing business strategies creating new routes to market through joint

ventures, new revenue share models, public private partnerships and business acceleration for

Cisco’s clients, governments, and ecosystems partners in sectors that include Education, Health and

Wellness, Transportation, Utilities, and much more.

Bob Wimmer, National Manager of Toyota Motor North America’s Energy and Environmental

Research Group, leads a team of research engineers assessing how changes in energy and

environmental technology, such as alternative fuels and advanced vehicle technologies will affect

the automotive industry, as well as policy and regulatory standards. Additionally, he manages

TMA‘s energy collaborations with other corporations, the company‘s interaction with the US

Department of Energy and a portion of TMA‘s university research activities.

Shane Stephens, Co-Founder, Chief Development Officer, Principal, FirstElement Fuel, is in charge

of investments and business development as well as government and policy related issues and

company growth. Prior to FirstElement, he earned a Ph.D. in Engineering at the University of

California Irvine, where he produced groundbreaking research on hydrogen fuel cell technology and

infrastructure.

Richard Azer is the Director of Development for Black & Veatch’s SII service line and is involved

in developing smart city initiatives, such as microgrids, distributed renewable energy and intelligent

utility networks. Azer has over 20 years of experience in developing and implementing emerging

technologies. He is currently involved in a program to deliver the first nationwide network of high-

power, fast electric vehicle charging stations.

DoD Infrastructure Programs

Monday, April 20 – 2:00pm – 4:00pm

Presented by Miroslav Kurka, Mead and Hunt; Patricia Coury, Office of the

Assistant Secretary of Defense; Beth Lachman, Rand; Lucian Niemeyer, The

Niemeyer Group, LLC

A panel of OMB and Dept. of Defense officials.

ABOUT THE SPEAKERS

Miro Kurka, PE, PMP, COL USA (Ret) leads Mead & Hunt’s Water Resources Group. He has

oversight responsibilities for all design project managers and is responsible for technical

planning and analysis, project management, developing project work scopes and negotiating

task orders. Miro has successfully managed numerous large planning and feasibility studies and

was Principal-In-Charge of a highly successful new hydroelectric project on an existing United

States Army Corps of Engineers (USACE) dam.

Beth Lachman is a policy analyst in RAND's Washington office. Her expertise includes

systems analysis of environmental problems, environmental science and technology policy,

sustainable development policy, mathematical modeling and GIS analysis of urban systems.

Ms. Lachman is currently leading a project to analyze federal, state, and local government

collaboration in the development and implementation of environmental technologies for

sustainability.

Lucian Niemeyer recently retired from the United States Senate Committee on Armed Services

after 11 years and formed the Niemeyer Group, LLC, offering business development strategies

and consulting expertise on national defense issues. He is currently partnering with numerous

firms to establish project-specific teams dedicated to efficiently and effectively meeting client

goals as well as speak publicly and lecture on federal legislative and national defense issues.

Patricia Coury spent the first 20+ years of her professional career with the U.S. Army Corps of

Engineers. She is responsible for programmatic oversight and policy development affecting the

cradle-to-grave life cycle for DoD’s worldwide facilities, the management of defense

installations, and the Department’s government-owned, leased and privatized housing and

privatized lodging.

1

DOD Infrastructure ProgramsThe Congressional Perspective

Lucian Niemeyer ([email protected]) March 2015

American Council of Engineering Companies

Congressional Issues Affecting Engineering Companies

• Sequestration of Defense Budgets• Forecast for Facility Investment Accounts

•Armed Forces Reductions

• Specter of BRAC Authorization• Intergovernmental Support Agreements

•Public Private Initiatives

2

Sequestration of Defense Budgets

The Budget Control Act of 2011• Mandates that the “base” Defense Budget will be sequestered to $499 billion in FY 2016 – Congress will not repeal.

• A $35 billion reduction over President’s Budget Request

Funds for Overseas Contingency Operations (OCO)• Intended for combat operations in Afghanistan and elsewhere

• “Off‐Budget” Emergency Supplemental Appropriations

• President Requested $51 Billion for DOD in FY16 – about $25 Billion more than needed based on historical expenses in theater

• Congress will add another $38 Billion to OCO for DOD in FY16• Intended to offset sequestration without raising non‐security spending

Forecast of Facility Investment Accounts

Military Construction• Good News ‐ FY2016 Total DOD MILCON request of $8.4 Billion is $1.8 Billion more than the FY15 enacted amount for MILCON of $6.6 Billion.

