Embed Size (px)

Citation preview

Z,&A/ -7 , - T/.

Document of

Thle World Bank

Report No. 12700-TH

STAFF APPRAISAL REPORT

THAILAND

SECOND GAS TRANSMISSION PROJECT

AUGUST 30, 1994

Industry and Energy Operations DivisionCountry Department IEast Asia and Pacific Regional Office

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS(As of December 31, 1993)

Currency Unit = Baht (B)US$1.0 = B 25.52

B 100 US$3.92

UNITS AND EQUIVALENTS

bbl barrelbcf billion cubic feetbpd barrels per daybtu British thermal unitGWh gigawa.t hourskcal kilocaloriekWh kilowatt-hourkoe kilogram oil equivalentkm kilometerlb poundmcf thousand cubic feetmmbtu million British thermal unitmmcfd million standard cubic feet per dayMW megawattppm parts per milliontcf trillion cubic feettoe tons of oil equivalenttonne metric ton (= 2,205 lb)

ABBREVIATIONS AND ACRONYMS

ADB Asian Development BankCNG Compressed Natural GascO Carbon monoxideCO2 Carbon dioxideDMR Department of Mineral ResourcesEIA Environmental Impact AssessmentEIB European Investment BankECCT Energy Conservation Center of ThailandEGAT Electricity Generating Authority of ThailandJDA Joint Development AreaJEXIM Export-Import Bank of JapanLNG Liquefied Natural GasLPG Liquefied Petroleum GasMIS Management Information SystemMOF Ministry of FinanceNEA National Energy AdministrationNEB National Environmental BoardNEPC National Energy Policy ComrnitteeNEPO National Energy Policy OfficeNESDB National Economic and Social Development BoardPTT Petroleum Authority of ThailandPTTEP PTT Exploration and Production Co. Ltd.SCADA Supervisory Control and Data Acquisition

PIT's FISCAL YEAR

October 1 to September 30

THAILAND

SECOND GAS T SMSSION PROJECT

Loan and Project Summary

Borrower: Petfoleum Authority of Thailand (PTT)

Guarantor: Kingdom of Thailand

Amount: US$155.0 million equivalent

Terms: 17 years, including a grace period of four years, at the Bank'sstandard variable interest rate.

Project Obiectives: The project's objectives are to promote greater sector efficiency andincrease the utilization of domestic natural gas resources. As such,they will help PTT to: (a) move towards a fully commercial operation(corporatization) under the new organization, as well as continueprevious efforts to strengtnen its institutional capacity to apply safetyand environmental standards and conduct project aralyses, includinginvestment programming and (b) construct a pipeline for transportingdomestic gas, which is the .cast-cost option to meet Thailand'sgrowing power generation requirements.

Project Description: The project includes: (a) a comprehensive study regarding PTM'scorporate strategy, organizational effectiveness and ownershipstructure; (b) institutional building and training of PTT's staff; (c) a36" diameter, 425 km offshore gas transmission pipeline that extendsfrom an existing platform at the Erawan fields in the Gulf of Thailandto onshore receiving facilities at Rayong; (d) a 28" diameter, 110 kmonshore pipeline that extends from Rayong to an area near the EGATpower plant at Bang Pakong; (e) related facilities, including acompressor station, metering stations, gas processing facilities, andtelecommunication and control systems and (f) project engineering andmanagement consultancy services.

Benefits: The project would have significant economic and environmentalbenefits. The gas would be used for power generat.on, in combined-cycle plants, which has been shown to be part of Thailand's least-costsolution to power generation. The economic benefits of the project arederived from the higher value that gas attains, when displacing otherfuels. Equally important, natural gas is a clean and low-polluting fuelwhen compared to alternative sources of energy. In addition, theproject will provide a detailed analyses for PMT's corporatization andeventual privatization.

Risks: Risks entail the following: (a) the availability of sufficient gasreserves and the cost of producing such reserves; (b) safety andenvironmental problems associated with the construction and operationof the project facilities and (c) potential disputes in various contractualarrangements. However, the gas reserves have been assessed andcertified to be sufficient. nle risks associated with a potenial increasein production cost.- have been minmized because appropriate

- ii -

contingencies have been included in the cost parameters. The safetyand environmental risks have been miniimzed because appropratemitigation measures have been designed. The potential for contractualdispute has been reduced because the agreements have been structuredaccording to international norms.

Estimated Cost:Locarl Tot

U ~US$ million (1993)Land & right of wav 4.8 - 4.8Linepipe & coatings - 236.8 236.8Onshore pipeline construction 10.0 30.0 40.0Offshore pipeline construction 24.5 103.0 127.5Facilities 7.5 31.3 38.8Engineering consultants services

and project management 16.9 15.2 32.1Studies & TA - 2.0 2.0Insurance and others 3.3 3.7 7.0Taxes and duties 22.2 - 22.2

Base costs 89.2 422.0 511.2

Physical contingencies 8.9 42.2 51.1Price contingencies 10.8 26.3 37.1

Total project costs 108.9 490.5 599.4

Interest during construction - 75.1 75.1

Total financing required 108.9 565.6 674.5

Ei-nanciLnS Plan:- TJS$ million (1993)

JEXIM - 100.0 100.0ADB - 100.0 100.0EIB - 47.0 47.0Equity 93.6 78.9 172.5Commercial borrowing - 100.0 100.0IBRD 15.3 139.7 155.0

TOTAL 108.9 565.6 674.5

Estimated Disbursements:

IBRD Fiscal Year 1995 1996 197-S$ million-

Amuwal 75.0 65.0 15.0Cumive 75.0 140.0 155.0

Pover Cag : Not Applicable

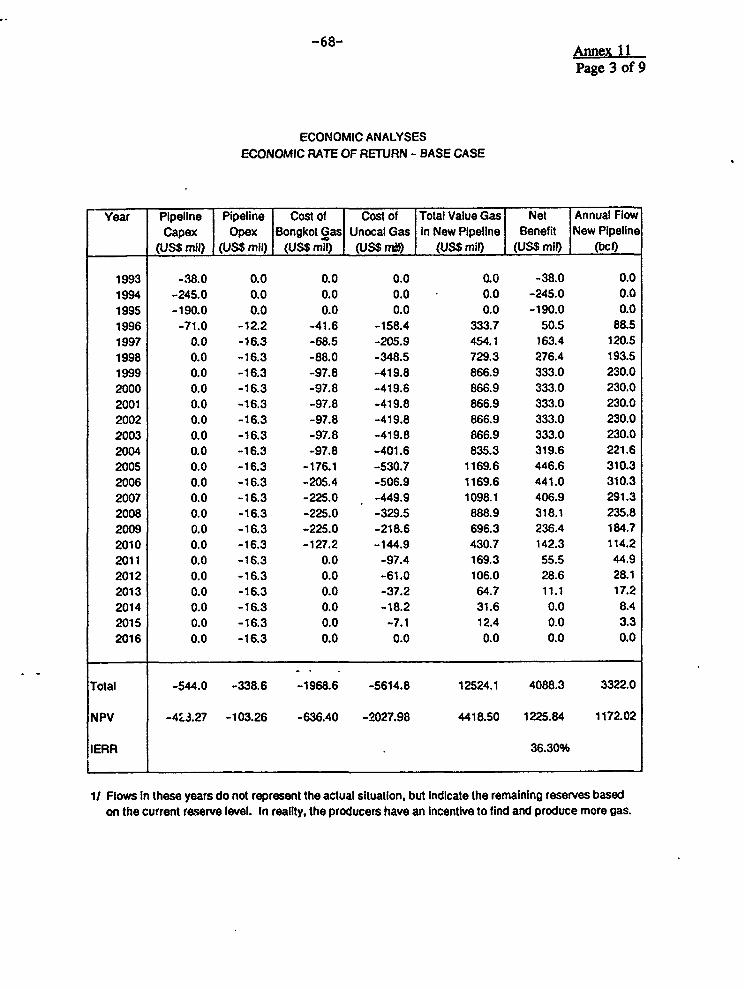

Economic Rate of Reun: 36%

Maos: IBRD No. 25766 and IBRD No. 25767

- iii -

T1HAELAND

SECOND GAS TRANSMISSION PROJECT

Table of Contents

M eNo.

Loan and Project Summary .................................... i

I. ENERGY SECTOR

A. Background . ......................................... 1B. Resource Endowment ............ ........................ 2C. Future Outlook and EnergyDem-d ........ ................... 4D. Insutions........................................... 5E. Prices .............................. ...... .... 6F. Issues and Strategy ............................. ...... 6

L. GAS SUB-SECTOR

A. Background .... 9B. Domestic Gas Supply and Import Potenti .. . . 9C. Gas Demand ..... 11D. Gas rices ..... 11E. Role of the Private Sector .... 12F. Experience with Previous Bank Loans .... 13G. Raionae for Bank Involvement .... 14

ii. TiHE PROJECT

A. Project Background .... 15B. Project Objectives .... 15C. Project Descrption .... 16D. Stats of Project Preparaon .... 16E. Environmental and Safety Aspects .... 17F. Project Implementation and Schedule .... 19G. Project Costs .... 19H. Project Financing Plan .... 20I. Procurement and Disbursement .... 21J. Monitoring, Reporting and Supervision .. . . 24

This report is based on ft findinp of an appraisal mbsion to hailand in Septembe I9 tha included MessrsiMme. M.Fabnd Crisk Managr), N. Chamou (Financial Speciit), T. Fizgead (Ptreum Geology), P. Wrg (ervoirSpecalist) W R. Pickford ESpedaist). Ih report was ediwd by Ms. B. Koeppel. Mr. M. Edmondsprovided research assisae and procesed the repoft T Pee Reiews are Mes. P. billa and C. Redfer Mr.A. Mhalotm acted as advir for die reorganizatio component The proct was clared by Mes. C. Madavo, DirecEAI and V. Nayyar, Cf EAIME.

