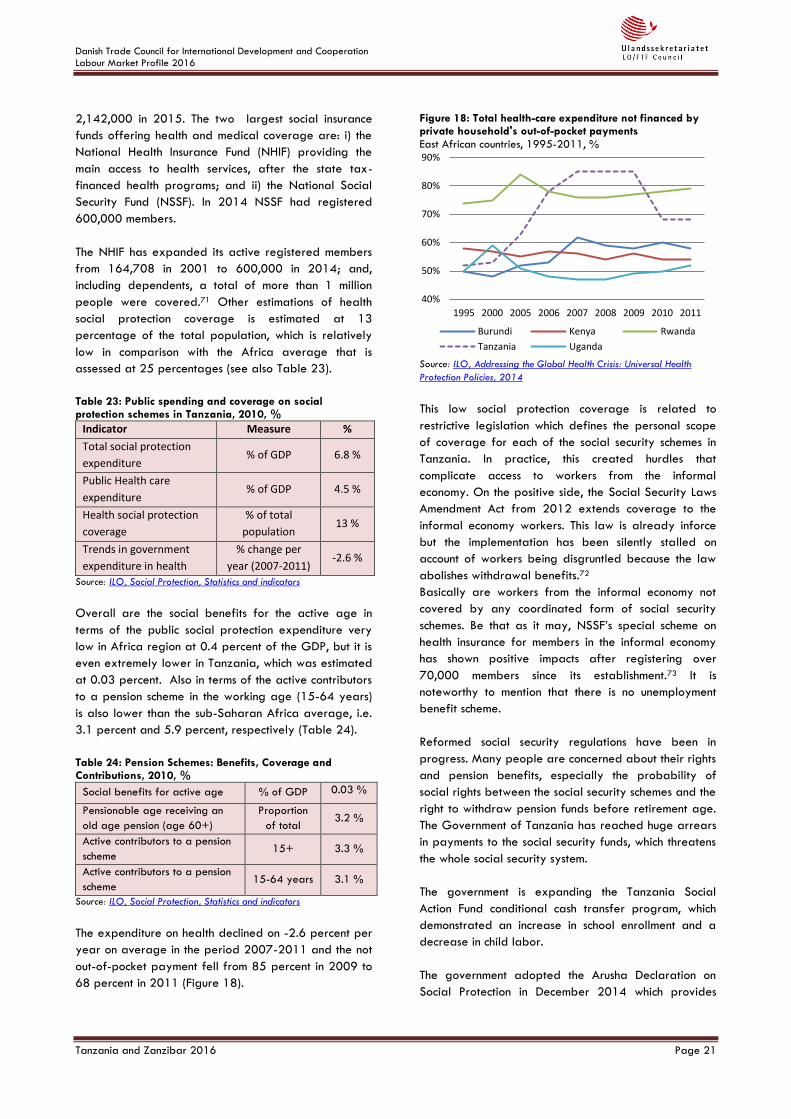

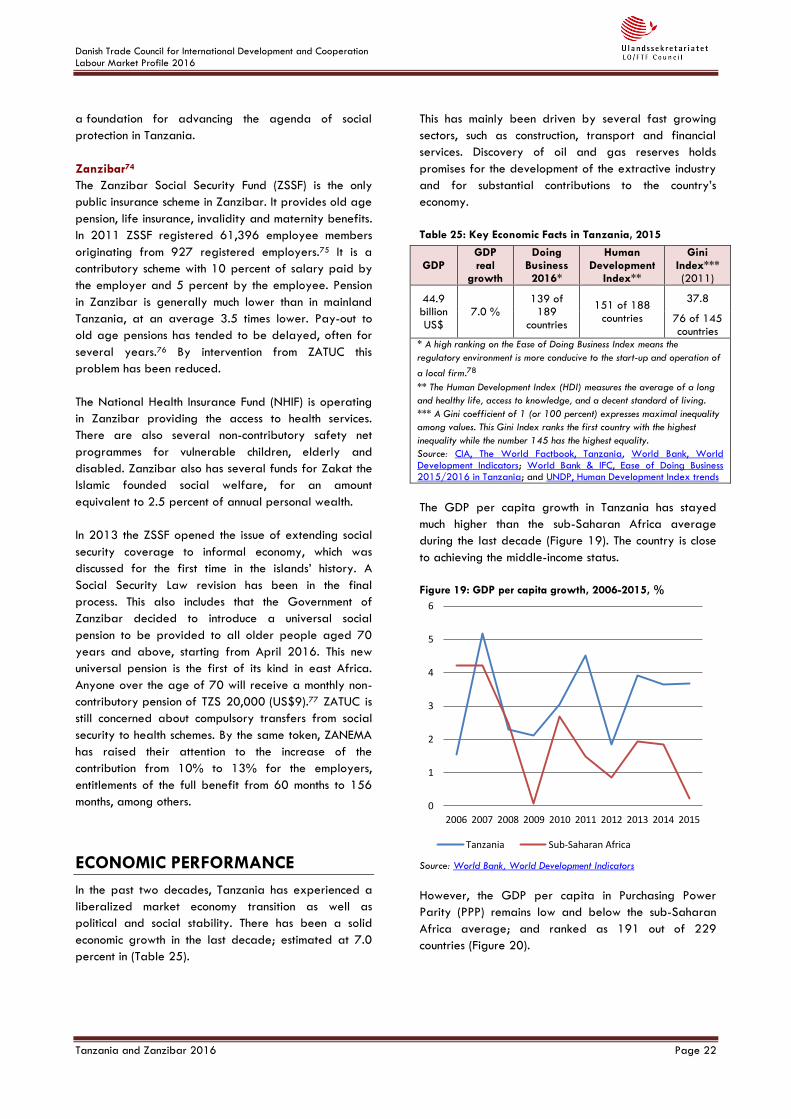

LABOUR MARKET PROFILE

2016 Tanzania and Zanzibar

LO/FTF Council’s Analytical Unit

Copenhagen, Denmark

Danish Trade Council for International Development and Cooperation

Labour Market Profile 2016

Tanzania & Zanzibar 2016 Page ii

PREFACE

The LO/FTF Council is the Danish trade union council for

international development co-operation. It was

established, under a slightly different name, in 1987 by

the two largest Danish confederations, the Danish

Federation of Trade Unions (LO) and the Danish

Confederation of Salaried Employees and Civil

Servants (FTF). The organization activities are related

to: i) to support democratic development of the trade

union movements in Africa, Middle East, Asia and Latin

America; and ii) to contribute to democratic

development in the societies in which the unions operate.

The LO/FTF Council presents this Labour Market Profile

as a yearly updated report that provides an overview

of the labour market's situation.

This country profile presents the recent main

developments and is not an in-depth analysis.

Nevertheless, it shows a wide range of data in a

reader-friendly style. Certain key findings of this report

can be found on the Executive Summary.

The report is divided in 11 thematic sections, which

includes trade unions, employers’ organizations,

tripartite structures, national labour legislation,

violations of trade union rights, working conditions,

situation of the workforce (with subsections such as

unemployment, sectoral employment, migration,

informal economy, child labour, gender, and youth),

education (with subsection vocational training), social

protection, general economic performance, and trade.

Additionally, the reader finds an Appendix with a list

of the ratified ILO Conventions and an updated status

of trade unions in Tanzania in terms of members and

CBAs.

As indicated, the report is driven by statistical data

selection from international databanks, surveys and

reports (e.g. the International Labour Organization

(ILO), the International Trade Union Confederation

(ITUC), the World Bank, the U.S. Department of State’s

Annual Country Reports on Human Rights Practices,

WageIndicator Foundation, the Africa Labour Research

& Educational Institute (ALREI), etc.) as well as national

statistical institutions and ministries, and others.

Moreover, narrative inputs are collected from

international news sources (e.g. The Economist, the British

Broadcasting Corporation (BBC), LabourStart, The

Guardian, etc.) together with local sources such as trade

unions centers, NGOs, national news, the LO/FTF

Council’s Sub-Regional Office, among others.

This report also collects references from several

indexes, e.g. the Global Rights Index, the Doing

Business Index, the Governance Indicators, and the

Human Development Index. The indexes’ methodologies

and the data quality can be followed by the sources

websites.

Most statistical data of trade union membership is

gathered through collaboration with trade centers and

research. Notwithstanding, the measurements of trend

of trade union membership, Collective Bargaining

Agreements (CBAs), women’s trade union membership

and occupational health and safety (OHS) committees

are a challenge. The used data of these

abovementioned indicators should be interpreted with

some reservations.

ACKNOWLEDGMENT This Labour Market Profile is prepared by the LO/FTF

Council’s Analytical Unit in Copenhagen with support

from our Sub-Region Office in Tanzania as well as the

Trade Unions Congress of Tanzania (TUCTA) and the

Zanzibar Trade Union Congress (ZATUC) in terms of

data collection of trade union membership.

All other labour market profiles of the countries where

LO/FTF Council operates are available at our website:

http://www.ulandssekretariatet.dk/content/landeanaly

ser

Should you have questions about the profiles you can

contact Kasper Andersen ([email protected]), Manager of

the Analytical Unit.

Cover Photo: Carsten Snejbjerg

Design and layout: Adriana Romero

Danish Trade Council for International Development and Cooperation

Labour Market Profile 2016

Tanzania and Zanzibar 2016 Page iii

Tanzania & Zanzibar Labour Market Profile

EXECUTIVE SUMMARY

he United Republic of Tanzania has experienced a

rapid economic growth during the last decade

followed by a steady increasing labour productivity.

The number of working poor has dropped fast; a

middle-class is on a rise and with an improving equality

in terms of the income distribution. The volatile inflation

in Tanzania has affected the real wages purchasing

power, though. In additiion, the country continues being

far below the sub-Saharan Africa average in terms of

the Gross Domestic Product (GDP) per capita in the

purchasing power parity (PPP). It remains complicated

doing business, especially trading across borders,

getting credit and paying taxes.

The government in Tanzania mainland implemented five

labour market related legislations in 2015 along with

one new act in Zanzaniar, but none in 2016. The

International Trade Union Confederation (ITUC) has

various observations with legislations that affect

negatively the labour markets environment. Two key

points are that the state has lack of resources to

implement the labour market regulations in practice in

the formal sector and indirectly not covering a vast

majority (85 percent) of the labour force that operate

in the informal economy. It has also been noted that

workers are confronting regular violations of trade

union rights.

The labour force employment rate fell during the last

decade, especially among the youth. More and more

people were instead inactive on the labour market.

Unemployment is not a critical issue in Tanzania, but is

more affected by skills mismatch between job

requirements and qualifications due to a high incidence

of under-education.

The employment in the agricultural sector has been

fallen significantly, entering into the service sector and

slightly also in the industry sector. This is reflected in a

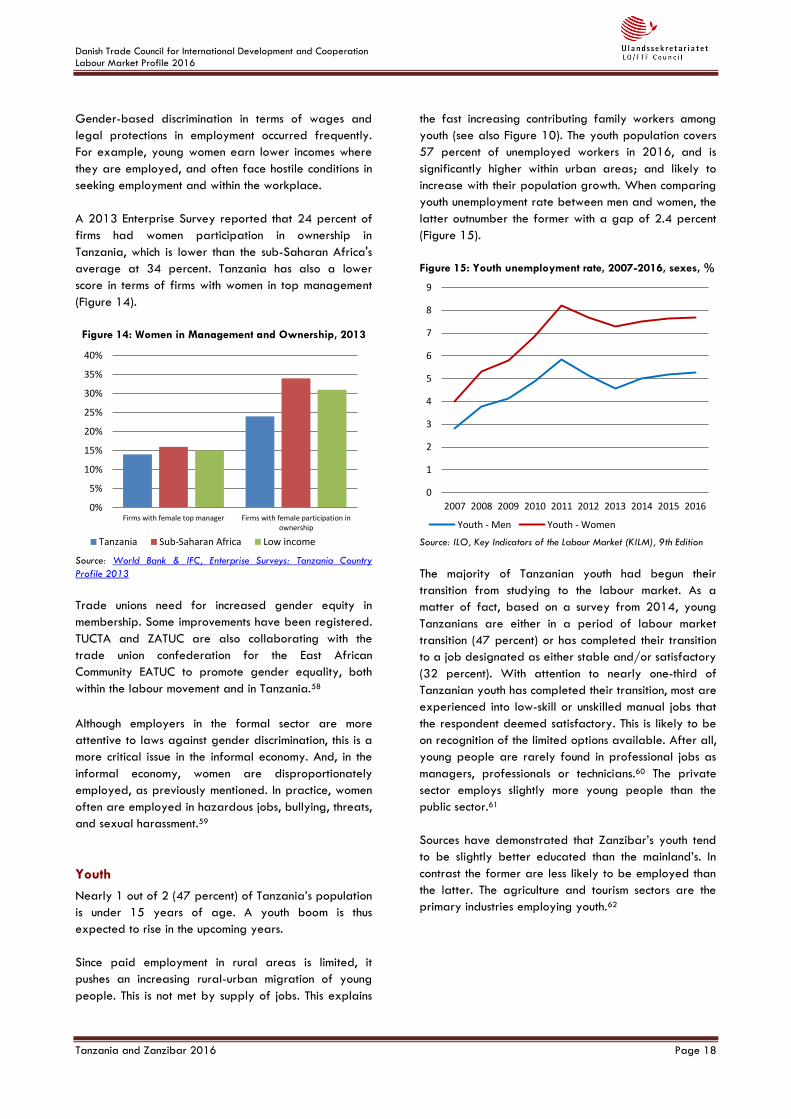

considerable drop of own-account workers that instead

became contributing family workers or wage &

salaried workers. These changes have been illustrated

by an increasing GDP growth in the industry sector

while the agricultural sector has more or less been flat

and the service sector was dwindling. On the positive

side, the changes in the industry sector is a step towards

a more economic transformation On the negative side,

that latter sector is not offering enough new jobs and a

majority find their possibilities in the service sector with

a lower labour productivity.

