Corporate Presentation June 2014

2

Disclaimer

This presentation has been prepared by Ashok Leyland Limited (“Company") solely for information purposes without any regard to any specific objectives, financial situations or informational needs of any particular person. This presentation may not be copied, distributed or disseminated, directly or indirectly, in any manner. Failure to comply with this directive may result in a violation of the applicable law in certain jurisdictions. By reviewing this presentation, you agree to be bound by the restrictions contained herein, and to maintain absolute confidentiality, regarding the information disclosed in these materials. This presentation does not constitute or form part of and should not be construed as, directly or indirectly, any offer or invitation or inducement to sell or issue, or any solicitation of any offer to purchase or subscribe for, any securities of the Company by any person in any jurisdiction, including in India, nor shall it or any part of it or the fact of its distribution form the basis of, or be relied on in connection with, any investment decision or any contract or commitment therefor. This presentation contains statements that constitute forward looking statements. These statements include descriptions regarding the intent, belief or current expectations of the Company or its directors and officers with respect to the results of operations and financial condition of the Company. These statements can be recognized by the use of words such as ''expects", "plans", 'will", "estimates", "projects", or other words of similar meaning. Such forward-looking statements are not guarantees of future performance and involve risks and uncertainties, and actual results may differ materially from those in such forward-looking statements as a result of various factors and assumptions which the Company believes to be reasonable in light of its operating experience in recent years. The risks and uncertainties relating to these statements include, but not limited to, risks and uncertainties, regarding fluctuations in earnings, our ability to manage growth, competition, our ability to manage our international operations, government policies, regulations, etc. The Company does not undertake any obligation to revise or update any forward looking statement that may be made from time to time by or on behalf of the Company including to reflect actual results, changes in assumptions or changes in factors affecting these statements. Given these risks, uncertainties and other factors, viewers of this presentation are cautioned not to place undue reliance on these forward looking statements. This presentation may contain certain currency exchange rates and the same have been provided only for the convenience of readers. No representation is made that the Rupee amounts actually represent such USD amounts or could have been, or could be, converted into USD at the indicated rates. This presentation is not a complete description of the Company and may not be all inclusive and may not contain all of the information that you may consider material. The information contained in this presentation has not been independently verified. No representation, warranty, guarantee or undertaking, express or implied, is or will be made as to, and no reliance should be placed on, the accuracy, completeness, correctness or fairness of the information, estimates, projections and opinions contained in this presentation. Viewers of this presentation must make their own assessment of the relevance, accuracy and adequacy of the information contained in this presentation and must make such independent investigation as they may consider necessary or appropriate for such purpose. Such information and opinions are in all events not current after the date of this presentation. Further, past performance is not necessarily indicative of future results. Any opinions expressed in this presentation or the contents of this presentation are subject to change without notice. This presentation should not be construed as legal, tax, accounting, investment or other advice. Any person placing reliance on the information contained in this presentation or any other communication by the Company does so at his or her own risk and none of the Company nor any of its affiliates, advisers or representatives, any placement agent, promoters or any other persons that may participate in any offering of any securities of the Company shall have any responsibility or liability whatsoever, whether arising in tort, contract or otherwise, for any errors, omissions, insufficiencies or inaccuracies in such information or opinions or for any loss, cost or damage suffered or incurred howsoever arising, directly or indirectly, from any use of this presentation or its contents or otherwise in connection with this presentation. Securities of the Company may not be offered or sold in the United States absent registration or an applicable exemption from registration under the United States Securities Act of 1933, as amended. This presentation has not been and will not be registered as a prospectus with any Registrar of Companies in India. This presentation is not a prospectus, a statement in lieu of a prospectus, an offering circular, an advertisement, a private placement offer letter or an offer document under the Companies Act, 2013 and the rules made thereunder, the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2009, as amended, or any other applicable law.

3

Hinduja Group – an Overview

• Promoted by the Hinduja Family

• Operations in over 35 countries

• Products and services available in more than 100 countries

• Employs over 72,000 personnel

• Multi-billion dollar turnover Group

“My dharma (duty) is to work so that I can give”

4

Group Business Verticals

Banking & Finance

Chemical/ Lubes

Automotive Power

Real Estate Media

Information Technology

Healthcare Project

Development Trading

5

Ashok Leyland: An Introduction

Established presence

Global footprint

2nd largest medium and heavy commercial vehicle (Truck and Bus) player in India

Among the largest bus-makers in the World

Exports to 34 countries

Targeted expansion strategy in 5 geographic clusters

Rich history and track record

Over 65 years of operations with unbroken track-record of profitability

History of innovation in products - Multi-axle trucks, Articulated buses

History of innovation in technology - Air brakes, CNG vehicles, Plug-in hybrids

Diversified, de-risked portfolio

Presence in heavy trucks, heavy buses, light commercial vehicles, defence logistics, power solutions, spare parts , and construction equipment

Vision:

Be in the global Top 10 in Medium & Heavy Commercial Vehicle Trucks (>7.5t GVW) and global Top 5 in Medium & Heavy Commercial Vehicle Buses (8 m and above) in volume terms

6

1,936 2,714 3,273 4,413 4,693 1,900

4,237 6,313 5,660

4,337 294

FY 04 FY 05 FY 06 FY 07 FY 08 FY 09 FY 10 FY 11 FY 12 FY13 FY14

Profitable over Cycles …

49 55 62 83 83 54 64 94 102 114 89

39,273 48,108 60,531 83,047 89,471

66,666 78,726 121,530 137,208 132,985

105,608

Sales volume (‘000 nos)

Sale revenue (gross) (in Rs.mn)

Profit after tax (PAT) (in Rs.mn)

Note: Figures mentioned above are standalone. Sales volume includes MHCV, LCV and defence vehicle volumes. Revenues include aftermarket business as well Source: SIAM, Company Audited Financials

7

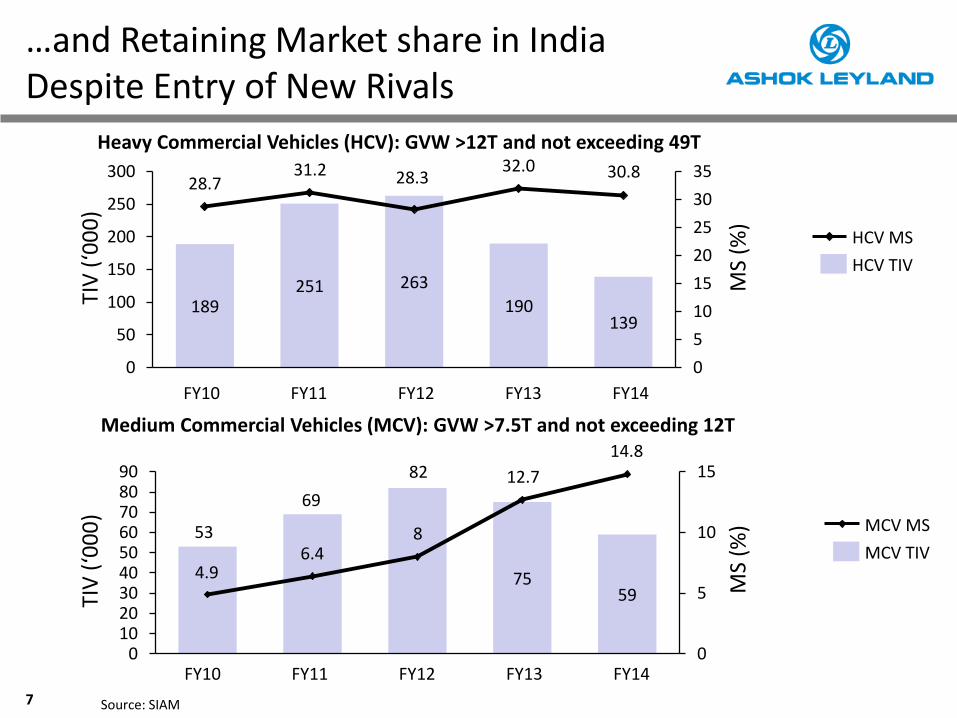

Heavy Commercial Vehicles (HCV): GVW >12T and not exceeding 49T

Medium Commercial Vehicles (MCV): GVW >7.5T and not exceeding 12T

189 251 263

190 139

28.7 31.2 28.3

32.0 30.8

0

5

10

15

20

25

30

35

0

50

100

150

200

250

300

FY10 FY11 FY12 FY14 FY13

HCV TIV

HCV MS

82

75 59

4.9 6.4

8

12.7

14.8

0

5

10

15

0102030405060708090

FY11 FY10

53

FY14 FY13 FY12

69

MCV TIV

MCV MS

TIV

(‘0

00

)

