8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 1/42

Analysis of Indian Logistics Sector

Manoj Bharadwaj. B Fortress Financial Services Ltd. Mumbai

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 2/42

Overview of the Logistics Sector

Flow of the PresentationStructure of the Logistics Sector

Major Demand and Growth Drivers of Indian Logistics

Comparison of Indian Logistics Sector with different countries

3PL and 4PL

SWOT Analysis

Challenges and Opportunities

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 3/42

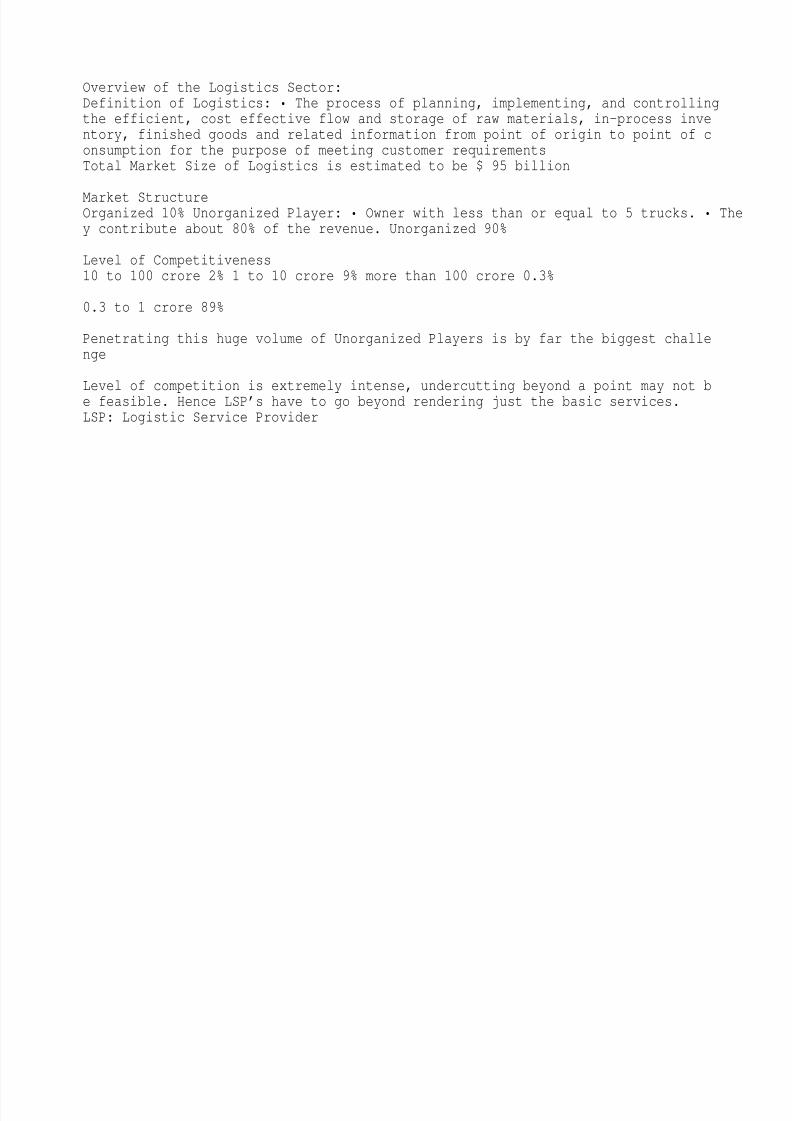

Overview of the Logistics Sector:Definition of Logistics: • The process of planning, implementing, and controllingthe efficient, cost effective flow and storage of raw materials, in-process inventory, finished goods and related information from point of origin to point of consumption for the purpose of meeting customer requirementsTotal Market Size of Logistics is estimated to be $ 95 billion

Market StructureOrganized 10% Unorganized Player: • Owner with less than or equal to 5 trucks. • They contribute about 80% of the revenue. Unorganized 90%

Level of Competitiveness10 to 100 crore 2% 1 to 10 crore 9% more than 100 crore 0.3%

0.3 to 1 crore 89%

Penetrating this huge volume of Unorganized Players is by far the biggest challenge

Level of competition is extremely intense, undercutting beyond a point may not be feasible. Hence LSP’s have to go beyond rendering just the basic services.LSP: Logistic Service Provider

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 4/42

Share amongst different segments of Logistics sector:Cargo Share amongst different SegmentsCivil Aviation (Negligible)

Share in Revenue Generation amongst different SegmentsCivil Aviation 1% Railways 13% Warehousin g 37% Roadways 47%

Segments Railways Roadways Ports Warehousing Civil Aviation

Annual Turnover in 2008-09 (INR billion) 534 2086 91 1,500 43

Railways 24% Roads 55% Major Ports 15%

Minor Ports 6%

Ports 2%

Where do we stand Globally .. Nearly 70% of domestic freight is carried by the Road segment and the remaining by Rail segment while the contribution of the rema

ining two segments is comparatively negligible. International freight is completely dominated by Sea Port Segment. •Indian Railways is 2nd largest in the world just marginally behind China •Indian Roadways is also the 2nd largest behind U.S which has 6.4 million km of network. •India has the largest merchant shipping fleet among the developing countries and is ranked 17th globally. •Constitutes just 3% ofglobal air cargo.