Changes are also demonstrated by an internal

migration from rural to urban areas in the country. This

is driven by by the youth that is seeking for better jobs.

Also child labour remains very acute. Gender-based

discriminations in terms of wages and protections in

employment are present. The education system has

been hard affected by resource shortages during

recent years and the enrolment in schools on all levels

experienced drops. The membership of social protection

shemes have increased fast, but remain with very low

national coverages.

Tanzania mainland

The growth of trade union membership in Tanzania

mainland were on a fast increase on absolute terms

during the last decade. This influx has mainly been

related to a growing number of wage & salaried

workers. In recent years, the total membership’s

intensification has been stalled, though. Likewise the

coverage of collective bargaining agreements (CBAs)

also increased but lost its tempo. These negative

impacts have been related to financial constraints as

well as challenges in the education system, among

others.

Zanzibar

The trade union movement in Zanzibar had an influx of

new members due to an improved social dialogue with

the government and employers’ organizations as well

as creating possibilities of affiliated organized workers

from the informal economy. Despite these

improvements, organizational reforms in 2015 affected

hard the membership that fell by 11 percent in the

period from 2015 to 2016 (September). On the

positive side, social security schemes have opened up

for workers from the informal economy.

T

Danish Trade Council for International Development and Cooperation

Labour Market Profile 2016

Tanzania and Zanzibar 2016 Page iv

COUNTRY MAP

Source: The CIA World Factbook

Danish Trade Council for International Development and Cooperation

Labour Market Profile 2016

Tanzania and Zanzibar 2016 Page v

TABLE OF CONTENTS Preface ................................................................................................................................................................................................................ ii

Acknowledgment ................................................................................................................................................................................................ ii

Executive Summary ........................................................................................................................................................................................... iii

Country Map ......................................................................................................................................................................................................iv

Trade Unions .......................................................................................................................................................................................................1

Tanzania, mainland ............................................................................................................................................................................................................... 1

Zanzibar ................................................................................................................................................................................................................................. 2

Employers’ Organisations ..................................................................................................................................................................................3

Tanzania, mainland ............................................................................................................................................................................................................... 3

Zanzibar ................................................................................................................................................................................................................................. 4

Central Tripartite Structures ................................................................................................................................................................................4

Tanzania, mainland ............................................................................................................................................................................................................... 4

Zanzibar ................................................................................................................................................................................................................................. 6

National Labour Legislation ...............................................................................................................................................................................6

Tanzania, mainland ............................................................................................................................................................................................................... 7

Zanzibar ................................................................................................................................................................................................................................. 7

Observations on the labour legislation .............................................................................................................................................................................. 7

Ratified ILO Conventions ...................................................................................................................................................................................................... 8

TRADE UNION RIGHTS VIOLATIONS .................................................................................................................................................................8

Working Conditions ............................................................................................................................................................................................9

Workforce ......................................................................................................................................................................................................... 10

Unemployment ..................................................................................................................................................................................................................... 12

Sectoral Employment ........................................................................................................................................................................................................... 13

Migration .............................................................................................................................................................................................................................. 15

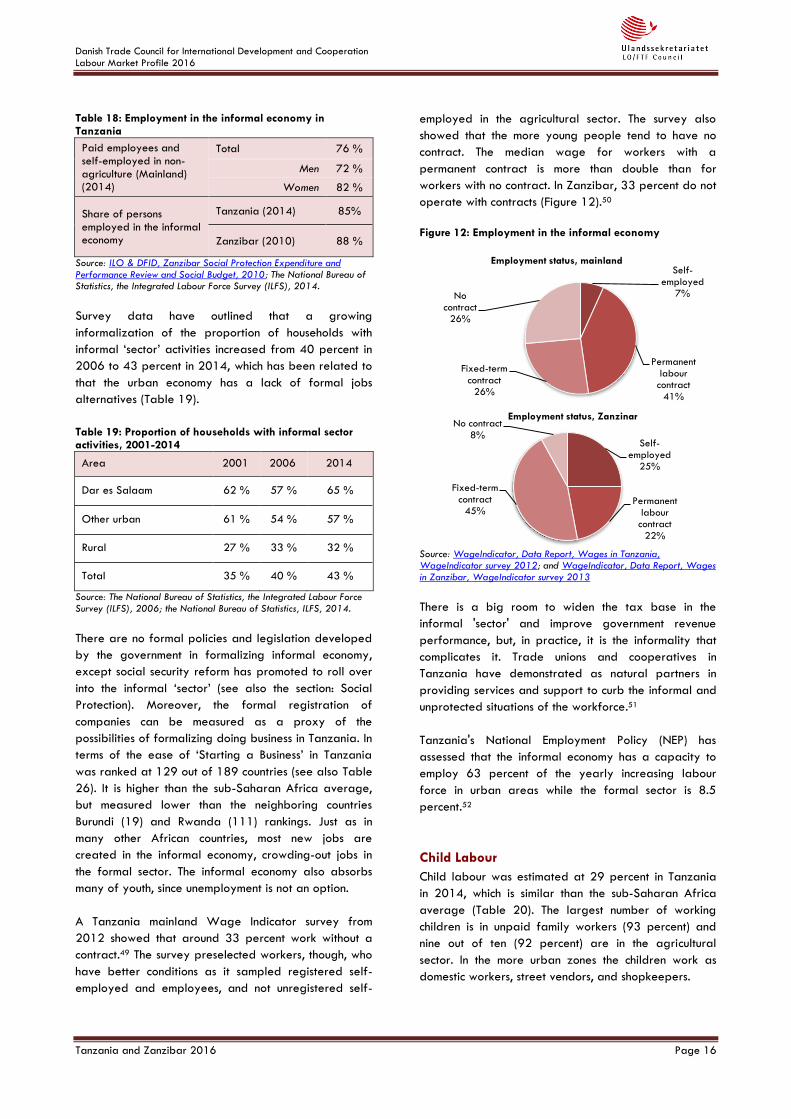

Informal Economy ................................................................................................................................................................................................................ 15

Child Labour ......................................................................................................................................................................................................................... 16

Gender .................................................................................................................................................................................................................................. 17

Youth...................................................................................................................................................................................................................................... 18

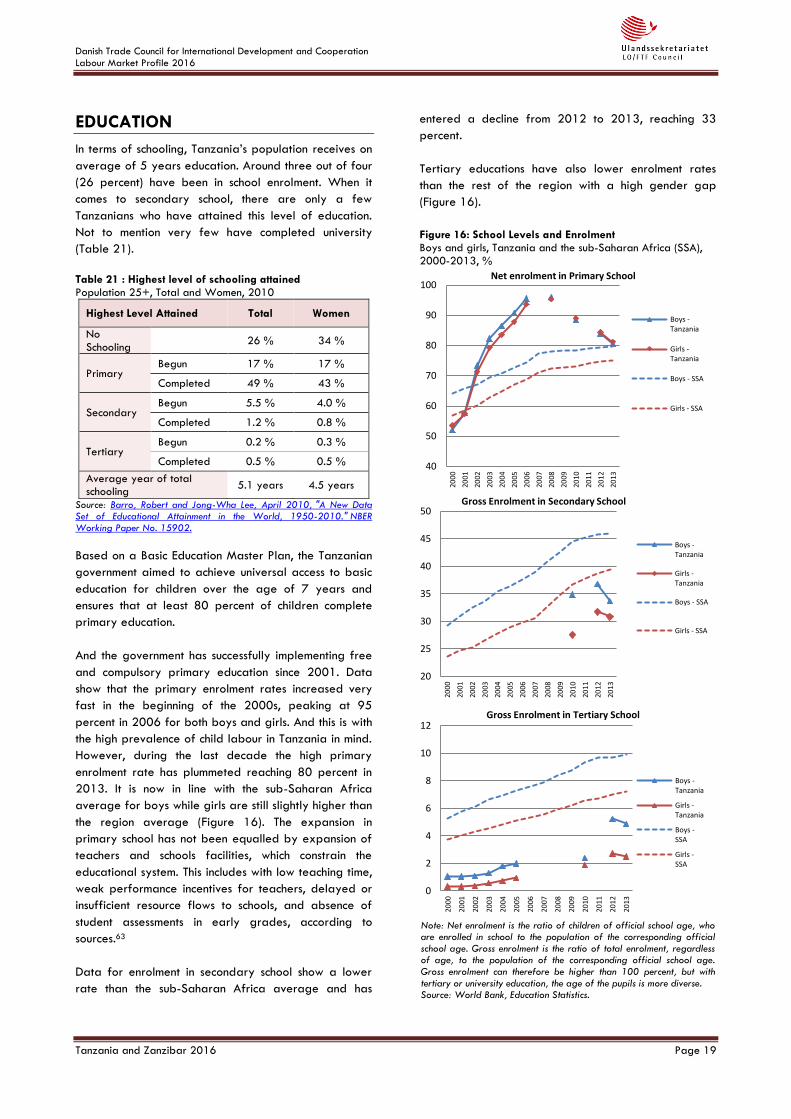

Education ......................................................................................................................................................................................................... 19

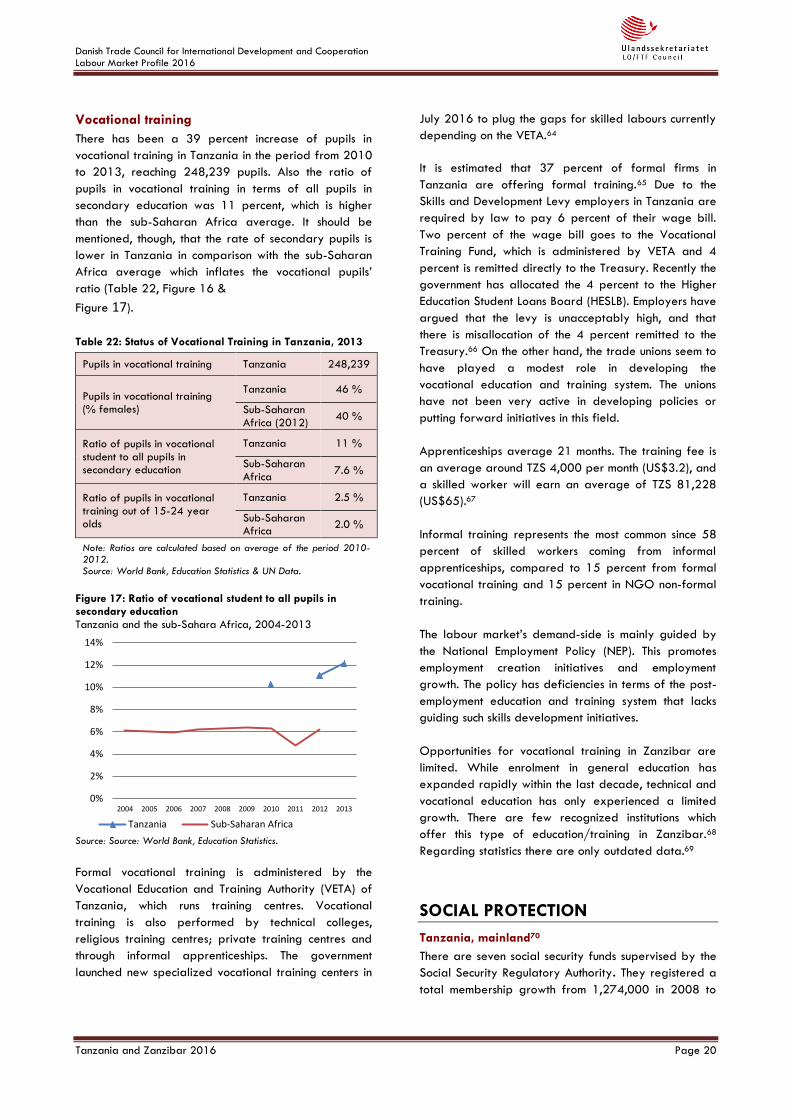

Vocational training .............................................................................................................................................................................................................. 20

