ACKNOWLEDGEMENTS

This report would not have been possible without the 49 states responding to the

in-depth state assessment earlier this year. The Center is tremendously thankful

for the states on the State Engagement Subcommittee (AL, DC, CT, FL, IA, MD,

MO, NE, NJ, OK, TX, and UT) for helping shape the on-line questionnaire. The

Center is extremely grateful for USDOL’s input, and commitment to helping

states combat UI fraud and improper payments. The Center’s Steering

Committee (CO, FL, MT, NE, NJ, NY, OH, SC, TX, UT, and WA) also supported the

State Engagement effort and played an important role for the issuance of this

report. Finally, Members of the State Engagement Team: Brian Langley—Team

Lead, UI SMEs: Laura Boyett, Maria Nobel, Christine Paquette, and Bill Starks,

Center Project Director, Randy Gillespie, and Senior Policy Advisor, Jim Van

Erden.

2

UNEMPLOYMENT INSURANCE

DETAILED INTEGRITY STATE ASSESSMENT REPORT November 2016

Executive Summary

The 2016 Unemployment Insurance (UI) Integrity Detailed Assessment is a

snapshot in time of current state efforts to combat UI fraud and improper

payments, their integrity tools, and related procedures. The responses to this

assessment may not portray all of the integrity tools and practices currently

being discussed or employed by the states as the assessment questions targeted

specific integrity functions.

This report is the second state assessment report developed under the National

Association of State Workforce Agencies (NASWA)’s UI Integrity Center (Center)

State Engagement effort. The State Engagement effort involves states in Center

activities with the goal of improving UI integrity. These activities include state

assessments and reporting on current integrity efforts, convening states in

regularly scheduled information sharing sessions, and creating a model integrity

operational blueprint to inform and guide states’ integrity efforts.

The information gathered through the 2016 assessment, and others, will be a

catalyst for a series of white papers on integrity topics of most interest to the UI

community. All of the assessment information will ultimately be loaded into a

fully accessible, continuously maintained, State Portfolio Data Base (SPD). The

SPD application will provide an interactive resource of state integrity practices

for easier consumption and use by the states. The SPD will be available early

next year through the UI Community of Practice Integrity tab on the Center’s

website. The SPD application in the Center’s Digital Library will allow states to

exchange state-specific information as it relates to UI fraud and improper

payments.

The 2016 state assessment is more robust than the 2015 version, with fifty main

questions and over one hundred subset questions depending on how the main

questions were answered. The assessment was released to states earlier this

year with 49 states completing the on-line in-depth state assessment resulting in

a ninety-four percent response rate.

The responses show that states are making in-roads in implementing new tools

and processes to help identify UI fraudulent activities, reduce UI improper

payments, and strengthen trust fund solvency. This report also highlights a

continuing need for future outreach to states to gather additional information

and clarify existing procedures and tools.

3

Table of Contents Executive Summary ................................................................................................................................................... 2

The 2016 State Integrity Assessment............................................................................................................................. 5

Operations Section ......................................................................................................................................................... 7

Q1) Does your state have a shareable copy of your UI agency’s organizational chart? ............................................ 7

Q2) Does your state verify out-of-state work registration? ....................................................................................... 7

Q3) Does your state have an automated case management system for the UI Benefit Payment Control (BPC) unit?

................................................................................................................................................................................... 8

Q4) Adjudication - Does your BPC Unit issue determinations? ................................................................................ 9

Q5) Does your state use the SIDES Earnings Verification system (E-Response)? ................................................. 10

Q6) Has your state modified its integrity messaging in the last twelve months? .................................................... 10

Protocol (IP) Address Section ..................................................................................................................................... 12

Q7) As part of your state’s UI process, does your state capture a claimant’s or employer’s IP address? ............... 12

Q8) Does your state screen IP addresses? ................................................................................................................ 13

Q9) Some states have a repository for a "hot" IP address list for known bad or prior fraudulent IP address. Does

your state compile a "hot" IP address list? ............................................................................................................... 17

Q10) Does your state have a process for verifying IP addresses that are "masked" or filed from a proxy server? . 18

Training Section .......................................................................................................................................................... 19

Q11) Does your state UI agency offer training programs specific to addressing BPC or UI integrity issues

designed to prevent, detect, and recover improper payments (both fraud and non-fraud)? ..................................... 19

Recoupment Section .................................................................................................................................................... 21

Q12) Does your state currently participate in TOP to collect delinquent UI employer tax debts? .......................... 21

Q13) Does your state use any outside data sources or tools for locating (skip tracing) debtors' most current

address? ................................................................................................................................................................... 22

Q14) Does your state have an automated collections case management system (separate and apart from your

automated billing system)? ...................................................................................................................................... 23

Q15) Does your state have any automated processes for contacting debtors to recover benefit overpayments or tax

debts? ....................................................................................................................................................................... 24

Q16) Does your state allow electronic payment options on overpayments or tax debts? ........................................ 25

Q17) Does your state have a State Income Tax offset program? ............................................................................. 26

Q18) Does your state actively recover UI benefit overpayments through wage garnishments issued to the

claimant's current employer(s)? ............................................................................................................................... 26

Q19) Does your state actively process liens or levy bank accounts on overpayments or tax debts? ....................... 27

Q20) Does your state leverage the issuance and/or renewal of any business or professional licenses to recover UI

overpayment and/or delinquent employer tax debts? .............................................................................................. 28

Q21) What other sources are actively used to recover UI overpayments and/or delinquent employer tax debts? .. 28

Q22) Does your state actively file adversary proceedings objecting to the discharge of fraudulent UI

overpayments in bankruptcy? .................................................................................................................................. 30

Q23) Does your state require certain employers to post a cash bond amount to ensure future tax debts are paid? . 30

Q24) Does your state refer or contract out UI debt recovery? ................................................................................. 31

Q25) What other collection actions does your state find motivating for employers or claimants to settle their UI

debts? ....................................................................................................................................................................... 32

4

Prosecution Section ..................................................................................................................................................... 34

Q26) Does your state prosecute for criminal charges on UI fraud overpayment cases? .......................................... 34

Q27) Does your state prosecute for criminal charges on employer tax cases? ........................................................ 35

Q29) Does your state use law enforcement officers to support the criminal prosecution of UI fraud cases? .......... 37

Data Analytics and Predictive Modeling Section ........................................................................................................ 38

Q30) Does your state use predictive modeling for fraud prevention and detection? ............................................... 38

Q31) Does your state use data analytics for fraud prevention and detection? ......................................................... 40

Q32) Does your state have any Standard Operating Procedures or other documentation of work processes used in

conjunction with your data analytics and predictive modeling applications that could be shared with the Center? 42

Cross Match Section .................................................................................................................................................... 43

Q33) Does your UI agency cross match with your state’s State Directory of New Hires (SDNH)? ....................... 43

Q34) Which UI claims does your state run against the National Directory of New Hires (NDNH)? ..................... 45

Q35) What is the frequency of your cross match with the NDNH? ........................................................................ 46

Q36) Does your state UI agency cross match against incarceration data? ............................................................... 46

Q37) Does your state have an agreement in place with the U.S. Social Security Administration to access

their Prisoner Update Processing System (PUPS) information? .............................................................................. 47

Q38) Does your state cross match Continued Claims against death records or the U.S. Social Security

Administration's Death Master File (DMF)? ........................................................................................................... 47

Q39) Does your state run a cross match on death records or the Death Master File against claimants with existing

overpayments? ......................................................................................................................................................... 48

Q40) Does your state conduct fictitious employer detection cross matches? .......................................................... 49

Q41) Does your state's quarterly wage cross match run more than once a quarter? ................................................ 50

Q42) As it relates to cross matches being run, does your state have a process (automated or not) for prioritizing

hits to investigators as workload assignments? ....................................................................................................... 52

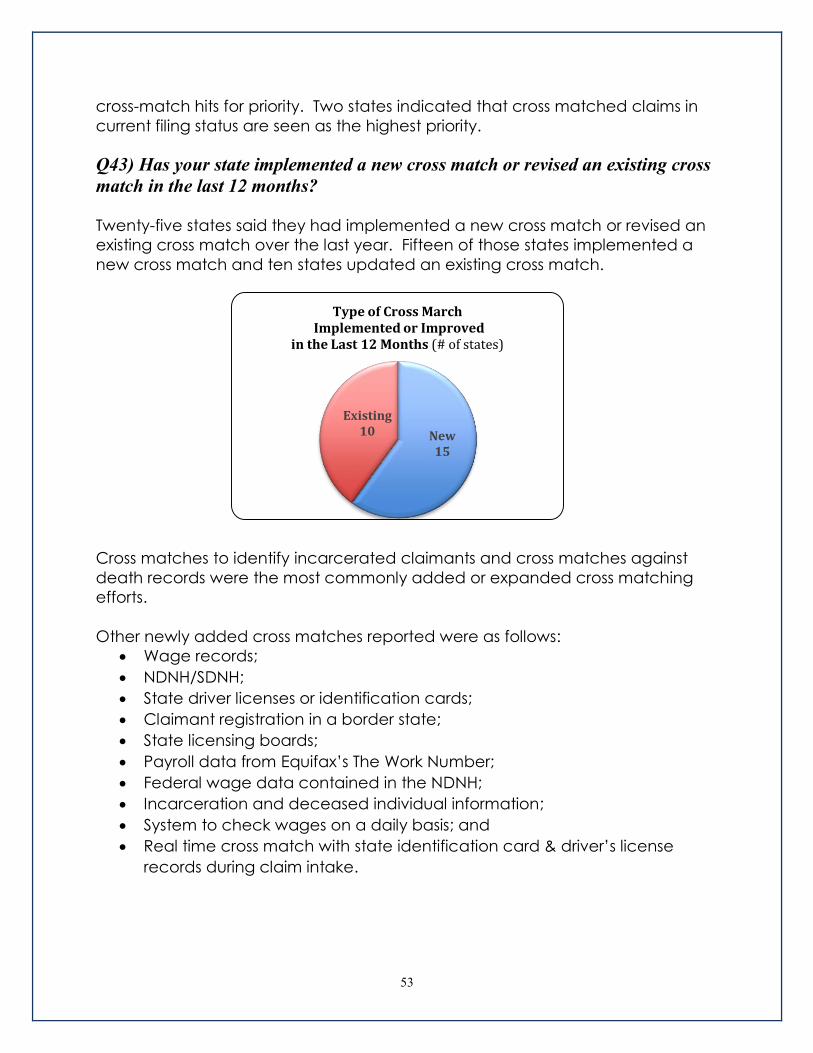

Q43) Has your state implemented a new cross match or revised an existing cross match in the last 12 months?... 53

ID Verification Section ................................................................................................................................................ 55

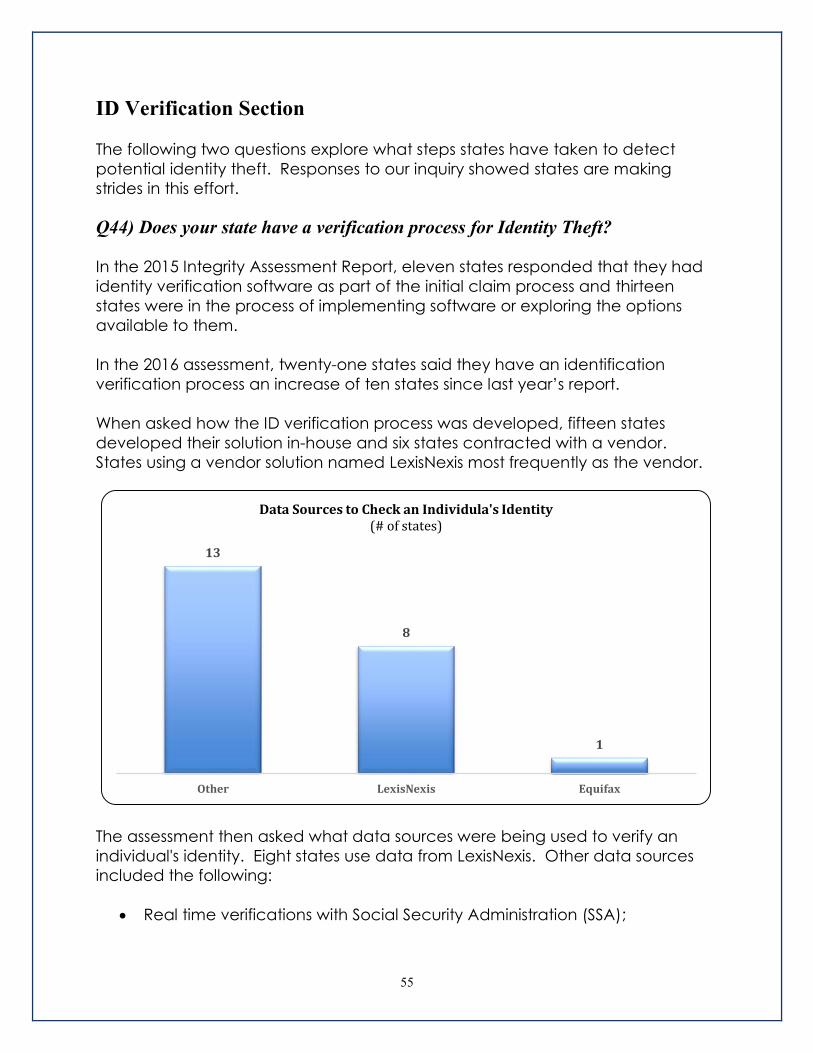

Q44) Does your state have a verification process for Identity Theft? ..................................................................... 55

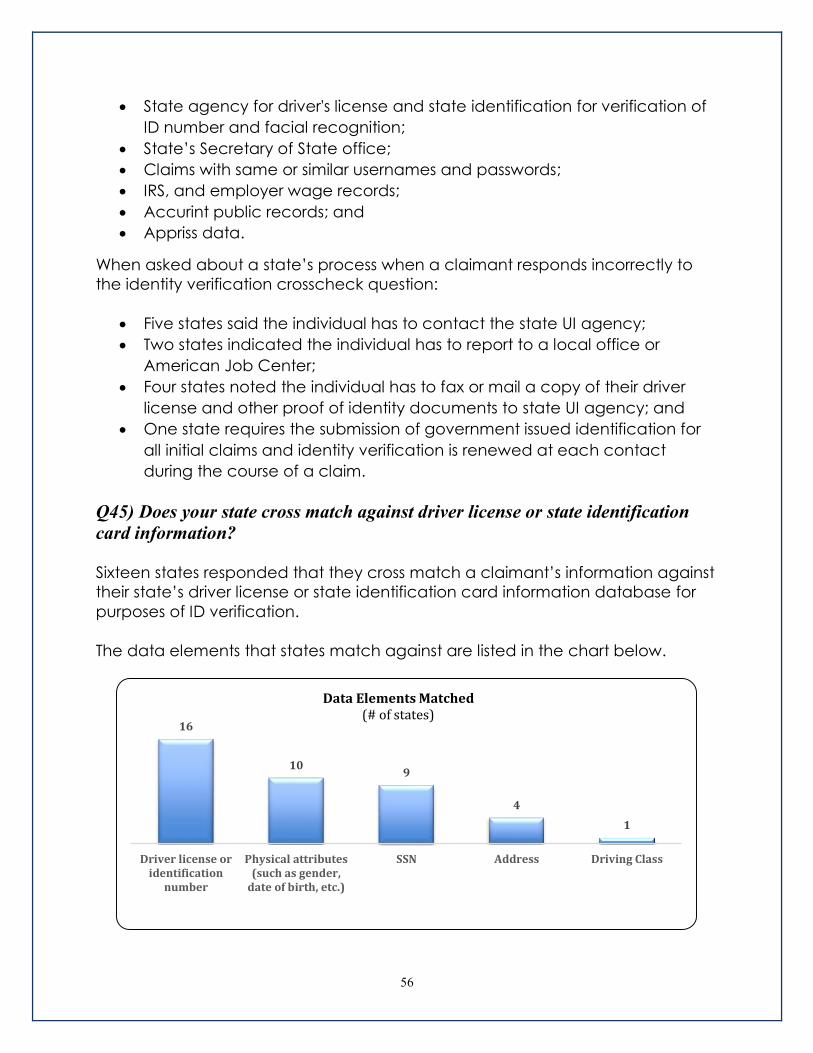

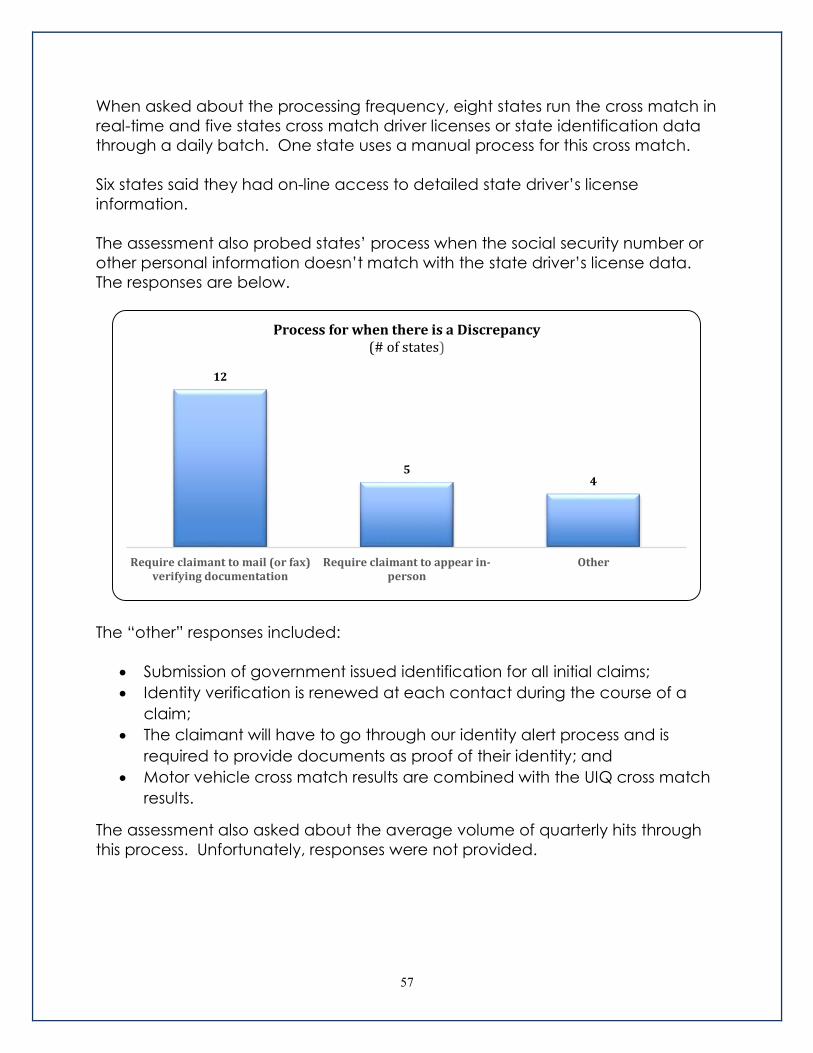

Q45) Does your state cross match against driver license or state identification card information? ......................... 56

Integrity Data Hub Section .......................................................................................................................................... 58

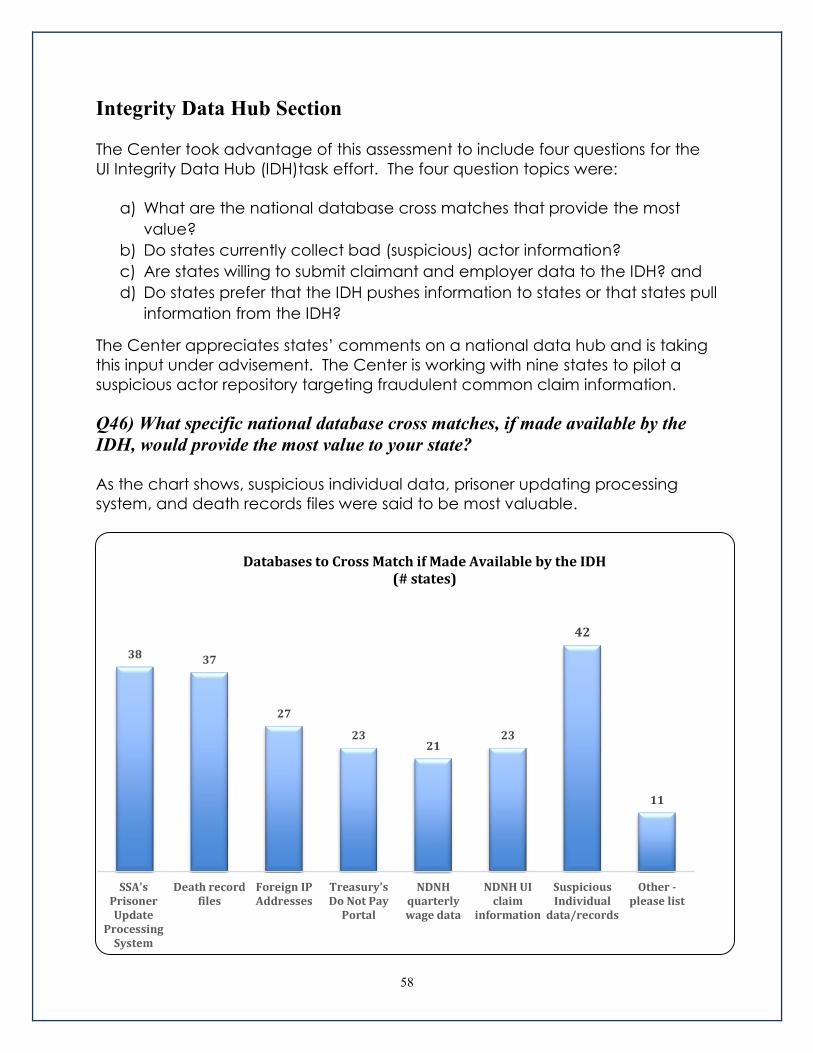

Q46) What specific national database cross matches, if made available by the IDH, would provide the most value

to your state? ............................................................................................................................................................ 58

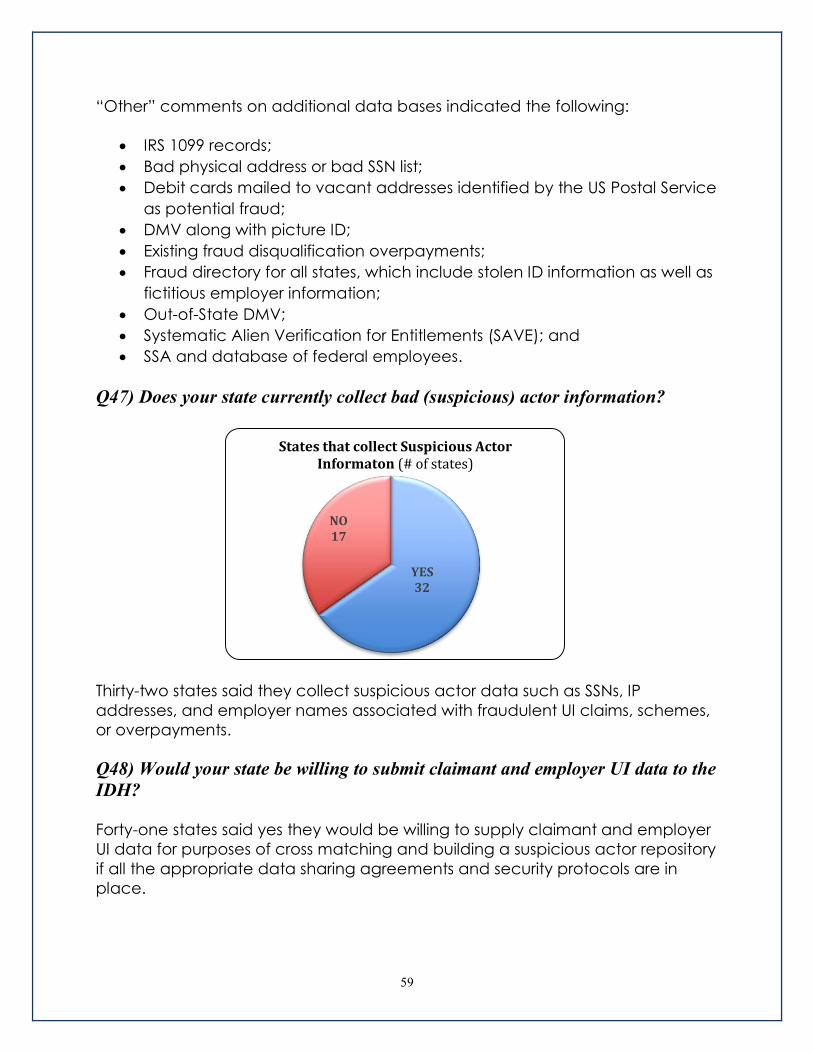

Q47) Does your state currently collect bad (suspicious) actor information? ........................................................... 59

