1

“We Accelerate Growth” May 2014

Key Trends in the Turkish Energy

Market

Potential Opportunities and Pitfalls for

Investors

2

Key trends in the Turkish energy market

Source: Frost & Sullivan analysis.

Key Trends in the Turkish Market

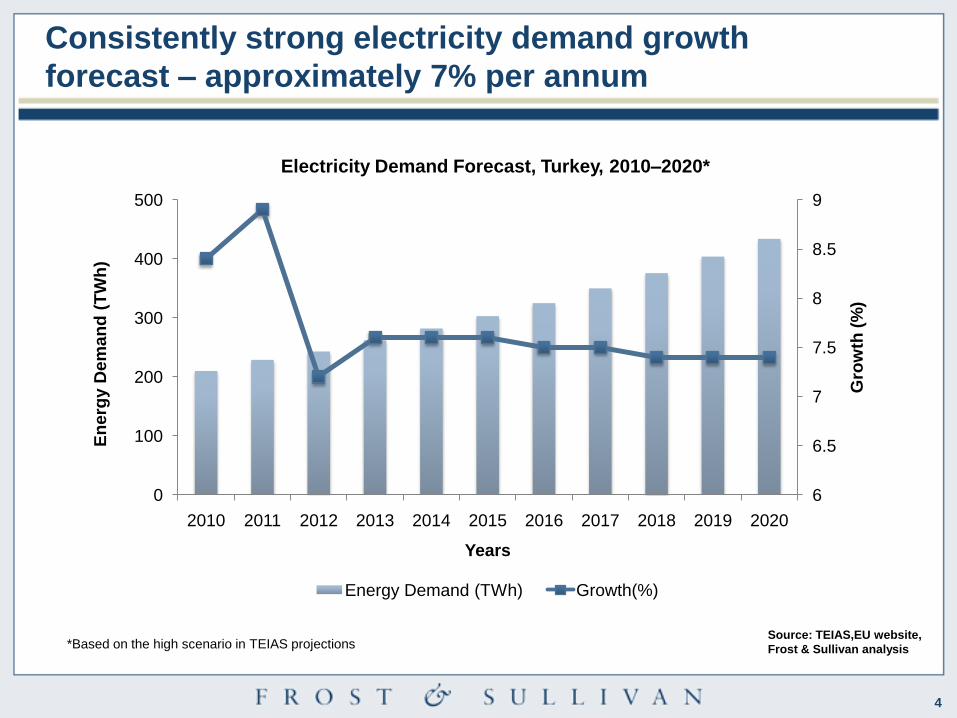

1Demand for power will continue to rise at approximately 7% per year, necessitating

new capacity additions

2The market reform process is progressing with private companies keen to expand their

presence in the market

3Turkey’s fuel mix will diversify, with greater investment in renewables. Coal and gas will

remain a key element of the fuel mix

4Once a functioning bureaucracy is in place, the solar power market is expected to

boom fuelled particularly by the 'below 500 kW regulation'. This regulation will unlock a

significant amount of investment

5Power generation is dominated by local, diversified industrial groups. While several

international utilities are partnering with Turkish companies, most projects are run solely

by local companies, involved in the construction industry

6New competitors are continuing to emerge though and international investors are also

keen to expand their presence

7With most equipment imported from abroad, Turkey is an attractive market for

equipment OEMs. The presence of Chinese players is increasing

8There remains a bottleneck around financing, but this can be overcome as global

lending conditions improve

3

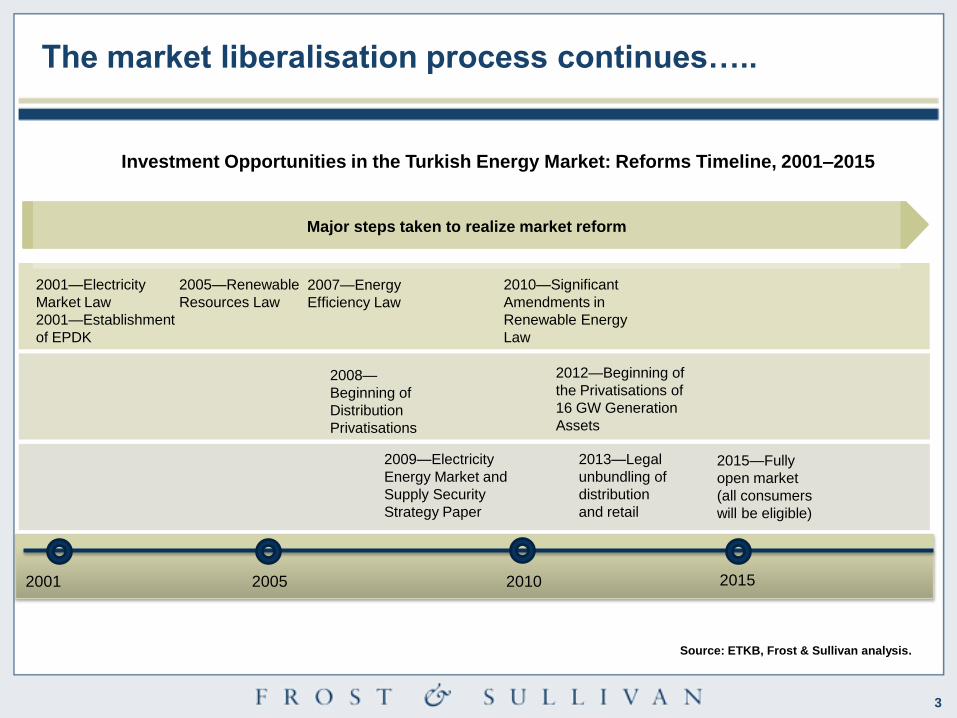

Source: ETKB, Frost & Sullivan analysis.

2001 2005 2010 2015

2001—Electricity

Market Law

2001—Establishment

of EPDK

2005—Renewable

Resources Law

2007—Energy

Efficiency Law

2010—Significant

Amendments in

Renewable Energy

Law

Major steps taken to realize market reform

Investment Opportunities in the Turkish Energy Market: Reforms Timeline, 2001–2015

2008—

Beginning of

Distribution

Privatisations

2012—Beginning of

the Privatisations of

16 GW Generation

Assets

2015—Fully

open market

(all consumers

will be eligible)

2013—Legal

unbundling of

distribution

and retail

2009—Electricity

Energy Market and

Supply Security

Strategy Paper

The market liberalisation process continues…..