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 5/42

Structure of Logistics SectorProjected Barriers to Growth Rate entry Dominance of Players 20-25% 20-25% Low High Unorganized Organized Capex Requirement Low High

Logistics Segment Courier XPS

Growth Drivers Domestic growth FMCG, Retail, Auto & Auto Ancillaries Agriculture

commodities, Manufacturing activity Agriculture commodities, Manufacturing activity EXIM and domestic trade

Nature of Competition Local National

Warehousing Trucking Container Inland Container Depots / Container Freight Stations

40% 12% 15-20%

Medium Low Medium

Unorganized Unorganized Organized Organized / Unorganized

High Low High

Regional to National Local National

EXIM

15-20%

Low

High

Local

Characteristics of Logistics Sector High costs of operations Low margins Shortage of talent Infrastructural bottlenecks Demand from clients for investing in technology and providing one-stop solutions to all their needs. Consolidation through acquisitions, mergers and alliances.

Value Driver: Competitive Pricing Safety Customer Satisfaction Wide Geographic Reach Operational Efficiency Time Factor Value added services

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 6/42

Major Cost ElementsCustomer Shopping 6% Losses 14% Transportation 35%

Packaging 11%

Loses of 14% translates into roughly INR 290 billion for various industries primarily due to the Unorganized section

Inventory Handling and Warehousing 34%

Certainly a huge opportunity for Organized players to cash in by providing the requisite safety and the insurance coverage for the truck load of goods.

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 7/42

Major Demand and Growth Drivers of Indian Logistics:

Enhances the market reach of the industry Logistics Growth Driver

Growth Driver

Demand Driver

Government Policies, Plans and Taxation

Agricultural industry

Manufacturing Industry

Infrastructure

Roads Implementation of GST Auto Textiles

Accounts for about 50% of the total logistics market

Railways Cement Food & Beverages Ports Steel FMCG Civil Aviation Warehouses

Favorable policies drives the growth of logistics sector

FMCG, Pharma and Food processing apart from agro products have substantial requirement

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 8/42

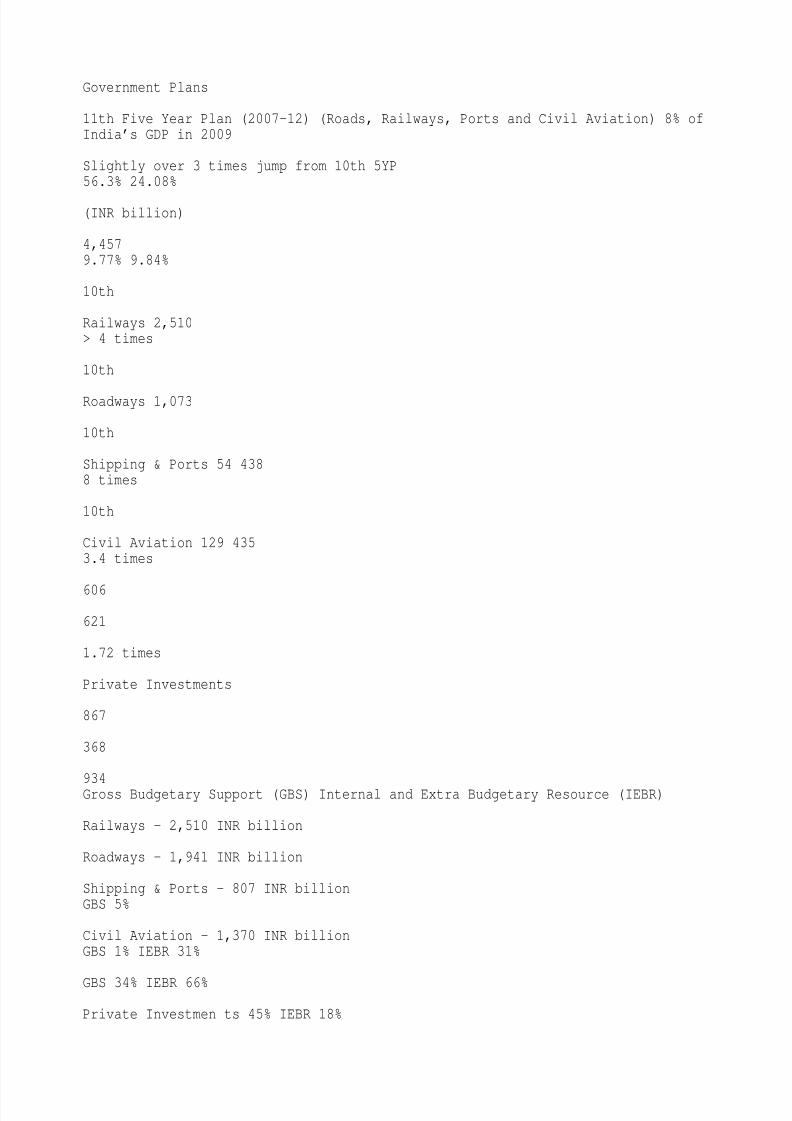

Government Plans

11th Five Year Plan (2007-12) (Roads, Railways, Ports and Civil Aviation) 8% ofIndia’s GDP in 2009

Slightly over 3 times jump from 10th 5YP56.3% 24.08%

(INR billion)

4,4579.77% 9.84%

10th

Railways 2,510> 4 times

10th

Roadways 1,073

10th

Shipping & Ports 54 4388 times

10th

Civil Aviation 129 4353.4 times

606

621

1.72 times

Private Investments

867

368

934Gross Budgetary Support (GBS) Internal and Extra Budgetary Resource (IEBR)

Railways - 2,510 INR billion

Roadways - 1,941 INR billion

Shipping & Ports – 807 INR billionGBS 5%

Civil Aviation - 1,370 INR billionGBS 1% IEBR 31%

GBS 34% IEBR 66%

Private Investmen ts 45% IEBR 18%

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 9/42

GBS 37%

Private Investme nts 46%

IEBR 49%

Private Investments 68%

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 10/42

Government Policies and TaxationRationalization of tax:Goods and Services Tax (GST) – Proposed to be implemented by April 2010.