-iv

IV. BORROWER

A. Background .................... 25B. Organization .................... 26C. Staffing and Training .................... 27D. Operations and Mangement .................... 27

V. FINANCIAL ANALYSIS

A. Past Financial Perfomance .................... 33

VI. PROJECT BENEFITS AND RISKS

A. Benefits .................... 37B. Rsks ...................... 38

VII. RECOMMENDATION . ................................... 39

ANNEXES

1. Domestic Energy Prices .................................. 402. Geology and Petroleum Potential of Thiland and Adjoing Basins ........ 413. Gas Production Forecast . ................................. 454. Project Schedule ............................ 465. Project I le on Orgmzation ...... 5.................... S06. Digramatic Description of the Project ....................... 517. Estmated Schedule of Disbursement . 528. Project Supervision Plan . ................................. 539. PTT Historical Financial Stements ......... ................. 5510. PTr Projected PFnancial Sttements ........... ............... 6011. Economic Anayses and Underlying Assumptions ........ .......... 6612. Selected Docments and Data Available in Project File .. ........... 75

CHARTS

Energy Sector Organizati.s . ................................. 76PTT Organ on ....................................... 77

MAPS : IBRD No.25766 and IBRD No. 25767

CHArR I

ENERGY SECTOR

A. Backgomund

1.1 Over the last decade, energy consumption in Thailand has been strongly affected by rapideconomic growth and funmentl dhanges in the structure of the economy. During this period, theGovernment and the Bank have cooperated to devise the best policy mix with regad to investmentplaniing, pnce formulation and institutional strucuing in order to meet the country's future energyrequirements and avoid ifrastructure botflenecks that could hamper economic performance. in thiseffort, the Bank helped Thailand construct several major energy projects and cenducted a major studyto identify the optimum fuel supply options over the next decade or two, while the Govermnent isconsidering to introduce organizional reforms that should corporaize, and, eventually, privatize theenergy entities. The proposed project represents another step towards this end.

1.2 Psas Consption Patern In 1991, the total supply of commerial energy in Thailandwas about 33 million tons of oil equivalent (toe) - a two-and-one-half fold increase over 1980 - andthe figure was growing at an average rate of 11% per year. Petroleum represented 62% of the total,natural gas 21%, lignite 13%, hydropower 3% and coal 1%, and 60% of the supply was imported. Inaddition, Thailand consumed about 10 million toe of renewable eneirgy in 1991, mainly in the form ofwood-fuels. However, despite the country's impressive economi;, growth (10% a year, for the last sixyears), per capita energy consumption and the type of energy consumed is that of a low-incomedeveloping country, which is a modest 540 kg oil equivalent of energy per capita and a reltively highshare (25%) of traditional fuels. This pattern is due to the large mrual popuation and the relatively highprice of commercial energy (compared with rural income levels), which plases commercial energybeyond the reach of the low-income group. Table 1.1 shows the past supply of primary energy bysources.

TABLE 1.1: THAILAND - Prhiary Eney Supply by Sores(million toe)

Eneiu Sources 9

Oil 10.5 20.5Naural Gas 3.2 7.0Hydro Power 0.9 1.1Coal/gnite 1.6 4.5Renewable 112 10.8

Totia 27A 43.9

Source: DE, Thailand.

1.3 Commercial energy, particularly oil and gas, plays a critical role in the economy because(a) the country is only modesdy endowed with these resources and (b) the dramatic in usalion inrecent years has led to a sharp increase in energy consumption. In fhat, demand continues to far exceeddomestic supply and this gap is likely to increase in the future, in view of the conthiued and rapid

-2-

economic growth expected and the uncertain prospects of discovering any additional major oil and gasreserves.

1.4 Final commercial energy consumption in the economy is dominated by the transportsector, which in 1991 accounted for 39%, followed by the industrial sector (31 %), and residental andcommercial sectors (24%). Traditional fuels continue to represent a significant, albeit rapidly decliningshare of energy consumption in the rural residential sector (see Table 1.2).

TABLE 1.2: THAILAND - Final Energy Consunptlon by Sectors(million toe)

Sector 195 I 1991

TrnpwQX i 6.0 11.9bJnduy 5.4 9.6Residential and Commerci 6.1 7.2Agriculltue 1 1.4 1.8

TOtW 18.9 130.3Source: DEA, Thailand.

1.5 Providing fuel in the power sector is a particularly critical issnie. since electricity demandhas grown by about 14% a year over the iast five years: To meet projected demand for the year 2000,the Electricity Generating Authority of Thailand (EGAT) needs to double its generating capacity fromthe current 9,000 MW to about 18,000 MW. In 1991, the fuels used to generate power includednatral gas (40 %), lignite (25%) and heavy oil (24%), while hydro was about 9%. However, EGAT'scholzes are increai1 ngly limited. First, the remaining supply of hydro is difficult to develop because ofhigh costs and environmental and resettlement problems. Second, lignte reserves are insufficient tomeet the increased requirements and its use creates environmental problems, as well. However, if gas(which is the most preferred fuel) would ultimately not be available, then EGAT must include locaUyproduced lignite plants (or imported coal-based plans) and dual-firing capability (to supplement gaswith fuel oil) in its master plan.

B. Resource Endowmenot

1.6 While Thailand has a diversified energy resource base, consisig of petroleum (oil,condensate and natural gas), lignite, hydropower, biomass and geothermal energy (which is still at anexploratory stage in the northern region), these resources are limited, which means Thailand is a netimporter of energy.

1.7 Oil. Given the geological features of the country's hydrocarbon basins, crude oil is notexpected to be a major contributor. At the end of 1992, there were about 245 million barrels of provenand probable oil reserves. Of these, about 177 million barrels are condensate, which would have to beproduced in association with offshore gas, and about 68 million barrels are crude oil. Additional oilreserves are estimated at about 440 million barrels, of which about 350 million barrels are condensateand 90 million barrels are oil. Production is currantly limited to Phet crude from the Sirikit oil field,which produced 22,000 barrels per day (bpd) in 1991. In addition, about 27,000 bpd of condensate

-3-

were produced in association with gas fro;n offshore fields in the Gulf of Thailand. To meet the oildemand, Thailand imported 160,000 bpd of finished petroleum products, and 220,000 bpd of crude forprocessing in its three local refineries.

1.8 Gas. Natural gas has been discovered mostly by companies looking for oil. At the end of1992, the remaining reserves were 7-8 trillion cubic feet (tcf). Gas production in 1992 was 850 millioncubic feet per day (mmcfd), of which 750 mmefd were produced from the offshore fields However,the country's natural gas resources will not be sufficient to meet future demand; therefore, Thailand haslooked into importing piped gas from neighboring countries (potentially from Malaysia, Myanmar and,recently, Vietnam), or importing it in the form of LNG from international markets. The demand fornatural gas arises mostly from the power sector and the trend is expected to continue in the foreseeablefuture: A conservative estimate indicates that the country's demand will continue to exceed supply byover 60% for the next 1D-20 years. Gas is an attractive option for power generation, both economicallyand environmentally, when used in combined-cycle power plants (para. 6.4); it is ths feature of nauralVs in the context of Thailand's economy, along with its environmental benefits, that gives rise to thep.oposed project. Table 1.3 shows past gas consunpption.

TABLE 1.3: THAILAND: Natural Zas Consumption_(mmrfd)

Feedstock 69 100hxl Y 20 40Power 252 554

ToWal 341 694

Source: DEA, Thailand.

1.9 Coal. Coal resources are all relatively low grade; the quality is generally categorized aslignite, although some deposits verge on being sub-bituminous. Information about reserves is somewhatambiguous since no common standards are used to classify them. Total minable reserves are estimatedat around 1,200 million tons which, according to current projections for lignite demand for power;.- -teration and industry (about 25 million tons per year by 1996), should last for about three decades.Ln 991, about 65% of the total coal consumed in the country was for power generation which usesdomestic coal (lignite) exclusively. Non-power n e of domestic lignite is mainly in the cement ;tdustry.Lignite therefore, is expected to play a long-term, albeit limited role as an energy source.

1.10 Hydro. Hydroelectric potential is estimated at about 10,600 MWV, of which only 3,000MW have already been developed or committed. The remaining potential is, in general, economicallyless attractive and environmentally quite difficult to develop. Thus, the potential for hydro would belimited to small/medium scale new projects and low-impact pumped-storage stations. This said, noserious attempts have been made so far to clearly define and classify the various environmetalproblems involved, and, particularly, to quantify the costs of mitigating measures needed to curtil theadverse impacts. Thus, given the country's large and unexploited hydro potential, and given its needfor increased energy supply, Thailand should more rigorously reexamine its potential hydro projects;and, through an enhanced financing plan (schemes such as BOOT or BOT) and an enhanced design ofthe environmental mitigation plan, some options which are economically and environmentally viable,could materialize.

-4-

C. Future Outlook and Energy Demand

1.11 Thailand's economic performance over the last ten years has been very impr.ssive,registering double-digit GDP growth over much of that period. While growth is expected to slow, theoutlook continues to be good because of a favorable international economic environment for Thailandand the country's sound economic policies and credit-worthiness. The Bank's long term projection isfor Thailand's economy to grow at 6%-8% over the next 10-15 years. With regard to the energysector, it is expected that private sector participation will increase, that the energy entities will soon becorporatized (and eventually privatized), and that the Government wil: intervene less in energy affairs.

1.12 Final energy demand projected by the Bank (as part of the analyses carried out for theFuel Option Study) is presented in Table 1.4 below. The Bank's forecast is slightly different from theGovernment's in that the Bank calculates a higher share of energy consumption in the transport andindustrial sectors.

TABLE 1.4: THA1AND - Forecast for Final Sectoral Energy Demand for 1993-2010(ktoe)

Sectar 1991a/ 1992y h [993- 1" 200s 2010hndustrial 9,533 10,382 11,089 15,415 22,813 28,510Transport 11,910 12,696 13,786 20,815 32,474 43,191Residential & Commercial 7,29 7,389 7,714 9,567 12,437 14,921Agrichre 1,827 1,922 2,003 2,464 3,154 3,612

TOTAL 30,4791 32,389 34,592 48,2611 70,7 90,234Implied Elasticity for Period 0.78 0.70 0.88 0.881 0.84 0.76Average Annual Growth for Peiod 6.9% 5 5.6% 5.0%

al Actual.h/ Estimated.Source: Bank Mission.