Social Protection .............................................................................................................................................................................................. 20

Tanzania, mainland ............................................................................................................................................................................................................. 20

Zanzibar ............................................................................................................................................................................................................................... 22

Economic Performance .................................................................................................................................................................................... 22

Trade ................................................................................................................................................................................................................ 25

Trade Agreements ............................................................................................................................................................................................................... 25

Export Processing Zones (EPZ) ........................................................................................................................................................................................... 26

Appendix: Additional Data ............................................................................................................................................................................. 28

Status of Tanzania’s Ratified ILO Conventions ................................................................................................................................................................ 28

Status of Trade Unions in Tanzania, 2016 ...................................................................................................................................................................... 29

Trade Union Centre and affiliates in Zanzibar, 2016 ................................................................................................................................................... 30

References ........................................................................................................................................................................................................ 31

Danish Trade Council for International Development and Cooperation

Labour Market Profile 2016

Tanzania and Zanzibar 2016 Page vi

Tables Table 1: Status of trade unionism in Tanzania mainland, 2016 (est.).................................................................................................................................................. 1 Table 2: Paid employees with trade unions or employees associations, 2014 .................................................................................................................................. 1

Table 3: Status of trade unionism in Zanzibar, 2016 ............................................................................................................................................................................. 2 Table 4: Membership of Association of Tanzania Employers (ATE), 2008 ......................................................................................................................................... 3

Table 5: Number of cases in Tanzania Commission for Meditation and Arbitration, 2013-2015.................................................................................................. 4 Table 6: Status of Collective Bargaining Agreements (CBAs) in Tanzania, 2016 ............................................................................................................................. 5

Table 7: Status of Collective Bargaining Agreements in Zanzibar, 2016 .......................................................................................................................................... 6 Table 8: Status of the national labour, social security and human rights related legislations in Tanzania .................................................................................... 7

Table 9: Global Rights Index, Tanzania ranking, 2014-2016 ............................................................................................................................................................. 8 Table 10: Wages and earnings Monthly average and legal minimum wages .................................................................................................................................. 9

Table 11: Working Conditions in Tanzania ...........................................................................................................................................................................................10 Table 12: Employment-to-population ratio, Age and Sexes distribution, 2016 ..............................................................................................................................10

Table 13: Inactivity rate in Tanzania, 2016, % ....................................................................................................................................................................................11 Table 14: Skills mismatch between job requirements and qualifications in Tanzania, 2013 .........................................................................................................11

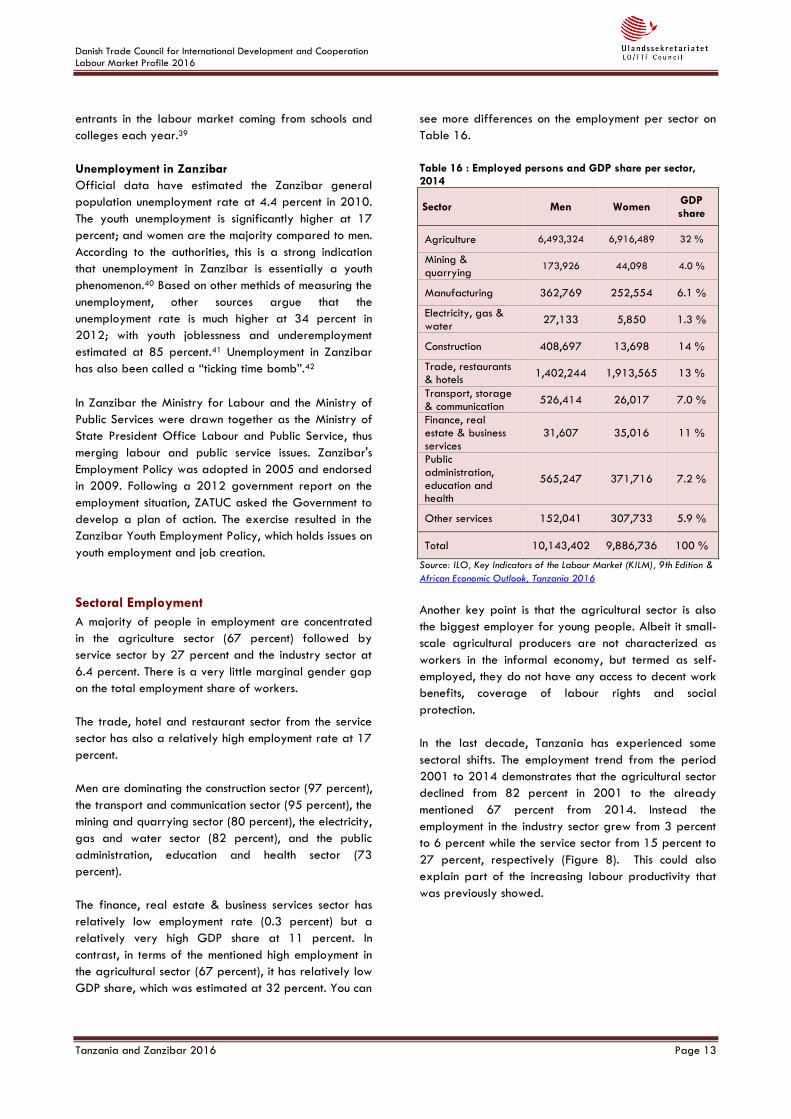

Table 15: Unemployment in Tanzania, 2016 ........................................................................................................................................................................................12 Table 16 : Employed persons and GDP share per sector, 2014 .......................................................................................................................................................13

Table 17: Key Migration Facts in Tanzania ...........................................................................................................................................................................................15 Table 18: Employment in the informal economy in Tanzania ..............................................................................................................................................................16 Table 19: Proportion of households with informal sector activities, 2001-2014 .............................................................................................................................16

Table 20: Working children Proportion of all children, age 5-17 years ..........................................................................................................................................17 Table 21 : Highest level of schooling attained ......................................................................................................................................................................................19

Table 22: Status of Vocational Training in Tanzania, 2013 ...............................................................................................................................................................20 Table 23: Public spending and coverage on social protection schemes in Tanzania, 2010, % ....................................................................................................21

Table 24: Pension Schemes: Benefits, Coverage and Contributions, 2010, % .................................................................................................................................21 Table 25: Key Economic Facts in Tanzania, 2015 ................................................................................................................................................................................22

Table 26: Ease of Doing Business in Tanzania .......................................................................................................................................................................................24 Table 27: Tanzania's Governance Indicators, 2009-2014 .................................................................................................................................................................24

Table 28: Trade and Foreign Direct Investment in Tanzania, 2015 ..................................................................................................................................................25 Table 29: Status of Tanzania’s Ratified ILO Conventions, 2016 ........................................................................................................................................................28

Table 30: Status of Trade Unions in Tanzania, 2016 ..........................................................................................................................................................................29 Table 31: Trade Union Centre and affiliates in Zanzibar, 2016 .......................................................................................................................................................30

Figures Figure 1: Trend of number of members in TUCTA and the trade union density, 2008-2016 .......................................................................................................... 1

Figure 2: TUCTA membership covered by Collective Bargaining Agreements (CBA), 2008-2016 ................................................................................................ 5 Figure 3: Minimum wage trend in Tanzania, 2000-2016 ...................................................................................................................................................................10

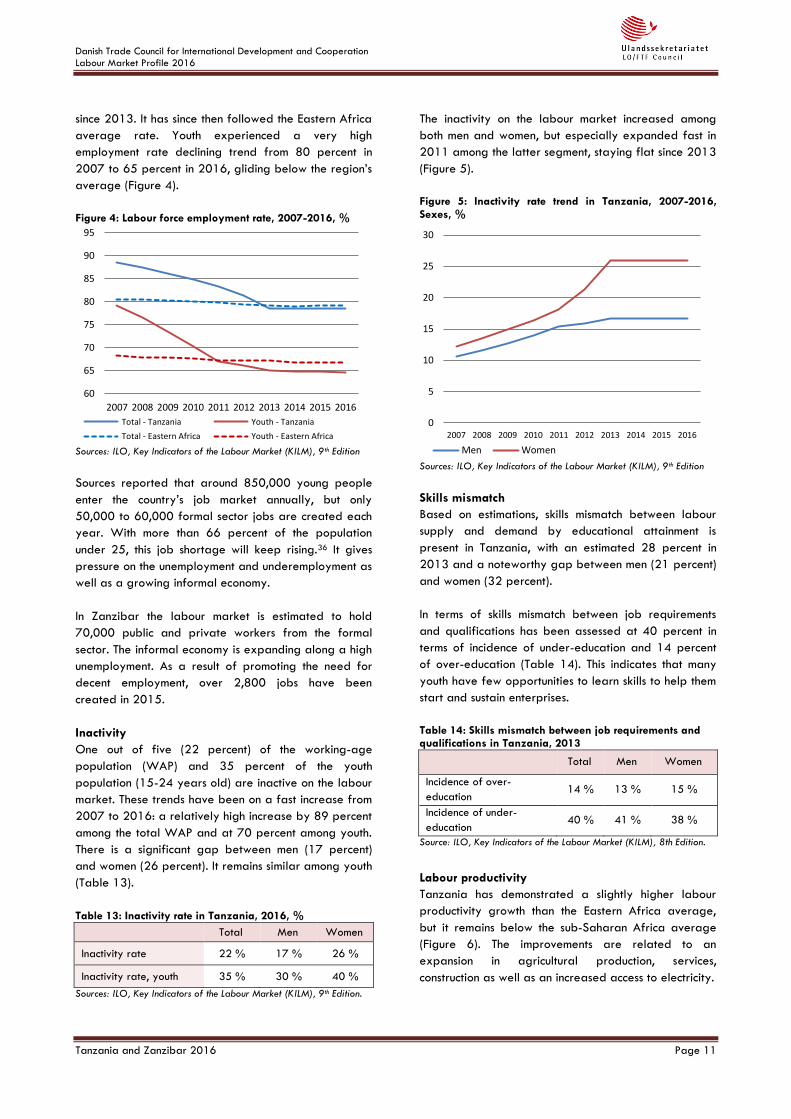

Figure 4: Labour force employment rate, 2007-2016, % ..................................................................................................................................................................11 Figure 5: Inactivity rate trend in Tanzania, 2007-2016, Sexes, % ...................................................................................................................................................11

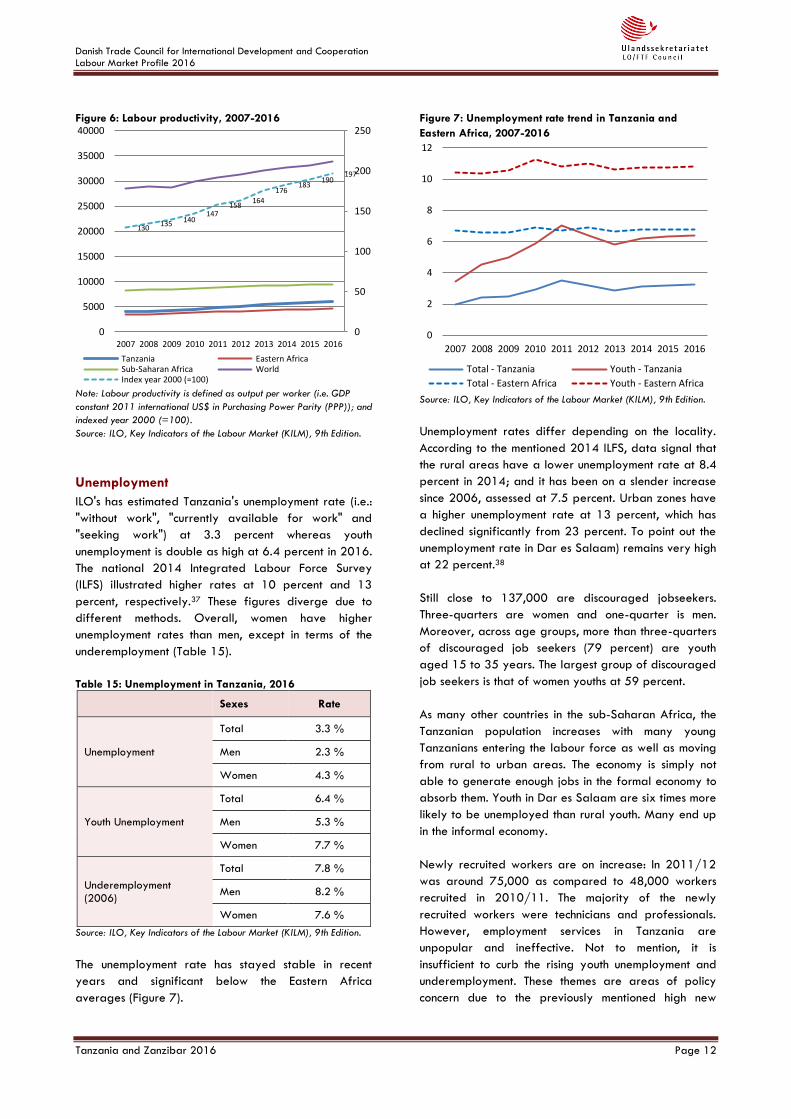

Figure 6: Labour productivity, 2007-2016 ............................................................................................................................................................................................12 Figure 7: Unemployment rate trend in Tanzania and Eastern Africa, 2007-2016 .........................................................................................................................12

