Embed Size (px)

Citation preview

Year-end Press Conference

Enrique García Executive President

Andean Development Corporation Caracas, December 14, 2004

Highlights 2004

• Economic recovery of Latin America

• Greater stability in the region

• New momentum in integration processes

• CAF’s growing role in the region:

• Conceptual and financial stimulus for a renewed development agenda

• Record figures in operations and financial results

• Confirmation of risk ratings

• international recognition

• Best issuing agency of the year (Euromoney)

• Best multilateral bank (Latin Finance)

• Best bond issue to finance development (Emerging Markets)

Regional environment

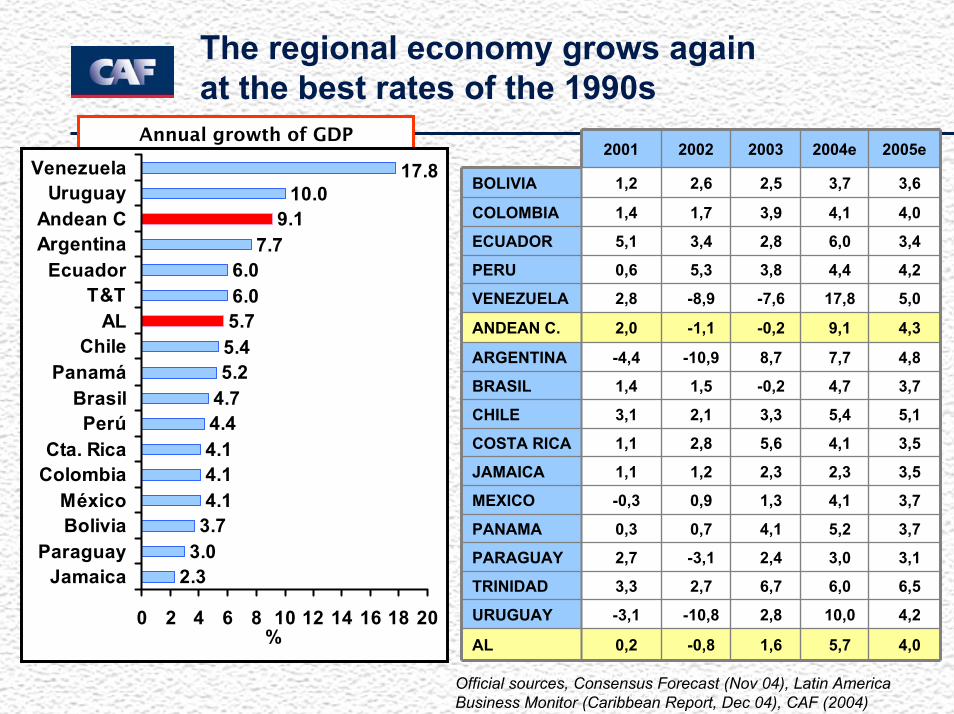

The regional economy grows againat the best rates of the 1990s

Fuentes oficiales, Consensus Forecast (Nov. 04), Latin AmericaBusiness Monitor (Caribbean Report, Dic 04), CAF (2004)

Annual growth of GDP-2004e-

Official sources, Consensus Forecast (Nov 04), Latin America Business Monitor (Caribbean Report, Dec 04), CAF (2004)

5,7

10,0

6,0

3,0

5,2

4,1

2,3

4,1

5,4

4,7

7,7

9,1

17,8

4,4

6,0

4,1

3,7

2004e

1,6

2,8

6,7

2,4

4,1

1,3

2,3

5,6

3,3

-0,2

8,7

-0,2

-7,6

3,8

2,8

3,9

2,5

2003

4,0-0,80,2AL

4,2

6,5

3,1

3,7

3,7

3,5

3,5

5,1

3,7

4,8

4,3

5,0

4,2

3,4

4,0

3,6

2005e

0,70,3PANAMA

0,9-0,3MEXICO

1,21,1JAMAICA

2,81,1COSTA RICA

2,13,1CHILE

1,51,4BRASIL

-10,8

2,7

-3,1

-10,9

-1,1

-8,9

5,3

3,4

1,7

2,6

2002

-3,1URUGUAY

2,0ANDEAN C.