• Bad News – MILCON is subject to sequestration (about 10‐15% cut)

• DOD projects MILCON to be flat through Future Years Defense Program (FYDP) ‐unsequestered

• FY17 ‐ $8.7 B; FY18 ‐ $8.5 B; FY19 ‐ $7.9 B; FY20 ‐ $7.1 B

Facility Sustainment, Restoration, Modernization (FSRM)• DOD continues to take risk in facility sustainment accounts

• The FY2016 DOD request of $10.8 billion is better than the FY15 enacted amount of $9.0 billion, but well below the FY2014 amount of $13.3 Billion

• Congress may add small amounts back to FSRM in 2016, but still not enough to meet goals for 90% of sustainment requirement

3

Armed Force Reductions

Army• Currently 490,000 Active duty soldiers with an FY2016 President’s Budget request to drop to 475,000.

• Army is planning for sequestration to require Army to drop to 420,000

• Will have a dramatic impact on installations and housing privatization

Navy/USMC• Navy requires a 308 ship fleet to meet COCOM requirements • Currently at 272 ships after Congressional rejection of cruiser/LPD retirements• Competing pressures from sequestration and huge capital investments (Ohio Class submarine replacement, aircraft carrier construction, next small surface combatant) leaves future size of the fleet uncertain.

• Impact to shore infrastructure and facility investments Air Force

• Trying to retire weapon systems – rejected by Congress

Specter of BRAC AuthorizationDepends on the Positions of the “Big 4”• HASC Chairman – No BRAC Until sequestration fixed and force structure stabilized

• HASC RM – Supports BRAC and has drafted legislation• SASC Chairman – Included in letter to the Budget committee an endorsement of management reforms “that could reduce or consolidate military headquarters, commands and infrastructure.”

• SASC RM ‐ Endorsed a need for a BRAC round in a hearing on March 3 with Secretary Carter

Scorecard ‐ That’s 2 for, 1 against, and 1 unknown who was a primary BRAC advocate in 2001 for the 2005 round.

4

Spector of BRAC Authorization

Other Positions• SASC Readiness Chair – “Even after acknowledging the shortcomings of the 2005 round, the department continues to request the same legislative framework…I remain opposed to BRAC and do not want to give the department the open‐ended authority to pursue another BRAC round that has the potential to incur significant upfront costs”

• HASC Readiness Chair – Will propose again legislation for a BRAC facility capacity analysis – this time with force structure assumptions

• OSD/Installations – Open to discussion on changes to legislation –offered an overall cap on total BRAC implementation costs

• USAF – Updated estimate of 30% excess facilities (24% last year)• Army – Even at 490,000 soldier end strength – 18% excess facilities• Navy – “We’re good.”

Intergovernmental Support Agreements

Congress established Section 2336 of Title 10 USC in 2013

• Authorizes the military services to enter into agreement with a State or local government to provide, receive, or share installation‐support services if the Secretary determines that the agreement will serve the best interests of the department.

•Many defense communities are seeking agreements with DOD for shared utility and infrastructure maintenance or operations.

• Potential for engineering companies to facilitate the agreements

• Still considered a new authority as Services wrestle with templates, level of effort, and applicability of Federal Acquisition Regulations

5

Public Private InitiativesCongress Continues to Provide Pilot Legislative Authorities for certain programs•Military Housing Privatization is transitioning to long‐term maintenance phase with pressure from proposed reductions in the Base Allowance for Housing (BAH)

• Congress may expand legislation for utilities privatization to incorporate stormwater and allow for system expansion

• DOD using Power Purchase Agreements to facilitate construction of renewable energy sources – Congress may redirect investments to on base energy resiliency

• Renewable energy goals may be reassessed by new Congress.Renewed effort by industry and Congress to address OMB scoring with updates to OMB Circular A‐11

Questions?Lucian Niemeyer

March 2015

American Council of Engineering Companies

DoD Infrastructure Programs: Key Trends that

Will Shape Installations of Tomorrow

Beth Lachman

RAND Corporation

April 20, 2015

American Council of Engineering Companies

2015 Spring Convention

2

Key U.S. Trend Areas that Will Affect Installations

Topic Area Main Trend Area Infrastructure

Implications ?

Water Issues Water scarcity Yes

Sustainable Building Practices and

Sustainable buildings Yes

Energy Technologies Energy Yes

Community and Sustainable communities Yes

Transportation Design Sustainable transportation Yes

Encroachment

Urbanization and increased development

Indirect

Loss of biodiversity Indirect

Societal trends ??

Quality of Life Online communities ??

Issues Pervasive computing ??

