Emerging business models for energy efficiency in buildings

Dario Di Santo, FIRE

ECEEE, 3 June 2015

2

www.fire-italia.org

The Italian Federation for the Rational use of Energy is a no-profit association founded in 1987 that promotes energy efficiency, supporting energy manager, ESCOs and other companies dealing with energy.

Besides the activities directed to its nearly 450 members, FIRE operates under an implementing agreement with the Ministry of Economic Development to manage the Italian energy manager network since 1992.

In order to promote energy efficiency FIRE cooperates and deals with public authorities, energy technology and service companies, consultants, medium and large consumers, universities and associations to promote best practices and improve the legislation.

FIRE manages SECEM - an accredited body - to certify the Energy management experts according to the standard UNI CEI 11339.

FIRE: the association for energy efficiency

3

445 members in 2014, 228 persons and 217 organizations.

FIRE: the association for energy efficiency

Some members of FIRE:

A2A calore e servizi S.r.l. - ABB S.p.a. - Acea S.p.a. - Albapower S.p.a. - Anigas - Atlas Copco S.p.a. - Avvenia S.r.l. - AXPO S.p.a. - Banca d’Italia - Banca Popolare di Sondrio - Bit Energia S.r.l. - Bosh Energy and Building Solution Italy S.r.l. - Bticino S.p.a. - Burgo Group S.p.a. - Cabot Italiana S.p.a. - Carraro S.p.a. - Centria S.p.a. - Certiquality S.r.l. - Cofely Italia S.p.a. - Comau S.p.a. - Comune di Aosta - CONI Servizi S.p.a. - CONSIP S.p.a. - Consul System S.r.l. - CPL Concordia Soc. Coop - Comitato Termotecnico Italiano - DNV S.r.l. - ENEL Distribuzione S.p.a. - ENEL Energia S.p.a. - ENEA - ENI S.p.a. - Fenice S.p.a. - Ferriere Nord S.p.a. - Fiat Group Automobiles - Fiera Milano S.p.a. - FINCO - FIPER - GSE S.p.a. - Guerrato S.p.a. - Heinz Italia S.p.a. - Hera S.p.a. - IBM Italia S.p.a. - Intesa Sanpaolo S.p.a. - Iren Energia e Gas S.p.a. - Isab s.r.l. - Italgas S.p.a. - Johnson Controls Systems and Services Italy S.r.l. - Lidl Italia s.r.l. - Manutencoop Facility Management S.p.a. - Mediamarket S.p.a. - M&G Polimeri Italia - Omron Electronics S.p.a. - Pasta Zara S.p.a. - Pirelli Industrie Pneumatici S.p.a. - Politecnico di Torino - Provincia di Cremona - Publiacqua S.p.a. - Raffineria di Milazzo S.c.p.a. - RAI S.p.a. - Rete Ferroviaria Italiana S.p.a. - Rockwood Italia S.p.a. - Roma TPL S.c.a.r.l. - Roquette Italia S.p.a. - RSE S.p.a. - Sandoz Industrial Products S.p.a. - Schneider Electric S.p.a. - Siena Ambiente S.p.a. - Siram S.p.a. - STMicroelectronics S.p.a. - TIS Innovation Park - Trenitalia S.p.a. - Turboden S.p.a. - Università Campus Bio-Medico di Roma - Università Cattolica Sacro Cuore - Università degli studi di Genova - Varem S.p.A. - Wind Telecomunicazioni S.p.a. - Yousave S.p.a.

Our membership include organization and professionals both from the supply and the demand side of energy efficiency services and solutions.

4

4

FIRE: the association for energy efficiency

Besides being involved in many European projects, listed next, FIRE implement surveys and market studies on energy related topics, information and dissemination campaigns, and advanced training.

Some of FIRE clients over the years: Ministry of Environment, ENEA, GSE, RSE, large organizations (such as Centria, ENEL, Ferrovie dello Stato, FIAT, Finmeccanica, Galbani, H3G, Telecom Italia, Unioncamere), universities, associations, energy agencies and exhibition organizers.

www.fire-italia.org

5

www.secem.eu

SECEM

SECEM, European System for Certification in Energy Management, is a certification body created by the FIRE.

SECEM was the first body to offer third-party certification for Energy Management Experts (EMEs) according to UNI CEI 11339 and is accredited according to the ISO/IEC 17024 standard.

In Italy two standards were developed in order to promote the qualification of energy efficiency operators: UNI CEI 11339 for EMEs was issued in 2009, UNI CEI 11352 for ESCOs was published in 2010. A new standard for energy auditor is presently under preparation.

Both the mentioned standards are recognized from the national legislation within the energy audit obl igat ions for large companies introduced by the EED directive and the white certificate scheme.

FIRE’s study on EE in the building sector

The study “Energy efficiency in the building sector: skills, business models and public private partnerships” aimed to analyze innovative tasks, business models, and public support to promote energy efficiency in the building sector, linking up with the development of an industrial policy in line with the Green Growth Strategy, also through the development of the ESCO model.

The study, which concentrated on the Italian situation, in particular examined:

1. The degree of integration of available technologies, the skills asked for and the skills necessary to manage this integration, and the interaction between the various players and the (public and private) parties concerned.

2. The financial, administrative and legal barriers that are obstacles to the massive dissemination of efficient construction-industry technologies on a larger scale, and that impede an integrated and holistic approach – instead of the actual fragmented one – from catching on.

