Shri Lakshmi Cotsyn Limited

Independent Equity Research Enhancing investment decisions

In-depth analysis of the fundamentals and valuation

Business Prospects Financial Performance

Corporate Governance

Management Evaluation

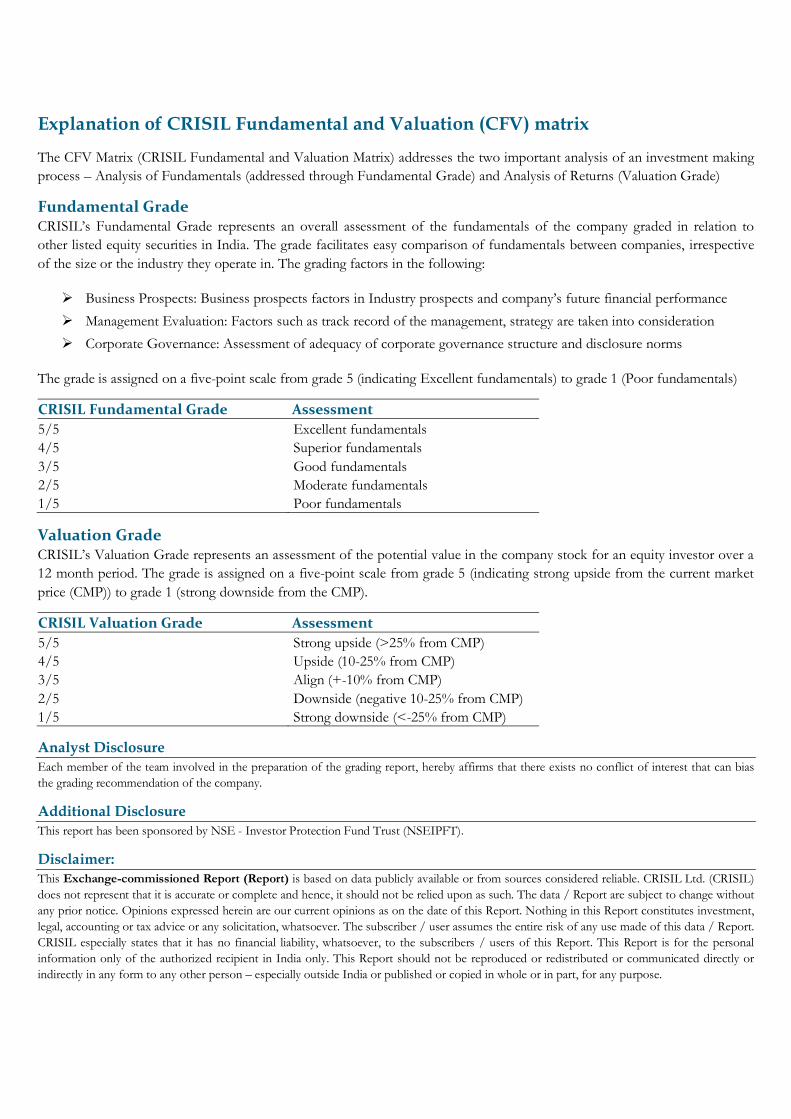

Explanation of CRISIL Fundamental and Valuation (CFV) matrix The CFV Matrix (CRISIL Fundamental and Valuation Matrix) addresses the two important analysis of an investment making process – Analysis of Fundamentals (addressed through Fundamental Grade) and Analysis of Returns (Valuation Grade)

Fundamental Grade CRISIL’s Fundamental Grade represents an overall assessment of the fundamentals of the company graded in relation to other listed equity securities in India. The grade facilitates easy comparison of fundamentals between companies, irrespective of the size or the industry they operate in. The grading factors in the following:

Business Prospects: Business prospects factors in Industry prospects and company’s future financial performance Management Evaluation: Factors such as track record of the management, strategy are taken into consideration Corporate Governance: Assessment of adequacy of corporate governance structure and disclosure norms

The grade is assigned on a five-point scale from grade 5 (indicating Excellent fundamentals) to grade 1 (Poor fundamentals)

CRISIL Fundamental Grade Assessment 5/5 Excellent fundamentals 4/5 Superior fundamentals 3/5 Good fundamentals 2/5 Moderate fundamentals 1/5 Poor fundamentals

Valuation Grade CRISIL’s Valuation Grade represents an assessment of the potential value in the company stock for an equity investor over a 12 month period. The grade is assigned on a five-point scale from grade 5 (indicating strong upside from the current market price (CMP)) to grade 1 (strong downside from the CMP).

CRISIL Valuation Grade Assessment 5/5 Strong upside (>25% from CMP) 4/5 Upside (10-25% from CMP) 3/5 Align (+-10% from CMP) 2/5 Downside (negative 10-25% from CMP) 1/5 Strong downside (<-25% from CMP) Analyst Disclosure Each member of the team involved in the preparation of the grading report, hereby affirms that there exists no conflict of interest that can bias the grading recommendation of the company. Additional Disclosure This report has been sponsored by NSE - Investor Protection Fund Trust (NSEIPFT). Disclaimer: This Exchange-commissioned Report (Report) is based on data publicly available or from sources considered reliable. CRISIL Ltd. (CRISIL) does not represent that it is accurate or complete and hence, it should not be relied upon as such. The data / Report are subject to change without any prior notice. Opinions expressed herein are our current opinions as on the date of this Report. Nothing in this Report constitutes investment, legal, accounting or tax advice or any solicitation, whatsoever. The subscriber / user assumes the entire risk of any use made of this data / Report. CRISIL especially states that it has no financial liability, whatsoever, to the subscribers / users of this Report. This Report is for the personal information only of the authorized recipient in India only. This Report should not be reproduced or redistributed or communicated directly or indirectly in any form to any other person – especially outside India or published or copied in whole or in part, for any purpose.

CRISIL Equities 1

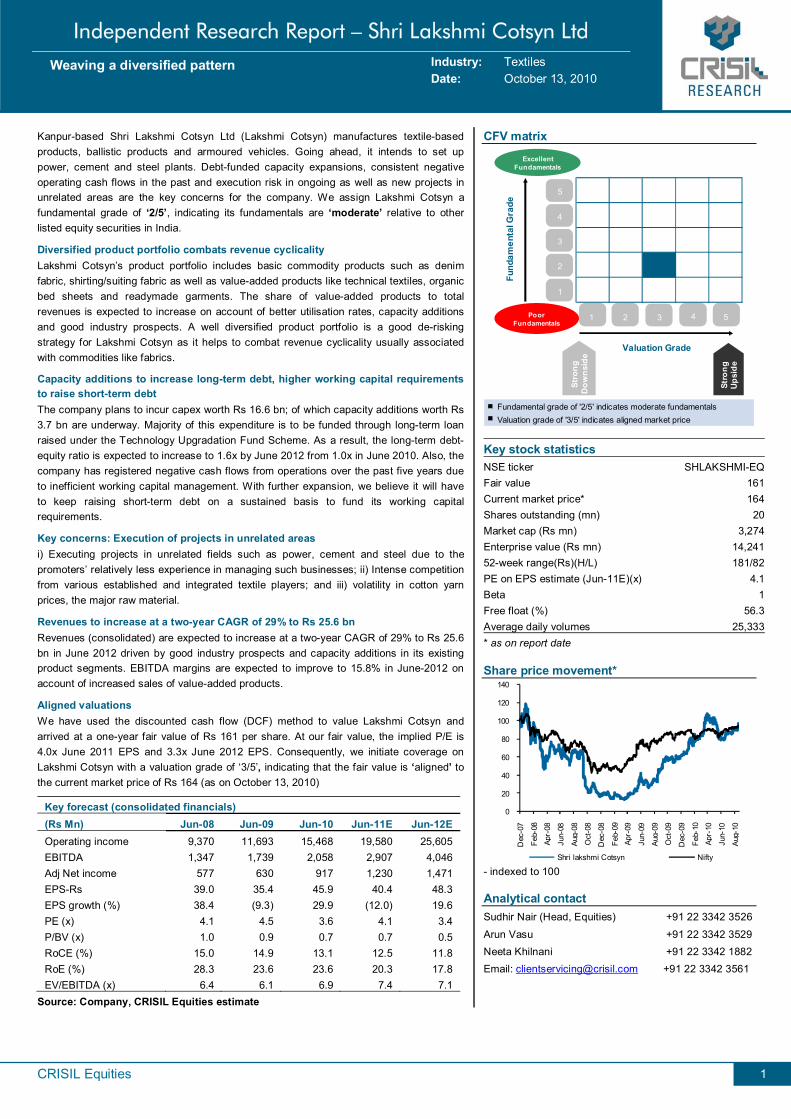

Weaving a diversified pattern Industry: Textiles Date: October 13, 2010

Independent Research Report – Shri Lakshmi Cotsyn Ltd

Kanpur-based Shri Lakshmi Cotsyn Ltd (Lakshmi Cotsyn) manufactures textile-based products, ballistic products and armoured vehicles. Going ahead, it intends to set up power, cement and steel plants. Debt-funded capacity expansions, consistent negative operating cash flows in the past and execution risk in ongoing as well as new projects in unrelated areas are the key concerns for the company. We assign Lakshmi Cotsyn a fundamental grade of ‘2/5’, indicating its fundamentals are ‘moderate’ relative to other listed equity securities in India.

Diversified product portfolio combats revenue cyclicality Lakshmi Cotsyn’s product portfolio includes basic commodity products such as denim fabric, shirting/suiting fabric as well as value-added products like technical textiles, organic bed sheets and readymade garments. The share of value-added products to total revenues is expected to increase on account of better utilisation rates, capacity additions and good industry prospects. A well diversified product portfolio is a good de-risking strategy for Lakshmi Cotsyn as it helps to combat revenue cyclicality usually associated with commodities like fabrics.

Capacity additions to increase long-term debt, higher working capital requirements to raise short-term debt The company plans to incur capex worth Rs 16.6 bn; of which capacity additions worth Rs 3.7 bn are underway. Majority of this expenditure is to be funded through long-term loan raised under the Technology Upgradation Fund Scheme. As a result, the long-term debt-equity ratio is expected to increase to 1.6x by June 2012 from 1.0x in June 2010. Also, the company has registered negative cash flows from operations over the past five years due to inefficient working capital management. With further expansion, we believe it will have to keep raising short-term debt on a sustained basis to fund its working capital requirements.

Key concerns: Execution of projects in unrelated areas i) Executing projects in unrelated fields such as power, cement and steel due to the promoters’ relatively less experience in managing such businesses; ii) Intense competition from various established and integrated textile players; and iii) volatility in cotton yarn prices, the major raw material.

Revenues to increase at a two-year CAGR of 29% to Rs 25.6 bn Revenues (consolidated) are expected to increase at a two-year CAGR of 29% to Rs 25.6 bn in June 2012 driven by good industry prospects and capacity additions in its existing product segments. EBITDA margins are expected to improve to 15.8% in June-2012 on account of increased sales of value-added products.

Aligned valuations We have used the discounted cash flow (DCF) method to value Lakshmi Cotsyn and arrived at a one-year fair value of Rs 161 per share. At our fair value, the implied P/E is 4.0x June 2011 EPS and 3.3x June 2012 EPS. Consequently, we initiate coverage on Lakshmi Cotsyn with a valuation grade of ‘3/5’, indicating that the fair value is ‘aligned’ to the current market price of Rs 164 (as on October 13, 2010)

Key forecast (consolidated financials) (Rs Mn) Jun-08 Jun-09 Jun-10 Jun-11E Jun-12E Operating income 9,370 11,693 15,468 19,580 25,605 EBITDA 1,347 1,739 2,058 2,907 4,046 Adj Net income 577 630 917 1,230 1,471 EPS-Rs 39.0 35.4 45.9 40.4 48.3 EPS growth (%) 38.4 (9.3) 29.9 (12.0) 19.6 PE (x) 4.1 4.5 3.6 4.1 3.4 P/BV (x) 1.0 0.9 0.7 0.7 0.5 RoCE (%) 15.0 14.9 13.1 12.5 11.8 RoE (%) 28.3 23.6 23.6 20.3 17.8 EV/EBITDA (x) 6.4 6.1 6.9 7.4 7.1

Source: Company, CRISIL Equities estimate

CFV matrix

Fundamental grade of '2/5' indicates moderate fundamentalsValuation grade of '3/5' indicates aligned market price

1

2

3

4

5

1 2 3 4 5

Valuation Grade

Fund

amen

tal G

rade

Poor Fundamentals

ExcellentFundamentals

Stro

ngD

owns

ide

Stro

ngUp

side

Key stock statistics NSE ticker SHLAKSHMI-EQFair value 161Current market price* 164Shares outstanding (mn) 20Market cap (Rs mn) 3,274Enterprise value (Rs mn) 14,24152-week range(Rs)(H/L) 181/82PE on EPS estimate (Jun-11E)(x) 4.1Beta 1Free float (%) 56.3Average daily volumes 25,333* as on report date Share price movement*

0

20

40

60

80

100

120

140

Dec

-07

Feb-

08

A pr-

08

Jun-

08

Aug-

08

Oct

-08

Dec

-08

Feb-

09Ap

r-09

Jun-

09

Aug-

09

Oct

-09

Dec

-09

Feb-

10

A pr-

10

Jun-

10

Aug-

10

Shri lakshmi Cotsyn Nifty - indexed to 100 Analytical contact Sudhir Nair (Head, Equities) +91 22 3342 3526

Arun Vasu +91 22 3342 3529 Neeta Khilnani +91 22 3342 1882 Email: [email protected] +91 22 3342 3561

CR

ISIL

Equ

ities

Shri

Laks

hmi C

otsy

n Li

mite

d

2

Tabl

e 1:

Lak

shm

i Cot

syn:

Bus

ines

s O

verv

iew

Pa

ram

eter

Shir

ting/

Suiti

ngDe

nim

Tech

nica

l tex

tiles

Hom

e fu

rnis

hing

Bott

om w

eigh

tG

arm

ents

Oth

ers

Reve

nue

cont

ribu

tion

(Jun

e 20

10)

14.1

%14

.5%

32.4

%22

.0%

4.5%

0.5%

12.0

%

Reve

nue

cont

ribu

tion

(Jun

e 20

12)

8.4%

9.0%

25.1

%30

.7%

2.8%

14.2

%9.

8%

i)

Fusi

ble

Inte

rlini

ng u

nder

the

bran

d 'S

tar T

rack

'-use

d in

col

lars

, cuf

fs, e

tc.

i)

Val

ue-a

dded

/ org

anic

bed

she

ets,

fo

r eg.