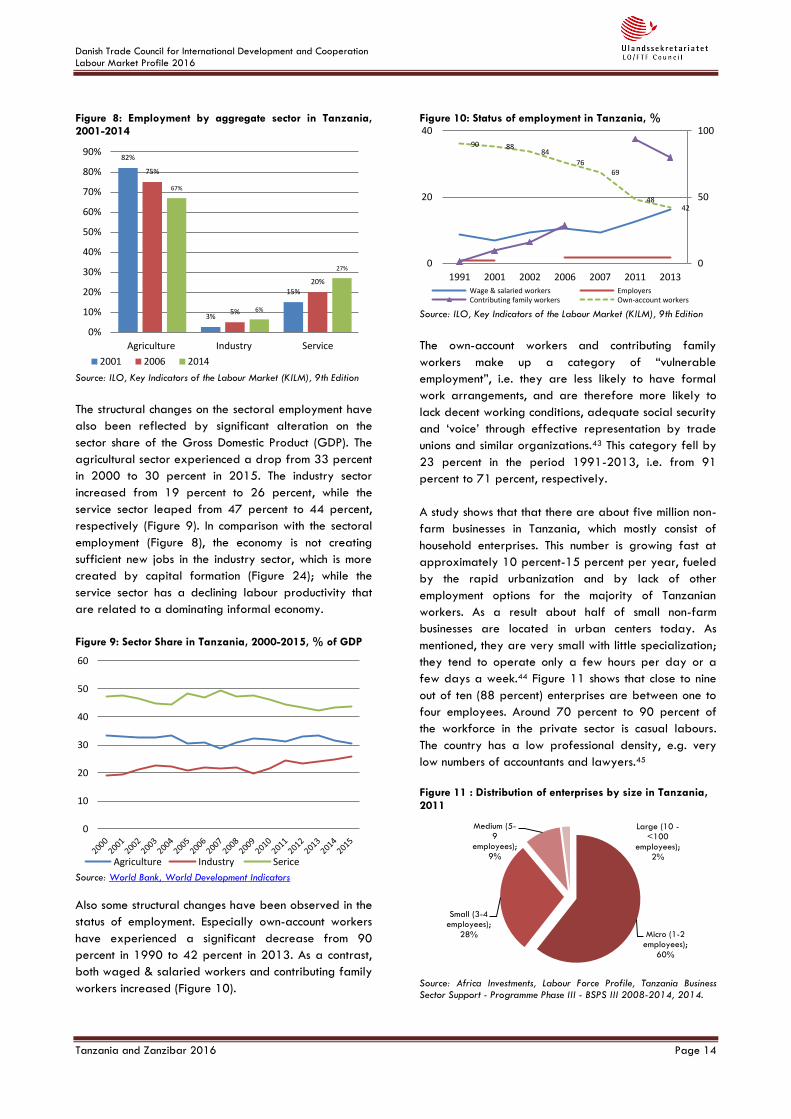

Figure 8: Employment by aggregate sector in Tanzania, 2001-2014 .............................................................................................................................................14 Figure 9: Sector Share in Tanzania, 2000-2015, % of GDP .............................................................................................................................................................14 Figure 10: Status of employment in Tanzania, % .................................................................................................................................................................................14

Figure 11 : Distribution of enterprises by size in Tanzania, 2011 .....................................................................................................................................................14 Figure 12: Employment in the informal economy ..................................................................................................................................................................................16

Figure 13: Labour force participation rate, sexes, % ..........................................................................................................................................................................17 Figure 14: Women in Management and Ownership, 2013 ................................................................................................................................................................18

Figure 15: Youth unemployment rate, 2007-2016, sexes, % .............................................................................................................................................................18 Figure 16: School Levels and Enrolment .................................................................................................................................................................................................19

Figure 17: Ratio of vocational student to all pupils in secondary education ....................................................................................................................................20 Figure 18: Total health-care expenditure not financed by private household's out-of-pocket payments ...................................................................................21

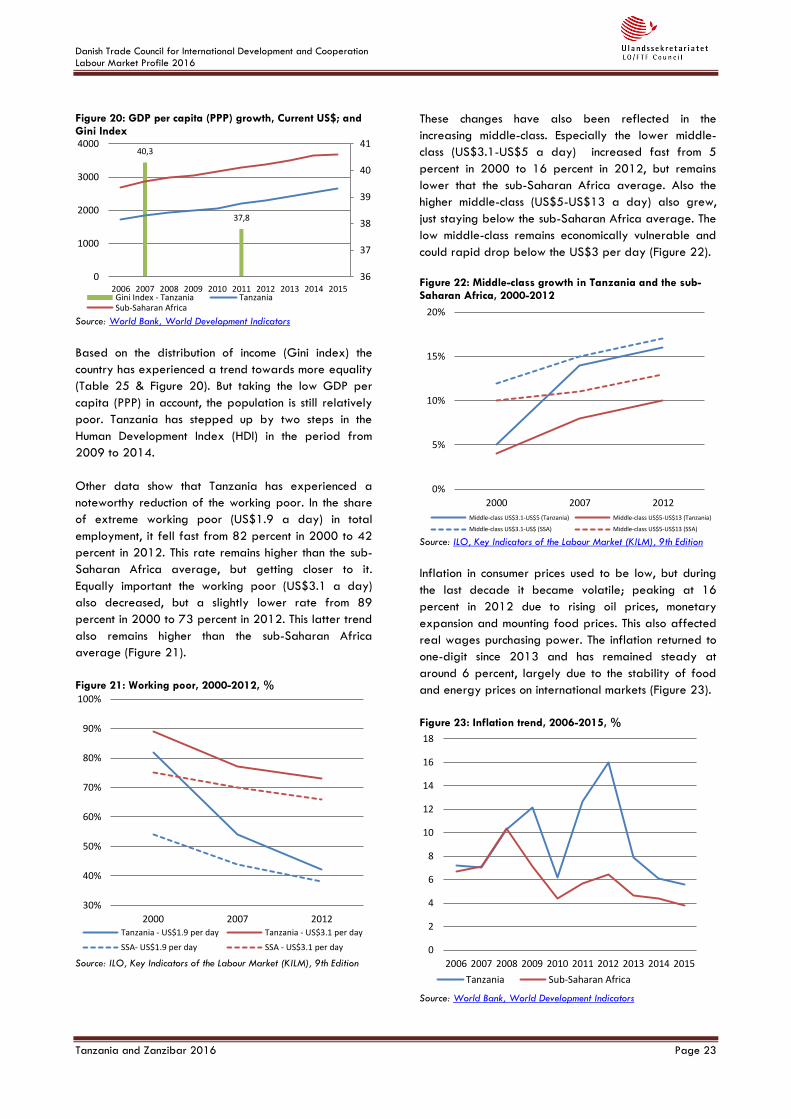

Figure 19: GDP per capita growth, 2006-2015, % ............................................................................................................................................................................22 Figure 20: GDP per capita (PPP) growth, Current US$; and Gini Index ..........................................................................................................................................23

Figure 21: Working poor, 2000-2012, % ............................................................................................................................................................................................23 Figure 22: Middle-class growth in Tanzania and the sub-Saharan Africa, 2000-2012 ................................................................................................................23

Figure 23: Inflation trend, 2006-2015, % .............................................................................................................................................................................................23 Figure 24: Gross Fixed Capital Formation, 2006-2015, % of GDP .................................................................................................................................................24

Figure 25: Export, Import and Foreign Direct Investment (FDI) trends ...............................................................................................................................................25 Figure 26: Tanzania's main products share of exports, 2014 ............................................................................................................................................................25

Figure 27: Tanzania's main export markets, 2015 ...............................................................................................................................................................................25 Figure 28: Number of Zone Developers and Operators since established of EPZA, 2006-2010 ................................................................................................26

Danish Trade Council for International Development and Cooperation

Labour Market Profile 2016

Tanzania and Zanzibar 2016 Page 1

TRADE UNIONS

Tanzania, mainland

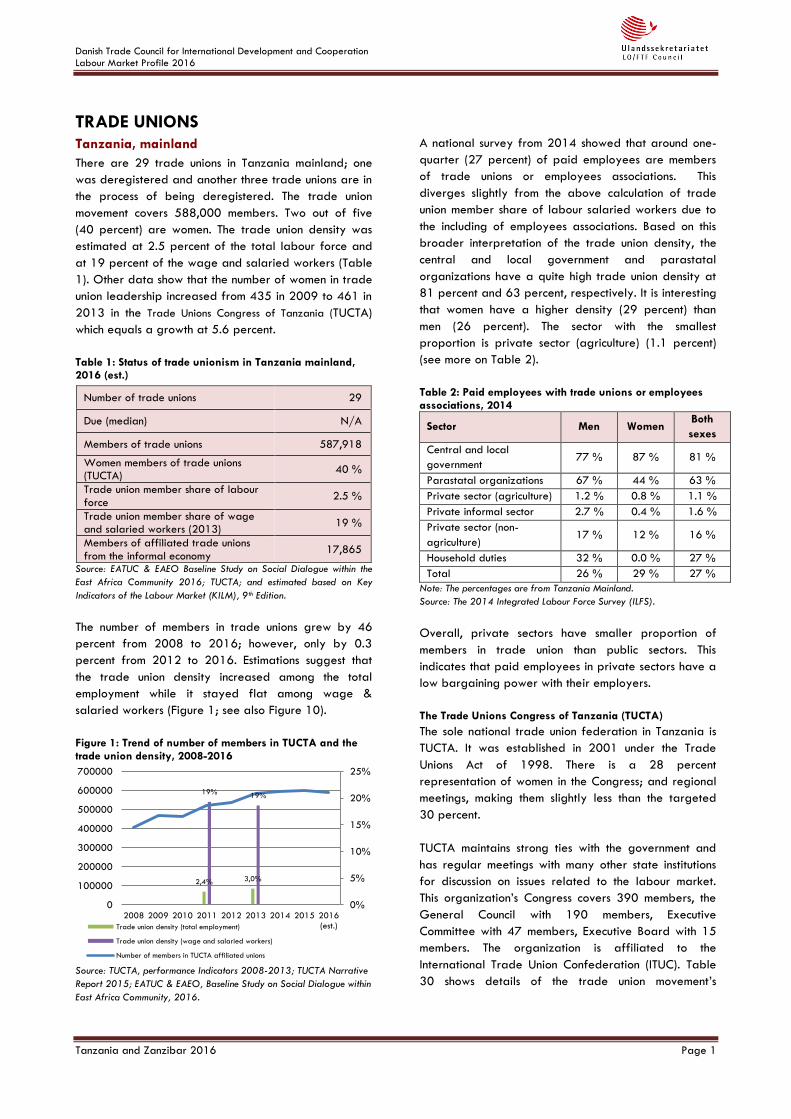

There are 29 trade unions in Tanzania mainland; one

was deregistered and another three trade unions are in

the process of being deregistered. The trade union

movement covers 588,000 members. Two out of five

(40 percent) are women. The trade union density was

estimated at 2.5 percent of the total labour force and

at 19 percent of the wage and salaried workers (Table

1). Other data show that the number of women in trade

union leadership increased from 435 in 2009 to 461 in

2013 in the Trade Unions Congress of Tanzania (TUCTA)

which equals a growth at 5.6 percent.

Table 1: Status of trade unionism in Tanzania mainland, 2016 (est.)

