Emerging Evidence on Electricity Markets: A

Public Power Perspective

By John Kelly

Michigan State University Institute of Public Utilities

38th Annual Regulatory Policy Conference

Richmond, VADecember 4-6, 2006

Oil- and Gas-Fired Generation as a Percentage of Total Generation – Mid-Atlantic and South, 1990-2004

Source: Analysis of the Impact of Coordinated Electricity Markets onConsumer Electricity Charges, LECG Corp., using EIA data

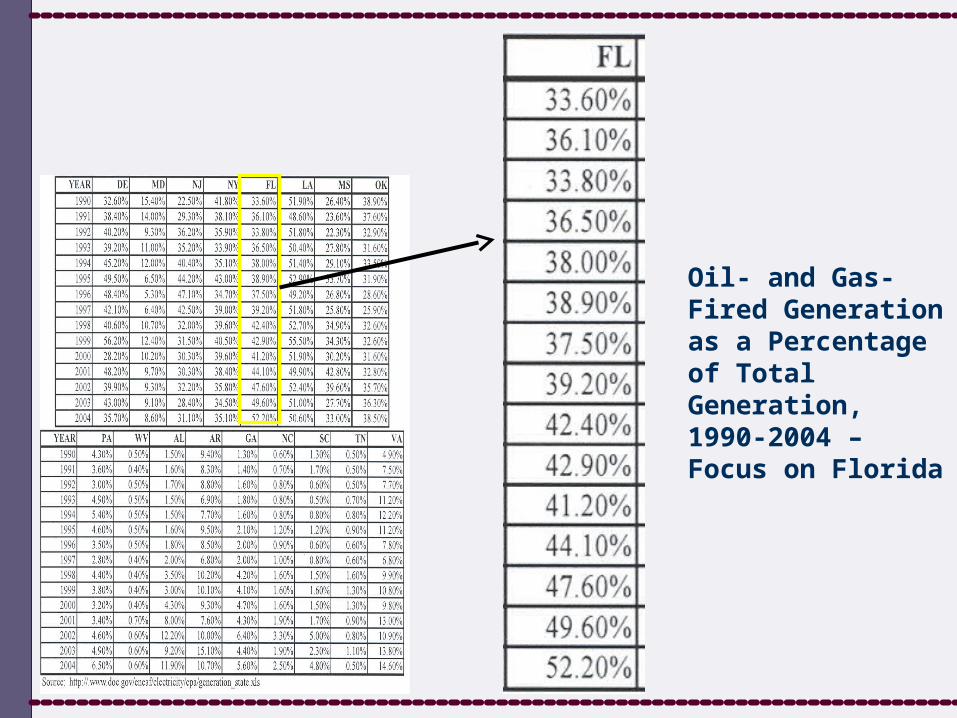

Oil- and Gas-Fired Generation as a Percentage of Total Generation, 1990-2004 – Focus on Florida

• “Reality trumps economic theory and flawed research methodology. Trying to cast today’s RTOs as money-saving institutions with consumer benefits is like trying to hammer a square peg into a round hole. It just doesn’t fit.”

-Joe Nipper, APPA Senior Vice President

of Government Relations

• Delaware Municipal Electric Corp. President and CEO Patrick McCullar:– “Customers in Delaware are paying

substantially more for electricity” since PJM was formed

– “No significant transmission has been built in the East in 35 years.”

– “Ten percent of the cost [of purchasing power in the bulk electricity market] was congestion charges.”

Blue Ridge Power Agency (VA)

• When Blue Ridge agency signed a new power supply contract after PJM was certified, prices had risen 75%– A year later, the price had risen by

