Economic and Real Estate Outlook

By Lawrence Yun, Ph.D.Chief Economist

National Association of REALTORS®

How’s the Economy?

GDP Quarterly Activity

2007 - Q1

2007 - Q3

2008 - Q1

2008 - Q3

2009 - Q1

2009 - Q3

2010 - Q1

2010 - Q3

2011 - Q1

2011 - Q3

2012 - Q1

2012 - Q3

2013 - Q1

2013 - Q3

2014 - Q1

2014 - Q3

2015 - Q1

-10

-8

-6

-4

-2

0

2

4

6

Annualized Growth Rate

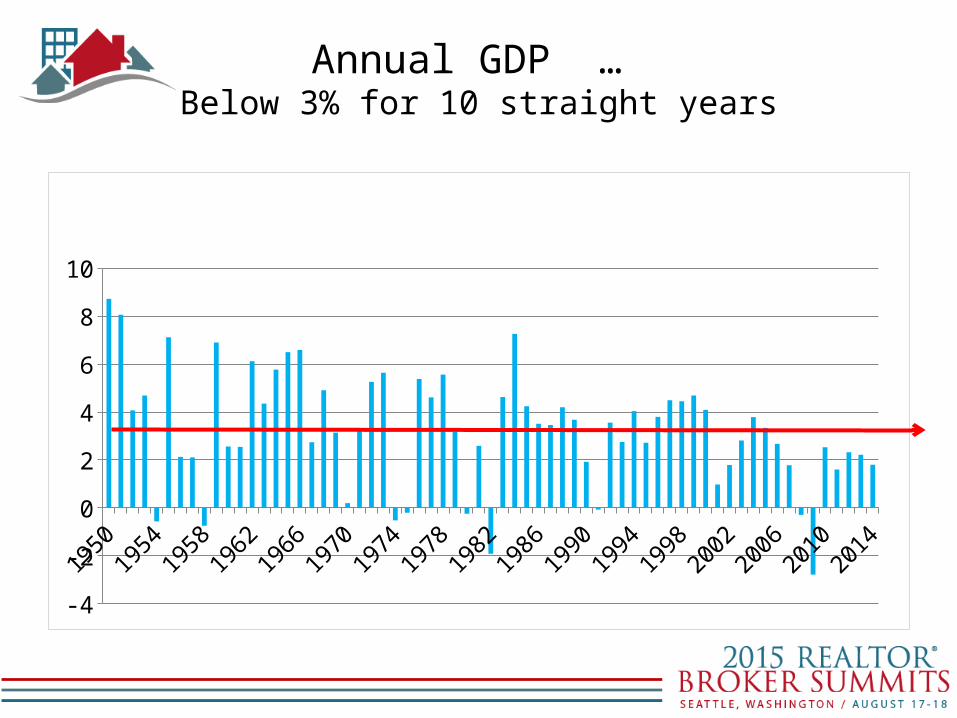

Annual GDP … Below 3% for 10 straight years

19501953

19561959

19621965

19681971

19741977

19801983

19861989

19921995

19982001

20042007

20102013

-4

-2

0

2

4

6

8

10

GDP Annual Growth Rate

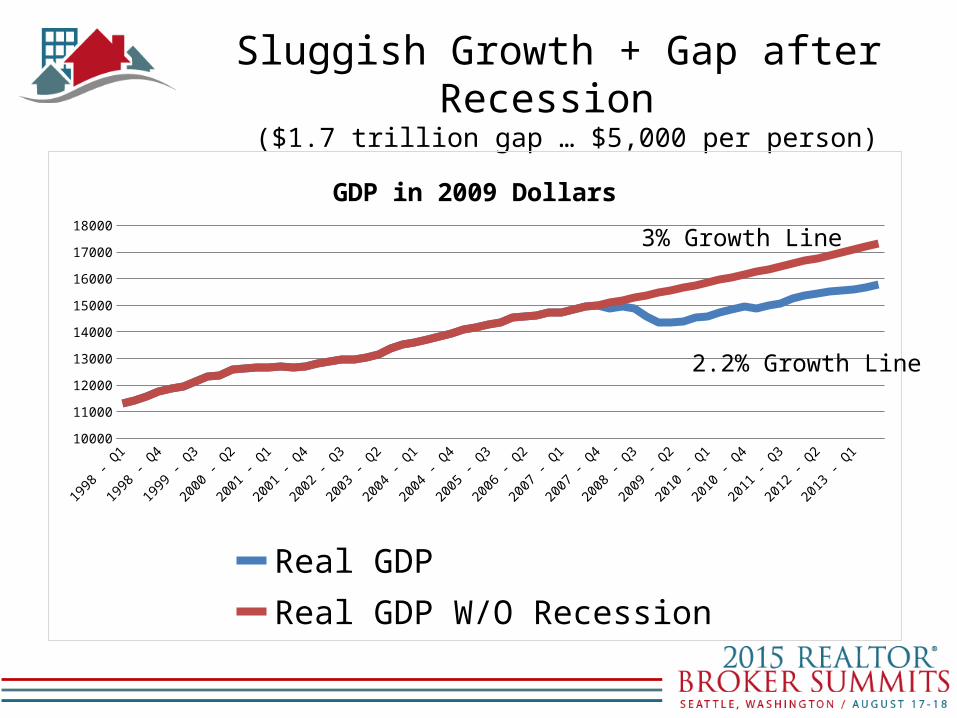

Sluggish Growth + Gap after Recession ($1.7 trillion gap … $5,000 per person)

1998 - Q1

1998 - Q3

1999 - Q1

1999 - Q3

2000 - Q1

2000 - Q3

2001 - Q1

2001 - Q3

2002 - Q1

2002 - Q3

2003 - Q1

2003 - Q3

2004 - Q1

2004 - Q3

2005 - Q1

2005 - Q3

2006 - Q1

2006 - Q3

2007 - Q1

2007 - Q3

2008 - Q1

2008 - Q3

2009 - Q1

2009 - Q3

2010 - Q1

2010 - Q3

2011 - Q1

2011 - Q3

2012 - Q1

2012 - Q3

2013 - Q1

2013 - Q3

10000

11000

12000

13000

14000

15000

16000

17000

18000

GDP in 2009 Dollars

Real GDP Real GDP W/O Recession

3% Growth Line

2.2% Growth Line

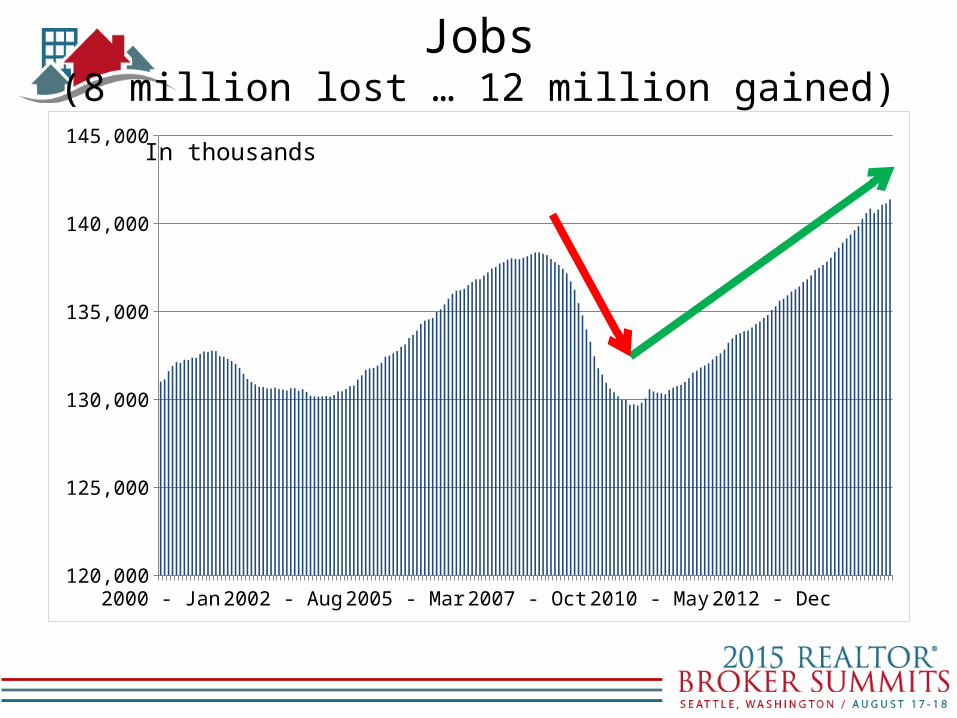

Jobs(8 million lost … 12 million gained)

2000 - Jan 2001 - Oct 2003 - Jul 2005 - Apr2007 - Jan 2008 - Oct 2010 - Jul 2012 - Apr2014 - Jan120,000

125,000

130,000

135,000

140,000

145,000In thousands

Fresh Unemployment Insurance Claims

2000 - Jan 2001 - Oct 2003 - Jul 2005 - Apr 2007 - Jan 2008 - Oct 2010 - Jul 2012 - Apr 2014 - Jan250