3. The actual implementation of innovative and successful business models to improve energy efficiency in the public building sector (ESCO, utilities, “green banks”, etc.).

The analysis focused on the Italian situation and resulted in a study structured in ten chapters.

6

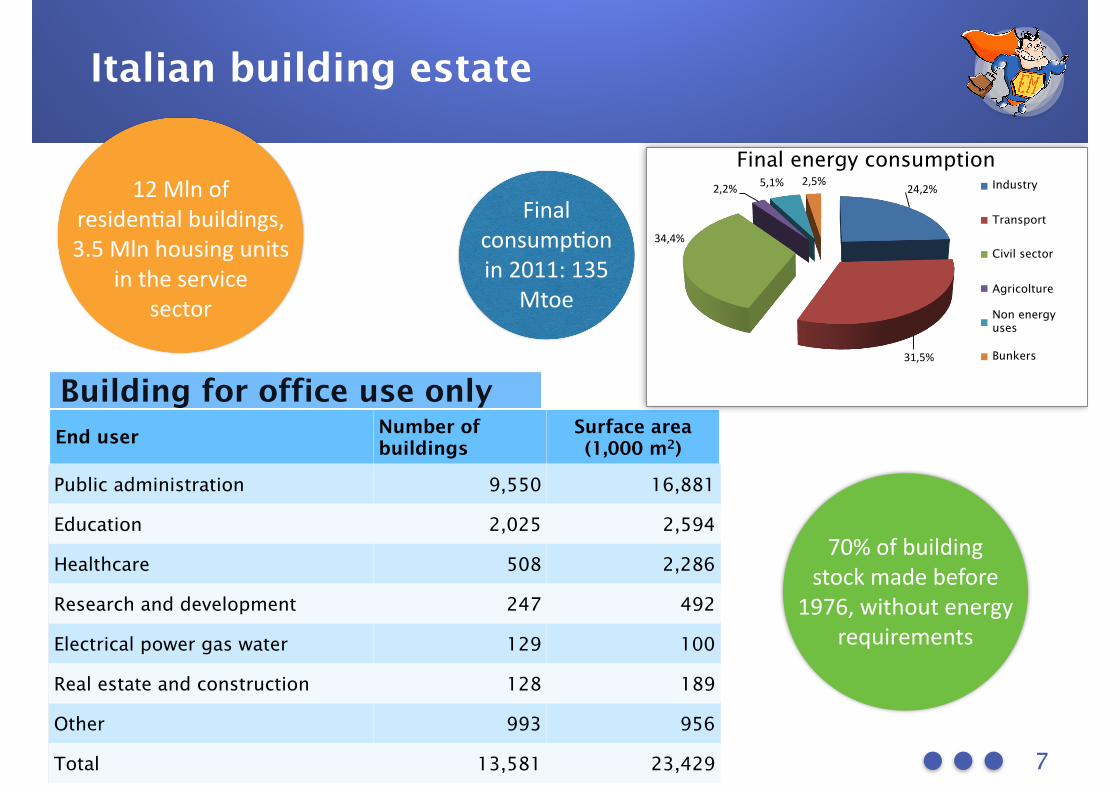

Italian building estate

7

End user Number of buildings

Surface area (1,000 m2)

Public administration 9,550 16,881

Education 2,025 2,594

Healthcare 508 2,286

Research and development 247 492

Electrical power gas water 129 100

Real estate and construction 128 189

Other 993 956

Total 13,581 23,429

70% of building stock made before

1976, without energy requirements

12 Mln of residen@al buildings, 3.5 Mln housing units

in the service sector

RAEE 2011 – Executive Summary

6

scorte di carburante per il trasporto marittimo internazionale (cosiddetti bunkeraggi), mentre il 5,1% è destinato ad usi non energetici, in particolare nell’industria petrolchimica (figura 2).

L’andamento del consumo nei settori di uso finale evidenzia una riduzione del 2,65% rispetto al 2010; tale diminuzione ha riguardato tutti i settori, per gli effetti della crisi economica e delle misure di promozione e incentivazione dell’efficienza energetica.

Le maggiori riduzioni sono relative agli usi non energetici (dal 6,1 al 5,1%), che hanno risentito della crisi del settore petrolchimico, e ai consumi per usi civili (dal 35,5 al 34,4%).

Il profilo dinamico dei consumi energetici nei settori di impiego finale per il periodo 2000-2011 è mostrato in figura 3.

I dati fino al 2005 evidenziano un andamento crescente del consumo finale seguito da una progressiva diminuzione, che nel 2011 ha fatto tornare il valore dei consumi finali ai livelli del 2000 (l’eccezione del 2010 è dovuta a un effetto “rimbalzo” dopo la forte contrazione del 2009).

Il confronto 2011-2000 mostra una consistente riduzione dei consumi del settore industriale (-23%) e un significativo aumento di quelli relativi agli usi civili (+15%), mentre i consumi degli altri settori hanno registrato variazioni di entità trascurabile.

