1

Diversified Industrials – Specialty Distribution I Q4 2017

Investment Banking I Industry Spotlight

2

Diversified Industrials – Specialty Distribution I Industry Spotlight

Q4 2017

Key Industrial Sector Contacts

Investment Banking

Debt Capital Markets Equity Capital Markets

Mike Brothers Managing Director

Mike Ryan Managing Director

Corporate Banking

Industry Expertise Capital Mkts. Capabilities

Full-service platform with over 200 professionals, offering the following:

Investment Banking

M&A Advisory

Capital Raising

Debt Capital Markets

Loan Capital Markets:

– Pro Rata

– Institutional

Bond Capital Markets:

– Investment Grade

– High Yield

– Acquisition & Bridge Finance

Private Placements

Equity Capital Markets

Initial Public Offerings

Follow-On Offerings

Convertible Debt

Sponsor Coverage

Bill Tyson Co-Head Capital Markets [email protected]

Jeff Thieman Managing Director

Diversified Industrials Group Overview

Jeremy Eberlein Managing Director

Select Diversified Industrials Investment Banking Advisory Transactions

Joe Carson Managing Director

Marc Hirschfield Vice President

Melina Audinelle Director

Chemicals, Plastics & Packaging

Coatings Diversified Chemicals

Packaging Plastics Manufacturing

Industrial Technology

Flow Control Process/Motion Control

Test & Measurement

Metals & Materials

Metal Forming & Machining

Mills & Specialty Metal

Natural Resources & Mining

Processors/Distributors Scrap/Recycling

Specialty Distribution

Automotive Aftermarket

Building & Construction Products

Electrical & Communication

Industrial, MRO & Safety

Transportation & Logistics

Automotive & Heavy Duty Vehicles

Marine

Rail & Rail Services Third Party Logistics

acquired by

portfolio company of

acquired by

portfolio company of

a business unit of

acquired by

Advanced Energy Technologies LLC

a subsidiary of

acquired by

acquired by

acquired assets of

a subsidiary of

GT Acquisition, LLC

recapitalized with

Exclusive Financial Advisor Exclusive Financial Advisor Exclusive Financial Advisor Exclusive Financial Advisor Exclusive Financial Advisor Exclusive Financial Advisor Exclusive Financial Advisor Exclusive Financial Advisor

recapitalized by

Ross Breunig Team Lead

Gregory Eck Asset Based Lending

3

Diversified Industrials – Specialty Distribution I Industry Spotlight

Q4 2017

Senior Diversified Industrials Investment Banking Team

21+ years of investment banking experience, inclusive of: merger & acquisition advisory, restructuring advisory, equity offerings, debt placements, and principal investing

Career primarily focused on middle market industrial companies

Prior to joining Fifth Third in 2014, served as a Director in the Industrials Group of Harris Williams & Co, where Jeremy led the Metals Industry Practice

Previously, Jeremy worked as a Director at National City Capital Markets Investment Banking Group, and was involved in the founding of Resilience Capital Partners, executing transactions both as an advisor and as principal investor

BSBA – Ohio University

11+ years of investment banking experience and 16+ years financial industry experience

Prior to joining Fifth Third in 2015, Marc served as vice president at Corporate Fuel, a New York City-based financial advisory and private equity firm focused on middle market private and public companies

Previously, Marc was with Sterne Agee, a regional investment banking and brokerage firm based in Birmingham, Alabama

BS – University of Florida; MBA – New York University

Jeremy Eberlein (Managing Director)

Marc Hirschfield (Vice President)

Joe Carson (Managing Director)

24+ years of investment banking and financial advisory services experience covering public and private companies in the middle market sector. Joe has significant experience in providing advisory services for mergers and acquisitions, acquisition financings, defense advisory/hostile takeovers, and leveraged buyouts

Prior to joining Fifth Third in 2017, Joe served as Senior Vice President at Caldwell Tanks, in Louisville, KY, a manufacturer of tanks and storage structures that are used for a number of industrial purposes. Joe headed Caldwell Tanks’ Energy Division

Previously, Joe served as a managing director for Western Reserve Partners in Cleveland, where he was co-head of the Industrial Group and executed transactions across the industrials vertical

BSBA – Miami University; MBA – Case Western University

Melina Audinelle (Director)

17+ years of investment banking experience covering public and private companies in both the large corporate and middle market sectors. Melina has significant experience in providing advisory services for mergers and acquisitions, acquisition financings, defense advisory/hostile takeovers, and leveraged buyouts

Prior to joining Fifth Third in 2014, Melina spent five years at Challenger Capital Group, a boutique investment bank providing M&A advisory and structured capital raising

Previously, Melina served as an investment banking associate for JPMorgan Securities, Inc. in Chicago, where she was a member of the Mid-Corporate Investment Banking M&A group

BS – Northwestern University

Office: 216-274-5008 Email: [email protected] Location: Cleveland, OH

Office: 216-274-5152 Email: [email protected] Location: Cleveland, OH

Office: 312-704-4092

Email: [email protected] Location: Chicago, IL

Office: 678-237-4376

Email: [email protected] Location: Atlanta, GA

4

Diversified Industrials – Specialty Distribution I Industry Spotlight

Q4 2017

Highlighted FTS Advisory Transaction

January 2018: Fifth Third Securities, Inc. Advises Auto-Vehicle Parts Company on its Recapitalization by Tenex Capital Management

Fifth Third Securities, Inc. acted as the exclusive financial advisor to Auto-Vehicle Parts Company (or “Auveco”) on its January 2018 recapitalization by Tenex Capital Management (“Tenex”). Advising Auveco on the transaction from Fifth Third were Mike Burr, Senior Managing Director; Jeremy Eberlein, Managing Director; Melina Audinelle, Director; C.J. Andriole, Senior Associate; and Colin Schulz, Senior Analyst.

About Auveco

Founded in 1916, Auveco has become one of the predominant providers of automotive fasteners to the body hardware aftermarket as well as general industrial fasteners used in maintenance, repair, and operations applications within North America. Auveco sells to thousands of wholesale distribution customers who subsequently service hundreds of thousands of collision centers, repair shops, dealerships, and general manufacturers located throughout North America.

About Tenex

Tenex is a private equity firm that invests in middle-market companies. Tenex uses an in-house team of hybrid investment professionals skilled in operational leadership, investing and capital markets structuring to maximize long-term value creation. Tenex’s deep operating experience allows the firm to collaborate with management teams to capitalize on business and market opportunities. Tenex has successfully invested in a diverse range of industries, including industrials, manufacturing, and health and business services.

January 2018

has been recapitalized by

The undersigned served as Exclusive Financial Advisor to Auveco in connection with this transaction

5

Diversified Industrials – Specialty Distribution I Industry Spotlight

Q4 2017

Highlighted FTS Advisory Transaction

January 2018: Fifth Third Securities, Inc. Advises Diamond Metals Distribution, LLC on its Recapitalization with Kian Capital

January 2018

has been recapitalized with

The undersigned served as Exclusive Financial Advisor to Diamond in connection with this transaction

Fifth Third Securities, Inc. acted as the exclusive financial advisor to Diamond Metals Distribution, LLC (“Diamond”) on its January 2018 recapitalization with Kian Capital (“Kian”). Advising Diamond on the transaction from Fifth Third were Jeremy Eberlein, Managing Director; C.J. Andriole, Senior Associate; and Colin Schulz, Senior Analyst.

About Diamond

Diamond is a Cleveland, Ohio based steel service center with customers that include tool and die shops, mold shops, machine shops, and general metalworking manufacturers. Diamond provides value-added services, such as production saw cutting, flame cutting, pre-squared finishing, and grinding and milling services to tool steels, hot and cold rolled steels, powdered metals, and alloy plates and rounds.

