LIQUEFIEDNATURALGAS(LNG)SUPPLYTOGHANA:THEPOLITICS

ANDTHEREALITY

ANADVISORYPAPERFORTHEGOVERNMENT

August,2017

1

1.0BackgroundGastopowerhasbeentrendinggloballygiventhebenefitsithasofbeingcheaperandcleaner

comparedtootherfossilfuels.GhanasigneduptotheWestAfricaPipelineProject(WAGPP)

inrecognitionoftheimportantrolegascouldplayinthepowersector.Theinitialcontracted

volumeofgaswas120millionstandardcubicfeet(mmscfd).Aftercompletionoftheproject,

Nigeriacouldnotdeliverthecontractedvolumefromfirstgas inDecember2008. In2012

NigeriaGassupplywascutasaresultofanaccidentinTogowherethepipelinewassevered

bytheanchorofaship.Atthesametime,Ghana’sdomesticgassupplycouldnotbedelivered

ontime.TheJubileefieldwasexpectedtoheralddomesticgassupplybytheendof2012.

Thiscouldnotbeachievedbecauseof technicaland financial reasons.Ghanastruggled in

manyinstancestosatisfytheconditionsforthedisbursementoftheChineseDevelopment

Bank(CDB)loanfacilityandtimelydisbursementofcounterpartfundingbygovernmentitself.

In2012thepowercrisisstartedasaresultofgassupplycurtailmentsfromNigeriaandJubilee.

Thepush foralternativesupplyofgasheightenedandLiquefiedNaturalGas (LNG)supply

throughtheuseofFloatingStorageandRegasificationUnit(FSRU)washighlyconsideredby

government throughprivatecapital.TheEnergyCommission (EC), thetechnicaladviser to

government, by 2013 had licensed seven (7) companies to develop LNG projects.

Notwithstanding, there remainsan indecisionover thesupplyofLNGtoGhanawhichhas

lastedformorethan5years.

Initially, the fear of gas glut blighted any seriousness to consider LNG. The general

assumptionswerethatdomesticsupplyofgascouldreach350mmcfd;beyondtheJubilee

gas,GhanaalsoexpectedadditionalgasfromtheTweneboah-Enyenra-Ntomme(TEN)field,

theSankofa-Gye-Nyame(SGN)fields,andtheMahogany-Teak-Akasa(MTA)field.Moreover,

Nigeriagascouldberestoredtoatleastthecontractedvolumeof120mmcfd,pushingtotal

gassupplyinexcessof450mmcfd,whichwouldbeenoughtopowerabout2600MWofgas

turbines.Therefore,basedonthoseassumptionsandprojecteddemandforelectricity,an

LNGcommitmentwasrisky forgovernment.Asa result,noneof theseven (7)companies

licensedbytheEnergyCommissiontosupplyLNGsince2012haveprogressedbeyondthe

licensetocommissionanLNGfacility.

2

TheoutcomeoftheindecisiononLNGandoverrelianceonNigeriagascontributedtothe

long period of power supply deficit which affected the health of the Ghanaian economy

between2012and2015.

From 2015 to date, government has renewed seriousness to procure LNG. In 2015, the

government signed contracts withWest Africa Gas Limited (WAGL). The Ghana National

PetroleumCorporation(GNPC)alsosignedanLNGsupplyagreementwithKaheelInvestment

ofDubaiin2016,thesecondafteranagreementwithQuantumgasLimitedwassignedbefore

2015. The government is also considering an LNG supply agreementwith Blystad Energy

Management(BEM).

Inthispolicypaper,ACEPhasanalysedthecostofGhana’sindecisiononLNGsupplyandthe

unendingpoliticswhichriskthesustainabilityofthepowersector.

2.0 HowMuchDidGasContributetotheEnergyCrisisbetween2012and2015?

Thechallengesofthepowersectorhaveevolvedovertimetobesummarizedinthesector’s

lexiconasTechnical,FinancialandManagerial.However,fuelsecuritywasaprimaryfactor

whichescalatedthechallengesbeyondcontrolin2012andtheyearsafter.Thecessationof

gassupplyfromNigeriarenderedthermalplantslikeAsogli,MineReservePlant(MRP),and

TemaThermal2Plant(TT2P)redundant.Aship’sanchorseveredtheWestAfricaGasPipeline

inAugust2012intheterritorialwaterofTogo.Ittookoneyearforgastoberestored,against

theexpectationofashorttermfix.Afterthepipelinewasfixed,thesupplylevelsremained

belowthecontractedminimum.ThisputsignificantpressureonVoltaRiverAuthority’s(VRA)

dualfuelplantsandthehydroplantstogeneratethepowerdemandedbythecountry.

