1

GM

O Q

uant

itat

ive

Res

earc

h

abcd2003 Pensions Convention

1 - 3 JuneGrand Hotel, Brighton

TMT 1999 – 2001 A Bubble MovieAn analysis of the biggest investment bubble in history!

Simon Harris, GMO

What happened: a reminderUK Equities

GM

O Q

uant

itat

ive

Res

earc

h

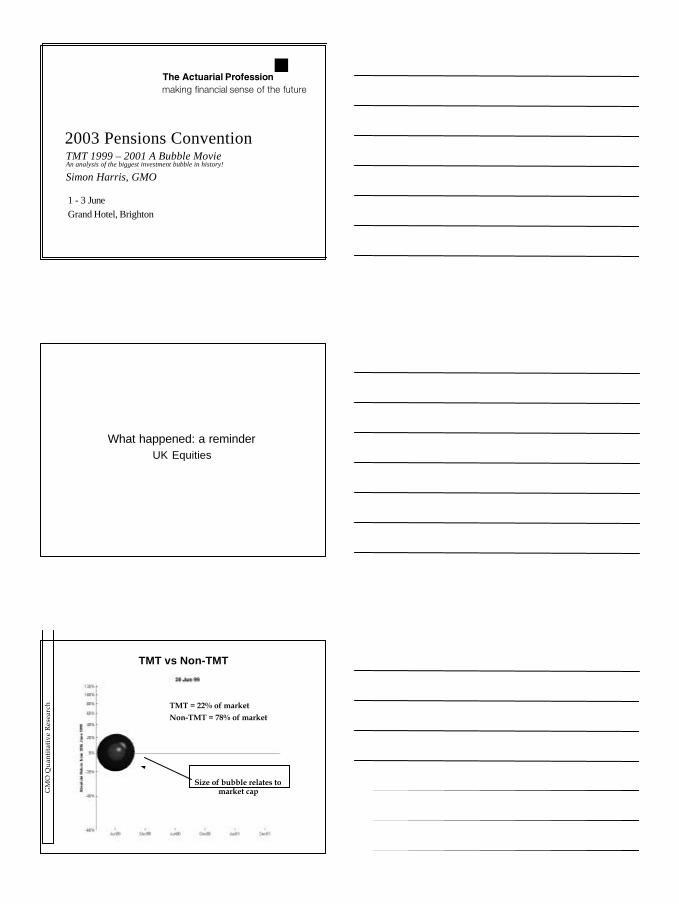

TMT vs Non-TMT

Size of bubble relates tomarket cap

Non-TMT = 78% of marketTMT = 22% of market

2

GM

O Q

uant

itat

ive

Res

earc

h

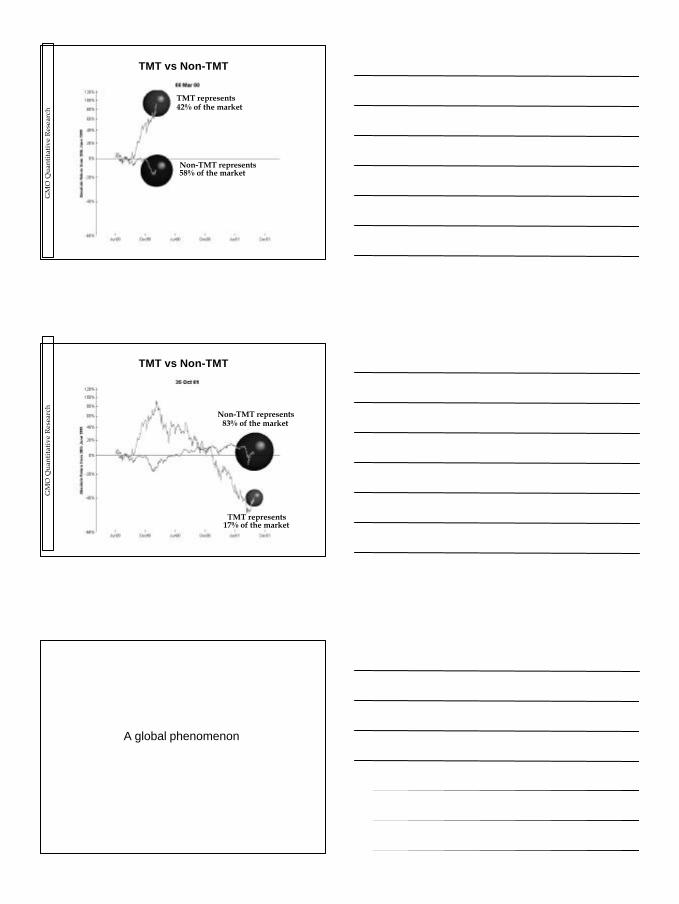

TMT vs Non-TMT

TMT represents42% of the market

Non-TMT represents58% of the market

GM

O Q

uant

itat

ive

Res

earc

h

TMT vs Non-TMT

TMT represents17% of the market

Non-TMT represents83% of the market

A global phenomenon

3

GM

O Q

uant

itat

ive

Res

earc

h

7

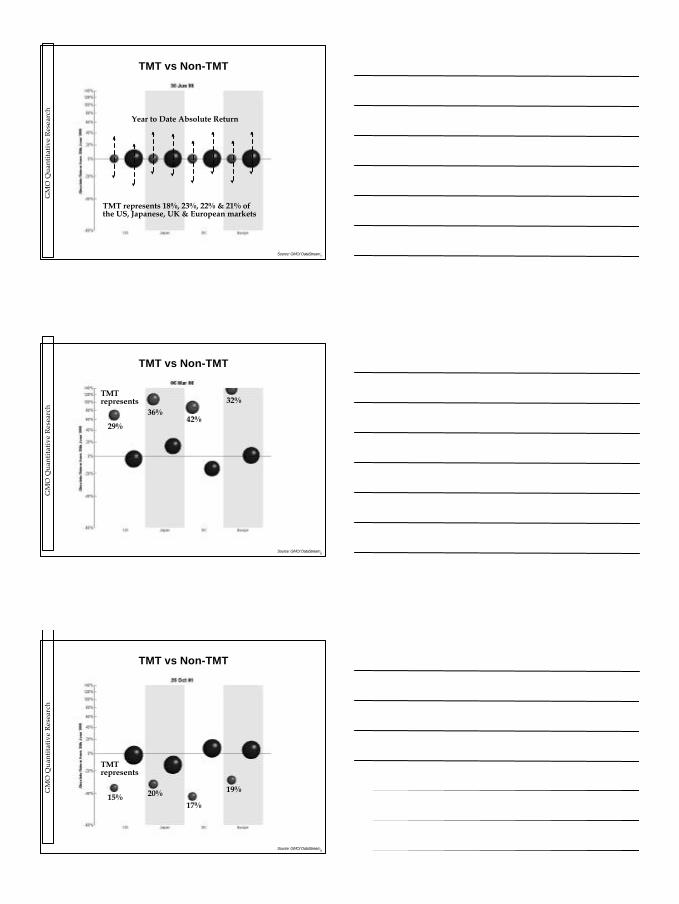

TMT represents 18%, 23%, 22% & 21% ofthe US, Japanese, UK & European markets

