LatAm Macro Monthly Scenario Review

February 2014

Please refer to the last page of this report for important disclosures, analyst and additional information. Itaú Unibanco or its subsidiaries may do or seek to do business with companies covered in this research report. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should not consider this report as the single factor in making their investment decision.

Page Global Economy

The Global Scenario Remains one of Growth Recovery. Emerging Markets will Continue Under Pressure 3 Emerging markets had a rough ride in the past month. Some of the stress might ebb. Unfortunately, this will not bring relief to economies with weak fundamentals. Differentiation will play a role again.

Brazil

Growth Without Energy 8 Growth has lost momentum in recent months, we have reduced our forecast for GDP growth in 2014. However, we expect now a longer monetary tightening cycle, in response to the more volatile global scenario.

Mexico

A Bumpy Recovery 15 The economy weakened in 4Q13, we reduced our growth forecast for this year. Considering the better prospects for FDI and the exposure of the U.S. economy, the peso will likely continue to outperform other emerging market currencies.

Chile

An Easing Bias Amid Higher Volatility 18 The central bank left the policy rate unchanged in January, but reinforced the easing bias. We expect a 25-bp rate cut this month, but further weakening of the peso could lead the central bank to wait a bit more.

Peru

Recovery and No Further Rate Cut 20 Growth improved, mostly due to solid consumption.To protect the sol, the central bank reduced reserve requirements and is intervening in the market, but we do not expect further interest rate cuts.

Colombia

Comfortable Exchange Rate Level 22 Consumption is growing at a robust pace, while the Manufacturing sector remains in negative territory. Authorities seem comfortable with the weaker currency, especially considering the low inflation.

Argentina

Sharp Depreciation of the Peso, Higher Interest Rates 25 The government allowed sharp depreciation in the peso and a moderate hike in interest rates. New adjustments in these variables are on the way.

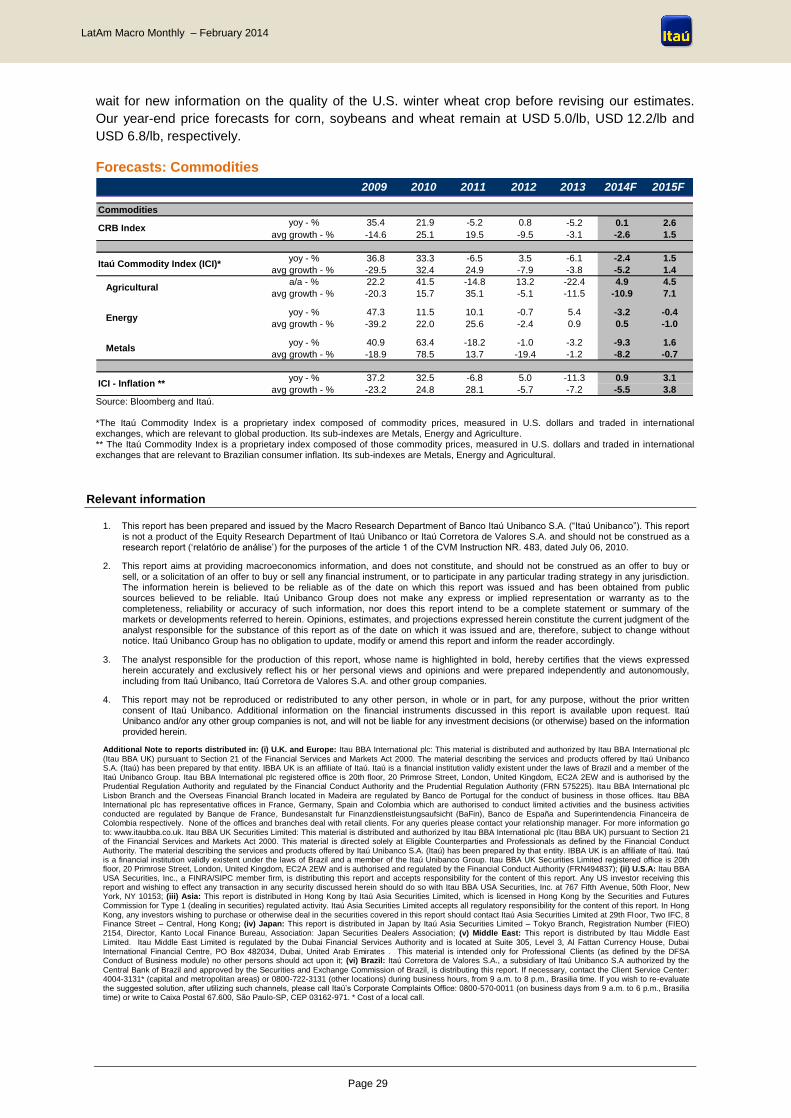

Commodities

Weather-Related Uncertainty 27 Hot and dry weather in Brazil has led to reduced crop forecasts for coffee, sugar, corn and soybeans, in descending order of likelihood and magnitude. Non-precious metals prices remain on a downward trend.

Macro Research – Itaú

Ilan Goldfajn – Chief Economist

Tel: +5511 3708-2696 – E-mail: [email protected]

Page 2

LatAm Macro Monthly – February 2014

Turbulent Markets in Search of Differentiation

It was a turbulent start of the year for emerging economies. Unlike last year, when the turbulence was

a reaction to changes in U.S. monetary policy, this time around the main concern is the sustainability

of the global recovery and the quality of fundamentals in some emerging markets.

This stress seems exaggerated. The global scenario continues to suggest that growth will rebound.

Weakness in U.S. and Chinese data seems temporary. Emerging economies are less vulnerable than

the market assumes – we are not back in the 1990s.

Still, volatility and risk aversion will likely continue throughout the year, affecting emerging economies,

particularly those with fragile fundamentals. Markets are searching to distinguish between the more

robust and the more fragile economies.

In this environment, Latin America experienced turmoil at the beginning of the year. The exchange

rate weakened in most countries in the region. We expect this move to be partly reversed, but

uncertainty will likely affect monetary policy decisions. We no longer forecast interest rate cuts in Peru

and Colombia. We only expect interest rate cuts in Chile. Nevertheless, we expect a recovery in

growth in these nations in 2014 after a slow year in 2013.

Mexico was hit to a lesser extent by the negative market sentiment. Proximity to the U.S. and

recently-approved reforms improved the outlook for the country in the eyes of investors.

In Brazil, the focus is on the sluggish economic activity growth. Weak manufacturing results, higher

energy costs and the possible effects of the Argentine crisis led us to revise our forecast for GDP

growth downward this year. With slower growth and lower-than-expected inflation in January, the

central bank may reduce the pace of interest rate increases in its next Copom meeting, as long as the

international scenario allows it.

Amid international turmoil, the crisis is Argentina has gotten deeper. The government allowed sharp

depreciation in the peso and a moderate hike in interest rates. New adjustments in these variables

are on the way, likely before year-end. All in all, the much anticipated macro adjustment in Argentina

seems to have started at the beginning of the year.

Hope you enjoy,

Ilan Goldfajn and Macro Team

Current Previous Current Previous Current Previous Current Previous

GDP - % 3.5 3.5 3.5 3.5 GDP - % 2.1 2.7 2.8 2.6

Current Previous Current Previous Current Previous Current Previous

GDP - % 1.4 1.9 2.0 2.2 GDP - % 3.3 3.6 3.8 3.8

BRL / USD eop 2.55 2.55 2.55 2.55 MXN / USD eop 12.8 12.8 12.8 12.8

Monetary Policy Rate - eop - % 11.00 10.75 12.00 11.50 Monetary Policy Rate - eop - % 3.50 3.50 4.50 4.50

IPCA - % 6.2 6.2 6.0 6.2 CPI - % 3.7 3.7 3.2 3.2

Current Previous Current Previous Current Previous Current Previous

GDP - % -3.0 0.0 0.0 -3.0 GDP - % 4.2 4.2 4.5 4.5

ARS / USD eop 11.0 9.5 14.3 13.7 CLP / USD eop 540 540 550 550

BADLAR - eop - % 40.0 27.0 30.0 35.0 Monetary Policy Rate - eop - % 4.00 4.00 4.50 4.50

CPI - % (Private Estimates) 37.0 37.0 27.0 30.0 CPI - % 2.8 2.8 3.0 3.0

Current Previous Current Previous Current Previous Current Previous

GDP - % 4.2 4.2 4.5 4.5 GDP - % 5.3 5.3 5.6 5.6

COP / USD eop 2000 2000 2025 2025 PEN / USD eop 2.90 2.90 2.95 2.95

Monetary Policy Rate - eop - % 3.25 3.00 4.00 4.00 Monetary Policy Rate - eop - % 4.00 3.50 4.00 4.00

CPI - % 2.9 2.9 3.0 3.0 CPI - % 2.5 2.5 2.0 2.0

Scenario Review

Latin America and Caribbean

2014 2015 2014 2015

Peru

Chile

Colombia

Argentina

2014 2015 2014 2015

World

2014 2015 2014 2015

Brazil

2014 2015 2014 2015

Mexico

Page 3

LatAm Macro Monthly – February 2014

Global economy The Global Scenario Remains one of Growth Recovery. Emerging Markets will Continue Under Pressure

• The global scenario is still a story of recovering growth. The data weakness in the U.S. is likely to

be temporary, and concerns about China might be exaggerated.

• Emerging markets have had a rough ride in the past month. What started last year as a reaction to

changes in monetary policy in the U.S. took on new dimensions after idiosyncratic shocks and amid

rising concerns about the global recovery.

• Some of the stress might soon ebb. Concerns about the global economy could fade, and as a

group, emerging markets have less financial vulnerability than they did in the 1990s.

• Unfortunately, this is not likely to bring relief to the emerging market economies that have weak

fundamentals. At the very least, differentiation will matter again.