another 25%

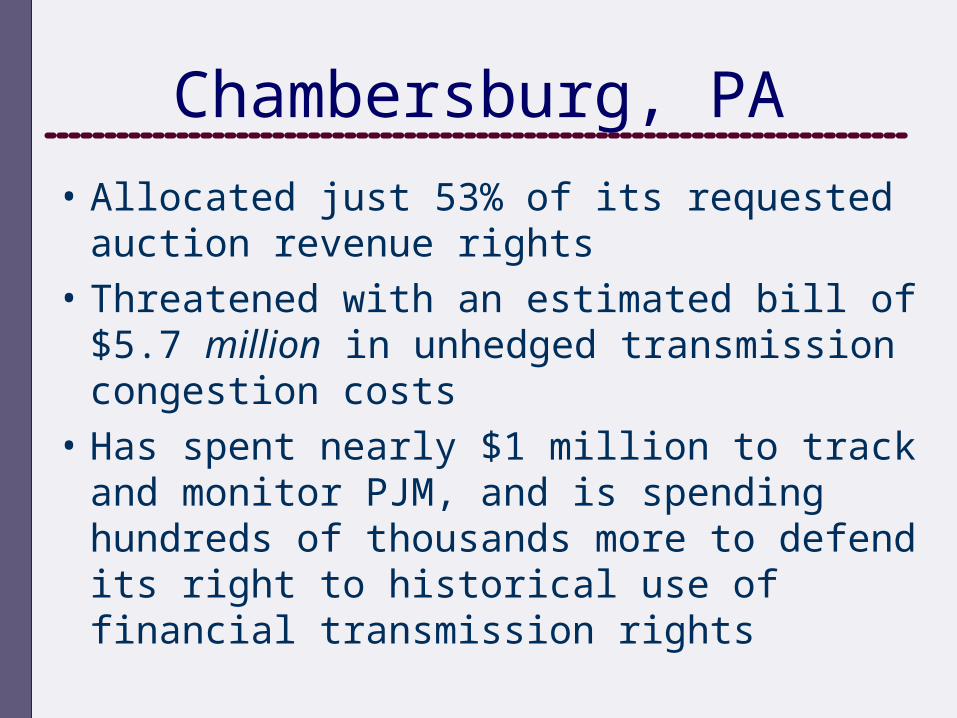

Chambersburg, PA

• Allocated just 53% of its requested auction revenue rights

• Threatened with an estimated bill of $5.7 million in unhedged transmission congestion costs

• Has spent nearly $1 million to track and monitor PJM, and is spending hundreds of thousands more to defend its right to historical use of financial transmission rights

Front Royal, VA

• Received only 54% of its requested ARRs

• Exposed to an estimated $3.3 million bill for unhedged transmission congestion costs

• Naperville Postpones Awarding Wholesale Electric Power Contract

Source: Naperville Web site

Media release, 4/25/2006

Warren Buffet on Electric Utilities

• Investing in electric utilities is “not a way to get rich, it’s a way to stay rich.”

• “Most of deregulation was a mistake” because, in a deregulated market, “generators have a clear incentive to reduce power reserves.”

• Owners of generating assets want the market to be tight

• “The last thing in the world an unregulated operator wants is excess capacity.”

Source: Platts Electric Utility Week 20 November 2006

• “The correct test, where markets have been introduced, is not whether prices have fallen but whether electricity prices would have been lower than those today if the old formula of regulated wholesale prices had remained in effect.”

-Branko Terzic,Former FERC commissioner

New York Times letter to the editor11/21/2006

• “Competition has elsewhere encouraged efficiency and innovation better than regulation. That electricity must be consumed when produced is no different from other time-perishable commodities like airline seats, hotel rooms, movie seats and advertising time on television. No barrier there. The solution is to improve market rules and market oversight.”

-Branko Terzic,Former FERC commissioner

New York Times letter to the editor11/21/2006

CT has not created a hot, active market

• “…shopping has been tepid at best during the three years that Connecticut’s transition service offer (TSO) – ending this year – has been in effect.”

• Four marketers were serving competitive customers in September, CL&P (Northeast Utilities) reported.”

• Constellation NewEnergy is the dominant player in the C&I makret with 1,335 of the 1,585 C&Is buying.”

Source: Restructuring Today

Increasing Power Supply Costs

• Kennebunk Light & Power

• Blue Ridge Power Agency

• Braintree Electric Light Department

• Municipal Electric Systems of Oklahoma

• Michigan Public Power Agency

• Lafayette Utilities System

• Iowa Municipal Utilities Association

• AMP-Ohio• St. Charles, Ill.

Not Very Somewhat Very

Capital intensiveness

Financial capital requirements

Scale economies

Lumpiness of investments

Location of facilities

Technology

Product durability

Sunk costs

Substitutes

Seasonality

Product differentiation

Vertical integration

Number of sellers and buyers

Mobility of resources/ Asset specificity

Foreign competition

Network industry

Relevance of industry characteristics to competitiveness

Not Very Somewhat Very

Capital intensiveness

Financial capital requirements

Scale economies

Lumpiness of investments

Location of facilities

Technology

Product durability

Sunk costs

Substitutes

Seasonality

Product differentiation

Vertical integration

Number of sellers and buyers

Mobility of resources/ Asset specificity

Foreign competition

Network industry

Relevance of industry characteristics to competitiveness

Recommended