Embed Size (px)

Citation preview

2010 NC-CCIM Charlotte Commercial

Real Estate Market Forecast

“Commercial Real Estate Debt: Market, Availability, and Characteristics”

Review

Where have we been?

2005 -- 2007

2009

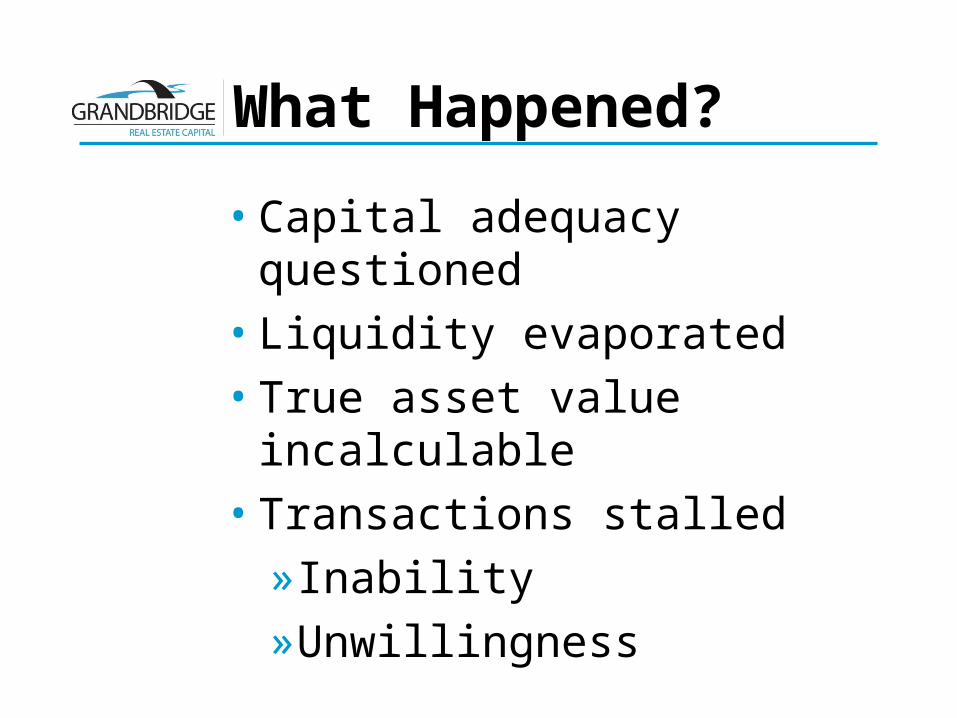

What Happened?

• Capital adequacy questioned

• Liquidity evaporated• True asset value

incalculable• Transactions stalled

»Inability»Unwillingness

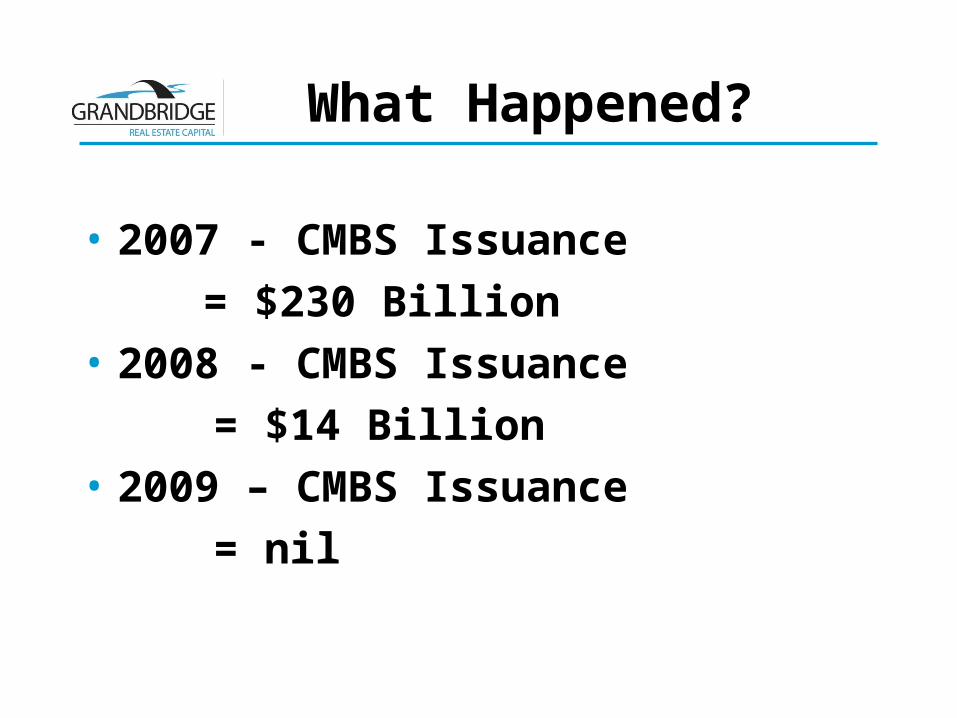

What Happened?

