www.CharlestonCommercialMarketForecast.com

September 30, 2015

www.CharlestonCommercialMarketForecast.com

Keep Up Digitally

Event Hashtag

#CMF15

CharlestonCommercialMarketForecast.com

www.CharlestonCommercialMarketForecast.com

Thank You to Our Planning Committee

Blair Belk, Belk | Lucy

Thomas Boulware, NAI Avant

Benjie Lanier, Wells Fargo SBA

Thomas Mathewes, Roadstead Real Estate

Doug Roland, NAI Avant

Gerry Schauer, Avison Young

Bryan Stange, ECS Carolinas

Vitre Stephens, Avison Young

Clayton Taylor, Taylor Consulting

Ryan Welch, Lee & Associates-Charleston

www.CharlestonCommercialMarketForecast.com

Tri-City Bronze Sponsors

www.CharlestonCommercialMarketForecast.com

Tri-City Silver Sponsors

www.CharlestonCommercialMarketForecast.com

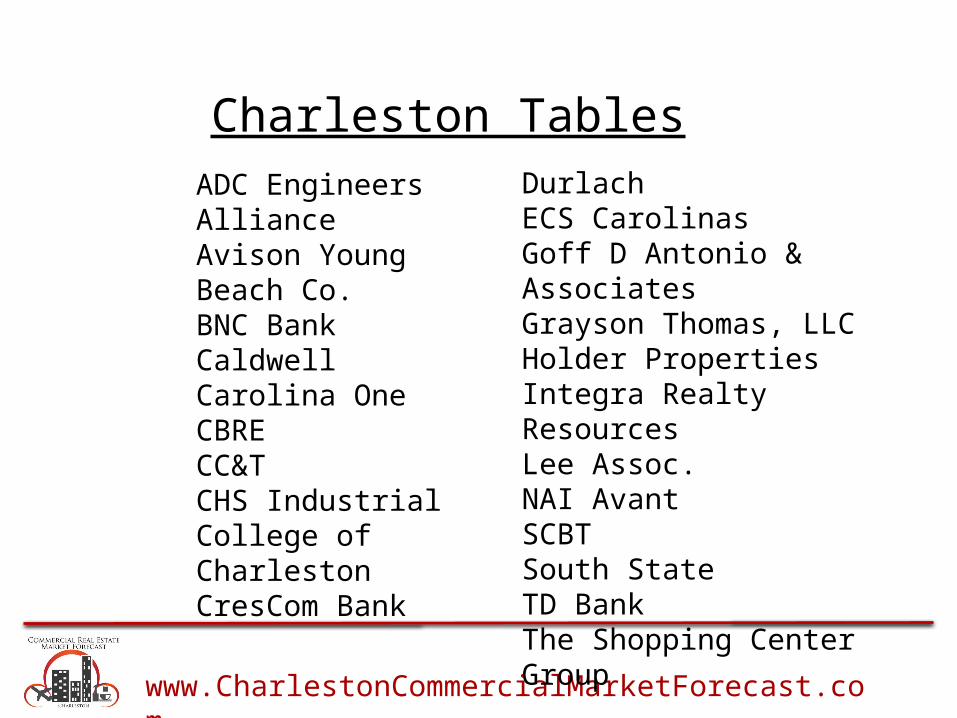

Charleston Tables

ADC EngineersAllianceAvison YoungBeach Co.BNC BankCaldwellCarolina OneCBRECC&TCHS IndustrialCollege of CharlestonCresCom Bank

DurlachECS CarolinasGoff D Antonio & AssociatesGrayson Thomas, LLCHolder PropertiesIntegra Realty ResourcesLee Assoc.NAI AvantSCBTSouth StateTD BankThe Shopping Center Group

www.CharlestonCommercialMarketForecast.com

Stage Sponsor

www.CharlestonCommercialMarketForecast.com

Charleston Bronze Sponsors

www.CharlestonCommercialMarketForecast.com

Charleston Silver Sponsors

www.CharlestonCommercialMarketForecast.com

Charleston Gold Sponsor

www.CharlestonCommercialMarketForecast.com

Jim HillVice President,

Commercial and Industrial Development & Land SalesWestRock Community Development and Land Management Division

