© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

15-1

GLOBAL BUSINESS AND ACCOUNTING

Chapter

15

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

15-2

GlobalizationGlobalization

Occurs as managers become aware of an engage in cross-border trade and operations. A high level of globalization is a multinational enterprise that

begins with raw material extraction and ends with final product assembly and sales in multiple foreign

locations.

Occurs as managers become aware of an engage in cross-border trade and operations. A high level of globalization is a multinational enterprise that

begins with raw material extraction and ends with final product assembly and sales in multiple foreign

locations.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

15-3

GlobalizationGlobalization

Typically progresses through a series of stages that include:

1. Exporting,

2. Licensing,

3. Joint ventures,

4. Wholly owned subsidiaries, and

5. Global sourcing.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

15-4

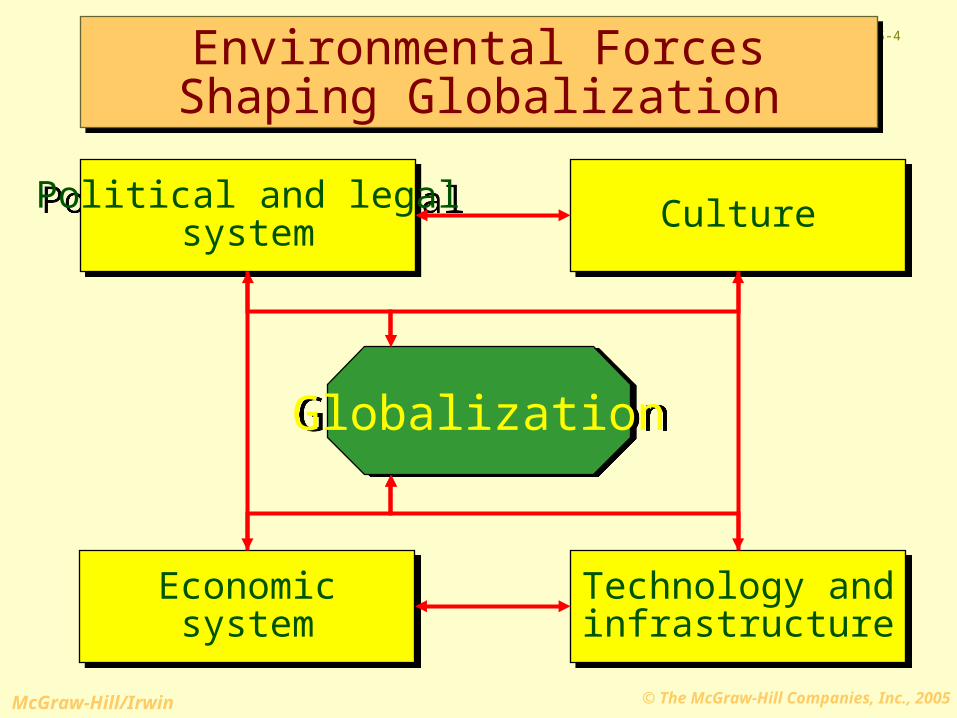

Environmental Forces Shaping Globalization

Environmental Forces Shaping Globalization

GlobalizationGlobalization

Political and legalsystem

Political and legalsystem

Economicsystem

Economicsystem

CultureCulture

Technology andinfrastructure

Technology andinfrastructure

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

15-5

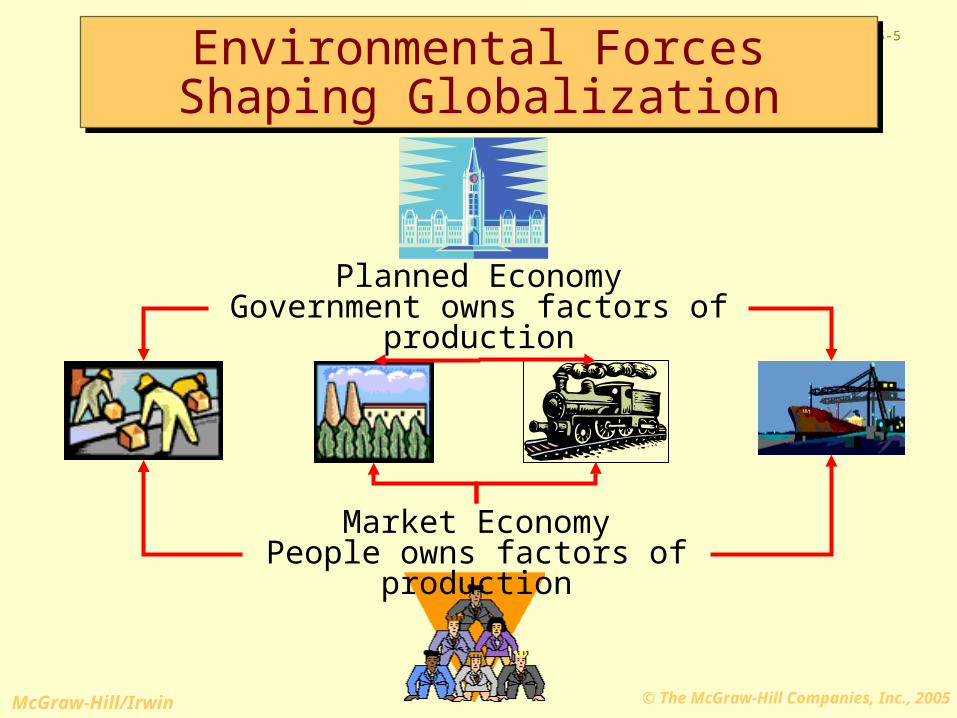

Environmental Forces Shaping Globalization

Environmental Forces Shaping Globalization

Planned EconomyGovernment owns factors of production

Market EconomyPeople owns factors of production

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

15-6

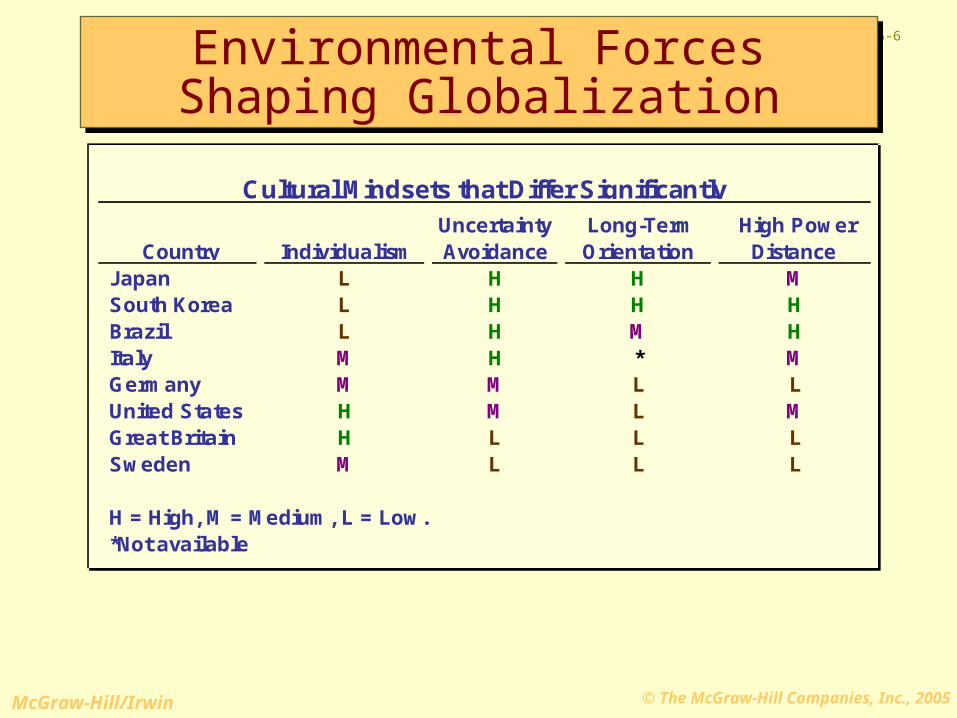

Environmental Forces Shaping Globalization

Environmental Forces Shaping Globalization

Country Individualism

Uncertainty Avoidance

Long-Term Orientation

High Power Distance

Japan L H H MSouth Korea L H H HBrazil L H M HItaly M H * MGermany M M L LUnited States H M L MGreat Britain H L L LSweden M L L L

H = High, M = Medium, L = Low.*Not available

Cultural Mindsets that Differ Significantly

Country Individualism

Uncertainty Avoidance

Long-Term Orientation

High Power Distance

Japan L H H MSouth Korea L H H HBrazil L H M HItaly M H * MGermany M M L LUnited States H M L MGreat Britain H L L LSweden M L L L

H = High, M = Medium, L = Low.*Not available

Cultural Mindsets that Differ Significantly

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

15-7

Harmonization of Financial Reporting Standards

Harmonization of Financial Reporting Standards

The International Accounting Standards Board (IASB) has as one of its stated goals the harmonization of accounting standards.

Harmonization is used to describe the standardization of accounting methods and

principles used in different countries throughout the world.

The International Accounting Standards Board (IASB) has as one of its stated goals the harmonization of accounting standards.

Harmonization is used to describe the standardization of accounting methods and

principles used in different countries throughout the world.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