• 2007 - CMBS Issuance = $230 Billion

• 2008 - CMBS Issuance= $14 Billion

• 2009 – CMBS Issuance= nil

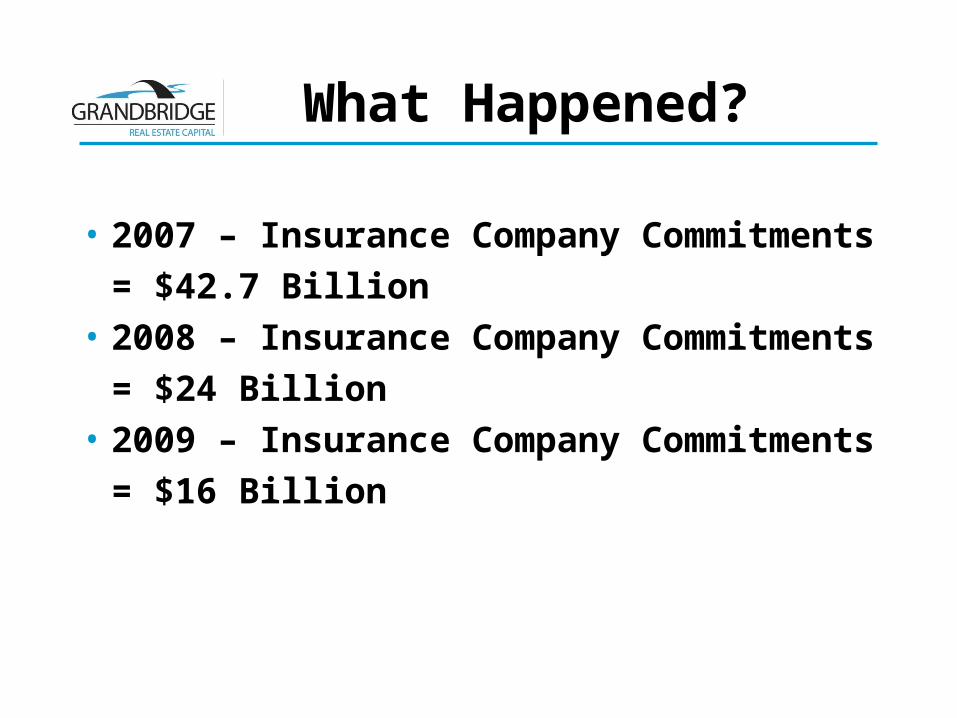

What Happened?

• 2007 – Insurance Company Commitments

= $42.7 Billion• 2008 – Insurance Company

Commitments= $24 Billion

• 2009 – Insurance Company Commitments

= $16 Billion

Can you finance multifamily and

commercialreal estate??

SURE! (cautiously…..)SURE! (cautiously…..)

MARKET

2010

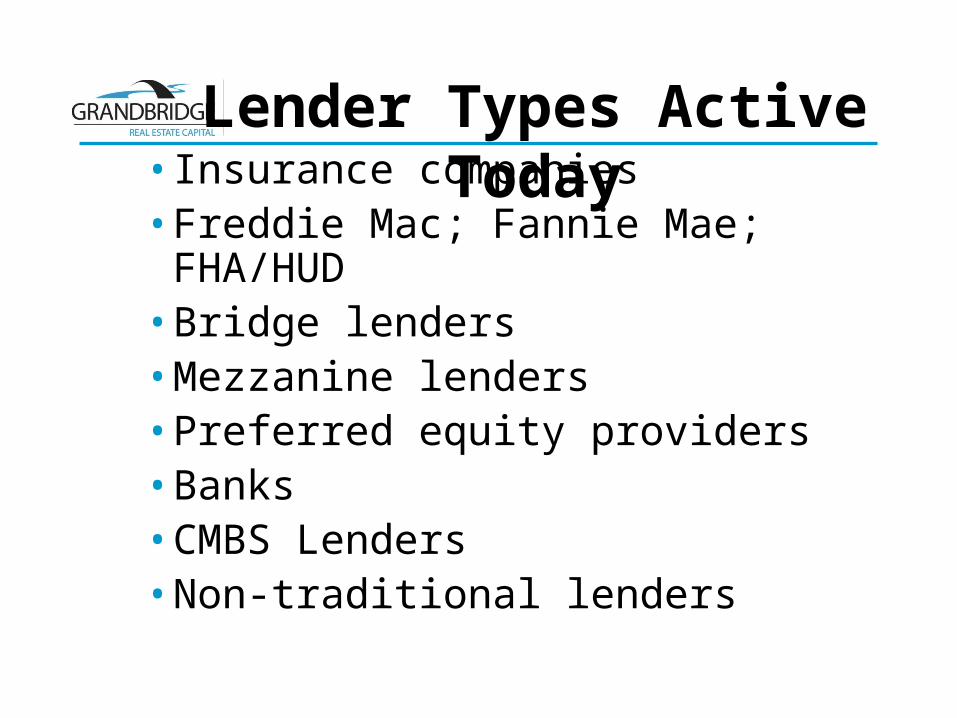

Lender Types Active Today•Insurance companies

•Freddie Mac; Fannie Mae; FHA/HUD

•Bridge lenders•Mezzanine lenders•Preferred equity providers•Banks•CMBS Lenders•Non-traditional lenders