www.CharlestonCommercialMarketForecast.com

September 30, 2015

www.CharlestonCommercialMarketForecast.com

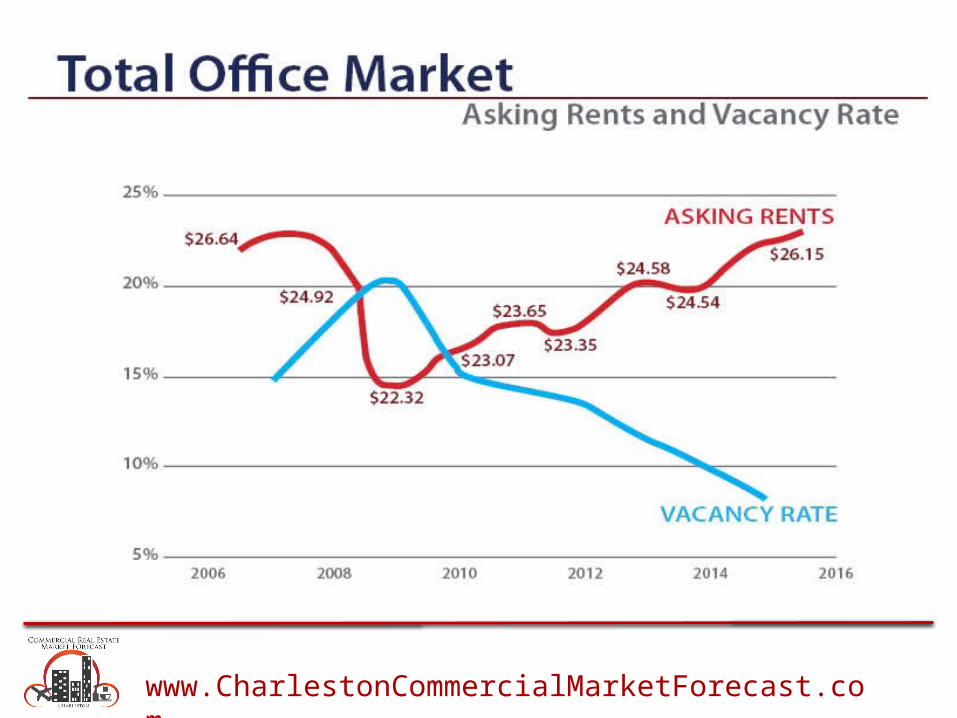

RETAIL REPORT

Retail Analysis and Outlook 2015

Presented by: Jeff Yurfest, CCIM

www.CharlestonCommercialMarketForecast.com

www.CharlestonCommercialMarketForecast.com

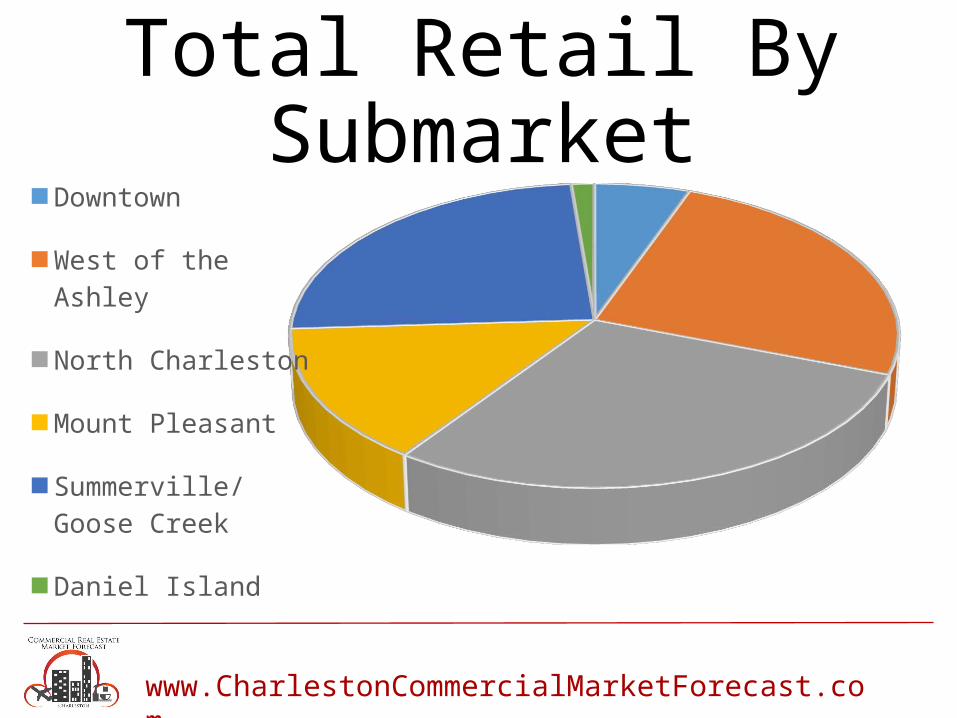

Total Retail By Submarket

Downtown

West of the Ashley

North Charleston

Mount Pleasant

Summerville/Goose Creek

Daniel Island

www.CharlestonCommercialMarketForecast.com

www.CharlestonCommercialMarketForecast.com

Charleston Retail Vacancy Rate

20112012

20132014

2015

0%1%2%3%4%5%6%7%8%9%

8.25% 8.50%

6.50%6.25%

5.10%

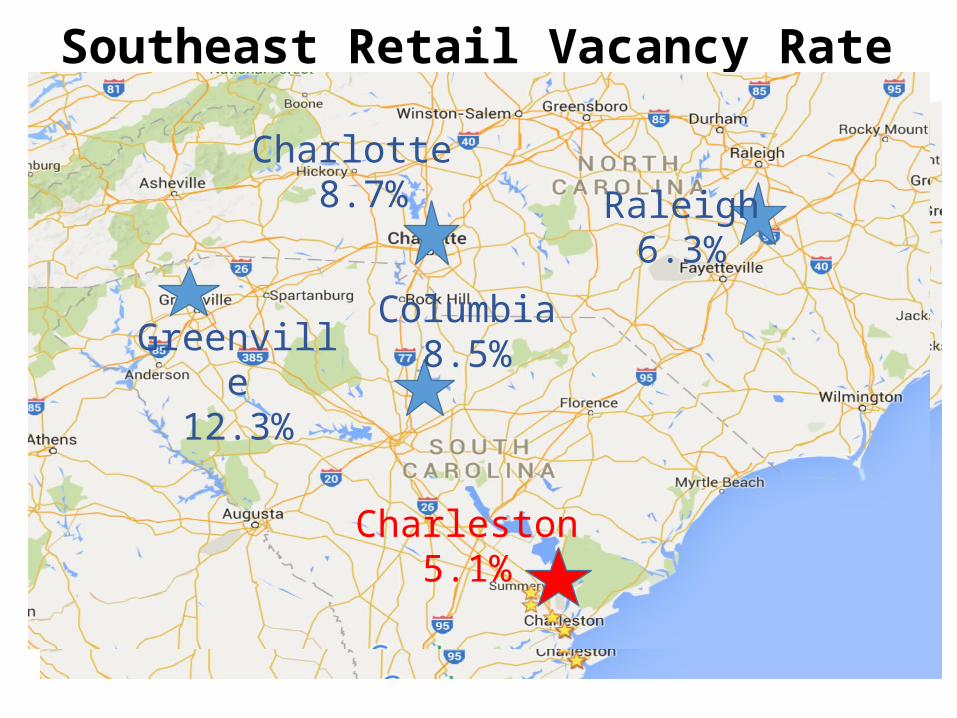

Southeast Retail Vacancy Rate

Greenville12.3%

Columbia8.5%

Charleston5.1%

Raleigh6.3%

Charlotte 8.7%

Greenville12.3%

Columbia8.5%

Charleston5.1%

Raleigh6.3%

Charlotte 8.7%

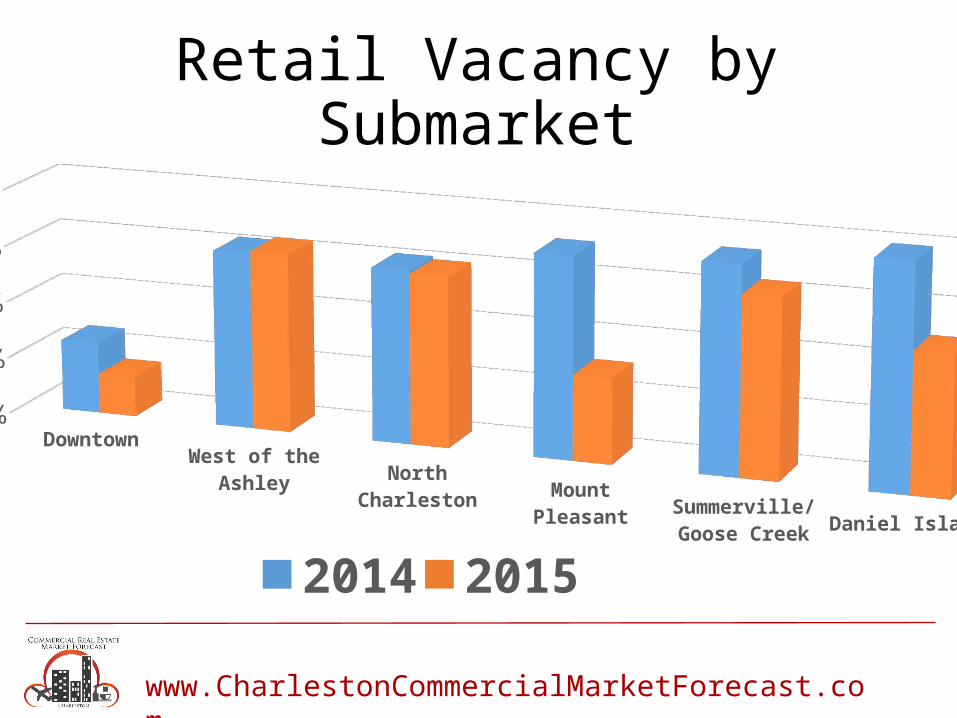

Retail Vacancy by Submarket

Downtown

West of th

e Ashley

North Charle

ston

Mount Pleasant

Summervi

lle/ G

oose Creek

Daniel Island

0.0%1.0%2.0%3.0%4.0%5.0%6.0%7.0%8.0%

2014 2015

www.CharlestonCommercialMarketForecast.com

Asking Rents for Charleston Retail

20112012

20132014

2015

$0.00$2.00$4.00$6.00$8.00

$10.00$12.00$14.00$16.00$18.00$20.00

$14.75 $14.25 $15.25 $15.25$18.40

www.CharlestonCommercialMarketForecast.com

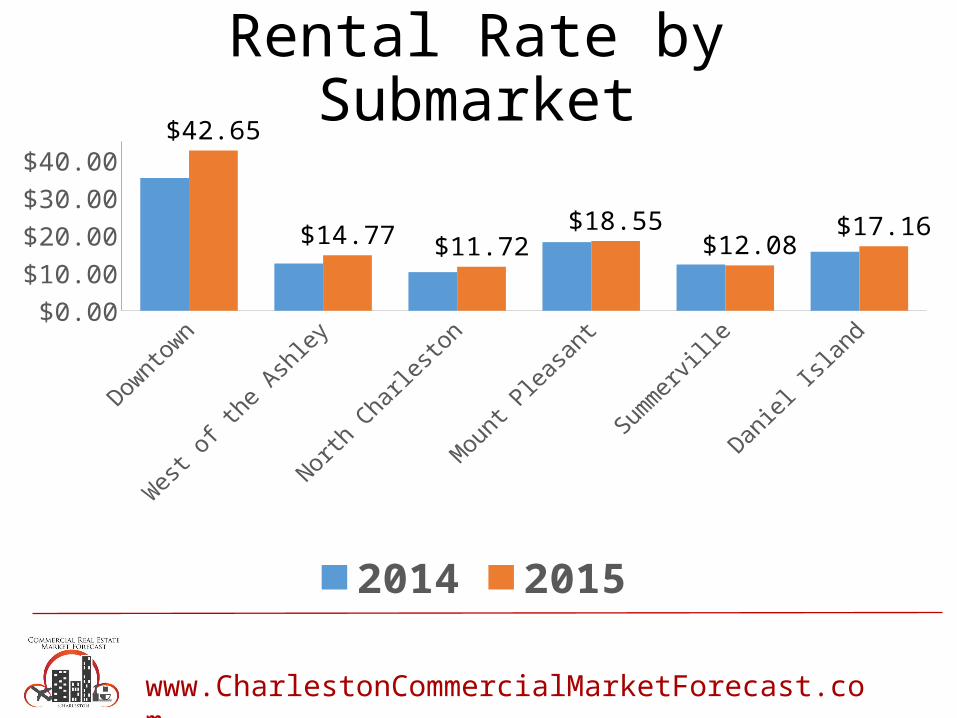

Rental Rate by Submarket

Downtown West of the Ashley

North Charleston

Mount Pleasant

Summerville Daniel Island$0.00$5.00

$10.00$15.00$20.00$25.00$30.00$35.00$40.00$45.00 $42.65

$14.77$11.72

$18.55

$12.08$17.16

2014 2015

www.CharlestonCommercialMarketForecast.com