Year to Date Absolute Return

TMT vs Non-TMT

Source: GMO/ DataStream

GM

O Q

uant

itat

ive

Res

earc

h

8

29%

36%42%

32%

TMT vs Non-TMT

TMTrepresents

Source: GMO/ DataStream

GM

O Q

uant

itat

ive

Res

earc

h

9

15% 20%17%

19%

TMT vs Non-TMT

TMTrepresents

Source: GMO/ DataStream

4

GM

O Q

uant

itat

ive

Res

earc

h

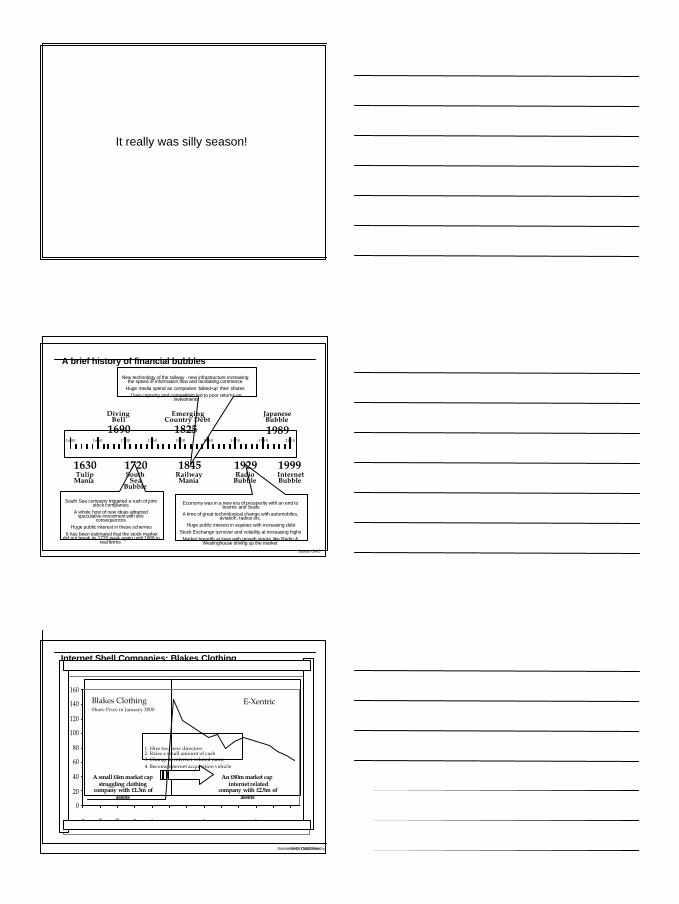

It really was silly season!

GM

O Q

uant

itat

ive

Res

earc

h

New technology of the railway - new infrastructure increasingthe speed of information flow and facilitating commerce

Huge media spend as companies ‘talked-up’ their sharesOver capacity and competition led to poor returns on

investments

Economy was in a new era of prosperity with an end tobooms and busts

A time of great technological change with automobiles,aviation, radios etc.

