Copyright © 2004 South-Western. All rights reserved. PowerPoint Presentation by Charlie Cook

Copyright © 2004 South-Western. All rights reserved. 10–2

ObjectivesAfter studying this chapter, you should be able to:

1. Discuss the basic requirements for successful implementation of incentive programs.

2. Identify the types of, and reasons for implementing, individual incentive plans.

3. Explain why merit raises may fail to motivate employees adequately and discuss ways to increase their motivational value.

4. Indicate the advantage of each of the principal methods used to compensate salespeople.

Copyright © 2004 South-Western. All rights reserved. 10–3

Objectives (cont’d)After studying this chapter, you should be able to:

5. Differentiate how gains may be shared with employees under the Scanlon, Rucker, Improshare, and earnings-at-risk gainsharing systems.

6. Differentiate between profit-sharing plans and explain advantages and disadvantages of these programs.

7. Describe the main types of ESOP plans and discuss the advantages of ESOP to employers and employees.

Copyright © 2004 South-Western. All rights reserved. 10–4

Strategic Reasons for Incentive Plans

• Variable PayTying pay to some measure of individual, group, or

organizational performance.

• Incentive Pay ProgramsEstablish a performance “threshold” to qualify for

incentive payments.Emphasize a shared focus on organizational

objectives.Create shared commitment in that every individual

contributes to organizational performance and success.

Copyright © 2004 South-Western. All rights reserved. 10–5

Advantages of Incentive Pay Programs

• Incentives are most useful when:Focused on key performance targets that produce

employee and organizational gains.

Variable costs of payouts are linked to the achievement of competitively important results.

Directly relating payouts to achieving operating performance objectives (quantity and/or quality).

Teamwork and unit cohesiveness are fostered by basing payments to individuals on team results.

Used to distribute success among those responsible for producing that success.

Figure 10.1Presentation Slide 10–1

Copyright © 2004 South-Western. All rights reserved. 10–6

Employee Opposition to Incentive Plans

• Production standards are set unfairly.• Incentive plans are really “work speedup.”• Incentive plans create competition among

workers.• Increased earnings result in tougher standards.• Payout formulas are complex and difficult to

understand.• Incentive plans cause friction between

employees and management.

Presentation Slide 10–2

Copyright © 2004 South-Western. All rights reserved. 10–7

Types of Incentive Plans

INDIVIDUAL GROUP ENTERPRISE

Piecework Team compensation Profit sharing

Standard hour plan Scanlon Plan Stock options

Bonuses Rucker Plan Employee stockMerit pay Improshare ownership plans

Lump-sum merit pay Earnings-at-risk plans (ESOPs)

Sales incentives

Incentives for professional employees

Executive compensation

Figure 10.1Presentation Slide 10–3

Copyright © 2004 South-Western. All rights reserved. 10–8

Successful Incentive Plans

• Employees have a desire for an incentive plan.

• Employees are encouraged to participate.

• Employees see a clear connection between the incentive payments they receive and their job performance.

• Employees are committed to meeting the standards.

• Standards are challenging but achievable.

• Payout formulas are simple and understandable.

• Payouts are a separate, distinct part of compensation.

Copyright © 2004 South-Western. All rights reserved. 10–9

Assessing Incentive Program Effectiveness

HRM 1Source: Christian M. Ellis and Cynthia L. Paluso, “Blazing a Trail to Broad-Based Incentives,” WorldatWork Journal 9, no. 4 (Fourth Quarter 2000): 33–41. Used with permission, WorldatWork, Scottsdale, Arizona.

Copyright © 2004 South-Western. All rights reserved. 10–10

Setting Performance Measures—the Keys

• Managers or supervisors should:

Ensure that performance measures are consistent with the strategic goals of the organization.

Define the intent of performance measures and champion the cause relentlessly.

Involve employees at all levels.

Consider the organization’s culture and workforce demographics.

Widely communicate the importance of performance measures.

HRM 2Source: Source: Adapted from Christian M. Ellis, “Improving the Impact of Performance Management,” Workspan 45, no. 2 (February 2002): 7–8.

Copyright © 2004 South-Western. All rights reserved. 10–11

Effective Incentive Plan Administration

• Grant incentives based on individual performance differences.

• Have the financial resources to reward performance.

• Set clearly defined, accepted, and challenging yet achievable performance standards.

• Use an easily understood payout formula

• Keep administrative costs reasonable.

• Do not “ratchet up” performance standards.

Copyright © 2004 South-Western. All rights reserved. 10–12

Individual Incentive Plans

• Straight PieceworkAn incentive plan under which employees receive a

certain rate for each unit produced.

