Benchmarking of Key Global OEMs Vehicle Platform Strategies

Vishwas Shankar, Industry AnalystVishwas Shankar, Industry Analyst

Automotive and Transportation Automotive and Transportation

12 October 201112 October 2011

Today’s Presenter: Vishwas Shankar

Functional Expertise

Over eight years of total work experience and specific expertise in:

• Competitive intelligence and benchmarking

• Market analysis and business opportunity assessment

• New products product price positioning in the electric vehicle space

• New product development and vehicle component sourcing

Industry Expertise

Experience base covering a broad range of sectors including:

• Strong understanding of electric vehicles and their technologies

• Global microcars and micro mobility outlook

• Production platform strategy of global automakers

What I Bring to the Team

2

What I Bring to the Team

• Strategic thinking & strong analytical skills using quantitative techniques and management tools

• Ability to contribute as an individual and team player in structuring and executing complex engagements

Career Highlight

Worked with leading firms and associations in the following capabilities:

• Purchase Manager, Renault Nissan Technology and Business Centre India Private Ltd.

• Purchase Manager, Mahindra Renault Private Ltd.

• Engineer, Mahindra & Mahindra Automotive

• Project Assistant / Teaching Assistant, Birla Institute of Technology and Science, Pilani

• Member – Production Engineering, Sundaram-Clayton Ltd.

• Member – Foundry, Perambur LocoworksEducation

• Master of Engineering – Manufacturing Systems Engineering, Birla Institute of Technology and Science, Pilani

• Master of Science – Engineering Technology, Birla Institute of Technology and Science, Pilani

Vishwas ShankarIndustry Analyst

Automotive &

Transportation

Frost & Sullivan

Europe

Aims and Objectives

Understand and evaluate key modules, systems and components targeted for sharing

Understand key OEM groups’ current and future platform standardization strategy in the

light vehicle category and draw comparisons’

To provide an insight into platform adoption roadmap of key OEM group platforms

A

B

3

Understand and evaluate key modules, systems and components targeted for sharing

across platforms

Provide strategic conclusions and recommendations

To estimate the total investments and expected savings by key OEM groups from platform

standardization strategy

C

D

E

Source: Frost & Sullivan analysis.

Definition

Platform

There is no standard definition of a platform; however, the commonly accepteddefinition is:A collection of fixed design elements that define its architecture.Platforms usually consist of steering system, front suspension, rear suspension,driveline, braking system, powertrain orientation, and mountings, along with thefloor pan that supports all these parts.

Shared PlatformFor the purpose of this research, a shared platform is defined as a platformshared between two or more models within the same segment or differentsegments.

4

Architecture

An architecture defines the overall framework of the vehicle including itsfootprint, driveline and engine orientations, suspension which forms thevehicle’s DNA, and its driving dynamics.Examples of key architectures are FR (Front Engine and Rear Drive), RR (RearEngine and Rear Drive), MR (Mid Engine and Rear Drive), and so on.

Modular Toolkit

An engineering discipline conceptualized by OEMs’ to build a wide variety ofvehicle architectures, potentially using common standardized components, anddifferentiated using vehicle wheelbase, track width, size, and shape.For instance, Volkswagen group plans to make millions of vehicles from justthree key platforms based on modular toolkit strategy.

Source: Frost & Sullivan analysis.