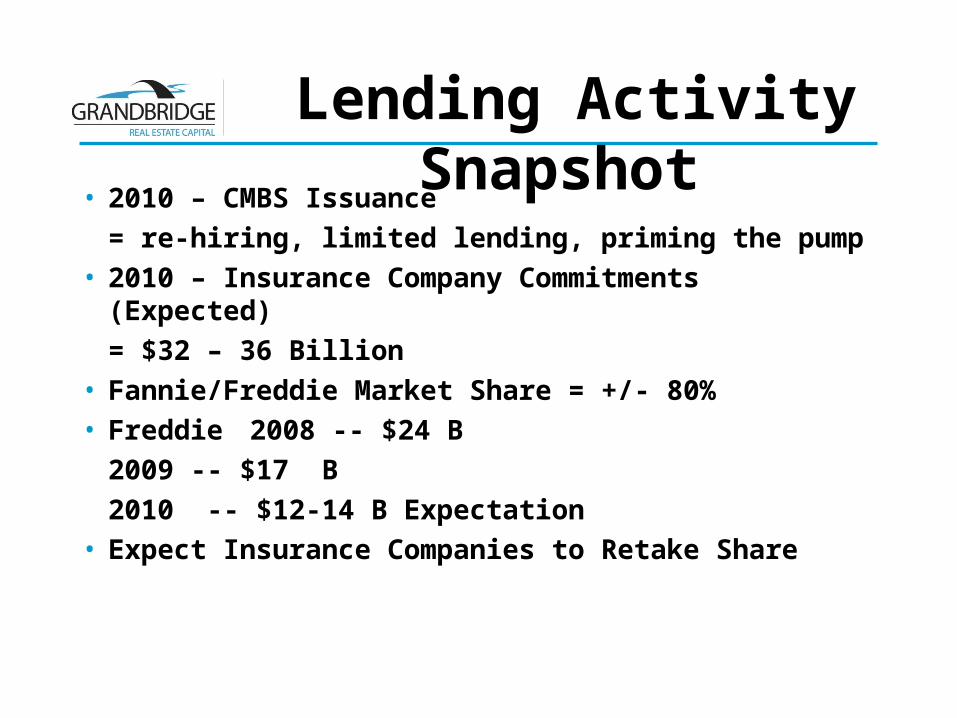

Lending Activity Snapshot

• 2010 – CMBS Issuance= re-hiring, limited lending, priming the

pump• 2010 – Insurance Company Commitments

(Expected)= $32 – 36 Billion

• Fannie/Freddie Market Share = +/- 80% • Freddie 2008 -- $24 B

2009 -- $17 B2010 -- $12-14 B Expectation

• Expect Insurance Companies to Retake Share

AVAILABILITY

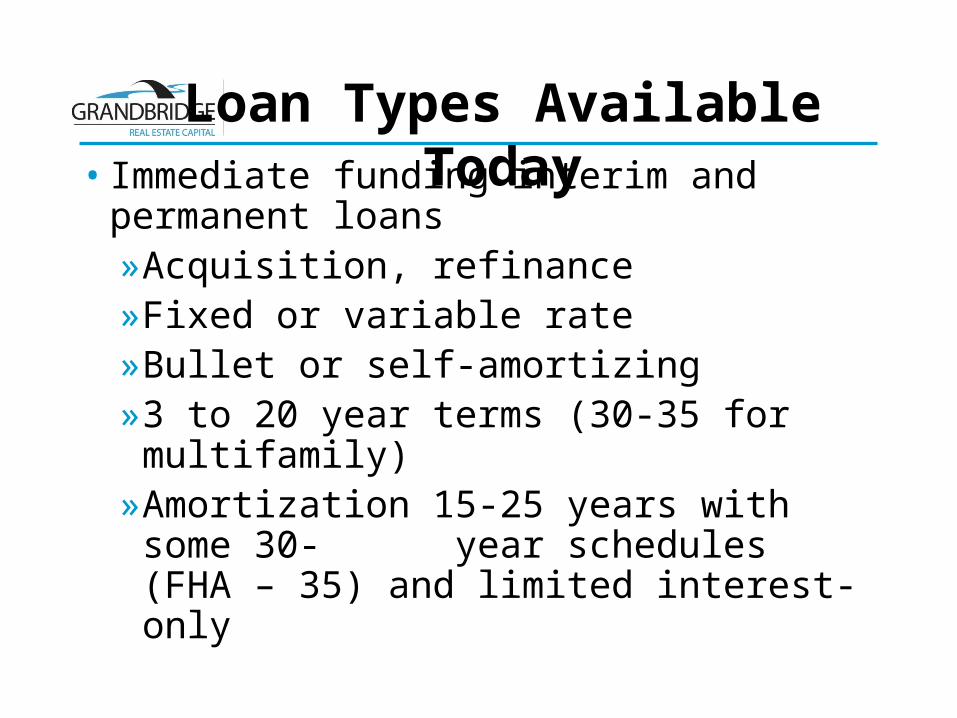

Loan Types Available Today• Immediate funding interim and

permanent loans»Acquisition, refinance»Fixed or variable rate»Bullet or self-amortizing»3 to 20 year terms (30-35 for multifamily)