Vita

min

-E e

nric

hed

bed

shee

ts

sold

und

er th

e br

and

nam

e 'W

eave

s'

i)

Qui

lted

and

embr

oide

ry fa

bric

s un

der t

he b

rand

nam

e 'G

alax

y'

ii)

P.U.

coa

ted

nylo

n fa

bric

ii)

Terr

y to

wel

ii)

Defe

nce

arm

oure

d ve

hicl

es

sold

und

er th

e br

and

'Dhr

uv',

'Dro

na' a

nd 'V

iper

' thr

ough

its

who

lly o

wne

d su

bsid

iary

Lak

shm

i De

fenc

e So

lutio

ns L

tdiii)

Fire

reta

rdan

t fab

riciii)

Cus

hion

s, ta

ble

cove

rs, e

tc.

iii) S

ales

from

UA

E Su

bsid

iary

w

hich

mai

nly

trade

s in

dre

ss

mat

eria

lsiv

) IR

R fa

bric

v)

Cam

oufla

ge p

rinte

d fa

bric

vi)

Ballis

tic p

rodu

cts

Geo

grap

hic

pres

ence

(Jun

e 20

10)

i)

A s

mal

l pla

yer i

n th

e hi

ghly

frag

men

ted

shirt

ing

and

suitin

g se

gmen

t

i)

Arv

ind

and

Aar

vee

Deni

ms

are

the

two

larg

est p

laye

rs in

the

dom

estic

den

im in

dust

ry w

ith m

arke

t sh

ares

of 2

4% a

nd12

%

resp

ectiv

ely

as o

f end

of 2

009

i)

The

mar

ket s

ize

of th

is s

egm

ent i

s es

timat

ed to

be

Rs 3

9.8

bn a

s of

200

8-09

; Lak

shm

i Cot

syn

has

a sh

are

of ~

8%

ii)

Mar

ket s

ize

for

shirt

ing/

suitin

g w

as 2

,236

m

n m

eter

s at

the

end

of

2008

, with

Lak

shm

i Cot

syn

havi

ng a

sha

re o

f ~1%

ii)

Laks

hmi C

otsy

n is

a re

lativ

ely

smal

l pla

yer i

n th

e de

nim

indu

stry

w

ith a

mar

ket s

hare

of ~

4% a

s at

en

d of

200

9

ii)

It is

one

of t

he la

rges

t m

anuf

actu

rers

of m

icro

dot f

usib

le

inte

rlini

ng, w

hich

form

s ~1

.5%

of t

he

tota

l tec

hnic

al te

xtile

s se

gmen

t

Key

com

petit

ors

Siya

ram

, Ray

mon

dsA

rvin

d, A

arve

e De

nim

s, K

.G D

enim

s V

ardh

man

, Bom

bay

Dyei

ng, A

shim

a,

Sang

am (I

ndia

), A

rex

Indu

strie

s, o

ther

sm

all u

norg

anis

ed p

laye

rs

Alo

k In

dust

ries,

Wel

spun

Indi

a A

lok

Indu

strie

s, V

ardh

man

Te

xtile

s, S

iyar

am a

nd v

ario

us

othe

r org

anis

ed p

laye

rs

Mad

ura

Gar

men

ts, K

ewal

Ki

ran

Clot

hing

Lim

ited,

Zo

diac

, Alo

k In

dust

ries,

V

ardh

man

Tex

tiles

Tata

Adv

ance

d M

ater

ials

Ltd

, M

ahin

dra

Defe

nce

Syst

ems

Text

iles

Prod

uct /

ser

vice

of

feri

ngSh

irtin

g/su

iting

fabr

ic

mai

nly

for t

he lo

wer

mid

dle-

clas

s se

gmen

t

Deni

m fa

bric

Botto

mw

eigh

tfa

bric

used

intro

user

s, e

tc.

Gar

men

ts u

nder

the

bran

d 'S

tero

id' a

nd 'D

YFI

'

iv)

Mis

c sa

les

such

as

clot

hing

ac

cess

orie

s un

der t

he b

rand

'A

lisha

'

Dom

estic

sal

es: 9

4%; e

xpor

ts: 6

%

- Maj

ority

of t

he d

omes

tic s

ales

is to

uno

rgan

ised

dea

lers

/dis

tribu

tors

/trad

ers.

-M

ajor

ity o

f the

exp

ort s

ales

is to

IKEA

, Sw

eden

and

Wal

mar

t, Ca

nada

Mar

ket p

ositi

onHo

me

furn

ishi

ng m

arke

t siz

e es

timat

ed

to b

e ~R

s 13

5 bn

as

of e

nd 2

009.

The

co

mpa

ny h

as a

mar

ket s

hare

of ~

2%

The

tota

l mar

ket s

ize

for

read

ymad

e tro

user

s w

as 3

87

mn

met

ers

(323

mn

piec

es) a

s of

200

8. L

aksh

mi C

otsy

n is

a

rela

tivel

y sm

all p

laye

r with

a

capa

city

of

6 m

n m

eter

s an

d a

mar

ket s

hare

of ~

1.5%

Rel

ativ

ely

smal

l pla

yer i

n th

e br

ande

d re

adym

ade

garm

ents

seg

men

t

A n

ew e

ntra

nt in

the

field

of

man

ufac

turin

g ar

mou

red

vehi

cles

. Fa

ces

stiff

com

petit

ion

from

es

tabl

ishe

d pl

ayer

s lik

e Ta

ta a

nd

Mah

indr

a

So

urce

: CR

ISIL

Equ

ities

, Min

istr

y of

Tex

tiles

, Tex

tile

Surv

ey C

omm

ittee

200

9

CRISIL Equities

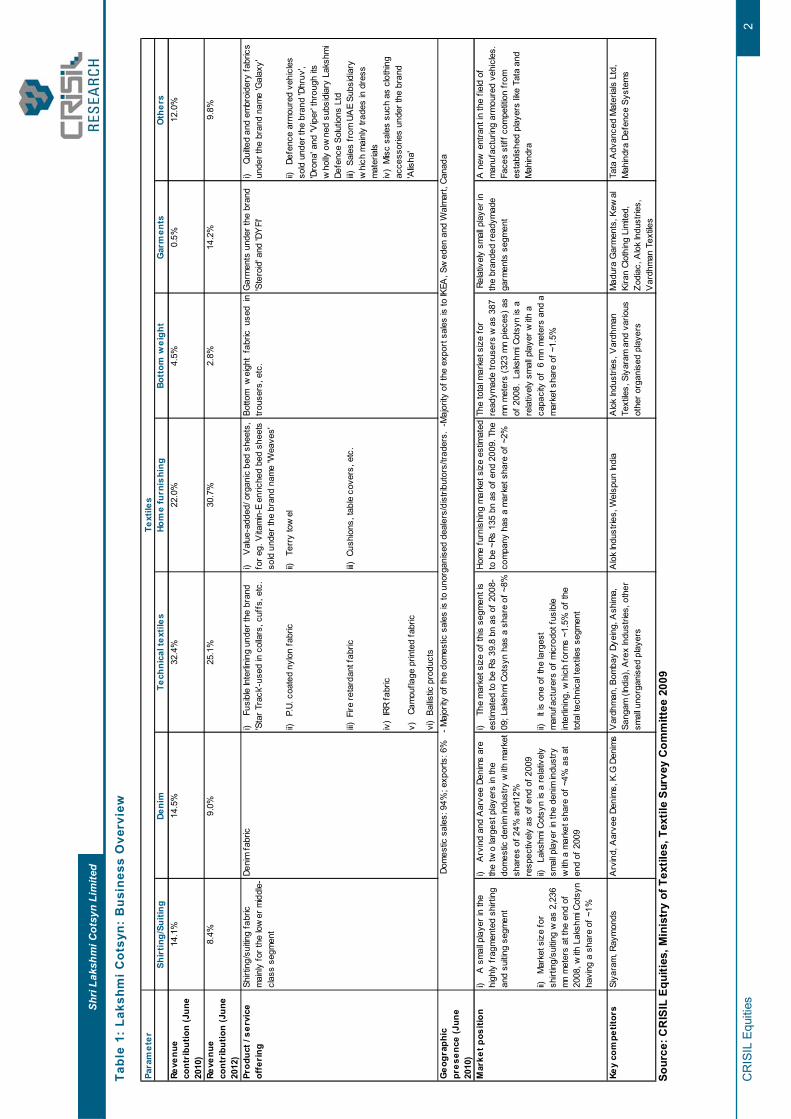

Shri Lakshmi Cotsyn Limited

3

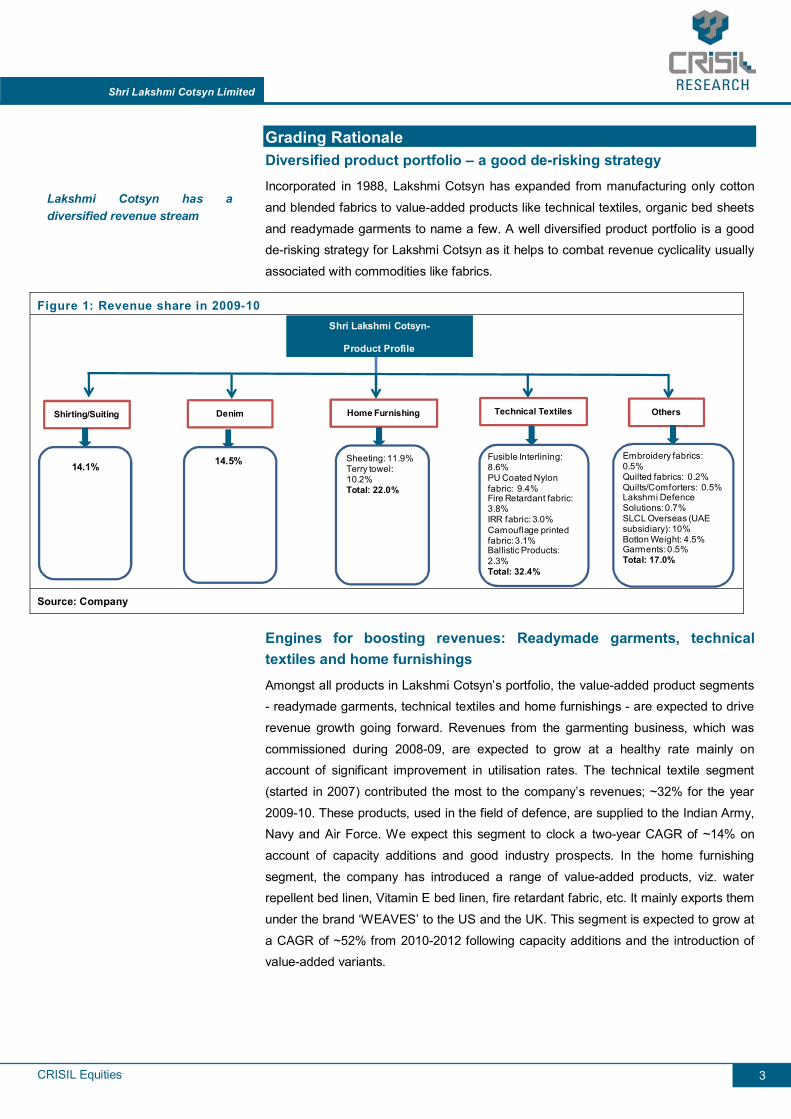

Grading Rationale Diversified product portfolio – a good de-risking strategy Incorporated in 1988, Lakshmi Cotsyn has expanded from manufacturing only cotton

and blended fabrics to value-added products like technical textiles, organic bed sheets

and readymade garments to name a few. A well diversified product portfolio is a good de-risking strategy for Lakshmi Cotsyn as it helps to combat revenue cyclicality usually

associated with commodities like fabrics.

Figure 1: Revenue share in 2009-10 Shri Lakshmi Cotsyn-

Product Profile

Shirting/Suiting Denim Home Furnishing Technical Textiles Others

14.1% 14.5% Sheeting: 11.9% Terry towel: 10.2%Total: 22.0%

Fusible Interlining: 8.6%PU Coated Nylon fabric: 9.4%Fire Retardant fabric: 3.8% IRR fabric: 3.0%Camouflage printed fabric: 3.1%Ballistic Products: 2.3%Total: 32.4%

Embroidery fabrics: 0.5%Quilted fabrics: 0.2%Quilts/Comforters: 0.5% Lakshmi Defence Solutions: 0.7%SLCL Overseas (UAE subsidiary): 10%Botton Weight: 4.5%Garments: 0.5%Total: 17.0%

Source: Company

Engines for boosting revenues: Readymade garments, technical textiles and home furnishings

Amongst all products in Lakshmi Cotsyn’s portfolio, the value-added product segments - readymade garments, technical textiles and home furnishings - are expected to drive

revenue growth going forward. Revenues from the garmenting business, which was

commissioned during 2008-09, are expected to grow at a healthy rate mainly on account of significant improvement in utilisation rates. The technical textile segment

(started in 2007) contributed the most to the company’s revenues; ~32% for the year

2009-10. These products, used in the field of defence, are supplied to the Indian Army, Navy and Air Force. We expect this segment to clock a two-year CAGR of ~14% on

account of capacity additions and good industry prospects. In the home furnishing

segment, the company has introduced a range of value-added products, viz. water repellent bed linen, Vitamin E bed linen, fire retardant fabric, etc. It mainly exports them

under the brand ‘WEAVES’ to the US and the UK. This segment is expected to grow at

a CAGR of ~52% from 2010-2012 following capacity additions and the introduction of value-added variants.

Lakshmi Cotsyn has a diversified revenue stream

CRISIL Equities

Shri Lakshmi Cotsyn Limited

4

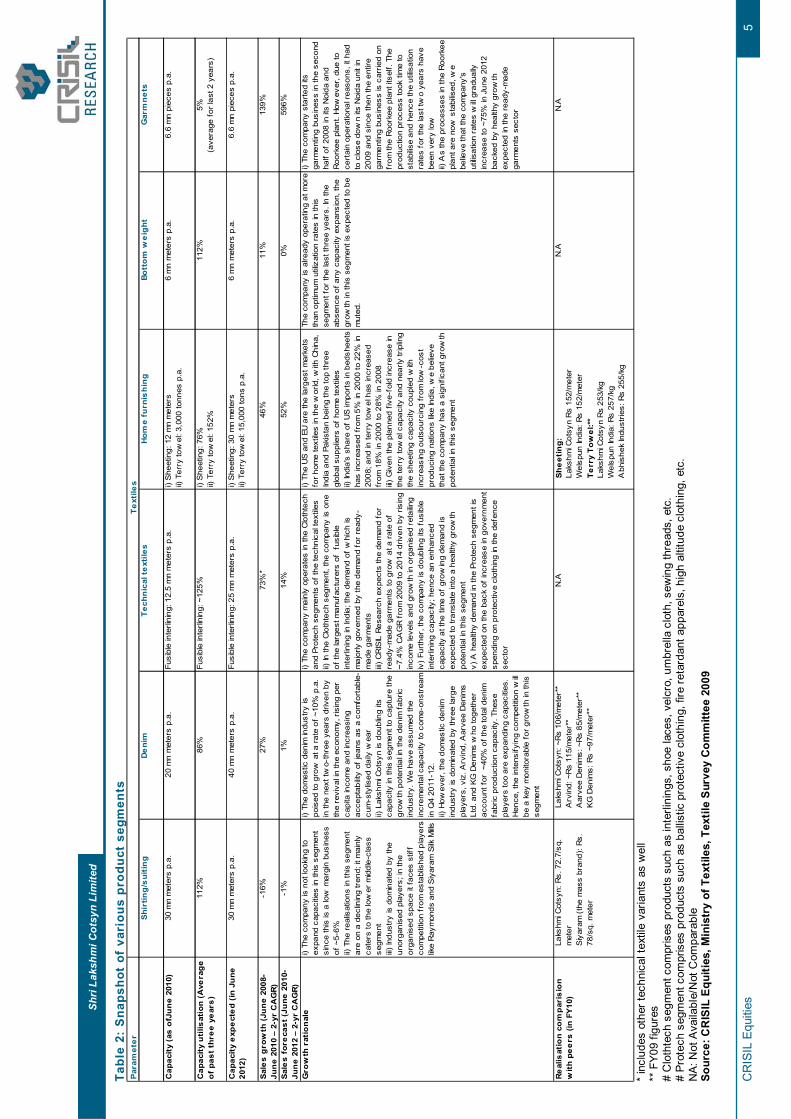

Industry outlook: CRISIL Research has estimated the domestic readymade garments

industry to grow at a CAGR of 7.4% from Rs 1,155 bn in 2009 to Rs 1,649 bn by 2014

driven by a rise in income levels, growing preference for readymade garments vis-à-vis tailored garments, and growth in organised retailing. The market size of the technical

textile segment in India is estimated to be ~Rs 39.8 bn as of 2008-09 and is expected

to grow at a CAGR of 11% to Rs 66.4 bn in 2012-13.(Source: Ministry of textiles) Majority of the home-furnishing products manufactured domestically are exported to the

US and the European Union. India, Pakistan and China are the key players in the US

market for bed linen, accounting for ~85% of the total market in value terms. Although, the slowdown in the US economy had impacted Indian exports, India managed to

slightly improve its market share from 16.8% during January-July 2008 period to 17.8%

during January-July 2009 period (Source: CRISIL Research). Post the downturn, home furnishing exports are expected to grow given the increased outsourcing from low-cost

producing nations like India.