Q48) Would your state be willing to submit claimant and employer UI data to the IDH? ...................................... 59

Q49) Do states prefer that the Data Hub pushes information to states or that states pull information from the Data

Hub. ......................................................................................................................................................................... 60

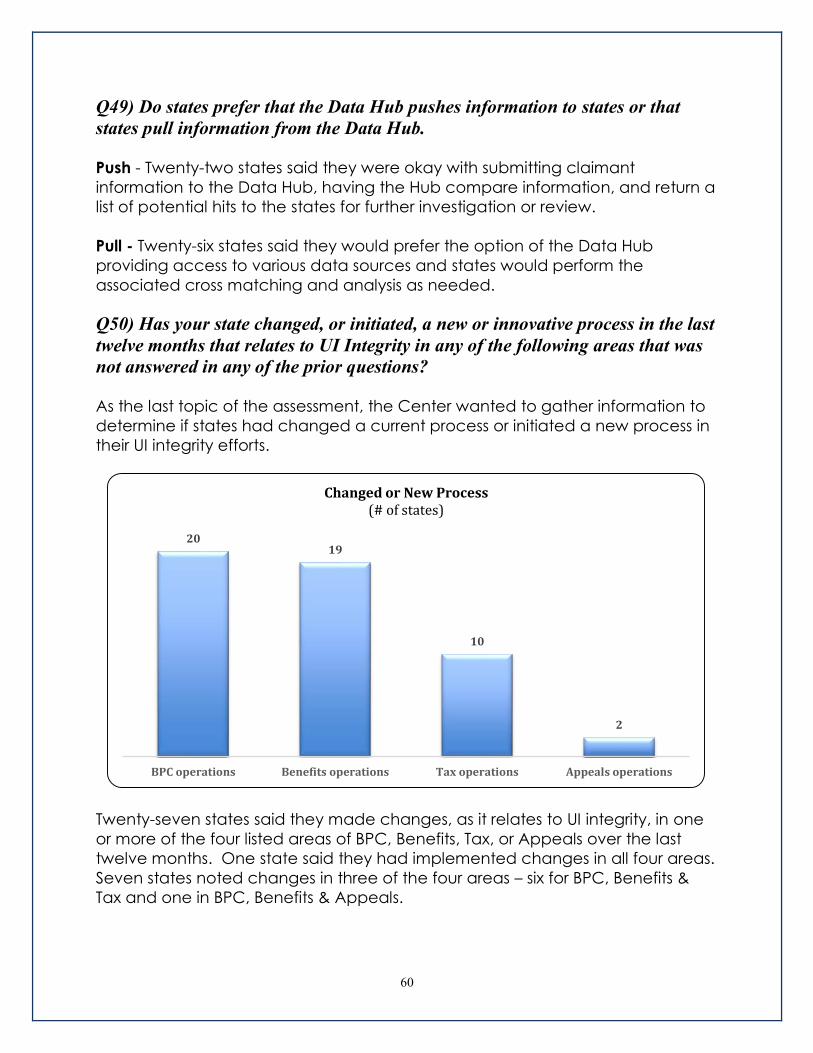

Q50) Has your state changed, or initiated, a new or innovative process in the last twelve months that relates to UI

Integrity in any of the following areas that was not answered in any of the prior questions? ................................. 60

Conclusion ................................................................................................................................................................... 63

Future Efforts ........................................................................................................................................................... 63

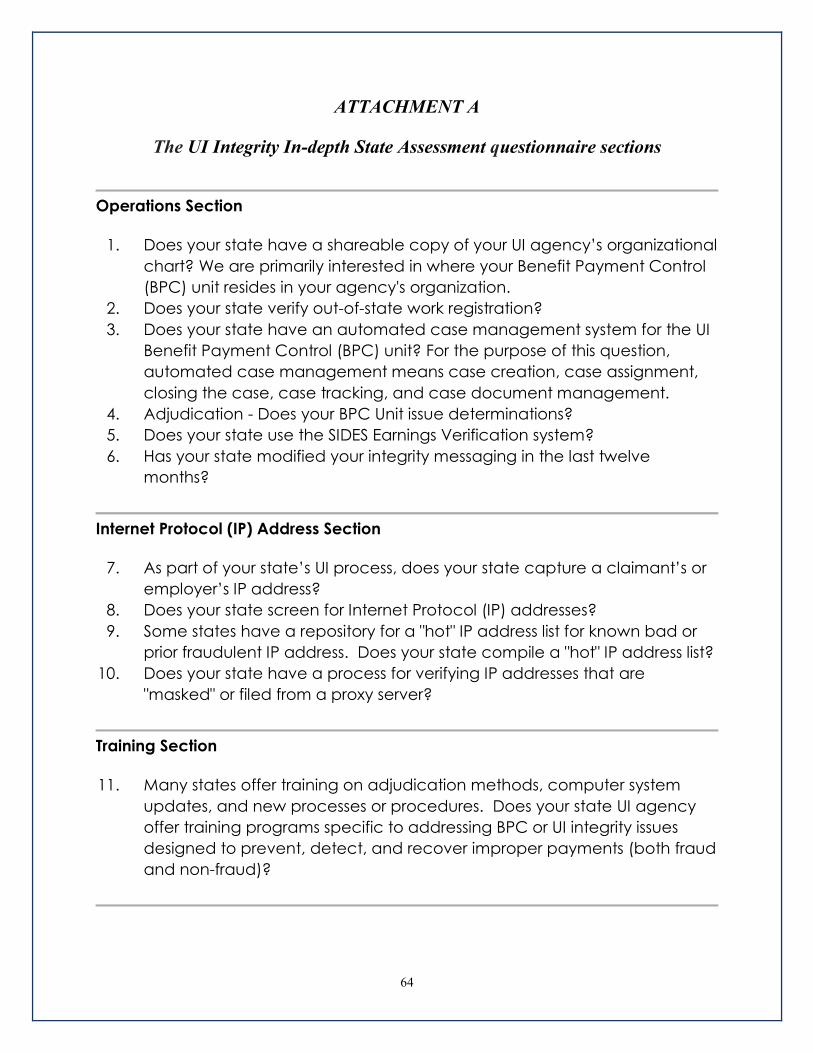

ATTACHMENT A .................................................................................................................................................. 64

The UI Integrity In-depth State Assessment questionnaire sections ........................................................................ 64

5

The 2016 State Integrity Assessment

The Center is a joint Federal and State initiative through NASWA, funded by the

U.S. Department of Labor, to assist states in their efforts to improve integrity in

their unemployment insurance programs. The Center’s mission is to be a source

for integrity strategies, information, and resources, focusing particularly on the

prevention, detection, and recovery of improper payments, fraud and

delinquent employer contributions.

The completion of this assessment and accompanying report falls under the

Center’s State Engagement effort, a cornerstone of the Center’s mission. This

report facilitates that effort by gathering and sharing integrity-related

information among states.

The 2016 Unemployment Insurance Integrity Detailed Assessment Report (IDAR)

describes the inventory of specific UI integrity practices, tools, and strategies

currently used in state operations. This report is the second in a continuing series

of state assessment reports with the first completed and published in October

2015.

This IDAR is divided into nine main sections including:

Operations;

Internet Protocol (IP) Usage;

Training;

Benefit Recoupment;

Fraud Prosecutions;

Predictive Modeling and Data Analytics;

Data Cross matching;

Identity Verification; and

Integrity Data Hub.

The information gathered through this assessment, and other state polling, will

serve as a catalyst for upcoming white papers on integrity topics of most interest

to the UI community. All of the assessment information will ultimately be loaded

into a fully accessible, continuously maintained SPD application of state integrity

practices for easier consumption and use by the states. The information will be

available early next year through the UI Community of Practice Integrity tab on

the Center’s website.

The 2016 IDAR contains fifty primary questions and more than one hundred

subset questions that were addressed depending on how the primary questions

were answered. While the assessment was comprehensive in nature, the

6

responses from states may not portray all of the integrity tools and practices

currently being discussed or employed.

The assessment was released to states at the end of February 2016 and

responses were complete in April 2016. Forty-nine states completed the on-line

assessment resulting in a ninety-four percent response rate. For an overview of

the assessment questions, please see Appendix A.

For more information on the Center and all of our initiatives, please visit:

https://ui.workforcegps.org/ and click the “Integrity” tab

or

http://www.naswa.org/integrity/.

7

Operations Section

Q1) Does your state have a shareable copy of your UI agency’s organizational

chart?

The Center gathered individual state organizational information to better inform

its work as we continue to map out our engagement strategy. Developing a

better understanding of various state structures throughout the country, and the

roles and responsibilities of each, will be helpful when states assess their own

restructuring needs and/or look for examples of how effective operations are

structured.

Thirty-six states shared a copy of their organizational chart. The information

gathered is not listed in this report but will be made available online through the

SPD application.

Insights gained from a review of the organizational charts include the following:

Twenty-five states have their Benefit Payment Control (BPC), or UI Integrity

unit, report to the UI Director;

Seven states have their BPC, or UI Integrity unit, report to the Agency’s

Commissioner/Director/Secretary; and

Four states have their BPC, or UI Integrity unit, report to a different office

such as the General Council, separate agency division, or split reporting

duties across divisions.

Q2) Does your state verify out-of-state work registration?

One of the leading causes for improper payments occurs when claimants do

not adhere to work registration requirements as prescribed in state laws and

policies. The Center inquired as to what states were doing to verify if interstate

claimants’ had registered for work in the agent state’s public workforce system.

In this assessment, twenty-three states said they verify out-of-state work

registrations as a matter of protocol. Five states identify all out-of-state

claimants and send a notification of the requirement to register for work. In

those states, claimants are given a date to provide proof of their registration. If

no proof is provided, a hold, denial, or adjudication appointment is put on the

claim. Some states have agreements with neighboring states for an automated

interface, whereas other states perform this via a manual process.

8

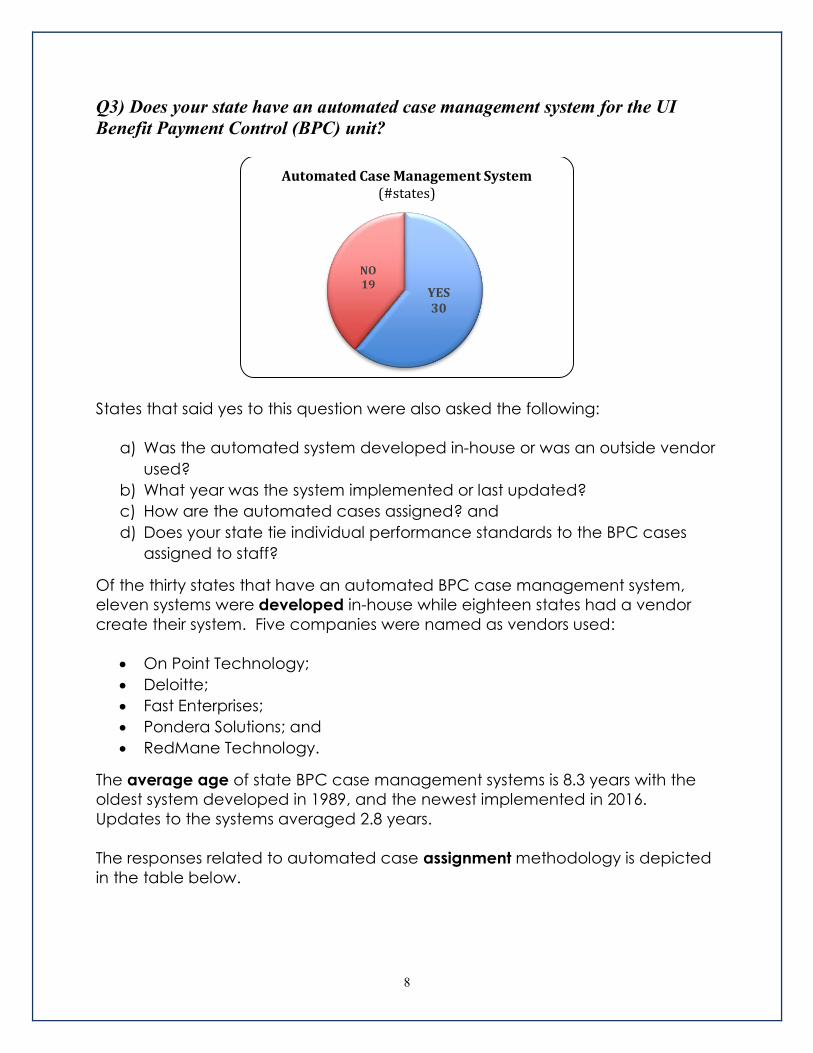

Q3) Does your state have an automated case management system for the UI

Benefit Payment Control (BPC) unit?

States that said yes to this question were also asked the following:

a) Was the automated system developed in-house or was an outside vendor

used?

b) What year was the system implemented or last updated?

c) How are the automated cases assigned? and

d) Does your state tie individual performance standards to the BPC cases

assigned to staff?

Of the thirty states that have an automated BPC case management system,

eleven systems were developed in-house while eighteen states had a vendor

create their system. Five companies were named as vendors used:

On Point Technology;

Deloitte;

Fast Enterprises;

Pondera Solutions; and

RedMane Technology.

The average age of state BPC case management systems is 8.3 years with the

oldest system developed in 1989, and the newest implemented in 2016.

Updates to the systems averaged 2.8 years.

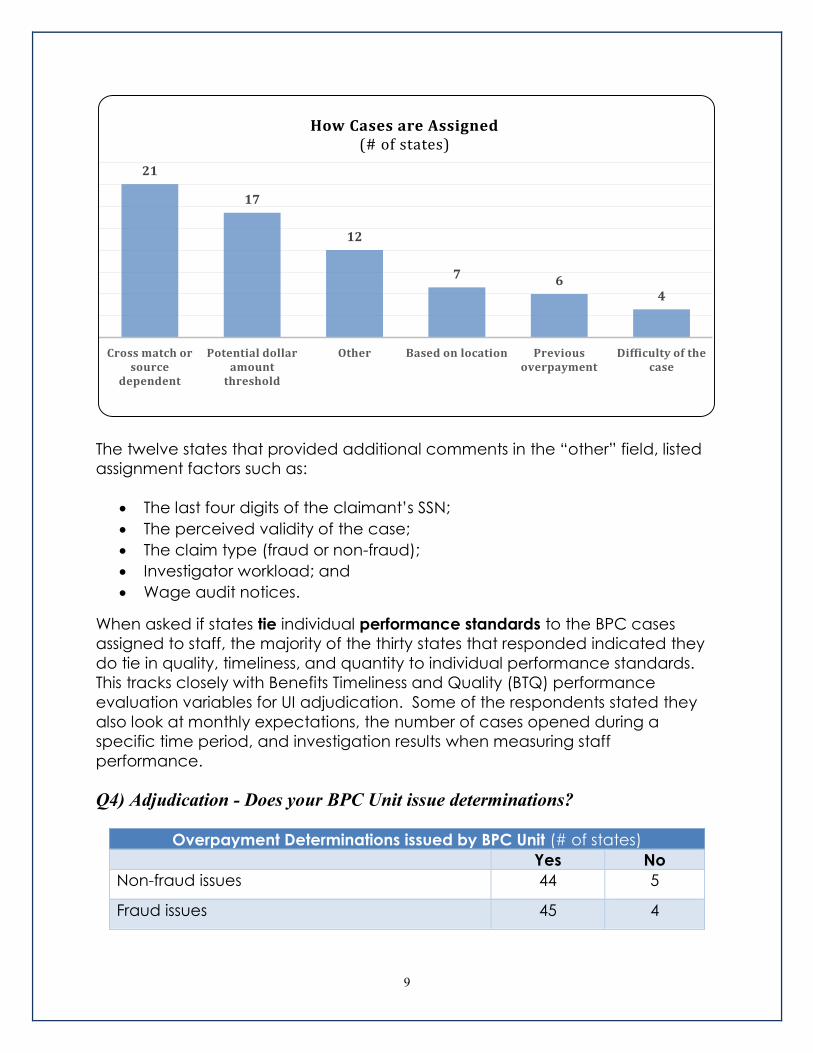

The responses related to automated case assignment methodology is depicted

in the table below.

YES 30

NO19

Automated Case Management System(#states)

9

The twelve states that provided additional comments in the “other” field, listed

assignment factors such as:

The last four digits of the claimant’s SSN;

The perceived validity of the case;

The claim type (fraud or non-fraud);

Investigator workload; and

Wage audit notices.

When asked if states tie individual performance standards to the BPC cases

assigned to staff, the majority of the thirty states that responded indicated they

do tie in quality, timeliness, and quantity to individual performance standards.

This tracks closely with Benefits Timeliness and Quality (BTQ) performance

evaluation variables for UI adjudication. Some of the respondents stated they

also look at monthly expectations, the number of cases opened during a

specific time period, and investigation results when measuring staff

performance.

Q4) Adjudication - Does your BPC Unit issue determinations?

Overpayment Determinations issued by BPC Unit (# of states)

Yes No

Non-fraud issues 44 5

Fraud issues 45 4

21

17

12

7 64

Cross match or source

dependent

Potential dollar amount

threshold

Other Based on location Previous overpayment

Difficulty of the case

How Cases are Assigned (# of states)

10

The majority of states’ BPC units adjudicate both fraud and non-fraud issues. In

addition, one state indicated their agency does not structurally have a BPC unit.

In the 2015 assessment, three common procedures for adjudication were

mentioned:

UI fraud investigative staff adjudicate all issues and refer other non-

monetary issues to another unit;

UI fraud investigative staff adjudicate all non-monetary and fraud/non-

fraud issues for their cases; and

All non-monetary and fraud/non-fraud determinations are made by an

adjudications unit outside the UI fraud or BPC unit.

The state responses this year reinforced the answers to last year’s assessment,

that states’ fraud operations have their investigators adjudicate both fraud and

non-fraud issues once the investigation is complete. A few states forward non-

fraud issues to their regular UI adjudication process.

Q5) Does your state use the SIDES Earnings Verification system (E-Response)?

The SIDES Earnings Verification application automatically sends wage

verification notices to employers through a state specific employer portal. Using

an automated process to communicate and receive information from

employers, provides faster information for weekly wage data allowing states to

more quickly identify if a claimant is working and subsequently failing to report

their weekly earnings. Manual paper responses from employers are less timely

and are a leading cause of overpayments.

The results of state responses demonstrated confusion in answering this question.

It appears respondents didn’t distinguish between the SIDES’ Separation

Information exchange and the SIDES’ Earnings Verification exchange.

For more information about SIDES and E-Response, please visit

http://www.itsc.org/Pages/ui_SIDES_home.aspx.

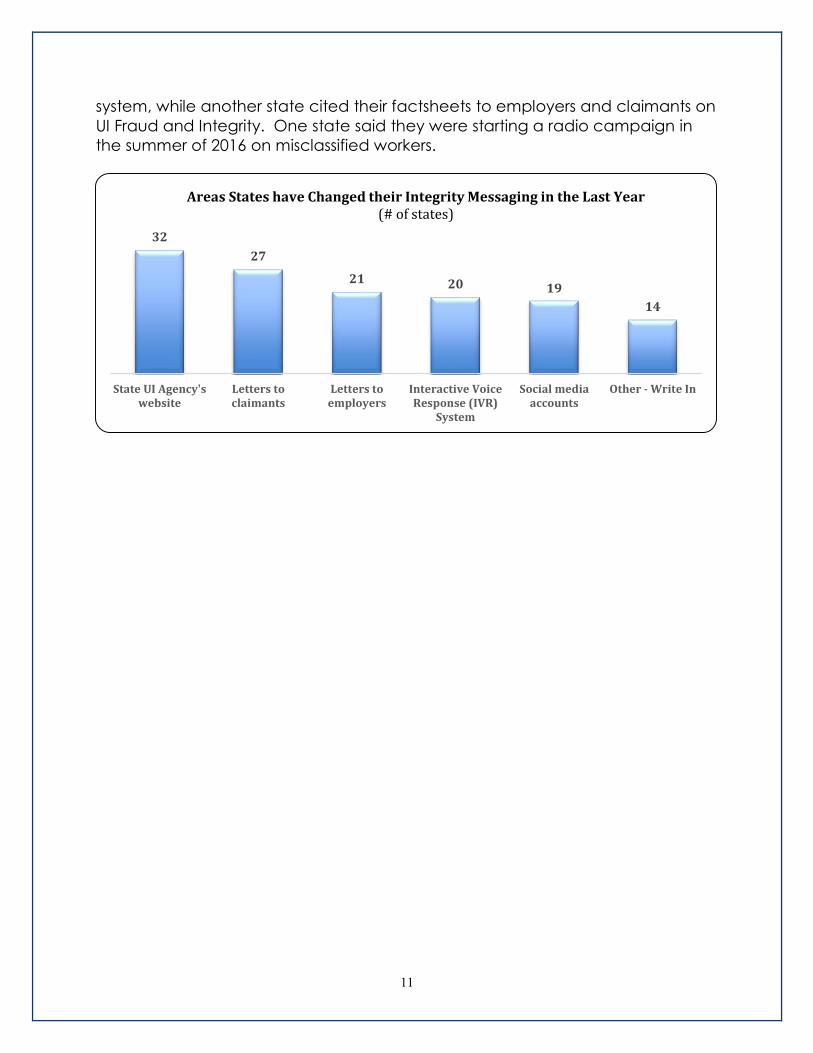

Q6) Has your state modified its integrity messaging in the last twelve months?

Forty-four states answered this question. The majority of current upgrades to UI

integrity messaging involve the state UI agency’s website as the medium for

their messaging, with specific letters to claimants and employers as the

secondary medium. Eighteen states indicated they had modified their UI

integrity messaging on social media accounts. Fourteen states also provided

written comments such as, a pop-up messaging (“nudging”) in their claimant

11

system, while another state cited their factsheets to employers and claimants on

UI Fraud and Integrity. One state said they were starting a radio campaign in

the summer of 2016 on misclassified workers.

