1

Luis Enrique Berrizbeitia Executive Vice President

Conference on Energy in South America

The Center for Latin American Issues

George Washington University

March 2002

Economic development in Latin America:a brief comment why growth and development have not been sustainable

updating the development model the importance of integration for competitiveness.

Prospects for energy market integration in Latin America potential benefits relevant issues progress toward energy market integration

Contents

2

Reforms have been mainly focused on macroeconomics, not enough on microeconomics

Continued dependence on natural resources and external savings

excessive vulnerability to external shocks

Growth has not been sustained nor sufficient, and income distribution remains very inequitable

Not enough attention has been paid to social and environmental issues

Weak institutions

Why growth and development have not been sustainable in Latin America

3

The evolving development model

Necessary to preserve and improve on the progress achieved though macroeconomic and structural reforms, but also to focus increasingly on the microeconomic aspects of development

achieve a better balance between the economic basis of development, and its social, environmental and institutional dimensions

attain higher levels of sustained growth and development

improve income distribution reduce poverty

4

Focusing on the micro-dimensions of development

Greater productivity and competitiveness infrastructure ICTs SMEs

Increase investment in human capital education pension reform

Protection, promotion and development of environmental resources

mitigation of environmental risks development of sustainable “green markets”

Institutional development improve the quality and efficiency of response to social needs strengthen the mechanisms of democratic governance improve economic and social management

physical & economic integration domestic savings globalization

public health services unemployment coverage

5

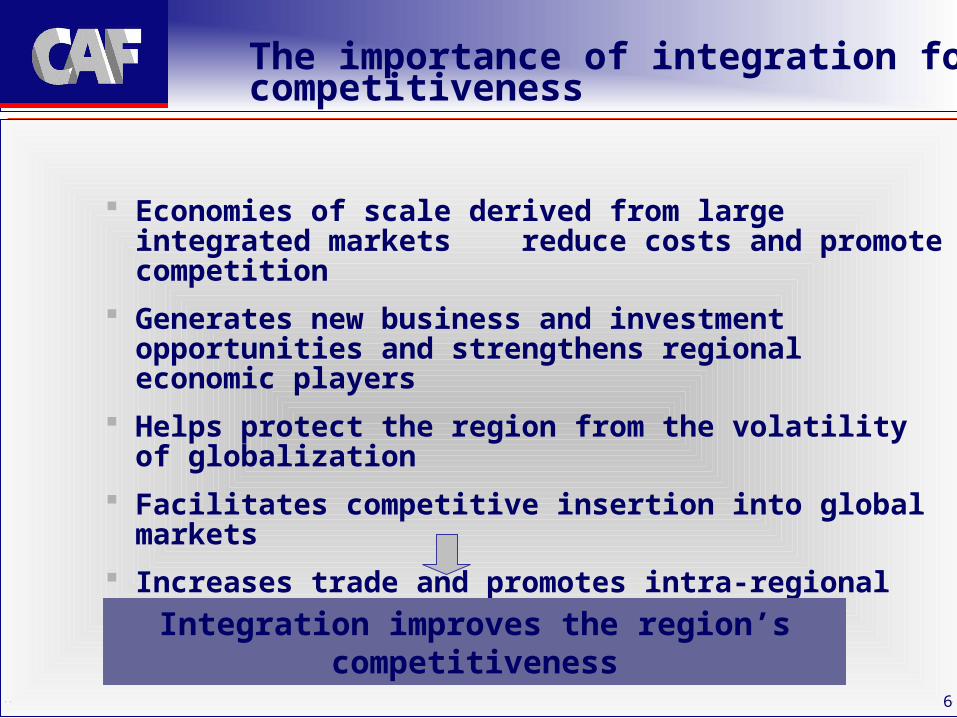

The importance of integration for competitiveness

Economies of scale derived from large integrated markets reduce costs and promote competition

Generates new business and investment opportunities and strengthens regional economic players

Helps protect the region from the volatility of globalization

Facilitates competitive insertion into global markets

Increases trade and promotes intra-regional development of technology and service sectors