300

350

400

450

500

550

600In thousands

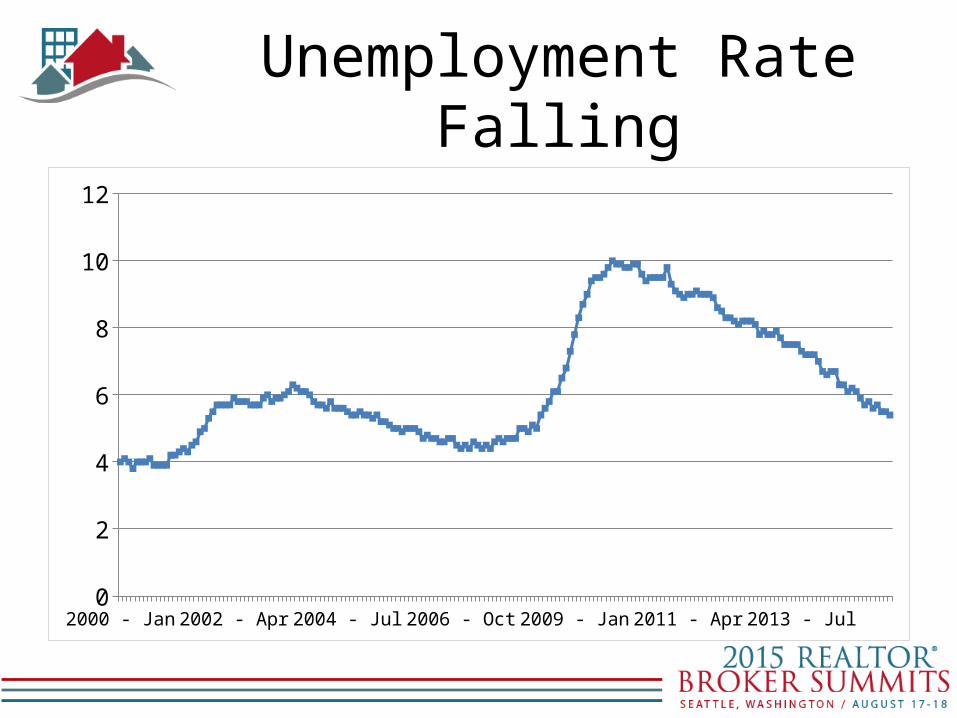

Unemployment Rate Falling

2000 - Jan 2001 - Oct 2003 - Jul 2005 - Apr 2007 - Jan 2008 - Oct 2010 - Jul 2012 - Apr 2014 - Jan0

2

4

6

8

10

12

But Employment Rate Not Rising

2000 - Jan 2001 - Oct 2003 - Jul 2005 - Apr 2007 - Jan 2008 - Oct 2010 - Jul 2012 - Apr 2014 - Jan54

56

58

60

62

64

66

Part-time Workers

2000 - Jan 2001 - Oct 2003 - Jul 2005 - Apr 2007 - Jan 2008 - Oct 2010 - Jul 2012 - Apr 2014 - Jan20000

21000

22000

23000

24000

25000

26000

27000

28000

29000In thousands

Wage Growth(% change from one year ago)

2000 - Jan 2001 - Oct 2003 - Jul 2005 - Apr 2007 - Jan 2008 - Oct 2010 - Jul 2012 - Apr 2014 - Jan0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

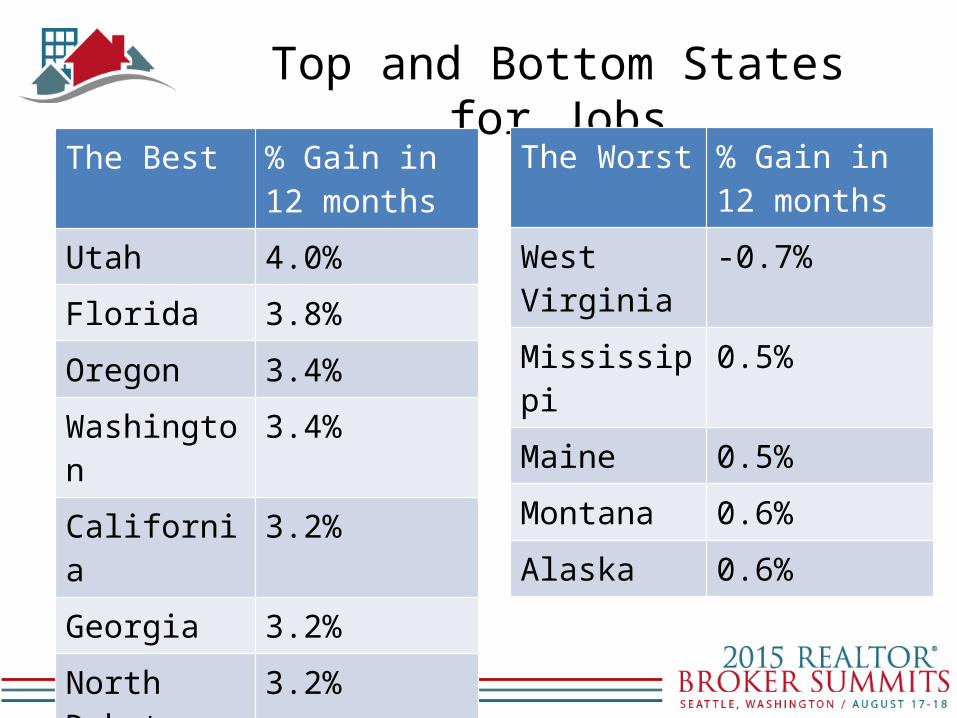

Top and Bottom States for JobsThe Best % Gain in 12

months

Utah 4.0%

Florida 3.8%

Oregon 3.4%

Washington 3.4%

California 3.2%

Georgia 3.2%

North Dakota 3.2%

Nevada 3.0%

Idaho 2.9%

The Worst % Gain in 12 months

West Virginia -0.7%

Mississippi 0.5%

Maine 0.5%

Montana 0.6%

Alaska 0.6%

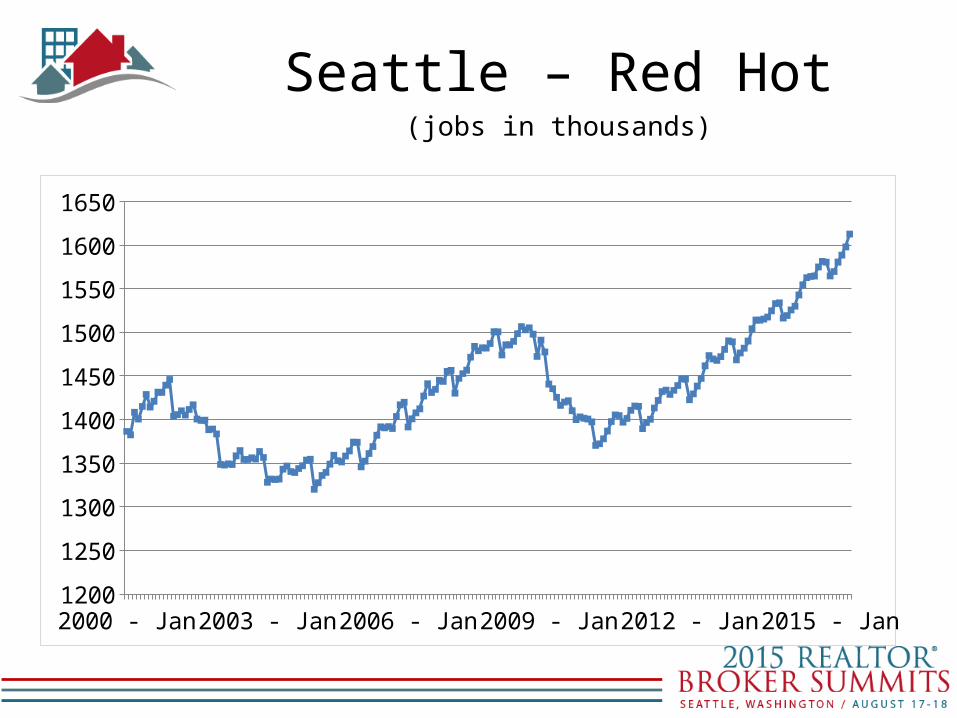

Seattle – Red Hot(jobs in thousands)

2000 - Jan 2002 - Jan 2004 - Jan 2006 - Jan 2008 - Jan 2010 - Jan 2012 - Jan 2014 - Jan1200

1250

1300

1350

1400

1450

1500

1550

1600

1650

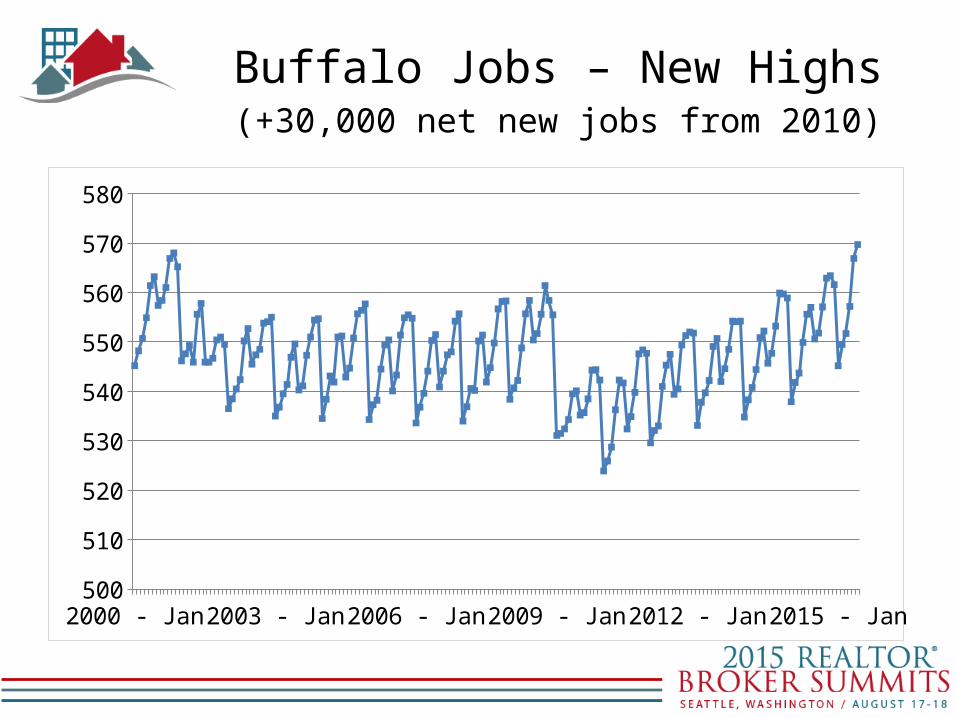

Lake Erie Downfall and Resurgence

Buffalo Jobs – New Highs(+30,000 net new jobs from 2010)