Figura 2 - Impieghi finali di energia per settore, anno 2011 - Totale 134,9 Mtep

Fonte: elaborazione ENEA su dati MSE

24,2%

31,5%

34,4%

2,2% 5,1% 2,5% Industria

Trasporti

Usi civili

Agricoltura

Usi non energetici

Bunkeraggi

Final energy consumptionIndustry

Transport

Civil sector

Agricolture

Non energy uses

Bunkers

Final consump@on in 2011: 135

Mtoe

Building for office use only

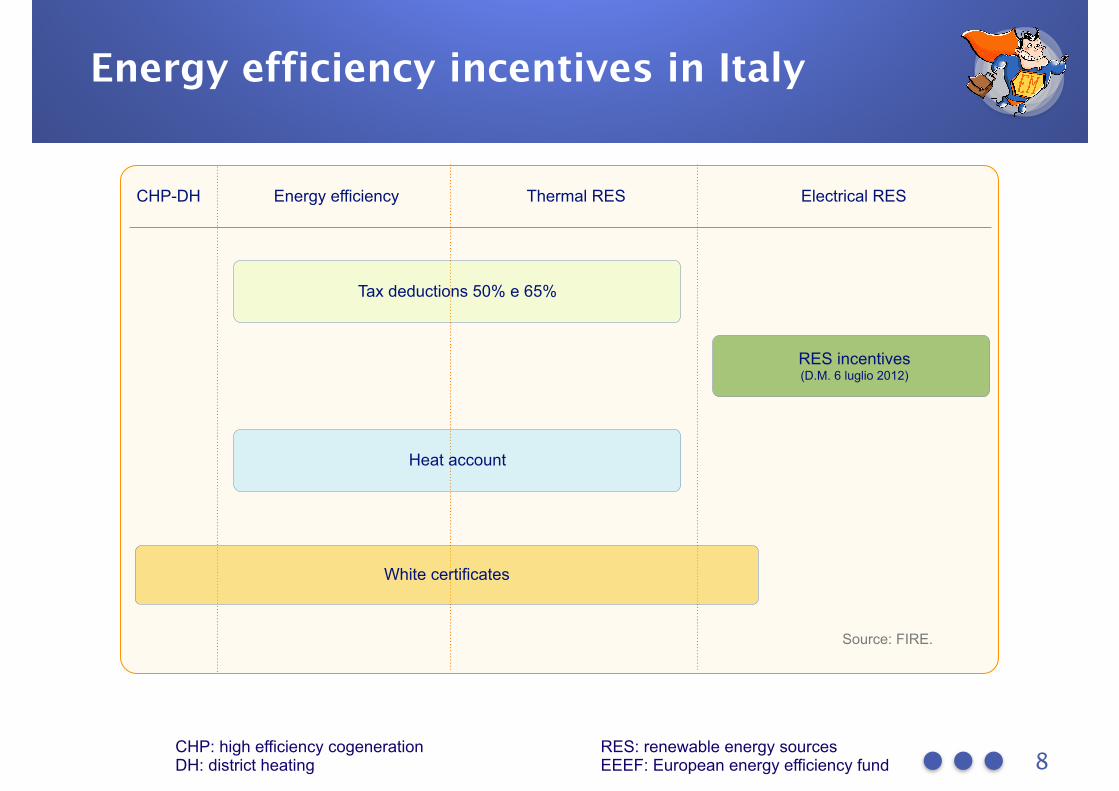

Energy efficiency incentives in Italy

8

White certificates

Tax deductions 50% e 65%

RES incentives (D.M. 6 luglio 2012)

Heat account

Source: FIRE.

