Chapter 6 Appendix:

Cash Budget

Cash BudgetCash Budget

Contributes to more effective cash management

Shows managers the need for additional financing before actual need arises

Indicates when excess cash will be available

Cash BudgetCash Budget

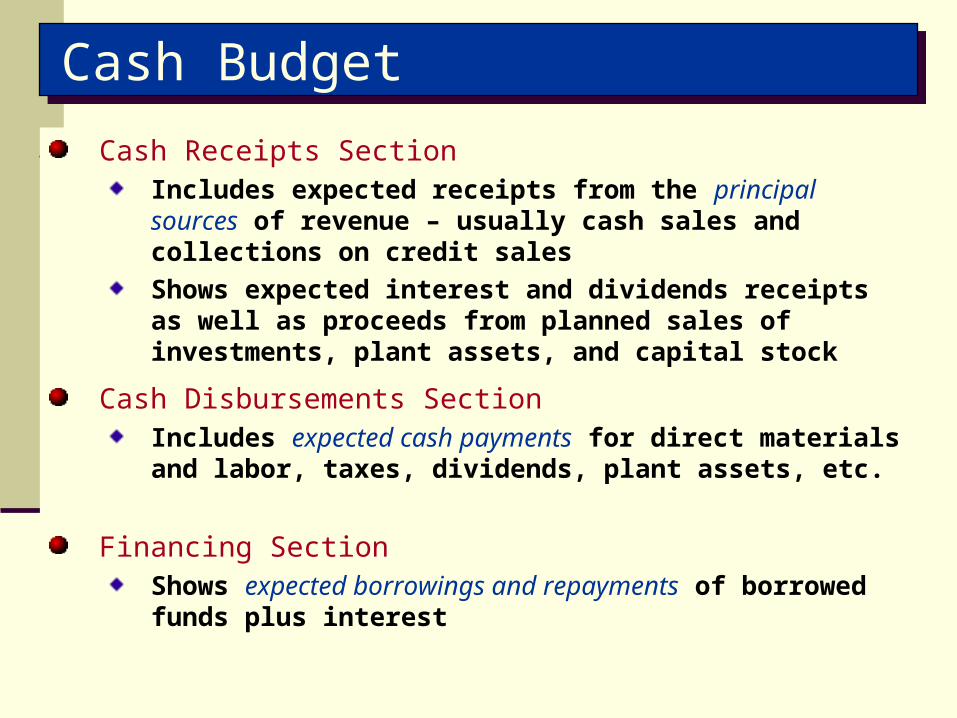

Cash Receipts Section

Cash Disbursements Section

Financing Section

Cash BudgetCash Budget

Cash Receipts SectionIncludes expected receipts from the principal sources of revenue – usually cash sales and collections on credit salesShows expected interest and dividends receipts as well as proceeds from planned sales of investments, plant assets, and capital stock

Cash Disbursements SectionIncludes expected cash payments for direct materials and labor, taxes, dividends, plant assets, etc.

Financing SectionShows expected borrowings and repayments of borrowed funds plus interest