TheimmediateresponsewasthatVRAhadtoswitchitsdualfuelplantsfromgastomore

expensive Light Crude Oil (LCO) without commensurate tariff to compensate for the

additional cost incurred in procuring LCO. This trended to the point where VRA’s credit

worthinesswaserodedagainstrisingoilpricesontheinternationalmarket.Atthesametime,

3

the stress on the hydro plants resulted in over-drafting of the dams which necessitated

significantdropinoutput.BuiAuthorityissuedastatementtosaythat“Theexceedinglyhigh

levelofgenerationsupportthattheBuiGeneratingStationhasbeenprovidingforthenational

electricitygridsincetheinaugurationoftheBuiplanthascausedtheBuireservoirleveltofall

to the minimum operating level of 168 metres above sea level (masl)”.1 The dams were

politicallymanageduntiltheyoperatedbelowminimumlevels.

OwingtothepressureonVRAtogeneratepowerfromthedualfuelthermalplant,theVRA

missed some scheduled maintenance timelines. This affected the plants, resulting in

avoidablefaultswhichcompoundedthepowerproblems.

Itisthereforewithoutargumentthatgassupplycurtailmentwascentraltothegenesisand

protractionofthepowercrisisinGhanabetween2012and2015.

3.0 RiskaversionagainsttheresultantcosttoGhana

AtypicalcostofLNGfacility,usingFSRU,couldrangebetween$400Millionto$600million

depending on scale, siting and existing infrastructure for evacuation of gas to demand

centres.ThisisthepotentialriskthatGhanafacedintheeventthattheinvestmentbecame

unnecessary,assumingalltheplansfordomesticgasandNigeriagassupplymaterialised.The

power sectorwouldhavehad toabsorb the cost in that scenario.However, this scenario

paints a significant cost burden in the absence of a counterfactual analysis of the cost

associatedwiththeeventualitythatallplansfordomesticgasandgasfromNigeriadidnot

materialize.

AlltheanalysesontheneedforLNGaroundthetimeGhananeededtotakeadecisionfailed

toanalysethecostontheGhanaianeconomyofpotentialfailureofthegassupplyplansfrom

domesticsourcesandNigeriathroughWAGP.TheWorldBankprojectedthatGhanamaynot

needLNGbeyond2017whendomesticsupplyfromJubilee,TENandSankofawereexpected

1http://www.graphic.com.gh/news/general-news/bui-power-reduces-generation.html

4

tocomeonstreamandthereforeLNGmaynotbenecessary.2Thiswasbasedonassumption

thatLNGcouldtakeupto4yearstobedelivered,whichfurtherassumedthatLNGprojects

signed up for could coincide with the timing for adequate domestic gas supply. This

assumption failed to recognised that the delivery of LNG through an FSRU could be fast-

trackedandachievedwithin18months.

TheEnergyCommission(EC)wasquiteemphaticinits2012EnergyOutlookforGhanathat

LNGwasnecessaryanddemandedcommitmentfromGovernmenttomobiliseinvestmentin

theshortestpossibletime.TheCommissionrecommended“Governmentshouldproactively

create incentives to encourage investment in LNG regas facility built at her coast at the

shortest possible time. An investment workshop for stakeholders where the government

entities including Ghana Investment Promotion Centre and the Ministries of Energy and

Financecantabletheeconomicandinvestmentincentivesthatthegovernmentcouldoffer

wouldbeveryessential”.Between2012and2014,LNGcouldhavebeendeliveredonafast-

trackbasis.Unfortunately,theEC’sveryimportantsignaltothegovernmentfailedtogetthe

neededattention.