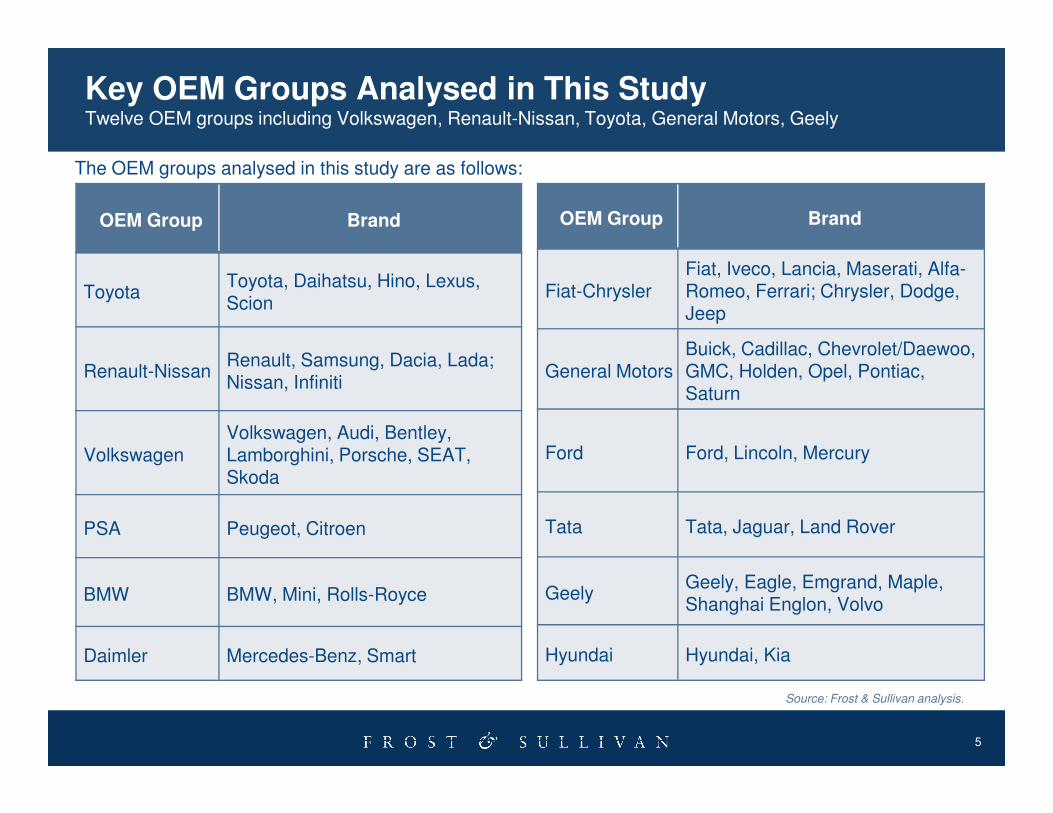

Key OEM Groups Analysed in This StudyTwelve OEM groups including Volkswagen, Renault-Nissan, Toyota, General Motors, Geely

OEM Group Brand

ToyotaToyota, Daihatsu, Hino, Lexus, Scion

Renault-NissanRenault, Samsung, Dacia, Lada;Nissan, Infiniti

OEM Group Brand

Fiat-ChryslerFiat, Iveco, Lancia, Maserati, Alfa-Romeo, Ferrari; Chrysler, Dodge, Jeep

General MotorsBuick, Cadillac, Chevrolet/Daewoo, GMC, Holden, Opel, Pontiac, Saturn

The OEM groups analysed in this study are as follows:

5

VolkswagenVolkswagen, Audi, Bentley, Lamborghini, Porsche, SEAT, Skoda

PSA Peugeot, Citroen

BMW BMW, Mini, Rolls-Royce

Daimler Mercedes-Benz, Smart

Ford Ford, Lincoln, Mercury

Tata Tata, Jaguar, Land Rover

GeelyGeely, Eagle, Emgrand, Maple, Shanghai Englon, Volvo

Hyundai Hyundai, Kia

Source: Frost & Sullivan analysis.

Key Takeaways

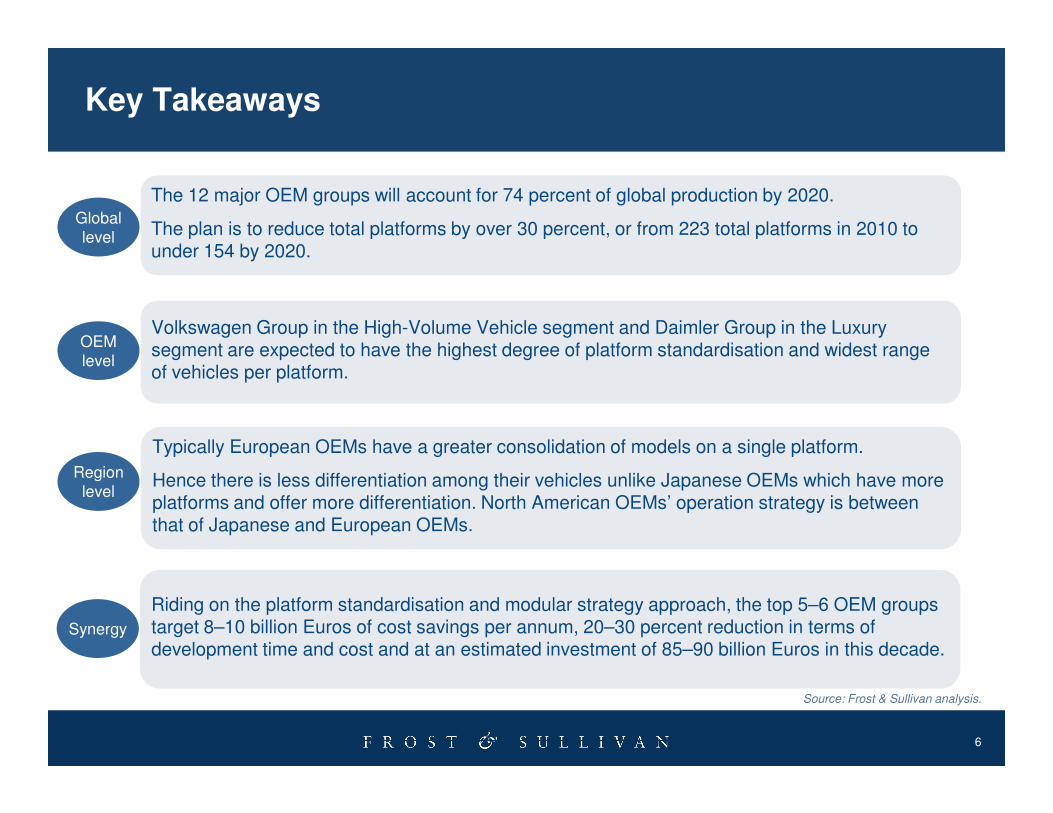

The 12 major OEM groups will account for 74 percent of global production by 2020.