Huge public interest in equities with increasing debtStock Exchange turnover and volatility at increasing highs

Market breadth at lows with growth stocks like Radio &Westinghouse driving up the market

South Sea company triggered a rush of jointstock companies

A whole host of new ideas attractedspeculative investment with dire

consequencesHuge public interest in these schemes

It has been estimated that the stock marketdid not break its 1720 peak again until 1968 in

real terms

1720South

SeaBubble

1845RailwayMania

1690Diving

Bell

1929Radio

Bubble

1999InternetBubble

1630Tulip

Mania

1825Emerging

Country Debt

1989

JapaneseBubble

2000195019001600 1650 1700 1750 1800 1850

A brief history of financial bubbles

Source: GMO

GM

O Q

uant

itat

ive

Res

earc

h

Internet Shell Companies: Blakes Clothing

0

20

40

60

80

100

120

140

160

3-Jan

5-Jan

7-Jan

9-Jan

11-Jan

13-Jan

15-Jan

17-Jan

19-Jan

21-Jan

23-Jan

25-Jan

27-Jan

A small £4m market capstruggling clothing

company with £1.3m ofassets

1. Hire two new directors2. Raise a small amount of cash3. Change to internet-related name4. Become internet acquisition vehicle

An £80m market capinternet related

company with £2.9m ofassets

Blakes ClothingShare Price in January 2000

E-Xentric

Source: GMO WoolleySource: GMO/ DataStream

5

GM

O Q

uant

itat

ive

Res

earc

h

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

Feb-99Mar-99

Apr-99 May-99Jun-99

Jul-99 Aug-99Sep-99

Oct-99

Nov-99Dec-9

9Jan-00

8 Feb

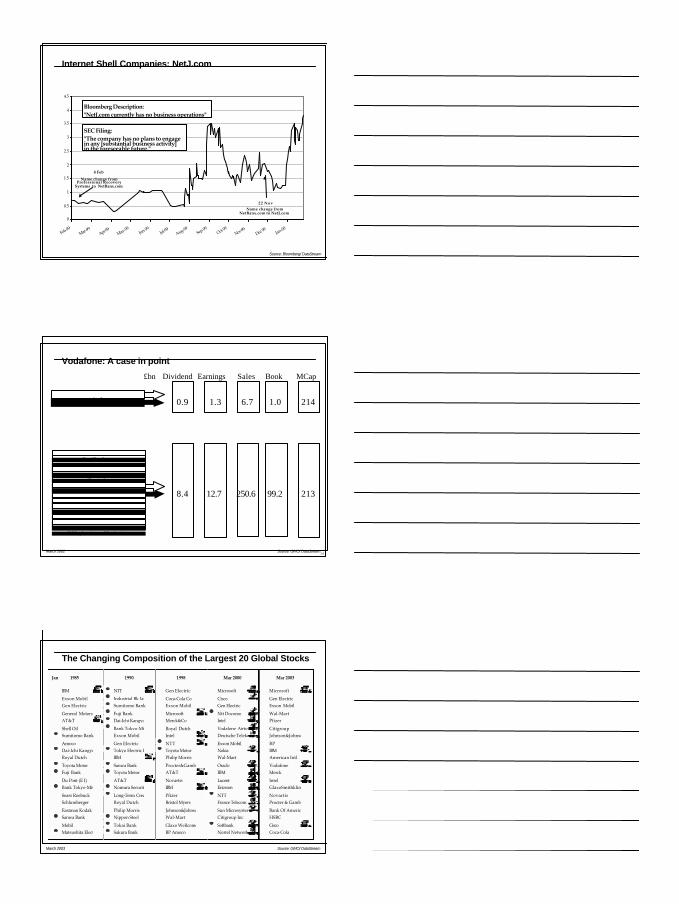

Name change fromProfessional Recovery

Systems to NetBanx.com

22 NovName change from

NetBanx.com to NetJ.com

Bloomberg Description:"NetJ.com currently has no business operations"

SEC Filing:"The company has no plans to engagein any [substantial business activity]in the foreseeable future."