HadtheadviceoftheECbeenheeded,andhadtheMinistryinvestigatedthecostofinaction

tothecountry,thepowersectorwillnotbeashighlyindebtedasitis

today. ACEP estimates that the power sector lost $1.042 billion in

revenuein2014and2015duetoloadshedding.A2015reportbythe

InstituteofStatisticalSocialandEconomicResearch(ISSER)alsoputs

thecostofloadsheddingontheGhanaianatbetweenUS$320million

andUS$924millionannually.Noanalysishasbeenabletoquantifyloss

ofhuman lives,propertyandbusinesses thatpermanentlycollapsed.Again,asat the first

quarterof2017, theenergy sectorwasestimated tobe in$2.4billiondebt.TheVRA, for

example,whichmadeprofitsin2011wouldhavecollapsedwithitscurrentdebtburdenifit

2Suniletal(2013).EnergizingEconomicGrowthinGhana:MakingthePowerandPetroleum

SectorsRisetotheChallenge.Availableat

http://documents.worldbank.org/curated/en/485911468029951116/Energizing-economic-

growth-in-Ghana-making-the-power-and-petroleum-sectors-rise-to-the-challenge.

Accessedon7/25/2017at3:53PM

ACEPestimatesthatthepowersectorlost$1.042billioninrevenuein2014and2015duetoloadshedding

5

wereaprivatecompany.

The cost of taking a $600million investment risk in LNGwould have amounted to three

pesewasperkilowatt-hour(Kwh)onelectricityforfiveyearstocoverinvestmentandinterest.

ThisisfarnegligiblecomparedtowhatGhanaiansarepayingtoday,followingtheredemptive

measure to rescue theenergy sector through the institutionalisationof theEnergySector

Levies Act (ESLA). The ESLA imposes levies on electricity consumption to the tune of 3

pesewas/Kwh,andonpetroleumproductstothetuneof28pesewasperlitreoverafive-year

period.Thesecometoatotalof31pesewas.TheindecisiontobringinLNGthereforeimposes

anavoidableextraburdenof39pesewasonconsumersofelectricityandpetroleumproducts.