15-8

Harmonization of Financial Reporting Standards

Harmonization of Financial Reporting Standards

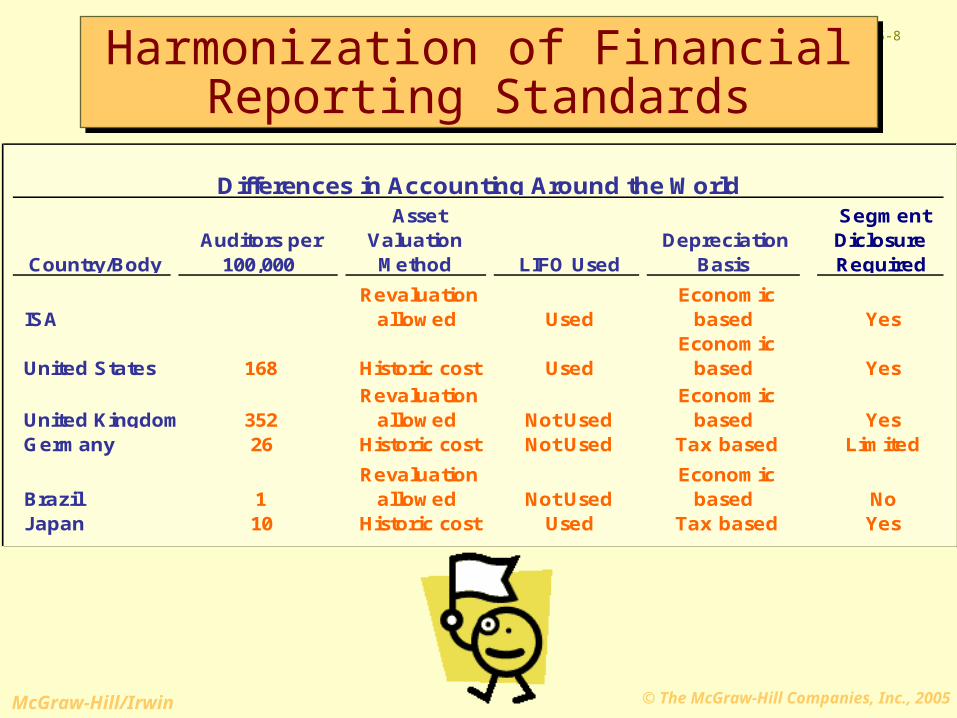

Country/Body Auditors per

100,000

Asset Valuation Method LIFO Used

Depreciation Basis

Segment Diclosure Required

ISA Revaluation

allowed Used Economic

based Yes

United States 168 Historic cost Used Economic

based Yes

United Kingdom 352 Revaluation

allowed Not Used Economic

based Yes Germany 26 Historic cost Not Used Tax based Limited

Brazil 1 Revaluation

allowed Not Used Economic

based No Japan 10 Historic cost Used Tax based Yes

Differences in Accounting Around the World

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

15-9

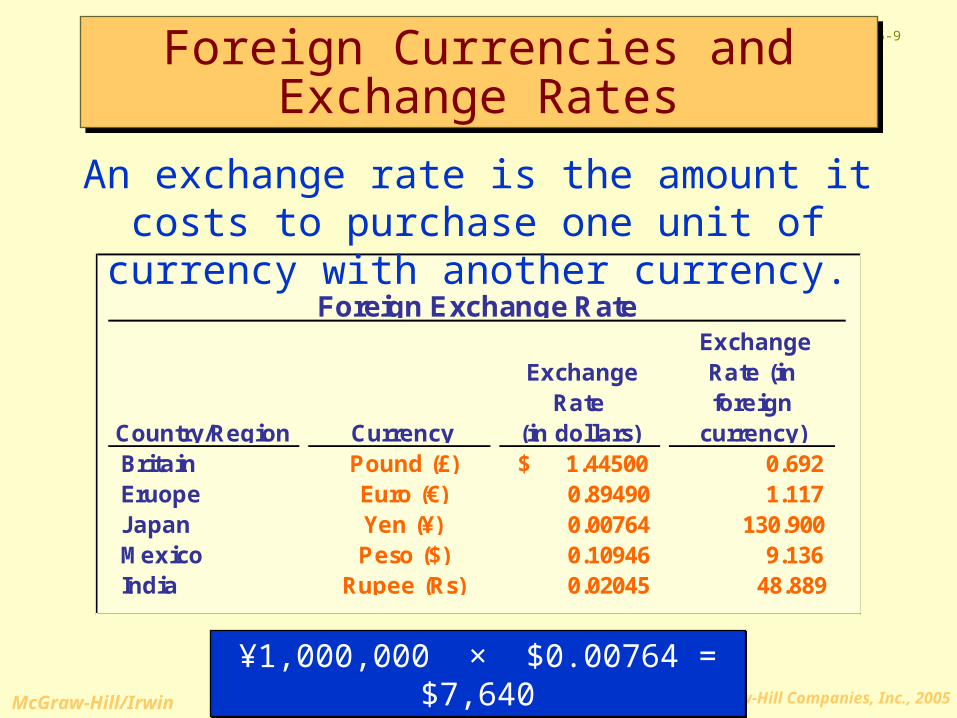

Foreign Currencies and Exchange RatesForeign Currencies and Exchange Rates

Country/Region Currency

Exchange Rate

(in dollars)

Exchange Rate (in foreign

currency) Britain Pound (£) $ 1.44500 0.692 Eruope Euro (€) 0.89490 1.117 Japan Yen (¥) 0.00764 130.900 Mexico Peso ($) 0.10946 9.136 India Rupee (Rs) 0.02045 48.889

Foreign Exchange Rate

An exchange rate is the amount it costs to purchase one unit of currency with another currency.

¥1,000,000 × $0.00764 = $7,640¥1,000,000 × $0.00764 = $7,640