Number of trade unions 29

Due (median) N/A

Members of trade unions 587,918

Women members of trade unions (TUCTA)

40 %

Trade union member share of labour force

2.5 %

Trade union member share of wage and salaried workers (2013)

19 %

Members of affiliated trade unions from the informal economy

17,865

Source: EATUC & EAEO Baseline Study on Social Dialogue within the

East Africa Community 2016; TUCTA; and estimated based on Key

Indicators of the Labour Market (KILM), 9th Edition.

The number of members in trade unions grew by 46

percent from 2008 to 2016; however, only by 0.3

percent from 2012 to 2016. Estimations suggest that

the trade union density increased among the total

employment while it stayed flat among wage &

salaried workers (Figure 1; see also Figure 10).

Figure 1: Trend of number of members in TUCTA and the trade union density, 2008-2016

Source: TUCTA, performance Indicators 2008-2013; TUCTA Narrative

Report 2015; EATUC & EAEO, Baseline Study on Social Dialogue within

East Africa Community, 2016.

A national survey from 2014 showed that around one-

quarter (27 percent) of paid employees are members

of trade unions or employees associations. This

diverges slightly from the above calculation of trade

union member share of labour salaried workers due to

the including of employees associations. Based on this

broader interpretation of the trade union density, the

central and local government and parastatal

organizations have a quite high trade union density at

81 percent and 63 percent, respectively. It is interesting

that women have a higher density (29 percent) than

men (26 percent). The sector with the smallest

proportion is private sector (agriculture) (1.1 percent)

(see more on Table 2).

Table 2: Paid employees with trade unions or employees associations, 2014

Sector Men Women Both

sexes

Central and local

government 77 % 87 % 81 %

Parastatal organizations 67 % 44 % 63 %

Private sector (agriculture) 1.2 % 0.8 % 1.1 %

Private informal sector 2.7 % 0.4 % 1.6 %

Private sector (non-

agriculture) 17 % 12 % 16 %

Household duties 32 % 0.0 % 27 %

Total 26 % 29 % 27 %

Note: The percentages are from Tanzania Mainland.

Source: The 2014 Integrated Labour Force Survey (ILFS).

Overall, private sectors have smaller proportion of

members in trade union than public sectors. This

indicates that paid employees in private sectors have a

low bargaining power with their employers.

The Trade Unions Congress of Tanzania (TUCTA)

The sole national trade union federation in Tanzania is

TUCTA. It was established in 2001 under the Trade

Unions Act of 1998. There is a 28 percent

representation of women in the Congress; and regional

meetings, making them slightly less than the targeted

30 percent.

TUCTA maintains strong ties with the government and

has regular meetings with many other state institutions

for discussion on issues related to the labour market.

This organization’s Congress covers 390 members, the

General Council with 190 members, Executive

Committee with 47 members, Executive Board with 15

members. The organization is affiliated to the

International Trade Union Confederation (ITUC). Table

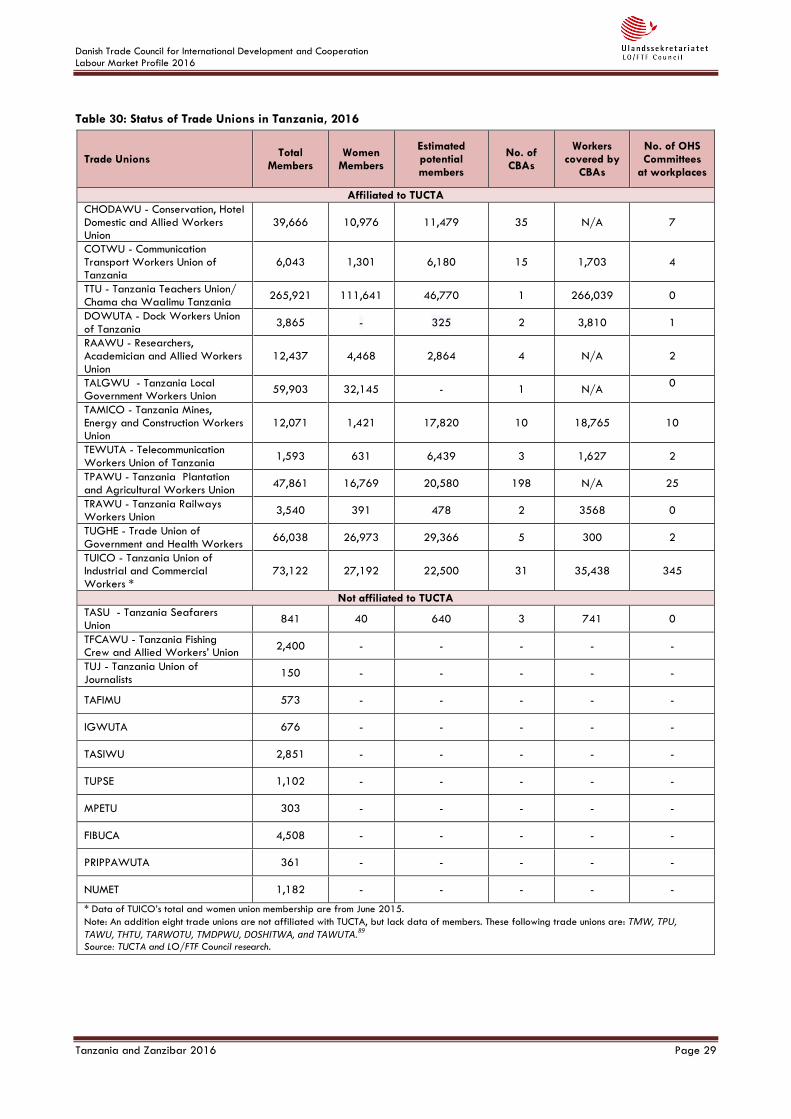

30 shows details of the trade union movement’s

2,4% 3,0%

19% 19%

0%

5%

10%

15%

20%

25%

0

100000

200000

300000

400000

500000

600000

700000

2008 2009 2010 2011 2012 2013 2014 2015 2016

(est.)Trade union density (total employment)

Trade union density (wage and salaried workers)

Number of members in TUCTA affiliated unions

Danish Trade Council for International Development and Cooperation

Labour Market Profile 2016

Tanzania and Zanzibar 2016 Page 2

membership, number of Collective Bargaining

Agreements, and number of Occupational Health and

Safety Committees at workplaces.

One third of TUCTA’s total membership is organized by

the Tanzania Teacher Union (TTU), which is one of the

strongest trade unions in Tanzania. TTU, together with

the trade unions for government workers (TUGHE) and

local government workers (TALGWU), represent more

than 50 percent of the total TUCTA membership (see

more on Appendix Table 30).

TUCTA has had regular consultations with the president

and officials as well as the employers’ association, the

Association of Tanzania Employers (ATE), on labour

issues. Meetings in tripartite institutions such as the

Institution Labour, Economic and Social Council (LESCO)

have been seldom, though (see also the section: Central

Tripartite Structures).

TUCTA conducted advocacy campaigns through

national media on topics like domestic workers, gender

labour rights and labour rights compliance, workman’s

compensation fund, informal economy contributions to

social security schemes, among others. TUCTA managed

to pressurize government to allow workers from the

informal economy to pay contributions to - and benefit

from - social security schemes. On the same token,

TUCTA has supported regional trainers’ network through

training of (master) trainers, researchers and regional

trade union representatives.

The TUCTA strategic plan 2012-2016 continues to

promote attention to strengthen the financial situation of

the organization. The management of the real estate

owned by the organization has been improved and a

business plan has been developed for the revamping of

the Mbeya Labour College. Furthermore, a membership

database is under development. Also a draft policy has

been developed on how TUCTA and affiliated unions

can engage and organize in the informal sector.

The organization is recognized as an institutional player

in the labour market. However, TUCTA is faced with

serious financial constraints due to lack of income from

fees from affiliated unions, real estates, and losing

external donor support, among others. TUCTA is

working on financial recovery plans. Internal conflicts

have also arisen because affiliated unions oppose

TUCTA’s constitutional right to direct check-off from the

source (5 percent of member fees paid to unions). In

addition, TUCTA hardly pay salaries to the secretariat,

and most activities have been donor funded. It is

equally important to note, that TUCTA faces challenges

and competition from new and fragmented unions.

Zanzibar

Zanzibar’s labour concerns have historically been

neglected when it comes to constitutional matters. The

Zanzibar House of Representatives was compelled to

enact the Zanzibar Trade Union Act of 2001, which

allowed registration of trade unions in Zanzibar.

Subsequently, the national trade union centre -

Zanzibar Trade Union Congress (ZATUC) - was

established in 2003. The ITUC affiliates the Zanzibar

Trade Union Congress (ZATUC).

The labour law requires a union with 50 or more

members to be registered and sets literacy standards

for trade union officers. Not to mention the law

provides considerable powers of the registrar to restrict

registration by setting forth criteria for determining

whether an organization’s constitution contains suitable

provisions to protect its members’ interests.1

The trade union movement covers nine trade unions. In

ZATUC is now recruiting members who are paying

contributions to their unions and those who are not

paying at all are not considered as members any more.

Consequently basing on such criteria, ZATUC

membership has been registered from 21,000 in 2015

to 19,000 as of September 2016, i.e. 11 percent

decrease. Around 40 percent are women. The trade

union density was estimated at 2.4 percent as a share

of the total workforce in Zanzibar (Table 3).

Table 3: Status of trade unionism in Zanzibar, 2016

Number of trade unions 9

Due (median) 4,000

Members of trade unions 19,000

Women members of trade unions 7,397

Trade union members share of workforce

2.4 %

Members of affiliated trade unions from the informal economy

896

Labour force (2012 )2 776,176

Source: ZATUC; LO/FTF Council research; and ILO, Key Indicators of

the Labour Market (KILM), 9th Edition.

The Zanzibar Trade Union Congress (ZATUC)

ZATUC continues its positive development and is

continuously consulted by the government. Among

others, trade union leaders are placed centrally in

standing committees in the House of Representatives to

lobby tabled Bills. For instance, ZATUC participated in

formulating the new regulation on public service to

Danish Trade Council for International Development and Cooperation

Labour Market Profile 2016

Tanzania and Zanzibar 2016 Page 3

establish committee of negotiating machinery for public

sector employees.

The trade union movement in Zanzibar is under reforms.

Internally ZATUC is merging resources together to make

fewer and stronger unions. So far it has managed to

reduce the number of affiliates from eleven to nine. The

new Zanzibar Public Sector Workers Union (ZAPSWU)

is in place, while another merger process for private

sector unions has been initiated. It is without the

Zanzibar Teachers’ Union (ZATU). In addition, TUICO-Z

and ZAFICOWU are in last stages of merger. Should

this merger be completed, then ZATUC Affiliates will

further drop from current 9 to 7.

ZATUC continues to strengthening its working relations

with the Government of Zanzibar as well as employers’

organization. ZATUC presented a proposal for public

sector negotiation machinery to the Government and

succeeded having it established. ZATUC also played a

major role in the development of the Zanzibar Youth

Employment Action Plan and developed a strategic

plan and guidelines for combating HIV/AIDS in private

sector work places.

ZATUC Congress was held in December 2013. The

number of women leaders increased at national level

from 27 percent to 54 percent. ZATUC continued in

2015 of promoting young and women leaders in the

affiliated unions in line with its new policies on gender

and youth.

A new five year strategic plan and a work plan were

adopted, which is related on how to engage with

informal economy. So far 896 members from the

informal economy have been organized. In 2015

ZATUC set up a national union committee and informal

economy desk on informal economy to organize its

workers, and informal economy associations have been

trained on trade unionism and labour rights.

It is noteworthy to mention that the teachers union ZATU

has reached a membership rate of 52 percent of all

public teachers in Zanzibar and the largest affiliated

union in ZATUC. However, ZATU is facing a membership

saturation point, and has reached a deadlock in

collecting dues/payment arrears especially from

secondary teachers who are opposed to a flat rate of

2 percent direct check-off. In 2015 ZATU intensified its

membership service by disseminating newsletters,

training manuals and cluster visits to schools.

Regionally, ZATU is active in the federation for East

African Teachers’ Unions (FEATU) that recently gained

legal registration in Tanzania and is in the process to

finalize establishment of permanent office in Arusha

and receiving official observer status in the East Africa

Community (EAC) in line with the East African Trade

Union Confederation (EATUC) (only on issues pertaining

teachers’ rights and education matters).