Exagerated stress

A sequence of weaker data releases in the U.S. and in China, combined with increasing

turbulence in the emerging markets, challenged the scenario of global recovery and spooked

investors at the start of 2014.

We think that the data weakness in the U.S. is temporary and that the concerns about China’s

economy might be exaggerated.

We expect the U.S. economy to continue its recovery this year, as the fundamentals remain

good. Financial conditions are supportive, and the fiscal drag is lightening. The recent slowdown is

mainly related to the inventory accumulation cycle and weather effects. We continue to forecast GDP

growth rates of 3.0% in 2014 and 3.1% in 2015, up from 1.9% in 2013.

China seems more risky, but we expect the country to avoid major mistakes this year and to

successfully manage a gradual slowdown of its economy. A decline in the Purchasing Managers’

Indexes in January and the near-default of a Chinese trust fund brought back fears of a hard landing

in China. We are cautious about putting too much emphasis on the few and noisy data releases

available at this time of the year, just after the Chinese New Year. Moreover, the country’s credit

problems seem manageable, as there is fiscal space for state-sponsored solutions without creating

much stress. We still expect China’s GDP growth to slow only gradually, falling to 7.5% in 2014

and 7.3% in 2015 from the 7.7% rate posted in 2013.

In the euro zone, economic activity remains good but inflation surprised on the downside

again. Leading indicators showed some improvement in January, but inflation came in at 0.7% yoy,

down from 0.8% in December. We still see the European Central Bank staying on hold, but the odds

of another rate cut in March are increasing.

In Japan, activity picked up at the turn of the year. Consumers are accelerating their spending

ahead of the VAT increase scheduled for April, and economic activity has picked up as a result. We

expect some deceleration after the VAT increase. If the economy decelerates, the Bank of Japan

might need to begin a new round of stimulus by mid-year.

The emerging markets have had a rough ride over the past month. Continuing outflows,

idiosyncratic events and weaker numbers from China and the U.S. all contributed to the stress. What

started last year as a reaction to changes in monetary policy in the U.S. soon took on new

dimensions.

Page 4

LatAm Macro Monthly – February 2014

We think some of this stress reflects exaggerated fears. The global scenario remains a story of

recovering growth. And as a group, emerging markets have less financial vulnerability than they did in

the 1990s, when they faced a series of systemic crises.

Unfortunately, an easing of the stress will likely not bring relief to those emerging market

economies that have weak fundamentals. Manufacturing exports, at least, will benefit as the global

recovery regains its footing. But interest rates in the U.S. will likely resume their upward trend, and

capital will continue to leave the emerging markets.

U.S. – Weakness in activity data is likely to be temporary

Activity data in U.S. decelerated around the turn of the year. A weak non-farm payroll figure in

December was followed by a sequence of poor economic data releases. The ISM survey of supply

management professionals declined to 51.3 in January from 56.5 in December. And the labor market

disappointed again in January, with nonfarm payrolls increasing by only 113,000 jobs, below the

market consensus forecast of 180,000 jobs. Indeed, our surprise index for the U.S. activity data

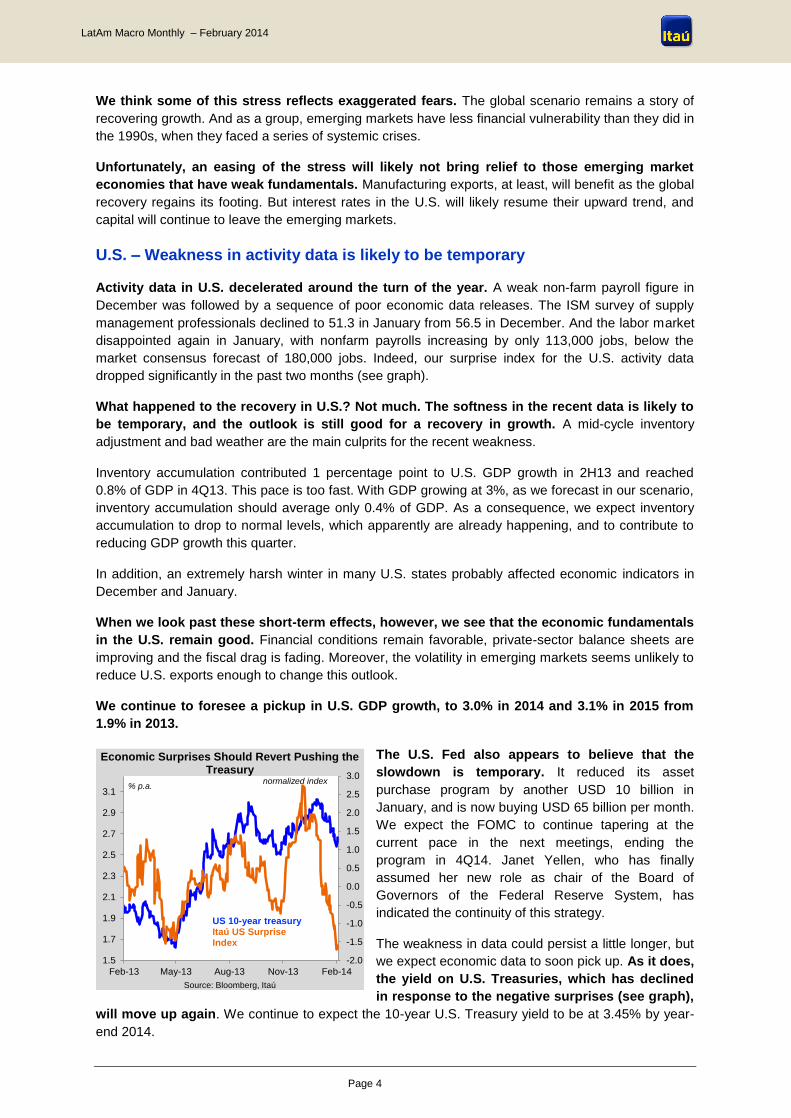

dropped significantly in the past two months (see graph).

What happened to the recovery in U.S.? Not much. The softness in the recent data is likely to

be temporary, and the outlook is still good for a recovery in growth. A mid-cycle inventory

adjustment and bad weather are the main culprits for the recent weakness.

Inventory accumulation contributed 1 percentage point to U.S. GDP growth in 2H13 and reached

0.8% of GDP in 4Q13. This pace is too fast. With GDP growing at 3%, as we forecast in our scenario,

inventory accumulation should average only 0.4% of GDP. As a consequence, we expect inventory

accumulation to drop to normal levels, which apparently are already happening, and to contribute to

reducing GDP growth this quarter.

In addition, an extremely harsh winter in many U.S. states probably affected economic indicators in

December and January.

When we look past these short-term effects, however, we see that the economic fundamentals

in the U.S. remain good. Financial conditions remain favorable, private-sector balance sheets are

improving and the fiscal drag is fading. Moreover, the volatility in emerging markets seems unlikely to

reduce U.S. exports enough to change this outlook.

We continue to foresee a pickup in U.S. GDP growth, to 3.0% in 2014 and 3.1% in 2015 from

1.9% in 2013.

The U.S. Fed also appears to believe that the

slowdown is temporary. It reduced its asset

purchase program by another USD 10 billion in

January, and is now buying USD 65 billion per month.

We expect the FOMC to continue tapering at the

current pace in the next meetings, ending the

program in 4Q14. Janet Yellen, who has finally

assumed her new role as chair of the Board of

Governors of the Federal Reserve System, has

indicated the continuity of this strategy.

The weakness in data could persist a little longer, but

we expect economic data to soon pick up. As it does,

the yield on U.S. Treasuries, which has declined

in response to the negative surprises (see graph),

will move up again. We continue to expect the 10-year U.S. Treasury yield to be at 3.45% by year-

end 2014.

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1.5

1.7

1.9

2.1

2.3

2.5

2.7

2.9

3.1

Feb-13 May-13 Aug-13 Nov-13 Feb-14

Source: Bloomberg, Itaú

US 10-year treasuryItaú US Surprise Index

% p.a.normalized index

Economic Surprises Should Revert Pushing the Treasury

Page 5

LatAm Macro Monthly – February 2014

China – Risks come to the forefront, but we still see a gradual moderation

The NBS manufacturing PMI declined to 50.5 in January from 51.0 in December, renewing

concerns over a pronounced slowdown in China. The fall followed disappointing activity data in

December, when industrial production growth slowed to 9.7% yoy from 10.0% in November.

A near-default of a “shadow banking” product

added to concerns over China’s economic health.

Total credit in China has increased from 120% of

GDP in 2008 to 185% of GDP last year (see graph).

Most of the rise has occurred outside the banking

system, in products ranging from traditional capital

market securities like corporate bonds to special

financing vehicles, usually seen as opaque and

labeled “shadow banking”. Combined, these products

now account for 32% of the outstanding credit in the

economy, compared with 17% in 2008 (see graph).

Their rapid growth, together with the investment boom

in China, has sparked fears of a credit meltdown. In

January, a USD 500 million trust fund, which had

made loans to a mining company, nearly defaulted on its investors. A last-minute rescue by the

combined forces of a local government, the bank responsible for marketing the fund and the trust

company that created the product averted a default. But the episode touched a nerve among

investors who worry about credit quality in China.

Despite the risks, we continue to expect a gradual moderation and no hard landing.

A moderate slowdown in growth, after the strong 7.8% pace seen in 2H13, seems unavoidable

as the economy shifts to a more sustainable mix of growth sources, with less investment and more

consumption. The People’s Bank of China also appears willing to allow higher interest rates and push

for some deleveraging in the financial system, putting additional downward pressure on activity.

But January data from China is noisy and could be distorted to the downside. The Chinese

Lunar New Year holidays came early this year and likely slowed down activity in the month of

January. The latest PMI drop could be reflecting this effect. We don’t think that one should read too

much into the data for this period. We will only have a reliable picture of activity trends around mid-

March, when the main activity data for January and February will be released.