Cash BudgetCash Budget

Must prepare in sequence: Ending cash balance of one

period is the beginning cash balance for the next

Data obtained from other budgets and from management

Cash BudgetCash Budget

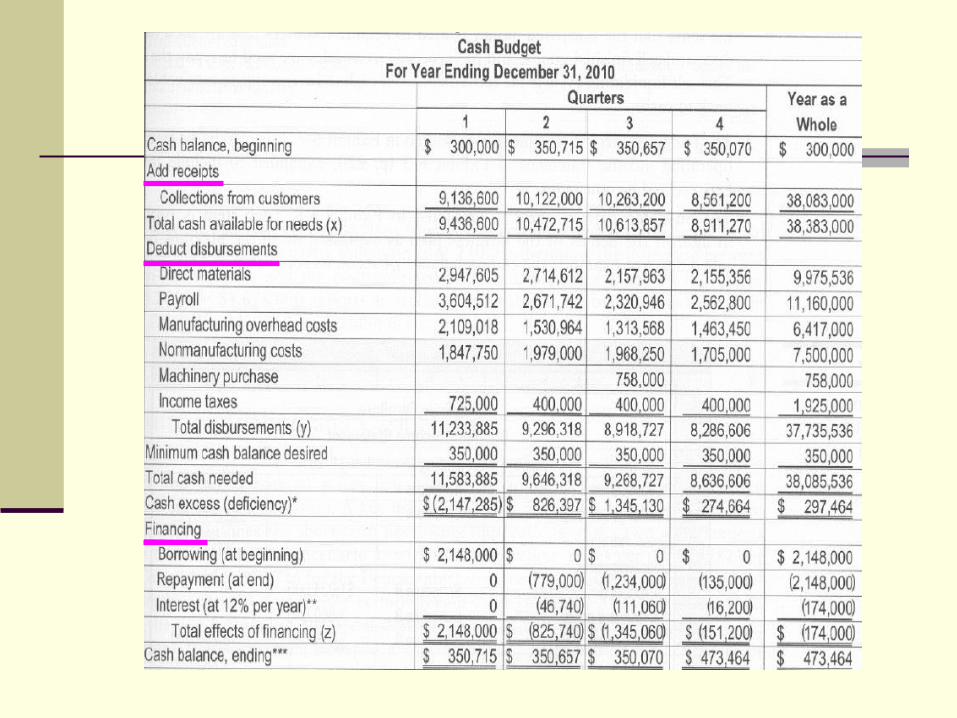

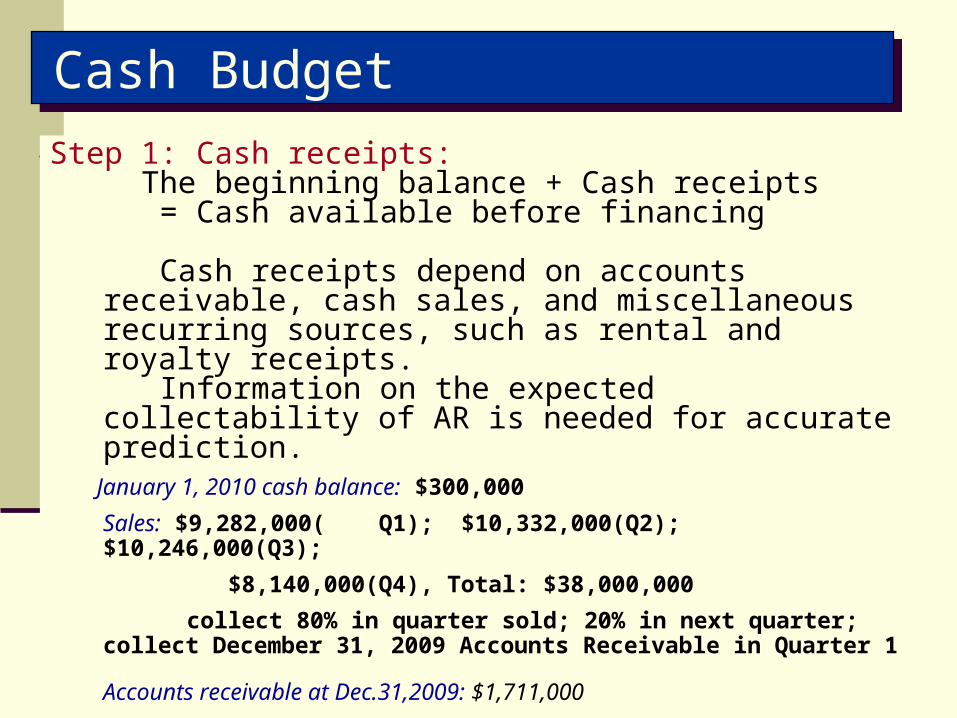

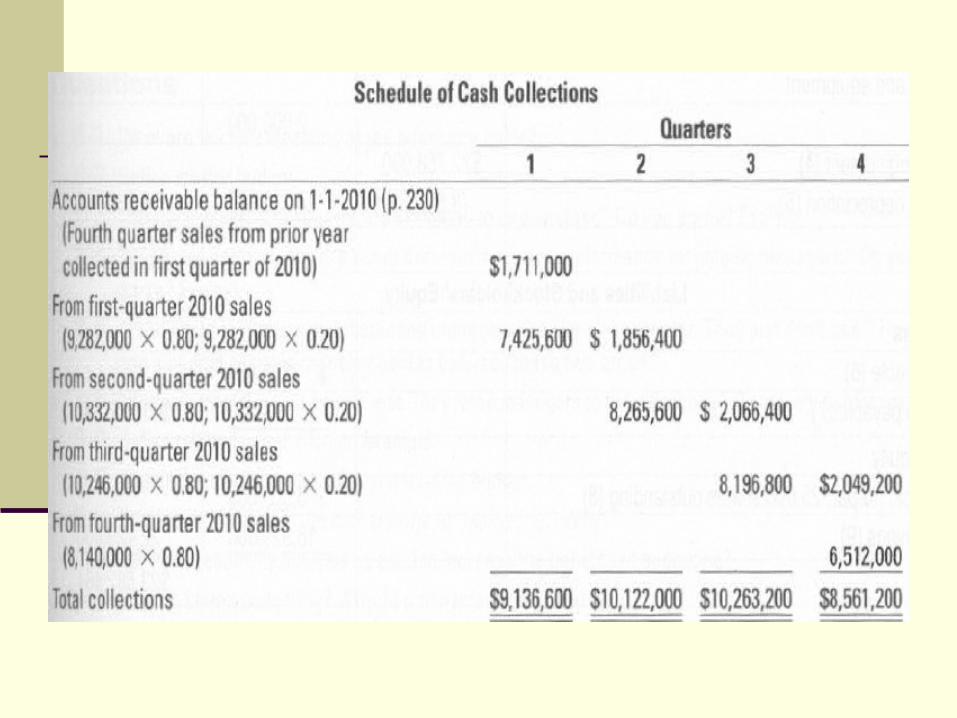