• Differential Piece RateA compensation rate under which employees whose

production exceeds the standard amount of output receive a higher rate for all of their work than the rate paid to those who do not exceed the standard amount.

Copyright © 2004 South-Western. All rights reserved. 10–13

Computing the Piece Rate

hourper units 5 unit)per time(standard minutes 12

hour)(per minutes 60=

unitper $1.50 hour)(per units 5

rate)(hourly $7.50=

Copyright © 2004 South-Western. All rights reserved. 10–14

Piecework drawbacks

• Problems with piecework systems:Piecework standards can be difficult to develop. Individual contributions can be difficult measure.Not easily applied to work that is highly mechanized

with little employee control over output.Piecework may conflict with organizational culture

(teamwork) and/or group norms (“rate busting”).When quality is more important than quantity.When technology changes are frequent.When cross-training is required for scheduling

flexibility.

Copyright © 2004 South-Western. All rights reserved. 10–15

Individual Incentive Plans:

• Standard hour planAn incentive plan that sets pay rates based on the

completion of a job in a predetermined “standard time.” If employees finish the work in less than the expected

time, their pay is still based on the standard time for the job multiplied by their hourly rate.

Copyright © 2004 South-Western. All rights reserved. 10–16

Bonuses

• Bonus Incentive payment that is supplemental to the

base wage for cost reduction, quality improvement, or other performance criteria.

• Spot bonusUnplanned bonus given for employee effort

unrelated to an established performance measure.

Copyright © 2004 South-Western. All rights reserved. 10–17

Merit Pay

• Merit Pay Program (merit raise)Links an increase in base pay to how successfully an

employee achieved some objective performance standard.

• Merit GuidelinesGuidelines for awarding merit raises that are tied to

performance objectives.

Copyright © 2004 South-Western. All rights reserved. 10–18

Merit Pay Guidelines Chart

HRM 3

QUINTILE (POSITION IN RANGE),%

PERFORMANCE LEVEL 1 2 3 4 5

Outstanding (5) 9 9 8 7 6

Superior (4) 7 7 6 5 4

Competent (3) 5 5 4 3 3

Needs improvement (2) 0 0 0 0 0

Unsatisfactory (1) 0 0 0 0 0

MERIT PAY GUIDE CHART

Copyright © 2004 South-Western. All rights reserved. 10–19

Problems with Merit Raises

• Inadequate funding for merit increases.

• Vagueness in how to define and measure performance.

• Employees not believing that merit compensation is tied to effort and performance

• Allowing organizational politics to influence merit pay decisions.

• Failing to differentiate between merit pay and other types of pay increases.

• Mistrust between management and employees.

• An “overall” merit pay plan that does not motivate.

Copyright © 2004 South-Western. All rights reserved. 10–20

Motivation Through Merit Raises

• Develop employee confidence and trust in performance appraisal.

• Establish job-related performance criteria.

• Separate merit pay from regular pay.

• Distinguish merit raises from cost-of-living raises.

• Withhold merit payments when performance declines.

Presentation Slide 10–4

Copyright © 2004 South-Western. All rights reserved. 10–21

Lump-Sum Merit Pay

• Lump-sum Merit ProgramProgram under which employees receive a year-end

merit payment, which is not added to their base pay.Advantages

Provides financial control by maintaining annual salary expenses and not escalating base salary levels.

Contains employee benefit costs for levels of benefits normally calculated from current salary levels.

Provides a clear link between pay and performance.

Copyright © 2004 South-Western. All rights reserved. 10–22

Sales Incentives

Straight CommissionStraight Commission

Sales Incentive PlansSales Incentive Plans

Straight SalaryStraight Salary

Salary and CommissionSalary and CommissionCombinationsCombinations

Copyright © 2004 South-Western. All rights reserved. 10–23

Incentive Plans for Salespersons

• Straight Salary PlanCompensation plan that permits salespeople to be

paid for performing various duties that are not reflected immediately in their sales volume.

Encourages building customer relationships.

Provides compensation during periods of poor sales.

May not provide sufficient motivation for maximizing sales volume.

Copyright © 2004 South-Western. All rights reserved. 10–24

Incentive Plans for Salespersons

• Straight Commission PlanCompensation plan based upon a percentage of

sales.Disadvantages

Emphasis is on sales volume rather than on profits.

Customer service after the sale is neglected.

Earnings tend to fluctuate widely between good and poor periods of business.

Temptation to grant price concessions to get sales.

