GFNORTE 2Q09

July, 2009.

1. 2Q09 Results

2. Asset Quality

3. Capital Management

4. Subsidiaries

5. Final Remarks

Index

3

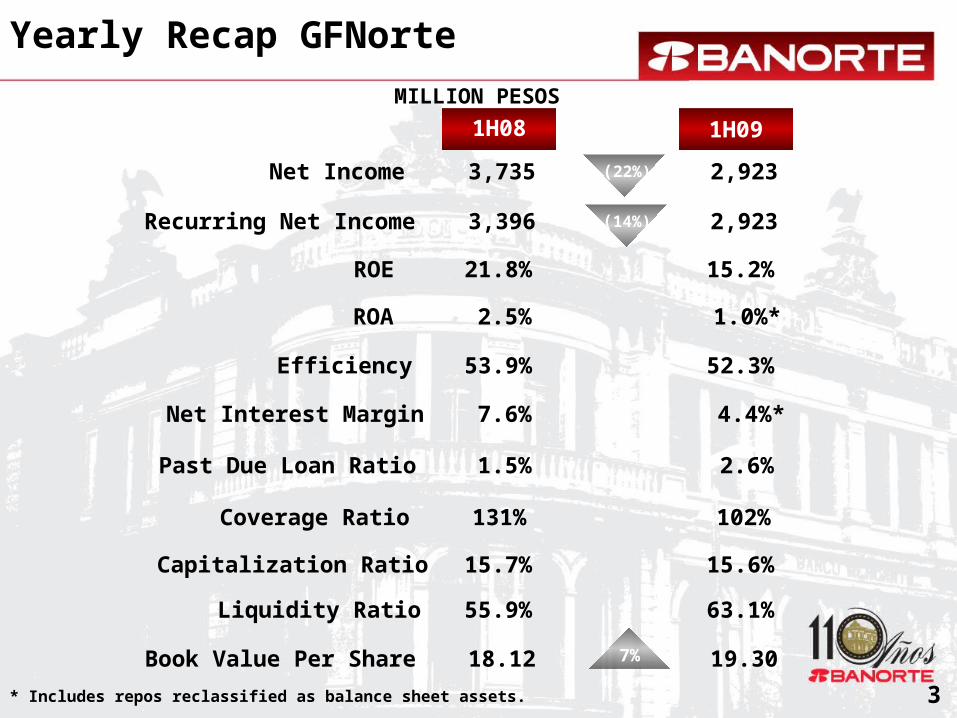

Yearly Recap GFNorte

Past Due Loan Ratio 1.5% 2.6%

1H09

Net Income

Capitalization Ratio

Book Value Per Share

1H08

3,735

Net Interest Margin

(22%)

15.7%

18.12

7.6%

19.30

4.4%*

2,923

15.6%

ROE 21.8% 15.2%

ROA 2.5% 1.0%*

Efficiency 53.9% 52.3%

Coverage Ratio 131% 102%

Liquidity Ratio 55.9% 63.1%

7%

Recurring Net Income 3,396 (14%) 2,923

* Includes repos reclassified as balance sheet assets.

MILLION PESOS

Income Statement

MILLION PESOS

Net Interest Income

Service Fees

Recovery

Non Interest Income

Total Income

Non Interest Expense

Net Operating Income

Income Tax

Net Income

Provisions

Subs & Minority Interest

FX & Trading

QoQ YoY1Q092Q08 2Q09

Non Operating Income, Net

6,199

1,465

138

2,070

8,269

(4,341)

3,928

425

(574)

1,611

(2,162)

(6)

1,611

242

Recurring Net Income

5,225

1,695

117

159

-

1,971

7,196

(3,903)

3,293

576

(751)

1,806

(1,255)

(57)

1,742

Other Income and Expense 226

1,454

164

157

147

1,922

7,760

(4,037)

3,723

193

(429)

1,312

(2,188)

14

5,838

1,312

12%

(14%)

40%

(1%)

100%

(2%)

8%

3%

13%

(66%)

(43%)

(27%)

74%

(125%)

(27%)

(6%)

(1%)

19%

(35%)

(35%)

(7%)

(6%)

(7%)

(5%)

(55%)

(25%)

(19%)

1%

(333%)