CR

ISIL

Equ

ities

Shri

Laks

hmi C

otsy

n Li

mite

d

5

Tabl

e 2:

Sna

psho

t of

var

ious

pro

duct

seg

men

ts

Par

amet

er

Shi

rtin

g/s

uiti

ng

De

nim

Tec

hnic

al t

ext

iles

Hom

e fu

rnis

hin

gBo

tto

m w

eig

htG

arm

ne

ts

Cap

acit

y (a

s o

fJu

ne

201

0)30

mn

met

ers

p.a.

20 m

n m

eter

s p.

a.Fu

sibl

e in

terli

ning

: 12.

5 m

n m

eter

s p.

a.i)

She

etin

g: 1

2 m

n m

eter

s

ii)

Ter

ry to

wel

: 3,0

00 to

nnes

p.a

.6

mn

met

ers

p.a.

6.6

mn

piec

es p

.a.

Cap

acit

y u

tilis

atio

n (

Ave

rag

e

of

past

thr

ee

ye

ars

)11

2%86

%Fu

sibl

e in

terli

ning

: ~12

5%i)

She

etin

g: 7

6%

ii) T

erry

tow

el: 1

52%

112%

5%

(ave

rage

for l

ast 2

yea

rs)

Cap

acit

y e

xpe

cte

d (

in J

une

20

12)

30 m

n m

eter

s p.

a.40

mn

met

ers

p.a.

Fusi

ble

inte

rlini

ng: 2

5 m

n m

eter

s p.

a.i)

She

etin

g: 3

0 m

n m

eter

s

ii) T

erry

tow

el: 1

5,00

0 to

ns p

.a.

6 m

n m

eter

s p.

a.6.

6 m

n pi

eces

p.a

.

Sal

es

gro

wth

(Ju

ne

200

8-Ju

ne

201

0 –

2-yr

CA

GR

)-1

6%27

%73

%*

46%

11%

139%

Sal

es

for

eca

st (J

une

201

0-Ju

ne

201

2 –

2-yr

CA

GR

) -1

%1%

14%

52%

0%59

6%

Gro

wth

rat

ion

ale

i) Th

e co

mpa

ny is

not

look

ing

to

expa

nd c

apac

ities

in th

is s

egm

ent

sinc

e th

is is

a lo

w m

argi

n bu

sine

ss

of ~

5-6%

ii)

The

real

isat

ions

in th

is s

egm

ent

are

on a

dec

linin

g tr

end;

it m

ainl

y ca

ters

to th

e lo

wer

mid

dle-

clas

s se

gmen

t

iii) In

dust

ry is

dom

inat

ed b

y th

e un

orga

nise

d pl

ayer

s; in

the

orga

nise

d sp

ace

it fa

ces

stiff

co

mpe

titio

n fr

om e

stab

lishe

d pl

ayer

s lik

e R

aym

onds

and

Siy

aram

Silk

Mills

i) Th

e do

mes

tic d

enim

indu

stry

is

pois

ed to

gro

w a

t a ra

te o

f ~10

% p

.a.

in th

e ne

xt tw

o-th

ree

year

s dr

iven

by

the

revi

val i

n th

e ec

onom

y, r

isin

g pe

r ca

pita

inco

me

and

incr

easi

ng

acce

ptab

ility

of je

ans

as a

com

fort

able

- cu

m-s

tylis

ed d

aily

wea

r

ii) L

aksh

mi C

otsy

n is

dou

blin

g its

ca

paci

ty in

this

seg

men

t to

capt

ure

the

grow

th p

oten

tial in

the

deni

m fa

bric

in

dust

ry. W

e ha

ve a

ssum

ed th

e in

crem

enta

l cap

acity

to c

ome-

onst

ream

in

Q4

2011

-12.

ii) H

owev

er, t

he d

omes

tic d

enim

in

dust

ry is

dom

inat

ed b

y th

ree

larg

e pl

ayer

s, v

iz. A

rvin

d, A

arve

e D

enim

s Lt

d. a

nd K

G D

enim

s w

ho to

geth

er

acco

unt f

or ~

40%

of t

he to

tal d

enim

fa

bric

pro

duct

ion

capa

city

. The

se

play

ers

too

are

expa

ndin

g ca

paci

ties.

H

ence

, the

inte

nsify

ing

com

petit

ion

will

be a

key

mon

itora

ble

for g

row

th in

this

se

gmen

t

i) Th

e co

mpa

ny m

ainl

y op

erat

es in

the

Clo

thte

ch

and

Prot

ech

segm

ents

of t

he te

chni

cal t

extil

es

ii) In

the

Clo

thte

ch s

egm

ent,

the

com

pany

is o

ne

of th

e la

rges

t man

ufac

ture

rs o

f f

usib

le

inte

rlini

ng in

Indi

a; th

e de

man

d of

whi

ch is

m

ajor

ly g

over

ned

by th

e de

man

d fo

r re

ady-

mad

e ga

rmen

ts

iii) C

RIS

IL R

esea

rch

expe

cts

the

dem

and

for

read

y-m

ade

garm

ents

to g

row

at a

rat

e of

~7

.4%

CA

GR

fro

m 2

009

to 2

014

driv

en b

y ris

ing

inco

me

leve

ls a

nd g

row

th in

org

anis

ed r

etai

ling

iv)

Furth

er, t

he c

ompa

ny is

dou

blin

g its

fus

ible

in

terli

ning

cap

acity

; hen

ce a

n en

hanc

ed

capa

city

at t

he ti

me

of g

row

ing

dem

and

is

expe

cted

to tr

ansl

ate

into

a h

ealth

y gr

owth

po

tent

ial i

n th

is s

egm

ent

v)

A h

ealth

y de

man

d in

the

Prot

ech

segm

ent i

s ex

pect

ed o

n th

e ba

ck o

f in

crea

se in

gov

ernm

ent

spen

ding

on

prot

ectiv

e cl

othi

ng in

the

defe

nce

sect

or

i) Th

e U

S a

nd E

U a

re th

e la

rges

t mar

kets

fo

r hom

e te

xtile

s in

the

wor

ld, w

ith C

hina

, In

dia

and

Paki

stan

bei

ng th

e to

p th

ree

glob

al s

uppl

iers

of

hom

e te

xtile

s

ii)

Indi

a's

shar

e of

US

impo

rts

in b

edsh

eets

ha

s in

crea

sed

from

5%

in 2

000

to 2

2% in

20

08; a

nd in

terr

y to

wel

has

incr

ease

d fr

om 1

8% in

200

0 to

28%

in 2

008

iii)

Giv

en th

e pl

anne

d fiv

e-fo

ld in

crea

se in

th

e te

rry

tow

el c

apac

ity a

nd n

early

trip

ling

the

shee

ting

capa

city

cou

pled

with

in

crea

sing

out

sour

cing

fro

m lo

w-c

ost

prod

ucin

g na

tions

like

Indi

a, w

e be

lieve

th

at th

e co

mpa

ny h

as a

sig

nific

ant g

row

th

pote

ntia

l in

this

seg

men

t

The

com

pany

is a

lread

y op

erat

ing

at m

ore

than

opt

imum

util

izat

ion

rate

s in

this

se

gmen

t for

the

last

thre

e ye

ars.

In th

e ab

senc

e of

any

cap

acity

exp

ansi

on, t

he

grow

th in

this

seg

men

t is

expe

cted

to b

e m

uted

.

i) Th

e co

mpa

ny s

tarte

d its

ga

rmen

ting

busi

ness

in th

e se

cond

ha

lf of

200

8 in

its

Noi

da a

nd

Roo

rkee

pla

nt. H

owev

er, d

ue to

ce

rtai

n op

erat

iona

l rea

sons

, it h

ad

to c

lose

dow

n its

Noi

da u

nit i

n 20

09 a

nd s

ince

then

the

entir

e ga

rmen

ting

busi

ness

is c

arrie

d on

fr

om th

e R

oork

ee p

lant

itse

lf. T

he

prod

uctio

n pr

oces

s to

ok ti

me

to

stab

ilise

and

henc

e th

e ut

ilisat

ion

rate

s fo

r th

e la

st tw

o ye

ars

have

be

en v

ery

low

ii) A

s th

e pr

oces

ses

in th

e R

oork

ee

plan

t are

now

sta

bilis

ed, w

e be

lieve

that

the

com

pany

's

utilis

atio

n ra

tes

will

grad

ually

in

crea

se to

~75

% in

Jun

e 20

12

back

ed b

y he

alth

y gr

owth

ex

pect

ed in

the

read

y-m

ade

garm

ents

sec

tor

Re

alis

atio

n co

mp

aris

ion

wit

h p

ee

rs (

in F

Y10

)La

kshm

i Cot

syn:

Rs.

72.

7/sq

. m

eter

Siy

aram

(th

e m

ass

bran

d): R

s.

78/s

q. m

eter

Laks

hmi C

otsy

n: ~

Rs

106/

met

er**

A

rvin

d: ~

Rs

115/

met

er**

A

arve

e D

enim

s: ~

Rs

85/m

eter

**

KG

Den

ims:

Rs

~97/

met

er**

N.A

S

he

etin

g:

La

kshm

i Cot

syn

Rs

152/

met

er

W

elsp

un In

dia:

Rs

152/

met

er

Te

rry

To

wel

:**

La

kshm

i Cot

syn

Rs

253/

kg

W

elsp

un In

dia:

Rs

257/

kg

Abh

ishe

k In

dust

ries:

Rs

255/

kg

N.A

N.

A

Te

xtile

s

*

incl

udes

oth

er te

chni

cal t

extil

e va

riant

s as

wel

l **

FY0

9 fig

ures

#

Clo

thte

ch s

egm

ent c

ompr

ises

pro

duct

s su

ch a

s in

terli

ning

s, s

hoe

lace

s, v

elcr

o, u

mbr

ella

clo

th, s

ewin

g th

read

s, e

tc.

# Pr

otec

h se

gmen

t com

pris

es p

rodu

cts

such

as

ballis

tic p

rote

ctiv

e cl

othi

ng, f

ire re

tard

ant a

ppar

els,

hig

h al

titud

e cl

othi

ng, e

tc.

NA:

Not

Ava

ilabl

e/N

ot C

ompa

rabl

e So

urce

: CR

ISIL

Equ

ities

, Min

istr

y of

Tex

tiles

, Tex

tile

Surv

ey C

omm

ittee

200

9

CRISIL Equities

Shri Lakshmi Cotsyn Limited

6

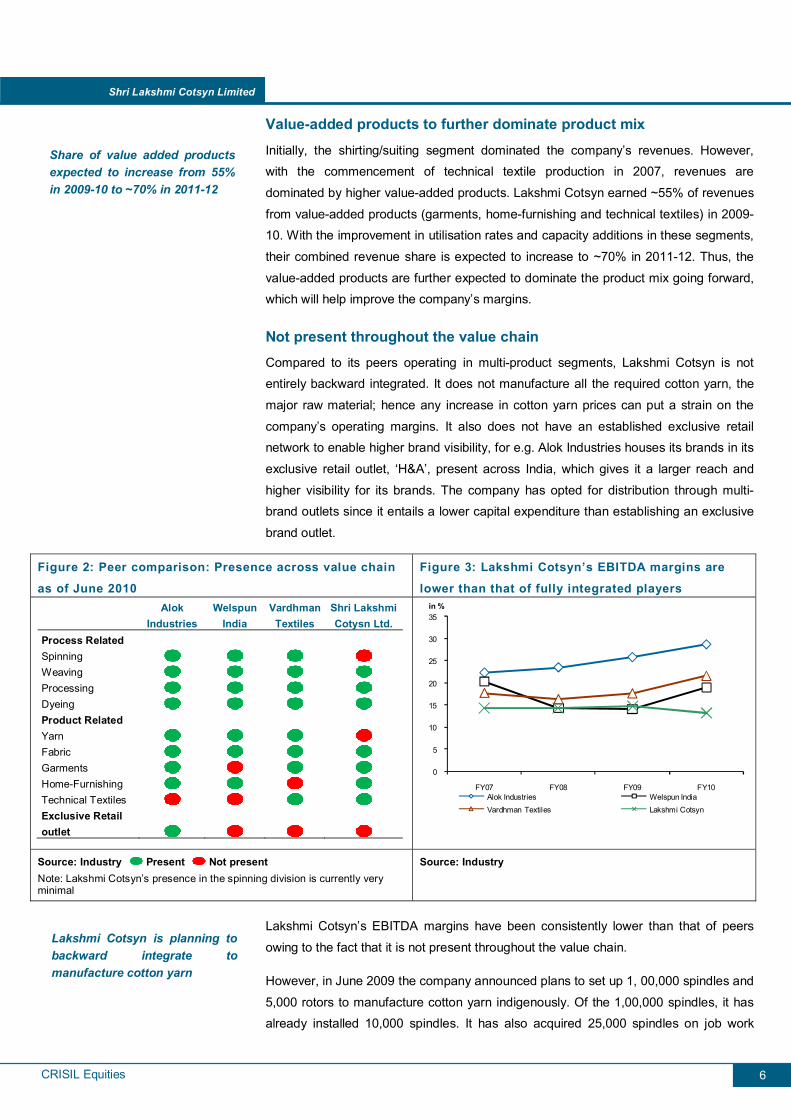

Value-added products to further dominate product mix

Initially, the shirting/suiting segment dominated the company’s revenues. However, with the commencement of technical textile production in 2007, revenues are

dominated by higher value-added products. Lakshmi Cotsyn earned ~55% of revenues

from value-added products (garments, home-furnishing and technical textiles) in 2009-10. With the improvement in utilisation rates and capacity additions in these segments,

their combined revenue share is expected to increase to ~70% in 2011-12. Thus, the

value-added products are further expected to dominate the product mix going forward, which will help improve the company’s margins.

Not present throughout the value chain Compared to its peers operating in multi-product segments, Lakshmi Cotsyn is not entirely backward integrated. It does not manufacture all the required cotton yarn, the

major raw material; hence any increase in cotton yarn prices can put a strain on the

company’s operating margins. It also does not have an established exclusive retail network to enable higher brand visibility, for e.g. Alok Industries houses its brands in its

exclusive retail outlet, ‘H&A’, present across India, which gives it a larger reach and

higher visibility for its brands. The company has opted for distribution through multi-brand outlets since it entails a lower capital expenditure than establishing an exclusive

brand outlet.