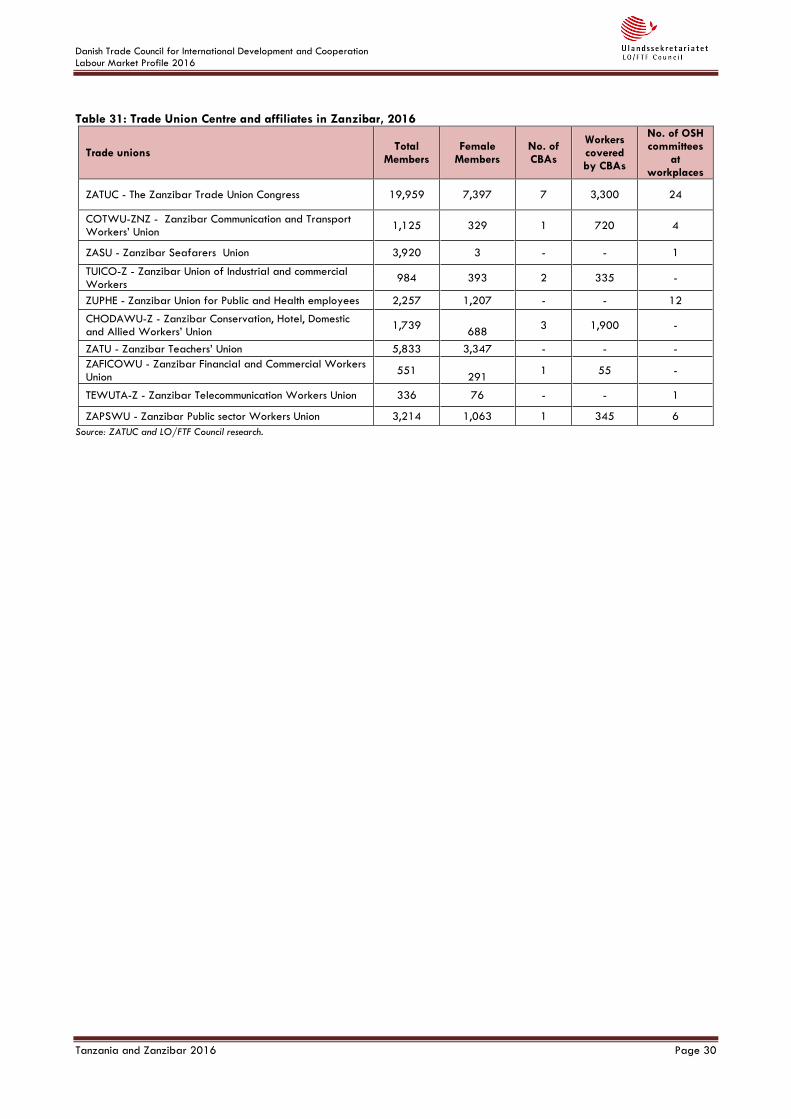

Table 31 shows details of the trade union movement’s

membership, number of Collective Bargaining

Agreements, and number of Occupational Health and

Safety Committees at workplaces.

EMPLOYERS’ ORGANISATIONS

Tanzania, mainland

Founded in 1960, the Association of Tanzania

Employers (ATE) is the main employers’ organization in

Tanzania. The organization has representatives in most

important bi/tripartite organs. Their main objective is to

enhance sustainable socio-economic development in

coordination with the government and trade union

movement.

ATE has at least 10 representatives at secretariat and

board level. Based on the limited of data availability,

the eight divisions in ATE had a total 826 enterprise

members in 2008, employing 165,089 workers, which is

roughly equivalent of 14 percent of all formal workers

(Table 4). In 2016 it has been estimated that ATE

operates with 1,300 enterprise members.3 The majority

of the enterprises are based in Dar es Salaam (70

percent) and the remainder in other parts of Tanzania

mainland.

Table 4: Membership of Association of Tanzania Employers (ATE), 2008

Divisions No. of

enterprises per division

No. of employees per

division

Agriculture 30 25,956

Banking and finance 42 10,298

Commerce 288 25,210

Industry 259 41,263

Mining 20 6,238

Oil industry 17 1,694

Utilities and services 170 54,430

Total members 826 165,089

Source: ILO, Decent Work Country Profile, Tanzania (mainland), 2010

Danish Trade Council for International Development and Cooperation

Labour Market Profile 2016

Tanzania and Zanzibar 2016 Page 4

The organization provides advisory and representation

services to its members with industrial relations, legal,

management, among others. ATE is governed by an

annual general meeting and an executive council.

ATE is an active member of Tanzania Private Sector

Foundation (TPSF) and East African Business Council

(EABC). The organization is affiliated to the

International Organization of Employers (IOE) and it is

also a founder member of the Business Africa formerly

known as Pan African Employers Confederation (PEC).

ATE participates in ILO’s annual conference of which

Tanzania is a member and has one vote as an apex

employers’ association in Tanzania. Finally, ATE is

member of the East African Employers Organization

(EAEO).

ATE launched the Female Future Program in February

2016 that aims to attract more women into

management positons, decision making processes and

on Corporate Boards.

Zanzibar

Zanzibar's employers’ organization is the Employers

Association of Zanzibar (ZANEMA). Main activities are

to represent the private sector in policy advocacy and

to conduct training workshops for members. ZANEMA

maintains good working relations with ZATUC, but the

organization faces constraints in terms of manpower

resources. Recently ZANEMA expressed that despite

hefty work permit fees to protect domestic labour

forces from alien workers, it should also apply other

measures, such as upgrading skills of the workforce.4

ZANEMA is member of the East African Employers

Organization (EAEO).

CENTRAL TRIPARTITE STRUCTURES

Tanzania, mainland

Labour, Economic and Social Council (LESCO)

LESCO advises the Minister on e.g. national labour

market policy, any proposed labour law before it is

submitted to cabinet. It also collects and compiles

information and statistics relating to the administration

of the labour laws. LESCO consists of an independent

chairperson and sixteen members all appointed by the

Minister of Labour, which represent the interest of the

government, employers, workers; and four members

appointed because of their expertise.

Meeting in LESCO have not been often, but with

occasional consultations with trade unions.

Representatives’ on some issues prior to meetings have

been effectuated albeit coordination mechanisms are

not well established. What affects the dialogue has

frequently been related to its recommendations are not

acted on by the government because of political

position.

Labour Court

The Labour Court is a division of the high court, which

settles labour disputes referred to it. This Court is

presided by a judge and two assessors from the

employers’ organizations and trade unions.

It has also been registered that there is no

administrative sanctions or fines available to labour

inspectors. According to ILO, labour inspectors are

hindered in their ability to ensure labour law

compliance because sanctioning an employer through

the courts is cumbersome and appears to depend on the

seldom-used delegation of prosecutorial authority from

the Director of Public Prosecutions.5 In addition, the

Labour Court lacks resources and processing slightly less

than half of the cases it receives.6

Commission for Mediation and Arbitration (CMA)

Labour disputes are mainly regulated and resolved by

mediation through the CMA. It is an independent

department of the government and has been operating

since 2007. The functions of this Commission are to

mediate or arbitrate in any dispute referred to the

Commission in terms of any labour laws, including

antiunion discrimination, if the parties to the dispute

agree to arbitration or the Labour Court refers a

dispute. The CMA is well functioning and therefore an

important organ in the Tanzanian labour market.7

CAM has received 10,281 cases, 6,057 have been

resolved and 4,224 have been appealed to the Labour

Court for revision during the period 2010-2015 (April)

(Table 5).

Table 5: Number of cases in Tanzania Commission for Meditation and Arbitration, 2013-2015

Year 2013 2014 2015

(Jan-April)

Total number of cases 1,751 1,732 1,285

Source: Commission for Mediation and Arbitration in Tanzania

CAM has encountered a number of challenges, e.g. no

common understanding on how Workers’ Council

contract should be prepared and applied in practice.

Likewise budgetary crisis/inadequate fund to support

and accomplish matters of workers councils at work

Danish Trade Council for International Development and Cooperation

Labour Market Profile 2016

Tanzania and Zanzibar 2016 Page 5

places, e.g. the problems with documentation when

registering the workers council contract e.g. its

commencement and expiry time

Sectoral Wage Boards

The members of the Wage Boards are appointed by

the Minister of Labour and Employment in consultation

with LESCO. The functions of the Wage Boards are to: i)

conduct an investigation on a minimum remuneration

and other conditions of employment; ii) promote

collective bargaining between registered trade unions,

employers and registered employer’s associations, and

iii) make recommendations to the Minister on minimum

wages and conditions of employment. Wage boards

have been established in sectors such as domestic

service, private security, agriculture, mining, and

health.8

Essential Services Committee

The Essential Services Committee is composed of

employers, workers, and government representatives.

Workers in certain “essential” sectors, which may not

strike without a pre-existing agreement to maintain

“minimum services”, and workers in other sectors may

also be subject to strike limitation as determined by the

Essential Services Committee. This committee has the

authority to deem periodically which services are

essential.9

Collective Bargaining Agreements (CBAs) in Tanzania

Mainland

The number of CBAs was recorded by 325 in 2016. It

has been estimated that the CBAs are covering

424,000 workers, i.e. 14 percent of the wage and

salaried workers (Table 6).

Table 6: Status of Collective Bargaining Agreements (CBAs) in Tanzania, 2016

Number of valid CBAs 325

Workers covered by CBAs 423,950

Annual increase of wages per CBAs 0-20 %

Share of wage workers covered by CBAs 14 %

Source: The Ministry Advisory Board; WageIndicator 2015, Country

Profile 2015, Tanzania; LO/FTF Council.

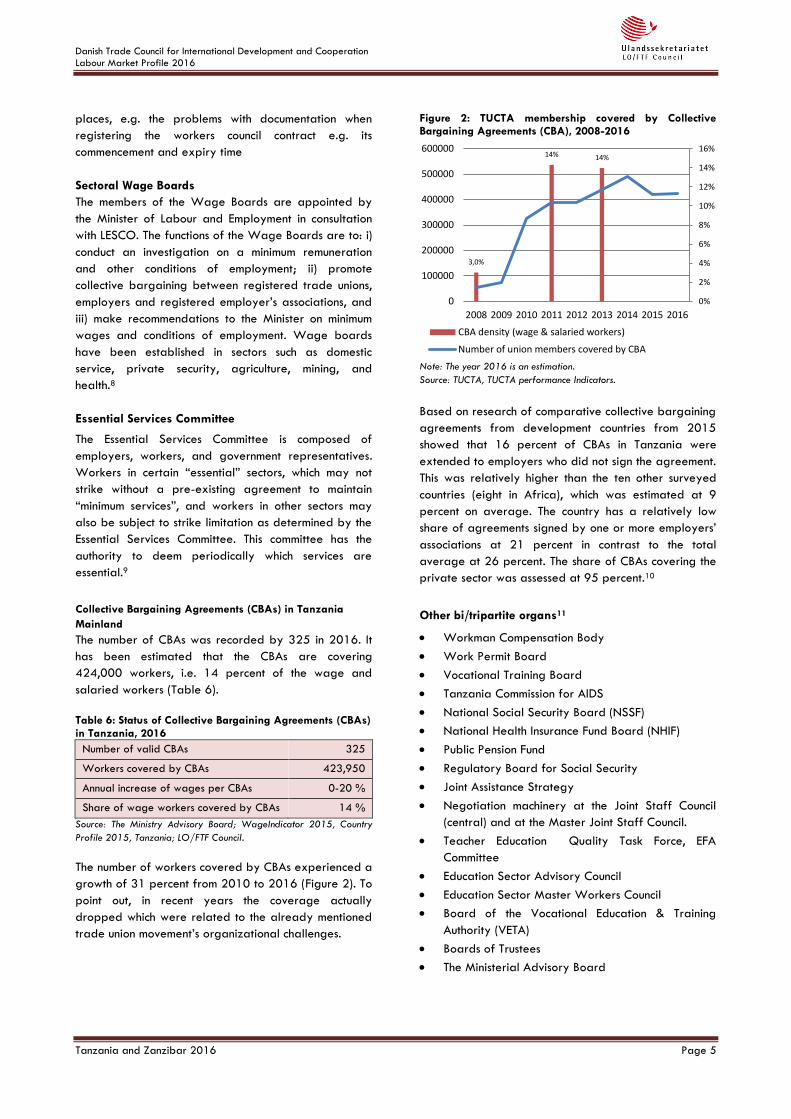

The number of workers covered by CBAs experienced a

growth of 31 percent from 2010 to 2016 (Figure 2). To

point out, in recent years the coverage actually

dropped which were related to the already mentioned

trade union movement’s organizational challenges.

Figure 2: TUCTA membership covered by Collective Bargaining Agreements (CBA), 2008-2016

Note: The year 2016 is an estimation.

Source: TUCTA, TUCTA performance Indicators.

Based on research of comparative collective bargaining

agreements from development countries from 2015

showed that 16 percent of CBAs in Tanzania were

extended to employers who did not sign the agreement.