Sustainable agriculture No

3

• U.S. water trends: – Clean water becoming significantly more scarce

– More and more people using limited water supplies

– More local and other government restrictions on water use

– More water partnerships and collaboration activities

• Implications for DoD installations: – May have installation operational restrictions because of water

shortages and water restrictions

– Will cost significantly more later if wait to address – Need for innovative, efficient, and collaborative investments

• Regional partnerships, ESPCs, UESCs, EULs,technologies, etc.

• Benefits to DoD strategic actions: – Provide significant cost savings

– Prevent water from becoming an operational problem – Help meet future requirements and improve environmental quality

– Improved community relationships

Address Water Issues to Avoid Significant Future Costs

4

Implement Sustainable Building Practices to Avoid Significant Future Costs

• Sustainable building trends: – State and local building codes, voluntary standards, and labeling

programs define higher and higher performance goals – More best practices for building management that save money over the

long term, such as commissioning and life-cycle analysis (LCA) – Federal, state, and local requirements for more sustainable buildings – Likely more emphasis on LCA, green procurement, and designing

buildings for reducing waste and deconstruction

• Implications for DoD installations: – If wait to act, will miss significant cost savings if have less efficient

buildings and will have high future costs to retrograde buildings for stricter requirements

– Need for investment in sustainable and strategic building improvements to save money over the long term

• Benefits to DoD strategic actions: – Provide significant cost savings with more efficient buildings – Able to meet future stricter requirements more efficiently and improve

environmental quality

5

Implement Efficient Energy Technologies to Avoid Significant Future Costs

• Energy trends: – Energy demand and prices will continue to rise – Renewable power generation and use of natural gas growing – Increasing federal, state, and local requirements for increased

investments in efficiency and renewable energy technologies

– Improvements in energy technology performances and costs • Implications for DoD installations:

– If wait to act, will miss significant cost savings if using less energy efficient technologies and incur high future costs to implement energy technologies to meet stricter requirements

– Need for innovative investments in energy efficiency and renewable energy technologies • Partnerships, ESPCs, UESCs, PPAs, etc.

• Benefits to DoD strategic actions: – Provide significant cost savings with improved energy

technologies

– Able to meet future stricter requirements more efficiently and improve environmental quality

6

Strategically Address the Design of Installation Communities

• Key sustainable community trends: – Emphasis on land use planning, compact development, growth

management, and community design • Traditional neighborhood development (TND)/New urbanism

– Development of industrial ecology/eco-industrial parks – Improved waste management, such as composting & waste-to-

energy • Implications for DoD installations:

– If wait to act, high cost to redo community infrastructure in the future and a decrease in installation land-use flexibility

– Need to include more compact development and community design principles in installation master plans

– Should explore eco-industrial park pilots with neighboring industry

• Benefits to DoD strategic actions: – Help save costs with compact development – Environmental quality and aesthetic improvements – Military personnel and family Quality of Life (QOL) improvements

7

Strategically Address Transportation Design

• Key sustainable transportation trends: – Emphasis on compact land use and less personal vehicle travel

because of the benefits to the environment, mobility, QOL, and community

– Increasing number of diverse personal mobility options, such as car sharing

– More electric and other alternative energy vehicles – More transportation system planning and operations improvements

• Implications for DoD installations: – If wait to act, in the future, will incur a high cost to redo

transportation infrastructure and have more traffic congestion and environmental problems

– Need to include more sustainable transportation planning • Infrastructure and activities that encourage decreased personal vehicle

travel, such as car sharing, more convenient buses, and bike lanes • Benefits to DoD strategic actions:

– Help save costs with better transportation planning – Environmental quality improvements – Military personnel and family Quality of Life (QOL) improvements

8

Strategically Address Encroachment

• Key Encroachment Trends: – Increases in incompatible development from nearby sprawling

communities and continuing significant loss of biodiversity • More likely to have more political, policy, and regulatory activities

protecting biodiversity • More likely to have more threatened and endangered species

(T&ES) – Causes encroachment for training and other operations – More restrictions on training and building activities

• Implications for DoD installations: – If do not address, likely to have major restrictions on

installation testing, training and other operations from more incompatible development and more T&ESs and very high future costs if not impossible to address later

– Develop partnerships with communities on growth management and to protect habitat surrounding installations

• Benefits to DoD strategic actions: – Help prevent installation encroachment and T&ESs, preserve

installation operational flexibility, and save high future costs

9

Collaboration and Partnerships are Becoming More Important to Military Installations

• Installations are increasingly surrounded by nearby communities • More military personnel and their families live in surrounding

communities • Installation partnerships and collaboration are ways to help

– Save costs by leveraging resources and expertise – Preserve installation operational flexibility – Improve military personnel and family quality of life