Figure 2: Peer comparison: Presence across value chain

as of June 2010

Figure 3: Lakshmi Cotsyn’s EBITDA margins are

lower than that of fully integrated players

Alok

Industries Welspun

India Vardhman

Textiles Shri Lakshmi Cotysn Ltd.

Process Related Spinning

Weaving

Processing

Dyeing

Product Related Yarn

Fabric

Garments

Home-Furnishing

Technical Textiles

Exclusive Retail outlet

0

5

10

15

20

25

30

35

FY07 FY08 FY09 FY10

in %

Alok Industries Welspun IndiaVardhman Textiles Lakshmi Cotsyn

Source: Industry Present Not present Note: Lakshmi Cotsyn’s presence in the spinning division is currently very minimal

Source: Industry

Lakshmi Cotsyn’s EBITDA margins have been consistently lower than that of peers

owing to the fact that it is not present throughout the value chain.

However, in June 2009 the company announced plans to set up 1, 00,000 spindles and

5,000 rotors to manufacture cotton yarn indigenously. Of the 1,00,000 spindles, it has already installed 10,000 spindles. It has also acquired 25,000 spindles on job work

Share of value added products expected to increase from 55% in 2009-10 to ~70% in 2011-12

Lakshmi Cotsyn is planning to backward integrate to manufacture cotton yarn

CRISIL Equities

Shri Lakshmi Cotsyn Limited

7

from the U.P. State Co-operative Federation in the latter half of 2009. These met ~20%

of its cotton yarn requirements. The rest is purchased from outside sources. The

management has indicated that the backward integration project is expected to be commissioned by the end of December 2011. Once commissioned, the company’s

margins are expected to improve due to savings in raw material costs resulting from in-

house manufacturing of cotton yarn instead of purchasing it externally.

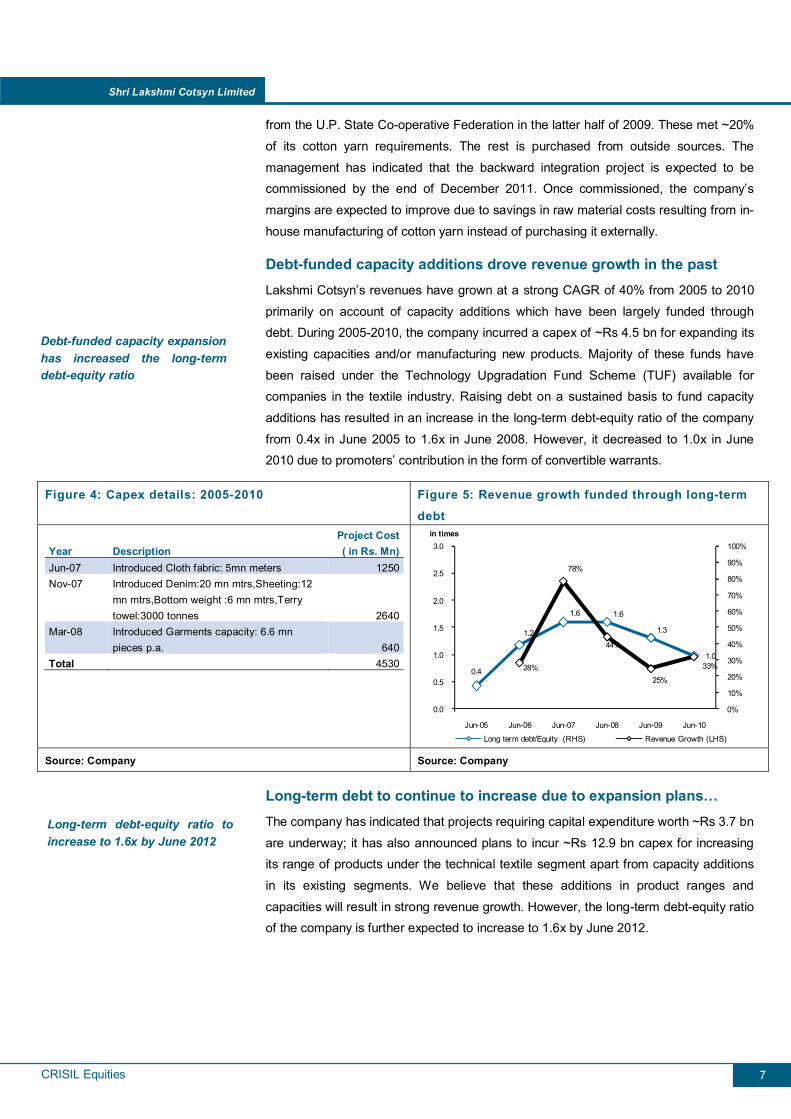

Debt-funded capacity additions drove revenue growth in the past Lakshmi Cotsyn’s revenues have grown at a strong CAGR of 40% from 2005 to 2010

primarily on account of capacity additions which have been largely funded through debt. During 2005-2010, the company incurred a capex of ~Rs 4.5 bn for expanding its

existing capacities and/or manufacturing new products. Majority of these funds have

been raised under the Technology Upgradation Fund Scheme (TUF) available for companies in the textile industry. Raising debt on a sustained basis to fund capacity

additions has resulted in an increase in the long-term debt-equity ratio of the company

from 0.4x in June 2005 to 1.6x in June 2008. However, it decreased to 1.0x in June 2010 due to promoters’ contribution in the form of convertible warrants.

Figure 4: Capex details: 2005-2010 Figure 5: Revenue growth funded through long-term

debt

Year Description Project Cost( in Rs. Mn)

Jun-07 Introduced Cloth fabric: 5mn meters 1250Nov-07 Introduced Denim:20 mn mtrs,Sheeting:12

mn mtrs,Bottom weight :6 mn mtrs,Terry towel:3000 tonnes 2640

Mar-08 Introduced Garments capacity: 6.6 mn pieces p.a. 640

Total 4530 0.4

1.2

1.6 1.6

1.3

1.028%

78%

44%

25%

33%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Jun-05 Jun-06 Jun-07 Jun-08 Jun-09 Jun-10

in times

Long term debt/Equity (RHS) Revenue Growth (LHS)

Source: Company Source: Company

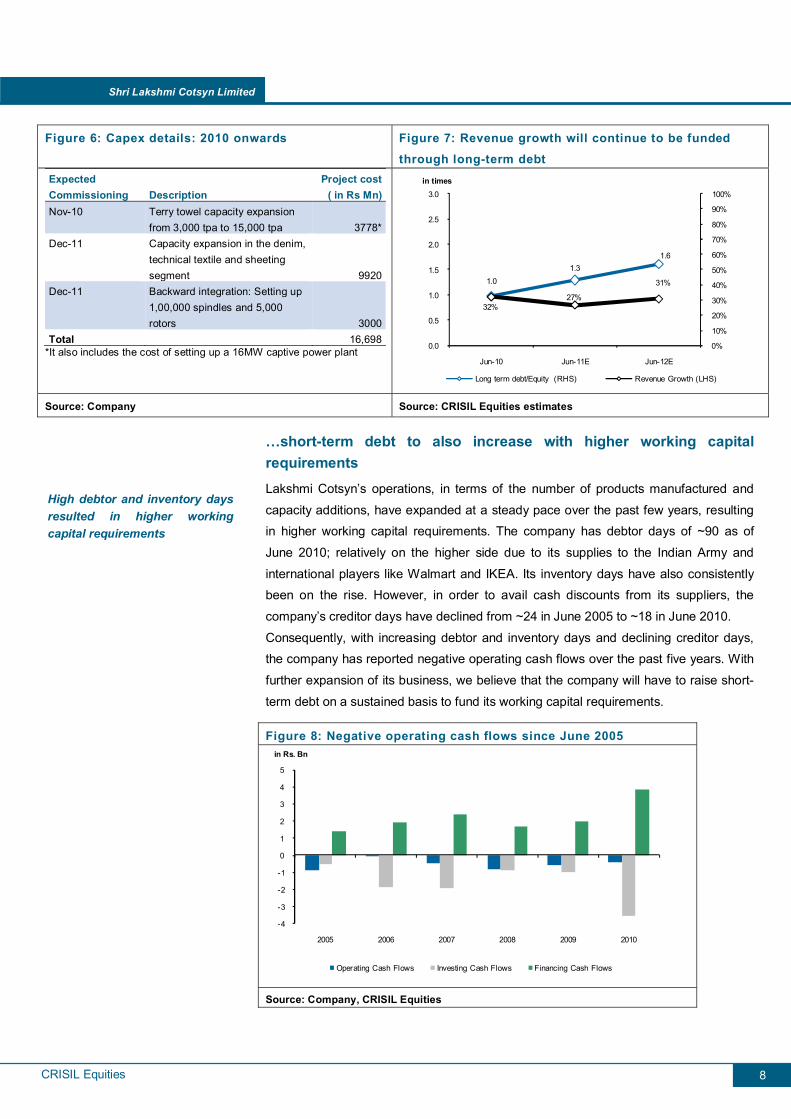

Long-term debt to continue to increase due to expansion plans… The company has indicated that projects requiring capital expenditure worth ~Rs 3.7 bn

are underway; it has also announced plans to incur ~Rs 12.9 bn capex for increasing its range of products under the technical textile segment apart from capacity additions

in its existing segments. We believe that these additions in product ranges and

capacities will result in strong revenue growth. However, the long-term debt-equity ratio of the company is further expected to increase to 1.6x by June 2012.

Debt-funded capacity expansion has increased the long-term debt-equity ratio

Long-term debt-equity ratio to increase to 1.6x by June 2012

CRISIL Equities

Shri Lakshmi Cotsyn Limited

8

Figure 6: Capex details: 2010 onwards Figure 7: Revenue growth will continue to be funded

through long-term debt Expected Commissioning Description

Project cost( in Rs Mn)

Nov-10 Terry towel capacity expansion from 3,000 tpa to 15,000 tpa 3778*

Dec-11 Capacity expansion in the denim, technical textile and sheeting segment 9920

Dec-11 Backward integration: Setting up 1,00,000 spindles and 5,000 rotors 3000

Total 16,698*It also includes the cost of setting up a 16MW captive power plant

1.01.3

1.6

32%27%

31%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Jun-10 Jun-11E Jun-12E

in times

Long term debt/Equity (RHS) Revenue Growth (LHS)

Source: Company Source: CRISIL Equities estimates

…short-term debt to also increase with higher working capital requirements Lakshmi Cotsyn’s operations, in terms of the number of products manufactured and

capacity additions, have expanded at a steady pace over the past few years, resulting in higher working capital requirements. The company has debtor days of ~90 as of

June 2010; relatively on the higher side due to its supplies to the Indian Army and

international players like Walmart and IKEA. Its inventory days have also consistently been on the rise. However, in order to avail cash discounts from its suppliers, the

company’s creditor days have declined from ~24 in June 2005 to ~18 in June 2010.

Consequently, with increasing debtor and inventory days and declining creditor days, the company has reported negative operating cash flows over the past five years. With

further expansion of its business, we believe that the company will have to raise short-

term debt on a sustained basis to fund its working capital requirements.

Figure 8: Negative operating cash flows since June 2005

-4

-3

-2

-1

0

1

2

3

4

5

2005 2006 2007 2008 2009 2010

in Rs. Bn

Operating Cash Flows Investing Cash Flows Financing Cash Flows

Source: Company, CRISIL Equities

High debtor and inventory days resulted in higher working capital requirements

CRISIL Equities

Shri Lakshmi Cotsyn Limited

9

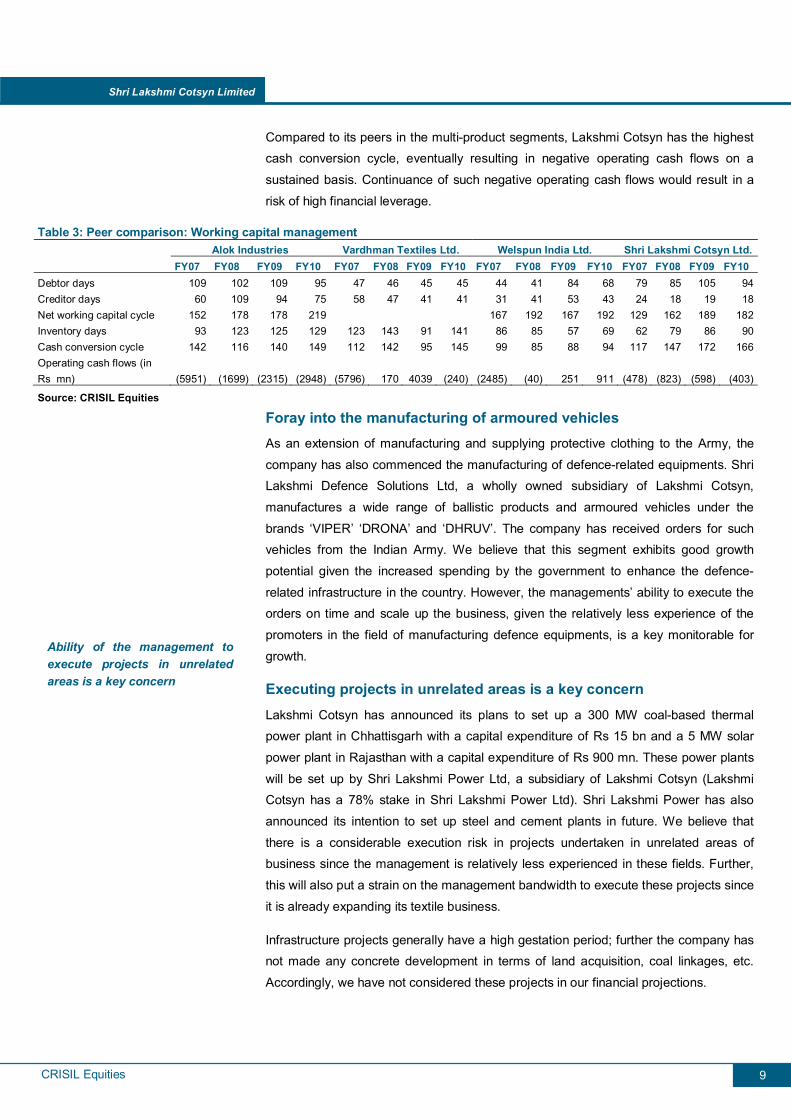

Compared to its peers in the multi-product segments, Lakshmi Cotsyn has the highest cash conversion cycle, eventually resulting in negative operating cash flows on a

sustained basis. Continuance of such negative operating cash flows would result in a

risk of high financial leverage. Table 3: Peer comparison: Working capital management Alok Industries Vardhman Textiles Ltd. Welspun India Ltd. Shri Lakshmi Cotsyn Ltd. FY07 FY08 FY09 FY10 FY07 FY08 FY09 FY10 FY07 FY08 FY09 FY10 FY07 FY08 FY09 FY10 Debtor days 109 102 109 95 47 46 45 45 44 41 84 68 79 85 105 94Creditor days 60 109 94 75 58 47 41 41 31 41 53 43 24 18 19 18Net working capital cycle 152 178 178 219 167 192 167 192 129 162 189 182Inventory days 93 123 125 129 123 143 91 141 86 85 57 69 62 79 86 90Cash conversion cycle 142 116 140 149 112 142 95 145 99 85 88 94 117 147 172 166Operating cash flows (in Rs mn) (5951) (1699) (2315) (2948) (5796) 170 4039 (240) (2485) (40) 251 911 (478) (823) (598) (403)

Source: CRISIL Equities Foray into the manufacturing of armoured vehicles As an extension of manufacturing and supplying protective clothing to the Army, the

company has also commenced the manufacturing of defence-related equipments. Shri Lakshmi Defence Solutions Ltd, a wholly owned subsidiary of Lakshmi Cotsyn,

manufactures a wide range of ballistic products and armoured vehicles under the

brands ‘VIPER’ ‘DRONA’ and ‘DHRUV’. The company has received orders for such vehicles from the Indian Army. We believe that this segment exhibits good growth

potential given the increased spending by the government to enhance the defence-

related infrastructure in the country. However, the managements’ ability to execute the orders on time and scale up the business, given the relatively less experience of the

promoters in the field of manufacturing defence equipments, is a key monitorable for

growth.