This was relatively higher than the ten other surveyed

countries (eight in Africa), which was estimated at 9

percent on average. The country has a relatively low

share of agreements signed by one or more employers’

associations at 21 percent in contrast to the total

average at 26 percent. The share of CBAs covering the

private sector was assessed at 95 percent.10

Other bi/tripartite organs11

Workman Compensation Body

Work Permit Board

Vocational Training Board

Tanzania Commission for AIDS

National Social Security Board (NSSF)

National Health Insurance Fund Board (NHIF)

Public Pension Fund

Regulatory Board for Social Security

Joint Assistance Strategy

Negotiation machinery at the Joint Staff Council

(central) and at the Master Joint Staff Council.

Teacher Education Quality Task Force, EFA

Committee

Education Sector Advisory Council

Education Sector Master Workers Council

Board of the Vocational Education & Training

Authority (VETA)

Boards of Trustees

The Ministerial Advisory Board

3,0%

14% 14%

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

100000

200000

300000

400000

500000

600000

2008 2009 2010 2011 2012 2013 2014 2015 2016

CBA density (wage & salaried workers)

Number of union members covered by CBA

Danish Trade Council for International Development and Cooperation

Labour Market Profile 2016

Tanzania and Zanzibar 2016 Page 6

Zanzibar

Zanzibar Industrial Court

The Zanzibar Industrial Court is a division of the High

Court of Zanzibar, which settles formal labour disputes

conferred to it and like its mainland counterpart the

Zanzibar Industrial Court is presided by a judge and

two assessors from employers’ organisations and trade

unions.12 The courts are the only venue in which labour

disputes can be heard. According to an ILO labour

administration audit,13 the industrial court is functioning,

but is slow and irregular due to lack of resources.

During 2015 the government advised for the speeding

up of the establishment of industrial court. Among

others, the Ministry for Justice and Legal Affairs

initiated hearings with experts to improve the trust of

the courts as well as delimit the case delays.14

Other sources argue that Zanzibar judges and all

judicial officers, members of special departments, and

employees of the House of Representatives are

excluded from labour law protection.15

Labour Advisory Board

The Labour Advisory Board consists of nine member,

with three members each from the government,

employers and workers, all appointed by the Labour

Minister. The board provides advice on labour related

issues, such as proposed legislation, ILO conventions,

industrial relations, and working conditions. It is required

to meet four times a year.16 However, the board is

reported not to function effectively and bipartite

meetings between trade union and employers

association are very informal with general discussions.

Wages Advisory Board

The Wages Advisory Board consists of 13 members,

representing government, employers, workers, informal

economy, commerce and independent experts. It

provides recommendation for minimum wages and

working conditions. The board is required to meet twice

a year. This board takes consequential decisions

annually and one of the major recent decisions was the

new minimum wage fixing in the private sector (see

more in section: Labour Conditions). However, when the

political tensions are high the dialogue is somewhat

affected.

Collective Bargaining Agreements in Zanzibar

Unions affiliated to ZATUC have concluded 7 CBA’s,

which is up from two in 2012 (Table 7). In the private

sector, affiliated unions have negotiated at least 3

CBAs at workplaces; others still on-going.

Table 7: Status of Collective Bargaining Agreements in Zanzibar, 2016

Number of CBAs (Oct. 2016) 7

Workers covered by CBAs 3,300

Share of workers covered by CBA 5.1%

Source: ZATUC and LO/FTF Council research.

National OSH Committee

This committee negotiates for all matters concerning

labour with a legal mandate with reference to the

Labour Relation Act. Two people from each constituent

(Employer, Employee and Government) and the chair is

appointed by the minister concerning with labour.

Mainly decision is made by consensus thus the influence

of the parties is high.

Other important bi/tripartite organs

Conflict Resolution Committee

Zanzibar Social Security Board

Zanzibar Disabled Board

Zanzibar Business Council (bipartite)

MKUZA on Irrigation/Poverty Board

National Committee on HIV/AIDS

Committee on Education Policy

Aids Business Coalition Zanzibar (ABCZ)

Education Coordinating Board

National Tripartite for Dispute Handling Unit

NATIONAL LABOUR LEGISLATION

Constitution17

The Constitution applies to the United Republic of

Tanzania. The state is obliged to realize the right to

work and social welfare. The freedom of association is

guaranteed, though with several restrictions. Equal

opportunity and just remuneration is enshrined in the

constitution.

A Constitution Review process was initiated in 2013. It

was finalized in 2015. However, the constitutional

referendum was planned to be held in Tanzania in April

2015, but due to heightening political tensions, delays

to voter registration and security sectarian issues led to

be postponed.

The participating trade union representatives ensured

inclusion of labour rights clauses in a draft constitution

that awaits the coming referendum. There has been

concerns mainly relate to the division of Tanzania

mainland and Zanzibar, ethnic relations, ownership of

Danish Trade Council for International Development and Cooperation

Labour Market Profile 2016

Tanzania and Zanzibar 2016 Page 7

oil and gas reserves, among others. The same awaits

the proposed amendment of employment and labour

legislation that takes into account ILO core conventions.

***

The Tanzania mainland and Zanzibar have separate

labour laws:

Tanzania, mainland

Employment and Labour Relations Act18

The Employment and Labour Relations Act of 2004 sets

fundamental rights at work and regulates hours of

work, remuneration, leave, termination of employment,

trade unions and employers’ organizations,

organizational rights, collective bargaining, strikes and

lockouts and sets dispute resolution under the

Commission for Mediation and Arbitration. The labor

laws cover all workers, including foreign and migrant

workers.

The Labour Relations Act is contradicted by the Public

Service (Negotiation Machinery) of 200319 for civil

servants by having conflicting regulations concerning

strikes. Amendments of the Act are prepared and are

underway to parliament discussions.

Labour Institutions Act20

The Labour Institutions Act of 2004 applies to the

United Republic of Tanzania. It establishes the Labour,

Economic and Social Council, the Commission for

Mediation and Arbitration, the Essential Services

Committee, the Sectoral Wage boards, the Labour

Administration and Inspection, and the Labour Court.

According to an assessment from 2013 by the Legal

and Human Rights Centre in Tanzania, 67% of workers

are completely unaware of the labour laws.21

Zanzibar

Labour Relations Act22

Of the laws specifically to Zanzibar, the Labour

Relations Act from 2005 regulates fundamental

employees’ rights, establishes the framework for

registration of trade unions and organizations,

organizational rights, collective bargaining and

agreements, labour disputes / right to strike, dispute

prevention and resolution and establishes the Zanzibar

Industrial Court.

The Employment Act

The Employment Act from 2005 regulates fundamental

rights and protection, employment procedures and

foreign employment, contracts of service and

employment standards and rights (hours at work,

wages, leave, vacation, penalties, termination of

employment, etc.). The law also establishes the Labour

Advisory Board, wage fixing machinery and wages

protection as well as the Labour Commission and labour

inspection.

Other legislations

Several other legislations exist from Tanzania mainland

and Zanzibar which regulate and set standards and

restrictions for the labour market.23 ILO has registered

a total 283 national labour, social security and related

human rights legislations. Six were registered in 2015

(none in 2014 and 2016) (see also Table 8):

Employment and Labour Laws (Miscellaneous

Amendments) Act, 2015.

Zanzibar Public Leaders Code of Ethics Act, 2015

(Act No. 4 of 2015).

Youth Council of Tanzania Act, 2015 (registered

among ‘Elimination of child labour, protection of

children and young persons’ as well as

‘Employment policy, promotion of employment and

employment services’).

Non-Citizens (Employment Regulations) Act 2015.

Teacher's Service Commission Act, 2015 (No. 25 of

2015).

Table 8: Status of the national labour, social security and human rights related legislations in Tanzania

2014 2015 2016

Number of new legislations 0 6 0

Source: ILO, NATLEX, Tanzania

Observations on the labour legislation

Equally important the International Trade Union

Confederation (ITUC) has registered several

observations of the legislations. Among others, they

vary from:24

Power to refuse official registration on arbitrary,

unjustified or ambiguous grounds;

formalities or requirements which excessively delay

or substantially impair the free establishment of

organizations;

restrictions on trade unions’ right to establish

branches, federation and confederation or to

affiliate with national and international

organizations;

administrative authorities’ power to unilaterally

dissolve, suspend or de-register trade union

organizations;

Danish Trade Council for International Development and Cooperation

Labour Market Profile 2016

Tanzania and Zanzibar 2016 Page 8

Compulsory conciliation and/or binding arbitration

procedure in the event of disputes during collective

bargaining, other than in essential services;

Compulsory recourse to arbitration, or to long and

complex conciliation and mediation procedures

prior to strike actions; and

discretionary determination or excessively long list

of “essential services” in which the right to strike is

prohibited or severely restricted.

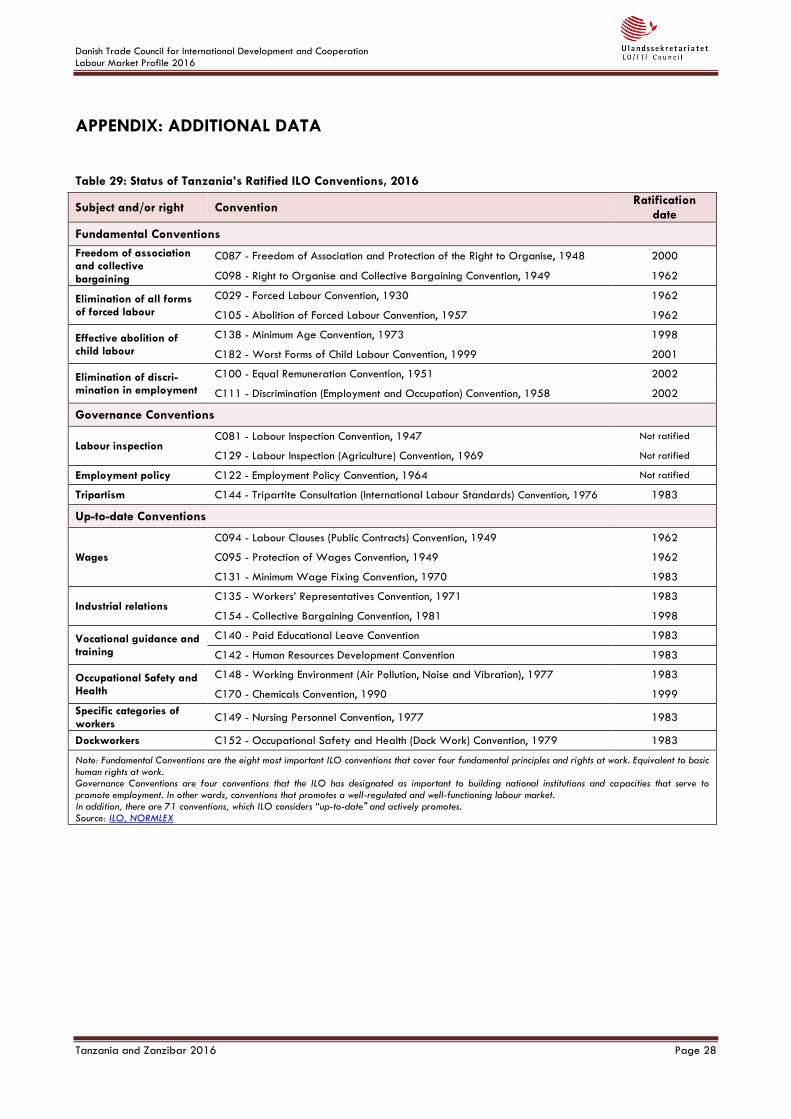

Ratified ILO Conventions

With reference to Tanzania’s ratification of

international labour standards, a total 35 ILO

Conventions are ratified (see also Appendix Table

29):25

Ratifications for the United Republic of Tanzania

Fundamental Conventions: 8 of 8.

Governance Conventions (Priority): 1 of 4

Technical Conventions: 26 of 177.

Out of 35 Conventions ratified by Tanzania, of

which 34 are in fovece, 1 Convention has been

denounced; none has been ratified in the past 12

months.

The latest ratified Conventions were the Discrimination

(Employment and Occupation) Convention (C111) and

the Equal Remuneration Convention (C100), both from

February 2002.

A tripartite plan of action of promoting the ratification

of the Domestic Workers Convention No. 189 was

launched in February 2014.