CHP: high efficiency cogeneration DH: district heating

RES: renewable energy sources EEEF: European energy efficiency fund

Energy efficiency Thermal RES Electrical RESCHP-DH

Barriers

1) Economic barriers

2) Lack of awareness and know-how

3) Energy is not core business

4) Qualification of market operators

5) Supply chain not adequately developed

6) Integration difficulties and complexity

7) Legislation and standards

8) Access to incentive schemes

9) Financing

10) Public sector barriers

9

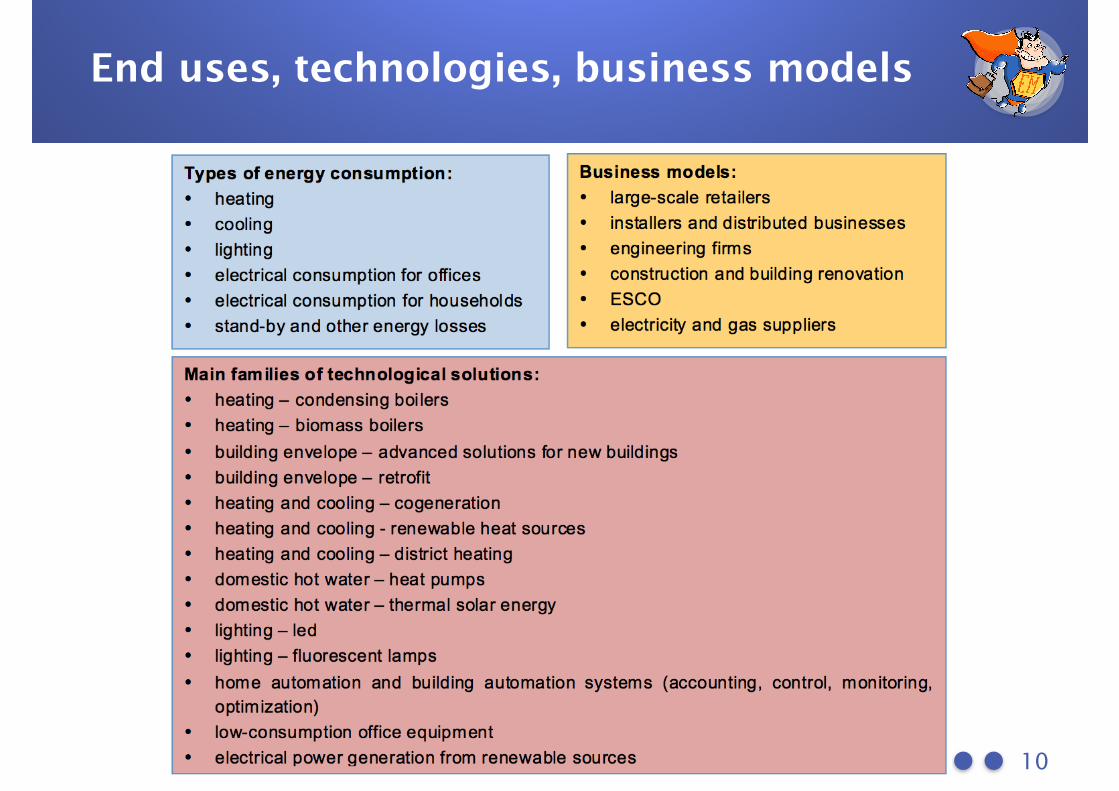

End uses, technologies, business models

10

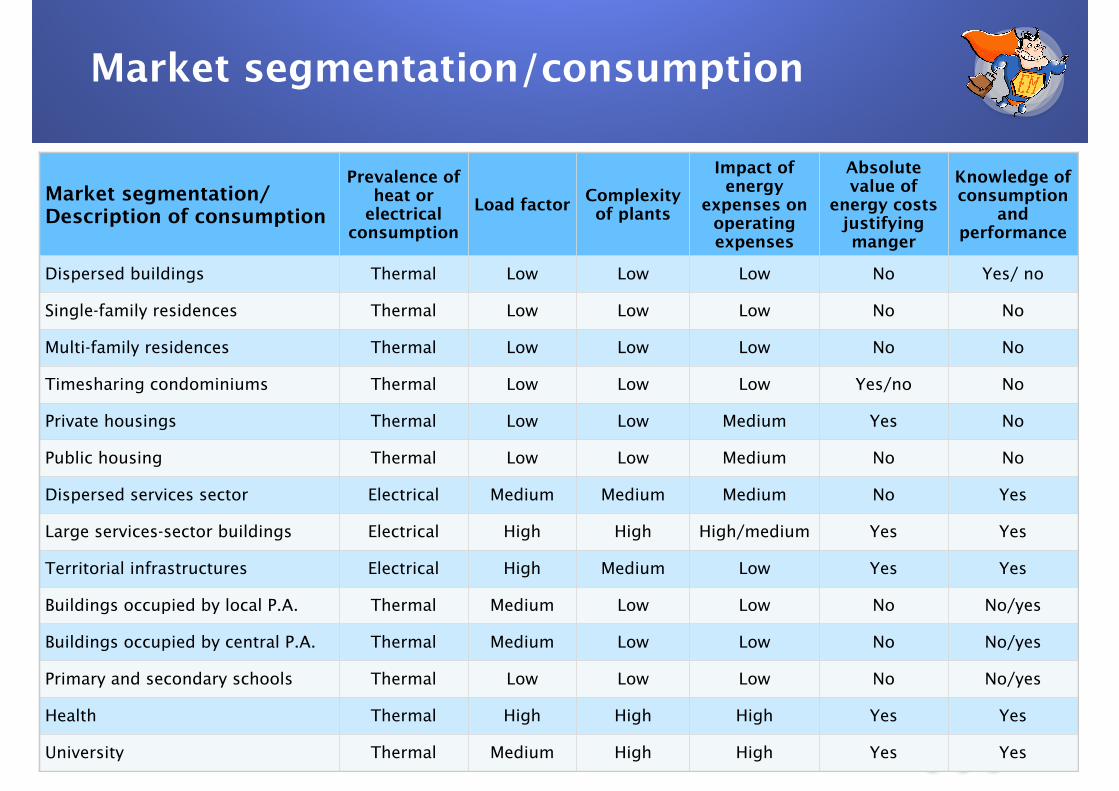

Market segmentation/consumption

11

Market segmentation/Description of consumption

Prevalence of heat or

electrical consumption

Load factor Complexity of plants

Impact of energy

expenses on operating expenses

Absolute value of

energy costs justifying manger

Knowledge of consumption

and performance

Dispersed buildings Thermal Low Low Low No Yes/ no

Single-family residences Thermal Low Low Low No No

Multi-family residences Thermal Low Low Low No No

Timesharing condominiums Thermal Low Low Low Yes/no No

Private housings Thermal Low Low Medium Yes No

Public housing Thermal Low Low Medium No No

Dispersed services sector Electrical Medium Medium Medium No Yes

Large services-sector buildings Electrical High High High/medium Yes Yes

Territorial infrastructures Electrical High Medium Low Yes Yes