Impact •Aims to remove multiple taxation by abolishing taxes such as Octroi, Central sales tax, State level sales tax, entry tax, stamp duty, telecom licence fees, turnover tax, tax on consumption or sale of electricity, taxes on transportati

on of goods and services •Hopes to increase the tax base •Aims to remove the disparity in taxation or differential treatment to manufacturing and service sector. •Theintroduction of GST in India would mean that manufactures will now base their logistics decisions on operational efficiency instead of tax optimization. •Will enable manufacturers and 3PLs to set-up and position their warehouses and distribution channels based on the considerations of time, cost and logic. •Manufacturerswill now be encouraged to outsource their logistics and supply chain operations.

Other Tax Reliefs The 100 % deduction allowed in respect of capital expenditurefor the business of setting up and operating cold chain facilities for specifiedproducts, and setting up and operating warehousing facilities for storage of agricultural produce. The enhancement of limit for disallowance of expenditure mad

e in the case of transporters i.e. to raise the limit from Rs 20,000 to Rs 35,000 effective October 1, 2009 and NIL TDS for road transport, would certainly address the stringent practical difficulties, which is step towards moving of this Industry from unorganised to organised structure. Deductions under section 80-IAmeant for infrastructure industry, which has been extended to railways.

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 11/42

InfrastructureRoadways:Type of Road Expressways National Highways (NH) State Highways (SH) Major District Roads (MDR) Rural and Other Roads Total Length(as of 2009)

Length (in km) 200 70,548 1,31,699 4,67,763 26,50,000 33,20,210

Percentage --2.12%

Post-Liberalization Average Growth of NH during each 5 YP is 24.08%

A few Vital Stats .. •70% of freight taken by roads •NH carries about 40% of road traffic •Avg. truck speed in NH – 20 to 30 km / hr

3.96% 14.08% 79.81% Number of kilometers added postliberalization 39,901 km. •SH and MDR carries 40% of road traffic •Traffic on roads is growing by 7% - 10% •Vehiclepopulation 12% growthSale of Commercial Vehicles (in lakhs)

Road Freight Valuation (INR billion)2500 2086 2000 1500 1000 610 500 0 1995 2000 2005 2009 (Source till 2005: KPMG)840 1430

Post liberalization growth 9.1% and growth from 2000 is 10.6%

6 5 4 3.1 3 2 1.9 2.6 3.5 4.6 4.9 3.8

Growth in Commercial vehicles from 2002-03 is 12.2%

1 0

(Source : SIAM)