»Amortization 15-25 years with some 30- year schedules (FHA – 35) and limited interest-only

Loan Types Available Today

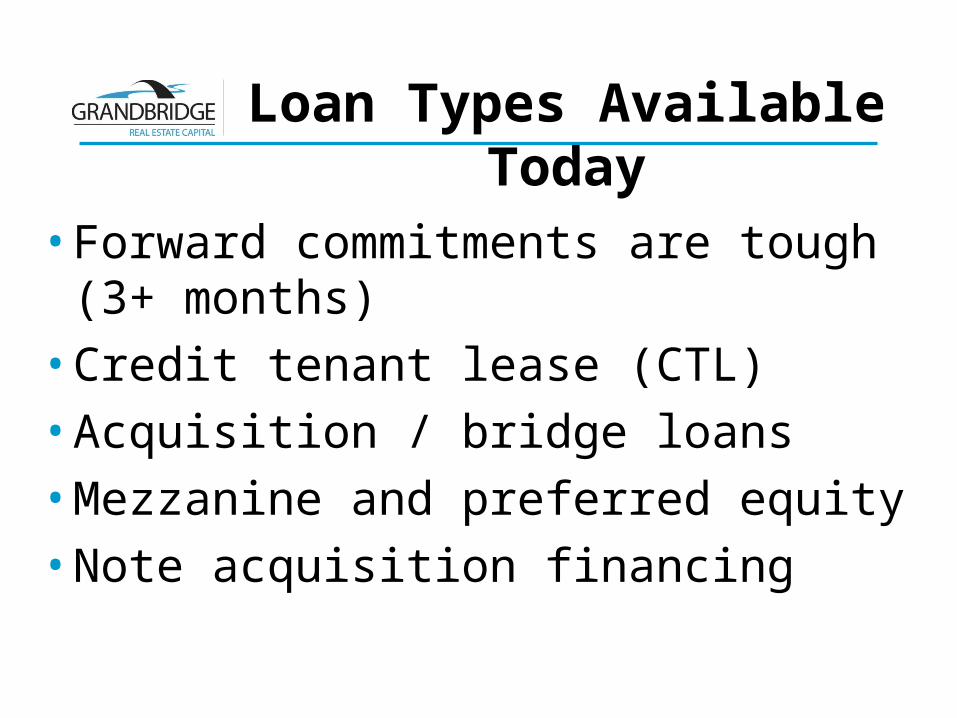

•Forward commitments are tough (3+ months)

•Credit tenant lease (CTL)•Acquisition / bridge loans•Mezzanine and preferred equity•Note acquisition financing

CHARACTERISTICS

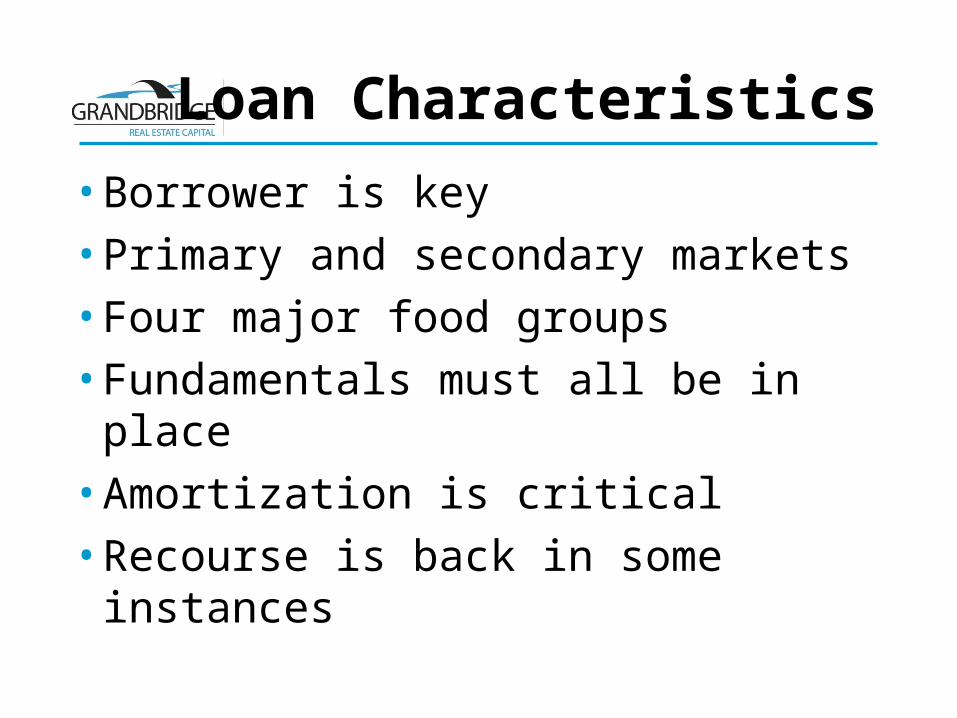

Loan Characteristics

•Borrower is key•Primary and secondary markets•Four major food groups•Fundamentals must all be in