Moreover, Chinese policy-makers are sending a message of stable policies and growth. We

believe that they will be able to manage a smooth transition in China’s economy. If a deeper

slowdown is in fact occurring, there is room for some small and localized stimulus measures, as

inflation remains well behaved.

In addition, we don’t expect a major crisis in China’s financial sector. The risk of a Chinese

financial crisis is probably overestimated. Trust companies, where a large part of this risk lies,

manage about RMB 10 trillion (USD 1.65 trillion). But half of that is made up of equity investments,

whose investors likely understand the risks. The other half is trust loans, and this is where most of the

potential issues are. Yet it seems to us that any eventual problems would not be likely to create a

liquidity crisis that could have a domino effect, mainly because there is little cross-participation in the

trust industry. Given the low presence of foreign investors and the fiscal capacity of China’s

government, a state-sponsored solution might become available without much stress. In the end, the

main issue is credit quality.

We continue to see China’s GDP growth slowing gradually, to 7.5% in 2014 and 7.3% in 2015

from the 7.7% posted in 2013.

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

2004200520062007200820092010201120122013

Credit Stock has been Growing Mainly Outside of Traditional Bank Loans

Source: PBoC, Itaú

Bank loans in local currency"Shadow banking"

in % of GDP

Page 6

LatAm Macro Monthly – February 2014

Emerging Markets – A full-blown crisis is unlikely, but there will be continued

pressure on countries with weak fundamentals

Emerging markets have had a rough ride over the past month. The sharp exchange rate

depreciation in Argentina, emergency interest rates hikes in Turkey, political turmoil in Ukraine and

contagion everywhere recalled the emerging-market crises of past decades.

Weaker-than-expected activity numbers from China and the U.S. contributed to the stress.

What started last year as a reaction to changes in monetary policy in the U.S. later took on

new dimensions. The correlation between the yield on U.S. Treasuries and emerging markets

currencies broke down. Last year, a rise in the former made the latter depreciate. This time around,

emerging-market exchange rates depreciated while yields on Treasuries declined, in a typical flight-

to-quality movement. Even developing countries with solid fundamentals suffered.

We think that the fears of a full-blown crisis in the emerging markets are unjustified. These

economies are less financially vulnerable than they were in the 1990s (for details, see our LatAm

Macro Monthly from July 2013). In addition, in our view, to worry about low growth and higher interest

rates in the United States at the same time is inconsistent.

As concerns over the global recovery ease, differentiation will return, with countries that have

weak fundamentals continuing to be under pressure.

We expect the real to depreciate further. The recent exchange rate depreciations in Chile, Colombia

and Mexico might partly revert. We believe that their currencies will end 2014 stronger than they are

now. In Peru – a partially dollarized economy – the central bank is intervening aggressively to protect

the PEN from volatility, so its exchange rate remains stronger than our year-end forecast.

The recent turmoil might prompt some central banks to be more cautious about further easing.

Hence, we no longer expect Colombia and Peru to reduce their policy rates. However, we continue to

see room for easing in economies where inflation and current-account deficits are not a concern.

Chile can further cut rates, for example, while Mexico can postpone rate hikes.

In Brazil, we continue to believe that the tightening cycle is close to an end, but we now see slightly

higher interest rates at the end of 2014 (11%, up from 10.75% previously)

Apart from external shocks, idiosyncratic issues will continue to matter and may contribute to

negative sentiment toward the whole emerging-market asset class. In Argentina, the government

allowed sharp exchange-rate depreciation after it became clear that currency controls were failing to

address the overvaluation of the ARS. However, the depreciation has not been accompanied with a

proper monetary response. The country needs much higher interest rates to encourage USD inflows.

In the absence of such an adjustment, pressure on reserves has continued even after the

depreciation. We expect a further weakening and a significant increase in interest rates over the next

few months. During this period, Argentina could once again create noise in the markets.

Commodities – Weather risks

The Itaú Commodity Index (ICI) rose by 1.7% from its recent low (January 9) as weather

conditions pushed up agricultural prices (+4.1%) and energy prices (+3.4%), and despite a new

drop in metal prices (-4.0%). Agricultural prices were affected by strong export sales for grains and

unfavorable weather for production (a frigid winter in the U.S., as mentioned in our last report and a

dry spell in Brazil). Energy prices were up due to the cold weather in North America and to regional

improvements in the oil transportation infrastructure, which increases the outflow capacity for “WTI

oil”. Nevertheless, we are leaving our 2014 year-end forecasts unchanged (see below).

Page 7

LatAm Macro Monthly – February 2014

Agricultural prices rose recently due to a drought in Brazil, which also adds uncertainty to the

scenario, and to very strong external demand indicators for corn and soybeans. The former

poses a significant upside risk for coffee and sugar prices, but should not affect soybean or corn

prices. Regarding soybeans, the negative impact on the Brazilian crop is being offset by more rain in

Argentina. For corn, the drought is delaying the second-crop planting, increasing the risk of ground

frost affecting crops later in the year. However, we expect only domestic prices to be affected, given

the strong global surplus in corn. All things considered, we are maintaining our year-end price

forecasts for agricultural commodities, but we see an upside bias to our price estimates for sugar

(USD 0.184/lb) and coffee (USD 1.50/lb).

Metal prices have fallen amid renewed concerns about the global economy, concerns which,

as discussed above, we expect to be temporary. The ICI-metals has fallen by 7.6% year-to-date,

driven down by lower prices for iron ore (-11.4%), aluminum (-5.5%) and copper (-3.6%). The

renewed worries about China and other emerging markets and the weak data from the U.S. explain

this poor performance. However, we expect the China concerns to fade and see the U.S. data

weakness as temporary. Hence, we are maintaining our year-end forecasts for metal prices, which

imply a less steep drop (-2.4%) from current levels over the remainder of the year.

Finally, the environment for WTI prices is more constructive. WTI oil prices have risen by 8.2%

since January 9, driven by the combination of marginally lower oil production in the U.S. and

increased outflow capacity from the Cushing region of in the central United States. Meanwhile, Brent

prices continue to slide on the prospect of a looser balance in 2014 and lower geopolitical risk.

Hence, the shrinking in the discount of WTI to Brent prices is consistent with the fundamentals and is

likely to persist throughout the year, as we already expected. We are maintaining our year-end

forecasts for both Brent (USD 105/bbl) and WTI (USD 101/bbl) prices.

Forecasts: World Economy

GDP Growth

World GDP growth - % -0.4 5.2 3.9 3.2 2.8 3.5 3.5

USA - % -2.8 2.5 1.8 2.8 1.9 3.0 3.1

Euro Area - % -4.4 2.0 1.5 -0.6 -0.4 0.9 1.3

Japan - % -5.5 4.7 -0.6 2.0 1.8 1.5 1.1

China - % 9.2 10.4 9.3 7.8 7.7 7.5 7.3

Interest rates and currencies

Fed Funds - % 0.1 0.2 0.1 0.2 0.1 0.1 1.3

USD/EUR - eop 1.43 1.34 1.30 1.32 1.37 1.30 1.30

YEN/USD - eop 92.1 81.5 77.6 86.3 103.6 110.0 110.0

DXY Index* - eop 76.8 80.0 79.6 79.8 80.3 83.8 83.8

2015F2013F 2014F2009 2010 2011 2012

Source: Central Banks, IMF, Haver and Itaú. * The DXY is a leading benchmark for the international value of the U.S. dollar, measuring its performance against a basket of currencies that includes the euro, yen, pound, Canadian dollar, Swiss franc and Swedish krona.

Page 8

LatAm Macro Monthly – February 2014

Brazil

Growth Without Energy

• Brazil’s economic growth has lost momentum in recent months. Weakening investment and

inventory adjustments suggest slower-than-expected economic expansion in 4Q13 and sluggish

growth in 1Q14. Scarce rainfall and higher electricity prices are risks. The impact on growth

expectations will depend on the evolution of weather conditions over the year. The situation in

Argentina is another drag on the Brazilian economy. We have lowered our forecast for GDP growth in

2014 to 1.4% from 1.9%, and to 2.0% from 2.2% in 2015.

• An expected decline in exports to Argentina prompted us to lower our forecast for the 2014 trade

balance to USD 6 billion from USD 7 billion, which in turn contributed to a revision in our forecast for

the 2014 current account deficit, to 3.6% of GDP from 3.5%. Our year-end forecasts for the exchange

rate remain at 2.55 reais to the dollar for both 2014 and 2015.

• We have raised our year-end 2014 estimate for the Selic benchmark interest rate to 11.00% from

10.75%, incorporating our projection of two 25-bp hikes in February and April. Our forecast for 2015

has been revised upward to 12.00% from 11.50%. Consequently, we have reduced our 2015

estimate for the consumer price index IPCA to 6.0% from 6.2%. Our IPCA forecast for 2014 remains

unchanged, at 6.2%.

• Our estimate for the 2014 primary budget surplus is still at 1.3% of GDP, but the breakdown has

changed. We now expect faster growth in expenses, smaller tax revenues and larger extraordinary

revenues.

Drop in investment and industrial production leads to lower growth forecasts

Lower investment and inventory adjustments

caused a widespread decline in industrial

production in December. Fundamentals less

favorable to investment – higher interest rates and

low business confidence levels, for instance –

affected the production of capital goods in December

(-11.6% mom/sa). Inventory adjustments also

weighed on several sectors in late 2013. Industrial

output slid by 3.5% mom/sa in December, marking

the sharpest drop since January 2009. Following this

retreat in production, inventories became more

balanced in many sectors, but there are still signs of

imbalances in some segments. Furthermore, demand

indicators related to capital goods continue to show

weakness, and growth in consumer spending is likely

to decelerate. Hence, despite signs of a strong

rebound in January, industrial production is still

slowing down.