About Kian

With offices in Atlanta, GA and Charlotte, NC, Kian is a private investment firm that makes mezzanine debt and equity investments in leading lower middle-market companies across a broad range of industries, typically providing between $5 million and $20 million of capital per transaction. Kian partners with management teams and independent sponsors to build and grow successful, high-quality businesses. Kian’s team has deep expertise across the capital structure, including control private equity, mezzanine debt and leveraged senior debt, which enables Kian to be flexible, value-added partners to help support the long-term objectives of business owners.

6

Diversified Industrials – Specialty Distribution I Industry Spotlight

Q4 2017

(30%)

(10%)

10%

30%

50%

Dec-16 Mar-17 Jun-17 Sep-17 Dec-17

Automotive Aftermarket Building & ConstructionElectrical & Communication Industrial, MRO & SafetyS&P 500

Latest Twelve Months (“LTM”) Share Price Performance

+2%

Automotive Aftermarket: Number of Vehicles & Miles Driven [2]

U.S. Manufacturers’ Inventories Relative to Sales [3]

Market Insights Specialty Distribution

+7%

[1] Source: Auto Care Association 2017 Digital Auto Care Factbook [2] According to the Bureau of Transportation [3] Source: U.S. Census Bureau; * Data is published monthly on a two-month lag Other Source: Modern Distribution Management, S&P Capital IQ, Industry Research

-1%

+35%

+18%

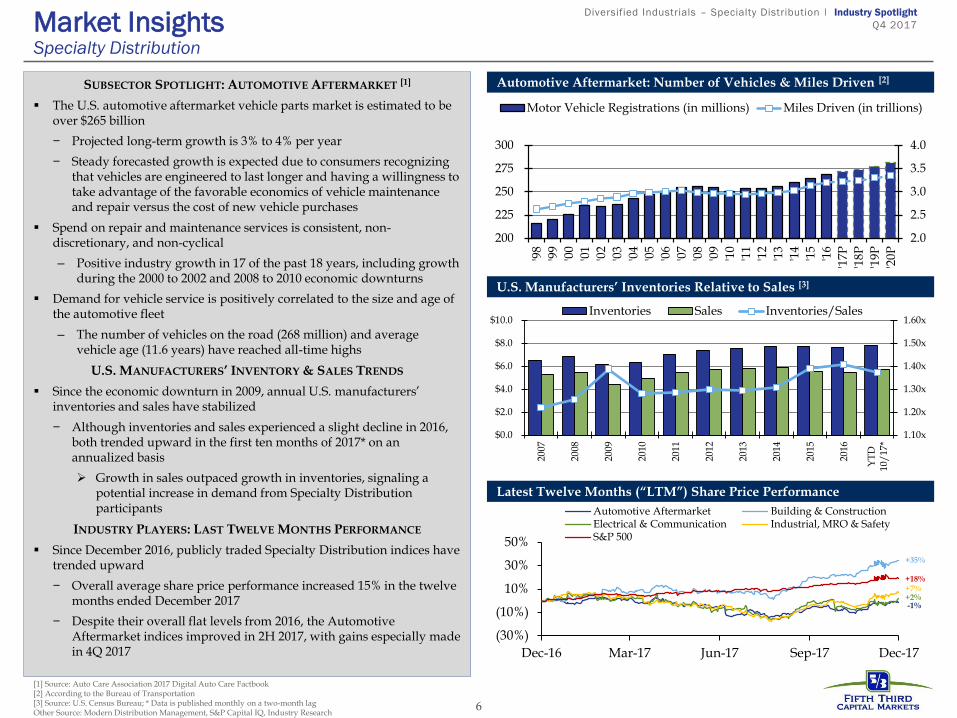

SUBSECTOR SPOTLIGHT: AUTOMOTIVE AFTERMARKET [1]

The U.S. automotive aftermarket vehicle parts market is estimated to be over $265 billion

− Projected long-term growth is 3% to 4% per year

− Steady forecasted growth is expected due to consumers recognizing that vehicles are engineered to last longer and having a willingness to take advantage of the favorable economics of vehicle maintenance and repair versus the cost of new vehicle purchases

Spend on repair and maintenance services is consistent, non-discretionary, and non-cyclical

– Positive industry growth in 17 of the past 18 years, including growth during the 2000 to 2002 and 2008 to 2010 economic downturns

Demand for vehicle service is positively correlated to the size and age of the automotive fleet

– The number of vehicles on the road (268 million) and average vehicle age (11.6 years) have reached all-time highs

U.S. MANUFACTURERS’ INVENTORY & SALES TRENDS

Since the economic downturn in 2009, annual U.S. manufacturers’ inventories and sales have stabilized

− Although inventories and sales experienced a slight decline in 2016, both trended upward in the first ten months of 2017* on an annualized basis

Growth in sales outpaced growth in inventories, signaling a potential increase in demand from Specialty Distribution participants

INDUSTRY PLAYERS: LAST TWELVE MONTHS PERFORMANCE

Since December 2016, publicly traded Specialty Distribution indices have trended upward

− Overall average share price performance increased 15% in the twelve months ended December 2017

− Despite their overall flat levels from 2016, the Automotive Aftermarket indices improved in 2H 2017, with gains especially made in 4Q 2017

2.0

2.5

3.0

3.5

4.0

'98

'99

'00

'01

'02

'03

'04

'05

'06

'07

'08

'09

'10

'11

'12

'13

'14

'15

'16

'17P

'18P

'19P

'20P

200

225

250

275

300

Motor Vehicle Registrations (in millions) Miles Driven (in trillions)

1.10x

1.20x

1.30x

1.40x

1.50x

1.60x

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

YT

D10

/17

*

Inventories Sales Inventories/Sales

7

Diversified Industrials – Specialty Distribution I Industry Spotlight

Q4 2017

(50%)

0%

50%

100%

150%

Dec-12 Dec-13 Dec-14 Dec-15 Dec-16 Dec-17

Automotive Aftermarket Building & Construction

Electrical & Communication Industrial, MRO & Safety

S&P 500

Sub Sector Indices’ Stock Price Performance and Valuation Summary

Specialty Distribution 5-Year Share Price Performance Specialty Distribution 5-Year Avg. EV / Forward EBITDA Valuation