4

Electricity Demand Forecast, Turkey, 2010–2020*

Source: TEIAS,EU website,

Frost & Sullivan analysis*Based on the high scenario in TEIAS projections

6

6.5

7

7.5

8

8.5

9

0

100

200

300

400

500

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Gro

wth

(%

)

En

erg

y D

em

an

d (

TW

h)

Years

Energy Demand (TWh) Growth(%)

Consistently strong electricity demand growth

forecast – approximately 7% per annum

5

0

3 000

6 000

9 000

12 000

15 000

18 000

21 000

2011 2023

Ins

talle

d C

ap

ac

ity (

MW

)

Expansion of Coal, 2011 and 2023

Installed Capacity by Share of Coal, 2011

Source: ETKB,TKI, Frost & Sullivan analysis.

*

* 17.5 GW is the set target of the government which is stated

as 17-18 GW until 2023.

12.4

GW

12.4 GW

17.5 GW

Coal24%

Others76%

Of the 12.4GW of capacity, 8.5GW utilises

domestic coal reserves. Turkey has 11.8 billion

tonnes of reserves; 1.3 billion tonnes of hard-

coal and 10.8 billion tonnes of lignite.

Coal plants built between 1980 and 1990 are

currently being privatised. A further 7GW of

capacity is being lined up to be tendered to the

private sector.

Despite government pronouncements on using

domestic coal, a high amount of investment is

planned based on imported coal, determined

from the licences currently under assessment

and examination. Project developers are

preferring to utilise higher calorific valued-coal, in

order to ensure higher returns and a shorter ROI.

Recent study predicts 5GW of additional coal

capacity to be online by 2023

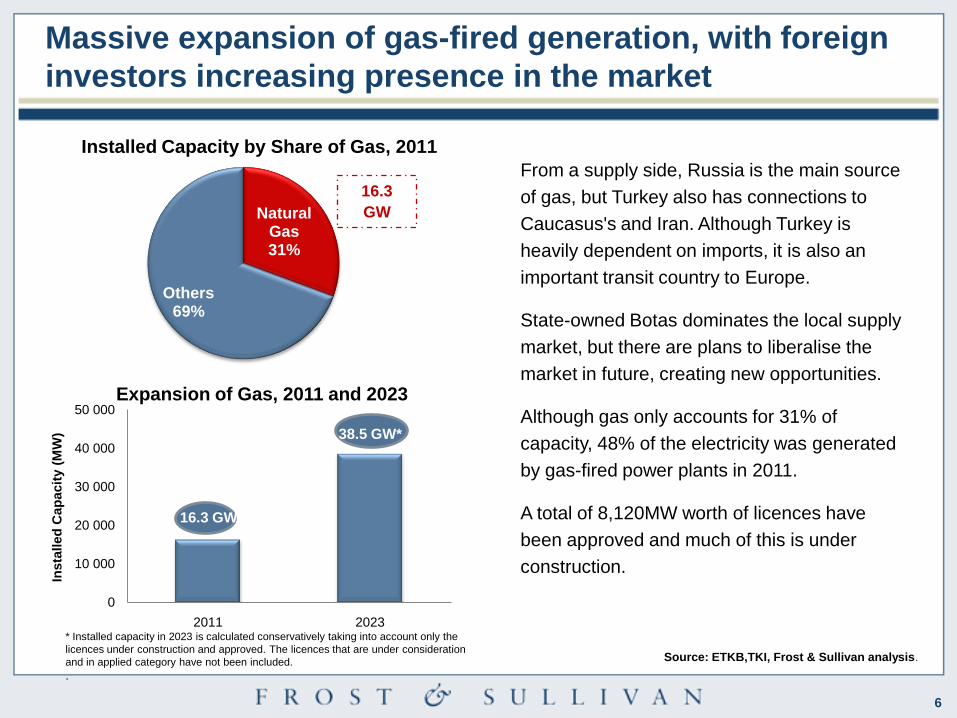

6

Natural Gas31%

Others69%

Expansion of Gas, 2011 and 2023

Installed Capacity by Share of Gas, 2011

Source: ETKB,TKI, Frost & Sullivan analysis.

From a supply side, Russia is the main source

of gas, but Turkey also has connections to

Caucasus's and Iran. Although Turkey is

heavily dependent on imports, it is also an

important transit country to Europe.

State-owned Botas dominates the local supply

market, but there are plans to liberalise the

market in future, creating new opportunities.

Although gas only accounts for 31% of

capacity, 48% of the electricity was generated

by gas-fired power plants in 2011.

A total of 8,120MW worth of licences have

been approved and much of this is under

construction.

Massive expansion of gas-fired generation, with foreign

investors increasing presence in the market

16.3 GW

38.5 GW*

* Installed capacity in 2023 is calculated conservatively taking into account only the

licences under construction and approved. The licences that are under consideration

and in applied category have not been included.

.

0

10 000

20 000

30 000

40 000

50 000

2011 2023

Insta

lled

Cap

acit

y (

MW

)

16.3

GW

7

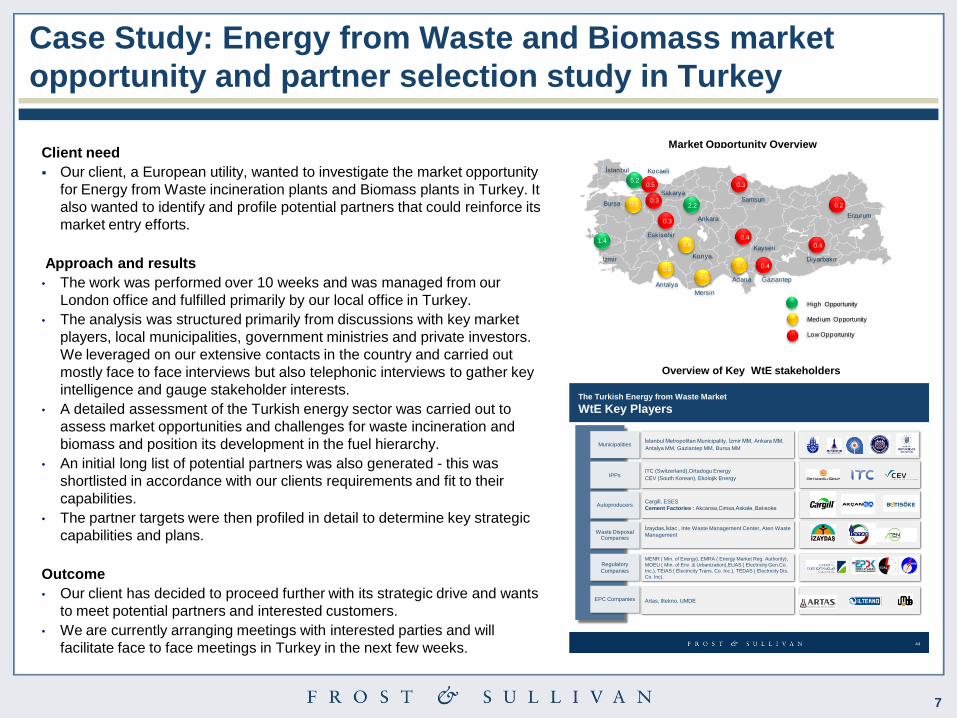

Client need

Our client, a European utility, wanted to investigate the market opportunity

for Energy from Waste incineration plants and Biomass plants in Turkey. It

also wanted to identify and profile potential partners that could reinforce its

market entry efforts.