32

27

21 20 19

14

State UI Agency'swebsite

Letters toclaimants

Letters toemployers

Interactive VoiceResponse (IVR)

System

Social mediaaccounts

Other - Write In

Areas States have Changed their Integrity Messaging in the Last Year (# of states)

12

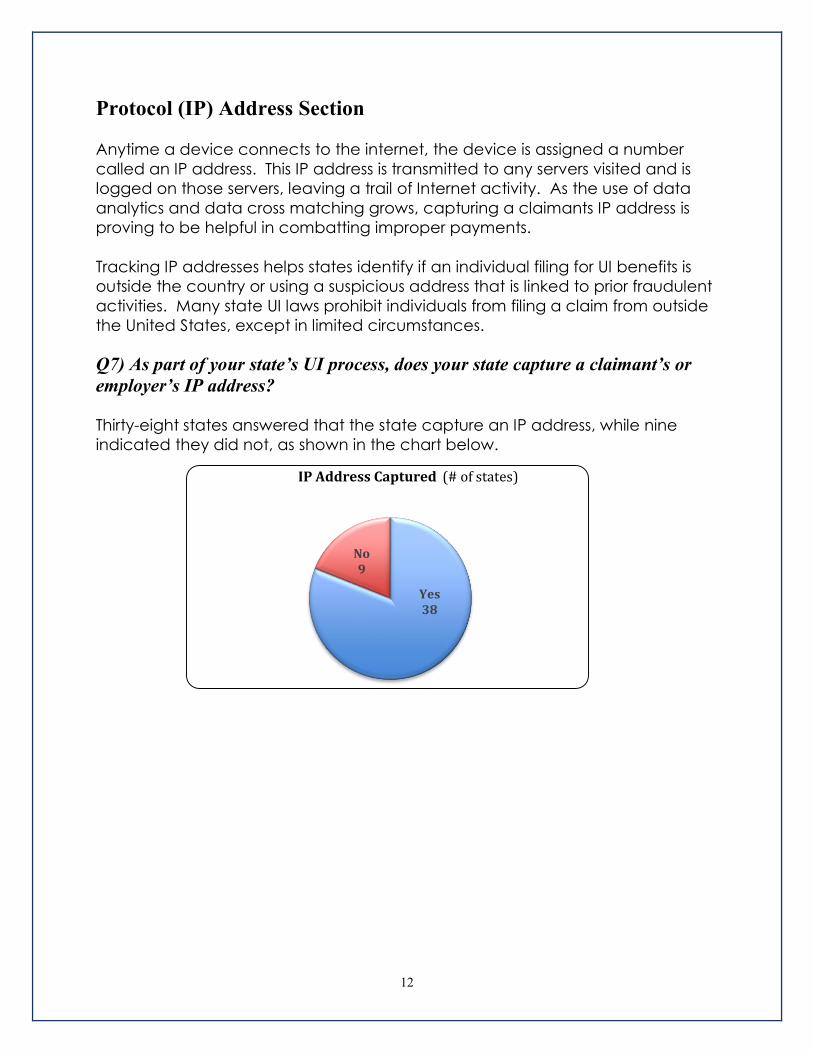

Protocol (IP) Address Section

Anytime a device connects to the internet, the device is assigned a number

called an IP address. This IP address is transmitted to any servers visited and is

logged on those servers, leaving a trail of Internet activity. As the use of data

analytics and data cross matching grows, capturing a claimants IP address is

proving to be helpful in combatting improper payments.

Tracking IP addresses helps states identify if an individual filing for UI benefits is

outside the country or using a suspicious address that is linked to prior fraudulent

activities. Many state UI laws prohibit individuals from filing a claim from outside

the United States, except in limited circumstances.

Q7) As part of your state’s UI process, does your state capture a claimant’s or

employer’s IP address?

Thirty-eight states answered that the state capture an IP address, while nine

indicated they did not, as shown in the chart below.

Yes38

No9

IP Address Captured (# of states)

13

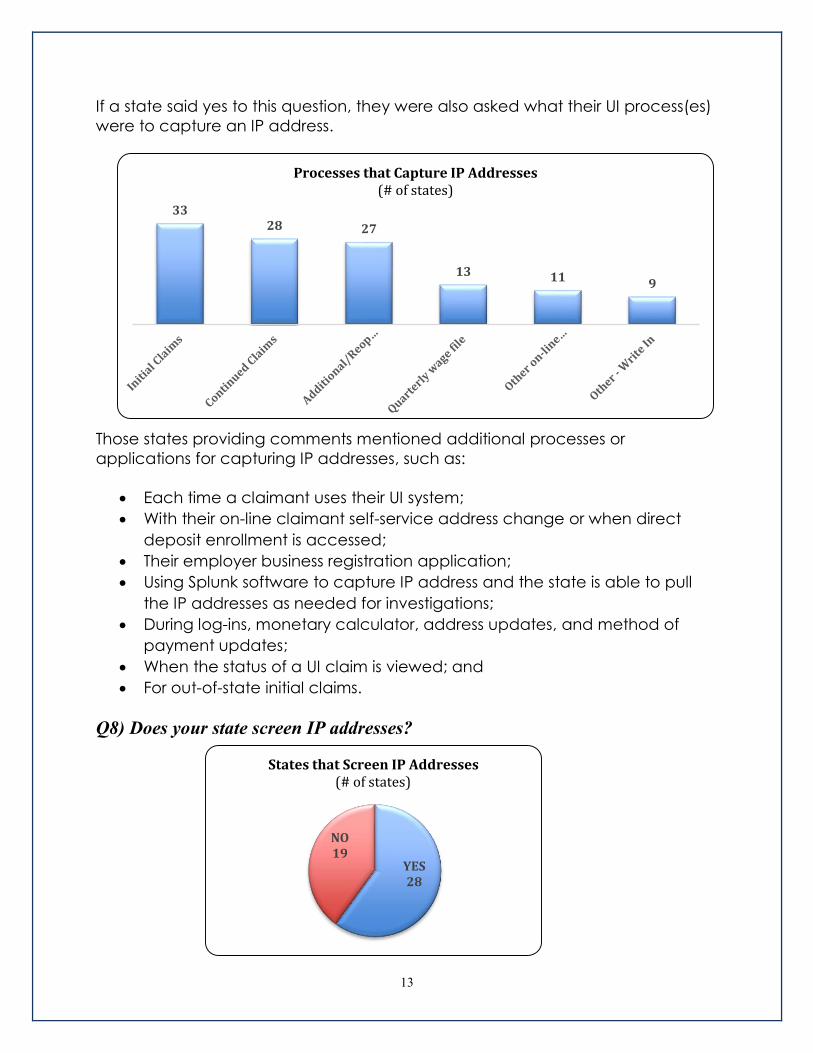

If a state said yes to this question, they were also asked what their UI process(es)

were to capture an IP address.

Those states providing comments mentioned additional processes or

applications for capturing IP addresses, such as:

Each time a claimant uses their UI system;

With their on-line claimant self-service address change or when direct

deposit enrollment is accessed;

Their employer business registration application;

Using Splunk software to capture IP address and the state is able to pull

the IP addresses as needed for investigations;

During log-ins, monetary calculator, address updates, and method of

payment updates;

When the status of a UI claim is viewed; and

For out-of-state initial claims.

Q8) Does your state screen IP addresses?

YES28

NO19

States that Screen IP Addresses(# of states)

3328 27

13 11 9

Processes that Capture IP Addresses (# of states)

14

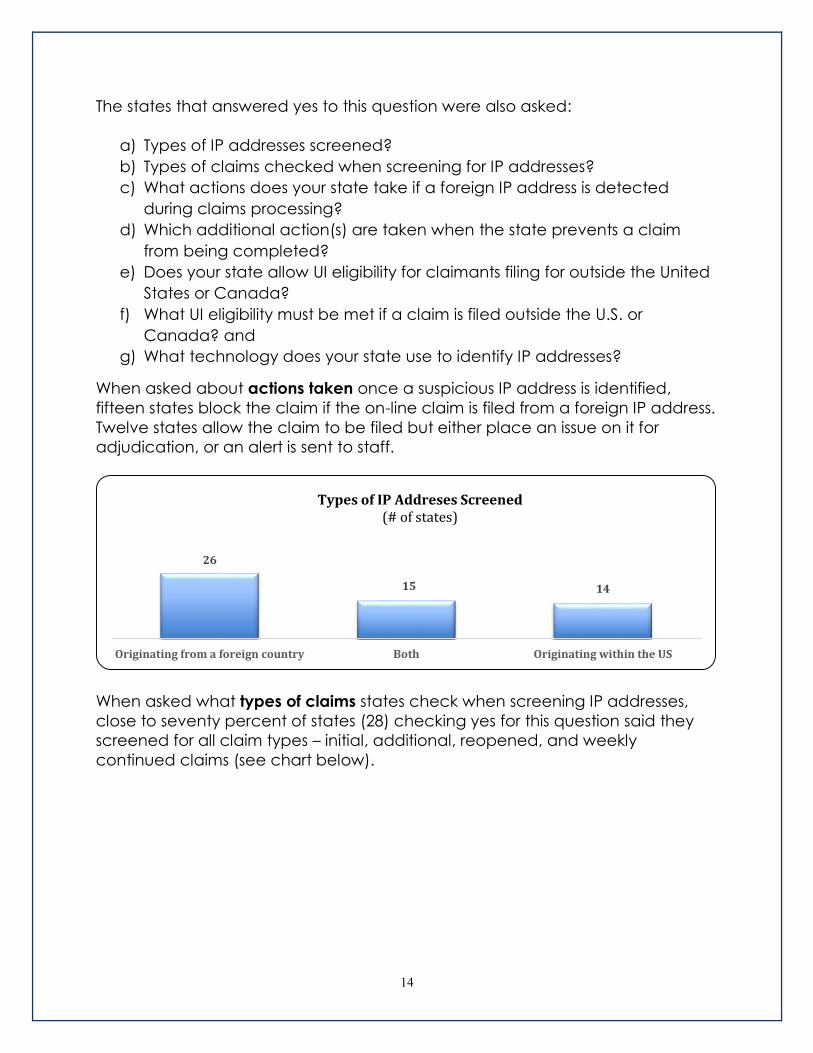

The states that answered yes to this question were also asked:

a) Types of IP addresses screened?

b) Types of claims checked when screening for IP addresses?

c) What actions does your state take if a foreign IP address is detected

during claims processing?

d) Which additional action(s) are taken when the state prevents a claim

from being completed?

e) Does your state allow UI eligibility for claimants filing for outside the United

States or Canada?

f) What UI eligibility must be met if a claim is filed outside the U.S. or

Canada? and

g) What technology does your state use to identify IP addresses?

When asked about actions taken once a suspicious IP address is identified,

fifteen states block the claim if the on-line claim is filed from a foreign IP address.

Twelve states allow the claim to be filed but either place an issue on it for

adjudication, or an alert is sent to staff.

When asked what types of claims states check when screening IP addresses,

close to seventy percent of states (28) checking yes for this question said they

screened for all claim types – initial, additional, reopened, and weekly

continued claims (see chart below).

26

15 14

Originating from a foreign country Both Originating within the US

Types of IP Addreses Screened (# of states)

15

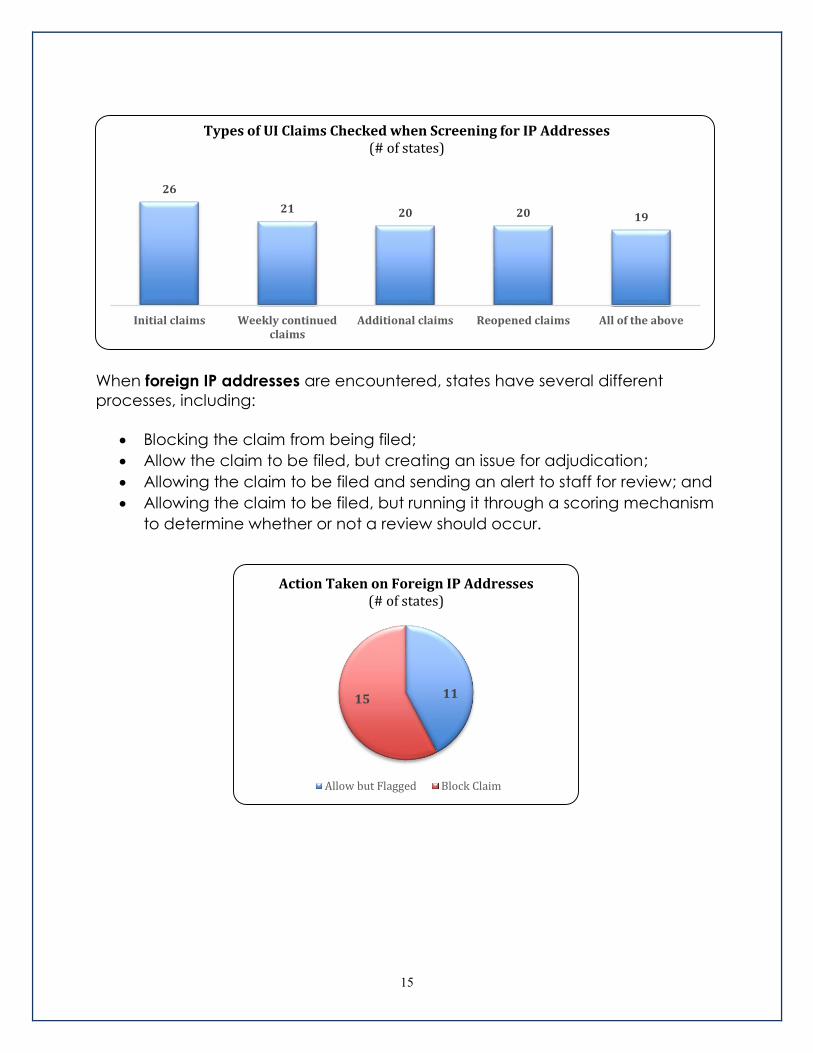

When foreign IP addresses are encountered, states have several different

processes, including:

Blocking the claim from being filed;

Allow the claim to be filed, but creating an issue for adjudication;

Allowing the claim to be filed and sending an alert to staff for review; and

Allowing the claim to be filed, but running it through a scoring mechanism

to determine whether or not a review should occur.

26

21 20 20 19

Initial claims Weekly continuedclaims

Additional claims Reopened claims All of the above

Types of UI Claims Checked when Screening for IP Addresses(# of states)

1115

Action Taken on Foreign IP Addresses(# of states)

Allow but Flagged Block Claim

16

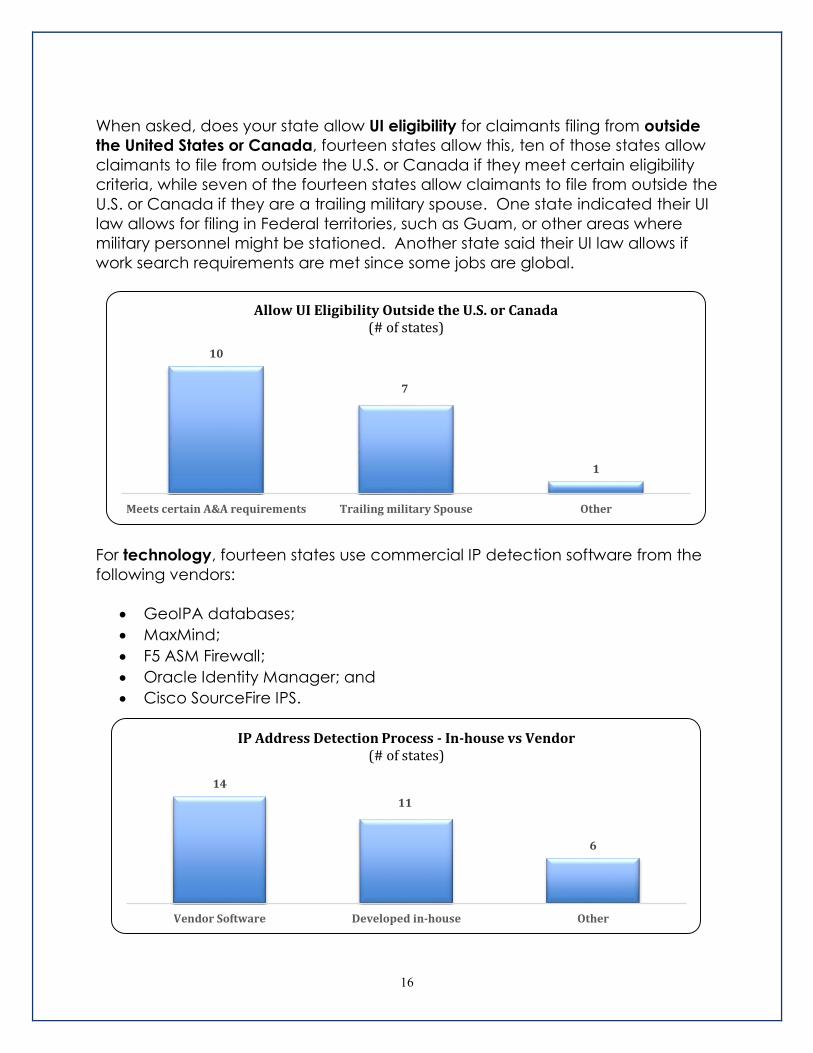

When asked, does your state allow UI eligibility for claimants filing from outside

the United States or Canada, fourteen states allow this, ten of those states allow

claimants to file from outside the U.S. or Canada if they meet certain eligibility

criteria, while seven of the fourteen states allow claimants to file from outside the

U.S. or Canada if they are a trailing military spouse. One state indicated their UI

law allows for filing in Federal territories, such as Guam, or other areas where

military personnel might be stationed. Another state said their UI law allows if

work search requirements are met since some jobs are global.

For technology, fourteen states use commercial IP detection software from the

following vendors:

GeoIPA databases;

MaxMind;

F5 ASM Firewall;

Oracle Identity Manager; and

Cisco SourceFire IPS.

10

7

1

Meets certain A&A requirements Trailing military Spouse Other

Allow UI Eligibility Outside the U.S. or Canada (# of states)

14

11

6

Vendor Software Developed in-house Other

IP Address Detection Process - In-house vs Vendor (# of states)

17

Additional information provided includes eleven states that block both foreign

and suspicious American IP addresses as well as having the IP address check as

part of all of their claim functions.

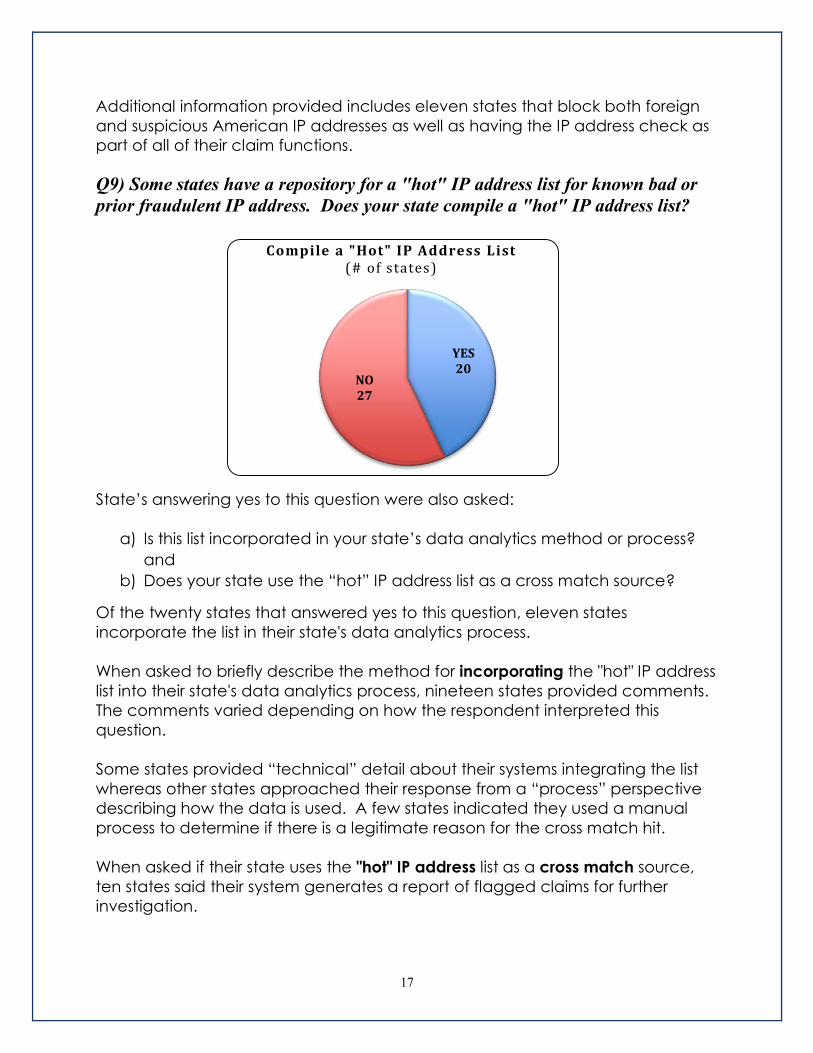

Q9) Some states have a repository for a "hot" IP address list for known bad or

prior fraudulent IP address. Does your state compile a "hot" IP address list?

State’s answering yes to this question were also asked:

a) Is this list incorporated in your state’s data analytics method or process?

and

b) Does your state use the “hot” IP address list as a cross match source?

Of the twenty states that answered yes to this question, eleven states

incorporate the list in their state's data analytics process.

When asked to briefly describe the method for incorporating the "hot" IP address

list into their state's data analytics process, nineteen states provided comments.

The comments varied depending on how the respondent interpreted this

question.

Some states provided “technical” detail about their systems integrating the list

whereas other states approached their response from a “process” perspective

describing how the data is used. A few states indicated they used a manual

process to determine if there is a legitimate reason for the cross match hit.

When asked if their state uses the "hot" IP address list as a cross match source,

ten states said their system generates a report of flagged claims for further

investigation.

YES20

NO27

Compile a "Hot" IP Address List (# of states)

18

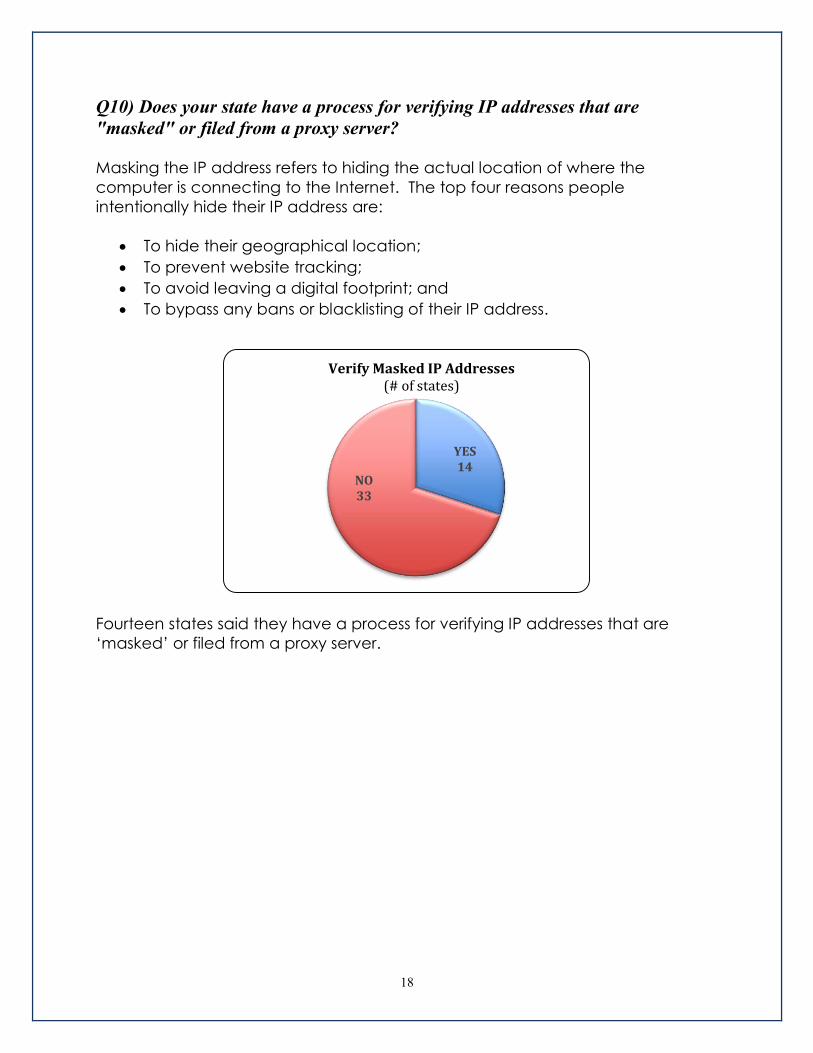

Q10) Does your state have a process for verifying IP addresses that are

"masked" or filed from a proxy server?