Integration improves the region’s competitiveness

6

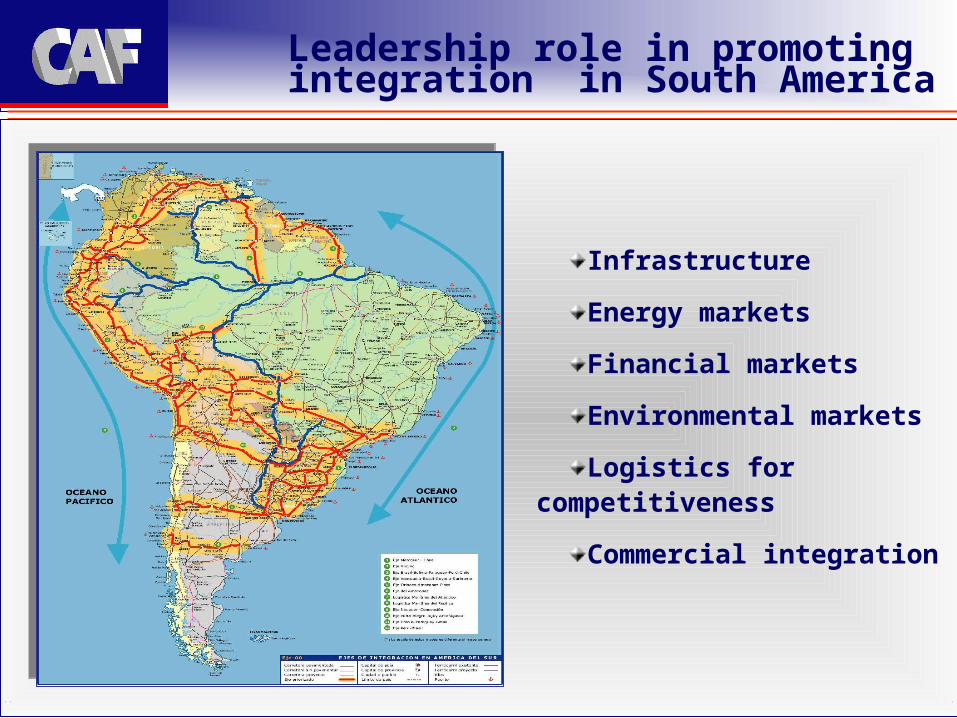

Leadership role in promoting integration in South America

Infrastructure

Energy markets

Financial markets

Environmental markets

Logistics for competitiveness

Commercial integration

Benefits of energy market integration

Contributes to optimize the use of existing hydro/thermal capacity

compensates for variations in hydrological and climatic cyclestakes advantage of differing demand patterns across time zones

Contributes to compensate for large differences in energy resource endowment

promotes increased intra-regional trade in energy

Improves the region’s overall competitiveness lowers costs and promotes competition in energy generation improves the quality and reliability of electric power services

8

Creates new opportunities for intra-regional technological development and trade in energy services

Helps drive the integration of natural gas markets

Generates measurable environmental benefits

can improve r.o.i. through “Kyoto” mechanisms (cdm)

Benefits of energy market integration

9

Greater homogeneity of energy policies across countries

regional vs. national policy orientation market driven vs. planning orientation private vs. public sector roles adequate investment climate regulatory compatibility

Harmonization of regulatory criteria separation of generation/transmission/distribution transparent pricing mechanisms based on LTMC,

including transmission costs and pricing transparent and direct subsidies where needed joint or harmonized power and gas market regulation

Relevant issue for energy market integration in Latin America

10

Use existing fora to intensify exchanges among key players, including the private sector:

potential and benefits of market-based integration harmonization of policies and regulations fora include: OLADE/CIER/CAF/CAN/MERCOSUR/

IIRSA/FTAA

Build upon existing infrastructure to evolve from opportunity exchanges to market integration

more intensive use of existing interconnections binational hydroelectric dams (Itaipú, Yaciretá,

Salto Grande)

Aim toward firm policy commitments and specific but realistic objectives

11

Progress toward energy market integration in Latin America

12

Existing interconnections in South America

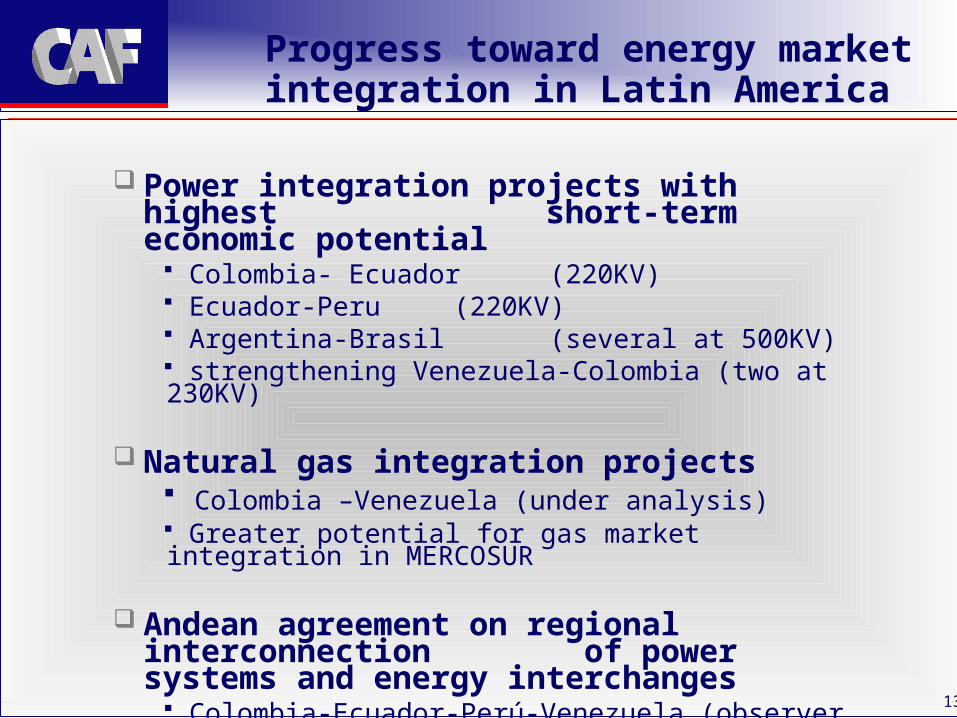

Power integration projects with highest short-term economic potential

Colombia- Ecuador (220KV) Ecuador-Peru (220KV) Argentina-Brasil (several at 500KV) strengthening Venezuela-Colombia (two at 230KV)