MS

(%)

TIV

(‘0

00

)

MS

(%)

…and Retaining Market share in India Despite Entry of New Rivals

Source: SIAM

8

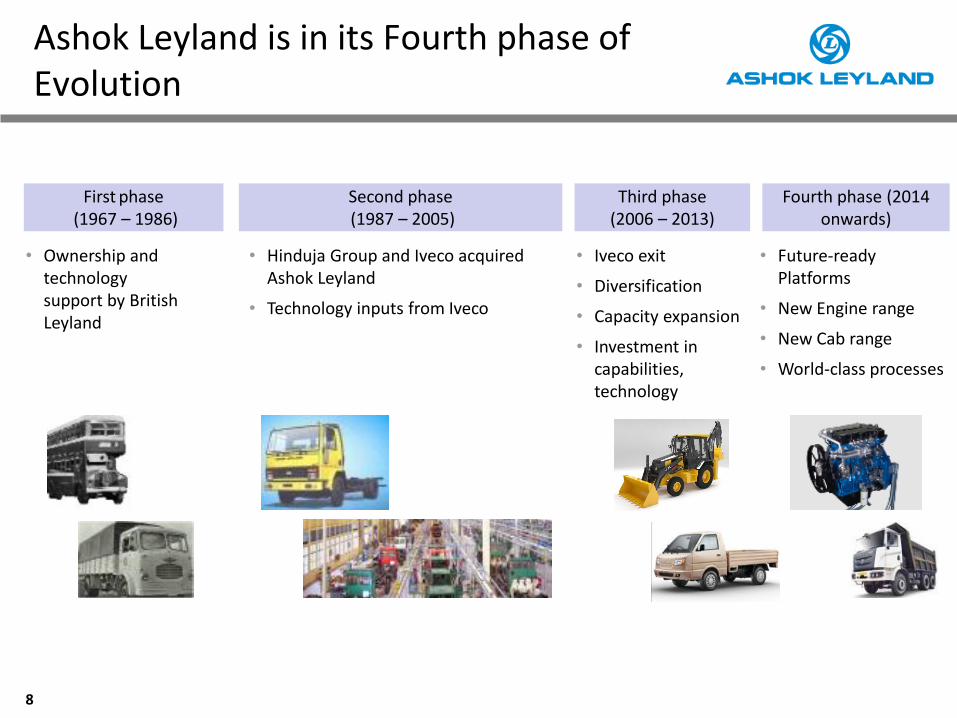

Ashok Leyland is in its Fourth phase of Evolution

First phase (1967 – 1986)

Second phase (1987 – 2005)

Third phase (2006 – 2013)

Fourth phase (2014 onwards)