Public Market Valuation Trends Specialty Distribution

Source: S&P Capital IQ as of December 29th, 2017

+96% +88%

+118%

+18% +3%

6.0x

8.0x

10.0x

12.0x

14.0x

Dec-12 Dec-13 Dec-14 Dec-15 Dec-16 Dec-17

Automotive Aftermarket Building & Construction

Electrical & Communication Industrial, MRO & Safety

S&P 500

Sub SectorNumber of

Companies

Median

Enterprise Value

Average

% Change in Stock Price

Median TEV /

LTM Multiples

Median TEV /

Forward Multiples

$ in millions 6 Months 12 Months Revenue EBITDA Revenue EBITDA

Automotive Aftermarket 6 $15,180 4% (1%) 1.9x 12.1x 1.9x 11.4x

Building & Construction Products 6 5,371 23% 35% 1.2x 11.1x 1.1x 11.2x

Electrical & Communication 3 4,545 8% 2% 0.5x 11.0x 0.6x 10.8x

Industrial, MRO & Safety 6 10,737 12% 7% 1.8x 12.9x 1.8x 12.0x

S&P 500 500 10% 18% 2.5x 12.8x 2.3x 10.8x

8

Diversified Industrials – Specialty Distribution I Industry Spotlight

Q4 2017

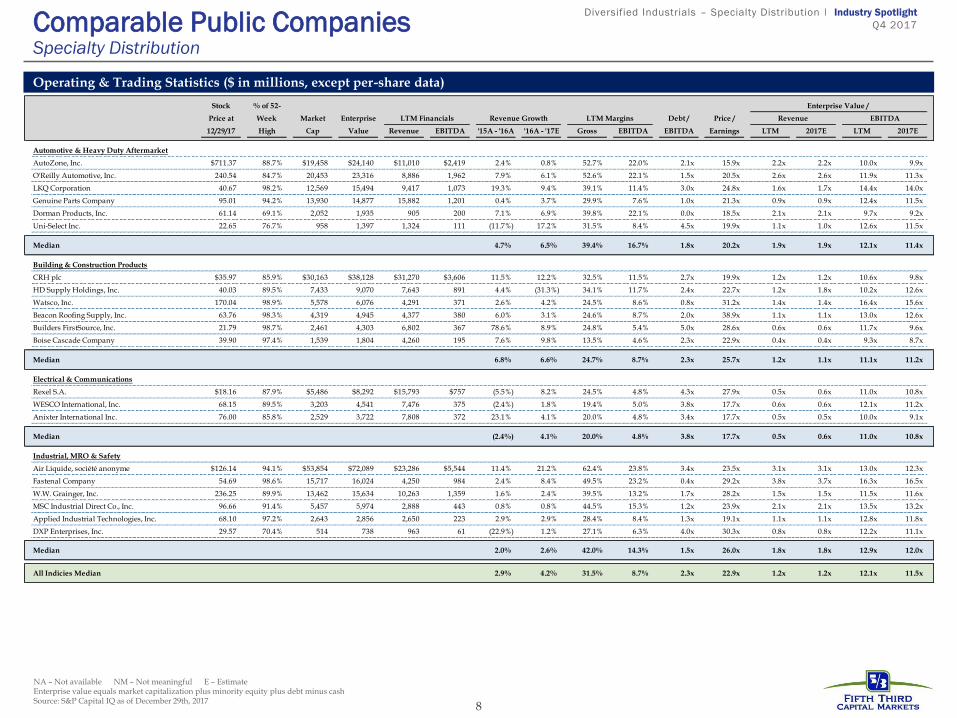

Operating & Trading Statistics ($ in millions, except per-share data)

NA – Not available NM – Not meaningful E – Estimate Enterprise value equals market capitalization plus minority equity plus debt minus cash Source: S&P Capital IQ as of December 29th, 2017

Comparable Public Companies Specialty Distribution

Stock % of 52- Enterprise Value /

Price at Week Market Enterprise LTM Financials Revenue Growth LTM Margins Debt / Price / Revenue EBITDA

12/29/17 High Cap Value Revenue EBITDA '15A - '16A '16A - '17E Gross EBITDA EBITDA Earnings LTM 2017E LTM 2017E

Automotive & Heavy Duty Aftermarket

AutoZone, Inc. $711.37 88.7% $19,458 $24,140 $11,010 $2,419 2.4% 0.8% 52.7% 22.0% 2.1x 15.9x 2.2x 2.2x 10.0x 9.9x

O'Reilly Automotive, Inc. 240.54 84.7% 20,453 23,316 8,886 1,962 7.9% 6.1% 52.6% 22.1% 1.5x 20.5x 2.6x 2.6x 11.9x 11.3x

LKQ Corporation 40.67 98.2% 12,569 15,494 9,417 1,073 19.3% 9.4% 39.1% 11.4% 3.0x 24.8x 1.6x 1.7x 14.4x 14.0x

Genuine Parts Company 95.01 94.2% 13,930 14,877 15,882 1,201 0.4% 3.7% 29.9% 7.6% 1.0x 21.3x 0.9x 0.9x 12.4x 11.5x

Dorman Products, Inc. 61.14 69.1% 2,052 1,935 905 200 7.1% 6.9% 39.8% 22.1% 0.0x 18.5x 2.1x 2.1x 9.7x 9.2x

Uni-Select Inc. 22.65 76.7% 958 1,397 1,324 111 (11.7%) 17.2% 31.5% 8.4% 4.5x 19.9x 1.1x 1.0x 12.6x 11.5x

Median 4.7% 6.5% 39.4% 16.7% 1.8x 20.2x 1.9x 1.9x 12.1x 11.4x

Building & Construction Products

CRH plc $35.97 85.9% $30,163 $38,128 $31,270 $3,606 11.5% 12.2% 32.5% 11.5% 2.7x 19.9x 1.2x 1.2x 10.6x 9.8x

HD Supply Holdings, Inc. 40.03 89.5% 7,433 9,070 7,643 891 4.4% (31.3%) 34.1% 11.7% 2.4x 22.7x 1.2x 1.8x 10.2x 12.6x

Watsco, Inc. 170.04 98.9% 5,578 6,076 4,291 371 2.6% 4.2% 24.5% 8.6% 0.8x 31.2x 1.4x 1.4x 16.4x 15.6x

Beacon Roofing Supply, Inc. 63.76 98.3% 4,319 4,945 4,377 380 6.0% 3.1% 24.6% 8.7% 2.0x 38.9x 1.1x 1.1x 13.0x 12.6x

Builders FirstSource, Inc. 21.79 98.7% 2,461 4,303 6,802 367 78.6% 8.9% 24.8% 5.4% 5.0x 28.6x 0.6x 0.6x 11.7x 9.6x

Boise Cascade Company 39.90 97.4% 1,539 1,804 4,260 195 7.6% 9.8% 13.5% 4.6% 2.3x 22.9x 0.4x 0.4x 9.3x 8.7x

Median 6.8% 6.6% 24.7% 8.7% 2.3x 25.7x 1.2x 1.1x 11.1x 11.2x

Electrical & Communications

Rexel S.A. $18.16 87.9% $5,486 $8,292 $15,793 $757 (5.5%) 8.2% 24.5% 4.8% 4.3x 27.9x 0.5x 0.6x 11.0x 10.8x

WESCO International, Inc. 68.15 89.5% 3,203 4,541 7,476 375 (2.4%) 1.8% 19.4% 5.0% 3.8x 17.7x 0.6x 0.6x 12.1x 11.2x

Anixter International Inc. 76.00 85.8% 2,529 3,722 7,808 372 23.1% 4.1% 20.0% 4.8% 3.4x 17.7x 0.5x 0.5x 10.0x 9.1x

Median (2.4%) 4.1% 20.0% 4.8% 3.8x 17.7x 0.5x 0.6x 11.0x 10.8x

Industrial, MRO & Safety

Air Liquide, société anonyme $126.14 94.1% $53,854 $72,089 $23,286 $5,544 11.4% 21.2% 62.4% 23.8% 3.4x 23.5x 3.1x 3.1x 13.0x 12.3x

Fastenal Company 54.69 98.6% 15,717 16,024 4,250 984 2.4% 8.4% 49.5% 23.2% 0.4x 29.2x 3.8x 3.7x 16.3x 16.5x

W.W. Grainger, Inc. 236.25 89.9% 13,462 15,634 10,263 1,359 1.6% 2.4% 39.5% 13.2% 1.7x 28.2x 1.5x 1.5x 11.5x 11.6x

MSC Industrial Direct Co., Inc. 96.66 91.4% 5,457 5,974 2,888 443 0.8% 0.8% 44.5% 15.3% 1.2x 23.9x 2.1x 2.1x 13.5x 13.2x

Applied Industrial Technologies, Inc. 68.10 97.2% 2,643 2,856 2,650 223 2.9% 2.9% 28.4% 8.4% 1.3x 19.1x 1.1x 1.1x 12.8x 11.8x

DXP Enterprises, Inc. 29.57 70.4% 514 738 963 61 (22.9%) 1.2% 27.1% 6.3% 4.0x 30.3x 0.8x 0.8x 12.2x 11.1x