(25%) 4

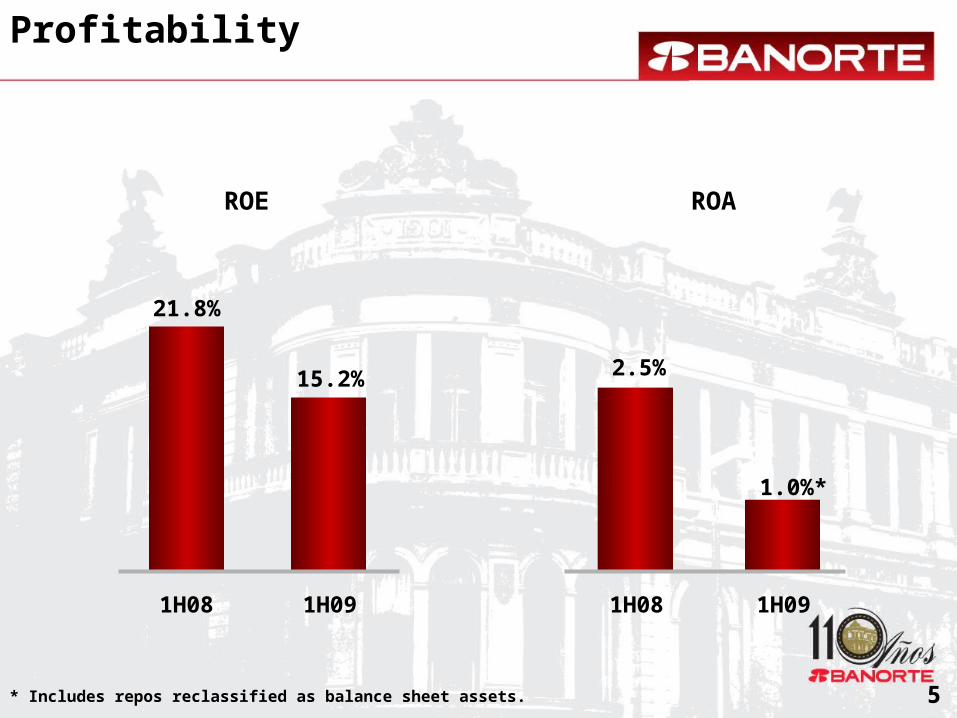

5

ROE ROA

2.5%

1H08

21.8%

1H08

15.2%

1H09

1.0%*

1H09

Profitability

* Includes repos reclassified as balance sheet assets.

Cost to Income

BILLION PESOS

EFFICIENCY RATIO

Total Income

2Q08

7.2

2Q09

7.8

Non Interest Expense 3.9 4.0

54%

2Q08

53%

1Q09

8%

3%

YoYQoQ1Q09

8.3

4.3

(6%)

(7%)