The plan is to reduce total platforms by over 30 percent, or from 223 total platforms in 2010 to under 154 by 2020.

Global

level

OEM

level

Volkswagen Group in the High-Volume Vehicle segment and Daimler Group in the Luxury segment are expected to have the highest degree of platform standardisation and widest range of vehicles per platform.

6

Source: Frost & Sullivan analysis.

Region

level

Typically European OEMs have a greater consolidation of models on a single platform.

Hence there is less differentiation among their vehicles unlike Japanese OEMs which have more platforms and offer more differentiation. North American OEMs’ operation strategy is between that of Japanese and European OEMs.

Synergy

Riding on the platform standardisation and modular strategy approach, the top 5–6 OEM groups target 8–10 billion Euros of cost savings per annum, 20–30 percent reduction in terms of development time and cost and at an estimated investment of 85–90 billion Euros in this decade.

Key Global OEMs Platform Reduction Roadmap

Geely Group

Daimler Group

BMW Group

Tata Group

Platform Strategy: Platform Reduction Plan of Key Global OEMs (World), 2010 - 2020

-30 percent

223

154

• The 12 key OEM groups to constitute over 74 percent of global production by 2020. • Over 100 platforms existing today will disappear and pave the way for nearly 40 new platforms to take over

by end of this decade.

Num

ber

of P

latf

orm

s

High

7

2010 Total Platforms 2010 Shared Platforms 2020 Total Platforms 2020 Shared Platforms

Tata Group

PSA Group

Fiat-Chrysler Group

Ford Group

Hyundai Group

General Motors Group

Renault-Nissan Group

Toyota Group

Volkswagen Group

Source: Frost & Sullivan analysis.

-15 percent

110

94

Num

ber

of P

latf

orm

s

Year

Low

Platform Summary of Key Global OEMs

Platform Strategy: Platform Summary (World), 2010 and 2020

To

tal

No

. O

f P

latf

orm

s

XV, E B, B0 Gamma, Delta 3

Global C, Global

C

SR1, C-EVO

PF1, BVH1

Vista, Ace

PL2, PL2

W, MRA B, Basic

PQ35, MQB

HD, HD

• By 2020, 12 key global OEM groups with their total 154 platforms to account for nearly 74 percent of the global production.

High

8

2010 Key Platform, 2020 Key Platform Note: All figures are rounded. The base year is 2010. Source: Frost & Sullivan analysis.