Internet Shell Companies: NetJ.com

Source: Bloomberg/ DataStream

GM

O Q

uant

itat

ive

Res

earc

h

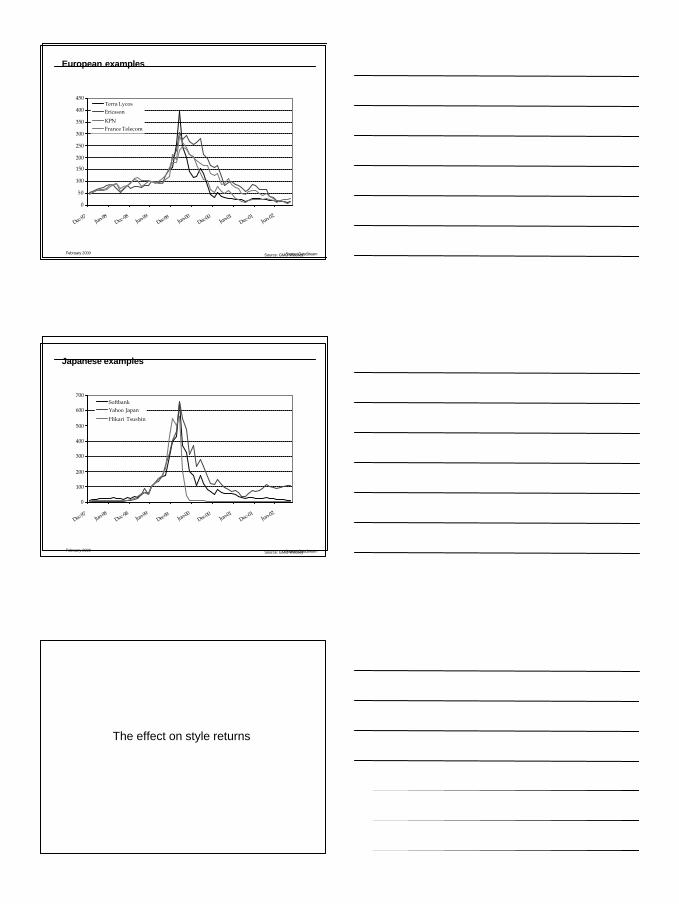

Vodafone: A case in point

Gas DistributionReal Estate

Food Retailers

Construction & Building MaterialsHealthcare

Engineering Vehicles

DistributorsDiversified Industrials

TobaccoChemicals

Alcoholic Beverages

Water

0.9 1.3 6.7 1.0

8.4 12.7 250.6 99.2

Dividend Earnings Sales Book£bn MCap

Vodafone 214

213

March 2002

Print, Paper & Packaging

Oil Exploration and ProductionHousehold Goods

14Source: GMO/ DataStream

GM

O Q

uant

itat

ive

Res

earc

h

Jan 1985 1990 1998 Mar 2000 Mar 2003

IBM NTT Gen Electric Microsoft Microsoft

Exxon Mobil Industrial Bk Japan Coca-Cola Co Cisco Gen Electric

Gen Electric Sumitomo Bank Exxon Mobil Gen Electric Exxon Mobil

General Motors Fuji Bank Microsoft Ntt Docomo Wal-Mart

AT&T Dai-Ichi Kangyo Bank Merck&Co Intel Pfizer

Shell Oil Bank Tokyo-Mitsubish Royal Dutch Vodafone Airtouch Citigroup

Sumitomo Bank Exxon Mobil Intel Deutsche Telekom Johnson&Johnson

Amoco Gen Electric NTT Exxon Mobil BP

Dai-Ichi Kangyo Bank Tokyo Electric Power Toyota Motor Nokia IBM

Royal Dutch IBM Philip Morris Wal-Mart American Intl

Toyota Motor Sanwa Bank Procter&Gamble Oracle Vodafone

Fuji Bank Toyota Motor AT&T IBM Merck

Du Pont (E I) AT&T Novartis Lucent Intel

Bank Tokyo-Mitsubish Nomura Securities Co IBM Ericsson GlaxoSmithkline

Sears Roebuck Long-Term Credit Ban Pfizer NTT Novartis

Schlumberger Royal Dutch Bristol Myers France Telecom Procter & Gamble

Eastman Kodak Philip Morris Johnson&Johnson Sun Microsystems Bank Of America

Sanwa Bank Nippon Steel Wal-Mart Citigroup Inc HSBC

Mobil Tokai Bank Glaxo Wellcome Softbank Cisco

Matsushita Elect Sakura Bank BP Amoco Nortel Networks Coca-Cola

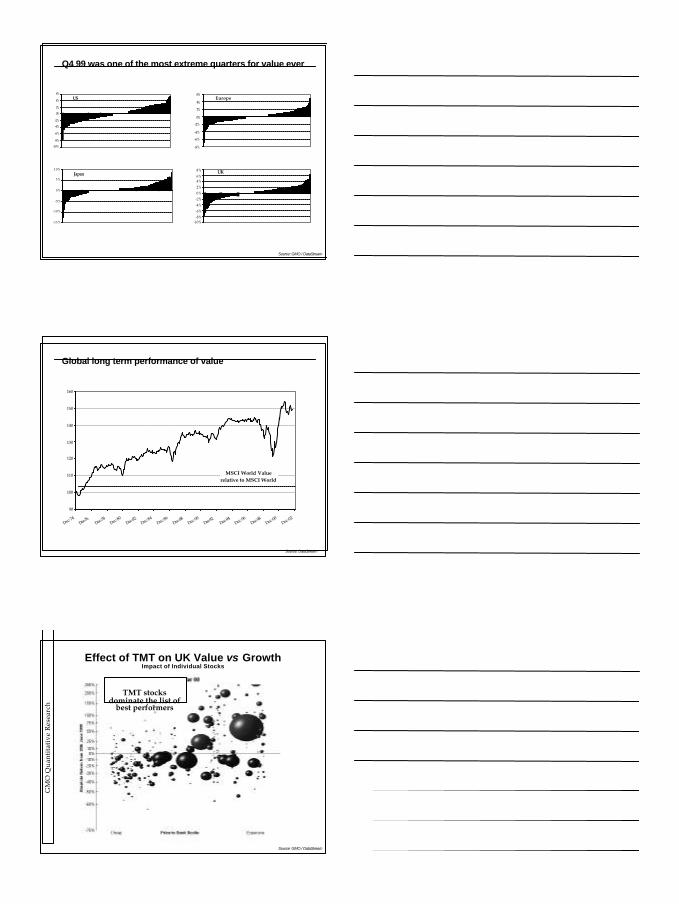

The Changing Composition of the Largest 20 Global Stocks

Jan 1985 1990 1998 Mar 2000

IBM NTT Gen Electric Microsoft

Exxon Mobil Industrial Bk Japan Coca-Cola Co Cisco

Gen Electric Sumitomo Bank Exxon Mobil Gen Electric

General Motors Fuji Bank Microsoft Ntt Docomo

AT&T Dai-Ichi Kangyo Bank Merck&Co Intel