• Future-ready Platforms

• New Engine range

• New Cab range

• World-class processes

• Ownership and technology support by British Leyland

• Hinduja Group and Iveco acquired Ashok Leyland

• Technology inputs from Iveco

• Iveco exit

• Diversification

• Capacity expansion

• Investment in capabilities, technology

9

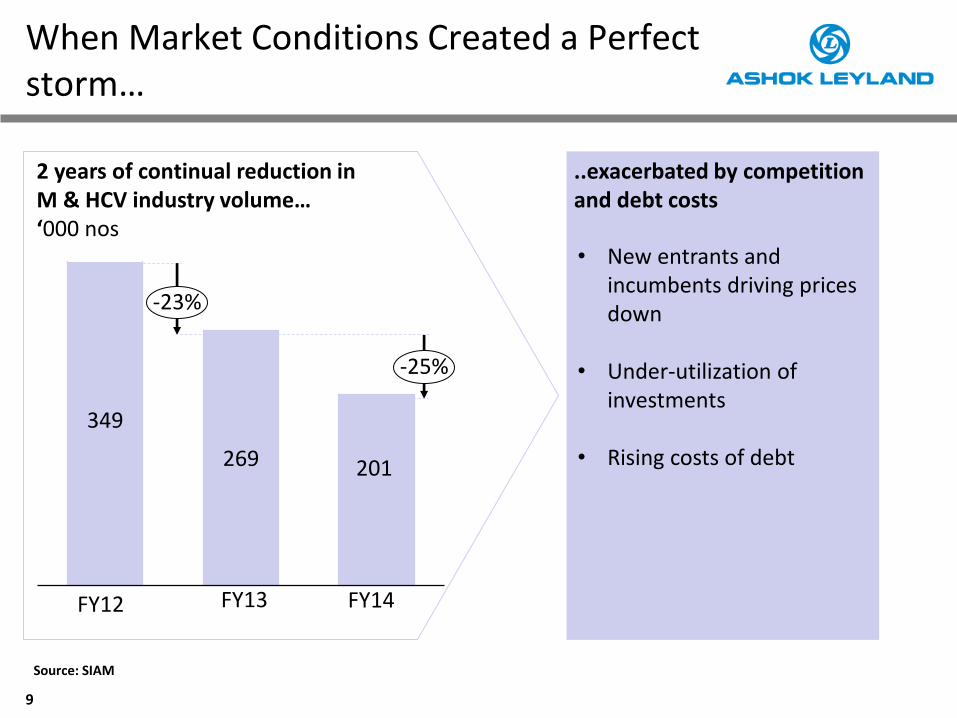

When Market Conditions Created a Perfect storm…

Source: SIAM

• New entrants and

incumbents driving prices down

• Under-utilization of investments

• Rising costs of debt

349

269

-25%

FY14 FY13

201

FY12

-23%

2 years of continual reduction in M & HCV industry volume… ‘000 nos

..exacerbated by competition and debt costs

10

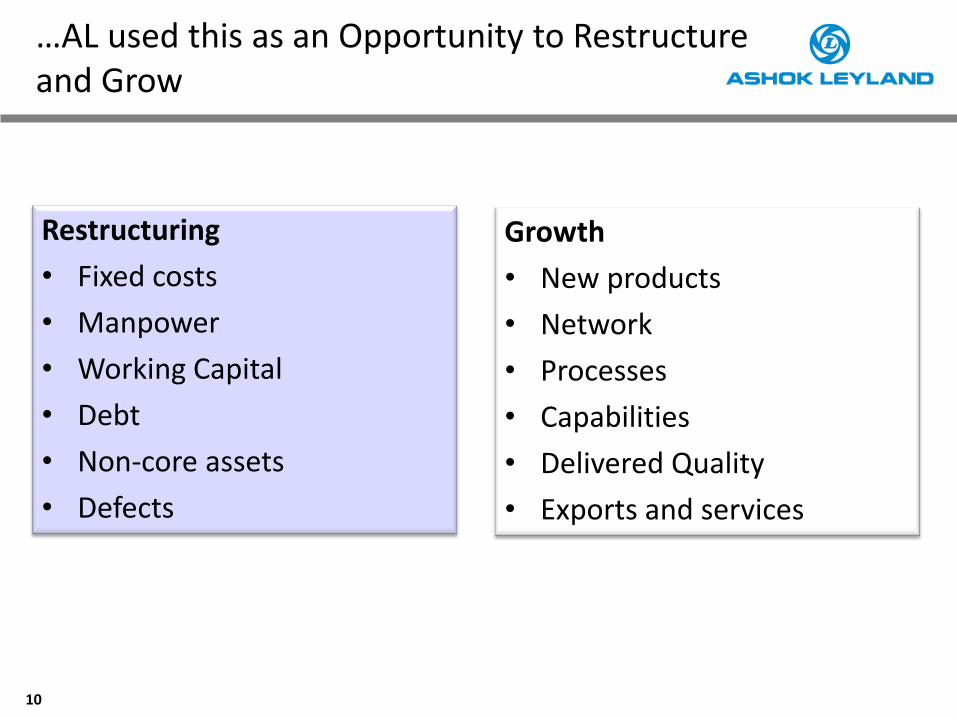

Restructuring

• Fixed costs

• Manpower

• Working Capital

• Debt

• Non-core assets

• Defects

…AL used this as an Opportunity to Restructure and Grow

Growth

• New products

• Network

• Processes

• Capabilities

• Delivered Quality

• Exports and services

11

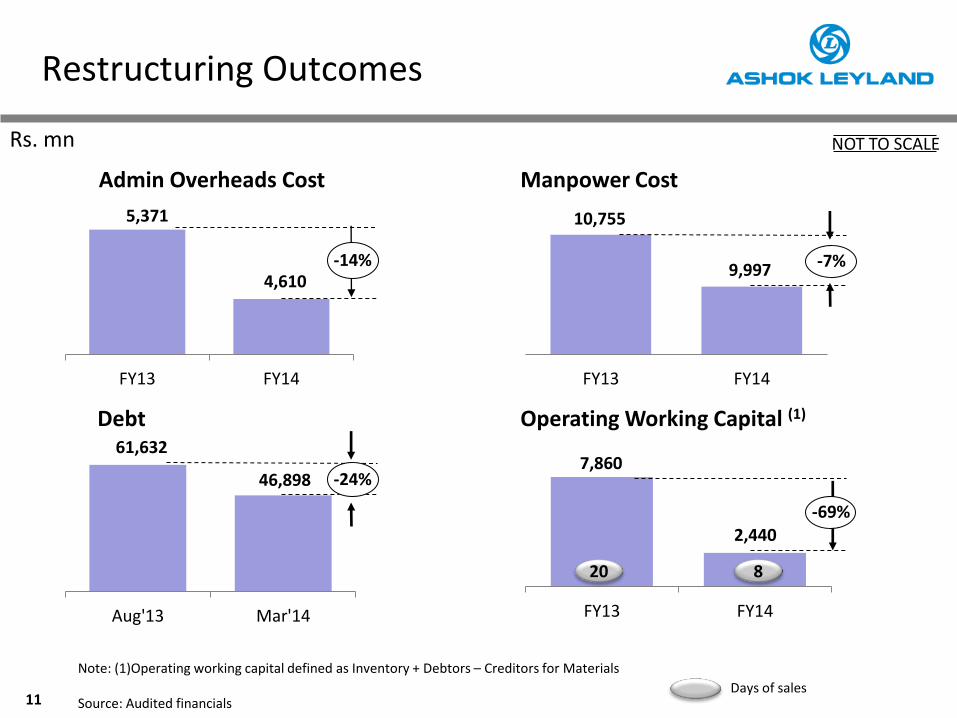

FY13 FY14

Restructuring Outcomes

FY13 FY14

FY13 FY14

Admin Overheads Cost Manpower Cost

Operating Working Capital (1)

-7%

Note: (1)Operating working capital defined as Inventory + Debtors – Creditors for Materials Source: Audited financials

-69%

20 8

Days of sales

10,755

9,997

7,860

2,440

5,371

4,610

Aug'13 Mar'14

61,632

46,898 -24%

Debt

Rs. mn

-14%

NOT TO SCALE

12

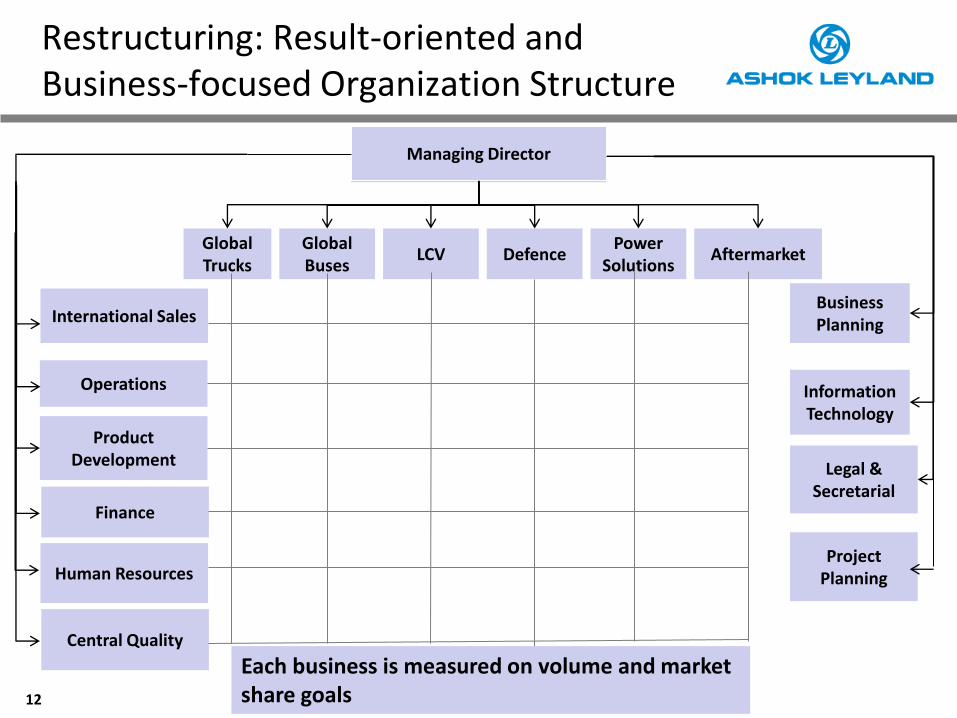

Restructuring: Result-oriented and Business-focused Organization Structure

Managing Director

Global Buses

LCV Defence

Operations

Product Development

Finance

Human Resources

Business Planning

Information Technology

Legal & Secretarial

Project Planning

Central Quality

International Sales

Managing Director

Power Solutions

Aftermarket Global Trucks

Each business is measured on volume and market share goals

13

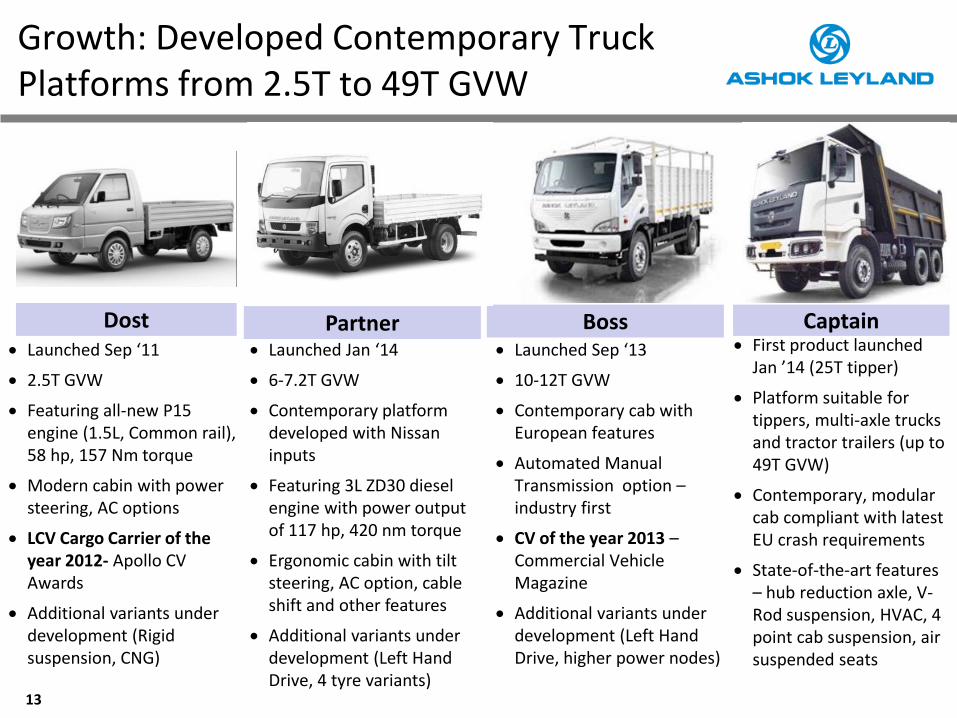

Launched Sep ‘13

10-12T GVW

Contemporary cab with European features

Automated Manual Transmission option – industry first

CV of the year 2013 – Commercial Vehicle Magazine

Additional variants under development (Left Hand Drive, higher power nodes)

Boss First product launched

Jan ’14 (25T tipper)

Platform suitable for tippers, multi-axle trucks and tractor trailers (up to 49T GVW)

Contemporary, modular cab compliant with latest EU crash requirements

State-of-the-art features – hub reduction axle, V-Rod suspension, HVAC, 4 point cab suspension, air suspended seats

Captain

Growth: Developed Contemporary Truck Platforms from 2.5T to 49T GVW

Partner Launched Jan ‘14

6-7.2T GVW

Contemporary platform developed with Nissan inputs

Featuring 3L ZD30 diesel engine with power output of 117 hp, 420 nm torque

Ergonomic cabin with tilt steering, AC option, cable shift and other features

Additional variants under development (Left Hand Drive, 4 tyre variants)

Dost Launched Sep ‘11

2.5T GVW

Featuring all-new P15 engine (1.5L, Common rail), 58 hp, 157 Nm torque

Modern cabin with power steering, AC options

LCV Cargo Carrier of the year 2012- Apollo CV Awards

Additional variants under development (Rigid suspension, CNG)