Based on fundamentals and current data, we have

lowered our forecast for GDP growth in 2014 to

1.4% from 1.9%. We have lowered our forecast for

4Q13 GDP growth to 0.4% from 0.6% to reflect the

impact of the weak industrial production in December

(our growth estimate for 2013 is unchanged, at 2.2%).

This performance reduced the carryover into 2014.

Even if we assume that there is a strong recovery in

80

85

90

95

100

105

110

115

120

Dec-07 Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13

Investment Retreats

Source: Itaú

Gross fixed capital formation index

index, sa,

2008=100

2,0

1,21,0 1,0

0,8

0,4

0,0 0,1 0,1 0,2

0,6

0,9

0,0

1,8

-0,5

0,4

0,0

0,50,6 0,6

-2

-1

0

1

2

3

2010.I 2010.IV 2011.III 2012.II 2013.I 2013.IV 2014.III

Source: IBGE, Itaú

%, QoQ

GDP Grows at a Moderate Pace

Page 9

LatAm Macro Monthly – February 2014

January, industrial activity in 1Q14 is likely to be weaker than initially anticipated. We have thus

lowered our forecast for GDP growth in 1Q14 to 0% from 0.4%. These drivers have led to a reduction

in our forecast for GDP growth in 2014, to 1.4% from 1.9%. We have changed our GDP forecast for

2015 to 2.0% from 2.2% due to our upward revision for the Selic rate.

Slowing economic activity in Argentina contributed to lower domestic growth. A deteriorating

scenario in Argentina may lead to a 15-pp decline in the growth rate for Brazilian exports to

Argentina, according to our calculations. Through the trade channel, a reduction of such magnitude

would have an impact of -0.2 pp on Brazil’s GDP growth in 2014. In our view, the weakness in the

Argentine economy, in particular the reduction in demand for manufactured products, will contribute

to preventing industrial production from sustaining the expected improvement in the January figures.

The slowdown in exports, particularly shipments of motor vehicles and auto parts, will likely contribute

to weaker performance in the industrial sector in 1Q14. Also, the deceleration in Argentina may be

even more intense than anticipated, and financial conditions in Brazil may also be affected.

The impact of higher electricity costs on the economic activity scenario for 2014 will depend

on the evolution of weather conditions. The increase in electricity costs in the spot market will

have little impact on economic activity this year if the rainfall picks up to close to its historical average

in the next months, as we consider in our base case scenario. However, even in this scenario, it could

have more intense effects over shorter periods of time (such as a month or a quarter). The hike in

electricity costs in the spot market may lead to a reduction in output in some manufacturing sectors –

either because production has become more expensive or because the return from trading contracted

energy has exceeded the return obtained by producing goods.

In the credit market, indicators showed a recovery in December. In the final month of 2013, the

daily average of new non-earmarked loans rose by 4.6% mom/sa in real terms, with gains of 7.8% in

consumer loans and 3.3% in corporate loans. Overall delinquency declined again, reaching 3%,

although delinquency in non-earmarked consumer loans increased slightly, to 6.7% from 6.6%. Both

interest rates and spreads slid. Total outstanding loans kept widening as a share of GDP, reaching

56.5%. The market share of state-owned banks also continued to increase, to 51.2% from 50.9%.

However, annual growth in the balances of state-owned banks has been decelerating since July.

Reservoirs: Unfavorable weather points to higher usage of thermal power

plants in 2014

Hot and dry weather in early 2014 has reduced generation by hydropower plants and

increased electricity usage. Hydroelectric reservoirs started 2014 at 42.8% of capacity,1 higher than

in early 2013 (30.5%) but lower than the average of the past 10 years (52.6%). Hence, the system

had a wider safety margin than last year. Some thermal power plants with higher operational costs

had been turned off during the second half of 2013 as reservoir levels got closer to seasonal norms.

From January to mid-February, however, temperatures were much higher than the seasonal pattern

and rainfall was far below normal (50% of the historical average), affecting the energy balance

through two channels: i) less generation by hydroelectric plants and ii) higher electricity consumption.

This year to date, hydropower generation is considerably below potential: natural affluent energy

(NAE) was 70.4% of its long-term average (LTA, or the amount of energy generated under historical

hydrological conditions) in January and stands at only 41.2% of LTA so far in February. In addition,

unseasonably warm temperatures drove average electricity consumption to a 10.6% yoy increase in

January, up from approximately 3% yoy in 4Q13.

1 Aggregate level of the four basins in the National Integrated System.

Page 10

LatAm Macro Monthly – February 2014

Reservoirs have fallen to lower levels than in

2013. With low hydropower generation and higher

demand, reservoir levels are falling, counter to the

normal seasonal pattern of accumulation throughout

the rainy period (December through May). Hence,

thermal power plants with high operational costs are

once again being used, and the debate over possible

rationing is heating up again.

Thermal power usage is up again and will likely

remain high. As noted above, low reservoir levels

have pushed thermal plant usage back up. Capacity

has increased from last year, so that the system’s

capacity to offset low hydro generation is higher, but

the capacity comes at a hefty cost. Specialists expect

normalization of weather conditions in late February. Rainfall following the historical pattern starting in

March would reduce the risk of rationing. However, even with possible normalization of weather

conditions ahead, the dry weather early in the year will likely dampen hydropower generation until

April. Hence, reservoir levels will probably rise slowly over nearly the entire rainy season, leading to

reservoirs ending the period at low levels. An intense usage of thermal plants (higher than in 2013)

will therefore likely be needed throughout the year.

Higher usage of thermal plants comes with higher

costs. A more intensive usage of thermal power

plants (for instance, average generation 3 GW above

its 2013 level) would raise the cost paid to power

distributors (by approximately 20 billion reais, in this

example), which may be offset by government

subsidies or tariff hikes. The government budget for

2014 already sets aside 9 billion reais for the Energy

Development Account (CDE), but this amount will

likely not be enough to cover the additional costs. The

government’s current message is that it intends to

minimize tariff hikes by entirely or partly covering the

extra costs. We will thus incorporate into our scenario

additional fiscal costs to subsidize the CDE.

Favorable external factors hold back depreciation in the real

We maintain our forecasts for a year-end exchange rate of 2.55 reais to the dollar in both 2014

and 2015. This year, the real weakened less than most of its peer emerging-market currencies,

thanks to Brazil’s more restrictive monetary policy, its USD auctions in the futures market and

external fundamentals, especially negative net external debt. These favorable factors – Brazil’s large

reserves and its foreign debt profile (low and predominantly private debt, with long-term maturities

and fixed rates) – should curb the contagion from the turmoil in other emerging markets. Another

factor supporting our unchanged year-end forecasts for the exchange rate is our view that recent

turmoil in emerging economies will be temporary.

For 2013, the current account deficit was 3.7% of GDP. The December reading was marked by a

continuation of the gradual decline in the service deficit (USD 4.2 billion) and large remittances of

profits, interest and dividends (USD 7.5 billion). In the capital account, foreign direct investment

totaled USD 6.5 billion in December and USD 64 billion (2.9% of GDP) in 2013, in line with USD 65

billion in the previous year. However, the breakdown of inflows in 2013 was less benign than in 2012,

as only 65% of inflows involved equity capital transactions, compared with 81% in 2012.

11.7

10.0

11.310.3 9.9 9.7

13.4

0

3

6

9

12

15

18

Jan-13 Apr-13 Jul-13 Oct-13 Jan-14

Source: ONS, taú

Avg monthly generation2013 average

GWmed

Thermal Power Usage is Up Again in 2014

Un

til

Fe

b 1

0

0

10

20

30

40

50

60

70

80

90

100

Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov

Source: ONS, Itaú

2012Avg 2000-201220132014

% of agregated capacity

Reservoirs Below 2013 Levels

Page 11

LatAm Macro Monthly – February 2014

The economic slowdown and sharp currency

depreciation in Argentina will likely have negative

consequences for Brazil’s trade balance.

Argentina is the main destination for manufactured

products made in Brazil, particularly motor vehicles

and auto parts. Although exchange rate depreciation

may be partly offset by customs controls, Argentina’s

importance as a trade partner and the magnitude of

the expected slowdown there (we estimate a

contraction of 3% in GDP) mean that this move will

almost certainly affect Brazil’s trade balance. We

estimate the loss at USD 1 billion, so that the

expected surplus for 2014 is now USD 6 billion (down

from USD 7 billion previously). We have changed our

forecast for the 2014 current account deficit to 3.6% of GDP from 3.5% due to a lower trade balance

and GDP growth expectations.

The retreat in inflation early in the year is likely to be temporary

Brazil’s consumer price index, the IPCA, climbed by 0.55% in January, below our estimate

(0.60%) and that of the market consensus (median of 0.61%). The result was also lower than one

year earlier (0.86%), slowing the year-over-year change to 5.59% from 5.91% as of the end of 2013.

In our view, a significant portion of the slowdown in inflation in January is related to

temporary factors, such as cuts in airfares and lower prices for some fresh fruits and

vegetables. Airfares fell by 15.9% in January, as opposed to a 5.1% gain one year earlier. Likewise,

the food component comprising tubercles, roots and legumes slid by 0.9% in January 2014 after

having risen by nearly 20% in January 2013. We would highlight lower prices for tomatoes (-10.6%)

and potatoes (-4.5%), in contrast to the sharp increases early last year (26% and 21%, respectively).