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

15-10

Accounting for Transactions with Foreign Companies

Accounting for Transactions with Foreign Companies

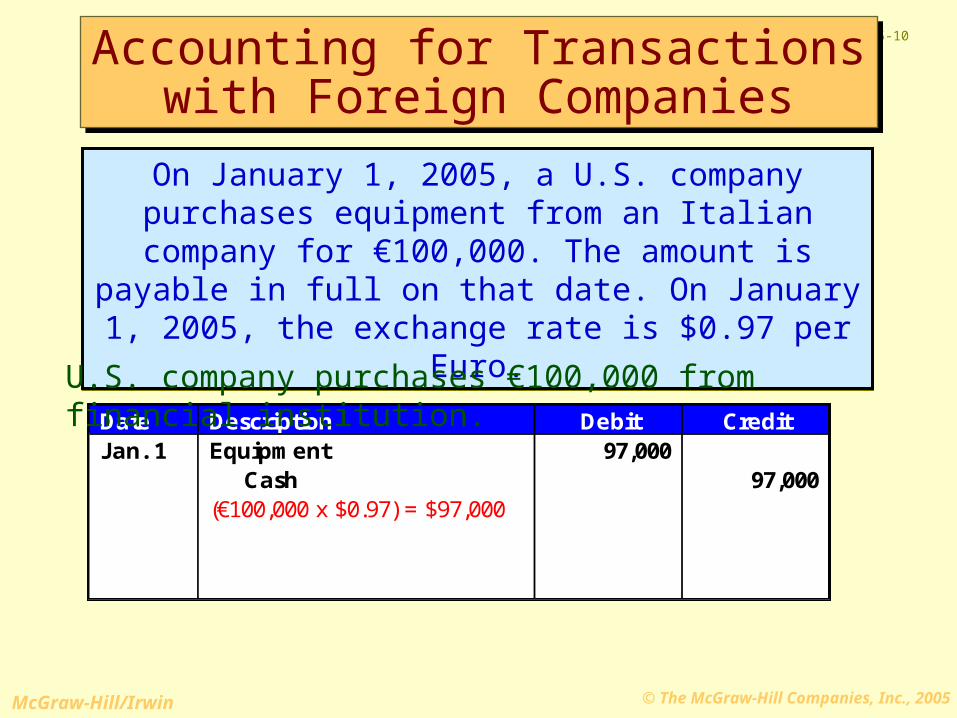

On January 1, 2005, a U.S. company purchases equipment from an Italian company for €100,000. The amount is payable in full on that date. On January 1,

2005, the exchange rate is $0.97 per Euro.

On January 1, 2005, a U.S. company purchases equipment from an Italian company for €100,000. The amount is payable in full on that date. On January 1,

2005, the exchange rate is $0.97 per Euro.

Date Description Debit CreditJan. 1 Equipment 97,000

Cash 97,000 (€100,000 x $0.97) = $97,000

U.S. company purchases €100,000 from financial institution.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

15-11

Accounting for Transactions with Foreign Companies

Accounting for Transactions with Foreign Companies

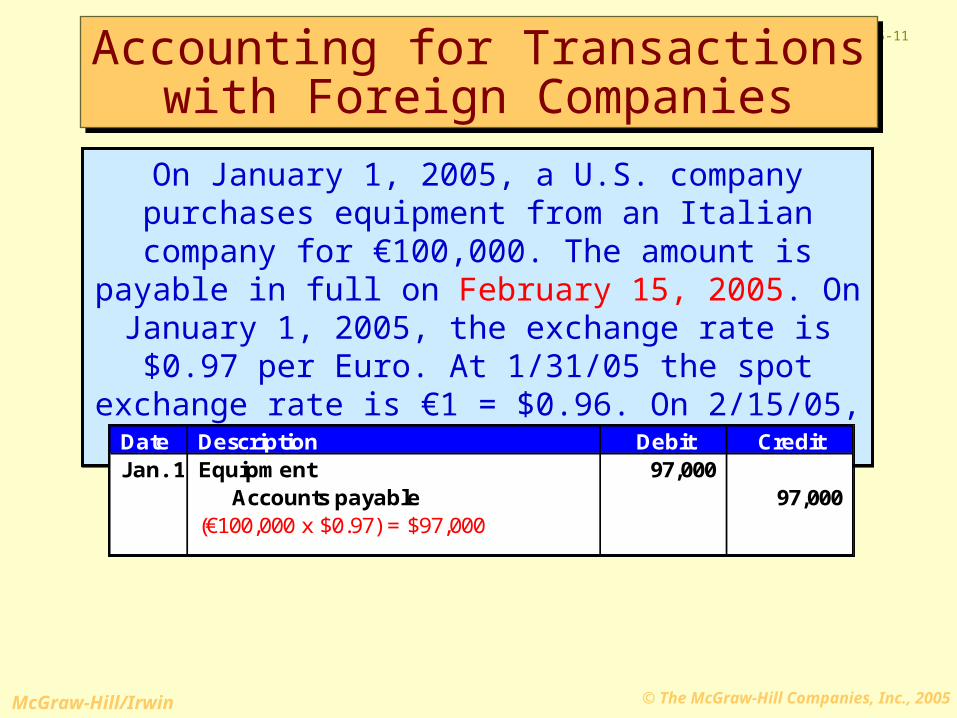

On January 1, 2005, a U.S. company purchases equipment from an Italian company for €100,000. The

amount is payable in full on February 15, 2005. On January 1, 2005, the exchange rate is $0.97 per Euro. At 1/31/05 the spot exchange rate is €1 = $0.96. On

2/15/05, the exchange rate is €1 = $0.98.