2000 - Jan 2002 - Jan 2004 - Jan 2006 - Jan 2008 - Jan 2010 - Jan 2012 - Jan 2014 - Jan500

510

520

530

540

550

560

570

580

Detroit Jobs(+300,000 net new jobs from 2010)

2000 - Jan 2002 - Jan 2004 - Jan 2006 - Jan 2008 - Jan 2010 - Jan 2012 - Jan 2014 - Jan1500

1600

1700

1800

1900

2000

2100

2200

2300

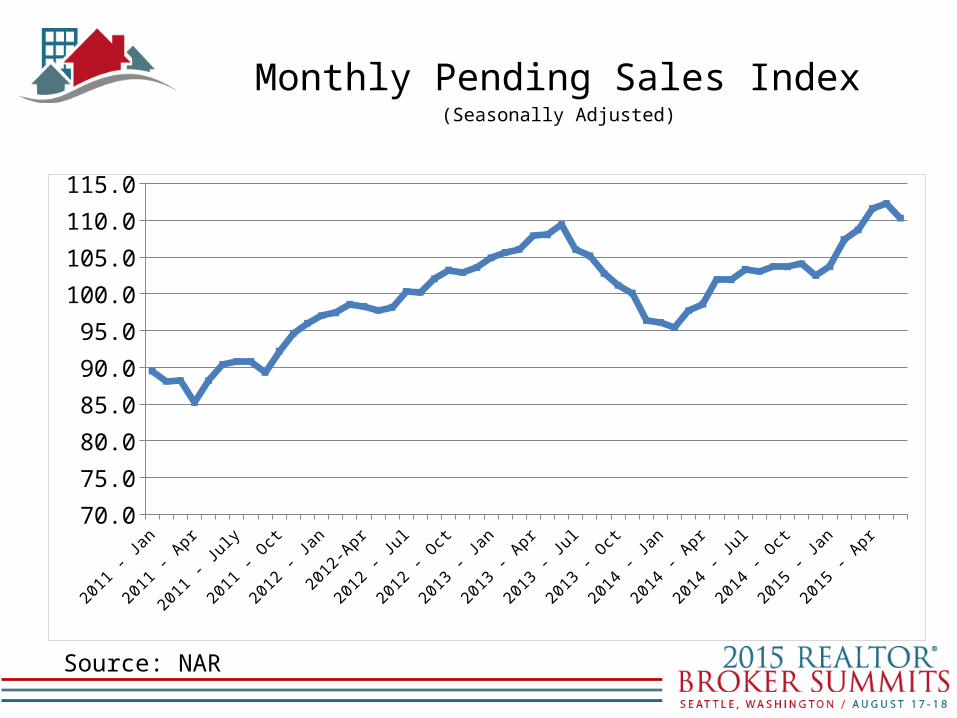

Monthly Pending Sales Index(Seasonally Adjusted)

2011 - Jan

2011 - Mar

2011 - May

2011 - July

2011 - Sep

2011 - Nov

2012 - Jan

2012- Mar

2012 - May

2012 - Jul

2012 - Sep

2012 - Nov

2013 - Jan

2013 - Mar

2013 - May

2013 - Jul

2013 - Sep

2013 - Nov

2014 - Jan

2014 - Mar

2014 - May

2014 - Jul

2014 - Sep

2014 - Nov

2015 - Jan

2015 - Mar

2015 - May

70.0

75.0

80.0

85.0

90.0

95.0

100.0

105.0

110.0

115.0

Source: NAR

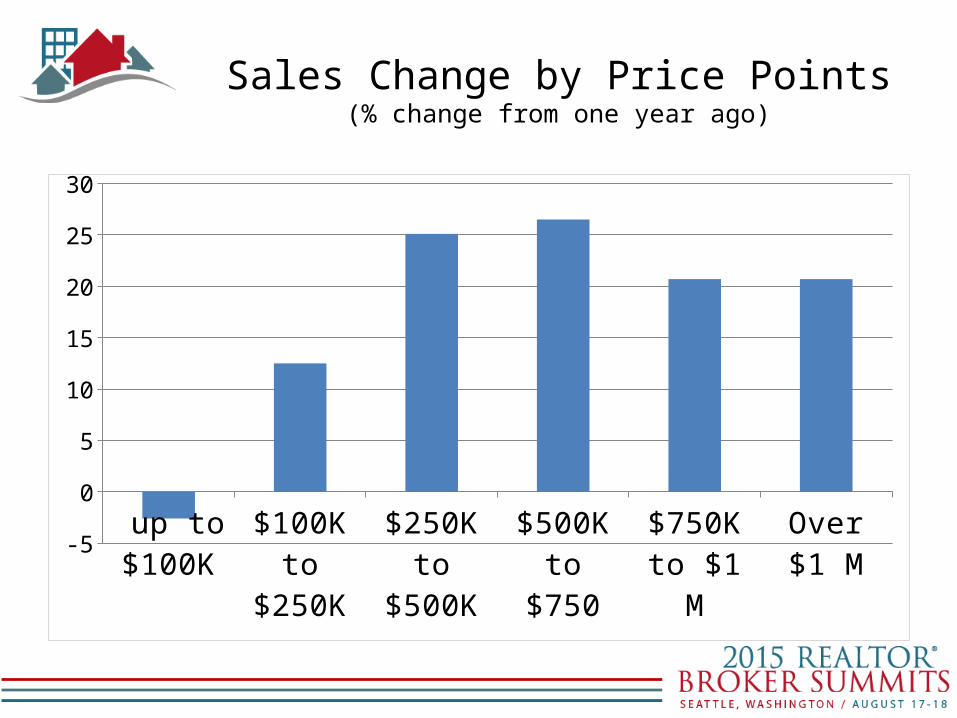

Sales Change by Price Points(% change from one year ago)

up to $100K

$100K to $250K

$250K to $500K

$500K to $750

$750K to $1 M

Over $1 M-5

0

5

10

15

20

25

30

Distressed Sales

2008 - Oct

2009 - Feb

2009 - Jun

2009 - Oct

2010 - Feb

2010 - Jun

2010 - Oct

2011 - Feb

2011 - Jun

2011 - Oct

2012 - Feb

2012 - Jun

2012 - Oct

2013 - Feb

2013 - Jun

2013 - Oct

2014 - Feb

2014 - Jun

2014 - Oct

2015 - Feb

2015 - Jun

0

10

20

30

40

50

60

Foreclosure Short-Sale

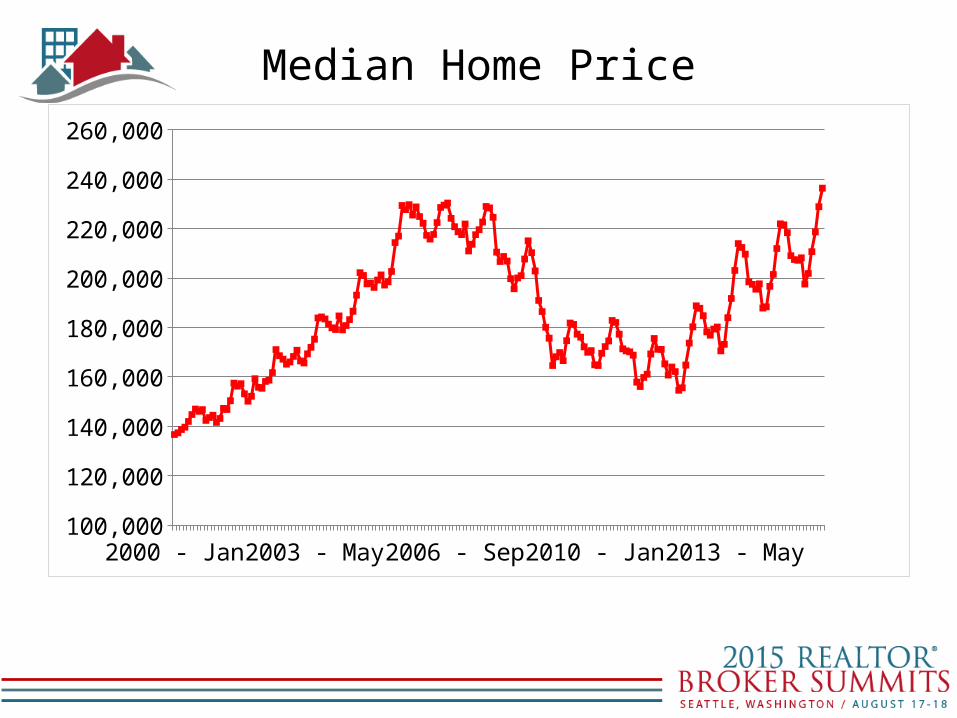

Median Home Price

2000 - Jan 2002 - Apr 2004 - Jul 2006 - Oct 2009 - Jan 2011 - Apr 2013 - Jul100,000