place•Amortization is critical•Recourse is back in some

instances

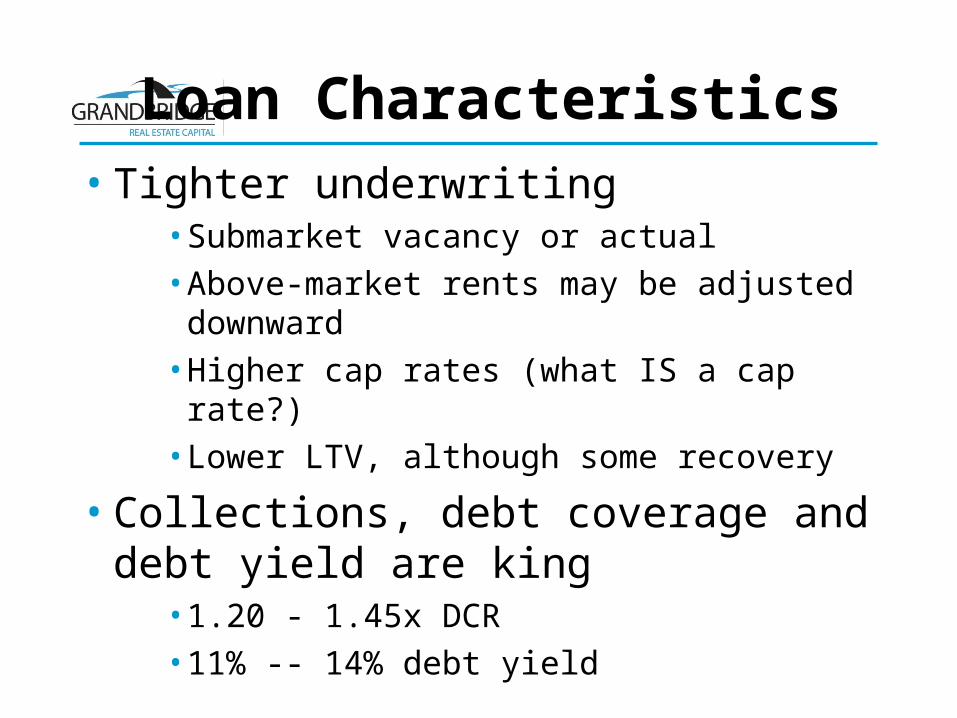

Loan Characteristics• Tighter underwriting

•Submarket vacancy or actual•Above-market rents may be adjusted

downward•Higher cap rates (what IS a cap rate?)•Lower LTV, although some recovery

• Collections, debt coverage and debt yield are king

•1.20 - 1.45x DCR•11% -- 14% debt yield

Loan Characteristics

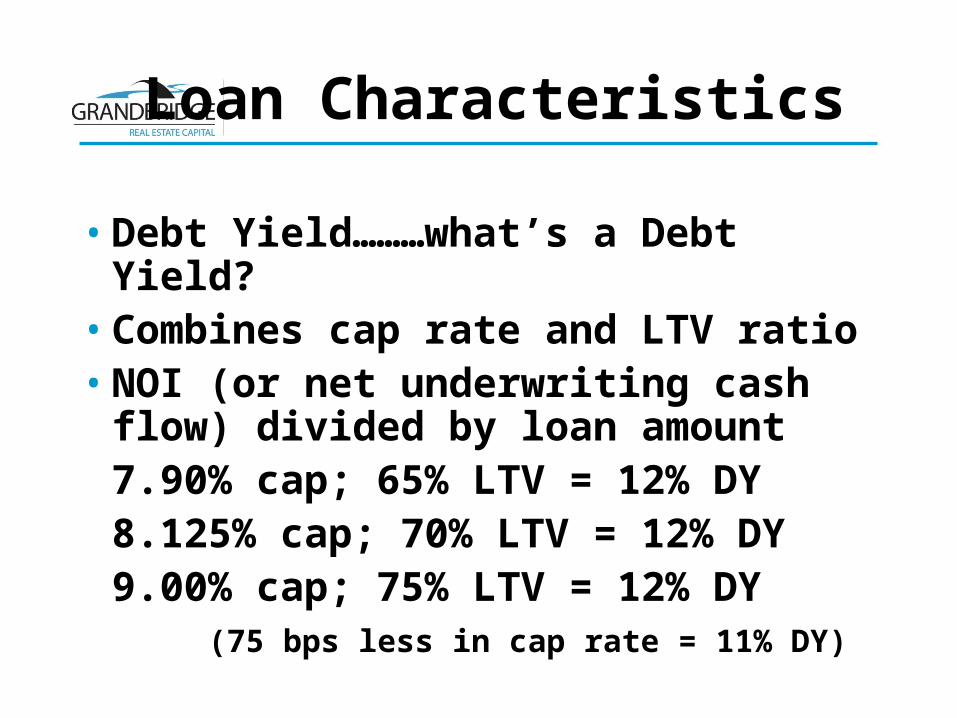

• Debt Yield………what’s a Debt Yield?• Combines cap rate and LTV ratio• NOI (or net underwriting cash flow)

divided by loan amount7.90% cap; 65% LTV = 12% DY8.125% cap; 70% LTV = 12% DY9.00% cap; 75% LTV = 12% DY (75 bps less in cap rate = 11% DY)