Masking the IP address refers to hiding the actual location of where the

computer is connecting to the Internet. The top four reasons people

intentionally hide their IP address are:

To hide their geographical location;

To prevent website tracking;

To avoid leaving a digital footprint; and

To bypass any bans or blacklisting of their IP address.

Fourteen states said they have a process for verifying IP addresses that are

‘masked’ or filed from a proxy server.

YES14

NO33

Verify Masked IP Addresses (# of states)

19

Training Section

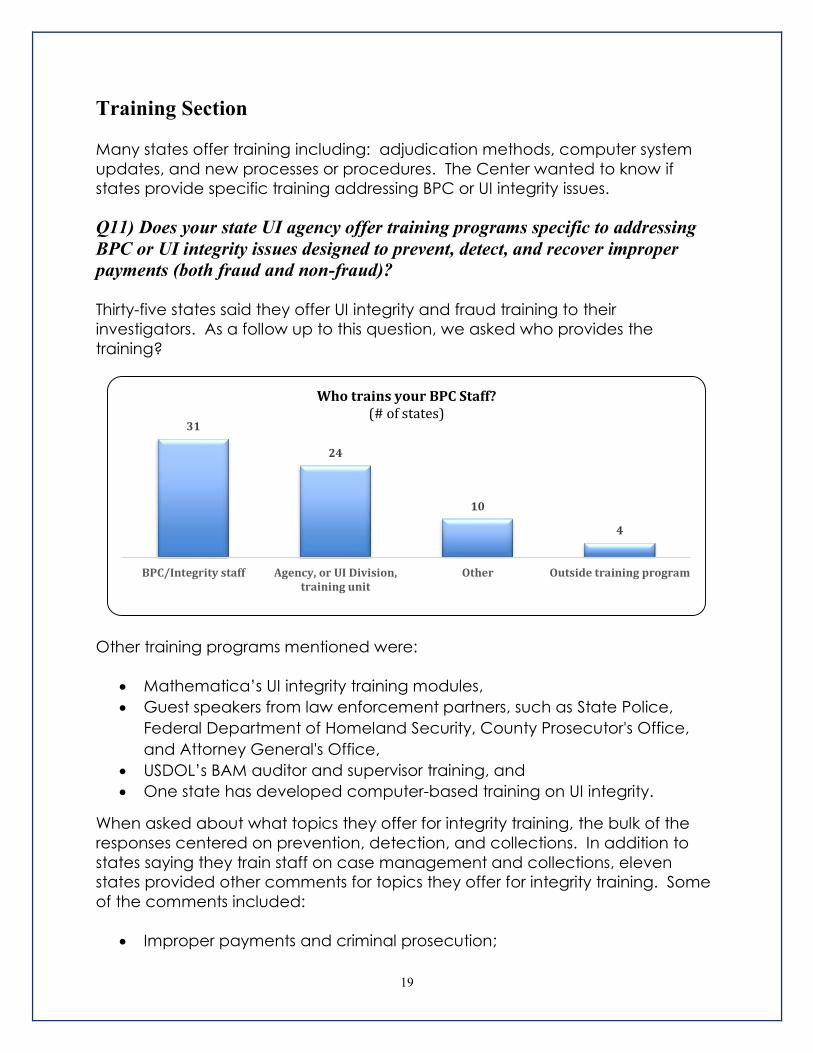

Many states offer training including: adjudication methods, computer system

updates, and new processes or procedures. The Center wanted to know if

states provide specific training addressing BPC or UI integrity issues.

Q11) Does your state UI agency offer training programs specific to addressing

BPC or UI integrity issues designed to prevent, detect, and recover improper

payments (both fraud and non-fraud)?

Thirty-five states said they offer UI integrity and fraud training to their

investigators. As a follow up to this question, we asked who provides the

training?

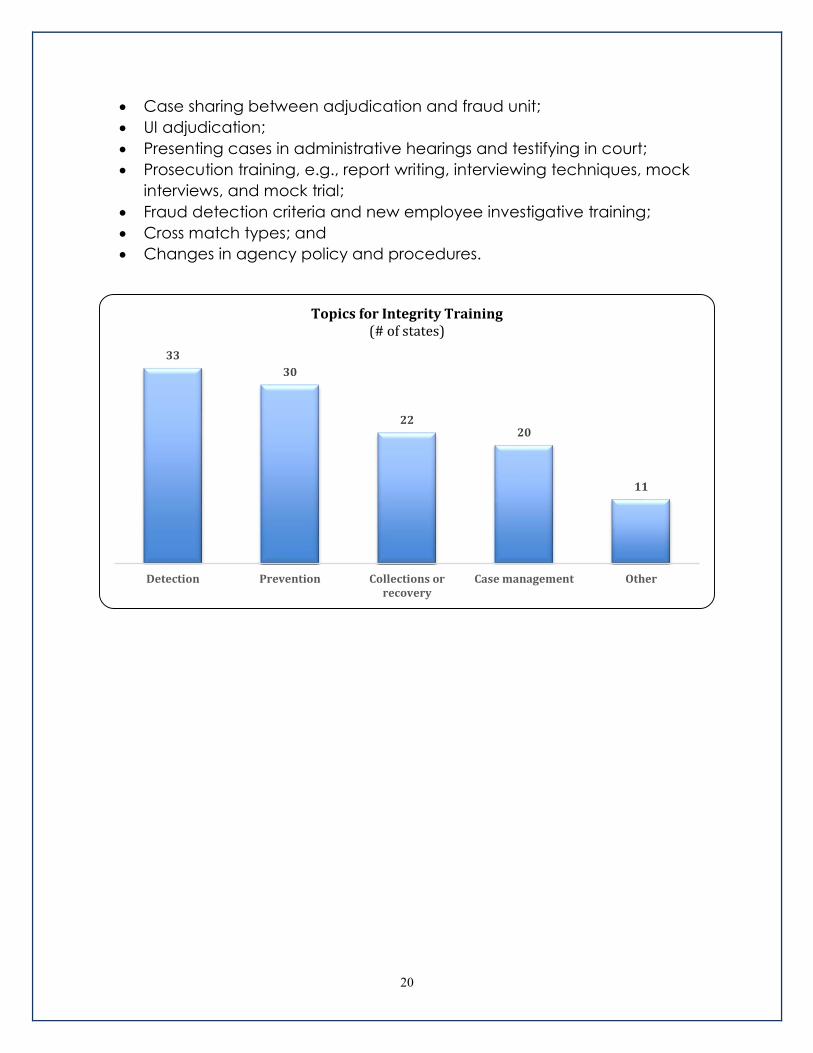

Other training programs mentioned were:

Mathematica’s UI integrity training modules,

Guest speakers from law enforcement partners, such as State Police,

Federal Department of Homeland Security, County Prosecutor's Office,

and Attorney General's Office,

USDOL’s BAM auditor and supervisor training, and

One state has developed computer-based training on UI integrity.

When asked about what topics they offer for integrity training, the bulk of the

responses centered on prevention, detection, and collections. In addition to

states saying they train staff on case management and collections, eleven

states provided other comments for topics they offer for integrity training. Some

of the comments included:

Improper payments and criminal prosecution;

31

24

10

4

BPC/Integrity staff Agency, or UI Division,training unit

Other Outside training program

Who trains your BPC Staff? (# of states)

20

Case sharing between adjudication and fraud unit;

UI adjudication;

Presenting cases in administrative hearings and testifying in court;

Prosecution training, e.g., report writing, interviewing techniques, mock

interviews, and mock trial;

Fraud detection criteria and new employee investigative training;

Cross match types; and

Changes in agency policy and procedures.

33

30

2220

11

Detection Prevention Collections orrecovery

Case management Other

Topics for Integrity Training (# of states)

21

Recoupment Section

UI Improper payment recoupment methods vary widely by state. Gaining an

understanding of processes, procedures, vendors, and software used for

recoupment is the intent of these questions. Areas of interested included: the

Treasury Offset Program (TOP), skip tracing, case management systems, liens,

levying bank accounts, any automated processes, electronic payment options,

leveraging business licenses, bankruptcy filing, bonds, and contracting out for UI

debt recovery.

State responses to the following fourteen questions demonstrated how the

various state UI laws, regulations, and policies impact what collection tools

states have in recovering UI debts.

Q12) Does your state currently participate in TOP to collect delinquent UI

employer tax debts?

Federal law requires state UI agencies to participate in TOP to recover certain UI

benefit overpayments and tax debt. If a state said yes to this question, they

were also asked:

a) What were your recoveries for 2015?

b) Was your state using an automated or manual process to record the UI

employer tax debts in your state UI system? and

c) Was your state planning on including UI employer tax debt to TOP

requests? If so, when?

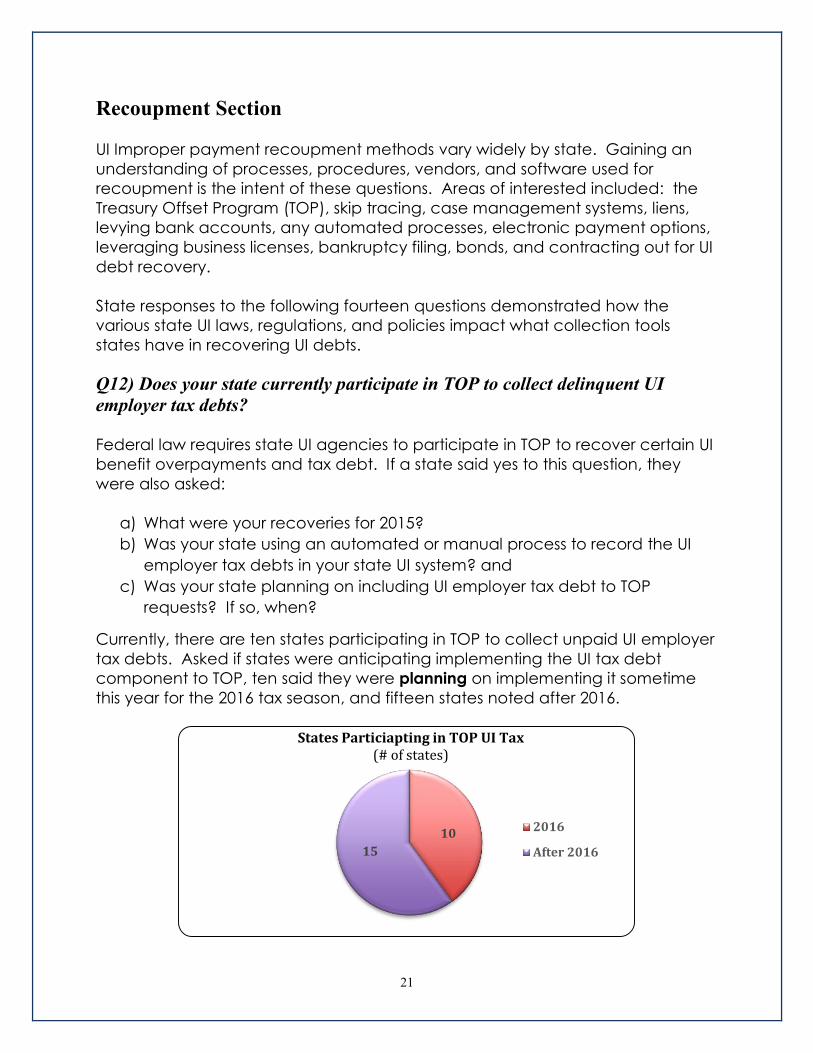

Currently, there are ten states participating in TOP to collect unpaid UI employer

tax debts. Asked if states were anticipating implementing the UI tax debt

component to TOP, ten said they were planning on implementing it sometime

this year for the 2016 tax season, and fifteen states noted after 2016.

10

15

States Particiapting in TOP UI Tax (# of states)

2016

After 2016

22

For more information on the collection numbers from TOP, please visit’s

Treasury’s most recent newsletter at:

https://fiscal.treasury.gov/fsservices/gov/debtColl/dms/top/stOutrch/debt_offse

ts_matter.htm.

Q13) Does your state use any outside data sources or tools for locating (skip

tracing) debtors' most current address?

Skip tracing is a colloquial term used to describe the process of locating a

person's whereabouts for any number of purposes.

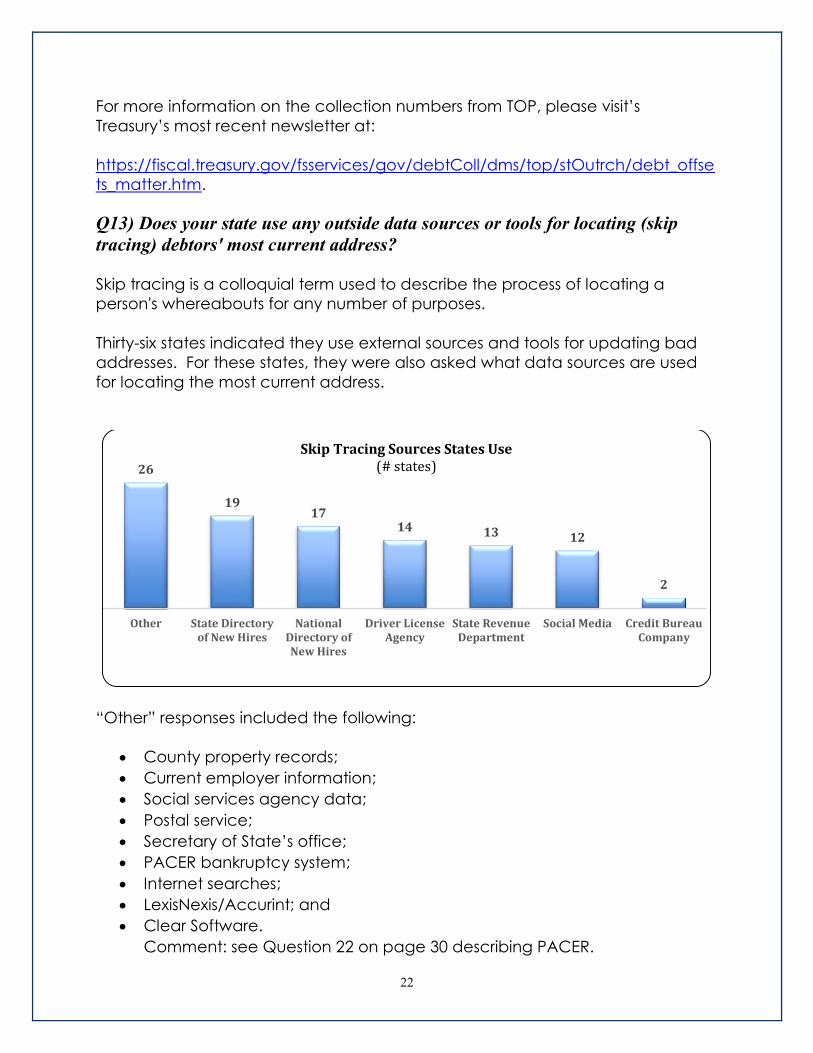

Thirty-six states indicated they use external sources and tools for updating bad

addresses. For these states, they were also asked what data sources are used

for locating the most current address.

“Other” responses included the following:

County property records;

Current employer information;

Social services agency data;

Postal service;

Secretary of State’s office;

PACER bankruptcy system;

Internet searches;

LexisNexis/Accurint; and

Clear Software.

Comment: see Question 22 on page 30 describing PACER.

26

1917

14 13 12

2

Other State Directoryof New Hires

NationalDirectory ofNew Hires

Driver LicenseAgency

State RevenueDepartment

Social Media Credit BureauCompany

Skip Tracing Sources States Use(# states)

23

Q14) Does your state have an automated collections case management system

(separate and apart from your automated billing system)?

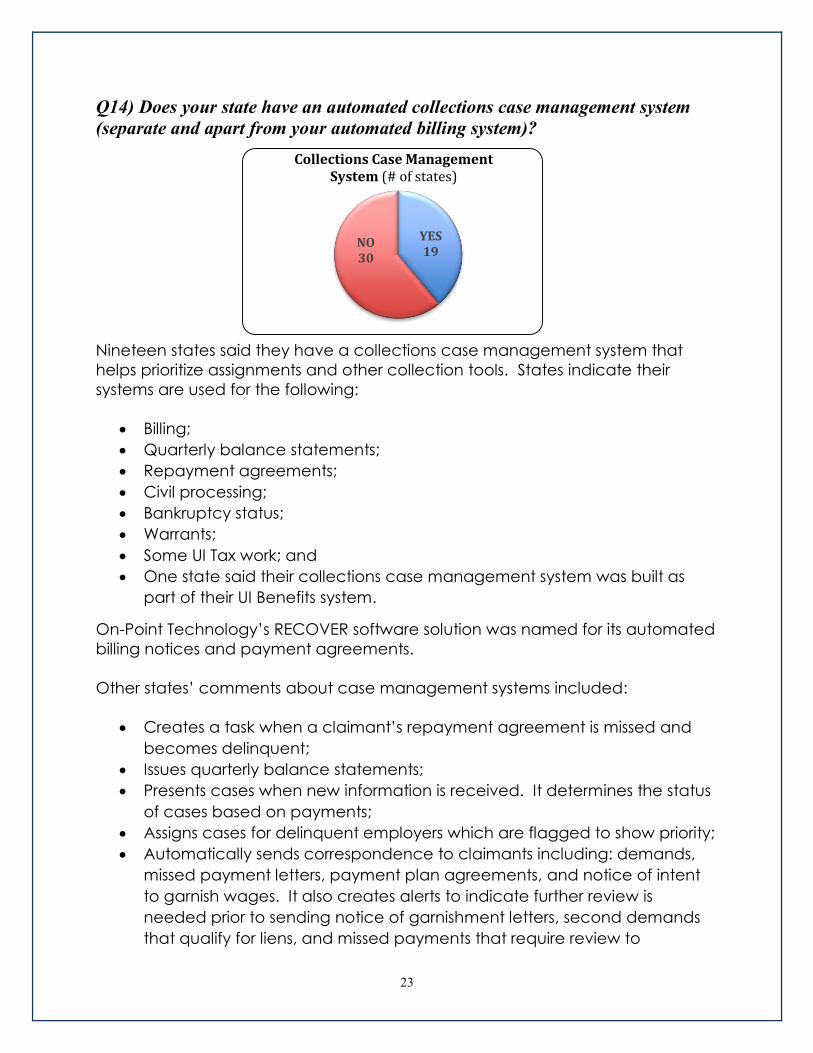

Nineteen states said they have a collections case management system that

helps prioritize assignments and other collection tools. States indicate their

systems are used for the following:

Billing;

Quarterly balance statements;

Repayment agreements;

Civil processing;

Bankruptcy status;

Warrants;

Some UI Tax work; and

One state said their collections case management system was built as

part of their UI Benefits system.

On-Point Technology’s RECOVER software solution was named for its automated

billing notices and payment agreements.

Other states’ comments about case management systems included:

Creates a task when a claimant’s repayment agreement is missed and

becomes delinquent;

Issues quarterly balance statements;

Presents cases when new information is received. It determines the status

of cases based on payments;

Assigns cases for delinquent employers which are flagged to show priority;

Automatically sends correspondence to claimants including: demands,

missed payment letters, payment plan agreements, and notice of intent

to garnish wages. It also creates alerts to indicate further review is

needed prior to sending notice of garnishment letters, second demands

that qualify for liens, and missed payments that require review to

YES19

NO30

Collections Case Management System (# of states)

24

determine next steps. Bankruptcy cases are tracked in the system but

handled manually by staff;

Advises staff of failed payment agreements or not meeting monthly

minimum payments, and generates work items for examiners. Also,

notifies of judgments and garnishment opportunities and expired payment

agreements where balances exist;

Automates the collection cycle and assignments are automatically

assigned to Tax Enforcement Officers at the time a Tax Warrant is issued;

Allows workload to be managed through the use of follow-up codes by

activity type, such as, debt has a bad address, sent to private collection

agency, or have bank proceedings underway;

Provides timely review and handling of civil actions and auto population

of applicable documents; and

Tracks a case throughout the collection process - it notifies staff if a

payment hasn't been received or if paperwork has not been received.

Q15) Does your state have any automated processes for contacting debtors to

recover benefit overpayments or tax debts?

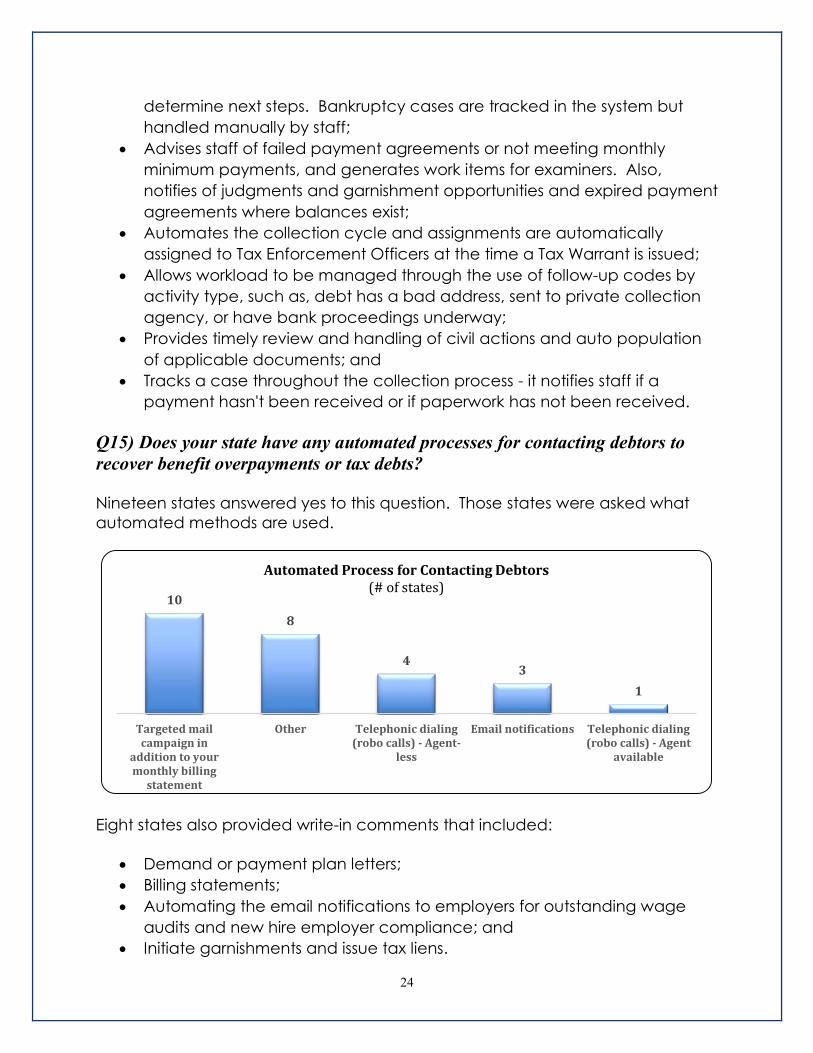

Nineteen states answered yes to this question. Those states were asked what

automated methods are used.

Eight states also provided write-in comments that included:

Demand or payment plan letters;

Billing statements;

Automating the email notifications to employers for outstanding wage

audits and new hire employer compliance; and

Initiate garnishments and issue tax liens.

10

8

43

1

Targeted mailcampaign in

addition to yourmonthly billing

statement

Other Telephonic dialing(robo calls) - Agent-

less

Email notifications Telephonic dialing(robo calls) - Agent

available

Automated Process for Contacting Debtors (# of states)

25

Q16) Does your state allow electronic payment options on overpayments or tax

debts?