Vo

lksw

age

n G

rou

p

To

yota

Gro

up

Re

na

ult

-Nis

san

Gro

up

Ge

ne

ral M

oto

rs G

rou

p

Hyu

nd

ai G

rou

p

Fo

rd G

rou

p

Fia

t-C

hry

sle

r G

rou

p

PSA

Gro

up

Ta

ta G

rou

p

BM

W G

rou

p

Da

imle

r G

rou

p

Ge

ely

Gro

up

To

tal

No

. O

f P

latf

orm

s

2010 2020OEM Group

Low

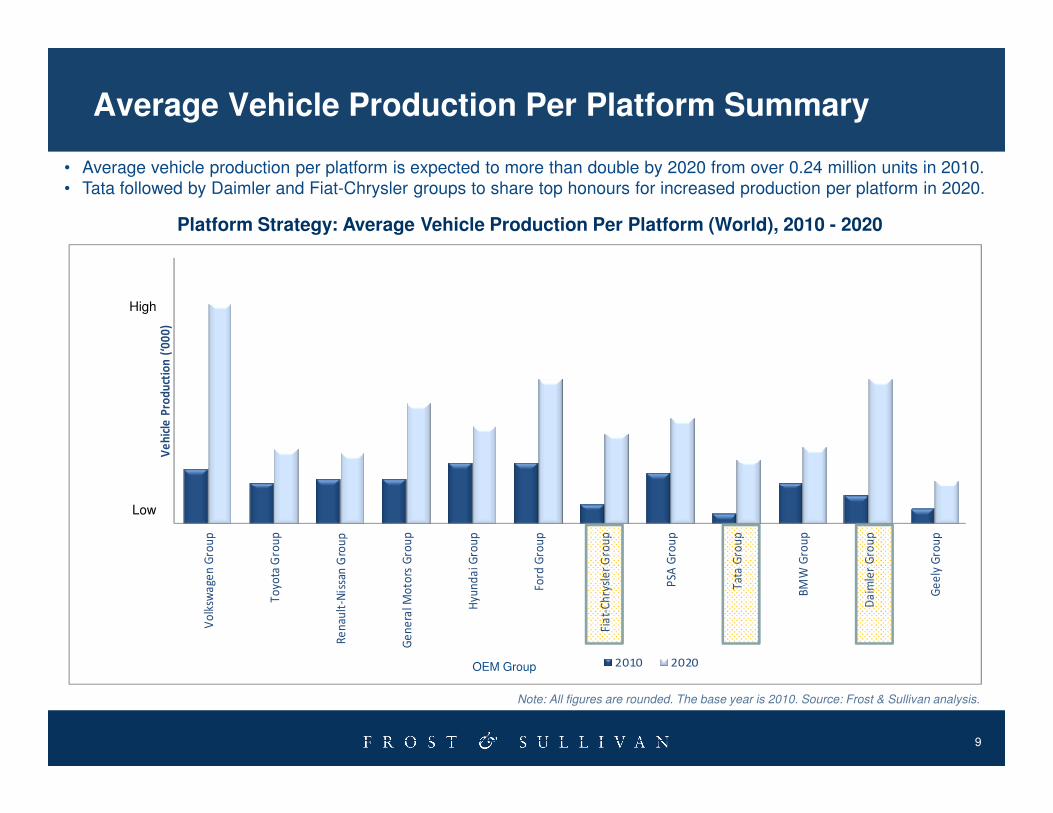

Average Vehicle Production Per Platform Summary

• Average vehicle production per platform is expected to more than double by 2020 from over 0.24 million units in 2010.

• Tata followed by Daimler and Fiat-Chrysler groups to share top honours for increased production per platform in 2020.

Ve

hic

le P

rod

uct

ion

(‘0

00

)

Platform Strategy: Average Vehicle Production Per Platform (World), 2010 - 2020

High

9

Note: All figures are rounded. The base year is 2010. Source: Frost & Sullivan analysis.

Vo

lksw

age

n G

rou

p

To

yota

Gro

up

Re

nau

lt-N

issa

n G

rou

p

Ge

ne

ral M

oto

rs G

rou

p

Hyu

nd

ai G

rou

p

Ford

Gro

up

Fia

t-C

hry

sle

r G

rou

p

PSA

Gro

up

Tat

a G

rou

p

BM

W G

rou

p

Da

imle

r G

rou

p

Ge

ely

Gro

up

Ve

hic

le P

rod

uct

ion

(‘0

00

)