On January 1, 2005, a U.S. company purchases equipment from an Italian company for €100,000. The

amount is payable in full on February 15, 2005. On January 1, 2005, the exchange rate is $0.97 per Euro. At 1/31/05 the spot exchange rate is €1 = $0.96. On

2/15/05, the exchange rate is €1 = $0.98.

Date Description Debit CreditJan. 1 Equipment 97,000

Accounts payable 97,000 (€100,000 x $0.97) = $97,000

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

15-12

Accounting for Transactions with Foreign Companies

Accounting for Transactions with Foreign Companies

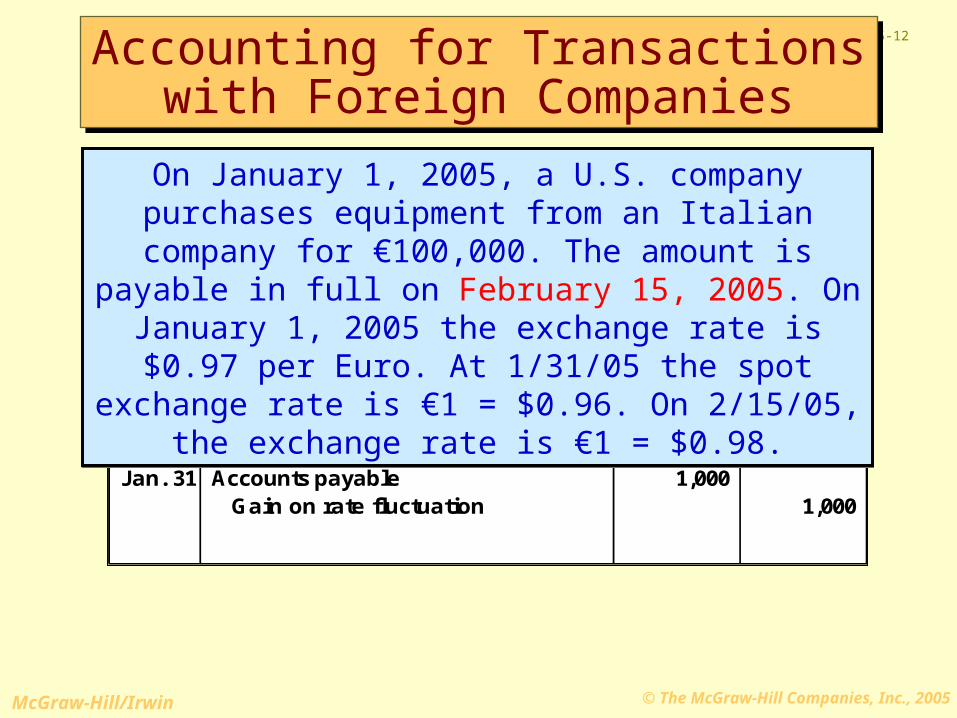

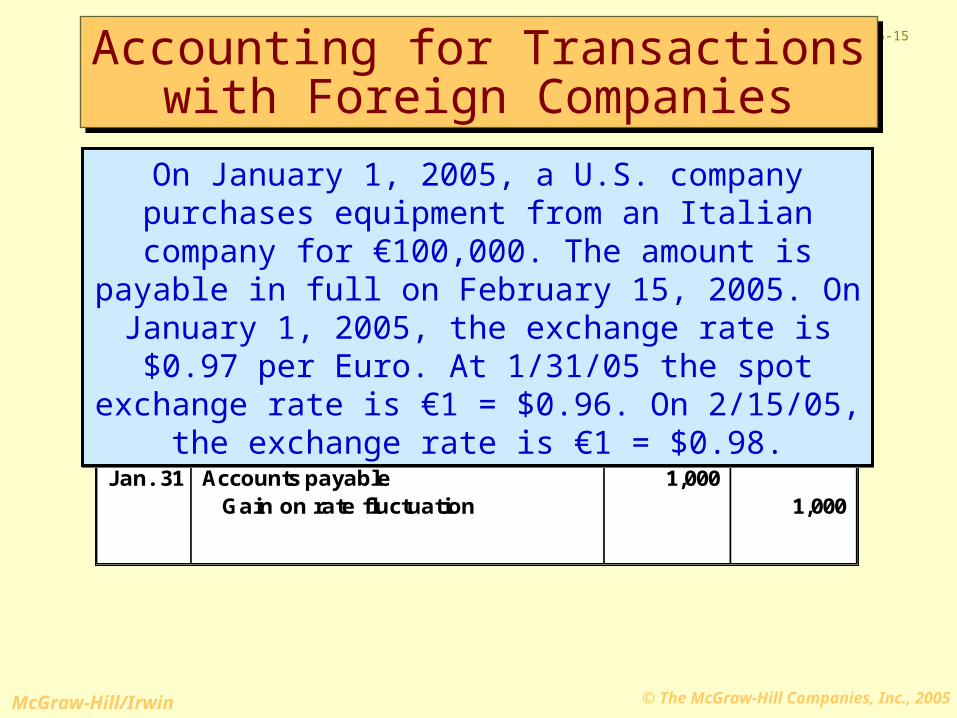

Date Description Debit CreditJan. 31 Accounts payable 1,000

Gain on rate fluctuation 1,000

On January 1, 2005, a U.S. company purchases equipment from an Italian company for €100,000. The

amount is payable in full on February 15, 2005. On January 1, 2005 the exchange rate is $0.97 per Euro. At 1/31/05 the spot exchange rate is €1 = $0.96. On

2/15/05, the exchange rate is €1 = $0.98.