Median 2.0% 2.6% 42.0% 14.3% 1.5x 26.0x 1.8x 1.8x 12.9x 12.0x

All Indicies Median 2.9% 4.2% 31.5% 8.7% 2.3x 22.9x 1.2x 1.2x 12.1x 11.5x

9

Diversified Industrials – Specialty Distribution I Industry Spotlight

Q4 2017

$587

$700 $704$664

$612 $641 $618

$688 $715 $733 $739

'06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16

Cu

mu

lati

ve

Dry

Po

wd

er

($ i

n b

illi

on

s)

2017

2016

2015

2014

2013

2012

2011

2010

2009

Overhang by Vintage

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17

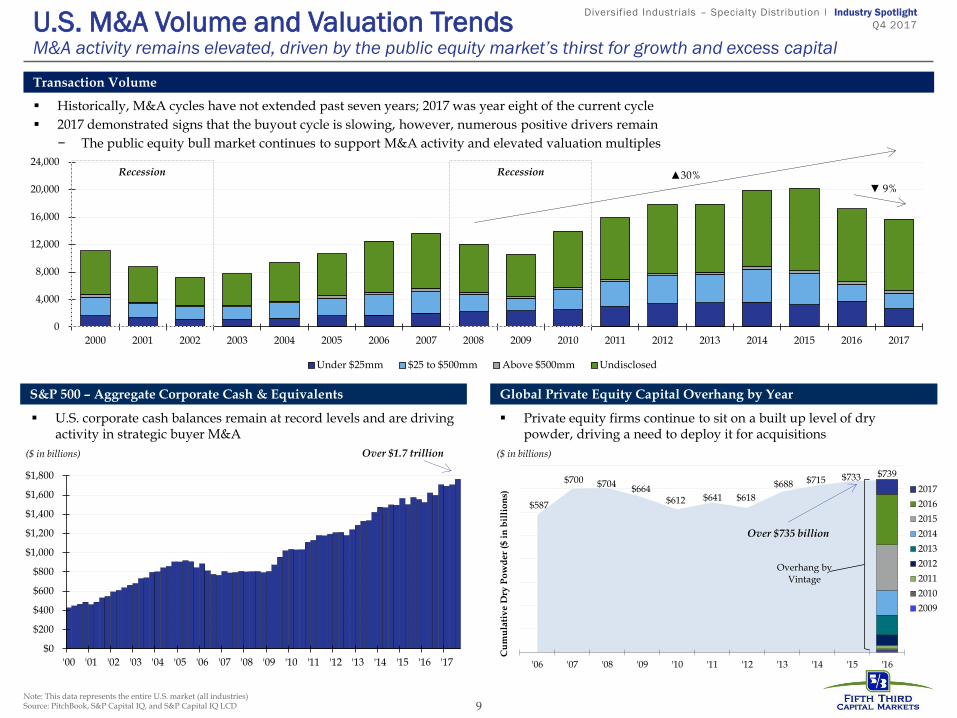

U.S. corporate cash balances remain at record levels and are driving activity in strategic buyer M&A

Historically, M&A cycles have not extended past seven years; 2017 was year eight of the current cycle

2017 demonstrated signs that the buyout cycle is slowing, however, numerous positive drivers remain

− The public equity bull market continues to support M&A activity and elevated valuation multiples

Note: This data represents the entire U.S. market (all industries) Source: PitchBook, S&P Capital IQ, and S&P Capital IQ LCD

0

4,000

8,000

12,000

16,000

20,000

24,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Under $25mm $25 to $500mm Above $500mm Undisclosed

Transaction Volume

Recession Recession

▼ 9% ▲30%

S&P 500 – Aggregate Corporate Cash & Equivalents

Over $1.7 trillion

Global Private Equity Capital Overhang by Year

Private equity firms continue to sit on a built up level of dry powder, driving a need to deploy it for acquisitions

Over $735 billion

U.S. M&A Volume and Valuation Trends M&A activity remains elevated, driven by the public equity market’s thirst for growth and excess capital

($ in billions) ($ in billions)

10

Diversified Industrials – Specialty Distribution I Industry Spotlight

Q4 2017

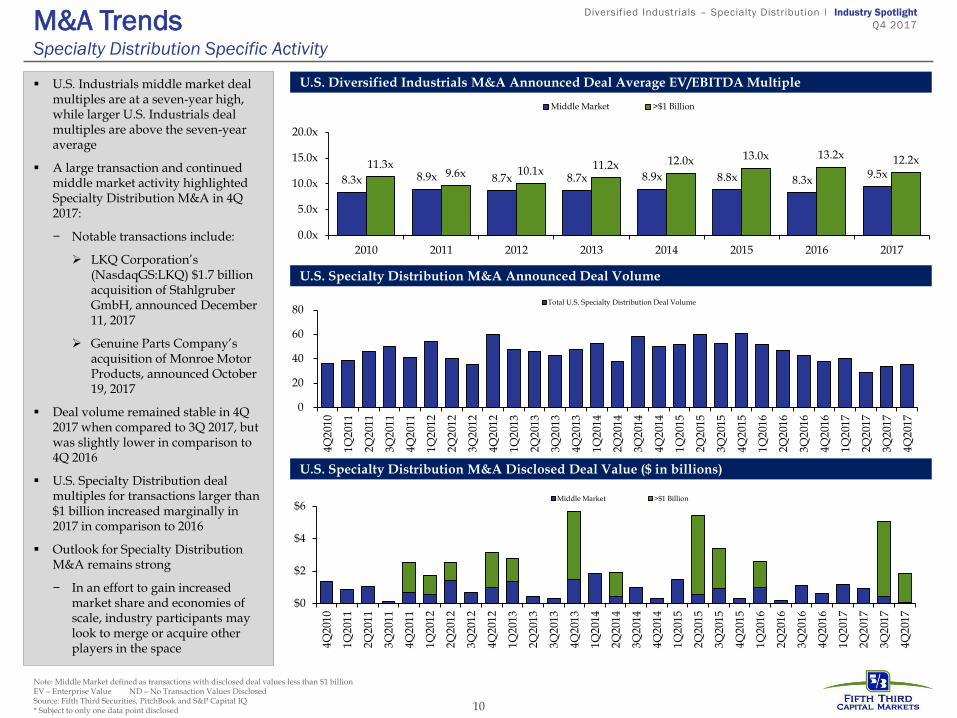

U.S. Diversified Industrials M&A Announced Deal Average EV/EBITDA Multiple U.S. Industrials middle market deal

multiples are at a seven-year high, while larger U.S. Industrials deal multiples are above the seven-year average

A large transaction and continued middle market activity highlighted Specialty Distribution M&A in 4Q 2017:

− Notable transactions include:

LKQ Corporation’s (NasdaqGS:LKQ) $1.7 billion acquisition of Stahlgruber GmbH, announced December 11, 2017

Genuine Parts Company’s acquisition of Monroe Motor Products, announced October 19, 2017

Deal volume remained stable in 4Q 2017 when compared to 3Q 2017, but was slightly lower in comparison to 4Q 2016

U.S. Specialty Distribution deal multiples for transactions larger than $1 billion increased marginally in 2017 in comparison to 2016

Outlook for Specialty Distribution M&A remains strong

− In an effort to gain increased market share and economies of scale, industry participants may look to merge or acquire other players in the space

U.S. Specialty Distribution M&A Announced Deal Volume

U.S. Specialty Distribution M&A Disclosed Deal Value ($ in billions)

Note: Middle Market defined as transactions with disclosed deal values less than $1 billion EV – Enterprise Value ND – No Transaction Values Disclosed Source: Fifth Third Securities, PitchBook and S&P Capital IQ * Subject to only one data point disclosed