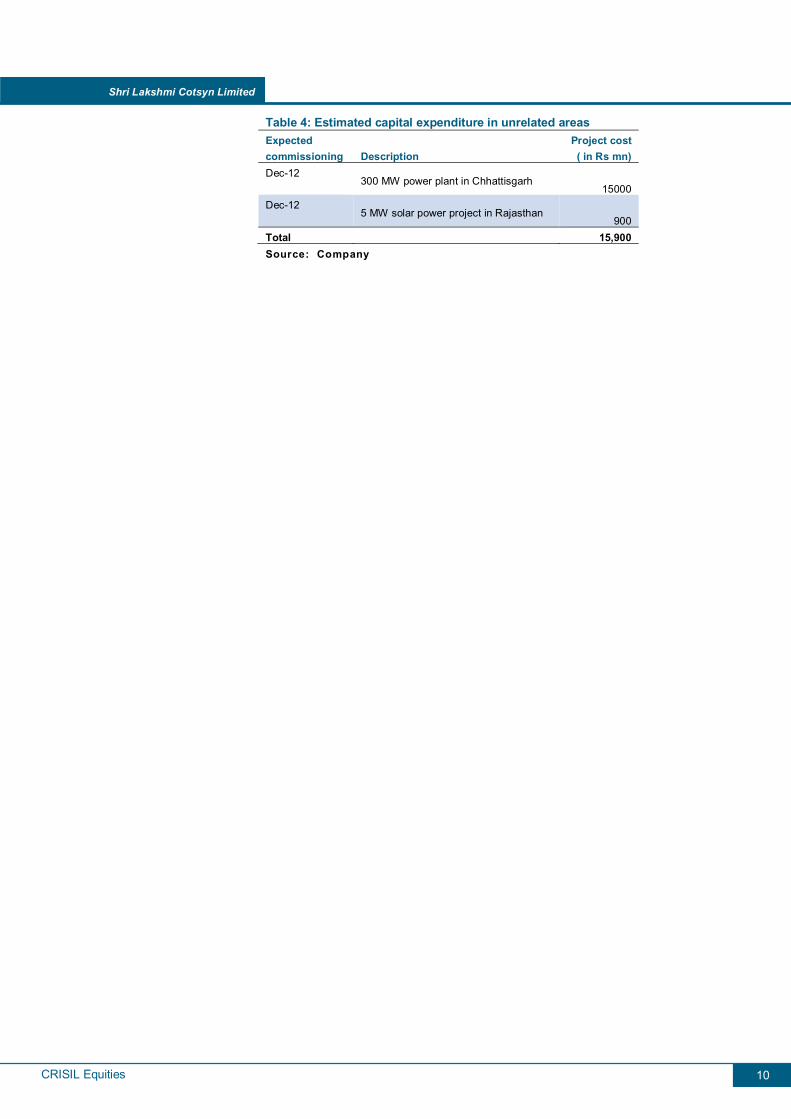

Executing projects in unrelated areas is a key concern Lakshmi Cotsyn has announced its plans to set up a 300 MW coal-based thermal power plant in Chhattisgarh with a capital expenditure of Rs 15 bn and a 5 MW solar

power plant in Rajasthan with a capital expenditure of Rs 900 mn. These power plants

will be set up by Shri Lakshmi Power Ltd, a subsidiary of Lakshmi Cotsyn (Lakshmi Cotsyn has a 78% stake in Shri Lakshmi Power Ltd). Shri Lakshmi Power has also

announced its intention to set up steel and cement plants in future. We believe that

there is a considerable execution risk in projects undertaken in unrelated areas of business since the management is relatively less experienced in these fields. Further,

this will also put a strain on the management bandwidth to execute these projects since

it is already expanding its textile business.

Infrastructure projects generally have a high gestation period; further the company has not made any concrete development in terms of land acquisition, coal linkages, etc.

Accordingly, we have not considered these projects in our financial projections.

Ability of the management to execute projects in unrelated areas is a key concern

CRISIL Equities

Shri Lakshmi Cotsyn Limited

10

Table 4: Estimated capital expenditure in unrelated areas Expected commissioning Description

Project cost ( in Rs mn)

Dec-12 300 MW power plant in Chhattisgarh

15000 Dec-12

5 MW solar power project in Rajasthan 900

Total 15,900 Source: Company

CRISIL Equities

Shri Lakshmi Cotsyn Limited

11

Key risks

Project execution risk in related and unrelated areas

The company has announced various capacity additions in the textile segment. It also has plans to venture into unrelated areas such as power, cement and steel. The

company is estimated to incur ~Rs 16.6 bn to fund the capacity additions in the textile

business and ~Rs 15.9 bn to fund the infrastructure-related projects in the medium term (excluding the funding for cement and steel businesses). We believe that it faces

a moderate execution risk in the textile-related projects since it has successfully

implemented such product introductions/additions in the past, albeit with a few delays (ranging from three months to a year). However, it faces a considerable execution risk

in its infrastructure-related projects due to the relatively less experience of the

promoters in managing such businesses.

Intense competition in the textile industry The company faces intense competition from various established and integrated players like Vardhman Textiles, and Alok Industries, as well as from a large number of

unorganised players.

Volatile raw material prices The company’s EBITDA margins are susceptible to volatile raw material prices, which

form ~90% of the total operating costs. The company is not entirely backward

integrated and procures majority of cotton yarn, its major raw material, from external sources. Given the company’s limited pricing flexibility due to its relatively small size

and the intensifying competition in the textile industry, any increase in the prices of

cotton could strain the company’s EBITDA margins.

Execution risks, increasing competition, volatility in raw material costs are the key risks

CRISIL Equities

Shri Lakshmi Cotsyn Limited

12

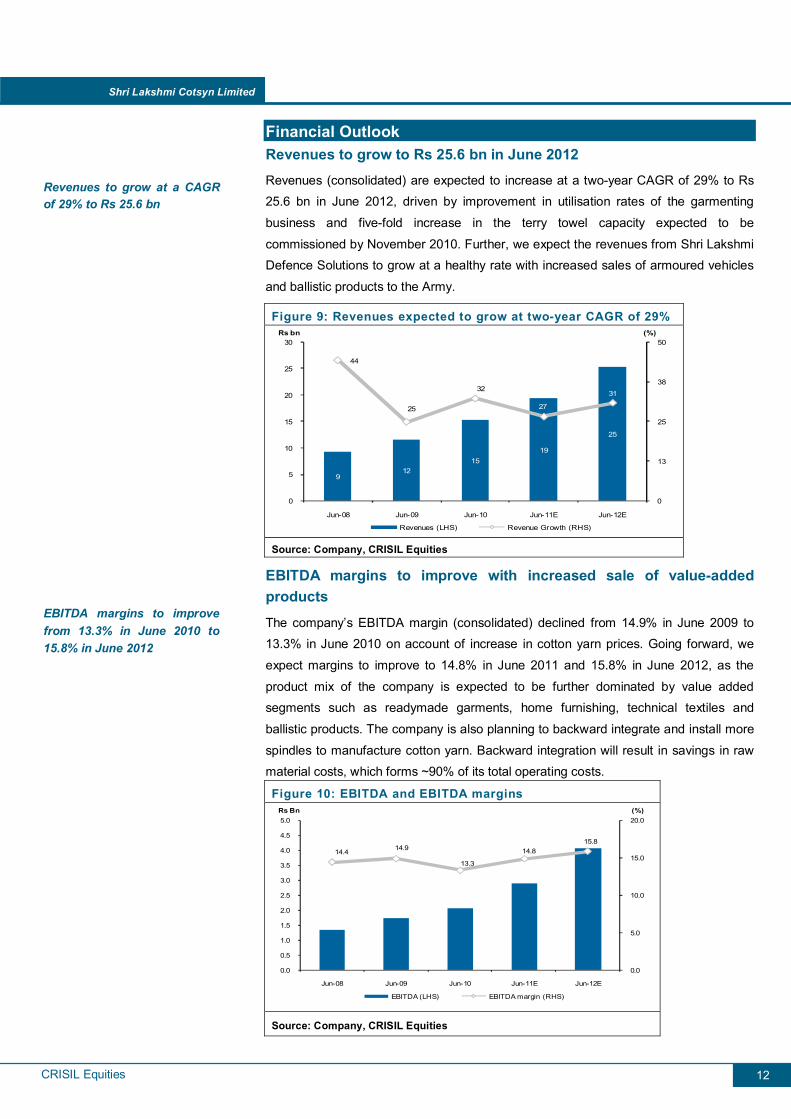

Financial Outlook Revenues to grow to Rs 25.6 bn in June 2012 Revenues (consolidated) are expected to increase at a two-year CAGR of 29% to Rs 25.6 bn in June 2012, driven by improvement in utilisation rates of the garmenting

business and five-fold increase in the terry towel capacity expected to be

commissioned by November 2010. Further, we expect the revenues from Shri Lakshmi Defence Solutions to grow at a healthy rate with increased sales of armoured vehicles

and ballistic products to the Army.

Figure 9: Revenues expected to grow at two-year CAGR of 29%

912

1519

25

44

25

32

27

31

0

13

25

38

50

0

5

10

15

20

25

30

Jun-08 Jun-09 Jun-10 Jun-11E Jun-12E

(%)Rs bn

Revenues (LHS) Revenue Growth (RHS)

Source: Company, CRISIL Equities

EBITDA margins to improve with increased sale of value-added products

The company’s EBITDA margin (consolidated) declined from 14.9% in June 2009 to 13.3% in June 2010 on account of increase in cotton yarn prices. Going forward, we

expect margins to improve to 14.8% in June 2011 and 15.8% in June 2012, as the

product mix of the company is expected to be further dominated by value added segments such as readymade garments, home furnishing, technical textiles and

ballistic products. The company is also planning to backward integrate and install more

spindles to manufacture cotton yarn. Backward integration will result in savings in raw material costs, which forms ~90% of its total operating costs.

Figure 10: EBITDA and EBITDA margins

14.4 14.9

13.3

14.815.8

0.0

5.0

10.0

15.0

20.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Jun-08 Jun-09 Jun-10 Jun-11E Jun-12E

(%)Rs Bn

EBITDA (LHS) EBITDA margin (RHS)

Source: Company, CRISIL Equities

Revenues to grow at a CAGR of 29% to Rs 25.6 bn

EBITDA margins to improve from 13.3% in June 2010 to 15.8% in June 2012

CRISIL Equities

Shri Lakshmi Cotsyn Limited

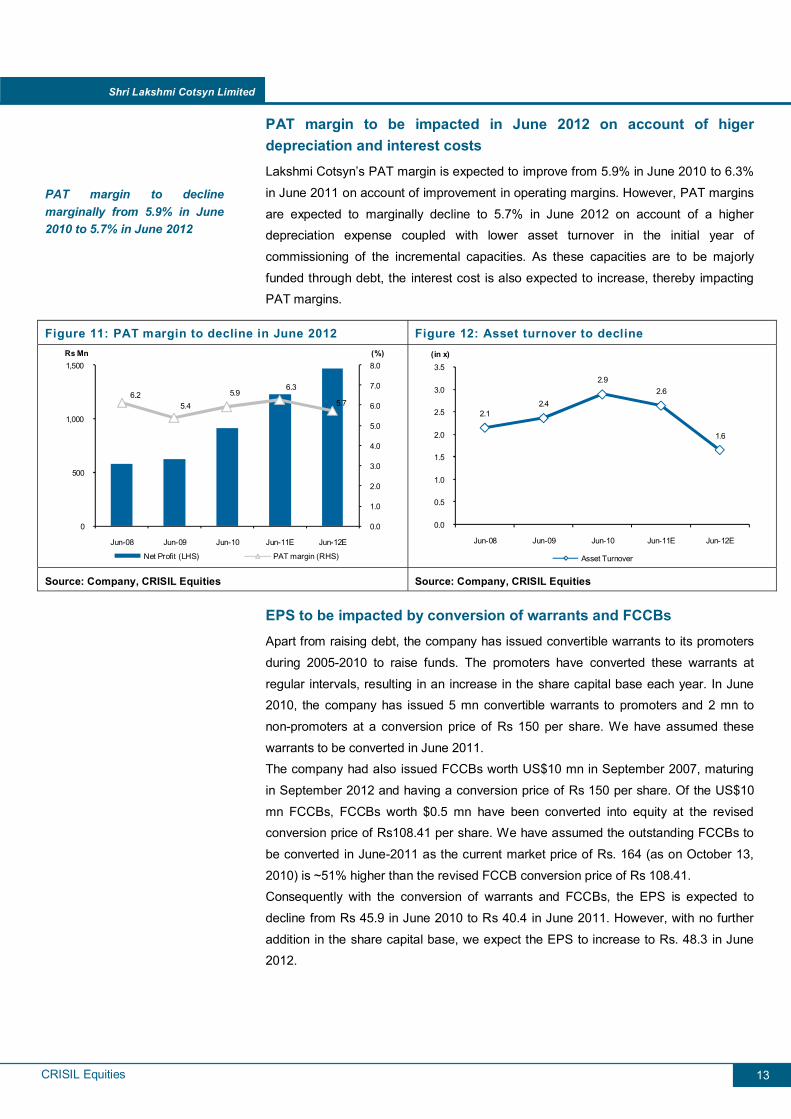

13

PAT margin to be impacted in June 2012 on account of higer depreciation and interest costs Lakshmi Cotsyn’s PAT margin is expected to improve from 5.9% in June 2010 to 6.3%

in June 2011 on account of improvement in operating margins. However, PAT margins

are expected to marginally decline to 5.7% in June 2012 on account of a higher depreciation expense coupled with lower asset turnover in the initial year of

commissioning of the incremental capacities. As these capacities are to be majorly

funded through debt, the interest cost is also expected to increase, thereby impacting PAT margins.

Figure 11: PAT margin to decline in June 2012 Figure 12: Asset turnover to decline

6.25.4

5.96.3

5.7

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

0

500

1,000

1,500

Jun-08 Jun-09 Jun-10 Jun-11E Jun-12E

(%)Rs Mn

Net Profit (LHS) PAT margin (RHS)

2.12.4

2.92.6

1.6

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Jun-08 Jun-09 Jun-10 Jun-11E Jun-12E

(in x)

Asset Turnover

Source: Company, CRISIL Equities Source: Company, CRISIL Equities

EPS to be impacted by conversion of warrants and FCCBs Apart from raising debt, the company has issued convertible warrants to its promoters

during 2005-2010 to raise funds. The promoters have converted these warrants at

regular intervals, resulting in an increase in the share capital base each year. In June 2010, the company has issued 5 mn convertible warrants to promoters and 2 mn to

non-promoters at a conversion price of Rs 150 per share. We have assumed these

warrants to be converted in June 2011. The company had also issued FCCBs worth US$10 mn in September 2007, maturing

in September 2012 and having a conversion price of Rs 150 per share. Of the US$10

mn FCCBs, FCCBs worth $0.5 mn have been converted into equity at the revised conversion price of Rs108.41 per share. We have assumed the outstanding FCCBs to

be converted in June-2011 as the current market price of Rs. 164 (as on October 13,

2010) is ~51% higher than the revised FCCB conversion price of Rs 108.41. Consequently with the conversion of warrants and FCCBs, the EPS is expected to

decline from Rs 45.9 in June 2010 to Rs 40.4 in June 2011. However, with no further

addition in the share capital base, we expect the EPS to increase to Rs. 48.3 in June 2012.