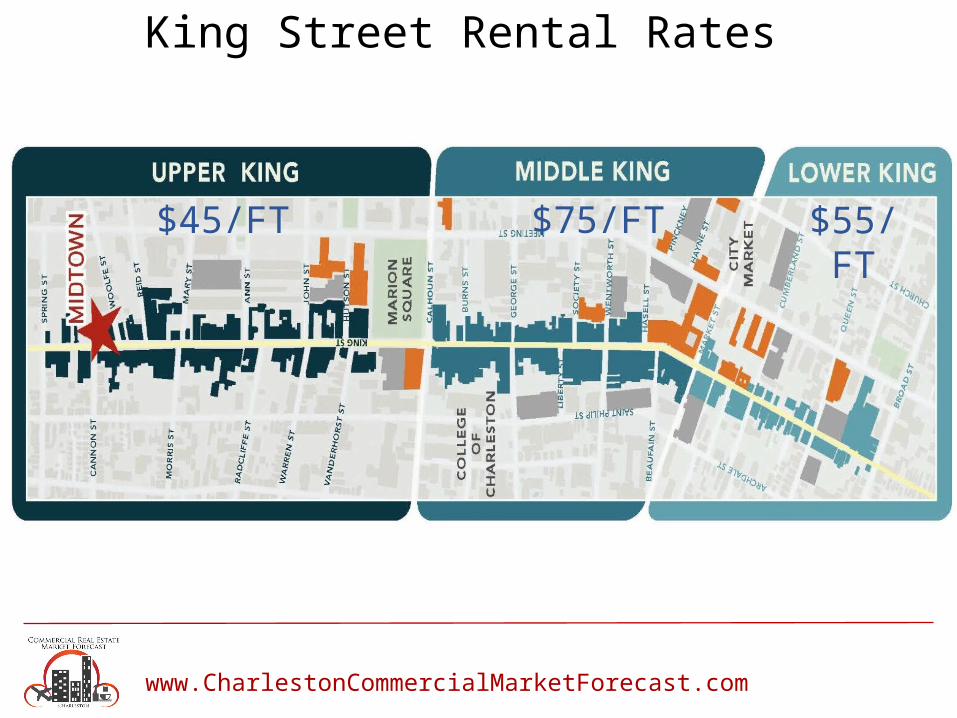

King Street Rental Rates

www.CharlestonCommercialMarketForecast.com

$55/FT$75/FT$45/FT

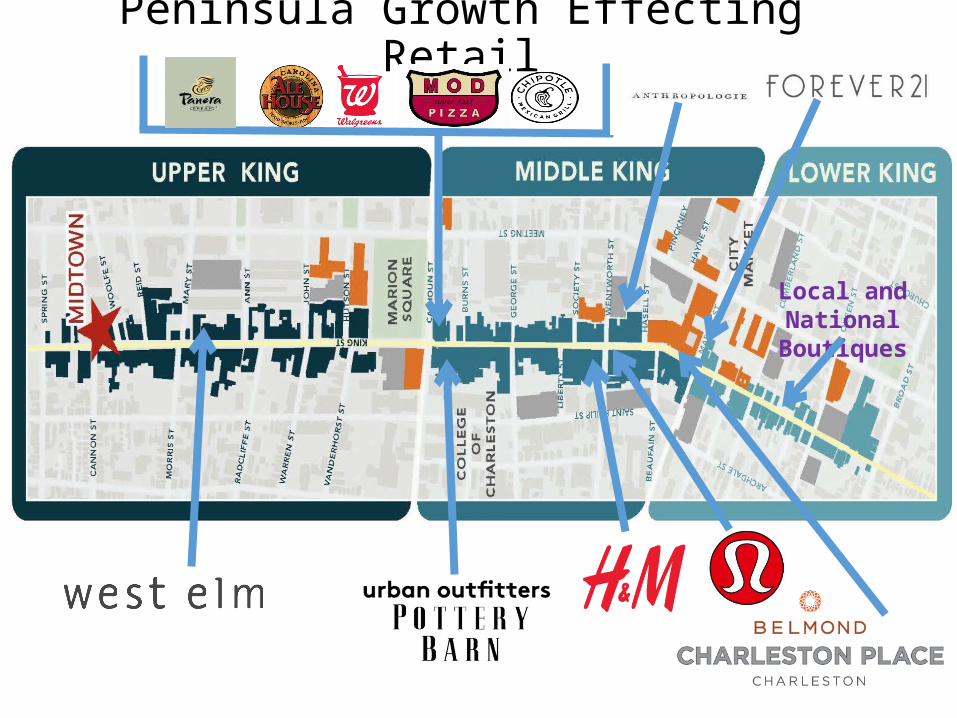

Peninsula Growth Effecting Retail

Local and National Boutiques

Sportsman Wars

www.CharlestonCommercialMarketForecast.com

New and Expanding Grocers

www.CharlestonCommercialMarketForecast.com

Retailers on the rise

www.CharlestonCommercialMarketForecast.com

Retailers on the rise

www.CharlestonCommercialMarketForecast.com

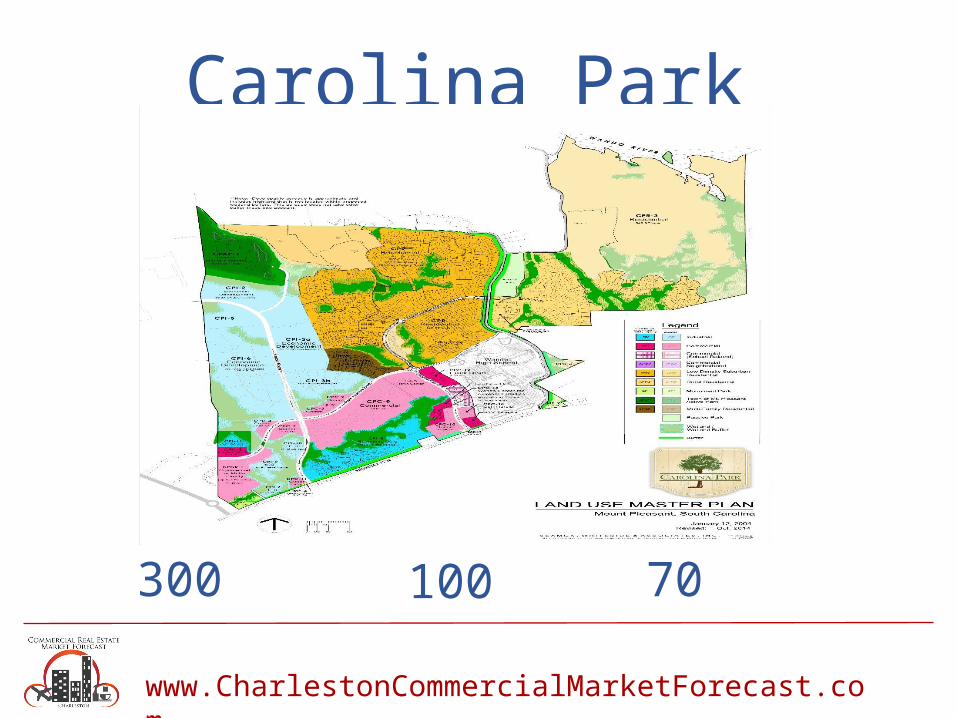

Carolina Park

www.CharlestonCommercialMarketForecast.com

300 100 70

West Edge

www.CharlestonCommercialMarketForecast.com

290,000 Square Feet

Ingleside Plantation

www.CharlestonCommercialMarketForecast.com

750K – 1 Million Square Feet

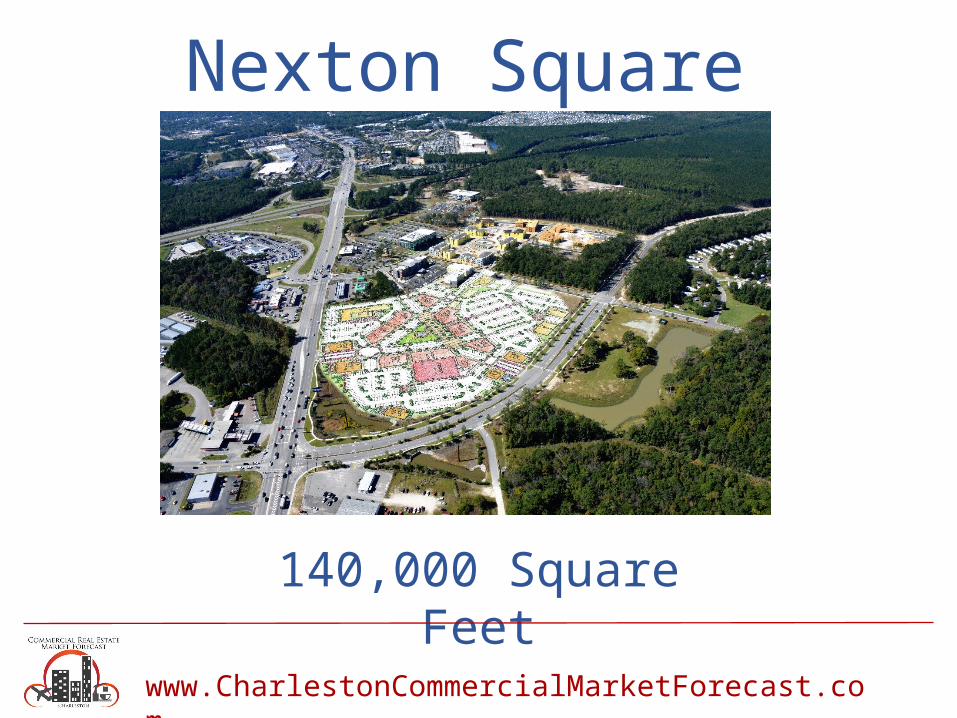

Nexton Square

www.CharlestonCommercialMarketForecast.com

140,000 Square Feet

Cainhoy Plantation

www.CharlestonCommercialMarketForecast.com

300,000 Square Feet

Courier Square

www.CharlestonCommercialMarketForecast.com

19,000 Square Feet

Key Takeaways•Declining vacancies and increasing development

costs create historically high rental rates.•Strong retailer interest supports new construction.•National expansion continues into Charleston. •Tourism remains beneficial for downtown retailers.•Many large mixed use developments are on the

horizon.•All interior doors must match!

www.CharlestonCommercialMarketForecast.com

Jeffrey Yurfest, CCIM

www.CharlestonCommercialMarketForecast.com

www.CharlestonCommercialMarketForecast.com

OFFICE REPORT

www.CharlestonCommercialMarketForecast.com

Jeremy N. WillitsPrincipal, Office ServicesAvison Young

www.CharlestonCommercialMarketForecast.com