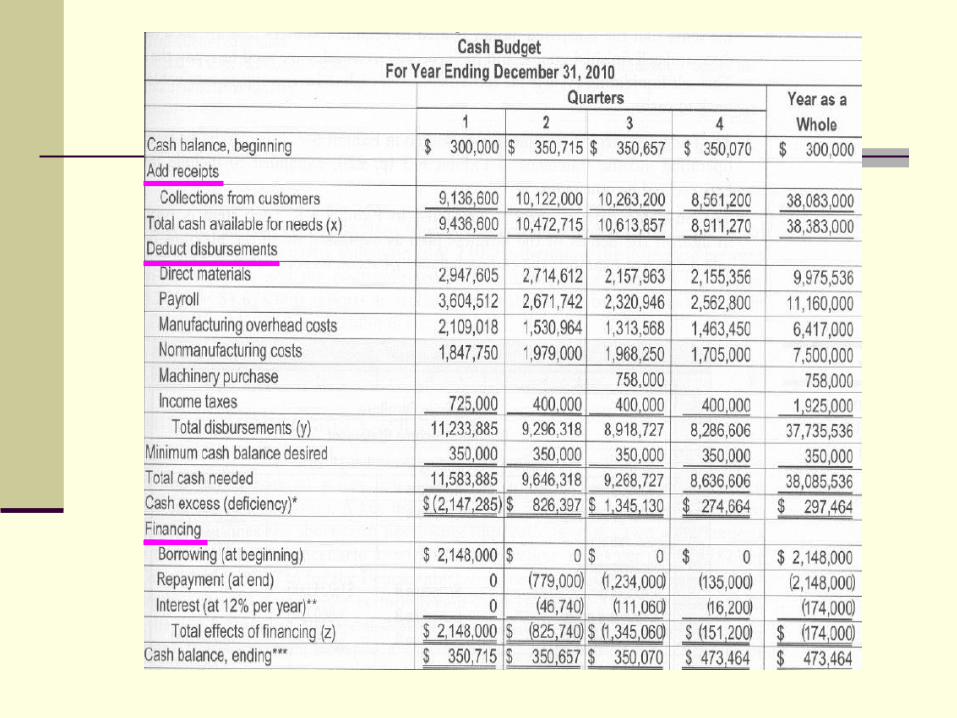

Step 1: Cash receipts: The beginning balance + Cash receipts = Cash available before financing

Cash receipts depend on accounts receivable, cash sales, and miscellaneous recurring sources, such as rental and royalty receipts.

Information on the expected collectability of AR is needed for accurate prediction.