14

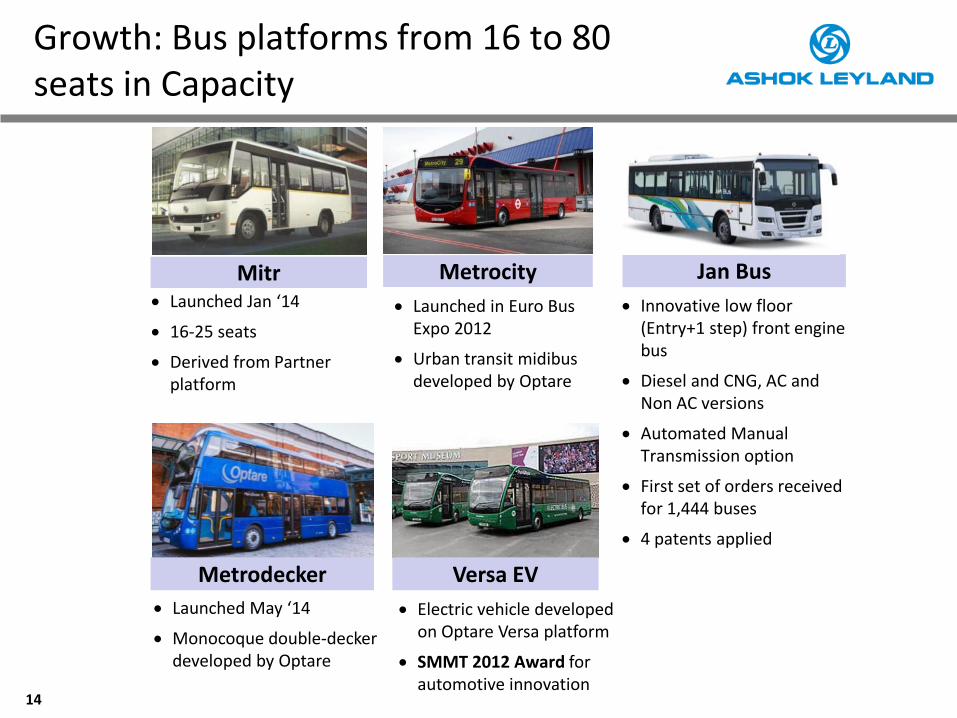

Launched Jan ‘14

16-25 seats

Derived from Partner platform

Mitr

Innovative low floor (Entry+1 step) front engine bus

Diesel and CNG, AC and Non AC versions

Automated Manual Transmission option

First set of orders received for 1,444 buses

4 patents applied

Jan Bus

Growth: Bus platforms from 16 to 80 seats in Capacity

Metrodecker

Launched May ‘14

Monocoque double-decker developed by Optare

Metrocity

Launched in Euro Bus Expo 2012

Urban transit midibus developed by Optare

Versa EV

Electric vehicle developed on Optare Versa platform

SMMT 2012 Award for automotive innovation

15

5.3L 4 Cyl and 8L 6 Cyl engines

160-360 hp, 600 -1475 nm, flat torque curves

3rd generation common rail, 4 valves/ cylinder

Available in Euro 3, Euro 4, upgradable to Euro 5, 6

Launched in Vehicles and Power Solutions

Neptune

Growth: Critical Aggregates Engineered to Support Future Growth

1.5L 3 cyl engine

58 hp, 157.5 Nm Torque

Common Rail direct injection

Available in Euro 3, Euro 4, CNG variants

Applied in Dost light commercial vehicles

Variants offering higher power and torque under development

P15 H Series 3.8L 4 cyl and 6L 6 cyl

engines

120-230 hp range, 500-850 Nm torque

Mechanical and Common Rail options

Upgraded to Euro 3, Euro 4 and CNG Variants

Widely used across most current and upcoming vehicle platforms and power solutions

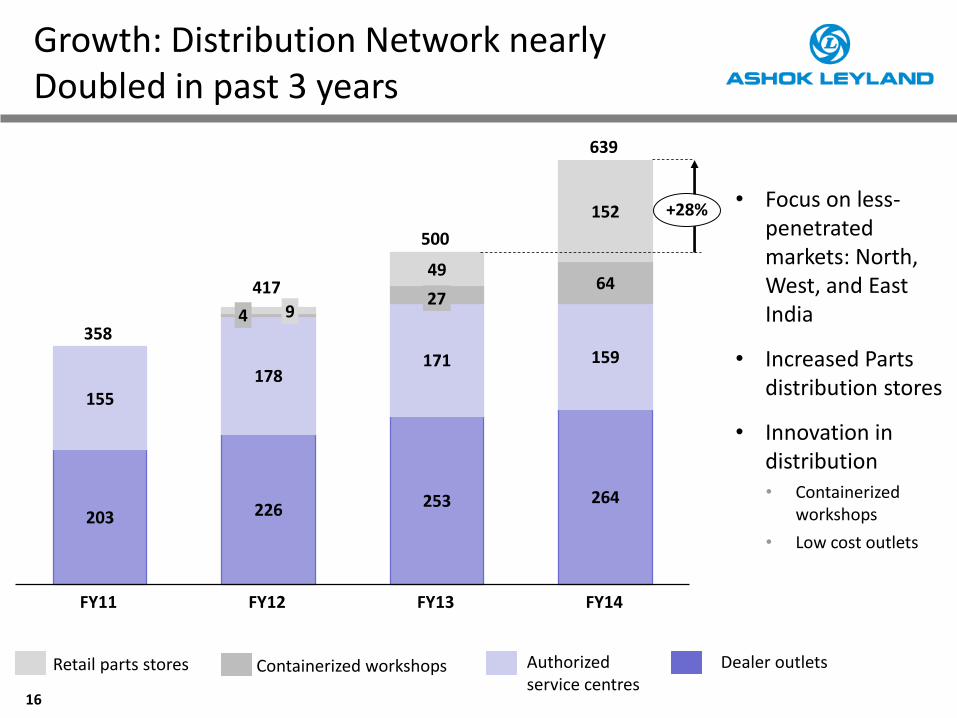

16

203 226 253 264

155 178

171 159

64 49

152

639

+28%

FY14 FY13

4 9

FY11

358

FY12

417 27

500

Dealer outlets Containerized workshops Authorized service centres

Retail parts stores

Growth: Distribution Network nearly Doubled in past 3 years

• Focus on less-penetrated markets: North, West, and East India

• Increased Parts distribution stores

• Innovation in distribution • Containerized

workshops

• Low cost outlets

17

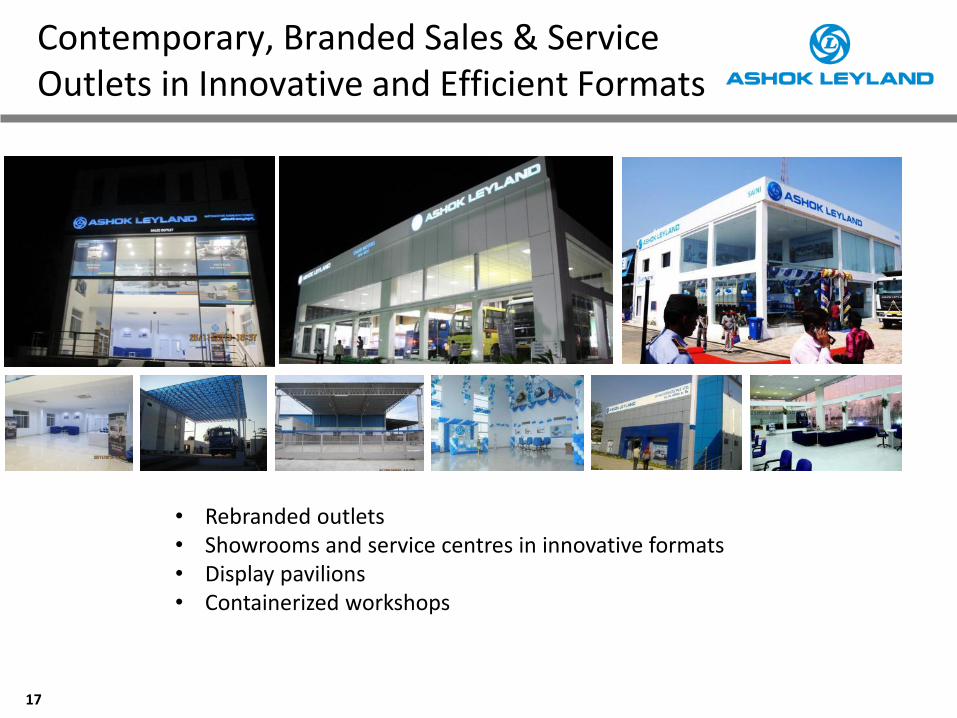

Contemporary, Branded Sales & Service Outlets in Innovative and Efficient Formats