1.13 With regard to the type of fuel needed to meet the above sectoral demand, it is expectedthat (a) the consumption of non-wcommercial energy, such as bagasse in the industrial sector andwoodfuels and charcoal in the residential sector, will decline from its current share of 24% to 11% ofthe total by 2010, as the country develops; (b) industrial use of gas will be reduced to a level lowerthan the one currently projected by PTT, consistent with the priority ranking of the economic value ofgas in different applications (this will mean more gas for the power sector); (c) residential andcommercial sectors will increasingly use either LPG, as long as it is subsidized, or electricity (gas is noteconomic as there is no need for space heating, and kerosene, the most common woodfuel replacement,is not subsidized); (d) transport and agriculture will continue to use mainly oil (the role of compressednatural gas (CNG) in transport is expected to be very limited, if any) and (e) where end-use applicationis not a constmaint, imported coal, fuel oil, lignite and electricity will compete based on their totaleconomic costs, which include environmental costs. Table 1.5 provides the total prianry energyrequirements, including the fuels needed for the power sector.

-5-

TABLE 1.5: THAILAND - Projected Primary Energy Requirement(ktoe)

1993 1998- 2005-- 2010--Oil 23,694 32,537 48,796 63,717

Gas 7,376 12,923 13,826 7,661

Coal 380 828 8,895 22,733

Lignite 4,536 5,875 9,331 12,551

Hydro 378 480 538 643

Total Commercial 36,364 '2,644 81,387 107,305

Non-Commercial 7,470 8,384 9,308 a 952

TOTAL 1 43,8341 61,0281 90,6951 117,1571

Source: Bank mission.

D. institutions

1.14 The institutions in Thailand's energy sector are mature, and their inter- and intra-sectoralarrangements are quite sophisticated. The policy framework is extensive and there are numerousenergy-related agencies that spread across many ministries and include several cabinet-level committees.The chart in the annex provides an organizational diagram of Thailand's energy sector.

1.15 The key governmental organizations involved in energy affairs are:

(a) At the highest level, the National Energy Policy Council (NEPC), which is chaired by thePrime Minister, and whose members include deputy prime ministers and ministers whoseportfolios involve energy, as well as representatives from the National Economic andSocial Development Board (NESDB), the secretary general of National Energy PolicyOffice (NEPO), the director general of the Department of Energy Development anidPromotion (DEDP) and the director of the Budget Bureau. On behalf of the cabinet,NEPC approves major policy changes, plans ar.2 projects in the energy sector and definesroles, functions and priorities of the various ministries and state enterprises in the sector;

(b) The NEPO, which is the secretariat to NEPC, and adts as an operating arm to theCouncil. NEPO functions primarily as a link between NEPC and the country's stateenergy enterprises. NEPO plays a pivotr4 role in fonrulating the energy sector policy aswell as providing coordination and advisory functions;

(c) The Department of Mineral Resources (DMR), whose Director General reports to thePermanent Secretary of the Min!stry of Industry; it is responsible for assessing thecountry's coal and petroleum reserves, and for the preliminary exploration of coal andpetroleum. Two of its important functions are to grant concession licenses for explorationand mining, and to supervise the various exploration and production activities (includingthe monitoring of their enviromnental impacts);

-6-

(d) NESDB, which is a central planning agency that assesses the country's economy andprepares the five-year plans. In the energy sector, it is responsible for recommending tothe Council of Ministers whether it should approve or reject major energy projects;

(e) DEDP, which is a recent establishment (it assumed the responsibilities of the now-defunctNational Energy Administration), is under the Ministry of Science, Trchnology andEnvironment (MSTE), and is responsible for developing non-conventional energy sources.

1.16 The two major state energy enterprises are the Petroleum Authority of Thailand (PTI) andthe Electricity Generating Authority of Thailand (EGAT). PTT, the proposed borrower (see para. 4.1),is involved in downstream oil and gas activities (upstream activities are carried out by the privatesector; see para. 2.12). EGAT is involved in generating electricity and producing and utilizingdomestic coal (lignite). Since it was established about 25 years ago, EGAT has grown to a staff of32,000 with US$2 billion in annual revenues. At the end of 1991, it had an installed capacity of 8,000MW and generate. 50,000 GWh of electricity. As with ?1T, EGAT is devis4g plans for restruct'rngand privatization to promote a larger private sector role in power development. From 1994-1996, thiswill invoive (a) corporatizing EGAT, including the sale of EGAT equity on the security market; (b)selling 51% of the Electricity Generating Company (EGCO), an EGAT subsidiary created in 1992; (c)soliciting build-own-operate (BOO) proposals for new generating plants through an open competitionamong independent power producers and EGCO and (d) incorporating the Metropolitan ElectricityAuthority (MEA) and Provincial Electricity Authority (PEA), and increasing PEA's regionalization, toprepare for privatization.

E. Prices

1.17 Current prices for all energy products in Thailand reflect their actual economic costs,except lignite. Thai lignite, due to its poor quality (high sulphur and ash content), can not be traded inthe international market; therefore, its economic cost is based on EGAT's internal transfer price. Whileno other major issue exists in the pricing structure of the energy products in Thailand, some minordistortions remain in the price structure of petroleum products (LPG continues to be subsidized) and inelectricity tariffs (power distribution companies .ay no capacity charge). The Government is aware ofthe potentially negative effects these minor distortions can have on investment decisions and inter-fuelsubstitution and is taldng steps to narrow the differences, consistent with the structure of economiccosts. (Annex 1 provides the domestic prices of energy products. Gas prices are discussed in paras.2.8-2.11).

F. Issues and Strategy

1.18 In principle, Thailand's energy sector faces two major is-sues. The first is how to meet thecountry's future ena.gy requiemets, given the insuiiciency of domestic energy resources, in a mannerwhich is econrmically rational, enviromnentally sound and financially viable. The second is how todivide the heavy burden of massive energy investment between the public and private sector - giventhat neither can carry this alone - so as to ultimately shift investment to the private sector completely,

-7-

without disrupting the country's rapid economic growth. The proposed project contains elements whichaddress both: The pipeline would transport domestic gas to the market (the fuel is the least-cost andleast-polluting solution for power generation in Thailand), and the proposed technical assistance includesa component for restructuring PTT to a corporatized and, eventually, privatized entity (see paras. 3.7and 4.234.28).

1.19 Other ;mportant issues in the sector are:

(a) Enviironental impacts. The environmental impact of energy production and consumptionhas become a topic of public debate and a real constraint to developing lignite powergeneration and hydropower. The Government recognizes the importance of these issuesand is committed to developing the sector in an environmentally sound manner. Thw, itnow requires the power sector and major industries to use pollution-control technologies,such as scrubbers, in all existing and future lignite-fired power plants and in the cementindustry. Further, the Bank is helping the refinery operation, through the Air QalityEnhancement Project (scheduled to be appraised in July 1994), to produce less pollutingprod cts. In addition, the Government is in the process of developing enviromnentalpolicies and standards to mitigate pollution through taxes, penalties and incentives.

(b) Reguatory Jfamework. The Govermnent has pursued sector efficiency objectives withconviction and the results are impressive. However, one key issue is that there is noindependent regulatory body. Given that the need for sector regulation in Thailand is notdriven by inefficiency, but by the need to bring in private investment, the regulatoryframework must be designed in conjunction with the decision on restructuring the sector.While the issue of regulatory framework at macro level is being currently addressedthrough an on-going sector study by the Bank (Increasing Private Participation andImproving Efficiency in State Enterprises), there is still need to examine the benefits ofregulatory framework at sectoral level. Therefore, the Bank has recommended (in theFuel Option Study) that the Govermment prepare an independent regulatory framework thatcould be functioning by the time Thailand restructures the sector (during the plannedcorporatization of the energy entities).

(c) Energy conservaion. The Govermnent recogiizes that energy use must be rationalized ifthe country is to cope with its supply constraints. Thus, conservation is a formal objectiveof Thailand's energy sector policy, which is beginning to move towards an integrated-resource planning approach that focuses both on supply and demand. Two prograrAs thatpresently address this are adopting a master plan for demand side management (D¶SM) andintroducing time-of-day tariffs aimed at reducing peak demand. The DSM mAster planproposed an initial five-year pilot program t'rough which EGAT would saveapproxinately 1,427 GWh per year by the end of the fifth year. These savings, whichalso include a capacity saving of 225 MW, would be achieved through iroentives for allcategores of consumers to produce and/or instaU energy-effitcent technologies. Theprogram is estimated to cost US$188 million. Potential benefits are calculated to be aboutUS$260 million in capital investment and US$30 million per year in fuel expenses. Thiswould equal a very low energy supply cost of US$2.051 per kWh. Also, the structure ofelectricity tariffs is being gradually improved through the introduction of time-of-daytariffs for major consumers. This measure aims to increase the power system's loadfactor, thus reducing expansion needs.

(d) Environmental ad S4fey Stand. There is a need to create an acceptable se,, ofenviroMnental and safety standards to exploit hydrocarbon resources in the Gulf ofThailand. This issue is currently being addressed through a study carried out by DMR(para. 3.13).

CHIAPrER B

GAS SUB-SECTOR

A. Badcground

2.1 Exploration for hydrocarbon in Thailand began about 1971 after the Governmentestablished the petroleum Law. Oil and gas exploration and development activities have been extensiveenough to conclude that the area has gas resources but relatively minor oil potential. The country'stotal hydrocarbon resources are spread over at least eight different geological structures, offshore andonshore. In the offshore areas, the most sigrificant to date have been found in (a) the Pattani Basin,which extends through the middle of the Gulf of Thailand and includes all the currenty producingUnocal fields (the source of supply for the proposed project) and (b) the Malay Basin, which extendsfrom Malaysian waters into the Gulf of Thailand and includes the Bongkot structure, the largest knownexisting gas field in the Gulf (also the source of supply for the proposed project). In the onshore areas,hydrocarbon potential is believed to exist in the northeast (in the Khorat Basin), and in the central-west(in the Phitsanulok Basin), where Shell's small Sirikit oil field is situated. Annex 2 provides adescription of Thailand's petroleum geology.