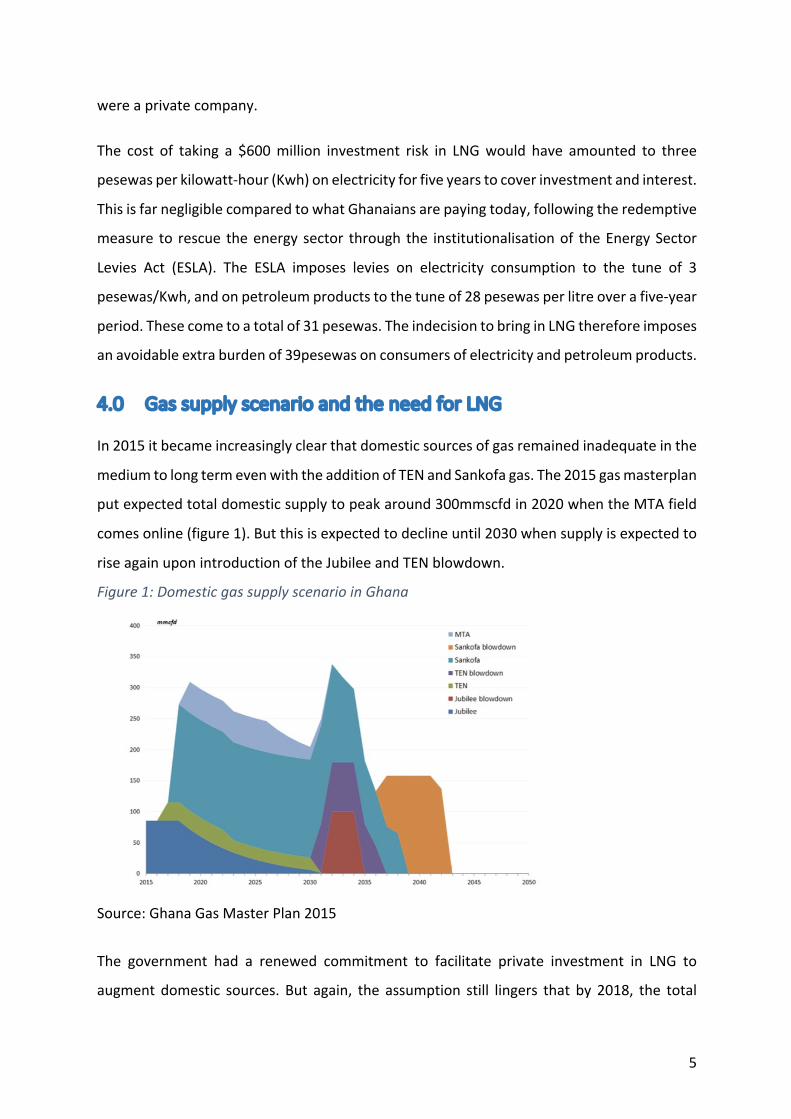

4.0 GassupplyscenarioandtheneedforLNG

In2015itbecameincreasinglyclearthatdomesticsourcesofgasremainedinadequateinthe

mediumtolongtermevenwiththeadditionofTENandSankofagas.The2015gasmasterplan

putexpectedtotaldomesticsupplytopeakaround300mmscfdin2020whentheMTAfield

comesonline(figure1).Butthisisexpectedtodeclineuntil2030whensupplyisexpectedto

riseagainuponintroductionoftheJubileeandTENblowdown.

Figure1:DomesticgassupplyscenarioinGhana

Source:GhanaGasMasterPlan2015

The government had a renewed commitment to facilitate private investment in LNG to

augment domestic sources. But again, the assumption still lingers that by 2018, the total

6

domesticgassupplycouldexceed300mmcfd.TheSankofafieldisexpectedtoproducethe

largestvolumeof180mmscfdwhiletheJubileegascouldstabiliseintheregionof100mmscfd,

withadditional50mmscfdfromTENfields.Thesedomesticsourceswillbeenoughtopower

time-of-use projected demand from thermal plants in 2018 (assuming expected gas

productionfromthedomesticproducingfieldsarerealized).Also,theriskposedbypotential

supplyofcontractedvolumefromNigeriaunderthetake-or-payarrangementinjectsmuch

nervousnessintothedecisiontoprocureLNG.

GRIDCoprojectsthatin2018,thedemandforelectricitywillbeabout2600MW,whichwill

largelybemetbyhydroandthermalsources.Aspresentedinfigure2,electricitydemandis

expectedtogrowovertheperiodbetween2018and2022.Hydroisprojectedtosupplyan

annual average of 1,120MWduring that period. Thismeans that thermal generationwill

significantlyaccountforthedifferenceindemandgrowthwhichwillrisefrom1500MWin

2018to2700MWin2022.Thisindicatesthatsecurityofgassupplyis importanttoensure

that the thermal plants can generate the needed power, at the cheapest cost, to meet

demand.

Figure2:ProjectedElectricityDemand,2018-2022

Source:GRIDCo,20173

3PresentationatGhanaEnergySummit,2017

1120 1120 1120 1120 1120

15262008

23422592 2708

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2018 2019 2020 2021 2022

ProjectedElectricityDemandfrom2018to2022

HydroAverageSupply Time-of-useThermalDemand

7

Giventheuncertaintyinthegassupplymarket,boththeEnergycommissionandGRIDCohave

recommended the importation of gas through LNG facility. ACEP believes this

recommendation is accurate to the extent that the three domestic sources will still not

provideenoughsecurityofsupply,andNigeriagasstillremainsunreliableandarisktothe

economicfortunesofthecountry.Ifoneofthedomesticfieldsundergoesmaintenancefor

example,therewillbesignificantvolumereductioninsupply.

5.0HowmuchLNGisrequired?

ACEPhasbeenmonitoring therenewedcommitmentbygovernment to importLNGsince

2015. In this process the Centre conducted gas needs assessment of the country and

cautionedthatthetrendindomesticgassupplyrequirednotmorethanoneLNGcontractby

government. At the time, governmentwas considering two LNGprojects using FSRU; the

WestAfricanGasLimited (WAGL)project (sponsoredbySaharaandtheNigerianNational

PetroleumCorporation(NNPC)),andtheQuantumPower(QPR)project(sponsoredbyajoint

ventureinvolvingUKandGhanaianinvestors,andGNPC).TheWAGLproposedtosupply180

mmscfperday,whilstQPRproposed250mmscfperday.Parliamentsubsequentlyapproved

theWAGLprojecteventhoughthecosttothenationwashigherthanthatofQPR.