2010 2020OEM Group

Low

General Motors Delta 3

Renault-Nissan B0

Volkswagen MQB

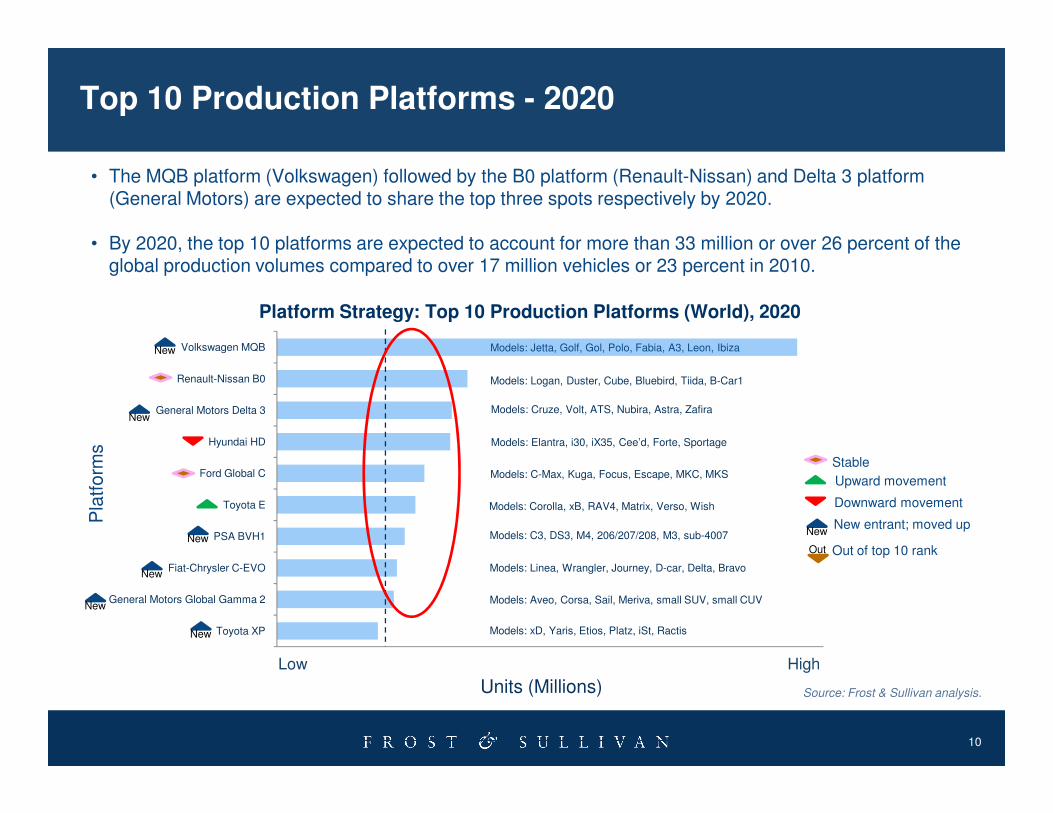

Top 10 Production Platforms - 2020

Platform Strategy: Top 10 Production Platforms (World), 2020

Models: Jetta, Golf, Gol, Polo, Fabia, A3, Leon, IbizaNew

• The MQB platform (Volkswagen) followed by the B0 platform (Renault-Nissan) and Delta 3 platform (General Motors) are expected to share the top three spots respectively by 2020.

• By 2020, the top 10 platforms are expected to account for more than 33 million or over 26 percent of the global production volumes compared to over 17 million vehicles or 23 percent in 2010.

Models: Logan, Duster, Cube, Bluebird, Tiida, B-Car1

Models: Cruze, Volt, ATS, Nubira, Astra, Zafira

10

Toyota XP

General Motors Global Gamma 2

Fiat-Chrysler C-EVO

PSA BVH1

Toyota E

Ford Global C

Hyundai HD

General Motors Delta 3

Source: Frost & Sullivan analysis.

Pla

tform

s

Stable

Upward movement

Downward movement

NewNew entrant; moved up

Out Out of top 10 rank

New

New

New

New

New

Units (Millions)

Models: Cruze, Volt, ATS, Nubira, Astra, Zafira

Models: Elantra, i30, iX35, Cee’d, Forte, Sportage

Models: C-Max, Kuga, Focus, Escape, MKC, MKS

Models: Corolla, xB, RAV4, Matrix, Verso, Wish

Models: C3, DS3, M4, 206/207/208, M3, sub-4007

Models: Linea, Wrangler, Journey, D-car, Delta, Bravo

Models: Aveo, Corsa, Sail, Meriva, small SUV, small CUV

Models: xD, Yaris, Etios, Platz, iSt, Ractis

Low High

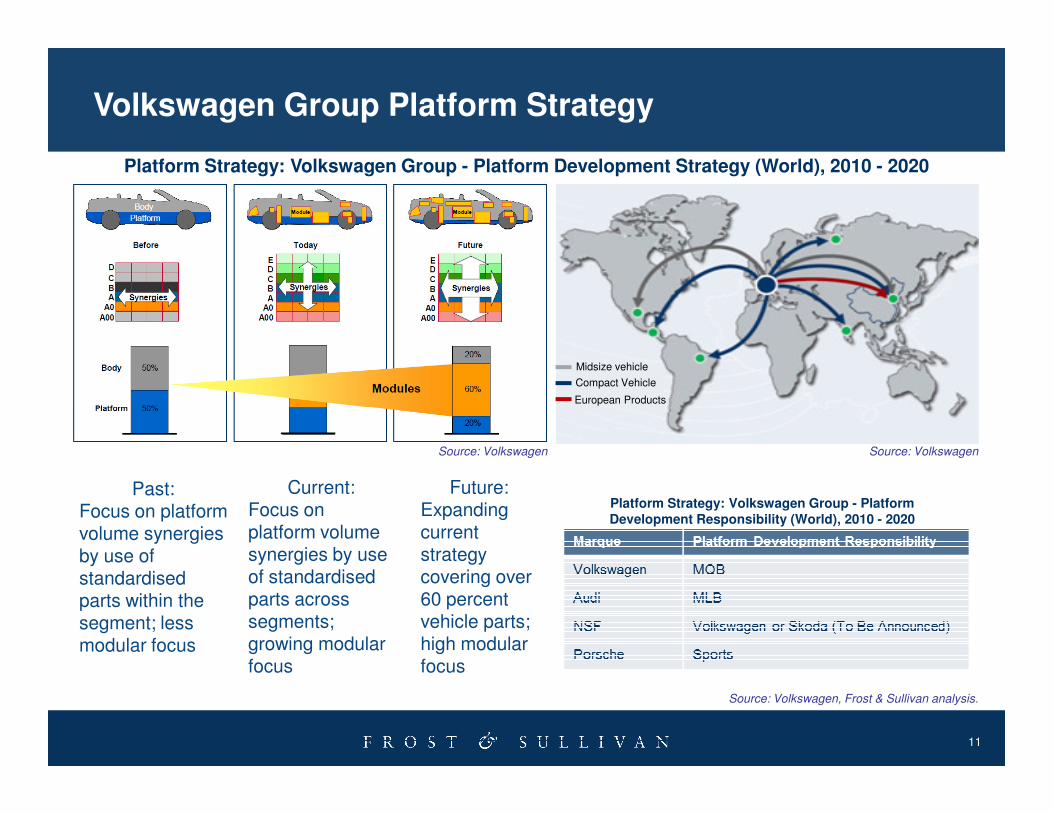

Platform Strategy: Volkswagen Group - Platform Development Strategy (World), 2010 - 2020