• Rebranded outlets • Showrooms and service centres in innovative formats • Display pavilions • Containerized workshops

18

Growth: New Processes Implemented across the Value Chain

Design and Development

Manufacturing Sales and Marketing

PSales and Marketing Excellence

RISM

• Portfolio of shop-floor initiatives for continuous workplace improvement

• Initiatives across productivity, safety, cost, quality and other metrics

• New product development process , benchmarked against global best-practices through external consultants

• ‘Stage-gate’ process , enabling development first time right

• Breakthrough process focusing on improving process efficiency in front end marketing, sales. service and spares delivery

• Developed with inputs from leading consultants

SAP driven business transformation driving business process efficiency – Implementation completed across all functions, verticals

19

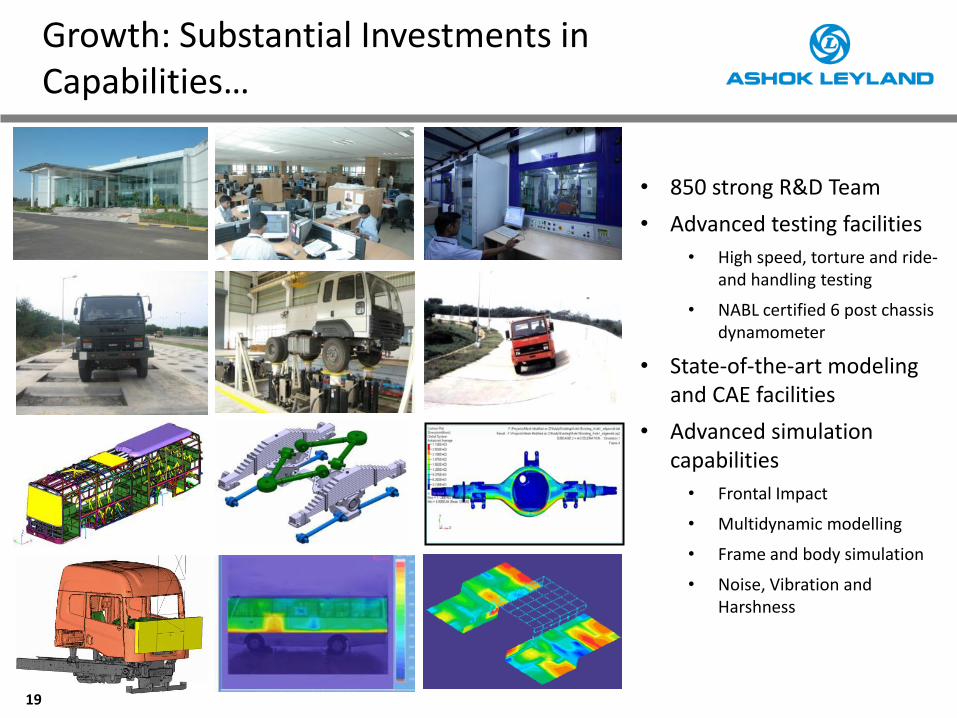

Growth: Substantial Investments in Capabilities…

• 850 strong R&D Team

• Advanced testing facilities

• High speed, torture and ride-and handling testing

• NABL certified 6 post chassis dynamometer

• State-of-the-art modeling and CAE facilities

• Advanced simulation capabilities

• Frontal Impact

• Multidynamic modelling

• Frame and body simulation

• Noise, Vibration and Harshness

20

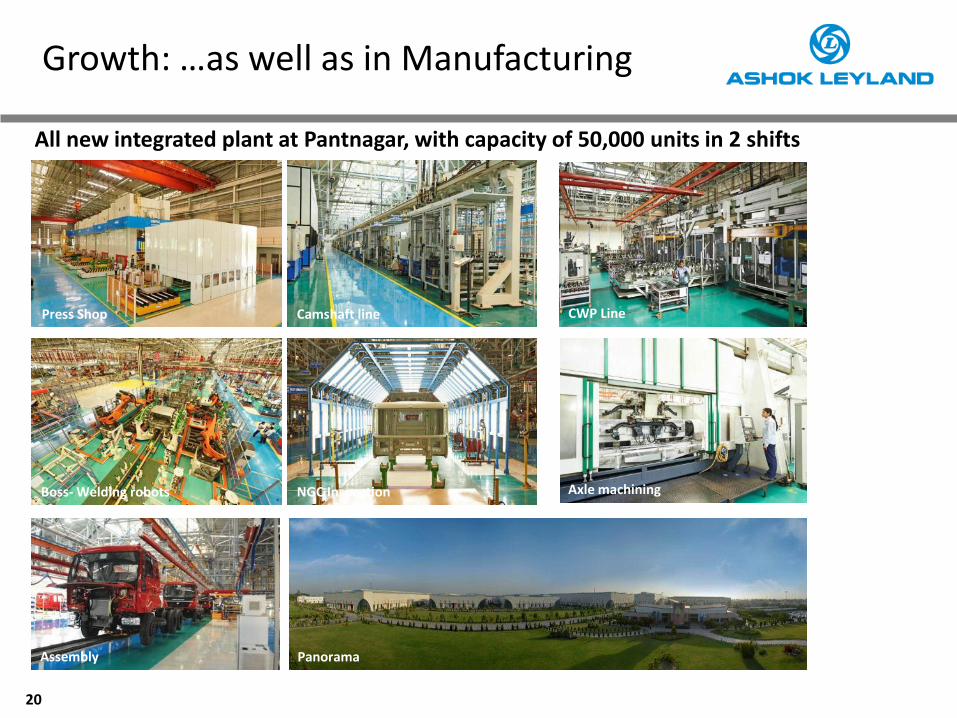

Growth: …as well as in Manufacturing

All new integrated plant at Pantnagar, with capacity of 50,000 units in 2 shifts

Press Shop Camshaft line CWP Line

Boss- Welding robots NGC Inspection Axle machining

Assembly Panorama

21

Growth: Enhancement in Delivered Quality

Vehicle delivered factory-fresh… …with zero km on odometer

22 Source: Audited financials * EBITDA & EBITDA Margin Excludes other income

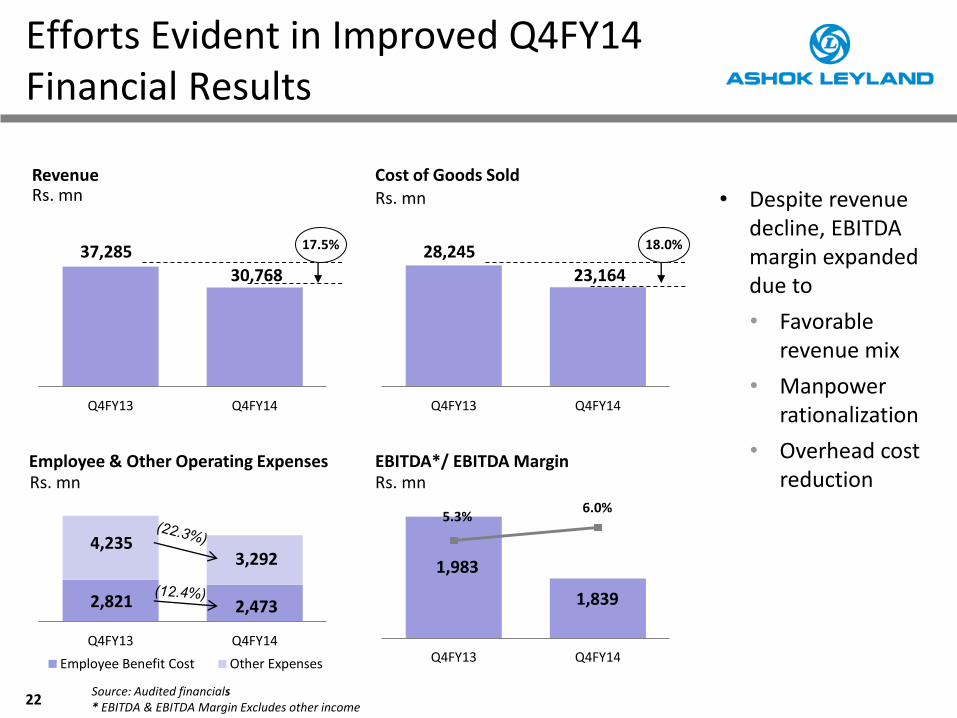

Efforts Evident in Improved Q4FY14 Financial Results

Cost of Goods Sold Revenue

EBITDA*/ EBITDA Margin Employee & Other Operating Expenses

Rs. mn

Rs. mn Rs. mn

Rs. mn

Q4FY13 Q4FY14

37,285

30,768

17.5%

Q4FY13 Q4FY14

28,245

23,164

18.0%

Q4FY13 Q4FY14

Employee Benefit Cost Other Expenses Q4FY13 Q4FY14

1,983

1,839

4,235 3,292

2,821 2,473

5.3% 6.0%

• Despite revenue decline, EBITDA margin expanded due to