Buildings occupied by local P.A. Thermal Medium Low Low No No/yes

Buildings occupied by central P.A. Thermal Medium Low Low No No/yes

Primary and secondary schools Thermal Low Low Low No No/yes

Health Thermal High High High Yes Yes

University Thermal Medium High High Yes Yes

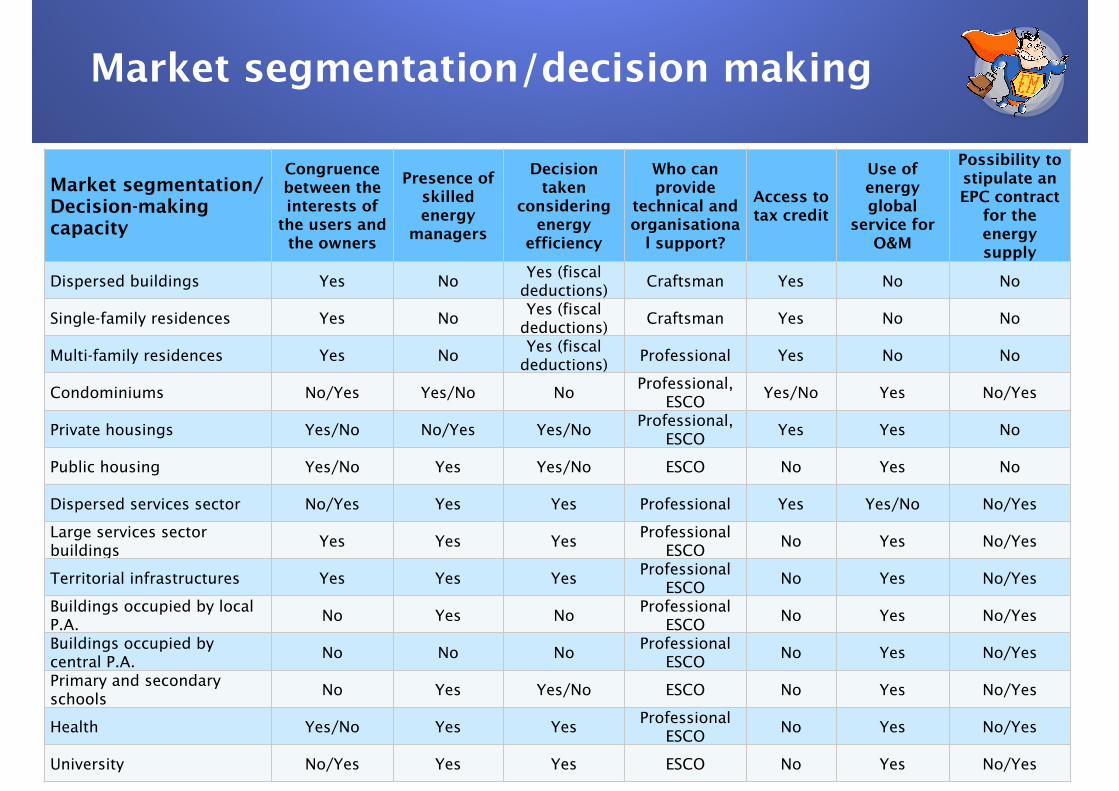

Market segmentation/decision making

12

Market segmentation/Decision-making capacity

Congruence between the interests of

the users and the owners

Presence of skilled energy

managers

Decision taken

considering energy

efficiency

Who can provide

technical and organisationa

l support?

Access to tax credit

Use of energy global

service for O&M

Possibility to stipulate an EPC contract

for the energy supply

Dispersed buildings Yes NoYes (fiscal

deductions)Craftsman Yes No No

Single-family residences Yes NoYes (fiscal

deductions)Craftsman Yes No No

Multi-family residences Yes NoYes (fiscal

deductions)Professional Yes No No

Condominiums No/Yes Yes/No NoProfessional,

ESCOYes/No Yes No/Yes

Private housings Yes/No No/Yes Yes/NoProfessional,

ESCOYes Yes No

Public housing Yes/No Yes Yes/No ESCO No Yes No

Dispersed services sector No/Yes Yes Yes Professional Yes Yes/No No/Yes

Large services sector buildings

Yes Yes YesProfessional

ESCONo Yes No/Yes

Territorial infrastructures Yes Yes YesProfessional

ESCONo Yes No/Yes

Buildings occupied by local P.A.

No Yes NoProfessional

ESCONo Yes No/Yes

Buildings occupied by central P.A.