Midsize vehicle

Compact Vehicle

European Products

Volkswagen Group Platform Strategy

11

Past: Focus on platform volume synergies by use of standardised parts within the segment; less modular focus

Current: Focus on platform volume synergies by use of standardised parts across segments; growing modular focus

Future: Expanding current strategy covering over 60 percent vehicle parts; high modular focus

Platform Strategy: Volkswagen Group - Platform Development Responsibility (World), 2010 - 2020

Source: Volkswagen, Frost & Sullivan analysis.

Source: VolkswagenSource: Volkswagen

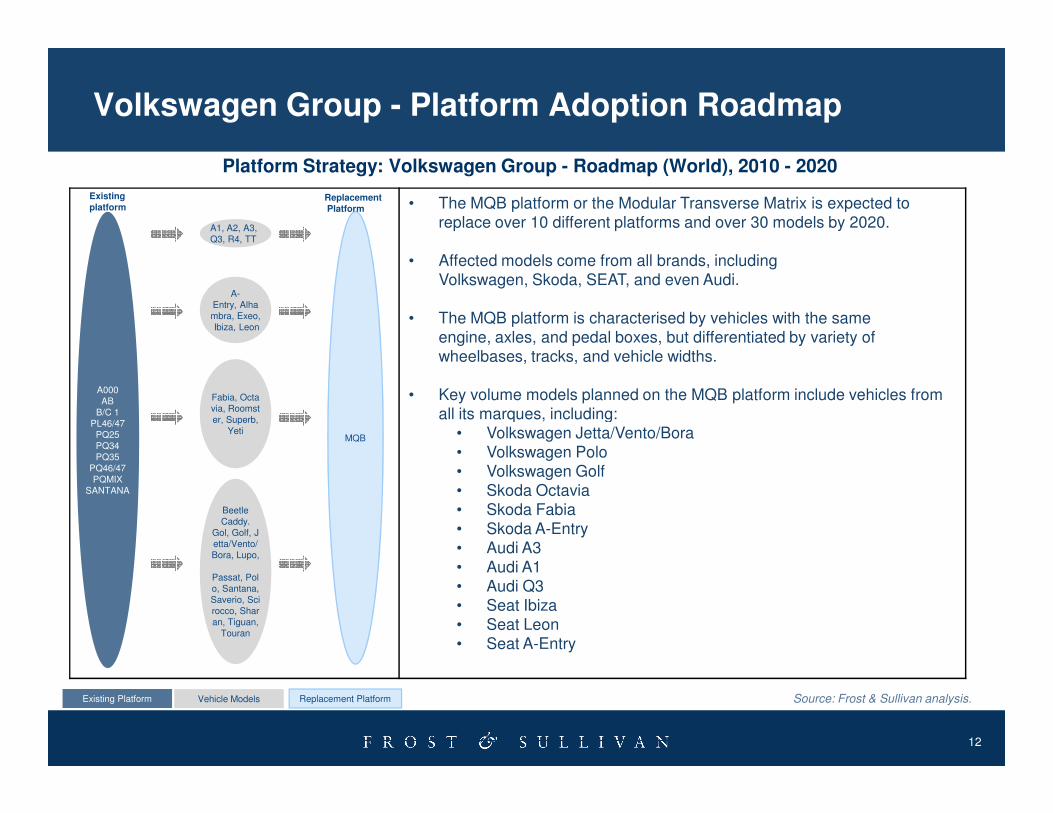

• The MQB platform or the Modular Transverse Matrix is expected to

replace over 10 different platforms and over 30 models by 2020.

• Affected models come from all brands, including

Volkswagen, Skoda, SEAT, and even Audi.

• The MQB platform is characterised by vehicles with the same

engine, axles, and pedal boxes, but differentiated by variety of

wheelbases, tracks, and vehicle widths.