Approach and results

• The work was performed over 10 weeks and was managed from our

London office and fulfilled primarily by our local office in Turkey.

• The analysis was structured primarily from discussions with key market

players, local municipalities, government ministries and private investors.

We leveraged on our extensive contacts in the country and carried out

mostly face to face interviews but also telephonic interviews to gather key

intelligence and gauge stakeholder interests.

• A detailed assessment of the Turkish energy sector was carried out to

assess market opportunities and challenges for waste incineration and

biomass and position its development in the fuel hierarchy.

• An initial long list of potential partners was also generated - this was

shortlisted in accordance with our clients requirements and fit to their

capabilities.

• The partner targets were then profiled in detail to determine key strategic

capabilities and plans.

Outcome

• Our client has decided to proceed further with its strategic drive and wants

to meet potential partners and interested customers.

• We are currently arranging meetings with interested parties and will

facilitate face to face meetings in Turkey in the next few weeks.

Case Study: Energy from Waste and Biomass market

opportunity and partner selection study in Turkey

Overview of Key WtE stakeholders

Market Opportunity Overview

İstanbul Kocaeli

Sakarya

Eskisehir

Ankara

Samsun

Erzurum

Izmir

Antalya

Konya.

Mersin

Adana

Kayseri

Gaziantep

Diyarbakır

Bursa

5.2

1.4

2.2 0.2

0.3

0.3

0.3

0.6

0.6

0.70.8

0.8

0.4

0.4

0.4

0.5

High Opportunity

Medium Opportunity

Low Opportunity

44

İstanbul Metropolitan Municipality, İzmir MM, Ankara MM,

Antalya MM, Gaziantep MM, Bursa MMMunicipalities

EPC Companies

Regulatory

Companies

IPPs

Autoproducers

Waste Disposal Companies

The Turkish Energy from Waste Market

WtE Key Players

ITC (Switzerland),Ortadogu Energy

CEV (South Korean), Ekolojik Energy

Cargill, ESES

Cement Factories : Akcansa,Cimsa,Askale, Batısoke

İzaydas,İstac , Inte Waste Management Center, Aten Waste

Management

MENR ( Min. of Energy), EMRA ( Energy Market Reg. Authority),

MOEU ( Min. of Env .& Urbanization),EUAS ( Electricity Gen.Co.

Inc.), TEIAS ( Electricity Trans. Co. Inc.), TEDAS ( Electricity Dis.

Co. Inc).

Artas, Iltekno, UMDE

8

Hydro32%

Others68%

Expansion of Hydropower, 2011 and 2023

Installed Capacity by Share of Hydropower, 2011 The current installed capacity as of 2011, was

17.1GW, with 15.2 GW of hydropower plants

under construction.

On the equipment supply side, Turkey has

increasingly become a battleground as

Chinese manufacturers have been increasing

their presence in the market, especially

supplying hydro turbines below 15MW. Over

15 MW, the investors tend to work with the

Western OEMs such as Voith

Hydro, Alstom, and Andritz Hydro.

Challenges facing the market include:

• Poor coordination between the responsible

corporations

• Public protest based on the environmental

impacts

• Lack of control mechanism of the

hydropower plants during

feasibility, construction, and after

commissioning period.

Significant expansion of hydropower + refurbishment

work makes Turkey a key European market

17.1

GW

0

10000

20000

30000

40000

50000

2011 2023

Insta

lled C

apacity

(MW

)

Years

17.1 GW

45 GW*

*45 GB represents the government’s set target in the 2009 strategy paper. The projects in the pipeline indicate that things are on track as planned and the target

is reachable if conflicts stemming from environmental problems can be solved with necessary precautions.

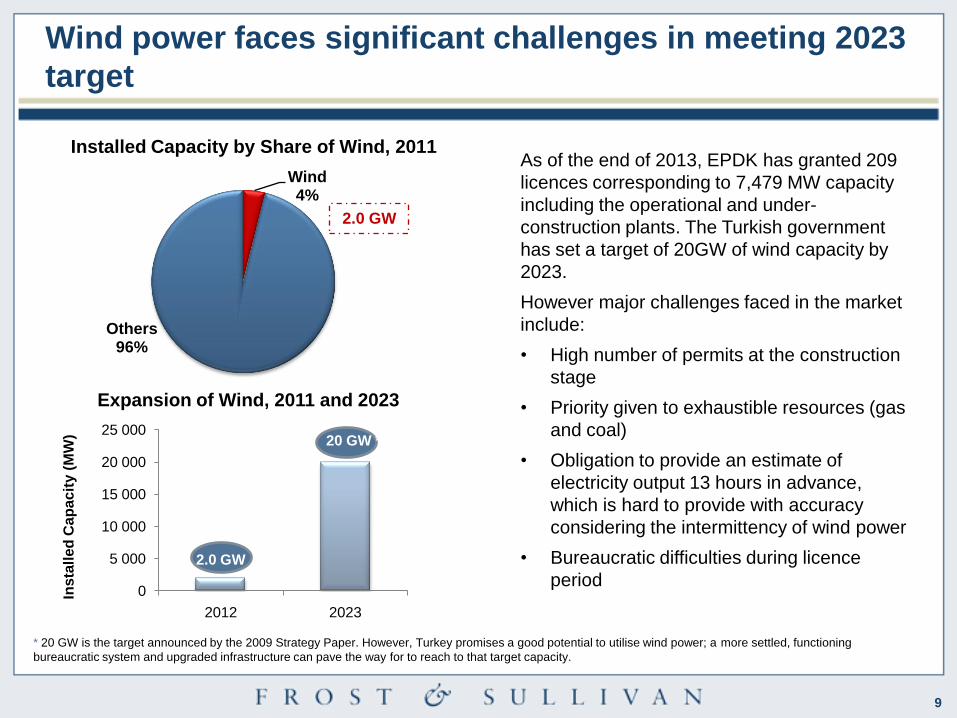

9

Wind4%

Others96%

Expansion of Wind, 2011 and 2023

Installed Capacity by Share of Wind, 2011As of the end of 2013, EPDK has granted 209

licences corresponding to 7,479 MW capacity

including the operational and under-

construction plants. The Turkish government

has set a target of 20GW of wind capacity by

2023.