2,8VENEZUELA

0,6PERU

5,1ECUADOR

1,4COLOMBIA

1,2BOLIVIA

3,3TRINIDAD

2,7PARAGUAY

-4,4ARGENTINA

2001

2.33.03.74.14.14.14.44.75.25.45.76.06.0

7.79.1

10.017.8

0 2 4 6 8 10 12 14 16 18 20

JamaicaParaguay

BoliviaMéxico

ColombiaCta. Rica

PerúBrasil

PanamáChile

ALT&T

EcuadorArgentinaAndean C

UruguayVenezuela

%

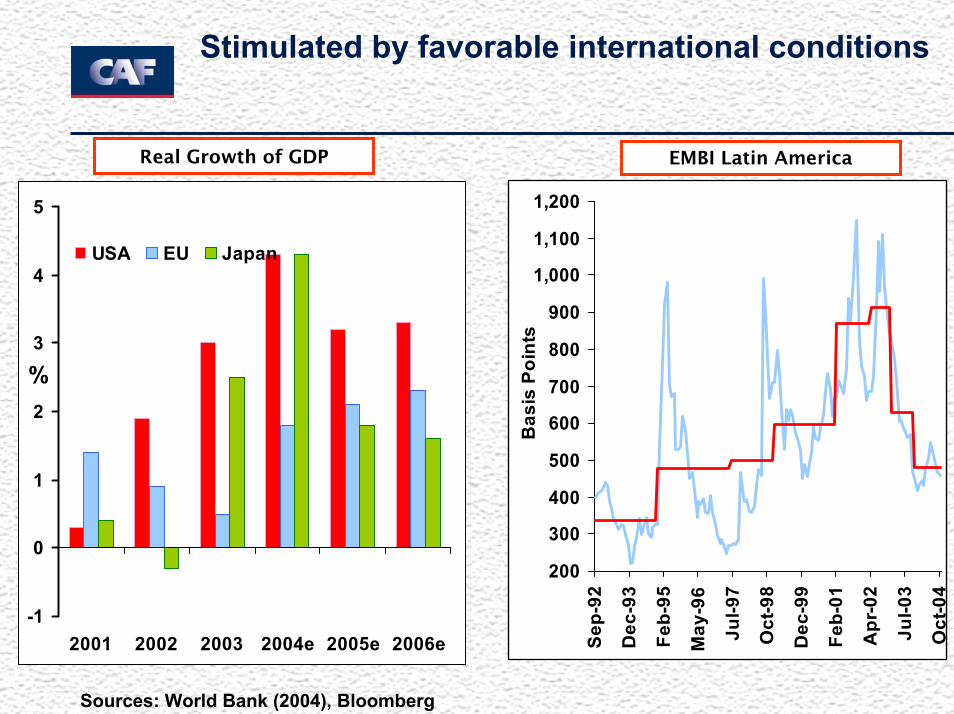

Stimulated by favorable international conditions

-1

0

1

2

3

4

5

2001 2002 2003 2004e 2005e 2006e

%

USA EU Japan

Real Growth of GDP

200

300

400

500

600

700

800

900

1,000

1,100

1,200

Sep

-92

Dec

-93

Feb-

95

May

-96

Jul-9

7

Oct

-98

Dec

-99

Feb-

01

Apr

-02

Jul-0

3

Bas

is P

oint

s

EMBI Latin America

Oct

-04

Sources: World Bank (2004), Bloomberg