Copyright © 2004 South-Western. All rights reserved. 10–25

Incentive Plans for Salespersons

• Combined Salary and Commission PlanA compensation plan that includes a straight salary

and a commission component (“leverage”).Advantages

Combines the advantages of straight salary and straight commission forms of compensation.

Offers greater design flexibility to develop the most favorable ratio of selling expense to sales.

Motivates sales force to achieve specific company marketing objectives in addition to sales volume.

Copyright © 2004 South-Western. All rights reserved. 10–26

Incentives for Professional Employees

Profit sharing and stock ownershipProfit sharing and stock ownershipProfit sharing and stock ownershipProfit sharing and stock ownership

Double-track wage systemsDouble-track wage systemsDouble-track wage systemsDouble-track wage systems

Managerial and Executive IncentivesManagerial and Executive IncentivesManagerial and Executive IncentivesManagerial and Executive Incentives

Bonuses and merit increasesBonuses and merit increasesBonuses and merit increasesBonuses and merit increases

Performance incentive bonusesPerformance incentive bonusesPerformance incentive bonusesPerformance incentive bonuses

Executive perquisites (perks)Executive perquisites (perks)Executive perquisites (perks)Executive perquisites (perks)

Copyright © 2004 South-Western. All rights reserved. 10–27

Executive Compensation

• The Executive Pay PackageBase salaryShort-term incentives or bonusesLong-term incentives or stock plansPerquisites (perks)

Copyright © 2004 South-Western. All rights reserved. 10–28

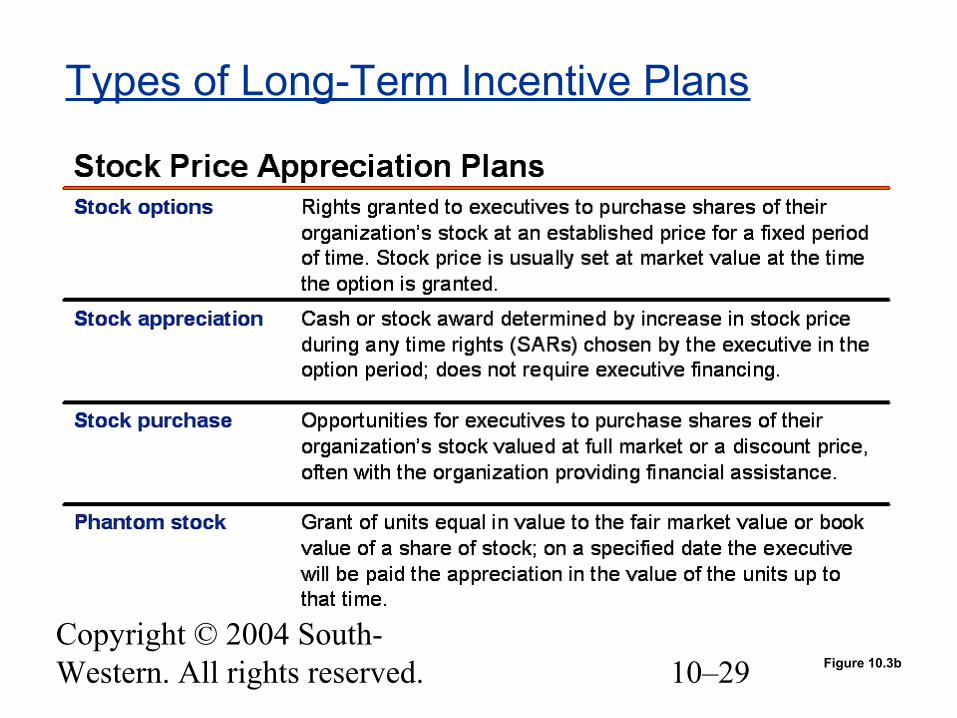

Types of Long-Term Incentive Plans

Figure 10.3a

Stock Price Appreciation Plans

Stock Options

Stock Appreciation Rights (SARS)

Stock Purchase

Phantom Stock

Restricted Stock/Cash Plans

Restricted Stock

Restricted Cash

Performance-Based Plans

Performance Units

Performance Shares

Formula-value Grants

Dividend Units

Copyright © 2004 South-Western. All rights reserved. 10–29

Types of Long-Term Incentive Plans

Figure 10.3b

Copyright © 2004 South-Western. All rights reserved. 10–30

Types of Long-Term Incentive Plans (cont’d)

Figure 10.3c

Copyright © 2004 South-Western. All rights reserved. 10–31

Types of Long-Term Incentive Plans (cont’d)

Figure 10.3d

Copyright © 2004 South-Western. All rights reserved. 10–32

Criticisms of Executive Incentive Plans

• Incentive payments are excessive compared with return to stockholders.