• Favorable revenue mix

• Manpower rationalization

• Overhead cost reduction

23

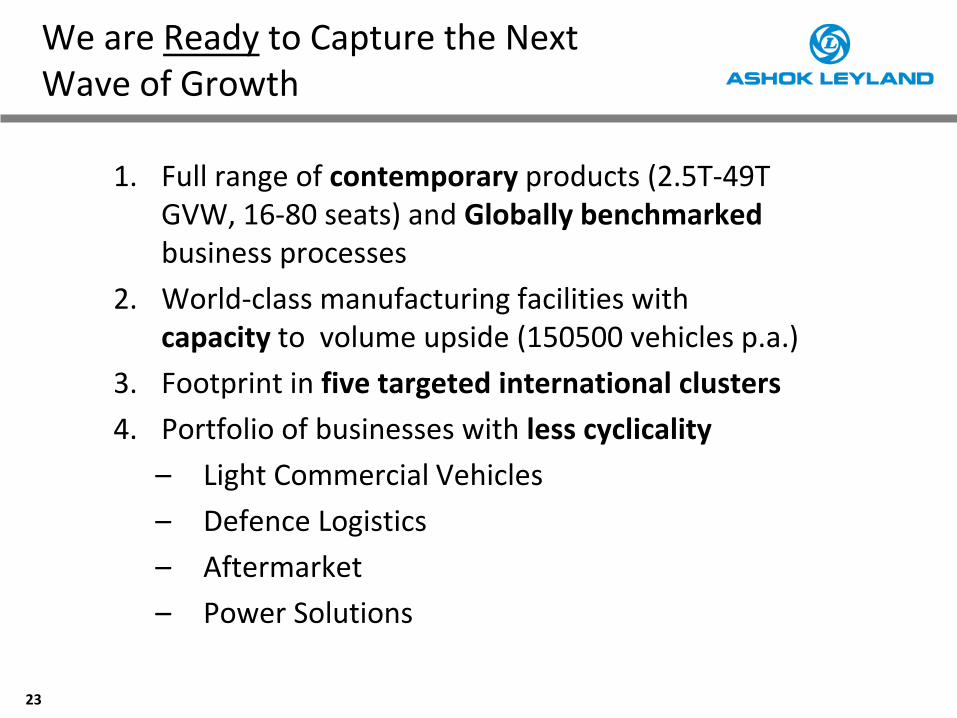

We are Ready to Capture the Next Wave of Growth

1. Full range of contemporary products (2.5T-49T GVW, 16-80 seats) and Globally benchmarked business processes

2. World-class manufacturing facilities with capacity to volume upside (150500 vehicles p.a.)

3. Footprint in five targeted international clusters

4. Portfolio of businesses with less cyclicality

– Light Commercial Vehicles

– Defence Logistics

– Aftermarket

– Power Solutions

24

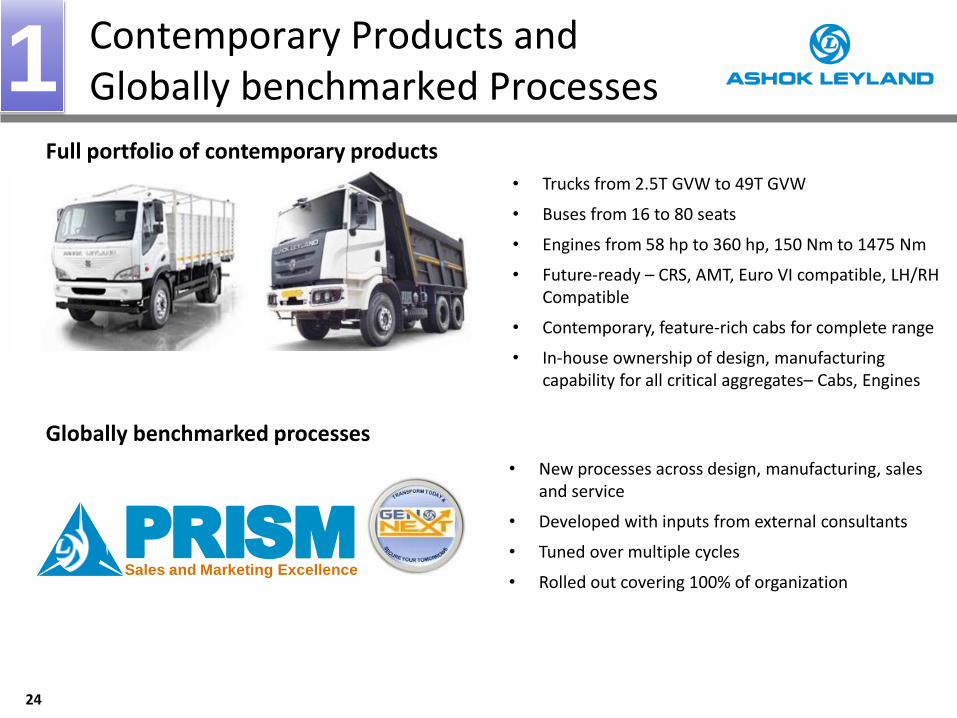

Contemporary Products and Globally benchmarked Processes

PSales and Marketing Excellence

RISM

Full portfolio of contemporary products

Globally benchmarked processes

• Trucks from 2.5T GVW to 49T GVW

• Buses from 16 to 80 seats

• Engines from 58 hp to 360 hp, 150 Nm to 1475 Nm

• Future-ready – CRS, AMT, Euro VI compatible, LH/RH Compatible

• Contemporary, feature-rich cabs for complete range

• In-house ownership of design, manufacturing capability for all critical aggregates– Cabs, Engines

• New processes across design, manufacturing, sales and service

• Developed with inputs from external consultants

• Tuned over multiple cycles

• Rolled out covering 100% of organization

1

25

World-class Manufacturing Facilities with Capacity to Capture Demand Upside

UAE: Bus

manufacturing in

partnership with

RAKIA

Ashok Leyland, India • Seven facilities with capacity of 150500

per annum

• Fully integrated plant at Pantnagar

• Fully built bus facility at Alwar

• Revamped machining and assembly facility at Ennore

• Hosur facilities revamped for LCV manufacture AL UAE LLC, Ras Al Khaimah, UAE

• Established as a JV with Ras Al Khaimah Investment Authority

• Well-equipped vehicle manufacturing facility

• Capacity 2000 per year, expandable with limited investments

Optare PLC, Leeds, UK

• Modern assembly line bus body facility

• Replaces dated facilities used previously by Optare

• Capable of assembling diesel, hybrid and electric buses

UK: Optare bus

manufacturing

facility

India: Six

manufacturing

facilities with total

capacity of 150500

vehicles p.a.