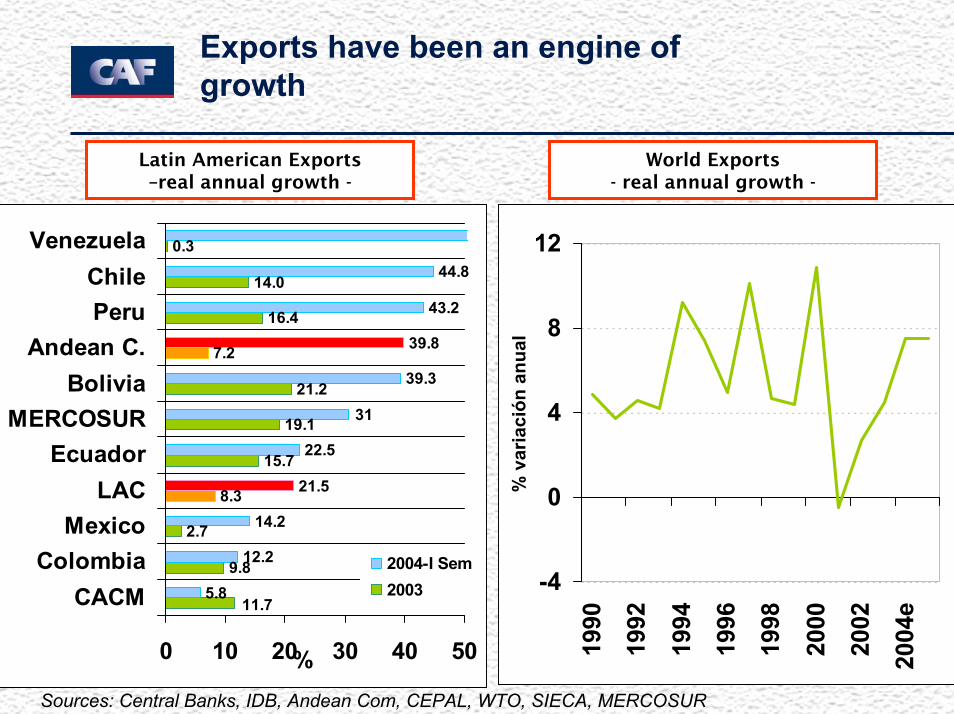

Exports have been an engine of growth

9.8

2.7

8.3

15.7

19.1

21.2

7.2

16.4

14.0

0.3

5.8

12.2

14.2

21.5

22.5

39.3

39.8

43.2

44.8

11.7

31

0 10 20 30 40 50

CACMColombia

MexicoLAC

EcuadorMERCOSUR

BoliviaAndean C.

PeruChile

Venezuela

%

2004-I Sem2003 -4

0

4

8

12

1990

1992

1994

1996

1998

2000

2002

2004

e

% v

aria

ción

anu

al

Latin American Exports –real annual growth -

World Exports- real annual growth -

Sources: Central Banks, IDB, Andean Com, CEPAL, WTO, SIECA, MERCOSUR

The improved regional outlook should not lead to complacency

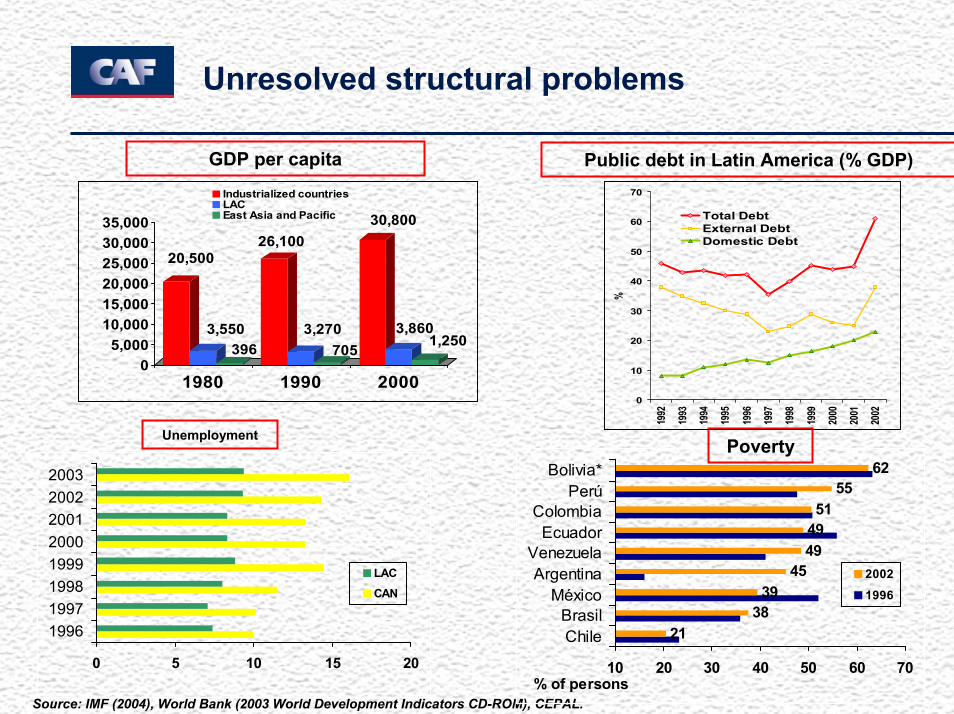

Unresolved structural problems

Source: IMF (2004), World Bank (2003 World Development Indicators CD-ROM), CEPAL.