No No NoProfessional

ESCONo Yes No/Yes

Primary and secondary schools

No Yes Yes/No ESCO No Yes No/Yes

Health Yes/No Yes YesProfessional

ESCONo Yes No/Yes

University No/Yes Yes Yes ESCO No Yes No/Yes

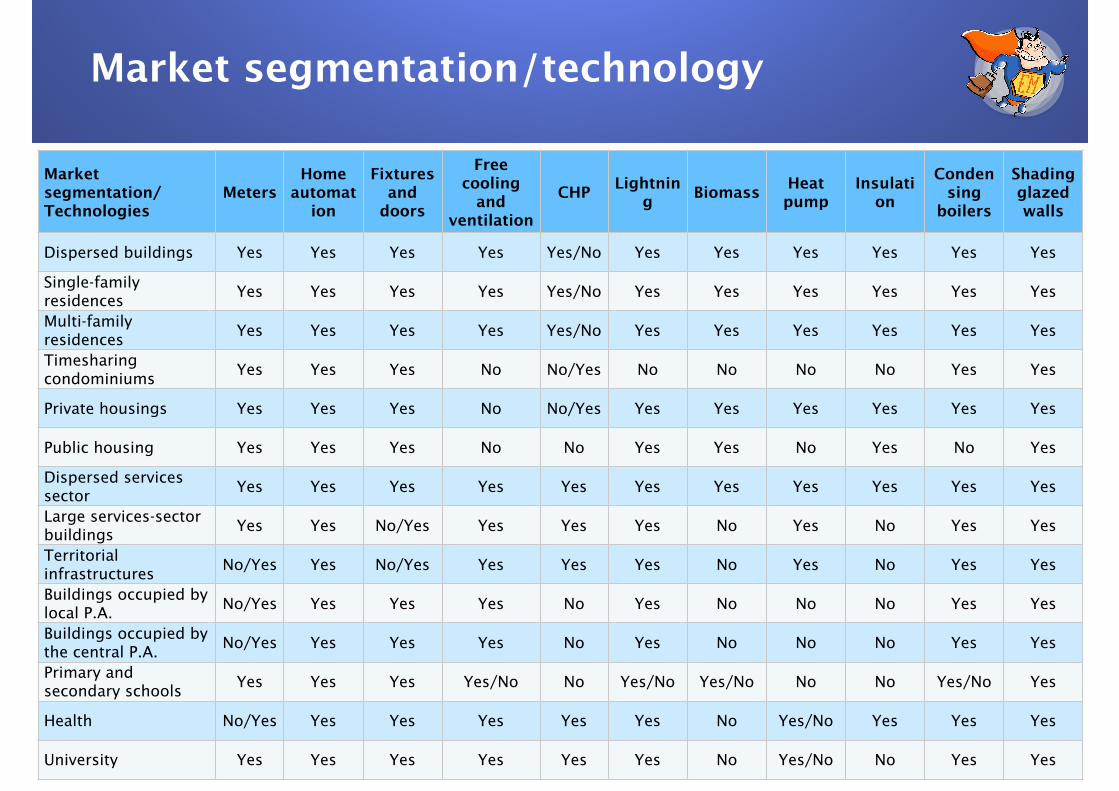

Market segmentation/technology

13

Market segmentation/Technologies

MetersHome

automation

Fixtures and

doors

Free cooling

and ventilation

CHPLightnin

gBiomass

Heat pump

Insulation

Condensing

boilers

Shading glazed walls

Dispersed buildings Yes Yes Yes Yes Yes/No Yes Yes Yes Yes Yes Yes

Single-family residences

Yes Yes Yes Yes Yes/No Yes Yes Yes Yes Yes Yes

Multi-family residences

Yes Yes Yes Yes Yes/No Yes Yes Yes Yes Yes Yes

Timesharing condominiums

Yes Yes Yes No No/Yes No No No No Yes Yes

Private housings Yes Yes Yes No No/Yes Yes Yes Yes Yes Yes Yes

Public housing Yes Yes Yes No No Yes Yes No Yes No Yes

Dispersed services sector

Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes

Large services-sector buildings

Yes Yes No/Yes Yes Yes Yes No Yes No Yes Yes

Territorial infrastructures

No/Yes Yes No/Yes Yes Yes Yes No Yes No Yes Yes

Buildings occupied by local P.A.

No/Yes Yes Yes Yes No Yes No No No Yes Yes

Buildings occupied by the central P.A.