PAT margin to decline marginally from 5.9% in June 2010 to 5.7% in June 2012

CRISIL Equities

Shri Lakshmi Cotsyn Limited

14

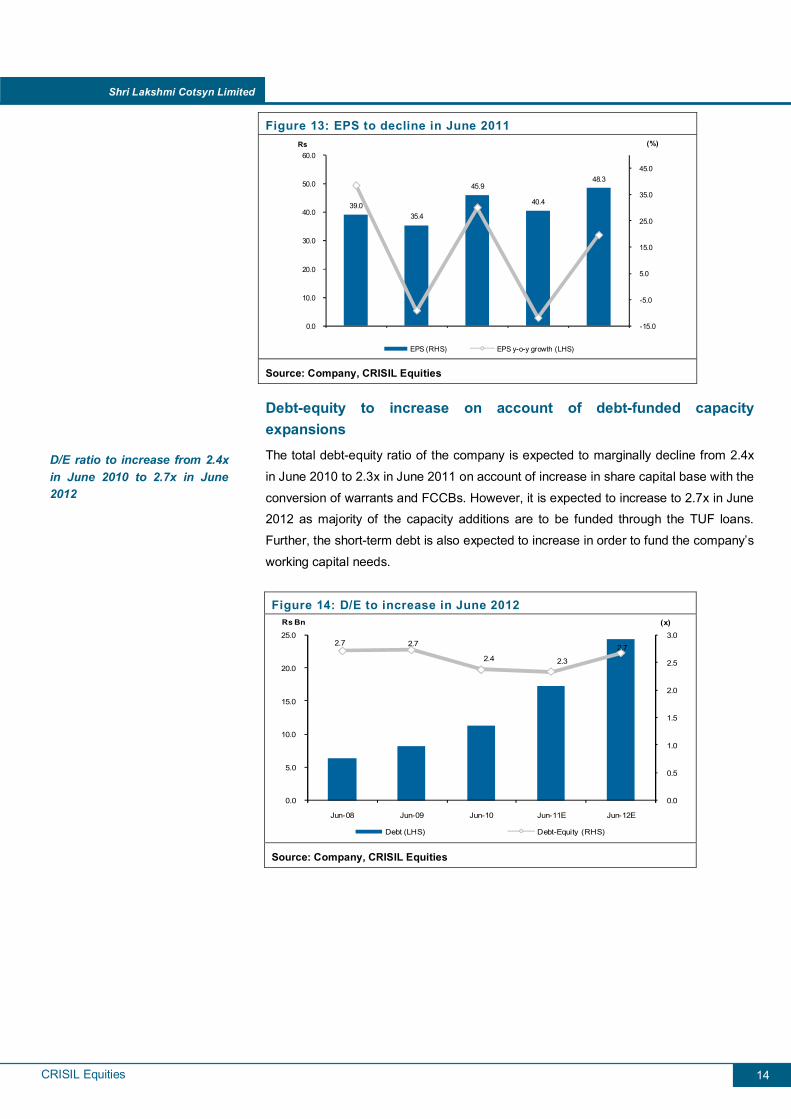

Figure 13: EPS to decline in June 2011

39.035.4

45.9

40.4

48.3

-15.0

-5.0

5.0

15.0

25.0

35.0

45.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0(%)Rs

EPS (RHS) EPS y-o-y growth (LHS)

Source: Company, CRISIL Equities

Debt-equity to increase on account of debt-funded capacity expansions The total debt-equity ratio of the company is expected to marginally decline from 2.4x

in June 2010 to 2.3x in June 2011 on account of increase in share capital base with the

conversion of warrants and FCCBs. However, it is expected to increase to 2.7x in June 2012 as majority of the capacity additions are to be funded through the TUF loans.

Further, the short-term debt is also expected to increase in order to fund the company’s

working capital needs.

Figure 14: D/E to increase in June 2012

2.7 2.7

2.4 2.3

2.7

0.0

0.5

1.0

1.5

2.0

2.5

3.0

0.0

5.0

10.0

15.0

20.0

25.0

Jun-08 Jun-09 Jun-10 Jun-11E Jun-12E

(x)Rs Bn

Debt (LHS) Debt-Equity (RHS)

Source: Company, CRISIL Equities

D/E ratio to increase from 2.4x in June 2010 to 2.7x in June 2012

CRISIL Equities

Shri Lakshmi Cotsyn Limited

15

Management Overview CRISIL's fundamental grading methodology includes a broad assessment of management quality, apart from other key factors such as industry and business

prospects, and financial performance.

Experienced but ambitious management Lakshmi Cotsyn has an experienced management headed by Mr M. P. Agarwal,

chairman and managing director, who has more than three decades of experience in

the textile industry. Mr Pawan Agarwal, Mr. M. P. Agarwal’s son, is the joint managing director. He has been looking after the company’s production, quality control and

marketing operations for the past 18 years.

The management is reasonably experienced and well versed with the dynamics of the

textile industry. However, it has ambitious plans of setting up a thermal coal based power and solar power plants, cement and steel plants through its subsidiary Shri

Lakshmi Power Ltd in the medium term. All these projects are in the initial stage of

registration with the concerned state government. Hence, we believe that without any concrete development in terms of land acquisitions (the company is in the process of

acquiring land), coal linkages, etc., the management’s target of completing these

projects in the next two-three years is ambitious.

Management’s strategy of diversifying into unrelated areas a concern The businesses in the infrastructure space do not add any synergies to the existing textile business and their execution remains a risk given the promoters’ relatively less

experience in these areas.

Largely a family-driven firm Based on our interactions and assesment, we believe that the company has a

reasonably good second line of management. The company is highly dependent on the

promoters for all important strategic decisions. We believe that the top management posts are likely to remain with the family members since Lakshmi Cotsyn is

fundamentally a promoter-driven company.

Management’s plans in the infrastructure space are ambitious

CRISIL Equities

Shri Lakshmi Cotsyn Limited

16

Corporate Governance

CRISIL’s fundamental grading methodology includes a broad assessment of corporate

governance as along with other key factors such as industry, business prospects, financial performance and management quality. In this context, CRISIL Equities

analyses the shareholding structure, board composition, typical board processes,

disclosure standards and related-party transactions. Any qualifications by regulators or auditors also serve as useful inputs while assessing a company’s corporate

governance.

Overall, the corporate governance at Lakshmi Cotsyn is average due to the low levels

of attendance of the independent directors at the board meetings.

Board composition Lakshmi Cotsyn’s board comprises 11 members, of whom six are independent

directors, which is in line with the requirements under Clause 49 of Sebi’s listing guidelines. Given the background of directors, we believe the board is fairly

experienced. However, they do not have the desired level of attendance in the board

meetings. For instance, in 2009, the company conducted 13 board meetings, of which the independent directors attended only three on an average. Low levels of attendance

indicate that the independent directors are not entirely involved in the decision-making

process of the company.

Board’s processes The company’s quality of disclosure can be considered good judged by the level of information and details furnished in the annual report, websites and other publicly

available data. The company has all the necessary committees – audit, remuneration

and investor grievance - in place to support corporate governance practices. The audit committee is chaired by an independent director, Mr R. K. Garg. The company has also

constituted a finance committee with the purpose of overseeing the day-to-day

business activities. The finance committee, which met 20 times during June 2009, is headed by the CMD, Mr M. P. Agarwal, and none of the independent directors are a

part of this committee.

Regulatory charges on the company The company has faced certain regulatory charges in the past. For instance, the

company failed to submit the corporate governance report to the Bombay Stock

Exchange (BSE) for the quarter ended September 2007. Further, in 2006, Sebi imposed a penalty on the promoter family for acquiring 6.8% shares through the

preferential allotment route (thereby increasing their stake to 31.5% in Lakshmi Cotsyn)

without making any public announcement. Given this history of non-compliance of regulatory requirements and the low attendance of independent directors, we are of the

opinion that the corporate governance practices at Lakshmi Cotsyn are average.

Corporate governance practices at Lakshmi Cotsyn are average

CRISIL Equities

Shri Lakshmi Cotsyn Limited

17

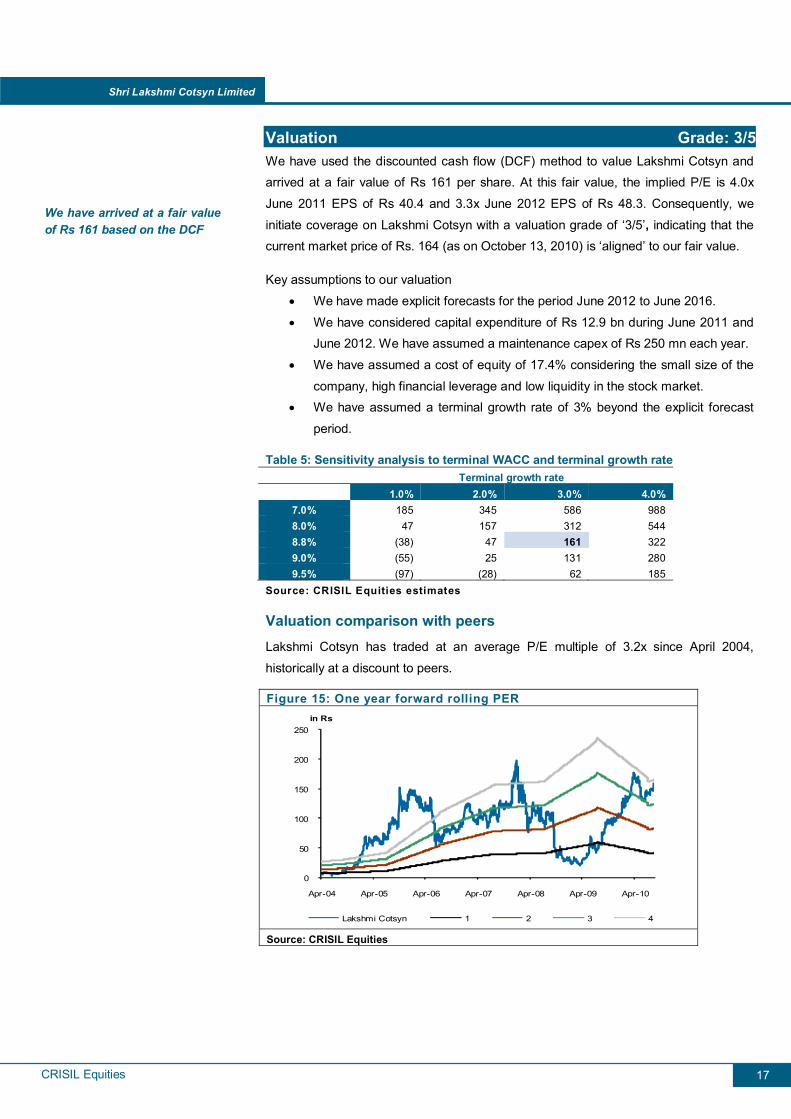

Valuation Grade: 3/5 We have used the discounted cash flow (DCF) method to value Lakshmi Cotsyn and arrived at a fair value of Rs 161 per share. At this fair value, the implied P/E is 4.0x

June 2011 EPS of Rs 40.4 and 3.3x June 2012 EPS of Rs 48.3. Consequently, we

initiate coverage on Lakshmi Cotsyn with a valuation grade of ‘3/5’, indicating that the current market price of Rs. 164 (as on October 13, 2010) is ‘aligned’ to our fair value.

Key assumptions to our valuation

• We have made explicit forecasts for the period June 2012 to June 2016.

• We have considered capital expenditure of Rs 12.9 bn during June 2011 and June 2012. We have assumed a maintenance capex of Rs 250 mn each year.

• We have assumed a cost of equity of 17.4% considering the small size of the

company, high financial leverage and low liquidity in the stock market. • We have assumed a terminal growth rate of 3% beyond the explicit forecast

period.

Table 5: Sensitivity analysis to terminal WACC and terminal growth rate Terminal growth rate

1.0% 2.0% 3.0% 4.0% 7.0% 185 345 586 988 8.0% 47 157 312 544 8.8% (38) 47 161 322 9.0% (55) 25 131 280 9.5% (97) (28) 62 185

Source: CRISIL Equities estimates

Valuation comparison with peers Lakshmi Cotsyn has traded at an average P/E multiple of 3.2x since April 2004,

historically at a discount to peers.

Figure 15: One year forward rolling PER

0

50

100

150

200

250

Apr-04 Apr-05 Apr-06 Apr-07 Apr-08 Apr-09 Apr-10

in Rs

Lakshmi Cotsyn 1 2 3 4

Source: CRISIL Equities

We have arrived at a fair value of Rs 161 based on the DCF

CRISIL Equities

Shri Lakshmi Cotsyn Limited

18

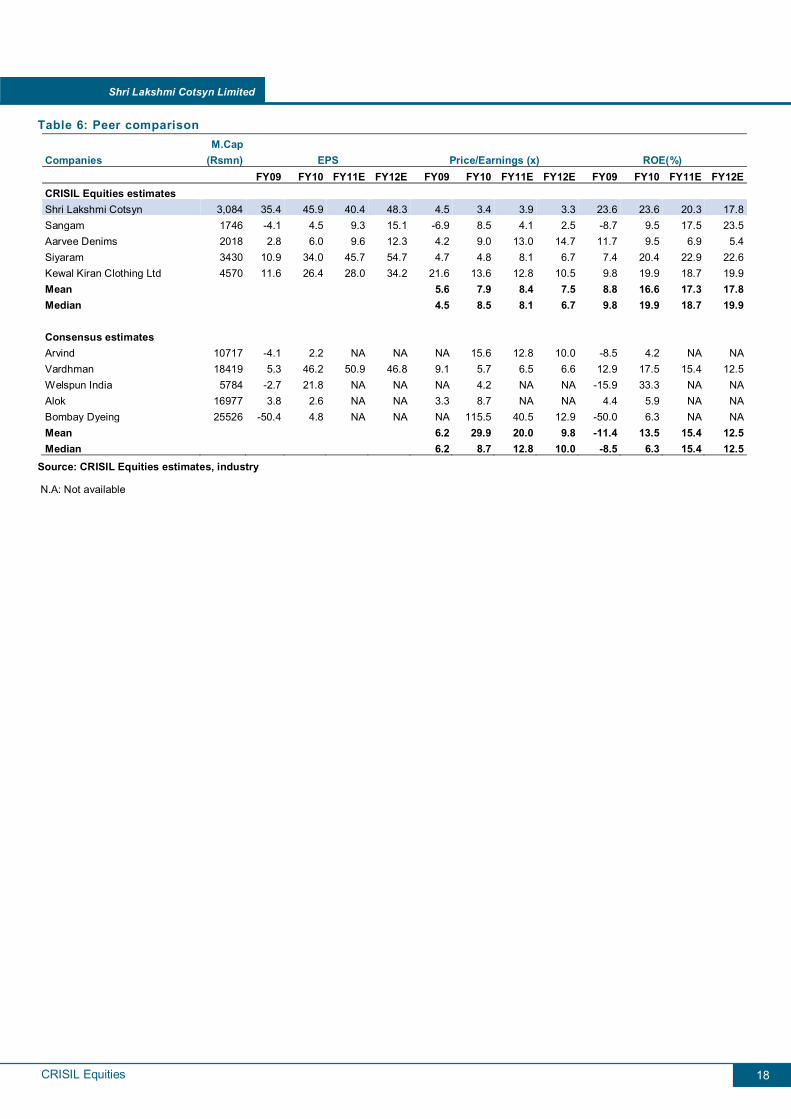

Table 6: Peer comparison

Companies M.Cap

(Rsmn) EPS Price/Earnings (x) ROE(%) FY09 FY10 FY11E FY12E FY09 FY10 FY11E FY12E FY09 FY10 FY11E FY12E