However major challenges faced in the market

include:

• High number of permits at the construction

stage

• Priority given to exhaustible resources (gas

and coal)

• Obligation to provide an estimate of

electricity output 13 hours in advance,

which is hard to provide with accuracy

considering the intermittency of wind power

• Bureaucratic difficulties during licence

period

Wind power faces significant challenges in meeting 2023

target

2.0 GW

0

5 000

10 000

15 000

20 000

25 000

2012 2023

Ins

tall

ed

Ca

pa

cit

y (

MW

)

2.0 GW

20 GW *

* 20 GW is the target announced by the 2009 Strategy Paper. However, Turkey promises a good potential to utilise wind power; a more settled, functioning

bureaucratic system and upgraded infrastructure can pave the way for to reach to that target capacity.

10

The Client: A Global Tier 1 Supply of Wind Turbines

The Challenge Project Objectives

A leading global supplier of wind turbines has

recently entered the market in Turkey. Given

its late entrance to the market, the company

wanted to gain detailed insights into the

market trends and dynamics to ascertain the

realistic market opportunity. In addition, our

client wanted to understand the operational

activities of competitors in order to ramp up its

business in an optimal manner through best

practices and lessons learned in the market.

• To assess the market opportunity of the wind power

plant services market in revenues;

• To forecast the market size to 2017 (with 2012 as the

base year)

• To identify key trends, revenues drivers/enablers and

restraints and how this will impact the market;

• To identify key competitors and provide detailed profiles

on their operational architecture; and

• To provide key conclusions and actionable

recommendations for our client to maximise their

success in this market.

Our Approach and Work

Frost and Sullivan initially utilised data from out internal studies, key public sources and databases. These

were used as a platform on which the remaining market intelligence was built. Our analysts used detailed

expert interviews with key market participants to uncover the details and provide insightful results. Overall, 30

interviews were conducted.

Outcome and Business Impact

The client will use the data to plan its next operational investments in Turkey to build its wind power services

networks most effectively incurring the least investments that will have the maximum coverage for its

customers. The intelligence will feed into the structured roll out of team build up and the ramp up of its

capabilities.

Case Study: Strategic Analysis of the Wind Power

Services Market in Turkey

11

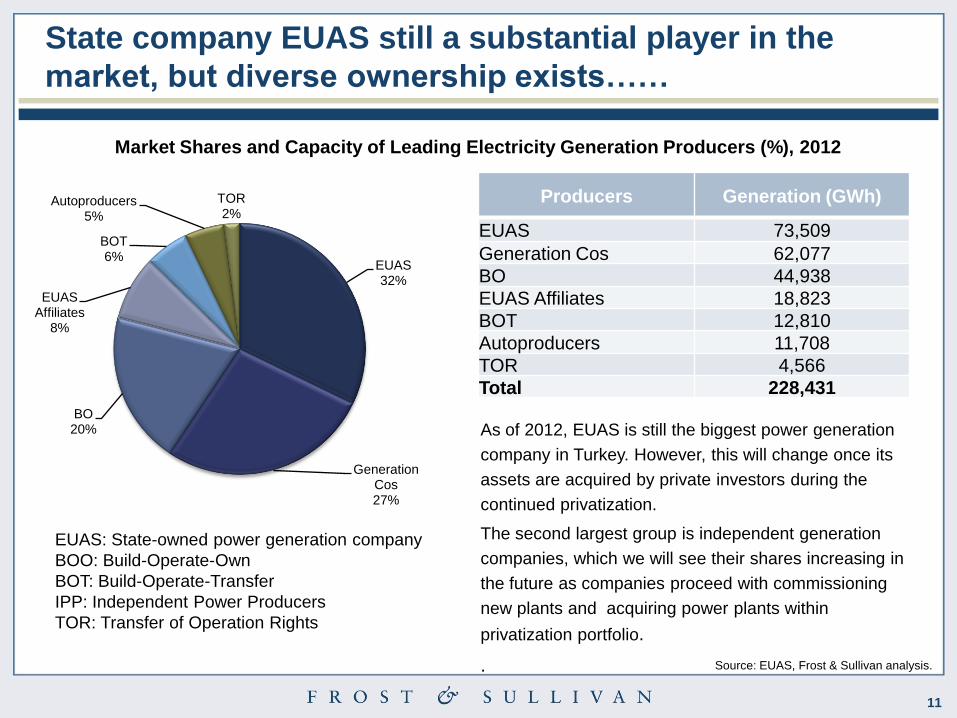

State company EUAS still a substantial player in the

market, but diverse ownership exists……

Market Shares and Capacity of Leading Electricity Generation Producers (%), 2012

EUAS: State-owned power generation company

BOO: Build-Operate-Own

BOT: Build-Operate-Transfer

IPP: Independent Power Producers

TOR: Transfer of Operation Rights

As of 2012, EUAS is still the biggest power generation

company in Turkey. However, this will change once its

assets are acquired by private investors during the

continued privatization.

The second largest group is independent generation

companies, which we will see their shares increasing in

the future as companies proceed with commissioning

new plants and acquiring power plants within

privatization portfolio.

. Source: EUAS, Frost & Sullivan analysis.

EUAS32%

Generation Cos27%

BO 20%

EUAS Affiliates

8%

BOT6%

Autoproducers5%

TOR2%

Producers Generation (GWh)