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 12/42

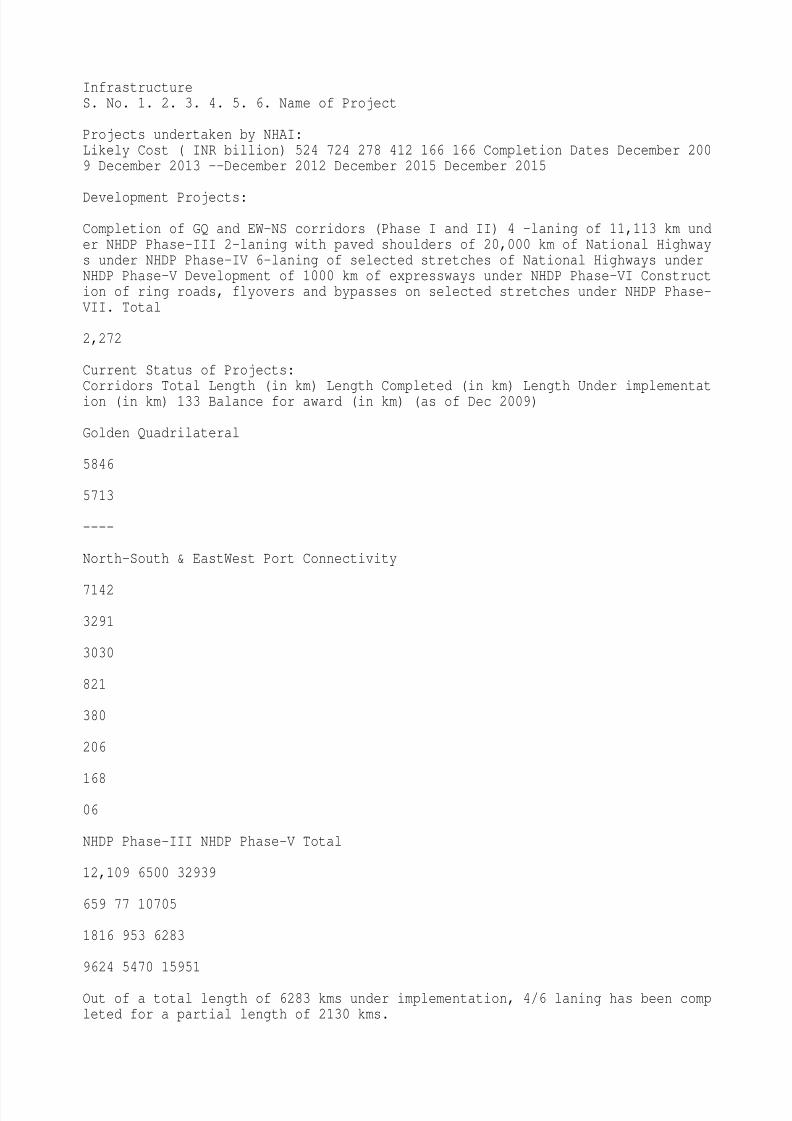

InfrastructureS. No. 1. 2. 3. 4. 5. 6. Name of Project

Projects undertaken by NHAI:Likely Cost ( INR billion) 524 724 278 412 166 166 Completion Dates December 2009 December 2013 --December 2012 December 2015 December 2015

Development Projects:

Completion of GQ and EW-NS corridors (Phase I and II) 4 -laning of 11,113 km under NHDP Phase-III 2-laning with paved shoulders of 20,000 km of National Highways under NHDP Phase-IV 6-laning of selected stretches of National Highways underNHDP Phase-V Development of 1000 km of expressways under NHDP Phase-VI Construction of ring roads, flyovers and bypasses on selected stretches under NHDP Phase-VII. Total

2,272

Current Status of Projects:

Corridors Total Length (in km) Length Completed (in km) Length Under implementation (in km) 133 Balance for award (in km) (as of Dec 2009)

Golden Quadrilateral

5846

5713

----

North-South & EastWest Port Connectivity

7142

3291

3030

821

380

206

168

06

NHDP Phase-III NHDP Phase-V Total

12,109 6500 32939

659 77 10705

1816 953 6283

9624 5470 15951

Out of a total length of 6283 kms under implementation, 4/6 laning has been completed for a partial length of 2130 kms.

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 13/42

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 14/42

InfrastructureDevelopment Projects:Major Industrial Regions

Delhi Mumbai Industrial Corridor Delhi-Mumbai Industrial Corridor is a mega infra-structure project of $90 billion with the financial & technical aids from Japan, covering an overall length of 1483 KMs between the Dadri in Delhi and JNPT in

Mumbai. This Dedicated Freight Corridor envisages a high-speed connectivity forHigh Axle Load Wagons (25 Tonne) of Double Stacked Container Trains supported by high power locomotives. Distribution of length of the corridor indicates thatRajasthan (39%) and Gujarat (38%) together constitute 77% of the total length ofthe alignment of freight corridor, followed by Haryana and Maharashtra 10% eachand Uttar Pradesh and National Capital Region of Delhi 1.5 % of total length each.

National Expressway: Target: 15,766 km. Phasing of expressway: 2012, 2017, 2022Project Cost estimation: >> INR 2.5 trillion Plan for Phase I: 3,530 km (Reportfrom Yahoo News 9th Dec ’09) Estimated Cost for Phase I: Rs. 20,000 crore. Lanes:6 to 8 lanes 11 stretches and 12 states identified

This project incorporates Nine Mega Industrial zones of about 200-250 sq. km., High speed freight line, Three ports, and Six air ports; Six-lane intersection-free expressway connecting Delhi and Mumbai 4000 MW power plant. Several industrial estates and clusters, industrial hubs, with top-ofthe-line infrastructure would be developed along this corridor to attract more foreign investment. Funds forthe projects would come from the Indian government, Japanese loans, and investment by Japanese firms and through Japan depository receipts issued by the Indiancompanies.

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 15/42

Infrastructure Railways:Passenger traffic / day Freight traffic / day Railway coverage Freights wagons Coaches Locomotives(as of 2009)

Railways Cargo Constituents and its shareIron & Steel 3%

18 million 2 million tonnes 63,465 km 2,00,000 50,000 8,000

Fertilizers 5% Foodgrains 6%

Others 14% Coal 43%

POL 5%

Cement 9% Ore to Steel plants 8%

Ore Export 7%

Freight Earnings (INR billion) Cargo (in million metric tonnes)600 500 416 400 308 300 200 100 0 363 473 534

Growth of 14.75%

Growth of 8.9%

900 800 700 600 500 400 300 200 100 0

602

667

726

785

848

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 16/42

InfrastructureDedicated Freight Corridor – Rs. 40,000 crore

Development Projects: States TraversedWestern DFC (in kms) Haryana Rajasthan Gujarat Maharashtra Total 192 553 588 1501483

Western Corridor 1483 km JNPT in Mumbai to Dadri in U.PProjected Traffic (in million tonnes)45 40 35 30 25 20 15 10 5 0 2005-06 Western Corridor 2021-22 Container WC 0.69 6.2 23 40

Logistics Park: Proposed to set up Logistics Parks at 1. 2. 3. 4. 5. 6. Mumbai area, particularly in the vicinity of Kalyan-Ulhasnagar or VashiBelapur in Navi Mumbai. Vapi in southern Gujarat Ahmedabad area in Gujarat, Gandhidham in the Kutch region of Gujarat Jaipur area in Rajasthan, NCR of Delhi.