120,000

140,000

160,000

180,000

200,000

220,000

240,000

260,000

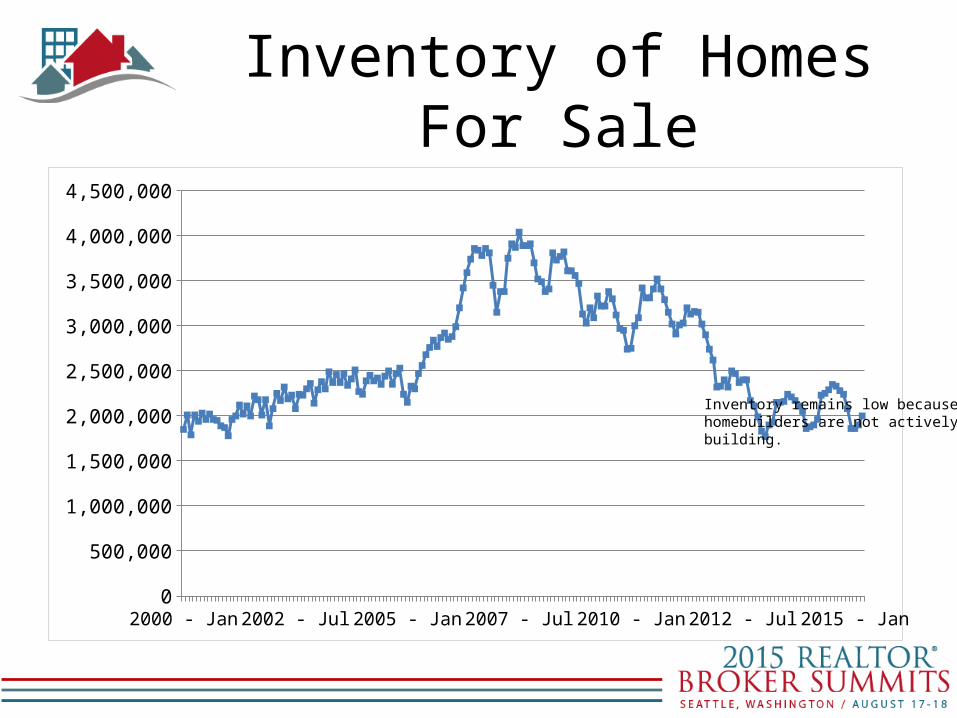

Inventory of Homes For Sale

2000 - Jan 2001 - Oct 2003 - Jul 2005 - Apr 2007 - Jan 2008 - Oct 2010 - Jul 2012 - Apr 2014 - Jan0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

Inventory remains low becausehomebuilders are not activelybuilding.

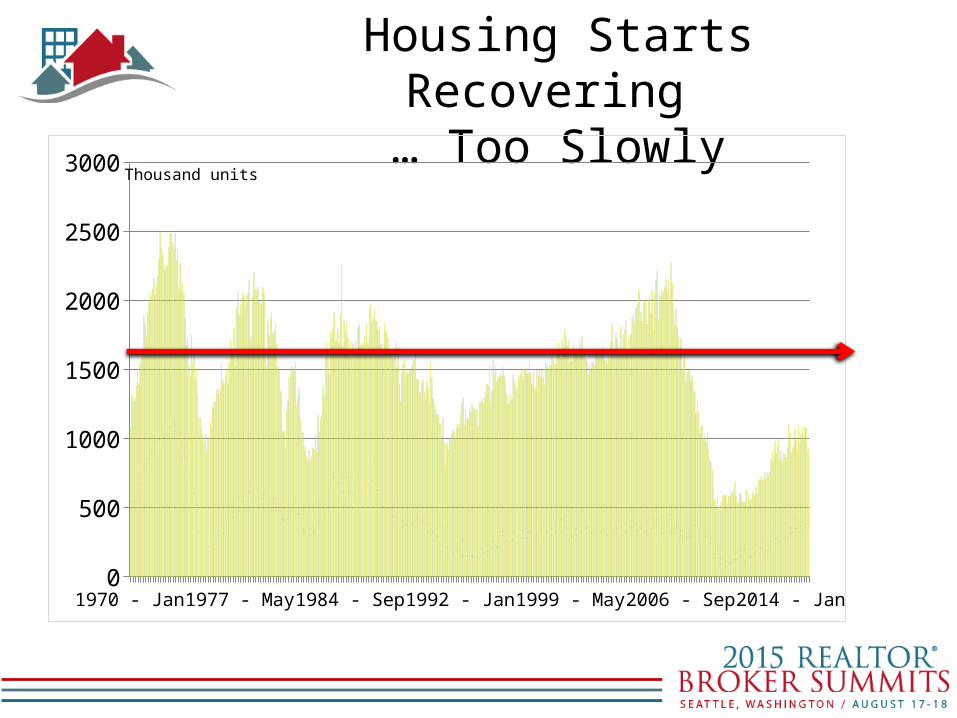

Housing Starts Recovering … Too Slowly

1970 - Jan 1975 - Jul 1981 - Jan 1986 - Jul 1992 - Jan 1997 - Jul 2003 - Jan 2008 - Jul 2014 - Jan0

500

1000

1500

2000

2500

3000Thousand units

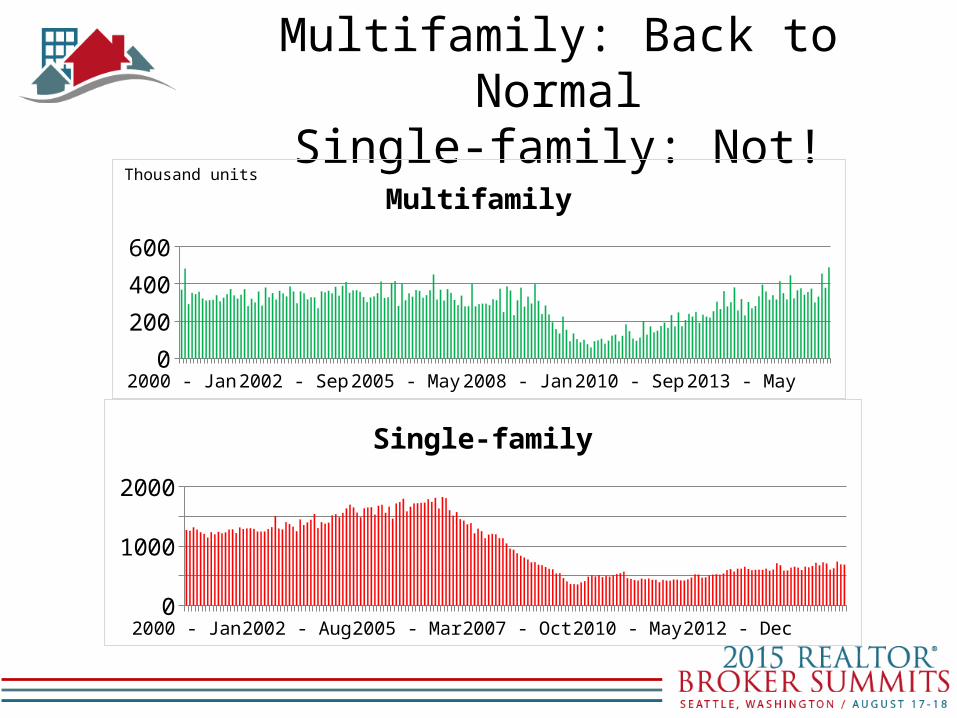

Multifamily: Back to NormalSingle-family: Not!

2000 - Jan 2002 - Jan 2004 - Jan 2006 - Jan 2008 - Jan 2010 - Jan 2012 - Jan 2014 - Jan0

200

400

600

MultifamilyThousand units

2000 - Jan 2002 - Jan 2004 - Jan 2006 - Jan 2008 - Jan 2010 - Jan 2012 - Jan 2014 - Jan0

500100015002000

Single-family

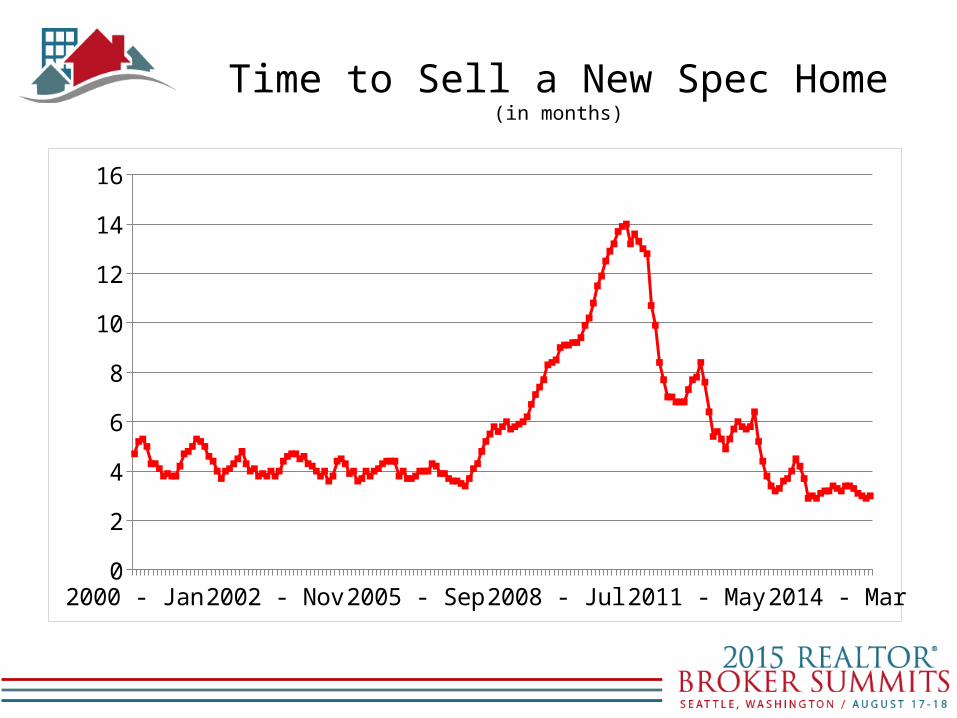

Time to Sell a New Spec Home(in months)

2000 - Jan 2002 - Jan 2004 - Jan 2006 - Jan 2008 - Jan 2010 - Jan 2012 - Jan 2014 - Jan0