-20%

-10%

0%

10%

20%

30%

40%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Unusual Low Airfares

Five years avg. (+- 1 standard deviation)2014 (Forecast to February)

Source: IBGE, Itaú

MoM prices var. (IPCA)

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Source: IBGE, Itaú

Five years avg. (+- 1 standard deviation)2014 (Forecast to February)

MoM prices var. (IPCA)

Tubercles, Roots and Legumes Falling

Our assessment that the early-year drop in inflation has been driven by temporary factors has

led us to keep our 2014 forecast for the IPCA at 6.2%. Our preliminary forecast for February

now stands at 0.67%, slightly higher than February 2013 (0.60%). For 1Q14, we expect IPCA

inflation of 1.83%, compared with 1.94% in 1Q13. On one hand, there will be no repetition of the cut

in electricity tariffs of early last year (which lowered the IPCA by 0.60 pp). On the other hand, the

price behavior of food should partly offset this effect, with food prices rising by 2.1% in 1Q14,

according to our estimates, compared with 4.6% in 1Q13. Transportation costs should also provide

some inflation relief in 1Q14, given that fuel prices, which were adjusted early last year, are unlikely to

rise now. In the education component, preliminary information points to slightly larger increases in

Iron Ore5%

Others consumption

goods8%

Others intermediate

goods29%

Fuel3%

Cars24%

Auto parts17%

Heavy Vehicles

9%

Others capital goods

6%

Exports to Argentina* Concentrated in Manufacturing Products

*2013 data Source: Funcex

Page 12

LatAm Macro Monthly – February 2014

tuitions than last year at this time, particularly in college-level courses (the sub-item with the greatest

weight in the IPCA). Slower economic growth this year so far has not affected our inflation forecasts

for the full year of 2014 because the unemployment rate has not shown significant changes.

We have maintained our 2014 forecast for market-set prices and slightly raised our estimate

for regulated prices. We still forecast 6.7% inflation for market-set prices (vs. 7.3% in 2013), with

smaller increases in food and service prices. We expect a 6% hike in food consumed at home (vs.

7.6% in 2013) and an 8.2% increase in service costs (vs. 8.7% in 2013). These segments account for

two-thirds of the weight of market-set prices and slightly more than half of the IPCA weight.

Regarding regulated prices, we adjusted our estimate to 4.7% from 4.5% (vs. 1.5% in 2013),

incorporating a 9% increase in urban bus fares in Rio de Janeiro.

Our IPCA forecast for 2015 has been revised downward to 6.0% from 6.2%, due to an upward

revision in our estimate for the benchmark Selic rate and downward revision in our GDP forecasts.

Our forecast for the general price index IGP-M still points to a 5.8% increase this year, vs.

5.5% last year. We estimate that producer prices (IPA-M) will climb by 5.5% in 2014, with industrial

prices rising by 6% and agricultural prices rising by 4%. Despite the pressure arising from a weaker

exchange rate, the hike in the IPA should be cushioned by the expected decline in prices for

soybeans (grain and meal) and iron ore. As for the other components in the IGP-M, we expect gains

of 6% in the IPC-M and 7.7% in the INCC-M.

Fiscal accounts: we maintain our forecast for the primary budget surplus in

2014, but with a different breakdown

The primary balance for the consolidated public sector was 10.4 billion reais for December

2013, or 2.5% of monthly GDP. This reading was in line with the 2.4% average for the month of

December in the post-crisis period (2009-2012). The conventional consolidated primary balance (not

adjusted for accounting or economic cycles) for 2013 was 1.9% of GDP (91 billion reais), down from

2.4% of GDP (105 billion reais) for 2012.

Although the central government met its fiscal target for 2013 (73 billion reais, or 1.5% of

GDP), the fiscal performance of the public sector last year was the worst since the beginning

of the historical series (2002). There was deterioration in every sector of government. Overall, the

data point to an expansionary fiscal stance. The recurring consolidated primary surplus (which

excludes atypical revenues and expenses2) over 12 months was 1.0% of GDP in 2013, also one of

the lowest results in the historical series (2012: 1.8%).

Despite the effect of tax breaks, which caused federal tax revenues to slide by 0.3 pp from

2012 (to 20.9% of GDP), the hike in total federal spending (to 18.8% of GDP from 18.3%) was

the main driver of the decline in the fiscal surplus. The increase in central government expenses

came largely from transfers and administrative expenses, showing that incentives for aggregate

investment are still low. Capital expenditures by the central government (including spending on the

low-income housing subsidy program known as Minha Casa Minha Vida) receded to 1.3% of GDP in

2013 from 1.4% in 2012.

In 2014, the fiscal situation will be complicated by a tougher scenario in terms of revenues,

reflecting the likelihood of slower growth in economic activity this year and the adverse base-

effect created by high extraordinary revenues in 2013. Regarding spending, several constraints

on an adjustment in federal expenses in the very short term (for instance, tied expenses) are also

likely to weigh on fiscal performance this year.

2 In 2013, our calculation excluded revenues from the tax amnesty program Refis (0.5% of GDP), from the concession of the

Libra oil field (0.3%) and from the Refis program for São Paulo state (0.1%).

Page 13

LatAm Macro Monthly – February 2014

We are leaving our forecast for the 2014 consolidated primary budget surplus unchanged at

1.3% of GDP (central government: 1.1%), but we expect a slightly different breakdown relative

to our previous scenario. We have lowered our estimate for 2014 federal tax revenues by 0.2% of

GDP, to 21.0%, due to our expectation of slower economic activity in 2014. We have lifted our

forecast for federal expenses by around 0.2 pp, to 19.3%, to include larger subsidies for the electricity

sector (through injections in the Energy Development Account, or CDE, totaling 15 billion reais) and

larger administrative outlays. Our scenario also considers the possibility that part of the costs related

to the higher utilization of electricity from thermal plants will be deferred through public credit

instruments (i.e., quasi-fiscal subsidies).

On the other hand, we have also incorporated into our forecast for 2014 a higher volume of

non-tax revenues (atypical revenues included), which we now forecast at 3.4% of GDP (up

from 3.1% previously). We maintain our forecast for the primary balance of regional governments of

0.2% of GDP (2013: 0.3%). These numbers are consistent with a recurring primary balance coming in

slightly below its 2013 reading (1.0% of GDP). Despite our expectation of a worsening fiscal effort in

2014, we think the government will signal greater caution in fiscal policy, as there will be less room to

implement fiscal stimulus measures (given the scarce international liquidity and the threat of a

sovereign-rating downgrade).

The government may announce a considerable

adjustment when the budget-freezing decree

known as contingenciamento is published

(probably in the next few days). The spending

freeze could amount to 40 billion reals, or 3.9% of

total expenses set out by the budget law for 2014. (In

2013, the contingenciamento amounted to 28 billion

reals, or 2.9% of expenditures written in the budget

law for that year). However, problems during the year

could lead to a re-estimation (and unfreezing) of

spending in late 2014.

Copom: external scenario suggests a longer monetary policy cycle, while

domestic scenario suggests a slower tightening pace

The external scenario may require a more conservative Brazilian monetary policy. The recovery

in the U.S. economy and negative sentiment toward emerging economies have put pressure on the

exchange rate, demanding more conservative monetary policy, particularly in countries where

inflation is relatively high, as in Brazil. This situation may drive Brazil’s monetary policy committee

(Copom) to hike the benchmark rate by another 50 bps at this month’s meeting.

On the domestic front, however, recent data indicate less pressure on inflation and lower

growth. The IPCA reading in January and the result for industrial production in December indicate

that there is less pressure on inflation and that growth remains weak. In recent weeks, the central

bank’s Focus survey showed a decline in average market forecasts for GDP and IPCA in 2014.

These trends favor a reduction in the pace of interest rate increases.

This difference between the external and domestic scenarios had been spotted by the Copom

already. In the minutes of its last meeting, the Copom noted that it sees both more strength and more

volatility in the external scenario, as well as a domestic situation that is more favorable in terms of

inflation. This more favorable domestic situation will likely be read by the Copom as being a

consequence of the monetary tightening cycle started in April 2013, which is relieving the inflationary

pressures in the economy.

0%

1%

2%

3%

4%

5%

6%

7%

-

10

20

30

40

50

60

2002 2004 2006 2008 2010 2012 2014E

Source: Federal Budget Secretariat, Itaú

Billion reals% expenses inthe budget law

Government Budget-Freezing

Page 14

LatAm Macro Monthly – February 2014

We maintain our forecast for a 25-bp increase in February, but we now expect the rate-hiking

cycle to be extended through April. As the volatility in external markets has receded in recent

weeks, we believe that domestic factors will prevail in the decisions by Copom members. Accordingly,

we maintain our call that the Copom will slow the pace of rate increases to 25 bps at its February

meeting. But we now believe that the Copom will also opt for an additional increase in April, in

response to the more complex external environment. Therefore, we have revised our forecast for the

year-end Selic rate to 11.00% from 10.75%.

However, if the external scenario deteriorates further before the end of the month, putting

pressure on the exchange rate, the Copom may decide to keep the tightening pace at 50 bps

at its next meeting.

We now expect higher interest rates in 2015: 12.00%. In order to ensure that inflation remains

around current levels, we believe that the Copom will hike rates again in 2015. We anticipate a hiking

cycle of 100 bps in the first half of the year pushing the Selic rate to 12.00%. In our previous forecast,

we expected a smaller increase in 2015 that would drive the Selic to 11.50%.