Header

Text in Calibri font

www.CharlestonCommercialMarketForecast.com

Header

Text in Calibri font

www.CharlestonCommercialMarketForecast.com

Header

Text in Calibri font

www.CharlestonCommercialMarketForecast.com

Header

Text in Calibri font

www.CharlestonCommercialMarketForecast.com

North Morrison “No-Mo” District

•Technology Jobs

•Upper Peninsula Zoning District

•Increasing Land Values

www.CharlestonCommercialMarketForecast.com

Header

Text in Calibri font

www.CharlestonCommercialMarketForecast.com

Header

Text in Calibri font

www.CharlestonCommercialMarketForecast.com

Summerville/I-26 Corridor

•Nexton

•Direct/Indirect jobs

•Service jobs followManufacturing

•Less than 250,000 square feet class A

www.CharlestonCommercialMarketForecast.com

What the Future Holds

•Significant development inside I-526

•Rental Rates Increase

•Values increase

www.CharlestonCommercialMarketForecast.com

Jeremy N. WillitsPrincipal, Office ServicesAvison [email protected]

www.CharlestonCommercialMarketForecast.com

INDUSTRIAL REPORT

www.CharlestonCommercialMarketForecast.com

CTAR-CID COMMERCIAL & INDUSTRIAL MARKET FORECAST

Derek J. Mathis, Director of Industrial Development, WestRock

www.CharlestonCommercialMarketForecast.com

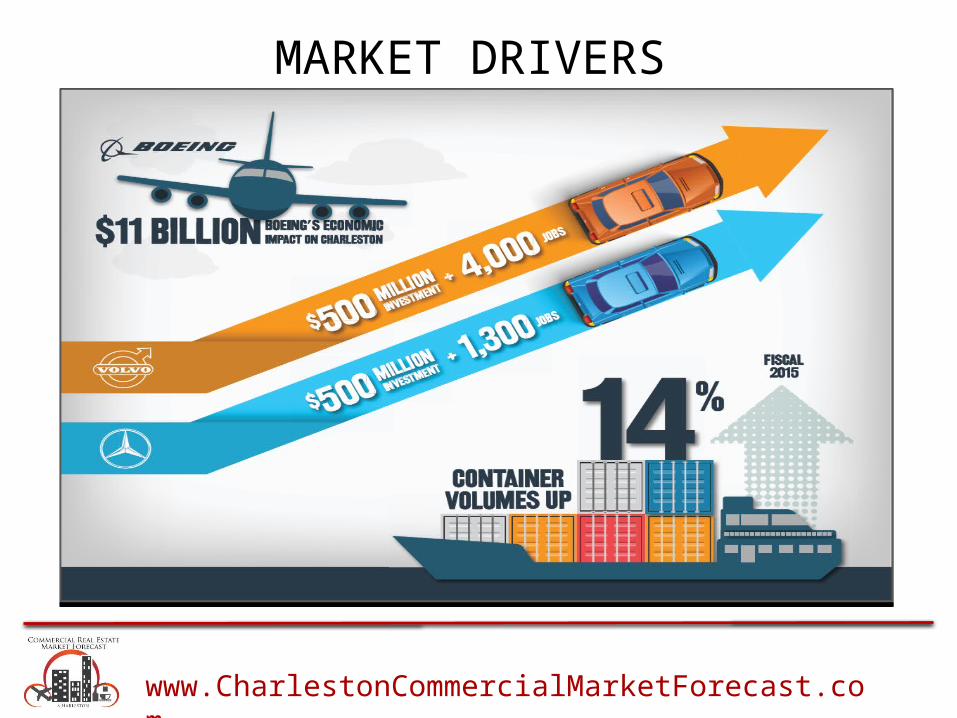

MARKET DRIVERS

www.CharlestonCommercialMarketForecast.com

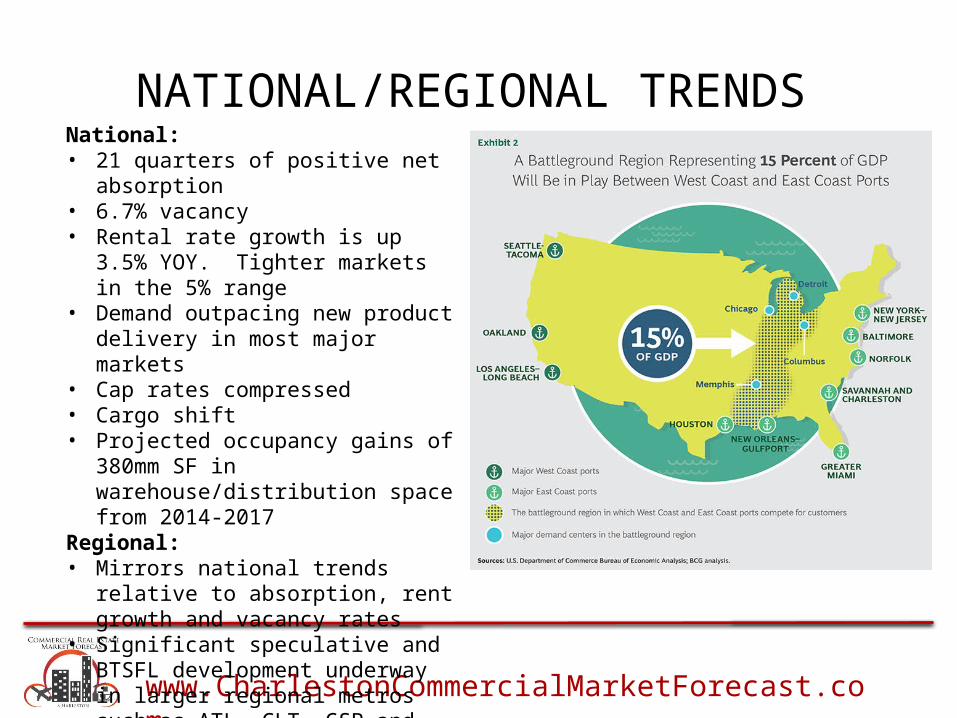

NATIONAL/REGIONAL TRENDS

National:• 21 quarters of positive net absorption• 6.7% vacancy• Rental rate growth is up 3.5% YOY. Tighter

markets in the 5% range• Demand outpacing new product delivery

in most major markets • Cap rates compressed• Cargo shift• Projected occupancy gains of 380mm SF