Shell Oil Bank Tokyo-Mitsubish Royal Dutch Vodafone Airtouch

Sumitomo Bank Exxon Mobil Intel Deutsche Telekom

Amoco Gen Electric NTT Exxon Mobil

Dai-Ichi Kangyo Bank Tokyo Electric Power Toyota Motor Nokia

Royal Dutch IBM Philip Morris Wal-Mart

Toyota Motor Sanwa Bank Procter&Gamble Oracle

Fuji Bank Toyota Motor AT&T IBM

Du Pont (E I) AT&T Novartis Lucent

Bank Tokyo-Mitsubish Nomura Securities Co IBM Ericsson

Sears Roebuck Long-Term Credit Ban Pfizer NTT

Schlumberger Royal Dutch Bristol Myers France Telecom

Eastman Kodak Philip Morris Johnson&Johnson Sun Microsystems

Sanwa Bank Nippon Steel Wal-Mart Citigroup Inc

Mobil Tokai Bank Glaxo Wellcome Softbank

Matsushita Elect Sakura Bank BP Amoco Nortel Networks

Jan 1985 1990 1998

IBM NTT Gen Electric

Exxon Mobil Industrial Bk Japan Coca-Cola Co

Gen Electric Sumitomo Bank Exxon Mobil

General Motors Fuji Bank Microsoft

AT&T Dai-Ichi Kangyo Bank Merck&Co

Shell Oil Bank Tokyo-Mitsubish Royal Dutch

Sumitomo Bank Exxon Mobil Intel

Amoco Gen Electric NTT

Dai-Ichi Kangyo Bank Tokyo Electric Power Toyota Motor

Royal Dutch IBM Philip Morris

Toyota Motor Sanwa Bank Procter&Gamble

Fuji Bank Toyota Motor AT&T

Du Pont (E I) AT&T Novartis

Bank Tokyo-Mitsubish Nomura Securities Co IBM

Sears Roebuck Long-Term Credit Ban Pfizer

Schlumberger Royal Dutch Bristol Myers

Eastman Kodak Philip Morris Johnson&Johnson

Sanwa Bank Nippon Steel Wal-Mart

Mobil Tokai Bank Glaxo Wellcome

Matsushita Elect Sakura Bank BP Amoco

Jan 1985 1990

IBM NTT

Exxon Mobil Industrial Bk Japan

Gen Electric Sumitomo Bank

General Motors Fuji Bank

AT&T Dai-Ichi Kangyo Bank

Shell Oil Bank Tokyo-Mitsubish

Sumitomo Bank Exxon Mobil

Amoco Gen Electric

Dai-Ichi Kangyo Bank Tokyo Electric Power

Royal Dutch IBM

Toyota Motor Sanwa Bank

Fuji Bank Toyota Motor

Du Pont (E I) AT&T

Bank Tokyo-Mitsubish Nomura Securities Co

Sears Roebuck Long-Term Credit Ban

Schlumberger Royal Dutch

Eastman Kodak Philip Morris

Sanwa Bank Nippon Steel

Mobil Tokai Bank

Matsushita Elect Sakura Bank

Jan 1985

IBM

Exxon Mobil

Gen Electric

General Motors

AT&T

Shell Oil

Sumitomo Bank

Amoco

Dai-Ichi Kangyo Bank

Royal Dutch

Toyota Motor

Fuji Bank

Du Pont (E I)