52%

2Q09

6

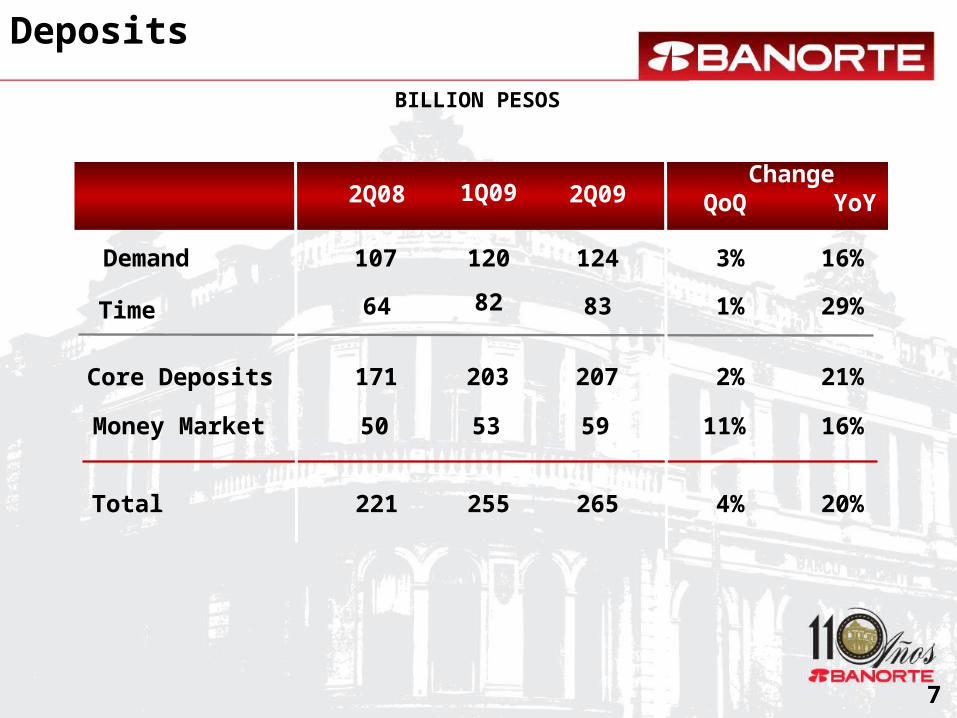

Deposits

Demand

Time

Total

2Q09

124

83

265

Core Deposits 207

Money Market 59

BILLION PESOS

QoQChange

YoY

16%

29%

20%

21%

16%

3%

1%

4%

2%

11%

1Q09

120

82

255

203

53

2Q08

107

64

221

171

50

7

BILLION PESOS

Performing Loan Portfolio

2Q08 1Q09 2Q09 YoYChange

QoQ

2Q08 1Q09 2Q09

217235 235

Commercial 10%(3%)

Corporate 0%(2%)

Government 31%12%

Total 8%0%

Consumer 4%(1%)

86

43

32

235

74

89

44

29

235

74

79

43

24

217

71

8

Consumer Loan Portfolio

BILLION PESOS

2Q08 1Q09 2Q09

7174 74

Consumer

Car

Credit Card

Payroll / Personal

Mortgage

2Q08 1Q09 2Q09 YoYChange

QoQ

(2%)(2%)

(20%)(7%)

(4%)(1%)

4%(1%)