– Meet installation current and future requirements • More collaborative approaches and practices

– Intergovernmental Support Agreements – ESPCs, UESCs, EULs, and PPAs – Housing and utility privatization

• Community relationships becoming more important to military installations is a cross-cutting trend, for areas such as

– Community growth and transportation planning – Water supply and environmental management

10

RAND References

• Reports available online

– "Key Trends That Will Shape Army Installations of Tomorrow”

http://www.rand.org/pubs/monographs/MG1255.html

– "Making the Connection: Beneficial Collaboration Between Army Installations and Energy Utility Companies”

http://www.rand.org/pubs/monographs/MG1126.html

– "The Thin Green Line: An Assessment of DoD's Readiness and Environmental Protection Initiative to Buffer Installation Encroachment”

http://www.rand.org/pubs/monographs/MG612/

• For more information about RAND see

– www.rand.org

2 Dec Joint Base WG: ITSM COLS Changes 1

Acquisition, Technology and Logistics

DoD Infrastructure Programs

Patricia L. Coury Deputy Director

Facilities Investment & ManagementOffice of the Assistant Secretary of Defense

(Energy, Installations and Environment)

Acquisition, Technology and Logistics

DoD Real Property Portfolio

• 562,600 Facilities– 284,458 buildings ($484B Plant Replacement Value)

• 191,309 owned; 7,519 leased; 85,630 other • 2.18B sq ft

– 176,931 Structures– 101,211 Linear Structures

• 24.7M Acres – 98% in U.S.

• 523 Installations– 4,855 DoD Sites (86% in U.S.)

(Data as of Sep 2014)

2

2 Dec Joint Base WG: ITSM COLS Changes 2

Acquisition, Technology and Logistics

Base Realignment & Closure (BRAC)

• DoD has requested BRAC authority the past three years– 2004 DoD capacity assessment indicated 24% aggregate excess

– 2015 Budget testimony:

• Air Force - 30% excess capacity

• Army - 18% excess capacity

• BRAC 2005 reduced just 3.4% of DoD’s infrastructure as measured in Plant Replacement Value (PRV) – BRAC 2005 focused primarily on transformation rather than

efficiency

• Transformation recommendations cost $29B for $1B annual savings

• Efficiency recommendations cost $6B for $3B annual savings

– Subsequent force structure reductions point to additional excess capacity

• Large private companies would not retain excess capacity

3

DoD Options Limited

Acquisition, Technology and Logistics

European Infrastructure Consolidation (EIC)

• Holistic, joint review completed Jan 2015– Focused on reducing our European footprint while continuing to

support operational requirements and strategic commitments

– Used a BRAC-like process to review capacity, requirements, military value, cost, and diplomatic dynamics

– 26 recommendations

• ROI – Expected $800M cost to construct facilities at receiving sites

– Anticipated $500M annual, recurring savings once all actions implemented

• Majority of $800M in construction supports:– RAF Mildenhall - restationing of 3200 U.S. personnel elsewhere

– Offset slightly by 1,200 personnel that will support F-35s being stationed at nearby RAF Lakenheath