On January 1, 2005, a U.S. company purchases equipment from an Italian company for €100,000. The

amount is payable in full on February 15, 2005. On January 1, 2005 the exchange rate is $0.97 per Euro. At 1/31/05 the spot exchange rate is €1 = $0.96. On

2/15/05, the exchange rate is €1 = $0.98.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

15-13

Accounting for Transactions with Foreign Companies

Accounting for Transactions with Foreign Companies

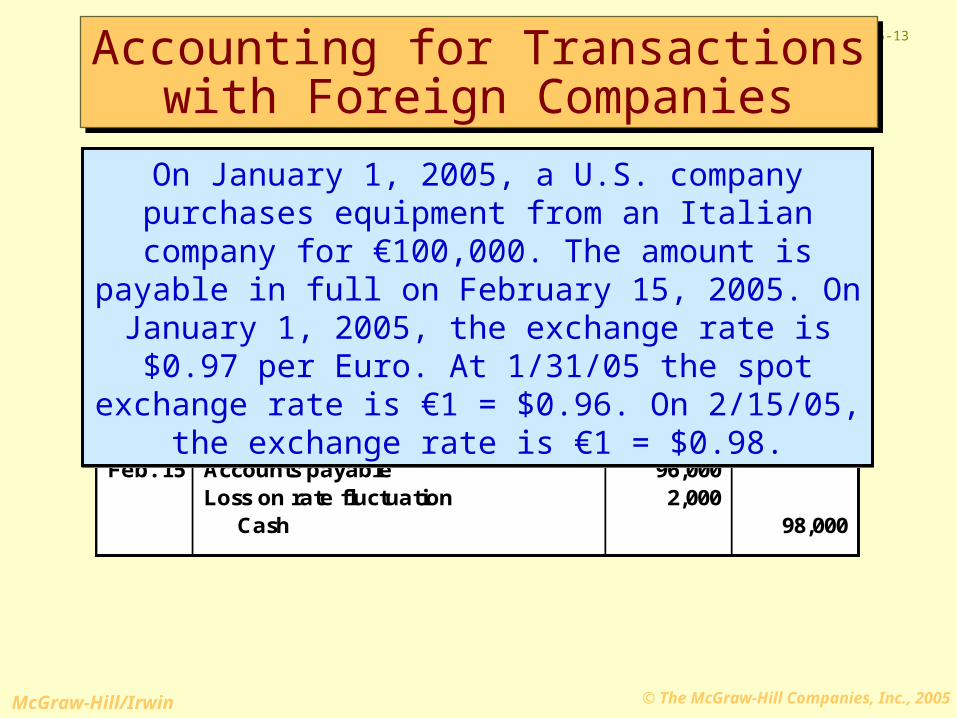

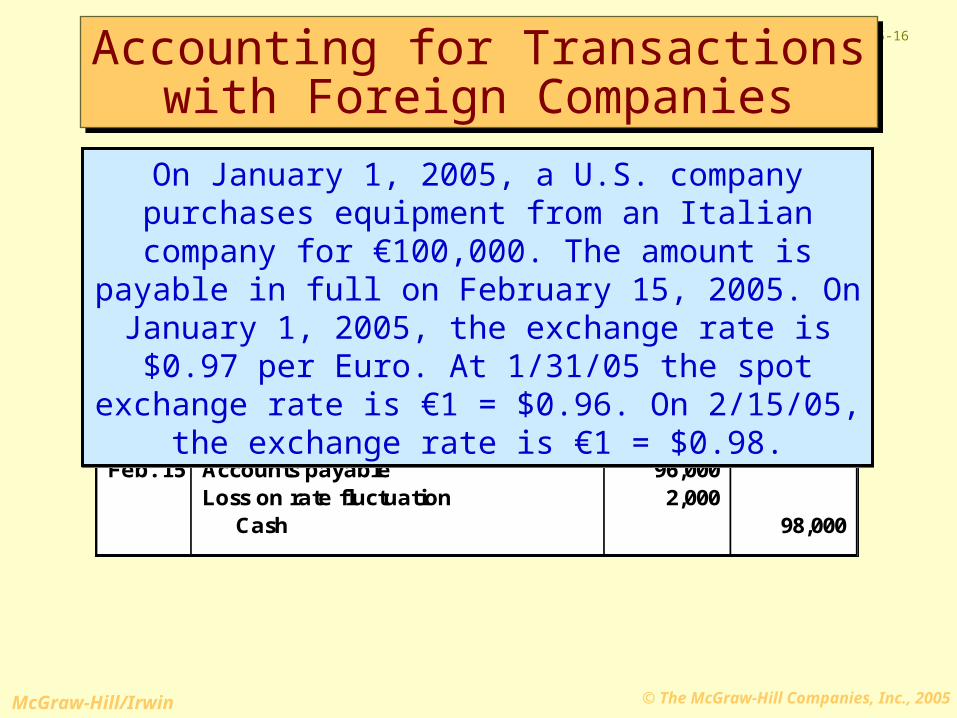

Date Description Debit CreditFeb. 15 Accounts payable 96,000

Loss on rate fluctuation 2,000 Cash 98,000

On January 1, 2005, a U.S. company purchases equipment from an Italian company for €100,000. The

amount is payable in full on February 15, 2005. On January 1, 2005, the exchange rate is $0.97 per Euro. At 1/31/05 the spot exchange rate is €1 = $0.96. On

2/15/05, the exchange rate is €1 = $0.98.

On January 1, 2005, a U.S. company purchases equipment from an Italian company for €100,000. The

amount is payable in full on February 15, 2005. On January 1, 2005, the exchange rate is $0.97 per Euro. At 1/31/05 the spot exchange rate is €1 = $0.96. On

2/15/05, the exchange rate is €1 = $0.98.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