These parks are proposed to be developed on Public Private Partnership mode by creating a sub-SPV for the same. Cargo Constituents: ISO containers from JNPT and

Mumbai Port in Maharashtra and ports of Pipavav, Mundra and Kandla in Gujarat destined for ICDs located in northern India POL, Fertilizers, Food grains, Salt,Coal, Iron & Steel and Cement.

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 17/42

Infrastructure

Development Projects:

States TraversedEastern DFC (in kms) Punjab Haryana Uttar Pradesh Bihar Total 102 82 1002 93 1279

Eastern Corridor 1279 km Sonnagar in Bihar to Ludhiana in PunjabLogistics Parks: It is also proposed to set up Logistics Park at Kanpur in U.P.and Ludhiana in Punjab. The parks are proposed to be developed on Public PrivatePartnership mode by creating a sub-SPV for the same. Cargo constituents: Coal,finished steel, food grains, cement, fertilizer, limestone and general goods Projected Traffic (in million tonnes)140 120 100 80 60 40 20 0 2005-06 2021-22 38 116

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 18/42

Capacity Enhancement – Spread of FundsOther Measures for Enhancing Capacity 3% Metropolitan Projects 6% New Line Projects 12% Other Railway Electrification 4% Traffic Facility works Logistic Park 3%1% Freight Terminals 2% Grade Separators/Flyovers/Byepass lines 2% Terminals atState Capitals and important tourists places Traffic Facility Works 1% 11% MegaTerminals at Metropolitan cities 2% Running Of 25 Tones Axle Load On Iron Ore Routes 3% Running Of 23/24 Coach Length Trains 1%

Funds for setting up Logistics park Rs. 770 crore

Gauge Conversion 24%

Doubling 25%

Total Funds allocated in 11th five year plan: Rs. 77,050 crore

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 19/42

Infrastructure Ports:No. Traffic Capacity

A few Vital Stats .. *Some 60% of India’s container traffic is handled by the Jawaharlal Nehru Port Trust in Mumbai *It has just 9 berths compared to 40 in the main port of Singapore. *It takes an average of 21 days to clear import cargo in India compared to just 3 in Singapore. *Cargo handling is projected to grow at 7.

7% until 2013-14. *Only 43 of the 187 minor ports can handle cargo *Mundra portalone handles 60% of minor port traffic Traffic Capacity Others 17% Coal 13%

Major Ports Minor Ports

12 187

465.7 MT 170 MT

508.6 MT 228.31 MT(as of 2006-07)

Projections for 2012:

Major ports Minor ports

800 MT 300 MT

1001.8 MT 345.19 MT Ports Cargo Constituents and its ShareContainer 12%

Development Project: Fertilizer Iron Ore and FRM 18% NMDP (National Maritime Development Programme): 4% Objective: • Upgrade and modernize the port infrastructurein India and benchmark its performance against global standards. • Total investment for the programme is Rs. 1, 00,339 crore and out of them about Rs. 34,505 cro

re is expected from the private sector. Allocation Rs. 55,804 crore for port sector. Rs. 44,535 crore for shipping and inland water transport sectors. Target No. of Projects To be completed in phases within 201112. 276 •Other related schemesfor creation of backup facilities. Project Covers •Construction / up gradation ofbirth, •Deepening of channels, •Rail / road connectivity projects, •Equipment up gradation and modernization scheme,

POL & its products 36%

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 20/42

Infrastructure Civil Aviation:No. of Airports Under AAI Major Airports Non Metro Airports Domestic Airports International Airports 449 airports / airstrips 92 airports and 28 Civil enclavesat defence airfields 6 35 87 12(as of 2009) 2 1.8 1.6 1.4 1.2 1 0.8 0.6 0.4 0.2 0

Cargo (in million metric tonnes)

1.8

1.2 0.8 0.6

Major Cargo Constituents •Express Mail •Computers •Chips •Electronic and Optical Equipment •Precision Instruments •Perishable food stuffShare in cargo traffic

2008-09 International

2011-12 (E) Domestic

•12.1% growth rate in Internatinal cargo •10.1% growth rate in domestic cargo

Non Metro Airport s 12%

Major Airport s 88%

AAI: Airport Authority of India

Development Project: MIHAN (Multi-modal International Cargo Hub and Airport at Nagpur.)

The Cargo hub in Nagpur is built to handle nearly 50% of the total air cargo traffic all over India

Cost: INR 25.8 billion >> Spread over an area of 4025 Hectares >> The airport will have parking space for 50 aircraft at any time with 50 additional bays at fringe areas. >> With a projected target of serving 14 million passengers and handle 0.87 million tonnes of cargo this is one of largest aviation project in India.