2.2 Most of the discoveries from work in the existng basins have been non-associated gmadeposits, which have been rich in heavier hydrocarbons, including ethane, propane and natural gasliquids (NGL).

2.3 Although the poteal for hydrocarbon resources exists, the prevailing geology in thebasins indicates that further development will not be easy: Due to the erratic deposit of fluvialreservoirs and complex structurig, the hydrocarbons are trapped in numerous small reservoirs thatned sophistcated drilling and recovery techniques. Further, the small size of many fields and therapid reservoir depletion create the need for a large number of offshore platforms, which, in turn, leadto high development and production costs. In a number of cases, the long lead time and additionalcosts have made field development uneconomic.

B. Domestic Gas Supply and lInport Potential

2.4 Due to the complex geology mentioned above, calculations of Thai reserves (prior toproduction history) are generally based on statistical occurrence rather than measured quantities. Inessence, when statistical methods are used, the disinction between the proven and probable reservesbecomes less clear, with the proven reserves being somewhat less assured and the probable reservesbeing somewhat more probable than indicated by the American Petroleum Institute (API). The officialbasis for the data on Thailad's hydrocarbon reserves are the DMR reports, which, in turn, arecompiled primarily from the latet information submitted by each company that has made discoveries.Based on these reports, the most likly level of gas resemves remaining in Thailand ranges from 6.5 to11 tef, and the possible reserves could be as high as 17 tcf. However, for the purpose of the proposedproject, only the cerdfied level of gas reserves has been used in the project analyses, which represents

-10-

a conservative estimate. The details of the certified reserves which have been designated to the projecthave been provided to the Bank.

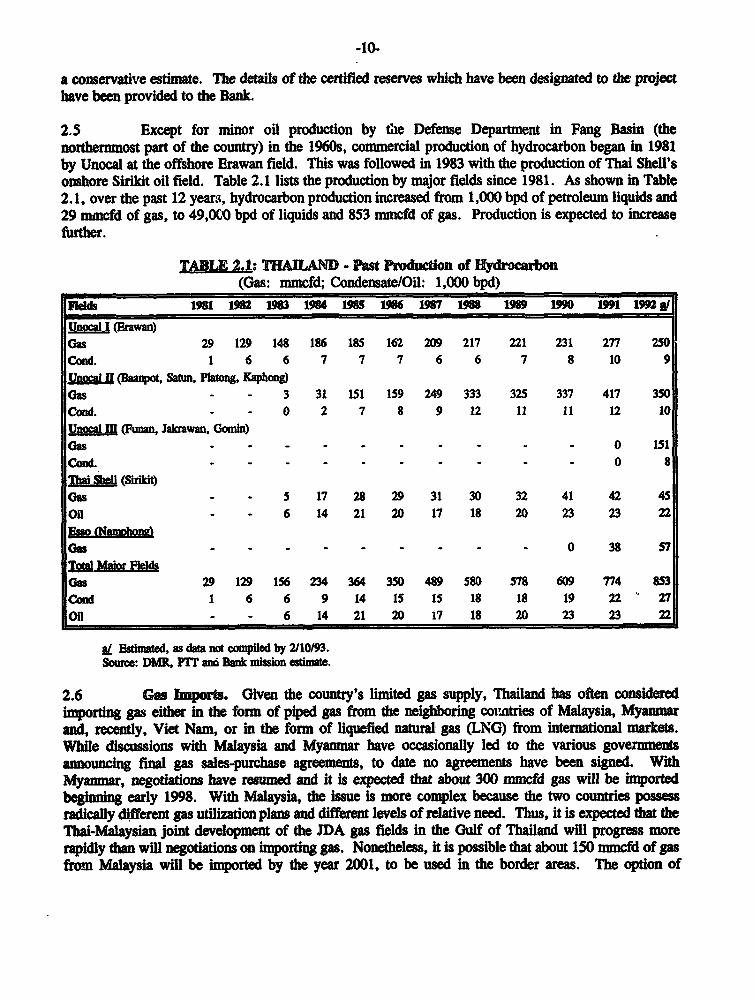

2.5 Except for minor oil production by tie Defense Department in Fang Basin (thenorthernmost part of the country) in the 1960s, comnercial production of hydrocarbon began in 1981by Unocal at the offshore Erawan field. This was followed in 1983 with the production of Thai Shell'sonshore Sirikit oil field. Table 2.1 lists the production by major fields since 1981. As shown in Table2.1, over the past 12 years, hydrocarbon production increased from 1,000 bpd of petroleum liquids and29 mmcfd of gas, to 49,00 bpd of liquids and 853 mmcfd of gas. Production is expected to increasefurther.

TABLE 2.1: I AD - Past Production of Hydrocatbon(Gas: mmcfd; Condensate/Oil: 1,000 bpd)

meI.da 1981 19s 13 1984 95 96 1967 6 169 1o L1 199 n go

Unoca I (Bwan)Gas 29 129 148 186 185 162 209 217 221 231 277 250coad. 1 6 6 7 7 7 6 6 7 8 10 9

Unocxl 1Baanpot, Satm, unatong. Kaphong)Gas 3 31 151 159 249 333 325 337 417 350Cond. - - 0 2 7 8 9 12 11 11 12 10

UnoalM (Funan, Jakrawan Gomin)Gas - - - - - - - - - - 0 151Co-d. - - - - - - - - - - 0 8

uXshell (Shirii)l

Gaslkc - - 5 17 28 29 31 30 32 41 42 45on!W - - 6 14 21 20 17 18 20 23 23 22

Es so (N_ }=Gas - - - - - - - 0 38 57

-§-XsoudPar Firddbanbs 29 129 156 234 364 350 489 580 578 609 774 853-- <>wad 1 6 6 9 14 1S 1S 18 18 19 22 27onR - - 6 14 21 20 17 18 20 23 23 22

a/ EsimatAd, as data not compiled by 2/10/93.Souce: DMR, PTr ana Bank nission esdmaWe.

2.6 Gas Imports. Given the country's limited gas supply, Thalba has often consideredimpordng gas either in the form of piped gas from the neighboring cointes of Malaysia, Myamarand, recently, Viet Nam, or in the form of liquefied natural gas (LNG) from international markets.While discssions with Malaysia and Myanmar have occasionally led to the various goveentsamnouncing final gas sales-prchase agreemens, to date no agreements have been signed. WithMyanar, negotations have resumed and it is expected that about 300 mmcfd gas will be importedbegining early 1998. With Malaysia, the issue is more complex because the two countries possessradically different gas utilization plans and different levels of relative need. Thus, it is expected that theThai-Malaysian joint development of the JDA gas fields in the Gulf of Thailand will progress morerapidly than will negotiations on imporng gas. Nonetheless, it is possible that about 150 mmcfd of gasfrom Malaysia will be imported by the year 2001, to be used in the border areas. The option of

-11-

importing gas from Viet Nam is not being considered because that country does not produce enough gasto export. The high netback value that natural gas produces, and the projected growth in the country'spower generation (which ensures a high-volume gas consumption), justifies, prima facie, the large-scaleinvestments required to import LNG. The potential use of LNG in Thailand would be identical to thatof imported gas with regard to its economic value and priority ranking in various applications andsectors. The Government is looking into LNG option, to detennine whether it is viable.

C. Gas Demand

2.7 Demand for gas in Thailand is substantial: Based on estimates, it will exceed the projecteddomestic supply by an average of over 60% for the next 15-20 years. The largest consumer is thepower sector which currently uses over 90% of the country's total supply. Because of the enhancedeconomic value of gas (para. 6.4) when used in a combined-cycle power plant, as well as itsenvironmental benefits, the demand for gas in the power sector is growing. And, because demand forelectricity has grown at 14% a year over the last five years, even under a high-case gas supply scenarioof 1,700 mmcfd available by 2003, this quantity meets roughly just one-third of Thailand's powerrequirment, under a low growth scenario. Moreover, if the requirements of industrial users are addedto those of the power sector, the covAtry could use an estimated 3,000-3,500 bcf. This quantity wouldnot be available through domestc resources or from imports from neighboring countries.

D. Gas Prices

2.8 The unique features of the domestic gas industry in Thailand have produced a relatvelysophisticated pricing structure which involves a separate pricing system for producers and consumers.

2.9 Prodcer Prices. The cost of producing gas in Thailand is relatively expensive comparedto neighboring countries such as Malaysia or Indonesia. This is due to the gas fields' complexgeological features which result in tho well-head transfer price bearing the high cost of fielddevelopment and production. At present, only one major company, Unocal, is producing offshore gasin the Gulf of Thailand. By mid,-i94, Total Company will also produce offshore gas from theBongkot field (in the Gulf). While the gas sales-purchase contracts between PTT and the twocompanies are different, the principles are essentially the same: (a) the initial transfer price is based onthe long-run economic cost of supply and on the replacement value of altemative fuels; (b) the price-adjustment mechanism contains indices reflecting the international prices of energy products (mostlyfuel oil), the fluctuations in foreign exchange rates and in the domestic and international rates ofinflation; (c) prices include a floor and ceiling level to protect sellers and buyers and (d) prices areadjusted annually, except after devaluatons, when they are inmnediately.Y' The Bank-estimatedaverage well-head price for Unocal's gas ranges from US$1.77 per mmbtu to US$2.08 per mmbzu; for

.1/ The gs pcing stuctue for the Namphong field, which produces a relatively small amont of the dry gas used in theadjacent power plant, is somewhat different because of specific development costs and the composition of the gas (all methme).The average well-head price for Namphong gas is about US$1 per mmbtu.

-12-

the Bongkot gas, the range is US$1.98 to USZ2.25 per mmbtu. The structure and level of producerprices in Thailand is consistent with international norms.

2. 10 Consumer Prices. The principle the Government applies when setting consumer prices(for power and industry) is also sound in that it links the consumer gas prices to alternative fuel pricesin each activity. The present price of gas to industry, which consumes less than 6% of the total, isintende,i to encourage LPG consumers to shift to gas-.' The price to the power sector - which usesover 90% of total gas - was previously set by the Government. However, on December 12, 1991, anagreement was signed between PTT and EGAT which set the price based on (a) the price paid by PTTto upstream producers (well-head price); (b) the average cost of gas transmission including a reasonablereturn to PTT and (c) the value-added tax. The Bank estimates that the current average price of gassold by PTT to EGAT is about 78 Baht per nmmbtu (US$3.06 per mmbtu). During negotiationsagreement was reached with PTT that it submit to the Bank, by December 31, 1994, an amendment tothe gas sales-purchase agreement (between PTf and EGAT), to ensure the sale and purchase of new gasreserves under terms and conditions satisfactory to the Bank.