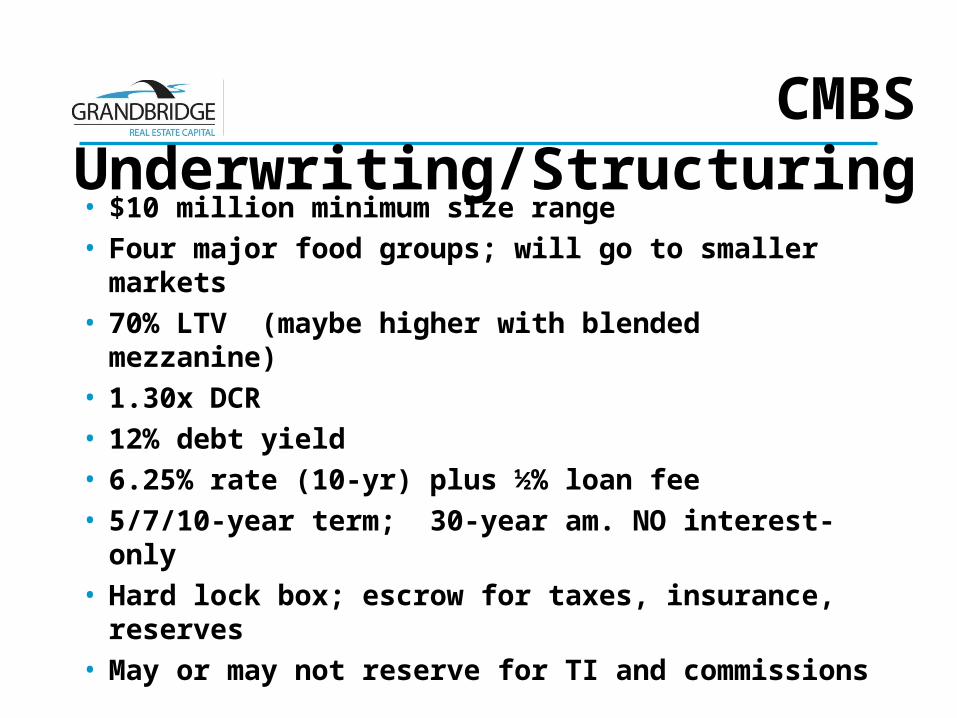

CMBS Underwriting/Structuring• $10 million minimum size range• Four major food groups; will go to smaller

markets• 70% LTV (maybe higher with blended

mezzanine)• 1.30x DCR• 12% debt yield• 6.25% rate (10-yr) plus ½% loan fee• 5/7/10-year term; 30-year am. NO interest-only• Hard lock box; escrow for taxes, insurance,