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 21/42

Infrastructure Warehouses:As per planning commission & industry estimates: • Total existing warehousing capacity is 80 million MT out of which CWC has 10.8 million MT and 21.9.million MT in SWC • There are three agencies in the public sector which are engaged in building large scale storage/warehousing capacity, namely, Food Corporation of India (FCI), Central Warehousing Corporation (CWC) and 17 State Warehousing Corporations(SWCs). Requirement: • Additional warehousing capacity of 35 million MT in next 5

to 10 years at an investment of about INR 6 billion. Current Status: Major investments on these infrastructures have come from Government agencies like CWC, SWC, CONCOR etc. Current private sector initiatives are small and sporadic. Private sector warehousing are of poor quality, small, fragmented and does not meet infrastructure standards. No quality standards or benchmarks are followed in infrastructure creation Developmental Works: • IL&FS is working with Continental Warehousing Corporation Ltd to set up six agri parks across India FTWZ • Primary objective is to create trade related infrastructure, envisaging world-class infrastructure for warehousing of various products • FTWZ addresses these issues effectivelyas they would enable supply chain / logistics to function much more efficientlyby removing the cargo bottlenecks witnessed at the ICDs • In addition, such zonesare envisaged to provide common infrastructure such as storage and handling equi

pments, shared storage space, etc. which would enable the apportionment of associated capital costs across a larger base of users leading to significant costs reduction.Reference: IF&LS

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 22/42

INLAND CONTAINER DEPOTS (ICD) Robust growth of exim trade and capacity constraints in movement and evacuation of cargo has lead to a surging demand for greenfield ICDs and expansion of existing facilities At least 40 to 50 new rail/ road ICDs/ CFS across the country needed to handle the projected traffic in next 5 to 10 years IL&FS is initiating development of ICDs on PPP format with agencies likeCONCOR as well as private enterprises with the objective of filling up this critical infrastructure need To create economies of scale, the business plan of ICD

is being expanded to include SCM functions like warehousing, C&F and other value added services to give the project shape of “Mega Logistics Park”

INTEGRATED TRANSPORT CENTER The unplanned development of transport nagars acrossmajor industrial townships, metros, mini metros etc. This has led to inefficient utilization of space, shabby infrastructures, road jams and danger to human life IL&FS has initiated development of integrated and modern logistics cum transport centers across major locations in the country on PPP format The centers willlead to integrated development of warehousing, transportation and traffic planning leading to a much better logistics operations Development of such integratedestates on in Uttaranchal, Chattisgarh, North East and Jharkahnd, in collaboration with respective State Governments

Reference: IF&LS

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 23/42

Manufacturing Industry16% 14% 12% 10% 8% 6% 4% 2% 0% 15% 3000

Industry Size in 2009 (in INR billion)2500 2000 2412

Cost of Logistics to Total Sales

2200 1480 605 590

6%

1500 5% 4% 3% 3% 1000 500 0 Steel Textiles Auto Cement FMCG F&B 489

Impact on the Logistics Sector Cement Industry: Challenge: •Road transportation beyond 200 kms is not economical therefore about 55% of cement is being moved by the railways. There is also the problem of inadequate availability of wagons especially on western railways and southeastern railways. Opportunity: •Under this scenario, manufacturers are looking for sea routes, this being not only cheap but a

lso reducing the losses in transit. •Today, 70% of the cement movement worldwide is by sea compared to 1% in India.

Share of Logistics (in INR billion)160 140 120 100 80 60 40 20 0 Steel Textiles Auto Cement FMCG F&B 66 44 24 24 91145

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 24/42

Comparison amongst different countriesDeveloped Infrastructure Bottlenecks

Country China US, UK Europe Japan India (45% of GDP) Country

Logistics Cost / GDP 13% to 15% 9% 10% 11.4% 13% to 14% Logistics activities performed by 3PL / Logistics activities <10% 57% 30% to 40% 80%

China, IndiaEmerging Low High

US, UK Europe Japan

Estimated Size of 3PL and 4PL in 20 YearsCurrent GDP (in INR trillion) GDP in 2029 with a growth rate of 7% (in INR trillion) Share of Logistics (11% of 45% of GDP) (in INR trillion) Share of 3PL and 4PL with a 30% market Share (in INR trillion) Share of 3PL and 4PL with 40% market share (in INR trillion)

That’s about 40 times jump in market size in a span of 20 years from the current market size of INR 78 billion

55

212.83

10.53

3.16

4.21

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 25/42

Definition of 3PL:• • A 3PL provider is a company which supplies /co-ordinates logistics functions across multiple links in the supply chain. The company acts as a ‘third party’ facilitator between seller/manufacturer (the ‘first party’) and buyer/user (the ‘second party’).”

Supply Chain Model3PL 3PL

Manufacturing Unit

Design

Market Customers / End Users

Supplier’s Supplier

Suppliers

Acquire

Convert

Distribute

Distributers

Mngmt

Control

3PL

3PL

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 26/42

Why 3PL ?For Operation Efficiency Operational cost reduction Reduced cycle time More specialized logistics expertise Improve on time delivery Enhance geographic reach Flexibility in operations For Business Growth Improve focus on core activities Improve return on assets Diverting capital investment Access/ Expansion to unfamiliar market Higher Profitability Increased Sales and Market Share Enhanced Customer Service

Why not?• Inability to respond to changing needs • Lack of grasp of business goals • Unreliable promises from providers • Concerns about capability of providers • Fear of leakageof important information • Non compatibility of IT systems • Difficulty to manage and change provider • Fear of loss of control • Lack of confidence in provider • Poor infrastructure of providers company

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 27/42

4PL: It acts as single interface between the client and multiple logistics service providers. All aspects of the client’s supply chain are managed by the 4PL organisation. The 4PL organization is often separate entity established as a joint venture or long term contract between a primarily client and one or more partners. It is also possible for a major 3PL provider to form a 4PL organisation withinexisting structure.