– Consolidation of Joint Intelligence Analysis Facilities at RAF Croughton4

2 Dec Joint Base WG: ITSM COLS Changes 3

Acquisition, Technology and Logistics

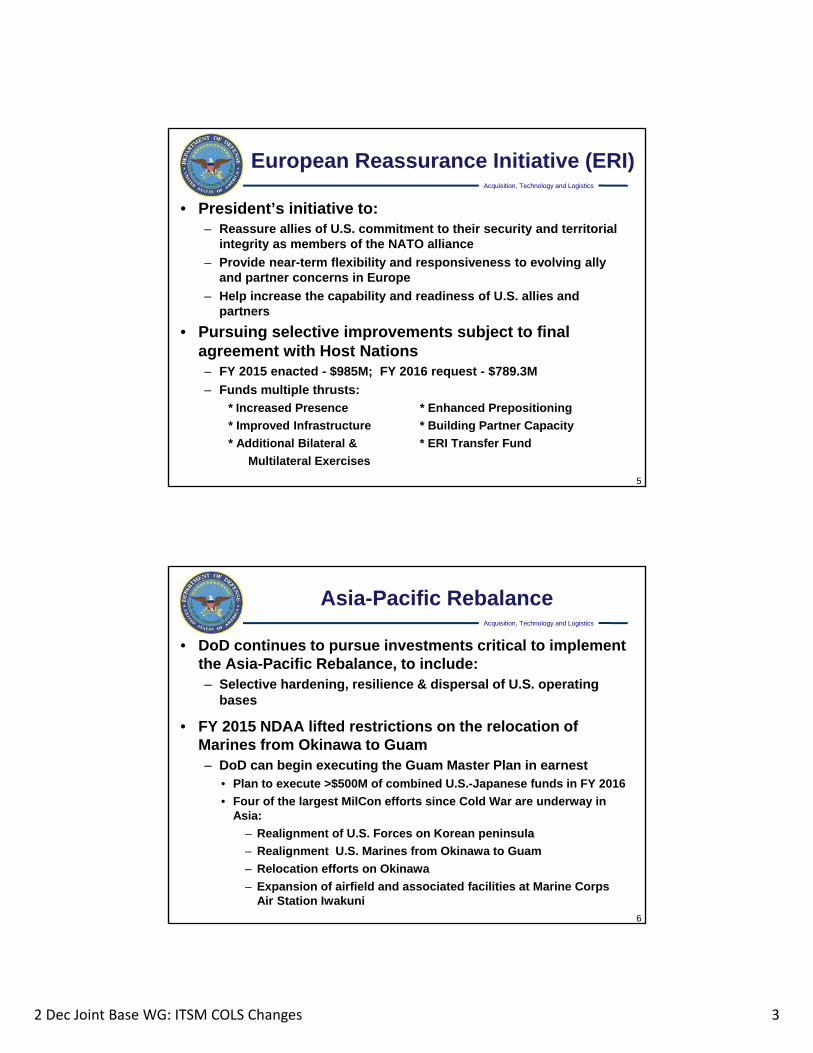

European Reassurance Initiative (ERI)

• President’s initiative to:– Reassure allies of U.S. commitment to their security and territorial

integrity as members of the NATO alliance

– Provide near-term flexibility and responsiveness to evolving ally and partner concerns in Europe

– Help increase the capability and readiness of U.S. allies and partners

• Pursuing selective improvements subject to final agreement with Host Nations– FY 2015 enacted - $985M; FY 2016 request - $789.3M

– Funds multiple thrusts:

* Increased Presence * Enhanced Prepositioning

* Improved Infrastructure * Building Partner Capacity

* Additional Bilateral & * ERI Transfer Fund

Multilateral Exercises

5

Acquisition, Technology and Logistics

Asia-Pacific Rebalance

• DoD continues to pursue investments critical to implement the Asia-Pacific Rebalance, to include:– Selective hardening, resilience & dispersal of U.S. operating

bases

• FY 2015 NDAA lifted restrictions on the relocation of Marines from Okinawa to Guam– DoD can begin executing the Guam Master Plan in earnest

• Plan to execute >$500M of combined U.S.-Japanese funds in FY 2016

• Four of the largest MilCon efforts since Cold War are underway in Asia:

– Realignment of U.S. Forces on Korean peninsula

– Realignment U.S. Marines from Okinawa to Guam

– Relocation efforts on Okinawa

– Expansion of airfield and associated facilities at Marine Corps Air Station Iwakuni

6

2 Dec Joint Base WG: ITSM COLS Changes 4

Acquisition, Technology and Logistics

Facilities Sustainment

• Sep 2013 – Facility Condition Assessment Policy– Standardized DoD-wide facility inspection process using DoD

Sustainment Management System (SMS) software suite (e.g., BUILDER)

– Requires completed inspections using SMS by Sep 2017

– Requires qualified technical personnel

– Supports FCI data necessary to inform programming & budgeting decisions

• Apr 2014 – Facility Sustainment & Recapitalization Policy– Reiterates DoD goal to budget sustainment at > 90% of modeled

requirement

– Established DoD Component inventory-wide average FCI program/budget goals with minimum average FCI > 80%

– Established DoD Component annual business plans for assets with FCIs < 60%

7

Acquisition, Technology and Logistics

Alternative Financing

• Public-Private Partnerships – examples:

– Military Housing Privatization Initiative (10 USC § 2871-2885)

– Enhanced Use Leases (10 USC § 2667)

– Energy Savings Performance Contracts (ESPCs) (42 USC § 8287 & 10 USC § 2913)

– Utility Energy Service Contracts (UESCs) (10 USC § 2913)

• Public-Public Partnerships– Section 331, NDAA 2013 (10 USC § 2679)

• Installation Support Services using Intergovernmental Support Agreements

8

DoD Fully Supports the Use of Third Party Financing

2 Dec Joint Base WG: ITSM COLS Changes 5

Acquisition, Technology and Logistics

9

Questions?

For more information:

http://www.acq.osd.mil/ie/fim/index.shtm

Recommended