Natural gas integration projects Colombia –Venezuela (under analysis) Greater potential for gas market integration in MERCOSUR

Andean agreement on regional interconnection of power systems and energy interchanges

Colombia-Ecuador-Perú-Venezuela (observer status) Bilateral agreement: MEM (Ven.) - Termotasajero (Col.)

13

Progress toward energy market integration in Latin America

CAF and the energy sector (at Dec. 31, 2001)

• Total portfolio: $ 6.5 billion• Infrastructure portfolio: $ 4.3 billion• Energy portfolio: $ 1.2 billion• Electricity portfolio: $ 1.0 billion• Approvals, electricity projects: $ 1,4 billion • Number of electricity projects: 27

CAF is currently well positioned to play a catalytic role in promoting energy market integration in South America, on account of its mandate, its strong regional position, its leadership role in IIRSA, its partnership with CIER and OLADE and its close relations with regional authorities.

14

15

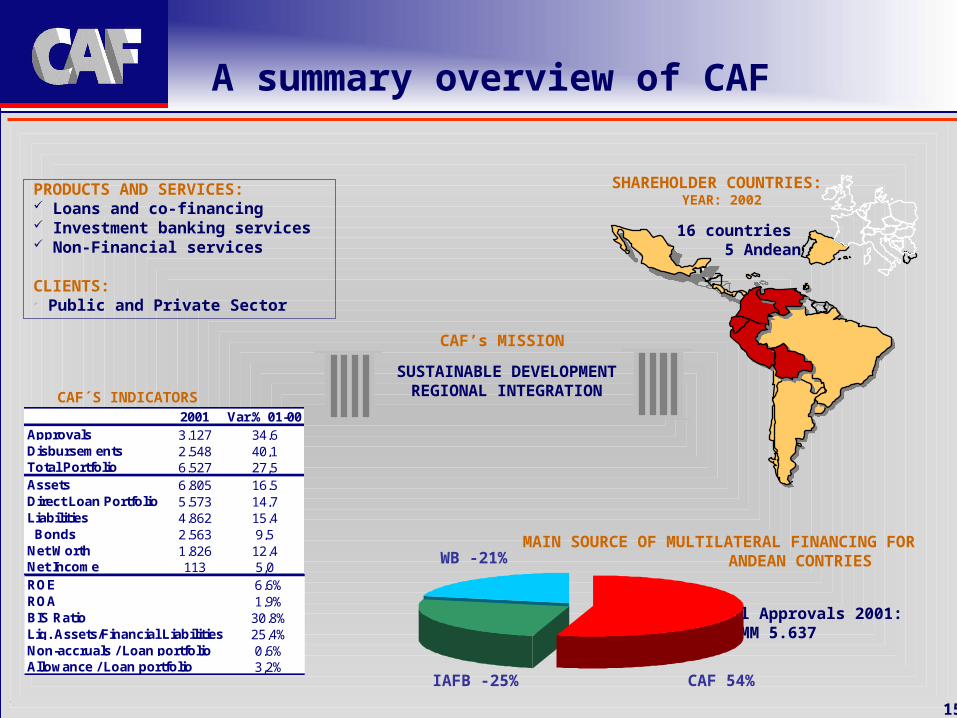

A summary overview of CAF

PRODUCTS AND SERVICES: Loans and co-financing Investment banking services Non-Financial services

CLIENTS: Public and Private Sector

CAF´S INDICATORS

16 countries 5 Andean

SHAREHOLDER COUNTRIES: YEAR: 2002

Total Approvals 2001: US$ MM 5.637

SUSTAINABLE DEVELOPMENT REGIONAL INTEGRATION

CAF’s MISSION

MAIN SOURCE OF MULTILATERAL FINANCING FOR ANDEAN CONTRIES

2001 Var.% 01-00Approvals 3.127 34,6Disbursements 2.548 40,1Total Portfolio 6.527 27,5Assets 6.805 16,5Direct Loan Portfolio 5.573 14,7Liabilities 4.862 15,4 Bonds 2.563 9,5Net Worth 1.826 12,4Net Income 113 5,0ROE 6,6%ROA 1,9%BIS Ratio 30,8%Liq. Assets/Financial Liabilities 25,4%Non-accruals / Loan portfolio 0,6%Allowance / Loan portfolio 3,2%

WB -21%

IAFB -25% CAF 54%

16

Corporación Andina de FomentoCorporación Andina de Fomento

www.caf.comwww.caf.com

/marzo2002

Recommended