• Key volume models planned on the MQB platform include vehicles from

all its marques, including:

A1, A2, A3,

Q3, R4, TT

Replacement

Platform

A000

AB

Existing

platform

A-

Entry, Alha

mbra, Exeo,

Ibiza, Leon

Fabia, Octa

via, Roomst

Platform Strategy: Volkswagen Group - Roadmap (World), 2010 - 2020

Volkswagen Group - Platform Adoption Roadmap

12

all its marques, including:

• Volkswagen Jetta/Vento/Bora

• Volkswagen Polo

• Volkswagen Golf

• Skoda Octavia

• Skoda Fabia

• Skoda A-Entry

• Audi A3

• Audi A1

• Audi Q3

• Seat Ibiza

• Seat Leon

• Seat A-Entry

MQB

B/C 1

PL46/47

PQ25

PQ34

PQ35

PQ46/47

PQMIX

SANTANA

via, Roomst

er, Superb,

Yeti

Beetle

Caddy.

Gol, Golf, J

etta/Vento/

Bora, Lupo,

Passat, Pol

o, Santana,

Saverio, Sci

rocco, Shar

an, Tiguan,

Touran

Source: Frost & Sullivan analysis.Replacement PlatformExisting Platform Vehicle Models

MQB Platform - Gas and Electric Compatibility

MQB MQB

Volkswagen – Electric Vehicle Platform Strategy

• Volkswagen is expected to invest modular EV toolkits to build its electric vehicles with minimal part replacement.

• Nissan is expected to invest in dedicated platforms to build electric vehicles, as in the case of the Nissan Leaf.

Nissan – Electric Vehicle Platform Strategy

13

Source: Frost & Sullivan analysis.

• Modular replacement• Gas engine toolkit replaced by electric toolkit • Minimal discrete parts between electric and engine vehicle

Source: VolkswagenSource: Volkswagen Source: Nissan

Li-ion

rechargeable

batteries

Inverter and

drive motor

Dedicated Nissan

Leaf platform with

aerodynamic smooth

floor

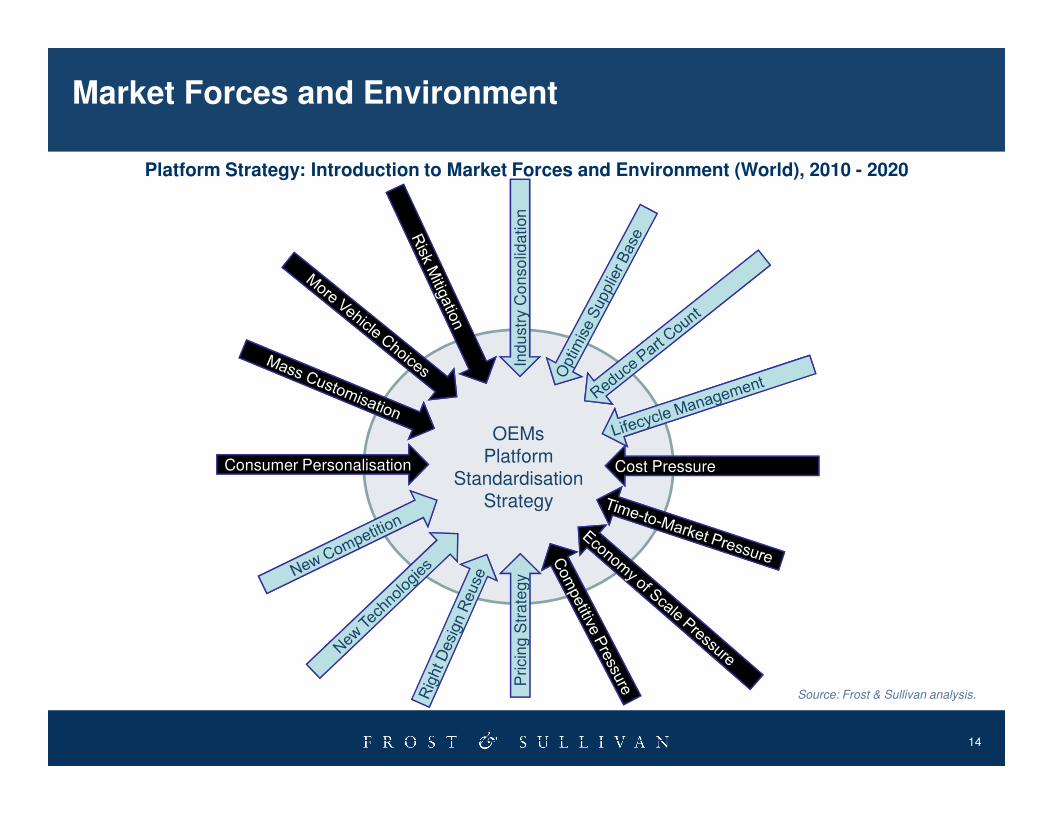

Market Forces and Environment

Platform Strategy: Introduction to Market Forces and Environment (World), 2010 - 2020

Ind

ustr

y C

on

so

lida

tion

Ind

ustr

y C

on

so

lida

tion

14

Source: Frost & Sullivan analysis.