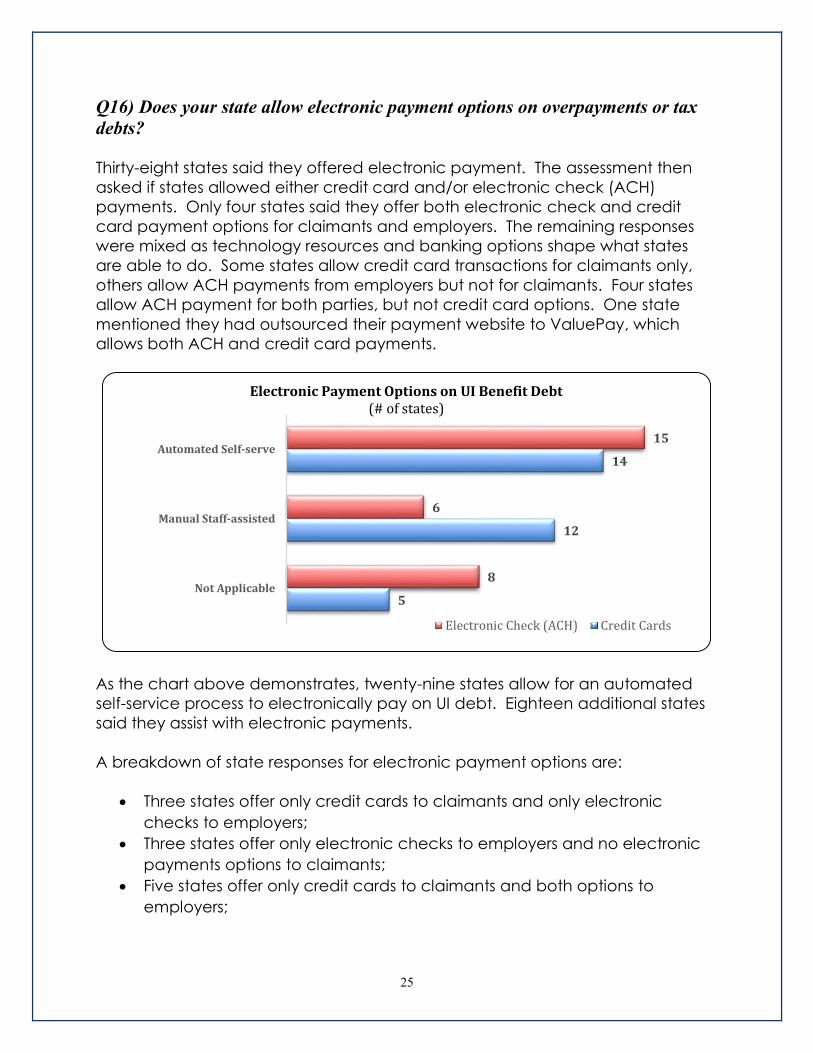

Thirty-eight states said they offered electronic payment. The assessment then

asked if states allowed either credit card and/or electronic check (ACH)

payments. Only four states said they offer both electronic check and credit

card payment options for claimants and employers. The remaining responses

were mixed as technology resources and banking options shape what states

are able to do. Some states allow credit card transactions for claimants only,

others allow ACH payments from employers but not for claimants. Four states

allow ACH payment for both parties, but not credit card options. One state

mentioned they had outsourced their payment website to ValuePay, which

allows both ACH and credit card payments.

As the chart above demonstrates, twenty-nine states allow for an automated

self-service process to electronically pay on UI debt. Eighteen additional states

said they assist with electronic payments.

A breakdown of state responses for electronic payment options are:

Three states offer only credit cards to claimants and only electronic

checks to employers;

Three states offer only electronic checks to employers and no electronic

payments options to claimants;

Five states offer only credit cards to claimants and both options to

employers;

5

12

14

8

6

15

Not Applicable

Manual Staff-assisted

Automated Self-serve

Electronic Payment Options on UI Benefit Debt (# of states)

Electronic Check (ACH) Credit Cards

26

One state offers both options to claimants and no electronic payment

options for employers;

Two states offer only credit cards to both claimants and employers;

Two states offer only electronic checks to claimants and both options to

employers;

Four states offer only the electronic check payment option to both

claimants and employers;

Two states offer both options to claimants and only electronic checks to

employers; and

Four states offer both options to claimants and employers.

When asked how credit card transaction fees are covered, the majority of the

twenty-six states responding said the transaction fees were passed along to the

employer and claimant. Six states said they covered the fees for claimants and

employers through their penalty and interest fund, while two states said they

covered the fees through the state’s general fund.

Q17) Does your state have a State Income Tax offset program?

Thirty-six states have a state income tax offset program, three do not, and nine

states do not have a state income tax. Five states indicated they are active in

offsetting employer tax debts in addition to claimant overpayments.

Q18) Does your state actively recover UI benefit overpayments through wage

garnishments issued to the claimant's current employer(s)?

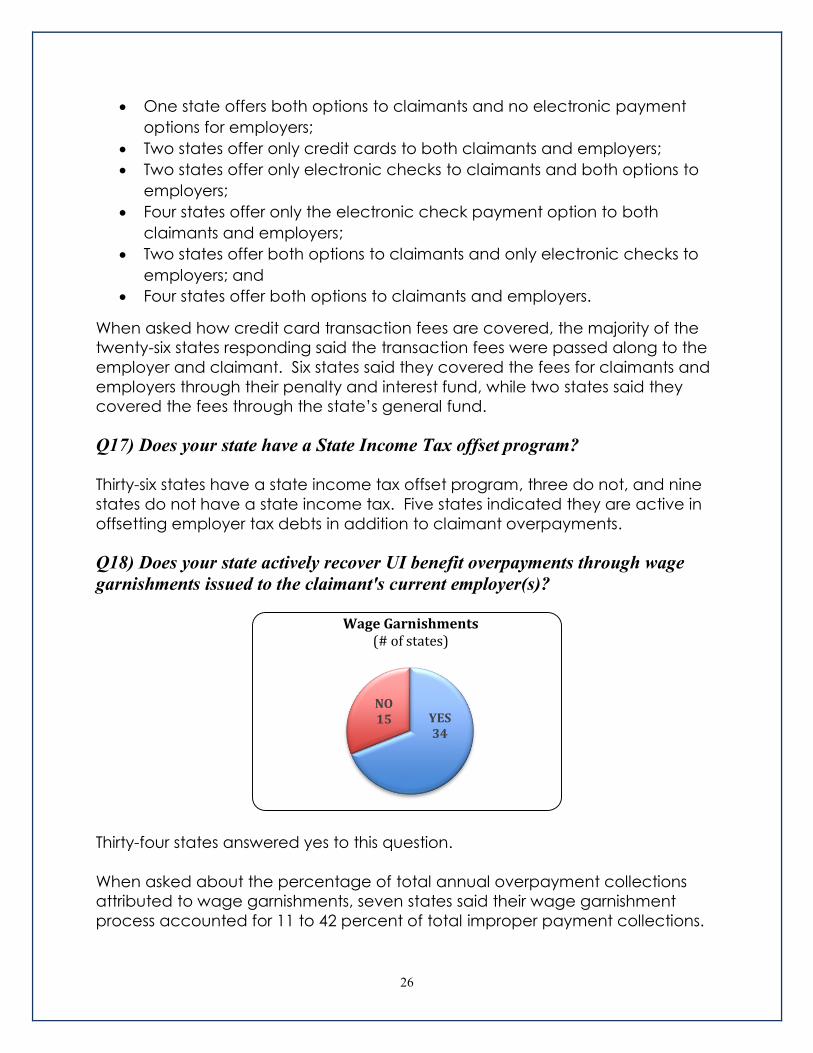

Thirty-four states answered yes to this question.

When asked about the percentage of total annual overpayment collections

attributed to wage garnishments, seven states said their wage garnishment

process accounted for 11 to 42 percent of total improper payment collections.

YES34

NO15

Wage Garnishments (# of states)

27

The Center will use these responses to gather more information from states with

high collection percentages so best practices can be promoted to the UI system.

In the 2015 Assessment, states reported:

Cost to file the paperwork and time required to send staff to court to

obtain judgments were some reasons why several states don’t conduct

garnishments or do very few;

States most successful in collecting outstanding UI debt through

garnishments generally have an automated process with the courts or

state law doesn’t require a court order;

Several states use a lien process or an administrative order, rather than a

court order, to conduct wage garnishments; and

Most of the states not currently administering wage garnishments would

require state law changes in order to begin this practice.

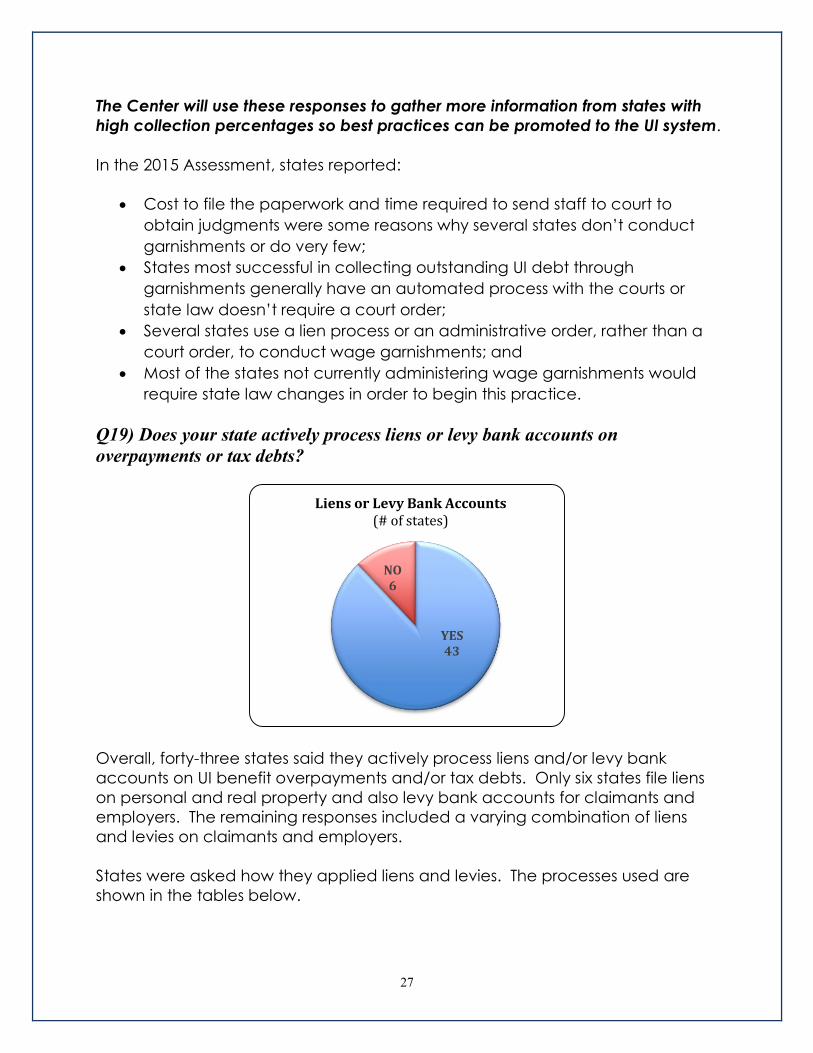

Q19) Does your state actively process liens or levy bank accounts on

overpayments or tax debts?

Overall, forty-three states said they actively process liens and/or levy bank

accounts on UI benefit overpayments and/or tax debts. Only six states file liens

on personal and real property and also levy bank accounts for claimants and

employers. The remaining responses included a varying combination of liens

and levies on claimants and employers.

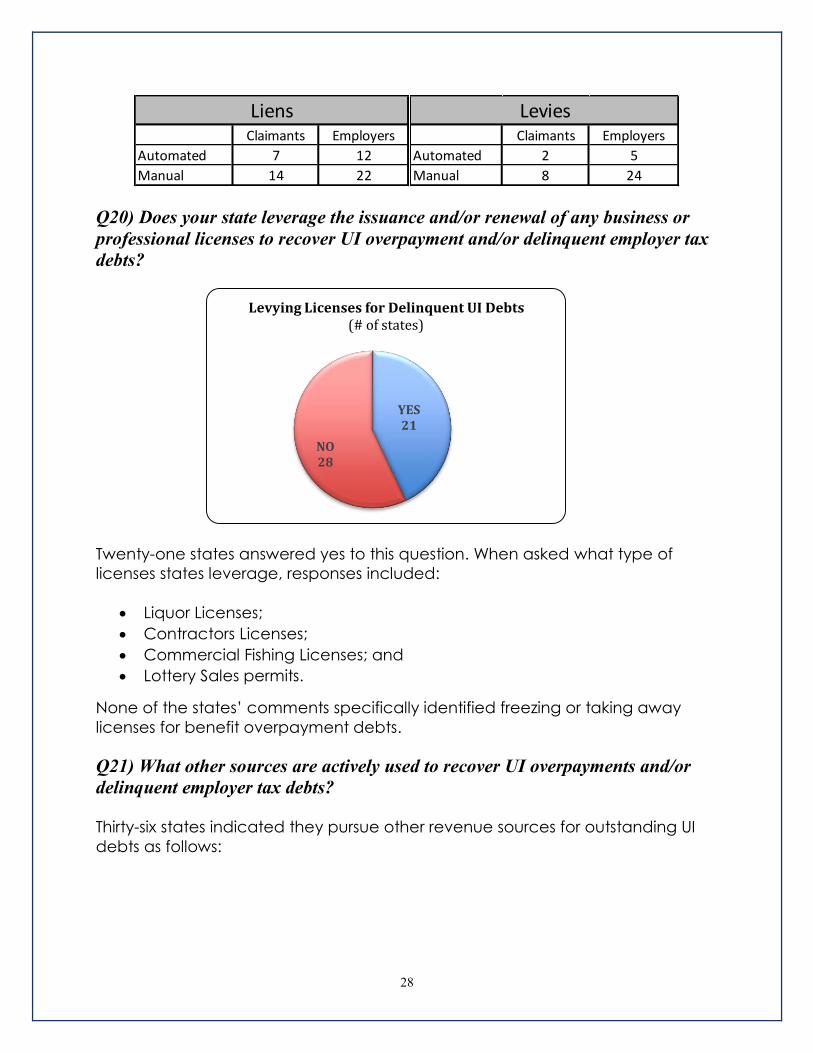

States were asked how they applied liens and levies. The processes used are

shown in the tables below.

YES43

NO6

Liens or Levy Bank Accounts(# of states)

28

Q20) Does your state leverage the issuance and/or renewal of any business or

professional licenses to recover UI overpayment and/or delinquent employer tax

debts?

Twenty-one states answered yes to this question. When asked what type of

licenses states leverage, responses included:

Liquor Licenses;

Contractors Licenses;

Commercial Fishing Licenses; and

Lottery Sales permits.

None of the states’ comments specifically identified freezing or taking away

licenses for benefit overpayment debts.

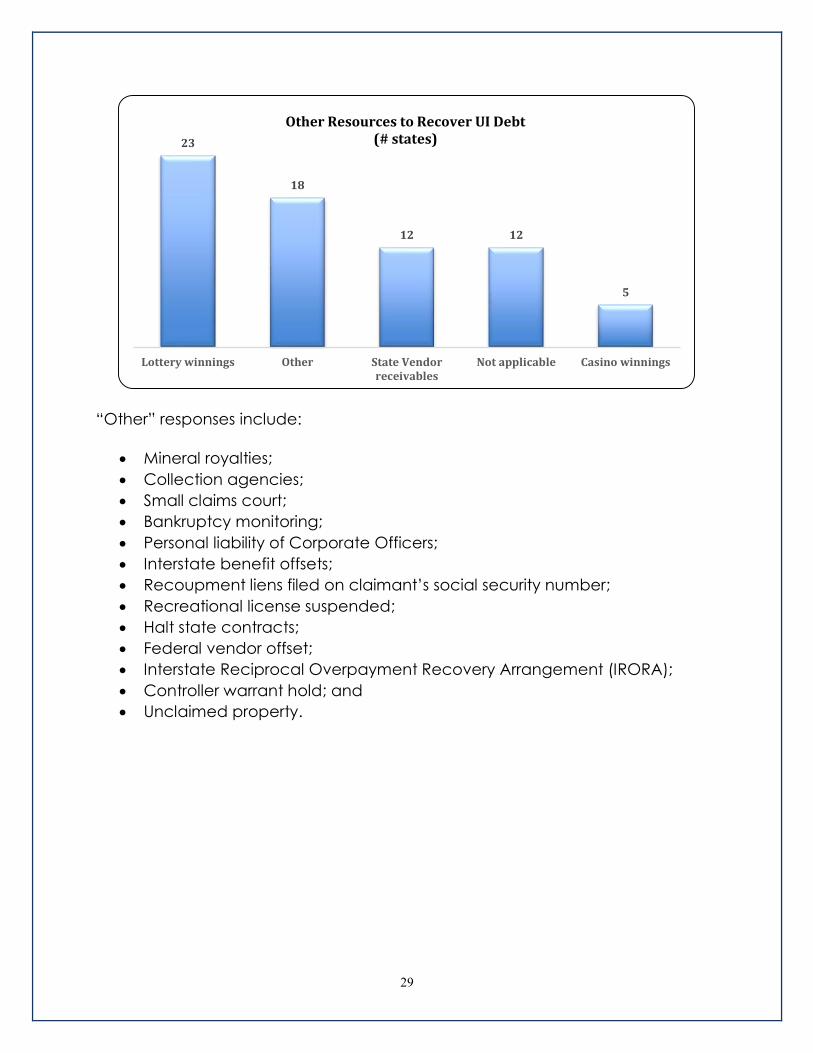

Q21) What other sources are actively used to recover UI overpayments and/or

delinquent employer tax debts?

Thirty-six states indicated they pursue other revenue sources for outstanding UI

debts as follows:

Claimants Employers

Automated 7 12

Manual 14 22

LiensClaimants Employers

Automated 2 5

Manual 8 24

Levies

YES21

NO28

Levying Licenses for Delinquent UI Debts(# of states)

29

“Other” responses include:

Mineral royalties;

Collection agencies;

Small claims court;

Bankruptcy monitoring;

Personal liability of Corporate Officers;

Interstate benefit offsets;

Recoupment liens filed on claimant’s social security number;

Recreational license suspended;

Halt state contracts;

Federal vendor offset;

Interstate Reciprocal Overpayment Recovery Arrangement (IRORA);

Controller warrant hold; and

Unclaimed property.

23

18

12 12

5

Lottery winnings Other State Vendorreceivables

Not applicable Casino winnings

Other Resources to Recover UI Debt (# states)

30

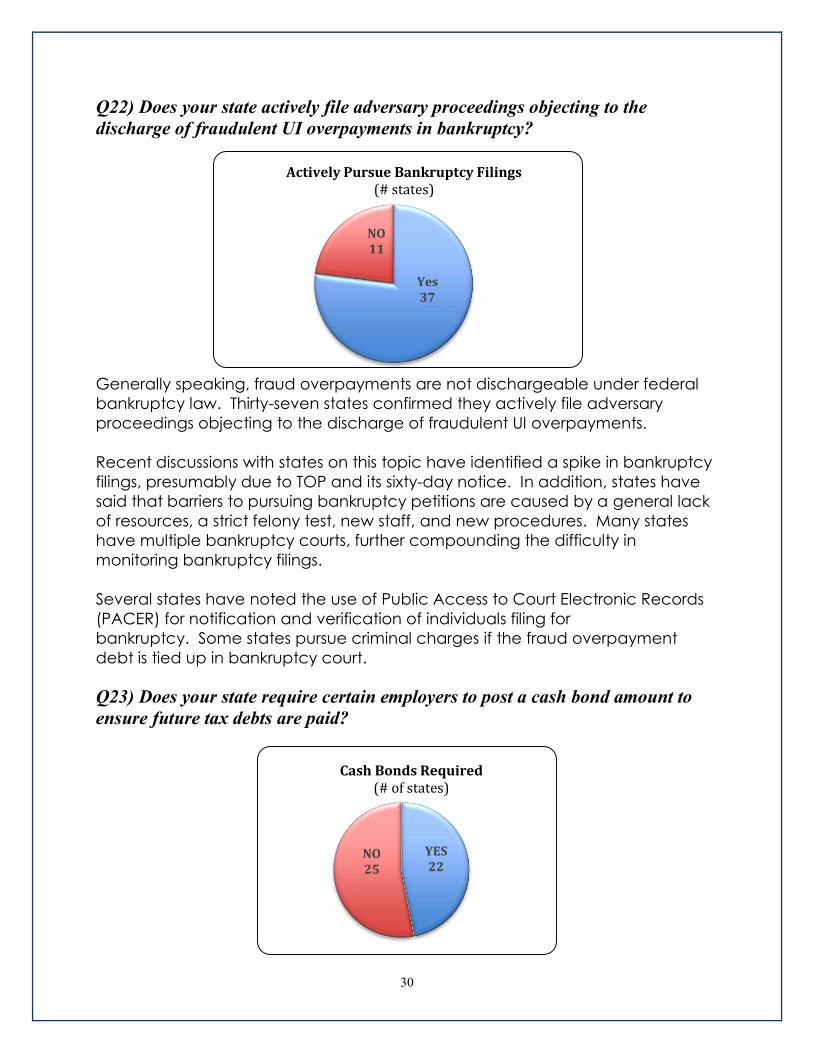

Q22) Does your state actively file adversary proceedings objecting to the

discharge of fraudulent UI overpayments in bankruptcy?

Generally speaking, fraud overpayments are not dischargeable under federal

bankruptcy law. Thirty-seven states confirmed they actively file adversary

proceedings objecting to the discharge of fraudulent UI overpayments.

Recent discussions with states on this topic have identified a spike in bankruptcy

filings, presumably due to TOP and its sixty-day notice. In addition, states have

said that barriers to pursuing bankruptcy petitions are caused by a general lack

of resources, a strict felony test, new staff, and new procedures. Many states

have multiple bankruptcy courts, further compounding the difficulty in

monitoring bankruptcy filings.

Several states have noted the use of Public Access to Court Electronic Records

(PACER) for notification and verification of individuals filing for

bankruptcy. Some states pursue criminal charges if the fraud overpayment

debt is tied up in bankruptcy court.

Q23) Does your state require certain employers to post a cash bond amount to

ensure future tax debts are paid?

YES22

NO25

Cash Bonds Required (# of states)

Yes37

NO11

Actively Pursue Bankruptcy Filings (# states)

31

Twenty-two states require certain employer groups to post a surety bond for UI

covered employment.

Seventeen states require it for reimbursable employers, four states utilize this for

industry specific employers, and four states make this a requirement for

chronically delinquent employers.

Four states in this group also commented they require a cash bond on

chronically delinquent employer accounts for both reimbursable and

contributory employers.