The GNPC also entered into another agreement with Kaheel Investments, a company

registeredinDubai.ThiswasbafflingtotheextentthatGNPCisinapartnershipwithQPRto

supply the same product against the reality that Ghana needed only one LNG project.

However,withachangeingovernmentin2017,theKaheelprojectseemstohavedissipated

withthetransitions.

The threeprojectswillbe remembered for thecontroversy thatensuedafterHonourable

BoakyeAgyarko,currentMinisterforEnergy,insistedathisvettingthatGhananeededonly

oneLNGprojectandyet, thepreviousgovernment signed three. Theministervindicated

ACEP’spositionandwasthereforeexpectedtoinitiateprocessestoensurethatonlyoneFSRU

wascontractedwithdueregardforvalueformoney,capacityoftheinvestortoinvestinan

LNGfacility,andtheriskstogovernmentfinances.Theprocessoftakingthedecisionhasbeen

slow,butperhapscompensatedforbythesavingsseenbythecurrentprocessesofreviewing

thecontracts.ACEPcanconfirmthatfacility-use-chargesseenonrevisedproposalssentto

8

the ministry presents annual savings of $15million and $63million on QPR and WAGL

respectively. Currently another company, Blystad Energy Management, has joined the

competitiontoincreasethenumberofcompaniestofour.

6.0 BriefsonthefourLNGprojects

Theanalysisissequencedonthetimethecompaniesapproachedgovernmentoranagency

ofstate.

6.1 QuantumPower(QPR)Project

Thisprojecthadinitial20-yearperiodforamortizationwhichhasbeenrevisedto10yearsin

responsetothedirectiveoftheMinistrytolimitthecontractperiodfortheproposalsto10

years.ItisaBuild,Own,OperateandTransfer(BOOT)arrangementbetweenQuantumPower

(QPR)andGNPCwhichwillseetheinfrastructuretransferredtoGNPCafterthecostofthe

projectisamortized.

TherequirementonGhanaisforGNPCtoofftaketheuseofanFSRUwiththeflexibilitytobe

active in the procurement of LNG either through GNPC’s own arrangement, or an

arrangement between the government of Ghana and governments of LNG producing

countries.

QPRisproposingafacilityuserchargeof$1.3perMMBtufora10yearlevelizedvolumeof

250mmscfd.Thisconstitutes$0.17reductionoftheinitialproposalof$1.47onthe20-year

timescale,translatingtoanannualsavingsof$15.5million.Theinitialsitingoftheprojectat

12kmoffshorehashoweverbeenreducedto5kmoffshore.

6.2 WestAfricanGasLimited(WAGL)Project

ThisprojectissponsoredbySaharaEnergyandTheNigeriaNationalPetroleumCorporation

(NNPC).ThisprojecthasacompositearrangementforthesupplyofFSRUandLNG.Theinitial

proposalbyWAGLhasbeenrevisedfortheprovisionofFSRUfrom$2.2perMMBtuto$1.5

perMMBtu. This translates into a savingsof about $63million annually on their revised

project.WAGLgotparliamentaryapprovalforaGasSalesAgreement(GSA)withgovernment

inOctober,2016whichlocked-inminimumLNGpriceof$7.15perMMBtuindexedagainst

9

Brentcrudeoil.TheformulaapprovedbyparliamentstipulatesthatLNGpriceswillbeequal

to$7.15ataBrentpriceofbelow$40/bbl.WhenBrentPriceisbetween$40and$80/bbl,LNG

pricewillbe8%ofBrentplus$3.98.WhenBrentisabove$80/bbltheLNGpricewillbe10%

ofBrentplus$2.35.TheWAGLprojecthasalsobeenconvertedintoaBOOTprojectinthe

currentproposaltoallowgovernmenttoowntheFSRUafter10years.

6.3 TheKaheelGroupProject

GNPC entered into another agreement with the Kaheel Terminal Investment (owned by

ownersoftheAmeriGroup)toprovideanotherLNGfacilityusingFSRUinthewesternRegion

ofGhana.Thisarrangementissurprisinginlightofthefactthatallanticipateddomesticgas

supplyarelocatedintheWesternRegionandexceedsthegasrequirementofexistingpower

plants.Notwithstanding,GNPC,ceasedwiththerealitiesofthegassupplyscenario,entered

intotheKaheelcontractinOctober2016.