in warehouse/distribution space from 2014-2017

Regional:• Mirrors national trends relative to

absorption, rent growth and vacancy rates• Significant speculative and BTSFL

development underway in larger regional metros such as ATL, CLT, GSP and SAV

www.CharlestonCommercialMarketForecast.com

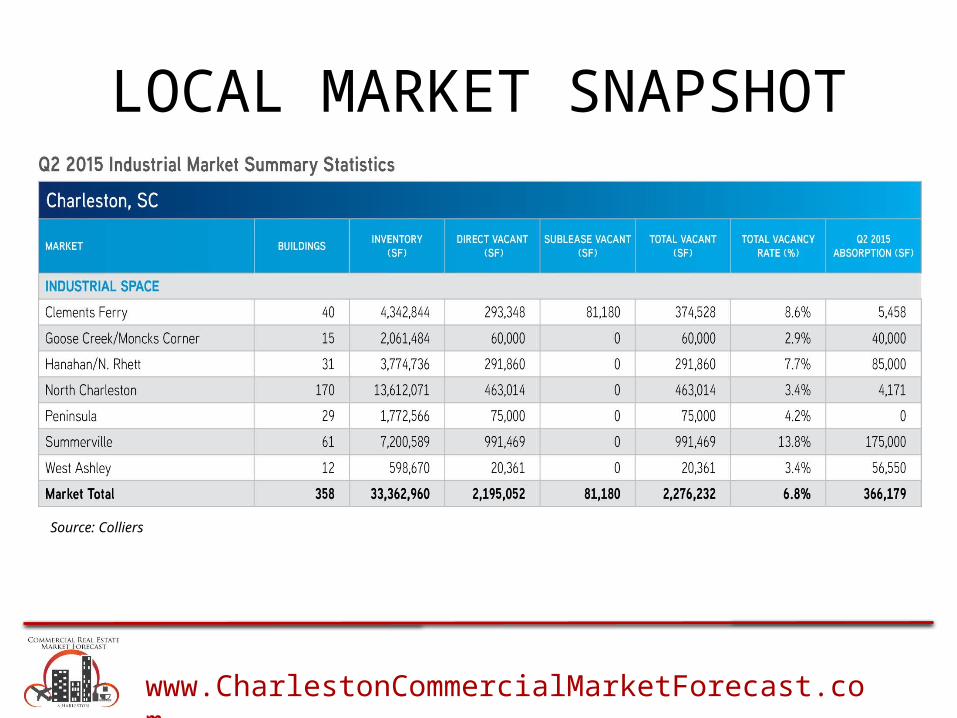

LOCAL MARKET SNAPSHOT

Source: Colliers

www.CharlestonCommercialMarketForecast.com

LOCAL TRENDSTYPE OF ACTIVITY?• FDI driving SC economy• Balanced mix of manufacturing and

distributionWHERE?• Prospects prefer “project ready” locations• Infill traditionally preferred location but that

is changing • Jedburg sub-market activity has increased

significantlyWHY?• Favorable business climate• Right to Work• Infrastructure• Clustering• Reshoring trend• It’s Charleston…

Relative to prior periodMarket Indicators+

Vacancy

Net absorption

Construction

Rental Rate

+ +

Note: Construction is the change in Under Construction*Projected

Q2 2015 Q3 2015*

+Source: Colliers International

WRK – Active projects by type

54% Manufacturing 45% Distribution

1% Other

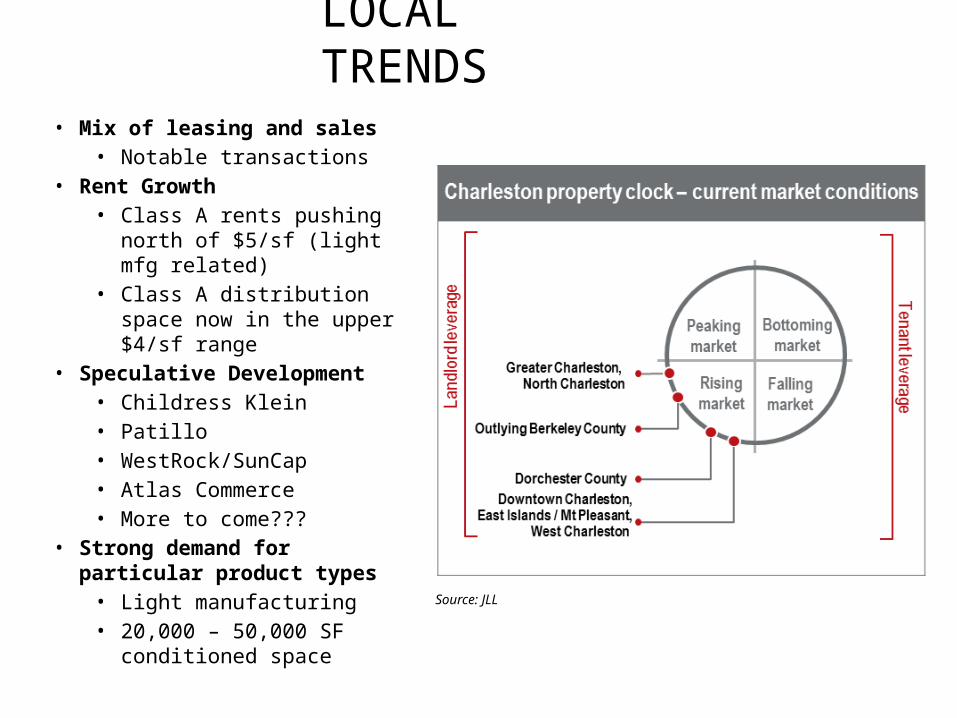

LOCAL TRENDS• Mix of leasing and sales

• Notable transactions• Rent Growth

• Class A rents pushing north of $5/sf (light mfg related)

• Class A distribution space now in the upper $4/sf range

• Speculative Development• Childress Klein• Patillo• WestRock/SunCap• Atlas Commerce• More to come???

• Strong demand for particular product types• Light manufacturing• 20,000 – 50,000 SF

conditioned space

Source: JLL

www.CharlestonCommercialMarketForecast.com

Case Study: GERBER CHILDRENSWEAR

Market Impact?• $33mm in investment• 100-125 jobs• Further reinforces/validates the Jedburg market

as viable location for large distribution projects

Why Berkeley County?• Logistical advantages (proximity to Port and growth markets)• Favorable business climate• Available economic incentives• Operational cost efficiencies to be achieved

Why Rockefeller – MWV Foreign Trade Zone Park?• Speed to market/site readiness• Confidence in Development team’s ability to deliver• Costs• Connectivity to future Exit 197 along with Nexton

amenities and housing• Class A environment and neighboring tenants help to

ensure long term valuation of asset

www.CharlestonCommercialMarketForecast.com

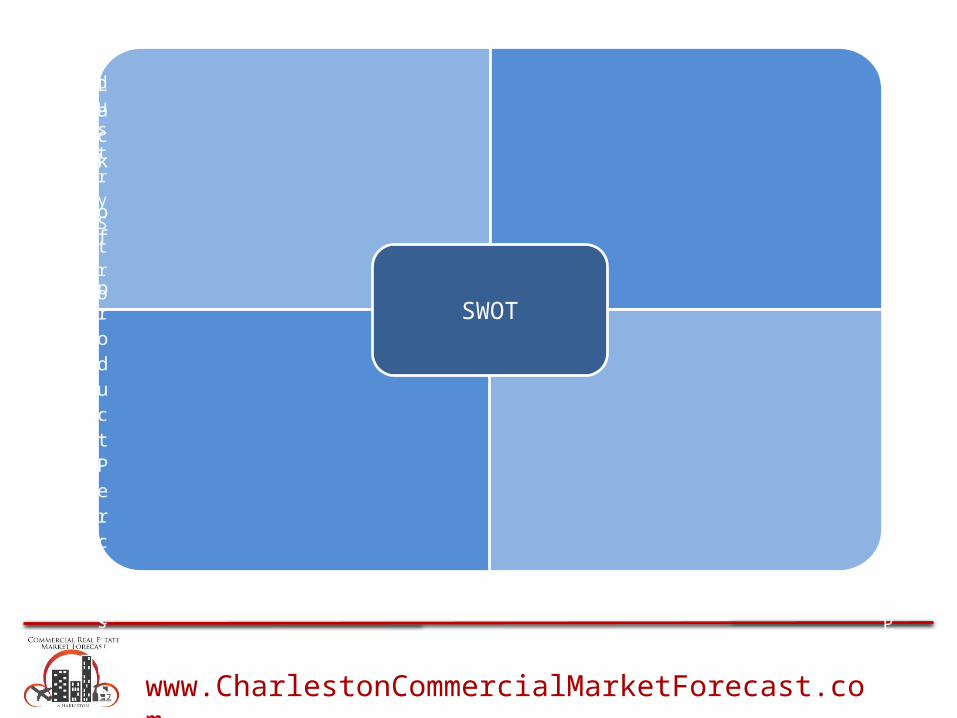

STRENGTHSQuality of lifeBreadth of industryStrong PortPro-business leadership

OPPORTUNITIESMomentumAbility to attract and retain talentPublic/Private collaboration