2.11 Although current gas sales-purchase agreement referred to in para. 2.10 covers theprinciples of gas sales-purchase between PTT and EGAT, since last year, P1T and EGAT have beeninvolved in a Bank-sponsored study which would establish a long-term pricing formula for future gassupply that is in line with international standards. It would create two separate contracts - one for the"firm" gas supply and one for the "interruptible." A daily quantity would be defined for the firmsupply (about 500 mmcfd), to fuel EGAT's combined-cycle power plants, and the contract would be atake-or-pay agreement. The price of the firm contract would be equal to the pipeline cost oftransporting the gas, plus the gas commodity price, which is equal to PTT's volume-weighted averagepurchase cost. The price of an interruptible contract would be based on the cost of alternative fuel andnegotiated by the parties. The new price mechanism was approved by the Government on August 17,1992.

E. Role of the Private Sector

2.12 Thailand's hydrocarbon resources are produced either totally by the private sector orthrough a joint venture between the private sector and PTTEP, which is a subsidiary of PTT. In thelatter case, the private sector is the major shareholder and has included major international oilcompanies such as Unocal, Shell, Esso, Total and British Gas. In the oil sector, Thailand's threeexisting refineries are either privately owned (by Esso), or owned through joint ventures between theprivate sector and PTT (PTT owns 30% and 49% of Bangchok and Thai Oil refineries). ihailand iscurrently constructing two new refineries, with majority shares owned by Caltex and Shell. Indistributing and marketing oil, PTT competes with international oil companies, having a one-third share

2/ No such inecntive is provided to fuel oil users, because gas has a lower netback value when substiting for fuel oil.

3/ Industry's price is significantly higher than the one established for the power sector, since the margin of subsion betweenLPG and gas has been high, even after a discount, to allow for penetration of gas into the LPG market.

-13-

of the market. The other two-thirds are shared among Caltex, Shell and smaller finns. The only areain which PTT has sole responsibility is the transmission of gas, the bulk of which is sold to EGAT.V1

2.13 With regard to private sector participation in gas transmission, the most likely investorswould be Unocal and Total, the two private gas producers currently active in the Gulf of Thailand.However, both have told the Bank they are not interested in participating in gas transmission because ofcorporate strategic reasons.1Y Not only are Unocal and Total disinterested, but no other private partyhas approached PTT or the Government to invest in the project. ADB, JEXIM and EIB, which arecofinancing it, have also found this same lack of interest from the private sector. In fact, with projectsin the oil and gas sectors of this dimension, where investors are interested in participating, they registerthis very early in the project cycle, often even before the Bank is involved. Thus, it is unlikely thatthere are any viable interested parties.

F. Experience with Previous Bank Loans

2.14 Until now, the Bank has made four loans to Thailand's oil and gas sector: The first (loan1773-TH) was to construct the country's first gas transmission pipeline; the second (loan 2184-TH) wasto construct a gas separation plant; the third (loan 2184-TH) supported oil field development; and thefourth (loan 3508-TH), now being disbursed, is to construct the Bongkot gas transmission pipeline.These projects, implemented over the past 11 years, have been completed on schedule and within thebudget, and have realized their main objectives. Three lessons are particularly relevant to the design ofthe proposed project. First, given that the region's geology is complex, the hydrocarbon reserves mustbe evaluated comprehensively (before proceeding to full development and production) and the high costof developing the fields should be addressed: The proposed project has considered these factors.Second, given Thailand's procurement practices and import tax laws, the Bank has learned to prepareprocurement packages in a way that inimzes their numbers, yet conforms with Bank guidelines, henceavoiding potential delays resulting from procurement-related issues. As a result, the proposed projectconsists of only about eight main single-responsibility contracts, of which the Bank loan will fund two.Third, the Bank learned that coordination at two levels was problematic; this occurs within the PTT(between the Engineering and Finance Departments), and outside (between PTT and EGAT), regardingthe timing, load requirements, capacity and type of power plants that rely on the PTT gas supply.During project preparation, the Bank helped increase cooperation and interactions between PTT andEGAT, as well as within the agency.

i/ Pff is also responsible for the primary transportation of oil in the country. However, Thailand has very little indigenous oil.

5/ In an October 27, 1992 letter to the Bank, Unoal stated that its 'reason for not wanting to paricipate is rooted in thebeliefthat we can return the maximum benefits to our shareholders when we stick to our core business, and that is developing andproducing oil and gas.' Total provided essetially the same response with regard to the Bongkot project. Moreover, thecompanies believe th e large capial commitment neerd to develop and produce the additional gas would constrain theirresources.

-14-

G. Ratonale for Bank Involvement

2.15 The overriding rationale for Bank involvement is to continue helping the country build apolicy framework with which it can operate the sec or efficiently. For the many years that the Bank hasbeen involved in Thailand's oil and gas industry, the Government and energy-affiliated agencies havesought and implemented Bank advice on how to build such a framework. These interactions haveproduced major energy projects based on economnically-rational justifications, deregulation of all but oneof the petroleum product prices, rigorous analyses of environmental impacts (of the energy projects),and the initial reforms to ultimately create completely commercial entities. Further, the Bank, with helpfrom the agencies, identified the optimum fuel choice (see the Fuel Option Study) and prepared a masterplan for utilization of domestic and imported gas over the next decade or two. These activities havesignificantly enhanced the sector efficiency and its profitability; however, issues remain. The mostimportant are corporatizing/privatizing the energy entities (so as to raise capital to meet the massiveinvestment requirements); establishing an independent regulatory body (to assure private investors theirventure capital is protected by a fixed set of rules and procedures): creating an internationally-acceptable set of uniform environmental standards and regulations (to cxploit hydrocarbon resources inthe Gulf of Thailand); and amending the country's legal codes for oil and gas activities (to provide anenvironment that would attract greater private sector participation). The proposed project addresses oneof the key issues of corporatization, which constitutes a first step towards privatization. As for creatingappropriate regulatory structures, these can only be defined after the Government decides the nature ofthe restructuring (corporatization).

2.16 The project is consistent with the country strategy discussed by the Board in September1994, because the physical infrastructure and institutional weaknesses will be the main issues for thenext decade or two. It includes components relevant to both constraints. First, it helps finance theconstruction of a pipeline, which will ease the bottleneck in transporting the domestic natural gas.Second, it will train staff to carry out project analyses and application of safety and environmentalstandards, as well as help the borrowing entity reorganize towards a corporatized structure, whichwould reduce the public sector's need for investment capital.

2.17 The project is also consistent with the sector strategy because it promotes the use ofnatural gas, which the recendy completed Fuel Option Study concluded was the least-pollutng andleast-cost fuel with which to generate power.

2.18 Therefore, Bank lending in the sector is consistent with both the country and sectorstrategies and the Government decision regarding sectoral priorities. Without Bank involvement, keysectoral issues may not receive proper attention, and the development of an enabling environment, forgreater private sector participation may be deferred.

THI PROJECT

A. Background

3.1 Over 90% of Thailand's natural gas comes from the Gulf of Thailand, transported thr )ugha 34-inch offshore pipeline from the Erawan platform to Rayong, on the northern shore. The pipelinehas been operating for almost nine years, and its present flow rate is about 750 mmcfd. Althougn thepipeline has never operated at its maximum capacity of 850 mmcfd (because of limited supply), thelatest major inspection confirmed that the pipeline could safely transport that amount.Y

3.2 During the negotiations (in the spring of 1992) of Loan 3508-TH (Bongkot GasTransmission Project), PTT and the Bank agreed that the need for the second pipeline depended on (a)the present and projected reserves and production of gas from the Unocal and Bongkot fields; (b)maximum allowable capacity of the existing 34-inch pipeline (at that time, the latest inspection reportwas not yet completed) and (c) the possibility of malfunctions in the existing (sole) pipeline to Rayongand the speed in which the malfunction could be corrected.

3.3 To assess the above factors and to determine whether the second pipeline project wasneeded, the Bank agreed to provide, as part of Loan 3508-THl, US$2 million for the requiredinvestigations. The studies intended to confirm the reserves' availability, the time needed to developand produce gas and the optimal means of transporting it from the Erawan platform to the onshoreconsumig centers. Also, the studies would establish whether the proposed pipeline should beconstructed offshore, closer to the shore, or onshore.

3.4 Two studies were conducted. The first confirmed that gas was indeed available and a gasulization master plan study concluded that the proposed project should be given high priority and alsoddetrined the routing and size of the pipeline. The Bank reviewed the consultant's report and agreedthat the project constituted a high priority investment in the master plan created for the country's gastransmission network.

B. Project Objectives

3.5 The objectives of the project are to achieve greater efficiency in sector operations andincrease the utilization of domestic natural gas resources. They involve helping PITT to: (a) movetowards a fully commercial operation under the new organization; (b) strengthen its institutionalcapacity to apply safety and environmental standards as well 'as carry out project analyses and

6/ The Brish Gas Corporation conducted a comprehe inspection in April 1993, using the lates tectnology and asophiscated surveying mehanism to detect any corrosion and/or defonration the pipeline. MTe resutd of the inspection, inform of a summaiy report, was made available to the Bank, confirmig that the pipeline could in fiact wthstand a maximum flowTe of 85O mmcfd.

-16-

investment programnming and (c) construct a pipeline to transport domest-i gas, which is the least-costoption to meet the country's growing power-generation requirements.

C. Project Description

3.6 The project consists of an offshore and an onshore pipeline and the facilities to transportthe natural gas produced in the Bongkot and Unocal fields in Gulf of Thailand to onshore locations incentral part of the country. Map IBRD No. 25766 shows the location of the offshore and onshorefacilities and the routing of the proposed pipeline as well as the existing pipeline. Annex 6 describesthe project facilities.