Key Characteristics: Client 3PL Hybrid organisation formed from a number of different entities Typically established as a JV or long term contract 3PL 4PL Responsible for management and operation of entire supply chain Continuous flow of information between partners and 4PL organisation

3PL

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 28/42

SWOT Analysis of Logistics Sector:WEAKNESS STRENGTHS Extremely critical for manufacturing High cost – low margin business industry and agri commodity industry Large number of unorganized players No dearth in volumes Low IT penetration Critical component in operational efficiency Highly fragmented Contributes heavily towards customer High Capital expenditure satisfaction OPPORTUNITIES • Implementation of GST from 1st April 2011 • Implementation of Golden quadrilateral and NS-EW corridors. • Heavy investments to improv

e infrastructure through developmental projects like Mihan, delhi-mumbai industrial corridor, Dedicated freight corridor and National Maritime Development Projects.

THREATS Increase in fuel costs Government Policy Taxation

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 29/42

Challenges:Unfair Competition Unorganized players get away without paying taxes Don’t followthe operating norms stipulated in the motor vehicle act such as quality of drivers, vehicles, volume and weight restriction. Diseconomies of scale Differentialsales tax structure in different states Apart from non-uniform tax structure, LSP’s (Logistics Service Provider) have to pay other kinds of taxes like octrois. Governments failure in implementation of VAT since 1st of April 2005 Face multiple

check post This delays the process of delivery Compliance with varying documentation requirement of different states is certainly a difficulty. Low IT penetration Lack of communication infrastructure Lack of visibility Lack of real time tracking ability This leads to a lot of uncertainty and lack of transparency in terms of cost structure and service delivery Highly Fragmented Sector LSP’s stick totheir basic services. They don’t provide value added services like packaging / labeling, order processing, distribution, customer support etc. Solution / Opportunity: Integration of IT into the process like EDI could greatly speed up the whole process and bring in the required efficiency. Solution / Opportunity: Impliesthat a truckload loss of Goods is always round the corner. Organized players can cash in by providing the requisite level of safety and insurance cover for goods. Solution / Opportunity: Proposal for implementation of GST. With uniform tax

ation across all states companies could focus on supply chain efficiency ratherthan Tax avoidance optimization.

Solution / Opportunity: Penetration of 3PL players and high level of investmentsinto technology like GPRS would change the scenario.

Solution / Opportunity: Value Added Services provides a great opportunity to increase the margins.

Bribery and Police harassment $5 billion paid by truckers annually

Solution / Opportunity: The scenario could grossly change with greater penetration of Organized players.

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 30/42

Some of the major logistics companies ..Listed Shipping Companies - Large Essar Shipping GE Shipping Co Adani Agri Log.Great Offshore Agarwal Indl. Mercator Lines Agrocargo Trans. SCI Allcargo GlobalVarun Ship. Co. Alltrans Logistc Listed Shipping Companies – Medium & Small Chowgule Steam Garware Offshore SEAMEC Ltd Shreyas Shipping SKS Logistics Blue Dart Exp. Chokhani Global Elbee Services Gati Killick Air Cour Skypak Serv. Sp. ElbeeExpress Alltrans Port Arshiya Intl. Arvind Roadlines Assam Beng.Carr Containerwa

y Int Wilson Sandhu Vins Overseas Chart.Logistics Coastal Roadways Inland VikashInter State Oil Kausar India Southern Roadwys Sri Venkatesa Tr T N St Trans CoiT N St Trans Kum Transport Corp. Central Province Frontline Corp. SER Inds. Bulk Cem.Corpn. E I T A India Roadways India Broekman Logisti DLF Retail Reliance Logis. Balurghat Tech Premier Road Car

Road Transport CompaniesABC India

Associated Road Autoriders Intl.

CRC Carrier Delhi Assam Rdwy

Patel Integrated Peirce Leslie(I)

Courier

Corporate Courier Orbit Multimedia

Container Corpn. mundra port Delhi Metro Rail gateway dis

Konkan Rly.Corpn

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 31/42

Source and References

MERCI BEAUCOUP ..

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 32/42

National ExpresswayMumbai-Pune Expressway Taj Expressway Delhi-Noida Direct Flyway Chennai-Bangalore Expressway Jaipur-Kishangarh Expressway Durgapur Expressway Belghoria Expressway Panipat Elevated Expressway Shimla-Chandigarh Expressway Ganga Expressway Kundli-Manesar-Palwal Expressway(KMP) Eastern Peripheral Expressway Pathankot-Jalandhar-Ajmer Expressway Bangalore-Mysore Expressway Hosur Road Expressway PV Narsimha Rao Expressway to HIAL PSU: Passenger Carrying Units Chennai Elevated Expres

sway Mumbai eastern Freeway that starts from CST

Cost estimation for a 100 km 4 lane expressway - Rs. 1784 Cost estimation for a100 km 6 lane expressway - Rs. 2548 Funding options including PPP mode, cost sharing by states/ Centre, Commercial utilization of land within/beyond ROW etc. Atpresent expressway handles about 30,000 PCUs and is designed to handle up to 10,00,000 PCUs.

The Uttar Pradesh government is planning five more expressways in the state.• Greater Noida-Saharanpur-Dehradun expressway (in partnership with the Uttarakhand state government)

• Jhansi-Lucknow expressway • Lucknow-Gorakhpur expressway • Agra-Kanpur-Lucknow expressway • Farrukhabad-Kotdwar expressway.

The five proposed expressways will have a combined length of around 1,400km.