17%2%

7

13

6

74

47

8

14

6

74

46

8

16

7

71

40

9

Loans to Deposits Ratio

TOTAL LOANS /TOTAL DEPOSITS

103%

1Q08

99%

2Q08

97%

3Q08

10

93%

4Q08

92%

1Q09

88%

2Q09

2. Asset Quality

Asset Quality

Past Due Loans

Loan Loss Reserves

RESERVECOVERAGE RATIO

PAST DUE LOANRATIO

Total Loan Portfolio

BILLION PESOS

2Q08 1Q09 2Q09

102%

131%

109%

2Q08 1Q09 2Q09

2.6%

1.5%

2.3%

2Q08 1Q09 2Q09

3.2

4.2

220

6.3

6.4

238

5.6

6.1

239

12

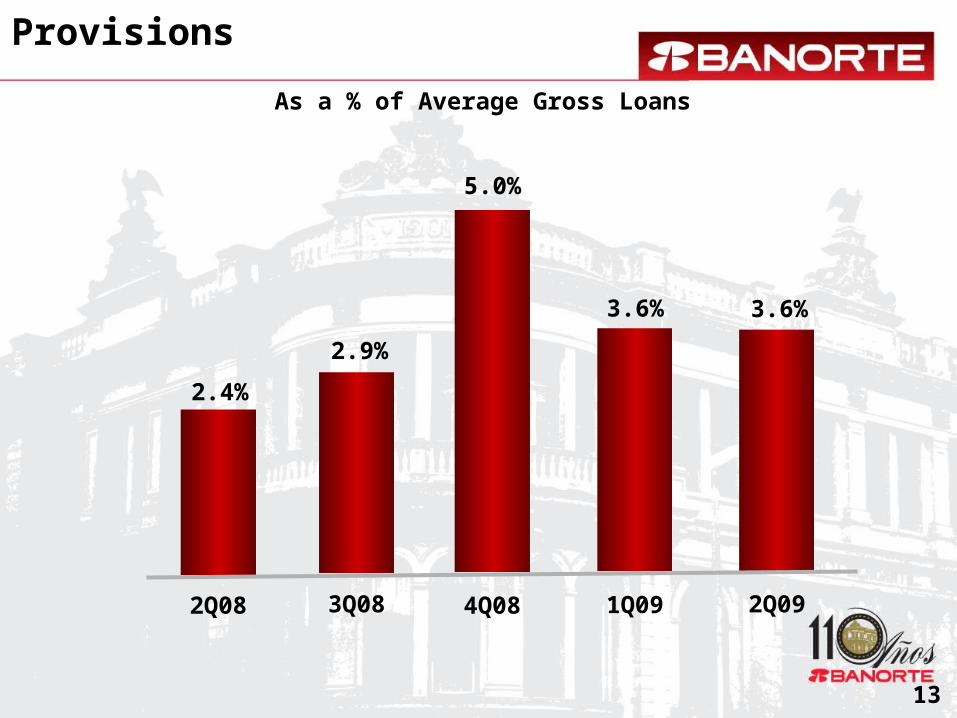

Provisions

As a % of Average Gross Loans

2.4%

2Q08

3.6%

2Q09

3.6%

1Q09

2.9%

3Q08

5.0%

4Q08

13

14

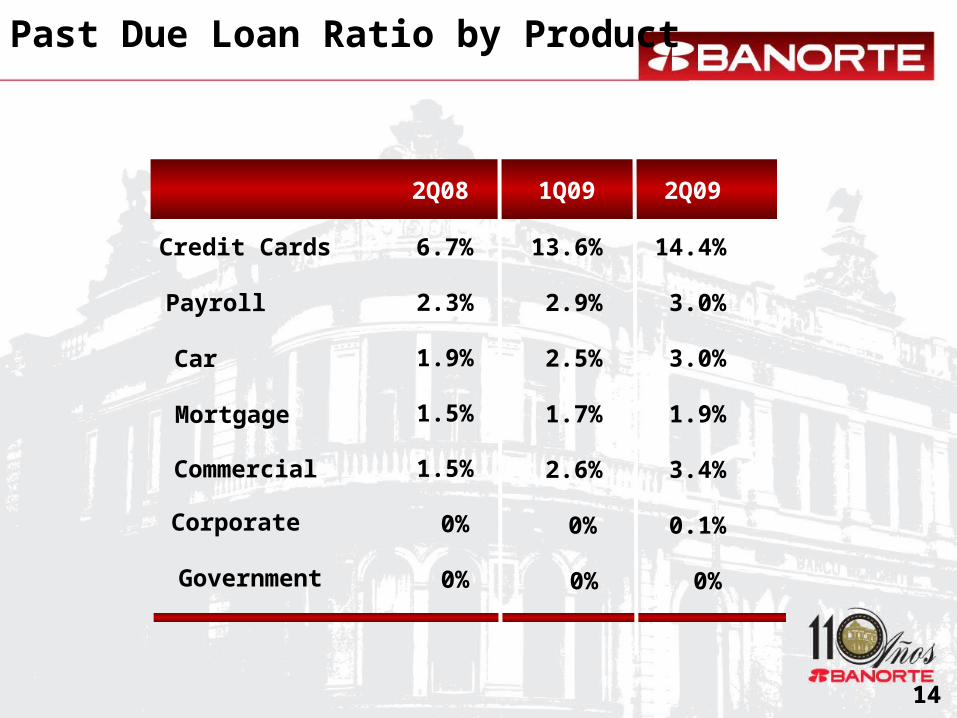

Past Due Loan Ratio by Product

Payroll

Car

Mortgage

Credit Cards

Commercial

Corporate

Government

14

2Q08

2.3%

1.9%

1.5%

6.7%

1Q09 2Q09

13.6%