No/Yes Yes Yes Yes No Yes No No No Yes Yes

Primary and secondary schools

Yes Yes Yes Yes/No No Yes/No Yes/No No No Yes/No Yes

Health No/Yes Yes Yes Yes Yes Yes No Yes/No Yes Yes Yes

University Yes Yes Yes Yes Yes Yes No Yes/No No Yes Yes

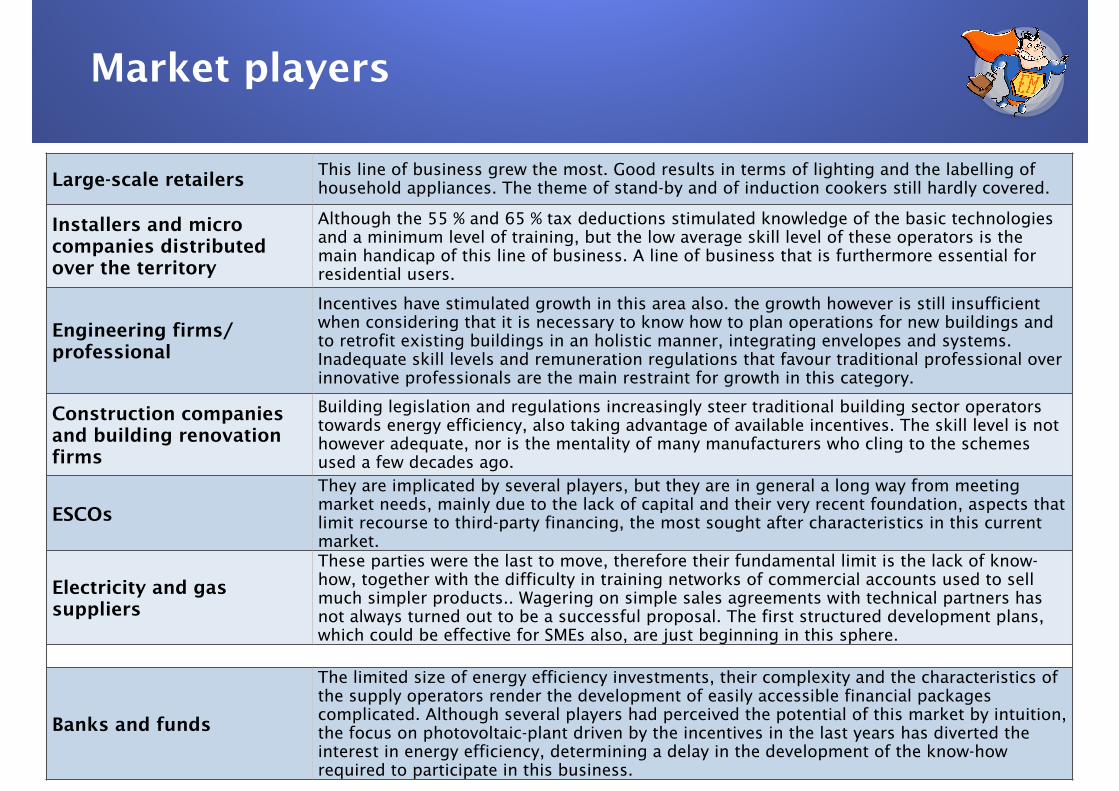

Market players

14

Large-scale retailersThis line of business grew the most. Good results in terms of lighting and the labelling of household appliances. The theme of stand-by and of induction cookers still hardly covered.

Installers and micro companies distributed over the territory

Although the 55 % and 65 % tax deductions stimulated knowledge of the basic technologies and a minimum level of training, but the low average skill level of these operators is the main handicap of this line of business. A line of business that is furthermore essential for residential users.

Engineering firms/ professional

Incentives have stimulated growth in this area also. the growth however is still insufficient when considering that it is necessary to know how to plan operations for new buildings and to retrofit existing buildings in an holistic manner, integrating envelopes and systems. Inadequate skill levels and remuneration regulations that favour traditional professional over innovative professionals are the main restraint for growth in this category.

Construction companies and building renovation firms

Building legislation and regulations increasingly steer traditional building sector operators towards energy efficiency, also taking advantage of available incentives. The skill level is not however adequate, nor is the mentality of many manufacturers who cling to the schemes used a few decades ago.

ESCOs

They are implicated by several players, but they are in general a long way from meeting market needs, mainly due to the lack of capital and their very recent foundation, aspects that limit recourse to third-party financing, the most sought after characteristics in this current market.

Electricity and gas suppliers

These parties were the last to move, therefore their fundamental limit is the lack of know-how, together with the difficulty in training networks of commercial accounts used to sell much simpler products.. Wagering on simple sales agreements with technical partners has not always turned out to be a successful proposal. The first structured development plans, which could be effective for SMEs also, are just beginning in this sphere.

Banks and funds

The limited size of energy efficiency investments, their complexity and the characteristics of the supply operators render the development of easily accessible financial packages complicated. Although several players had perceived the potential of this market by intuition, the focus on photovoltaic-plant driven by the incentives in the last years has diverted the interest in energy efficiency, determining a delay in the development of the know-how required to participate in this business.

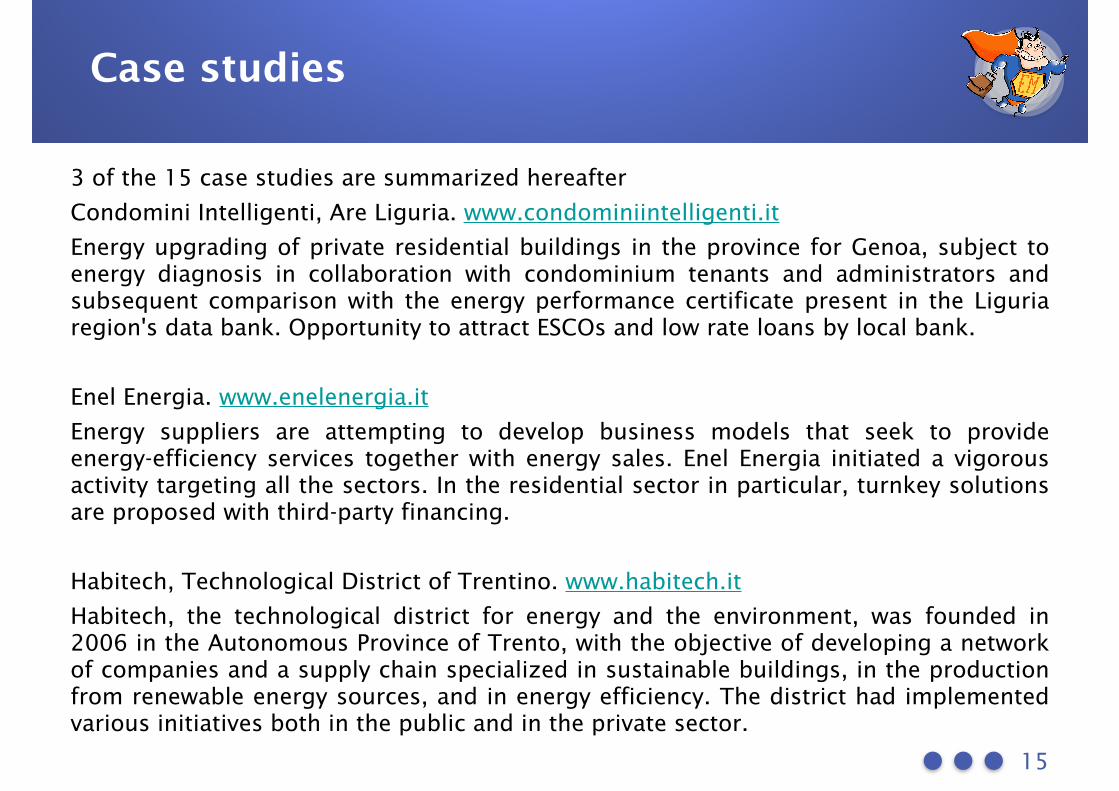

Case studies

3 of the 15 case studies are summarized hereafter

Condomini Intelligenti, Are Liguria. www.condominiintelligenti.it

Energy upgrading of private residential buildings in the province for Genoa, subject to energy diagnosis in collaboration with condominium tenants and administrators and subsequent comparison with the energy performance certificate present in the Liguria region's data bank. Opportunity to attract ESCOs and low rate loans by local bank.