15-14

Accounting for Transactions with Foreign Companies

Accounting for Transactions with Foreign Companies

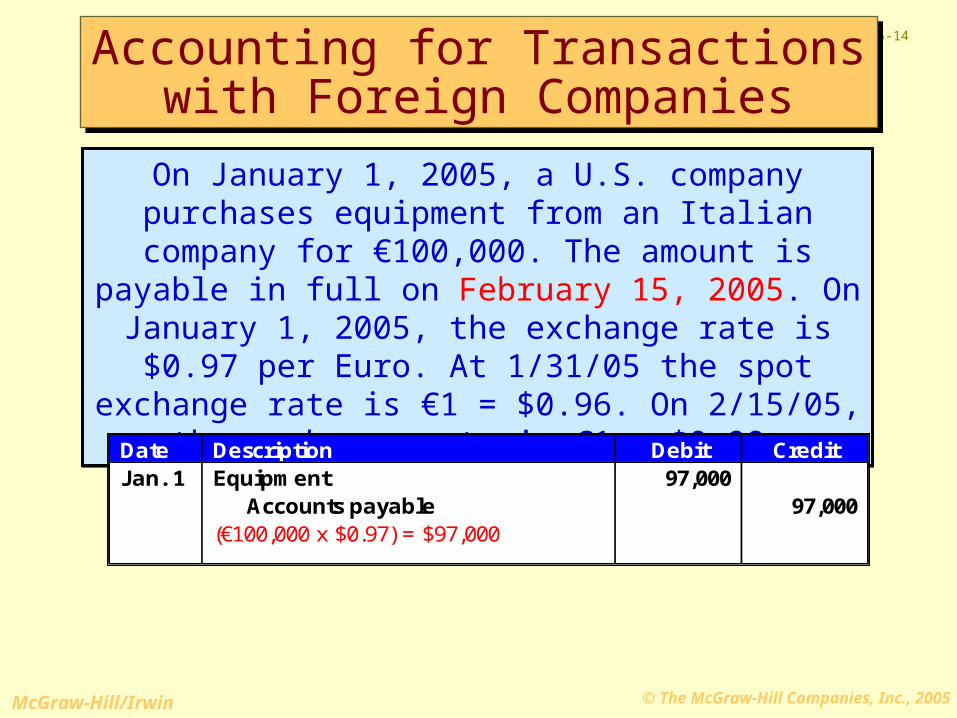

On January 1, 2005, a U.S. company purchases equipment from an Italian company for €100,000. The

amount is payable in full on February 15, 2005. On January 1, 2005, the exchange rate is $0.97 per Euro. At 1/31/05 the spot exchange rate is €1 = $0.96. On

2/15/05, the exchange rate is €1 = $0.98.

On January 1, 2005, a U.S. company purchases equipment from an Italian company for €100,000. The

amount is payable in full on February 15, 2005. On January 1, 2005, the exchange rate is $0.97 per Euro. At 1/31/05 the spot exchange rate is €1 = $0.96. On

2/15/05, the exchange rate is €1 = $0.98.

Date Description Debit CreditJan. 1 Equipment 97,000

Accounts payable 97,000 (€100,000 x $0.97) = $97,000

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

15-15

Accounting for Transactions with Foreign Companies

Accounting for Transactions with Foreign Companies

Date Description Debit CreditJan. 31 Accounts payable 1,000

Gain on rate fluctuation 1,000

On January 1, 2005, a U.S. company purchases equipment from an Italian company for €100,000. The

amount is payable in full on February 15, 2005. On January 1, 2005, the exchange rate is $0.97 per Euro. At 1/31/05 the spot exchange rate is €1 = $0.96. On

2/15/05, the exchange rate is €1 = $0.98.

On January 1, 2005, a U.S. company purchases equipment from an Italian company for €100,000. The

amount is payable in full on February 15, 2005. On January 1, 2005, the exchange rate is $0.97 per Euro. At 1/31/05 the spot exchange rate is €1 = $0.96. On

2/15/05, the exchange rate is €1 = $0.98.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

15-16

Accounting for Transactions with Foreign Companies

Accounting for Transactions with Foreign Companies

Date Description Debit CreditFeb. 15 Accounts payable 96,000

Loss on rate fluctuation 2,000 Cash 98,000

On January 1, 2005, a U.S. company purchases equipment from an Italian company for €100,000. The

amount is payable in full on February 15, 2005. On January 1, 2005, the exchange rate is $0.97 per Euro. At 1/31/05 the spot exchange rate is €1 = $0.96. On

2/15/05, the exchange rate is €1 = $0.98.

On January 1, 2005, a U.S. company purchases equipment from an Italian company for €100,000. The

amount is payable in full on February 15, 2005. On January 1, 2005, the exchange rate is $0.97 per Euro. At 1/31/05 the spot exchange rate is €1 = $0.96. On

2/15/05, the exchange rate is €1 = $0.98.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

15-17

HedgeHedge

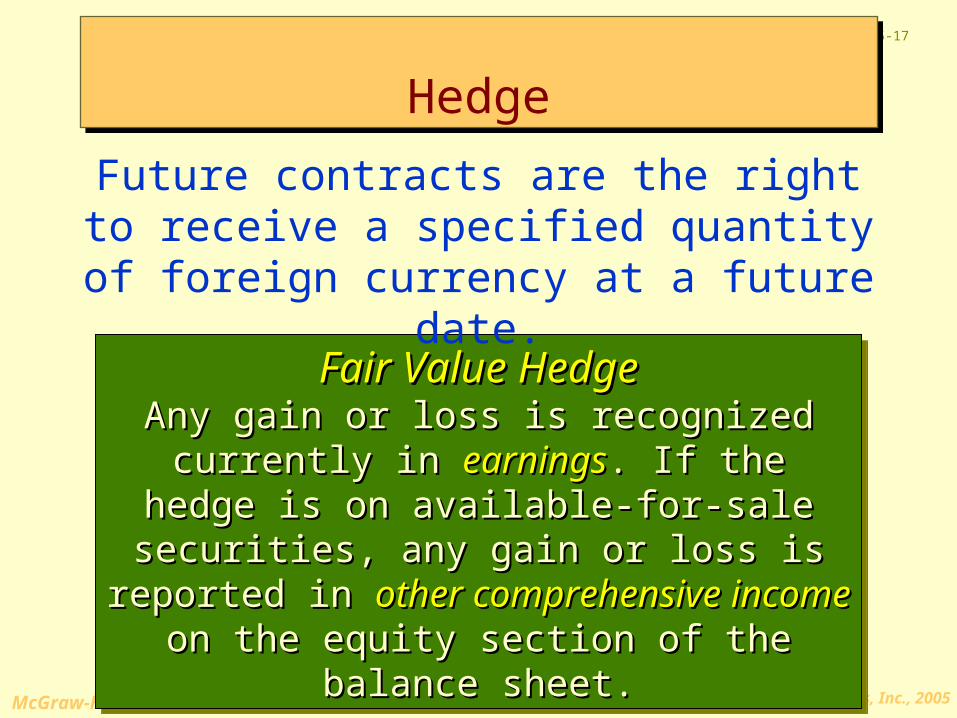

Fair Value HedgeFair Value HedgeAny gain or loss is recognized currently in Any gain or loss is recognized currently in

earningsearnings. If the hedge is on available-for-sale . If the hedge is on available-for-sale securities, any gain or loss is reported in securities, any gain or loss is reported in

other comprehensive incomeother comprehensive income on the equity on the equity section of the balance sheet.section of the balance sheet.