ItisclearfromtheactionoftheMinistryofEnergyinrecenttimesthattheKaheelprojectis

notoneoftheoptionsbeingconsidered.ACEPwillthereforeskipanalysisofthedetailsfor

thisagreement.

6.4 BlystadEnergyManagement(BEM)Project

The addition to the number of companies interested in delivering LNG is BEM. It is a

partnershipbetweenBEManditslocalPartner,WestCoastGhanaGas(WCGG).Thesolution

proposedbyBEMissimilartothatofWAGLintermsofsitingandLNGprocurement.BEM

proposes locating its facility at the Tema Port. The technology however differs in

configuration.BEM’ssolutioncomprisesoftwovesselconfigurationofFloatingRegasification

Unit (FRU)andFloatingStorageUnit (FSU).Thismeansthatatanytimetherewillbetwo

vesselsdockedattheport,andathirdvesselduringdeliveryofLNGintotheFSU.Thiswill

requiresignificantexpansionofthePorttoprovidetherightmanoeuvrability,andlimitthe

impactonporttraffic.

Thepricing forBEM isalsocomposite,proposing to supplyequipment (FRU/FSU)and the

commodity.Thepriceforfacilityuseisquotedat$1.38perMMBtuwhilethatofLNGsupply

isarrivedatusingBrentindexedformula.AtaBrentpriceabove$60theLNGpricewillbe

10

12.5%ofBrentpriceminus$0.82perMMBtu.AndataBrentPricebelow$60theLNGprice

willbe$7.5%ofBrentpriceplus$2.18perMMBtu.

7.0 KeyDynamicsofthe3ProposedOptions(QPR,WAGLandBEM)

Thetablebelowexplainsthekeysubtletiesthatdefineeachoftheproposals,givenalevelized

tenureof10-yearsand250mmscfdsupplyvolume.AlltheprojectsalsoprovideforaBOOT

model.

Table1:ComparisonamongthefourLNGprojects

QPR WAGL BEM CommentsSiting The FSRU will

be sited 5km

offshoreTema,

moored in

position to

supply LNG

through

undersea

pipelinetothe

shore.

TheFSRUwillbe

berthed at the

Tema Port,

requiring Deep

dredging and

construction of

Breakwater.

This is similar to

WAGL’s

requirementand

may require

biggerexpansion

of the port to

provide

manoeuvrability

for a third

vessels during

LNGintake

Siting at the Port is a

more popular and

conventional solution in

the use of FSRUs.

However, out of Port

solutionsaretestedand

viable. The choice of

either In-Port or

Offshore site should

rather be informed by

contextual

determination. There is

currently a study by

Genesis and Technip

whichsuggeststhathigh

pressure gas cannot be

safely evacuated from

thebuild-upareaof the

Tema Port. GE’s Early

Power was denied the

opportunitytoconstruct

their LPG pipeline for

same reason. The

expansion work for the

FSRU could provide

benefits for other uses.

However, this may not

be necessary

considering that siting

the FSRU in the Port

could be risky, and also

that there is already an

ongoing $1.5 billion

11

expansionofthePortby

Ghana Ports and

Harbour Authority

(GPHA) which will

provide similar benefits

that an FSRU-based

expansionmaybring.

Pricing-EquipmentUse

$1.3 $1.5 $1.38 QPR provides the

cheapest option

followed by BEM and

WAGL. However with

BEM’s pipeline cost not

known yet, its price

couldenduptobemore

expensive at the final

estimation.

LNGPrice QPR does not

offer LNG

supply.

However

GNPC

presented a

priceof$5.854

to AfDB from

its preliminary

negotiations

WhenBrentis

<$40/bbl,LNG

Price=$7.15.

WhenBrentis

between$40

and$80/bbl,

LNGPrice=$8%

of Brent +

$3.95; and

when Brent is

greater than

$80/bbl.

LNG Price =

10% Brent +

2.35. Thereforeintoday’stermsLNG will beequal to$8.10925

When Brent is

above $60/bbl,

LNG Price =

12.5%Brent + (-

0.82),

and when Brent

is equal to or

below$60/bbl,

LNGPrice=7.5%

Brent+2.18,

In today’s termsLNGpricewillbe$6.079256

QPR provides the

optionality for

government to

negotiate for its LNG

supply. The other two

provide composite

facility and commodity

agreement. The

composite arrangement

increasesthetakeorpay

risk for Ghana on both

LNG procurement and

facilityuse.