2138

3945

494951

5562

10 20 30 40 50 60 70

ChileBrasil

MéxicoArgentina

VenezuelaEcuador

ColombiaPerú

Bolivia*

% of persons

2002

1996

Poverty

0 5 10 15 20

19961997199819992000200120022003

LAC

CAN

Unemployment

20,500

3,550396

26,100

3,270705

30,800

3,8601,250

05,000

10,00015,00020,00025,00030,00035,000

1980 1990 2000

Industrialized countriesLACEast Asia and Pacific

0

10

20

30

40

50

60

70

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

%

Total DebtExternal DebtDomestic Debt

GDP per capita Public debt in Latin America (% GDP)

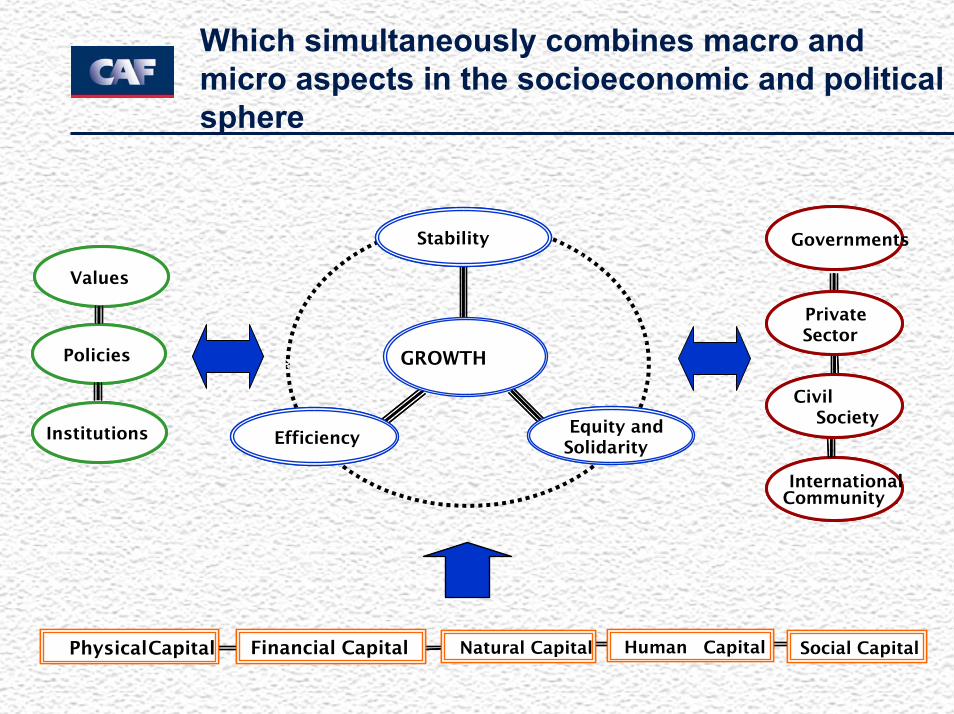

In this context the CAF is working for a renewed development agenda

Which simultaneously combines macro and micro aspects in the socioeconomic and political sphere

Capital Físico Capital Financiero Capital Natural Capital Humano Capital SocialCapital Físico Capital FinancieroPhysicalCapital Financial Capital Capital Natural Capital Humano Capital SocialNatural Capital Human Capital Social Capital