EUAS 73,509

Generation Cos 62,077

BO 44,938

EUAS Affiliates 18,823

BOT 12,810

Autoproducers 11,708

TOR 4,566

Total 228,431

12

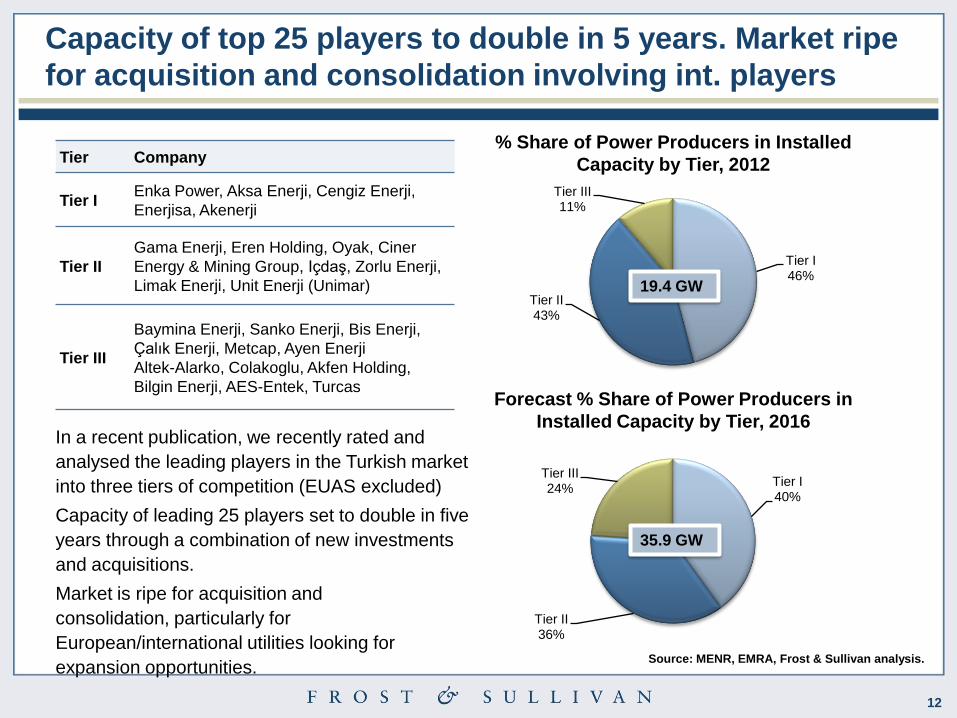

Capacity of top 25 players to double in 5 years. Market ripe

for acquisition and consolidation involving int. players

Tier Company

Tier IEnka Power, Aksa Enerji, Cengiz Enerji,

Enerjisa, Akenerji

Tier II

Gama Enerji, Eren Holding, Oyak, Ciner

Energy & Mining Group, Içdaş, Zorlu Enerji,

Limak Enerji, Unit Enerji (Unimar)

Tier III

Baymina Enerji, Sanko Enerji, Bis Enerji,

Çalık Enerji, Metcap, Ayen Enerji

Altek-Alarko, Colakoglu, Akfen Holding,

Bilgin Enerji, AES-Entek, Turcas

Source: MENR, EMRA, Frost & Sullivan analysis.

Tier I40%

Tier II 36%

Tier III24%

Tier I46%

Tier II43%

Tier III11%

% Share of Power Producers in Installed

Capacity by Tier, 2012

Forecast % Share of Power Producers in

Installed Capacity by Tier, 2016

19.4 GW

35.9 GW

In a recent publication, we recently rated and

analysed the leading players in the Turkish market

into three tiers of competition (EUAS excluded)

Capacity of leading 25 players set to double in five

years through a combination of new investments

and acquisitions.

Market is ripe for acquisition and

consolidation, particularly for

European/international utilities looking for

expansion opportunities.

13

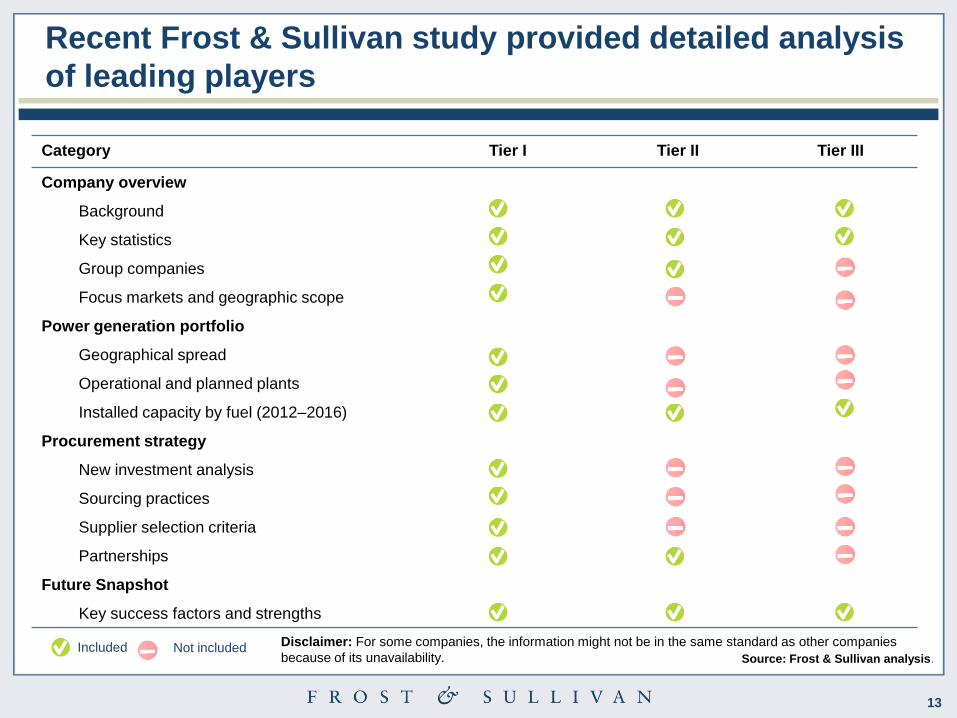

Recent Frost & Sullivan study provided detailed analysis

of leading players

Category Tier I Tier II Tier III

Company overview

Background

Key statistics

Group companies

Focus markets and geographic scope

Power generation portfolio

Geographical spread

Operational and planned plants

Installed capacity by fuel (2012–2016)

Procurement strategy

New investment analysis

Sourcing practices

Supplier selection criteria

Partnerships

Future Snapshot

Key success factors and strengths

Not includedIncluded Disclaimer: For some companies, the information might not be in the same standard as other companies

because of its unavailability. Source: Frost & Sullivan analysis.