WEAKNESSESLack of productPerception that CHS is too expensive

THREATSInfrastructureWorkforce availability

SWOT

STRENGTHS

www.CharlestonCommercialMarketForecast.com

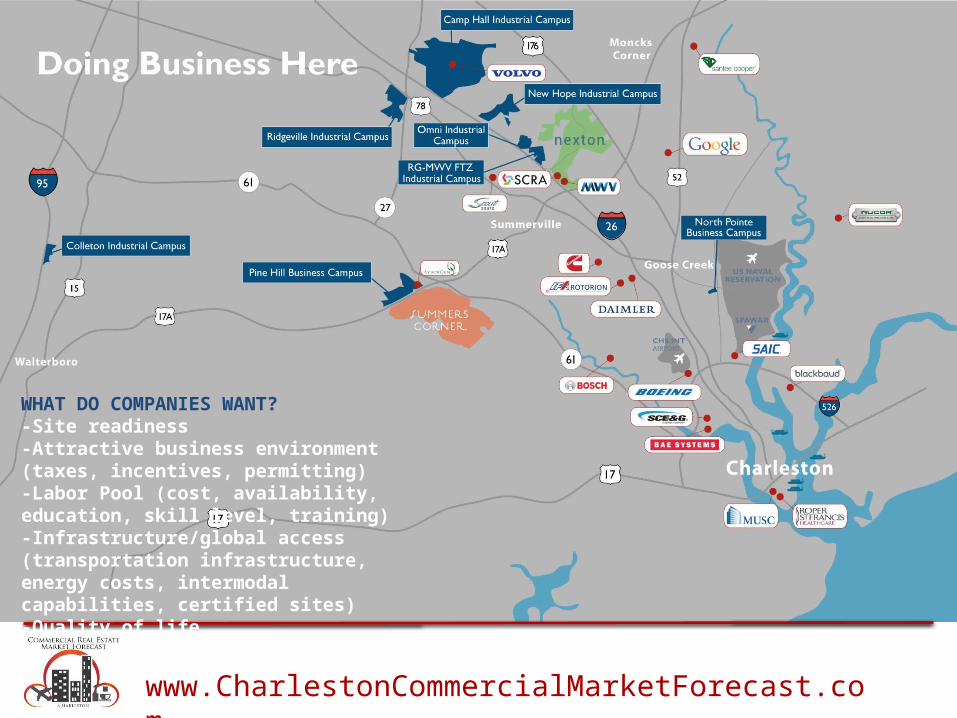

WHAT DO COMPANIES WANT?-Site readiness-Attractive business environment (taxes, incentives, permitting)-Labor Pool (cost, availability, education, skill level, training)-Infrastructure/global access (transportation infrastructure, energy costs, intermodal capabilities, certified sites)-Quality of life

www.CharlestonCommercialMarketForecast.com

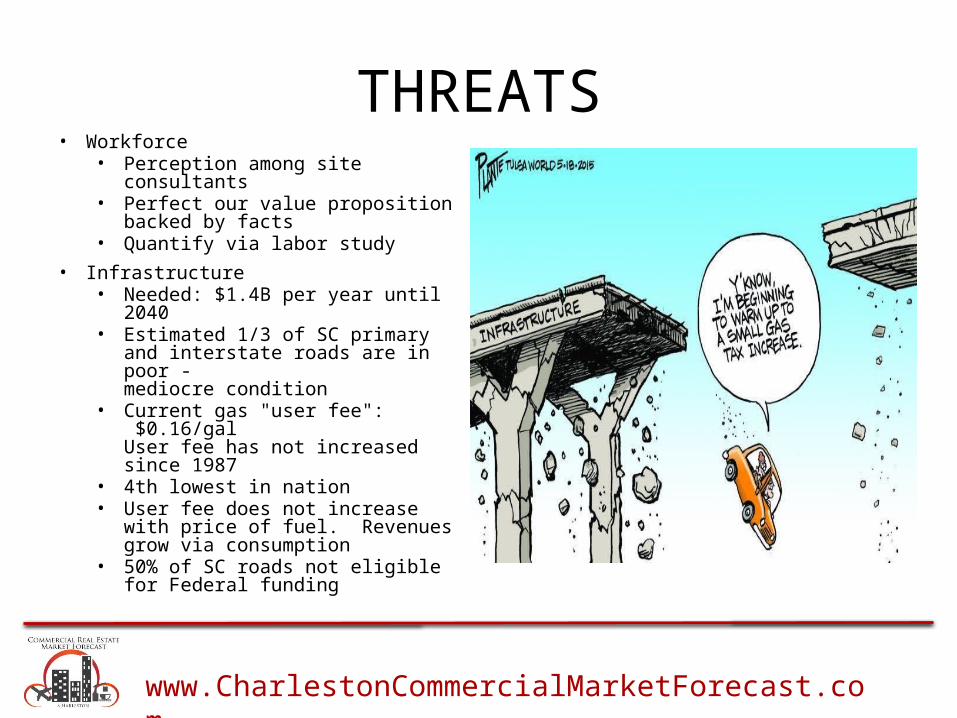

THREATS• Workforce

• Perception among site consultants• Perfect our value proposition

backed by facts• Quantify via labor study

• Infrastructure • Needed: $1.4B per year until 2040• Estimated 1/3 of SC primary and

interstate roads are in poor -mediocre condition

• Current gas "user fee": $0.16/galUser fee has not increased since 1987

• 4th lowest in nation• User fee does not increase with

price of fuel. Revenues grow via consumption

• 50% of SC roads not eligible for Federal funding

www.CharlestonCommercialMarketForecast.com

LOOKING AHEAD…

www.CharlestonCommercialMarketForecast.com

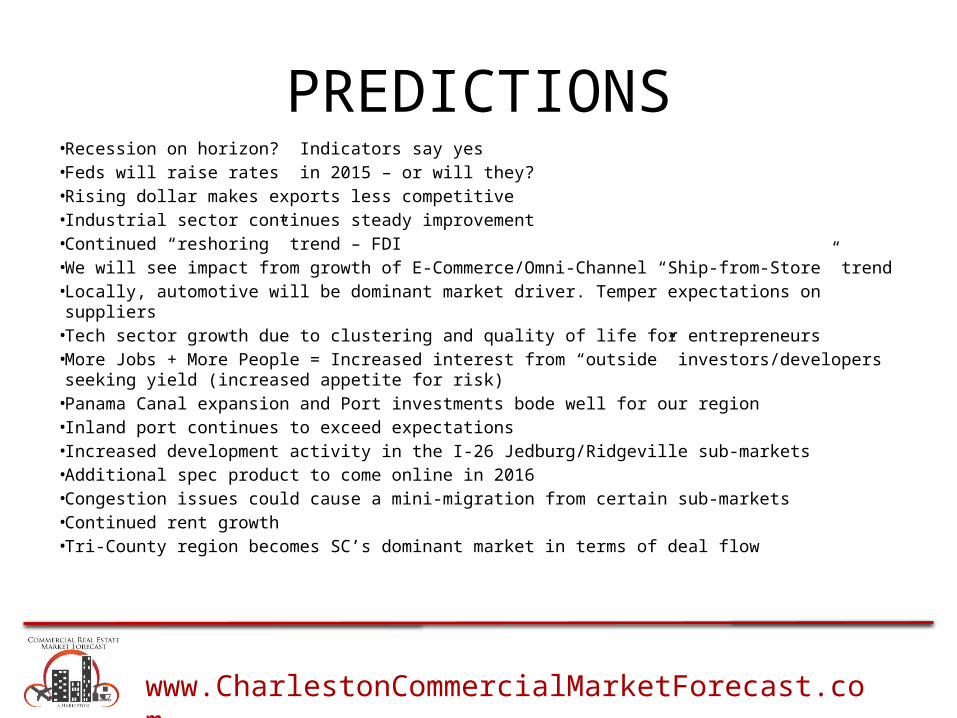

• Recession on horizon? Indicators say yes• Feds will raise rates in 2015 – or will they?• Rising dollar makes exports less competitive• Industrial sector continues steady improvement • Continued “reshoring” trend – FDI • We will see impact from growth of E-Commerce/Omni-Channel “Ship-from-Store” trend• Locally, automotive will be dominant market driver. Temper expectations on suppliers• Tech sector growth due to clustering and quality of life for entrepreneurs• More Jobs + More People = Increased interest from “outside” investors/developers seeking yield (increased

appetite for risk)• Panama Canal expansion and Port investments bode well for our region• Inland port continues to exceed expectations• Increased development activity in the I-26 Jedburg/Ridgeville sub-markets • Additional spec product to come online in 2016• Congestion issues could cause a mini-migration from certain sub-markets• Continued rent growth• Tri-County region becomes SC’s dominant market in terms of deal flow