CRISIL Equities estimates Shri Lakshmi Cotsyn 3,084 35.4 45.9 40.4 48.3 4.5 3.4 3.9 3.3 23.6 23.6 20.3 17.8Sangam 1746 -4.1 4.5 9.3 15.1 -6.9 8.5 4.1 2.5 -8.7 9.5 17.5 23.5Aarvee Denims 2018 2.8 6.0 9.6 12.3 4.2 9.0 13.0 14.7 11.7 9.5 6.9 5.4Siyaram 3430 10.9 34.0 45.7 54.7 4.7 4.8 8.1 6.7 7.4 20.4 22.9 22.6Kewal Kiran Clothing Ltd 4570 11.6 26.4 28.0 34.2 21.6 13.6 12.8 10.5 9.8 19.9 18.7 19.9Mean 5.6 7.9 8.4 7.5 8.8 16.6 17.3 17.8Median 4.5 8.5 8.1 6.7 9.8 19.9 18.7 19.9

Consensus estimates Arvind 10717 -4.1 2.2 NA NA NA 15.6 12.8 10.0 -8.5 4.2 NA NAVardhman 18419 5.3 46.2 50.9 46.8 9.1 5.7 6.5 6.6 12.9 17.5 15.4 12.5Welspun India 5784 -2.7 21.8 NA NA NA 4.2 NA NA -15.9 33.3 NA NAAlok 16977 3.8 2.6 NA NA 3.3 8.7 NA NA 4.4 5.9 NA NABombay Dyeing 25526 -50.4 4.8 NA NA NA 115.5 40.5 12.9 -50.0 6.3 NA NAMean 6.2 29.9 20.0 9.8 -11.4 13.5 15.4 12.5Median 6.2 8.7 12.8 10.0 -8.5 6.3 15.4 12.5

Source: CRISIL Equities estimates, industry

N.A: Not available

CRISIL Equities

Shri Lakshmi Cotsyn Limited

19

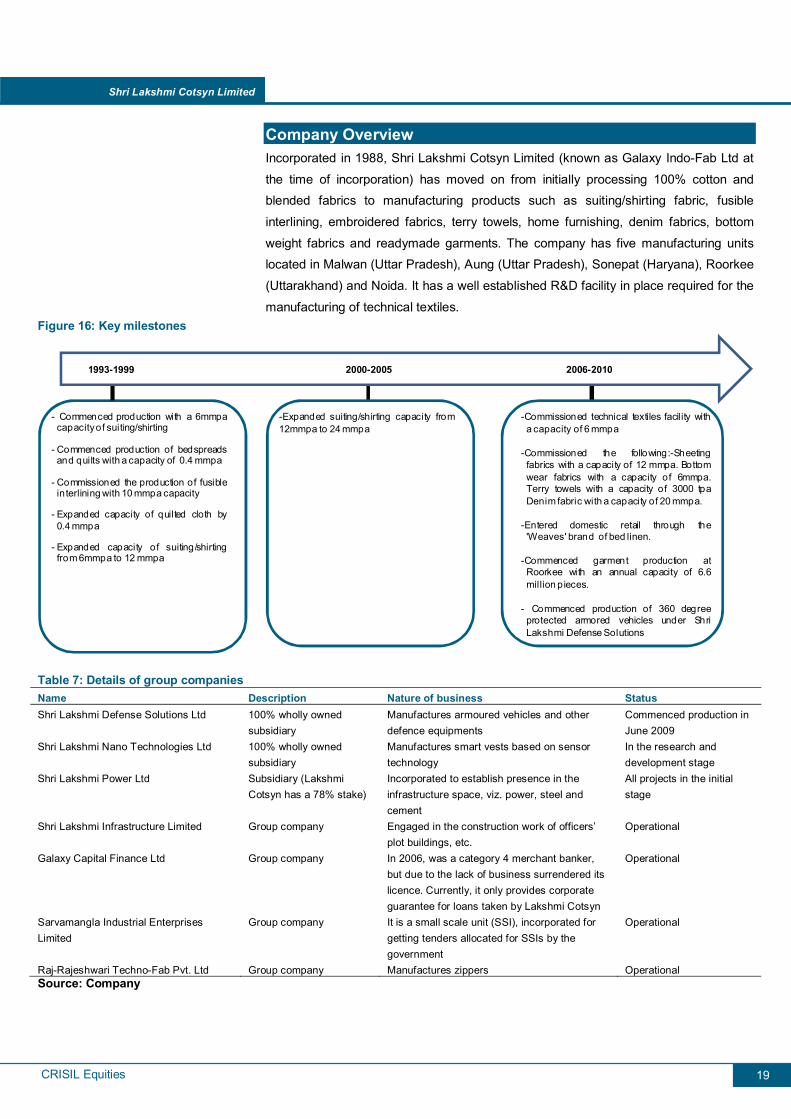

Company Overview Incorporated in 1988, Shri Lakshmi Cotsyn Limited (known as Galaxy Indo-Fab Ltd at

the time of incorporation) has moved on from initially processing 100% cotton and blended fabrics to manufacturing products such as suiting/shirting fabric, fusible

interlining, embroidered fabrics, terry towels, home furnishing, denim fabrics, bottom

weight fabrics and readymade garments. The company has five manufacturing units located in Malwan (Uttar Pradesh), Aung (Uttar Pradesh), Sonepat (Haryana), Roorkee

(Uttarakhand) and Noida. It has a well established R&D facility in place required for the

manufacturing of technical textiles. Figure 16: Key milestones

1993-1999

- Commenced production with a 6mmpacapacityof suiting/shirting

- Commenced production of bedspreadsand quilts with a capacity of 0.4 mmpa

- Commissioned the production of fusibleinterlining with 10 mmpa capacity

- Expanded capacity of quilted cloth by0.4 mmpa

- Expanded capacity of suiting/shirtingfrom 6mmpa to 12 mmpa

2000-2005

-Expanded suiting/shirting capacity from12mmpa to 24 mmpa

-Commissioned technical textiles facility witha capacity of 6 mmpa

-Commissioned the following:-Sheetingfabrics with a capacity of 12 mmpa. Bottomwear fabrics with a capacity of 6mmpa.Terry towels with a capacity of 3000 tpaDenim fabric with a capacity of 20 mmpa.

-Entered domestic retail through the'Weaves' brand of bed linen.

-Commenced garment production atRoorkee with an annual capacity of 6.6million pieces.

- Commenced production of 360 degreeprotected armored vehicles under ShriLakshmi Defense Solutions

2006-2010

Table 7: Details of group companies Name Description Nature of business Status Shri Lakshmi Defense Solutions Ltd 100% wholly owned

subsidiary Manufactures armoured vehicles and other defence equipments

Commenced production in June 2009

Shri Lakshmi Nano Technologies Ltd 100% wholly owned subsidiary

Manufactures smart vests based on sensor technology

In the research and development stage

Shri Lakshmi Power Ltd Subsidiary (Lakshmi Cotsyn has a 78% stake)

Incorporated to establish presence in the infrastructure space, viz. power, steel and cement

All projects in the initial stage

Shri Lakshmi Infrastructure Limited Group company Engaged in the construction work of officers’ plot buildings, etc.

Operational

Galaxy Capital Finance Ltd Group company In 2006, was a category 4 merchant banker, but due to the lack of business surrendered its licence. Currently, it only provides corporate guarantee for loans taken by Lakshmi Cotsyn

Operational

Sarvamangla Industrial Enterprises Limited

Group company It is a small scale unit (SSI), incorporated for getting tenders allocated for SSIs by the government

Operational

Raj-Rajeshwari Techno-Fab Pvt. Ltd Group company Manufactures zippers Operational Source: Company

CRISIL Equities

Shri Lakshmi Cotsyn Limited

20

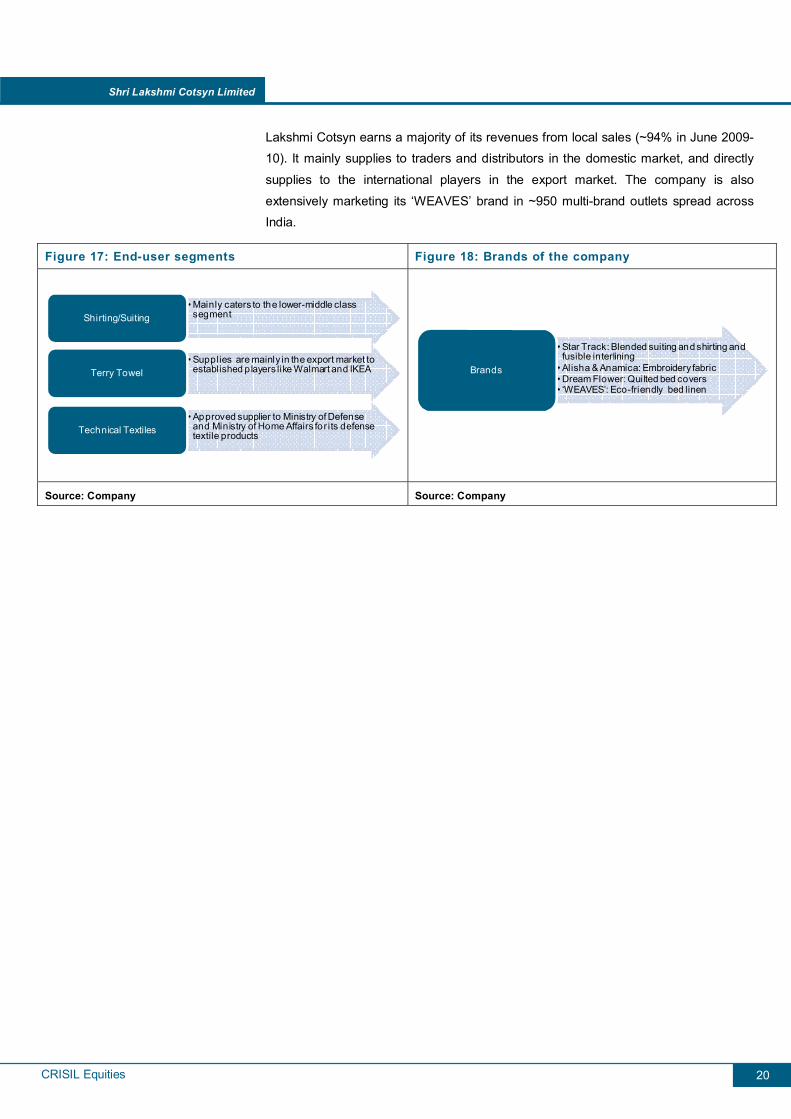

Lakshmi Cotsyn earns a majority of its revenues from local sales (~94% in June 2009-10). It mainly supplies to traders and distributors in the domestic market, and directly

supplies to the international players in the export market. The company is also

extensively marketing its ‘WEAVES’ brand in ~950 multi-brand outlets spread across India.

Figure 17: End-user segments Figure 18: Brands of the company

• Mainly caters to the lower-middle class segment Shirting/Suiting

• Supplies are mainly in the export market to established players like Walmart and IKEATerry Towel

• Approved supplier to Ministry of Defense and Ministry of Home Affairs for its defense textile products Technical Textiles

• Star Track: Blended suiting and shirting and fusible interlining

• Alisha & Anamica: Embroidery fabric• Dream Flower: Quilted bed covers• ‘WEAVES’: Eco-friendly bed linen

Brands

Source: Company Source: Company

CRISIL Equities

Shri Lakshmi Cotsyn Limited

21

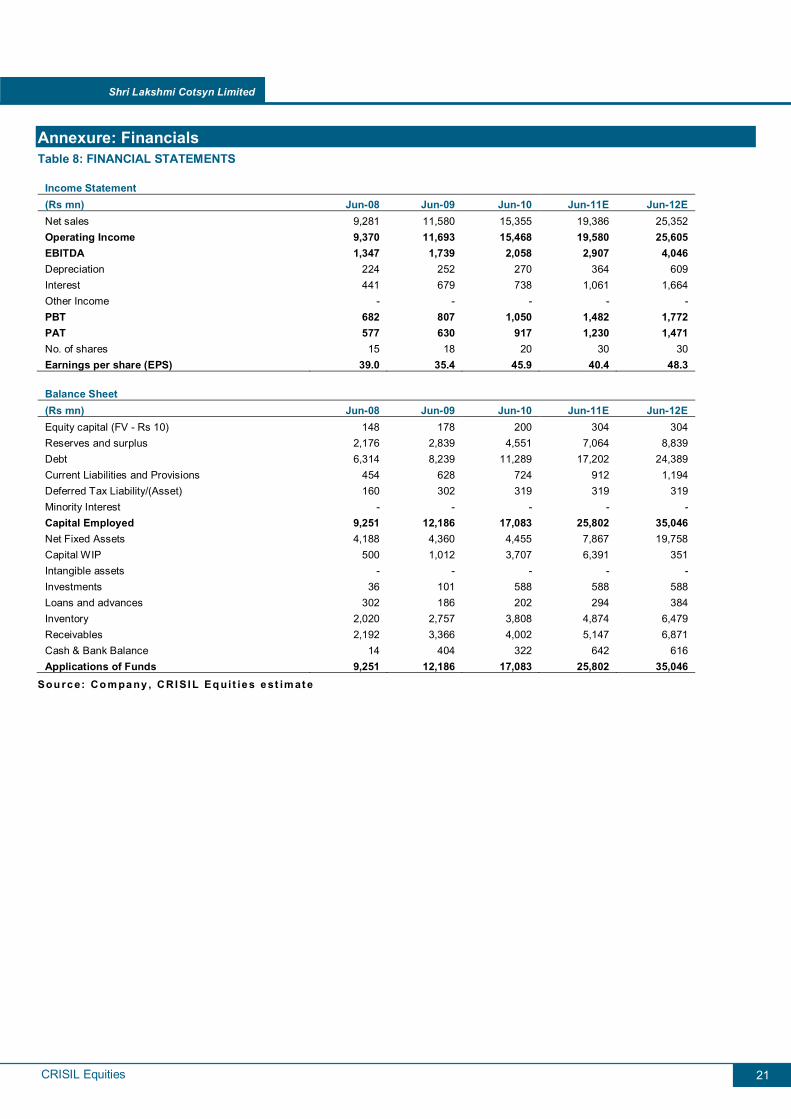

Annexure: Financials Table 8: FINANCIAL STATEMENTS

Income Statement (Rs mn) Jun-08 Jun-09 Jun-10 Jun-11E Jun-12E Net sales 9,281 11,580 15,355 19,386 25,352 Operating Income 9,370 11,693 15,468 19,580 25,605 EBITDA 1,347 1,739 2,058 2,907 4,046 Depreciation 224 252 270 364 609 Interest 441 679 738 1,061 1,664 Other Income - - - - - PBT 682 807 1,050 1,482 1,772 PAT 577 630 917 1,230 1,471 No. of shares 15 18 20 30 30 Earnings per share (EPS) 39.0 35.4 45.9 40.4 48.3