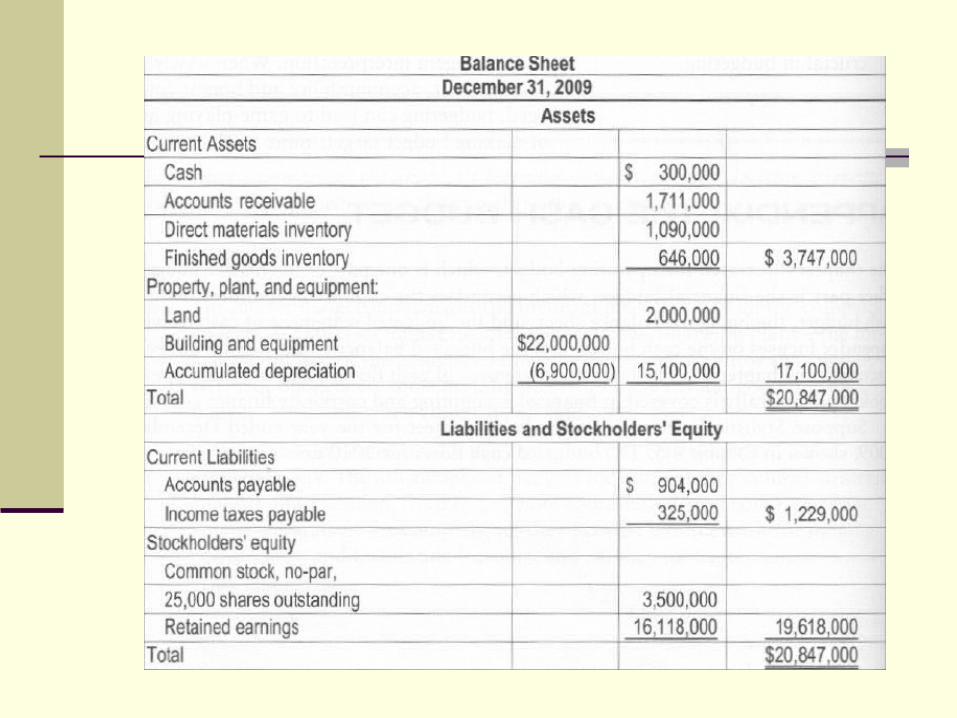

January 1, 2010 cash balance: $300,000

Sales: $9,282,000( Q1); $10,332,000(Q2); $10,246,000(Q3);

$8,140,000(Q4), Total: $38,000,000

collect 80% in quarter sold; 20% in next quarter;collect December 31, 2009 Accounts Receivable in