PREDICTIONS

www.CharlestonCommercialMarketForecast.com

CTAR-CID COMMERCIAL & INDUSTRIAL MARKET FORECAST

Derek J. Mathis, Director of Industrial Development, [email protected] | 843.851.4722

www.CharlestonCommercialMarketForecast.com

MULTI-FAMILY REPORT

www.CharlestonCommercialMarketForecast.com

Charleston Multifamily Report

RANDY BATES

RANDOLPH DEVELOPMENT

www.CharlestonCommercialMarketForecast.com

Target Market - Demographic Trends

• Millennials – 20 – 34 years old o Largest Demographic Group in American Historyo 85 Million to 95 Million Peopleo Staggering Student Debto Diminished Job Opportunitieso Delayed Marriageo Desire Flexibility & Job Mobilityo Opting Out of Home Ownership

www.CharlestonCommercialMarketForecast.com

Target Market - Demographic Trends

• Empty Nesters – 50 – 69 years oldo Active Baby Boomerso Less need for spaceo Desire Less Home Maintenanceo Selling Homes - Greater Equityo More Disposable Incomeo Returning to Cities

www.CharlestonCommercialMarketForecast.com

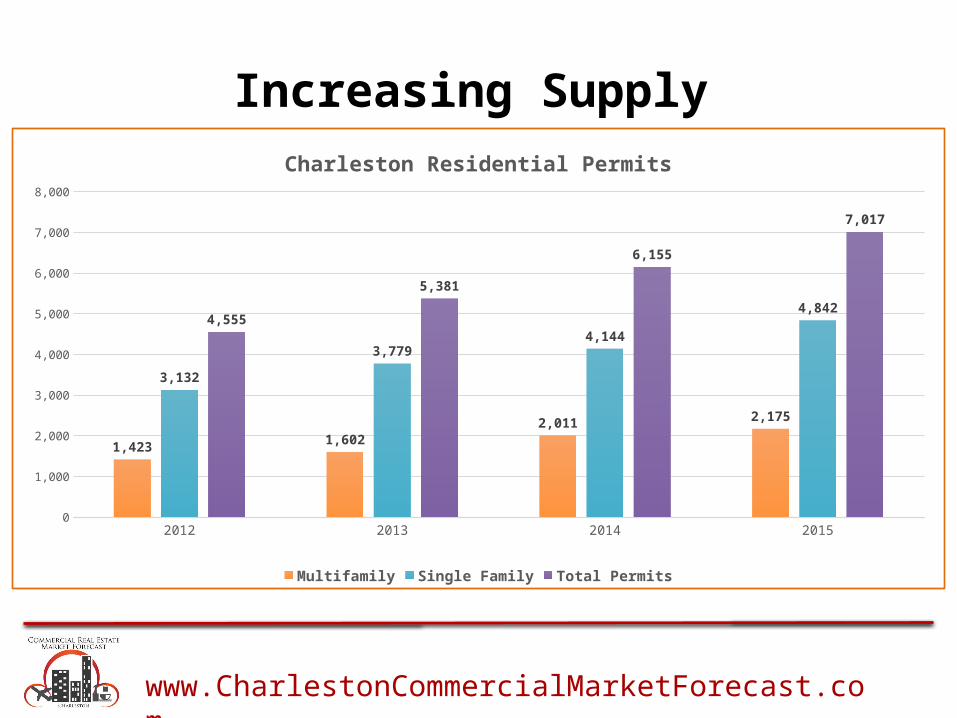

Increasing Supply

www.CharlestonCommercialMarketForecast.com

Increasing Supply

2012 2013 2014 20150

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

1,423 1,6022,011 2,175

3,132

3,7794,144

4,8424,555

5,381

6,155

7,017

Charleston Residential Permits

Multifamily Single Family Total Permits

www.CharlestonCommercialMarketForecast.com

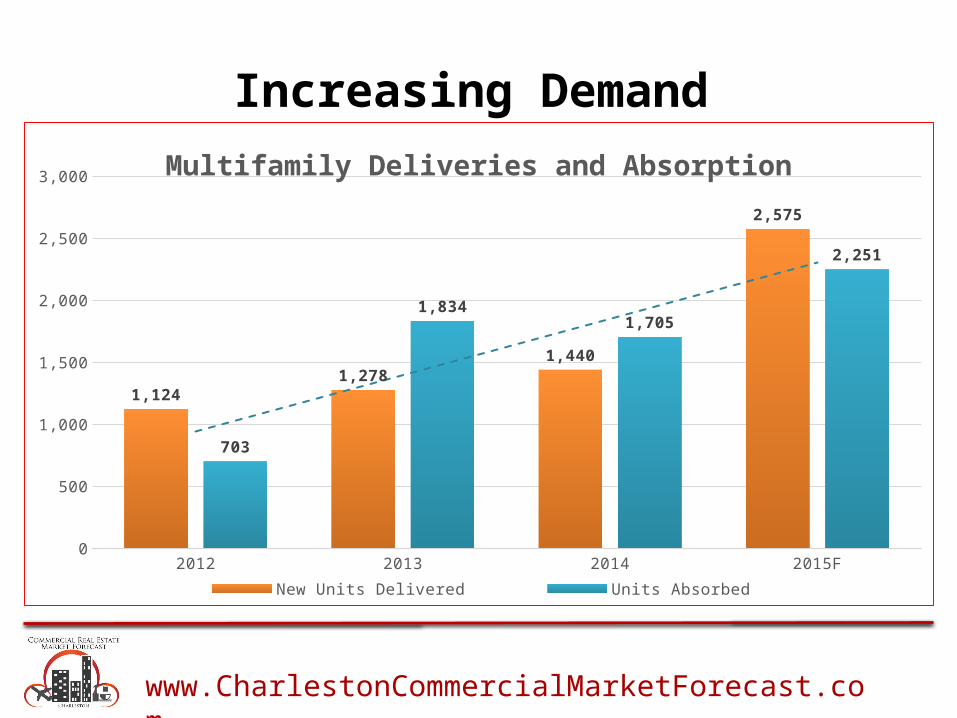

Increasing Demand

www.CharlestonCommercialMarketForecast.com

Increasing Demand

2012 2013 2014 2015F0

500

1,000

1,500

2,000

2,500

3,000

1,1241,278

1,440

2,575

703

1,8341,705

2,251

Multifamily Deliveries and Absorption

New Units Delivered Units Absorbed Linear (Units Absorbed)

www.CharlestonCommercialMarketForecast.com

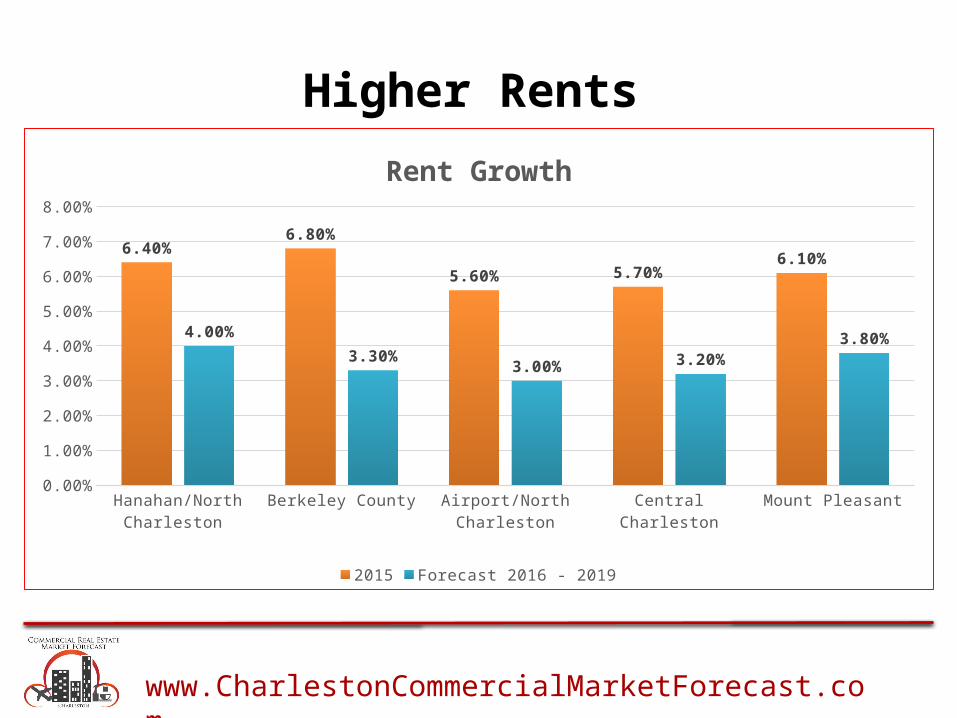

Higher Rents

Hanahan/North Charleston Berkeley County Airport/North Charleston Central Charleston Mount Pleasant0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