• Time periods for judging and rewarding performance are too short.

• Quarterly earnings growth is emphasized at the expense of research and development.

• Emphasis is placed upon equaling or exceeding executive salary survey averages.

• Benefits do not relate closely to individual performance.

Presentation Slide 10–5

Copyright © 2004 South-Western. All rights reserved. 10–33

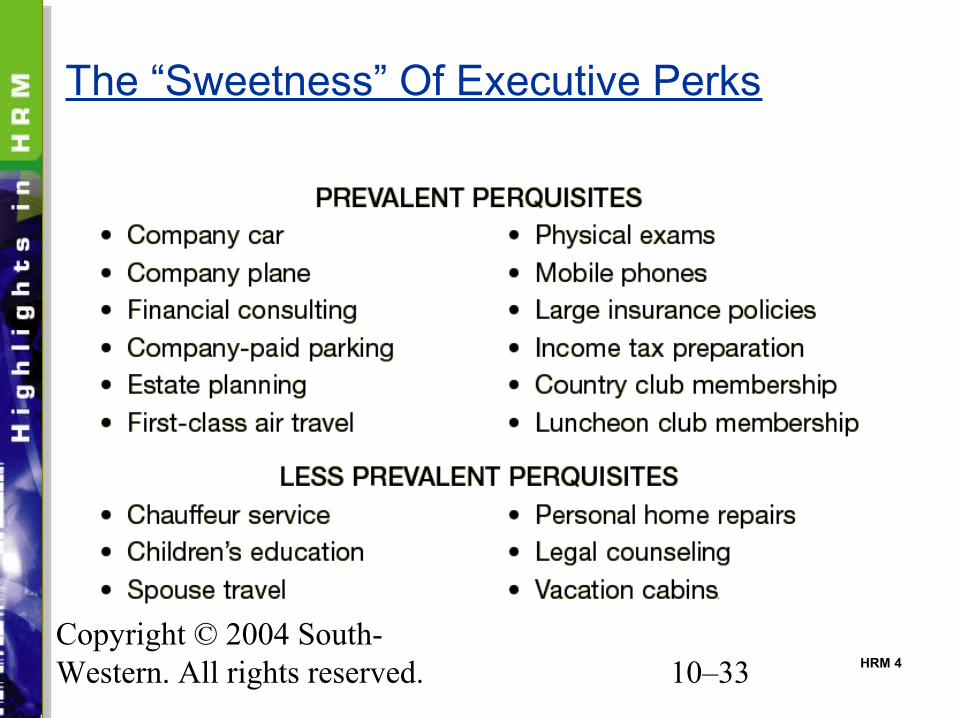

The “Sweetness” Of Executive Perks

HRM 4

Copyright © 2004 South-Western. All rights reserved. 10–34

Group Incentive Plans

• Team Incentive PlansCompensation plans where all team members receive

an incentive bonus payment when production or service standards are met or exceeded.

• Establishing Team Incentive PaymentsSet performance measures upon which incentive

payments are basedDetermine the size of the incentive bonus.Create a payout formula and fully explain to

employees how payouts will be distributed.

Copyright © 2004 South-Western. All rights reserved. 10–35

Group Incentive Plans

• Gainsharing PlansPrograms under which both employees and the

organization share the financial gains according to a predetermined formula that reflects improved productivity and profitability.

Copyright © 2004 South-Western. All rights reserved. 10–36

The Pros of Team Incentive Plans

• Team incentives are effective when:They support group planning and problem solving,

thereby building a team culture.

The contributions of individual employees depend on group cooperation.

They broaden the scope of the contribution that employees are motivated to make.

They reduce employee jealousies and complaints over “tight” or “loose” individual standards.

They encourage cross-training and the acquiring of new interpersonal competencies.

Figure 10.4a

Copyright © 2004 South-Western. All rights reserved. 10–37

The Cons of Team Incentive Plans

• Team incentives are ineffective when:

Individual team members perceive that “their” efforts contribute little to team success or to the attainment of the incentive bonus.

Intergroup social problems—pressure to limit performance and the “free-ride” effect— arise.

Complex payout formulas are difficult for team members to understand.

Figure 10.4b

Copyright © 2004 South-Western. All rights reserved. 10–38

Lessons Learned: Designing Effective Gainsharing Programs• Enlist total managerial support.

• Include all groups—labor, management, employees.

• Prevent political gamesmanship.