Quarter 1

Accounts receivable at Dec.31,2009: $1,711,000

Cash BudgetCash Budget

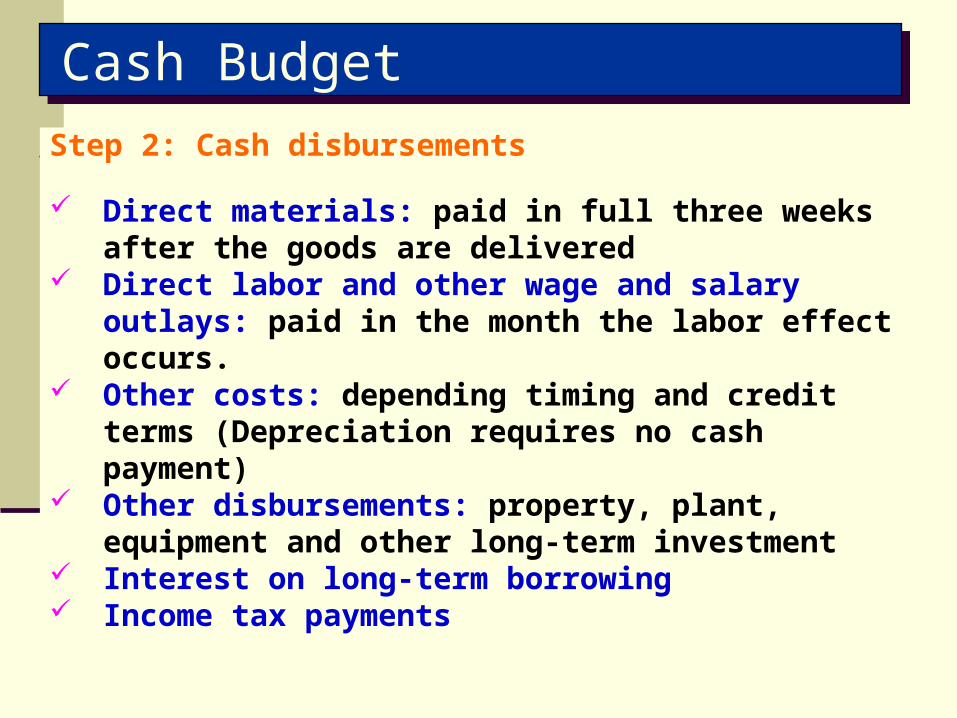

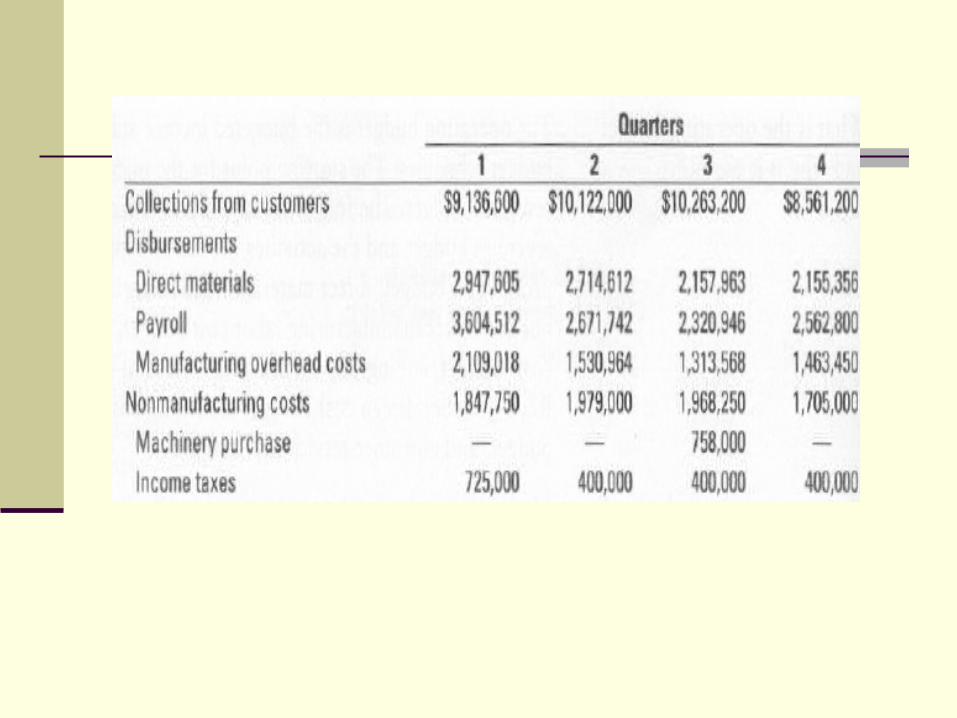

Step 2: Cash disbursements

Direct materials: paid in full three weeks after the goods are delivered

Direct labor and other wage and salary outlays: paid in the month the labor effect occurs.

Other costs: depending timing and credit terms (Depreciation requires no cash payment)

Other disbursements: property, plant, equipment and other long-term investment

Interest on long-term borrowing Income tax payments

Financial Budgets: Cash BudgetFinancial Budgets: Cash Budget

Step 3: Financing effects

Depending on the relationship between total cash available for needs and total cash

needed.

Total cash available for needs = beginning balance + cash receipts

Total cash needed= Cash disbursements + desired minimum cash

balance

Financial Budgets: Cash BudgetFinancial Budgets: Cash Budget

Step 3: Financing effects

If there is a deficiency of cash, loans obtained.If there is excess of cash, any outstanding loans

paid. Assume: the desired minimum cash balance is

$350,000. Interest is computed and paid when the principal is paid; interest rate 12% annually