With reference to the Article 22 of the ILO Constitution,

i.e. annual reports on ratified Conventions, both the

International Organization of Employers (IOE) and ITUC

had observations to the Convention 87 on Freedom of

Association and Protection of the Right to Organise in

Tanzania in 2015; only the latter organization received

responses from the government, so far.26

TRADE UNION RIGHTS VIOLATIONS

Tanzania has been ranked as 3 out of 5 at ITUC’s

Global Rights Index since 2014 (Table 9), which was

classified as ‘regular violations of rights’. This is

interpreted as governments and/or companies are

regularly interfering in collective labour rights or are

failing to fully guarantee important aspects of these

rights. There are deficiencies in laws and/or certain

practices which make frequent violations possible.

Table 9: Global Rights Index, Tanzania ranking, 2014-2016

2014 2015 2016

Ranking on the Global Rights

Index 3 3 3

Note: Five clusters in total with ratings from 1 to 5. A country is

assigned the rating 5+ by default, if the rule of law has completely

broken down.

Source: ITUC, Global Rights Index

ITUC registered one case on the regular violations of

rights in 2015.27 This was related to the labour division

of Tanzania’s High Court ruled that a strike by workers

of Tanzania-Zambia Authority Railways Authority

(TAZARA) was illegal. It had been agreed workers

would resume work if the salary arrears were paid.

However, not all salary arrears were paid in time, and

other demands were not met. The government ordered

the workers to resume work, failing which they would

lose their jobs, and directed the TAZARA management

to keep a record of the number of days the workers

were on strike and deduct their salaries accordingly.

A similarly problem was repeated. TAZARA workers

went on strike but were ordered back to work by the

High Court. The strike was called to demand five

months’ salary arrears. The strikers returned to work

after receiving promises that their salaries would be

paid. The workers did start receiving their salary

arrears, after they returned to work, but the process

was slow.

According to the U.S. Annual Country Report on Human

Rights Practices 2015, 28 many private sector employers

adopt antiunion policies or tactics, although case law

discourages discriminatory activities by an employer

against union members. This is on both the mainland and

Zanzibar.

Other antiunion activities were registered such as

international mining interests engaged in paying

officials from the Ministry of Labour Inspectorate to

ignore worker complaints or to write favorable reports

on working conditions. It was also registered that during

2015 some mining interests barred unions from

organizing and used security staff to block labour

inspectors from entering mines. TUCTA officials stated

there were many instances of discrimination against

union workers. Mining companies reportedly established

employer-controlled unions called “welfare committees”

and declared workers redundant to prevent organizers

from starting a union. The Tanzanian Mining and

Construction Workers Union (TAMICO) reported 120

active cases of unfair termination involving mining

companies in different stages of adjudication. TUCTA

Danish Trade Council for International Development and Cooperation

Labour Market Profile 2016

Tanzania and Zanzibar 2016 Page 9

also reported cases of hotels and construction firms

dismissing employees for attempting to unionize.

Both Tanzania mainland and Zanzibar have no cases

with the ILO's Committee of Freedom of Association.29

WORKING CONDITIONS

In Tanzania mainland minimum wages are fixed by the

Government after tripartite consultation in the LESCO

based on recommendations from 12 sub-sectoral wage

boards.

In July 2014 the minimum wages for public sector were

raised from 200,000 TZS (US$120) to 240,000 TZS

(US$144). TUCTA and the Ministry of Labour agreed to

increase minimum wages by 11 percent in 2015/16,

but in future, minimum wage negotiations will be dealt

by special wage regulatory committees and social

partners. Public civil servants have received increased

travel allowances (up to 50 percent) after years of

lobbying by trade unions to align salaries with the

rising cost of travelling fees and accommodations.

The government announced in July 2014 a substantial

increase in private sector minimum wages up to 65

percent. The decision to raise statutory minimum wages

for private sector employees came after years of

debate. The announced increase brought the minimum

wages to TZS 40,000 (US$25) per month for domestic

workers, which is the lowest, while TZS 400,000

(US$248) for workers in the commercial and

communication services is the highest (Table 10).

TUCTA has been advocating and lobbying for a

minimum wage policy, wage boards for public sector

put in place; and reduction of tax rates for low income

earners. Intensive TUCTA protests have eventually

caused the President to form a tripartite task force to

sort out the issue. As a result a new minimum salary

raise was reached in June 2015 at TZS 310,000

(US$167) per month. In addition, the Pay-As-You-Earn

(PAYE) – i.e. withholding tax on taxable incomes of

employees - was reduced from 12 percent in 2014 to

11 percent in 2015 (June) for income between TZS

170,000-360,000 per month. No income tax under TZS

170,000 per month. The government promised in May

2016 a PAYE reduction of 2 percent across the board

and it was welcomed by TUCTA and ATE. Be as it may,

the inflation of consumer prices, the exchange rate and

consumable tax increases are curbing the salaries tax-

cuts.

According to the Income Tax Act from 2004, the

resident individual income tax rates applicable in

Zanzibar differ from those which are applicable the

Mainland. The public sector minimum wage in Zanzibar

increased from TZS 180,000 (US$111) in 2013 to TZS

300,000 (US$137) per month from April 2016,

reaching an increase of 66 percent. In 2010, before the

minimum wage increase, the median wage was around

TZS 170,000 (US$122), notably higher than on the

mainland. It has been observed that officials

responsible for checking minimum wages are often

corrupt, with the result that some rival businesses can

ignore the law without being penalized, which includes

kept in check enterprises in the informal economy.30

Table 10: Wages and earnings Monthly average and legal minimum wages

Current Shilling (TZS)

Current US$

Tanzania, nation wide

Mean nominal, average wage (2012)

356,666 226

Minimum wage, average (2015) 310,000 167

Tanzania, mainland

Highest minimum wage (2013-16) 400,000 248

Lowest minimum wage (2013-16) 40,000 25

Median wage (2012) 114,400 72

Zanzibar

Minimum wage (public sector) (2016)

300,000 137

Median Wage (2010) 170,000 122

Source: ILO, Global Wage Report; The Citizen, Minimum salary raised

to Sh310,000, May 19, 2015; WageIndicator.org, Minimum Wages

in Tanzania with effect from 01-07-2013 to 30-06-2016; and

WageIndicator.org, Minimum Wages in Zanzibar with effect from 01-

04-2016.

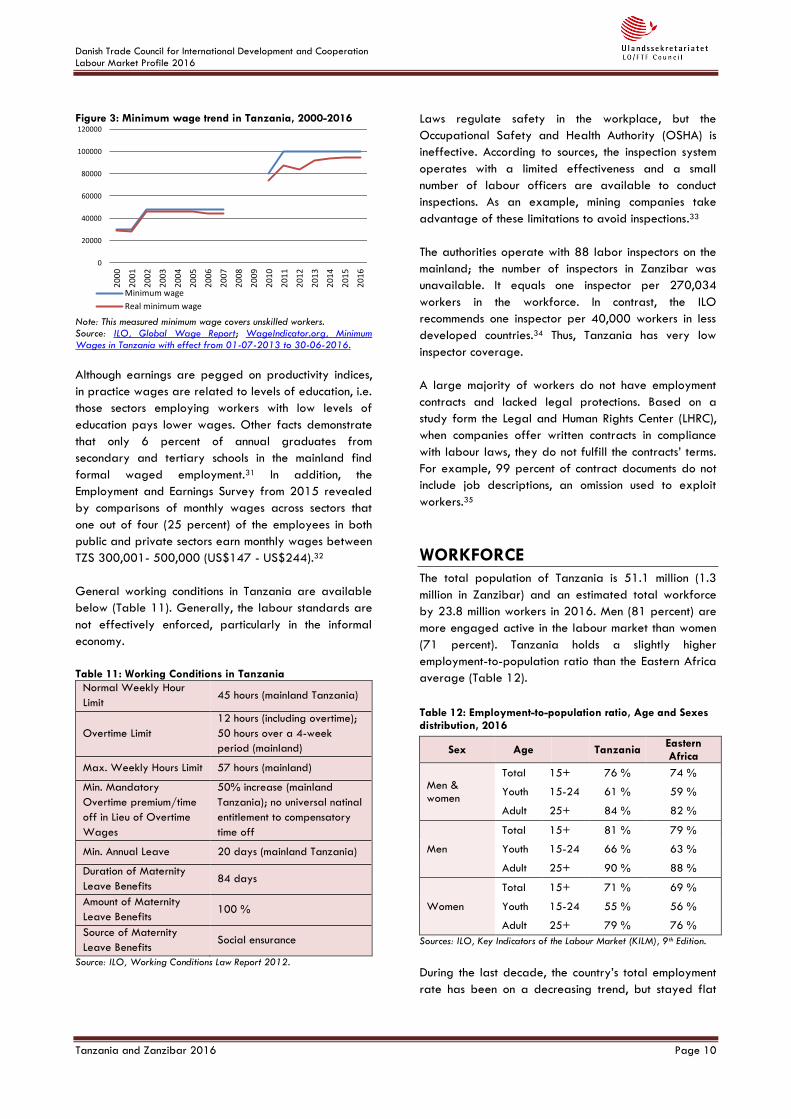

The real minimum wage has been affected negatively

by the rising inflation in consumer prices during the

2010s, so far (Figure 3 & Figure 23).

Danish Trade Council for International Development and Cooperation

Labour Market Profile 2016

Tanzania and Zanzibar 2016 Page 10

Figure 3: Minimum wage trend in Tanzania, 2000-2016

Note: This measured minimum wage covers unskilled workers. Source: ILO, Global Wage Report; WageIndicator.org, Minimum Wages in Tanzania with effect from 01-07-2013 to 30-06-2016.

Although earnings are pegged on productivity indices,

in practice wages are related to levels of education, i.e.

those sectors employing workers with low levels of

education pays lower wages. Other facts demonstrate

that only 6 percent of annual graduates from

secondary and tertiary schools in the mainland find

formal waged employment.31 In addition, the

Employment and Earnings Survey from 2015 revealed

by comparisons of monthly wages across sectors that

one out of four (25 percent) of the employees in both

public and private sectors earn monthly wages between

TZS 300,001- 500,000 (US$147 - US$244).32

General working conditions in Tanzania are available

below (Table 11). Generally, the labour standards are

not effectively enforced, particularly in the informal

economy.

Table 11: Working Conditions in Tanzania

Normal Weekly Hour

Limit 45 hours (mainland Tanzania)

Overtime Limit

12 hours (including overtime);

50 hours over a 4-week

period (mainland)

Max. Weekly Hours Limit 57 hours (mainland)

Min. Mandatory

Overtime premium/time

off in Lieu of Overtime

Wages

50% increase (mainland

Tanzania); no universal natinal

entitlement to compensatory

time off

Min. Annual Leave 20 days (mainland Tanzania)

Duration of Maternity

Leave Benefits 84 days

Amount of Maternity

Leave Benefits 100 %

Source of Maternity

Leave Benefits Social ensurance

Source: ILO, Working Conditions Law Report 2012.

Laws regulate safety in the workplace, but the

Occupational Safety and Health Authority (OSHA) is

ineffective. According to sources, the inspection system

operates with a limited effectiveness and a small

number of labour officers are available to conduct

inspections. As an example, mining companies take

advantage of these limitations to avoid inspections.33

The authorities operate with 88 labor inspectors on the

mainland; the number of inspectors in Zanzibar was

unavailable. It equals one inspector per 270,034

workers in the workforce. In contrast, the ILO

recommends one inspector per 40,000 workers in less

developed countries.34 Thus, Tanzania has very low

inspector coverage.

A large majority of workers do not have employment

contracts and lacked legal protections. Based on a

study form the Legal and Human Rights Center (LHRC),

when companies offer written contracts in compliance

with labour laws, they do not fulfill the contracts’ terms.

For example, 99 percent of contract documents do not

include job descriptions, an omission used to exploit

workers.35

WORKFORCE

The total population of Tanzania is 51.1 million (1.3

million in Zanzibar) and an estimated total workforce

by 23.8 million workers in 2016. Men (81 percent) are

more engaged active in the labour market than women

(71 percent). Tanzania holds a slightly higher

employment-to-population ratio than the Eastern Africa

average (Table 12).

Table 12: Employment-to-population ratio, Age and Sexes distribution, 2016

Sex Age Tanzania Eastern Africa

Men & women

Total 15+ 76 % 74 %

Youth 15-24 61 % 59 %

Adult 25+ 84 % 82 %

Men

Total 15+ 81 % 79 %

Youth 15-24 66 % 63 %

Adult 25+ 90 % 88 %

Women

Total 15+ 71 % 69 %

Youth 15-24 55 % 56 %

Adult 25+ 79 % 76 %

Sources: ILO, Key Indicators of the Labour Market (KILM), 9th Edition.

During the last decade, the country’s total employment

rate has been on a decreasing trend, but stayed flat

0

20000

40000

60000

80000

100000

120000

20

00

20

01

20

02

20

03

20

04

20