2

4

6

8

10

12

14

16

Seattle Single-family Housing Permits

20002001

20022003

20042005

20062007

20082009

20102011

20122013

20142015

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

Buyer Traffic Conditions

New Consumer Survey

Trade-Up Opportunitiesfrom Housing Equity

2000 - Q1

2000 - Q4

2001 - Q3

2002 - Q2

2003 - Q1

2003 - Q4

2004 - Q3

2005 - Q2

2006 - Q1

2006 - Q4

2007 - Q3

2008 - Q2

2009 - Q1

2009 - Q4

2010 - Q3

2011 - Q2

2012 - Q1

2012 - Q4

2013 - Q3

2014 - Q2

2015 - Q1

0

5000

10000

15000

20000

25000

Real Estate Value Mortgage Debt

$ billion

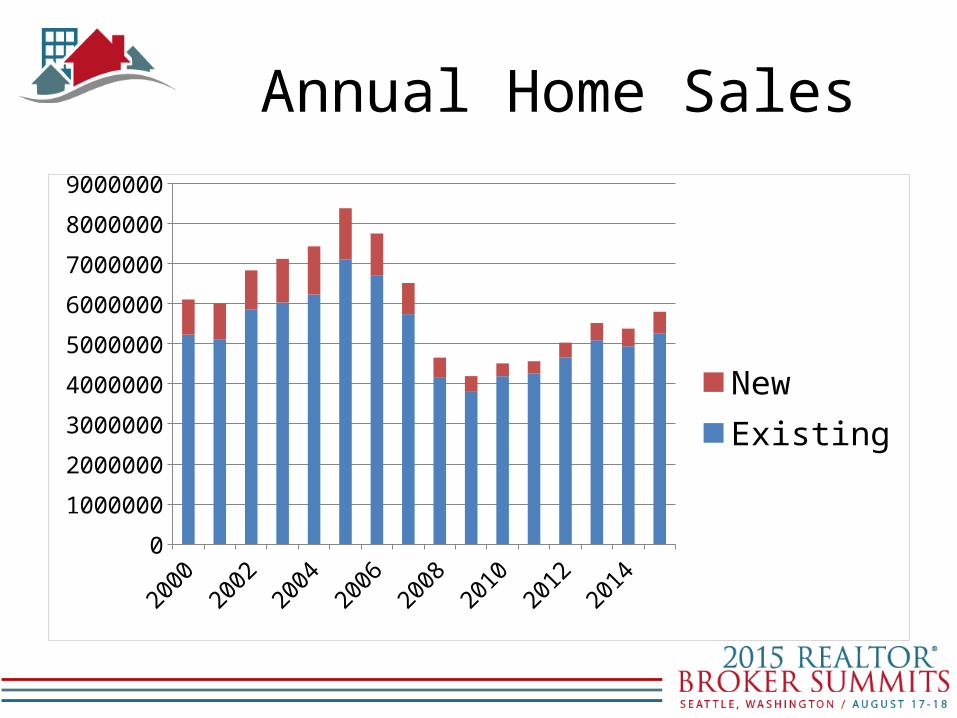

Annual Home Sales

20002001

20022003

20042005

20062007

20082009

20102011

20122013

20142015

0

1000000

2000000

3000000

4000000

5000000

6000000

7000000

8000000

9000000

NewExisting

New Price Bubble?

2005-2006 Bubble

• 7.2 m existing home sales

• 1.3 m new home sale

• Loose Credit

• 2.1 m housing starts

2015

• 5.3 m existing home sales

• 0.6 m new home sales

• Tight Credit and all-cash

• 1.1 m housing starts

Home Price Forecast for 2016 … 3% to 5%

First Scenario

• New construction slowly recover … housing shortage

• Prices initially rise fast

• Chokes demand and sales fall

• Home price grows 3% to 5%

• Not Desirable

Second Scenario

• New construction robustly recover … inventory relief

• Home price grows 3% to 5%

• Demand expands and sales rise

• Increase mobility and boost jobs

• Desirable

Monetary Policy andForecast

Fed Policy and Mortgage Rate

2000 - Jan 2002 - Jan 2004 - Jan 2006 - Jan 2008 - Jan 2010 - Jan 2012 - Jan 2014 - Jan0

1

2

3

4

5

6

7

8

9

Mortgage Rate Fed Funds Rate

What Determines Bond Yields?

• Federal Reserve’s short-term rate changes• Inflation and erosion of purchasing power• Foreign capital flow and demand for dollar• Savings rate• U.S. budget deficit• Printing of money• …

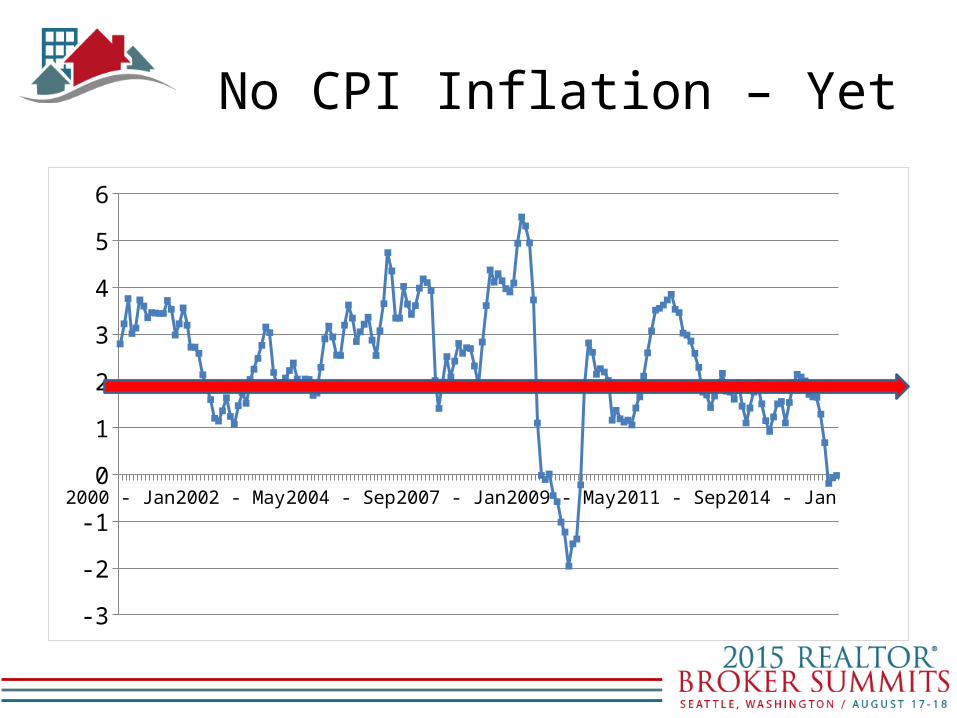

No CPI Inflation – Yet

2000 - Jan 2001 - Oct 2003 - Jul 2005 - Apr 2007 - Jan 2008 - Oct 2010 - Jul 2012 - Apr 2014 - Jan

-3

-2

-1

0

1

2

3

4

5

6

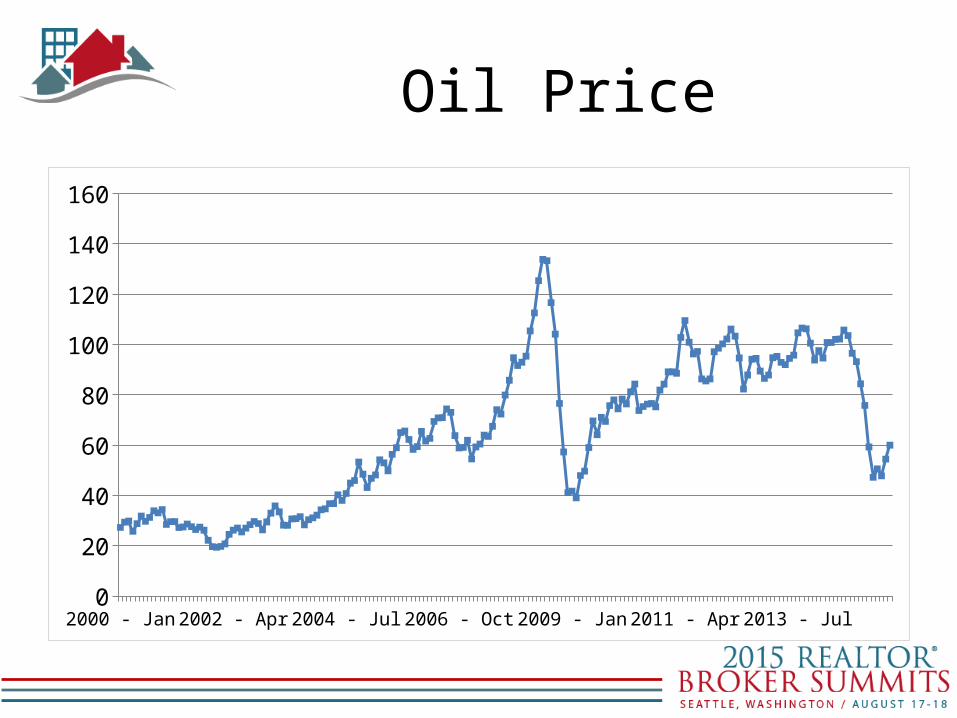

Oil Price

2000 - Jan 2001 - Oct 2003 - Jul 2005 - Apr 2007 - Jan 2008 - Oct 2010 - Jul 2012 - Apr 2014 - Jan0

20

40

60

80

100

120

140

160

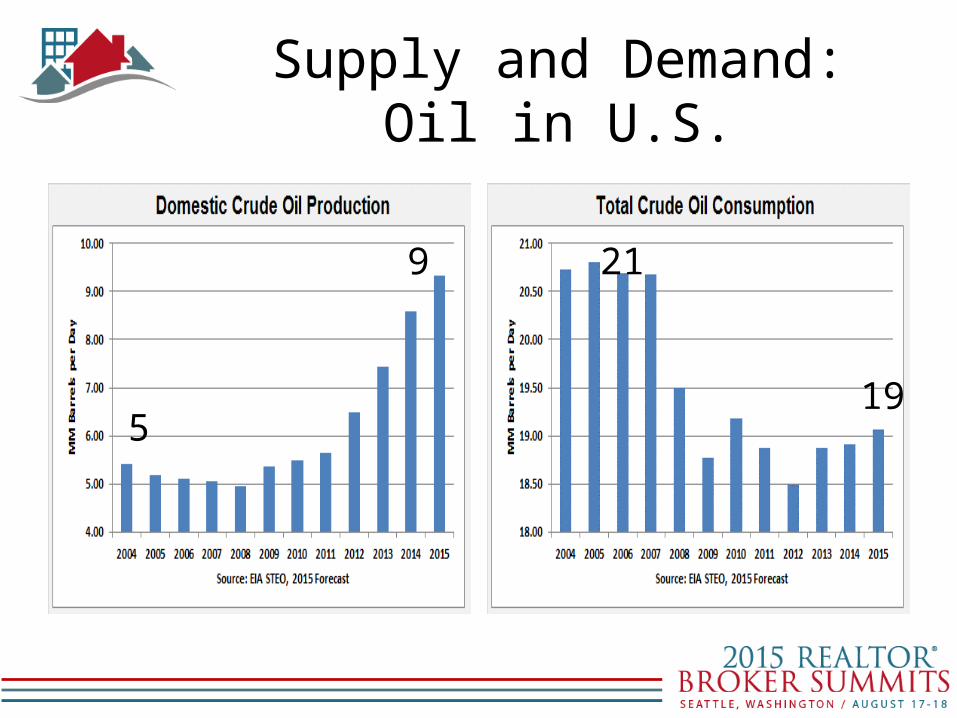

Supply and Demand: Oil in U.S.