M&A Trends Specialty Distribution Specific Activity

$0

$2

$4

$6

4Q

201

0

1Q

201

1

2Q

201

1

3Q

201

1

4Q

201

1

1Q

201

2

2Q

201

2

3Q

201

2

4Q

201

2

1Q

201

3

2Q

201

3

3Q

201

3

4Q

201

3

1Q

201

4

2Q

201

4

3Q

201

4

4Q

201

4

1Q

201

5

2Q

201

5

3Q20

15

4Q

201

5

1Q

201

6

2Q

201

6

3Q

201

6

4Q

201

6

1Q

201

7

2Q

201

7

3Q

201

7

4Q

201

7

Middle Market >$1 Billion

0

20

40

60

80

4Q

201

0

1Q

201

1

2Q

201

1

3Q

201

1

4Q

201

1

1Q

201

2

2Q

201

2

3Q

201

2

4Q

201

2

1Q

201

3

2Q

201

3

3Q

201

3

4Q

201

3

1Q

201

4

2Q20

14

3Q20

14

4Q

201

4

1Q

201

5

2Q

201

5

3Q

201

5

4Q

201

5

1Q

201

6

2Q

201

6

3Q

201

6

4Q

201

6

1Q

201

7

2Q

201

7

3Q

201

7

4Q

201

7

Total U.S. Specialty Distribution Deal Volume

8.3x 8.9x 8.7x 8.7x 8.9x 8.8x 8.3x9.5x

11.3x9.6x 10.1x 11.2x 12.0x 13.0x 13.2x 12.2x

0.0x

5.0x

10.0x

15.0x

20.0x

2010 2011 2012 2013 2014 2015 2016 2017

Middle Market >$1 Billion

11

Diversified Industrials – Specialty Distribution I Industry Spotlight

Q4 2017

Acquisitions of Specialty Distribution Companies ($ in millions)

M&A Activity Specialty Distribution – Select North American 2H 2017 Transactions

*Excluded from mean and median Source: Company Filings, S&P Capital IQ

Transaction's Specialty Implied

Date Enterprise Distribution Enterprise Value / LTM

Announced Acquirer Target Value Sub-sector

Jan-18 Tenex Capital Management Auto-Vehicle Parts Company - Auto Aftermarket Confidential

Dec-17 Winsupply Inc. Thomas Pipe & Supply Co. - Industrial, MRO & Safety

Dec-17 FinishMaster Canada, Inc. Substantially All Assets of T-W Pike Sales Ltd. - Industrial, MRO & Safety

Dec-17 SiteOne Landscape Supply, Inc. (NYSE:SITE) Pete Rose, Inc. - Building Products

Dec-17 Federal Resources Supply Company Wright Tool Company, Inc. - Industrial, MRO & Safety

Dec-17 SemiTorr Group, Inc. High Purity & Industrial Distribution of Aztech Controls Corporation - Industrial, MRO & Safety

Dec-17 LKQ Corporation (NasdaqGS:LKQ) Stahlgruber GmbH $1,770 Auto Aftermarket

Dec-17 Winsupply Inc. Tacoma Electric Supply, Inc. - Electrical & Communication

Dec-17 Cansel Survey Equipment Inc. Field Supply Business in Quebec of GeoShack North America, Inc. - Building Products

Dec-17 Fairmont Supply Company Industrial Pipe & Supply of Omaha and Industrial Pipe & Valve of Portland - Industrial, MRO & Safety

Nov-17 Five Points Capital Blake & Pendleton, Inc. - Industrial, MRO & Safety

Nov-17 The Cook & Boardman Group, LLC Pinnacle Door & Hardware, Inc. - Building Products

Nov-17 FCX Performance, Inc. The Eads Company - Industrial, MRO & Safety

Nov-17 McNaughton-McKay Electric Company, Inc. D Reynolds Company LLC - Electrical & Communication

Nov-17 Blue Sea Capital LLC RESA Power Solutions, LLC - Electrical & Communication

Nov-17 The Hillman Group, Inc. Hargis Industries, LP $48 Building Products

Nov-17 Winsupply Inc. APCO Inc. - Building Products

Nov-17 Quad-C Management, Inc. Galleher Corporation - Building Products

Nov-17 Foundation Building Materials, Inc. (NYSE:FBM) MCS Door & Hardware and Del-Pro Building Supplies, Inc. - Building Products

Nov-17 Clayton, Dubilier & Rice, Inc. STS Operating, Inc. - Electrical & Communication

Nov-17 Badger Meter, Inc. (NYSE:BMI) Carolina Meter & Supply Co - Electrical & Communication

Oct-17 Ardenton Capital Comtrad Strategic Sourcing Inc. - Building Products

Oct-17 ROHA Dyechem Pvt. Ltd. Cambrian Solutions Inc. - Industrial, MRO & Safety

Oct-17 Huron Capital Partners, LLC Hansons Holdings LLC - Building Products

Oct-17 Genuine Parts Company (NYSE:GPC) Monroe Motor Products Corp. - Auto Aftermarket

Oct-17 Triad Technologies, LLC Rilco Industrial Controls, Inc. - Electrical & Communication

Oct-17 Lawson Products, Inc. (NasdaqGS:LAWS) The Bolt Supply House, Ltd. $32 Industrial, MRO & Safety

Oct-17 Wieland-Werke AG Wieland-Kessler, LLC. - Industrial, MRO & Safety

Oct-17 Sager Electrical Supply Company, Inc. Power Sources Unlimited, Inc. - Electrical & Communication

Sep-17 Genuine Parts Company (NYSE:GPC) Alliance Automotive Holding Limited $2,017 Auto Aftermarket

Sep-17 Ogdon Ventures Westland Distributing Partners, LLC - Building Products

Sep-17 EnviroStar, Inc. (AMEX:EVI) Tri-State Technical Services, Inc. $17 Industrial, MRO & Safety

Sep-17 CanWel Building Materials Group Ltd. (TSX:CWX) Honsador Holding, LLC $80 Building Products

Aug-17 JELD-WEN Holding, inc. (NYSE:JELD) Milliken Millwork, Inc. - Building Products

Aug-17 Beacon Roofing Supply, Inc. (NasdaqGS:BECN) Oldcastle Distribution Inc. $2,625 Building Products

Aug-17 Hudson Technologies Inc. (NasdaqCM:HDSN) Airgas Refrigerants, Inc. $220 Industrial, MRO & Safety

Aug-17 MSC Industrial Direct Co., Inc. (NYSE:MSM) DECO Tool Supply Company, Inc. $42 Industrial, MRO & Safety

Aug-17 United Electrical Sales, Ltd. Electrical Products Inc. - Electrical & Communication

Aug-17 SiteOne Landscape Supply, Inc. (NYSE:SITE) South Coast Supply Inc. - Industrial, MRO & Safety

Jul-17 Crescent Electric Supply Co., Inc. Womack Electric Supply Co., Inc. - Electrical & Communication

Jul-17 TestEquity LLC Techni-Tool, Inc. - Industrial, MRO & Safety

Jul-17 Border States Industries, Inc. Kriz-Davis Co. - Electrical & Communication