Bank Tokyo-Mitsubish

Sears Roebuck

Schlumberger

Eastman Kodak

Sanwa Bank

Mobil

Matsushita Elect

Source: GMO/ DataStreamMarch 2003

6

GM

O Q

uant

itat

ive

Res

earc

h

0

50

100

150

200

250

300

350

400

450

Dec-97

Jun-98Dec-98

Jun-99Dec-9

9Jun-00

Dec-00

Jun-01Dec-01

Jun-02

Terra LycosEricsson

KPNFrance Telecom

0

50

100

150

200

250

300

350

400

450

Dec-97

Jun-98Dec-98

Jun-99Dec-9

9Jun-00

Dec-00

Jun-01Dec-01

Jun-02

Terra LycosEricsson

KPNFrance Telecom

February 2000 Source: GMO Woolley

European examples

Source: DataStream

GM

O Q

uant

itat

ive

Res

earc

h

0

100

200

300

400

500

600

700

Dec-97

Jun-98Dec-98

Jun-99Dec-9

9Jun-00

Dec-00

Jun-01Dec-01

Jun-02

SoftbankYahoo Japan

Hikari Tsushin

0

100

200

300

400

500

600

700

Dec-97

Jun-98Dec-98

Jun-99Dec-9

9Jun-00

Dec-00

Jun-01Dec-01

Jun-02

SoftbankYahoo Japan

Hikari Tsushin

February 2000 Source: GMO Woolley

Japanese examples

Source: DataStream

The effect on style returns

7

GM

O Q

uant

itat

ive

Res

earc

h

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%US

-10%-8%-6%-4%-2%0%2%4%6%8% UK

-8%

-6%

-4%

-2%

0%

2%

4%

6%Europe

-15%

-10%

-5%

0%

5%

10%Japan

Q4 99 was one of the most extreme quarters for value ever

Source: GMO / DataStream

GM

O Q

uant

itat

ive

Res

earc

h

Global long term performance of value

MSCI World Value relative to MSCI World

90

100

110

120

130

140

150

160

Dec-74Dec-76 Dec-7

8Dec-80

Dec-82

Dec-84Dec-86

Dec-88

Dec-90Dec-92 Dec-9

4Dec-96

Dec-98

Dec-00Dec-02

Source: DataStream

GM

O Q

uant

itat

ive

Res

earc

h

Effect of TMT on UK Value vs GrowthImpact of Individual Stocks

TMT stocksdominate the list of

best performers

Source: GMO / DataStream

8

GM

O Q

uant

itat

ive

Res

earc

h

Effect of TMT on UK Value vs GrowthImpact of Individual Stocks

The majority of TMTstocks have nowunderperformed

Source: GMO / DataStream

Volatility hell!