reserves• May or may not reserve for TI and commissions

Rate Comparison

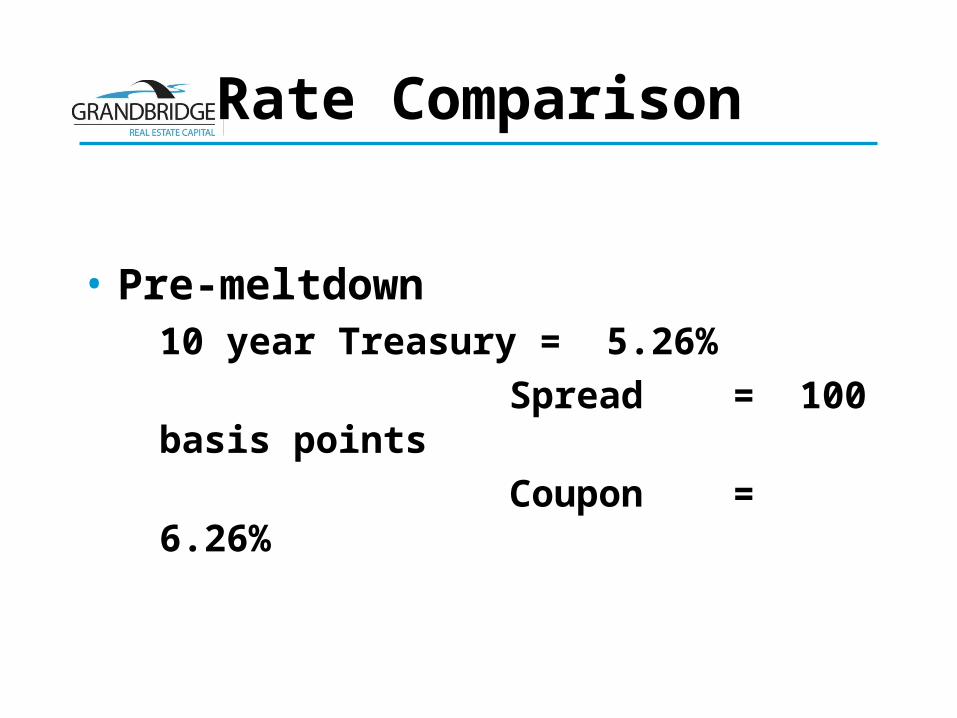

• Pre-meltdown10 year Treasury = 5.26%

Spread = 100 basis points

Coupon = 6.26%

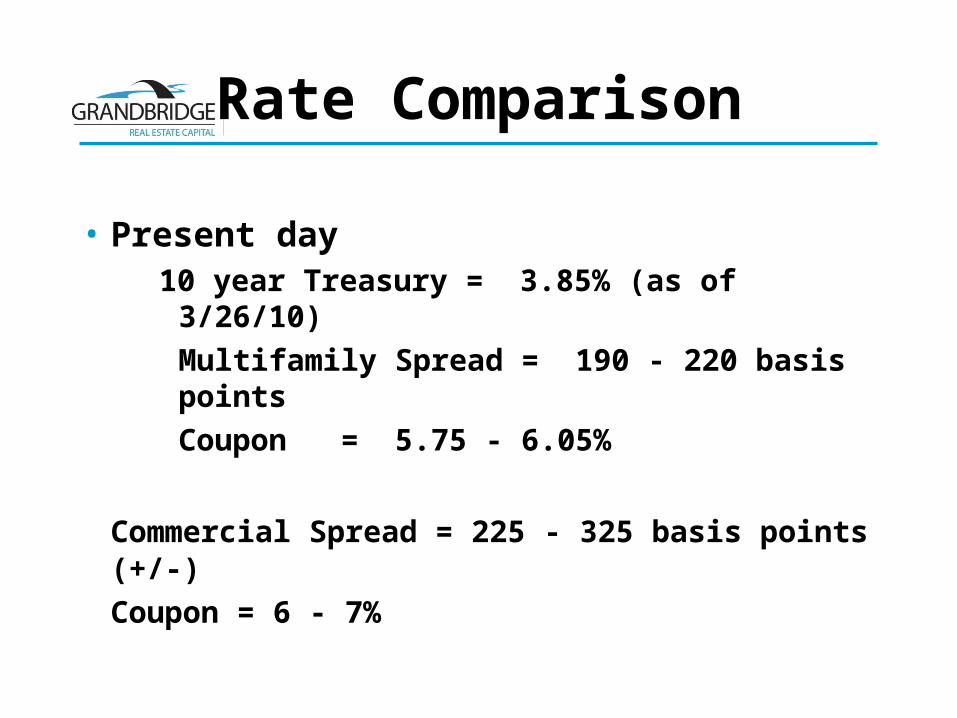

Rate Comparison

• Present day10 year Treasury = 3.85% (as of 3/26/10)Multifamily Spread = 190 - 220 basis points

Coupon = 5.75 - 6.05%

Commercial Spread = 225 - 325 basis points (+/-)