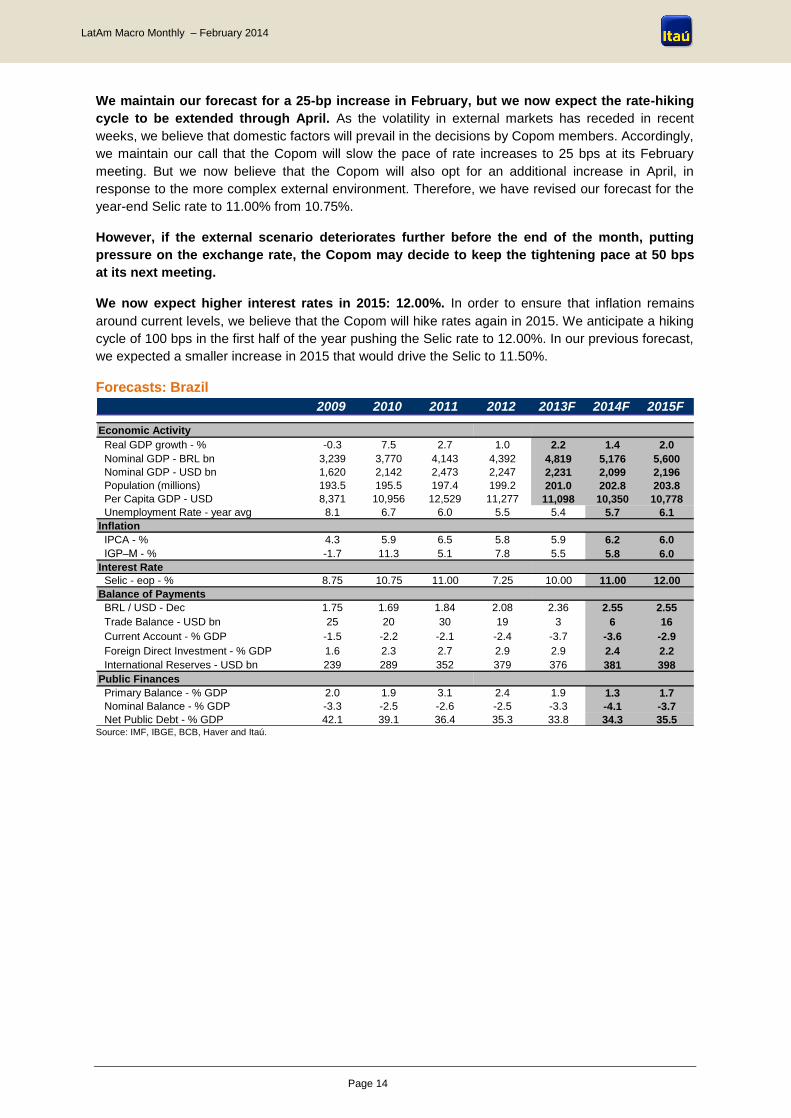

Forecasts: Brazil

Economic Activity

Real GDP growth - % -0.3 7.5 2.7 1.0 2.2 1.4 2.0

Nominal GDP - BRL bn 3,239 3,770 4,143 4,392 4,819 5,176 5,600

Nominal GDP - USD bn 1,620 2,142 2,473 2,247 2,231 2,099 2,196

Population (millions) 193.5 195.5 197.4 199.2 201.0 202.8 203.8

Per Capita GDP - USD 8,371 10,956 12,529 11,277 11,098 10,350 10,778

Unemployment Rate - year avg 8.1 6.7 6.0 5.5 5.4 5.7 6.1

Inflation

IPCA - % 4.3 5.9 6.5 5.8 5.9 6.2 6.0

IGP–M - % -1.7 11.3 5.1 7.8 5.5 5.8 6.0

Interest Rate

Selic - eop - % 8.75 10.75 11.00 7.25 10.00 11.00 12.00

Balance of Payments

BRL / USD - Dec 1.75 1.69 1.84 2.08 2.36 2.55 2.55

Trade Balance - USD bn 25 20 30 19 3 6 16

Current Account - % GDP -1.5 -2.2 -2.1 -2.4 -3.7 -3.6 -2.9

Foreign Direct Investment - % GDP 1.6 2.3 2.7 2.9 2.9 2.4 2.2

International Reserves - USD bn 239 289 352 379 376 381 398

Public Finances

Primary Balance - % GDP 2.0 1.9 3.1 2.4 1.9 1.3 1.7

Nominal Balance - % GDP -3.3 -2.5 -2.6 -2.5 -3.3 -4.1 -3.7

Net Public Debt - % GDP 42.1 39.1 36.4 35.3 33.8 34.3 35.5

2015F2009 2010 2011 2012 2013F 2014F

Source: IMF, IBGE, BCB, Haver and Itaú.

(

Page 15

LatAm Macro Monthly – February 2014

Mexico

A Bumpy Recovery

• Mexico’s economy weakened in 4Q13. We reduced our growth forecast for this year to 3.3% (from

3.6% in our previous scenario). For 2015, we see a 3.8% expansion.

• Inflation spiked in January due to tax hikes. Core inflation continues to be limited. We see inflation

at 3.7% by the end of this year and at 3.2% in 2015.

• Global market volatility increased, so the peso weakened against the dollar. However, the

Mexican peso is outperforming other currencies of the region. Considering the better prospects for

FDI (due to structural reforms) and the exposure of the economy to the U.S., the peso will likely

continue to outperform. We see the peso at 12.8 to the dollar by the end of this year and by the end

of 2015.

• The central bank left the policy rate unchanged in January, as widely expected. In the press

statement, the board said that the balance of risks for inflation worsened, but members didn’t

introduce a tightening bias. We see rate hikes only in 2015.

The economy slows during 4Q13

Activity indicators available for 4Q13 show that

the recovery seen in the previous quarter was

short-lived. The IGAE (monthly proxy for GDP) fell

0.04% year over year in November, surprising

expectations on the downside. Sequentially, the

index slowed to 0.8% qoq/saar (from 1.3% in October

and 2.8% in September), in spite of a 0.39% gain

between October and November.

External demand weakened during the last

quarter of 2013, in spite of the solid U.S. data in

that quarter. Manufacturing exports fell 2.2% from

November to December, contracting 1% qoq/saar,

after a 9.5% increase in 3Q13. Auto exports were

down by 12% qoq/saar, while non-auto exports slowed to 4.5% qoq/saar (8.7% in 3Q13).

The most recent consumption-related data was mixed. Retail sales improved markedly in

November, but it is unclear how important the “el buen fin” (the Mexican version of “Black Friday”)

was for the number. From October to November, retail sales were up 3.0%, following a 0.7%

increase. On the other hand, in January, consumer confidence retreated 6.2% from the previous

month, reaching its lowest level since early 2010, when Mexico was getting out of the recession.

Imports of consumer goods (excluding fuels) fell by 0.5% from November to December (-9.9%

qoq/saar) and domestic vehicle sales also weakened in the same month. While it is true that the labor

market improved during the last quarter of the year (according to our own seasonal adjustment,

formal employment increased by 3.4% qoq/saar, lifting the real wage bill by 3.8% qoq/saar), the tax

hikes introduced this year will likely reduce the real disposable income of households (in fact, we read

the drop in confidence in January as a consequence of extra taxes.) In addition, we can’t rule out that

the higher formal employment growth reflects a “formalization effect” induced by the labor reform, as

opposed to an actual expansion of aggregated employment.

On the investment side, there are signs of an incipient recovery. Gross fixed-capital formation

declined by 0.4% month over month in October (the sixth consecutive decline). However, imports of

capital goods gained 2.8% from November to December (5.7% qoq/saar). Construction activity was

Page 16

LatAm Macro Monthly – February 2014

up 1.8% month over month in November. While the trend in construction is still weak, public capital

expenditures (up by 50.7% year over year in nominal terms during 4Q13) will likely help to improve it.

We reduced our growth forecast for this year to 3.3% (from 3.6%). For 2015, our 3.8% forecast

is unchanged. Mexico’s economy is taking longer to recover than we previously expected. Still, we

are confident that the decoupling between Mexico’s exports and the U.S. industry will not last long.

Thus we expect a rebound of the activity in the near term. Apart from higher U.S. growth, the

economy will benefit from a more-expansionary fiscal policy and housing investment is unlikely to be

as weak as it was last year. In 2015, the first meaningful impacts of the reform agenda will add to the

above-trend U.S. growth.

A temporarily high inflation

The tax increases linked to the fiscal package approved last year raised headline inflation

markedly in January. Higher taxes added to the increased prices for non-core items. On a year-

over-year basis, inflation reached 4.48% (from 3.97% in December), above the upper bound of the

target range (2%-4%). The increase was led by higher non-core inflation (8.58% from 7.84%

previously).

However, even after the tax hikes, core inflation is only somewhat above the center of the

target. In the January, core inflation reached 3.21% (from 2.78% in December). Inflation for core

goods increased from 1.89% to 2.93% but continued below 3%. Core service inflation reached 3.47%

(from 3.54%), but we note that the high figure will not last much longer, as it is due to unfavorable

base effects.

We expect inflation to end this year at 3.7%. In 2015, inflation will likely fall to 3.2%. We expect

non-core inflation to fall, while core inflation continues to be limited. Next year, a favorable base effect

associated with the tax hikes this year will help to bring inflation closer to the target center.

The peso weakens against the dollar, but by less than the other currencies of

the region

The trade balance posted a strong USD 12.2 billion (seasonally adjusted and annualized)

surplus during the last quarter of 2013, up from USD 4.2 billion the previous quarter. The

improvement came mostly from the non-oil balance, which rose from a USD 5.3 billion deficit in 3Q13

to a USD 1.0 billion surplus, as weak internal demand more than offset the export slowdown. As a

result, in 2013 the trade deficit was USD 1.0 billion (from a USD 0.1 billion deficit in 2012). This is the

second-best trade balance result since 1996.

The Mexican peso depreciated as global market volatility increased, but it is performing better

than most currencies in the region. As Mexico is the emerging economy that benefits the most

from higher U.S. growth, and the structural reforms raise the FDI prospects for the country, the

Mexican peso will likely continue to outperform. We see the peso at 12.8 to the dollar by the end of

this year and by the end of 2015.

A worse balance of risks for inflation, but no tightening bias

As widely expected, Mexico’s central bank left the policy rate unchanged, at 3.5%, in its first

rate decision of the year. The press statement brought a tone of more concern over inflation,

but it did not introduce a tightening bias. In the press statement, the central bank did not sound

alarmed over growth in spite of the weak activity readings seen recently. In addition, the board

highlighted that the balance of risks for inflation has deteriorated, due to potentially higher global

market volatility and possible second-round effects from the recent increase in headline inflation.