DeliveredLNG

$7.15/MMBtu $9.61/MMBtu $7.46/MMBtu QPR and BEM present

lower figures of $7.15

and $7.46 respectively.

ThisprovidesQuantuma

$0.31/MMBtu price

4ThispriceisusedfortheanalysisthoughpricesarecheapertodaythanquotedbyGNPCin

December2016.5BasedonBrentpriceof$51.99asofAugust2,2017asreportedbyBloomberg

6ibid

12

advantage over BEM,

representing an annual

savings to Ghana of

$28.3 million. However

Brent indexation

subjects the pricing of

LNG to the volatility of

the crude oil price and

doesnotaccountforthe

analysis in section 8.0

below.

Risk/liabilityover a10yearperiod

1,186,250,000

8,769,125,000

6,807,250,000

The composite

equipment and LNG

supply heightens the

take or pay risk for

Ghanaat$8.8billionand

$6.8billiononWAGLand

BEM respectively. The

$1.2 billion risk on the

QPR allows government

to negotiate less risky

government to

governmentLNGsupply.

Timing ofFirst Gasafterfinancialclose

Quarter 3 in

2018

Quarter 3 in

2018

Quarter 1 in

2019

The timing for the In-

Port solutions look

conservative given the

dredging and

breakwaterconstruction

required. Especially

when the studies to

confirm the extent of

work needed have not

been done by BEM and

WAGL.

Source:ACEP,20177

8.0 WhyGhanaNeedsaFacilityUseAgreement(FUA)andNotacompositeFUAandLNGsupply.

GhananeedstheflexibilitytotakeadvantageofthefallingLNGpricetrend.Theindexationof

gaspricetotheBrentdoesnotreflecttheglobaltrendintheLNGmarket.LNGpriceshave

beenfallingtodefyprojectedincreasebyIMFandtheWorldBank.Japanwhichconsumesa

7ACEP’scompilationbasedonprojectproposalssubmittedbythethreecompaniestothe

Government.

13

thirdoftheglobalLNGrecentlyoutlawedLNGresalerestrictiontoallowtheirimportersto

sellcontractedLNGsupplyonthemarket.This is in responsetocurrentmarketdynamics

wherenewsuppliesfromUSandAustraliaareinfluencingpricereductions.AgainQatarisset

to increase LNG exports to 100 million metric tons from 70 million metric tons against

projecteddemandstagnation inEurope.At thesametime, theUnitedstates is increasing

exportsfromshalegasrevolution.ThedevelopmentinAfricaevensupportsanopenplanning

fortheprocurementofLNG.Tanzania,MozambiqueandSenegalwillsooninjectmoregas

ontothemarketthroughLNG,giventhebigdiscoveriesinthosecountries.

Itisthereforenotjustifiableforgovernmenttoapprovealocked-inLNGpricefor10years.

Thecommodityisassumingamarketofitsownandthereforepricebenchmarkingagainst

Brent crude is discouraged. Ghana should therefore rely on Government to Government

negotiationstosupportGNPCtoprocureLNGcheaply.

9.0 Recommendations

ACEP appreciates the challenges the Government of Ghana has faced over the years in

decidingontheneedforanLNGfacility.Thegassupplyscenariodefinitelyposessomerisk

which demands very careful analysis onmitigationmeasures. ACEP thereforemakes the

followingrecommendationstothegovernmentinitsassessmentoftheneedforLNG:

1. LNGisneeded-GhananeedsLNGtoprovideextragassupplysecurityevenin2018,

when local supply could be just enough for the time-of-use demand scenario.

Indigenous supply is still not diversified enough to provide confidence for

uninterruptedsupplyfromthefields.

2. NigeriaGas -Weobserve that gas supply fromNigeria does not hold any reliable

promise. The suppliershavenotdeliveredon foundational volumeover theyears,

largely influenced by growing demand for gas in Nigeria and export of LNG. The

current supply of only about 9mmscfd doesn’t give any assurance for the future.