Fair Value HedgeFair Value HedgeAny gain or loss is recognized currently in Any gain or loss is recognized currently in

earningsearnings. If the hedge is on available-for-sale . If the hedge is on available-for-sale securities, any gain or loss is reported in securities, any gain or loss is reported in

other comprehensive incomeother comprehensive income on the equity on the equity section of the balance sheet.section of the balance sheet.

Future contracts are the right to receive a specified quantity of foreign currency at a

future date.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

15-18

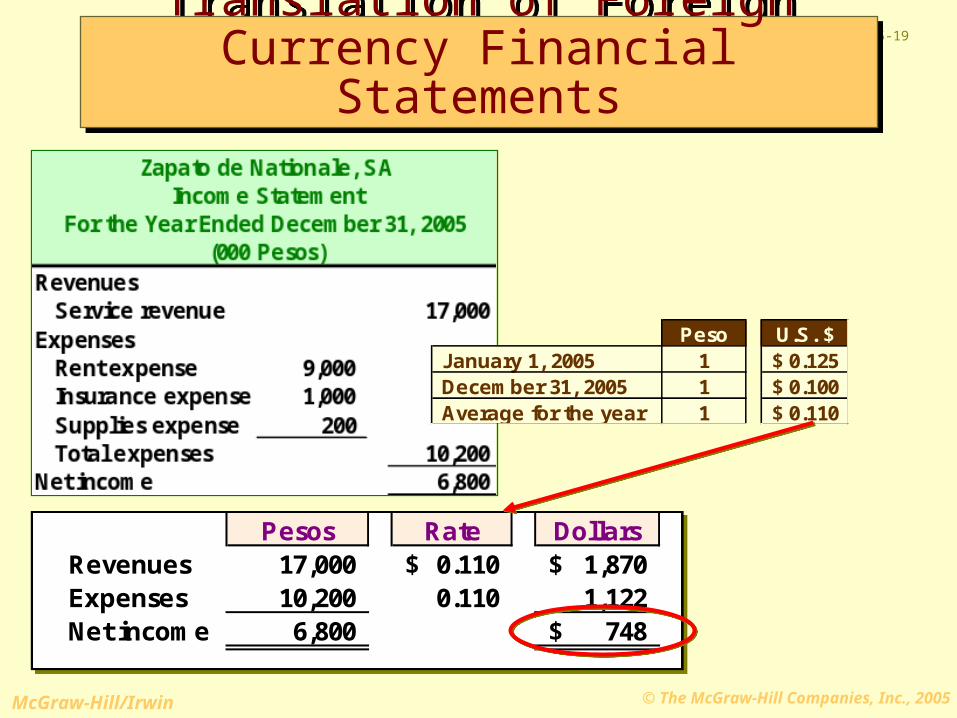

Translation of Foreign Currency Financial Statements

Translation of Foreign Currency Financial Statements

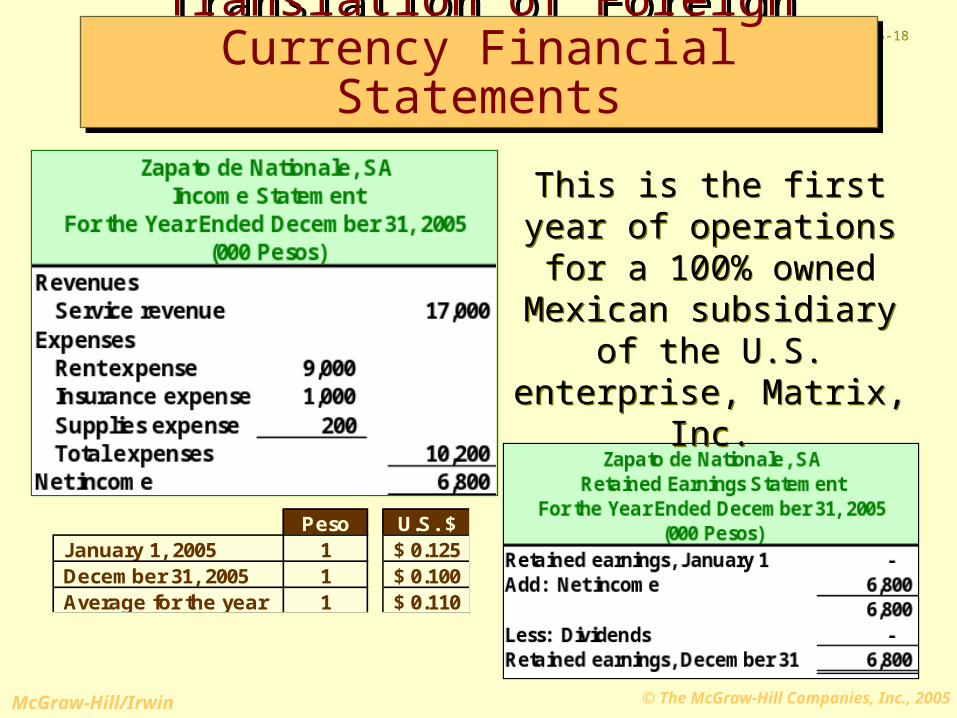

Peso U.S. $January 1, 2005 1 0.125$ December 31, 2005 1 0.100$ Average for the year 1 0.110$

This is the first year of operations for a 100%

owned Mexican subsidiary of the U.S. enterprise, Matrix, Inc.

This is the first year of operations for a 100%

owned Mexican subsidiary of the U.S. enterprise, Matrix, Inc.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

15-19

Translation of Foreign Currency Financial Statements

Translation of Foreign Currency Financial Statements

Pesos Rate DollarsRevenues 17,000 0.110$ 1,870$ Expenses 10,200 0.110 1,122 Net income 6,800 748$

Pesos Rate DollarsRevenues 17,000 0.110$ 1,870$ Expenses 10,200 0.110 1,122 Net income 6,800 748$

Peso U.S. $January 1, 2005 1 0.125$ December 31, 2005 1 0.100$ Average for the year 1 0.110$