Page 17

LatAm Macro Monthly – February 2014

In the board’s view, Mexico’s economy continues to recover gradually, lifted by external

demand and some recovery in private consumption and public expenditures. The board now

sees a better balance of risks for activity: in the short term, the U.S. will help, while in the medium

term, the structural reforms will benefit both demand and potential growth.

The board linked the increase in inflation seen at the end of 2013 to higher non-core prices

(regulated and non-processed food items) and to the tax hikes in the first half of January. The

board stressed that the increase in January was in line with the central bank’s forecasts, so there is

no sign of second-round effects at this point. In its view, inflation will likely stay above 4% during the

first months of the year but should go back to the target range afterwards. In 2015, inflation is

expected to fall significantly, to the center of the target, as the transitory “shocks” that are now lifting

inflation fade.

In the concluding remarks of the statement, the central bank pledged to carefully monitor the

domestic economy, the potential second-round effects of the increase in headline inflation

and the monetary policy stance of Mexico vis-à-vis the U.S., just as in the previous few

decisions.

We expect Mexico’s central bank to raise rates only in 2015 (together with the Fed), even

though we are expecting a significant rebound of the economy this year. In our view, there is

enough slack in the economy to absorb higher growth without leading to demand-side inflationary

pressures. In addition, Mexico has dealt with many inflationary supply shocks without having to raise

rates to avoid second-round effects, and we do not think that this time will be different. Finally, as

market volatility retreats, Mexico’s central bank will become more comfortable with the inflation

outlook.

Forecasts: Mexico

Economic Activity

Real GDP growth - % -4.7 5.1 4.0 3.9 1.2 3.3 3.8

Nominal GDP - USD bn 895 1,051 1,170 1,184 1,258 1,358 1,470

Population (millions) 112.6 114.3 115.7 117.1 118.2 119.4 120.6

Per Capita GDP - USD 7,947 9,197 10,111 10,112 10,637 11,373 12,192

Unemployment Rate - year avg 5.5 5.4 5.2 5.0 4.9 5.0 5.0

Inflation

CPI - % 3.6 4.4 3.8 3.6 4.0 3.7 3.2

Interest Rate

Monetary Policy Rate - eop - % 4.50 4.50 4.50 4.50 3.50 3.50 4.50

Balance of Payments

MXN / USD - eop 13.06 12.36 13.99 13.01 13.08 12.80 12.80

Trade Balance - USD bn -4.7 -3.0 -1.5 0.0 -1.0 -8.0 -10.0

Current Account - % GDP -0.9 -0.3 -1.0 -1.2 -2.0 -2.2 -2.4

Foreign Direct Investment - % GDP 1.9 2.2 2.0 1.3 2.5 2.5 2.9

International Reserves - USD bn 90.8 113.6 142.5 163.5 176.5 190.0 205.0

Public Finances

Nominal Balance - % GDP -2.3 -2.8 -2.4 -2.6 -2.3 -3.4 -3.0

Net Public Debt - % GDP 28.6 30.1 31.9 33.5 33.7 37.2 40.0

2015F2013F 2014F2009 2010 2011 2012

Source: Central Bank, IMF, INEGI, Haver and Itaú.

Page 18

LatAm Macro Monthly – February 2014

Chile

An Easing Bias Amid Higher Volatility

• Chile’s economy grew weakly during the last quarter of 2013, as investment continues to slow.

Consumption remains strong, supported by a tight labor market. We expect a 4.2% GDP expansion in

2014 and 4.5% in 2015.

• The Chilean peso depreciated due to weaker than expected activity numbers in China and in the

U.S. We see most of the weakness as transitory. Our year-end forecasts remain at 540 pesos to the

dollar in 2014 and 550 in 2015.

• The central bank left the policy rate unchanged in January, but reinforced the easing bias. We

expect a 25-bp rate decrease this month (to 4.25%), but the cut is not a done deal in our view.

Further weakening of the peso before the decision could lead the central bank to wait a bit more

before reducing rates. We expect the easing cycle to end with the policy rate at 4.0%, if global market

permit.

• President-elect Michelle Bachelet announced her cabinet, naming Alberto Arenas as her finance

minister. Arenas helped write Bachelet’s program, which includes plans to raise the corporate tax rate

to finance education reform.

Investment reduces GDP growth

Chile’s economy slowed substantially during the last quarter of 2013, bringing growth for the

full year to 4.0% (from 5.6% in 2012). The IMACEC (monthly proxy for GDP) increased by 2.6%

year over year in December, bringing growth for 4Q13 to 2.7% (from 4.7% the previous quarter).

However, on a sequential basis, the IMACEC gained a robust 0.8% between November and

December, after a 0.5% increase the previous month. Even so, the quarter-over-quarter growth rate

was weak (0.8% annualized). But the carry-over for the first quarter of the year is now favorable.

Investment continues to be the key drag on

growth. Gross fixed investment, which led aggregate

demand over the past few years, slowed to 3.2% year

over year in 3Q13. During the last quarter of 2013,

imports of capital goods fell by a remarkable 32%

year over year, hinting at a further weakness of

investment.

In spite of the weakening economy, the labor

market remains tight, lifting consumption. The

unemployment rate stood at 5.7% in 4Q13, down

from 6.1% one year before. Employment grew by

2.7% year over year, faster than in 3Q13, while

waged employment expanded by 2.3% (2.1% in

3Q13). Retail sales increased 9.4% year over year and 12% qoq/saar in 4Q13. However,

unemployment will likely rise as a result of below-potential growth. In fact, the labor-vacancy index

produced by the central bank – a leading indicator of the labor market – declined 13% year over year

in December.

We expect growth of 4.2% this year and 4.5% in 2014. Higher global growth will likely support

Chile’s economy. Monetary stimulus will help as well.

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

Aug-12 Dec-12 Apr-13 Aug-13 Dec-13

Strong Consumption, In Spite of the Slowdown

Source: INE, Central Bank, Itaú

Retail Sales IMACEC

yoy, 3mma

Page 19

LatAm Macro Monthly – February 2014

Most of the exchange-rate depreciation is temporary

In spite of weaker internal demand growth, the trade surplus is narrowing. Exports contracted

faster than imports in 4Q13 (-8.5% and -7.1% year over year, respectively). As a result, the trade

surplus fell to USD 0.6 billion in the last quarter of 2013, bringing the full-year surplus to USD 2.4

billion (from USD 3.4 billion in 2012).

The Chilean peso depreciated as a result of weaker-than-expected activity numbers in the U.S.

and China. Our scenario for the global economy suggests that most of the weakening is transitory.

Thus, our year-end forecasts for the exchange-rate are unchanged. We expect the peso to end this

year at 540 to the dollar and to be 550 by the end of 2015.

Inflation remains below the target center

Inflation in Chile continues to be tamed in spite of rising non-tradable inflation. Inflation fell to

2.8% in January, from 3.0% in December. The fall was attributable to a reduction in tradable inflation,

dropping to 1.9% from 2.4% in December. On the other hand, non-tradable inflation increased to

4.1% (from 3.8%), reflecting a tight labor market. Excluding food and energy, inflation increased to

2.4% (from 2.1% previously), remaining below the target center.

We expect inflation to end the year at 2.8%. Below-potential growth will likely ease some of the

pressure on non-tradable prices, while the weaker exchange rate could offset this. In 2015, we see

inflation at the 3.0% target.

Rate cuts are likely, but global market volatility is a risk

As expected, the central bank left the policy rate unchanged in January. The press statement

announcing the decision contained a far-more-determined easing bias than the central bank

had been showing up to that time. This highlights the concerns within the board over economic

growth. In the statement’s concluding remarks, the board explicitly said that greater monetary

stimulus will likely be necessary within the next few months to ensure that inflation remains at 3% in

the relevant monetary-policy horizon. The minutes of the meeting later revealed that the decision to

hold rates was unanimous. They also showed that the board unanimously agreed to signal the

stronger easing bias. From the debate over the policy options, it becomes clear that the key reason

for waiting a bit more to resume the easing cycle was the unwillingness to surprise markets, which

would potentially trigger an undesired drop in the interest-rate curve.

The decision to place the easing bias took place before the deterioration in global markets.

However, Enrique Marshall, who is a board member, recently said in an interview with a local

newspaper that he is comfortable with the exchange-rate weakening. According to him, the

depreciation should be seen more as a solution than a problem.

We expect the central bank to lower rates by 25-bps in February. A second 25-bp rate cut

before the end of 2Q14 is also likely if volatility retreats. Most market participants are now

expecting a cut in the next policy decision. Considering the unwillingness of the central bank to

surprise the markets, a rate cut in February seems very likely, but it is not a done deal. A further

increase of volatility before the February decision may convince the board to wait a bit more to reduce

the interest rate.

The new government takes shape

Michelle Bachelet announced her cabinet in January. Alberto Arenas will be her finance minister.

He is a member of the Socialist Party and was the budget director in the previous Bachelet

government. Arenas helped write Bachelet’s program, which includes plans to raise the corporate tax

rate to finance education reform. The deputy finance minister is Alejandro Micco and the minister of

Page 20

LatAm Macro Monthly – February 2014

economy, development and tourism (which shares responsibility over economic affairs with the

finance minister) is Luis Felipe Cespedes (both were advisors to the finance minister in Bachelet’s

first term.) The appointments were well received by the market. Meanwhile Bachelet has reaffirmed

the intention to reach a zero structural balance in 2018 (it is currently -0.7% of GDP), hinting that

social policies will not lead to fiscal deterioration.

Sebastian Piñera’s approval rating continues to be on the rise, reaching 49% in January (45% in

December), for five months of consecutive improvement and the highest rate since November 2010’s

50%. In January, disapproval fell to 39% (from 41%). Piñera’s better-performing categories continue

to be international relations, job creation and the running of the economy.