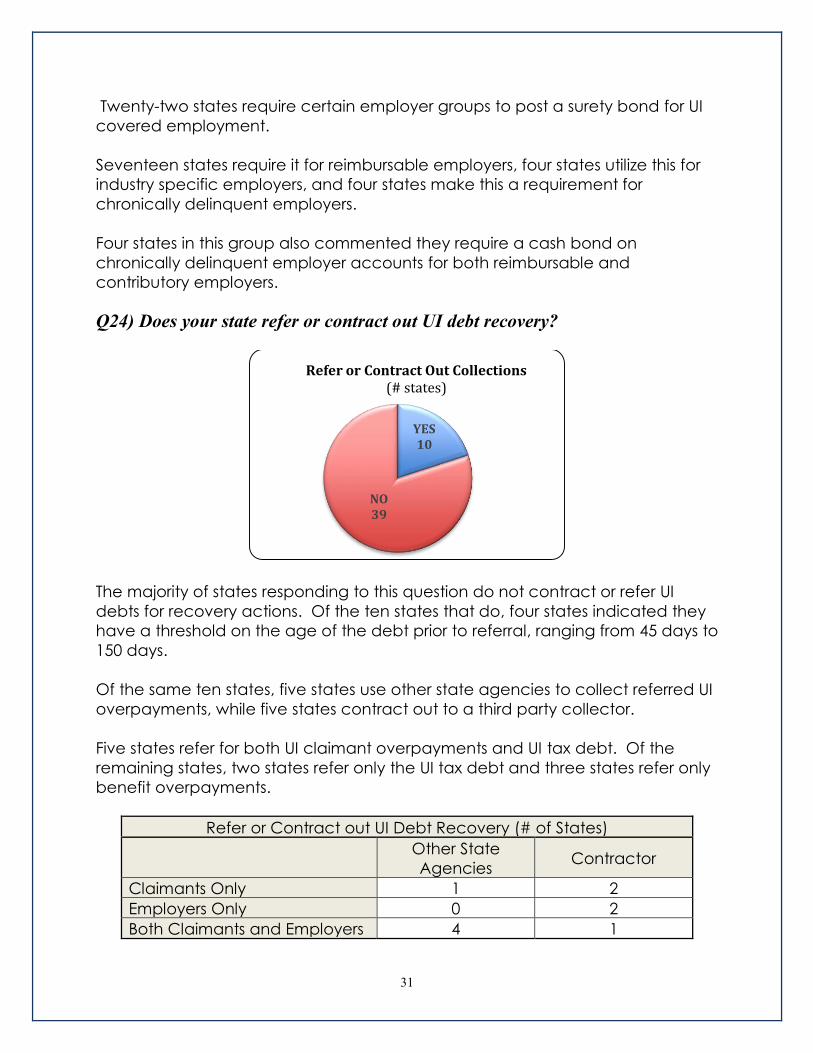

Q24) Does your state refer or contract out UI debt recovery?

The majority of states responding to this question do not contract or refer UI

debts for recovery actions. Of the ten states that do, four states indicated they

have a threshold on the age of the debt prior to referral, ranging from 45 days to

150 days.

Of the same ten states, five states use other state agencies to collect referred UI

overpayments, while five states contract out to a third party collector.

Five states refer for both UI claimant overpayments and UI tax debt. Of the

remaining states, two states refer only the UI tax debt and three states refer only

benefit overpayments.

Refer or Contract out UI Debt Recovery (# of States)

Other State

Agencies Contractor

Claimants Only 1 2

Employers Only 0 2

Both Claimants and Employers 4 1

YES10

NO39

Refer or Contract Out Collections(# states)

32

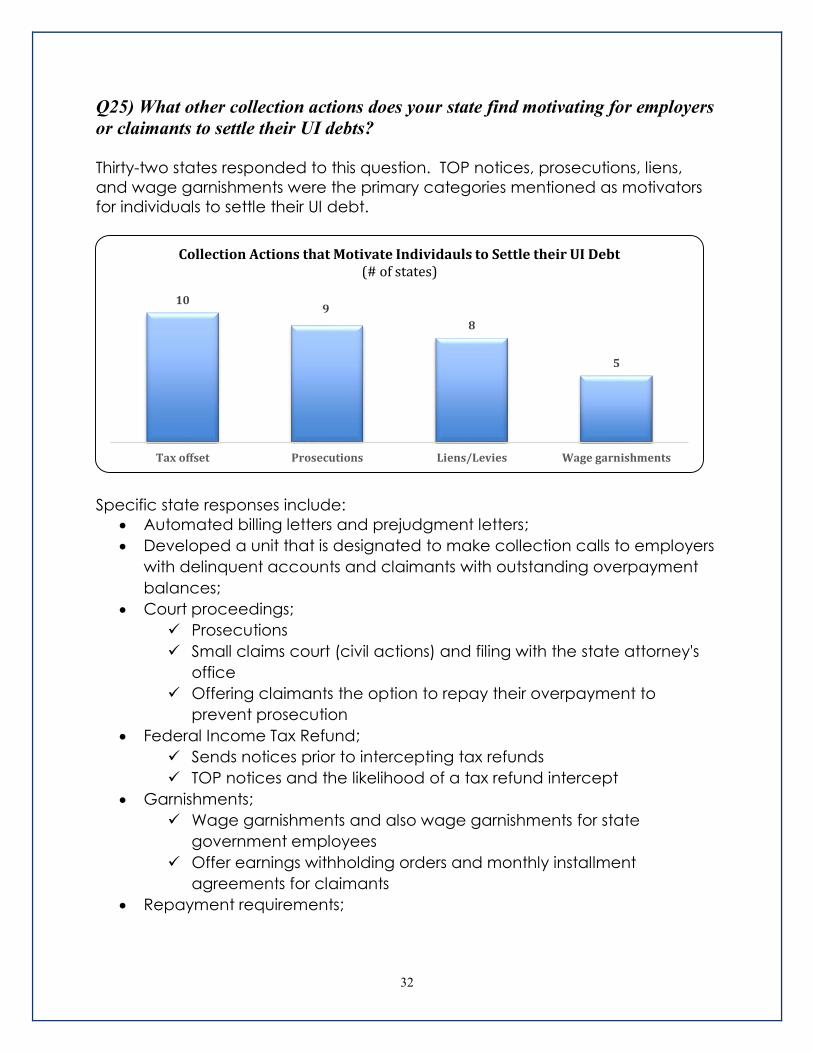

Q25) What other collection actions does your state find motivating for employers

or claimants to settle their UI debts?

Thirty-two states responded to this question. TOP notices, prosecutions, liens,

and wage garnishments were the primary categories mentioned as motivators

for individuals to settle their UI debt.

Specific state responses include:

Automated billing letters and prejudgment letters;

Developed a unit that is designated to make collection calls to employers

with delinquent accounts and claimants with outstanding overpayment

balances;

Court proceedings;

Prosecutions

Small claims court (civil actions) and filing with the state attorney's

office

Offering claimants the option to repay their overpayment to

prevent prosecution

Federal Income Tax Refund;

Sends notices prior to intercepting tax refunds

TOP notices and the likelihood of a tax refund intercept

Garnishments;

Wage garnishments and also wage garnishments for state

government employees

Offer earnings withholding orders and monthly installment

agreements for claimants

Repayment requirements;

109

8

5

Tax offset Prosecutions Liens/Levies Wage garnishments

Collection Actions that Motivate Individauls to Settle their UI Debt(# of states)

33

State law requires claimants to repay fraudulent debts including

penalties and interest in cash before being eligible to receive future

UI benefits

Claimants who have committed UI fraud are barred from future

benefits until all fraud debt is settled

Financial record matching

Flexible payment plans

Installment-payment plans

Tax; and

End of September deadline to have all employer debt satisfied to

maintain eligibility for a reduced UI tax rate

Civil penalties for employer’s failure to file required reports

Negotiation of settlements (employer debt)

State law that allows for the responsible party debt transfer making

the person liable for the entire UI tax debt in addition to the entity

being liable

Warrants and Levies.

A levy is filed against a person’s annual permanent fund dividend

Liens are the most motivating action for employer groups

Warrants and levies are very effective.

34

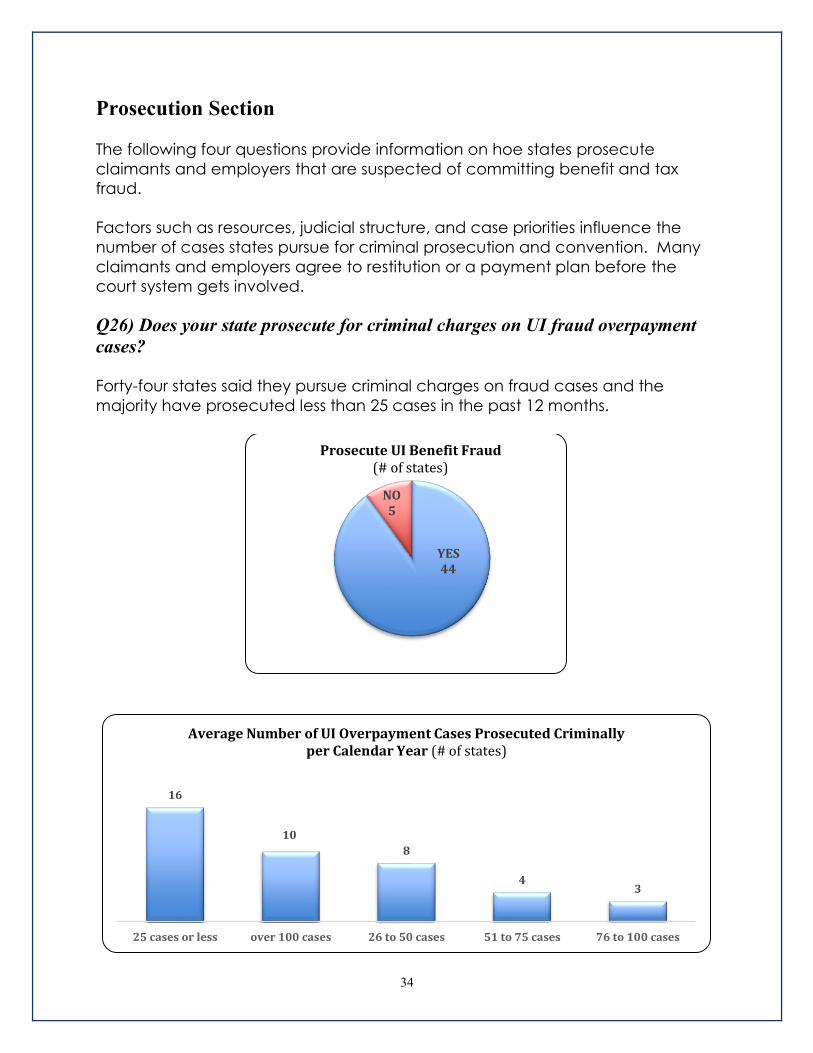

Prosecution Section

The following four questions provide information on hoe states prosecute

claimants and employers that are suspected of committing benefit and tax

fraud.

Factors such as resources, judicial structure, and case priorities influence the

number of cases states pursue for criminal prosecution and convention. Many

claimants and employers agree to restitution or a payment plan before the

court system gets involved.

Q26) Does your state prosecute for criminal charges on UI fraud overpayment

cases?

Forty-four states said they pursue criminal charges on fraud cases and the

majority have prosecuted less than 25 cases in the past 12 months.

YES44

NO5

Prosecute UI Benefit Fraud (# of states)

16

10

8

43

25 cases or less over 100 cases 26 to 50 cases 51 to 75 cases 76 to 100 cases

Average Number of UI Overpayment Cases Prosecuted Criminally per Calendar Year (# of states)

35

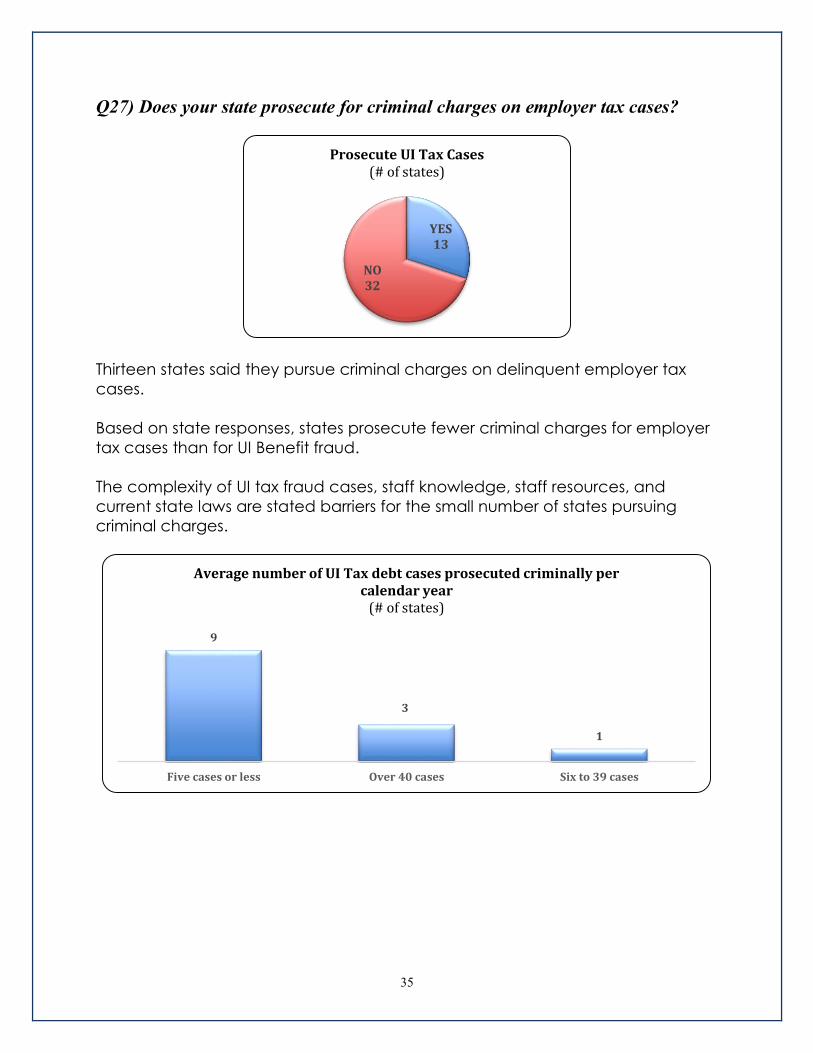

Q27) Does your state prosecute for criminal charges on employer tax cases?

Thirteen states said they pursue criminal charges on delinquent employer tax

cases.

Based on state responses, states prosecute fewer criminal charges for employer

tax cases than for UI Benefit fraud.

The complexity of UI tax fraud cases, staff knowledge, staff resources, and

current state laws are stated barriers for the small number of states pursuing

criminal charges.

YES13

NO32

Prosecute UI Tax Cases (# of states)

9

3

1

Five cases or less Over 40 cases Six to 39 cases

Average number of UI Tax debt cases prosecuted criminally per calendar year

(# of states)

36

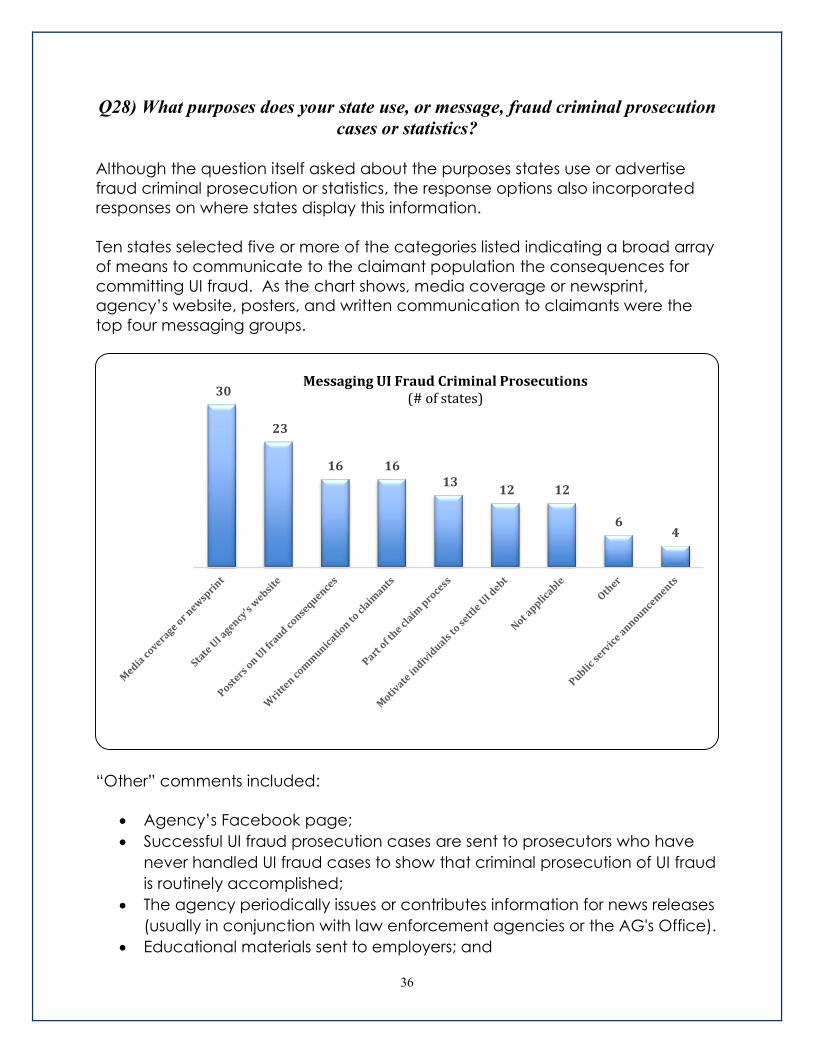

Q28) What purposes does your state use, or message, fraud criminal prosecution

cases or statistics?

Although the question itself asked about the purposes states use or advertise

fraud criminal prosecution or statistics, the response options also incorporated

responses on where states display this information.

Ten states selected five or more of the categories listed indicating a broad array

of means to communicate to the claimant population the consequences for

committing UI fraud. As the chart shows, media coverage or newsprint,

agency’s website, posters, and written communication to claimants were the

top four messaging groups.

“Other” comments included:

Agency’s Facebook page;

Successful UI fraud prosecution cases are sent to prosecutors who have

never handled UI fraud cases to show that criminal prosecution of UI fraud

is routinely accomplished;

The agency periodically issues or contributes information for news releases

(usually in conjunction with law enforcement agencies or the AG's Office).

Educational materials sent to employers; and

30

23

16 1613

12 12

64

Messaging UI Fraud Criminal Prosecutions (# of states)

37

Fraud consequences and warnings are posted to online claims and IVR

systems.

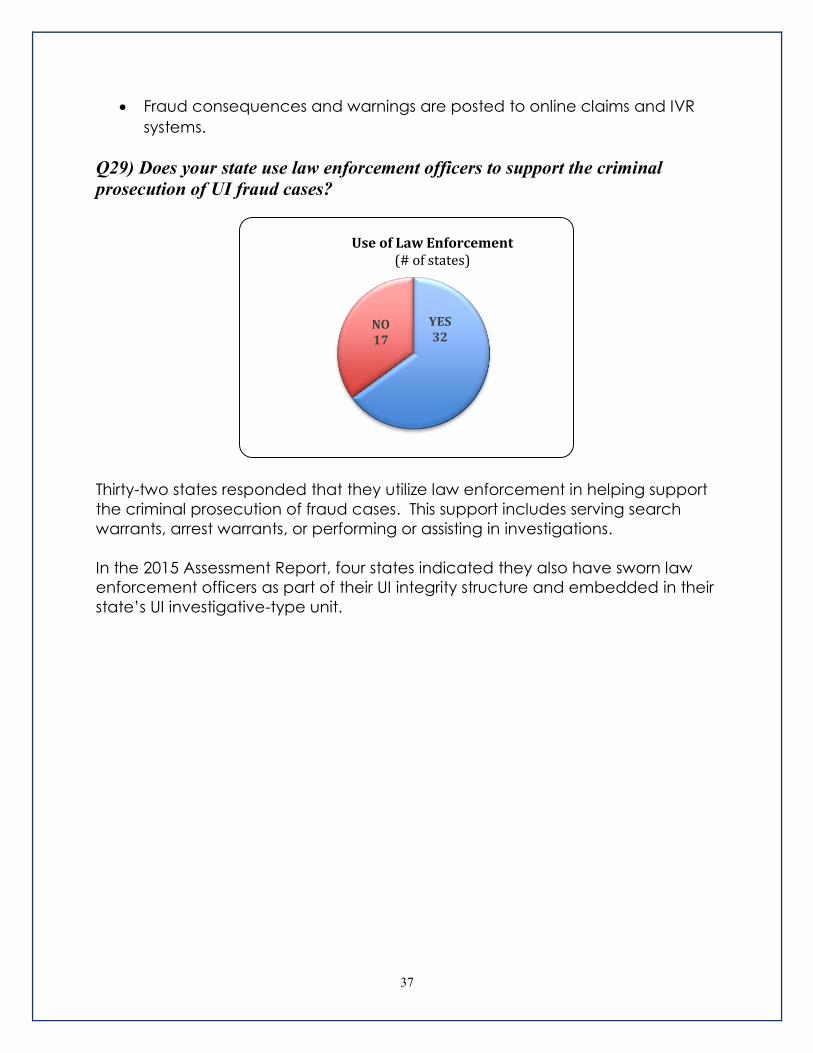

Q29) Does your state use law enforcement officers to support the criminal

prosecution of UI fraud cases?

Thirty-two states responded that they utilize law enforcement in helping support

the criminal prosecution of fraud cases. This support includes serving search

warrants, arrest warrants, or performing or assisting in investigations.

In the 2015 Assessment Report, four states indicated they also have sworn law

enforcement officers as part of their UI integrity structure and embedded in their

state’s UI investigative-type unit.

YES32

NO17

Use of Law Enforcement (# of states)

38

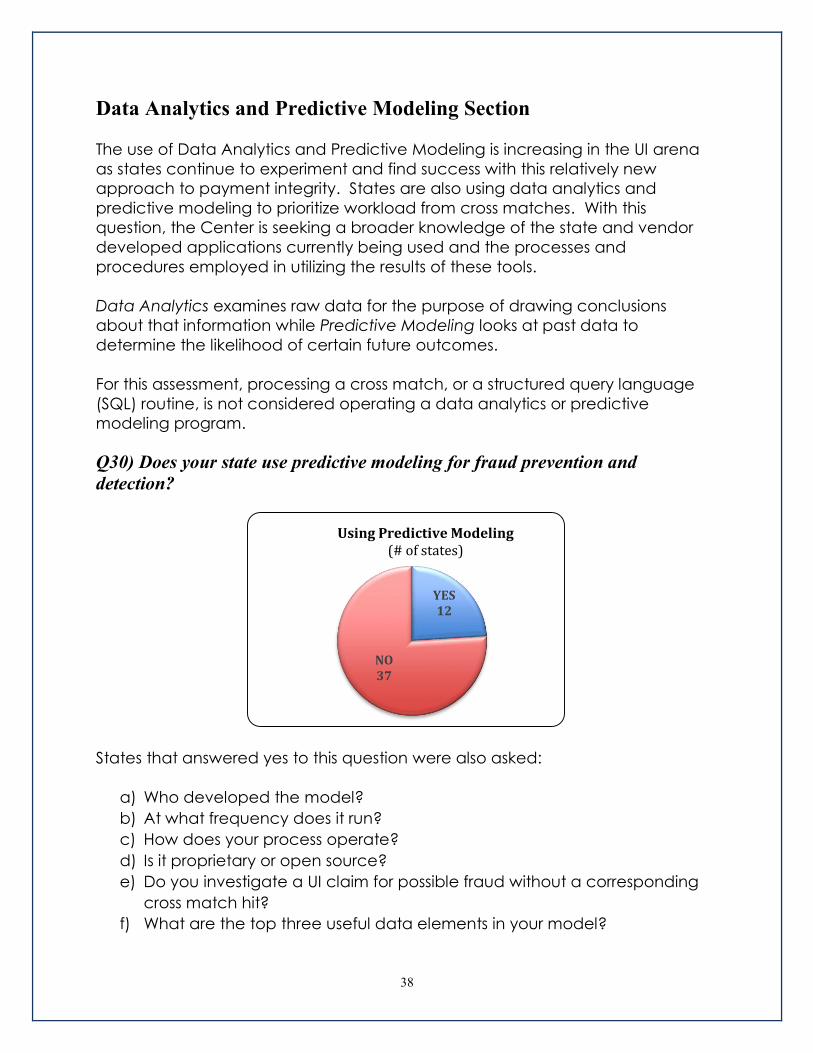

Data Analytics and Predictive Modeling Section

The use of Data Analytics and Predictive Modeling is increasing in the UI arena

as states continue to experiment and find success with this relatively new

approach to payment integrity. States are also using data analytics and

predictive modeling to prioritize workload from cross matches. With this

question, the Center is seeking a broader knowledge of the state and vendor

developed applications currently being used and the processes and

procedures employed in utilizing the results of these tools.