NNPC,whichisamajorplayerintheWAGPP,isnowexploringopportunitytoexport

LNGtoGhanathroughWAGL.Thisarrangementcouldbethedeathwarrantforthe

WAGPiftheLNGbusinesspresentshigherrevenuetoNNPCthanthroughtheWAGP.

Government should therefore take the necessary steps to revoke the take-or-pay

14

agreementundertheWAGPwithNNPCtorelieveGhanaofsomerisksassociatedwith

theimportationofLNG.

3. LocationoftheLNGFacility-TherearecontentionsaboutthesuitabilityoftheTema

PortforthesitingoftheLNGfacility.Regardlessofhowremotetheriskmaybe,ACEP

recommends that siting of the facility outside the Port should be considered. The

reasonisthat,thePortisamajorrevenuebasketforthestateandanyactivitythat

risks the size of revenue from the Port should be considered carefully. The fiscal

challengesofthecountrywillworsenifthePortdoesn’tfunctionasrequired.Thereis

noreasonforPortactivitiestosufferwhenthereareviablealternatives.

4. GovernmentshouldreservetherighttoprocureLNG–thecurrenttrendintheLNG

market presents an opportunity forGhana to take advantageof the falling prices,

negotiatestableprices,notbesubjectedtothevolatilityinthecrudeoilmarket,and

ineffectmakegreatersavings.

5. Scalability-GasdemandscenarioforGhanaislargelyinfluencebythepowersector.

This leavesthecountry largelyunabletoestimatefuturedemandbyothersectors.

Against the much talked about industrialisation agenda of the government, the

procurementofLNGfacilityshouldbeabletoaccountforgasneedsthatcannotbe

assessed in the short term. The remedy is to ensure that the facility thatwill be

contractedhasthepotentialtoscaleupsupplywithattendantbenefitsfromeconomy

ofscaleratherthantwoLNGfacilitieswhichwillbemoreexpensive.Scalabilityisnot

beingconsideredcurrentlyunderanyoftheproposals.

6. Managingtheriskofpotentialgasglut-theGhanaGasMasterPlanidentifiesother

potentialindustrialusesofgas,includingthetextile,cement,steel,paperandfertilizer

industries.Thereistheneedforaproactivepolicyshifttoactivatethosedemands.

This will align with Ghana’s industrialisation agenda and ensure that gas drives

industrywithitsclimatebenefits.

7. QPR is recommended- on the strength of the threemain proposals and available

informationusedforthisanalysis,ACEPisoftheviewthattheQPRprojectpresents

greatervalueonthestrengthsofprice,siting,andoptionalityforGhanatoprocureits

ownLNG.

8. Parliamentsshouldseekindependentopiniononcontracts-thesavingmadebythe

MinistryofEnergyontheWAGLcontractisagoodindicationthatparliamentneeds

15

independenttechnicalreviewof longtermcontracts.WAGLhasreduced itsfacility

usefeefrom$2.2perMMBtuto$1.5perMMBtu.ThisnewproposalsavesGhana$63

million annually (or $630million for 10 Years) on the use ofWAGL’s FSRU if it is

allowed to go ahead. The implication is that parliament could not assess the cost

burdenagainstthemarketvalueoftheproject.ThecompositesavingsonEquipment

supplyandLNGcouldbeintheregion$1.8billionand$2.6billionwhencomparedto

theotherproposals.

9. IntroducecompetitivebiddingforfutureLNGcontracts-ACEPproposesthatfuture

contractsshouldbesubjectedtotheProcurementActtoensurethatthereisfairness,

transparency,andcompetitionsforsuchcontracts.Thatway,thecompanywiththe

bestvaluetoGhanawillbeselected.

10. Conclusion

ACEP is of the view that the financial risk of importing LNG is lower than the risk of not

importingit.Ghana’senergysectorissufferingtodaybecausethecountrylackedtheboldness

totakerisksatthetimesomeanalystsestimateddomesticsupplyofgaswouldbeenoughfor

powergeneration.LNGwillprovidegreatersecurityofsupplywithdiversityofsources.Itis

inthisrespectthatACEPrecommendsthatthegovernmentshouldfacilitatetheprocurement

ofanLNGfacility,criticallyconsideringthescalability,timing,cost,andsitingoftheproject.

Recommended