The International Court of Justice (ICJ) in The Hague, the Netherlands, ruled that Chile and Peru

should split control over an area of sea off their cost. As a result of the ruling, Chile lost control over

part of that maritime territory. Politicians from both countries have agreed to implement the ruling,

avoiding any potential conflict.

Forecasts: Chile

Economic Activity

Real GDP growth - % -1.0 5.8 5.9 5.6 4.0 4.2 4.5

Nominal GDP - USD bn 172.3 217.6 251.2 267.5 283 286 295

Population (millions) 16.9 17.1 17.2 17.4 17.6 17.7 17.8

Per Capita GDP - USD 10,180 12,727 14,563 15,375 16,122 16,151 16,573

Unemployment Rate - year avg 9.6 8.3 7.2 6.5 6.0 7.0 7.3

Inflation

CPI - % -1.5 3.0 4.4 1.5 3.0 2.8 3.0

Interest Rate

Monetary Policy Rate - eop - % 0.50 3.25 5.25 5.00 4.50 4.00 4.50

Balance of Payments

CLP / USD - eop 506 468 521 479 526 540 550

Trade Balance - USD bn 15.4 15.6 10.5 3.4 2.4 0.1 0.5

Current Account - % GDP 2.0 1.5 -1.3 -3.5 -3.5 -3.4 -2.8

Foreign Direct Investment - % GDP 7.5 7.1 9.1 11.3 6.5 5.3 5.0

International Reserves - USD bn 25.4 27.9 42.0 41.6 41.1 45.0 46.0

Public Finances

Nominal Balance - % GDP -4.3 -0.3 1.5 0.6 -0.6 -0.6 -1.0

Net Public Debt - % GDP -12.0 -7.8 -10.7 -7.8 -7.8 -9.3 -9.3

2015F2013F 2014F2009 2010 2011 2012

Source: Central Bank, IMF, INE, Haver and Itaú.

Peru

Recovery and No Further Rate Cut

• Economic growth improved in 4Q13, mostly due to solid consumption. We expect GDP growth of

5.3% and 5.6% in 2014 and 2015, respectively, up from an estimated 4.9% last year.

• Annual inflation increased to 3.1% in January (from 2.9% last month), slightly above the upper

limit of the target range. We expect below-trend economic growth to contribute to a reduction of

inflation to 2.5% this year and 2.0% in 2015.

• As global market volatility increases, depreciation pressure on the sol gets more intense. To

protect the sol, the central bank is easing monetary policy, but only through reserve requirements,

and it is intervening in the exchange-rate market. We do not expect the central bank to resume

interest rate cuts.

• President Humala’s approval rating remains low, at 26% in January according to the Ipsos survey

(29% in December). This is now the sixth month in a row that the president’s approval hovers

between 25% and 30%. However, following the favorable maritime border ruling in The Hague, we

expect his rating to improve somewhat.

Page 21

LatAm Macro Monthly – February 2014

Data confirms the recovery in 4Q13

Economic growth improved in 4Q13, supported by consumption. Peru’s GDP grew 0.4% from

October to November, after a 0.9% increase, and as a result GDP expanded 4.8% qoq/saar in

November (up from 3.2% in 3Q13). Excluding the Natural Resources sector (in which growth is

determined more by supply conditions), growth was 5.9% qoq/saar (from 4.5% in 3Q13). While no

demand-side breakdown for the monthly GDP number is available, imports of capital goods and

construction (-6.5% qoq/saar in November) hint that investment continues to be weak, while the 9.6%

qoq/saar expansion in retail points to solid consumption.

In spite of weaker growth last year (from January to November the economy expanded by

4.9%), the labor market is still strong. The unemployment rate declined to 5.7% in December (from

5.8% in November), and it is only slightly higher than it was one year before (5.6%). Employment

grew by 2.0% year over year in December.

We expect the economy to grow by 5.3% this year and 5.6% in 2015, up from an estimated

4.9% expansion for 2013. Although we expect higher growth ahead, our forecasts are below the

growth rates that Peru has experienced over the past few years.

A temporary increase in annual inflation

The CPI rose to 3.1% in January (from 2.9% last month), slightly above the upper bound of the

central bank’s range. The two core measures closely tracked by the central bank were slightly

below 3% in December.

We see inflation at 2.5% by the end of this year and at 2.0% in 2015. In our view, the below-trend

economic growth will contribute to lower inflation.

The central bank maintains the policy rate unchanged and sold more dollars

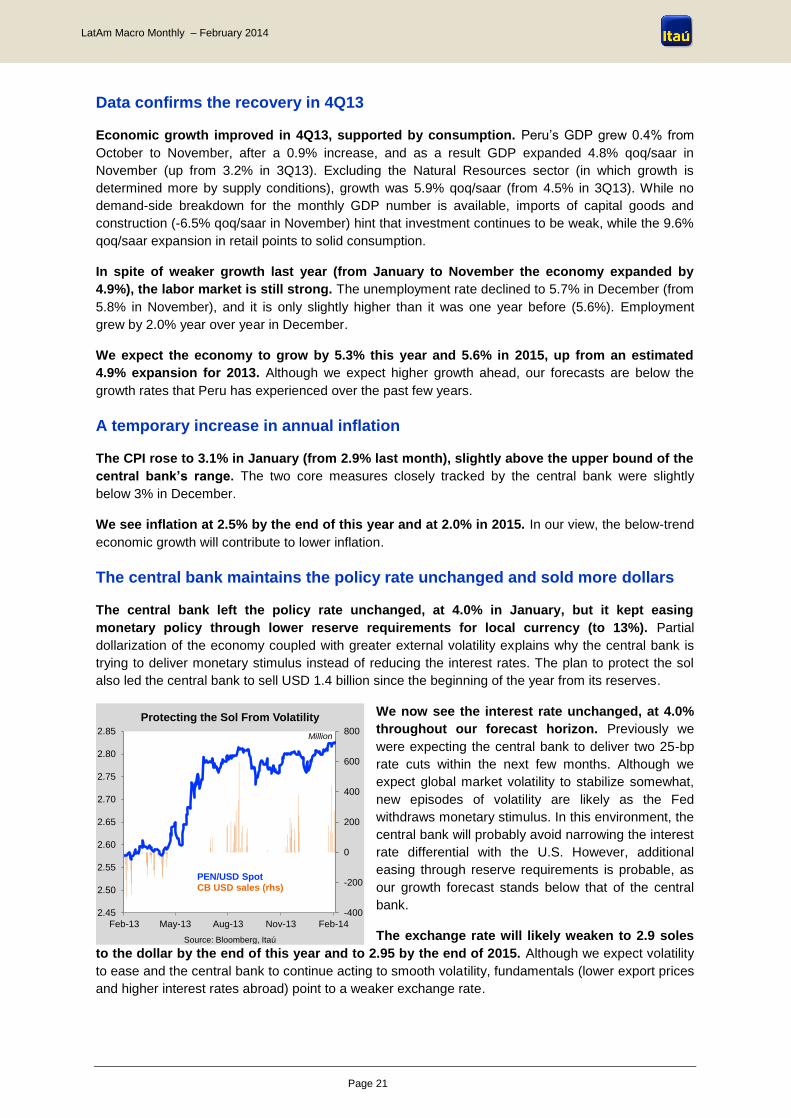

The central bank left the policy rate unchanged, at 4.0% in January, but it kept easing

monetary policy through lower reserve requirements for local currency (to 13%). Partial

dollarization of the economy coupled with greater external volatility explains why the central bank is

trying to deliver monetary stimulus instead of reducing the interest rates. The plan to protect the sol

also led the central bank to sell USD 1.4 billion since the beginning of the year from its reserves.

We now see the interest rate unchanged, at 4.0%

throughout our forecast horizon. Previously we

were expecting the central bank to deliver two 25-bp

rate cuts within the next few months. Although we

expect global market volatility to stabilize somewhat,

new episodes of volatility are likely as the Fed

withdraws monetary stimulus. In this environment, the

central bank will probably avoid narrowing the interest

rate differential with the U.S. However, additional

easing through reserve requirements is probable, as

our growth forecast stands below that of the central

bank.

The exchange rate will likely weaken to 2.9 soles

to the dollar by the end of this year and to 2.95 by the end of 2015. Although we expect volatility

to ease and the central bank to continue acting to smooth volatility, fundamentals (lower export prices

and higher interest rates abroad) point to a weaker exchange rate.

-400

-200

0

200

400

600

800

2.45

2.50

2.55

2.60

2.65

2.70

2.75

2.80

2.85

Feb-13 May-13 Aug-13 Nov-13 Feb-14

Million

Protecting the Sol From Volatility

Source: Bloomberg, Itaú

PEN/USD SpotCB USD sales (rhs)

Page 22

LatAm Macro Monthly – February 2014

Humala’s popularity declines, but The Hague ruling will likely boost it

President Humala´s approval rating remains low, at 26% in January according to the Ipsos

survey (29% in December). This is now the sixth month in a row that the president´s approval

hovers between 25% and 30%. The main positive for Humala is the 52% approval rating for the

implementation of social programs. Disapproval of the president is at 66% (64% in December), with

68% of respondents unhappy with the failure to implement campaign promises and 55% believing

there is a lack of public safety.

The International Court of Justice (ICJ) in The Hague, the Netherlands, ruled that Chile and Peru

should split control of an area of sea off their coasts. This topic has been an emotionally loaded issue

for Peru, and the partial victory is likely to boost Humala’s approval in the next survey.

Forecasts: Peru

Economic Activity

Real GDP growth - % 0.9 8.8 6.9 6.3 4.9 5.3 5.6

Nominal GDP - USD bn 127.0 153.5 176.2 200.4 214 227 227

Population (millions) 29.1 29.5 29.8 30.1 30.5 30.9 31.4

Per Capita GDP - USD 4,360 5,212 5,913 6,612 6,988 7,282 7,282