Data Analytics examines raw data for the purpose of drawing conclusions

about that information while Predictive Modeling looks at past data to

determine the likelihood of certain future outcomes.

For this assessment, processing a cross match, or a structured query language

(SQL) routine, is not considered operating a data analytics or predictive

modeling program.

Q30) Does your state use predictive modeling for fraud prevention and

detection?

States that answered yes to this question were also asked:

a) Who developed the model?

b) At what frequency does it run?

c) How does your process operate?

d) Is it proprietary or open source?

e) Do you investigate a UI claim for possible fraud without a corresponding

cross match hit?

f) What are the top three useful data elements in your model?

YES12

NO37

Using Predictive Modeling(# of states)

39

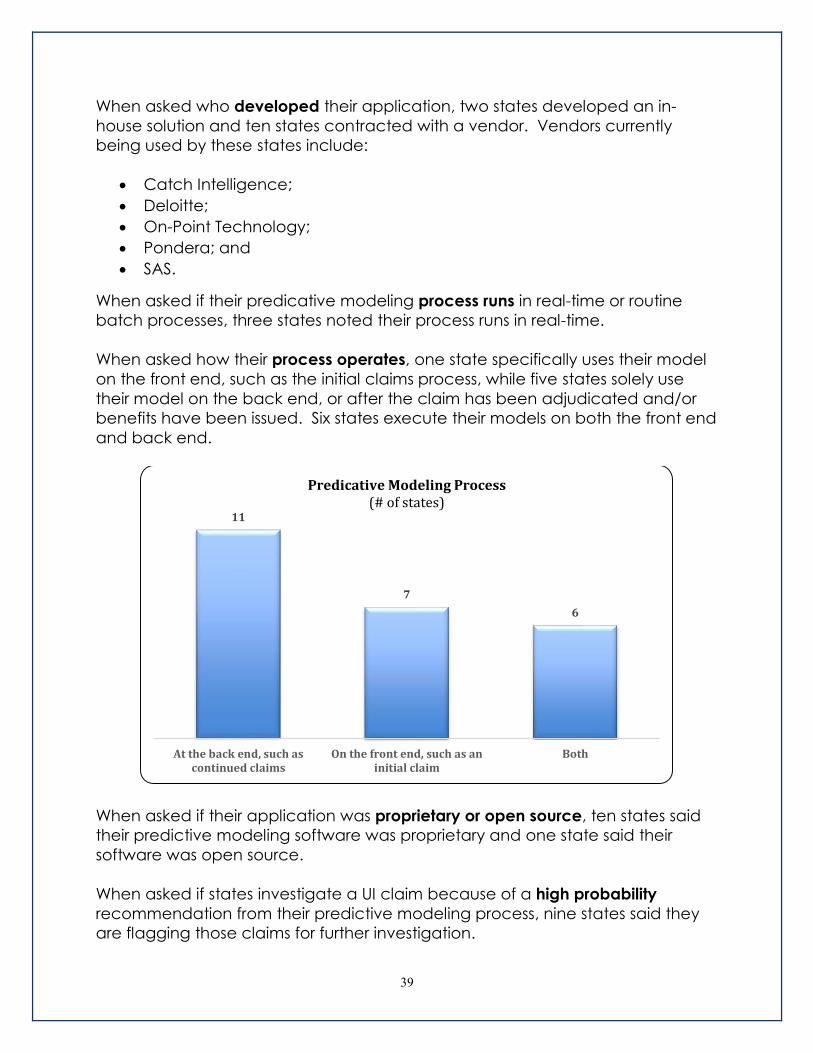

When asked who developed their application, two states developed an in-

house solution and ten states contracted with a vendor. Vendors currently

being used by these states include:

Catch Intelligence;

Deloitte;

On-Point Technology;

Pondera; and

SAS.

When asked if their predicative modeling process runs in real-time or routine

batch processes, three states noted their process runs in real-time.

When asked how their process operates, one state specifically uses their model

on the front end, such as the initial claims process, while five states solely use

their model on the back end, or after the claim has been adjudicated and/or

benefits have been issued. Six states execute their models on both the front end

and back end.

When asked if their application was proprietary or open source, ten states said

their predictive modeling software was proprietary and one state said their

software was open source.

When asked if states investigate a UI claim because of a high probability

recommendation from their predictive modeling process, nine states said they

are flagging those claims for further investigation.

11

7

6

At the back end, such ascontinued claims

On the front end, such as aninitial claim

Both

Predicative Modeling Process (# of states)

40

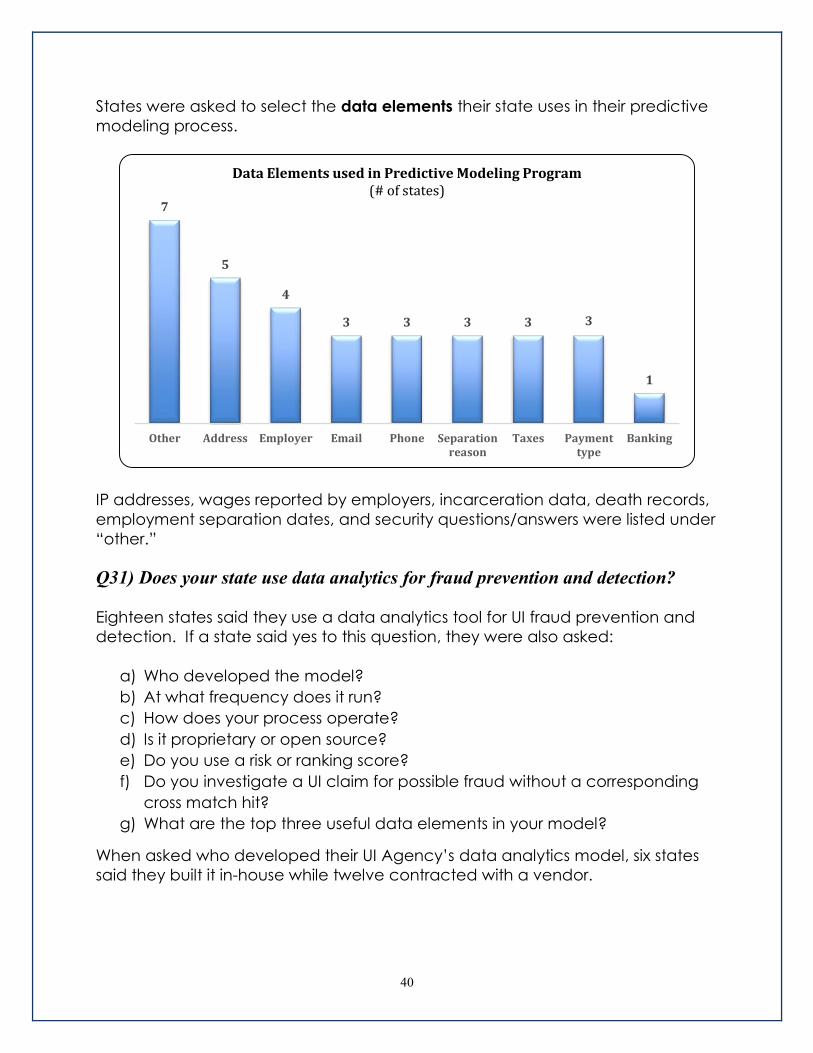

States were asked to select the data elements their state uses in their predictive

modeling process.

IP addresses, wages reported by employers, incarceration data, death records,

employment separation dates, and security questions/answers were listed under

“other.”

Q31) Does your state use data analytics for fraud prevention and detection?

Eighteen states said they use a data analytics tool for UI fraud prevention and

detection. If a state said yes to this question, they were also asked:

a) Who developed the model?

b) At what frequency does it run?

c) How does your process operate?

d) Is it proprietary or open source?

e) Do you use a risk or ranking score?

f) Do you investigate a UI claim for possible fraud without a corresponding

cross match hit?

g) What are the top three useful data elements in your model?

When asked who developed their UI Agency’s data analytics model, six states

said they built it in-house while twelve contracted with a vendor.

7

5

4

3 3 3 3 3

1

Other Address Employer Email Phone Separationreason

Taxes Paymenttype

Banking

Data Elements used in Predictive Modeling Program (# of states)

41

Vendors mentioned included:

Catch Intelligence;

Deloitte;

On-Point Technology;

Pondera;

RSI; and

SAS.

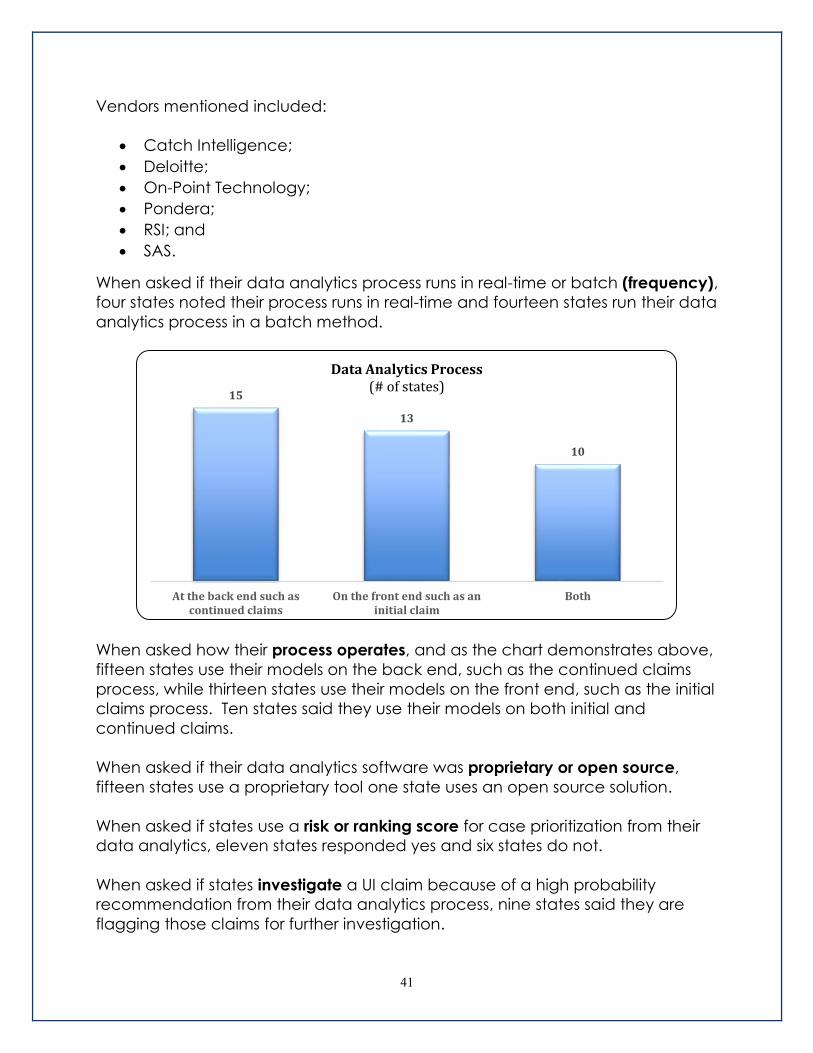

When asked if their data analytics process runs in real-time or batch (frequency),

four states noted their process runs in real-time and fourteen states run their data

analytics process in a batch method.

When asked how their process operates, and as the chart demonstrates above,

fifteen states use their models on the back end, such as the continued claims

process, while thirteen states use their models on the front end, such as the initial

claims process. Ten states said they use their models on both initial and

continued claims.

When asked if their data analytics software was proprietary or open source,

fifteen states use a proprietary tool one state uses an open source solution.

When asked if states use a risk or ranking score for case prioritization from their

data analytics, eleven states responded yes and six states do not.

When asked if states investigate a UI claim because of a high probability

recommendation from their data analytics process, nine states said they are

flagging those claims for further investigation.

15

13

10

At the back end such ascontinued claims

On the front end such as aninitial claim

Both

Data Analytics Process(# of states)

42

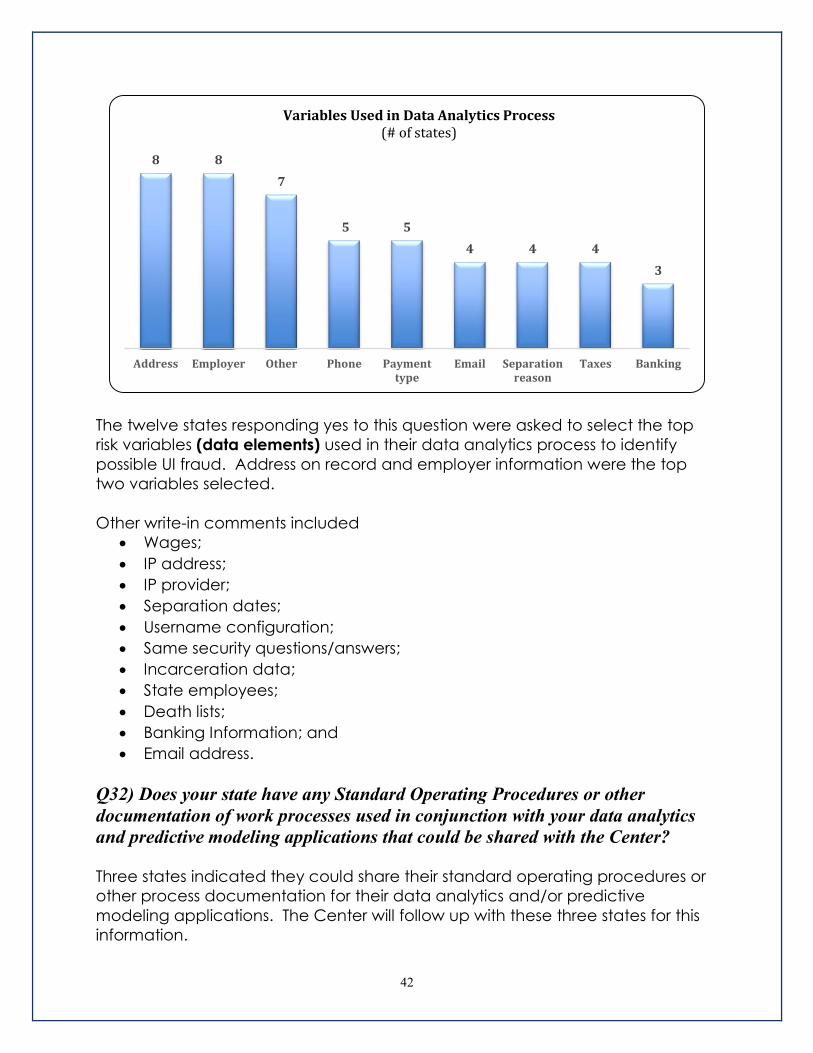

The twelve states responding yes to this question were asked to select the top

risk variables (data elements) used in their data analytics process to identify

possible UI fraud. Address on record and employer information were the top

two variables selected.

Other write-in comments included

Wages;

IP address;

IP provider;

Separation dates;

Username configuration;

Same security questions/answers;

Incarceration data;

State employees;

Death lists;

Banking Information; and

Email address.

Q32) Does your state have any Standard Operating Procedures or other

documentation of work processes used in conjunction with your data analytics

and predictive modeling applications that could be shared with the Center?

Three states indicated they could share their standard operating procedures or

other process documentation for their data analytics and/or predictive

modeling applications. The Center will follow up with these three states for this

information.

8 8

7

5 5

4 4 4

3

Address Employer Other Phone Paymenttype

Email Separationreason

Taxes Banking

Variables Used in Data Analytics Process(# of states)

43

Cross Match Section

With the increasing availability of data that can be used for cross matching and

analysis in the UI Integrity process, the Center wanted to get a better

understanding of specific state activities in this area. The eleven questions

covered the following areas:

State and National Directory of New Hires;

Prison information;

Death records;

Fictitious employers;

Frequency of the matches;

How cross match hits are prioritized for investigation;

Changes to existing cross matches; and

Implementing new cross matches.

Responses revealed that states are expanding their use of cross matches to

prevent and detect possible fraudulent or suspicious actions. Various states are

contracting with vendors to access national databases and/or additional public

information data to strengthen their existing cross match activities. States are

exploring and experimenting with processes to prevent improper payments

before they are issued, and are implementing cross matches during the initial

claim process to help stop UI fraud.

Q33) Does your UI agency cross match with your state’s State Directory of New

Hires (SDNH)?

Forty-four states said they cross match with their state’s SDNH database. If a

state said yes to this question, they were also asked:

a) The frequency,

b) Statutory authority to assess penalties,

c) Actively enforcing the penalty assessment, and

d) Identifying employers who are non-compliant.

44

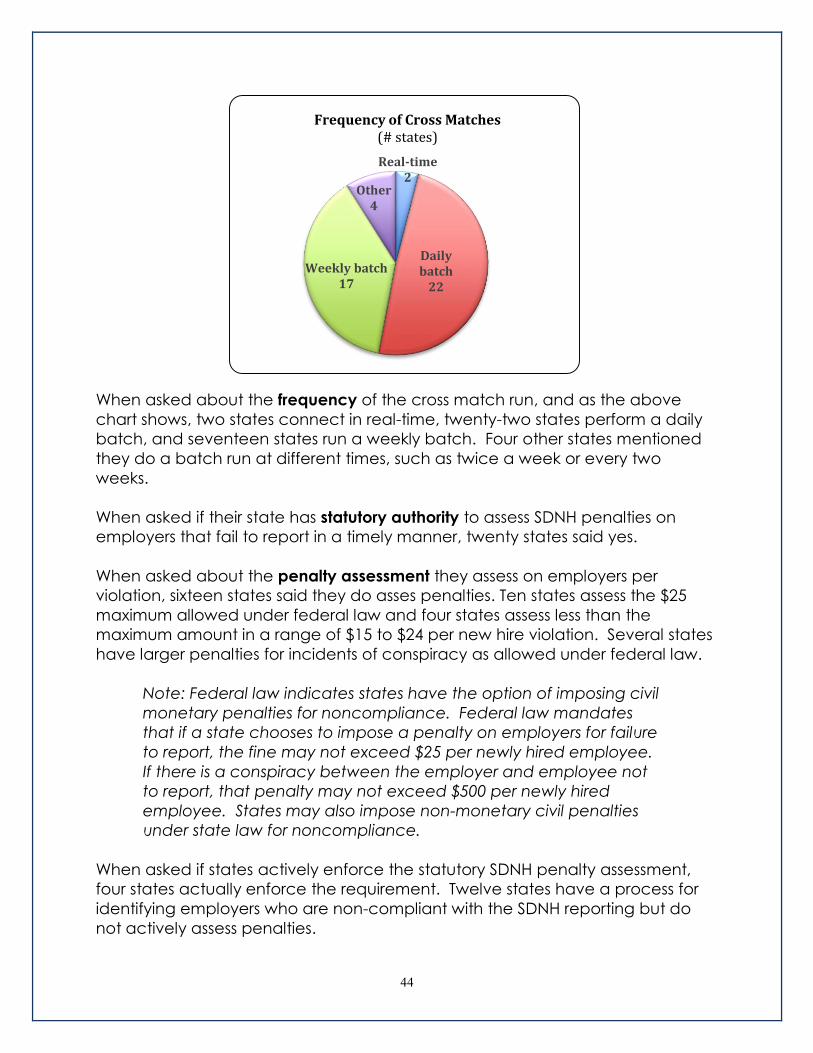

When asked about the frequency of the cross match run, and as the above

chart shows, two states connect in real-time, twenty-two states perform a daily

batch, and seventeen states run a weekly batch. Four other states mentioned

they do a batch run at different times, such as twice a week or every two

weeks.

When asked if their state has statutory authority to assess SDNH penalties on

employers that fail to report in a timely manner, twenty states said yes.

When asked about the penalty assessment they assess on employers per

violation, sixteen states said they do asses penalties. Ten states assess the $25

maximum allowed under federal law and four states assess less than the

maximum amount in a range of $15 to $24 per new hire violation. Several states

have larger penalties for incidents of conspiracy as allowed under federal law.

Note: Federal law indicates states have the option of imposing civil

monetary penalties for noncompliance. Federal law mandates

that if a state chooses to impose a penalty on employers for failure

to report, the fine may not exceed $25 per newly hired employee.

If there is a conspiracy between the employer and employee not

to report, that penalty may not exceed $500 per newly hired

employee. States may also impose non-monetary civil penalties

under state law for noncompliance.

When asked if states actively enforce the statutory SDNH penalty assessment,

four states actually enforce the requirement. Twelve states have a process for

identifying employers who are non-compliant with the SDNH reporting but do

not actively assess penalties.

Real-time2

Daily batch

22

Weekly batch17

Other4

Frequency of Cross Matches (# states)

45

States were asked what process they use to identify employers who are non-

compliant with the SDNH reporting requirements. Three states have automated

their cross match using quarterly wage data and the NDNH database. Five

states have automated their cross match using quarterly wage data, the SDNH

database, and "multi-state filer" database provided by Office of Child Support

Enforcement. One state finds non-compliant employers as a result of regular

scheduled employer UI Tax audits.

Four states use their process for identifying non-compliant employers solely for

marketing and outreach efforts to those employers to make them aware of the

reporting requirements.

Q34) Which UI claims does your state run against the National Directory of New

Hires (NDNH)?

State and federal law requires employers to report newly hired and re-hired

employees to the NDNH. The U.S. Department of Health & Human Services’

Office of Child Support Enforcement (OCSE) operates the NDNH, a database

established pursuant to the Personal Responsibility and Work Opportunity

Reconciliation Act of 1996. The primary purpose of the SDNH and NDNH is to

assist state child support agencies in locating parents and enforcing child

support orders. Congress also has authorized specific state and federal

agencies, including UI agencies, to receive information from the NDNH for

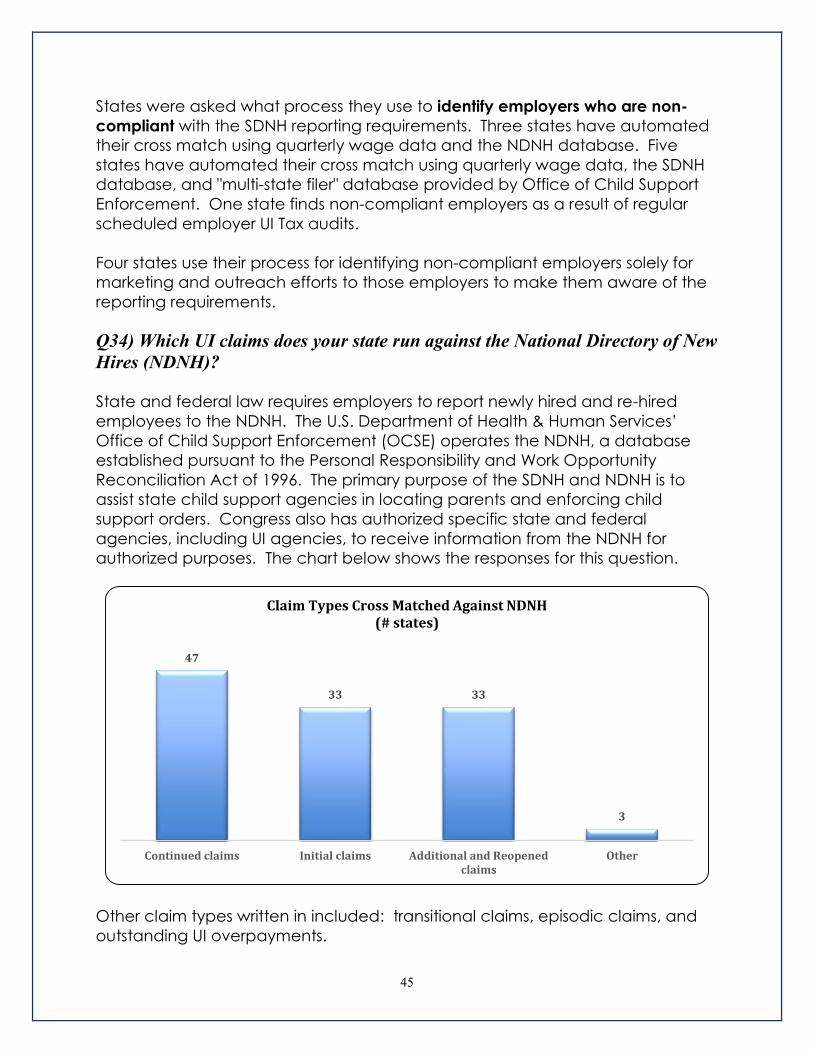

authorized purposes. The chart below shows the responses for this question.