2.9%

2.5%

1.5%

0%

0%

1.7%

2.6%

0%

0%

14.4%

3.0%

3.0%

1.9%

3.4%

0%

0.1%

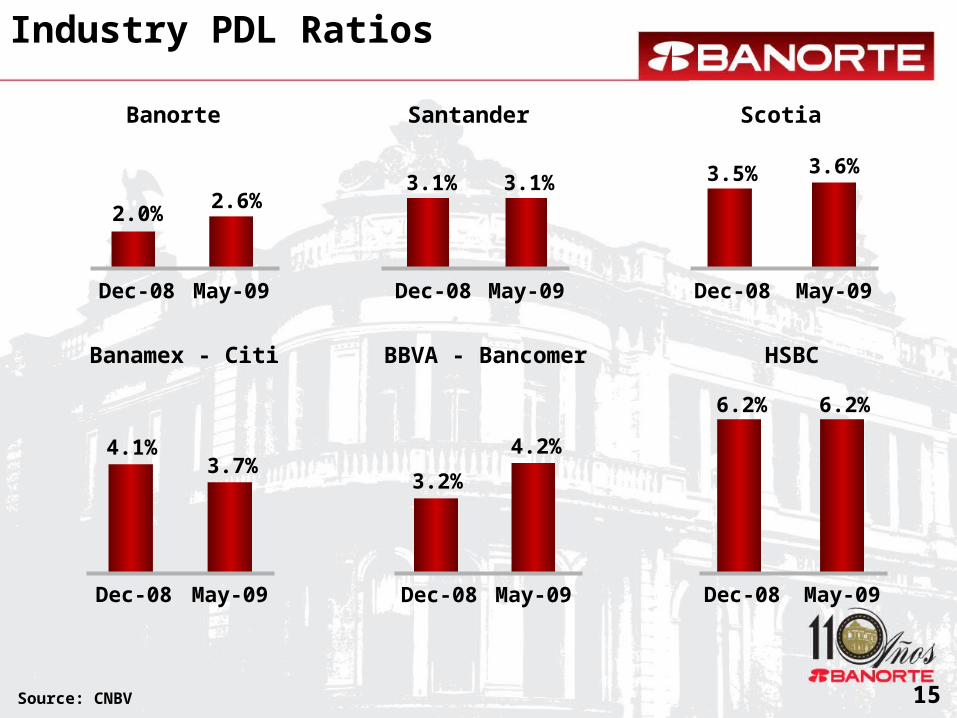

15

Banorte

2.0%2.6%

Dec-08 May-09

BBVA - Bancomer

3.2%

4.2%

Dec-08 May-09

Banamex - Citi

4.1%3.7%

Dec-08 May-09

HSBC

6.2% 6.2%

Dec-08 May-09

Santander

3.1% 3.1%

Dec-08 May-09

Scotia

3.5% 3.6%

Dec-08 May-09

Industry PDL Ratios

Source: CNBV

3. Capital Management

17

Capitalization

Tier 1

Tier 2

TOTAL

% Tier 1

17

2Q08 1Q09 2Q09

10.7%

5.0%

15.7%

68%

9.7%

4.9%

14.6%

66%

10.7%

4.9%

15.6%

69%

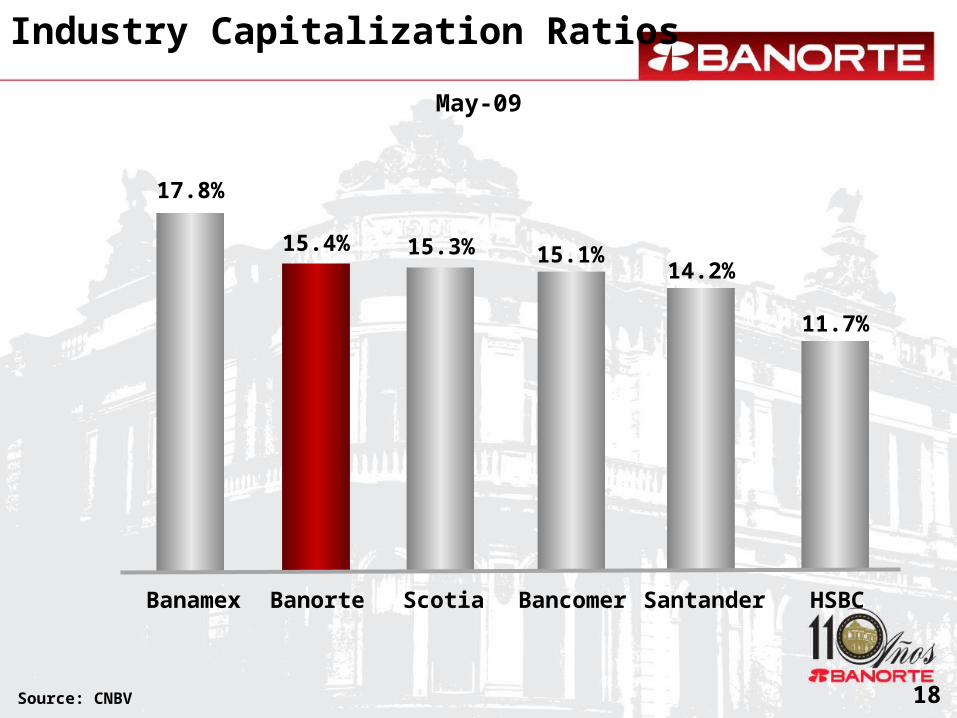

18

Industry Capitalization Ratios

Banamex Scotia Bancomer HSBCBanorte Santander

Source: CNBV

17.8%

15.4% 15.1%14.2%

11.7%

15.3%

May-09

19

IFC’s Investment in Banorte

IFC is a member of the World Bank Group.