Step 4: Ending cash balance

Total cash available for needs - Cash disbursements

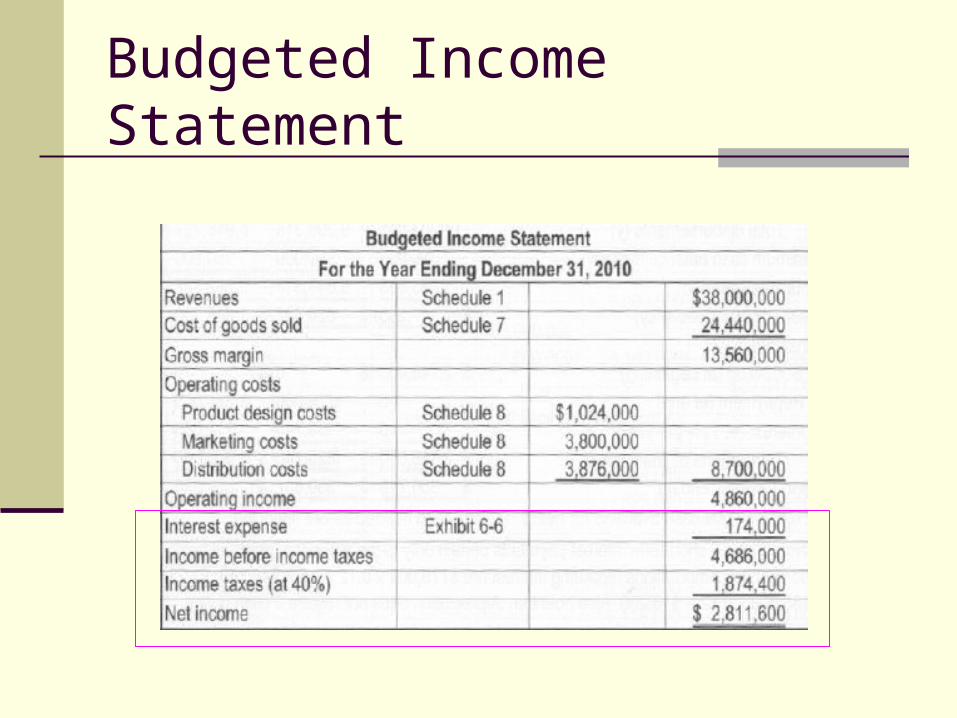

Budgeted Income Statement

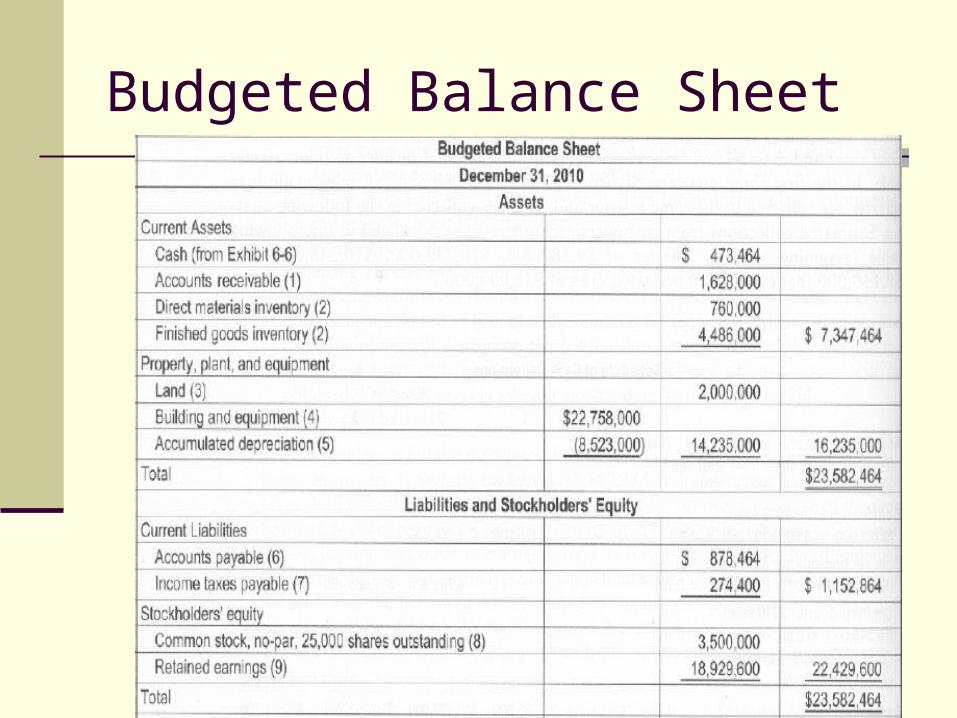

Budgeted Balance Sheet

Recommended