Enel Energia. www.enelenergia.it

Energy suppliers are attempting to develop business models that seek to provide energy-efficiency services together with energy sales. Enel Energia initiated a vigorous activity targeting all the sectors. In the residential sector in particular, turnkey solutions are proposed with third-party financing.

Habitech, Technological District of Trentino. www.habitech.it

Habitech, the technological district for energy and the environment, was founded in 2006 in the Autonomous Province of Trento, with the objective of developing a network of companies and a supply chain specialized in sustainable buildings, in the production from renewable energy sources, and in energy efficiency. The district had implemented various initiatives both in the public and in the private sector.

15

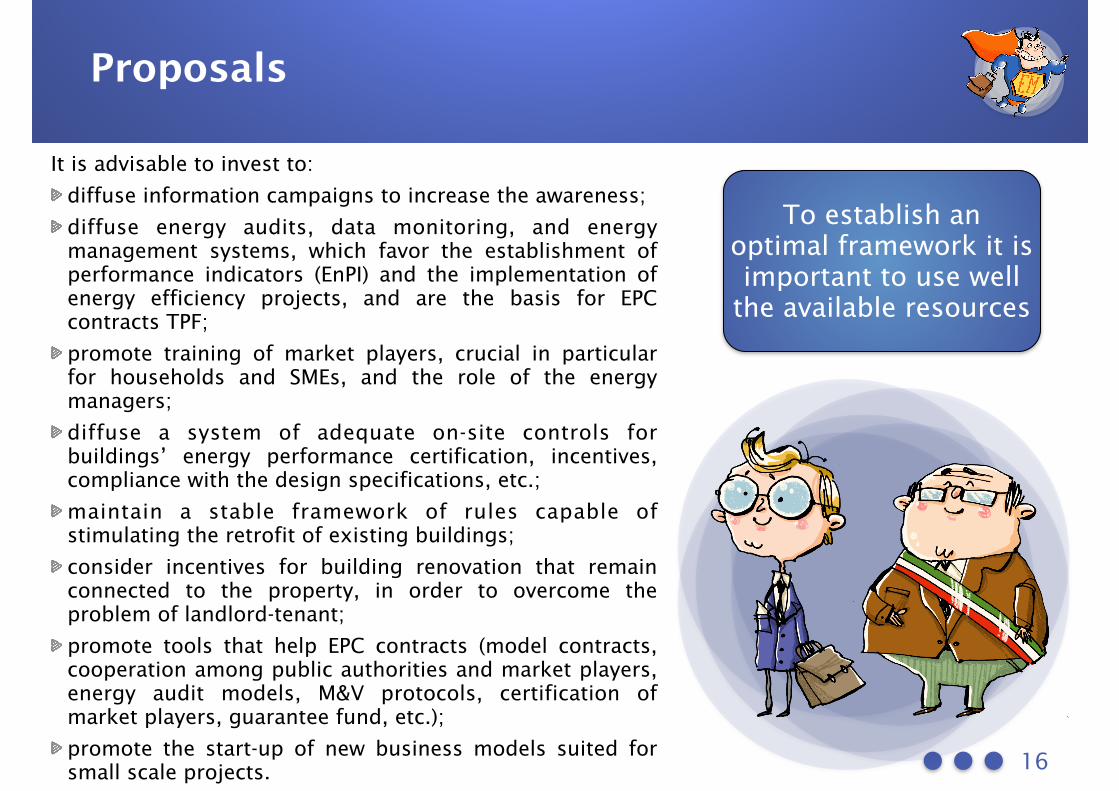

Proposals

16

To establish an optimal framework it is important to use well

the available resources

It is advisable to invest to:

diffuse information campaigns to increase the awareness;

diffuse energy audits, data monitoring, and energy management systems, which favor the establishment of performance indicators (EnPI) and the implementation of energy efficiency projects, and are the basis for EPC contracts TPF;

promote training of market players, crucial in particular for households and SMEs, and the role of the energy managers;

diffuse a system of adequate on-site controls for buildings’ energy performance certification, incentives, compliance with the design specifications, etc.;

maintain a stable framework of rules capable of stimulating the retrofit of existing buildings;

consider incentives for building renovation that remain connected to the property, in order to overcome the problem of landlord-tenant;

promote tools that help EPC contracts (model contracts, cooperation among public authorities and market players, energy audit models, M&V protocols, certification of market players, guarantee fund, etc.);

promote the start-up of new business models suited for small scale projects.

Thank you!

www.facebook.com/FIREenergy.manager

www.linkedin.com/company/fire-federazione-italiana-per-l'uso-razionale-dell'energia

www.twitter.com/FIRE_ita

For����������� ������������������ more����������� ������������������ information����������� ������������������ about����������� ������������������ our����������� ������������������ activities����������� ������������������ ����������� ������������������ visit����������� ������������������ our����������� ������������������ web����������� ������������������ site!����������� ������������������

www.dariodisanto.com

Recommended