Jul-17 WILsquare Capital LLC Walcro, Inc. - Building Products

12

Diversified Industrials – Specialty Distribution I Industry Spotlight

Q4 2017

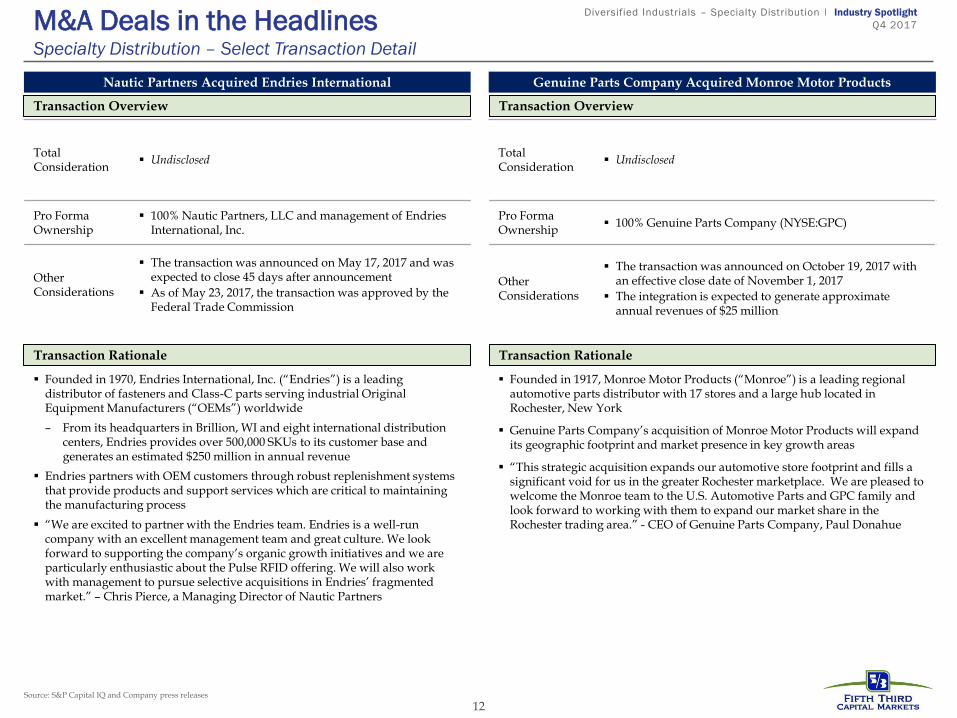

Total Consideration

Undisclosed

Pro Forma Ownership

100% Genuine Parts Company (NYSE:GPC)

Other Considerations

The transaction was announced on October 19, 2017 with an effective close date of November 1, 2017

The integration is expected to generate approximate annual revenues of $25 million

M&A Deals in the Headlines Specialty Distribution – Select Transaction Detail

Total Consideration

Undisclosed

Pro Forma Ownership

100% Nautic Partners, LLC and management of Endries International, Inc.

Other Considerations

The transaction was announced on May 17, 2017 and was expected to close 45 days after announcement

As of May 23, 2017, the transaction was approved by the Federal Trade Commission

Transaction Overview Transaction Overview

Transaction Rationale Transaction Rationale

Founded in 1970, Endries International, Inc. (“Endries”) is a leading distributor of fasteners and Class-C parts serving industrial Original Equipment Manufacturers (“OEMs”) worldwide

– From its headquarters in Brillion, WI and eight international distribution centers, Endries provides over 500,000 SKUs to its customer base and generates an estimated $250 million in annual revenue

Endries partners with OEM customers through robust replenishment systems that provide products and support services which are critical to maintaining the manufacturing process

“We are excited to partner with the Endries team. Endries is a well-run company with an excellent management team and great culture. We look forward to supporting the company’s organic growth initiatives and we are particularly enthusiastic about the Pulse RFID offering. We will also work with management to pursue selective acquisitions in Endries’ fragmented market.” – Chris Pierce, a Managing Director of Nautic Partners

Founded in 1917, Monroe Motor Products (“Monroe”) is a leading regional automotive parts distributor with 17 stores and a large hub located in Rochester, New York

Genuine Parts Company’s acquisition of Monroe Motor Products will expand its geographic footprint and market presence in key growth areas

“This strategic acquisition expands our automotive store footprint and fills a significant void for us in the greater Rochester marketplace. We are pleased to welcome the Monroe team to the U.S. Automotive Parts and GPC family and look forward to working with them to expand our market share in the Rochester trading area.” - CEO of Genuine Parts Company, Paul Donahue

Source: S&P Capital IQ and Company press releases

Genuine Parts Company Acquired Monroe Motor Products Nautic Partners Acquired Endries International

13

Diversified Industrials – Specialty Distribution I Industry Spotlight

Q4 2017

Overall U.S. Private Equity Deal Flow ($ in billions)

U.S. Specialty Distribution Private Equity Deal Flow ($ in billions)

U.S. Specialty Distribution Private Equity Exits ($ in millions)

*4Q17 preliminary PitchBook data ND – No Transaction Values Disclosed Source: Fifth Third Securities, PitchBook

Private Equity Activity Specialty Distribution

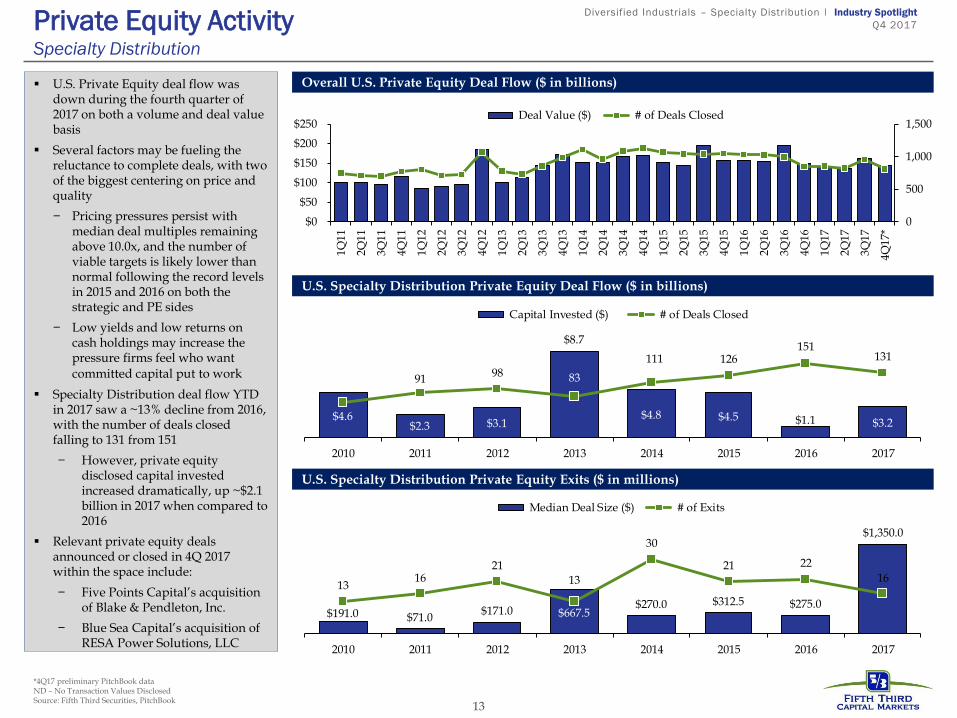

U.S. Private Equity deal flow was down during the fourth quarter of 2017 on both a volume and deal value basis

Several factors may be fueling the reluctance to complete deals, with two of the biggest centering on price and quality

− Pricing pressures persist with median deal multiples remaining above 10.0x, and the number of viable targets is likely lower than normal following the record levels in 2015 and 2016 on both the strategic and PE sides

− Low yields and low returns on cash holdings may increase the pressure firms feel who want committed capital put to work

Specialty Distribution deal flow YTD in 2017 saw a ~13% decline from 2016, with the number of deals closed falling to 131 from 151

− However, private equity disclosed capital invested increased dramatically, up ~$2.1 billion in 2017 when compared to 2016

Relevant private equity deals announced or closed in 4Q 2017 within the space include:

− Five Points Capital’s acquisition of Blake & Pendleton, Inc.