14

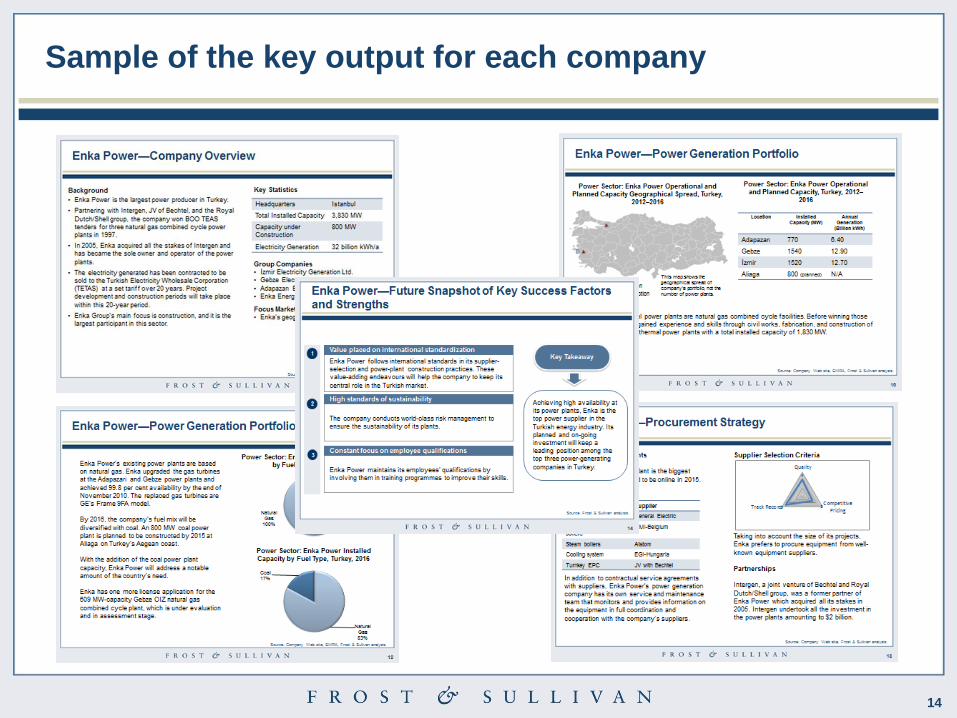

Sample of the key output for each company

15

0

20

40

60

80

100

120

140

160

180

200

2011 2012 2013 2014 2015 2016 2017

Industry 3.6 3.9 4.2 4.5 4.9 5.4 5.9

OIZ 6.4 7.2 7.8 8.5 9.5 10.6 11.5

Gas & Water Distribution 8.3 9.2 11.1 12.1 13.0 13.8 14.6

Power Distribution 62.0 71.3 75.1 80.7 86.5 93.0 100.5

Power Tranmission 9.7 7.6 8.1 10.2 9.9 10.6 10.9

Power Generation - - 4.3 6.9 10.3 15.3 22.1

To

tal M

ark

et

Reve

nu

es

(€

Mil

lio

n)

Total Market Revenues by Sectors, 2011 - 2017

CAGR: 10.8 %

Massive investment forecast for T&D, as Turkey seeks to

boost grid performance

16

The Challenge Project Objectives

A world leader for smart grid and automation

equipment wanted to assess the market

opportunity and develop a strategic road map

for Smart Grids Services and Solutions in

Turkey. The client wanted to assess 5 key

customer segments namely; power

generation, power transmission, power

distribution, organised industrial zones and

infrastructure and transportation.

• Provide a top level macro analysis of the Turkish

electricity market

• Assess the regulatory landscape and determine key

legislative impacts on future smart grid deployment

• Analyse the potential market opportunity for Smart Grid

Services and Solutions to 2020 (2011 base year)

•Identify key competitors and profile market leaders; and

• Provide key conclusions and recommendations for our

client to develop an effective market development strategy.

Our Approach and Work

Frost & Sullivan developed the analysis from both a ‘bottom –up’ approach, where customer bases were

concentrated and through a ‘top-down’ approach where industry databases were available and the

customers base was highly fragmented. Interviews were conducted with 100 key market participants

(competitors and customers) to ascertain current requirements and spending plans. In addition, extensive

desk research was used to cross check and supplement the analysis.

Outcome and Business Impact

• The project lasted for 12 weeks and this involved close interaction (weekly onsite work) with the client.

• Frost & Sullivan presented the data to the key strategy development stakeholders

•These inputs will be used in our clients yearly business strategy development plans.

Case Study: Strategic Analysis of the Smart Grid

Services and Solutions Market in Turkey

17

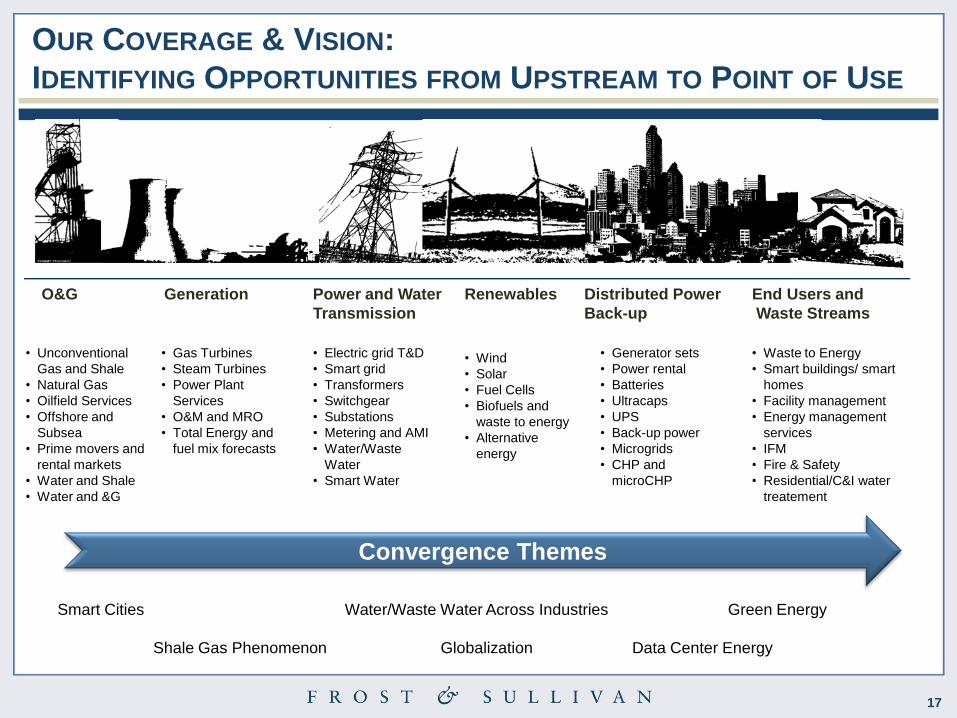

O&G Generation Power and Water

Transmission

Renewables Distributed Power End Users and

Back-up Waste Streams

OUR COVERAGE & VISION:

IDENTIFYING OPPORTUNITIES FROM UPSTREAM TO POINT OF USE

• Unconventional

Gas and Shale

• Natural Gas

• Oilfield Services

• Offshore and

Subsea

• Prime movers and

rental markets

• Water and Shale

• Water and &G

• Gas Turbines

• Steam Turbines

• Power Plant

Services

• O&M and MRO

• Total Energy and

fuel mix forecasts

• Electric grid T&D

• Smart grid

• Transformers

• Switchgear

• Substations

• Metering and AMI

• Water/Waste

Water

• Smart Water

• Wind

• Solar

• Fuel Cells

• Biofuels and

waste to energy

• Alternative

energy

Convergence Themes

• Generator sets

• Power rental

• Batteries

• Ultracaps

• UPS

• Back-up power

• Microgrids

• CHP and

microCHP

• Waste to Energy

• Smart buildings/ smart

homes

• Facility management

• Energy management

services

• IFM

• Fire & Safety

• Residential/C&I water

treatement

Smart Cities Water/Waste Water Across Industries Green Energy

Shale Gas Phenomenon Globalization Data Center Energy

18

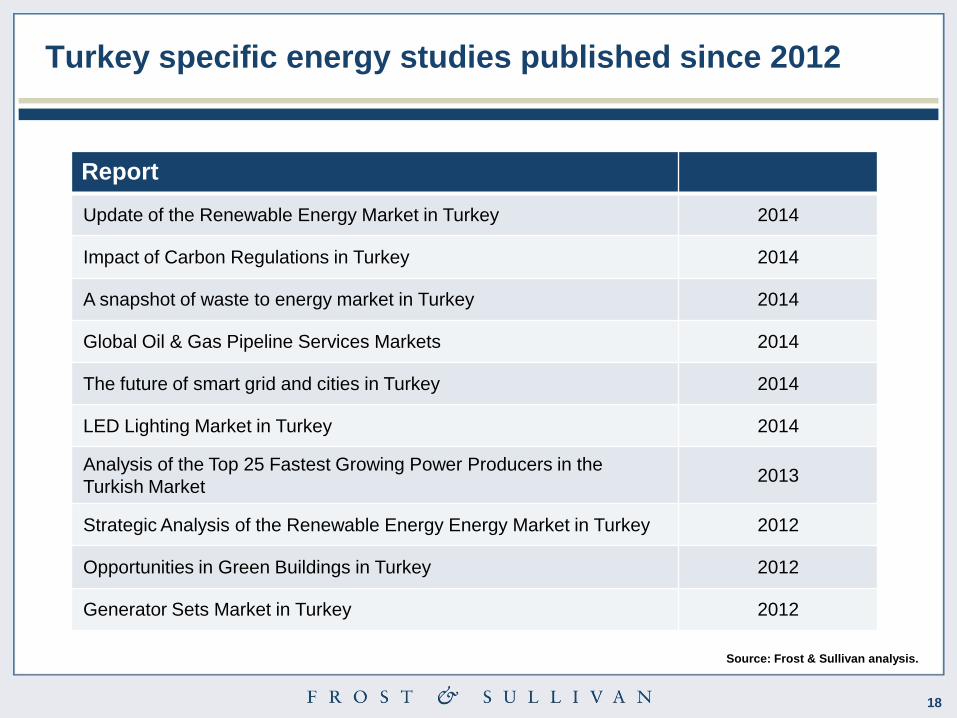

Turkey specific energy studies published since 2012

Source: Frost & Sullivan analysis.

Report

Update of the Renewable Energy Market in Turkey 2014

Impact of Carbon Regulations in Turkey 2014

A snapshot of waste to energy market in Turkey 2014

Global Oil & Gas Pipeline Services Markets 2014

The future of smart grid and cities in Turkey 2014

LED Lighting Market in Turkey 2014

Analysis of the Top 25 Fastest Growing Power Producers in the

Turkish Market2013

Strategic Analysis of the Renewable Energy Energy Market in Turkey 2012

Opportunities in Green Buildings in Turkey 2012

Generator Sets Market in Turkey 2012

19

Melih Nalcıoğlu

• Melih Nalcioglu is a research manager in Frost & Sullivan's Turkey office with 12 years consulting experience

on Turkey market cross industries. Before joining Frost & Sullivan, Melih was involved in boutique consulting

projects mainly for European companies that would like to enter Turkish market. Melih has managed

approximately 25 consulting projects for Frost & Sullivan.

Ozge Ozeke

• Ozge has been working as a Senior Research Analyst in Frost & Sullivan’s Energy & Environment team in

Turkey for 3 years. She has participated in several consulting studies in smart grid, wind, waste to

energy, building technologies, power back-up systems and authored research reports on

renewables, investment opportunities in energy and green buildings in Turkey.

Hikmet Cakmak

• Hikmet is an Industry Analyst and has been working in cross industry studies and projects, mostly in Energy

& Environment and Automotive & Transportation. He has participated in projects on smart grid, wind and

back up power, electric vehicles and urban mobility. He has authored reports on gas and diesel gensets and

lighting.

The team in Turkey is supported where required from our European offices. Local European project

management is also available.

Key members of the Turkish Energy team

20

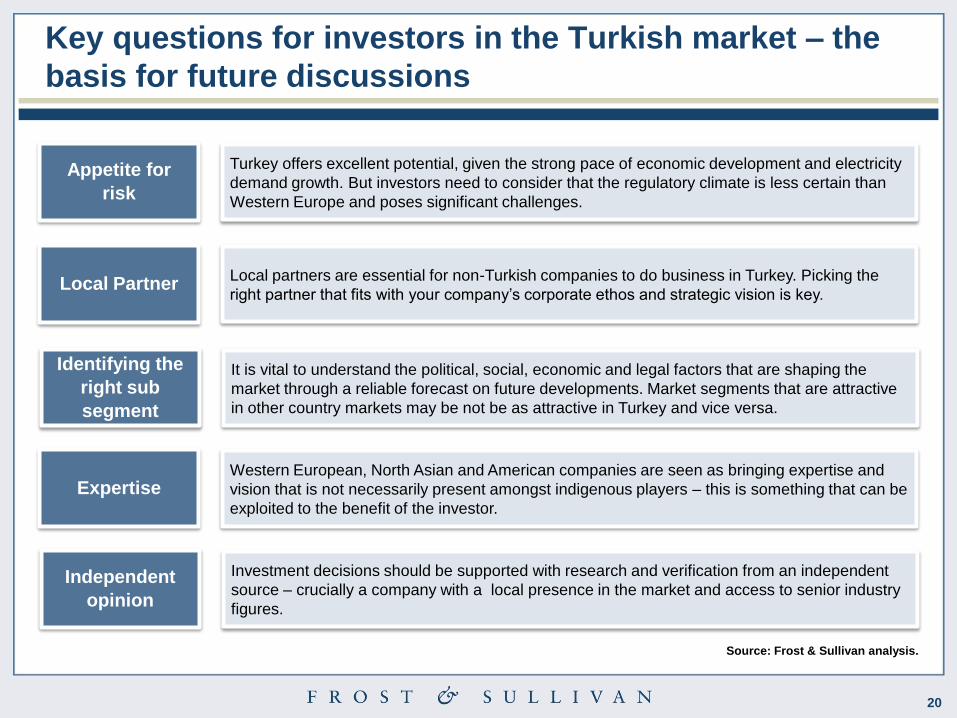

Key questions for investors in the Turkish market – the

basis for future discussions

Source: Frost & Sullivan analysis.

Independent

opinion

Investment decisions should be supported with research and verification from an independent

source – crucially a company with a local presence in the market and access to senior industry

figures.

Appetite for

risk

Turkey offers excellent potential, given the strong pace of economic development and electricity

demand growth. But investors need to consider that the regulatory climate is less certain than

Western Europe and poses significant challenges.