ComunidadInternacional

Gobiernos

SociedadCivil

Sector Privado

InternationalCommunity

Governments

CivilSociety

Private Sector

Valores

Políticas

Instituciones

Values

Policies

Institutions Equidad ySolidaridad

Estabilidad

EficienciaEquity and

Solidarity

Stability

Efficiency

GROWTH

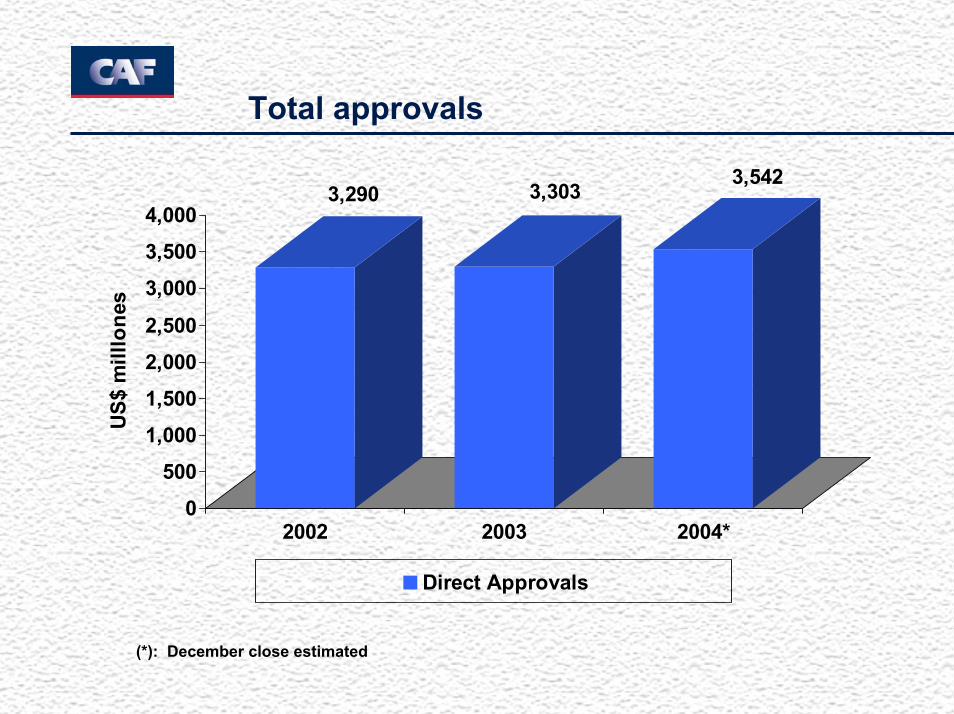

Total approvals

3,290 3,3033,542

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

US$

mill

lone

s

2002 2003 2004*

Direct Approvals

(*): December close estimated

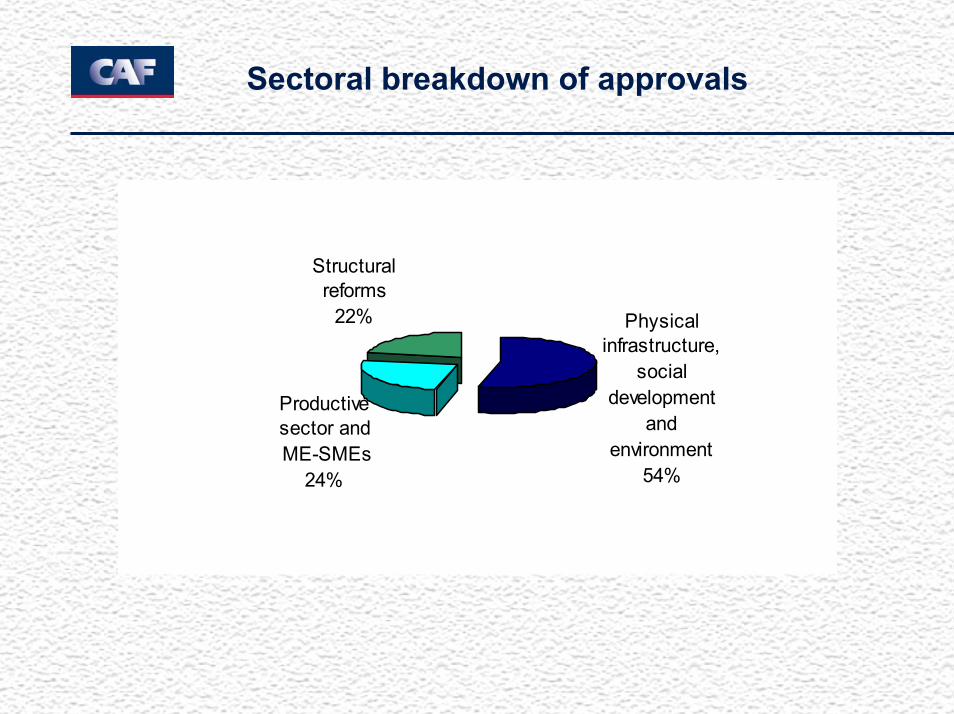

Sectoral breakdown of approvals