Coupon = 6 - 7%

Rate Comparison

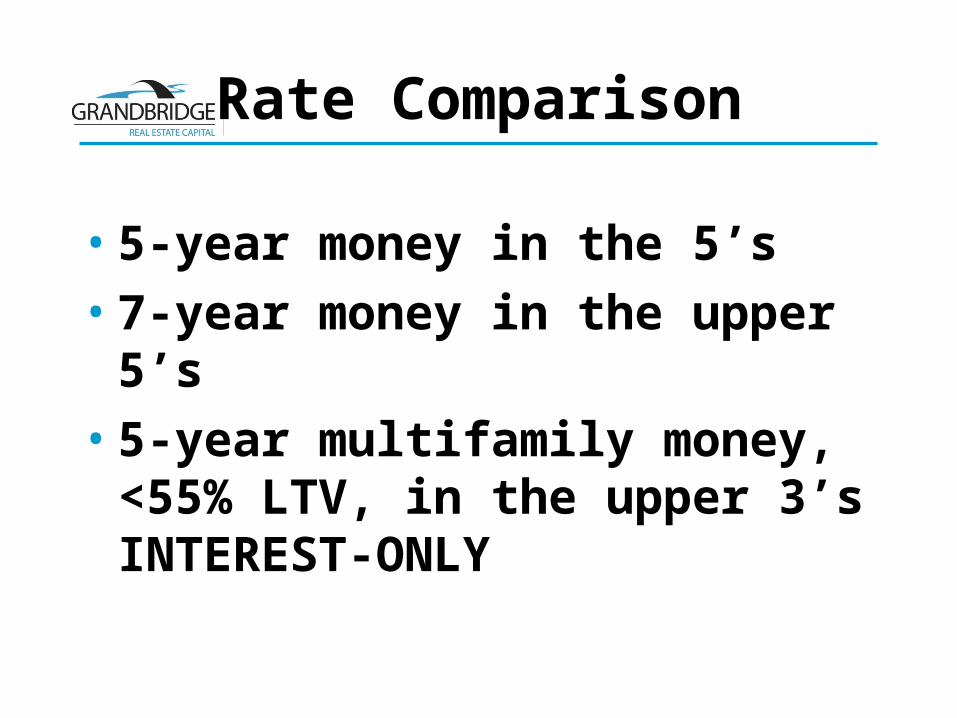

•5-year money in the 5’s•7-year money in the upper

5’s•5-year multifamily money,

<55% LTV, in the upper 3’s INTEREST-ONLY

Conclusions

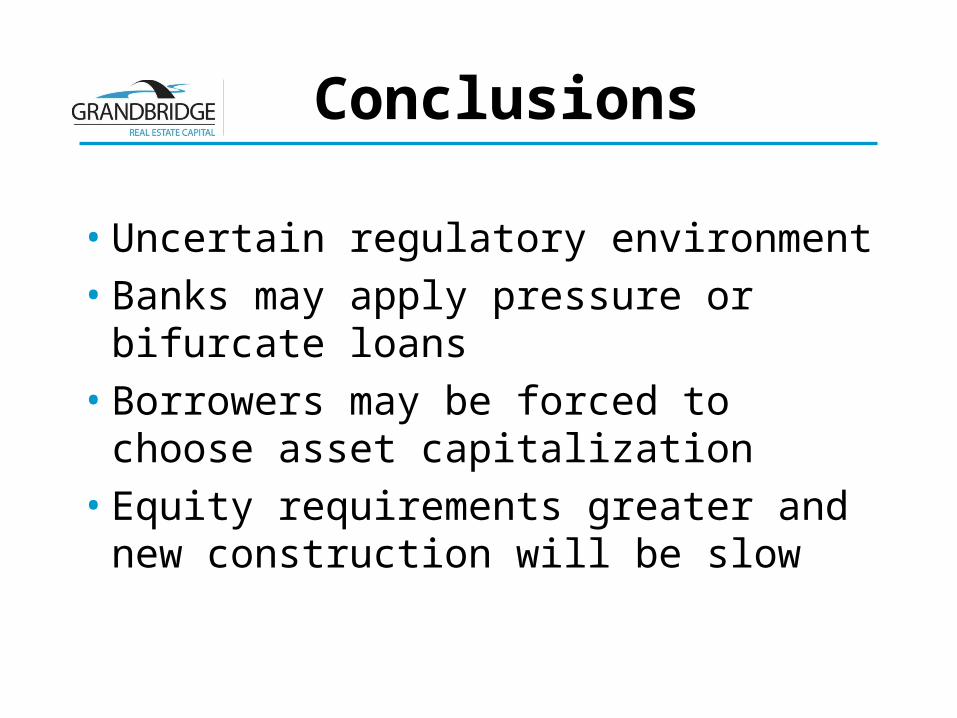

• Uncertain regulatory environment• Banks may apply pressure or

bifurcate loans• Borrowers may be forced to

choose asset capitalization• Equity requirements greater and

new construction will be slow

Conclusions

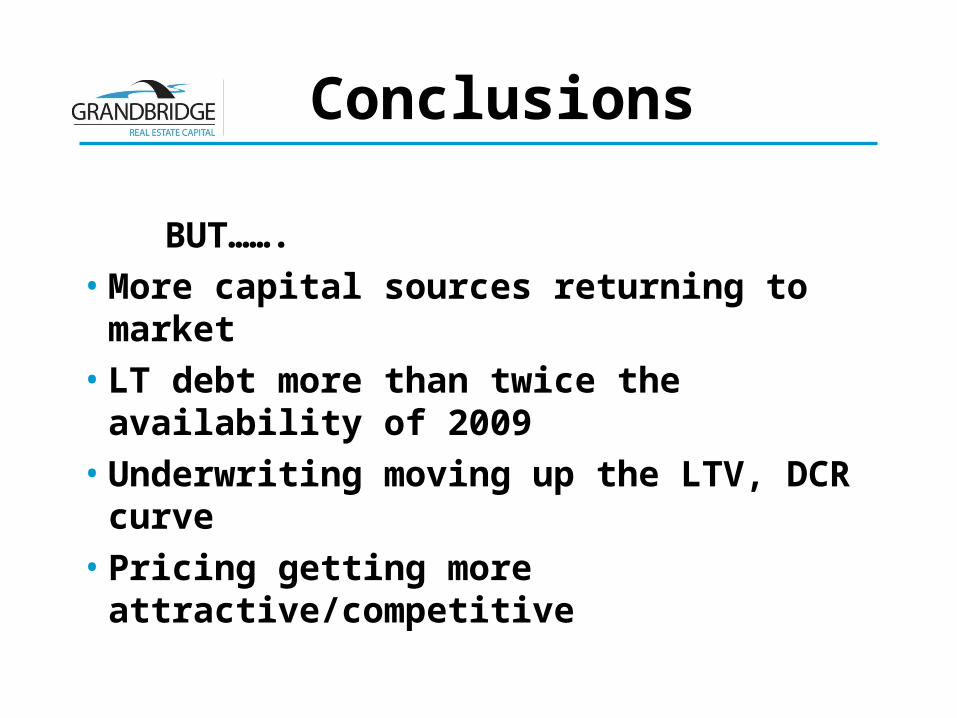

BUT…….•More capital sources returning to

market•LT debt more than twice the

availability of 2009•Underwriting moving up the LTV,

DCR curve•Pricing getting more

attractive/competitive

201?