Back

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 33/42

National Highways

Sr.No. 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21

Name of the State /Union Territory Length (Kms) Andhra Pradesh Arunachal PradeshAssam Bihar Chandigarh Chhatisgarh Delhi Goa Gujarat Haryana Himachal Pradesh Jammu & Kashmir Jharkhand Karnataka Kerala Uttarakhand Madhya Pradesh Maharashtra

Manipur Meghalaya Mizoram 4,537 1992 2836 3642 24 2184 72 269 3245 1512 1409 1245 1805 4396 1457 2042 4670 4176 959 810 927 22 23 24 25 26 27 28 29 30 31 32 33Nagaland Orissa Pondicherry Punjab Rajasthan Sikkim Tamil Nadu Tripura Uttar Pradesh Uttaranchal West Bengal Andaman & Nicobar Total 494 3704 53 1557 5585 62 4832 400 5874 1991 2524 300 70,548

Back

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 34/42

Cargo handled by the Major Ports in tonnes of

000PORT 2003-04 2004-05 2005-06 2006-07 2007-08 % Growth Annualised growth 12.13%

KOLKATA

8,693

9,945

10,806

12,596

13,741

58.07

HALDIA

32,567

36,262

42,337

42,454

43,541

33.70

7.53%

PARADIP

25,311

30,104

33,109

38,517

42,438

67.67

13.79%

VIZAG

47,736

50,147

55,801

56,385

64,597

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 35/42

35.32

7.86%

ENNORE

9,277

9,480

9,168

10,714

11,563

24.64

5.66%

CHEENAI

36,710

43,806

47,248

53,414

57,154

55.69

11.70%

TUTICORIN

13,678

15,811

17,139

18,001

21,480

57.04

11.94%

COCHIN

13,572

14,095

13,887

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 36/42

15,257

15,810

16.49

3.89%

NMPT

26,673

33,891

34,451

32,042

36,019

35.04

7.80%

MORMUGAO 27,874

30,659

31,688

34,241

35,128

26.02

5.95%

MUMBAI

29,995

35,187

44,190

52,364

57,039

90.16

17.43%

JNPT

31,190

32,808

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 37/42

37,836

44,815

55,756

57.60

15.63%

KANDLA

41,523

41,551

45,907

52,982

64,893

56.28

11.81%

TOTAL

3,44,799

3,83,746

4,23,567

4,63,782

5,19,159

50.58

10.77%

Back

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 38/42

GDP and industry contribution

Sector Agriculture Service Industrial

Employment 60.00% 28.00% 12.00%

Interms of contribution 27.00% 55.00% 18.00%

Back

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 39/42

EXIM* Gold,

Major Items of imports:

* Cashew Nuts Major items of exports: Major Exports Industries Petroleum products * manufactures of Metals Textile goods * Machinery and Instruments Gems and je

wellary * Man made Yarn, Fabrics Made ups Engineering goods * Transport equipment Chemicals * Primary and Semi finished iron and steel Leather * RMG cotton including accessories * Plastic and linoleum products * Inorganic/organic/agro chemicals. * Organic chemicals, * Machinery except elect. & electronic, * Fertilizercrude, * Electronic goods, * Pearls precious semiprecious stones. * Non ferrousmetals, * Pulp and waste paper, * Coal, coke & Briquettes etc. * Cotton raw. Comb/uncombed/waste, * Iron & Steel, * Cotton yarn, fabrics made ups etc. * drugs,pharmaceuticals and fine chemicals * Inorganic Chemicals, * Wood & Wood Products, * Metalifers ors & Metal Scrap,

Back

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 40/42

Catering to Agricultural Industry

Major agricultural products include •Rice •Wheat •Oilseed •Cotton •Tea •Potatoes •Jute sugne

Poultry and diary products •Cattle •Water buffalo •Sheep •Goats •Poultry •Fish

Back

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 41/42

Major Industries Textiles Chemicals Food processing Steel Transportation equipment Cement Mining Petroleum Machinery Software

Industrial Regions • Mumbai-Pune Region, • Hugli Region, Major Industrial belts • Bangalore-Tamil Nadu Region, .. Ambala-Amritsar • Gujarat Region, • ChhotaNagpur Region,• Vishakhapatnam-Guntur Region, • Gurgaon-Delhi-Meerut Region, • Kollam-Thiruvantapuram Region. .. Saharanpur-Muzzaffarnagar .. Indorer-Dewas-Ujjaini .. Jaipur-Ajmer

.. Kolhapur-South Kannada .. Northern-Malabar .. Middle Malabar .. Adilabad-Nizambad .. Allahabad-Varanasi-Mirzapur .. Bhojpur-Mungar .. Durg-Raipur .. Bilaspur-Korba .. Brahmaputra valley

Back

8/6/2019 28073759 Analysis of Indian Logistics Sector

http://slidepdf.com/reader/full/28073759-analysis-of-indian-logistics-sector 42/42

Recommended

![Indian Manufacturing & Logistics: On a Roller Coaster Ride! · PDF filethe-promise-of-indias-manufacturing-sector]. ... INDIAN MANUFACTURING & LOGISTICS: ON A ROLLER COASTER RIDE!](https://img.pdfslide.us/doc/110x75/5a81bf0b7f8b9aee018d8161/indian-manufacturing-logistics-on-a-roller-coaster-ride-indian-manufacturing.jpg)