19

21

5

9

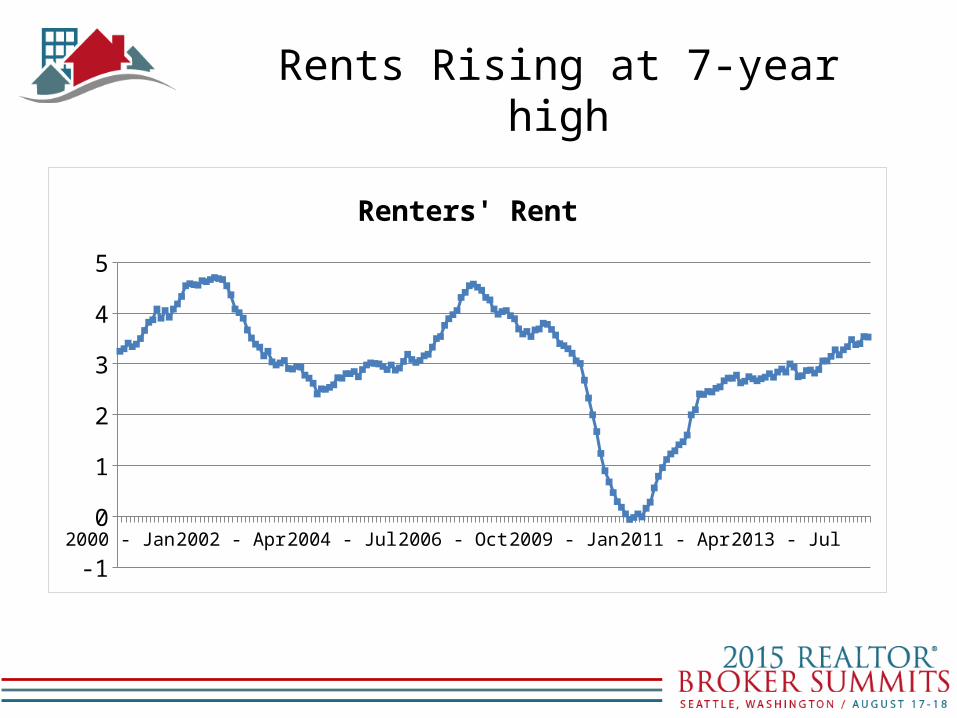

Rents Rising at 7-year high

2000 - Jan 2001 - Oct 2003 - Jul 2005 - Apr 2007 - Jan 2008 - Oct 2010 - Jul 2012 - Apr 2014 - Jan

-1

0

1

2

3

4

5

Renters' Rent

Rental Vacancy Rate(Census Measurement)

2000 - Q1

2000 - Q4

2001 - Q3

2002 - Q2

2003 - Q1

2003 - Q4

2004 - Q3

2005 - Q2

2006 - Q1

2006 - Q4

2007 - Q3

2008 - Q2

2009 - Q1

2009 - Q4

2010 - Q3

2011 - Q2

2012 - Q1

2012 - Q4

2013 - Q3

2014 - Q2

2015 - Q1

5

6

7

8

9

10

11

12

Rents will continue to rise because of historic low vacancy rate.

Monetary Policy

• Quantitative Easing … Finished

• Fed Funds Rate hike … September/October

• 10-year Treasury reaching – 2.5% by end of 2015 – 3.5% by end of 2016

Credit Box Opens?• FICO New Method• Fannie/Freddie

– Lower down payment products• FHA premiums … lowered • Portfolio Lending … historic low mortgage

default rates on recent vintages (2010-2014)

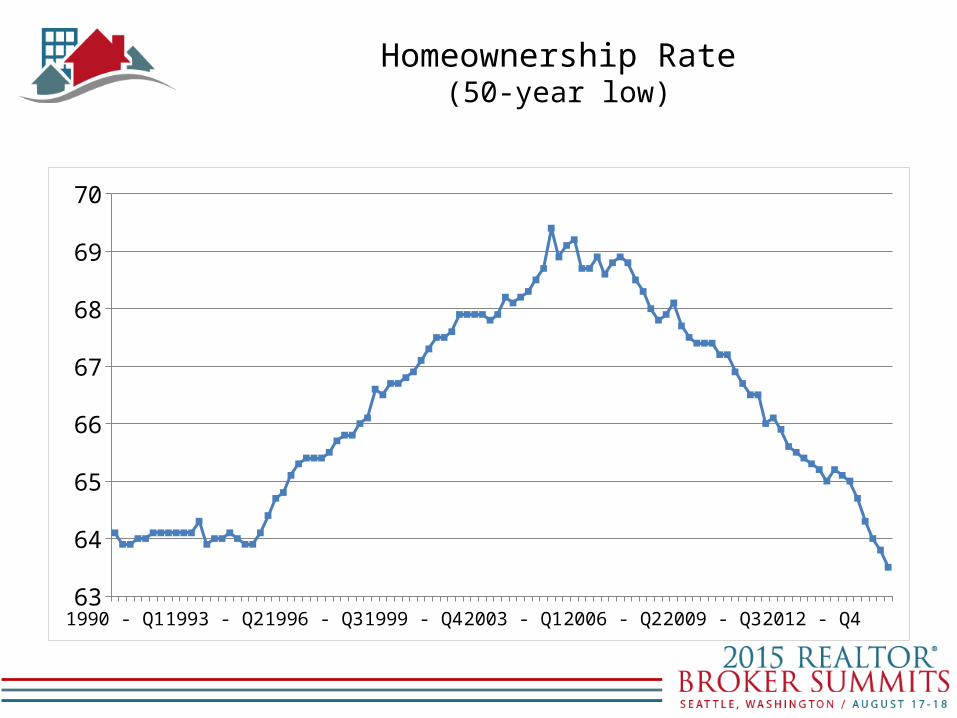

American Inequality?

Homeownership Rate(50-year low)

1990 - Q1 1992 - Q4 1995 - Q3 1998 - Q2 2001 - Q1 2003 - Q4 2006 - Q3 2009 - Q2 2012 - Q1 2014 - Q463

64

65

66

67

68

69

70

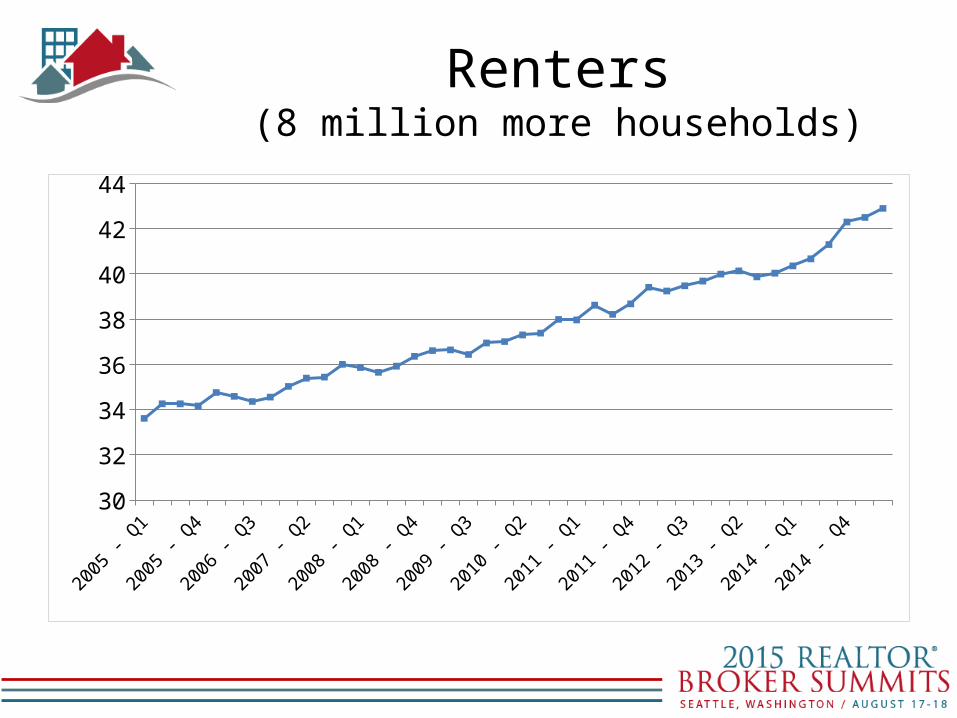

Renters(8 million more households)