3.7 The major project components are:

(a) A technical assistance component, which includes a study on corporate strategies andfinancing plans for PTT's corporatization, as well as a training program for PTT staff inproject analyses (including investment programming) and in applying safety andenvironmental standards (see paras. 4.23-4.28)

(b) A 36-inch diameter, 425 km offshore gas transmission pipeline installed in water depthsranging from 200 ft-270 ft. It will extend from an existing platform at the Erawan field toonshore receiving facilities at Rayong;

(c) A 28-inch diameter, 110 km onshore pipeline that extends from Rayong to the block valveNo. 6, near EGAT's power plant at Bang Pakong;

(d) Related facilities at Erawan riser platform, at Erawan compression and central processingplatform, at Rayong receiving terminal and at block valve no. 6, that include scraperlaunchers and receivers, slug catchers, pressure and flow controls, pipe manifolding,various tie-ins, as well as an onshore compressor station;

(e) Modification/expansion of the existing supervisory control and data acquisition (SCADA)system and the pipeline telecommunications network;

(f) Consultancy and management services for bisic design, detailed engineering, preparationof bid documents, procurement of goods and works, supervision of the construction andcommissioning the facilities;

D. Status of Project Preparation

3.8 The project is in an advanced stage of preparation. Technical specifications, details aboutthe project management unit, various studies and basic design have been partially completed. Contractsfor the pipeline materials and the coating (financed by the ADB and JEXM), have been awardedaccording the ADB's procurement guidelines. Bidding documents for the contract to lay offshore pipehad been prepared by PTT's consultants (Bechtel), and were reviewed with the Bank in late January.

-17-

The bid documents were issued and the bids have been received. The Bank is in the process ofreviewing the bid evaluation report submitted by PTT. Other engineering, procurement and projectrelated activities are progressing according to schedule. No land acquisition problem is anticipated (seepara. 3.15). The overall status of project implementation suggests no impediment to the current rate ofprogress.

E. EnvironmentW and Safety Aspects

3.9 Termns of reference for the environmental impact assessment (EIA) of the project wereprepared jointly by the Bank and PTT's environmental consultants (the Team Company), which alsoconducted the EIA for the Bongkot Gas Transmission Project (Loan 3508-TH). The final ETA reportfor the proposed project has incorporated the Bank's comments, including measures to ensure that theproject complies with the Bank's environmental guidelines (see Project File for a summary of the EIA).

3.10 Tht project would have minimal negative impact on the environment because the use ofnatural gas would be significantly less harmful than either fuel oil or coal. While natural gas is notpollution free, it is inherently cleaner than other fuels: It is free of most pollutants present in liquid andsolid fuels and generates less carbon dioxide (CO2). The reduced CO2 emissions offer a highly cost-effective response to the greenhouse effect. The gas used in combined-cycle power plants emits only40% as much CO. as a coal-fired power plant. Moreover, treated natural gas has no sulfur content. Inaddition, the gas to be transported by the project pipeline is non-associated gas, which carries much lessenvironmental risk than of oil or associated gas. Nonetheless, a few areas carry some potential risk tothe environment. These include the disruption to marine life (which could be caused by changes inseabed conditions near the pipeline during construction); the discharge of liquids such as processedwater, deck drainage and sewage from production and living quarters platforns; the disposal ofmercury (which is sometimes present in the gas) and the noise and vibration caused by equipment onthe production platforms. The EJA report fully addresses these issues and provides for appropriateactions such as pre-treatment of liquid effluent before discharge to the sea, safe disposal of solid wastesto approved land sites and safe disposal of elemental mercury. Any disruption to marine life would notbe severe because the project involves only about 0.37 square kilometers of seabed. In fact, once thepipeline is operating, it is expected that its surface would provide attachment points for plant speciesand will provide cover for fish. The design of equipment will be according to intenational standardsfor maximum safety and allowable levels of noise and vibration. Further, the EIA report will analyzealternatives, including the effect of various pipeline routings on natural biological resources such ascoral reefs. Proposed measures will ensure that the environmental impact, if any, will be kept withinlimits prescribed by Bank guidelines. During negotiations, agreement was reached with PIT that it willtake all measures required on its part to ensure full implementation of the action plan contained in theEnvironmental Assessment Report (pam. 3.9).

3.11 The entire project design will be in accord with international safety codes and standards.Natural gas condensates will be separated from gas on the production platforms, before the gas isintroduced into the pipeline. However, small quantities of liquids will be present in the gas as theresult of condensation of hydrocarbon gases; thus, the condensed gases will be periodically removedfrom the pipeline by a "pig." The pipeline route will be adequately demarcated, especially in shippinglanes and fishing areas, to avoid potential damage to the pipeline (e.g., by a ship's anchor).

-18-

3.12 Offshore facilities are being constructed by Unocal and the operator (Total) of the Bongkotgas field (for upstream facilities), .nd by PTT's construction contractor (for downstreatn facilities).Unocal and Total have extensive e perience in similar operations elsewhere in the world. Theconstruction of the downstream facilities will be supervised by Bechtel International, which also has vastexperience in this area. These companies use high standrds of safety and environmental protection,and they require the same from their sub-contractors.

3.13 Further, a study for Development of Environmental Standards and Regulations forHydrocarbon Exploration and Exploitation in the Gulf of Thailand was initiated by the Bank as part ofthe Bongkot Gas Transmission Project. The objectives were to assess present environmental legislationand regulatory provisions, as well as current concessionaires' practices, and drft regulations andguidelines for environmental control with respect to hydrocarbon exploration and exploitation in theGulf of Thailand. It recomnends (a) strengthening the Thai environmental institutional processes,including reporting, review and approval procedures; (b) providing standards and guidelines forenvironmental impact assessments and for environmental management and monitoring by DMR; (c)establishing concessionaires' requirements for environmental compliance and (d) notifying authoritiesabout oil spills or other releases. In addition, the study recommends various operational standards andguidelines for the construction process and management activities for both onshore and offshorefacilities. During negotiations, assurances were given by PTT that it would use its offices to encourageDMR to implement the recommendations contained in this study. Furthermore, during negotiations, itwas also understood that PTT would assist in persuading DMR to conduct a base-line environmentaldata survey for the Gulf of Thailand.

3.14 PTT's operational safety record has been excellent, and it is expected that it will operatenew facilities according to the same high standards. Notwithstanding PTT's excellent operational safetyrecord and its commitment to sustaining the environment, the oil and gas industry in Thailand is stillrelatively new and the industry has not yet produced the standards and regulations needed for safety andenvironmental protection. P'IT currently has no well-defined safety engineering standards andenvironmental regulations, nor does it have an adequate institutional framework with which it canproperly administer this aspect of its operation. As part of the loan 3508-TH, agreement was reachedthat US$200,000 would be included for consultancy services to help PIT adequately prepare safetyengineering and environental standards for its entire operation; also, that PIT would implement thestudy's recommendations. The study is currently being prepared and its implementation should beginby September 1994. During negotiations, agreement was reached with PfIT that it will implement therecommendations of the study. Regarding the institutional framework, PIT'S new organization,effective January 1, 1992, includes a safety and environmental committee chaired by P'IT's Governoras well as a safety and environmental standards divisions in each of four business units. The heads ofthese divisions report directly to the presidents of the respective business units. Further, each divisionhas one or more sub-divisions (e.g., for pipeline and gas plants within the natural gas business unit) toenforce the standards and regulations at the operational level. While PlT's environmental arrangementis satisfactory, the staff will need more skills and experience to properly apply and execute the safetyand environmental regulations resulting from the above study. Therefore, the proposed project includesabout US$150,000 to train PTT's environmental and safety staff. During the negotiations, agreementwas re: ched with PTT that it will carry out the training program for its staff by March 31, 1995.

3.15 The number of people expected to be resettled within the five meter right-of-way is about40. During the negotiations, PTT and the Bank agreed on "Principles for Payment of Compensationand Relocation" of the affected persons under the project. A field survey conducted by the Bank's

-19-

Resetlement Specialist after negotiations has confirmed that the number of affected people will beapproximately 40. Furthermore, some structures such as shacks and animal sheds would also need tobe acquired. For most of the route, the pipeline will be built in the existing EGAT right-of-way, whichis well protected and maintained. However, if, on the basis of subsequent detailed surveys, it is foundthat the number of affected people is substantially more than the numbers indicated in the informationcurrently available, the same principles of payment of compensation and resettlement would be appliedfor them. It was agreed that in that case, PTT and the Bank would, however, need to revisit the issueof compensation and resettlement.

F. Project lmplementation and Schedule

3.16 PTT will assume overall responsibility and control of project implementation (see Annex5, Project Implementation Organization). In the past, it has implemented several similar projectsincluding the construction of the existing 34-inch offshore pipeline and the Bongkot Gas Transmissionprojects, both financed by the Bank. PIT has appointed Bechtel International Inc. to assist in carryingout all stages of the project implementation cycle. PTT personnel will also be assigned to the projectfor on-the-job training and other selected tasks.

3.17 The critical-path master schedule prepared by PTT and Bechtel calls for completing thephysical works by March 1996 (Annex 4). This schedule may be somewhat optimistic, although thework has progressed according to this timetable until now. However, to allow for the possibility ofdelays during testing and commnssioning, the project completion date is assumed to be June 30, 1997.

G. Projet Cos

3.18 The project is estimated to cost the equivalent of US$674.5 million, including taxes andduties (US$22.2 million) and interest during construction (US$75.1 million). Foreign exchange coststotal US$565.6 million or 84% of total costs. Table 3.1 gives a breakdown of project costs by majorcomponents. The estinate is based on 1993 prices and many items reflect the acal prices or thoseprovided through informal but firm quotations. A 10% physical contingency has been added to the basecost estimate and price contingencies of 3.2% and 6% have been applied to the foreign and local costcomponents of the base cost plus physical contingenr v. respectively. The physical contingency isadequate considering the advanced stage of project desil. .. 4 the fact that pipeline engineering andmaterial involve few uncertainties. While the physical contiugency allowance for the constructioncontract may need to be higher than 10%, the allowance could be lower for pipeline material; therefore,an average of 10% is considered adequate. The price contingencies are based on Bank guidelines forintemational price increases (for foreign exchange costs) and the Bank's projection for price increases inThailand (for local costs). Taxes and duties were based on an average rate of 40% on all goods subjectto such rbarges. The interest during construction is calculated based on PIT's financing plan, applyingappropriate interest rates and the grace period of each lender, and assuming that interest will be accruedonly after funds are disbursed.