− Blue Sea Capital’s acquisition of RESA Power Solutions, LLC

$4.6 $2.3 $3.1

$8.7

$4.8 $4.5 $1.1 $3.2

7291

98 83

111 126151

131

2010 2011 2012 2013 2014 2015 2016 2017

Capital Invested ($) # of Deals Closed

$191.0 $71.0$171.0 $667.5

$270.0 $312.5 $275.0

$1,350.0

1316

21

13

30

21 22

16

2010 2011 2012 2013 2014 2015 2016 2017

Median Deal Size ($) # of Exits

0

500

1,000

1,500

$0

$50

$100

$150

$200

$250

1Q

11

2Q11

3Q11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q17

3Q17

4Q

17*

Deal Value ($) # of Deals Closed

14

Diversified Industrials – Specialty Distribution I Industry Spotlight

Q4 2017

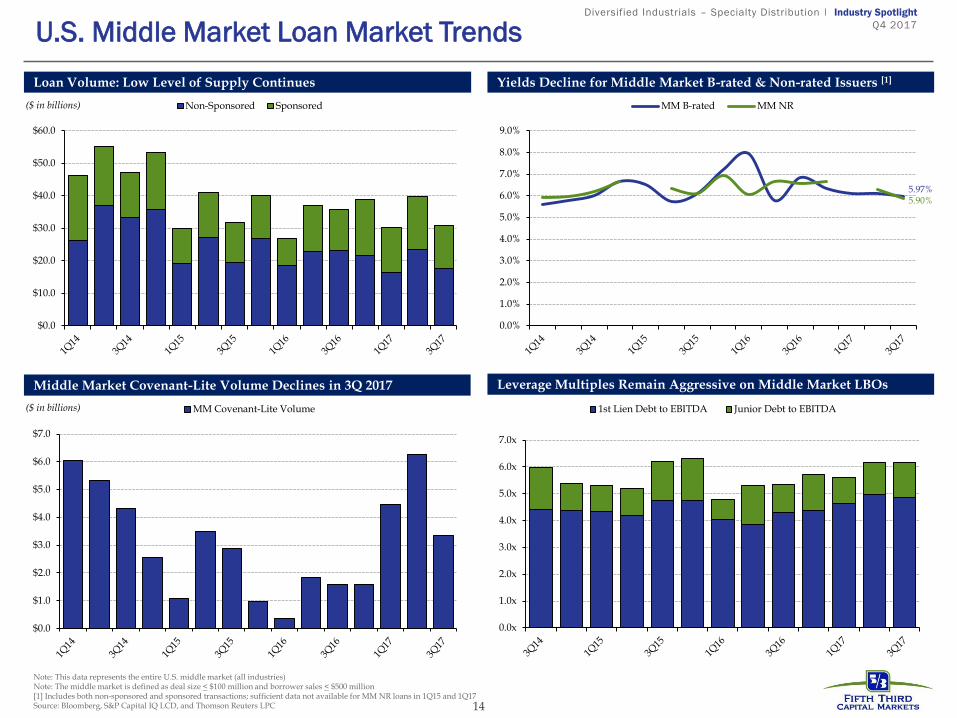

Note: This data represents the entire U.S. middle market (all industries) Note: The middle market is defined as deal size < $100 million and borrower sales < $500 million [1] Includes both non-sponsored and sponsored transactions; sufficient data not available for MM NR loans in 1Q15 and 1Q17 Source: Bloomberg, S&P Capital IQ LCD, and Thomson Reuters LPC

U.S. Middle Market Loan Market Trends

Loan Volume: Low Level of Supply Continues Yields Decline for Middle Market B-rated & Non-rated Issuers [1]

Middle Market Covenant-Lite Volume Declines in 3Q 2017 Leverage Multiples Remain Aggressive on Middle Market LBOs

$0.0

$10.0

$20.0

$30.0

$40.0

$50.0

$60.0

Non-Sponsored Sponsored($ in billions)

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

MM B-rated MM NR

5.97%

5.90%

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

$7.0

MM Covenant-Lite Volume($ in billions)

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

7.0x

1st Lien Debt to EBITDA Junior Debt to EBITDA

15

Diversified Industrials – Specialty Distribution I Industry Spotlight

Q4 2017 Pro Rata Market Update: 3Q 2017 Bank Terms Remain Relatively Unchanged Over Prior Quarter

Structure

Banks reported that standards for C&I loans were essentially unchanged

over the past three months for loans to both large and middle market firms.

However, terms on C&I loans became less restrictive, on balance, with all

specific loan terms either easing or remaining materially similar.

Specifically, a significant net percentage of banks reportedly narrowed

spreads of loan rates over the cost of funds, while a moderate net share of

banks reportedly increased the maximum size of credit lines and decreased

the use of interest rate floors for large and middle market firms

Observations from Fifth Third’s syndicated pro rata loan database:

− Financial Covenants – single covenant deals became slightly more

prevalent through LTM Q3 2017 representing just over 20% of

transactions, with two covenant deals remaining most common,

typically consisting of a maximum leverage and minimum interest or

fixed charge coverage ratio

− Tenors – static at 5 years, co-terminus revolver and term loans.

− Amortization – no discernable market-driven movement, with a

standard 5yr tenor term loan amortizing anywhere between 25-75%,

with ~30-35% amortization being most common

Pricing

While pricing in the pro rata market is highly subjective depending upon

banking relationships and ancillary business, respondents to the Fed Survey

have now reported net pricing reductions for 30 consecutive quarters

In-line with Fed Survey responses, Fifth Third’s pro rata loan database

displayed a 28 bps drop of YoY spread for the 3Q17 vs. 3Q16 period,

bringing the average drawn spread down to L+186

With many pricing grids reaching levels below L+200, pricing levels are

approaching similar levels to investment grade and asset based loans,

suggesting little runway left for further pricing concessions in the pro rata

market

Source: Fifth Third Securities, Federal Reserve Board

Note: based on forward-looking nature of questionnaire, results displayed are from the first month of each respective calendar quarter (e.g. Jul-17 survey shown as proxy for 3Q17)

Average Pro Rata Pricing at Close by Market Segment (as of 3Q17)

LTM 3Q17 Synthetic Leverage Grid for Pro Rata Executions

126 149 162

193 221

240 256

298 322 334

355

L+0

L+50

L+100

L+150

L+200

L+250

L+300

L+350

L+400

Observation: Closing leverage determines ~97% (R2) of the variations in pricing; every 0.5x turn of leverage costs ~25bps (slope)

392420 410

429

275247

269293

186214

192211

L + 0

L + 50

L + 100

L + 150

L + 200

L + 250

L + 300

L + 350

L + 400

L + 450

L + 500

Current Prior Yr. Current Prior Yr.

Trailing 3M Trailing 12M

Middle Market Sponsored Middle Market Non-Sponsored Pro Rata/Bank-Only

16

Diversified Industrials – Specialty Distribution I Industry Spotlight

Q4 2017

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Gen. Corp. Purp. Amend & Extends DIP/Exit Fin. M&A Other

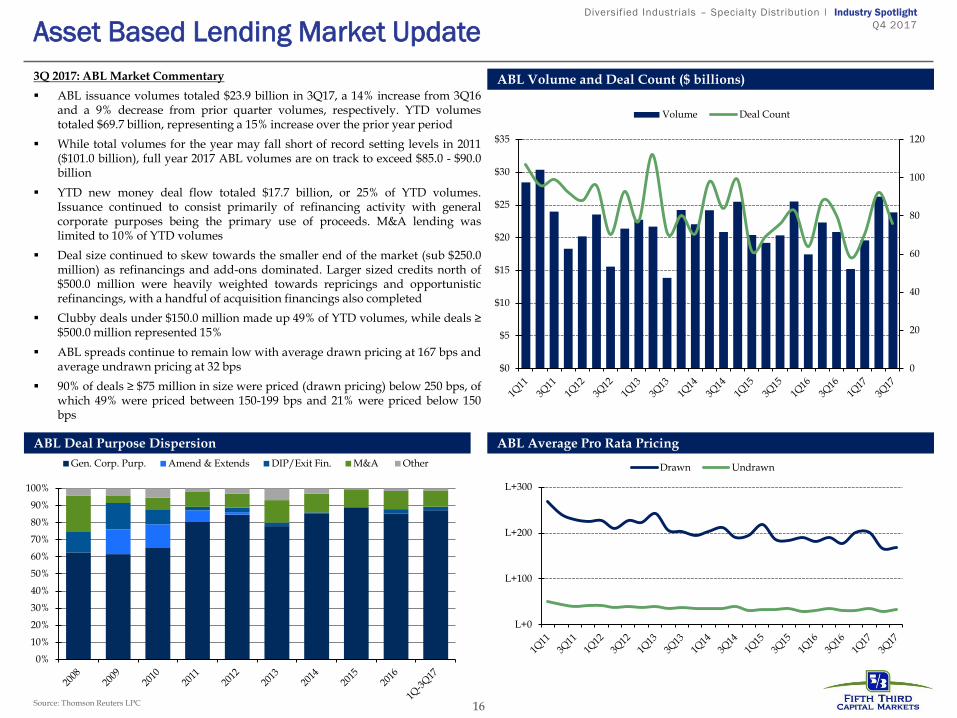

Asset Based Lending Market Update

ABL Volume and Deal Count ($ billions)