Identifying the

right sub

segment

It is vital to understand the political, social, economic and legal factors that are shaping the

market through a reliable forecast on future developments. Market segments that are attractive

in other country markets may be not be as attractive in Turkey and vice versa.

Local PartnerLocal partners are essential for non-Turkish companies to do business in Turkey. Picking the

right partner that fits with your company’s corporate ethos and strategic vision is key.

ExpertiseWestern European, North Asian and American companies are seen as bringing expertise and

vision that is not necessarily present amongst indigenous players – this is something that can be

exploited to the benefit of the investor.

21

About Frost & Sullivan

22

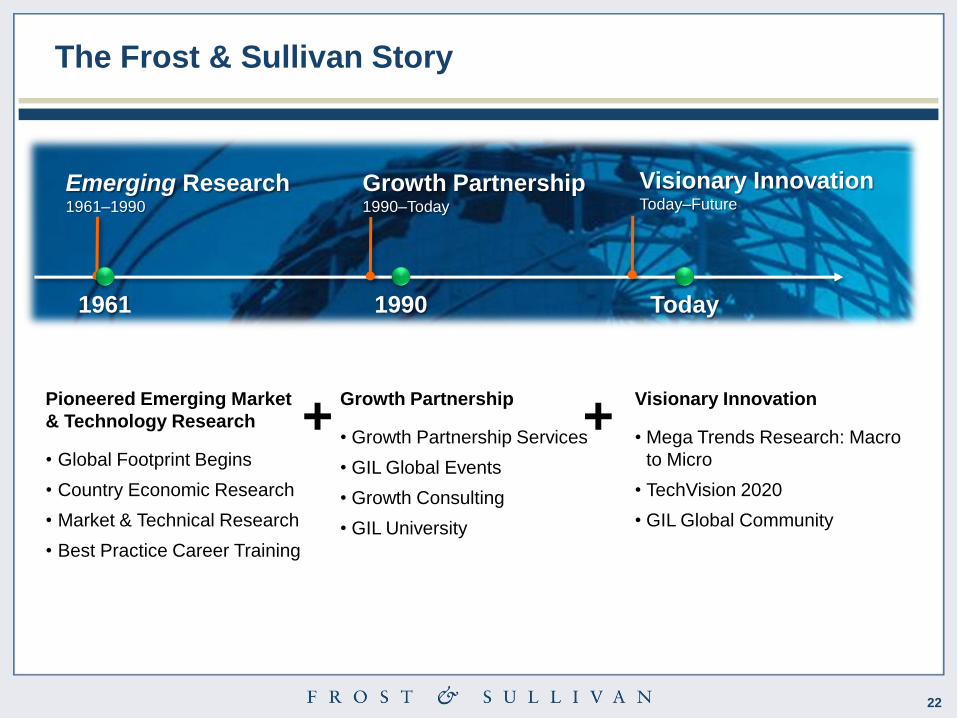

The Frost & Sullivan Story

1961 1990 Today

Emerging Research1961–1990

Pioneered Emerging Market

& Technology Research

• Global Footprint Begins

• Country Economic Research

• Market & Technical Research

• Best Practice Career Training

Growth Partnership

• Growth Partnership Services

• GIL Global Events

• Growth Consulting

• GIL University

Growth Partnership1990–Today

Visionary InnovationToday–Future

Visionary Innovation

• Mega Trends Research: Macro

to Micro

• TechVision 2020

• GIL Global Community

+ +

23

Our Global Footprint 40+ OfficesScanning the Globe for Opportunities and Innovation

24

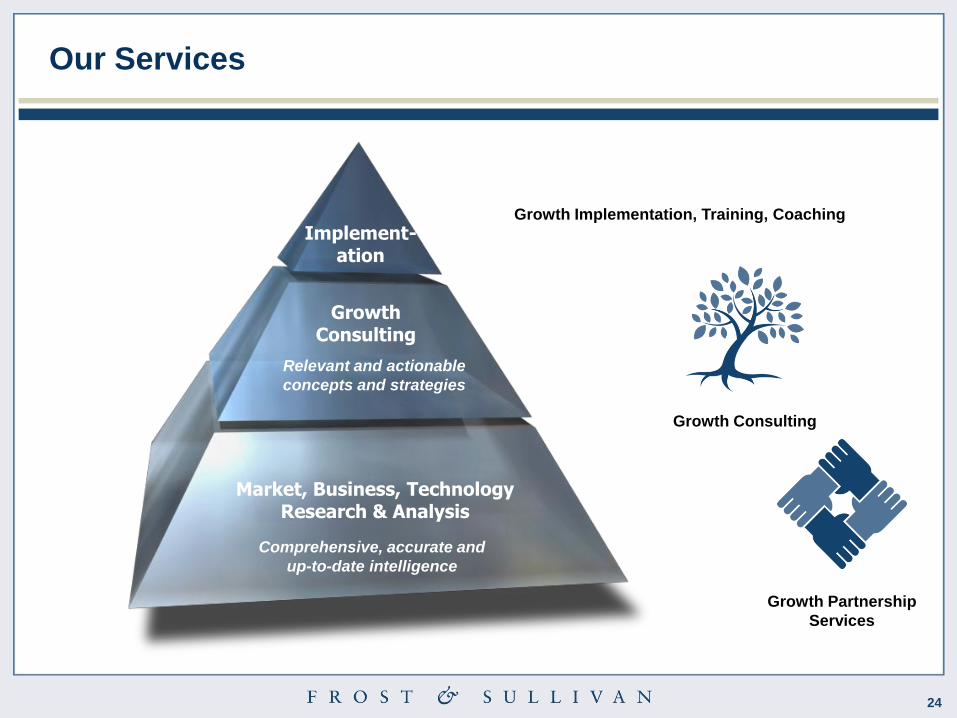

Our Services

Market, Business, Technology Research & Analysis

GrowthConsulting

Implement-ation

Relevant and actionable

concepts and strategies

Comprehensive, accurate and

up-to-date intelligence

Growth Implementation, Training, Coaching

Growth Consulting

Growth Partnership

Services

25

Our Industry Coverage

Automotive&

Transportation

Aerospace & Defense Measurement &

Instrumentation

Information &

Communication

Technologies

Healthcare

Environment & Building

Technologies

Energy & Power

Systems

Chemicals, Materials

& Food

Electronics &

Security

Industrial Automation

& Process ControlAutomotive

Transportation & Logistics

Consumer

Technologies

Minerals & Mining

26

Contacts

Jonathan Robinson

Senior Consultant

Energy, Environment & Building

Technologies

+(44)207.915.7883

Chiara Carella

Head of Corporate Communications

Europe, Israel and Africa

+44 (0) 207 343 8314

Recommended