Balance Sheet (Rs mn) Jun-08 Jun-09 Jun-10 Jun-11E Jun-12E Equity capital (FV - Rs 10) 148 178 200 304 304 Reserves and surplus 2,176 2,839 4,551 7,064 8,839 Debt 6,314 8,239 11,289 17,202 24,389 Current Liabilities and Provisions 454 628 724 912 1,194 Deferred Tax Liability/(Asset) 160 302 319 319 319 Minority Interest - - - - - Capital Employed 9,251 12,186 17,083 25,802 35,046 Net Fixed Assets 4,188 4,360 4,455 7,867 19,758 Capital WIP 500 1,012 3,707 6,391 351 Intangible assets - - - - - Investments 36 101 588 588 588 Loans and advances 302 186 202 294 384 Inventory 2,020 2,757 3,808 4,874 6,479 Receivables 2,192 3,366 4,002 5,147 6,871 Cash & Bank Balance 14 404 322 642 616 Applications of Funds 9,251 12,186 17,083 25,802 35,046

Sou rc e: Co m pa ny , CRI SI L Eq ui t ie s e st im at e

CRISIL Equities

Shri Lakshmi Cotsyn Limited

22

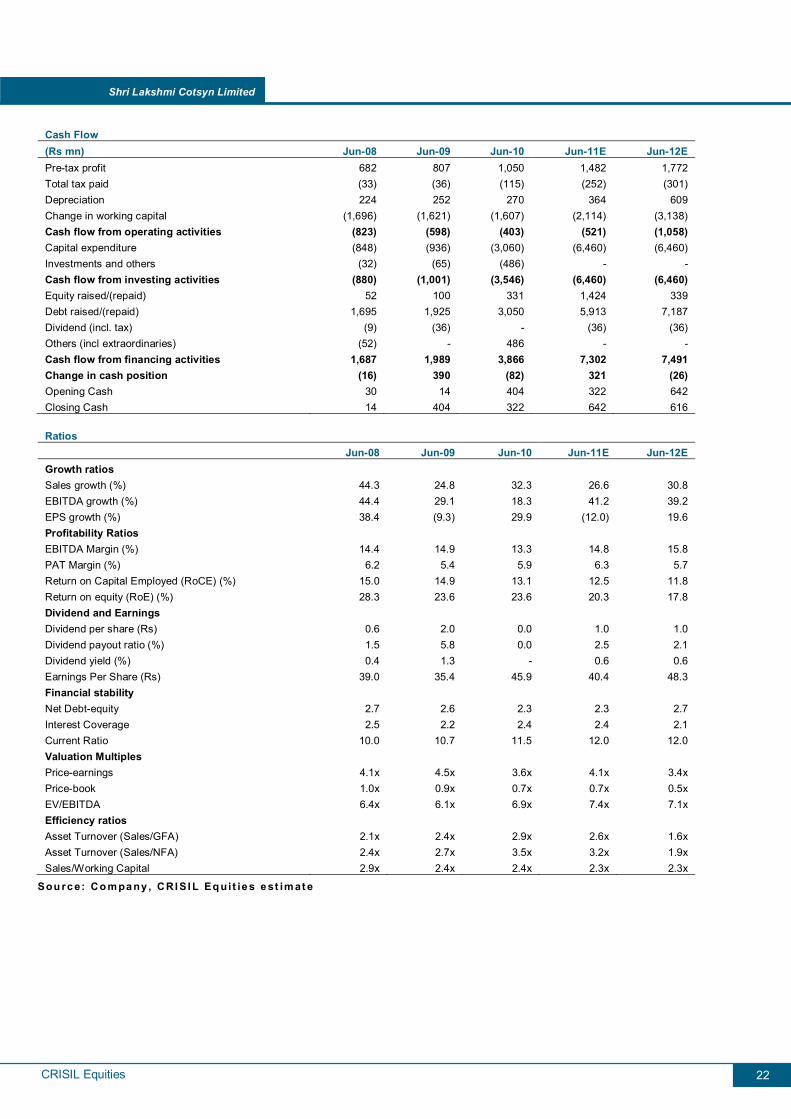

Cash Flow (Rs mn) Jun-08 Jun-09 Jun-10 Jun-11E Jun-12E Pre-tax profit 682 807 1,050 1,482 1,772 Total tax paid (33) (36) (115) (252) (301) Depreciation 224 252 270 364 609 Change in working capital (1,696) (1,621) (1,607) (2,114) (3,138) Cash flow from operating activities (823) (598) (403) (521) (1,058) Capital expenditure (848) (936) (3,060) (6,460) (6,460) Investments and others (32) (65) (486) - - Cash flow from investing activities (880) (1,001) (3,546) (6,460) (6,460) Equity raised/(repaid) 52 100 331 1,424 339 Debt raised/(repaid) 1,695 1,925 3,050 5,913 7,187 Dividend (incl. tax) (9) (36) - (36) (36) Others (incl extraordinaries) (52) - 486 - - Cash flow from financing activities 1,687 1,989 3,866 7,302 7,491 Change in cash position (16) 390 (82) 321 (26) Opening Cash 30 14 404 322 642 Closing Cash 14 404 322 642 616

Ratios Jun-08 Jun-09 Jun-10 Jun-11E Jun-12E Growth ratios Sales growth (%) 44.3 24.8 32.3 26.6 30.8 EBITDA growth (%) 44.4 29.1 18.3 41.2 39.2 EPS growth (%) 38.4 (9.3) 29.9 (12.0) 19.6 Profitability Ratios EBITDA Margin (%) 14.4 14.9 13.3 14.8 15.8 PAT Margin (%) 6.2 5.4 5.9 6.3 5.7 Return on Capital Employed (RoCE) (%) 15.0 14.9 13.1 12.5 11.8 Return on equity (RoE) (%) 28.3 23.6 23.6 20.3 17.8 Dividend and Earnings Dividend per share (Rs) 0.6 2.0 0.0 1.0 1.0 Dividend payout ratio (%) 1.5 5.8 0.0 2.5 2.1 Dividend yield (%) 0.4 1.3 - 0.6 0.6 Earnings Per Share (Rs) 39.0 35.4 45.9 40.4 48.3 Financial stability Net Debt-equity 2.7 2.6 2.3 2.3 2.7 Interest Coverage 2.5 2.2 2.4 2.4 2.1 Current Ratio 10.0 10.7 11.5 12.0 12.0 Valuation Multiples Price-earnings 4.1x 4.5x 3.6x 4.1x 3.4x Price-book 1.0x 0.9x 0.7x 0.7x 0.5x EV/EBITDA 6.4x 6.1x 6.9x 7.4x 7.1x Efficiency ratios Asset Turnover (Sales/GFA) 2.1x 2.4x 2.9x 2.6x 1.6xAsset Turnover (Sales/NFA) 2.4x 2.7x 3.5x 3.2x 1.9xSales/Working Capital 2.9x 2.4x 2.4x 2.3x 2.3x

Sou rc e: Co m pa ny , CRI SI L Eq ui t ie s e st im at e

CRISIL Equities

Shri Lakshmi Cotsyn Limited

23

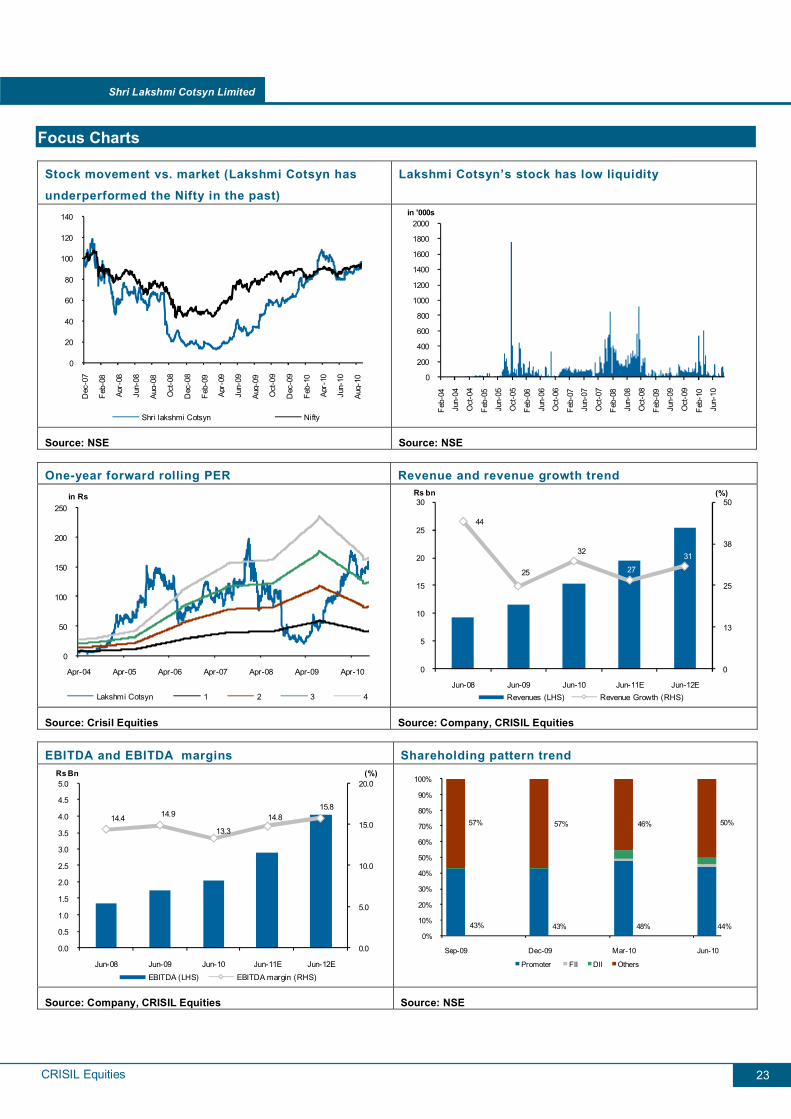

Focus Charts

Stock movement vs. market (Lakshmi Cotsyn has

underperformed the Nifty in the past)

Lakshmi Cotsyn’s stock has low liquidity

0

20

40

60

80

100

120

140

Dec

-07

Feb-

08

A pr-

08

Jun-

08

Aug-

08

Oct

-08

Dec

-08

Feb-

09

A pr-

09

Jun-

09

Aug-

09

Oct

-09

Dec

-09

Feb-

10

A pr-

10

Jun-

10

Aug-

10

Shri lakshmi Cotsyn Nifty

0

200

400

600

800

1000

1200

1400

1600

1800

2000

Feb-

04

Jun-

04

Oct

-04

Feb-

05

Jun-

05

Oct

-05

Feb-

06

Jun-

06

Oct

-06

Feb-

07

Jun-

07

Oct

-07

Feb-

08

Jun-

08

Oct

-08

Feb-

09

Jun-

09

Oct

-09

Feb-

10

Jun-

10

in '000s

Source: NSE Source: NSE

One-year forward rolling PER Revenue and revenue growth trend

0

50

100

150

200

250

Apr-04 Apr-05 Apr-06 Apr-07 Apr-08 Apr-09 Apr-10

in Rs

Lakshmi Cotsyn 1 2 3 4

44

25

32

27

31

0

13

25

38

50

0

5

10

15

20

25

30

Jun-08 Jun-09 Jun-10 Jun-11E Jun-12E

(%)Rs bn

Revenues (LHS) Revenue Growth (RHS)

Source: Crisil Equities Source: Company, CRISIL Equities

EBITDA and EBITDA margins Shareholding pattern trend

14.4 14.9

13.3

14.815.8

0.0

5.0

10.0

15.0

20.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Jun-08 Jun-09 Jun-10 Jun-11E Jun-12E

(%)Rs Bn

EBITDA (LHS) EBITDA margin (RHS)

43% 43% 48% 44%

57% 57% 46% 50%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Sep-09 Dec-09 Mar-10 Jun-10

Promoter FII DII Others

Source: Company, CRISIL Equities Source: NSE

This page is intentionally left blank

CRISIL Independent Equity Research Team Mukesh Agarwal [email protected] +91 (22) 3342 3035 Director Tarun Bhatia [email protected] +91 (22) 3342 3226 Director- Capital Markets Analytical Contacts Chetan Majithia [email protected] +91 (22) 3342 4148 Sudhir Nair [email protected] +91 (22) 3342 3526 Sector Contacts Nagarajan Narasimhan [email protected] +91 (22) 3342 3536 Ajay D'Souza [email protected] +91 (22) 3342 3567 Manoj Mohta [email protected] +91 (22) 3342 3554 Sachin Mathur [email protected] +91 (22) 3342 3541 Sridhar C [email protected] +91 (22) 3342 3546 Business Development Contacts Vinaya Dongre [email protected] +91 99 202 25174 Sagar Sawarkar [email protected] +91 98 216 38322 CRISIL’s Equity Offerings The Equity Group at CRISIL Research provides a wide range of services including:

Independent Equity Research IPO Grading White Labelled Research Valuation on companies for use of Institutional Investors, Asset Managers, Corporate

Other Services by the Research group include

CRISINFAC Industry research on over 60 industries and Economic Analysis Customised Research on Market sizing, Demand modelling and Entry strategies Customised research content for Information Memorandum and Offer documents

25

For further details or more information, please contact: Client Servicing CRISIL Research CRISIL House Central Avenue Hiranandani Business Park Powai, Mumbai - 400 076, India. Phone +91 (22) 3342 3561/ 62 Fax +91 (22) 3342 3501 E-mail: [email protected] E-mail: [email protected] www.ier.co.in

About CRISIL Limited CRISIL is India's leading Ratings, Research, Risk and Policy Advisory Company About CRISIL Research CRISIL Research is India's largest independent, integrated research house. We leverage our unique, integrated research platform and capabilities spanning the entire economy-industry-company spectrum to deliver superior perspectives and insights to over 600 domestic and global clients, through a range of subscription products and customised solutions.

Mumbai CRISIL House Central Avenue Hiranandani Business Park Powai, Mumbai - 400 076, India. Phone +91 (22) 3342 8026/29/35 Fax +91 (22) 3342 8088

New Delhi The Mira G-1 (FF),1st Floor, Plot No. 1&2 Ishwar Nagar, Near Okhla Crossing New Delhi -110 065, India. Phone +91 (11) 4250 5100, 2693 0117-21 Fax +91 (11) 2684 2212/ 13

Bengaluru W-101, Sunrise Chambers 22, Ulsoor Road Bengaluru - 560 042, India. Phone +91 (80) 4117 0622 Fax +91 (80) 2559 4801

Kolkata ‘Horizon’, Block ‘B’, 4th floor 57 Chowringhee Road Kolkata - 700 071, India. Phone +91 (33) 2283 0595 Fax +91 (33) 2283 0597

Chennai Mezzanine Floor, Thappar House 43 / 44, Montieth Road Egmore Chennai - 600 008, India. Phone +91 (44) 2854 6205/06, 2854 6093 Fax +91 (44) 2854 7531

Recommended