2005 - Q1

2005 - Q3

2006 - Q1

2006 - Q3

2007 - Q1

2007 - Q3

2008 - Q1

2008 - Q3

2009 - Q1

2009 - Q3

2010 - Q1

2010 - Q3

2011 - Q1

2011 - Q3

2012 - Q1

2012 - Q3

2013 - Q1

2013 - Q3

2014 - Q1

2014 - Q3

2015 - Q1

30

32

34

36

38

40

42

44

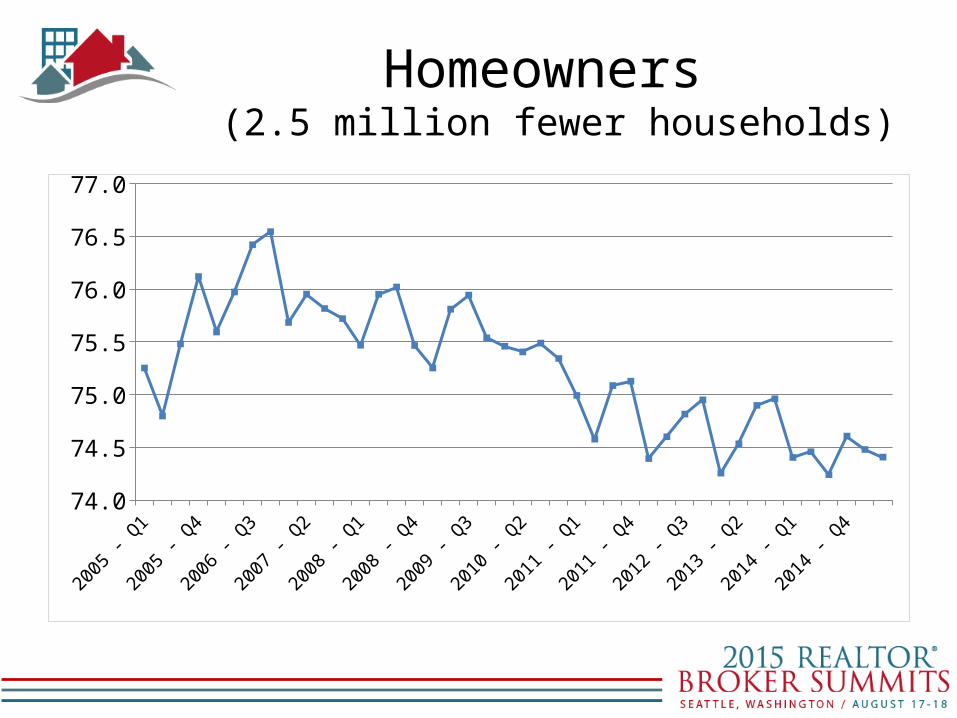

Homeowners (2.5 million fewer households)

2005 - Q1

2005 - Q3

2006 - Q1

2006 - Q3

2007 - Q1

2007 - Q3

2008 - Q1

2008 - Q3

2009 - Q1

2009 - Q3

2010 - Q1

2010 - Q3

2011 - Q1

2011 - Q3

2012 - Q1

2012 - Q3

2013 - Q1

2013 - Q3

2014 - Q1

2014 - Q3

2015 - Q1

74.0

74.5

75.0

75.5

76.0

76.5

77.0

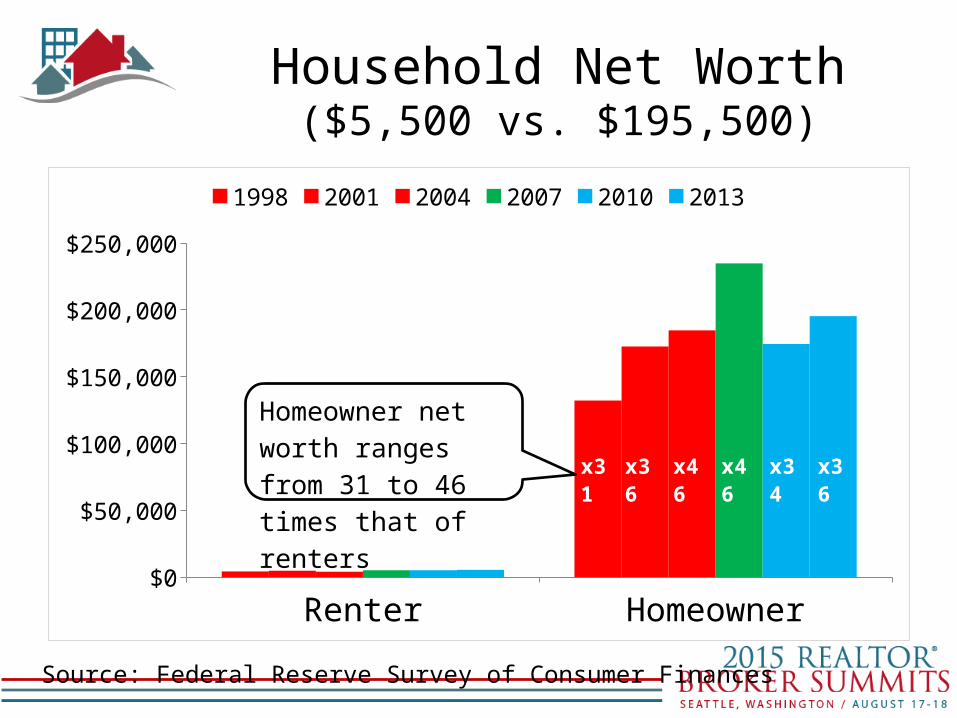

Household Net Worth($5,500 vs. $195,500)

Renter Homeowner$0

$50,000

$100,000

$150,000

$200,000

$250,000

1998 2001 2004 2007 2010 2013

x31 x46x36 x34x46

Homeowner net worth ranges from 31 to 46 times that of renters x36

Source: Federal Reserve Survey of Consumer Finances

Stock MarketS&P 500 Index

2000 - Jan 2002 - Jan 2004 - Jan 2006 - Jan 2008 - Jan 2010 - Jan 2012 - Jan 2014 - Jan700