• Bonus formulas must be fair, precise and easily calculated, offer frequent payouts, large enough to encourage employee effort, and create a pay-for-performance environment.

• Be certain that employees are predisposed to a gainsharing reward system.

• Launch the plan during a favorable business period.

HRM 5

Copyright © 2004 South-Western. All rights reserved. 10–39

Scanlon PlanScanlon Plan Rewards come from employee participation in Rewards come from employee participation in improving productivity and reducing costs.improving productivity and reducing costs.

Rewards come from employee participation in Rewards come from employee participation in improving productivity and reducing costs.improving productivity and reducing costs.

Rucker Plan (SOP)Rucker Plan (SOP)

Shared rewards come from the difference between Shared rewards come from the difference between labor costs and sales value of production.labor costs and sales value of production.

Shared rewards come from the difference between Shared rewards come from the difference between labor costs and sales value of production.labor costs and sales value of production.

ImproshareImproshare Gainsharing based on increases in productivity of Gainsharing based on increases in productivity of the standard hour output of work teams.the standard hour output of work teams.

Gainsharing based on increases in productivity of Gainsharing based on increases in productivity of the standard hour output of work teams.the standard hour output of work teams.

Employee Bonus and Gainsharing Plans

Earnings-at-riskEarnings-at-risk

Encourages employees to achieve higher output Encourages employees to achieve higher output and quality standards by placing a portion of their and quality standards by placing a portion of their base salary at risk of loss.base salary at risk of loss.

Encourages employees to achieve higher output Encourages employees to achieve higher output and quality standards by placing a portion of their and quality standards by placing a portion of their base salary at risk of loss.base salary at risk of loss.

Copyright © 2004 South-Western. All rights reserved. 10–40

Bonus and Gainsharing Plans

• Scanlon PlanEmployee and management committees cooperate in

cost-reduction improvements.

• Rucker PlanBonus based on the relationship between the total

earnings of hourly employees and the production value created by the employees.

• ImproshareGainsharing program for bonuses are based upon the

overall productivity of the work team.

Copyright © 2004 South-Western. All rights reserved. 10–41

Scanlon Plan Suggestion Process

Figure 10.5

Copyright © 2004 South-Western. All rights reserved. 10–42

Earnings-at-Risk Plans

• Profit SharingAny procedure by which an employer pays, or makes

available to all regular employees, in addition to their base pay, current or deferred sums based upon the profits of the enterprise.

Agreement over division of profits between company and employees.

Possibility of no payout due to financial condition of company.

Copyright © 2004 South-Western. All rights reserved. 10–43

Earnings-at-Risk Plans

• Earnings-at-Risk Incentive PlansA portion of the employee’s base pay is placed at

risk, but employees are given the opportunity to earn income above base pay when goals are met or exceeded.

Copyright © 2004 South-Western. All rights reserved. 10–44

Earnings-at-Risk Incentive Plans

• Stock OptionsGranting employees the right to purchase a specific

number of shares of the company’s stock at a guaranteed price (the option price) during a designated time period.

The value of an option is subject to stock market conditions at the time that option is exercised.

Copyright © 2004 South-Western. All rights reserved. 10–45

Earnings-at-Risk Incentive Plans

• Employee Stock Ownership Plans (ESOPs)Stock plans in which an organization contributes

shares of its stock to an established trust for the purpose of stock purchases by its employees.

The employer establishes an ESOP trust that qualifies as a tax-exempt employee trust under Section 401(a) of the Internal Revenue Code

Stock bonus plans are funded by direct employer contributions of its stock or cash to purchase its stock.

Leveraged plans are funded by employer borrowing to purchase its stock for the ESOP.

Copyright © 2004 South-Western. All rights reserved. 10–46

Employee Stock Ownership Plans

Rewards and Risks of ESOPSRewards and Risks of ESOPSRewards and Risks of ESOPSRewards and Risks of ESOPS

AdvantagesAdvantagesAdvantagesAdvantages DisadvantagesDisadvantagesDisadvantagesDisadvantages

Liquidity and valueLiquidity and valueLiquidity and valueLiquidity and value

Pride of ownershipPride of ownershipPride of ownershipPride of ownership

Deferred taxesDeferred taxesDeferred taxesDeferred taxes

Single funding basisSingle funding basisSingle funding basisSingle funding basis

Not insuredNot insuredNot insuredNot insured

Retirement benefitsRetirement benefitsRetirement benefitsRetirement benefits

Recommended

![Incentive pay and productivity[4]](https://img.pdfslide.us/doc/110x75/577d2f201a28ab4e1eb0dd23/incentive-pay-and-productivity4.jpg)