-20-

TABU 3.1: TlHlAND - Project Cost Estimates(US$ million - 1993)

Baht olon US$ dmil ForeipCoinpa_e_tsl a s % ofCouxponents ~ ~iLoc a Forgn Total Local_| Forelp | jTotalW

Land Acquisition 122.4 - 122.4 4.8 - 4.8 0

Pipe MaterW - 4,115.7 4,115.7 - 161.4 161.4 23.9

Pipeline Coating - 1,922.7 1,922.7 75.4 75.4 11.2

Onslhore Pipeline Construction and 255.0 765.0 1,020.0 10.0 30.0 40.0 5.9Commissioning

Offshore Pipeline Construction and 624.8 2,626.5 3,251.3 24.5 103.0 127.5 15.3Commissioning

Facilities- SCADA/Telecomniunication 51.0 63.8 114.8 2.0 2.5 4.5 0.4- Materials 30.6 66.3 96.9 1.2 2.6 3.8 0.4- Installtion 45.9 107.1 153.0 1.8 4.2 6.0 0.6- Cmpressor Station 61.8 561.0 624.8 2.5 22.0 24.5 3.2

Corrosion Control 76.5 40.8 117.3 3.0 1.6 4.6 0.2

Consultancy Services 329.0 387.6 716.6 12.9 15.2 28.1 2.2

Corporatization Study and Traminig 0.0 51.0 51.0 - 2.0 2.0 0.3Program

PTT Project Mane 102.0 0.0 102.0 4.0 4.0 -

Insurance 7.6 53.6 61.2 0.3 2.1 2.4 0.3

Taxes and Duties 566.1 0.0 566.1 22.2 - 22.2___ -.

Base Cost 2274.6 10,761.0 13,035.6 89.2 422 511.2 62.5

Physical Contingency 227.0 1,076.1 1,303.1 8.9 42.2 51.1 6.3

Price Conting-cncy 275.4 670.7 946.1 10.8 26.3 37.1 3.9

Total Project Cost 2777.0 12,507.8 15,284.7 108.9 490.5 599.4 72.7

1e s_During Con fuction (O 0.0 1,915.1 1,915.1 - 75.1 75.1 11.1

Total Ibang Required 2777.0 14,422.8 - 17,99.8 108.91 S65.6 6745 | 83.8

Source: Bank mission estims.

H. Project fTh Cindg Plan

3.19 Total fmnaning required, including interest during construction (estimated at US$75.1million based on the 4-year implementation period), would be US$674.5 million (see Table 3.2). Thefinacing plan has been developed on the basis of discussions with PIT, the Export-Import Bank ofJapan (JEXIM), the Asian Development Bank (ADB), and the European Investment Bank (EIB). Theprocurement packages were designed to take into account the various co-lenders' internal requirement3,the project implementation schedule, and IT's concern regarding its large exposure to non-dollar hardcurren-y, particularly the Japanese yen.

-21-

TABLE 3.2: THAILAND - Project Financig Plan(US$ million)

I Co4Lnauer Load Forep Tot| %

Asian Development Bank (ADB) - 100 100 14.8(ADD together with lEXIM will fIance 73% of pipeline material and coating)

Japan Exim Bank (JEXIM) 100 100 14.8

European Investment Bank (EIB) - 47 47 6.8(EIB will finance onshore pipeline construction)

PTT's commercial borrowings and bonds - 100 100 14.8

PTT's intermal cash generation 93.6 78.9 172.5 25.7

IBRD 15.3 139.7 155.0 23.1

Total Fb ng Required |5 56S.6 045 101

Source: Bank mission estimates.

3.20 The Bank loan would fnance the construction of the offshore pipeline as well asengineering and project management consultancy contracts, studies and training (US$155.0 million).ADB and JEXIM would joiindy finance about 72% of the cost of the pipeline materials (linepipe) andcoating contract, and the EIB would finance the construction of the onshore pipeline. The proposedBank loan of US$155.0 million would be made directly to PIT at the Bank's standard terms forThailand. PIyT would bear the foreign exchange and variable interest rate risks, which would beguaranteed by the Government. The Bank loan would be for 17 years, including four years of grace atthe Bank's variable interest rate. The loan would finance 23% of the total project financing requiredand 27% of its foreign expenditures.

3.21 Since the Bank loan will become effective after the ADB/JEXIM and BIB loans, it wasagreed that PIT would promptly notify the Bank when the respective loan become effective (the EIBLoan Agreement stipulates cross-effectivuiess with the Bank loan).

I. Procurement and Disbursement

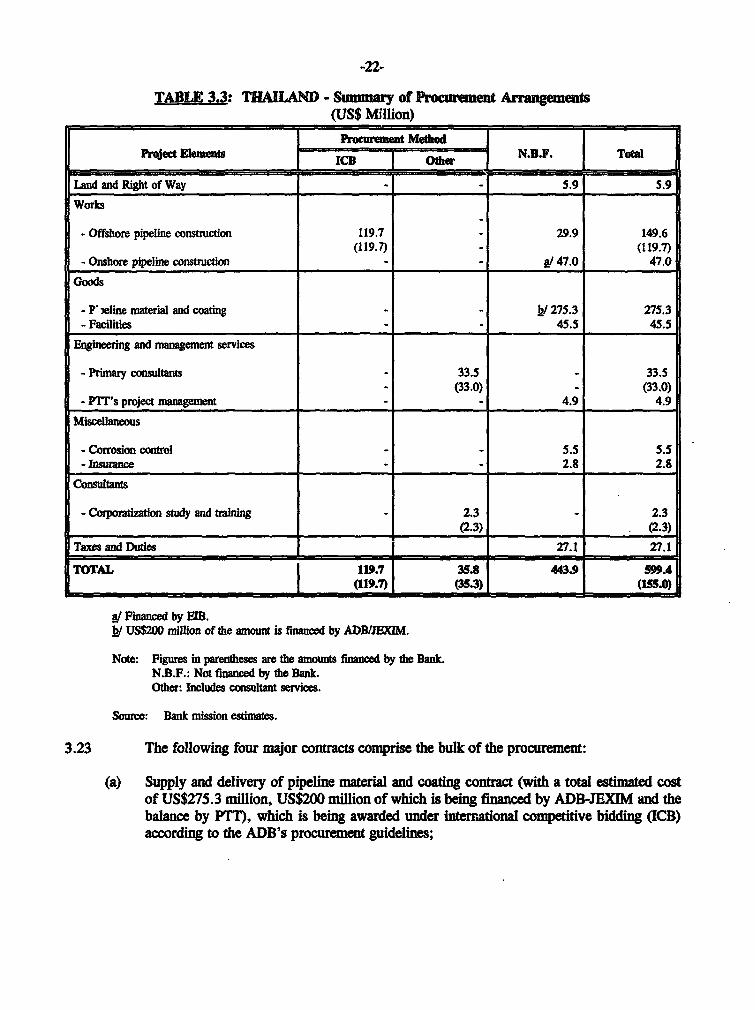

3.22 Procurement. Procurement arragements are summarized in Table 3.3 below. The costof each item includes its pro-rata share of the project's physical and price contingencies.

-22-

TABLE 3.3: THAILAND - Summary of Procment Angeme(US$ Million)

P focmurment Method TProject Elments f - O 1h N.B.F. TotS)

Ld and Right of Way . S.9 5.9

Works

- Offshore pipeline construction 119.7 29.9 149.6(119.7) (119.7)

- Onshore pipeline construicon a/ 47.0 47.0

- P 'eline material and coating - -l 275.3 275.3- Facilities - 45.5 45.5

Enigineeng and management services

- Primary consultans - 33.5 - 33.5- (33.0) - (33.0)

- Prr's project management - 4.9 4.9

Miscellaneous

- Corrosion contol - 5.5 5.5- Insurance - 2.8 2.8

Consultants

- Cipoatzation study and tning 2.3 - 2.3(2.3) (2.3)

Taxes and Duies 27.1 27.1

TOTAL | 119.7 35.8 443.9 599A_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ j (1 1 9.7)1(3 5.3 ) j _ _ _ _ _ _ j(1 5 O

I/ Financed by EIB._/ US$200 million of the amount is fnanced by ADBWJEXIM.

Note: Figures in parentheses are the amounts fianced by the Bank.N.B.F.: Not financed by the Bank.Other: Includes consultant services.

Soune: Bank mission esdmates.

3.23 The following four major contacts comprise the bulk of the procuremen:

(a) Supply and delivery of pipeline material and coating contract (with a total estmated costof US$275.3 million, US$200 million of which is being financed by ADB-JEXIM and thebalance by PMT), which is being awarded under international competitive bidding ([CB)according to the ADB's procurement guidelines;

-23-

(b) Engineering consultancy and project management contract (US$33.5 million), a Bank-financed component, which has already been awarded by PTT according to the Bank'sprocurement guidelines for the use of consultants;

(c) Construction of the onshore pipeline contract (US$47 million, financed by EIB), whichwill be awarded according to ElB's procurement procedures; and

(d) Construction of the offshore pipeline contract (US$149.6 million, of which US$119.7million is financed by IBRD), which will be procured through ICB according to theBank's procurement guidelines and using the Bank's standard bidding documents.

3.24 Various equipment and miscellaneous items, including compressors, are also needed forthe project. These items would be supplied and installed by PIf's contractors. PTT would alsoprocure land, civil works and buildings in accordance with its own procurement procedures, which aresatisfactory to the Bank. The remaining consultancies included in the project would be selected andappointed according to the Bank's guidelines for use of consultants.

3.25 All civil works and engineering-management consultant services contracts would be subjectto Bank's prior review except studies and training conts for the employment of consulting firmsestmated to cost less than US$100,000 or for the employment of individuals estimated to cost less thanUS$50,000.