900

1100

1300

1500

1700

1900

2100

2300

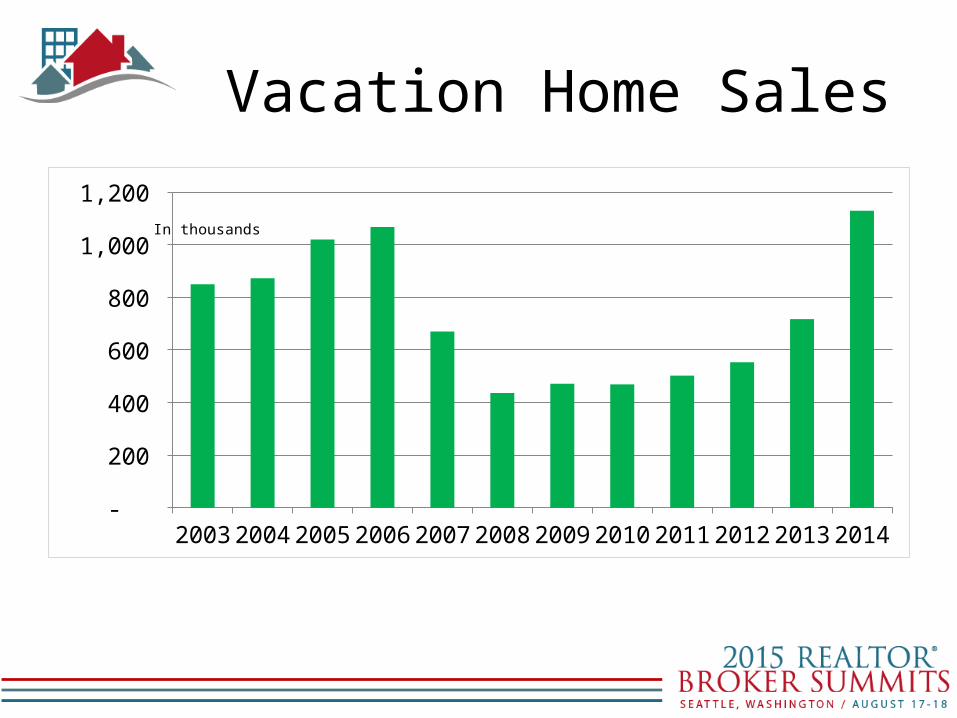

Vacation Home Sales

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 -

200

400

600

800

1,000

1,200

In thousands

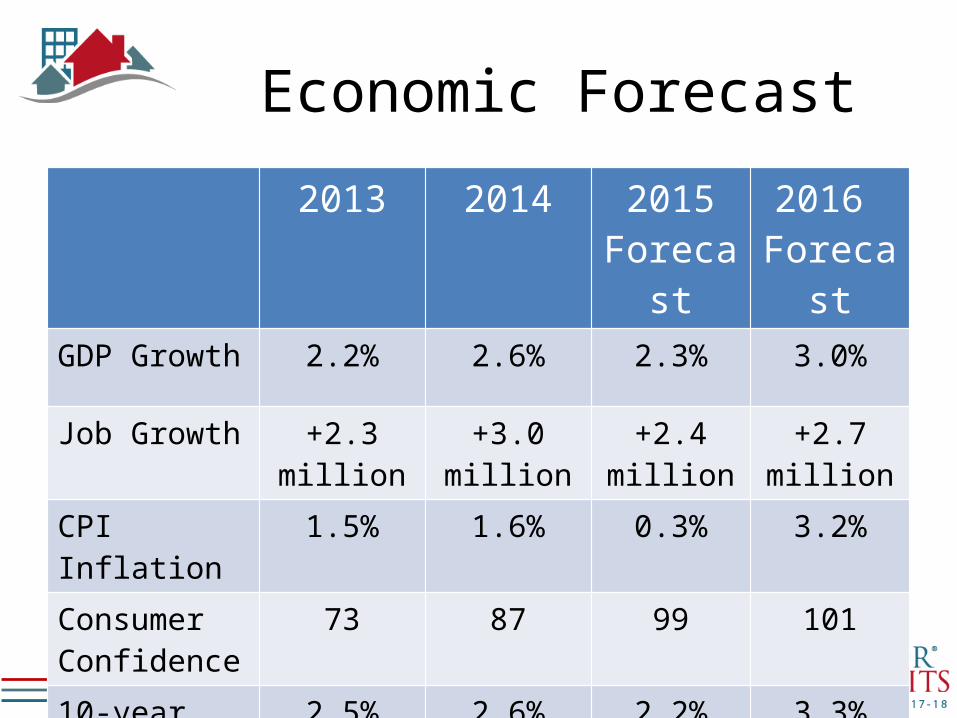

Forecast and Risks

Economic Forecast2013 2014 2015

Forecast2016

ForecastGDP Growth 2.2% 2.6% 2.3% 3.0%

Job Growth +2.3 million +3.0 million +2.4 million

+2.7 million

CPI Inflation 1.5% 1.6% 0.3% 3.2%

Consumer Confidence

73 87 99 101

10-year Treasury

2.5% 2.6% 2.2% 3.3%

Housing Forecast

2013 2014 2015Forecast

2016 Forecast

Housing Starts 925,000 1 million 1.1 million 1.4 million

New Home Sales

430,000 437,000 570,000 720,000

Existing Home Sales

5.1 million 4.9 million 5.3 million 5.5 million

Median Price Growth

+ 11.5% + 5.7% + 6% + 4%

30-year Rate 4.0% 4.2% 4.0% 5.2%

Underwriting Standards

Strict Strict Transition Normal

Washington Risks

• TRID?• Mortgage Availability?• Tax Preference Changes?

State and Local Risks• Foreclosure rules?• Eminent Domain?• Tax Preference Changes?

Commercial Real Estate

Commercial Investment Sales of Large Properties(Properties valued at $2.5 million and over)

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

130

212

362

423

571

174

67

147

233

299355

424470

500

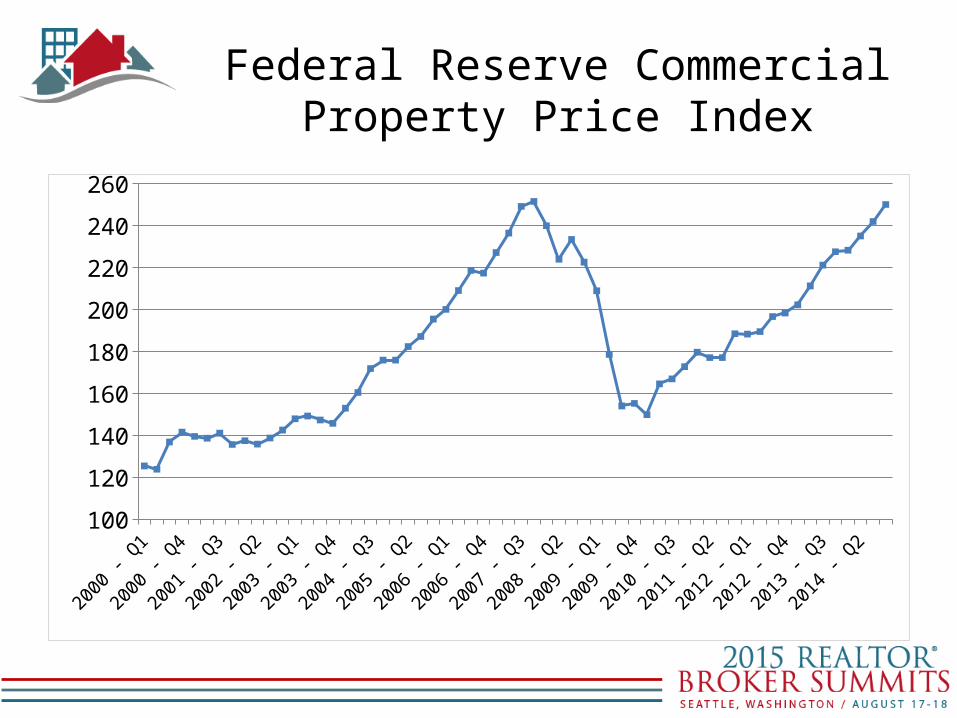

Federal Reserve Commercial Property Price Index

2000 - Q1

2000 - Q4

2001 - Q3

2002 - Q2

2003 - Q1

2003 - Q4

2004 - Q3

2005 - Q2

2006 - Q1

2006 - Q4

2007 - Q3

2008 - Q2

2009 - Q1

2009 - Q4

2010 - Q3

2011 - Q2

2012 - Q1

2012 - Q4

2013 - Q3

2014 - Q2

100

120

140

160

180

200

220

240

260

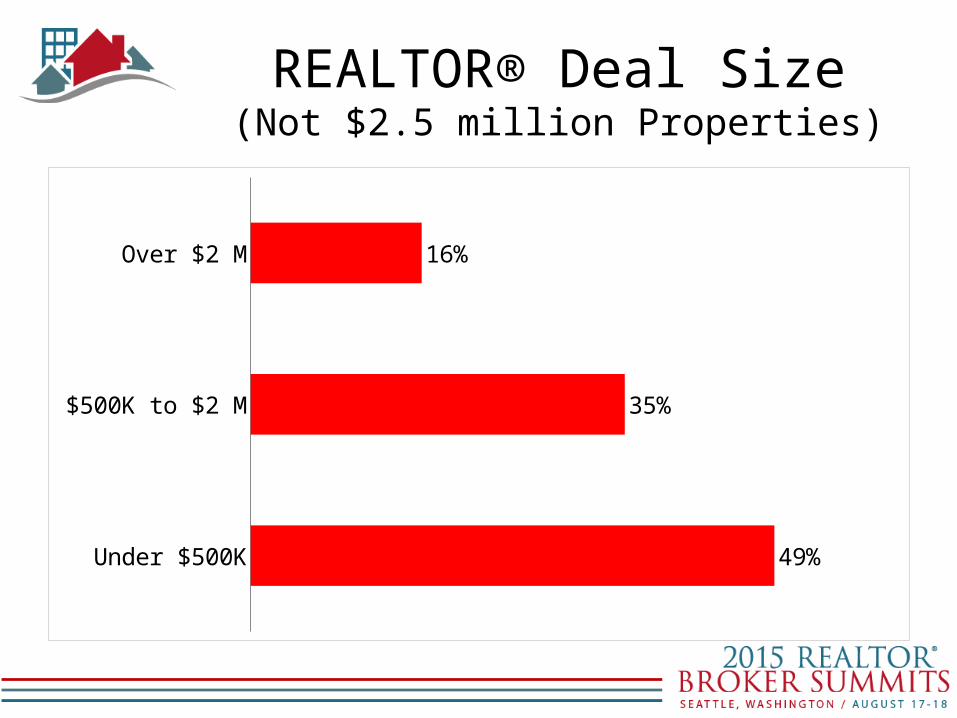

REALTOR® Deal Size(Not $2.5 million Properties)

Under $500K

$500K to $2 M

Over $2 M

49%

35%

16%

8%

17%

25%

7%

6%

4%

18%

1% 11%

3%National banks (“Big four”)

Regional banks

Local banks

Credit unions

Life insurance companies

REITs

Private investors

Public companies

Small Business Administration

Other, please specify

Source: NAR

Sources of Financing for Deals

Dodd-Frank?

• Big homebuilders in the game• Small homebuilders not really in the game

• Big commercial deals happening• Small commercial deals slowly happening

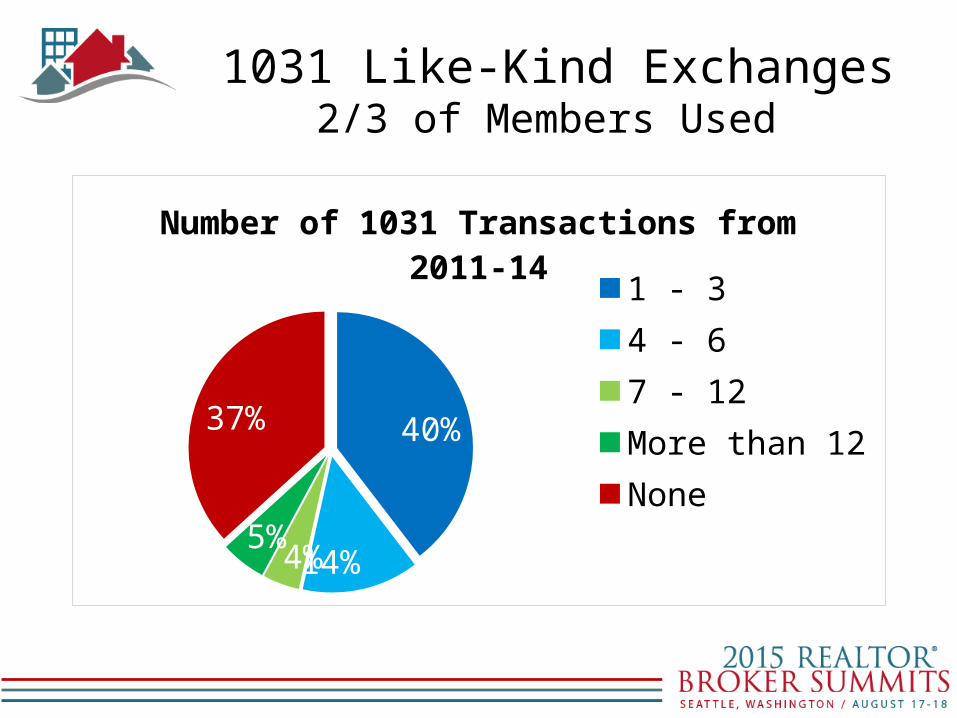

1031 Like-Kind Exchanges2/3 of Members Used

40%

14%4%5%

37%

Number of 1031 Transactions from 2011-14

1 - 34 - 67 - 12More than 12None

Recommended