Physical infrastructure,

social development

and environment

54%

Productive sector and ME-SMEs

24%

Structural reforms

22%

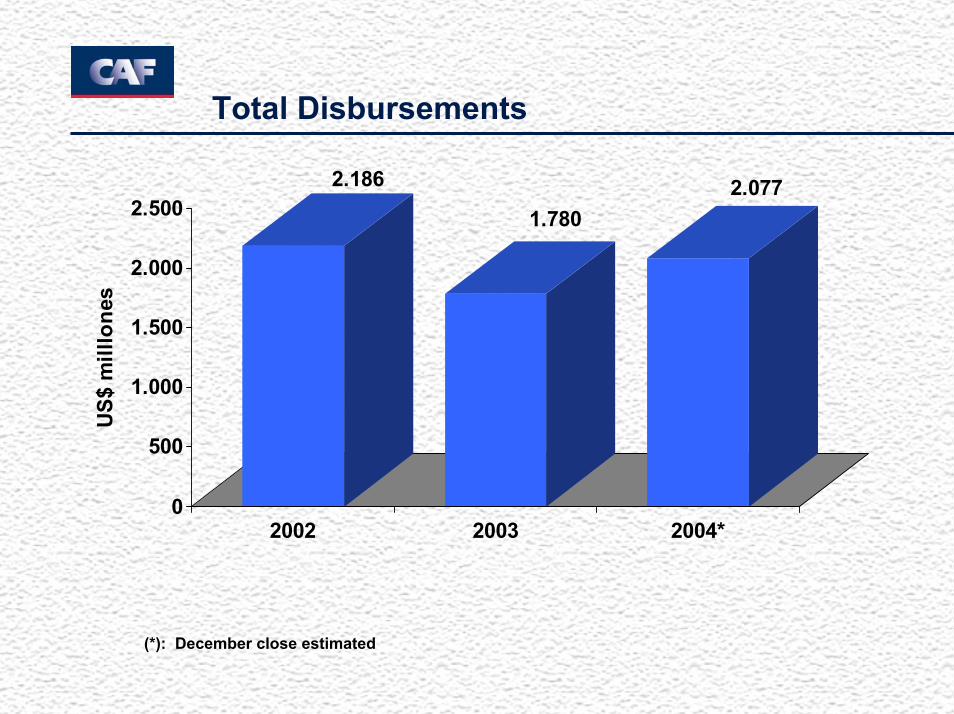

Total Disbursements

2.186

1.7802.077

0

500

1.000

1.500

2.000

2.500

US$

mill

lone

s

2002 2003 2004*

(*): December close estimated

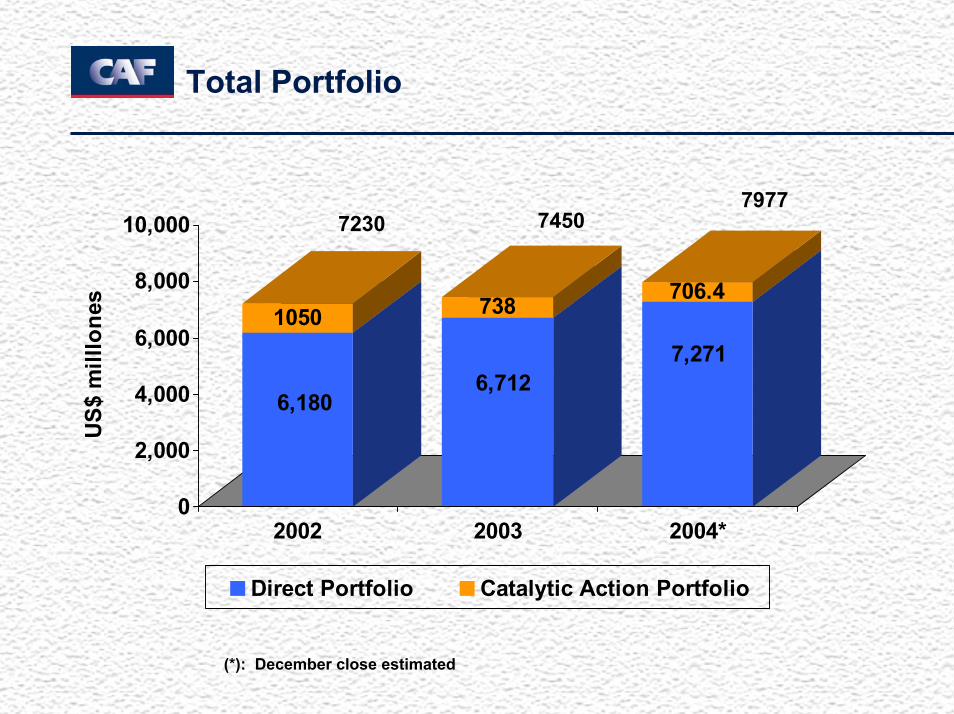

Total Portfolio

6,180

1050

6,712

738

7,271

706.4

0

2,000

4,000

6,000

8,000

10,000

US$

mill

lone

s

2002 2003 2004*

Direct Portfolio Catalytic Action Portfolio

72307977

7450

(*): December close estimated

httphttp:://www.caf.com//www.caf.com