OEMsPlatform

Standardisation Strategy

Pricin

g S

tra

tegy

Pricin

g S

tra

tegy

Cost PressureConsumer Personalisation

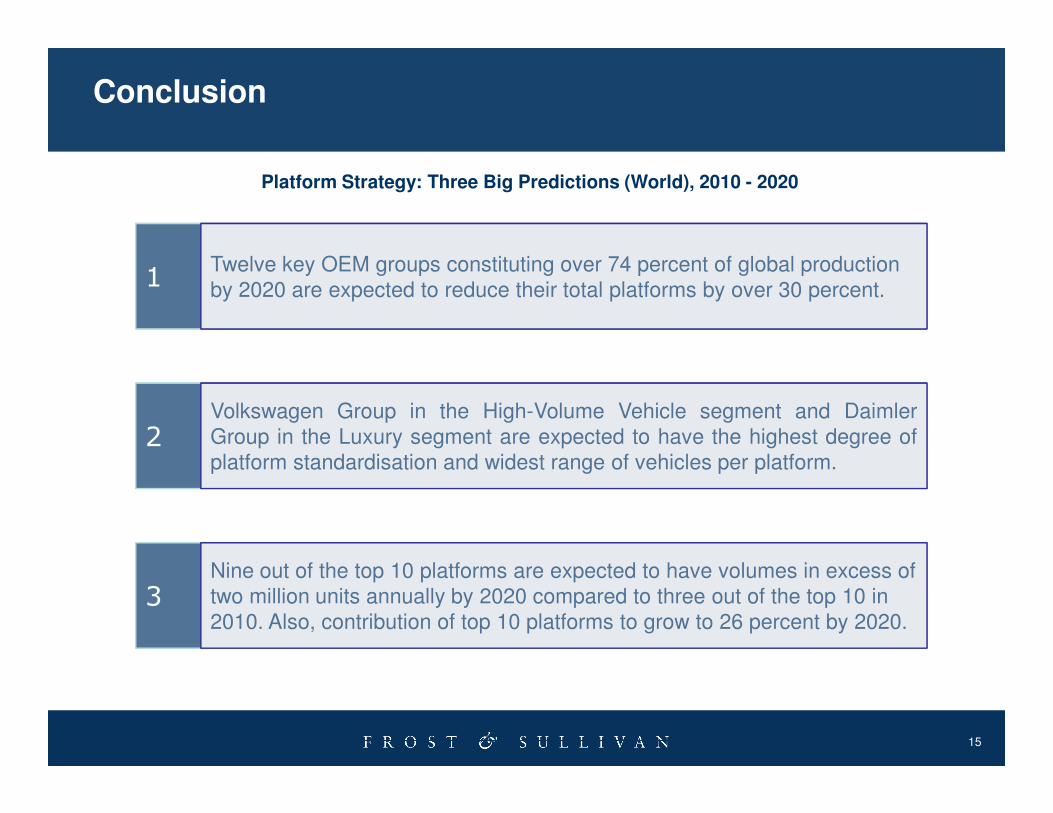

Conclusion

Volkswagen Group in the High-Volume Vehicle segment and Daimler

1Twelve key OEM groups constituting over 74 percent of global production

by 2020 are expected to reduce their total platforms by over 30 percent.

Platform Strategy: Three Big Predictions (World), 2010 - 2020

15

2

Volkswagen Group in the High-Volume Vehicle segment and Daimler

Group in the Luxury segment are expected to have the highest degree of

platform standardisation and widest range of vehicles per platform.

3

Nine out of the top 10 platforms are expected to have volumes in excess of

two million units annually by 2020 compared to three out of the top 10 in

2010. Also, contribution of top 10 platforms to grow to 26 percent by 2020.

Next Steps

� Request a proposal for Growth Partnership Services or Growth Consulting Services to support you and your team to accelerate the growth of your company. ([email protected])

� Join us at our annual Growth, Innovation, and Leadership 2012: A Frost & Sullivan Global Congress on Corporate Growthoccurring 15 – 16 May, 2012 (www.gil-global.com)

16

� Register for Frost & Sullivan’s Growth Opportunity Newsletter and keep abreast of innovative growth opportunities (www.frost.com/news)

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

What would you like to see from Frost & Sullivan?

17

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by rating this presentation

Frost & Sullivan’s Growth Consulting can assist with your growth strategies

Follow Frost & Sullivan on Facebook, LinkedIn, SlideShare, and Twitter

http://www.facebook.com/FrostandSullivan

http://www.linkedin.com/companies/4506

18

http://twitter.com/frost_sullivan

http://www.linkedin.com/companies/4506

http://www.slideshare.net/FrostandSullivan

For Additional Information

Katja FeickCorporate Communications

Automotive & Transportation

+49 (0) 69 [email protected]

Cyril Cromier

Sales Director

Europe

+33 1 42 81 22 44

19

Sarwant Singh

Partner

Global A&T

+44 207 915 7843

Recommended