6.40%6.80%

5.60% 5.70%6.10%

4.00%

3.30%3.00% 3.20%

3.80%

Rent Growth

2015 Forecast 2016 - 2019

www.CharlestonCommercialMarketForecast.com

Higher Rents

www.CharlestonCommercialMarketForecast.com

Charleston Multifamily ReportSo What Do We Make Of All This???

www.CharlestonCommercialMarketForecast.com

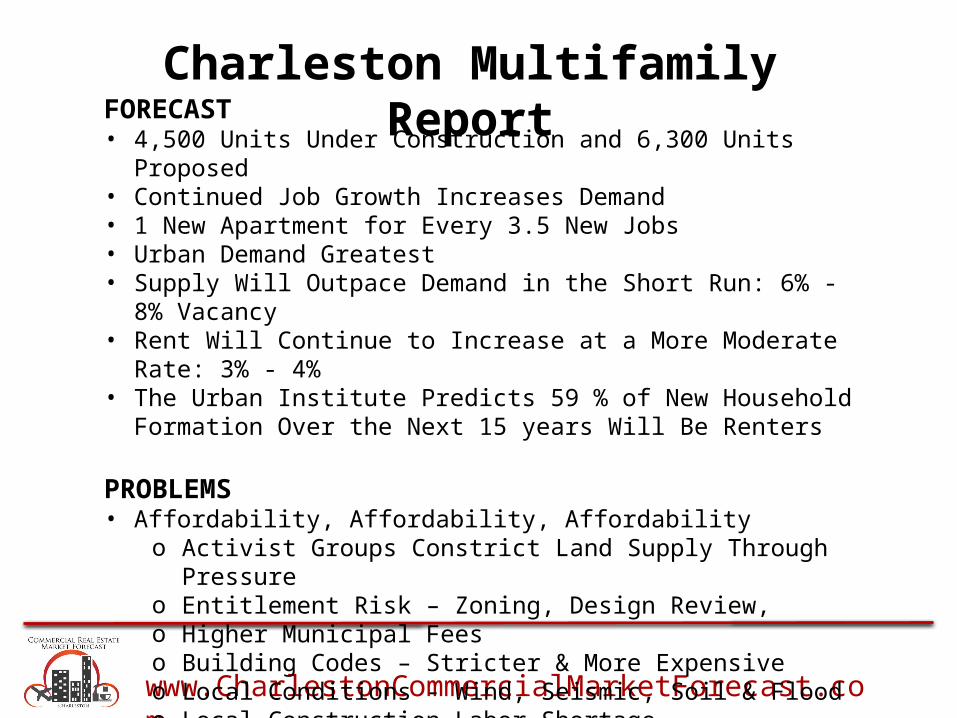

Charleston Multifamily Report

FORECAST• 4,500 Units Under Construction and 6,300 Units Proposed• Continued Job Growth Increases Demand• 1 New Apartment for Every 3.5 New Jobs• Urban Demand Greatest• Supply Will Outpace Demand in the Short Run: 6% - 8% Vacancy• Rent Will Continue to Increase at a More Moderate Rate: 3% - 4%• The Urban Institute Predicts 59 % of New Household Formation Over the

Next 15 years Will Be Renters

PROBLEMS• Affordability, Affordability, Affordability

o Activist Groups Constrict Land Supply Through Pressureo Entitlement Risk – Zoning, Design Review, o Higher Municipal Feeso Building Codes – Stricter & More Expensiveo Local Conditions - Wind, Seismic, Soil & Floodo Local Construction Labor Shortage

www.CharlestonCommercialMarketForecast.com

Charleston Multifamily Report

RANDY BATES

RANDOLPH DEVELOPMENT

[email protected] | 843.849.0739

www.CharlestonCommercialMarketForecast.com

DEVELOPMENT REPORT

www.CharlestonCommercialMarketForecast.com

Charleston Regional Overview

Michael Graney, VP Global Business Development

www.CharlestonCommercialMarketForecast.com

Top Relocation Trends

AVAILABLE LAND &

BUILDINGS“Speed to market”

with fast-track permitting

INCENTIVES & TRAINING

PROGRAMSProviding opportunities for business growth & success

MARKET ACCESS & LOGISTICS

Fast routes that create proximity to markets &

suppliers

TALENT AVAILBILITY

Importance on attracting skilled and advanced

labor

REVENUE GROWTH

Greater focus over cost-cutting

www.CharlestonCommercialMarketForecast.com

Target Strategy

www.CharlestonCommercialMarketForecast.com

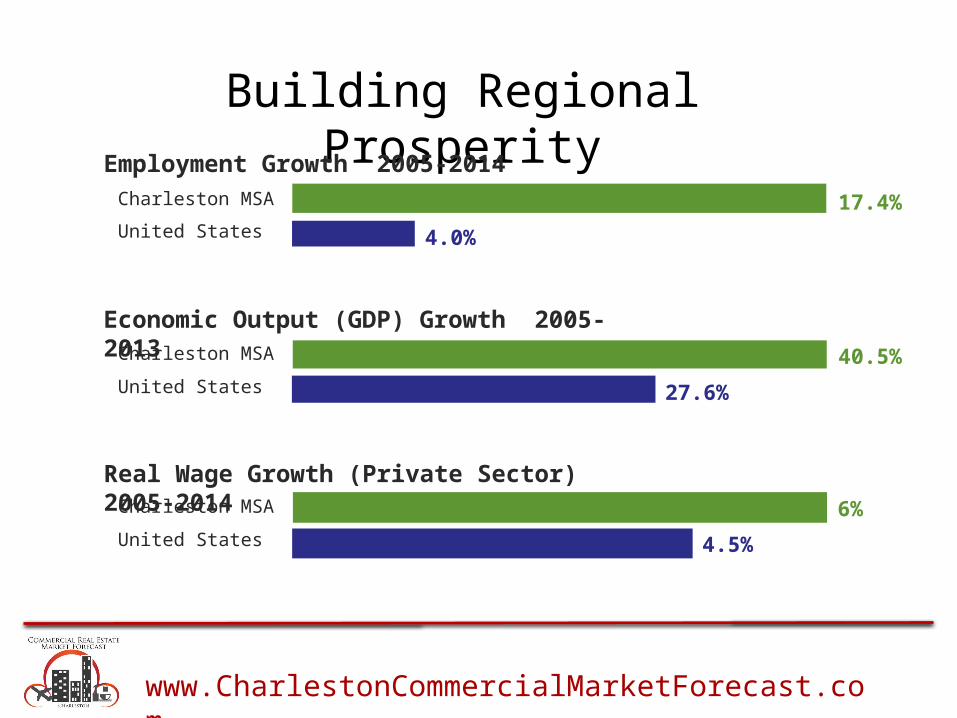

Building Regional Prosperity

Economic Output (GDP) Growth 2005-2013Charleston MSA

United States40.5%

27.6%

Employment Growth 2005-2014Charleston MSA

United States17.4%

4.0%

Real Wage Growth (Private Sector) 2005-2014Charleston MSA

United States

6%

4.5%

www.CharlestonCommercialMarketForecast.com

Business Development Missions

AerospaceAutomotiveLife ScienceAdvanced SecurityInformation Technology

www.CharlestonCommercialMarketForecast.com

Competitive Context

SC UPSTATE

www.CharlestonCommercialMarketForecast.com

Case Study

BERKELEY COUNTY 72 JOBS

www.CharlestonCommercialMarketForecast.com

Upcoming Trends

Medical Devices

www.CharlestonCommercialMarketForecast.com

Charleston Regional Overview

Michael Graney, VP Global Business Development843.760.4526 | [email protected]

www.CharlestonCommercialMarketForecast.com

QUESTIONS?

www.CharlestonCommercialMarketForecast.com

Launches Oct 13sccommercialmls. com

www.CharlestonCommercialMarketForecast.com

September 30, 2015

Recommended