Promotes sustainable economic development in emerging markets.

Characteristics:

IFC will have an equity stake in Banco Mercantil del Norte.

Banorte’s Board of Directors has approved the investment.

Approval by IFC’s Board and the Mexican authorities is still pending.

Long term investment.

Benefits:

Increase Banorte’s Tier 1 ratio.

Banorte and IFC will collaborate in various expansion programs.

Leverage IFC’s expertise in social responsibility, corporate

practices and environmental protection.

20

+1

+2

=

Notches above Inv.

Grade

Baa1

BBB

BBB-

Rating

Fitch

Moody’s

Standard & Poor’s

Agency

Stable

Stable

Negative

Outlook Date

Dec-08

Feb-09

Mar-09

Credit Ratings

4. Subsidiaries

Recovery Bank

Net Income

MILLION PESOS

AUMBILLION PESOS

2Q092Q08

Banorte’s Assets

Acquired Assets

%

Investment Projects

Total

IPAB

22

1H08

318

1H09

219

38.7

19.2

32.0

28.9

(18%)

50%

2.6 3.2 22%

62.0 66.0 6%

1.4 1.5 6%

Long Term Savings

NET INCOME IN MILLION PESOS

AFORE INSURANCEANNUITIES

Total

23

2Q08

64

2Q09

61

6

2Q08

22

2Q09

0

2Q08(4)

2Q09

58

2Q08

43

2Q09

24

Afore IXE client portfolio acquisition.

Transfer of 312,489 clients.

Ps 5.4 billion in AUM, nearly 10% of Afore Banorte-Generali’s AUMs.

Afore Ahorra Ahora client portfolio acquisition.

Transfer of 367,660 clients.

Ps $1.14 billion in AUM, 1.86% of Afore Banorte-Generali’s AUMs.

Through these acquisitions, Banorte becomes the 4th largest player in

terms of accounts managed.

Afore – Acquisitions

Subsidiaries

BROKER DEALER LEASING AND FACTORING

NET INCOME IN MILLION PESOS

WAREHOUSING

25

78

2Q08

106

2Q09

7

2Q08

7

2Q09

143

2Q08

32

2Q09

26

Inter National Bank

Net Income

Loan Loss Reserves

MILLION DOLLARS IN US GAAP

Change2Q08 2Q09

Net Interest Income

Non Interest Income

Total Income

Non Interest Expense

Demand Deposits

Performing Loans

Past Due Loans

Time Deposits

6.0

2.2

(150%)

482%

16.3 (16%)

3.7 11%

20.0 (11%)

8.7 12%

707 3%

1,018 7%

13.5 321%

713 35%

(3.0)

12.8

13.6

4.1

17.8

9.8

730

1,086

56.9

964

27

FINANCIAL RATIOS(%)

Reserve Coverage

PDL Ratio

Change2Q08

96.6

1.3

2Q09

37.4

4.9

(59.2 pp)

3.6 pp

MIN 4.2 3.3 (0.9 pp)

ROE 18.7 (4.6) (23.3 pp)

ROA 1.4 (0.6) (2.0 pp)

Efficiency 43.7 55.2 11.4 pp

Capitalization Ratio 11.6 14.1 2.5 pp

Tier 1 Capital 8.2 7.8 (0.4 pp)

Inter National Bank

5. Final Remarks

29

The most severe contraction in GDP since the great depression.

Second half of the year will be challenging.

Unemployment.

Consumption.

Interest rates at historically low levels.

Caution due to possible swine flu rebound.

Improve the bank’s fundamentals under this environment.

Conclusions

Capital.

Asset quality.

Collections and recoveries.

Cost of funding.

Cost containment.

Internal controls.

Contact Information

David SuarezInvestor Relations OfficerTel: (52 55) 52.68.16.80E-mail: [email protected] www.banorte.com/ri

Recommended