GM

O Q

uant

itat

ive

Res

earc

h

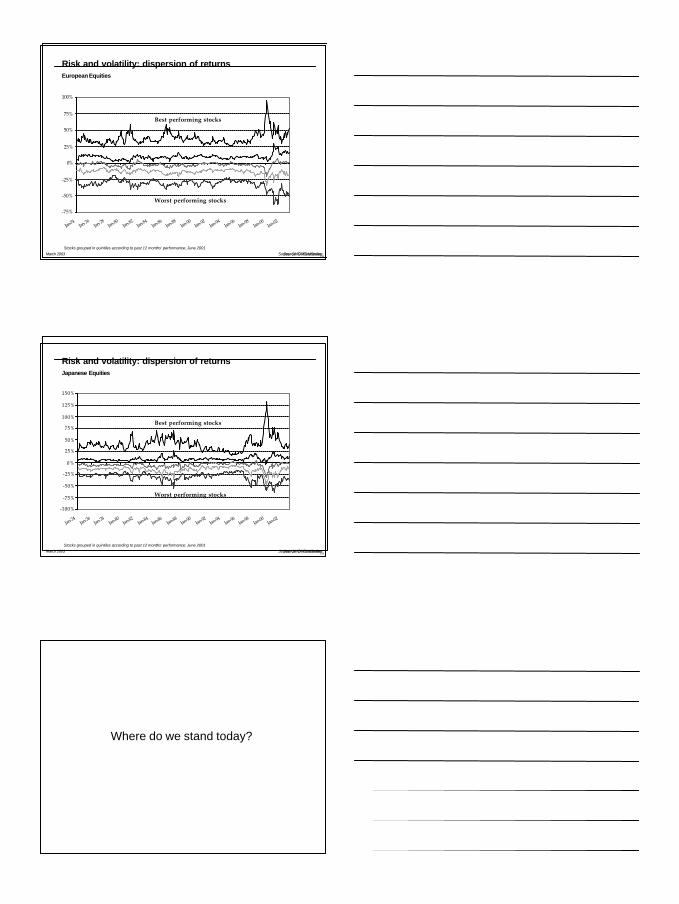

Market volatility90 day standard deviation

0%

1%

2%

3%

4%

Dec-69

Dec-71

Dec-73

Dec-75

Dec-77

Dec-79

Dec-81

Dec-83

Dec-85

Dec-87

Dec-89

Dec-91

Dec-93

Dec-95

Dec-97

Dec-99

Dec-01

FTSE-ALL SHARE S&P 500 DAXCAC-40 Nasdaq NikeiiNikkei

Source: GMO / DataStreamOctober 2002

9

GM

O Q

uant

itat

ive

Res

earc

h

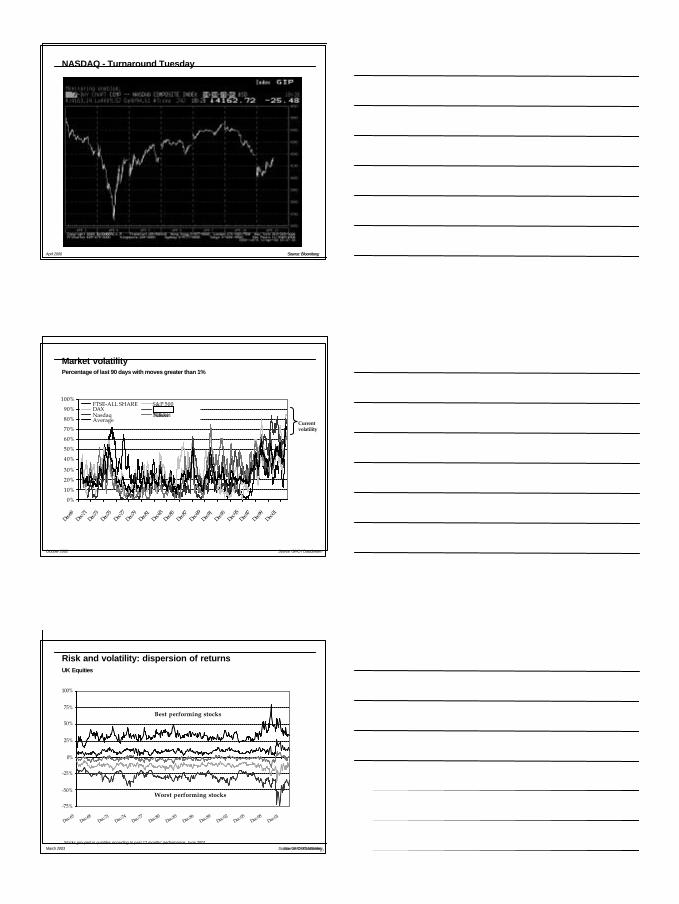

NASDAQ - Turnaround Tuesday

-13%

-5.8%

+14%

Source: BloombergApril 2000 Source: Bloomberg

GM

O Q

uant

itat

ive

Res

earc

h

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Dec-69

Dec-71

Dec-73

Dec-75

Dec-77

Dec-79

Dec-81

Dec-83

Dec-85

Dec-87

Dec-89

Dec-91

Dec-93

Dec-95

Dec-97

Dec-99

Dec-01

FTSE-ALL SHARE S&P 500DAX CAC-40Nasdaq NikeiiAverage

Nikkei

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Dec-69

Dec-71

Dec-73

Dec-75

Dec-77

Dec-79

Dec-81

Dec-83

Dec-85

Dec-87

Dec-89

Dec-91

Dec-93

Dec-95

Dec-97

Dec-99

Dec-01

FTSE-ALL SHARE S&P 500DAX CAC-40Nasdaq NikeiiAverage

Nikkei

Market volatilityPercentage of last 90 days with moves greater than 1%

Currentvolatility

October 2002 Source: GMO / DataStream

GM

O Q

uant

itat

ive

Res

earc

h

-75%

-50%

-25%

0%

25%

50%

75%

100%

Dec-65

Dec-68

Dec-71

Dec-74

Dec-77

Dec-80

Dec-83

Dec-86

Dec-89

Dec-92

Dec-95

Dec-98

Dec-01

-75%

-50%

-25%

0%

25%

50%

75%

100%

Dec-65

Dec-68

Dec-71

Dec-74

Dec-77

Dec-80

Dec-83

Dec-86

Dec-89

Dec-92

Dec-95

Dec-98

Dec-01

-75%

-50%

-25%

0%

25%

50%

75%

100%

Dec-65

Dec-68

Dec-71

Dec-74

Dec-77

Dec-80

Dec-83

Dec-86

Dec-89

Dec-92

Dec-95

Dec-98

Dec-01

-75%

-50%

-25%

0%

25%

50%

75%

100%

Dec-65

Dec-68

Dec-71

Dec-74

Dec-77

Dec-80

Dec-83

Dec-86

Dec-89

Dec-92

Dec-95

Dec-98

Dec-01

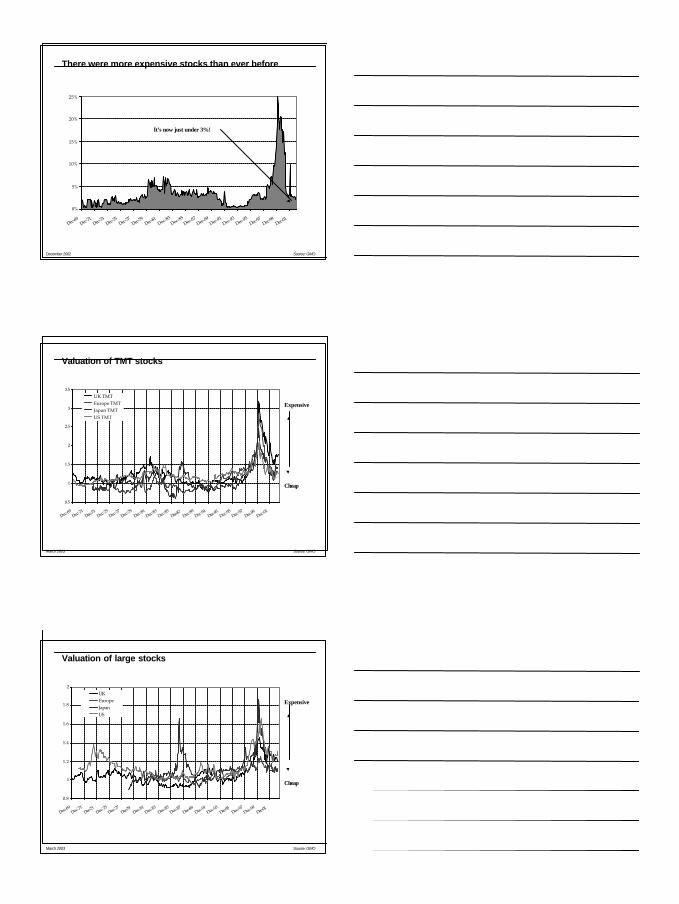

Source: GMO WoolleyStocks grouped in quintiles according to past 12 months’ performance; June 2001