ABL Average Pro Rata Pricing

Source: Thomson Reuters LPC

3Q 2017: ABL Market Commentary

ABL issuance volumes totaled $23.9 billion in 3Q17, a 14% increase from 3Q16 and a 9% decrease from prior quarter volumes, respectively. YTD volumes totaled $69.7 billion, representing a 15% increase over the prior year period

While total volumes for the year may fall short of record setting levels in 2011 ($101.0 billion), full year 2017 ABL volumes are on track to exceed $85.0 - $90.0 billion

YTD new money deal flow totaled $17.7 billion, or 25% of YTD volumes. Issuance continued to consist primarily of refinancing activity with general corporate purposes being the primary use of proceeds. M&A lending was limited to 10% of YTD volumes

Deal size continued to skew towards the smaller end of the market (sub $250.0 million) as refinancings and add-ons dominated. Larger sized credits north of $500.0 million were heavily weighted towards repricings and opportunistic refinancings, with a handful of acquisition financings also completed

Clubby deals under $150.0 million made up 49% of YTD volumes, while deals ≥ $500.0 million represented 15%

ABL spreads continue to remain low with average drawn pricing at 167 bps and average undrawn pricing at 32 bps

90% of deals ≥ $75 million in size were priced (drawn pricing) below 250 bps, of which 49% were priced between 150-199 bps and 21% were priced below 150 bps

ABL Deal Purpose Dispersion

L+0

L+100

L+200

L+300

Drawn Undrawn

0

20

40

60

80

100

120

$0

$5

$10

$15

$20

$25

$30

$35

Volume Deal Count

17

Diversified Industrials – Specialty Distribution I Industry Spotlight

Q4 2017 Economic Dashboard

Industrial Production Index Capital Goods Orders Housing Starts

Source: Board of Governors of the Federal Reserve System

($ in billions)

Source: United States Census Bureau

National Unemployment Rate Real GDP Growth Additions to Non-Farm Payrolls

Housing Starts

Source: Bureau of Economic Analysis Source: Bureau of Labor Statistics Source: Bureau of Labor Statistics

Source: United States Census Bureau

(in thousands of employees)

(in thousands of units)

$200

$225

$250

$275

96

102

108

114

2.3%2.0%

2.6%

2.0%

0.9% 0.8%1.4%

3.5%

2.1%

1.4%

2.6%3.0%

4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q

'15 '16 '170

100

200

300

400

750

850

950

1,050

1,150

1,250

1,350

4.0%

5.0%

6.0%

18

Diversified Industrials – Specialty Distribution I Industry Spotlight

Q4 2017 Notes & Definitions

S&P 500 Index- A broad index that includes American Companies. EBITDA- A company's earnings before interest, taxes, depreciation, and amortization, is an accounting measure calculated using a company's net earnings, before interest expenses, taxes, depreciation and amortization are subtracted, as a proxy for a company's current operating profitability. Dry Powder- Refers to cash reserves kept on hand to cover future obligations or to purchase assets. GDP- Gross domestic product is the market value of the goods and services produced by labor and property located in the United States Consumer Sentiment Index- The University of Michigan Consumer Sentiment Index is a consumer confidence index published monthly by the University of Michigan. The index is normalized to have a value of 100 in December 1964 National Unemployment Rate- the percentage of the total labor force that is unemployed but actively seeking employment and willing to work. Non-Farm Payroll- Nonfarm payroll employment is a compiled name for goods, construction and manufacturing companies in the US. It does not include farm workers, private household employees, non-profit organization employees, or government employees . It is an economic indicator released monthly by the United States Department of Labor as part of a comprehensive report on the state of the labor market. Housing Starts- are the number of new residential construction projects that have begun during any particular month. The Economist- offers authoritative insight and opinion on international news, politics, business, finance, science, technology and the connections between them LBO -- leveraged buyout (LBO) is the acquisition of another company using a significant amount of borrowed money to meet the cost of acquisition. The assets of the company being acquired are often used as collateral for the loans, along with the assets of the acquiring company. Industrial Production Index (IPI)- is an economic indicator published by the Federal Reserve Board of the United States that measures the real production output of manufacturing, mining, and utilities Capital Goods Orders. Covenant-lite loans- means that debt is being issued, both personally and commercially, to borrowers with less restrictions on collateral, payment terms, and level of income. IRR-Internal Rate of Return.

About Fifth Third Capital Markets

Fifth Third Capital Markets is the marketing name under which Fifth Third Bank and its subsidiary, Fifth Third Securities, Inc., provide certain securities and investment banking products and services. Banking products and services are offered by Fifth Third Bank. Securities products and services are offered by licensed securities representatives of Fifth Third Securities, Inc., who may be employees of Fifth Third Bank. Important notice This document has been prepared by Fifth Third Bank (“Fifth Third”) or one of its subsidiaries for the sole purpose of providing a proposal to the parties to whom it is addressed in order that they may evaluate the capabilities of Fifth Third to supply the proposed services. It is not intended to provide specific investment advice or investment recommendations and does not constitute either a commitment to enter into a specific transaction or an offer or solicitation, with respect to the purchase or sale of any security. The information contained in this document has been compiled by Fifth Third and includes material which may have been obtained from information provided by various sources and discussions with management but has not been verified or audited. This document also contains confidential material proprietary to Fifth Third. Except in the general context of evaluating our capabilities, no reliance may be placed for any purposes whatsoever on the contents of this document or on its completeness. No representation or warranty, express or implied, is given and no responsibility or liability is or will be accepted by or on behalf of Fifth Third or by any of its subsidiaries, members, employees, agents or any other person as to the accuracy, completeness or correctness of the information contained in this document or any other oral information made available and any such liability is expressly disclaimed. This document and its contents are confidential and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person in whole or in part without our prior written consent.. Fifth Third Capital Markets is a wholly owned subsidiary of Fifth Third Bank offering investment banking++, debt capital markets+, bond capital markets++, equity capital markets++, financial risk management+, and fixed income sales and trading++. Fifth Third Bank provides access to investments and investment services through various subsidiaries, including Fifth Third Securities. Fifth Third Securities is the trade name used by Fifth Third Securities, Inc., member FINRA/SIPC, a registered broker-dealer and registered investment advisor registered with the U.S. Securities and Exchange Commission (SEC). Registration does not imply a certain level of skill or training. Securities and investments offered through Fifth Third Securities, Inc. and insurance products: + Services and activities offered through Fifth Third Bank ++ Services and activities offered through Fifth Third Securities, Inc © Fifth Third Bank 2018

19

Are Not FDIC Insured Offer No Bank Guarantee May Lose Value

Are Not Insured By Any Federal Government Agency Are Not A Deposit

19

Recommended