3.26 Disbursement. Loan disbursement is based on the assumption that the loan will becomeeffective in the first quarter of the Bank's fiscal year 1995. The estimated disbursement of the Bankloan is smmized in Table 3.4 below. It is expected that it will be fully disbursed by June 30, 1997(para. 3.17), the scheduled completion date of the project. On this basis, the closing date is set forDecember 31, 1997. The scheduled disbursements are faster than the standard profiles for the regionand the subsector, reflecting the advanced stage of project preparation. Phasing of the estimateddisbursements and the Bank's standard disbursement profile for the subsector are shown in Annex 7.

TABLE 3.4: THAILAND - Esuimated Loau Disbursment(US$ Million)

Bank FY 199 196 1997

_nnual 7s 765Cumumla 75 140 155

Source: Bank mission esimates.

3.27 Due to a tight project implementation schedule and the critica nature of the engineeringconsultancy and management services, PTT had to advance its contract with Bechtel. Furthermore,advanced procurement action for offshore pipeline construction contracts would also be needed.Therefore, retroactive financing equal to US$15 million is recommended for expenses incurred afterSeptember 1, 1993, to partially reimburse amounts of the consultancy and offshore constructioncontracts, already paid by PIT through advanced contracting approved by the Bank.

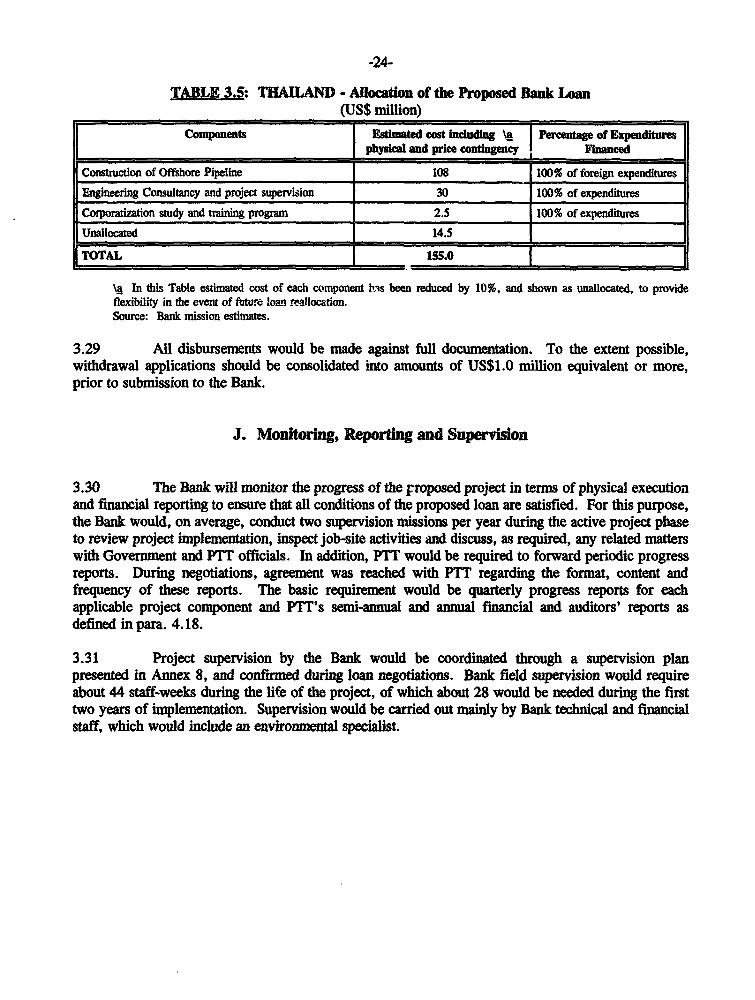

3.28 The Bank loan would be disbursed against the categories outlined in Table 3.5 below:

-24-

TABLE 3.5: THAILAND - Allocation of the Proposed Bank Loan(US$ million)

Components Estimated cost Inlding \a Pctage of Expeditesphyskal and price contgeny cced l

Construction of Offshore Pipeline 108 100% of foreign expenditures

Engineering Consultancy and project supervision 30 100% of expenditures

Corporatization study and training programn 2.5 100% of expenditures

Unallocated 14.5 I

TOTAL IqSSOl

\A In this Table estimated cost of each component h.7s been reduced by 10%, and shown as unallocated, to provideflexibility in the event of fubture loan reallocation.Source: Bank mission estimnates.

3.29 All disbursements would be made against full documentation. To the extent possible,withdrawal applications should be consolidated into amounts of US$1.0 million equivalent or more,prior to submission to the Bank.

J. Monitoring, Reportng and Supervision

3.30 The Bank will monitor the progress of the proposed project in terms of physical executionand financial reportng to ensure that all conditions of the proposed loan are satisfied. For this purpose,the Bank would, on average, conduct two supervision missions per year during the active project phaseto review project implementation, inspect job-site activities and discuss, as required, any related matterswith Government and PTT officials. In addition, PIT would be required to forward periodic progressreports. During negotiations, agreement was reached with PITT regarding the format, content andfrequency of these reports. The basic requirement would be quarterly progress reports for eachapplicable project component and PIT's semi-anmual and anmnal financial and auditors' reports asdefined in para. 4.18.

3.31 Project supervision by the Bank would be coordinated through a supervision planpresented in Annex 8, and confirmed during loan negotations. Bank field supervision would requireabout 44 staff-weeks during the life of the project, of which about 28 would be needed during the firsttwo years of implementation. Supervision would be carried out mainly by Bank technical and financialstaff, which would include an enviromental specialist.

THE BORROWER

A. Background

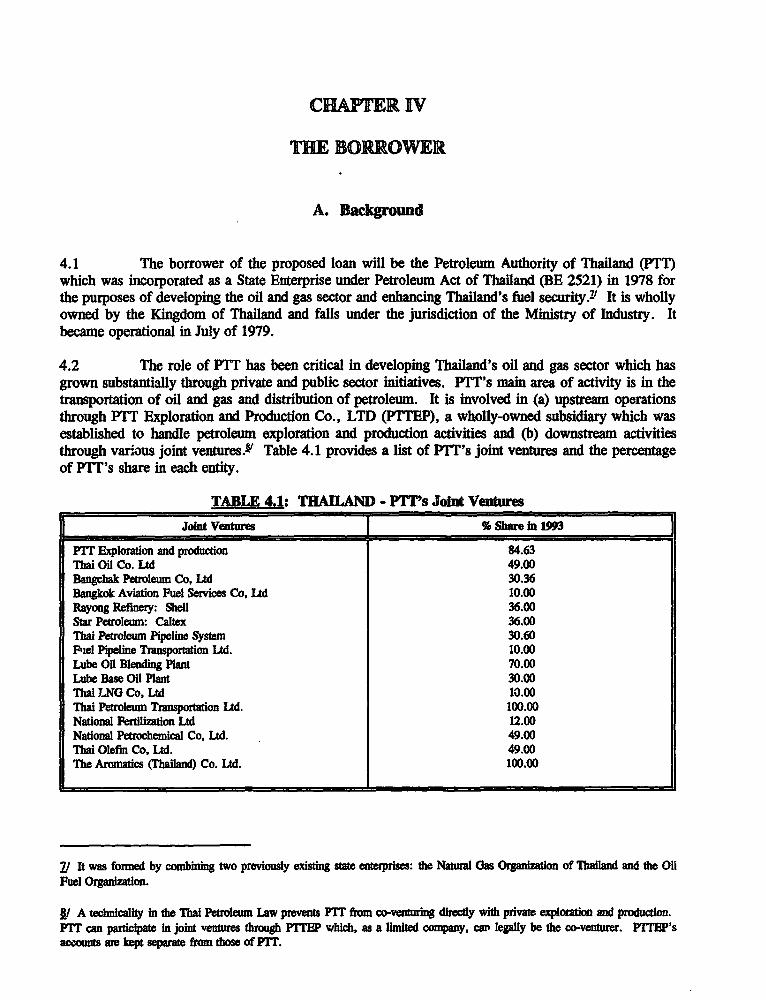

4.1 The borrower of the proposed loan will be the Petroleum Authority of Thailand (PTT)which was incorporated as a State Enterprise under Petroleum Act of Thailand (BE 2521) in 1978 forthe purposes of developing the oil and gas sector and enhancing Thailand's fuel security.-' It is whollyowned by the Kingdom of Thailand and falls under the jurisdiction of the Ministry of Industry. Itbecame operational in July of 1979.

4.2 The role of PTT has been critical in developing Thailand's oil and gas sector which hasgrown substantially through private and public sector initiatives. PTT's man area of activity is in thetransportation of oil and gas and distribution of petroleum. It is involved in (a) upstream operationsthrough PTT Exploration and Production Co., LTD (PTTEP), a wholly-owned subsidiary which wasestablished to handle petroleum exploration and production activities and (b) downstream activitiesthrough various joint ventures.Y Table 4.1 provides a list of PTT's joint ventures and the percentageof PfT's share in each entity.

TABLE 4.1: THAILAND - PITs Joit Ventures

[ ~~~~~Joint Vaiture % Sham n1a19

PrT RExploration and production 84.63Thai Oil Co. Ltd 49.00Bangclak Petroleum Co, Ltd 30.36Banglok Aviation Fiuel Services Co, Ltd 10.00Rayong Refinery: Shell 36.00Star Petroleum: Caltex 36.00Thai Petroleum Pipeline System 30.60lPiel Pipeline Tranwortion Ltd. 10.00Lube 0O Blending Plant 70.00Lube Base Oil Plant 30.00Thai LNG Co, Ltd 10.00Thai Petroleum Tanportion Ltd. 100.00National Fertlization Ltd 12.00National Petrochemical Co. Ltd. 49.00Thai Olefin Co, Ltd. 49.00The Aomatics Thailand) Co. Ltd. 100.00

1 it was formed by combining two previously existng state enterprises: the Naural Gas Organization of Thailand mid the OilFuel Organization.

It A tchnicality in the Thai Petroleum Law prevents P ftrm co-venturhg dhily with pivae exploration and production.PIT can participate in joint ventues trough PITEP which, as a limited company, can legally be the co-venturer. Pl'samounts are kept separte from those of PTT.

-26-

B. Organization