2

26

Growing Footprint in Five Targeted International Clusters

26

Commonwealth of Independent States

ASEAN

South America

Africa

Added since 2009 Present for over 5 years

Not present

Middle-East

• Bus assembly facility at Ras-Al-Khaimah

• Channel partners in multiple GCC nations

• Selling substantial number of buses

• Importer company established in Chile

• Sales commenced in Peru

• Bus body building partners in the Ukraine

• Avia Russia office in place, sales commenced

• Company in Nigeria, branch in Kenya

• Local assembler in Nigeria, Channel partners in Kenya

• Regular sales underway- trucks and buses

• Limited direct sales

• Partners selection underway

3

27

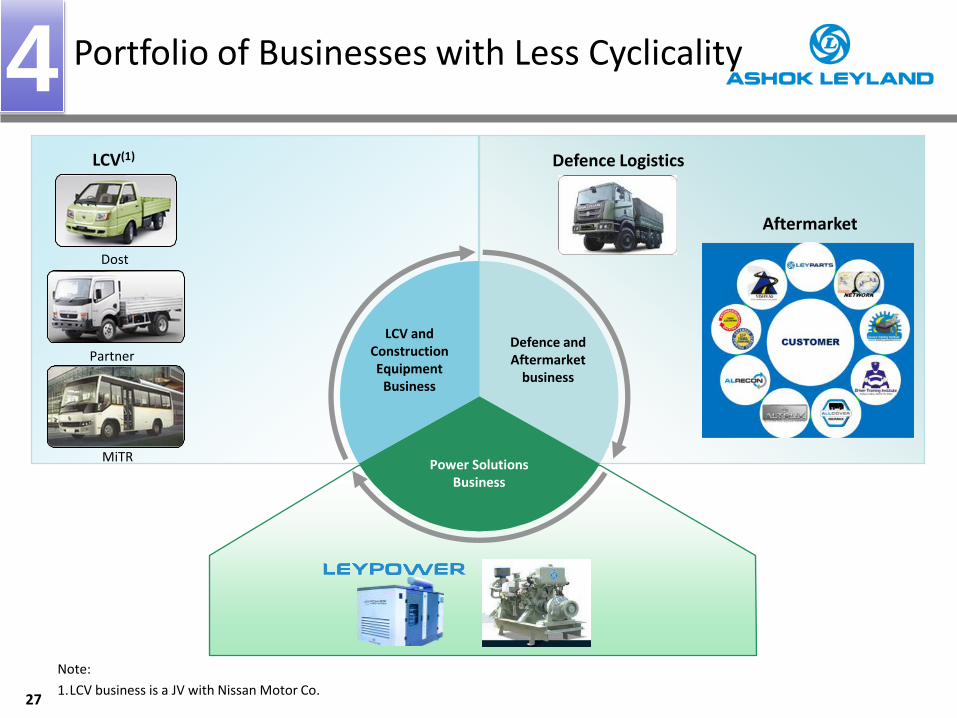

LCV and Construction Equipment

Business

Defence and Aftermarket

business

Power Solutions Business

LCV(1)

Portfolio of Businesses with Less Cyclicality

Note:

1.LCV business is a JV with Nissan Motor Co.