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

15-20

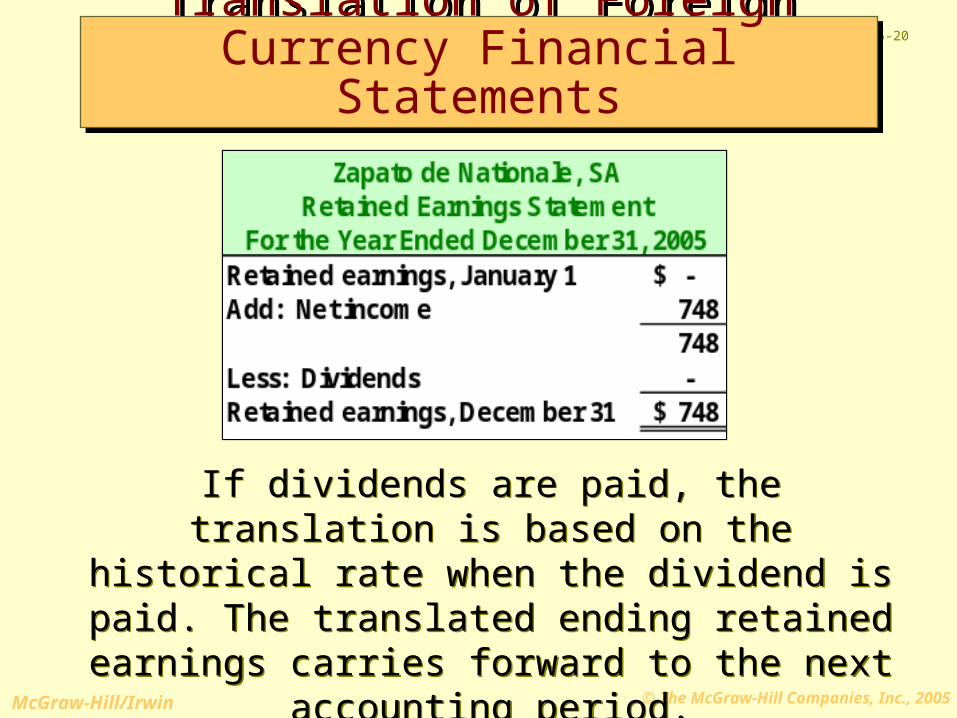

Translation of Foreign Currency Financial Statements

Translation of Foreign Currency Financial Statements

If dividends are paid, the translation is based on the historical rate when the dividend is paid. The

translated ending retained earnings carries forward to the next accounting period.

If dividends are paid, the translation is based on the historical rate when the dividend is paid. The

translated ending retained earnings carries forward to the next accounting period.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

15-21

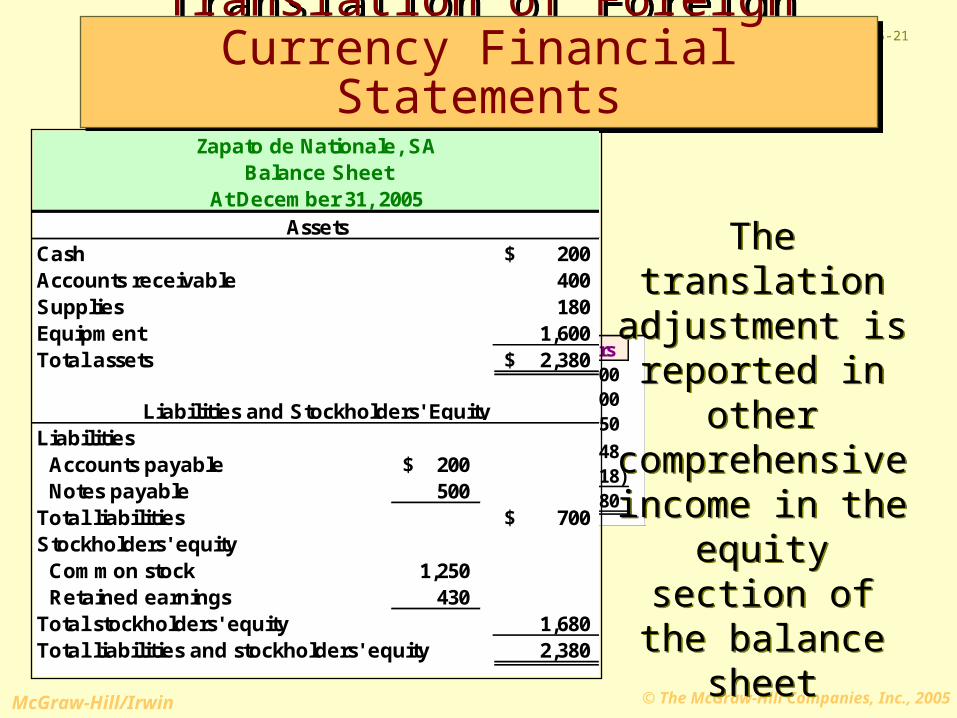

Pesos Rate DollarsCash 2,000 0.100$ 200$ Receivables 4,000 0.100 400 Inventory 1,800 0.100 180

Equipment 16,000 0.100 1,600 Total assets 23,800 2,380$

Translation of Foreign Currency Financial Statements

Translation of Foreign Currency Financial Statements

Pesos Rate DollarsAccounts payable 2,000 0.100$ 200$ Notes payable 5,000 0.100 500 Common stock 10,000 0.125 1,250

Retained earnings 6,800 748 Translation adjustments (318) Total assets 23,800 2,380$

Zapato de Nationale, SABalance Sheet

At December 31, 2005

Cash 200$ Accounts receivable 400 Supplies 180 Equipment 1,600 Total assets 2,380$

Liabilities Accounts payable 200$ Notes payable 500 Total liabilities 700$ Stockholders' equity Common stock 1,250 Retained earnings 430 Total stockholders' equity 1,680 Total liabilities and stockholders' equity 2,380

Assets

Liabilities and Stockholders' Equity

The translation adjustment is

reported in other comprehensive income in the

equity section of the balance

sheet

The translation adjustment is

reported in other comprehensive income in the

equity section of the balance

sheet

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

15-22

Global SourcingGlobal Sourcing

Differences in exchange rates in many different countries can create significant complexities for

firms practicing global sourcing.

Many companies underestimate the cost of globalizing their business operations because they

are not familiar with the environmental characteristics discussed on the early slides in this

presentation.

Differences in exchange rates in many different countries can create significant complexities for

firms practicing global sourcing.

Many companies underestimate the cost of globalizing their business operations because they

are not familiar with the environmental characteristics discussed on the early slides in this

presentation.

€€

¥¥

££₣₣₧₧

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

15-23

In many countries around the world, bribery is part of doing business. In many

countries, this officially sanctioned corruption is not viewed as wrong or

unethical. However, U.S.-based businesses are prohibited from influence peddling. The IMF and World Bank instituted policies to

cut off funding to countries ignoring corrupt practices.

In many countries around the world, bribery is part of doing business. In many

countries, this officially sanctioned corruption is not viewed as wrong or

unethical. However, U.S.-based businesses are prohibited from influence peddling. The IMF and World Bank instituted policies to

cut off funding to countries ignoring corrupt practices.

Foreign Corrupt Practices ActForeign Corrupt Practices Act

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

15-24

End of Chapter 15End of Chapter 15

Recommended