Other claim types written in included: transitional claims, episodic claims, and

outstanding UI overpayments.

47

33 33

3

Continued claims Initial claims Additional and Reopenedclaims

Other

Claim Types Cross Matched Against NDNH (# states)

46

Q35) What is the frequency of your cross match with the NDNH?

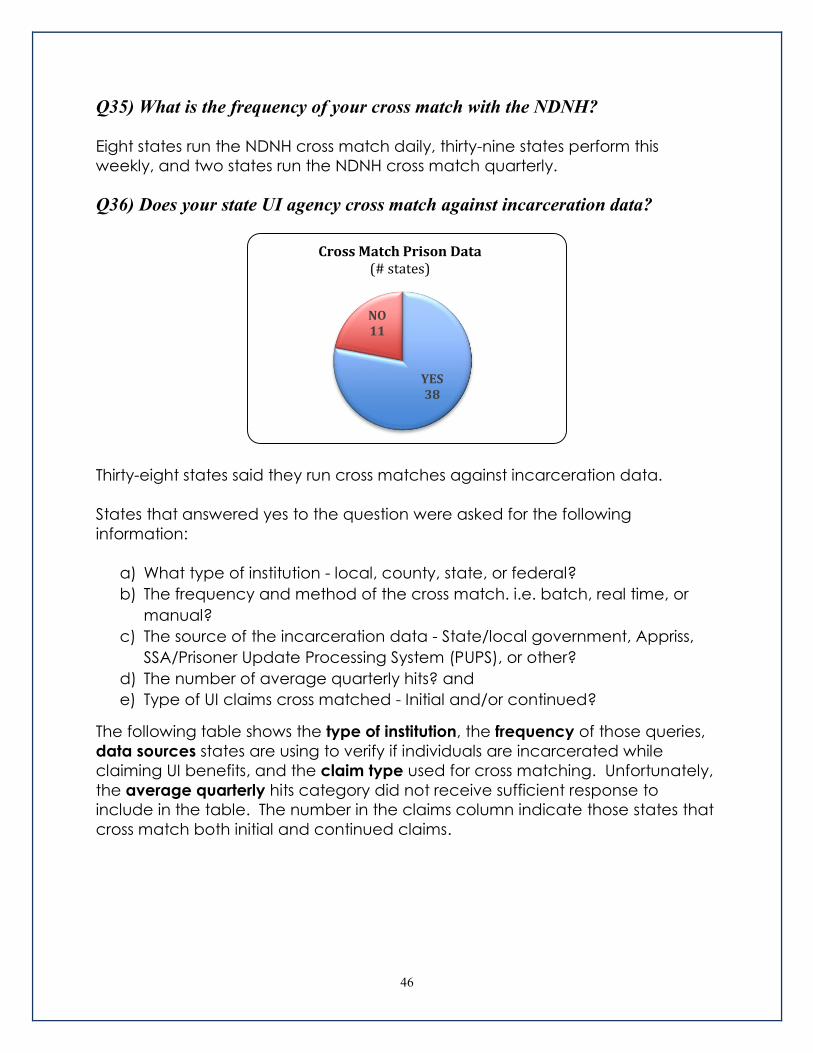

Eight states run the NDNH cross match daily, thirty-nine states perform this

weekly, and two states run the NDNH cross match quarterly.

Q36) Does your state UI agency cross match against incarceration data?

Thirty-eight states said they run cross matches against incarceration data.

States that answered yes to the question were asked for the following

information:

a) What type of institution - local, county, state, or federal?

b) The frequency and method of the cross match. i.e. batch, real time, or

manual?

c) The source of the incarceration data - State/local government, Appriss,

SSA/Prisoner Update Processing System (PUPS), or other?

d) The number of average quarterly hits? and

e) Type of UI claims cross matched - Initial and/or continued?

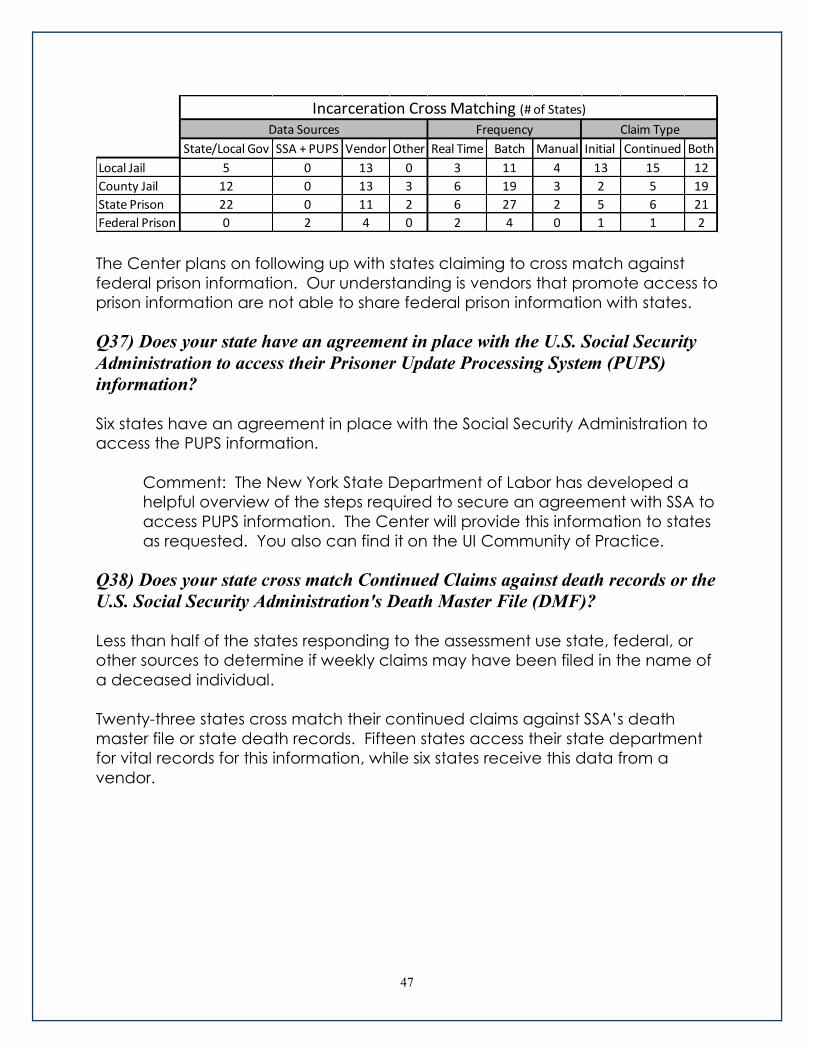

The following table shows the type of institution, the frequency of those queries,

data sources states are using to verify if individuals are incarcerated while

claiming UI benefits, and the claim type used for cross matching. Unfortunately,

the average quarterly hits category did not receive sufficient response to

include in the table. The number in the claims column indicate those states that

cross match both initial and continued claims.

YES38

NO11

Cross Match Prison Data(# states)

47

The Center plans on following up with states claiming to cross match against

federal prison information. Our understanding is vendors that promote access to

prison information are not able to share federal prison information with states.

Q37) Does your state have an agreement in place with the U.S. Social Security

Administration to access their Prisoner Update Processing System (PUPS)

information?

Six states have an agreement in place with the Social Security Administration to

access the PUPS information.

Comment: The New York State Department of Labor has developed a

helpful overview of the steps required to secure an agreement with SSA to

access PUPS information. The Center will provide this information to states

as requested. You also can find it on the UI Community of Practice.

Q38) Does your state cross match Continued Claims against death records or the

U.S. Social Security Administration's Death Master File (DMF)?

Less than half of the states responding to the assessment use state, federal, or

other sources to determine if weekly claims may have been filed in the name of

a deceased individual.

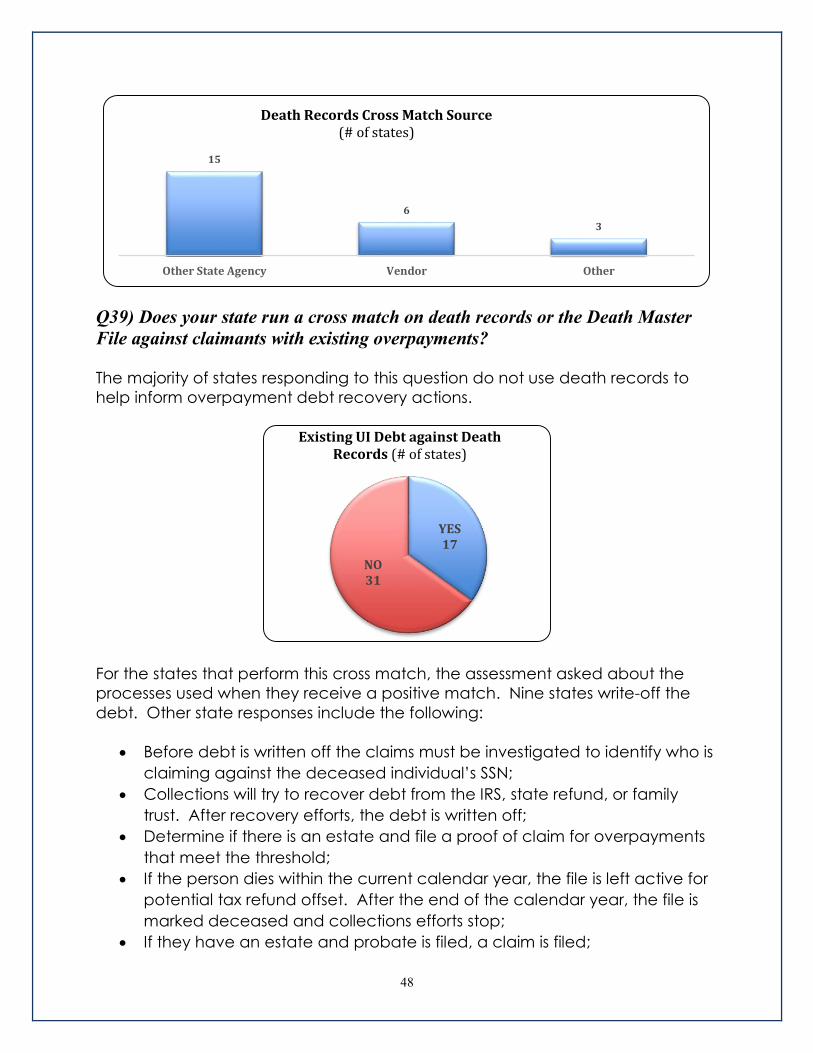

Twenty-three states cross match their continued claims against SSA’s death

master file or state death records. Fifteen states access their state department

for vital records for this information, while six states receive this data from a

vendor.

State/Local Gov SSA + PUPS Vendor Other Real Time Batch Manual Initial Continued Both

Local Jail 5 0 13 0 3 11 4 13 15 12

County Jail 12 0 13 3 6 19 3 2 5 19

State Prison 22 0 11 2 6 27 2 5 6 21

Federal Prison 0 2 4 0 2 4 0 1 1 2

Data Sources Frequency Claim Type

Incarceration Cross Matching (# of States)

48

Q39) Does your state run a cross match on death records or the Death Master

File against claimants with existing overpayments?

The majority of states responding to this question do not use death records to

help inform overpayment debt recovery actions.

For the states that perform this cross match, the assessment asked about the

processes used when they receive a positive match. Nine states write-off the

debt. Other state responses include the following:

Before debt is written off the claims must be investigated to identify who is

claiming against the deceased individual’s SSN;

Collections will try to recover debt from the IRS, state refund, or family

trust. After recovery efforts, the debt is written off;

Determine if there is an estate and file a proof of claim for overpayments

that meet the threshold;

If the person dies within the current calendar year, the file is left active for

potential tax refund offset. After the end of the calendar year, the file is

marked deceased and collections efforts stop;

If they have an estate and probate is filed, a claim is filed;

15

6

3

Other State Agency Vendor Other

Death Records Cross Match Source (# of states)

YES17

NO31

Existing UI Debt against Death Records (# of states)

49

Notate file as deceased and then the UI claim is stopped for active

collection;

Submit to estate for collection; and

Deceased claimants with overpayments are submitted for write-off

consideration through the state write-off approval process.

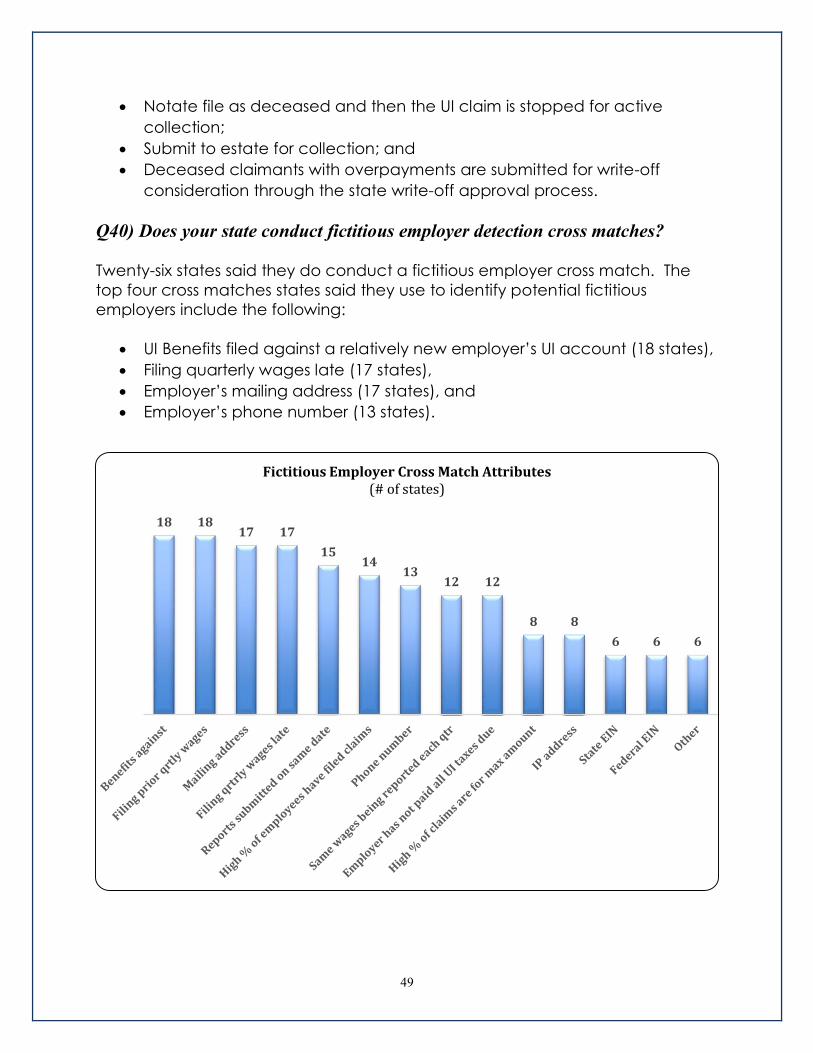

Q40) Does your state conduct fictitious employer detection cross matches?

Twenty-six states said they do conduct a fictitious employer cross match. The

top four cross matches states said they use to identify potential fictitious

employers include the following:

UI Benefits filed against a relatively new employer’s UI account (18 states),

Filing quarterly wages late (17 states),

Employer’s mailing address (17 states), and

Employer’s phone number (13 states).

18 1817 17

1514

1312 12

8 8

6 6 6

Fictitious Employer Cross Match Attributes(# of states)

50

Six states also provided additional comments on data sources they use for

fictitious employer queries or cross matches as follows:

State Department of Revenue or Tax Commission;

Manual review of employer information on quarterly wages;

No SSN for owners or officers, no FEIN for employer, or no predecessor for

employer;

Part of the analysis compares the employer IP address, mailing address

and phone number against the employee's claim information. Also

compare the employer's state tax ID to how new it is in the system and if it

has a preceding account;

Registration in person; and

Similar wages reported for all employees of the business.

The descending numeric order of the other information states said they use are

listed here:

Filing prior quarterly wages as a new employer – 18 states;

First UI benefits being filed against relatively new employer’s UI account –

18 states;

Filing quarterly wages late – 17 states;

Mailing address – 17 states;

Multiple wage reports submitted on same date – 15 states;

High percentage of employer’s employees have filed claims against the

employer – 14 states;

Phone number – 13 states;

Employer has not paid all taxes due – 12 states;

Same wages being reported per worker multiple quarters – 12 states;

High percentage of employer’s claims are for Maximum Weekly Benefit

amount – 8 states;

IP address – 8 states;

Federal employer identification number – 6 states; and

State employer identification number – 6 states.

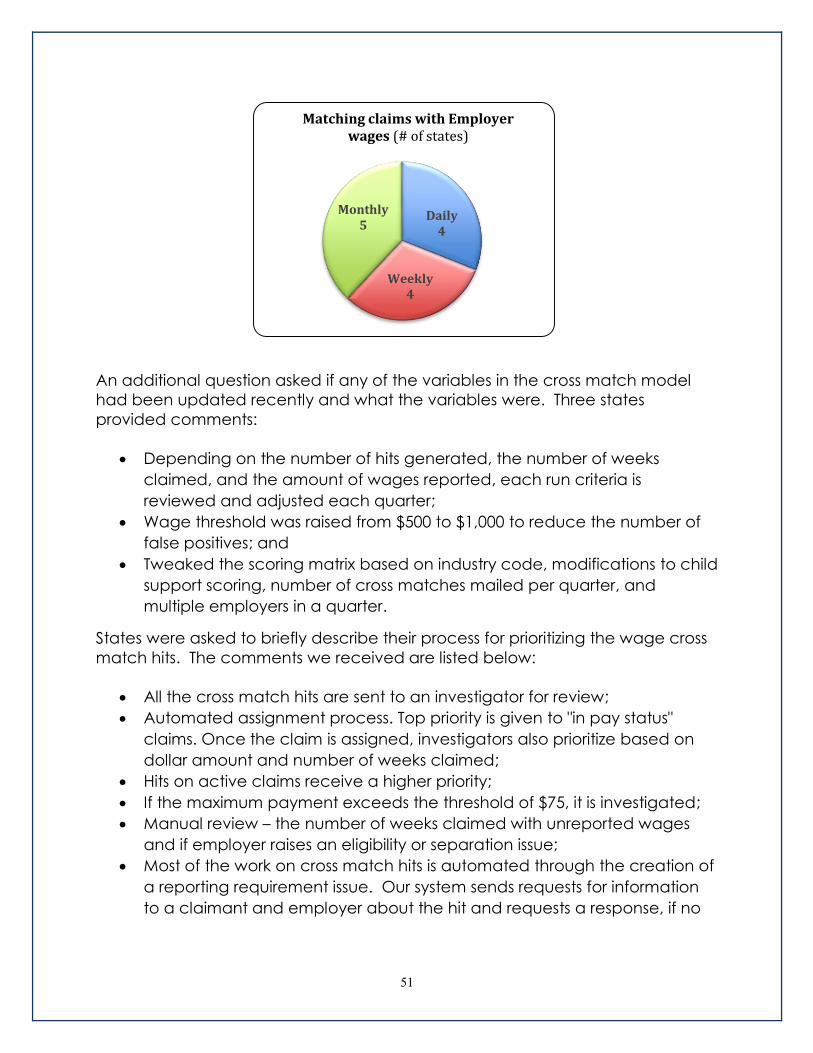

Q41) Does your state's quarterly wage cross match run more than once a

quarter?

Thirteen states run the quarterly wage cross match more than once a quarter. If

a state said yes to this question, they were also asked how often they match

claims against employer wages. The responses are indicated in the chart below.

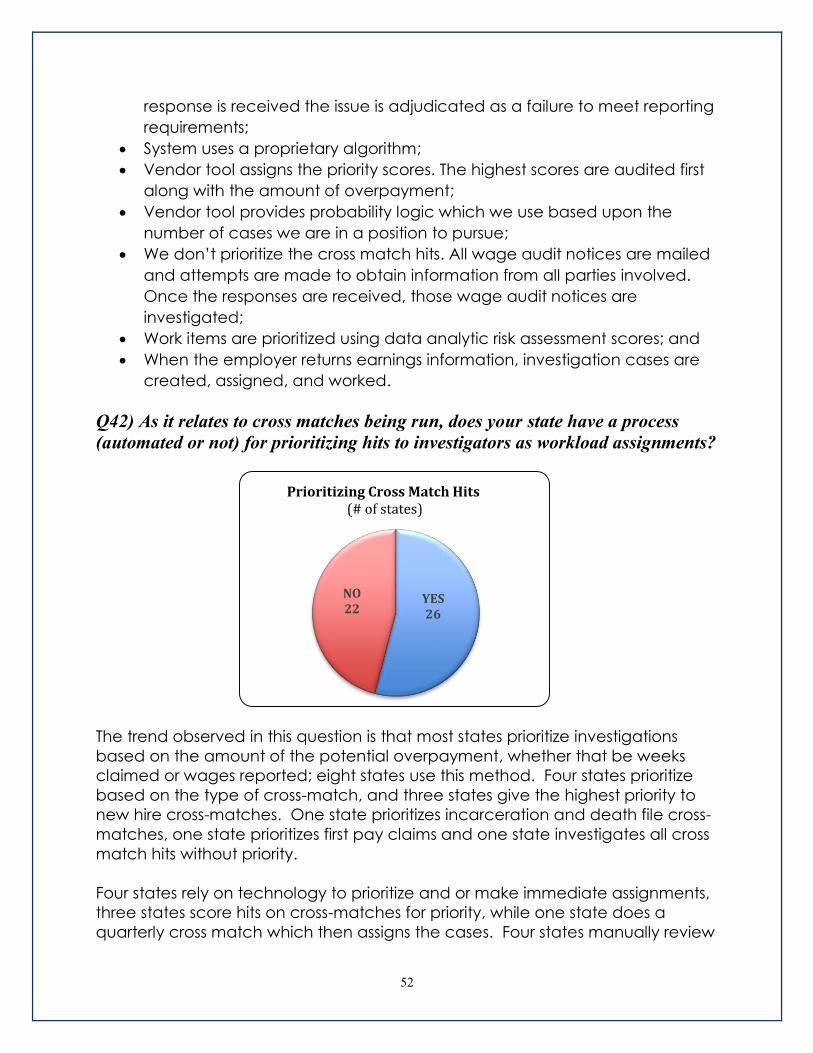

51

An additional question asked if any of the variables in the cross match model

had been updated recently and what the variables were. Three states

provided comments:

Depending on the number of hits generated, the number of weeks

claimed, and the amount of wages reported, each run criteria is

reviewed and adjusted each quarter;

Wage threshold was raised from $500 to $1,000 to reduce the number of

false positives; and

Tweaked the scoring matrix based on industry code, modifications to child

support scoring, number of cross matches mailed per quarter, and

multiple employers in a quarter.