27

Risk and volatility: dispersion of returnsUK Equities

Best performing stocks

Worst performing stocks

Source: GMO / DataStreamMarch 2003

10

GM

O Q

uant

itat

ive

Res

earc

h

-75%

-50%

-25%

0%

25%

50%

75%

100%

Jan-74 Jan-76Jan-78

Jan-80Jan-82

Jan-84Jan-86

Jan-88Jan-90

Jan-92Jan-94

Jan-96Jan-98

Jan-00Jan-02

-75%

-50%

-25%

0%

25%

50%

75%

100%

Jan-74 Jan-76Jan-78

Jan-80Jan-82

Jan-84Jan-86

Jan-88Jan-90

Jan-92Jan-94

Jan-96Jan-98

Jan-00Jan-02

Source: GMO WoolleyStocks grouped in quintiles according to past 12 months’ performance; June 2001

28

Risk and volatility: dispersion of returnsEuropean Equities

Best performing stocks

Worst performing stocks

Source: GMO / DataStreamMarch 2003

GM

O Q

uant

itat

ive

Res

earc

h

-100%

-75%

-50%

-25%

0 %

25%

50%

75%

100%

125%

150%

Jan-74Jan-76

Jan-78Jan-80

Jan-82Jan-84

Jan-86Jan-88

Jan-90Jan-92

Jan-94Jan-96

Jan-98Jan-00

Jan-02

-100%

-75%

-50%

-25%

0 %

25%

50%

75%

100%

125%

150%

Jan-74Jan-76

Jan-78Jan-80

Jan-82Jan-84

Jan-86Jan-88

Jan-90Jan-92

Jan-94Jan-96

Jan-98Jan-00

Jan-02

Source: GMO WoolleyStocks grouped in quintiles according to past 12 months’ performance; June 2001

29

Risk and volatility: dispersion of returnsJapanese Equities

Best performing stocks

Worst performing stocks

Source: GMO / DataStreamMarch 2003

Where do we stand today?

11

GM

O Q

uant

itat

ive

Res

earc

h

0%

5%

10%

15%

20%

25%

Dec-69

Dec-71

Dec-73

Dec-75

Dec-77

Dec-79

Dec-81

Dec-83Dec-85

Dec-87Dec-89

Dec-91Dec-93

Dec-95Dec-9

7Dec-9

9Dec-0

1

At the peak 25% of UK stocks weremore than 3 times overvalued

0%

5%

10%

15%

20%

25%

Dec-69

Dec-71

Dec-73

Dec-75

Dec-77

Dec-79

Dec-81

Dec-83Dec-85

Dec-87Dec-89

Dec-91Dec-93

Dec-95Dec-9

7Dec-9

9Dec-0

1

There were more expensive stocks than ever before

It’s now just under 3%!

Source: GMODecember 2002

GM

O Q

uant

itat

ive

Res

earc

h

0.5

1

1.5

2

2.5

3

3.5

Dec-69

Dec-71

Dec-73

Dec-75

Dec-77

Dec-79

Dec-81

Dec-83

Dec-85

Dec-87 Dec-89

Dec-91

Dec-93

Dec-95

Dec-97

Dec-99

Dec-01

UK TMTEurope TMTJapan TMTUS TMT

0.5

1

1.5

2

2.5

3

3.5

Dec-69

Dec-71

Dec-73

Dec-75

Dec-77

Dec-79

Dec-81

Dec-83

Dec-85

Dec-87 Dec-89

Dec-91

Dec-93

Dec-95

Dec-97

Dec-99

Dec-01

UK TMTEurope TMTJapan TMTUS TMT

Expensive

Cheap

Valuation of TMT stocks

March 2003 Source: GMO

GM

O Q

uant

itat

ive

Res

earc

h

0.8

1

1.2

1.4

1.6

1.8

2

Dec-69

Dec-71

Dec-73 Dec-75

Dec-77

Dec-79 Dec-81

Dec-83

Dec-85

Dec-87

Dec-89

Dec-91

Dec-93

Dec-95 Dec-97

Dec-99

Dec-01

UKEuropeJapanUS

0.8

1

1.2

1.4

1.6

1.8

2

Dec-69

Dec-71

Dec-73 Dec-75

Dec-77

Dec-79 Dec-81

Dec-83

Dec-85

Dec-87

Dec-89

Dec-91

Dec-93

Dec-95 Dec-97

Dec-99

Dec-01

UKEuropeJapanUS

Expensive

Cheap

Valuation of large stocks

March 2003 Source: GMO

12

GM

O Q

uant

itat

ive

Res

earc

h

abcd

2003 Pensions Convention

TMT 1999 – 2001A Bubble Movie

Simon Harris, GMO

Recommended