Partner

Dost

Defence Logistics

Aftermarket

MiTR

4

28

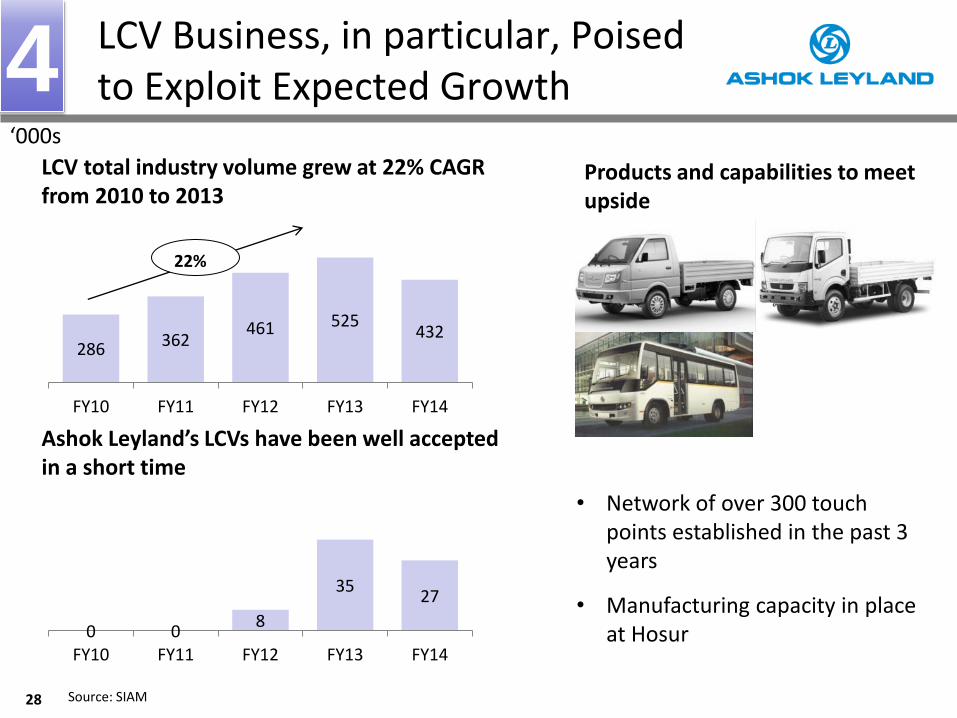

LCV Business, in particular, Poised to Exploit Expected Growth

Products and capabilities to meet upside

LCV total industry volume grew at 22% CAGR from 2010 to 2013

Ashok Leyland’s LCVs have been well accepted in a short time

286 362 461 525

432

FY10 FY11 FY12 FY13 FY14

22%

0 0 8

35 27

FY10 FY11 FY12 FY13 FY14

• Network of over 300 touch points established in the past 3 years

• Manufacturing capacity in place at Hosur

‘000s

Source: SIAM

4

29

Platforms and Capabilities for Growth in Defence Business Products

Stallion 4X4

Stallion 6X6

Super Stallion 6X6

Super Stallion 8X8

Prototypes under development

Garuda 4X4 Super Stallion 6X6 - New Cab

10X10

Capabilities

Prototype facility, Sengadu

Plant, Hosur

4

30

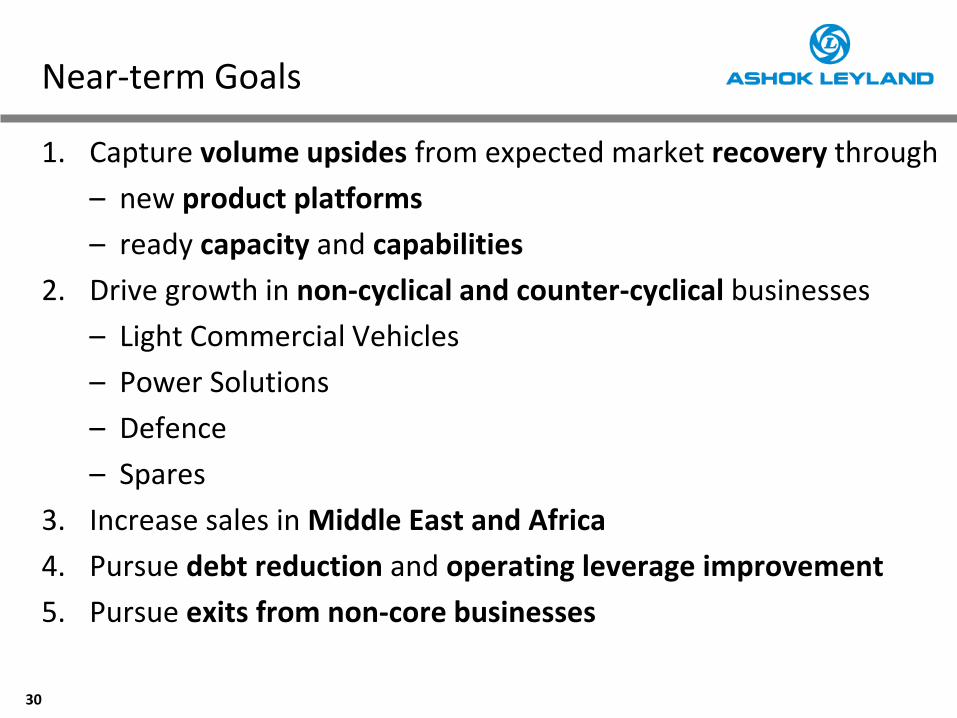

Near-term Goals

1. Capture volume upsides from expected market recovery through

– new product platforms

– ready capacity and capabilities

2. Drive growth in non-cyclical and counter-cyclical businesses

– Light Commercial Vehicles

– Power Solutions

– Defence

– Spares

3. Increase sales in Middle East and Africa

4. Pursue debt reduction and operating leverage improvement

5. Pursue exits from non-core businesses

31

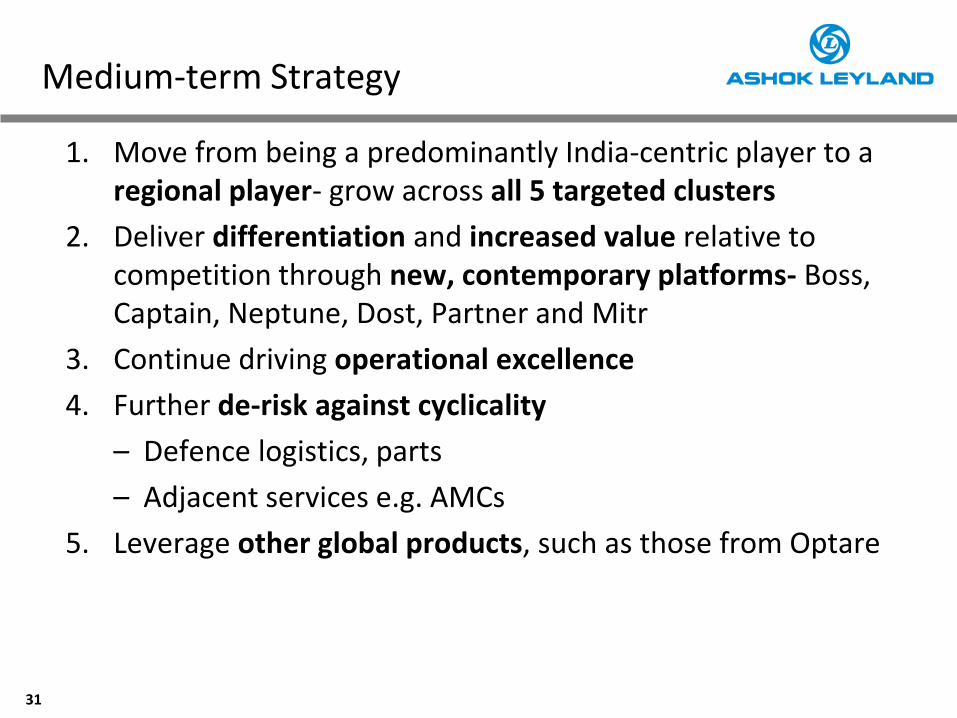

Medium-term Strategy

1. Move from being a predominantly India-centric player to a regional player- grow across all 5 targeted clusters

2. Deliver differentiation and increased value relative to competition through new, contemporary platforms- Boss, Captain, Neptune, Dost, Partner and Mitr

3. Continue driving operational excellence

4. Further de-risk against cyclicality

– Defence logistics, parts

– Adjacent services e.g. AMCs

5. Leverage other global products, such as those from Optare

32

Summary Take-aways

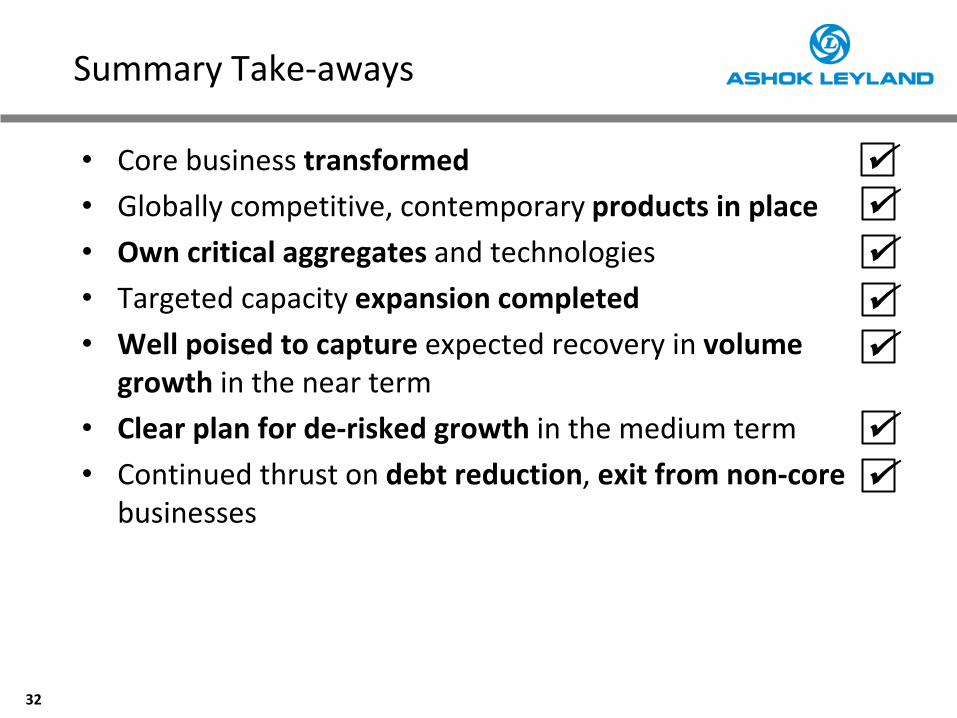

• Core business transformed

• Globally competitive, contemporary products in place

• Own critical aggregates and technologies

• Targeted capacity expansion completed

• Well poised to capture expected recovery in volume growth in the near term

• Clear plan for de-risked growth in the medium term

• Continued thrust on debt reduction, exit from non-core businesses

33

APPENDIX

34

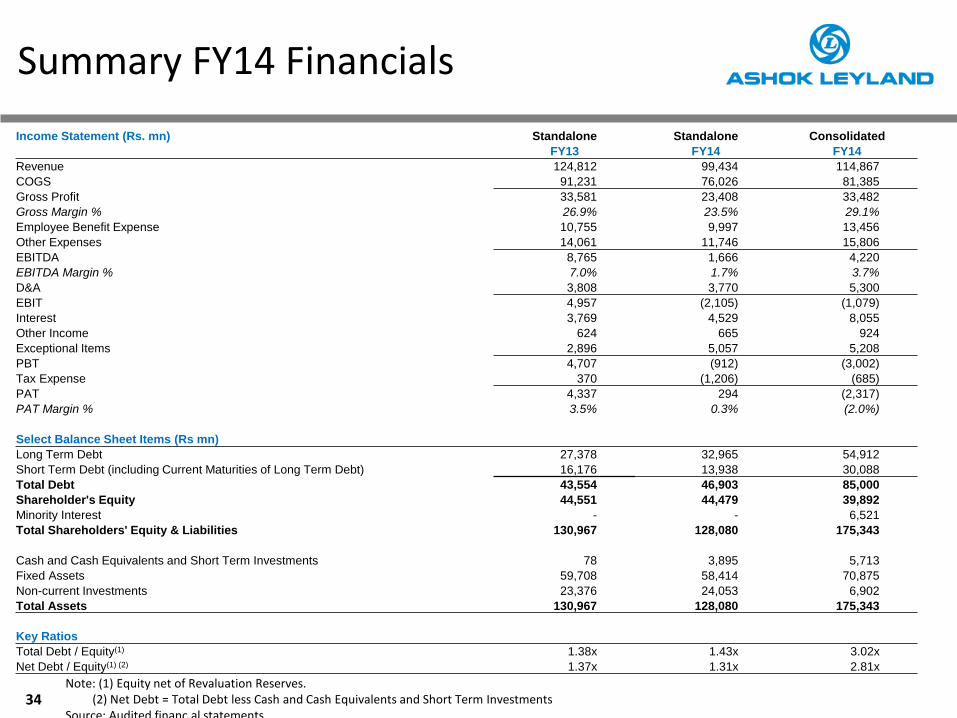

Summary FY14 Financials

Income Statement (Rs. mn) Standalone Standalone Consolidated

FY13 FY14 FY14

Revenue 124,812 99,434 114,867

COGS 91,231 76,026 81,385

Gross Profit 33,581 23,408 33,482

Gross Margin % 26.9% 23.5% 29.1%

Employee Benefit Expense 10,755 9,997 13,456

Other Expenses 14,061 11,746 15,806

EBITDA 8,765 1,666 4,220

EBITDA Margin % 7.0% 1.7% 3.7%

D&A 3,808 3,770 5,300

EBIT 4,957 (2,105) (1,079)

Interest 3,769 4,529 8,055

Other Income 624 665 924

Exceptional Items 2,896 5,057 5,208

PBT 4,707 (912) (3,002)

Tax Expense 370 (1,206) (685)

PAT 4,337 294 (2,317)

PAT Margin % 3.5% 0.3% (2.0%)

Select Balance Sheet Items (Rs mn)

Long Term Debt 27,378 32,965 54,912

Short Term Debt (including Current Maturities of Long Term Debt) 16,176 13,938 30,088

Total Debt 43,554 46,903 85,000

Shareholder's Equity 44,551 44,479 39,892

Minority Interest - - 6,521

Total Shareholders' Equity & Liabilities 130,967 128,080 175,343

Cash and Cash Equivalents and Short Term Investments 78 3,895 5,713

Fixed Assets 59,708 58,414 70,875

Non-current Investments 23,376 24,053 6,902

Total Assets 130,967 128,080 175,343

Key Ratios

Total Debt / Equity(1) 1.38x 1.43x 3.02x

Net Debt / Equity(1) (2) 1.37x 1.31x 2.81x

Note: (1) Equity net of Revaluation Reserves. (2) Net Debt = Total Debt less Cash and Cash Equivalents and Short Term Investments Source: Audited financ.al statements

35

Thank You

Recommended